Andrew Stallard Portfolio 2015

21

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810 Portfolio Andrew Stallard | Freelance Creative Artworker

-

Upload

andrew-stallard -

Category

Documents

-

view

299 -

download

4

Transcript of Andrew Stallard Portfolio 2015

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

PortfolioAndrew Stallard | Freelance Creative Artworker

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

ContentsBrochures 4 – 7

Calendars 8

Financial Brochures & Reports 9 – 11

Folders & Packaging 12 – 14

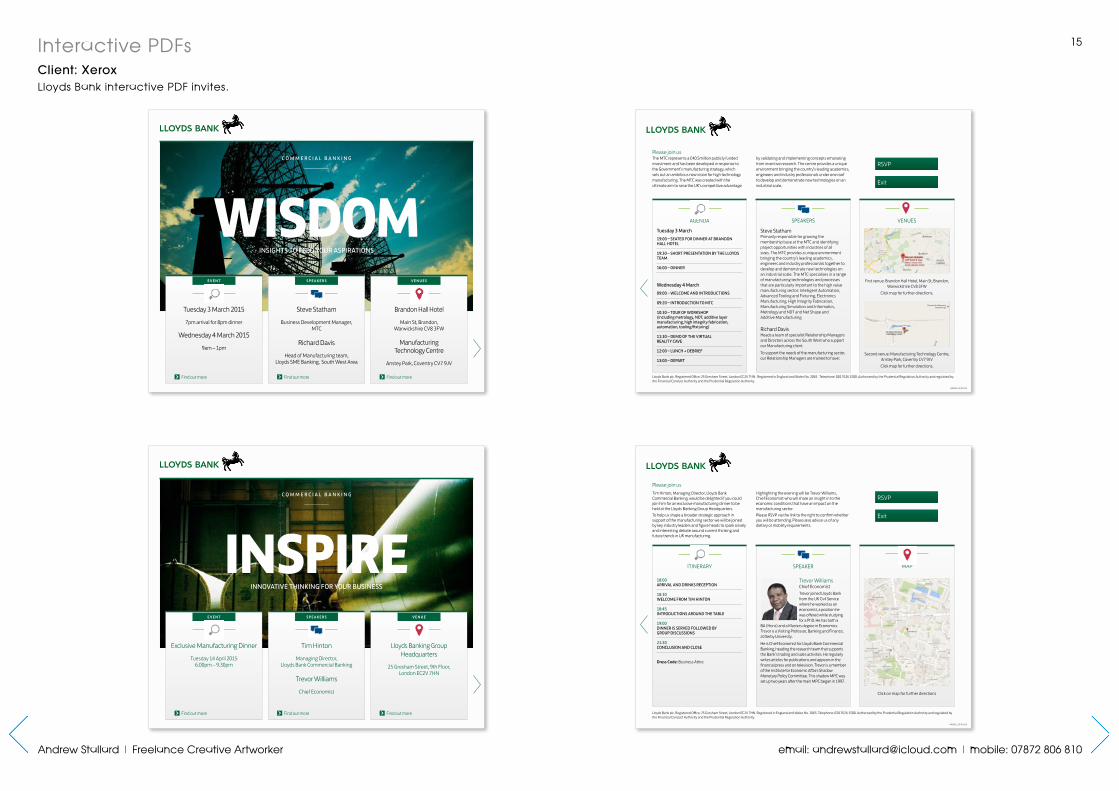

Interactive PDFs 15

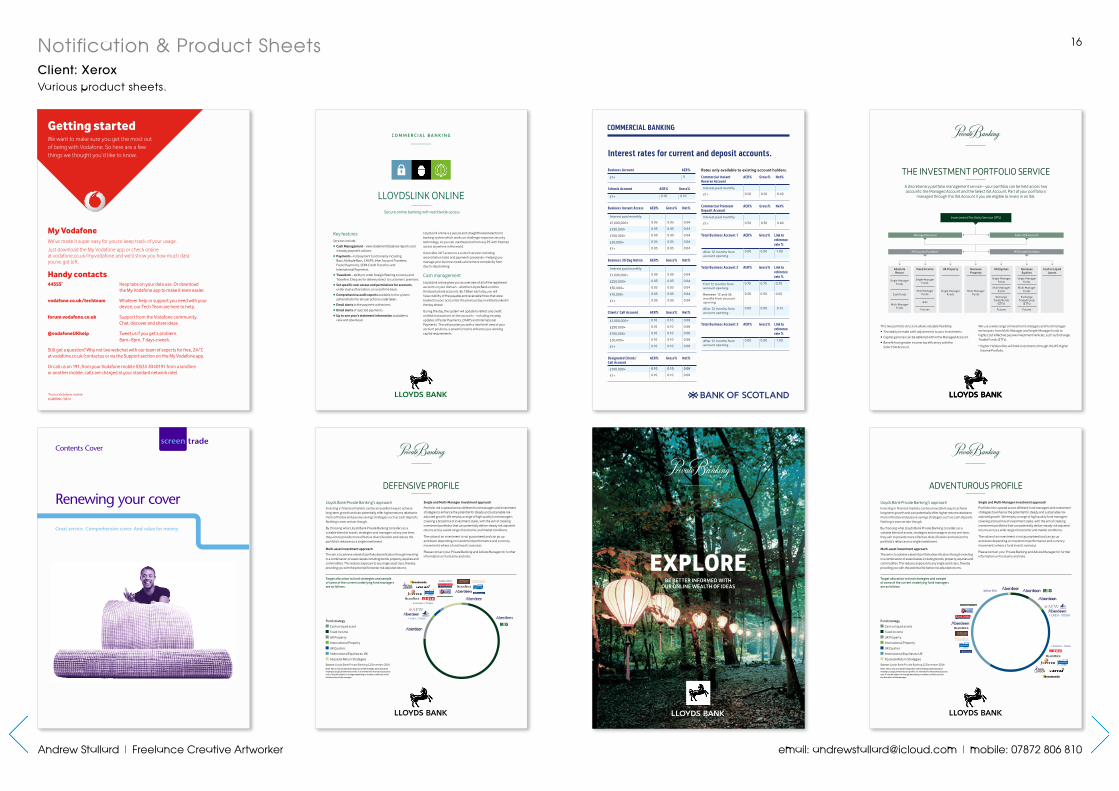

Notification & Product Sheets 16

Postcards & Flyers 17

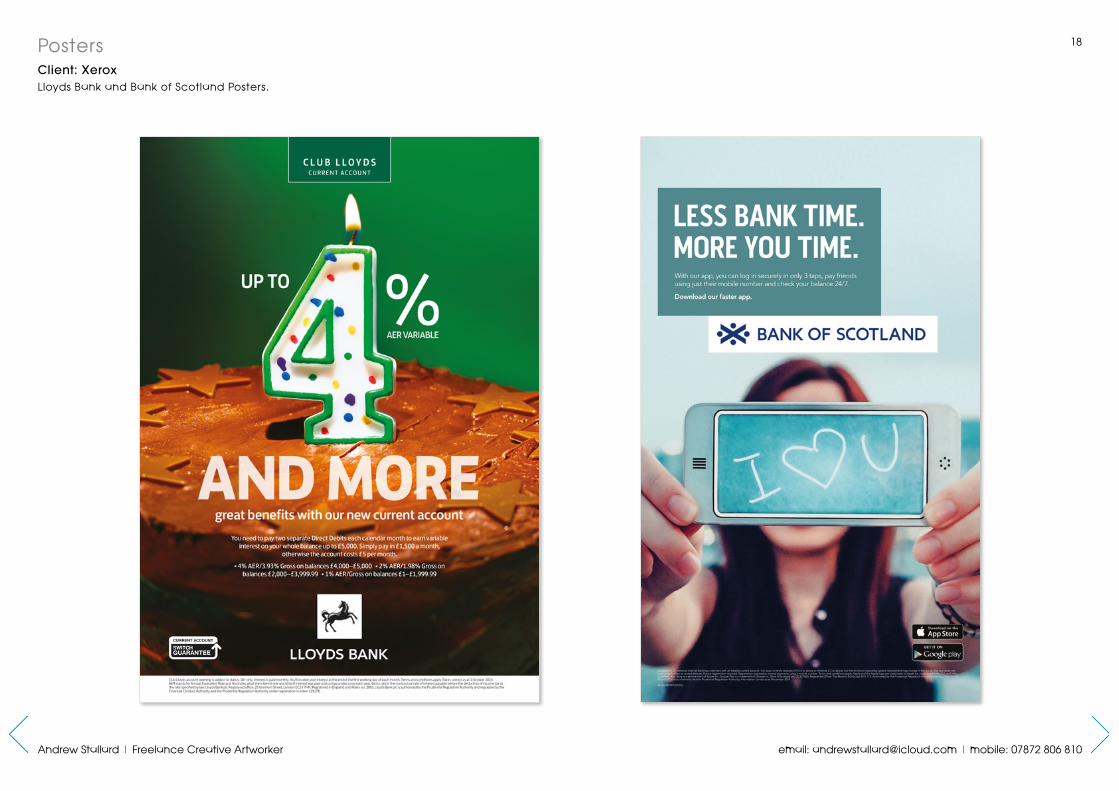

Posters 18

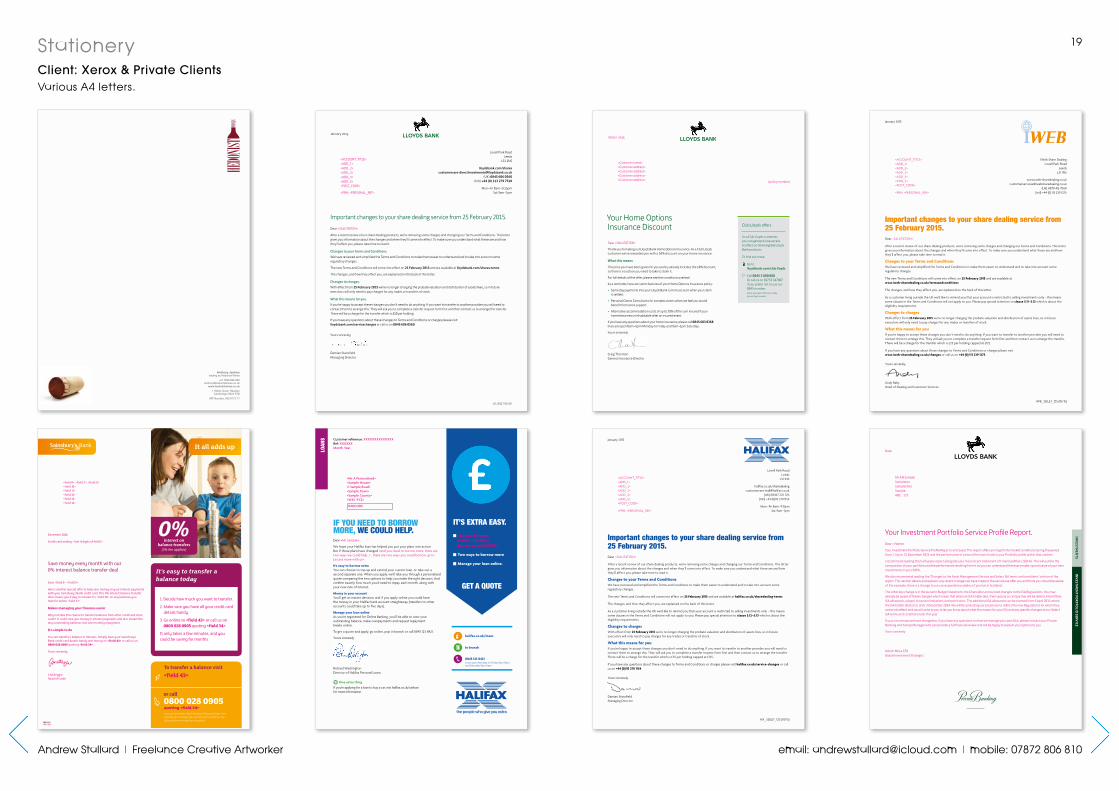

Stationery 19

Terms and Conditions Documents 20

Tickets 21

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

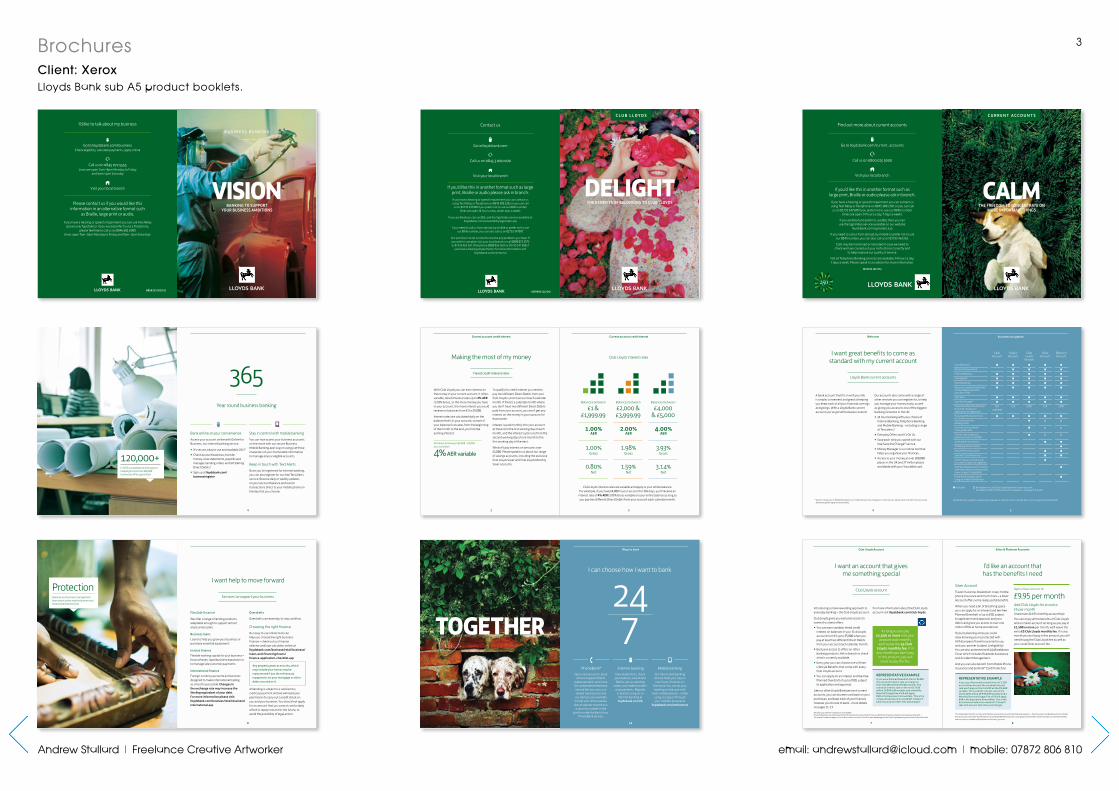

3BrochuresClient: XeroxLloyds Bank sub A5 product booklets.

£Bank online at your convenienceAccess your account online with Online for Business, our internet banking service.

• It’s secure, easy to use and available 24/71.

• Check account balances, transfer money, view statements, pay bills and manage standing orders and UK Sterling Direct Debits 2.

• Sign up at lloydsbank.com/ business/register

«Stay in control with mobile bankingYou can now access your business accounts on the move with our secure Business Mobile Banking app3. Log on using just three characters of your memorable information to manage all your eligible accounts.

Keep in touch with Text AlertsOnce you’ve registered for internet banking, you can also register for our free Text Alerts service. Receive daily or weekly updates on your account balance and recent transactions direct to your mobile phone on the day that you choose.

365Year round business banking

4

120,000+In 2013 our experience and support helped get more than 120,000 businesses off to a great start.

8

I want help to move forward

Services to support your business

Flexible financeWe offer a range of lending products, adaptable enough to support almost any business plan.

Business loansLoans to help you grow your business or purchase essential equipment.

Invoice financeFlexible working capital for your business – for purchases, rapid business expansion or to manage late customer payments.

International financeForeign currency accounts and services designed to make international trading as smooth as possible. Changes in the exchange rate may increase the Sterling equivalent of your debt. For more information please visit: lloydsbank.com/business/retail-business/ international.asp

Overdrafts

Overdrafts can ease day-to-day cashflow.

Choosing the right financeOur easy to use online tools can help you choose the right business finance – check out our finance selector and loan calculator online at lloydsbank.com/business/retail-business/ loans-and-financing/loans/ finance-application-checklist.asp

All lending is subject to a satisfactory credit assessment and we will need your permission to carry out a credit check on you and your business. You should not apply for an amount that you cannot comfortably afford to repay now and in the future, to avoid the possibility of legal action.

Any property given as security, which may include your home, may be repossessed if you do not keep up repayments on your mortgage or other debts secured on it.

ProtectionSpeak to your business management team about protecting the business you have worked hard to build

I’d like to talk about my business

£Go to lloydsbank.com/business

Check eligibility, calculate payments, apply online

Call us on 0845 072 5555Lines are open 7am–8pm Monday to Friday

and 9am–2pm Saturday

Visit your local branch

Please contact us if you would like this information in an alternative format such

as Braille, large print or audio.If you have a hearing or speech impairment you can use Text Relay

(previously Typetalk) or if you would prefer to use a Textphone, please feel free to call us on 0845 601 6909

(lines open 7am–8pm Monday to Friday and 9am–2pm Saturday).

BB58253 (02/15)

BANKING TO SUPPORT YOUR BUSINESS AMBITIONS

VISION

Club Lloyds interest rates are variable and apply to your whole balance. For example, if you have £4,000 in your account for 365 days, you’ll receive an

interest rate of 4% AER/3.93% Gross variable on your entire balance as long as you pay two different Direct Debits from your account each calendar month.

Balances between

£1 & £1,999.99

Balances between

£2,000 & £3,999.99

Balances between

£4,000 & £5,000

1.00% AER

2.00% AER

4.00% AER

1.00% Gross

1.98% Gross

3.93% Gross

0.80% Net

1.59% Net

3.14% Net

3

Current account credit interest

Club Lloyds interest ratesMaking the most of my money

Tiered credit interest rates

With Club Lloyds you can earn interest on the money in your current account. It offers variable, tiered interest rates up to 4% AER /3.93% Gross, so the more money you have in your account, the more interest you could receive on balances from £1 to £5,000.

