Anand Rathi Jan 11

44

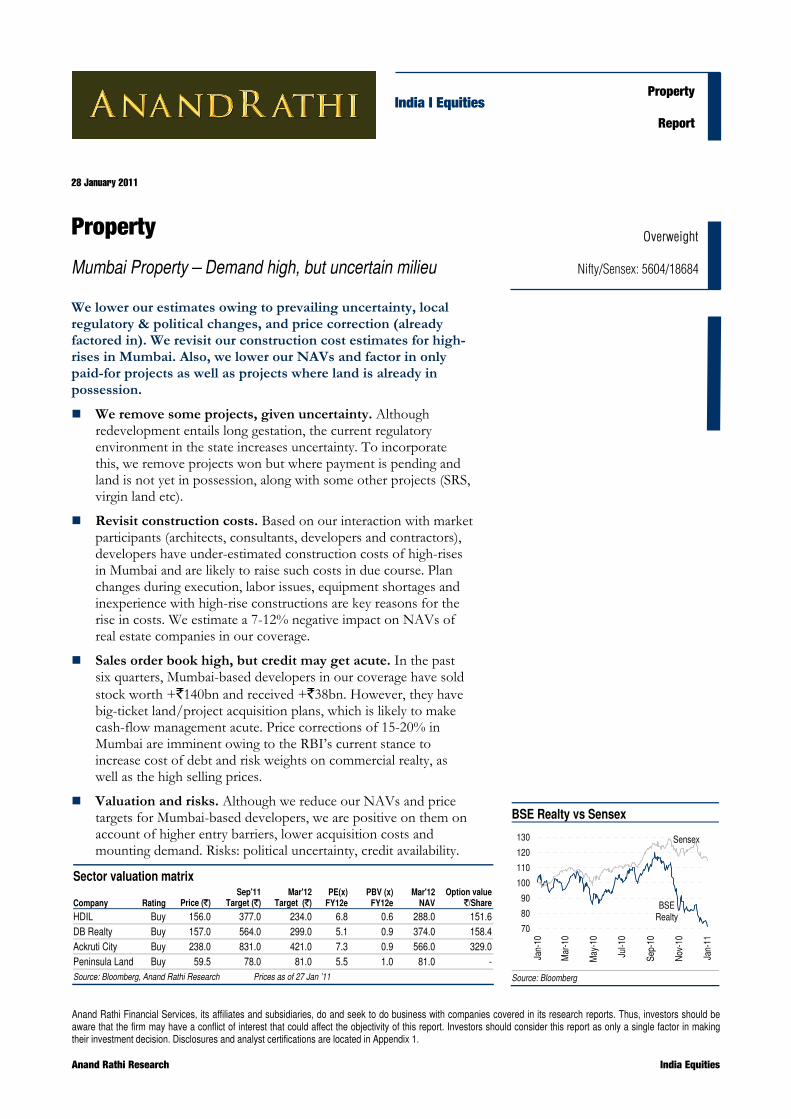

Anand Rathi Financial Services, its affiliates and subsidiaries, do and seek to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Disclosures and analyst certifications are located in Appendix 1. Anand Rathi Research India Equities India I Equities Property Report 28 January 2011 Property Mumbai Property – Demand high, but uncertain milieu We lower our estimates owing to prevailing uncertainty, local regulatory & political changes, and price correction (already factored in). We revisit our construction cost estimates for high- rises in Mumbai. Also, we lower our NAVs and factor in only paid-for projects as well as projects where land is already in possession. We remove some projects, given uncertainty. Although redevelopment entails long gestation, the current regulatory environment in the state increases uncertainty. To incorporate this, we remove projects won but where payment is pending and land is not yet in possession, along with some other projects (SRS, virgin land etc). Revisit construction costs. Based on our interaction with market participants (architects, consultants, developers and contractors), developers have under-estimated construction costs of high-rises in Mumbai and are likely to raise such costs in due course. Plan changes during execution, labor issues, equipment shortages and inexperience with high-rise constructions are key reasons for the rise in costs. We estimate a 7-12% negative impact on NAVs of real estate companies in our coverage. Sales order book high, but credit may get acute. In the past six quarters, Mumbai-based developers in our coverage have sold stock worth +`140bn and received +`38bn. However, they have big-ticket land/project acquisition plans, which is likely to make cash-flow management acute. Price corrections of 15-20% in Mumbai are imminent owing to the RBI’s current stance to increase cost of debt and risk weights on commercial realty, as well as the high selling prices. Valuation and risks. Although we reduce our NAVs and price targets for Mumbai-based developers, we are positive on them on account of higher entry barriers, lower acquisition costs and mounting demand. Risks: political uncertainty, credit availability. Overweight Nifty/Sensex: 5604/18684 BSE Realty vs Sensex BSE Realty Sensex 70 80 90 100 110 120 130 Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Source: Bloomberg Sector valuation matrix Company Rating Price (`) Sep'11 Target (`) Mar'12 Target (`) PE(x) FY12e PBV (x) FY12e Mar'12 NAV Option value `/Share HDIL Buy 156.0 377.0 234.0 6.8 0.6 288.0 151.6 DB Realty Buy 157.0 564.0 299.0 5.1 0.9 374.0 158.4 Ackruti City Buy 238.0 831.0 421.0 7.3 0.9 566.0 329.0 Peninsula Land Buy 59.5 78.0 81.0 5.5 1.0 81.0 - Source: Bloomberg, Anand Rathi Research Prices as of 27 Jan ’11

Transcript of Anand Rathi Jan 11

Anand Rathi Financial Services, its affiliates and subsidiaries, do and seek to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Disclosures and analyst certifications are located in Appendix 1. Anand Rathi Research India Equities

India I Equities Property

Report

28 January 2011

Property

Mumbai Property – Demand high, but uncertain milieu

We lower our estimates owing to prevailing uncertainty, local regulatory & political changes, and price correction (already factored in). We revisit our construction cost estimates for high-rises in Mumbai. Also, we lower our NAVs and factor in only paid-for projects as well as projects where land is already in possession.

We remove some projects, given uncertainty. Although redevelopment entails long gestation, the current regulatory environment in the state increases uncertainty. To incorporate this, we remove projects won but where payment is pending and land is not yet in possession, along with some other projects (SRS, virgin land etc).

Revisit construction costs. Based on our interaction with market participants (architects, consultants, developers and contractors), developers have under-estimated construction costs of high-rises in Mumbai and are likely to raise such costs in due course. Plan changes during execution, labor issues, equipment shortages and inexperience with high-rise constructions are key reasons for the rise in costs. We estimate a 7-12% negative impact on NAVs of real estate companies in our coverage.

Sales order book high, but credit may get acute. In the past six quarters, Mumbai-based developers in our coverage have sold stock worth +`140bn and received +`38bn. However, they have big-ticket land/project acquisition plans, which is likely to make cash-flow management acute. Price corrections of 15-20% in Mumbai are imminent owing to the RBI’s current stance to increase cost of debt and risk weights on commercial realty, as well as the high selling prices.

Valuation and risks. Although we reduce our NAVs and price targets for Mumbai-based developers, we are positive on them on account of higher entry barriers, lower acquisition costs and mounting demand. Risks: political uncertainty, credit availability.

Overweight

Nifty/Sensex: 5604/18684

BSE Realty vs Sensex

BSE Realty

Sensex

70

80

90

100

110

120

130

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

11

Source: Bloomberg

Sector valuation matrix

Company Rating Price (`) Sep'11

Target (`) Mar'12

Target (`) PE(x) FY12e

PBV (x) FY12e

Mar'12 NAV

Option value `/Share

HDIL Buy 156.0 377.0 234.0 6.8 0.6 288.0 151.6 DB Realty Buy 157.0 564.0 299.0 5.1 0.9 374.0 158.4 Ackruti City Buy 238.0 831.0 421.0 7.3 0.9 566.0 329.0 Peninsula Land Buy 59.5 78.0 81.0 5.5 1.0 81.0 -Source: Bloomberg, Anand Rathi Research Prices as of 27 Jan ’11

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 2

We remove some projects, given uncertainty Mumbai property developers, unlike peers in NCR and Bangalore, primarily use the rehabilitation/redevelopment route for development of property. This involves greater dependence on the regulatory and political machinery. Hence, project durations are lengthened and policy-dependent. Although we estimate longer gestation periods for such projects, given the current changes, we introduce further discounts in certain projects till clarity emerges on policies. Also, we remove from our valuation projects won but where payment is pending and land is not yet in possession, along with some other projects (SRS, virgin land etc). Such changes impact our NAVs and estimates for companies in our coverage.

Introduce discounts

On developable area

Mumbai-centered property developers largely follow the rehabilitation and redevelopment routes to property development – As many as 53% of regulated developers follow this. Although developers are using different routes/schemes for the maximum possible developable area on a plot, approvals for some projects with the same area would be difficult to obtain, given changes in government stance and infrastructure bottlenecks. Such projects could decrease in future or higher premiums would require to be paid. Such delays are likely to increase costs.

Given opaqueness in the sector and changes in recent government policies, we introduce a discount till further clarity emerges regarding disclosed projects of the developers.

On projects

We alter our position on development projects announced. We remove from our valuation projects won but where payment is pending and land is not yet in possession, given the potential for delays in land acquisition or in clearances/encroachments. Also, delay in some projects under construction, which could delay/affect rights to land parcels in future, have been removed from our project valuations.

Further, for virgin-land projects, where land has already been acquired but launch visibility is distant, we alter our position to include a certain premium to book value vs. initial development schedules assumed, as done for non-Mumbai developers.

53% of the organized developers in Mumbai follow the rehabilitation/

redevelopment route to property development

Fig 1 – Change in stance – SRS / re-development / PPP projects Company Project Earlier Now Remark

DB Realty Bandra (E) Gov Colony Development Value Removed LoA got, premium not paid yet

Ackruti City Bandra (E) Gov Colony Development Value Removed LoA got, premium not paid yet

HDIL Airport 65 acres Development Value Removed Delay in shifting, visibility on land not clear

Unitech Various Mumbai projects Development Value Removed Little movement (Ex Golibar, Andheri, Jogeshwari projects)

DB Realty PCMC Development Value Development Value Land under possession; approval delayed

Ackruti City Gujrat Biotech phase 3 Development Value Removed Phase 2 work slow; no visibility on Phase 3

Orbit Corp Kilachand House Development Value Removed Acquisition to be completed, under llegal process

Source: Anand Rathi Research

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 3

Slum-rehabilitation projects and redevelopment projects in Mumbai also entail more litigation/legal cases than virgin-land projects in Mumbai or other cities. Although property development involves legal hassles, timely clearances are also an issue.

Recent regulatory changes

Suburban FSI likely to go up

The government of Maharashta in its winter session in Dec ’10 gave in-principle clearance to increased FSI in suburban Mumbai, from 1 to 1.33. At the same time, it kept the cap of 2 on total development. Although, the official regulation paper has yet to come, this reduces demand for TDR (assuming same construction) by 0.33x.

