Emerging Market Business Cycles: The Cycle Is the Trend - SSCC - Home

Upload

timothy212Category

view

1.113download

14

Analyzing economic fluctuations in emerging market economies

Carlos C. Bautista

Abstract

Economic fluctuations are analyzed by economists in order to understand how the economy responds to shocks caused by both the external environment and local events (both political and economic). Adequate knowledge of the causes and consequences of these shocks on the economy allows authorities to design policies that help dampen its adverse effects. In advanced economies, this field is a rich area of research known as empirical business cycle analysis. There is however a dearth of studies of this kind in emerging market economies. This research adopts the econometric techniques used in developed economy empirical business cycle research to examine emerging market economies.

In the absence of recession dating committees like the NBER in the US, the study makes use of Markov-switching (MS) regressions to establish and to date periods of rapid growth, moderate growth and crisis episodes in emerging market economies. Information about the state of the economy per period obtained from MS regressions is used to date regimes. A series representing the state of the economy, Yt, is constructed using MS smoothed probabilities such that Yt = s if

( ) ( ) ( ) ( ){ }3,2,1max tttt pppsp = ; where ( ) ( ) ( ) 1321 =++ ttt ppp . This series is used in ordered probit regressions to model the probability of occurrence of regimes, conditional on changes in a set of macroeconomic variables (e.g., exchange rates, interest rates, foreign exchange reserves and money supply.) Quarterly data from 1986 to 2005 are used in the study. The countries where data of suitable length are available to the author are used in the study. These are Korea, Malaysia, Philippines, Chile and Mexico. The models constructed seem to perform adequately as can be seen by their tracking ability and out-of-sample confirmation of rapid and moderate growth phases experienced by the countries under study.

Keywords: Markov-switching, ordered probit, rapid growth, moderate growth, crisis episodes JEL Classification: E32

January 2007 First Draft

Correspondence:

Carlos C. Bautista Tel +63 2 928 4571 College of Business Administration Fax +63 2 920 7990 University of the Philippines E–mail [email protected], Quezon City 1101, Philippines Web www.upd.edu.ph/~cba/bautista

Analyzing economic fluctuations in emerging market economies

Carlos C. Bautista

1 Introduction

Approximately two decades ago, one can unambiguously determine whether an economy is

highly developed or less developed. This convenient dichotomy has been rendered obsolete to a

large extent with globalization and advances in technology that led to increases in productivity.

The subsequent growth in per capita incomes in some less developed economies created new

markets and another class of economies that is neither highly developed nor less developed – the

emerging market economies. These economies that liberalized and opened their borders

experienced unprecedented growth and significant improvements in the standards of living of

their citizens.

The growth paths of these economies were not easy ones to trek however as they try to cope

with changes in the international environment given their inadequate institutional structures

(inefficient banking systems for example). For a number of them, these led to economic crises

emanating from the external sector. Researchers of aggregate economic fluctuations in emerging

market economies find this an interesting but difficult phenomenon to analyze because the

resulting patterns of aggregate fluctuations do not lend themselves well to standard statistical

analysis that assume linearity. Indeed, one will notice the dearth of studies examining emerging

market economic fluctuations. This research tries to fill in the gap and hopes to contribute to the

body of knowledge on the analysis of fluctuations in developing economies.

Recently developed macro-econometric techniques that try to deal with non-linear

relationships have been applied successfully in empirical business cycle research in highly

developed economies (See Hamilton and Raj, 2002, for a survey). This area of Macroeconomics

has been one of the most dynamic fields of research because far richer insights as to how the

Analyzing economic fluctuations in emerging market economies | cc bautista

economy operates have been obtained with these techniques. This study adopts these methods to

examine economic fluctuations in emerging market economies especially those which

experienced crisis episodes.

The objectives of the study are (1) to find an adequate statistical representation of the

movements and direction of aggregate economic activity in selected emerging market economies

using techniques in non-linear time series/business cycle analysis and (2) to make these results

useful for policy analysis and in forecasting the direction of economic activity. For each country

in the study, Markov-switching (MS) regression is used to identify the state of the economy per

period over a particular time frame. The novelty in this study is the use of MS regressions in

dating the cycles in these economies. That is, the state of the economy with the highest

probability of occurrence generated by the MS model is taken to be the true state. This is a strong

assumption that needs to be made because of the absence of agencies that officially date

recessions like the NBER of the U.S. The choice of the dating mechanism may be justified by the

excellent record of the MS regression model’s in-sample predictions of recessions in highly

developed economies (See for example, Hamilton (1989) for the U.S.) Moreover, dating

mechanisms other than the NBER official dates of previous studies are not very useful when the

level of classification is more than 2 states. In this study, emerging market economies are

assumed to fall into 3 states: rapid growth, moderate growth and crisis states.

With the regime dates determined from MS regressions, an attempt is made to predict the

probability of occurrence of the state of the economy using ordered probit. These models permit

the specification of a set of predictor variables (e.g., exchange rates, interest rates, foreign

exchange reserves and money supply). This is done for the following countries where data of

suitable length are available: Chile, Korea, Malaysia, Mexico, and the Philippines. The next

section of the study reviews the methods used. Section 3 discusses the empirical strategy, the

data, and the empirical results. The last section concludes.

2

Analyzing economic fluctuations in emerging market economies | cc bautista

2 Methods in empirical business cycle research

A huge literature on non-stationary business cycle analysis has been generated since the

seminal article of Hamilton (1989). His article is among the first to recognize the inherent

nonlinearities that are present in macroeconomic time series describing the time path of the

economy. He finds that an econometric evaluation of GDP growth with regimes endogenously

determined by Markov switches accurately describes the US business cycles and that the dates

generated by his model in fact coincides with the NBER recession dates.

