Analyzing and Recording Transactions

60

© The McGraw-Hill Companies, Inc., 2005 McGraw-Hill/Irwin Analyzing and Recording Transactions Chapte r

-

Upload

nissim-norris -

Category

Documents

-

view

60 -

download

6

description

Analyzing and Recording Transactions. Chapter. Learning objectives. Analyzing and Recording Process Source document, Accounts & Ledger T-account vs. Debit & Credit Double-Entry Accounting Journalizing and Posting transactions Transaction analysis for FastForward Trial Balance. - PowerPoint PPT Presentation

Transcript of Analyzing and Recording Transactions

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Analyzing and Recording Transactions

Chapter

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

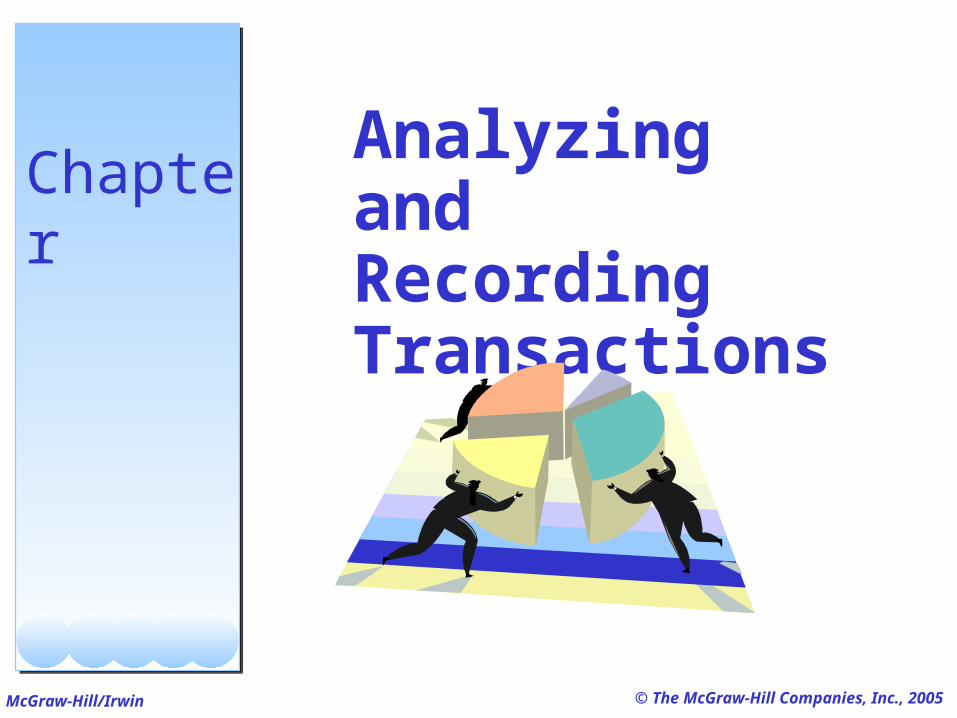

Learning objectivesLearning objectives

1. Analyzing and Recording Process

2. Source document, Accounts & Ledger

3. T-account vs. Debit & Credit

4. Double-Entry Accounting

5. Journalizing and Posting transactions

6. Transaction analysis for FastForward

7. Trial Balance

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

External Transactions occur between the

organization and an outside party.

Internal Transactions occur within the

organization.

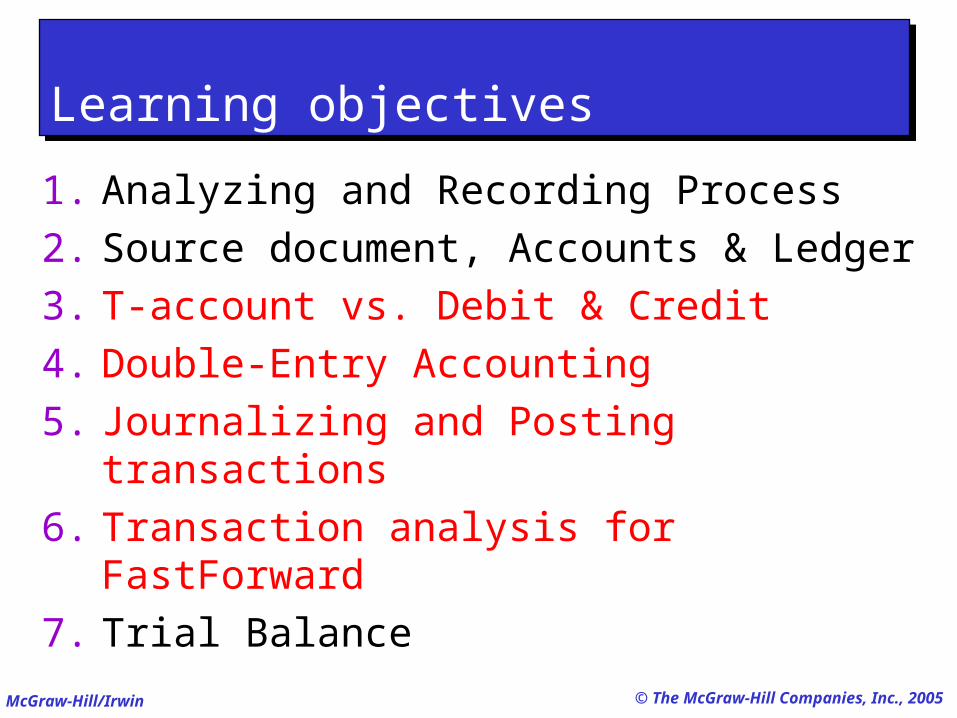

1. Analyzing and Recording Process- Transactions

1. Analyzing and Recording Process- Transactions

Exchanges of economic consideration between two parties.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Analyze each transaction and event form source documents

1.Analyzing and Recording Process - Transaction recording process1.Analyzing and Recording Process - Transaction recording process

Record relevant transactions and events in a journal

Post journal information to ledger accounts

Prepare and analyze the trial balance

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Sales Tickets

Bank Statement

Purchase Orders

Checks

2.Source Documents, Accounts & Ledger - Source documents2.Source Documents, Accounts & Ledger - Source documents

Bills from Suppliers

Employee EarningsRecord

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

An account is a record of

increases and decreases in a specific asset, liability, equity,

revenue, or expense item.

An account is a record of

increases and decreases in a specific asset, liability, equity,

revenue, or expense item.

2.Source Documents, Accounts & Ledger - The Account and its Analysis2.Source Documents, Accounts & Ledger - The Account and its Analysis

The general ledger is a record

containing all accounts used by

the company.

The general ledger is a record

containing all accounts used by

the company.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

LiabilitiesAccountsLiabilitiesAccounts

EquityAccounts

EquityAccounts

AssetsAccounts

AssetsAccounts

= +

2.Source Documents, Accounts & Ledger - The Account and its Analysis2.Source Documents, Accounts & Ledger - The Account and its Analysis

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

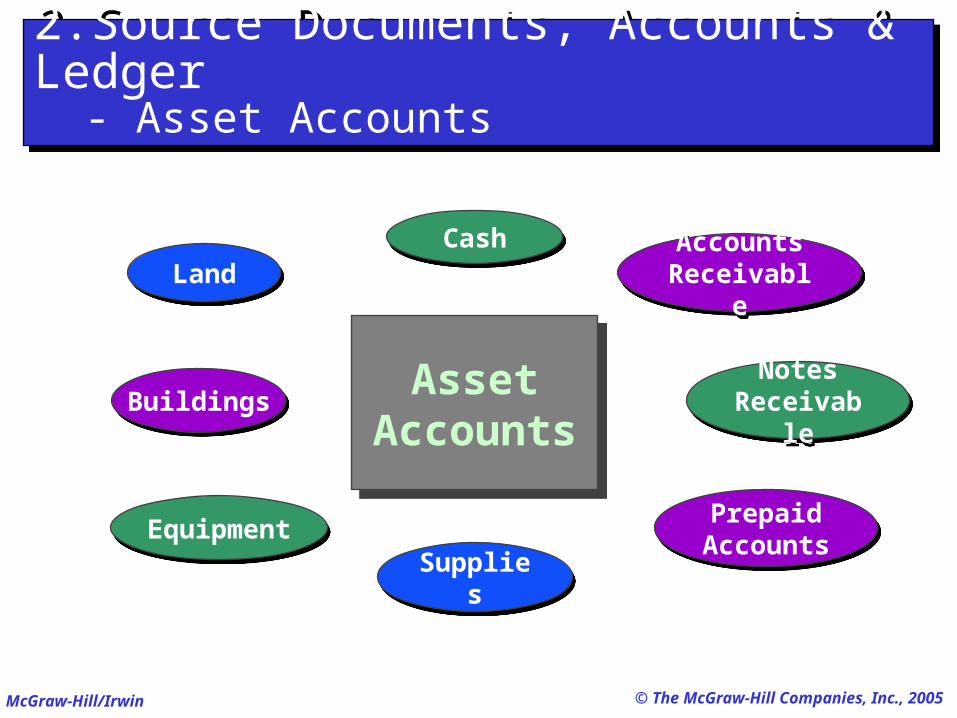

LandLand

EquipmentEquipment

BuildingsBuildings

CashCash

Notes Receivabl

e

Notes Receivabl

e

SuppliesSupplies

Prepaid AccountsPrepaid

Accounts

Accounts ReceivableAccounts

Receivable

AssetAccounts

AssetAccounts

2.Source Documents, Accounts & Ledger - Asset Accounts2.Source Documents, Accounts & Ledger - Asset Accounts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Accrued LiabilitiesAccrued