In addition to dependence on construction activity in Mumbai, prices of TDR would depend on the premium charged on FSI in micro-markets. We await clarity on this.

Developers affected: HDIL, DB Realty

Rethinking on public parking schemes - DCR 33(24)

The government is also rethinking the higher FSI given in lieu of providing public parking to MCGM (Municipal Corporation of Greater Mumbai) free of cost. This re-consideration takes into account the infrastructure bottlenecks in south-central Mumbai, where most such schemes were cleared. Although projects in the approval stage are likely to be cleared, the area cleared and FSI awarded could change.

Tax exemption for FSI sales, post-rehabilitation

As per an amendment to Finance Bill 2010, slum-rehab projects cleared before Mar ’08 and post-rehab FSI sales falling under Sec 80 I(B) would get complete tax benefits. Developers who could avail of such benefits are HDIL and Ackruti City.

Fig 2 – Change in stance: virgin land projects Company Project Earlier Now Remark

DB Realty Mira Road Development Premium to book value Land conversion to be done; launch likely to be delayed

DB Realty Sangamwadi Development Book Value Land acquisition still on; land conversion to be done

Ackruti City Panvel, Uran Khalapur Premium to book value Premium to book value in line with land sold recently

HDIL Vasai - Virar Premium to book value Premium to book value in line with land sold recently

HDIL Kochi, Hyd Book Value Book Value JDA projects, money paid nil, minimum

DLF HSIDC Development Book Value paid Land change to be done; 10% of total money paid

Source: Anand Rathi Research

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 4

Construction costs: underestimated We re-visit our construction-cost estimates for high-rises planned in the city. Our interaction with architects, consultants, contractors and developers lead us to believe that most present project costs have been under-estimated by developers and are likely to be raised, as in the past. Plan changes during execution, labor issues, equipment shortages and lack of experience in high-rise constructions are the key reasons for rise in construction costs. Our NAVs for Mumbai developers, therefore, drop 7-12%.

Evaluating cost pressures

Looking at construction-cost hikes by developers recently and in the past two years, we met contractors, consultants, architects and developer teams to evaluate construction timelines and costs for proposed high-rises planned or to be constructed in the next few years. We believe developers today have under-estimated construction costs, which would need to be increased 40-90% in coming years.

Fig 3 – Increase in construction costs as one goes higher No of Floors Const Cost (`/ sqft)

30 3,000

50 4,750

70 6,500

90 8,250

110 10,000

130 11,750

Source: Industry, Anand Rathi Research

Key reasons for increase in costs

Regulatory approvals are the biggest hindrance to starting construction. Equally, the time to finalize plans also leads to delays in construction and rise in prices. Lately, most large developers in Mumbai, particularly those with land parcels in South and South-Central Mumbai, have aimed at developing high-rises (towers of 60 floors and more). These require larger plots and an additional set of clearances. With limited space but higher FSI from other schemes, developers are planning higher developable area and high-rises. Although sellable area is likely to go up, costs of construction would also be higher.

According to our interactions, key variables to construction are:

Consultancy. For high-rise construction, architects and consultants charge more, given the other issues such as wind-funnel tests, lifts, infrastructure needs (fire-fighting, water treatment etc) that come into play.

Labor. Experienced and equipped labor is required but is scarce. Developers attract ex-pat workers, but these work on a single-project basis.

Contractors. Since most developers outsource construction, given the more-than-a-dozen new projects, execution capacity of contractors has to be ramped up, notwithstanding capability. A few developers plan to secure foreign contractors.

Construction-cost estimates could rise 40-90% in the next few years

Smaller plot size and large developable area are causing delay

in obtaining approvals

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 5

Equipment/technology. Although new processes are being introduced to replace traditional structural work, their greater efficiency has yet to be proven. This would raise cost effectiveness. With the greater amount of work, such techniques are cheaper.

Fig 4 – High-rises coming up in South-Central Mumbai Company Project Height Proposed (mtrs) Floors Proposed Units

DB Realty Crown 374 56 450

DB Realty Heights 394 85 264

DB Realty Turf View 385 60 300

DB Realty Views 350 60 NA

DB Realty Enclave 2 350 60 NA

DB Realty Park 350 60 260

DB Realty Enclave 3 365 72 189

DB Realty Skyz 350 60 180

DB Realty Splendour 350 64 246

DB Realty Central 362 62 164

Orbit Corp Terraces 360 60 120

Oberoi Realty Oasis 329 80 300

Lodha Developers World One 501 111 993

DLF NTC Mills 375* 85 1,102

Ackruti City H Mills 250 90 NA

IBREL Sky 365* 75 110

IBREL Sky Suites 365* 75 300

IBREL Forest 365* 75 315

Lokhandwala Minerva 360* 65* 334

Prakash Mills NA 370* 80 320

Sri Ram Urban Palace Royale 370* 80* NA

IBREL Sky Blue NA 90* 180

Source: Industry, Anand Rathi Research *estimated

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 6

Sales order-book high, but acquisitions to tighten purse In the past six quarters, the top 4 Mumbai-based listed developers have sold stock worth +`140bn, with receivables of +`38bn. These developers have big-ticket land/project acquisition plans, which are likely to lead to acute cash-flow management. The current RBI stance to increase the cost of debt and risk weights on commercial realty would lessen liquidity. Higher selling prices have hit volumes, and corrections (15-20% in certain micro-markets) are imminent.

Sales order book – In comfortable zone

With the uptake in the market and lower prices in 1QFY10, most launched projects then were readily absorbed in the suburbs, with absorption in the island city being investor-led. Across markets, developers have been able to sell projects with higher level of investors in South-Central Mumbai than in Mumbai suburbs.

Fig 5 – Sales order book of key Mumbai developers Developer Sales Value (`m) -

Till 2QFY11 Cash Received (`m) 3QFY11e Sales Value

(`m)

DB Realty 54,582.0 14,820.0 9,000.0

HDIL 50,000.0 9,820.0 7,500.0

Sunteck Realty 8,618.0 3,430.0 3,500.0

Ackruti City 16,800.0 5,395.0 1,500.0

Orbit Corp 11,335.0 4,957.0 1,500.0

Source: Anand Rathi Research.

Although we reiterate that there is little ready inventory in South-Central Mumbai at present and for the next two years, given the numerous high-ticket launches offering more units, we estimate prices in the region to correct the most vs. other sub-regions of the city. Although the western and central suburbs have also seen high price increases, the correction could be less, given differences in ticket size, and shifting of commercial activity towards the suburbs.

Fig 6 – Blended average price rises across Mumbai micro-markets Area (Mumbai) Price rise from March'09 to Dec'10

South 15%

South- Central 33%

Western Suburbs 21%

Central Suburbs 29%

Source: Anand Rathi Research

Although the breakeven of Mumbai developers comes earlier than others (given low land costs), most developers are into land/project acquisitions. With credit becoming harder to come by, developers are likely to correct prices/arrest price hikes.

Comfortable balance sheets – At least till 2QFY11

With the equity raised in the past few quarters, and with good sales recoverables, the balance sheets of most Mumbai developers have been light, till recently. With the recent bribery issue naming property companies, the RBI’s stance on raising weights on commercial loans and

Larger Mumbai-based developers have sold stock worth +`140bn;

with receivables of +`38bn

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 7

rates, credit to developers could be difficult. Also, disbursements for sanctioned loans could be delayed.

Fig 7 – Comfortable balance sheets – at least till date Developer Gross Debt - 2QFY11 (`bn) Net D/E (x) Repayment in 2HFY11 (`bn)

DB Realty 7.0 0.1 -

HDIL 41.3 0.3 2.2

Sunteck Realty 5.7 0.9 -

Ackruti City 18.1 1.0 1.3

Orbit Corp 9.2 1.0 1.1

Oberoi Realty - NA -

Source: Anand Rathi Research.

Fig 8 – Developers Developer Announced land acquisitions

DB Realty Land Acquisitions worth `80bn planned

Ackruti City Land Acquisitions worth `3.33bn planned

HDIL Land acquisition for MIAL project worth `6bn planned

Orbit Corp Kilachand House

HDIL Project investments worth `9bn

Source: Anand Rathi Research

28 January 2011 Mumbai Property – Demand high, but uncertain milieu

Anand Rathi Research 8

Company Section

Anand Rathi Financial Services Limited does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Disclosures and analyst certifications are located in Appendix 1 Anand Rathi Research India Equities

India I Equities

Key financials

Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Sales (`m) 17,284 15,021 22,991 26,262 22,560

Net profit (`m) 7,866 5,666 7,188 10,094 9,565

EPS (`) 15.4 13.0 16.3 22.9 21.7

Growth (%) (52.0) (15.5) 25.6 40.4 (5.2)

PE (x) 10.5 12.4 9.9 7.0 7.4

PBV (x) 1.6 1.0 0.8 0.6 0.6

RoE (%) 16.8 10.0 8.7 9.9 8.4

RoCE (%) 10.1 7.3 8.0 10.3 8.9

Dividend yield (%) - - - - -

Net gearing (%) 92.0 47.0 27.9 19.4 21.3

Source: Company, Anand Rathi Research Prices as of 27 Jan ’11

Property

Update

28 January 2011

HDIL

Looking beyond MIAL; maintain Buy

Though MIAL redevelopment has been steady, shifting of families has been delayed, raising risk for the 65 acres and phases 2&3. Of the funds raised from QIP, and land & FSI sales, we believe HDIL invested ~`9bn in three projects to further de-risk MIAL. We rollover our NAV to Mar 12e, lowering it to `255; we trim our price target to `228, at 10% discount to NAV. Buy.

MIAL project. Shifting of families in phase 1 is likely to lag due to issues at the government level (undecided cut-off dates of tenants) and resistance to shifting by some sections. This raises risk on the 65acre airport land and development of phases 2&3.

Utilizing cash, de-risking business. The +`15bn cash built up on the balance sheet was used to acquire projects, investing `9bn in three projects. This would add another 47-50m sqft land bank (of which, 29m sqft would be in Mumbai City). As projects are large, we await further clarity before assigning value to them.

Change estimates. Our NAV is impacted by removal of 65 acres of free-sale land in MIAL, part of phase 2, and phase 3 from valuation due to lack of land visibility and adding a discount to some under-construction slum-rehab projects in Mumbai. For now, the new acquisitions are taken at cost.

Valuation and risks. Our Mar ’12e NAV is `274 and target price is `247, which is at 10% discount to NAV. At CMP, the stock trades at 0.7x Mar ’12e PBV. Key risk: slowdown in execution.