Hamilton’s model was generalized by Lam (1990) to allow for a decomposition of the series

into a trend and a cycle. Lam was also able to replicate the NBER reference dates. Many other

extensions of the univariate MS regressions have been proposed and several applications to a

variety of problems in Macroeconomics and Finance can be found in the literature. Filardo (1994)

extended the Hamilton model to allow for time varying transition probabilities. In his study, the

duration of a state of the economy was made to vary with leading indicator variables. Kim (1994)

improved on Hamilton’s smoothing algorithm; Hamilton and Susmel (1994) studied ARCH

effects with Markov-switching in the US stock market and Krolzig (1997) provided an

implementation of Markov-switching VARs. A collection of more recent contributions can be

found in a volume edited by Hamilton and Raj (2002).

The original work by Burns and Mitchell emphasized 2 aspects of economic fluctuations: co-

movements of macroeconomic variables and characterization of business cycle phases into

expansions and recessions. The development of these ideas proceeded independently of each

other. The Markov-switching literature which focuses on the second aspect, developed alongside

models of co-movement: the dynamic factor models first used by Stock and Watson (1988, 1992)

in their articles on leading indicators. More recent work by Diebold and Rudebusch (1996)

allowed for regime switching in a dynamic factor model, thus allowing for joint analysis of co-

movements and business cycle phases.

3

Analyzing economic fluctuations in emerging market economies | cc bautista

To a certain extent, the recent literature on recession forecasting using qualitative dependent

variable modeling techniques pioneered by Estrella and Mishkin (1998) is related to the

coincident and leading indicator studies by Stock and Watson by the use of exogenous variables

in forecasting regime probabilities. The difference is that the latter does not rely on official

business cycle dates but rather, on the unobserved common components of the indicators

included in the study. Recession forecasting and regime probability modeling are also closely

related to studies on nonstationary business cycle analysis reviewed above but were developed at

a much later date. Both sets of studies use official dates of recessions determined by government

agencies as prediction targets. The main difference is that the latter is a univariate time series

technique while the former allows the utilization of other variables either as leading or coincident

indicators that enter the right-hand side of the forecasting equation.

Qualitative dependent variable models are a natural choice in the recession forecasting

literature because the problem being examined can be conveniently expressed as a choice of two

regimes. For example, zero is the value assigned to a recession and 1 to expansion. Estrella and

Mishkin (1998) make use of a logit model where financial variables are used as leading indicators

to forecast the US recessions. They find that a parsimonious specification is necessary to generate

reasonable predictions of recessions. The study also finds that in-sample and out-of-sample

forecast performance can differ significantly and that out-of-sample predictive performance can

be very dependent on the forecast horizon.

A similar study was done by Bernard and Gerlach (1998) for several European countries, the

US and Japan. Instead of using several financial and aggregate macroeconomic variables as in

Estrella and Mishkin, the term structure was used as the sole predictor of a recession. Recession

dates used for the G7 countries were obtained from a study by Artis et al (1995). Using logit

analysis, Birchenhall et al (1999) and Birchenhall et al (2001) attempted to predict business cycle

regimes for the US and the UK. In the UK study, they found that real money (M4) was the best

4

Analyzing economic fluctuations in emerging market economies | cc bautista

single leading indicator of a recession. In the case of the US, Dueker (2002) points out that there

seems to be some difficulties in predicting the 1990-91 recession even with a Markov switching

probit model.

Developed country analysis of aggregate economic activity diverges from LDC/emerging

market economies analysis because of the occurrence of crisis events which, while infrequent

relative to normal business cycle phases, renders 2-state models inadequate in providing a

realistic description of aggregate economic fluctuations. In almost all LDC studies, the focus is on

the prediction of the crisis and the formulation of early warning systems for use of policy makers

(See for example, Kaminsky and Reinhardt (2000)). A fairly recent application of nested logit in

the prediction of currency crisis was by Lau and Yan (2005). To predict speculative attacks and

determine successful defenses from attacks, they used data from 16 countries and utilized interest

differentials, and monetary and fiscal variables as explanatory variables. Liquidity and financial

fragility variables were found to be excellent predictors of a crisis. Except this last study that used

nested logit, all of the studies reviewed above assume two states of the economy – recession and

expansion - and all of them make use of reference dates and turning points determined by

government agencies of the respective countries or previous studies giving details of regime

histories.

The assumption that the state of the economy falls into two categories, while adequate for

most highly developed economies, may not be appropriate for emerging market economies

which have experienced crisis episodes. Sichel (1994) models the US economy with 3 business

cycle phases with the third phase being associated with a high-growth recovery phase. The

notion of a third phase was further developed by Kim and Murray (2002) who, extending the

Diebold and Rudebusch model, further decomposed recession into its permanent and transitory

components which are governed by Markov switching to be able to examine peak reversion

during the high-growth recovery phase.

5

Analyzing economic fluctuations in emerging market economies | cc bautista

This study follows a different path of analysis by assuming 3 states. As shown in the next

section, 2-state models classify the economy as falling into either a crisis or a non-crisis state,

which is not really interesting. This study seeks a further categorization of the non-crisis, normal

periods into high (or rapid) growth and low (or slow) growth states.1

As mentioned in the introduction, this study hinges heavily on the assumption that Markov

switching regressions correctly show the true state of the economy. This choice of rule to

determine the state of the economy is arguably the best given that one chooses from 3 states

instead of just 2. One can adopt rules similar to those made in studies analyzing turning points

(e.g., Birchenhall, 2001), but these procedures are not viable when the choice of regimes exceed 2.

