Analyzing Governor LePage’s Tax Reform Plan. Current-Law Tax System Sources of General Fund...

18

Analyzing Governor LePage’s Tax Reform Plan

-

Upload

margaret-jacobs -

Category

Documents

-

view

220 -

download

0

Transcript of Analyzing Governor LePage’s Tax Reform Plan. Current-Law Tax System Sources of General Fund...

Analyzing Governor LePage’s Tax Reform

Plan

$0.0

$300,000,000.0

$600,000,000.0

$900,000,000.0

$1,200,000,000.0

$1,500,000,000.0

$1,800,000,000.0

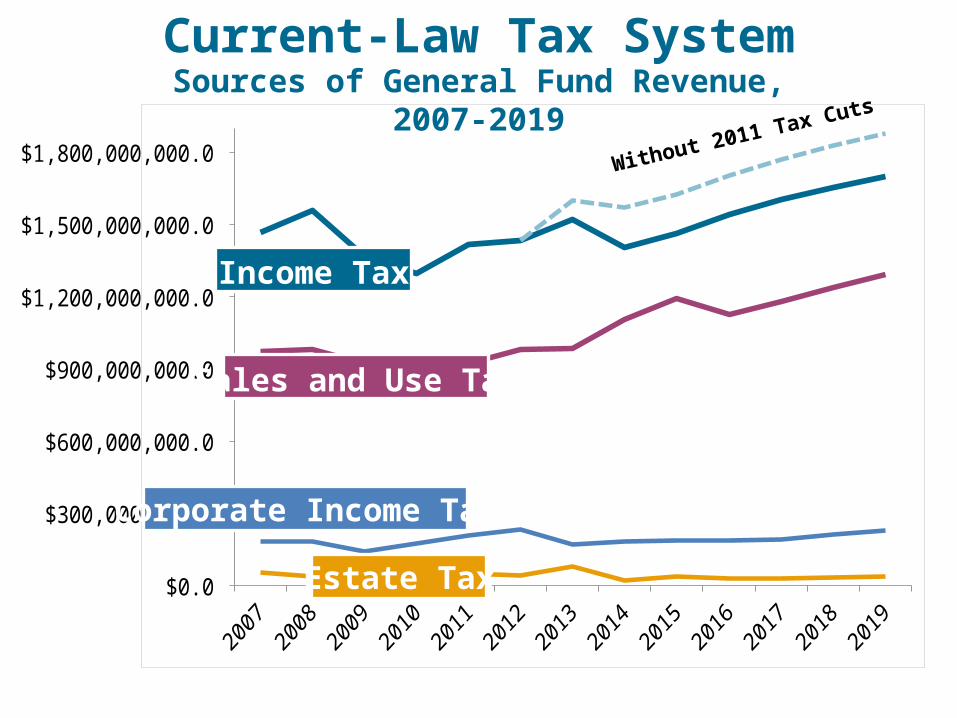

Current-Law Tax System Sources of General Fund Revenue,

2007-2019

Estate Tax

Income Tax

Corporate Income Tax

Sales and Use Tax

$0.0

$300,000,000.0

$600,000,000.0

$900,000,000.0