Rating: Buy Target Price: `228 Share Price: `156

Key data HDIL IN/HDIL.BO

52-week high/low `345/`152 Sensex/Nifty 18684/56043-m average volume US$27m Market cap `64bn/US$1405m

Shares outstanding 415mFree float 61.4%Promoters 38.6%Foreign Institutions 39.3%Domestic Institutions 0.5%Public 21.6%

Relative price performance

HDIL

Sensex

150

200

250

300

350

400

450

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

11

Source: Bloomberg

Change in Estimates Target Reco

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 10

Quick Glance – Financials and Valuations Fig 1 – Income statement (`m)

Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Net sales 17,284 15,021 22,991 26,262 22,560 Sales growth (%) (27.4) (13.1) 53.1 14.2 (14.1)- Op. expenses 8,358 6,186 11,660 10,449 7,510 EBITDA 7,797 7,893 9,722 14,238 13,696 EBITDA margins (%) 45.1 52.5 42.3 54.2 60.7 - Interest 582 462 724 1,166 1,170 - Depreciation 25 724 76 109 273 + Other income 540 345 414 497 500 - Tax 943 1,330 2,147 3,365 3,188 PAT 6,772 5,722 7,188 10,094 9,565 PAT growth (%) (52.0) (15.5) 25.6 40.4 (5.2)Consolidated PAT 7,866 5,666 7,188 10,094 9,565 FDEPS (`/share) 15.4 13.0 16.3 22.9 21.7 CEPS (`/share) 17.9 14.5 16.5 23.1 22.3 DPS (`/share) - - - - -Source: Company, Anand Rathi Research

Fig 2 – Balance sheet (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Share capital 2,755 3,588 4,150 4,410 4,410 Reserves & surplus 41,463 66,840 89,731 104,928 114,493 Shareholders’ fund 44,218 70,429 93,881 109,338 118,903 Debt 41,433 41,017 36,217 35,562 36,423 Def Tax Liab (net) 30 63 63 63 63 Minority interests 0 0 0 0 0 Capital employed 85,682 111,509 130,161 144,963 155,389 Fixed assets 1,228 4,638 5,050 6,323 14,050 Investments 2,491 2,429 2,429 2,429 2,429 Working capital 81,202 96,513 112,684 121,856 127,779 Cash 755 7,918 9,998 14,355 11,131 Capital deployed 85,682 111,509 130,161 144,963 155,389 No. of shares (m) 275.5 358.8 415.0 441.0 441.0 Net Debt/Equity (%) 92.0 47.0 27.9 19.4 21.3 Source: Company, Anand Rathi Research

Fig 3 – Cash flow statement (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Consolidated PAT 7,866 5,666 7,188 10,094 9,565 + Non Cash Items 635 690 88 109 273 Cash profit 8,501 6,355 7,276 10,203 9,838 - Incr/(Decr) in WC 19,775 15,311 16,171 9,172 5,923 Operating cash flow (11,274) (8,956) (8,895) 1,032 3,915 - Capex 566 4,134 489 1,382 8,000 Free cash flow (11,840) (13,090) (9,384) (350) (4,085)- Dividend - - - - -+ Equity raised (63) 20,545 16,264 5,363 (0)+ Debt raised 10,306 (416) (4,800) (655) 861 - Investments 576 (62) - - -- Misc. items (24) 0 0 - -Net cash flow (2,750) 7,163 2,081 4,357 (3,224)+ Opening cash 3,505 755 7,918 9,998 14,355 Closing cash 755 7,918 9,998 14,355 11,131 Source: Company, Anand Rathi Research

Fig 4 – PE Band

HDIL

8x

16x

24x

32x

40x

0

200

400

600

800

1,000

1,200

1,400

Jul-0

7

Oct

-07

Jan-

08

Apr-0

8

Jul-0

8

Oct

-08

Jan-

09

Apr-0

9

Jul-0

9

Oct

-09

Jan-

10

Apr-1

0

Jul-1

0

Oct

-10

Jan-

11

Source: Bloomberg, Anand Rathi Research

Fig 5 – Price-to-Book Band

HDIL

0.5x

1.0x

1.5x

2.0x

2.5x

0

200

400

600

800

1,000

1,200

Jul-0

7

Oct

-07

Jan-

08

Apr-0

8

Jul-0

8

Oct

-08

Jan-

09

Apr-0

9

Jul-0

9

Oct

-09

Jan-

10

Apr-1

0

Jul-1

0

Oct

-10

Jan-

11Source: Bloomberg, Anand Rathi Research

Fig 6 – HDIL vs BSE Realty

HDIL

BSE Realty

150

200

250

300

350

400

Jan-

10

Feb-

10

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Source: Bloomberg

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 11

MIAL: Shifting worries Shifting of families in phase 1 is likely to lag due to issues at the government level (undecided cut-off dates of tenants etc) and resistance to shifting of families by some sections. This raises risk on the 65acre airport land and development of phases 2&3. Hence, we remove the aforementioned projects from our valuation.

MIAL project

Phase 1: Shifting of families

Shifting of families in phase 1 of the MIAL project has been delayed by over a year. Initially to be completed before Feb ’10, shifting of families has been since delayed to Apr ’11 for want of water connections by local government agencies, legitimacy of families staying on MIAL land and conflict among government agencies regarding this, and resistance of certain societies to shift.

We understand that shifting of the families is the responsibility of the MMRDA (a Government body). On the part of HDIL, it has handed over more than 9,000 units at its Kurla site (phase 1) to shift the tenants. Units under construction for phase 1 and part of phase 2 are 33,000. The delay is mainly owing to undecided cut-off dates of tenants and resistance to shifting by some sections.

TDR generation; right on 65 acres of land

TDR generation of up to 98% depends on construction milestones; 2% depends on defect liability, up to six months after shifting of families to rehab buildings. Hence, generation of TDR is largely independent of the shifting of families.

Although the official ‘government rule’ has yet to come, we believe that the state government clearance in Dec ’10 to amend FSI in suburban Mumbai from 1 to 1.33 would have little impact on TDR pricing. The cost of additional FSI (0.33x) would depend on how the government charges it with respect to the ongoing ready reckoner rates in each micro-market. We re-iterate that TDR prices depend on construction activity in Mumbai.

Fig 7 – TDR generation and sales FY09 FY10 FY11e FY12e FY13e FY14e

Generated 5.6 4.8 4.3 3.3 7.3 2.9

Sold 2.0 6.8 4.7 2.5 4.9 5.1

Avg SP 1,100.0 2,150.0 2,700.0 2,400.0 2,200.0 2,500.0

Source: Anand Rathi Research

In FY12, TDR sales would also depend on the amount of construction required for MIAL phase 2 and land conveyed to the SRA for subsequent locations. On the company selling the Andheri (E) land parcel recently, we await more clarity on phase 2 projects. We estimate that HDIL, post-construction-commencement at Mahul, may also start rehab construction in the eastern suburbs, provided it gets some clarity regarding shifting of families in MIAL project.

The 65 acres to be allotted to HDIL, on which it plans to develop 10m sqft of commercial space, depends on families shifting from encroached airport land. Given the delay/uncertainty in shifting, we exclude the 10m sqft development potential from our NAV.

Shifting of families is the responsibility of the MMRDA

TDR prices, we believe, depend on construction activity

We exclude value assigned to 65 acres of leasehold land since land

has yet to be transferred to HDIL

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 12

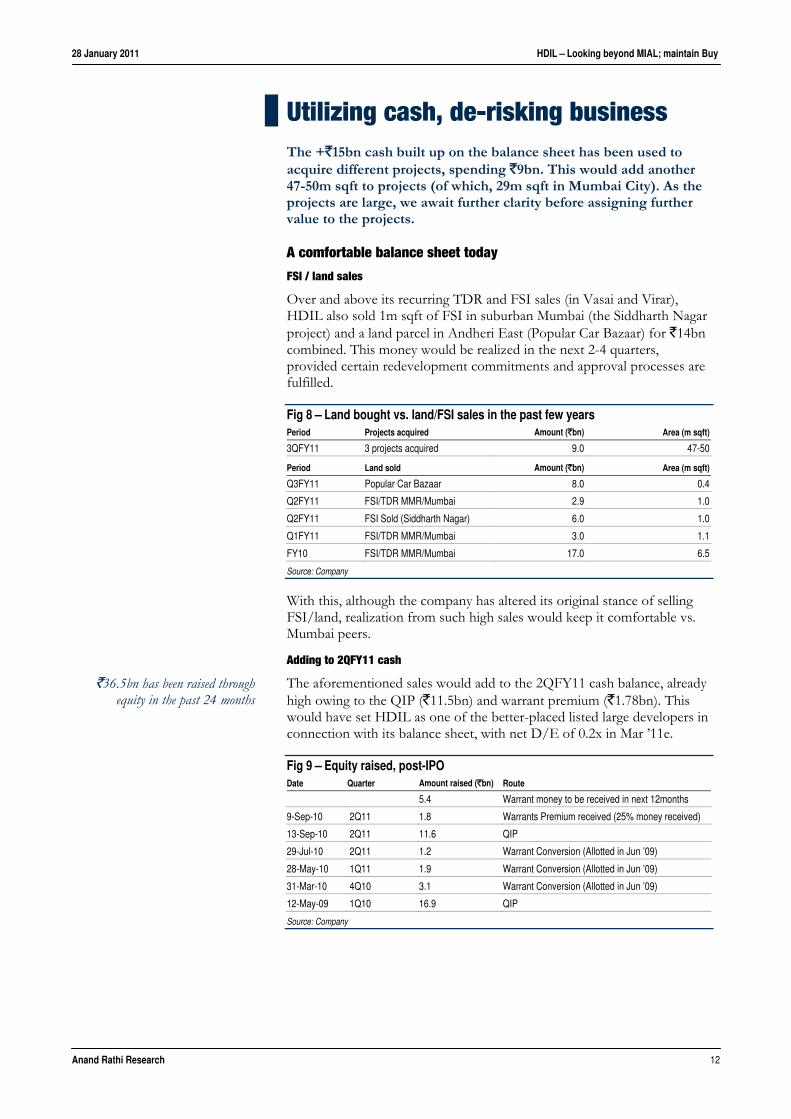

Utilizing cash, de-risking business The +`15bn cash built up on the balance sheet has been used to acquire different projects, spending `9bn. This would add another 47-50m sqft to projects (of which, 29m sqft in Mumbai City). As the projects are large, we await further clarity before assigning further value to the projects.

A comfortable balance sheet today

FSI / land sales

Over and above its recurring TDR and FSI sales (in Vasai and Virar), HDIL also sold 1m sqft of FSI in suburban Mumbai (the Siddharth Nagar project) and a land parcel in Andheri East (Popular Car Bazaar) for `14bn combined. This money would be realized in the next 2-4 quarters, provided certain redevelopment commitments and approval processes are fulfilled.

Fig 8 – Land bought vs. land/FSI sales in the past few years Period Projects acquired Amount (`bn) Area (m sqft)

3QFY11 3 projects acquired 9.0 47-50

Period Land sold Amount (`bn) Area (m sqft)

Q3FY11 Popular Car Bazaar 8.0 0.4

Q2FY11 FSI/TDR MMR/Mumbai 2.9 1.0

Q2FY11 FSI Sold (Siddharth Nagar) 6.0 1.0

Q1FY11 FSI/TDR MMR/Mumbai 3.0 1.1

FY10 FSI/TDR MMR/Mumbai 17.0 6.5

Source: Company

With this, although the company has altered its original stance of selling FSI/land, realization from such high sales would keep it comfortable vs. Mumbai peers.