The next section further discusses the empirical strategy and the estimation results.

3 Empirical strategy and estimation results

As outlined in the introduction above, MS regressions and ordered probit regressions are used

in sequence to examine economic fluctuations in selected emerging market economies. By

adopting these two techniques an improvement is made over the traditional way of analyzing

fluctuations especially in emerging market economies. Here, three states of the economy are

assumed instead of the two states assumed in the literature reviewed above. These states cover

periods of rapid growth, moderate growth and crisis episodes instead of the recession and

expansion phases. Hence instead of the traditional binary probit or logit regressions the study

uses ordered probit techniques.2

1 In this study, there is no range by which a particular growth figure can be associated with rapid or moderate growth. Here, rapid or moderate growth of a country is relative its own historical record. In this regard cross country comparisons cannot be done using this terminology because a country’s rapid growth figure could fall in the range of moderate growth in another.

2 Detailed discussions of the econometric techniques used here can be found in graduate textbooks; very brief expositions are relegated to the appendix.

6

Analyzing economic fluctuations in emerging market economies | cc bautista

From the univariate MS regressions of output growth, the state of the economy per period is

obtained and is assumed to be any of the three growth states mentioned above. The latent

variable used in the ordered probit models is then mapped using the probabilities of occurrence

of the state of the economy. A simple rule is followed in the determination of the state of the

economy per period. For each period, the state with the highest probability of occurrence,

denoted by Yt, is taken to be the prevailing state of the economy for that period. That is, Yt = s if

( ) ( ) ( ) ( ){ }3,2,1max tttt pppsp = ; where ( ) ( ) ( ) 1321 =++ ttt ppp .

The quarterly data used in this study come from different sources but a large portion was

obtained from the December 2005 IFS CD-ROM. The main indicator of economic activity in this

study is GDP growth. The MS regressions were estimated using GDP data (not deseasonalized)

from the earliest available data up to the last quarter of 1999. The cutoff date for the estimation

was chosen to be able to capture the effects of the Asian crisis. Post-crisis data are used for out-of-

sample prediction of the state of the economy.

Table 1 shows Hansen’s (1992, 1996) likelihood ratio tests of the null of a one-state AR(k)

model against the alternative of a 2-state Markov regime-switching model. As can be seen, for lag

lengths of 3 and 4, the tests show a rejection of the null hypothesis in most cases. As a

preliminary analysis, 2-state models were estimated and the results are shown in Table 2.

Statistically significant parameter estimates of two-state MS autoregressions for each of the five

countries under study can be seen from the table. It must be note however that 2-state models do

not seem to adequately capture normal movements in economic activity when economic crises

are deep. For example, the impact of the 1983-85 crisis in the Philippines is so huge that it dwarfs

the effects of the Asian crisis, causing a misclassification. These can be observed in Figure 1 which

shows the smoothed probabilities of each state along with actual growth rates using

deseasonalized GDP.

7

Analyzing economic fluctuations in emerging market economies | cc bautista

Next, the study proceeds to estimate 3-state MS autoregressions with maximum lag lengths of

4 as in the 2-state models. It is important to note here that because of the highly non-linear nature

of the problem, unrestricted maximum likelihood estimates of 3-state models are more difficult to

obtain. In this regard, some values of parameters that can be reasonably assumed to take on

boundary values were determined. This is not an unusual procedure and has been employed by

Hamilton (2005) in his study of U.S. unemployment. Inspection of the time series reveals that in

most cases, the movements in GDP growth around crisis periods show no abrupt decline from a

position of rapid growth to negative growth which indicates a crisis event. Rather, growth often

slows a bit before going into a crisis episode. This is also true when the economy is coming out of

the crisis – the economy does not shift immediately to a rapid growth path but has to climb

slowly out of the bottom. Hence, letting s = 1 as the state indicating rapid growth, s = 2 indicating

moderate growth and s = 3 representing a crisis state, it seems reasonable to assume that state 1 is

never followed by state 3 and vice versa. More precisely, let pij represent the transition

probabilities. This amounts to an assumption that p13 = p31 = 0.

