Analyst Conference FY 2013/2014 Bertrandt AG · Electronics competence center in Tappenbeck Testing...

32

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 0 Analyst Conference FY 2013/2014 Bertrandt AG Dietmar Bichler, CEO Markus Ruf, CFO Frankfurt am Main, December 11 th , 2014

-

Upload

truonghanh -

Category

Documents

-

view

214 -

download

0

Transcript of Analyst Conference FY 2013/2014 Bertrandt AG · Electronics competence center in Tappenbeck Testing...

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 0

Analyst Conference FY 2013/2014

Bertrandt AG

Dietmar Bichler, CEO

Markus Ruf, CFO

Frankfurt am Main, December 11th, 2014

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 1

Welcome to the analyst conference 2014 of Bertrandt AG

CHANGE.

KNOWLEDGE.

GROWTH.

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 2

Positive development of the most important business ratios (1/2)

Revenues*(EUR million)

Operating *(EUR million)

Earnings after income tax*(EUR million)

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 3

Capital spending*(EUR million)

Employees*

Positive development of the most important business ratios (2/2)

Dividend per share**(EUR)

*Financial indicators refer to the Group | **Dividend proposed by the Management and the Supervisory Board

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 4

Agenda

1. Fiscal year 2013/2014 – General framework

2. Fiscal year 2013/2014 – Figures

3. Fiscal year 2014/2015 – Outlook

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 5

Automotive industry with a successful year 2013/2014

Global new vehicle sales rose again in 2013

World market is growing by 5% to 72.2 million units

German automotive industry increases sales in

2013 by approx. one percent to EUR 361.6 billion

Higher spending on R&D,

outsourcing volume expanded again

Persistent technical trends

Environment-friendliness

Powertrain & Lightweight

Safety

Driver assistance systems & Connectivity

Variety of models & variants

Module-/Plattformstrategies

Source: VDA

Automotive

73%68%

27%

32%

0

5

10

15

20

25

30

35

2012 2013

22

27

Internal

R&D spending

Outsourced

R&D spending

R&D spending of the

German automotive industry(EUR billion)

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 6

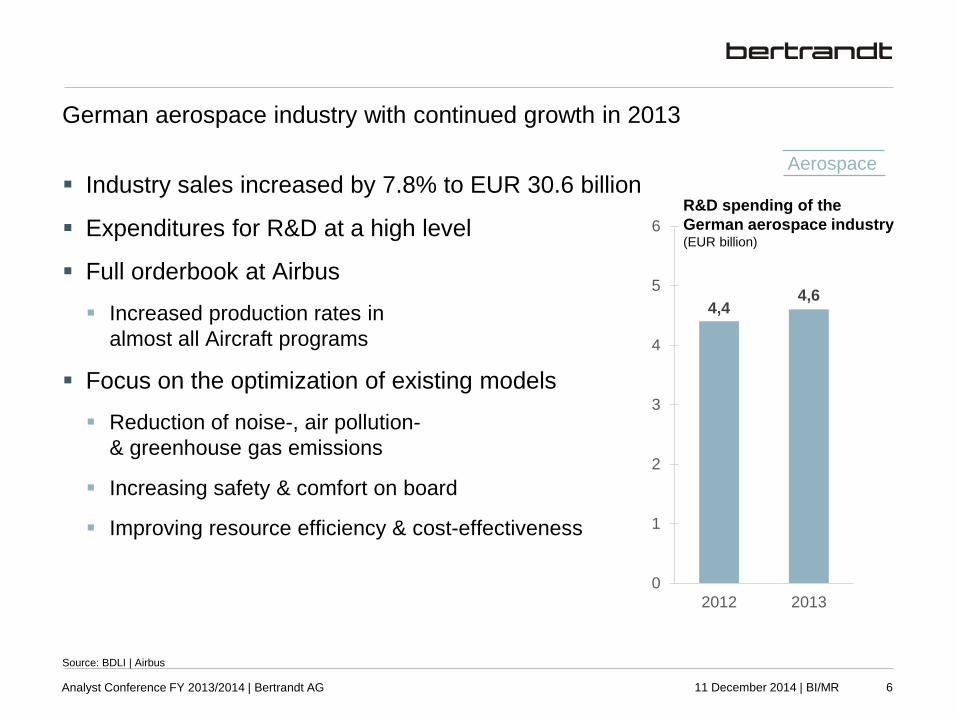

German aerospace industry with continued growth in 2013

Industry sales increased by 7.8% to EUR 30.6 billion

Expenditures for R&D at a high level

Full orderbook at Airbus

Increased production rates in

almost all Aircraft programs

Focus on the optimization of existing models

Reduction of noise-, air pollution-

& greenhouse gas emissions

Increasing safety & comfort on board

Improving resource efficiency & cost-effectiveness

Aerospace

Source: BDLI | Airbus

4,44,6

0

1

2

3

4

5

6

2012 2013

R&D spending of the

German aerospace industry(EUR billion)