Adding to 2QFY11 cash

The aforementioned sales would add to the 2QFY11 cash balance, already high owing to the QIP (`11.5bn) and warrant premium (`1.78bn). This would have set HDIL as one of the better-placed listed large developers in connection with its balance sheet, with net D/E of 0.2x in Mar ’11e.

Fig 9 – Equity raised, post-IPO Date Quarter Amount raised (`bn) Route

5.4 Warrant money to be received in next 12months

9-Sep-10 2Q11 1.8 Warrants Premium received (25% money received)

13-Sep-10 2Q11 11.6 QIP

29-Jul-10 2Q11 1.2 Warrant Conversion (Allotted in Jun ’09)

28-May-10 1Q11 1.9 Warrant Conversion (Allotted in Jun ’09)

31-Mar-10 4Q10 3.1 Warrant Conversion (Allotted in Jun ’09)

12-May-09 1Q10 16.9 QIP

Source: Company

`36.5bn has been raised through equity in the past 24 months

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 13

Focusing on suburban residential projects

From Mar ’09 to Dec ’10e, HDIL launched and sold stock in Mumbai suburbs worth `57bn. Its focus has been on suburban locations (as against the major focus of listed peers, of South-Central Mumbai) at a discount to its competitors. Its recent launch of entry-level housing in Palghar (the Mumbai Metropolitan Region) saw sales of ~`7bn (over 6,000 units).

Fig 10 – Launched residential projects Project Location Area (sq ft) Remark

Premier Residency Kurla (W) 100,000 Const on; majority sold out Galaxy Kurla (E) 475,000 Const on; majority sold out Metropolis Andheri (W) 650,000 Const on; majority sold out Majestic Bhandup 1,300,000 Const on; 40% sold Residency Park Virar (W) 1,250,000 Const on; majority sold out Harmony Goregaon (W) 43,568 Const on; majority sold out Meadows Goregaon (W) 1,000,000 Const on; 70% sold Whispering Towers Mulund (W) 800,000 Const on; 40% sold Paradise City 1 Palghar 290000* Const to start; 95% sold Paradise City 2 Palghar 290000* Const to start; 20% sold

Source: Company *Estimated

According to its 2QFY11 presentation, HDIL plans to launch 27m sqft of residential projects in the next 2-3 quarters. Residential projects, usually requiring negative working capital, would add to its cash book.

Fig 11 – Planned project launches Project Location Area (sq ft) Remark

Ekta Nagar Kandivili 1,500,000 Approvals Stage

Palghar P3/4 Palghar 5000000* Approvals Stage

Whispering Towers P2 Mulund 800,000 Post substantial Phase 1 sales

Meadows P2 Goregaon (W) 3,600,000 Post substantial Phase 1 sales

Daulat Santacruz 800,000 Rehab on; legal issues

Premier Residency 2 Kurla 800,000

Ghatkopar Ghatkopar (E) 509,457

Kochi Kochi 6,299,640

Source: Company

New mega projects acquired

HDIL has recently acquired three projects (one slum rehab, one redevelopment and one virgin land). Investment in the acquisition is `9bn as of date.

Fig 12 – New projects acquired: ~`9bn paid Project Location Free-sale Redevelopment Remark

Malvani SRS Malad (W) 25-28m sqft 25,000 families 3K' approval; 25% land premium paid; 67% stake acquired

SVP Nagar Andheri (W) 4m sqft 98 buildings Prime western suburb property

Biosar Biosar 18-20m sqft - Affordable, Entry level housing to be launched

Source: Company

In the Malvani project at Malad, HDIL acquired a 67% stake in Lashkariya Construction. The project is to be developed over 70-80 acres, rehabilitating ~25,000 families. We understand the project has already received “3K” approval from the state government and HDIL has paid a 25% premium to the SRA. It has estimated sellable area of 25-28m sqft.

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 14

HDIL has also acquired redevelopment rights to SVP Nagar in Andheri (W) for 98 buildings and ~3,200 and 3,500 families. Management expects this to generate ~4m sqft of saleable area.

The third land parcel acquired is ~400 acres at Boisar, a distant suburb in the MMR on the western side. We believe HDIL would launch an affordable/entry-level housing project here on the lines of the Palghar project launched in 3QFY11. We estimate this project to have a potential sellable area of 18-20m sqft. Management intends to launch it in the next six months.

With these three acquisitions, the company has maintained its focus on slum rehabilitation and the Mumbai suburban mass market.

Although the aforementioned projects add between 47m and 50m sqft of sellable area, we await further clarity on launch plans and status of the SRS and redevelopment projects. Both are huge and could take 7-9 years.

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 15

Change in estimates Our NAV is impacted by removal of 65 acres of free-sale land in MIAL, part of phase 2, and phase 3 from valuation due to lack of land visibility and adding a discount to some under-construction slum-rehab projects in Mumbai. For now, the new acquisitions are taken at cost

Valuation

We have removed the 10m sqft development (from the 65 acres of MIAL land) from our development schedule, owing to delays or uncertainties in shifting pf families. The impact on our NAV would be 18%

We remove MIAL phase 3 development schedule value on account of ongoing land acquisition (land payment) and clarity regarding phase 2 rehab construction. The impact on our NAV would be 13%

Fig 13 – Valuation: Mar’12e NAV Mar’12 (`m) (`/share)

Slum Rehab 39,860 90

MIAL Project 32,716 74

Rental Housing 10,664 24

MMR (incl Mumbai) 18,819 43

Other Cities 7,435 17

Residual Land 14,272 32

Hotels 821 2

Net Debt (21,207) (48)

3 new projects still considered at cost 9,000 21

Total 120,881 255

Source: Anand Rathi Research

Fig 14 – Optional value as of Mar '12 NAV Mar’12 (`m) (`/share)

MIAL - part pf P2 9,785.0 22.2

MIAL P3 23,914.0 54.2

65 acre of MIAL 33,163.3 75.2

Source: Anand Rathi Research

We have assumed development schedules for slum rehab schemes/ redevelopment schemes. To take into account uncertainties in certain projects, e.g., Bandra (E) SRS 1, we introduce a discount of 15%.

For valuation, we have considered only visible projects in SRS

Fig 15 – Slum projects with development uncertainty Project Location Area (sqft) Value Discount Remark

Bandra (E) SRS 1 Bharat Nagar 1,882,756.0 13,200.0 Environment clearance done, shifting issues

Bandra (E) SRS 2 159,074.0 1,186.0 Environment clearance done, shifting issues

Malad (E) Malad (E) 117,205.0 479.0 NA

BKC Dev Off WE highway 350,000.0 1,780.0 LoI received

Kammanwar Nagar Vikroli 350,000.0 490.0 Redevelopment ongoing

Daulat Nagar Santacruz 800,000.0 4,106.0

15%

Transit const on

Source: Company Anand Rathi Research

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 16

For planned (announced) launches in 2QFY11, we assume a development schedule other than JDAs, and JDAs where deposit has been paid.

For its land bank in Vasai, Virar, and other cities, we assign a certain premium to book value of acquisition (as taken before).

For our valuation, we have taken cost of equity as 19%, cost of debt as 13% and WACC of 15%.

Risks

Although we have taken into account delays in our MIAL assumptions, a change in government policy could affect the project and, hence, value.

A slowdown in construction in Mumbai could affect the TDR market (9% contribution)

Slowdown in sales

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 17

Financials HDIL follows the project-completion method of accounting. It is shifting to the percentage-completion method 1QFY12 onwards. We await further clarity on the threshold limit, and on percent of work on projects completed, in order to effect changes in our reporting format.

FY11 – Revenue recognized. In addition to TDR and FSI sales, we have estimated that HDIL would recognize revenue from the sale of FSI (of 1m sqft) in Siddharth Nagar, Goregaon (W) and from the sale of the Andheri (E) land parcel in FY11.

Inventory. Given the company’s accounting policy, all costs on projects not delivered would show in inventories. Besides, we believe HDIL has paid for other projects/land to be acquired and in acquisition/sanitization phases; e.g., BKC Developers, Novinon Land parcels’ acquisition, redevelopment project in Vikhroli etc., still to be announced for sale. Investment in this is likely to be over `15bn. Although such projects are likely to add more value, further clarity is required.

Fig 16 – Inventories vs. customer advances

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

FY09

FY10

FY11

e

FY12

e

FY13

e

0

5,000

10,000

15,000

20,000

25,000

30,000

Inventory Cust Advances Cash (RHS)

(`m) (`m)

Source: Company, Anand Rathi Research

HDIL is changing to the percentage-completion method of

accounting from 1QFY12

Cash increase is assuming no further land acquisition than

announced

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 18

Fig 17– Income statement (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Revenue 17,284 15,021 22,991 26,262 22,560

- Op. expenses 8,358 6,186 11,660 10,449 7,510

- Employee Costs 221 285 345 525 451

- Other Administrative 908 658 1,264 1,050 902

EBIDTA 7,797 7,893 9,722 14,238 13,696

- Interest 582 462 724 1,166 1,170

- Depreciation 25 724 76 109 273

+ Other income 540 345 414 497 500

- Tax 943 1,330 2,147 3,365 3,188

PAT 6,787 5,722 7,188 10,094 9,565

+ Minority Interests 0 0 - - -

+ Share of profit from Associates - - - - -

Consolidated PAT 7,866 5,666 7,188 10,094 9,565

Dividend - - - - -

FDEPS (` / share) 15.4 13.0 16.3 22.9 21.7

CEPS (` / share) 17.9 14.5 16.5 23.1 22.3

DPS (` / share) - - - - -

BV (` / share) 100.3 159.7 212.9 247.9 269.6

Shares outstanding 275.5 358.8 415.0 441.0 441.0

Growth Rates

Revenue (%) (27.4) (13.1) 53.1 14.2 (14.1)

EBIDTA (%) (49.9) 1.2 23.2 46.5 (3.8)

Net PAT (%) (51.9) (15.5) 25.6 40.4 (5.2)

Diluted EPS (%) (52.0) (15.5) 25.6 40.4 (5.2)

FY10-13e Revenue CAGR (%) 14.5

FY10-13e EBITDA CAGR (%) 20.2

FY10-13e EPS CAGR (%) 19.1

Margins

EBIDTA (%) 45.1 52.5 42.3 54.2 60.7

EBIT (%) 45.0 47.7 42.0 53.8 59.5

Net Profit (%) 45.5 37.7 31.3 38.4 42.4

Source: Company, Anand Rathi Research

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 19

Fig 18– Balance sheet (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Sources of Funds

