Analysis of Loan Markets

50

Page | 1 ASUTOSH COLLEGE CALCUTTA UNIVERSITY TITLE OF REPORT “COMPARATIVE STUDY OF SBI CAR LOAN SCHEME VIS-A-VIS OTHERS” Internship Report submitted to SBI in completion of the requirement of Summer Internship at State Bank of India NAME OF THE STUDENT: PROJECT MENTOR: BIKRAMJIT SAHA P.K.HALDER (CHIEF MANAGER) JUNE 24 th 2013 TO AUGUST 30 th 2013

-

Upload

bikramjit-saha -

Category

Documents

-

view

462 -

download

0

Transcript of Analysis of Loan Markets

Page | 1

ASUTOSH COLLEGE

CALCUTTA UNIVERSITY

TITLE OF REPORT

“COMPARATIVE STUDY OF SBI CAR LOAN SCHEME VIS-A-VIS OTHERS”

Internship Report submitted to SBI in completion of the requirement of Summer

Internship at State Bank of India

NAME OF THE STUDENT: PROJECT MENTOR:

BIKRAMJIT SAHA P.K.HALDER (CHIEF

MANAGER)

JUNE 24th 2013 TO AUGUST 30th 2013

Page | 2

Page | 3

ACKNOWLEGEMENT

I am thankful for these free and frank responses to the questionnaire and expressing their views

regarding the scheme. The valuable feedback helped me a lot to be aware with the ground

realities at the operation level to undertake this task. I also extend my thanks to those persons and

employees engaged with this project. I am very much thankful to all those who helped me to

undertake the task by supporting me beyond their boundaries and going beyond their business

ethics also. I would also like to thank my college principal Prof. Saumyabrata Chakrabarty for

their endless support, encouragement and believing in my capabilities. My special thanks to the

team of SBI, Madhyamgram for its whole hearted support & encouragement. And special thanks

to SBI for giving such a good opportunity to the young generation to explore the new fields of

banking experience and encouraging us to develop clear concept about the banking sector and its

processes. A bunch of thanks to the managers who helped me endlessly. And A special thanks to

my mentor cum branch manager Mr. P K Halder for supporting me and his valuable feedbacks

regarding the project undertaken by me.

Thanking you,

Bikramjit Saha

SBI, Madhyamgram Branch

Cell No.: 8961102172

Email: [email protected]

Dated: 30th August, 2013

Page | 4

TABLE OF CONTENTS

SERIAL

NUMBER

DESCRIPTION PAGE

NUMBER

1. LIST OF CHARTS

5

2. LIST OF TABLES 6

3. INTRODUCTION

7-8

A)Brief Profile Of Student

B)Brief Profile Of Project Mentor At

Bank

C)Brief Profile Of Organization

D)Nature Of Project

E)Objectives/Responsibilities

Assigned By Project Mentor

7

7

8

8

8

4. FRAMEWORK OF STUDY 9-16

A)Theoretical framework

B)Specific Objective

C)Scope of study

D)Limitation of study

E)Period of study

9-14

15

15

16

16

5. METHODOLOGY AND ANALYSIS

17-48

A)Methodology

B)Observations

C)Analysis

D)Conclusion

E)Recommendation

17-18

19-38

39-47

48

49

6. BIBLIOGRAPHY

50

Page | 5

LIST OF CHARTS

Number Name of Charts Page No.

Figure 1 Rate of Interest of Different Banks 39

Figure 2 Interest Rates of Used Cars 40

Figure 3 Market Share of Different Banks (Auto Hi-Tech) 41

Figure 4 Market Share of Different Banks (Saini Hyundai) 41

Figure 5 Market Share of Different Banks (Bhandari

Automobiles) 42

Figure 6 Market Share of Different Banks (Topsel Toyota) 42

Figure 7 Market Share of Different Banks (Dhulichand

Motors)

43

Figure 8 Future Tie-up between Dealer and SBI 43

Figure 9 Experience of Different Dealers with the Present

Bankers

44

Figure 10 Amount of Loan Sourced At Bakultala Branch 45

Figure 11 Amount of Loan Sanctioned At Bakultala Branch 46

Figure 12 The Correlation Between Loan Sourced and Loan

Sanctioned At Bakultala Branch

47

Page | 6

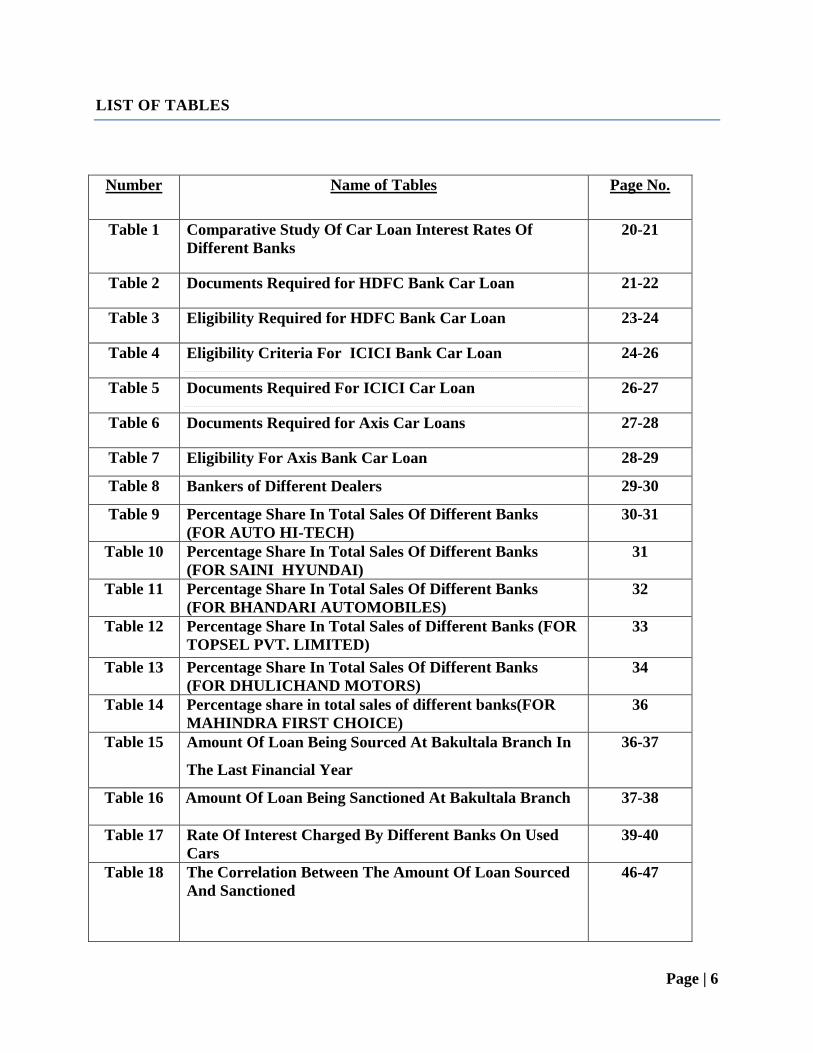

LIST OF TABLES

Number Name of Tables Page No.