Interest rates are calculated daily on the balance that’s in your account, so even if your balance fluctuates from the beginning of the month to the end, you’ll still be earning interest.

4% AER variable

On balances between £4,000 – £5,000 you could earn

To qualify for credit interest you need to pay two different Direct Debits from your Club Lloyds current account each calendar month. If there’s a calendar month where you don’t have two different Direct Debits paid from your account, you won’t get any interest on the money in your account for that month.

Interest is paid monthly into your account at the end of the first working day of each month, and the interest cycle runs from the second working day of one month to the first working day of the next.

We don’t pay interest on amounts over £5,000. Please speak to us about our range of savings accounts, including the exclusive Club Lloyds Saver and Club Lloyds Monthly Saver accounts.

2

Current account credit interest

PhoneBank®

Open new accounts, book a branch appointment,

make payments and more. Our automated telephone service lets you carry out simple transactions and

our advisers are available to help with other queries. Ask an adviser to send you

a security number in the post to make the best of our

PhoneBank service.

Internet bankingView statements, check

your balance, view Direct Debits, set up standing

orders and make transfers and payments. Register

in branch or log on to internet banking at lloydsbank.com/ib

Mobile bankingOur free mobile banking service helps you stay on

top of your finances on the move. You can do your banking on the spot with

most mobile phones – either using our app or through your mobile’s browser at

lloydsbank.com/onthemove

I can choose how I want to bank

247

14

Ways to bank

TOGETHER

Contact us

£Go to lloydsbank.com

Call us on 0845 3 000 000

Visit your local branch

If you'd like this in another format such as large print, Braille or audio please ask in branch. If you have a hearing or speech impairment you can contact us using Text Relay or Textphone on 0845 300 2281 or you can call

us on 01733 347500 if you prefer not to use our 0845 number (lines are open 24 hours a day, seven days a week).

If you are Deaf you can use BSL and the SignVideo service available at lloydsbank.com/accessibility/signvideo.asp

If you need to call us from abroad, by mobile or prefer not to use our 0845 number, you can also call us on 01733 347007.

Our promise is to do our best to resolve any problems you have. If you wish to complain visit your local branch or call 0800 072 3572 or 01733 462 267. (Textphone 0800 056 7614 or 01733 347 500, if

you have a hearing impairment). For more information visit lloydsbank.com/contactus

M59992 (12/14)

DELIGHTTHE BENEFITS OF BELONGING TO CLUB LLOYDS

C L U B L L O Y D S

Cash Account

Classic Account

Club Lloyds

Account

Silver Account

Platinum Account

Visa debit card

Optional cheque book

Internet Banking

PhoneBank®

Mobile Banking

Access to cashpoint machines at Lloyds Bank and other providers ATMs

Text alerts

Save the Change®

Interest and fee-free Planned Overdraft. (Subject to application and approval)

Not available

£25 £100 £50 £300

Everyday Offers & It’s On Us

Access to exclusive banking offers

A choice of one of three Lifestyle Benefits

Tiered credit interest on balances from £1 to £5,000

AA Roadside Assistance

AA Relay and Home Start

Mobile Phone Insurance

Sentinel® Card Protection

AXA European and UK Travel Insurance (subject to eligibility)

AXA Worldwide Travel Insurance with either family or winter sports cover (subject to eligibility)

Preferential charges when using your debit card abroad

Included Available if you add Club Lloyds benefits to your account. An additional £5 monthly account fee applies – see page 7, 8 and 9.

Overdrafts are subject to status and repayable on demand. You must be 18 or over to apply for an Overdraft.

5

Accounts at a glance

I want great benefits to come as standard with my current account

Lloyds Bank current accounts

A bank account that fits in with your life is simple, convenient and great at helping you keep track of all your financial comings and goings. With a Lloyds Bank current account you’ve got all the bases covered.

Our accounts also come with a range of other services you can register for, to help you manage your money easily, as well as giving you access to one of the biggest banking networks in the UK:

• 24 hour banking with your choice of Internet Banking, Telephone Banking and Mobile Banking – including a range of Text alerts*.

• Everyday Offers and It’s On Us.

• Save each time you spend with our free Save the Change® service.

• Money Manager is our online tool that helps you organise your finances.

• Access to your money at over 500,000 places in the UK and 27 million places worldwide with your Visa debit card.

* We don’t charge you for Mobile Banking but your mobile operator may charge you for some services, please check with them. Services may be affected by phone signal and functionality.