LiabilitiesUnearned RevenuesUnearned Revenues

Notes PayableNotes

PayableAccounts Payable

Accounts Payable

LiabilityAccountsLiability

Accounts

2.Source Documents, Accounts & Ledger

- Liability Accounts

2.Source Documents, Accounts & Ledger

- Liability Accounts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

EquityAccounts

EquityAccounts

RevenuesRevenues

Owner’s Capital

Owner’s Capital

Owner’s Withdrawals

Owner’s Withdrawals

ExpensesExpenses

2.Source Documents, Accounts & Ledger - Equity Accounts2.Source Documents, Accounts & Ledger - Equity Accounts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

LiabilitiesLiabilities EquityEquityAssetsAssets = +

2.Source Documents, Accounts & Ledger

- The Account and its Analysis

2.Source Documents, Accounts & Ledger

- The Account and its Analysis

Owner’s Capital

Owner’s Capital

Owner’s Withdrawals

Owner’s Withdrawals RevenuesRevenues ExpensesExpenses

+ +– –

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

A T-account represents a ledger account and is a tool used to understand the effects of one or more

transactions.

3. T-Account VS. Debits & Credits3. T-Account VS. Debits & Credits

(Left side) (Right side)Debit Credit

T- Account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

LiabilitiesLiabilities EquityEquityAssetsAssets = +

3. T-Account VS. Debits & Credits - Rules for debit & credit accounts3. T-Account VS. Debits & Credits - Rules for debit & credit accounts

Debit Credit Debit Credit Debit Credit

ASSETS

+ - + -

LIABILITIES

- + - +

EQUITIES

- + - +

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

RevenuesRevenues ExpensesExpensesOwner’s Capital

Owner’s Capital

Owner’s Withdrawals

Owner’s Withdrawals

__ ++ __

Debit Credit

Capital

- + - + Debit Credit

Withdrawals

+ - + - Debit Credit

Expenses

+ - + -Debit Credit

Revenues

- + - +

3. T-Account VS. Debits & Credits - Rules for debit & credit accounts(cont.)3. T-Account VS. Debits & Credits - Rules for debit & credit accounts(cont.)

EquityEquity

Exh.3.8

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

3. T-Account VS. Debits & Credits - account balance3. T-Account VS. Debits & Credits - account balance

An account balance is the difference between the increases and decreases in an account.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

LiabilitiesLiabilities EquityEquityAssetsAssets = +

4. Double-Entry Accounting4. Double-Entry Accounting

Each transaction affect al least 2 accounts In each transactions, amount debited = amount credited For all transactions, sum of debits = sum of credits Sum of debit account balance = sum of credit account

balance

Debit Credit Debit Credit Debit Credit

ASSETS

+ - + -

LIABILITIES

- + - +

EQUITIES

- + - +

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

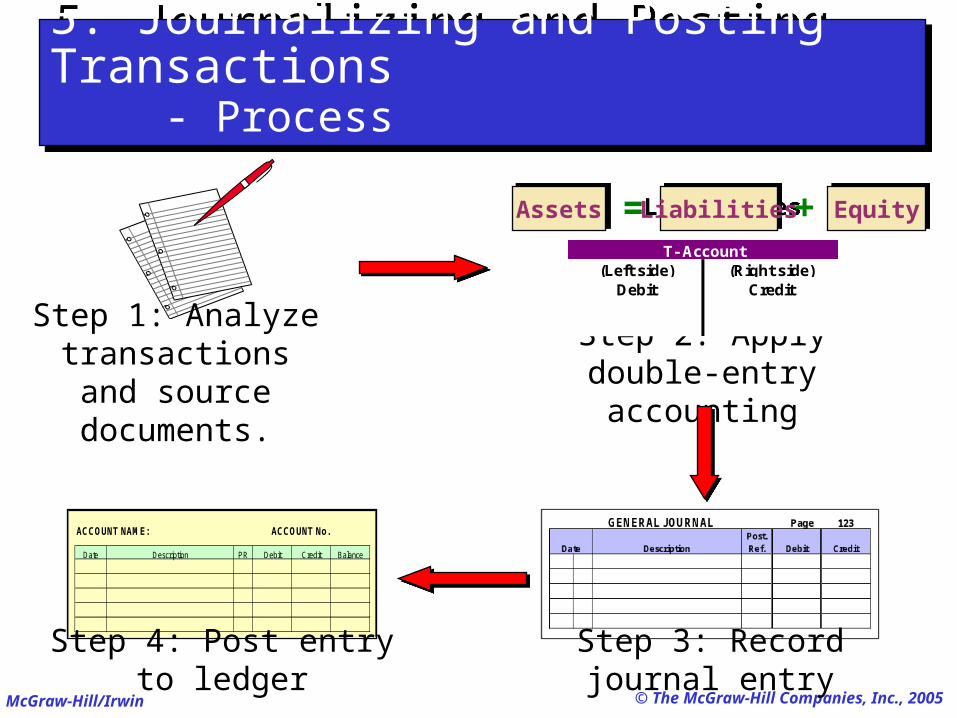

5. Journalizing and Posting Transactions - Process5. Journalizing and Posting Transactions - Process

Step 1: Analyze transactions and source

documents.

LiabilitiesLiabilities EquityEquityAssetsAssets = +

Step 2: Apply double-entry accounting

(Left side) (Right side)Debit Credit

T- Account

ACCOUNT NAME: ACCOUNT No.

Date Description PR Debit Credit Balance

Step 4: Post entry to ledger Step 3: Record journal entry

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Dollar amount of debits and credits

Dollar amount of debits and credits

5. Journalizing and Posting Transactions

- Journalizing Transactions

5. Journalizing and Posting Transactions

- Journalizing Transactions

Transaction Date

Transaction Date

Transaction explanation

Transaction explanation

Titles of Affected Accounts

Titles of Affected Accounts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

T-accounts are useful illustrations, but balance column ledger accounts are used in practice.

Three more columns• Post reference column• Description column• Balance column

5. Journalizing and Posting Transactions - Balance Column Account5. Journalizing and Posting Transactions - Balance Column Account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

11 Identify the account.

5. Journalizing and Posting Transactions

- Posting Journal Entries

5. Journalizing and Posting Transactions

- Posting Journal Entries

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

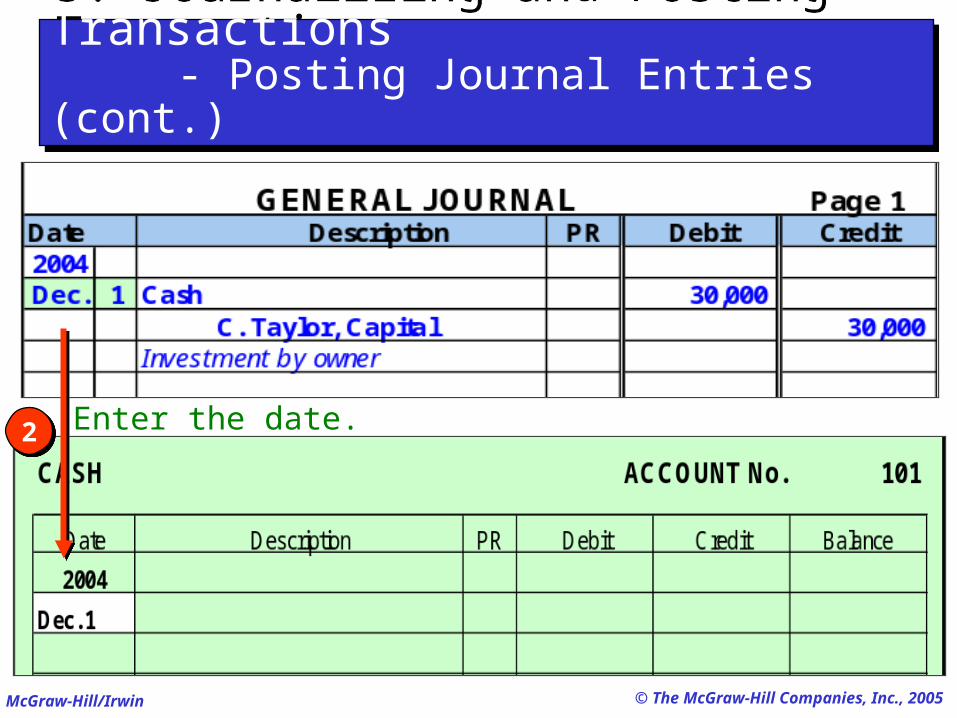

22 Enter the date.

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.)5. Journalizing and Posting Transactions - Posting Journal Entries (cont.)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

33Enter the amount and description.