Share capital 2,755 3,588 4,150 4,410 4,410

Reserves & surplus 41,463 66,840 89,731 104,928 114,493

Shareholders’ fund 44,218 70,429 93,881 109,338 118,903

Debt 41,433 41,017 36,217 35,562 36,423

Deferred Tax Liab (net) 30 63 63 63 63

Minority interests 0 0 0 0 0

Capital employed 85,682 111,509 130,161 144,963 155,389

Application of Funds

Gross Fixed Assets 654 1,937 2,426 3,808 11,807

Less: Depreciation 56 107 183 292 565

Net Fixed Assets 598 1,830 2,243 3,516 11,242

Capital Work in Progress 152 217 217 217 217

Investments 2,491 2,429 2,429 2,429 2,429

Goodwill 478 2,591 2,591 2,591 2,591

Current Assets

Inventories 69,128 87,567 97,823 108,908 122,791

Debtors 1,669 2,030 6,897 7,879 3,384

Loans and Advances 17,077 15,649 30,711 34,039 37,803

Current Liab and Provisions 6,693 8,761 22,775 28,998 36,227

Net Current Assets 81,957 104,431 122,682 136,211 138,910

Working Capital 81,202 96,513 112,684 121,856 127,779

Cash 755 7,918 9,998 14,355 11,131

Capital deployed 85,682 111,509 130,161 144,963 155,389

No. of shares (m) 275.5 358.8 415.0 441.0 441.0

Net Debt/Equity (%) 92.0 47.0 27.9 19.4 21.3

Source: Company, Anand Rathi Research

Fig 19– Cash flow statement (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Consolidated PAT 7,866 5,666 7,188 10,094 9,565

+ Depreciation 41 724 76 109 273

+ Deferred Tax 9 27 12 - -

+ Other non cash 585 (62) - - -

Cash profit 8,501 6,355 7,276 10,203 9,838

- Incr/(Decr) in WC 19,775 15,311 16,171 9,172 5,923

Operating cash flow (11,274) (8,956) (8,895) 1,032 3,915

- Capex 566 4,134 489 1,382 8,000

Free cash flow (11,840) (13,090) (9,384) (350) (4,085)

- Dividend - - - - -

+ Equity raised (63) 20,545 16,264 5,363 (0)

+ Debt raised 10,306 (416) (4,800) (655) 861

- Investments 576 (62) - - -

- Misc. items (24) 0 0 - -

Net cash flow (2,750) 7,163 2,081 4,357 (3,224)

+ Opening cash 3,505 755 7,918 9,998 14,355

Closing cash 755 7,918 9,998 14,355 11,131

Source: Company, Anand Rathi Research

28 January 2011 HDIL – Looking beyond MIAL; maintain Buy

Anand Rathi Research 20

Fig 20 - Ratio analysis @`156 Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Valuations

P / E 10.5 12.4 9.9 7.0 7.4

P / BV 1.6 1.0 0.8 0.6 0.6

M Cap / Sales 2.6 3.8 2.9 2.7 3.1

EV / Sales 4.8 5.9 3.9 3.4 4.2

EV / EBIDTA 10.6 11.2 9.3 6.3 6.9

Dividend

Dividend yield (%) - - - - -

Dividend payout (%) - - - - -

Leverage

Net Debt / Equity 92 47 28 19 21

Int Coverage 13 16 13 12 11

Return Ratios

ROE (%) 16.8 10.0 8.7 9.9 8.4

ROCE (%) 10.1 7.3 8.0 10.3 8.9

Source: Company, Anand Rathi Research

Anand Rathi Financial Services Limited does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Disclosures and analyst certifications are located in Appendix 1 Anand Rathi Research India Equities

India I Equities

Key financials

Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Sales (`m) 4,644 9,512 14,630 30,746 43,141

Net profit (`m) 1,417 2,520 3,912 7,516 13,097

EPS (`) 5.8 10.4 16.1 30.9 53.8

Growth (%) NA 77.9 55.2 92.1 74.3

PE (x) NA 15.2 9.8 5.1 2.9

PBV (x) NA 1.3 1.1 0.9 0.7

RoE (%) 18.7 14.1 13.2 20.7 32.9

RoCE (%) 12.9 15.1 16.7 26.9 42.6

Dividend yield (%) - - 0.3 0.6 0.6

Net gearing (%) 142.8 16.7 40.1 28.3 21.5

Source: Company, Anand Rathi Research Prices as of 27 Jan ’11

Property

Update

28 January 2011

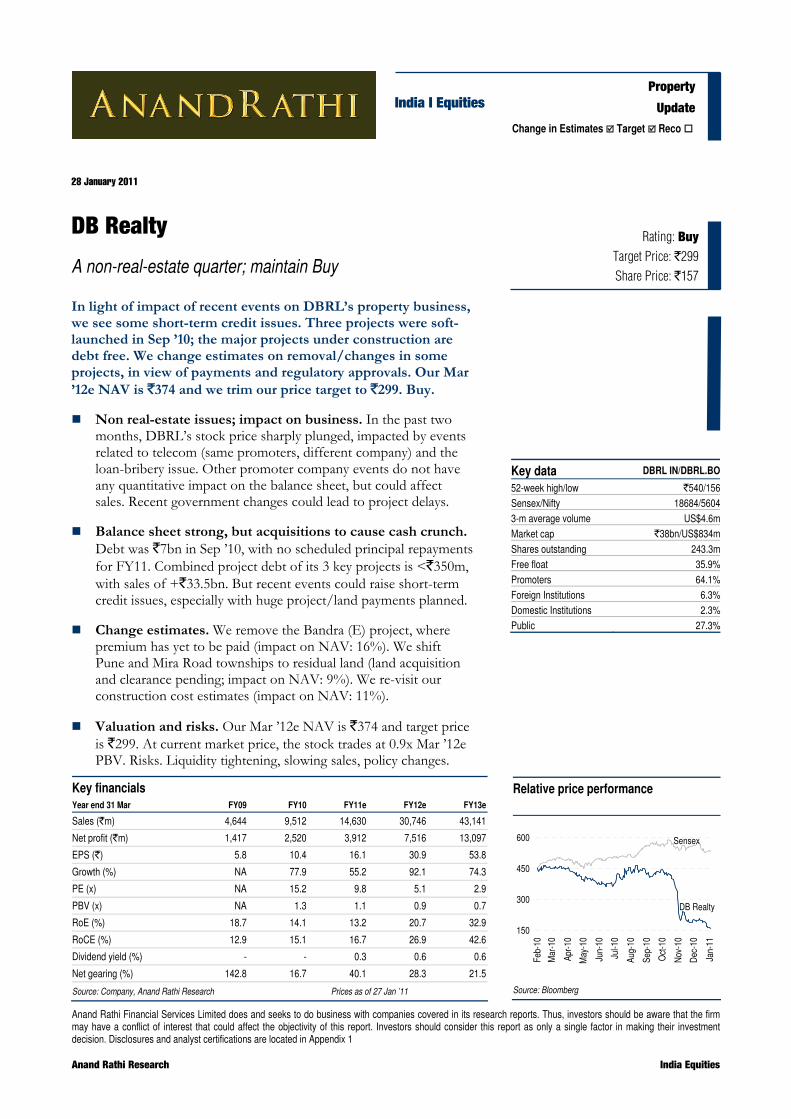

DB Realty

A non-real-estate quarter; maintain Buy

In light of impact of recent events on DBRL’s property business, we see some short-term credit issues. Three projects were soft-launched in Sep ’10; the major projects under construction are debt free. We change estimates on removal/changes in some projects, in view of payments and regulatory approvals. Our Mar ’12e NAV is `374 and we trim our price target to `299. Buy.

Non real-estate issues; impact on business. In the past two months, DBRL’s stock price sharply plunged, impacted by events related to telecom (same promoters, different company) and the loan-bribery issue. Other promoter company events do not have any quantitative impact on the balance sheet, but could affect sales. Recent government changes could lead to project delays.

Balance sheet strong, but acquisitions to cause cash crunch. Debt was `7bn in Sep ’10, with no scheduled principal repayments for FY11. Combined project debt of its 3 key projects is <`350m, with sales of +`33.5bn. But recent events could raise short-term credit issues, especially with huge project/land payments planned.

Change estimates. We remove the Bandra (E) project, where premium has yet to be paid (impact on NAV: 16%). We shift Pune and Mira Road townships to residual land (land acquisition and clearance pending; impact on NAV: 9%). We re-visit our construction cost estimates (impact on NAV: 11%).

Valuation and risks. Our Mar ’12e NAV is `374 and target price is `299. At current market price, the stock trades at 0.9x Mar ’12e PBV. Risks. Liquidity tightening, slowing sales, policy changes.

Rating: Buy Target Price: `299 Share Price: `157

Key data DBRL IN/DBRL.BO

52-week high/low `540/156Sensex/Nifty 18684/56043-m average volume US$4.6mMarket cap `38bn/US$834m

Shares outstanding 243.3mFree float 35.9%Promoters 64.1%Foreign Institutions 6.3%Domestic Institutions 2.3%Public 27.3%

Relative price performance

DB Realty

Sensex

150

300

450

600

Feb-

10

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Source: Bloomberg

Change in Estimates Target Reco

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 22

Quick Glance – Financials and Valuations Fig 1 – Income statement (`m)

Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Net sales 4,644 9,512 14,630 30,746 43,141 Sales growth (%) NA 104.8 53.8 110.1 40.3 - Op. expenses 2,064 5,470 7,521 17,008 17,205 EBITDA 2,258 3,655 6,583 12,847 24,729 EBITDA margins (%) 48.6 38.4 45.0 41.8 57.3 - Interest 747 726 571 861 764 - Depreciation 74 96 88 94 120 + Other income 68 291 - - - - Tax 67 413 1,659 4,043 8,107 PAT 1,438 2,712 4,265 7,849 15,738 PAT growth (%) NA 88.5 57.3 84.0 100.5 Consolidated PAT 1,417 2,520 3,912 7,516 13,097 FDEPS (`/share) 5.8 10.4 16.1 30.9 53.8 CEPS (`/share) 6.1 10.7 16.4 31.3 54.3 DPS (`/share) - - 0.5 1.0 1.0 Source: Company, Anand Rathi Research

Fig 2 – Balance sheet (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Share capital 91 2,433 2,433 2,433 2,433 Reserves & surplus 8,023 28,054 31,823 39,055 51,868 Shareholders’ fund 8,114 30,486 34,256 41,488 54,301 Debt 12,357 5,948 13,748 11,748 11,655 Def Tax Liab (net) 4 (2) (2) (2) (2)Minority interests 553 745 745 745 745Capital employed 21,028 37,177 48,747 53,979 66,698 Fixed assets 223 219 180 234 219 Investments 2 8,941 5,191 5,191 5,191 Working capital 20,028 27,157 36,376 37,770 42,771 Cash 769 860 7,000 10,784 18,518 Capital deployed 21,028 37,177 48,747 53,979 66,698No. of shares (m) 9 243 243 243 243 Net Debt/Equity (%) 142.8 16.7 40.1 28.3 21.5 Source: Company, Anand Rathi Research

Fig 3 – Cash flow statement (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Consolidated PAT 1,417 2,520 3,912 7,516 13,097 +Non Cash Items 77 90 88 94 120 Cash profit 1,494 2,609 4,000 7,611 13,217 - Incr/(Decr) in WC 9,131 7,130 9,219 1,394 5,001 Operating cash flow (7,637) (4,520) (5,219) 6,217 8,216 -Capex 150 91 49 149 104 Free cash flow (7,787) (4,611) (5,268) 6,068 8,112 -Dividend - - 142 285 285 + Equity raised (585) 19,853 (0) - - + Debt raised 6,327 (6,409) 7,800 (2,000) (93) -Investments (1,783) 8,938 (3,750) - - -Misc. items 5 (5) (0) - - Net cash flow (268) 92 6,140 3,784 7,734 +Opening cash 1,037 769 860 7,000 10,784 Closing cash 769 860 7,000 10,784 18,518 Source: Company, Anand Rathi Research

Fig 4 – PE Band

5x

10x

15x

20x

25x

0

100

200

300

400

500

600

700

800

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Source: Bloomberg, Anand Rathi Research

Fig 5 – Price-to-Book Band

DBRL

1x

2x

3x

4x

5x

0

100

200

300

400

500

600

700

800

900

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Source: Bloomberg, Anand Rathi Research

Fig 6 – DB Realty vs BSE Realty

DB Realty

BSE Realty

100

200

300

400

500

600

Feb-

10

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Source: Bloomberg, Anand Rathi Research

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 23

Non-real-estate issues; evaluating business impact In the past two months, DBRL’s stock price has reacted sharply to events related to telecommunications (same promoters, different company) and the loan-bribery issue. Other promoter company events, we believe, do not have any quantitative impact on the company’s balance sheet, but could affect sales. Recent government changes in the state could result in project delays (as with other developers in Mumbai).