$1,200,000,000.0

$1,500,000,000.0

$1,800,000,000.0

Current-Law Tax System Sources of General Fund Revenue,

2007-2019

Estate Tax

Income Tax

Corporate Income Tax

Sales and Use Tax

Without 2011 Tax Cuts

$0.0

$300,000,000.0

$600,000,000.0

$900,000,000.0

$1,200,000,000.0

$1,500,000,000.0

$1,800,000,000.0

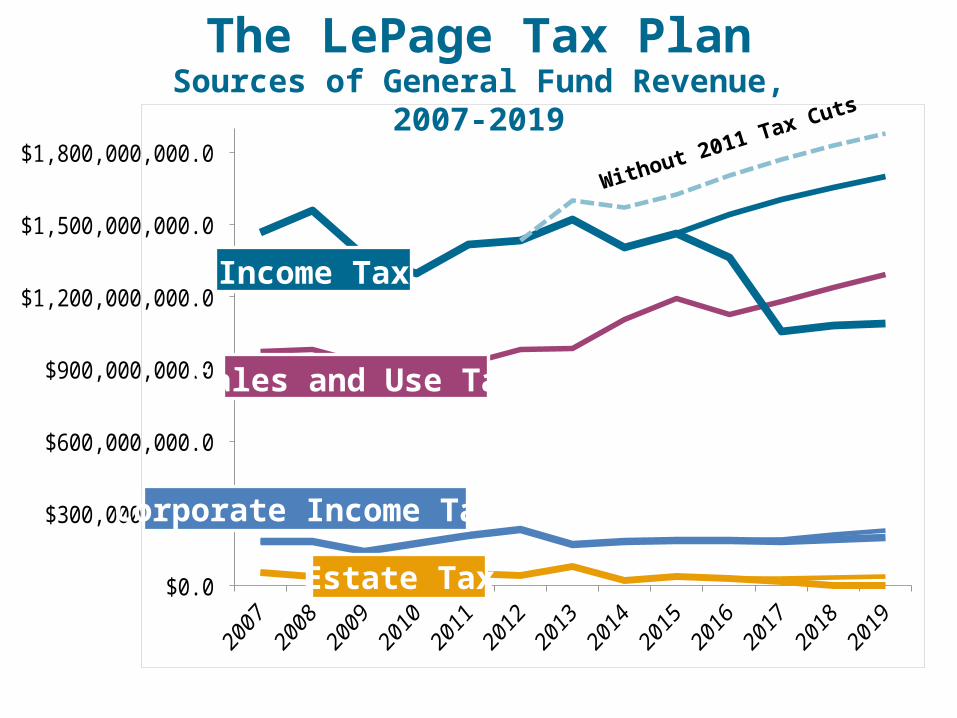

The LePage Tax Plan Sources of General Fund Revenue,

2007-2019

Estate Tax

Income Tax

Corporate Income Tax

Sales and Use Tax

Without 2011 Tax Cuts

$0.0

$300,000,000.0

$600,000,000.0

$900,000,000.0

$1,200,000,000.0

$1,500,000,000.0

$1,800,000,000.0

The LePage Tax Plan Sources of General Fund Revenue,

2007-2019

Estate Tax

Income Tax