5. Journalizing and Posting Transactions - Posting Journal Entries (cont.)5. Journalizing and Posting Transactions - Posting Journal Entries (cont.)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

44Enter the journal reference.

5. Journalizing and Posting Transactions

- Posting Journal Entries (cont.)

5. Journalizing and Posting Transactions

- Posting Journal Entries (cont.)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

55

Compute the balance.

5. Journalizing and Posting Transactions

- Posting Journal Entries (cont.)

5. Journalizing and Posting Transactions

- Posting Journal Entries (cont.)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Enter the ledger reference. 66

5. Journalizing and Posting Transactions

- Posting Journal Entries (cont.)

5. Journalizing and Posting Transactions

- Posting Journal Entries (cont.)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

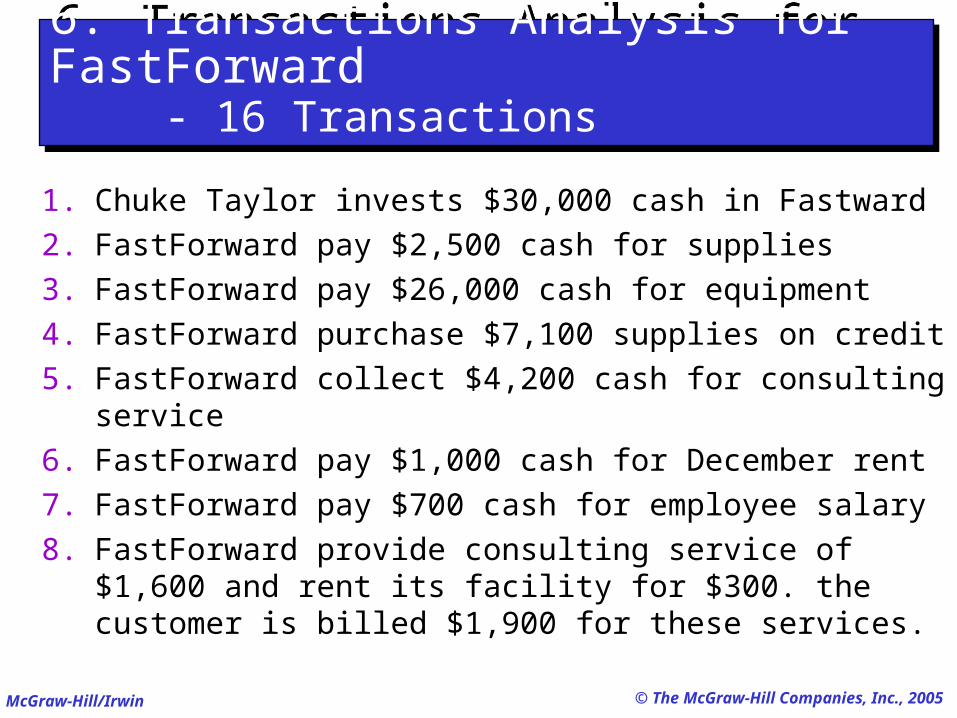

6. Transactions Analysis for FastForward - 16 Transactions6. Transactions Analysis for FastForward - 16 Transactions

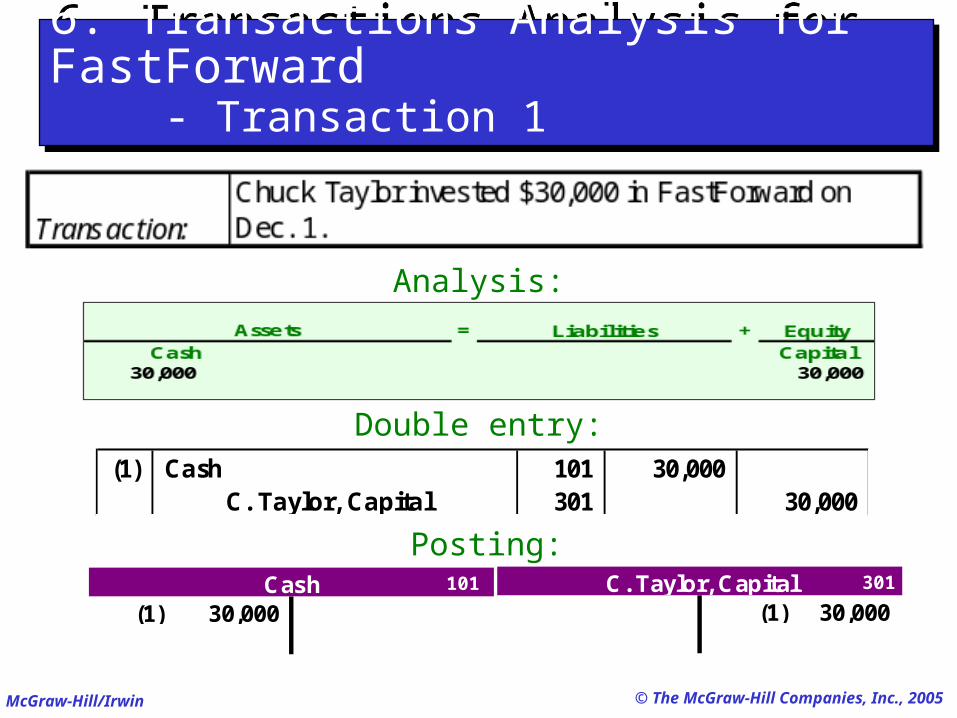

1. Chuke Taylor invests $30,000 cash in Fastward

2. FastForward pay $2,500 cash for supplies

3. FastForward pay $26,000 cash for equipment

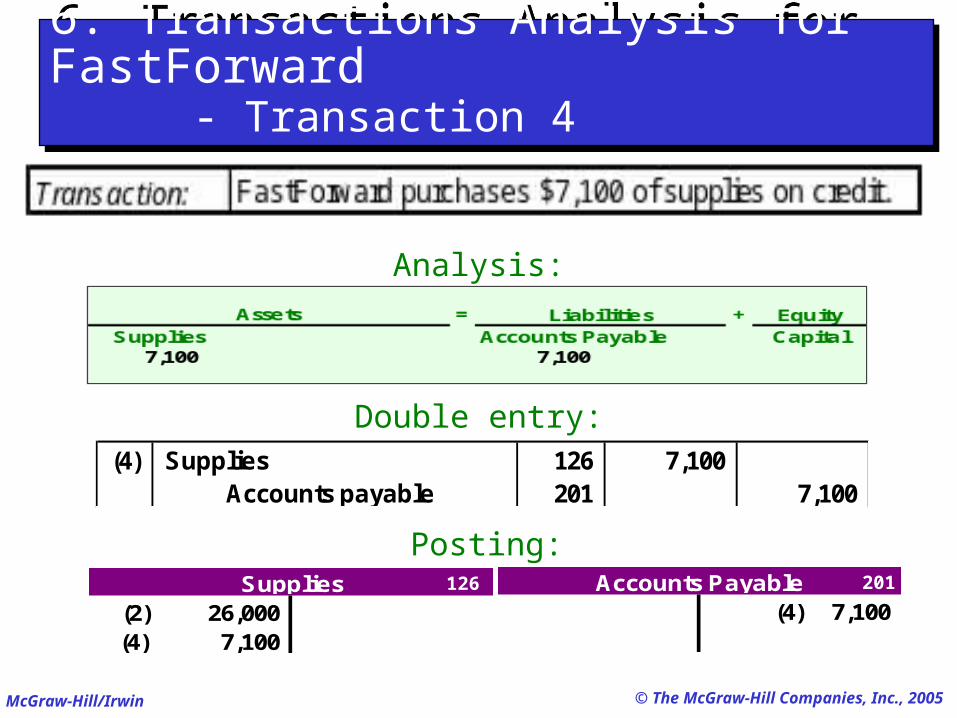

4. FastForward purchase $7,100 supplies on credit

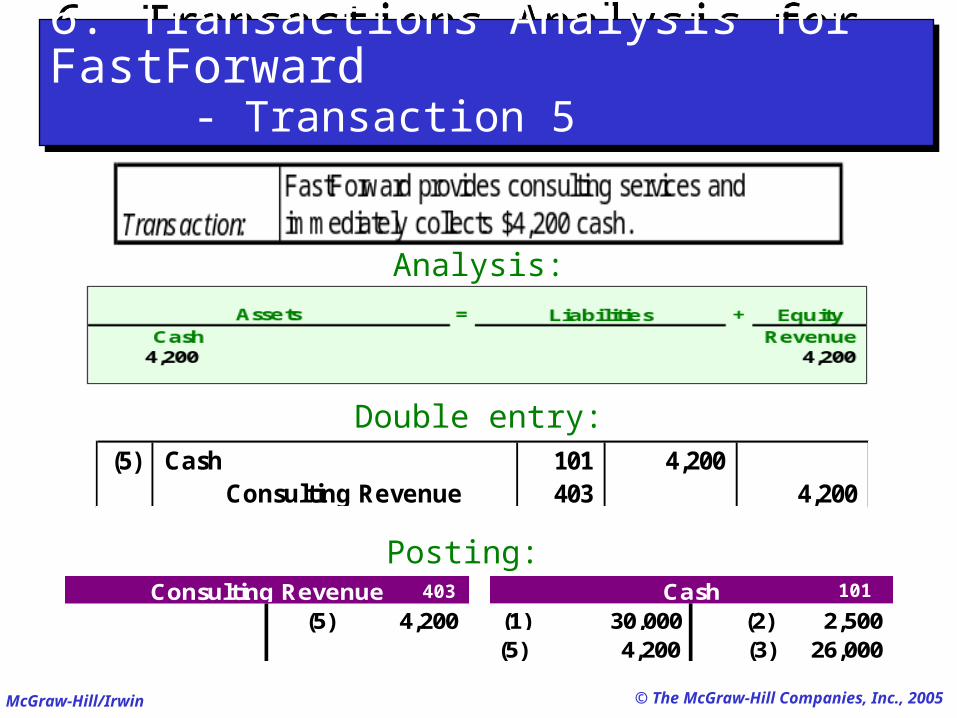

5. FastForward collect $4,200 cash for consulting service

6. FastForward pay $1,000 cash for December rent

7. FastForward pay $700 cash for employee salary

8. FastForward provide consulting service of $1,600 and rent its facility for $300. the customer is billed $1,900 for these services.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

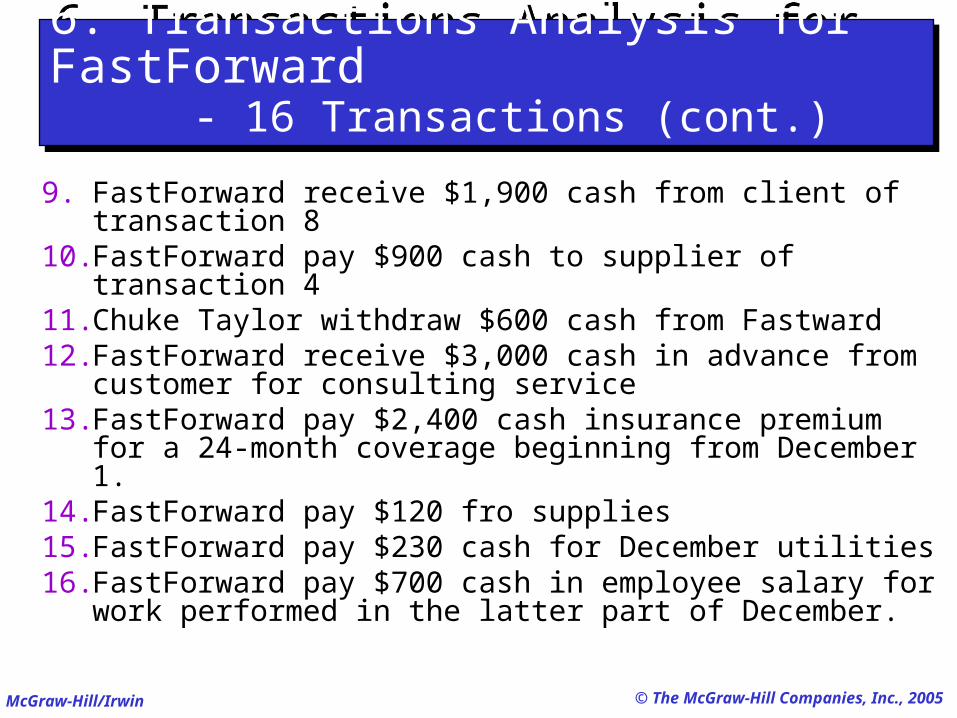

6. Transactions Analysis for FastForward - 16 Transactions (cont.)6. Transactions Analysis for FastForward - 16 Transactions (cont.)

9. FastForward receive $1,900 cash from client of transaction 8

10. FastForward pay $900 cash to supplier of transaction 4 11. Chuke Taylor withdraw $600 cash from Fastward 12. FastForward receive $3,000 cash in advance from

customer for consulting service13. FastForward pay $2,400 cash insurance premium for a