Table 1 Comparative Study Of Car Loan Interest Rates Of

Different Banks

20-21

Table 2 Documents Required for HDFC Bank Car Loan 21-22

Table 3 Eligibility Required for HDFC Bank Car Loan 23-24

Table 4 Eligibility Criteria For ICICI Bank Car Loan 24-26

Table 5 Documents Required For ICICI Car Loan 26-27

Table 6 Documents Required for Axis Car Loans 27-28

Table 7 Eligibility For Axis Bank Car Loan 28-29

Table 8 Bankers of Different Dealers 29-30

Table 9 Percentage Share In Total Sales Of Different Banks

(FOR AUTO HI-TECH)

30-31

Table 10 Percentage Share In Total Sales Of Different Banks

(FOR SAINI HYUNDAI)

31

Table 11 Percentage Share In Total Sales Of Different Banks

(FOR BHANDARI AUTOMOBILES)

32

Table 12 Percentage Share In Total Sales of Different Banks (FOR

TOPSEL PVT. LIMITED)

33

Table 13 Percentage Share In Total Sales Of Different Banks

(FOR DHULICHAND MOTORS)

34

Table 14 Percentage share in total sales of different banks(FOR

MAHINDRA FIRST CHOICE)

36

Table 15 Amount Of Loan Being Sourced At Bakultala Branch In

The Last Financial Year

36-37

Table 16 Amount Of Loan Being Sanctioned At Bakultala Branch 37-38

Table 17 Rate Of Interest Charged By Different Banks On Used

Cars

39-40

Table 18 The Correlation Between The Amount Of Loan Sourced

And Sanctioned

46-47

Page | 7

INTRODUCTION

PROFILE OF STUDENT:

I, Bikramjit Saha a B.Sc (Hons) graduate from Asutosh College under Calcutta University have

been a summer intern of SBI, Madhyamgram Branch for 8 weeks. Now I will be pursuing

Masters in Economics from Calcutta University. I passed my Higher Secondary Exam from

Vivekananda Mission School, Joka and Secondary Examination from same. I have scored 60%

in my graduation, 82% in my higher secondary exam and 87% in my secondary exam. I have

successfully completed my summer internship program (June to August'13). It was an excellent

experience to be a part of the summer internship program of a renowned banking institution like

STATE BANK OF INDIA.

PROFILE OF PROJECT MENTOR AT BANK:

My mentor P.K Halder was the Chief Manager of the SBI Madhyamgram branch. He was a very

helpful and kind person. He was always happy to help no matter whenever I approached him.

Being a Manager he has to be very efficient and always on keen concentration on his work but

apart from his busy schedule he was always ready to help me out in every possible way he could.

While doing a project work a mentor plays a very important role, he is the back bone of the

project without whose help it is impossible to perform any kind of work. Since I was new and

had no idea about this, my mentor would help me to understand and explained me every little

thing in details. I was lucky to get a mentor like him, a calm and polite person with eagerness to

help in every step and guide me. I am very great-full and obliged towards my mentor and very

lucky to get such a great human being to work with.

Page | 8

PROFILE OF ORGANISATION:

SBI (STATE BANK OF INDIA) it is one of the most popular, reputed and largest nationalist

bank all over the world. SBI the name itself serves all information. It is one of the best customer

satisfaction oriented banks. State bank group is 100% on core banking solution and globally

networked. I was working under the Madhyamgram Branch and the people were very co-

operative. Each and every detail that I wanted for my project was happily placed before me.

NATURE OF THE PROJECT: This project includes a comparative study of SBI car loan

schemes vis-à-vis the other banks. Thus the nature of the project is purely analytical and survey

based. It is also theory based. Most of the portions of my analysis is based on the data collected

from various sources.

BRIEF OBJECTIVES/RESPONSIBILITIES ASSIGNED BY THE PROJECT MENTOR:

I have received all kinds of help from my mentor (Branch Manager) required for my project. He

was quite helpful from the very first day of my joining. He assigned me various responsibilities

to me like:

1. Recommended me the names of the various car dealers for my survey.

2. Referred me the names of various books and suggested to read economic times.

3. Provided me with various data regarding car loans.

4. Helped me to understand the basic idea about SBI car loan schemes.

5. Introduced me with the working staffs of the bank so that I get all information from whoever

required.

Page | 9

FRAMEWORK OF STUDY

THEORETICAL FRAMEWORK:

The first car ran on India’s road in 1897.Until the 1930’s cars were imported directly, but in

very small numbers. As of 2012-13, India is home to 40 million passenger vehicles and it is the

second (after China) fastest growing automobile market in the world.

Cars are very important to our society today. Not having these machineries, travelling from one

place to another would be such an inconvenience .Cars are significantly one of the most

expensive merchandise of all time. Almost everyone dreams of owing their own car. Most of the

large and rapidly-growing middle class, largely responsible for powering car sales growth,

depend on loans and credit for big purchases.

An auto loan is a unique kind of private loan, which permits a person to spread the charge of the

car for a comprehensive period of time, instead of paying up the whole amount in one setting. In

response for this auto loan, there is an interest that must be paid to whichever bank or building

society which the individual has loaned the money from. Generally, a person would be paying

back a little proportion of the loan every month, in addition to the interest charge; this is termed

as monthly installment.