Key events

Probe in 2G spectrum allotment – DB Realty link

DBRL promoters run/own three businesses through separate entities – real-estate under DB Realty, hospitality under D B Hospitality, and telecoms, a JV with Etisalat under Etisalat DB Telecoms (Pvt). DB Realty has provided corporate guarantees for loans taken by its group companies, of `14.7bn. These guarantees have been provided since the last two years, also pointed out as risks in our report “Mumbai Property: The old order changeth, yielding place to new” dated 4 Oct ’10. Over and above this, the company has a minority stake in a hospitality project in DIAL.

Fig 7 – Etilisat DB: Extract from FY10 balance sheet (`m) Liabilities FY09 FY10

Shareholders Funds 2,527 2,527

Reserves & Surplus 40,792 40,780

Net Worth 43,318 43,307

Gross Debt 3 575

D/E 0.00 0.01

Net D/E (0.58) (0.37)

Assets

Fixed Assets 17,933 43,033

Investments 1,095 -

Cash & Equivalents 25,340 16,458

Net CA 43,321 43,882

Source: Registrar of Companies (RoC)

In addition to the guarantee provided by the company, both managing directors have provided personal guarantees of `16.57bn and US$138m each in the telecoms and hospitality businesses respectively. The net worth of the telecoms company is `40bn and cash on its books is ~`15bn.The hospitality company has a net worth of `5.5bn, with debt of ~`1.5bn.

DBRL’s link with other promoter companies is only the corporate

guarantees provided by it

The promoters in their personal capacity have provided guarantees of

`16.75bn and US$138m each

Fixed assets include license fees of `15.7bn, while liability to creditors

is `19.8bn

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 24

Fig 8 – DB Hospitality: Extract from FY10 balance sheet (`m) Liabilities FY09 FY10

Shareholders Funds 494 494

Reserves & Surplus 5,044 5,018

Net Worth 5,538 5,512

Gross Debt 1,321 3,904

D/E 0.24 0.71

Net D/E 0.23 0.69

Assets

Fixed Assets 2,456 4,608

Investments 1,469 1,623

Cash & Equivalents 28 112

Net CA 2,908 3,185

Source: RoC

Although the corporate guarantees provided by DBRL are huge, given its balance sheet, we believe there would be no material impact on the performance of the company nor a strain on its balance sheet.

Loan bribery case

DBRL’s name also came up in the recent loan bribery event, for `1.88bn drawn from LIC Housing Finance through a market intermediary. The company has clarified its position regarding the issue.

We believe this to be a non-event for DBRL. But, given the present environment, we believe credit would turn expensive and sanctions and disbursals would be difficult in the near term. Although the balance sheet is net cash (2QFY11) and DBRL has a sales order book of over `40bn, its huge project/land acquisition spending would slow down, given the low availability of credit and requirement of cash in hand for working capital.

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 25

Balance Sheet Debt stood at `7bn as of Sep ’10, with no scheduled principal repayments in FY11 and `1.96bn in FY12. The balance sheet in Nov ’10 was largely net cash, and three key projects – Orchid Crown, Orchid Heights and Orchid Turf View – have combined project debt of less than `350m, with sales of over `35.2bn. Recent events could lead to near-term credit issues, given the huge project/land payments planned.

Balance sheet not strained, but credit flow important

With the `15bn raised though its IPO in 4QFY10, the company was net cash in Sep ’10. Although it had no scheduled debt repayments in FY11 (after repaying `800m to IDFC as stated as the object of the IPO), it has, in addition, already repaid ~`3bn of debt as of Nov ’10. Scheduled repayment in FY12 is ~`1.96bn.

Fig 9 – Debt details Project Debt on books (`m) From

Heights 344.7 Public Sector Banks

Woods 1,300.0 Private Sector Bank

Corporate 2,431.5 MNCs, PSBs

Sanctioned to draw 7,090.0

Source: Company *as of Nov '10

Sales order book good

In the past six quarters, till Sep ’10, DBRL launched and sold stock worth ~`64bn. It also soft launched/launched a few projects in 3QFY11. We estimate DBRL to have sold stock worth +`9bn in 3QFY11.

Fig 10 – Sales value vs. value realized Project Value Sold (`m) Amount Received (`m) (%) Received

Mahul Nagar 11,784.0 9,504.0 81%

Orchid Woods 7,500.0 4,790.0 64%

Orchid Suburbia 3,615.0 1,343.0 37%

Orchid Ozone 8,734.0 1,717.0 20%

Orchid Crown 14,821.0 2,957.0 20%

Orchid Hills 1,535.0 1,500.0 98%

Orchid Heights 11,122.0 1,636.0 15%

Orchid Turf View 5,095.0 1,452.0 28%

Source: Company

In 3QFY11, DBRL soft-launched/launched five projects in Pune and Mumbai. Certain projects are subsequent phases of the under-construction projects.

Receivables from sold stock are ~`40bn; the current value of

unsold stock is `86.5bn

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 26

We revise our sales and sales duration estimates for a few projects, as the launched prices are above our estimated average selling prices.

Fig 12 – Changes in project assumptions Project Previous avg SP (`/sqft) New Avg SP (`/ sqft) Remark

Turf View 35,315 37,500 Prolonged project sales; to sell till FY18

Golf View 5,870 9,740 Launched at higher price and less units; project divided into phases

Source: Anand Rathi Research

Fig 11 – 3QFY11: New projects launched Project Location Launch price (`/ sqft)) ARG Estimate of Avg price (`/ sqft) Remark

Orchid Turfview - Wing D Mahalaxmi 40,000 35,315 Tower A&B - const started

Paradise Bandra (E) 17,000 20,950 Project acquired recently

View Mumbai Central 17,900 17,520 Rehab shifting to start

Golf View Pune 9,000 9,740 Excavation started

Centre Pune - - Construction started

Source: Company

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 27

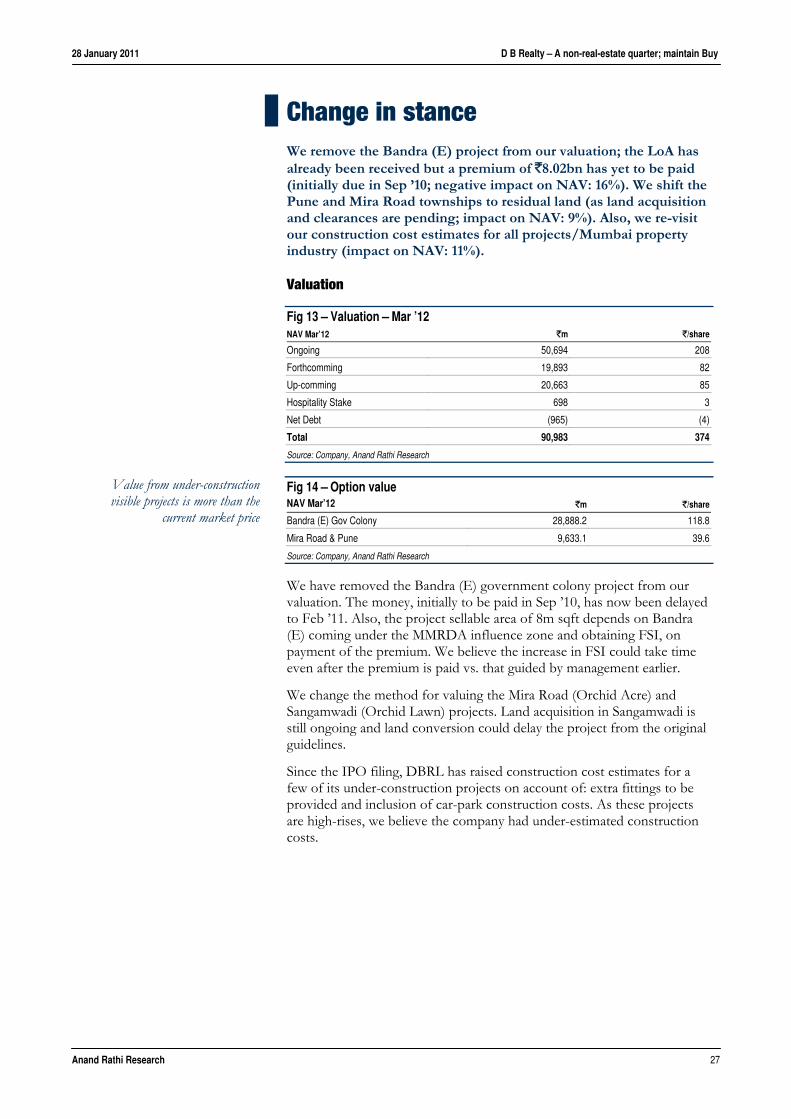

Change in stance We remove the Bandra (E) project from our valuation; the LoA has already been received but a premium of `8.02bn has yet to be paid (initially due in Sep ’10; negative impact on NAV: 16%). We shift the Pune and Mira Road townships to residual land (as land acquisition and clearances are pending; impact on NAV: 9%). Also, we re-visit our construction cost estimates for all projects/Mumbai property industry (impact on NAV: 11%).