4

Welcome

I’d like an account that has the benefits I need

Silver AccountTravel insurance, breakdown cover, mobile phone insurance and much more – a Silver Account offers some really useful benefits.

When you need a bit of breathing space you can apply for an interest and fee-free Planned Overdraft of up to £50, subject to application and approval, and your debit card gives you access to over one million ATMs at home and abroad.

If you’re planning a trip you could relax knowing you’re protected with AXA European Travel Insurance for you and your partner (subject to eligibility). You are also protected with AA Breakdown Cover which includes Roadside Assistance and Accident Management.

And you can also benefit from Mobile Phone Insurance and Sentinel® Card Protection.

REPRESENTATIVE EXAMPLEIf you use a Planned Overdraft limit of £1,200 on our Silver Account the overdraft interest rate we charge on the first £50 will be 0% EAR variable. The overdraft interest rate on the next £1150 will be 19.94% EAR variable and a Monthly Overdraft Usage Fee of £6 will apply. EAR is the Equivalent Annual Rate. This is the actual annual rate of an overdraft. It doesn’t take into account other fees and charges.

Open a Silver Account for

£9.95 per monthAdd Club Lloyds for an extra £5 per month (maximum £14.95 monthly account fee)You can enjoy all the benefits of Club Lloyds and our Silver account. As long as you pay in £1,500 or more per month, we’ll waive the extra £5 Club Lloyds monthly fee. If in any month you don’t pay in this amount, you will need to pay the Club Lloyds fee as well as your usual Silver account fee.

The following benefits for our Silver and Platinum accounts are provided by third party suppliers – Travel Insurance, AA Breakdown Cover, Mobile Phone Insurance, Sentinel® Card Protection and Lifestyle Benefits. Exclusions may apply to the benefits. More information on all these benefits and exclusions is available at lloydsbank.com/current_accounts

8

Silver & Platinum Accounts

I want an account that gives me something special

Club Lloyds account

Introducing a more rewarding approach to everyday banking – the Club Lloyds account.

Club Lloyds gives you exclusive access to some of our best offers:

• You can earn variable, tiered credit interest on balances in your Club Lloyds account from £1 up to £5,000 when you pay at least two different Direct Debits from your account each calendar month.

• Exclusive access to offers on other banking products. Ask in branch to check what is currently available.

• Every year you can choose one of three Lifestyle Benefits that come with every Club Lloyds account.

• You can apply for an interest and fee-free Planned Overdraft of up to £100, subject to application and approval.

Like our other Lloyds Bank personal current accounts, you can also earn cashback on your purchases, and keep track of your finances however you choose to bank – more details on pages 11–13.

For more information about the Club Lloyds account visit lloydsbank.com/club-lloyds

As long as you pay £1,500 or more into your

account each month, we’ll waive the £5 Club

Lloyds monthly fee. If in any month you don’t pay

in this amount, you will need to pay the fee.

REPRESENTATIVE EXAMPLEIf you use a Planned Overdraft limit of £1200 the overdraft interest rate we charge on the first £100 will be 0% EAR variable. The overdraft interest rate on the next £1100 will be 19.94% EAR variable and a Monthly Overdraft Usage Fee of £6 will apply. EAR is the Equivalent Annual Rate. This is the actual annual rate of an overdraft. It doesn’t take into account other fees and charges.

We don’t pay interest on balances over £5,000. Lifestyle Benefits are administered by The Grass Roots Group UK Ltd. They use different 3rd party suppliers to provide each benefit. Terms and Conditions apply. You need to continue to live in the UK to take advantage of the Club Lloyds banking offers and Lifestyle Benefits.

7

Club Lloyds Account

Find out more about current accounts

£Go to lloydsbank.com/current_accounts

ÕCall us on 0800 015 5000

uVisit your local branch

If you’d like this in another format such as large print, Braille or audio please ask in branch.

If you have a hearing or speech impairment you can contact us using Text Relay or Textphone on 0845 300 2281 or you can call

us on 01733 347500 if you prefer not to use our 0845 number (lines are open 24 hours a day, 7 days a week).

If you are Deaf and prefer to use BSL then you can use the SignVideo service available on our website:

lloydsbank.com/signvideo.asp

If you need to call us from abroad, by mobile or prefer not to use our 0845 number, you can also call us on 01733 462263.

Calls may be monitored or recorded in case we need to check we have carried out your instructions correctly and

to help improve our quality of service.

Not all Telephone Banking services are available 24 hours a day, 7 days a week. Please speak to an adviser for more information.

M54741 (02/15)

C U R R E N T A C C O U N T S

THE FREEDOM TO CONCENTRATE ON MORE IMPORTANT THINGS

CALM

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

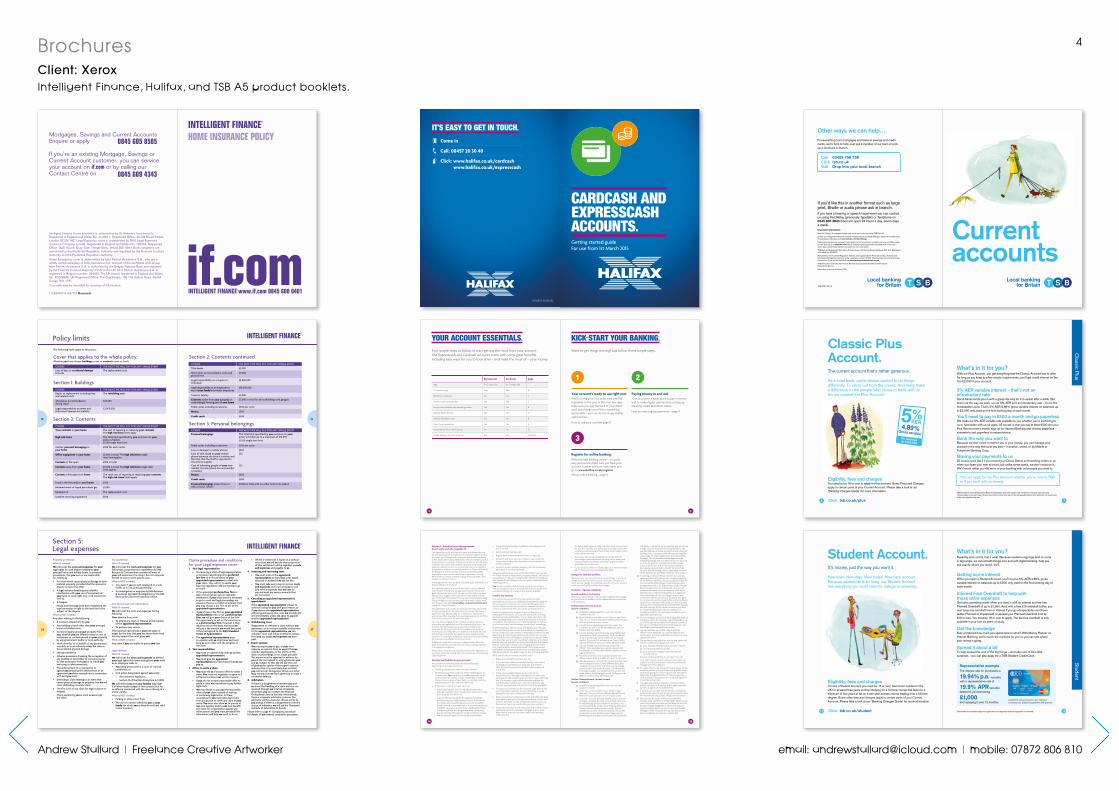

4BrochuresClient: XeroxIntelligent Finance, Halifax, and TSB A5 product booklets.

5

KICK-START YOUR BANKING.

Want to get things moving? Just follow these simple steps.

1

Your account’s ready to use right nowYou’ll receive your Visa debit card and PIN separately in the post in the next few days. Make sure you sign the back of your debit card, and change your PIN to something memorable – you can do this at any Halifax cash machine.

How to use your card see page 8

3

Register for online banking.Why not start banking online – it’s quick, easy and secure. Make sure you have your account number and sort code ready and go to www.halifax.co.uk/register

About online banking – page 6

2

Paying money in and outYour account is a great place to pay in money and to make regular payments by setting up standing orders and direct debits.

How to make regular payments – page 9

4

Expresscash Cardcash page

Age 11–15 years old 16–17 years old

Online banking Yes Yes 6

Telephone banking No Yes 7

Access to all our branches Yes Yes 6

Set up direct debits and standing orders Yes Yes 8

Mobile Alerts service Yes Yes 7

Halifax Visa debit card Yes Yes 8

Use of cash machines Yes Yes 6

Commission-free travel money No Yes 10

Credit interest on your account Yes Yes 12 and 31

YOUR ACCOUNT ESSENTIALS.

Four simple steps to follow to start getting the most from your account. Our Expresscash and Cardcash accounts come with some great benefits. Including easy ways for you to look after – and make the most of – your money.

15

• If a direct debit payment date is at a bad time in the month for you, (for example, just before you are paid), contact the company involved and ask them if they would collect it at a more convenient time.

• If you have fees to pay, remember to include these in your budget. Information that will help you to keep track of your finances is available in the rates and fees leaflet applicable to your account.

• If your account offers the facility, sign up to receive mobile alerts if you go into an unplanned overdraft.

Changes to facilities and fees We review our services and facilities, and the way in which we charge for them, from time to time. In Section 3 we set out when we may change the conditions and fees for your account and how we will tell you about the changes.

Section 2 – Special conditions

Special conditions for bankingThis section gives details of the special conditions which apply to your account in addition to the Halifax Bank Account terms and conditions.

Halifax Reward Current AccountSpecial conditions:

(a) Available to people aged 18 or over who must be resident in the UK.

(b) Up to two account holders on an “either to sign” basis only. You can hold one Reward Current Account in your sole name and one in joint names.

(c) You will receive reward payments if you meet the conditions set out in our Reward Payments, Interest and Account Fees leaflet.

(d) You can withdraw up to £500 a day using Halifax, Bank of Scotland or LINK cash machines. Cash withdrawals of up to £2,500 a day can be made over the branch counter. If you want to withdraw more than £2,500 a day you will need to give your branch advance notice.

(e) You can withdraw up to £300 a day at any Post Office®. Once registered, you can also deposit cash and cheques, as well as make balance enquires, on your registered account.

(f) Reward Current Accounts must have at least two different direct debit mandates set up on the account.

(g) We may review your account from time to time and if you have not kept a minimum of two different direct debit mandates on your account at all times, we may change your account to the Current Account, or if this account is no longer available, to a standard current account with similar features to the Current Account. We’ll give you at least two months’ notice before doing so.

Halifax Ultimate Reward Current AccountSpecial conditions:

(a) Available to people aged 18 or over who must be resident in the UK.

(b) Up to two account holders on an “either to sign” basis only. You can hold one Ultimate Reward Current Account in your sole name or one in joint names.

(c) Customers with the Ultimate Reward Current Account must pay a monthly fee (“the account fee”) which will be automatically deducted from the account by the second working day of the month (“the fee debit day”). Account fees are paid in arrears monthly. The first monthly account fee will be pro-rated by the number of days the account has been open. Please see the Reward Payments, Interest and Account Fees leaflet for

full details. In return for the account fee you will receive a range of account benefits including the day-to-day standard features of a bank account and the enhanced banking services associated with this account together with a range of other benefits (“the Account Benefits Package”). The Account Benefits Package is a single integrated package and no additional value or discount is, or can be, given to customers who either solely use just the account and/or the insurance benefits. All customers are entitled to benefit from all of the Account Benefits Package (where applicable) and none of the benefits are severable. Details are set out below.