Corporate Income Tax

Sales and Use Tax

Without 2011 Tax Cuts

Income Taxes -$610 Million

Estate Taxes -$37 Million

Corporate Taxes -$30 Million

Other -$13 Million

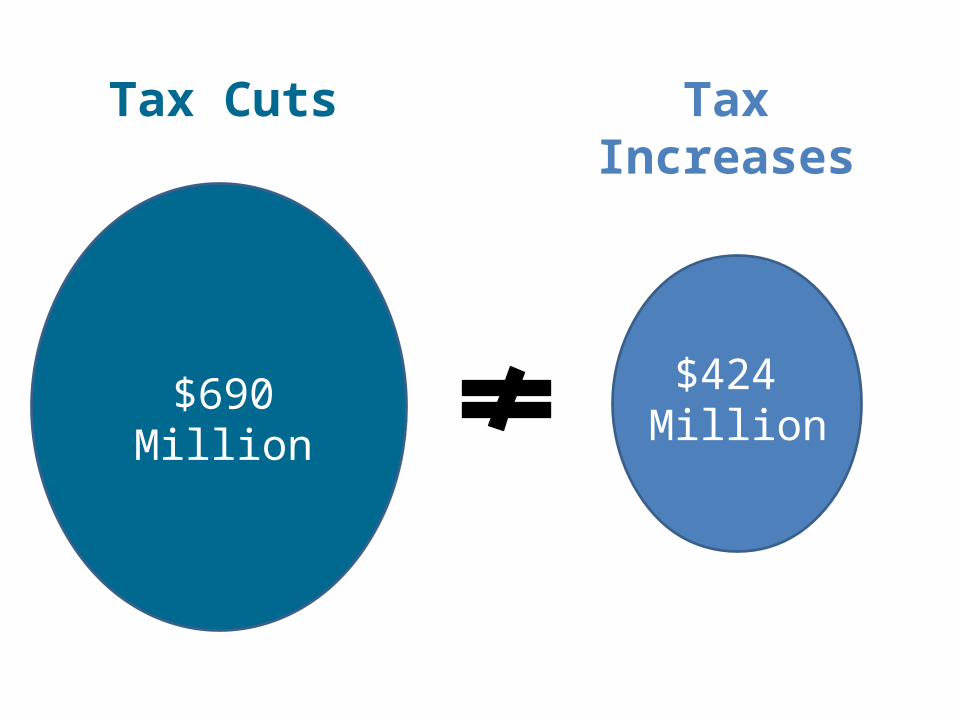

Summary of Tax Cuts in FY’19

-$690 Million

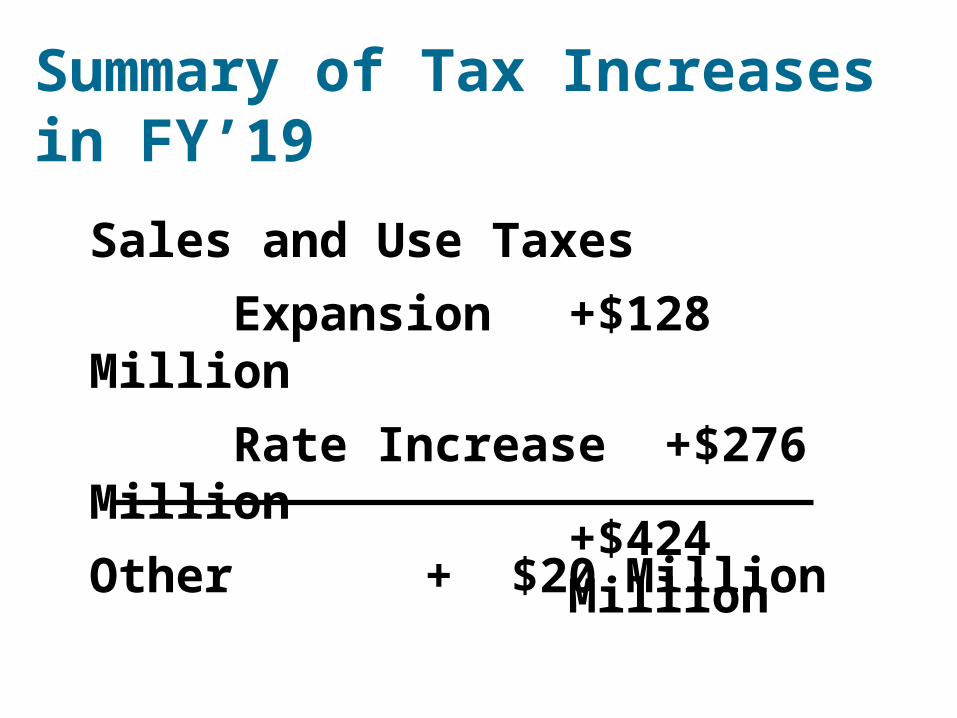

Summary of Tax Increases in FY’19

+$424 Million

Sales and Use Taxes

Expansion +$128 Million

Rate Increase +$276 Million

Other + $20 Million

$690 Million

Tax Cuts Tax Increases

$424 Million

$690M

Income and Estate Tax

Cuts

Sales Tax Increases + Spending Cuts

$424M

$266M

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

State Funding as a Share of the Economy is Historically

Low