SBI Car Loan:

SBI provides an attractive Car Loan Scheme with low interest rates, free accidental insurance,

easy repayment options, optional SBI life cover, total transparency, insurance and one time road

tax.. Loan finance will include vehicle registration charges, insurance, one-time road tax and

accessories worth Rs.25000/-.

In case of new cars, loan is provided on any make or model. In case of old cars too, the loan is

provided on any make or model, but the vehicle should not be more than 5 years old.

Page | 10

Eligibility:

Individual between the age of 21-65 years of age.

A Permanent employee of State / Central Government, Public Sector Undertaking, Private

company or a reputed establishment or

A Professional or self-employed individual.

A Person engaged in agriculture and allied activities.

Net Annual Income Rs. 100,000/- and above.

Loan Amount:

There is no upper limit for the amount of a car loan. A maximum loan amount of 2.5 times the

net annual income can be sanctioned. If married, one's spouse’s income could also be considered

provided the spouse becomes a co-borrower in the loan. The loan amount includes finance for

one-time road tax, registration plus insurance.

Documents Required:

One would need to submit the following documents along with the completed application form if

one is an existing SBI account holder:

Statement of Bank account of the borrower for last 12 months.

2 passport size photographs of borrower(s).

Signature identification from bankers of borrower(s).

A copy of passport /voters ID card/PAN card.

Proof of residence.

Latest salary-slip showing all deductions

I.T. Returns/Form 16: 2 years for salaried employees and 3 years for professional/self-

employed/businessmen duly accepted by the ITO wherever applicable to be submitted.

Proof of official address for non-salaried individuals.

If one is not an account holder with SBI he/she would also need to furnish documents that

establish his/her identity and give proof of residence.

Page | 11

Margin Money Scheme:

This is the most basic, and the most popular option. Here, the customer pays their share of

the cost of the car called the Margin Money and the bank gives the rest as a loan. The Margin

Money is usually 10-15% of the cost of the car. They repay the loan in the form of Equated

Monthly Installments(EMIs), which is paid in the form of Post Data Cheques(PDCs).

Tenure:

The tenure of this type of auto loan is usually 1 to 7 years. In most of the cases it is 84

months usually .As the tenure increases, the monthly EMI reduces for the same loan amount. But

since the tenure is long, one would pay many EMIs, and therefore would end up paying a lot

more in the form of interest compared to a shorter duration loan. So the customer chooses their

tenure depending on their need and repayment capacity.

Rate Of Interest:

The rate of interest on auto loans is higher than the home loans, but is normally lower the

personal loans .The interest rate is usually higher for the longer duration loans compared to the

shorter ones. The current rate of interest for new cars is 11.25% to 11.75% per annum. The

interest rate remains fixed for the entire tenure of the loan.

Repayment Procedures Of The Loan: SBI offers the longest repayment period in the

industry.

Repayment Period

Page | 12

For Salaried: Maximum of 84 months

For Self-employed & Professionals: Maximum 60 months

Repayment period for used vehicles: Up to 84 months from the date of original purchase of

the vehicle (subject to maximum tenure as above).

1. Equated Monthly Installment (EMI) is determined by the current rate of interest.

2. Loan must be repaid within 7 years from date of purchase of the car.

3. The borrower has the option to repay in a shorter duration.

4. Loan account should be closed before the guarantor reaches 65 years of age.

5. Funds for repayment may be:(in case of NRI car loan)

o Remittances from abroad through normal banking channels.

o NRE / FCNR (B) / NRO accounts.

o Remittances out of local funds by close relatives of NRIs.

Prepayment Penalty:

Prepayment fee of 2% of the amount of the loan prepaid is levied subject

to certain conditions. There can also be a limit to the amount the customer

can prepay – for example, the bank may stipulate that the customer would

incur a fee if he prepay more than 10% of his outstanding loan amount.

Some banks do offer zero prepayment penalties – especially during special

promotions. The customer should try to choose such a bank if possible.

Page | 13

Otherwise, they should opt for a loan that has the lowest prepayment

penalty.

Processing Fee:

0.50% of Loan amount to be paid up-front. Minimum: Rs. 500/-. Maximum Rs. 10,000/-. 25% of

Processing fee will be retained if application is rejected after pre-sanction survey.

Why SBI Car Loan?

No prepayment charges after 1 year. So if one has some money extra, he/she can pay it along

with the EMI and save on interest, which is not possible with other banks. Interest is daily

diminishing. There is no closing charges if you close your loan after 1 year. Others charge 2% to

6% of the remaining principle amount.

Current interest rates are:

1st year - 8%

2nd & 3rd year - 9%

4th year onwards - bank rate - will be 10% probably.

(And remember that one pays most of the interest on loan in first year. So 8% in first year

really counts!!!)

Advantages Of SBI Car Loan:

Lowest car loan interest rates

Longer repayment period of up to 84 months.

No hidden costs or administrative charges.

Finance for one-time road tax, registration fee, insurance premium and accessories

No advance EMIs. (Some Banks/companies ask you to pay one or more EMIs at the time of

disbursement of loan, thereby effectively reducing your loan amount.)

Page | 14

Complete transparency: SBI levy interest on daily reducing balance method. When one pay

one installment, the interest is automatically calculated on the reduced balance thereafter. When

one pay interest on an annual reducing balance, as charged by many other companies/banks, the

interest amount for the coming year is determined on the amount outstanding at the beginning of

the year. One continue to pay interest even on the amounts you repay during the year.

Good service: The service provided is more or less satisfactory.

The only disadvantage is that initial procedure is not that easy. In case of SBI the person will

need to go to the bank. Other banks will come to his/her doorstep.

Types Of SBI Car Loan:

I. SBI New Car Loan Scheme.

II. SBI Combo Loan Scheme.

III. Certified Pre-Owned Car Loans.

IV. SBI Car Loan Scheme for Used Cars.

V. NRI Car Loan.

Importance Of Car Loan:

Car has become an important mean for transport. Nowadays public transport has become too

much congested, it takes a lot of time to reach the destination on time. Hence people like to avail

personal transports. This growing necessity brings forward the demand for car loans. Further Car

Loan segment is a retail business, NPA (Non Performing Asset) percentage is very low. Hence

recovery in this segment is very good unlike housing loans. The project helps us to understand

the clear meaning of car loan of State Bank of India. It explains about the various criteria and

eligibility required for the car loan vis-à-vis the other banks. The comparative study of car loan

with that of other banks helps in understanding the fair car loan policies of the bank.