24-month coverage beginning from December 1.14. FastForward pay $120 fro supplies15. FastForward pay $230 cash for December utilities16. FastForward pay $700 cash in employee salary for

work performed in the latter part of December.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 16. Transactions Analysis for FastForward - Transaction 1

Analysis:

(1) Cash 101 30,000 C. Taylor, Capital 301 30,000

Double entry:

(1) 30,000Cash 101

(1) 30,000C. Taylor, Capital 301

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 26. Transactions Analysis for FastForward - Transaction 2

Analysis:

(2) Supplies 126 2,500 Cash 101 2,500

Double entry:

(2) 2,500Supplies 126

(1) 30,000 (2) 2,500Cash 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 36. Transactions Analysis for FastForward - Transaction 3

Analysis:

(3) Equipment 167 26,000 Cash 101 26,000

Double entry:

(1) 30,000 (2) 2,500(3) 26,000

Cash(3) 26,000

Equipment 167 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 46. Transactions Analysis for FastForward - Transaction 4

Analysis:

(4) Supplies 126 7,100 Accounts payable 201 7,100

Double entry:

(2) 26,000(4) 7,100

Supplies 126

(4) 7,100Accounts Payable 201

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 56. Transactions Analysis for FastForward - Transaction 5

Analysis:

(5) Cash 101 4,200 Consulting Revenue 403 4,200

Double entry:

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000

Cash(5) 4,200

Consulting Revenue 403 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 66. Transactions Analysis for FastForward - Transaction 6

Analysis:

(6) Rent expense 640 1,000 Cash 101 1,000

Double entry:

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000

(6) 1,000

Cash(6) 1,000

Rent Expense 640 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 76. Transactions Analysis for FastForward - Transaction 7

Analysis:

(7) Salary Expense 622 700 Cash 101 700

Double entry:

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000

(6) 1,000(7) 700

Cash(7) 700

Rent Expense 622 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

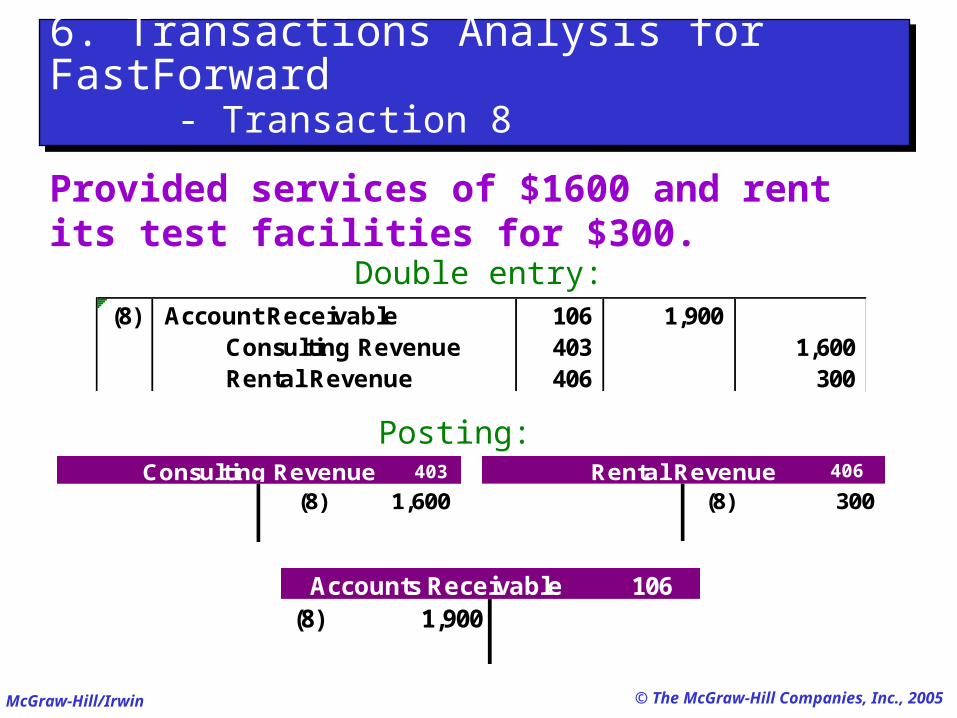

6. Transactions Analysis for FastForward - Transaction 86. Transactions Analysis for FastForward - Transaction 8

Provided services of $1600 and rent its test facilities for $300. the customer is billed

$1,900 for these services.