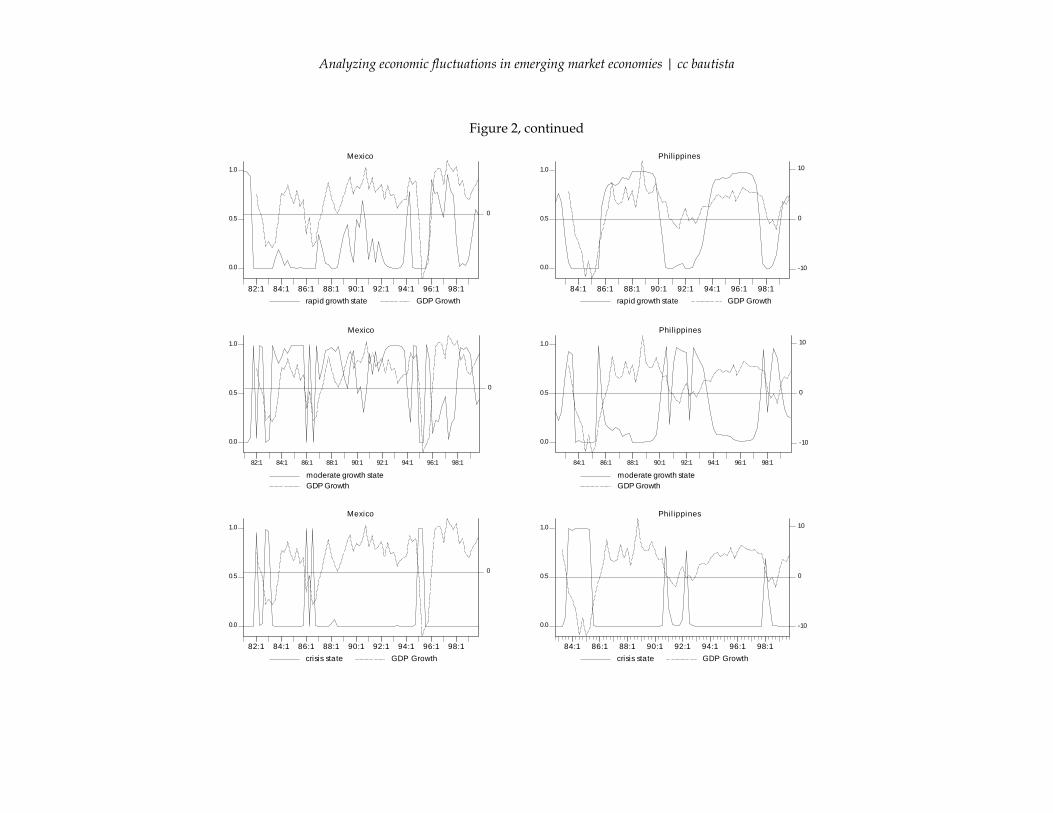

Table 3 reports the results of 3-state MS regression estimates. For each country, unrestricted

maximum likelihood estimates were computed and convergence was obtained for Chile,

Malaysia and the Philippines. The restrictions mentioned above were imposed for Korea and

Mexico in order to attain convergence. Table 4 shows the corresponding transition probability

matrix for each country estimate. To get an idea of how the 3-state MS model tracks economic

activity, Figure 2 plots the smoothed probabilities on the left scale and GDP growth on the right

scale. It is seen that this performs better than the 2-state model.

Table 5 presents the estimates of ordered probit models for each country. The study tries to

limit itself to major macroeconomic variables: nominal exchange rate, general price level, money

8

Analyzing economic fluctuations in emerging market economies | cc bautista

supply, and interest rate which appear in all country estimates.3 In some cases however, other

variables which are deemed important to the economy are included, e.g., for Mexico the price of

oil, foreign exchange reserves and country risk premium, defined as the difference between the

interest differential and the actual depreciation rate, were used. Also these variables percent

changes either on a quarterly or annually basis. The final estimates shown in the table were

chosen based on the pseudo-R2 and the significance of the coefficients.

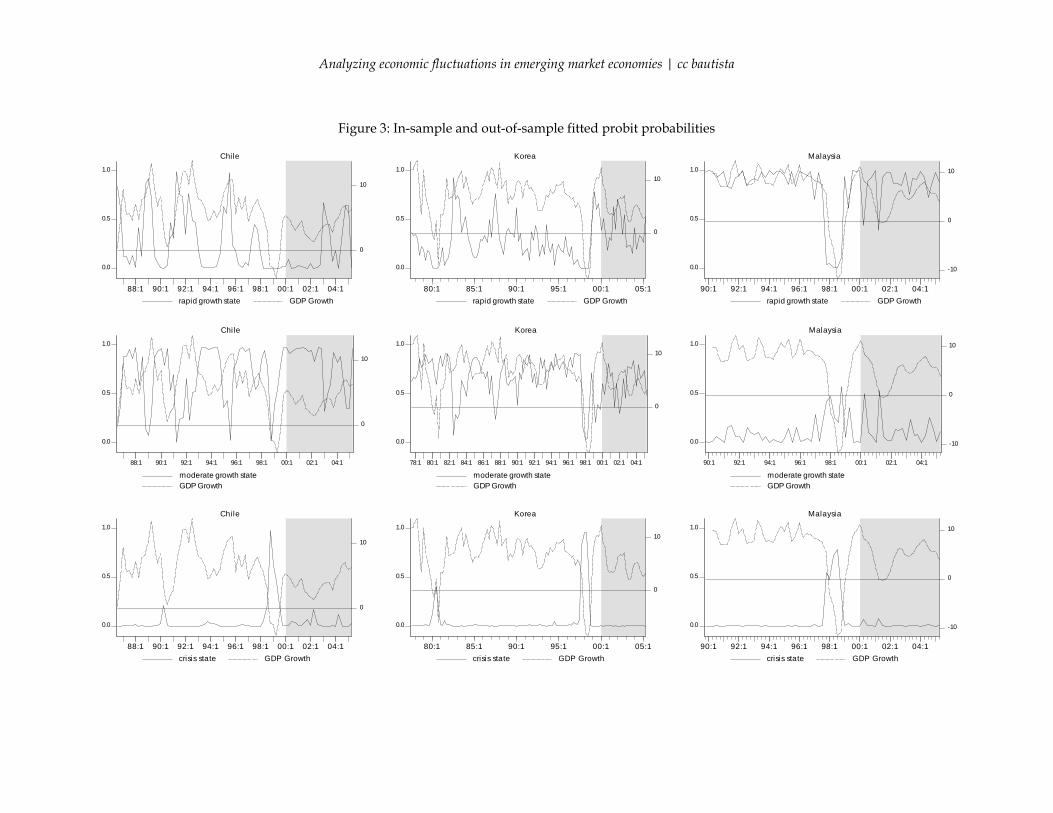

Figure 3 shows the fitted probabilities from the ordered probit estimates. For reference, the