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 7

Challenging conditions for technological key sectors

Development of the German industry

remained largely behind expectations

Slugging orders because of the

global economic slowdown

Effects of political & economic risks,

especially due to the Ukraine crisis

Delay in implementing the

turnaround in energy policy

Exception medical technology

Since 2009 stable sales growth, in 2013 by 2.2%

Strong market position of German medical

technology products in the world market

Source: VDMA | ZVEI | Spectaris

Industry

206,9 205,8

0

100

200

300

2012 2013

Sales of the German

mechanical engineering sector(EUR billion)

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 8

Bertrandt improved market position in FY 2013/2014 successfully

Revenues & operating profit rose

Increasing volume development

Trend to larger working packages

Intact market trends

Stable financial situation

Enables sustainable investments

as a basis for future growth

Success factors

Entire development process

Decentralized structure

Customized and consistent services

Extensive interface competence

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 9

Agenda

1. Fiscal year 2013/2014 – General framework

2. Fiscal year 2013/2014 – Figures

3. Fiscal year 2014/2015 – Outlook

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 10

Revenues increased repeatedly

*Financial indicators refer to the Group

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 11

Operating profit stays on a high level

EBIT-

Margin*10.2% 10.5% 10.6% 10.4% 10.2%

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 12

Revenues rose in all segments

9.5% 9.2% 11.8% 12.0%EBIT-

Margin*11.5%11.4%

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Physical Engineering*(EUR million)

Digital Engineering*(EUR million)

Electrics/Electronic*(EUR million)

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 13

Expenses rose due to the increased business volume

Expenditure

ratio* 8.2%8.0% 71.7%71.6% 2.5%2.5%

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Material expenses* (EUR million)

Personnel expenses* (EUR million)

Depreciation* (EUR million)