(d) In opening an Ultimate Reward Current Account you agree to be bound by the specific conditions applying to the different benefits and policies that form part of the Account Benefits Package. In particular you have an agreement with us for the provision of the Ultimate Reward Current Account and separate contracts of insurance with each insurance company under which the premium is collected and paid by us as agents of the underwriters. We do not charge you any fee in connection with the provision of insurance. You agree to comply with, and be bound by the policy conditions issued to you relating to the insurance cover and other services which comprise the Accounts Benefits Package; and with the right of the insurers or service providers to change the applicable cover or conditions, in accordance with the relevant policy conditions on the applicable notice periods.

(e) You can withdraw up to £500 a day using Halifax, Bank of Scotland or LINK cash machines. Cash withdrawals of up to £2,500 a day can be made over the branch counter. If you want to withdraw more than £2,500 a day you will need to give your branch advance notice.

(f) You can withdraw up to £300 a day at any Post Office®. Once registered, you can also deposit cash and cheques, as well as make balance enquires, on your registered account.

(g) The insurance cover and other services that come with the Account Benefits Package will end if:(i) your Ultimate Reward Current Account is closed;(ii) you fail to pay the account fee;(iii) your account is changed to another type of

account with us; (iv) your residential address is no longer in the UK. Any other insurance policies that you have taken out yourself at a discount as part of the Account Benefits Package will not be affected.

(h) You agree that we can change the insurer of any of the insurance policies or the providers of any of the other services by giving you notice in good time. This will be before the change takes effect if that is required by a code of practice that applies to us or by our regulators or another similar body.

(i) You agree that any fees, premiums or claims monies held by members of the group and its agents are held by them as agents of the underwriters.

(j) If a sole account holder dies the benefits and policies automatically cease. If one of two joint account holders dies the benefits and policies will pass to the survivor.

(k) We may vary all or part of the Account Benefits Package under condition 12 of the Halifax Bank Account terms and conditions (unless we withdraw the Account Benefits Package altogether, as referred to below in special condition (n)). If we vary the Account Benefits Package in whole or in part we may vary the account fee in accordance with special condition (m).

14

Section 1 – Introduction to this agreement – how it works and who it applies toThis agreement is for our bank accounts and related services for personal customers resident in the United Kingdom (“UK”). It is made up of the general conditions and special conditions in this document and any additional conditions we give you for these accounts or services. Additional conditions are the daily overdraft fees, other fees, interest rates and other terms that apply to a specific service or account that are not included in the general conditions or special conditions. These will include, for example the terms set out in the rates and fees leaflet applicable to your account and in your application form(s). We will tell you which conditions apply when you take a new product or service from us.

In this agreement, “we” are Bank of Scotland plc and Halifax is a division of Bank of Scotland.

An important part of our role as your bank is to provide you with services to help you manage your finances. We do not generally provide advice, but we can use information we have about you to suggest other services we think might interest you. To find out more about how we and other Lloyds Banking Group companies use your personal information, please read Our Privacy Statement www.halifax.co.uk/privacystatement or ask for a copy in branch.

This agreement only covers accounts and services we provide for your personal use. We do not have to accept that anyone, apart from you, has any right to, or interest in, the money in your account (for example if you are keeping some or all of the money in your account for someone else).

You may not be eligible for all of the accounts or services covered by this agreement or all the features they have – for example, we will not give you a planned overdraft if you are under 18. We may also limit the number of accounts or services you can hold with us. In addition, not all the services and facilities covered by this agreement are available on all accounts. For example, telephone, mobile and internet banking services are not available on some accounts.

Additional conditions or special conditions may add to the general conditions but may also override an overlapping term in the general conditions.

Please ask us if you have any questions about this agreement or any other matter by visiting one of our branches, or contacting us by telephone.

Services and facilities on your accountWe provide the following main services and facilities depending on the type of account:

• Crediting of payments made into your account.

• Debiting of payments made out of the credit balance on your account. You may ask us to make a payment out of your account in a variety of ways including by writing a cheque, by setting up a direct debit or standing order, by requesting cash or by using your debit card.

• If you have a current account, you may:

− specifically request, and we may agree to provide, a planned overdraft which will allow you to borrow money from us up to a certain limit;

− make an informal request for an unplanned overdraft, by instructing us to make a payment which, if we choose to comply with it, would make your account exceed (or further exceed) its overdraft limit or, if you have no planned overdraft, cause your account to be overdrawn (or further overdrawn). (Unless we have guaranteed to a third party that we will make the payment, we do not have to comply with an informal request for an unplanned overdraft.)

• Cheque book (including cancellation and replacement if lost or stolen).

• Debit and cash machine card.

• Regular bank statements (either online or by post).

• Access to a 24-hour service so that you can contact us at any time to carry out transactions, answer queries or obtain assistance.

• Access to a cash machine network in the UK and abroad (fees apply for card use abroad).

There are additional services and facilities which you may ask for. These include, among others, stopping cheques, the special presentation of cheques, issuing banker’s drafts, providing you with copies of paid cheques or extra copies of statements and CHAPS payments.

You should consider which account is best for you. If you wish to change the type of account that you have at any time, you should contact us to discuss the options available.

Fees for our servicesOur current fees are listed in the rates and fees leaflet applicable to your account. Additional fees may also apply for some transactions that are not covered by this agreement. Fees for these services are contained in separate conditions which you will receive when you ask to use those services.

Under this agreement you agree to pay us those fees in exchange for the various services that we provide, including the main services and facilities. You can keep up to date with them by telephoning us, by visiting a branch or by looking at our website. This will allow you to decide whether or not you wish to incur them, and to manage your account accordingly.

The fees which you will have to pay will depend upon the type of account that you have and the way in which you operate your account. If your account remains in credit then you will not usually have to pay any fees for having the benefit of the main services and facilities but we will charge you a daily fee or interest if at the end of any day, your account is overdrawn. Daily fees and interest rates for planned overdrafts are lower than daily fees and interest rates for unplanned overdrafts. Our charging structure means that, in exchange for receiving the benefit of the main services and facilities, including the benefit of any overdraft that causes a daily fee or interest, you agree to pay our fees, including daily fees.

What can you do to minimise overdraft fees?

• Repay any overdraft as soon as you can.

• If your account offers an overdraft facility, ask us about arranging an overdraft as our daily fees and interest rates are lower for planned overdrafts than unplanned overdrafts.

• Check your available balance on the internet, by telephoning us or through a cash machine to make sure you have enough money in your account to pay everything due. The money in your account must be available for withdrawal (for example you must have waited for any cheques you have paid into your account to be available).

• If you go into overdraft in the course of a day, ensure that your overdraft is repaid by the end of the day to avoid paying the daily fee or interest for that day.

• Keep a record of any cheques you write and when they have been paid, so that you know how much money is left in your account. Someone can pay a cheque you have written into their account up to six months after you have written it.

• Check your statements and make a list of the dates of your regular payments (for example, mortgage, loan or rent). Keep a list of when all your direct debits and standing orders are due.

IT’S EASY TO GET IN TOUCH.

1/3360117-10 (02/15)

( Come in

e Call: 08457 20 30 40

Y Click: www.halifax.co.uk/cardcash www.halifax.co.uk/expresscash

CARDCASH AND EXPRESSCASH ACCOUNTS. Getting started guide For use from 1st March 2015

7

Classic P

lus

What’s in it for you?With our Plus Account, you get everything that the Classic Account has to offer. As long as you keep to a few simple requirements, you’ll get credit interest on the first £2,000 in your account.

5% AER variable interest – that’s not an introductory rateSome banks tempt you in with a great rate only for it to vanish after a while. But that’s not the way we work, so our 5% AER isn’t an introductory rate – it’s for the foreseeable future. That’s 5% AER/4.89% gross variable interest on balances up to £2,000 only, paid on the first working day of each month.

You’ll need to pay in £500 a month and go paperlessWe make our 5% AER variable rate available to you whether you’re switching to us or have been with us for ages. All we ask is that you pay at least £500 into your Plus Account every month, sign up for Internet Banking and choose paperless statements and paperless correspondence.

Bank the way you want toBecause we don’t want to restrict you or your money, you can manage your account in the way that suits you best – in branch, online, or by Mobile or Telephone Banking. Easy.

Moving your payments to usOf course we’d like it if you moved your Direct Debits and standing orders to us when you open your new account, but unlike some banks, we don’t insist on it. We’d much rather you did more of your banking with us because you want to.

AER stands for Annual Equivalent Rate and illustrates what the interest rate would be if interest was paid and compounded once each year. Gross rate is the contractual rate of interest payable before the deduction of income tax at the rate specified by law

You can apply for the Plus Account whether you’re new to TSB or if you bank with us already.

6

Classic Plus Account.The current account that’s rather generous.

As a local bank, we’ve always wanted to do things differently. To stand out from the crowd. And really make a difference to the people who chose to bank with us. So we created the Plus Account.

4.89% On balances up to £2,000

5%AER

Gross variable

Eligibility, fees and chargesYou need to be 18 or over to apply for this account. Some Fees and Charges apply to certain parts of your Current Account. Please take a look at our ‘Banking Charges Guide’ for more information.

Click tsb.co.uk/plus

13

Student

Overdrafts are available subject to application and approval and are repayable on demand.

What’s in it for you?Flexibility and control, that’s what. Because student outgoings tend to come in big lumps, we can smooth things over and with digital banking, help you see exactly where you stand, 24/7.

Getting some interestWhen you open a Student Account, you’ll receive 5% AER/4.89% gross variable interest on balances up to £500 only, paid on the first working day of each month.

Interest Free Overdraft to help with those extra expensesGet extra spending power when you need it with an interest and fee-free Planned Overdraft of up to £1,500. And, with a free £10 overdraft buffer, you won’t pay any overdraft fees or interest if you go unexpectedly overdrawn (either Planned or Unplanned) or exceed your Planned Overdraft limit by £10 or less. You must be 18 or over to apply. The fee-free overdraft is only available in your first six years of study.

Get the knowledgeEver wondered how much you spend and on what? With Money Planner on Internet Banking, we’ll crunch the numbers for you so you can see where your money’s going.

Spread it about a bitTo help spread the cost of the big things – and take care of life’s little surprises – you can also apply for a TSB Student Credit Card.

Representative exampleThe interest rate for purchases is

19.94% p.a. variable with a representative rate of

19.9% APR variable based on you borrowing

£1,000 and repaying it over 12 months.

Credit limits will vary based on your individual circumstances. Subject to application and approval.

12

Student Account.It’s money, just the way you want it.

New town. New digs. New mates. New bank account. Because student life is for living, our Student Account has everything you could need for college or university.

Eligibility, fees and chargesTo have a Student Account you must be 17 or over, have been resident in the UK for at least three years and be studying for a full time course that lasts for a minimum of two years or be on a one-year access course leading onto a full time degree. Some other fees and charges apply to certain parts of your Current Account. Please take a look at our ‘Banking Charges Guide’ for more information.

Click tsb.co.uk/student

If you’d like this in another format such as large print, Braille or audio please ask in branch.If you have a hearing or speech impairment you can contact us using Text Relay (previously Typetalk) or Textphone on 0345 835 3843 (lines are open 24 hours a day, seven days a week).Important informationSave the Change® is a registered trade mark and is used under licence by TSB Bank plc.