The accounts involved are:

(1) Accounts Receivable (asset)

(2) Consulting Revenue (equity)

(3) Rental Revenue (equity)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 86. Transactions Analysis for FastForward - Transaction 8

(8) Account Receivable 106 1,900 Consulting Revenue 403 1,600 Rental Revenue 406 300

Double entry:

(8) 300Rental Revenue

(8) 1,600Consulting Revenue 403 406

Posting:

(8) 1,900Accounts Receivable 106

Provided services of $1600 and rent its test facilities for $300.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

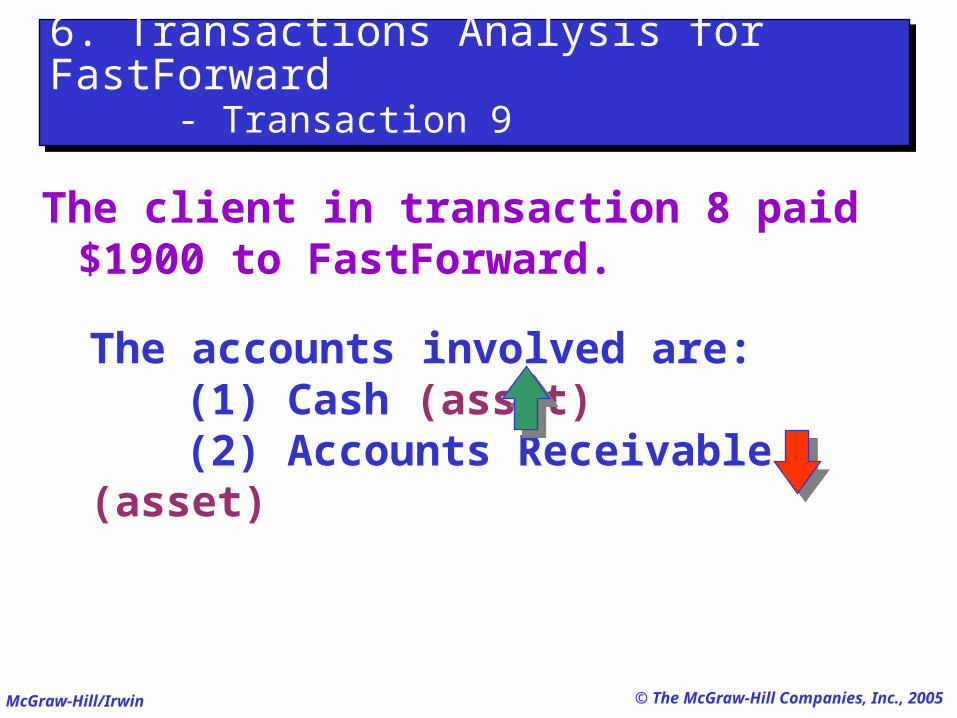

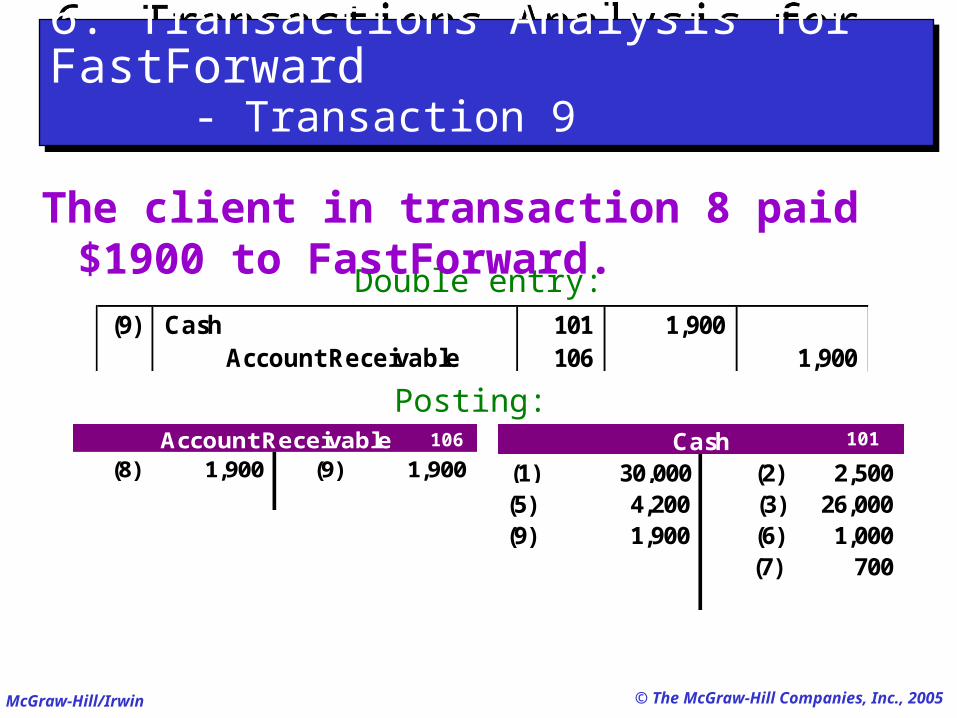

6. Transactions Analysis for FastForward - Transaction 96. Transactions Analysis for FastForward - Transaction 9

The client in transaction 8 paid $1900 to FastForward.

The accounts involved are:(1) Cash (asset) (2) Accounts Receivable (asset)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 96. Transactions Analysis for FastForward - Transaction 9

(9) Cash 101 1,900 Account Receivable 106 1,900

Double entry:

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000

(7) 700

Cash(8) 1,900 (9) 1,900

Account Receivable 106 101

Posting:

The client in transaction 8 paid $1900 to FastForward.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

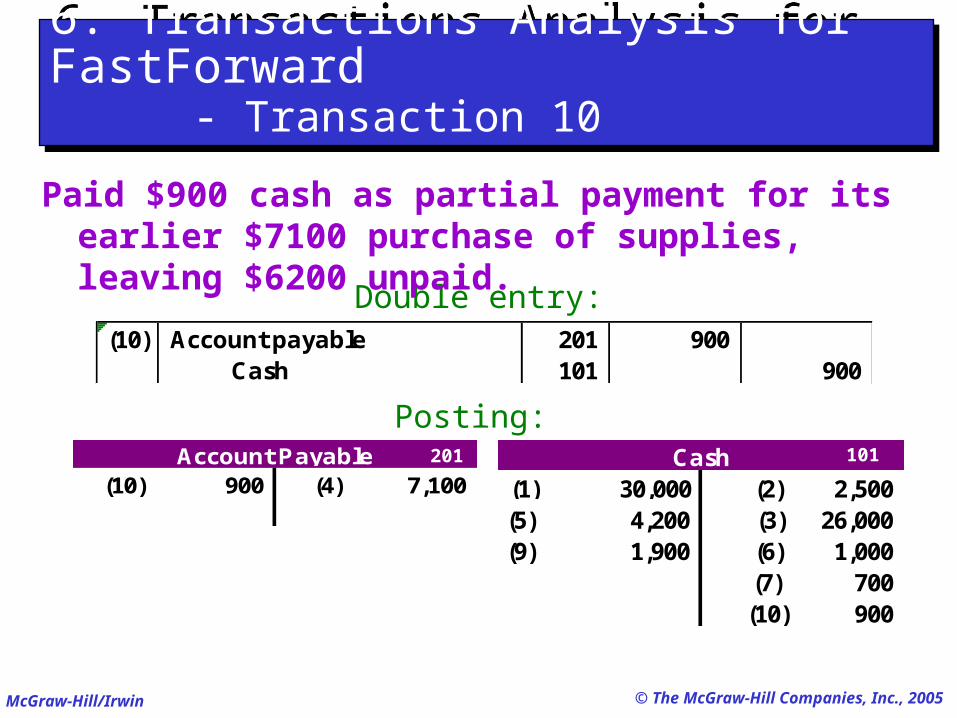

6. Transactions Analysis for FastForward - Transaction 106. Transactions Analysis for FastForward - Transaction 10

Paid $900 cash as partial payment for its earlier $7100 purchase of supplies,

leaving $6200 unpaid.

The accounts involved are:(1) Cash (asset) (2) Accounts Payable (liability)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 106. Transactions Analysis for FastForward - Transaction 10

(10) Account payable 201 900 Cash 101 900

Double entry:

Paid $900 cash as partial payment for its earlier $7100 purchase of supplies, leaving $6200 unpaid.