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 14

Earnings after income tax improved again

Earnings

per share*3.11 EUR 4.18 EUR 5.14 EUR 5.69 EUR 6.19 EUR

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 15

Equity increased further by consistent reinvestment

Equity ratio* 56.4% 56.3% 56.3% 59.4%58.5%

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 16

Net finance income positive

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 17

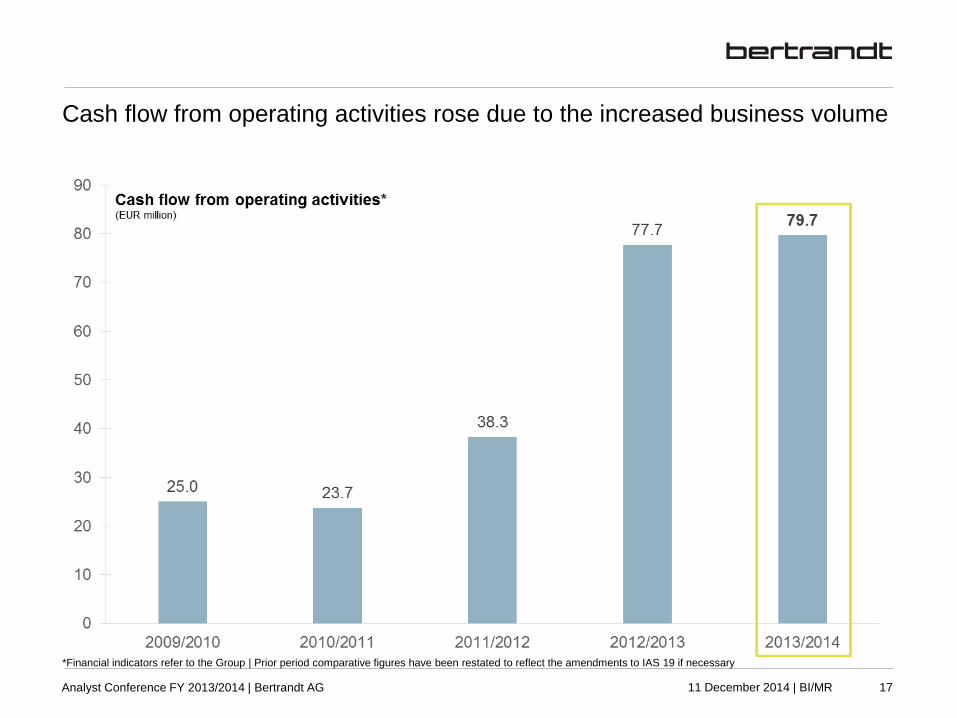

Cash flow from operating activities rose due to the increased business volume

*Financial indicators refer to the Group | Prior period comparative figures have been restated to reflect the amendments to IAS 19 if necessary