General Fund + Revenue Sharing as a share of the economy

19861987

19881989

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

20062007

20082009

20102011

20122013

20142015

20162017

20182019

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

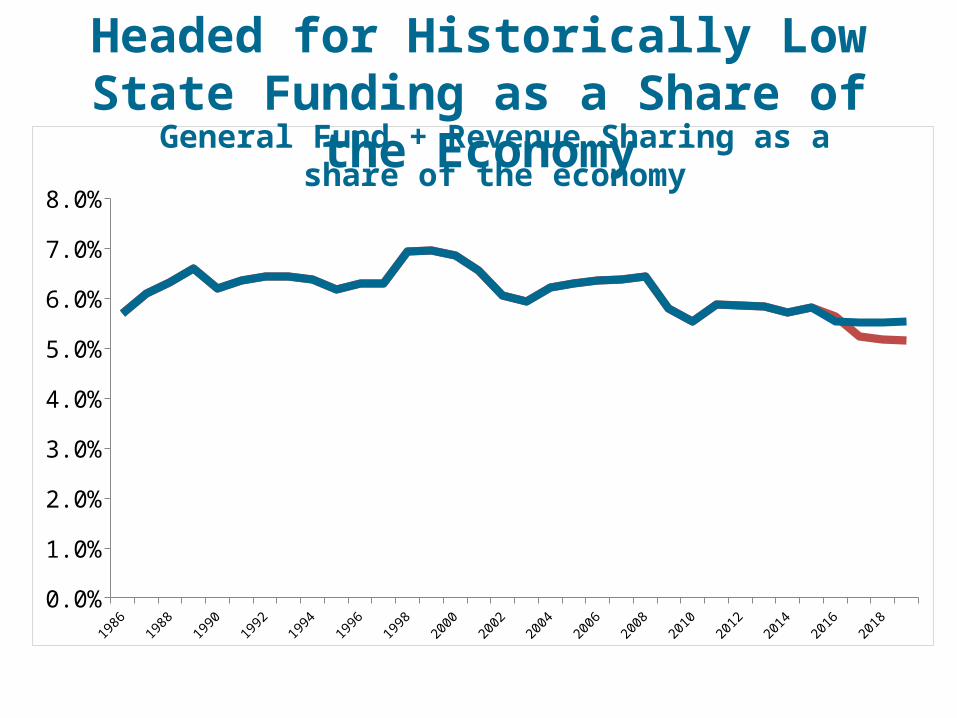

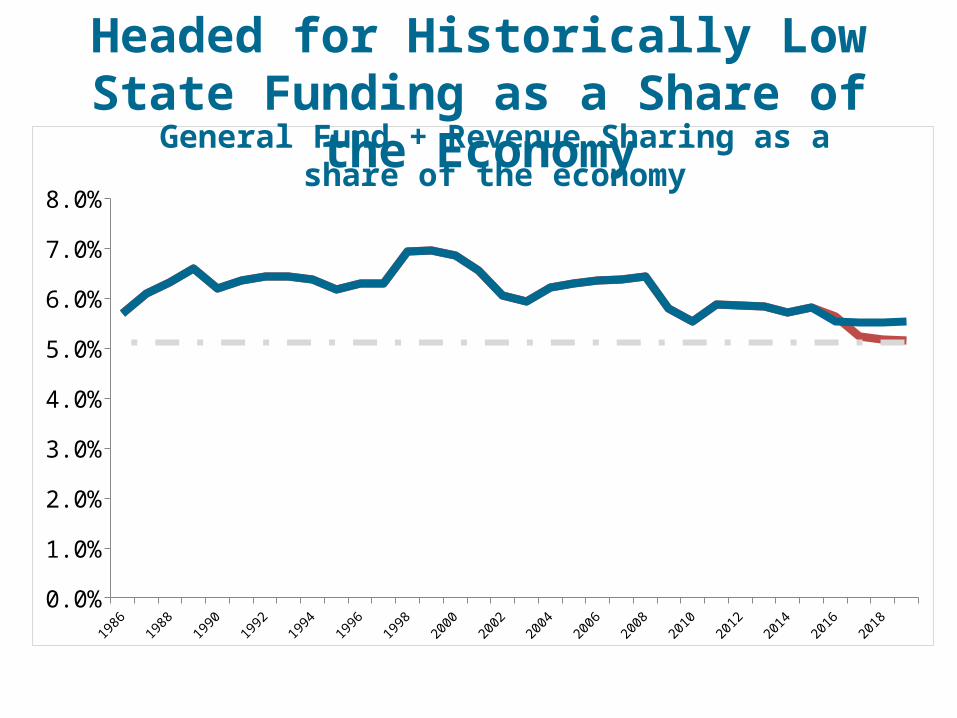

Headed for Historically Low State Funding as a Share of

the EconomyGeneral Fund + Revenue Sharing as a share of the economy

19861987

19881989

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

20062007

20082009

20102011

20122013

20142015

20162017

20182019

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Headed for Historically Low State Funding as a Share of