Defaqto is an independent financial research company. All use of Defaqto Ratings is subject to licensed terms. To read these in full please visit www.defaqto.com/Star-Ratings

Calls may be monitored or recorded. If you need to call us from abroad, or prefer not to use our 0345 number, you can also call us on 0203 284 1575. Not all Telephone Banking services are available 24 hours a day, seven days a week. Please speak to an advisor for more information.

TSB Bank plc Registered Office: Henry Duncan House, 120 George Street, Edinburgh EH2 4LH. Registered in Scotland No. SC95237.

Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under registration number 191240. We subscribe to the Lending Code; copies of the Code can be obtained from www.lendingstandardsboard.org.uk

TSB Bank plc is covered by the Financial Services Compensation Scheme and the Financial Ombudsman Service.

Information correct as at January 2015.

TSB10287 (02/15)

Other ways we can help…For everything from mortgages and loans to savings and credit cards, we’re here to help. Just ask a member of our team or pick up a brochure in branch.

Call 03459 758 758Click tsb.co.ukVisit Drop into your local branch

Current accounts

1514

Policy limits INTELLIGENT FINANCE®

£2,500Title deeds

Credit cards

£6,000Short term accommodation costs and ground rent

£2,000,000Legal responsibility as occupier or individual

£10,000,000

£5,000Tenant’s liability

£500 per cyclePedal cycles including accessories

£500Money

£500

£2,000 in total for all outbuildings and garagesContents stolen from your garage(s) or outbuilding(s) forming part of your home

Legal responsibility as an employer to any of your family’s domestic employeesCOVERS THE MOST WE WILL PAY FOR ANY SINGLE EVENT

Repair or replacement including fees and related costs

The rebuilding cost

Alternative accommodation during repair

Legal responsibility as owner and Defective Premises Act Liability

COVERS THE MOST WE WILL PAY FOR ANY SINGLE EVENTLoss of keys or accidental damage to locks

The replacement cost

The following limits apply to this policy:

£20,000

£2,000,000

COVERS THE MOST WE WILL PAY FOR ANY SINGLE EVENT

Section 1: Buildings

Cover that applies to the whole policy:Whether you have chosen buildings cover or contents cover or both:

Section 2: Contents continued

£500 in totalContents in the open

£5,000 in total. The high risk items single item limit applies

Contents away from your home

The total cost of repairing or replacing your contents The high risk items limits apply

Contents while you move home

COVERS THE MOST WE WILL PAY FOR ANY SINGLE EVENTThe cost of repairing or replacing your contents The high risk items limits apply

Your contents in your home

The total limit specified by you as shown on your policy schedule. £1,500 single item limit

High risk items

Section 2: Contents

£500 for each visitorVisitors’ personal belongings in your home

£5,000 in total. The high risk items single item limit applies

Office equipment in your home

£1,000 in total with no other limit to be added Personal belongings stolen from or with a motor vehicle

COVERS THE MOST WE WILL PAY FOR ANY SINGLE EVENT

Section 3: Personal belongings

The total limit specified by you as shown on your policy schedule up to a maximum of £10,000£1,500 single item limit

Personal belongings

£500 per cyclePedal cycles including accessories

£500£25

£25

£500Money

£500Credit cards

Loss or damage to mobile phonesCost of calls made on your mobile phone between the time it is stolen and the time that the theft is reported to the airtime supplierCost of informing people of your new number if a new phone line and number is needed

£500Food in the freezer(s) in your home

£1,000Metered water or liquid petroleum gas

The replacement costMetered oil

£500Satellite receiving equipment

3736

INTELLIGENT FINANCE®

Property protectionWhat IS coveredWe will cover the costs and expenses for your legal rights in a civil dispute relating to your principal home and holiday home, or personal possessions, that you own or are responsible for, following: • An event which causes physical damage to such

material property, provided that the amount in dispute is more than £100;

• A legal nuisance (meaning any unlawful interference with your use of enjoyment of your land, or some right over, or in connection with it);

• A trespass.Please note that you must have established the legal ownership or right to the land that is the subject of the dispute.

What is NOT coveredAny claim relating to the following: • A contract entered into by you. • Any building or land other than your principal

home or holiday home.• Someone legally taking your property from

you, whether you are offered money or not, or restrictions or controls placed on your property by any government, public or local authority.

• Work done by, or on behalf of, any government or public or local authority unless the claim is for accidental physical damage.

• Mining subsidence. • Adverse possession (meaning the occupation of

any building or land either by someone trying to take possession from you or of which you are trying to take possession).

• The enforcement of a covenant by or against you (meaning the enforcement of an agreement you have entered into in connection with land you own).

• Defending a claim relating to an event that causes physical damage to property, but we will cover defending a counter-claim.

• The first £250 of any claim for legal nuisance or trespass. This is payable by you as soon as we accept the claim.

Tax protectionWhat IS coveredWe will cover the costs and expenses for you following a comprehensive examination by HM Revenue & Customs that considers all areas of your self assessment tax return, but not enquiries limited to one or more specific area.What is NOT covered• Any claim if you are self-employed or a sole

trader, or in a business partnership.• An investigation or enquiries by HM Revenue

& Customs Specialist Investigations or the HM Revenue & Customs Prosecution Office.

Jury Service and court attendanceWhat IS coveredWe will cover the costs and expenses for the following:Your absence from work:• To attend any court or tribunal at the request

of the appointed representative.• To perform jury service.The maximum we will pay is your net salary or wages for the time that you are absent from work less any amount the court gives you.What is NOT coveredAny claim if you are unable to prove your loss.

Legal defenceWhat IS coveredWe will cover the costs and expenses to defend your legal rights if an event arising from your work as an employee leads to: • You being prosecuted in a court of criminal

jurisdiction; or• Civil action being taken against you under:

– discrimination legislation. – Section 13 of the Data Protection Act 1998.

We will defend you and your family’s legal right if an event leads to your or their prosecution for an offence connected with the use or driving of a motor vehicle.What is NOT covered• Parking or obstruction fines.• The use of a motor vehicle by you or your

family for which you or they do not have valid motor insurance.

Section 5: Legal expenses

Claims procedure and conditions for your Legal expenses cover 1. Your legal representation

• On receiving a claim, if legal representation is necessary, we will appoint a preferred law firm or in-house lawyer as your appointed representative to deal with your claim. They will try to settle your claim by negotiation without having to go to court.

• If the appointed preferred law firm or our in-house lawyer cannot negotiate settlement of your claim and it is necessary to go to court and legal proceedings are issued or there is a conflict of interest, then you may choose a law firm to act as the appointed representative.

• If you choose a law firm as your appointed representative who is not a preferred law firm, we will give your choice of law firm the opportunity to act on the same terms as a preferred law firm. However, if they refuse to act on this basis, the most we will pay is the amount we would have paid if they had agreed to the DAS Standard Terms of Appointment.

• The appointed representative must co-operate with us at all times and must keep us up to date with the progress of the claim.

2. Your responsibilities• You must co-operate fully with us and the

appointed representative. • You must give the appointed

representative any instructions that we ask you to.

3. Offers to settle a claim• You must tell us if anyone offers to settle a

claim. You must not negotiate or agree to a settlement without our written consent.

• If you do not accept a reasonable offer to settle a claim we may refuse to pay further legal costs.

• We may decide to pay you the reasonable value of your claim, instead of starting or continuing legal action. In these circumstances you must allow us to take over and pursue or settle any claim in your name. You must also allow us to pursue at our own expense and for our own benefit, any claim for compensation against any other person and you must give us all the information and help we need to do so.

• Where a settlement is made on a without-costs basis we will decide what proportion of that settlement will be regarded as costs and expenses and payable to us.

4. Assessing and recovering costs• You must instruct the appointed

representative to have legal costs taxed, assessed or audited if we ask for this.

• You must take every step to recover costs and expenses and court attendance and jury service expenses that we have to pay and must pay us any amounts that are recovered.

5. Cancelling an appointed representative’s appointmentIf the appointed representative refuses to continue acting for you with good reason, or if you dismiss the appointed representative without good reason, the cover we provide will end immediately, unless we agree to appoint another appointed representative.

6. Withdrawing coverIf you settle or withdraw a claim without our agreement, or do not give suitable instructions to the appointed representative, we can withdraw cover and will be entitled to reclaim from you any costs and expenses we have paid.

7. Expert opinionWe may require you to get, at your own expense, an opinion from an expert that we consider appropriate, on the merits of the claim or proceedings, or on a legal principle. The expert must be approved in advance by us and the cost agreed in writing between you and us. Subject to this, we will pay the cost of getting the opinion if the expert’s opinion indicates that it is more likely than not that you will recover damages (or obtain any other legal remedy that we have agreed to) or make a successful defence.

8. ArbitrationIf there is a disagreement between you and us about the handling of a claim and it is not resolved through our internal complaints procedure, you can contact the Financial Ombudsman Service for help. Alternatively, there is a separate arbitration process. The arbitrator will be a barrister chosen jointly by you and us. If there is a disagreement over the choice of arbitrator, we will ask the Chartered Institute of Arbitrators to decide.

Please refer to page 41 ‘Complaints procedure’ for details of our internal complaints procedure.

1/3390307-8 (03/15) Renewal

Mortgages, Savings and Current Accounts Enquire or apply

If you’re an existing Mortgage, Savings or Current Account customer, you can service your account on if.com or by calling our Contact Centre on

Intelligent Finance Home Insurance is underwritten by St Andrew’s Insurance plc, Registered in England and Wales No. 3104671, Registered Office: 33 Old Broad Street, London, EC2N 1HZ. Legal Expenses cover is underwritten by DAS Legal Expenses Insurance Company Limited, Registered in England and Wales No. 103274, Registered Office: DAS House, Quay Side, Temple Back, Bristol BS1 6NH. Both companies are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Home Emergency cover is underwritten by Inter Partner Assistance S.A., who are a wholly owned subsidiary of AXA Assistance S.A. and part of the worldwide AXA Group. Inter Partner Assistance S.A. is authorised by the Belgian National Bank and regulated by the Financial Conduct Authority (FCA) in the UK. Inter Partner Assistance S.A. is registered in Belgium number: 394025. The UK branch registered in England and Wales No. FC008998, UK Registered Office: The Quadrangle, 106-118 Station Road, Redhill, Surrey RH1 1PR. Your calls may be recorded for accuracy of information.