annual GDP growth is also plotted as broken lines. The shaded portion of the graphs covers the

out-of-sample forecasts from 2000 to 2005. It is clear from the diagrams that no crisis events took

place in the countries under study during this period. There are however fluctuations in the

growth patterns in some of them. For Chile for example, the probability of rapid growth is

highest for the first half of 2003 and the last quarter of 2004 and first quarter of 2005. Korea’s

growth pattern shifted between moderate and rapid from 2000 to the end of 2002 and then

remained in moderate growth mode. Malaysia remained at the rapid growth state until it

experienced a slowdown in exports in 2001. This is reflected in the shift from rapid to moderate

growth in the third quarter of that year. For the Philippines, deviations from rapid growth took

place in the first quarter of 2001 when a radical change in the country’s leadership occurred as

seen in the diagram.

4 Concluding remarks

This study has demonstrated that it is possible to adopt econometric tools used to analyze

fluctuations in advanced economies to emerging market economies. The results above show that

the models constructed are able to track the movements of aggregate economic activity fairly well

and have satisfactory out-of-sample performance. This exploratory model building exercise make

3 Unit root tests of these variables are shown in the Appendix.

9

Analyzing economic fluctuations in emerging market economies | cc bautista

use data from five selected emerging market economies. This procedure outlined in this paper

can be adapted to other emerging market economies as well. The models above can be used for

policy analysis because it makes use of macroeconomic variables to track and predict growth. The

results show to some extent the usefulness of these macroeconomic variables in predicting

slowdowns. Also simulations can be done to determine under what combination of values of

these variables can lead to crisis situations – similar to early warning systems. This is not done in

this study but is an area of further research.

10

Analyzing economic fluctuations in emerging market economies | cc bautista

References

Artis M, Kontelemis Z, D Osborn, (1995), Classical business cycles for G7 and European countries, CEPR Discussion Paper 1137.

Bernard H and S Gerlach, (1998), Does the term structure predict recessions? The international evidence, International Journal of Finance and Economics 3, 195-215.

Bautista C, (2003), Estimates of output gaps in four Southeast Asian countries, Economics Letters 80(3), pp. 365-371.

Bautista C, (2002), Boom–bust cycles and crisis periods in the Philippines: A regime–switching Analysis, Philippine Review of Economics.

Birchenhall C, Jessen H, Osborn D and P Simpson, (1999), Predicting U.S. business-cycle regimes, Journal of Business and Economic Statistics 17(3), 313-323.

Birchenhall C, Osborn D and M Sensier, (2001), “Predicting UK business cycle regimes, Scottish Journal of Political Economy 48(2), 179-195

Davidson R and J MacKinnon, (1993), Estimation and Inference in Econometrics, Oxford University Press.

Diebold F and G Rudebusch, (1996), Measuring business cycles: A modern perspective, Review of Economics and Statistics, 67-77

Dueker, M (2002), Regime-dependent forecast and the 2001 recession, Economic Review, Federal Reserve Board of St Louis, 29-36.

Filardo, A, (1994), Business-cycle phases and their transitional dynamics, Journal of Business and Economic Statistics, 299-308.

Hamilton J, (2005), What’s real about the business cycle?, Federal Reserve Bank of St Louis Review, 435-452.

Hamilton J, (1989), A new approach to the economic analysis of nonstationary time series and the business cycle, Econometrica, 357–384.

Hamilton J, and B Raj, (2002), New directions in business cycle research and financial analysis, in Advances in Markov-Switching Models, Hamilton J, and B Raj (eds.), Physica-Verlag.

Hamilton J, and R Susmel, (1994), Autoregressive conditional heteroskedasticity and changes in regime, Journal of Econometrics, 64, 307 – 333.

Hansen, Bruce (1992), “The likelihood ratio test under nonstandard conditions: Testing the Markov switching model of GNP,” Journal of Applied Econometrics 7, S61-S82. Erratum (1996), vol 11, 195-198.

Kaminsky G and C Reinhardt (2000), On crisis, contagion and confusion, Journal of International Economics 51, 145-168.

Kim C-J, (1994), Dynamic linear models with Markov-switching, Journal of Econometrics, 60, 1–22.

Kim C-J and C Murray, (2002), Permanent and transitory components of recessions, in Advances in Markov-Switching Models, Hamilton J, and B Raj (eds.), Physica-Verlag.

Kim C-J and C Nelson, (1999), State-Space Models with Regime Switching, The MIT Press, Cambridge, Massachusetts, USA.

11

Analyzing economic fluctuations in emerging market economies | cc bautista

Krolzig M, (1997), Markov-switching vector autoregressions, modelling, statistical inference and application to business cycle analysis, Lecture Notes in Economics and Mathematical Systems 454, Berlin: Springer.

Lam P-S, (1990), The Hamilton model with a general autoregressive component, Journal of Monetary Economics, 409–432.

Lau L and I Yan, (2005), Predicting currency crisis with a nested logit model, Pacific Economic Review 10(3), 296-316.

Sichel D, (1994), Inventories and the three phases of the business cycle, Journal of Business and Economic Statistics 12, 269–277.

Stock S and M Watson (1992), A procedure for predicting recessions with leading indicators: Econometric issues and recent experience, NBER working paper 4014.