the EconomyGeneral Fund + Revenue Sharing as a share of the economy

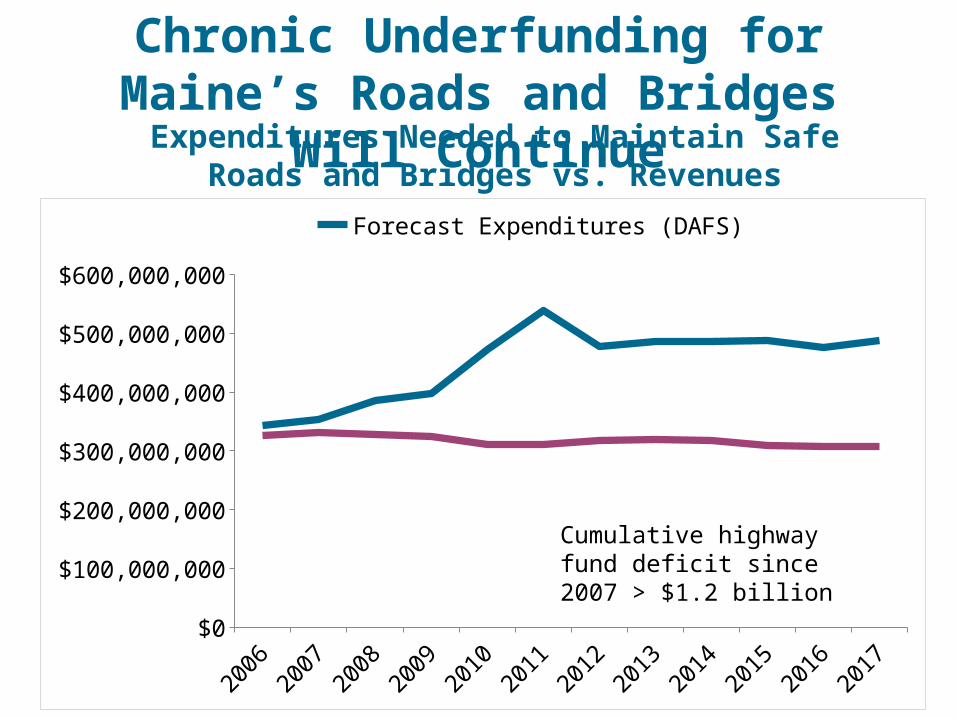

Chronic Underfunding for Maine’s Roads and Bridges

Will Continue

Expenditures Needed to Maintain Safe Roads and Bridges vs. Revenues

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

Forecast Expenditures (DAFS)