0845 605 8585

0845 609 4343

INTELLIGENT FINANCE

®

HOME INSURANCE POLICY

if.comINTELLIGENT FINANCE®

www.if.com 0845 600 0401

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

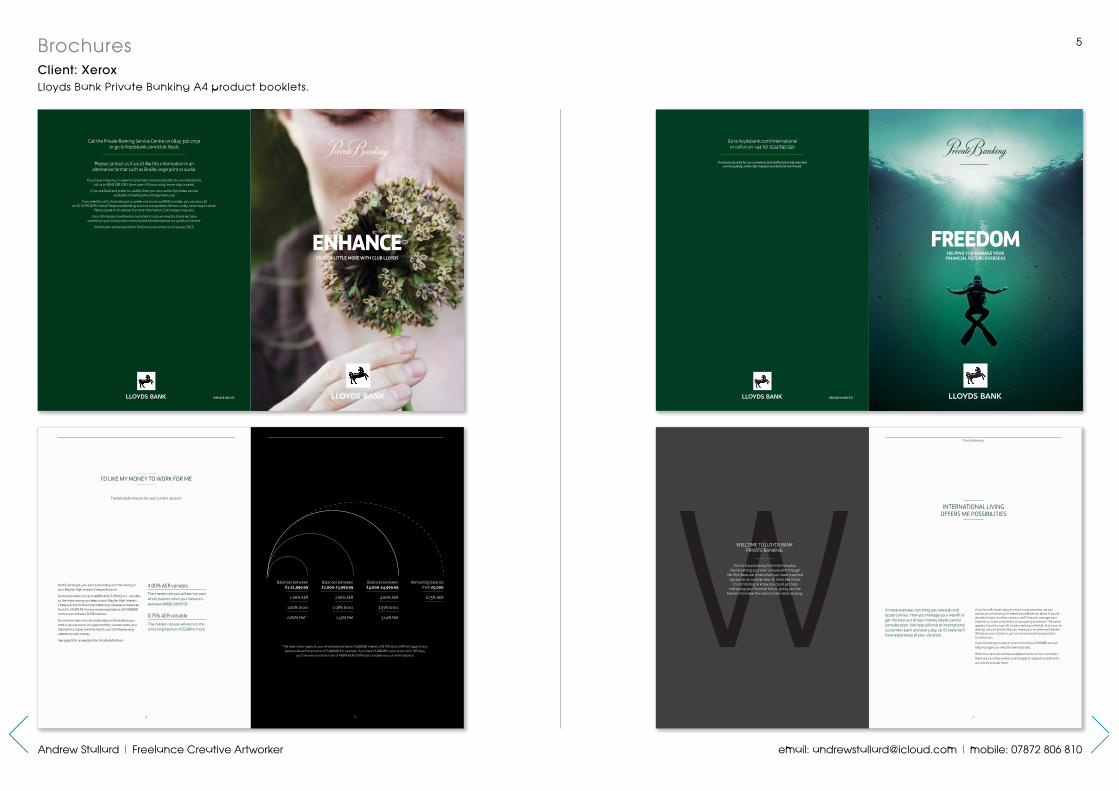

5BrochuresClient: XeroxLloyds Bank Private Banking A4 product booklets.

ENJOY A LITTLE MORE WITH CLUB LLOYDS

ENHANCE

WM1016 (01/15)

Call the Private Banking Service Centre on 0845 300 2750 or go to lloydsbank.com/club-lloyds

Please contact us if you’d like this information in an alternative format such as Braille, large print or audio.

If you have a hearing or speech impairment and would prefer to use a Textphone, call us on 0845 300 2281 (lines open 24 hours a day, seven days a week).

If you are Deaf and prefer to use BSL then you can use the SignVideo service available on lloydsbank.com/signvideo.asp

If you need to call us from abroad, or prefer not to use our 0845 number, you can also call on 0113 292 0276. Not all Telephone Banking services are available 24 hours a day, seven days a week.

Please speak to an adviser for more information. Call charges may vary.

Your call may be monitored or recorded in case we need to check we have carried out your instructions correctly and to help improve our quality of service.

Information contained within this brochure correct as of January 2015.

FREEDOMHELPING YOU maNaGE YOUr

fINaNcIaL fUtUrE OvErsEas

go to lloydsbank.com/international or call us on +44 (0) 1534 845 550

To ensure security for our customers and staff and to help maintain service quality, some calls may be recorded and monitored.

OB5100 a4 (09/13)

I’D LIKE MY MONEY TO WORK FOR ME

Tiered credit interest for your current account

With Club Lloyds, you earn extra interest on the money in your Mayfair High Interest Cheque Account.

Get tiered interest of up to 4.00% AER*/3.93% Gross** variable, so the more money you keep in your Mayfair High Interest Cheque Account, the more interest you receive on balances from £1–£4,999.99. For any remaining balance of £5,000.00 or more you will earn 0.75% interest.

Our interest rates are calculated daily on the balance you hold in your account. It is paid monthly, so even when your balance fluctuates over the month, you’ll still be earning interest on your money.

See page 9 for an explanation of rate definitions.

4.00% AER variableThe interest rate you will earn on your whole balance when your balance is between £4000-£4999.99. 0.75% AER variableThe interest rate you will earn on the remaining balance of £5,000 or more.

4

Balances between £1-£1,999.99

1.00% AER

1.00% Gross

0.80% Net***

Balances between £2,000-£3,999.99

2.00% AER

1.98% Gross

1.59% Net

Balances between £4,000-£4,999.99

4.00% AER

3.93% Gross

3.14% Net

Remaining balance from £5,000

0.75% AER

The rates shown apply to your whole balance below £5,000.00. Interest of 0.75% Gross/AER will apply to any balance above the amount of £5,000.00. For example, if you have £4,000.00 in your account for 365 days,

you’ll receive an interest rate of 4.00% AER/3.93% Gross variable on your entire balance.

5

welcome to lloyds bank private banking

you’ve stepped away from the everyday. you’re carving your own unique path through

life. but there are times when you need a second opinion or an outside view. at times like these,

it’s comforting to know you could get help managing your financial future, giving you the

freedom to make the most of international living.

international living offers me possibilities

a move overseas can bring you rewards and opportunities. How you manage your wealth to get the best out of your money needs careful consideration. we help all kinds of international customers each and every day, so it’s likely we’ll have experience of your situation.

if you’re a Uk citizen about to start living overseas, we can advise you on what you’ll need to do before you leave. if you’re already living in another country, we’ll help you manage your finances to cover school fees or a property purchase. the same applies if you’re a non-Uk citizen working in the Uk. and if you’re retiring, we can aim to help you make your income work harder. whatever your situation, we can recommend tax specialists to advise you.if you’re looking to save or invest more than £250,000, we can help manage your wealth internationally.

whilst our services will be available to many of our customers, there are countries where, due to legal or regulatory restraints, we cannot provide them.

private banking

1

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

6BrochuresClient: DS Print & RedesignUgg Retail Training Guide.

Spring 2013

retail training guideConfidential and proprietary material

— for internal uSe only —

tHanK youThank you for taking the time to educate yourself and gain a thorough understanding of the UGG australia

brand and products. This not only makes you a better salesperson, but also a better representative of the

UGG brand. Remember, this training guide is meant to be used as a resource tool that can be used to review

or search and locate the information you need.

Core footWearWoMen’s fooTWeaR 17

fe B r UarY: i s l a Co lleC ti o n

from warm-weather sandals to transitional essentials, the ultra-comfortable Isla Collection is back with a

variety of wedge finishes. showcasing accents like woven straps and snake-print burlap, this Marrakech-inspired

assortment offers something for every occasion, including everyday bright espadrilles, beautiful exotics, and

intricate basket weaves.

Highlighted spring ’13 features:

ww 100% natural jute wrapped midsole (Lucianna, Lucianna Marrakech, Lauri, Tawnie, Callia)

ww antiqued leather-wrapped platform wedge (Doha, Assia, Hamra), nubuck suede wrapped midsole (Toura), midsole wrap combining exotic snake printed burlap and nubuck suede (Ariah)

ww Insole: leather wrapped Poron® foam cushioning for comfort

ww Woven peep-toe bootie with elastic gore cut-outs, rear-zip for individual fit (Hamra)

ww outsole: 4 ½” wedge heel with a 1 ½” platform and cork infused rubber outsole

Key styles: Lucianna, Lucianna Marrakech, Lauri, Tawnie, Toura, Ariah, Assia, Noella

fe B r UarY: ad e ll a Co lleC ti o n

The adella Collection features essential sandal silhouettes combined with unexpected softness. Heavily

cushioned footbeds and fully leather-lined uppers keep feet stylish and comfortable all day long. new to the

collection — the elyza II features metallic leather uppers with metallic tencel cutouts, while the Vivyan showcases

nubuck leather with Moroccan-inspired laser-cutout patterns.

Highlighted spring ’13 features:

ww Insole: 3mm of Poron® plus 2mm of eVa with buttery-soft leather sock cover

ww outsole: Molded rubber outsole with allover UGG logo pattern

ww luxurious leather uppers

ww Heavily cushioned footbeds

Key styles: Salah, Vivyan II, Mireya, Elyza II

BrochuresClient: DS Print & RedesignCity Lit Course Guide.

Shaftesb

ury Av

enue

Kea

n St

Wild St

Monm

outh St

Bloomsbury

Square

Montague St

Bedford Pl

Bow St

Endell St

Drury LaneKee

ley St

Kemble

St

Mac

klin S

t

Parke

r St

Shorts

Gard

ens Gre

at Q

ueen

St

Long

Acre

Long

Acre

Great Russe

ll St

Bloomsbury Way

High Holborn

High Holborn

Bloomsbury St

Southampton Row

Kingsway

Stukeley S

tNew Oxford St

Oxford St

Rathbone Place

Gresse St

Tottenham C

ourt Rd

Holborn

CoventGarden

TottenhamCourt Road

1

2

3

4

St Giles High St

www.citylit.ac.uk

City LitKeeley Street, Covent Garden, London WC2B 4BA

Enrolment: 020 7831 7831 Switchboard: 020 7492 2600 Fax: 020 7492 2735 Email: [email protected]

Access: fully accessible for people with disabilities.

Other locationsEC (European College) 7–11 Stukeley Street, London WC2B 5LB

Photography studio 9 Kean Street, London WC2B 4AY

The Fashion Retail Academy 15 Gresse Street, London W1T 1QL

Have you finished with this guide?Don’t bin it! Add it to your recycling, or pass it on to a friend.

Students with visual impairmentsIf you would like information in Braille, large print or on audio, please contact the Access to Learning team on 020 7492 2506.

The City Literary Institute, a company limited by guarantee, registered in England No. 2471686. Registered office 1-10 Keeley Street, London WC2B 4BA. Registered Charity No. 803007. Design by Roundel.

City Lit main site

European College

Photography studio

Fashion Retail Academy

1

2

3

4

City Lit sum

mer course g

uide 2013

ww

w.citylit.ac.uk www.citylit.ac.uk

Where London learns...this summerSummer shortsCourses from July–Aug 2013

Where London learns...

CIT_2204_Summer_Courses_Guide_Cover_AW.indd 1 25/04/2013 12:06

Shaftesb

ury Av

enue

Kea

n St

Wild St

Monm

outh St

Bloomsbury

Square

Montague St

Bedford Pl

Bow St

Endell St

Drury LaneKee

ley St

Kemble

St

Mac

klin S

t

Parke

r St

Shorts

Gard

ens Gre

at Q

ueen

St

Long

Acre

Long

Acre

Great Russe

ll St

Bloomsbury Way

High Holborn

High Holborn

Bloomsbury St

Southampton Row

Kingsway

Stukeley S

tNew Oxford St

Oxford St

Rathbone Place

Gresse St

Tottenham C

ourt Rd

Holborn

CoventGarden

TottenhamCourt Road

1

2

3

4

St Giles High St

www.citylit.ac.uk

City LitKeeley Street, Covent Garden, London WC2B 4BA

Enrolment: 020 7831 7831 Switchboard: 020 7492 2600 Fax: 020 7492 2735 Email: [email protected]

Access: fully accessible for people with disabilities.