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000

(7) 700(10) 900

Cash(10) 900 (4) 7,100

Account Payable 201 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

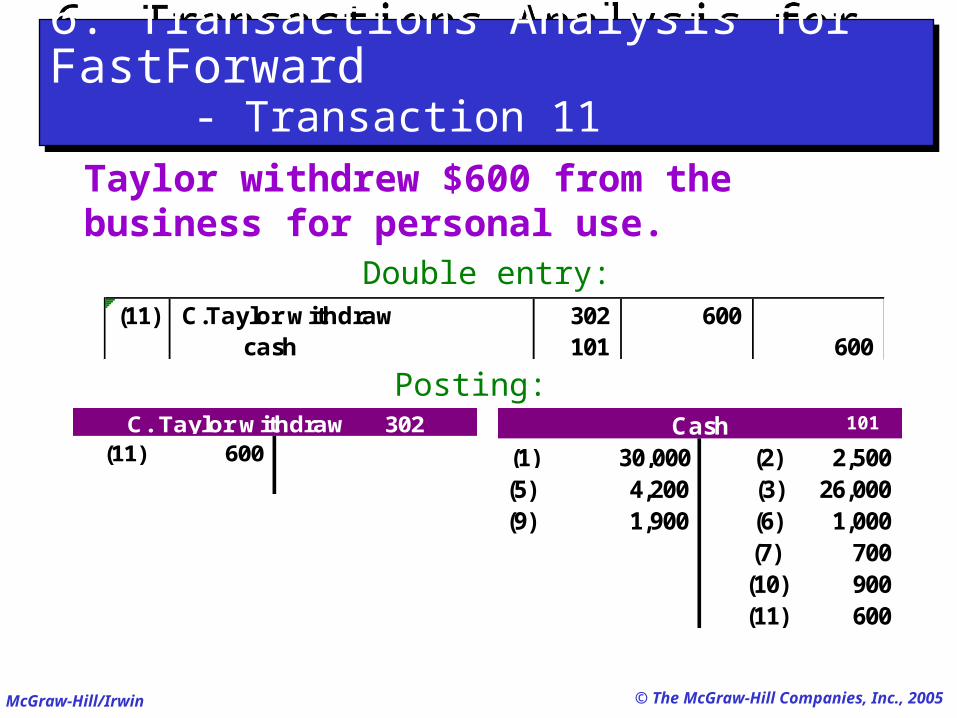

The accounts involved are:

(1) Cash (asset)

(2) Taylor, Withdrawals (equity)

6. Transactions Analysis for FastForward - Transaction 116. Transactions Analysis for FastForward - Transaction 11

Taylor withdrew $600 from the business for personal use.

Remember that the balance in the Taylor, Withdraws account actually increases.

But, equity actually decreases because withdraws reduce equity.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 116. Transactions Analysis for FastForward - Transaction 11

(11) C.Taylor withdraw 302 600 cash 101 600

Double entry:

Taylor withdrew $600 from the business for personal use.

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000

(7) 700(10) 900(11) 600

Cash(11) 600

C. Taylor withdraw 302 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

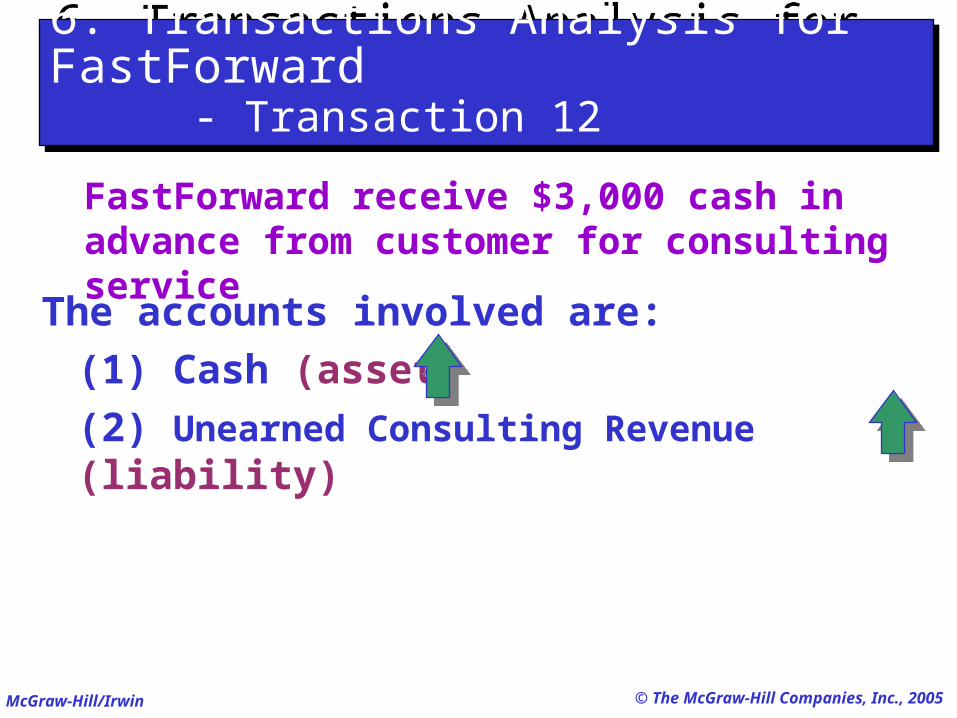

The accounts involved are:

(1) Cash (asset)

(2) Unearned Consulting Revenue (liability)

6. Transactions Analysis for FastForward - Transaction 126. Transactions Analysis for FastForward - Transaction 12

FastForward receive $3,000 cash in advance from customer for consulting service

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 126. Transactions Analysis for FastForward - Transaction 12

(12) Cash 101 3,000 Unearned Consult. Revenue 236 3,000

Double entry:

FastForward receive $3,000 cash in advance from customer for consulting service

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000(12) 3,000 (7) 700

(10) 900(11) 600

Cash(12) 3,000

Unearned Consult. Revenue 236 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

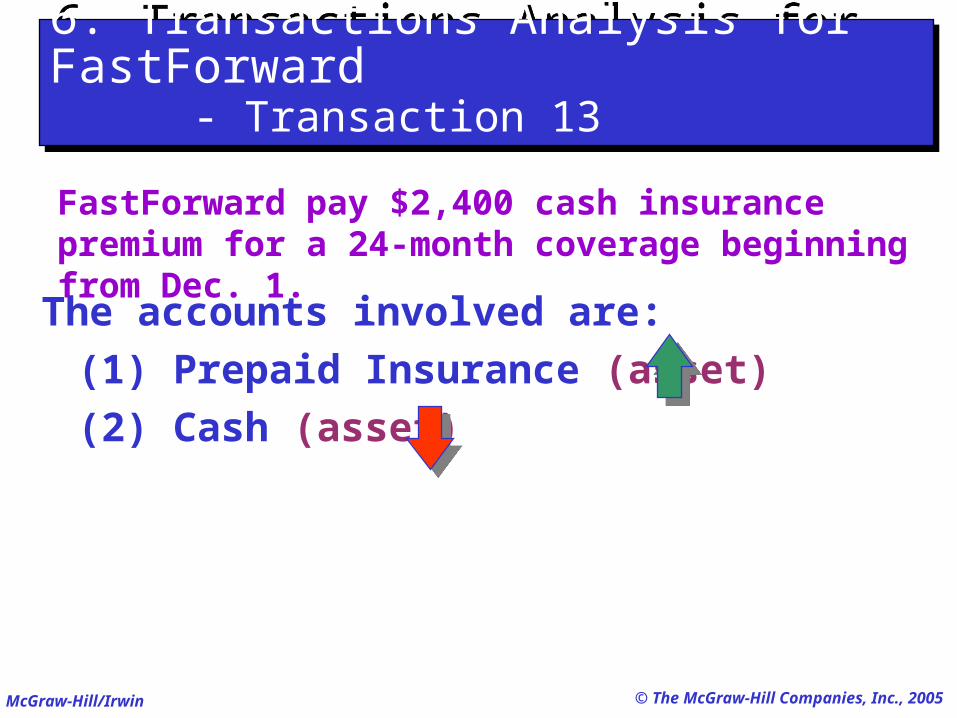

The accounts involved are:

(1) Prepaid Insurance (asset)

(2) Cash (asset)

6. Transactions Analysis for FastForward - Transaction 136. Transactions Analysis for FastForward - Transaction 13

FastForward pay $2,400 cash insurance premium for a 24-month coverage beginning from Dec. 1.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 136. Transactions Analysis for FastForward - Transaction 13

(13) Prpaid Insurance 128 2,400 Cash 101 2,400

Double entry:

FastForward pay $2,400 cash insurance premium for a 24-month coverage beginning from Dec. 1.

