Analyzing Transactions into Debit and Credit Parts Chapter 2.

38

Analyzing Transactions into Debit and Credit Parts Chapter 2

-

Upload

annabella-payne -

Category

Documents

-

view

301 -

download

3

Transcript of Analyzing Transactions into Debit and Credit Parts Chapter 2.

Analyzing Transactions into Debit and Credit

Parts

Chapter 2

Today’s Objectives

Engage prior knowledge using critical thinking skills

Demonstrate where a debit/credit is placed in a T-Account

Become familiar with the key elements and terms associated with analyzing transactions into Debit and Credit parts

Prior Knowledge

• Take out a sheet of paper• Open Books:

– Page 27

• Read about AAA

• When finished:– Discuss Critical Thinking #1 & #2 with

people sitting near you

Possible Answers…

• #1– What asset and liability account might AAA use to

record transactions?• Assets = Cash, Accounts Receivable, Supplies, etc.

Liability = Accounts Payable

• #2– List at least two (2) transactions AAA might record

• Buying supplies for cash• Buying supplies on account• Paying cash for salaries• Receiving cash for memberships

Introduction

• New Vocabulary– T Account– Debit– Credit– Normal Balance– Chart of Accounts

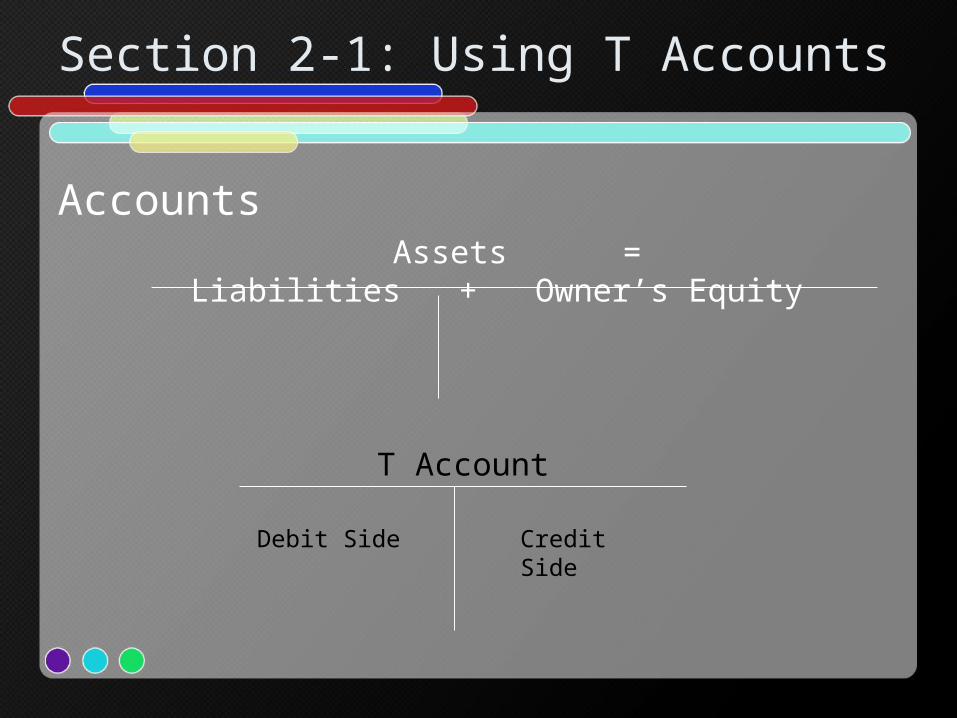

Section 2-1: Using T Accounts

Accounts Assets = Liabilities + Owner’s

Equity

T Account

Debit Side Credit Side

Accounts

Record summarizing all the information pertaining to a single item….

• Transactions change the balances of these accounts

• T account is an accounting device used to analyze transactions.