Other locationsEC (European College) 7–11 Stukeley Street, London WC2B 5LB

Photography studio 9 Kean Street, London WC2B 4AY

The Fashion Retail Academy 15 Gresse Street, London W1T 1QL

Have you finished with this guide?Don’t bin it! Add it to your recycling, or pass it on to a friend.

Students with visual impairmentsIf you would like information in Braille, large print or on audio, please contact the Access to Learning team on 020 7492 2506.

The City Literary Institute, a company limited by guarantee, registered in England No. 2471686. Registered office 1-10 Keeley Street, London WC2B 4BA. Registered Charity No. 803007. Design by Roundel.

City Lit main site

European College

Photography studio

Fashion Retail Academy

1

2

3

4

City Lit sum

mer course g

uide 2013

ww

w.citylit.ac.uk www.citylit.ac.uk

Where London learns...this summerSummer shortsCourses from July–Aug 2013

Where London learns...

CIT_2204_Summer_Courses_Guide_Cover_AW.indd 1 25/04/2013 12:06

3

Get in touch

Enrolment

020 7831 7831Switchboard

020 7492 2600

Or stay at City Lit and enjoy

Mojo Café Ground fl oorWith its selection of hot and cold drinks, cooked meals, sandwiches and snacks, our café is a good place to recharge and meet other students.

Supported learning centre MezzanineBrowse through our broad selection of books, journals, CDs, videos and DVDs covering a wide array of subjects and ideas, or work at one of the computer stations.

Sonia’s Garden Fourth fl oor Our cosy rooftop oasis is always a popular spot to relax or catch up with classmates in the open air. It’s named after our receptionist, Sonia, who designed the garden.

Lincoln’s Inn Field – 5 minsRelax in the leafy surroundings of London’s largest public square that’s always a crowd-puller once the sun comes out. Check out Barry Flanigan’s giant abstract sculpture ‘Camdonian’ in the north-east corner of the square.

Hunterian Museum – 5 minsAlso on Lincoln’s Inn Fields, this curious collection of medical and anatomical marvels is located in the grand premises of The Royal College of Surgeons of England.

Somerset House – 5 minsFrom refreshing fountains in the summer to winter ice-skating in stunning surroundings, this former royal palace also hosts free and paid exhibitions, an outdoor fi lm season, live music and more.

Courtauld Gallery – 7 minsFound within Somerset House, this art collection is dominated by Impressionist and Post-Impressionist work including paintings by Cézanne, Manet, Renoir, Van Gogh and Gauguin, with temporary exhibitions also drawing in the crowds.

St George’s Bloomsbury – 7 minsNicholas Hawksmoor’s Grade II listed church comes complete with lions, unicorns and King George I on its unusual steeple. It is usually open weekdays from 13:00–16:00 and also hosts free music concerts.

Covent Garden Market – 7 minsOne of London’s star attractions, there’s something for everyone in and around the famous piazza, from the selection of artisan goods on sale, the diverse street performances, or a chance to relax and people watch from one of the numerous pavement cafes.

Out and about at lunchtime

Make the most of lunchtime and take time out to explore our central London neighbourhood during your break, or before or after class. From contemporary art to iconic artefacts or an array of open spaces, there’s a lot to see and do around City Lit.

©Th

e C

our

taul

d G

alle

ry

©Th

e H

unte

rian

Co

llect

ion

Room 2 featuring The Courtauld Gallery’s Renaissance collection.

Crocodile and egg from Hunterian Collection

Win a weekend course from our summer school programme

To enter, just tweet: ‘I want to win a City Lit summer course’ using hashtag #citylitsummer and we’ll pick a tweet at random. Terms and conditions, and course ideas, on our website www.citylit.ac.uk

CIT_2204_Summer_Courses_Guide_Final_AW.indd 3 25/04/2013 12:12

2

Summer in the city

Fancy doing a summer short course but don’t know what to choose? Here’s ten short, fun courses to inspire you:

R 74 R 24

R 37 R 79

R 82 R 127

R 68 R 30

R 37 R 113

12345 10

9876Summer wine Puppetry

Design a small urban garden

Soap making (aromatherapy)

Film comedy Do black holesreally exist

Hip hop (dance) Superhero life drawing

Make a silver bangle

Ukulele

City Lit picks: fi ve top exhibitions

One of the world’s most culturally diverse cities, there’s always something new to see and do in London. Here’s our fi ve top picks for things to see this summer.

David Bowie IsThe Victoria and Albert Museum23 March–11 AugustOne of City Lit’s famous former students is the subject of a major retrospective that focuses on items from his personal archive.

www.vam.ac.uk

Lowry and the Painting of Modern LifeTate Britain26 June–20 OctoberFamous for his depictions of urban street scenes of Salford, painter LS Lowry (1887–1976) receives his fi rst posthumous retrospective, with around 80 works being brought together for the fi rst time.

www.tate.org.uk

Jerwood Makers Open 2013 Jerwood Space10 July–25 AugustApplied artists Maisie Broadhead, Linda Brothwell, Adam Buick, Nahoko Kojima and Roanna Wells reveal their work after winning Jerwood Makers Open commissions in this annual competition.

www.jerwoodspace.co.uk

Life and Death in Pompeii and HerculaneumBritish Museum28 March–29 SeptemberThis major show brings together over 200 objects discovered at Pompeii and Herculaneum, Roman towns engulfed by ash from Mount Vesuvius in AD79.

www.britishmuseum.org

Summer ExhibitionRoyal Academy10 June–18 AugustAn annual event since 1769, the summer exhibition allows amateur and emerging artists to show work next to some of the art world’s biggest names, in what is always a highly diverse experience.

www.royalacademy.org.uk

Art

ist:

Des

ign

by

Bri

an D

uffy

and

Cel

ia P

hilo

, m

ake

up b

y Pi

erre

La

Ro

che.

Dat

e: 1

973

© D

uffy

Arc

hive

© N

aho

ko K

ojim

a

Wal

ker A

rt G

alle

ry (L

iver

po

ol,

UK

)

Nahoko Kojima, The Cloud LeopardHandmade paper cut, 210cm x 110cm

L.S. Lowry The Fever Van 1935

Album cover shoot for Aladdin Sane

City Lit summer course guide 2013

CIT_2204_Summer_Courses_Guide_Final_AW.indd 2 25/04/2013 12:11

49Computing and digital communication

Find out more about your course. For a detailed outline enter the course code at www.citylit.ac.uk or call 020 7492 2600

Code Date(s) Day(s) Time Week(s) Site Fee Snr. Conc.

Basic computing

Computing: getting startedAn easy way to learn how to use a computer. You will be introduced to the basic features of Windows and the most frequently used software. Ideal if you’ve never used a computer before.

CAB04 8 Jul–22 Jul Mon & Tue 10:30–13:30 3 KS £105 £60 £43

The internet

Internet/email getting startedLearn how to surf the internet and use email in a friendly and supportive group. Knowledge required: ability to use a mouse and keyboard.

CIN04 23 Jul–6 Aug Mon & Tue 10:30–13:30 3 KS £105 £60 £43

Summer internet café Come and use the internet for your own projects in a supportive environment.

CSC01 3 Jul–7 Aug Wed 14:00–16:30 6 KS £54 £31 £22

Mobile devicesiPad and iPhone

iPad getting started Get to know the basic features of your iPad, use the touchscreen and learn how to interact with it and organise your tablet desktop.

CPD04 5 Aug Mon 14:00–17:00 1 KS £21 £12 £9

iPad moving on Learn to set up WiFi and email, surf the web, and save and organise web pages.

CPD05 6 Aug Tue 14:00–17:00 1 KS £21 £12 £9

iPhone and iPad: how to download appsLearn how to download and manage apps on your iPad or iPhone.

CPD06 15 Aug Thu 14:00–17:00 1 KS £21 £12 £9

iPhone and iPad workshop Troubleshoot common iPhone and iPad issues in a friendly and supportive environment.

CPD07 16 Aug Fri 14:00–17:00 1 KS £21 £12 £9

Tablets and laptops

Choosing a laptop Are you thinking of buying a laptop but don’t know where to start? There are hundreds of laptops to choose from and we can help you find the right one.

CLP01 14 Jul Sun 10:30–14:00 1 KS £25 £14 £10

Choosing a tablet Thinking about buying a tablet but don’t know where to start? This course will help you. We’ll outline the options available and what you should look for to get the right tablet to suit your needs.

CTA01 21 Jul Sun 10:30–14:00 1 KS £25 £14 £10

CIT_2204_Summer_Courses_Guide_Final_AW.indd 49 25/04/2013 12:12

48

Working with PCs, Macs and mobile devices, our summer courses range from beginner to advanced levels. We offer traditional Microsoft Office skills, computer programming, web and social media as well as guides for buying and making the best use of various digital devices.

All computing courses are taught by friendly, dedicated and experienced tutors who also offer bespoke IT training courses that can be delivered in your workplace.

See also computer-based visual arts courses in the ‘Photoshop, Illustrator and InDesign’ section, page 41.

Computing and digital communication

How to enrol – Online at www.citylit.ac.uk– Call us on 020 7831 7831– Pop in and enrol in person– Fill in and post the enrolment

form in the back of this brochure

Department contact020 7492 [email protected]

Telephone hoursMon–Fri 10:00–17:00

If your course is starred (eg CED01*) you will need to attend an interview with the Computing department so that you can be placed on the right course for you. ECDL interviews are held during the day and evening. Please contact the Computing department to book your appointment.

Computing drop in course advice times Tue 17:30–18:30Wed 12:30–13:30

ContentsBasic computing 49The internet 49Mobile devices 49Windows and file management 50Digital tools 50Courses leading to a qualification 50Microsoft applications 50Safety and security 52Technical computing 52Programming 52Web page design 52Desktop and digital publishing 53Design and illustration 53Open source software 54Vblogging 54Social media 54Business computing 55Buying and selling online 56Explore your interests using a computer 56

City Lit summer course guide 2013

CIT_2204_Summer_Courses_Guide_Final_AW.indd 48 25/04/2013 12:12

BODYAMRFriday 19 15:15h

www.bodyamr.com

Press: T: +44 (0)20 7691 2085

Sales: T: +44 (0)79 3281 5786

David Koma

Friday 19 14:15h

www.davidkoma.com

Press: T: +44 (0)20 7331 1421

Sales:T: +44 (0)77 6819 5428

Prophetik

Friday 19 13:00h

www.prophetik.com

Press: T: +44 (0)20 7495 3390

Sales: T: +1 (0)61 5554 2248

This season, Vauxhall Fashion Scout is expanding and is hosting a

new Exhibition space. Held in the beautiful Prince Regent room in

Freemasons’ Hall, the exhibition features 16 great designers and is

open 10.00 – 19.00 Sat 20th – Tue 23rd Feb.

We are also very excited to announce our presence at Paris

Fashion Week, with our brand new Paris Showroom based in the

centre of the Marais. Located in a spacious and bright artist’s

studio the showroom will run from Fri 5th- Mon 8th March and

features a selection of the best innovative designers.

Finally, Vauxhall Fashion Scout’s London event is the home of

the Off-Schedule Media Centre. Featuring free laptops and high

speed Wi-Fi the media centre enables industry access to all

Off-Schedule designers during Fashion Week. This popular

haven, funded by the London Development Agency’s Fashion

Showcasing Fund, also provides much needed respite and a

space to relax.We are extremely proud to present an exciting, varied

showcase of outstanding talent this season. A champion of

innovation, we can’t wait to see what the future holds for this

bright new generation of designers.