Page | 15

SPECIFIC OBJECTIVES OF THE PROJECT:

1. To analyze the car loan market share of State Bank Of India.

2. To find out marketing efforts put in by SBI viz-a-viz other banks.

3. Comparative analysis of SBI car loan scheme with other banks.

4. To suggest measures to improve the Car loan market share and loan portfolio.

5. To find out the problems in streamlining loans to businessmen.

6. To attract more customers to SBI Car Loan scheme.

7. To study the practical difficulties in extending car finance to businessmen.

8. To find out the strategies adopted by major private banks.

9. To examine the possibility of introducing alternate method of calculating

eligibility for car loan to businessmen.

SCOPE OF STUDY:

Car loan is that segment which accrues to the urban class people. Kolkata is a metropolitan city

and automobiles or cars are being heavily used. Every month a huge amount of loans from

different banks (both public and private) are being borrowed, sanctioned and disbursed. So there

is a vast scope of study on this topic. There are many private as well as public sector banks to

compete with the SBI. Though SBI offers the lowest interest rate on car loans its' market share is

not that good in comparison to other financial bodies. The scopes of study are:

1. To study the practical difficulties in extending car finance to the customers.

2. To find out the strategies adopted by major Private banks.

3. To find out suitable measures to increase the market of SBI Car Loans.

4. Making people aware of the various facilities that SBI provides.

5. Analyzing the sector of mob that injects liquidity into the banking sector through loans.

Page | 16

LIMITATIONS:

1. Time is a big constraint.

2. Again the scope of study is within Kolkata which makes it less broad based.

3. There prevails a lot of secrecy in the car loan market which makes it a bit difficult to

gather the proper information.

4. During survey in the private sector, lot of people did not turn up to the questions asked by

the intern.

5. Collection of data regarding the loans to businessmen was of great difficulty because

those loans are sanctioned only from SME branches.

6. The sample size does not represent the total population.

7. Amateur use MS-Excel for data analysis.

PERIOD OF STUDY:

The period of the study for the given project was 8 to 10 weeks. My starting date was 24th June

and date of completion was 30th August. Timings were from 11A.M. to 5P.M. from Monday to

Friday and Saturday till 3 P.M., excluding Sunday,

Page | 17

METHODOLOGY AND ANALYSIS

METHODOLOGY:

To fulfill the objective of my study I have taken both into consideration namely primary and

secondary data. I had also prepared a few questions to ask during the survey period.

Primary Data: Primary data have been collected through direct interview by direct contact

method. The method which was adopted to collect the information is ‘Personal Interview’

method. Personal interview and discussions were made with the branch manager and other

personnel in the branch. Apart from this interviews of various sale executives of different car

dealers were also taken for this purpose.

Secondary Data: Secondary data is mainly based on internet sites, text books, journals,

magazines, etc. Various sources that were used for the collection of secondary data are-

o Internal files and material.

o Websites like- sbitimes.com, Wikipedia.com, economictimes.com,

moneycontrol.com, sbi.co.in, investopedia.com, etc.

Questionnaire: It is a free frank communication such that their privacy is not interfered. A

questionnaire was prepared for the Dealer Executives to study the market scenario and the

problems faced by them with the SBI and the benefits with the other banks. The following

questions were placed:

1. What is the year of incorporation/ commencement of operation?

2. What is the business prospect?

3. Annual turnover: 2011-2012 2012-2013?

4. Next profit (approx.)?

5. Whether having banking arrangements?

6. If Yes, then who are the present bankers?

b) How is the banking experience with the banker?

c) Any constraints faced?

7. a) If No, then how they are meeting their financial needs?

Page | 18

b) Are they interested for any Banking arrangements?

8. Have they ever approached any Bank for banking arrangements?

9. If Yes, then how was the experience?

10. Constraints faced in the present business scenarios?

Page | 19

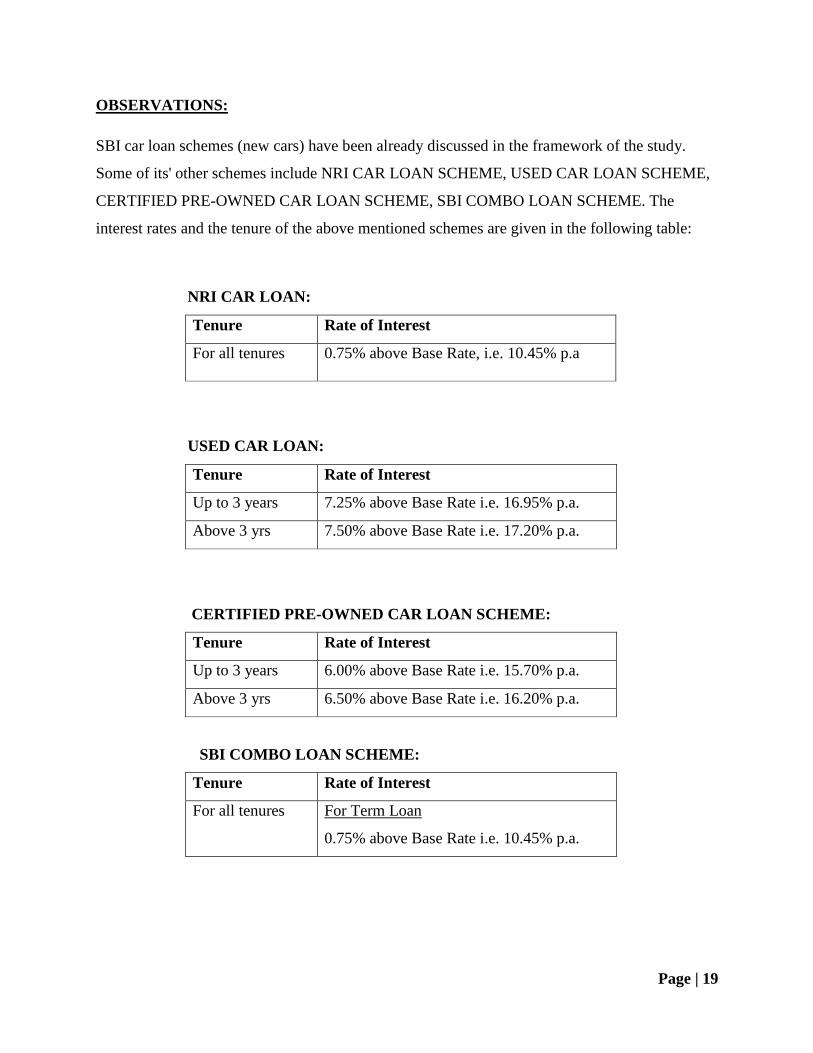

OBSERVATIONS:

SBI car loan schemes (new cars) have been already discussed in the framework of the study.