• Debit – amount recorded on left• Credit – amount recorded on right

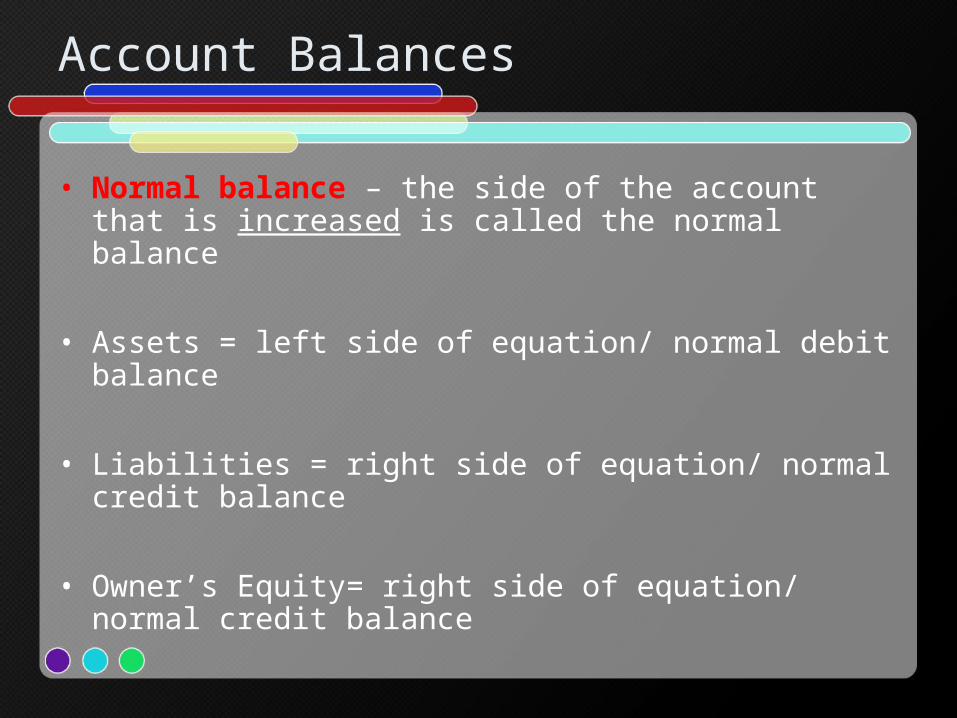

Account Balances

• Normal balance – the side of the account that is increased is called the normal balance

• Assets = left side of equation/ normal debit balance

• Liabilities = right side of equation/ normal credit balance

• Owner’s Equity= right side of equation/ normal credit balance

Rules –

Two basic accounting rules regulate increases and decreases in account balances

1. Account balances increase on the normal balance side of the account

2. Account balances decrease on the side opposite of the normal balance.

Debit & Credit

Assets Liabilities Owner’s Equity

Debit Debit DebitCredit Credit CreditNormal Balance

Normal Balance

Normal Balance

LET’S LEARN A CHEER!

• Everyone on the LEFT SIDE of the room:– “DEBITS ON THE LEFT!”

• Everyone of the RIGHT SIDE of the room:– “CREDITS ON THE RIGHT”

• EVERYONE TOGETHER:– “STAND UP. SIT DOWN. FIGHT, FIGHT,

FIGHT!”

Practice

• Handout• Working Together• On Your Own• Homework:

– Application Problem 2-1

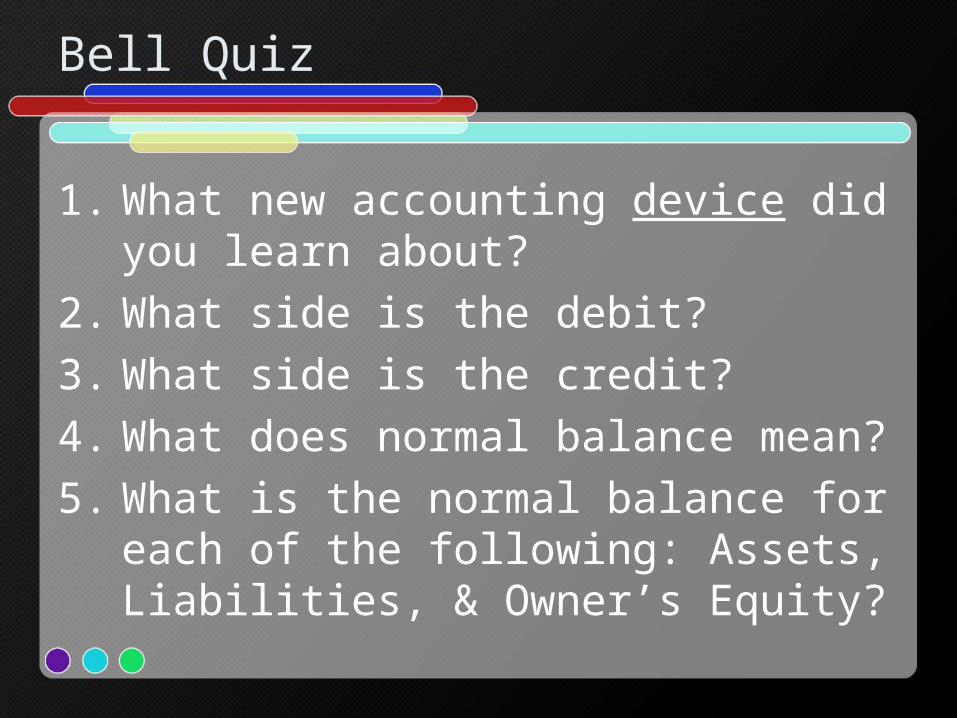

Bell Quiz

1. What new accounting device did you learn about?

2. What side is the debit?3. What side is the credit?4. What does normal balance mean?5. What is the normal balance for each

of the following: Assets, Liabilities, & Owner’s Equity?

Bell Quiz - Answers

1. T – Account2. Left3. Right4. Side the account increases on5. Debit, Credit, Credit

Review

• Creating T Accounts – Cheat Sheet• Go over Homework• Crossword Puzzle Review

Creating a Cheat Sheet

• Using the color paper make the following T accounts

• One large one• Small Assets • Small Liabilities• Small Owner’s Equity

– Follow Teacher Direction

2:2 – Analyzing How Transactions Affect Accounts

Steps to Analyzing a Transaction into Debit and Credit Parts

1. Which accounts are affected?2. How is each account classified?3. How is each classification changed?4. How is each amount entered in the

accounts?

Received Cash From Owner

Received cash from owner as an investment, $5,000.Remember:• Debits must equal credit

– DEBITS = CREDITS– Total Debits = Total Credits

1. What accounts? - Cash and Capital2. Assets & Owner’s Equity3. Increased, Increased4. Debit, Credit

A list of accounts used by a business is called a chart of accounts…..(page 3)

Cash OE

$5,000 $5,000

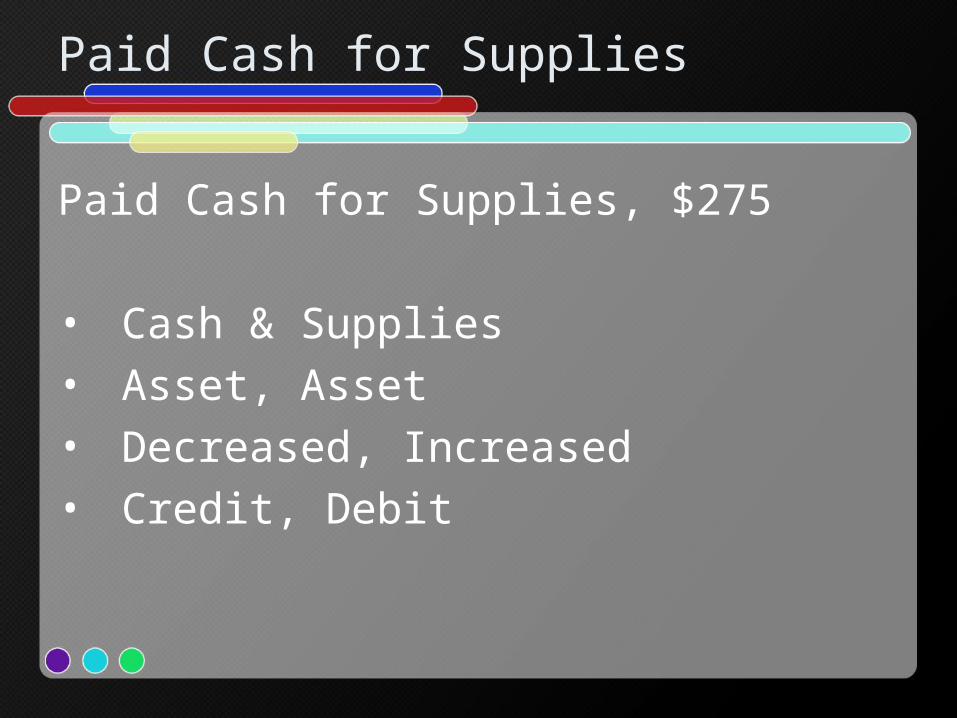

Paid Cash for Supplies

Paid Cash for Supplies, $275

• Cash & Supplies• Asset, Asset• Decreased, Increased• Credit, Debit

Paid Cash for Insurance

Paid cash for insurance, $1200.00

Cash and InsuranceAsset & AssetDecrease(Cash) Increase(PP

Insurance)Credit Cash Debit PP Insurance

Bought Supplies on Account

Bought Supplies on account from Supply Depot, $500.00

Supplies & A/P Suppy Depot

Asset LiabilityIncrease(Supplies) Increase (A/P)Debit Supplies Credit Cash

Paid Cash on Account

Paid Cash on account to Supply Depot, $300.00.