Stock S and M Watson (1988), A probability model of the coincident indicators, NBER working paper 2772.

12

Analyzing economic fluctuations in emerging market economies | cc bautista

Table 1: Hansen’s likelihood ratio test Chile Korea Malaysia

k Lags = 3 4 3 4 3 4 LR stat = 3.503 1.618 9.800 3.192 2.515 3.399

p-values Bandwidth: 0 0.012 0.478 0.000 0.016 0.077 0.011

1 0.010 0.437 0.000 0.017 0.102 0.013 2 0.009 0.398 0.000 0.014 0.105 0.015 3 0.006 0.359 0.000 0.013 0.119 0.017 4 0.010 0.349 0.000 0.011 0.134 0.025 5 0.012 0.328 0.000 0.011 0.144 0.029

Mexico Philippines

k Lags = 3 4 3 4 LR stat = 2.962 3.780 6.354 1.070

p-values Bandwidth: 0 0.018 0.000 0.000 0.676

1 0.030 0.002 0.000 0.671 2 0.026 0.002 0.000 0.675 3 0.025 0.002 0.000 0.680 4 0.031 0.002 0.001 0.663 5 0.028 0.003 0.001 0.646

H0: one-state AR(k) model; H1: 2-state Markov-switching model

13

Analyzing economic fluctuations in emerging market economies | cc bautista

Table 2 Two-State Markov Switching regression estimates

Chile Korea Malaysia Estimate SE Estimate SE Estimate SE μ1 1.821 0.244 2.311 0.080 2.238 0.113 μ2 -2.425 1.369 -1.840 0.255 -4.284 0.505 φ1 -0.265 0.122 -0.989 0.012 -0.565 0.143 φ2 -0.323 0.129 -0.976 0.015 -0.598 0.151 φ3 -0.222 0.121 -0.962 0.012 -0.508 0.149 φ4 0.592 0.122 0.360 0.146 σ2 3.834 0.876 3.880 0.590 2.639 0.571 p11 0.943 0.040 0.906 0.033 0.977 0.023 p22 0.268 0.308 0.339 0.128 0.655 0.267 LogLik. -79.12 -169.65 -49.02 Sample 1984:1-1999:4 1970:1-1999:4 1989:1-1999:4 Mexico Philippines Estimate SE Estimate SE μ1 1.009 0.135 0.888 0.170 μ2 -3.880 0.482 -2.382 0.485 φ1 -0.381 0.096 -0.380 0.101 φ2 -0.293 0.099 -0.365 0.102 φ3 -0.333 0.093 -0.359 0.103 φ4 0.569 0.091 0.616 0.101 σ2 2.177 0.421 3.619 0.657 p11 0.927 0.034 0.980 0.022 p22 0.275 0.173 0.815 0.159 LogLik. -87.37 -88.33 Sample 1980:1-1999:4 1981:1-1999:4

14

Analyzing economic fluctuations in emerging market economies | cc bautista

Table 3 Three-State Markov Switching regression estimates

Chile Korea Malaysia Mexico Philippines Estimate SE Estimate SE Estimate SE Estimate SE Estimate SE μ1 2.937 0.150 3.361 0.155 2.340 0.112 2.058 0.239 1.299 0.105 μ2 1.477 0.088 1.302 0.209 1.113 0.577 0.642 0.225 0.568 0.349 μ3 -2.994 0.325 -3.330 0.287 -3.831 0.481 -3.448 0.309 -2.505 0.206 φ1 -0.970 0.166 -0.992 0.009 -0.687 0.167 -0.939 0.049 -0.901 0.157 φ2 -1.023 0.163 -0.980 0.011 -0.714 0.176 -0.870 0.064 -0.896 0.159 φ3 -0.944 0.173 -0.966 0.009 -0.633 0.175 -0.910 0.049 -0.891 0.160 φ4 -0.064 0.160 0.253 0.170 0.095 0.157 σ2 1.721 0.359 1.949 0.407 2.246 0.529 1.566 0.408 2.136 0.431 p11 0.731 0.139 0.432 0.107 0.954 0.074 0.546 0.231 0.601 0.162 p12 0.086 0.053 0.302 0.107 0.405 0.310 0.189 0.144 0.152 0.084 p23 0.804 0.176 0.610 0.216 0.345 0.266 0.721 0.169 0.124 0.093 p32 0.096 0.047 0.041 0.024 0.200 0.223 0.098 0.044 0.199 0.154 p31 0.000 0.072 0.000 0.054 0.000 0.089 LogLik. -74.09 -154.15 -48.01 -93.64 -86.35 Sample 1984:1-1999:4 1970:1-1999:4 1989:1-1999:4 1980:1-1999:4 1981:1-1999:4

Table 4 Transition Probability Matrices

Chile Korea Malaysia 0.731 0.086 0.000 0.432 0.302 0.000 0.954 0.405 0.000 0.269 0.819 0.804 0.568 0.656 0.610 0.047 0.394 0.345 0.000 0.096 0.196 0.000 0.041 0.390 0.000 0.200 0.655

Mexico Philippines 0.546 0.189 0.000 0.876 0.199 0.000 0.454 0.714 0.721 0.124 0.649 0.399 0.000 0.098 0.279 0.000 0.152 0.601