Some of its' other schemes include NRI CAR LOAN SCHEME, USED CAR LOAN SCHEME,

CERTIFIED PRE-OWNED CAR LOAN SCHEME, SBI COMBO LOAN SCHEME. The

interest rates and the tenure of the above mentioned schemes are given in the following table:

NRI CAR LOAN:

Tenure Rate of Interest

For all tenures 0.75% above Base Rate, i.e. 10.45% p.a

USED CAR LOAN:

Tenure Rate of Interest

Up to 3 years 7.25% above Base Rate i.e. 16.95% p.a.

Above 3 yrs 7.50% above Base Rate i.e. 17.20% p.a.

CERTIFIED PRE-OWNED CAR LOAN SCHEME:

Tenure Rate of Interest

Up to 3 years 6.00% above Base Rate i.e. 15.70% p.a.

Above 3 yrs 6.50% above Base Rate i.e. 16.20% p.a.

SBI COMBO LOAN SCHEME:

Tenure Rate of Interest

For all tenures For Term Loan

0.75% above Base Rate i.e. 10.45% p.a.

Page | 20

TABLE 1

COMPARATIVE STUDY OF CAR LOAN INTEREST RATES OF DIFFERENT

BANKS:

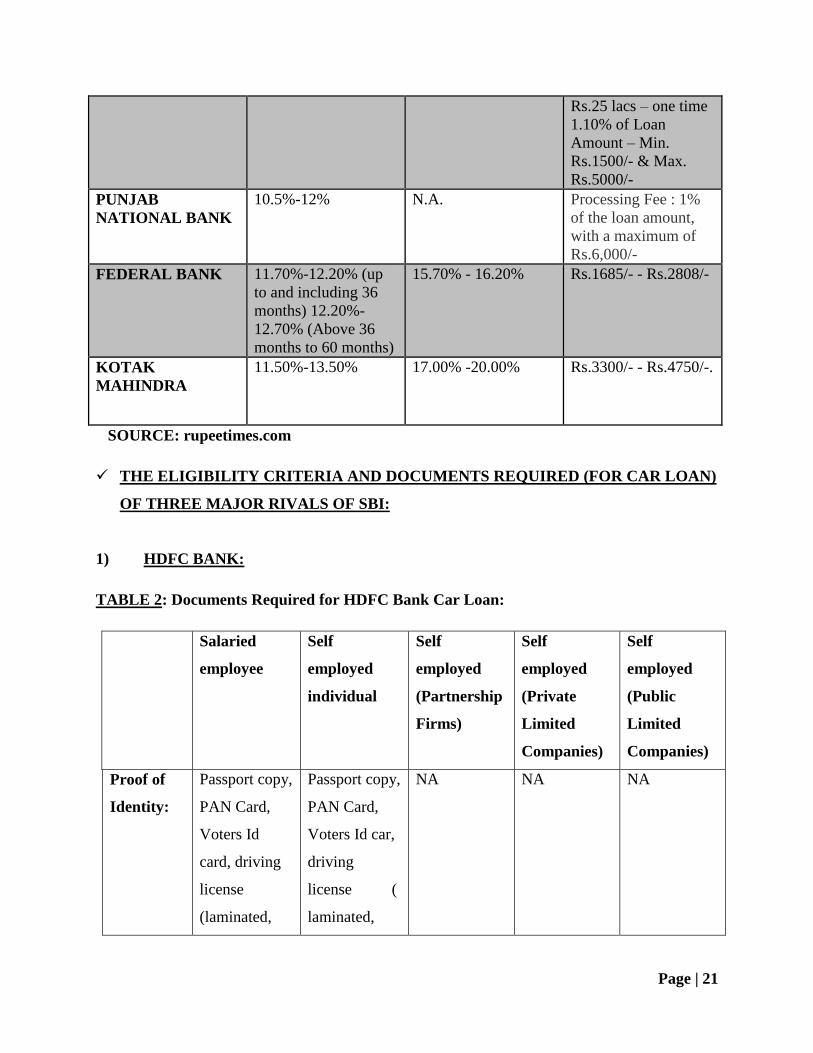

BANKS NEW CAR LOAN USED CAR LOAN PROCESSING FEE

HDFC BANK 10.25%-12.50% 15.25%-17.75% ( 60

months) 15.25%-

17.75% (48 months)

15.75%-18.25% (24

months) 15.75%-

18.25% (12 months)

Corporate Rates

13.50%-14.25%

Rs. 2325/- to Rs.

4275/-

For Corporates

Rs. 1500/-

BANK OF

BARODA

13.25% N.A. 0.75% ( Up to 15

lacs), Max Rs.

10000/-

0.5% (Above 15 lacs),

Min Rs. 10000/-, No

Maximum Limit

CANARA BANK 12.50% N.A. 0.1% of Loan

Amount.

(Min. Rs. 250/-, Max.

Rs.500/-)

CORPORATION

BANK

12%-12.50%

11.35%-11.70% (for

SRTOs Covered

under CGTMSE)

N.A. 0.5% of Loan Amount

AXIS BANK 11.50-14.50% 16.50% - 18.00% Rs.3000/--Rs.3500/-

ICICI BANK 11.50%-14.75%

(From 36-60 months)

13.75%-16% (From

24-35 months)

15.75%-17% (up to

23 months)

16.50% - 18.50% Rs.2500/- - Rs.5000/-

BANK OF INDIA 12.50%-13.50% 13.50% - 14.00% a) Loans up to

Rs.25,000/- one time

Rs.1000/-

b) Loans above

Rs.25,000/- up to

Page | 21

Rs.25 lacs – one time

1.10% of Loan

Amount – Min.