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000(12) 3,000 (7) 700

(10) 900(11) 600(13) 2,400

Cash(13) 2,400

Prepaid Insurance 128 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

FastForward pay $120 cash for supplies

The accounts involved are:

(1) Supplies (asset)

(2) Cash (asset)

6. Transactions Analysis for FastForward - Transaction 146. Transactions Analysis for FastForward - Transaction 14

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 146. Transactions Analysis for FastForward - Transaction 14

(14) Supplies 126 120 Cash 101 120

Double entry:

FastForward pay $120 cash for supplies

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000(12) 3,000 (7) 700

(10) 900(11) 600(13) 2,400(14) 120

Cash(14) 120

Supplies 126 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

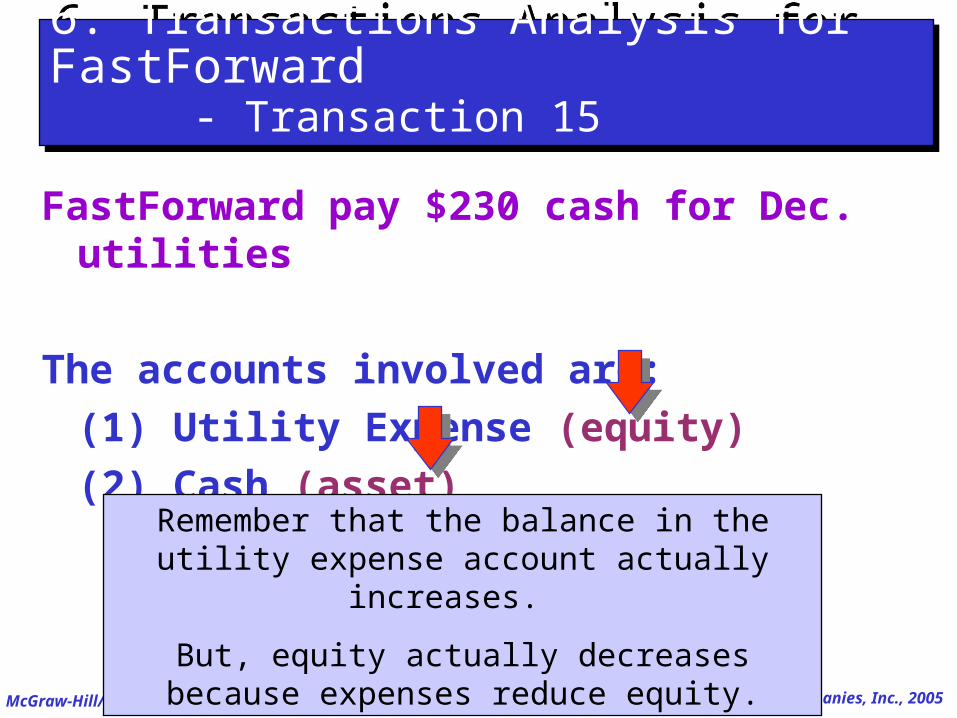

FastForward pay $230 cash for Dec. utilities

The accounts involved are:

(1) Utility Expense (equity)

(2) Cash (asset)

6. Transactions Analysis for FastForward - Transaction 156. Transactions Analysis for FastForward - Transaction 15

Remember that the balance in the utility expense account actually increases.

But, equity actually decreases because expenses reduce equity.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 156. Transactions Analysis for FastForward - Transaction 15

(15) Utility Expense 690 230 Cash 101 230

Double entry:

FastForward pay $230 cash for Dec. utilities

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000(12) 3,000 (7) 700

(10) 900(11) 600(13) 2,400(14) 120(15) 230

Cash(15) 230

Utility Expense 690 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

FastForward pay $700 cash in employee salary for work performed in the latter part of

December.

The accounts involved are:

(1) Salary Expense (equity)

(2) Cash (asset)

6. Transactions Analysis for FastForward - Transaction 166. Transactions Analysis for FastForward - Transaction 16

Remember that the balance in the salaries expense account actually increases.

But, equity actually decreases because expenses reduce equity.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6. Transactions Analysis for FastForward - Transaction 166. Transactions Analysis for FastForward - Transaction 16

(16) Salary Expense 622 700 Cash 101 700

Double entry:

FastForward pay $700 cash in employee salary for work performed in the latter part of December.

(1) 30,000 (2) 2,500(5) 4,200 (3) 26,000(9) 1,900 (6) 1,000(12) 3,000 (7) 700

(10) 900(11) 600(13) 2,400(14) 120(15) 230(16) 700

Cash(16) 700

Salary Expense 622 101

Posting:

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

7. Trial Balance7. Trial Balance

Trial Balance A list of accounts and their balance at a point of time

3 steps to prepare Trial Balance list each account and balance of account compute total debits and credit balance verify: total debits = total credits

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

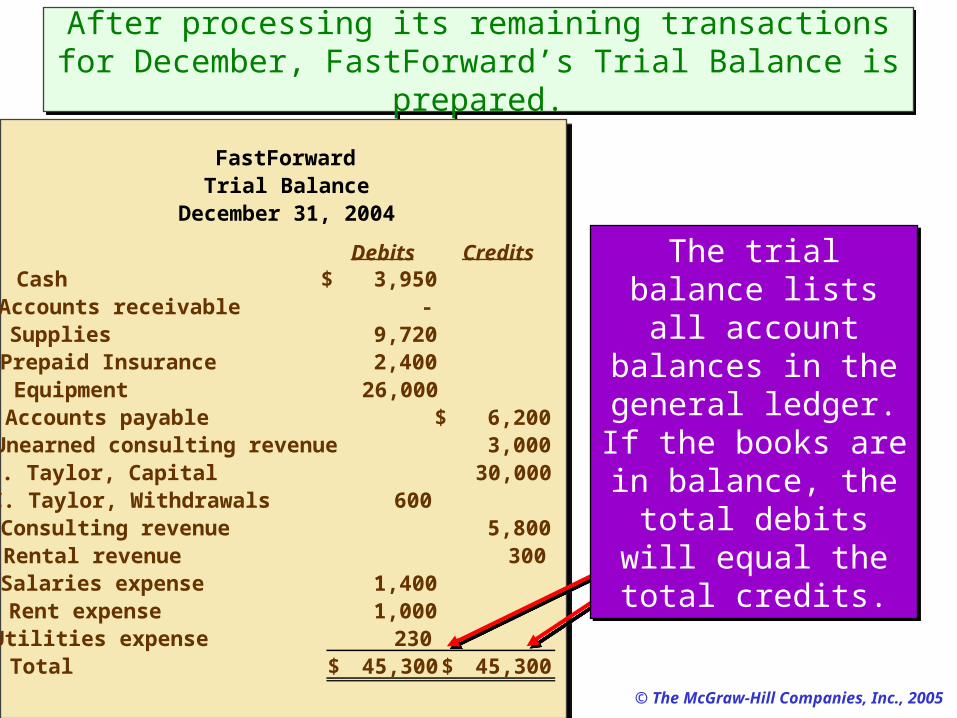

After processing its remaining transactions for December, FastForward’s Trial Balance is prepared.

After processing its remaining transactions for December, FastForward’s Trial Balance is prepared.

Debits CreditsCash 3,950$ Accounts receivable - Supplies 9,720 Prepaid Insurance 2,400 Equipment 26,000 Accounts payable 6,200$ Unearned consulting revenue 3,000 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 600 Consulting revenue 5,800 Rental revenue 300 Salaries expense 1,400 Rent expense 1,000 Utilities expense 230 Total 45,300$ 45,300$

FastForwardTrial Balance

December 31, 2004

The trial balance lists all account balances in the general ledger.

If the books are in balance, the total

debits will equal the total credits.

The trial balance lists all account balances in the general ledger.

If the books are in balance, the total

debits will equal the total credits.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Searching for and Correcting ErrorsSearching for and Correcting Errors

If the trial balance does not balance, the error(s) must be found and corrected.

Make sure the trial balance columns are correctly added.Make sure the trial balance columns are correctly added.

Make sure account balances are correctly entered into the ledger.

Make sure account balances are correctly entered into the ledger.

See if debit or credit accounts are mistakenly placed on the trial balance.

See if debit or credit accounts are mistakenly placed on the trial balance.

Recompute each account balance in the ledger.Recompute each account balance in the ledger.

Verify that each journal entry is posted correctly.Verify that each journal entry is posted correctly.

Verify that each original journal entry has equal debits and credits.