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 18

Forward-looking investments will ensure further growth

*Financial indicators refer to the Group

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 19

Examples for investments in FY 2013/2014

Technical testing centre in Mönsheim

Test systems for environmental simulation,

e-mobility & powertrain components

Electronics competence center in Tappenbeck

Testing facilities for interactive electronics, electrical

systems, system integration, electric powertrain &

infotainment

Acoustics center in Ingolstadt

Acoustic roller dynamometer for measuring noise,

vibration & harshness as well as sound design of

e-mobility

Safety competence center in Munich

E-liner-system for tests of parts & modules

concerning acceleration/deceleration

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 20

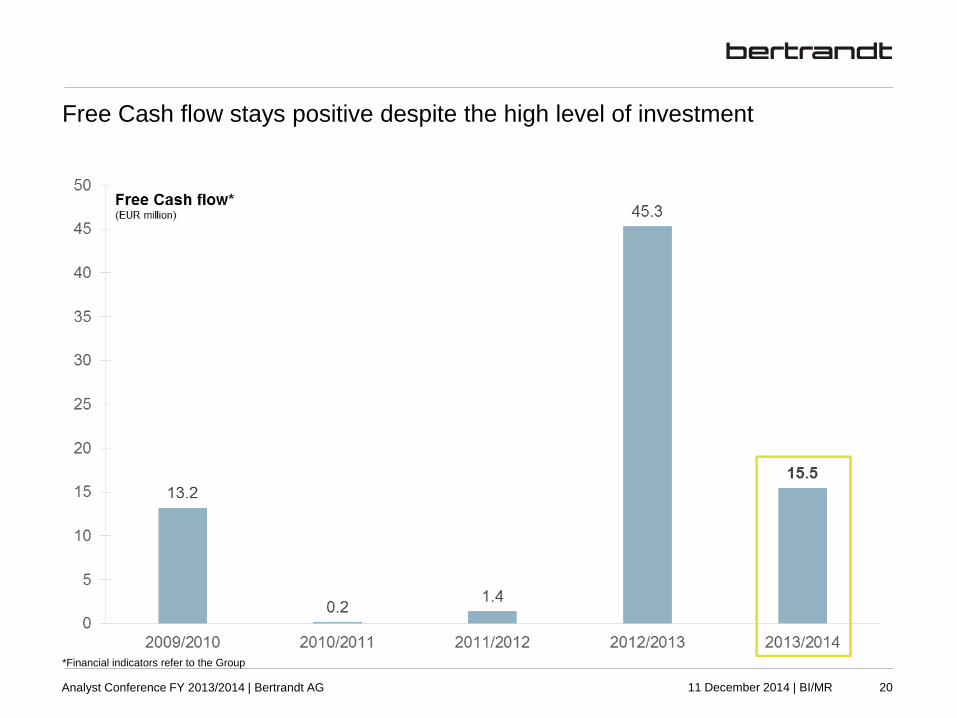

Free Cash flow stays positive despite the high level of investment

*Financial indicators refer to the Group

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 21

Number of employees at all-time high

*Financial indicators refer to the Group

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 22

Sustainable dividend policy will be continued

*Dividend proposed by the Management and the Supervisory Board

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 23

Agenda

1. Fiscal year 2013/2014 – General framework

2. Fiscal year 2013/2014 – Figures

3. Fiscal year 2014/2015 – Outlook

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 24

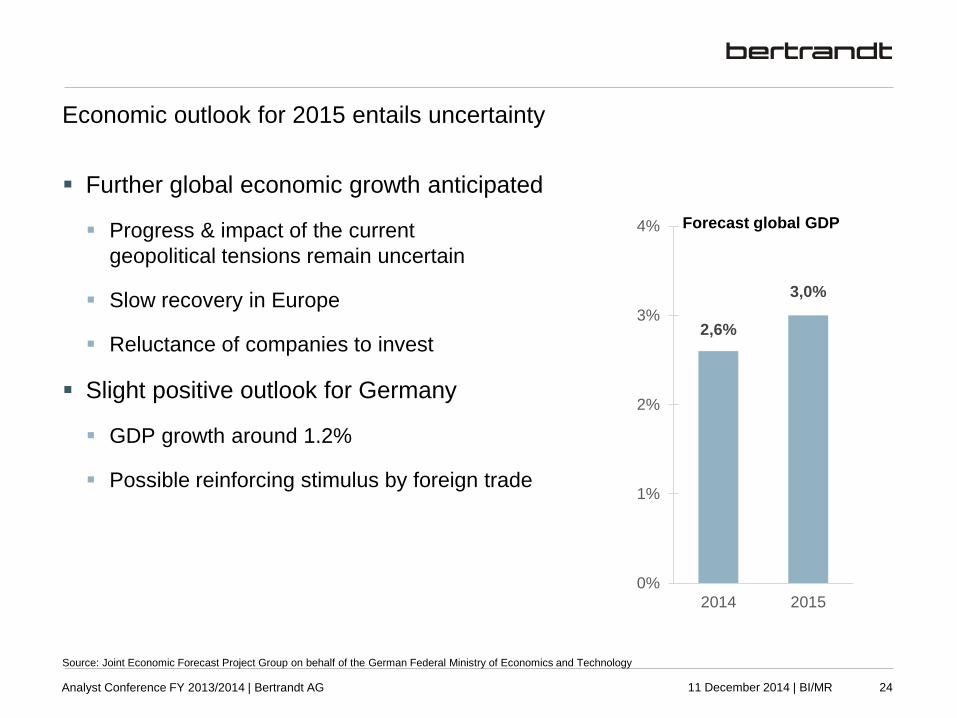

Economic outlook for 2015 entails uncertainty

Further global economic growth anticipated

Progress & impact of the current

geopolitical tensions remain uncertain

Slow recovery in Europe

Reluctance of companies to invest

Slight positive outlook for Germany

GDP growth around 1.2%

Possible reinforcing stimulus by foreign trade

Source: Joint Economic Forecast Project Group on behalf of the German Federal Ministry of Economics and Technology

2,6%

3,0%

0%

1%

2%

3%

4%

2014 2015

Forecast global GDP

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 25

Core business automotive industry with potential for further growth

Global new vehicle sales should continue to rise

2015 increase by 2% to 76.4 million units

Automotive industry continues

high spending on R&D

Achieving the legal CO2 regulations requires

technologically sophisticated solutions

Outsourcing in Europa shall rise by 19% until 2020

Consolidation amongst engineering

service providers expectetd

Trend towards larger working packages –

higher levels of complexity & responsibility

Source: Roland Berger Strategy Consultants | VDA | Berylls

6,2

7,4

0

2

4

6

8

10

2014 2020

European market for engineering

services in the automotive industry(EUR billion)