Rs.1500/- & Max.

Rs.5000/-

PUNJAB

NATIONAL BANK

10.5%-12% N.A. Processing Fee : 1%

of the loan amount,

with a maximum of

Rs.6,000/-

FEDERAL BANK 11.70%-12.20% (up

to and including 36

months) 12.20%-

12.70% (Above 36

months to 60 months)

15.70% - 16.20% Rs.1685/- - Rs.2808/-

KOTAK

MAHINDRA

11.50%-13.50% 17.00% -20.00% Rs.3300/- - Rs.4750/-.

SOURCE: rupeetimes.com

THE ELIGIBILITY CRITERIA AND DOCUMENTS REQUIRED (FOR CAR LOAN)

OF THREE MAJOR RIVALS OF SBI:

1) HDFC BANK:

TABLE 2: Documents Required for HDFC Bank Car Loan:

Salaried

employee

Self

employed

individual

Self

employed

(Partnership

Firms)

Self

employed

(Private

Limited

Companies)

Self

employed

(Public

Limited

Companies)

Proof of

Identity:

Passport copy,

PAN Card,

Voters Id

card, driving

license

(laminated,

Passport copy,

PAN Card,

Voters Id car,

driving

license (

laminated,

NA

NA

NA

Page | 22

recent,

legible)

recent,

legible)

Income

Proof:

Latest salary

slip with form

16

Latest ITR

Audited

balance sheet,

Profit & Loss

Account for

latest two

years and the

latest 2 years

IT returns of

the company

NA NA

Address

Proof:

Ration

card/Driving

license/Voters

card /passport

copy/telephon

e

bill/electricity

bill/Life

insurance

policy PAN

Card.

Ration

card/Driving

license/Voters

card/ passport

copy/telephon

e

bill/electricity

bill/Life

insurance

policy PAN

Card.

Telephone

Bill/Electricit

y Bill/Shop &

Establishment

Act

certificate/

SSI registered

certificate/

Sales Tax

certificate.

Telephone

Bill/Electricit

y Bill/Shop &

Establishment

Act

certificate/

SSI registered

certificate/

Sales Tax

certificate.

Telephone

Bill/Electricit

y Bill/Shop &

Establishment

Act certificate

/SSI

registered

certificate/

Sales Tax

certificate.

Bank

Statement:

Not

mandatory

Small cars:

waived.

Mid – sized

and premium

cars: waived

(income >15

lacs).

Small cars:

waived.

Mid – sized

and premium

cars: waived

(income >15

lacs).

NA

NA

Page | 23

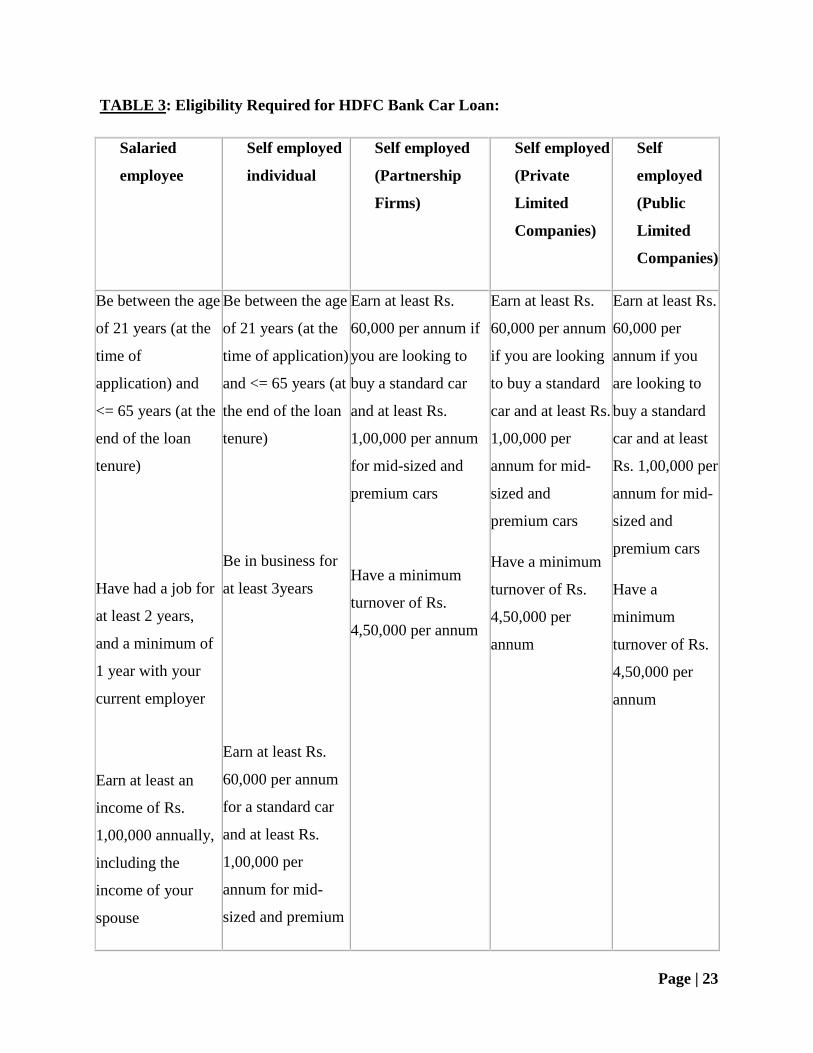

TABLE 3: Eligibility Required for HDFC Bank Car Loan:

Salaried

employee

Self employed

individual

Self employed

(Partnership

Firms)

Self employed

(Private

Limited

Companies)

Self

employed

(Public

Limited

Companies)

Be between the age

of 21 years (at the

time of

application) and

<= 65 years (at the

end of the loan

tenure)

Have had a job for

at least 2 years,

and a minimum of

1 year with your

current employer

Earn at least an

income of Rs.

1,00,000 annually,

including the

income of your

spouse

Be between the age

of 21 years (at the

time of application)

and <= 65 years (at

the end of the loan

tenure)

Be in business for

at least 3years

Earn at least Rs.

60,000 per annum

for a standard car

and at least Rs.

1,00,000 per

annum for mid-

sized and premium

Earn at least Rs.