Valuation

Fig 13 – Valuation – Mar ’12 NAV Mar’12 `m `/share

Ongoing 50,694 208

Forthcomming 19,893 82

Up-comming 20,663 85

Hospitality Stake 698 3

Net Debt (965) (4)

Total 90,983 374

Source: Company, Anand Rathi Research

Fig 14 – Option value NAV Mar’12 `m `/share

Bandra (E) Gov Colony 28,888.2 118.8

Mira Road & Pune 9,633.1 39.6

Source: Company, Anand Rathi Research

We have removed the Bandra (E) government colony project from our valuation. The money, initially to be paid in Sep ’10, has now been delayed to Feb ’11. Also, the project sellable area of 8m sqft depends on Bandra (E) coming under the MMRDA influence zone and obtaining FSI, on payment of the premium. We believe the increase in FSI could take time even after the premium is paid vs. that guided by management earlier.

We change the method for valuing the Mira Road (Orchid Acre) and Sangamwadi (Orchid Lawn) projects. Land acquisition in Sangamwadi is still ongoing and land conversion could delay the project from the original guidelines.

Since the IPO filing, DBRL has raised construction cost estimates for a few of its under-construction projects on account of: extra fittings to be provided and inclusion of car-park construction costs. As these projects are high-rises, we believe the company had under-estimated construction costs.

Value from under-construction visible projects is more than the

current market price

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 28

Fig 15 - Increase in construction costs (`m) Management guidance on est costs AR estimates

Project RHP Aug'10 Nov'10 (%) Increase Avg Const costs (`/sqft)*

Ozone 6,254.3 7,375.0 6,852.0 9.6 2,589.6

Woods 5,421.0 7,331.0 6,435.0 18.7 5,084.3

Heights 5,064.5 11,215.0 10,031.0 98.1 8,455.9

Suburbia 4,709.5 5,514.0 4,986.0 5.9 5,433.7

Mahul Nagar 8,538.6 8,539.0 8,539.0 0.0 940.9

Turf 6,753.7 12,870.0 10,760.0 59.3 6,410.5

Corporate Park 4,724.8 4,725.0 4,725.0 0.0 3,901.0

Centre 1,348.8 1,349.0 1,349.0 0.0 2,615.2

Crown 5,670.6 12,069.0 10,615.0 87.2 6,433.3

Source: Company, Anand Rathi Research *on total costs, including rehab, car parks construction

In our report “Mumbai Property: The old order changeth, yielding place to new” dated 4 Oct ’10, our construction cost estimates were 7% more than the estimates of the company. With more high-rises using different development schemes, differentiated product offerings and our interaction with different market participants, we have increased our construction costs estimates for under-construction and planned projects. We believe that management could revise its construction cost estimates upwards after construction commences, as it has done recently.

Fig 16 - Difference between DB Realty and ARG estimated construction costs RHP (`m) Nov'10 (`m) Increase in costs (%)

DB Realty Estimates 167,766 183,572 9%

Oct'10 (`m) Jan'11 (`m) Increase in cost (%)

ARG Estimates 179,991 213,943 19%

Difference between estimates 7% 17%

Source: Anand Rathi Research

Nine projects are being developed by securing higher FSI through the public parking schemes. Recently, the government of Maharastra decided to re-think DCR 33(24) relating to public parking schemes, especially for allotment in south-central Mumbai. Although DB Realty has secured primary approvals for all its projects and cancellation is unlikely, in certain projects the area could come down. We introduce a discount to account for this, till further clarity emerges.

Fig 17 - Status of public parking schemes Project Status

Turf View Approved by MCGM

Heights Approved by MCGM

Crown Approved by MCGM

Views With MCGM for Final approval

West View With MCGM for Final approval

Splendour With MCGM for Final approval

Central With MCGM for Final approval

Corporate Park With MCGM for Final approval

Park With MCGM for Final approval

Skyz With MCGM for Final approval

Enclave Approved by MCGM

Source: Company, Anand Rathi Research

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 29

Certain projects depend on securing higher FSI through the PPP format. Till approvals are obtained, we introduce a discount.

Fig 18 - PPP schemes yet to be cleared Project Remark

Centre P2 Police Station clearance to be done; P1 (Golf View) and Centre 1 started

Hill Park Police housing - to be cleared

Mahal Pictures Police Housing - to apply for it

Gov Colony Premium yet to be paid

Orchid Town Rental Housing; approval stage, some premium paid

Source: Company

We raise cost of debt by 100bps, resulting in an increase in WACC to 16%.

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 30

Financials Fig 19 – Income statement (`m) Year end 31 Mar FY09 FY10 FY11e FY12e FY13e

Revenue 4,644 9,512 14,630 30,746 43,141

- Op. expenses 2,064 5,470 7,521 17,008 17,205

- Employee Costs 36 53 88 123 129

- Other Administrative 286 334 439 769 1,079

EBITDA 2,258 3,655 6,583 12,847 24,729

- Interest 747 726 571 861 764

- Depreciation 74 96 88 94 120

+ Other income 68 291 - - -

- Tax 67 413 1,659 4,043 8,107

PAT 1,438 2,712 4,265 7,849 15,738

+ Minority Interests 22 192 353 332 2,641

+ Share of profit from Associates 0 (0) - - -

Consolidated PAT 1,417 2,520 3,912 7,516 13,097

Dividend - - 142 285 285

FDEPS (` / share) 5.8 10.4 16.1 30.9 53.8

CEPS (` / share) 6.1 10.7 16.4 31.3 54.3

DPS (` / share) - - 0.5 1.0 1.0

BV (` / share) 33.4 125.3 140.8 170.6 223.2

Shares outstanding 9.1 243.3 243.3 243.3 243.3

Growth Rates

Revenue (%) NA 104.8 53.8 110.1 40.3

EBITDA (%) (1,869.5) 61.9 80.1 95.2 92.5

Net PAT (%) (752.0) 77.9 55.2 92.1 74.3

Diluted EPS (%) (752.0) 77.9 55.2 92.1 74.3

FY10-13e Revenue CAGR(%) 65.5

FY10-13e EBITDA CAGR (%) 89.1

FY10-13e EPS CAGR (%) 73.2

Margins

EBITDA (%) 48.6 38.4 45.0 41.8 57.3

EBIT (%) 47.0 37.4 44.4 41.5 57.0

Net Profit (%) 30.5 26.5 26.7 24.4 30.4

Source: Company, Anand Rathi Research

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 31

Fig 20 – Balance sheet (`m) Year end 31 Mar FY09 FY10e FY11e FY12e FY13e

Sources of Funds

Share capital 91 2,433 2,433 2,433 2,433

Reserves & surplus 8,023 28,054 31,823 39,055 51,868

Shareholders’ fund 8,114 30,486 34,256 41,488 54,301

Preference Share Capital - - - - -

Debt 12,357 5,948 13,748 11,748 11,655

Deferred Tax Liab (net) 4 (2) (2) (2) (2)

Minority interests 553 745 745 745 745

Capital employed 21,028 37,177 48,747 53,979 66,698

Application of Funds

Gross Fixed Assets 301 310 397 545 650

Less: Depreciation 92 129 217 311 431

Net Fixed Assets 208 181 180 234 219

Capital Work in Progress 15 37 - - -

Goodwill - - - - -

Investments 2 8,941 5,191 5,191 5,191

Current Assets

Inventories 10,578 13,195 17,418 19,710 25,034

Debtors 426 3,058 4,478 5,142 12,765

Loans and Advances 12,442 18,554 24,284 26,854 27,289

Other Current Assets - - - - -

Current Liab and Provisions 3,418 7,649 9,803 13,936 22,317

Net Current Assets 20,797 28,018 43,376 48,554 61,289

Working Capital 20,028 27,157 36,376 37,770 42,771

Cash 769 860 7,000 10,784 18,518

Capital deployed 21,028 37,177 48,747 53,979 66,698

No. of shares (m) 9.1 243.3 243.3 243.3 243.3

Net Debt/Equity (%) 142.8 16.7 19.7 2.3 (12.6)

Source: Company, Anand Rathi Research

Fig 21 – Cash flow statement (`m) Year end 31 Mar FY09 FY10e FY11e FY12e FY13e

Consolidated PAT 1,417 2,520 3,912 7,516 13,097

+ Non cash exp 77 90 88 94 120

Cash profit 1,494 2,609 4,000 7,611 13,217

- Incr/(Decr) in WC 9,131 7,130 9,219 1,394 5,001

Operating cash flow (7,637) (4,520) (5,219) 6,217 8,216

- Capex 150 91 49 149 104

Free cash flow (7,787) (4,611) (5,268) 6,068 8,112

- Dividend - - 142 285 285

+ Equity raised (585) 19,853 (0) - -

+ Debt raised 6,327 (6,409) 7,800 (2,000) (93)

+ Minority interests (1) 192 - - -

-Investments (1,783) 8,938 (3,750) - -

- Misc. items 5 (5) (0) - -

Net cash flow (268) 92 6,140 3,784 7,734

+ Opening cash 1,037 769 860 7,000 10,784

Closing cash 769 860 7,000 10,784 18,518

Source: Company, Anand Rathi Research

28 January 2011 D B Realty – A non-real-estate quarter; maintain Buy

Anand Rathi Research 32

Fig 22 – Ratio Analysis @ `157 Year end 31 Mar FY09 FY10e FY11e FY12e FY13e

Valuations

P E NA 15.2 9.8 5.1 2.9

P/BV NA 1.3 1.1 0.9 0.7

M Cap/Sales NA 4.0 2.6 1.2 0.9

EV/Sales NA 3.6 2.7 1.1 0.6

EV/EBIDTA NA 9.4 6.0 2.6 1.1

Dividend

Dividend yield (%) - - 0.3 0.6 0.6

Dividend payout (%) - - 2.9 3.1 1.5

Leverage

Net Debt/Equity 142.8 16.7 19.7 2.3 (12.6)

Int Coverage 1.8 1.9 2.5 2.2 2.2

Return Ratios

ROE (%) 18.7 14.1 13.2 20.7 32.9

ROCE (%) 12.9 15.1 16.7 26.9 42.6

Source: Company, Anand Rathi Research

Anand Rathi Financial Services Limited does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Disclosures and analyst certifications are located in Appendix 1 Anand Rathi Research India Equities

India I Equities

Key financials

Year end 31 Mar FY09 FY10 FY11e FY12 e FY13 e

Sales (`m) 4,348 5,796 10,236 12,478 19,602

Net profit (`m) 2,647 1,649 2,302 2,349 3,017

EPS (`) 36.4 22.7 31.6 32.3 41.5

Growth (%) (12) (38) 40 2 28

PE (x) 6.5 10.4 7.5 7.3 5.7

PBV (x) 1.5 1.2 1.0 0.9 0.8

RoE (%) 28.3 13.1 14.5 13.0 14.6

RoCE (%) 21.7 15.4 17.2 16.5 20.9

Dividend yield (%) 0.4 2.1 0.4 0.4 0.4

Net gearing (%) 100.5 80.1 101.7 78.8 59.0

Source: Company, Anand Rathi Research Prices as of 27 Jan ’11

Property

Update

28 January 2011

Ackruti City

Premium land, but needs to be developed; retain Buy

Ackruti’s project portfolio is premium among peers. Post a good FY10, launches slowed. Though collections from pre-sales have been good, 1HFY11 has seen debt rising by ~`5bn, largely used for stake additions and working capital. We now value the stock at Mar ’12e NAV of `566 and trim our target price to `421. Buy.