Cash & A/P Supply DepotAsset LiabilityDecrease DecreaseCredit Debit

Practice

• Working Together• On Your Own• Application 2-2

Pass Out Note cards INCREASE

INCREASE SIDEDebit

Credit

A D E = L O Rs r x I . es a p a E ve w e b . et I n I n

n s l ug e i e

ty

FLIP THE CARD OVER

DECREASE SIDEDebit

Credit

L O R A D EI . e s r xA E v s a pB . e e w eI n t i nL u n sI e g eTY

Analyzing How Transactions Affect Owner’s Equity

Received Cash from Sales, $295– Revenue increases OE– Separate account for revenue: Sales– OE has a Credit normal balance

• Therefore, Revenue has a credit normal balance

CashOE, Capital

Sales

$295 $295

Sold Services on Account

Sold services on account to Oakdale School, $350.

1. Which accounts are affected?1. Accounts Receivable-Oakdale Schools & Sales

2. How is each account classified?1. Asset Account Owner’s

Equity

3. How is each classification changed?1. Increases Increases

4. How is each amount entered in the accounts?1. Debit A/R Credit

SalesA/R Oakdale School Sales

$350 $350

Paid Cash for an Expense

Paid cash for Rent, $300• Expenses decrease OE• Separate expense accounts are used to summarize

these decreases– Rent Expense

• O.E. has normal credit balance– Therefore, Rent Expense has a normal debit

balance since it decreases OE

Rent Expense Cash

$300 $300

Received Cash on Account

Received cash on account from Oakdale School, $200.

1. Which accounts are affected?1. Cash & Accounts

Receivable-Oakdale Schools

2. How is each account classified?1. Asset Asset

3. How is each classification changed?1. Increases Decreases

4. How is each amount entered in the accounts?1. Debit Cash A/R Oakdale Schools

Cash A/R Oakdale School

$200 $200

Paid Cash to Owner for Personal Use

Paid cash to owner for personal use, $125.

• Withdrawals decrease OE• Normal Debit balance

1. Which accounts are affected?1. Kim Park, Drawing & Cash

2. How is each account classified?1. O.E.

Asset

3. How is each classification changed?1. Decreases Decreases

4. How is each amount entered in the accounts?1. Debit Kim Park, Drawing CashKim Park, Drawing Cash

$125 $125

ADE=LOR vs. LOR=ADE

• SIMPLY stated: ADE=LOR for the POSITIVE/normal balance side (and vice versa); LOR=ADE for the DECREASE side.

• Make a note card!

Practice

• Working Together• On Your Own• Application Problem 2-3

Group Exercise

• Analyzing T- Account– Based on the information recorded on

your t-accounts, Determine the transaction by analyzing the way it was recorded.

• Share

Individual Review

• Audit your Understanding p. 37 and 44

• Audit Test• Go over Homework• Introduce DEAD COIL• Application Problems 2-4, 2-5, 2-6

Review Day – Preparing for Test

• In the Life of a Credit Union• Class Cheer• Cases and Auditing for Errors• Study Guide – Pairs• Catch Phrase• Review Game

A Life With A Credit Union Activity

• In your group listen to the following story

• When I say debit pass your pencils to the left!

• When I say credit pass your pencils to the right!

Class Cheer

Debits on the LeftCredits on the RightStand up, Sit DownFight Fight Fight!

Practice/ Assignments

• Cases page 50• Auditing for errors• Study Guide – Pairs• Catch Phrase• Review Game

![Chapter 02 Analyzing and Recording Transactions...Chapter 02 – Analyzing and Recording Transactions 2-1 Chapter 02 Analyzing and Recording Transactions True / False Questions [Question]](https://static.fdocuments.us/doc/165x107/5ea240e72b04b75f702106a5/chapter-02-analyzing-and-recording-transactions-chapter-02-a-analyzing-and.jpg)