60,000 per annum if

you are looking to

buy a standard car

and at least Rs.

1,00,000 per annum

for mid-sized and

premium cars

Have a minimum

turnover of Rs.

4,50,000 per annum

Earn at least Rs.

60,000 per annum

if you are looking

to buy a standard

car and at least Rs.

1,00,000 per

annum for mid-

sized and

premium cars

Have a minimum

turnover of Rs.

4,50,000 per

annum

Earn at least Rs.

60,000 per

annum if you

are looking to

buy a standard

car and at least

Rs. 1,00,000 per

annum for mid-

sized and

premium cars

Have a

minimum

turnover of Rs.

4,50,000 per

annum

Page | 24

Have a telephone

at your residence

cars.

Have a telephone

at residence

Have a landline at

office and residence.

Have a landline at

office

Have a landline

at office

SOURCE: hdfc.co.in

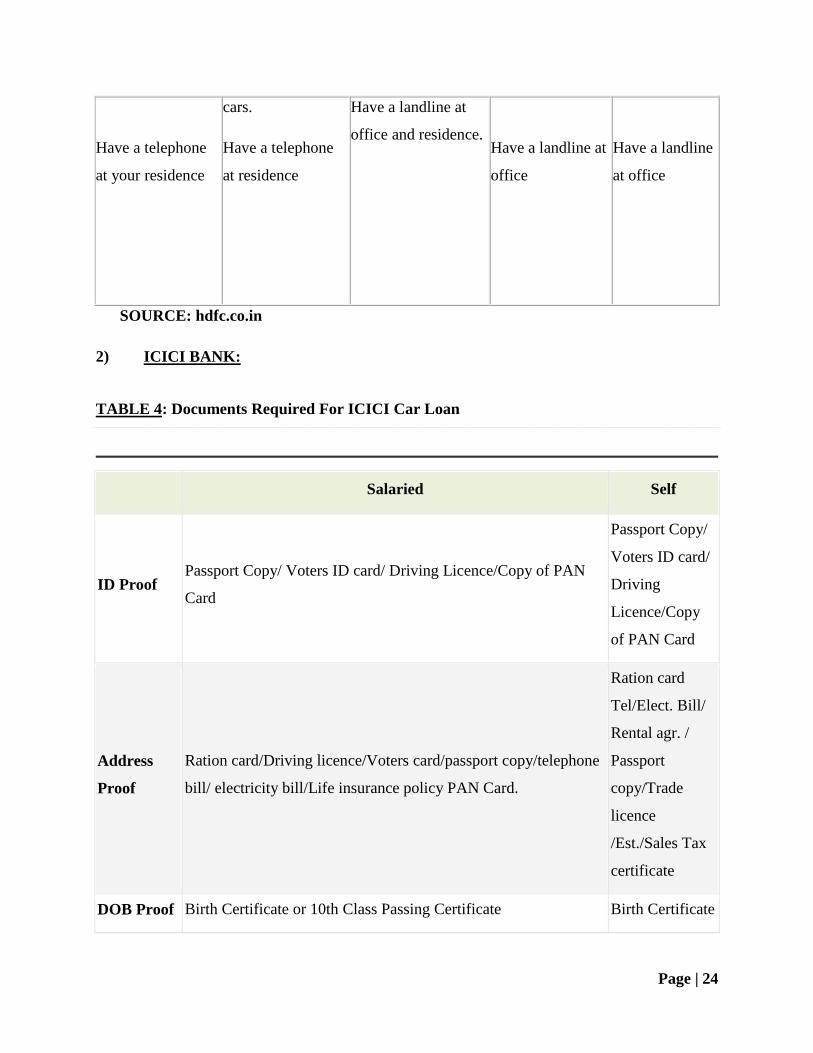

2) ICICI BANK:

TABLE 4: Documents Required For ICICI Car Loan

Salaried Self

ID Proof Passport Copy/ Voters ID card/ Driving Licence/Copy of PAN

Card

Passport Copy/

Voters ID card/

Driving

Licence/Copy

of PAN Card

Address

Proof

Ration card/Driving licence/Voters card/passport copy/telephone

bill/ electricity bill/Life insurance policy PAN Card.

Ration card

Tel/Elect. Bill/

Rental agr. /

Passport

copy/Trade

licence

/Est./Sales Tax

certificate

DOB Proof Birth Certificate or 10th Class Passing Certificate Birth Certificate

Page | 25

or 10th Class

Passing

Certificate

Financial

Docs

Salaried Individual:

Latest Salary slip or salary certificate.

2 Years Form 16 of the previous Financial Year or latest Income

Tax Returns.

Signature Proof

Self Employed

Individual:

Income Tax

Returns of 2

previous

financial years.

Partnership

Firms,

Societies &

Companies

: Income Tax

Returns of 2

previous

financial years

along with

Profit & Loss

Account

Statements and

Balance Sheets

of both years.

Signature Proof

Partnership

Firms:

Partnership

deed and Letter

signed by all

partners

Page | 26

authorizing one

partner to

execute the

required Car

Loan.

Societies and

Companies:

Resolution by

Board of

Directors (or

such managing

body) &

Memorandum

& Articles of

Association (or

Society/Trust

deed).