The Team at Vauxhall Fashion Scout

web: www.vauxhallfashionscout.com

blog: www.thefashionscout.com

As the driving force behind the best innovative designers, Vauxhall

Fashion Scout selects the finest designers and showcases their

talents to a global audience. Throughout the year we nurture and

develop these designers through our mentoring programme -

creating successful and sustainable fashion businesses. Returning this season is the hotly anticipated Merit Award with the

winner, CSM alumni Hermione de Paula, following in the successful

footsteps of our previous winners William Tempest and David Koma.

Ones to Watch, one of London’s leading group shows, is also

returning with designers ASKH, David Longshaw, Eudon Choi and

Florencia Kozuch making their LFW catwalk debut. Providing a

platform for our pick of the most cutting edge, exciting new designers,

this is a chance to catch a first glimpse of raw talent in the making.

HOLBORN

FREEMASONS’ HALL60 GREAT QUEEN STLONDON WC2B 5AZ4 MINUTES WALK FROM SOMERSET HOUSE

Pict

ure

front

cov

er: H

erm

onie

de P

aula

/ De

sign:

And

rea

Padr

ó

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

7BrochuresClient: Vauxhall Fashion ScoutLondon Fashion Week Guide.

Danny TangFriday 19 16:15h

www.danny-tang.com Press: T: +44 (0)20 8947 5475 E: [email protected] Sales: T: +44 (0)20 7737 6433 E: [email protected]

Gemma Slack PRESENTATION

www.gemmaslack.comPress: T: +44 (0)20 7436 9449 E: [email protected]: T: +44 (0)20 7377 6030 E: [email protected]

Friday 19 17:00-20:00h

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

8CalendarsClient: XeroxHalifax 2015 Calendar.

CALENDAR2015

INTERNAL USE ONLY

MARCH2015M T W T F S S

12 3 4 5 6 7 89 10 11 12 13 14 1516 17 18 19 20 21 2223 24 25 26 27 28 2930 31

INTERNAL USE ONLY

After the death of her husband, I took time to review my customer’s accounts with her. She said she’d prefer to have everything with the Halifax. So, we transferred her current account and home insurance making her £500 better off over the year. She was also delighted to receive the £100 switcher reward.

Scott Porter Banking Consultant, Eccles Branch

“ ”

}

+

=

JANUARY2015M T W T F S S

1 2 3 45 6 7 8 9 10 1112 13 14 15 16 17 1819 20 21 22 23 24 2526 27 28 29 30 31

INTERNAL USE ONLY

My customer had a credit card with a competitor with an interest rate over 25% – she’d just used it to pay for her annual holiday. I told her about our Clarity card and, as it met her needs, she quickly switched saving her interest and card usage fees on her holiday.

Chloe Brewer Customer Adviser, Morley Branch

“ ”

APRIL2015M T W T F S S

1 2 3 4 56 7 8 9 10 11 1213 14 15 16 17 18 1920 21 22 23 24 25 2627 28 29 30

INTERNAL USE ONLY

My customer wanted to pay a bill so we showed him how to set up a Faster Payment. Whilst in the branch he received a text to confirm the payment. He was amazed at the speed of the process and we heard him saying to another customer ‘Why would you want to bank anywhere else but here?’

Sarah-Louise Broughton Counter Support, Potters Bar Branch

“ ”

FEBRUARY2015M T W T F S S

12 3 4 5 6 7 89 10 11 12 13 14 1516 17 18 19 20 21 2223 24 25 26 27 28

INTERNAL USE ONLY

I helped my customer transfer his mortgage from Barclays to the Halifax reducing his payment by £400 a month and term by seven years. As a result he told me he’d be able to retire early!

Lauren Van Leer Customer Adviser, Northallerton Branch

“ ”

MAY2015M T W T F S S

1 2 34 5 6 7 8 9 1011 12 13 14 15 16 1718 19 20 21 22 23 2425 26 27 28 29 30 31

INTERNAL USE ONLY

My customer wasn’t confident using his computer. I showed him step-by-step how to use Online Banking so he could do his banking from home. He was thrilled that the next month he didn’t need to make the journey into town.

Katie Willis Banking Consultant, Luton Branch

“ ”

+

-

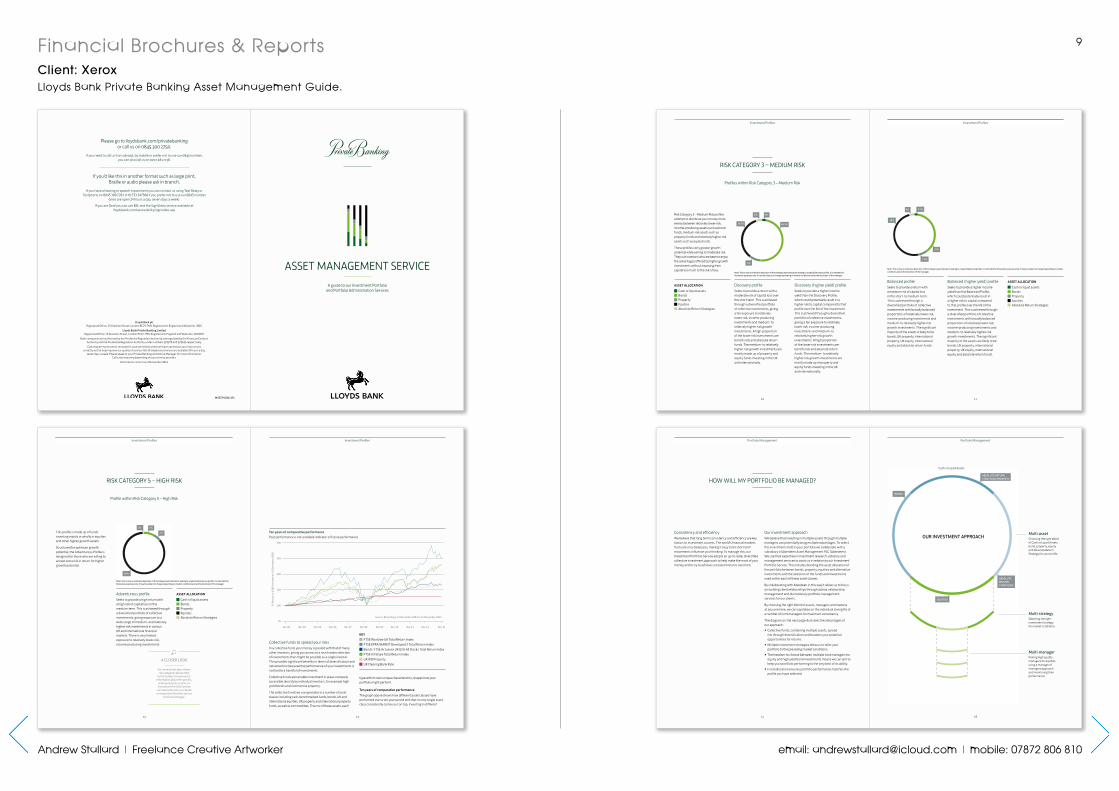

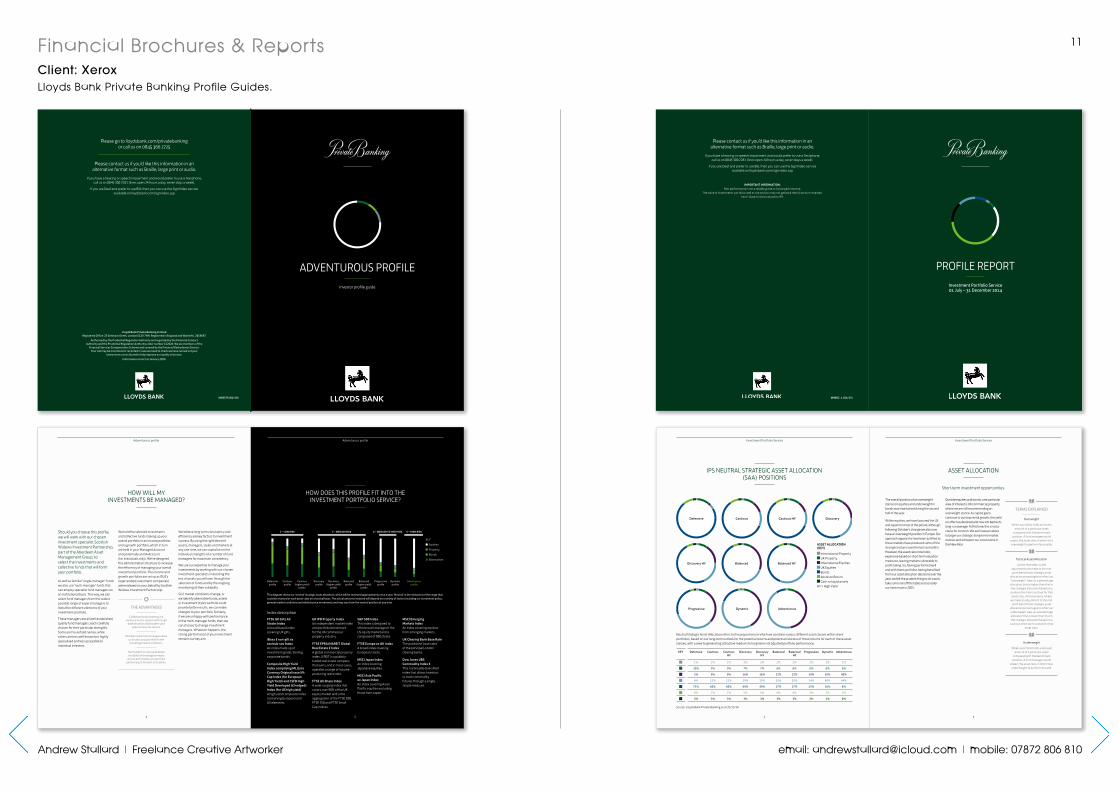

9Financial Brochures & ReportsClient: XeroxLloyds Bank Private Banking Asset Management Guide.

Andrew Stallard | Freelance Creative Artworker email: [email protected] | mobile: 07872 806 810

P R I V AT E B A N K I N G

ASSET MANAGEMENT SERVICE A guide to our Investment Portfolio

and Portfolio Administration Services

M55574 (01/15)

Please go to lloydsbank.com/privatebanking or call us on 0845 300 2750.

If you need to call us from abroad, by mobile or prefer not to use our 0845 number, you can also call us on 0207 4812138.

If you’d like this in another format such as large print, Braille or audio please ask in branch.

If you have a hearing or speech impairment you can contact us using Text Relay or Textphone on 0845 300 2281 or 01733 347500 if you prefer not to use our 0845 number

(lines are open 24 hours a day, seven days a week).

If you are Deaf you can use BSL and the SignVideo service available at lloydsbank.com/accessibility/signvideo.asp

Lloyds Bank plc Registered Office: 25 Gresham Street, London EC2V 7HN. Registered in England and Wales No. 2065.

Lloyds Bank Private Banking Limited Registered Office: 25 Gresham Street, London EC2V 7HN. Registered in England and Wales No. 2019697.

Both companies are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under numbers 119278 and 122626 respectively.Calls may be monitored or recorded in case we need to check we have carried out your instructions

correctly and to help improve our quality of service. Not all telephone services are available 24 hours a day, seven days a week. Please speak to your Private Banking and Advice Manager for more information.

Call costs may vary depending on your service provider.Information correct as of November 2014.