15

Analyzing economic fluctuations in emerging market economies | cc bautista

16

Table 5 Ordered Probit Estimates

Chile Korea Malaysia Mexico Philippines Independent variables Coef P-val Coef P-val Coef P-val Coef P-val Coef P-val QUARTERLY PERCENT CHANGES: ln (xt/xt – 1) except for interest rates depreciation(t – 1) 0.127 0.126 0.143 0.001 0.075 0.006 inflation(t – 1) -1.159 0.024 0.204 0.000 money growth(t – 1) -0.217 0.000 -0.031 0.089 reserve growth(t – 1) -0.012 0.043 stock inflation(t – 1) -0.018 0.004 interest differential(t–1) 1.185 0.008 0.610 0.060 0.897 0.000 ave oil price(t – 1) -0.007 0.538 interest differential 0.322 0.058 ave oil price -0.036 0.003 country risk premium 0.048 0.090 ANNUAL PERCENT CHANGES: ln (xt/xt – 4) except for interest rates depreciation(t – 1) 0.041 0.000 money growth(t – 1) -0.047 0.077 reserve growth(t – 1) -0.061 0.000 -0.016 0.000 Depreciation 0.036 0.018 money growth -0.051 0.001 reserve growth 0.008 0.176 inflation 0.041 0.104

γ2 -1.965 0.005 -0.665 0.069 1.020 0.005 -0.870 0.002 2.571 0.000 γ3 2.446 0.001 2.810 0.000 2.716 0.001 4.821 0.000 4.506 0.000

Pseudo-R2 0.474 0.299 0.522 0.481 0.421

Figure 1: Two-state Markov switching smoothed probabilities and GDP growth

0.0

0.5

1.0

0

10

86:1 88:1 90:1 92:1 94:1 96:1 98:1normal growth state GDP Growth

Chile

0.0

0.5

1.0

0

10

86:1 88:1 90:1 92:1 94:1 96:1 98:1low growth state GDP Growth

Chile

0.0

0.5

1.0

0

10

75:1 80:1 85:1 90:1 95:1normal growth state GDP Growth

Korea

0.0

0.5

1.0

0

10

75:1 80:1 85:1 90:1 95:1low growth state GDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 91:1 92:1 93:1 94:1 95:1 96:1 97:1 98:1 99:1normal growth state GDP Growth

Malaysia

0.0

0.5

1.0

-10

0

10

90:1 91:1 92:1 93:1 94:1 95:1 96:1 97:1 98:1 99:1low growth state GDP Growth

Malaysia

0.0

0.5

1.0

0

82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1normal growth state GDP Growth

Mexico

0.0

0.5

0.0

0.5

1.0

1.0

0

82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1low growth state GDP Growth

Mexico

-10

0

84:1 86:1

10

88:1 90:1 92:1 94:1 96:1 98:1normal growth state GDP Growth

Phil ippines

0.0

0.5

1.0

-10

0

84:1 86:1

10

88:1 90:1 92:1 94:1 96:1 98:1low growth state GDP Growth

Phil ippines

Figure 2: Three-state Markov switching smoothed probabilities and GDP growth

0.0

0.5

1.0

0

10

86:1 88:1 90:1 92:1 94:1 96:1 98:1rapid growth state GDP Growth

Chile

0.0

0.5

1.0

0

10

75:1 80:1 85:1 90:1 95:1rapid growth state GDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 91:1 92:1 93:1 94:1 95:1 96:1 97:1 98:1 99:1rapid growth state GDP Growth

Malaysia

0.0

0.5

1.0

0

10

86:1 87:1 88:1 89:1 90:1 91:1 92:1 93:1 94:1 95:1 96:1 97:1 98:1 99:1

moderate growth stateGDP Growth

Chile

0.0

0.5

1.0

0

10

72:1 74:1 76:1 78:1 80:1 82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1

moderate growth stateGDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 91:1 92:1 93:1 94:1 95:1 96:1 97:1 98:1 99:1

moderate growth stateGDP Growth

Malaysia

0.0

0.5

1.0

0

10

86:1 88:1 90:1 92:1 94:1 96:1 98:1crisis state GDP Growth

Chile

0.0

0.5

1.0

0

10

75:1 80:1 85:1 90:1 95:1crisis state GDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 91:1 92:1 93:1 94:1 95:1 96:1 97:1 98:1 99:1crisis state GDP Growth

Malaysia

Analyzing economic fluctuations in emerging market economies | cc bautista

Figure 2, continued

0.0

0.5

1.0

0

82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1rapid growth state GDP Growth

Mexico

0.0

0.5

1.0

-10

0

10

84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1rapid growth state GDP Growth

Philippines

0.0

0.5

1.0

0

82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1

moderate growth stateGDP Growth

Mexico

0.0

0.5

1.0

-10

0

10

84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1

moderate growth stateGDP Growth

Philippines

0.0

0.5

1.0

0

82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1crisis state GDP Growth

Mexico

0.0

0.5

1.0

-10

0

10

84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1crisis state GDP Growth

Phil ippines

19

Analyzing economic fluctuations in emerging market economies | cc bautista

Figure 3: In-sample and out-of-sample fitted probit probabilities

0.0

0.5

1.0

0

10

88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1rapid growth state GDP Growth

Chile

0.0

0.5

1.0

0

10

80:1 85:1 90:1 95:1 00:1 05:1rapid growth state GDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1rapid growth state GDP Growth