Cumulative highway fund deficit since 2007 > $1.2 billion

Elimination of Revenue Sharing With Towns and Cities =

Local Tax Increases

+ Local Spending

Cuts

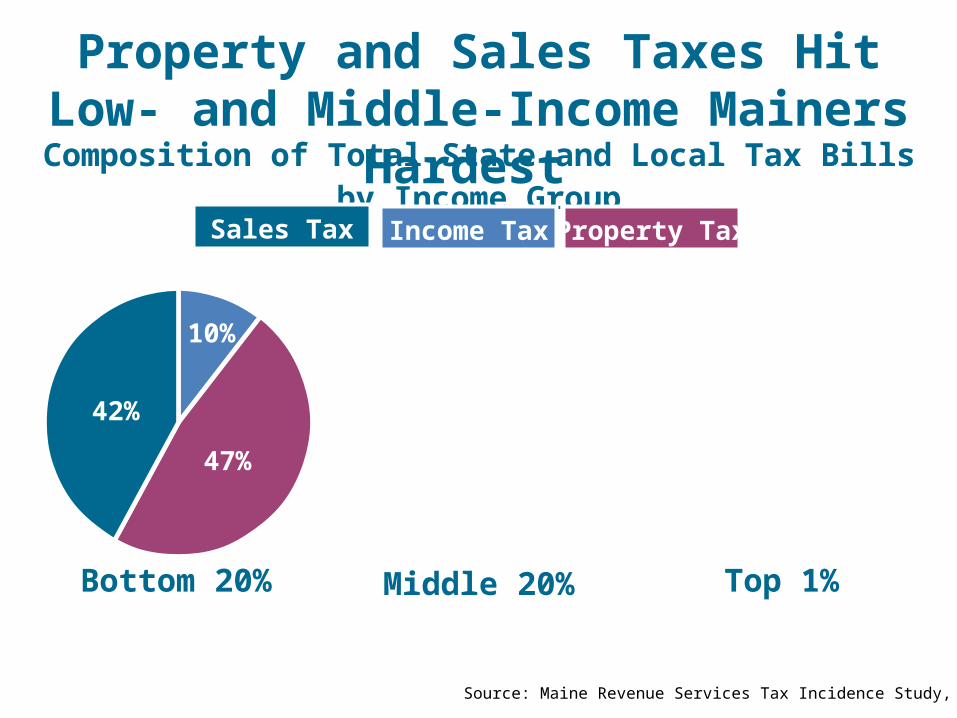

Composition of Total State and Local Tax Bills by Income Group

Property TaxSales Tax Income Tax

Property and Sales Taxes Hit Low- and Middle-Income Mainers

Hardest

Middle 20%Bottom 20% Top 1%

42%

47%

10%

32%

45%

23%

20%

17%

63%

Source: Maine Revenue Services Tax Incidence Study, 2009

I WIN!!!

I may come out ahead

too?!

Hmmm…

Hmmm…

Hmmm…

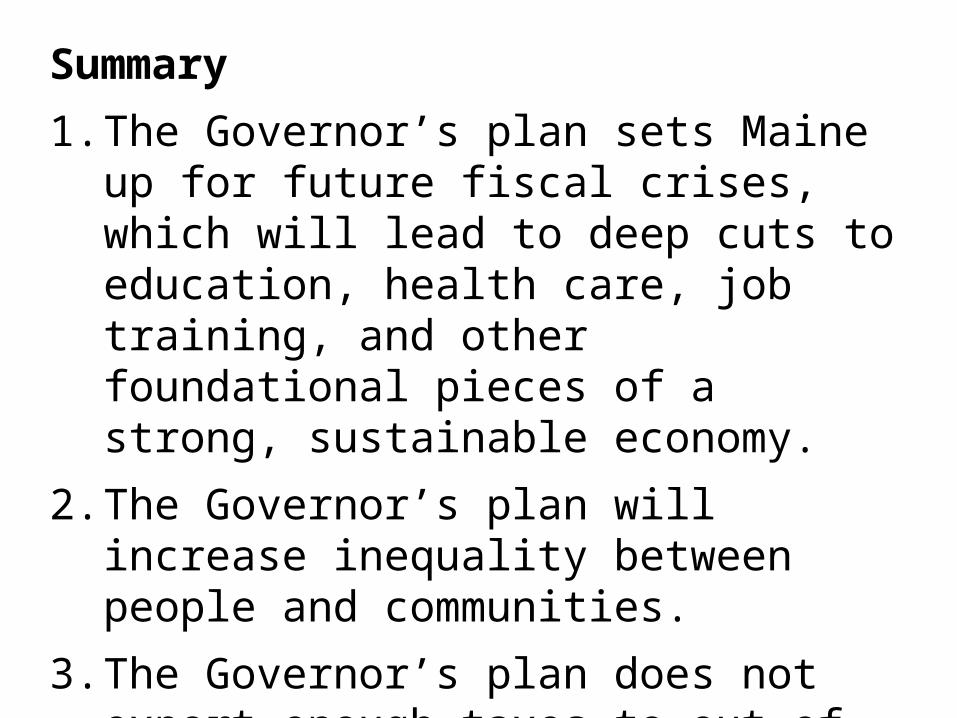

Summary

1. The Governor’s plan sets Maine up for future fiscal crises, which will lead to deep cuts to education, health care, job training, and other foundational pieces of a strong, sustainable economy.

2. The Governor’s plan will increase inequality between people and communities.

3. The Governor’s plan does not export enough taxes to out-of-state residents, seasonal residents, and tourists.

Joel [email protected]