Verify that each original journal entry has equal debits and credits.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

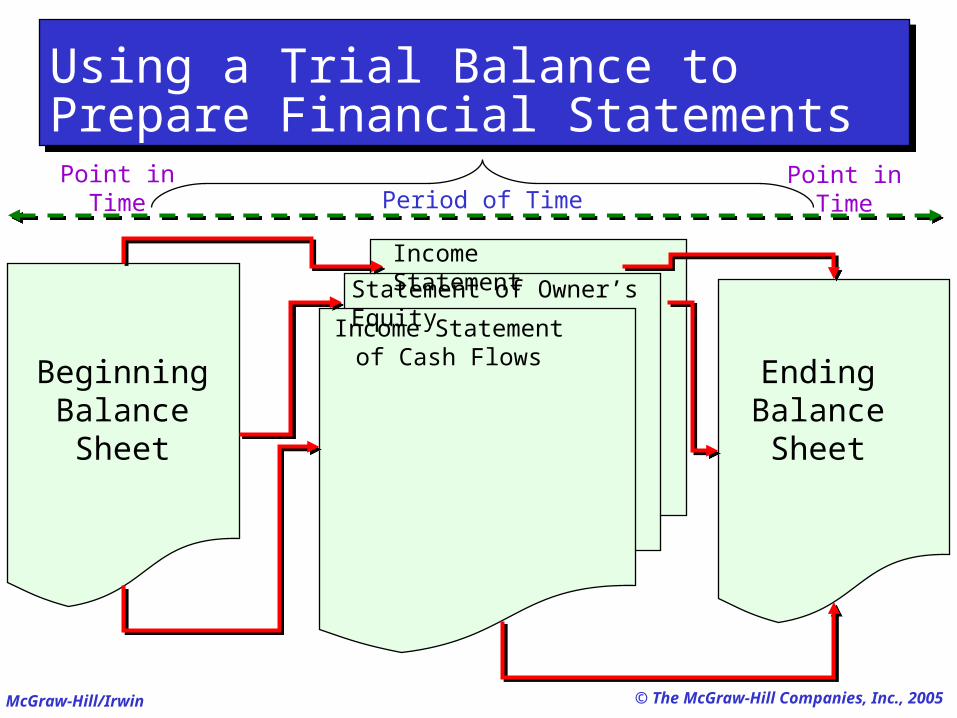

Using a Trial Balance to Prepare Financial StatementsUsing a Trial Balance to Prepare Financial Statements

Income Statement of Cash Flows

Income Statement

Statement of Owner’s Equity

Beginning Balance Sheet

Ending Balance Sheet

Period of TimePoint inTime

Point inTime

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

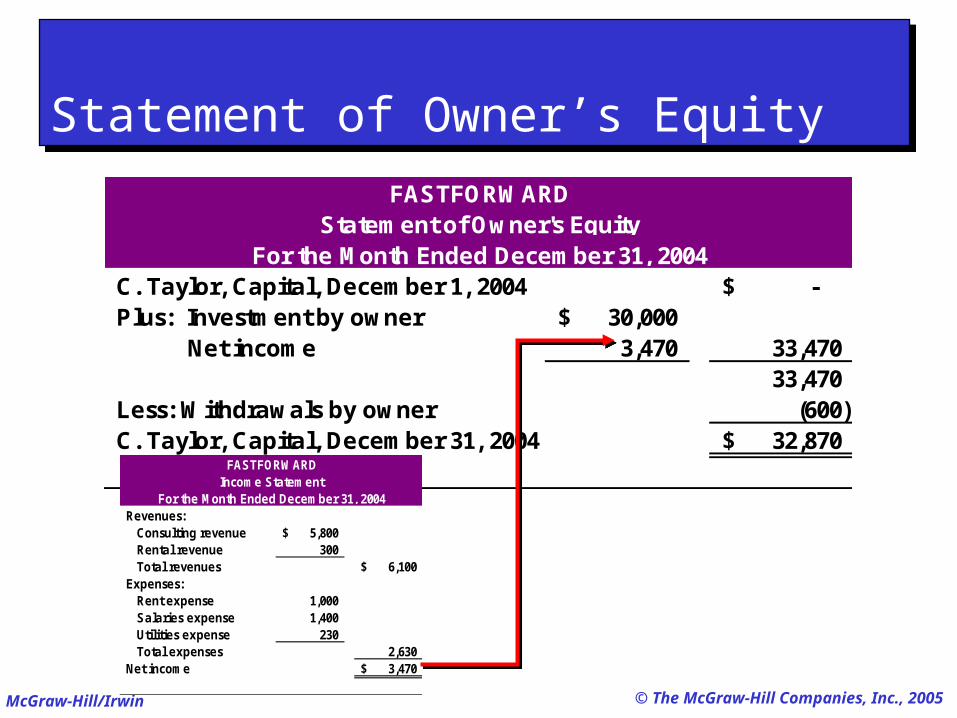

Income StatementIncome Statement

Revenues: Consulting revenue 5,800$ Rental revenue 300 Total revenues 6,100$ Expenses: Rent expense 1,000 Salaries expense 1,400 Utilities expense 230 Total expenses 2,630 Net income 3,470$

FASTFORWARDIncome Statement

For the Month Ended December 31, 2004

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Statement of Owner’s EquityStatement of Owner’s Equity

C. Taylor, Capital, December 1, 2004 -$ Plus: Investment by owner 30,000$ Net income 3,470 33,470

33,470 Less: Withdrawals by owner (600) C. Taylor, Capital, December 31, 2004 32,870$

FASTFORWARDStatement of Owner's Equity

For the Month Ended December 31, 2004

Revenues: Consulting revenue 5,800$ Rental revenue 300 Total revenues 6,100$ Expenses: Rent expense 1,000 Salaries expense 1,400 Utilities expense 230 Total expenses 2,630 Net income 3,470$

FASTFORWARDIncome Statement

For the Month Ended December 31, 2004

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

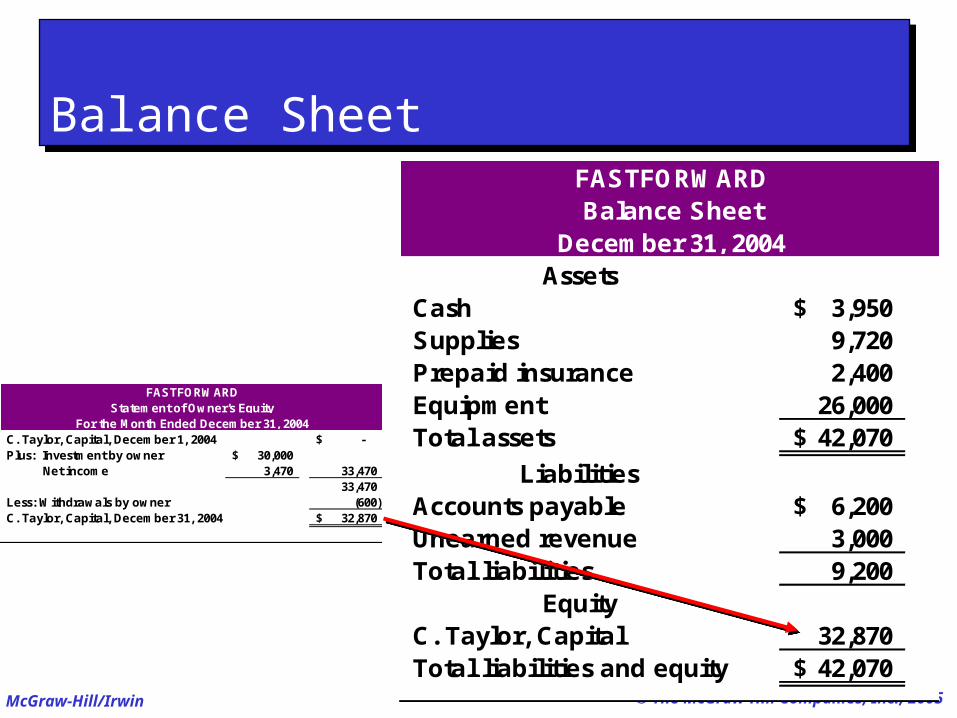

Balance SheetBalance Sheet

AssetsCash 3,950$ Supplies 9,720 Prepaid insurance 2,400 Equipment 26,000 Total assets 42,070$

LiabilitiesAccounts payable 6,200$ Unearned revenue 3,000 Total liabilities 9,200

EquityC. Taylor, Capital 32,870 Total liabilities and equity 42,070$

FASTFORWARDBalance Sheet

December 31, 2004

C. Taylor, Capital, December 1, 2004 -$ Plus: Investment by owner 30,000$ Net income 3,470 33,470

33,470 Less: Withdrawals by owner (600) C. Taylor, Capital, December 31, 2004 32,870$

FASTFORWARDStatement of Owner's Equity

For the Month Ended December 31, 2004

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

End of Chapter 2End of Chapter 2

![Chapter 02 Analyzing and Recording Transactionstestbankonly.com/pdf/Financial-and-Managerial... · Analyzing and Recording Transactions True / False Questions [Question] 1. Accounting](https://static.fdocuments.us/doc/165x107/5f09491b7e708231d4261881/chapter-02-analyzing-and-recording-tran-analyzing-and-recording-transactions-true.jpg)