Automotive

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 26

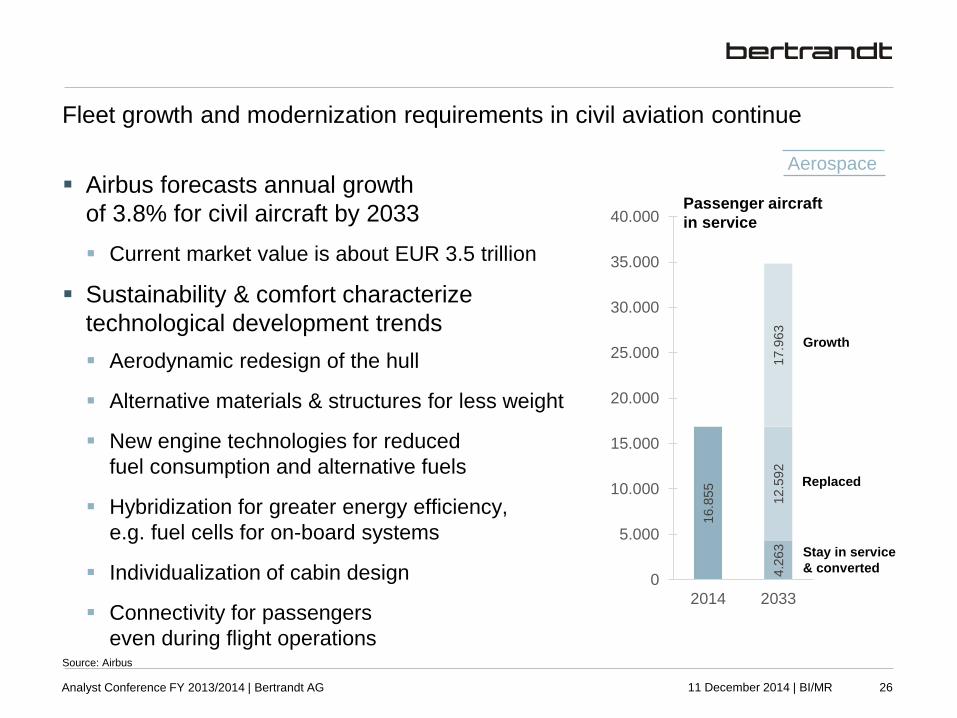

Fleet growth and modernization requirements in civil aviation continue

Source: Airbus

Airbus forecasts annual growth

of 3.8% for civil aircraft by 2033

Current market value is about EUR 3.5 trillion

Sustainability & comfort characterize

technological development trends

Aerodynamic redesign of the hull

Alternative materials & structures for less weight

New engine technologies for reduced

fuel consumption and alternative fuels

Hybridization for greater energy efficiency,

e.g. fuel cells for on-board systems

Individualization of cabin design

Connectivity for passengers

even during flight operations

16.8

55

4.2

63

12.5

92

17.9

63

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

2014 2033

Passenger aircraft

in service

Replaced

Stay in service

& converted

Growth

Aerospace

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 27

Industry 4.0 − Huge potential for value creation waiting to be tapped

Source: The Fraunhofer Institute for Industrial Engineering IAO

Industry

Ambition is the intelligent networking of products

& processes in the technological value added

Allows to generate additional benefit

by more efficient or new processes

For the six key industries in Germany an

additional value creation of EUR 70 billion

is expected until 2025

Innovative products, new services and business

models and efficient operational processes

Potential can only be realized through close

interaction between electrical, mechanical & IT

343.3

422.1

0,0

100,0

200,0

300,0

400,0

500,0

600,0

2013 2025

Potential for the gross value

added by Industry 4.0 in the

German industry(EUR billion)

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 28

FY2014/2015 with more business opportunities for Bertrandt

Good cross-sectoral demand for engineering services

Seize the opportunity out of the

new contract award strategy

Ongoing technologival investments on a high level

Continuous focus on current &

prospective customer requirements

Increase corporate value permanently & sustainable

Consolidate & expand market position as a engineering

service provider and technology group

Assuming that

underlying conditions remain on a favourable trend

carmakers keep their R&D spending at a high level

development work continues to be outsourced &

ample qualified personnel is available

Bertrandt expects ongoing growth in its revenues & earnings

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 29

Overview – Our financial calendar in FY 2014/2015

16.02.2015 Report on the 1st quarter FY 2014/2015

18.02.2015 General meeting in Sindelfingen

20.05.2015 10th Capital Market Day in Ehningen &

Report on the 2nd quarter FY 2014/2015

12.08.2015 Report on the 3th quarter FY 2014/2015

10.12.2015 Annual report 2014/2015 &

Annual press and analysts´ conference FY 2014/2015

17.02.2016 General meeting in Sindelfingen

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 30

Thank you for you attention!

Analyst Conference FY 2013/2014 | Bertrandt AG 11 December 2014 | BI/MR 31

Legal notice

This presentation contains inter alia certain foresighted statements about future

developments, which are based on current estimates of management. Such

statements are subjected to certain risks and uncertainties. If one of these factors of

uncertainty or other imponderables should occur or the underlying accepted

statements proved to be incorrent, the actual results could deviate substantially from

or implicitly from the expressed results specified in these statements We have neither

the intetion nor do we accept the obligation of updating foresighted statements

constantly since these proceed exclusively from the circumstances on the day of their

publication.

As far as this presentation refers to statements of third parties, in particular analyst

estimations, the organisation neither adopts these, nor are these rated or commented

thereby in other ways, nor is the claim laid to completeness in this respect.