Premium land – Execution is key. Compared with Mumbai peers, Ackruti’s projects have an edge as regards location (Mumbai island city) and spread (Mumbai suburbs). We believe successful and timely project development would drive value.

Growing debt may be a concern. In the past six quarters, Ackruti has sold property worth `16bn, realized debtors of `4bn, raised equity of `3bn and sold FSI/TDR of `3.1bn. But, debt also rose, by `5bn, mainly due to larger project additions and rehab construction. Although sanctioned debt for projects is `14.4bn, new project payments and stalling market volume are concerns.

Change in estimates. Our NAV is impacted by removal of the Bandra (E) project (premium yet to be paid), the Gujarat Biotech Park phase-3 (nil progress), and SRS/virgin land projects. We also increase discount to 25% from 20%, accounting for recent events and their medium-term impact.

Valuation and risks. Our Mar ’12e NAV stands at `566 and price target at `421, which is at 25% discount to NAV. At CMP, the stock trades at 0.9x Mar ’12e PBV. Key risk: Slowdown in sales.

Rating: Buy Target Price: `421 Share Price: `236

Key data AKCL IN/ ACKR.BO

52-week high/low `560/232Sensex/Nifty 18684/56043-m average volume US$1.6mMarket cap `17bn/US$373m

Shares outstanding 72.7mFree float 17.5%Promoters 82.5%Foreign Institutions 2.2%Domestic Institutions 0.8%Public 14.5%

Relative price performance

Ackruti City

Sensex

200

300

400

500

600

700

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

11

Source: Bloomberg

Change in Estimates Target Reco

28 January 2011 Ackruti City – Premium land, but needs to be developed; retain Buy

Anand Rathi Research 34

Quick Glance – Financials and Valuations Fig 1 – Income statement (`m)

Year end 31 Mar FY09 FY10 FY11 e FY12 e FY13 e

Net sales 4,348 5,796 10,236 12,478 19,602 Sales growth (%) (2) 33 77 22 57- Op. expenses (258) 1,314 3,720 5,269 9,824 EBITDA 4,095 3,825 5,526 5,961 7,720 EBITDA margins (%) 94.2 66.0 54.0 47.8 39.4 - Interest 1,402 1,680 2,240 2,456 2,204 - Depreciation 57 71 114 150 180 + Other income 200 385 200 200 -- Tax 232 817 1,147 1,209 1,814 PAT 2,603 1,641 2,226 2,346 3,521 PAT growth (%) (13.1) (37.0) 35.6 5.4 50.1Consolidated PAT 2,647 1,649 2,302 2,349 3,017 FDEPS (`/share) 36.39 22.67 31.65 32.30 41.47 CEPS (`/share) 37.20 24.37 33.21 34.36 43.95 DPS (`/share) 1.00 5.00 1.00 1.00 1.00 Source: Company, Anand Rathi Research

Fig 2 – Balance sheet (`m) Year end 31 Mar FY09 FY10 FY11 e FY12 e FY13 e

Share capital 667 727 727 727 727 Reserves & surplus 9,741 14,060 16,270 18,528 21,585 Shareholders’ fund 10,408 14,787 16,997 19,255 22,312 Debt 10,569 13,055 18,055 16,055 14,555 Def Tax Liab (net) (104) (50) (50) (50) (50)Minority interests 2 1 1 1 1 Capital employed 20,875 27,793 35,004 35,261 36,818 Fixed assets 982 2,400 3,360 3,863 4,400 Investments 3,025 3,563 3,563 3,563 3,563 Working capital 15,135 19,644 27,308 26,957 27,243 Cash 110 1,216 772 878 1,632Capital deployed 20,932 27,793 35,004 35,261 36,818No. of shares (m) 72.7 72.7 72.7 72.7 72.7 Net Debt/Equity (%) 99.9 80.1 101.7 78.8 59Source: Company, Anand Rathi Research

Fig 3 – Cash flow statement (`m) Year end 31 Mar FY09 FY10 FY11 e FY12 e FY13 e

Consolidated PAT 2,647 1,649 2,302 2,349 3,149+ Depreciation (53) 125 114 150 180 Cash profit 2,594 1,774 2,416 2,499 3,329- Incr/(Decr) in WC 2,683 4,510 7,663 (351) 266Operating cash flow (89) (2,736) (5,248) 2,850 3,063- Capex 1,515 835 105 653 718 Free cash flow (1,605) (3,571) (5,353) 2,197 2,345- Dividend 84 425 91 91 91 + Equity raised (78) 3,098 0 0 0+ Debt raised 2,277 2,486 5,000 (2,000) (1,500)- Investments 747 538 - - -- Misc. items 56 (56) - - -Net cash flow (293) 1,107 (444) 106 754+ Opening cash 403 110 1,216 772 878 Closing cash 110 1,216 772 878 1,632Source: Company, Anand Rathi Research

Fig 4 – PE Band

Ackruti City

6x 12x 18x 24x 30x

0

500

1,000

1,500

2,000

2,500

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Source: Bloomberg, Anand Rathi Research

Fig 5 – Price-to-Book Band

Ackruti City

1x

3x

5x

7x

9x

0

500

1,000

1,500

2,000

2,500

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Source: Bloomberg, Anand Rathi Research

Fig 6 – Ackruti City vs BSE Realty

Ackruti City

BSE Realty

200

300

400

500

600

Jan-

10

Feb-

10

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Source: Bloomberg

28 January 2011 Ackruti City – Premium land, but needs to be developed; retain Buy

Anand Rathi Research 35

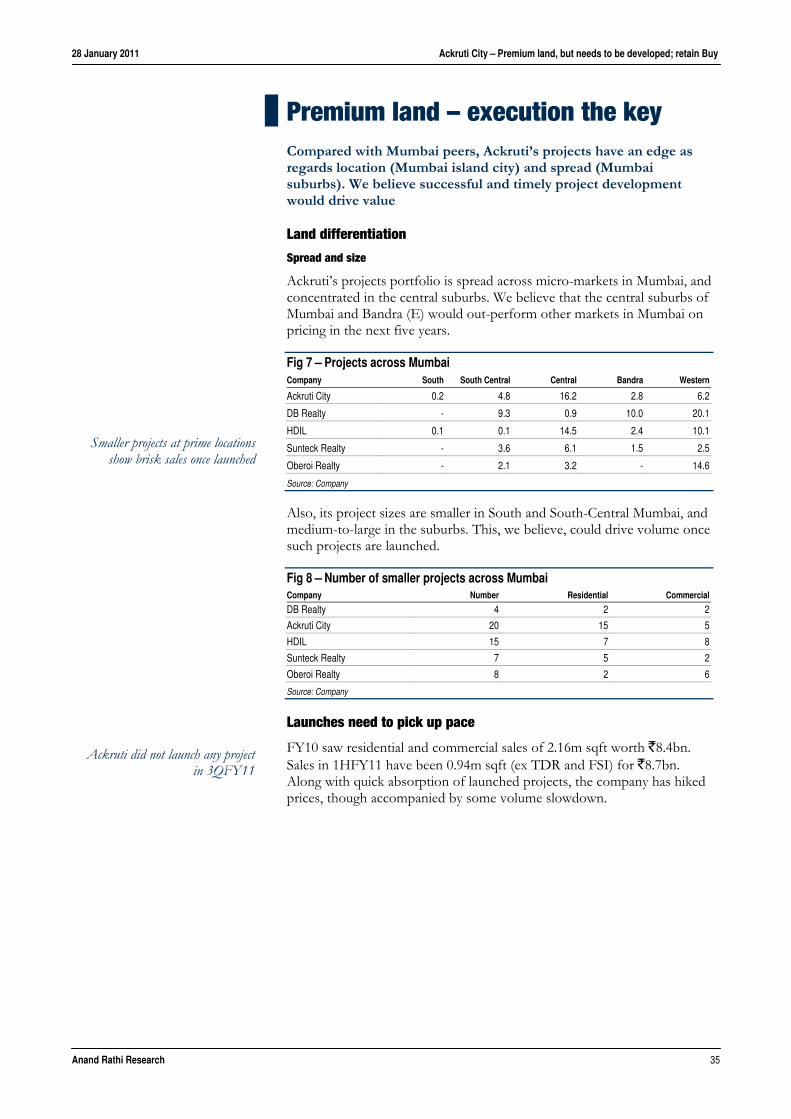

Premium land – execution the key Compared with Mumbai peers, Ackruti’s projects have an edge as regards location (Mumbai island city) and spread (Mumbai suburbs). We believe successful and timely project development would drive value

Land differentiation

Spread and size

Ackruti’s projects portfolio is spread across micro-markets in Mumbai, and concentrated in the central suburbs. We believe that the central suburbs of Mumbai and Bandra (E) would out-perform other markets in Mumbai on pricing in the next five years.

Fig 7 – Projects across Mumbai Company South South Central Central Bandra Western

Ackruti City 0.2 4.8 16.2 2.8 6.2

DB Realty - 9.3 0.9 10.0 20.1

HDIL 0.1 0.1 14.5 2.4 10.1

Sunteck Realty - 3.6 6.1 1.5 2.5

Oberoi Realty - 2.1 3.2 - 14.6

Source: Company

Also, its project sizes are smaller in South and South-Central Mumbai, and medium-to-large in the suburbs. This, we believe, could drive volume once such projects are launched.

Fig 8 – Number of smaller projects across Mumbai Company Number Residential Commercial

DB Realty 4 2 2

Ackruti City 20 15 5

HDIL 15 7 8

Sunteck Realty 7 5 2

Oberoi Realty 8 2 6

Source: Company

Launches need to pick up pace

FY10 saw residential and commercial sales of 2.16m sqft worth `8.4bn. Sales in 1HFY11 have been 0.94m sqft (ex TDR and FSI) for `8.7bn. Along with quick absorption of launched projects, the company has hiked prices, though accompanied by some volume slowdown.

Smaller projects at prime locations show brisk sales once launched

Ackruti did not launch any project in 3QFY11

28 January 2011 Ackruti City – Premium land, but needs to be developed; retain Buy

Anand Rathi Research 36

Fig 9 – Sales volume vs. sales value

0

1,600

3,200

4,800

6,400

8,000

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

0.0

0.2

0.4

0.6

0.8

1.0

Sales Value Sales Volume (RHS)

(`m) (msqft)

Source: Company

Further, on the sales value receivables front, Ackruti has been comparatively better than peers, with as much as 40% recovered from sales already concluded. Since all launches follow construction-linked payment plans, execution of launched projects is well on track.

Fig 10 – Sale value vs. sales value received

0

20

40

60

80

Ackr

uti C

ity

DB

Rea

lty

HD

IL

Sunt

eck

Rea

lty0

15

30

45

Value Sold Value Received (%) Received (RHS)

(`m) (%)

Source: Companies