Malaysia

0.0

0.5

1.0

0

10

88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1

moderate growth stateGDP Growth

Chile

0.0

0.5

1.0

0

10

78:1 80:1 82:1 84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1

moderate growth stateGDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1

moderate growth stateGDP Growth

Malaysia

0.0

0.5

1.0

0

10

88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1crisis state GDP Growth

Chile

0.0

0.5

1.0

0

10

80:1 85:1 90:1 95:1 00:1 05:1crisis state GDP Growth

Korea

0.0

0.5

1.0

-10

0

10

90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1crisis state GDP Growth

Malaysia

20

Analyzing economic fluctuations in emerging market economies | cc bautista

21

0.0

0.5

1.0

0

86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1rapid growth state GDP Growth

Mexico

0.0

0.5

1.0

-10

0

10

84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1rapid growth state GDP Growth

Philippines

0.0

0.5

1.0

0

86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1

moderate growth stateGDP Growth

Mexico

0.0

0.5

1.0

-10

0

10

84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1

moderate growth stateGDP Growth

Philippines

0.0

0.5

1.0

0

86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1crisis state GDP Growth

Mexico

0.0

0.5

1.0

-10

0

10

84:1 86:1 88:1 90:1 92:1 94:1 96:1 98:1 00:1 02:1 04:1crisis state GDP Growth

Phil ippines

Figure 3, continued

Appendix

Markov-Switching Regression

The univariate MS regression model used in this study is of the form:

1) ( ) ( ) tsktkstst ktttyyy εμφμφμ +−++−+=

−− −− ...111

where yt is the variable of interest; in this study, this variable is output growth; the φks are the k autoregression parameters and εt is a white noise process. is the mean of y

tsμ t when the economy is in state st. In this study, the state of the economy is assumed to be the outcome of an unobserved first-order 3-state Markov process (i.e., st = 1, 2, 3). Its evolution can be described by transition probabilities, ( ) ijtt pisjs === − 1Pr , that can be written in matrix form:

2) ⎥⎥⎥

⎦

⎤

⎢⎢⎢

⎣

⎡=

332313

332212

312111

ppppppppp

P

where . Each element shows the probability that state i is followed by state j. The

process is assumed to depend on past values of y

∑=

=3

1

1j

ijp

t and st only through st–1. Note that since only yt is observed but not the state of the economy, a way must be found to form optimal inferences about the current state based on the observed values of yt. Given the number of states, Hamilton (1989) shows how to estimate the parameters of the model and the transition probabilities governing the motion of the variable of interest. He provides a recursive method for drawing probabilistic inferences about what state the economy is in (the value of st) given the history of yt. This is the basic MS regression that is going to be utilized in the proposed study to establish regime dates. As mentioned in the review above, several extensions of the basic model have been done since then (see also Kim and Nelson (1999).) A three-state model has been estimated for the Philippines by Bautista (2002).

Ordered Response Models

In ordered response models, one can specify a latent variable, , that are assumed to be *ty

influenced by a set of exogenous variables. Suppose there are K exogenous variables denoted by xkt, where k = 1, …, K. Then one can write:

3) tttKtKtt zxbxbby εε +=++++= ...110*

εt is a disturbance term. The latent variable, , can be mapped onto an ordered categorical *ty

variable:

4)

3*

2

2*

1

1*

0

3

2

1

ayaifY

ayaifY

ayaifY

tt

tt

tt

≤<=

≤<=

≤<=

Analyzing economic fluctuations in emerging market economies | cc bautista

where a0, a1, a2 and a3 are thresholds that serve to determine the value of Yt to be given to the latent variable. To preserve the ordering, these thresholds that are to be estimated econometrically along with the coefficients of equation (4) must satisfy: a0 > a1 > a2 > a3. The latent variable’s boundary values are unknown. Hence, one can simply set the beginning and ending thresholds to minus and plus infinity respectively (in this case, a0 = –∞ and a3 = +∞) and need not be estimated. From the above expressions, one can write the ordered regression model as:

5)

( ) ( )( )

( ) ( )( ) ( )

( ) ( )( )t

ttKttt

tt

tttKttt

t

ttKttt

zaFzaxxY

zaFzaFzazaxxY

zaFzaxxY

−−=

−≥==

−−−=

−≤<−==

−=

−≤==

2

21

12

211

1

11

1Pr...,,3Pr

Pr...,,2Pr

Pr...,,1Pr

ε

ε

ε

where F denotes the cumulative distribution function of ε. Let there be a total of T sample periods, (t = 1, …, T), each of which can be treated as a single draw from a multinomial distribution. Suppose T1, T2 and T3 are the number of periods belonging to states 1, 2 and 3 respectively, with T1 +T2 + T3= T. Then the likelihood of observing the sample is given by:

6) ( ) ( ) ( )[ ] [ ( )] 3212121 1 T

tT

ttT

t zaFzaFzaFzaFL −−−−−−=

The parameters of the model, the ah’s and the bk’s, can be estimated by maximizing the (log of the) likelihood function given by equation (6). can be computed once the b coefficients are tzestimated. With estimates of the limit coefficients, , and , the probability of being at a sahˆ tzparticular state can be predicted for each period t in the sample:

7)

( )

( ) ( )

( )tt

ttt

tt

zaFp

zaFzaFp

zaFp

ˆˆ1ˆ

ˆˆˆˆˆ

ˆˆˆ

23

122

11

−−=

−−−=

−=

where . The disturbance term, ε1ˆˆˆ 321 =++ ttt ppp t, can be assumed to follow a normal or a logistic distribution to produce either the ordered probit or the ordered logit model, respectively. A good reference on qualitative and limited dependent variables regression like the above is Davidson and MacKinnon (1993). Ordered probit and logit models are known to be well-behaved and are easily implemented using commercially available econometric programs.

23