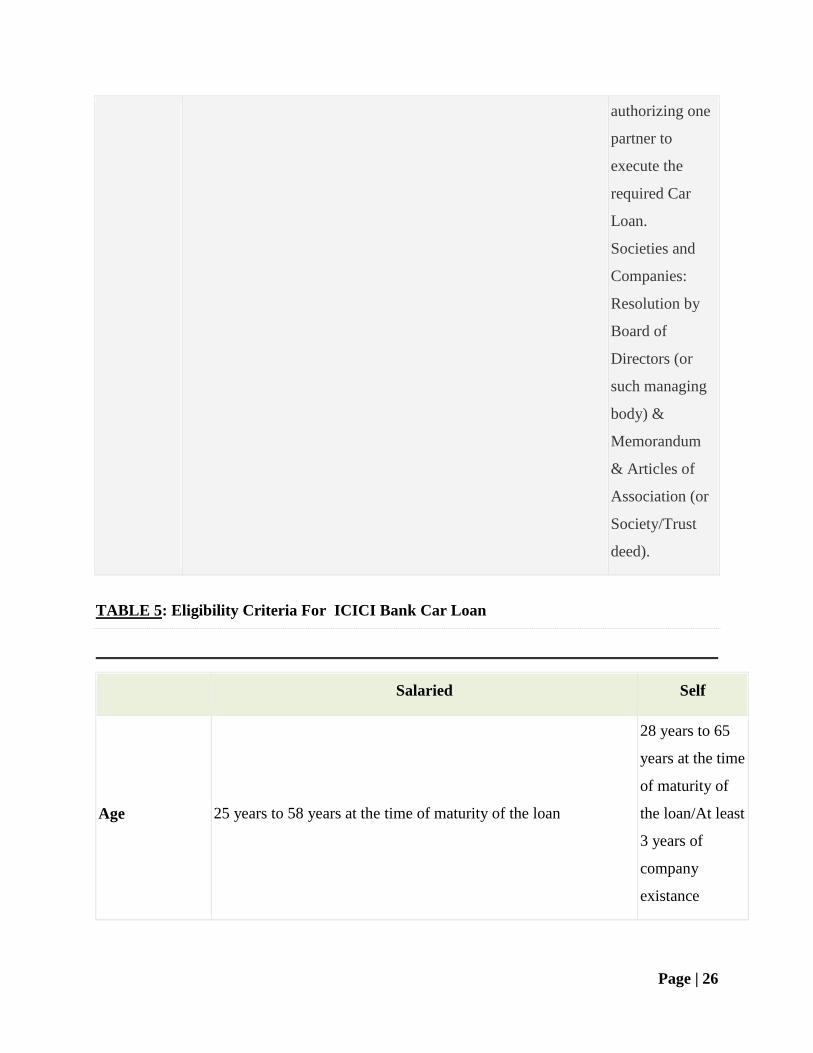

TABLE 5: Eligibility Criteria For ICICI Bank Car Loan

Salaried Self

Age 25 years to 58 years at the time of maturity of the loan

28 years to 65

years at the time

of maturity of

the loan/At least

3 years of

company

existance

Page | 27

Income Gross annual salary of at least Rs. 2.5 lac per annum

Gross annual

income of at

least Rs. 2 lac

per annum;

Firm should

have a

minimum PAT

(profit after tax)

of Rs. 1.25

lakhs

Job Experience The total employment stability should be more than 2 years and

current employment stability of minimum 1 year

Business

stability should

be more than 3

years

Residence

Proof Information Not Available

Information Not

Available

SOURCE: icici.co.in

3) AXIS BANK:

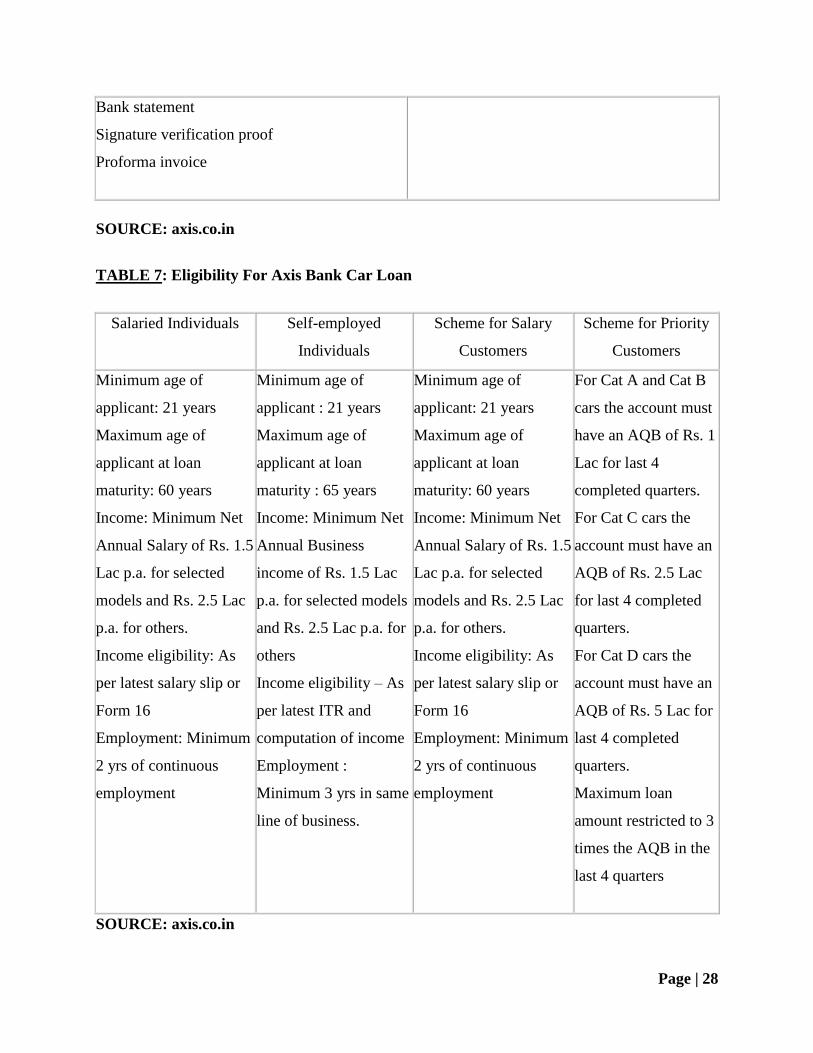

TABLE 6: Documents Required for Axis Car Loans:

List of Car Loan documents required Post Sanction / Pre Disbursement

Documentation

Age proof

ID proof

Application form

Photograph

Residence proof

Income proof

Loan Agreement duly signed along with RTO

set

Post Dated Cheques (PDCs) / ECS form /

Standing Instruction (SI) request

Margin money receipt

Page | 28

Bank statement

Signature verification proof

Proforma invoice

SOURCE: axis.co.in

TABLE 7: Eligibility For Axis Bank Car Loan

Salaried Individuals Self-employed

Individuals

Scheme for Salary

Customers

Scheme for Priority

Customers

o Minimum age of

applicant: 21 years

o Maximum age of

applicant at loan

maturity: 60 years

o Income: Minimum Net

Annual Salary of Rs. 1.5

Lac p.a. for selected

models and Rs. 2.5 Lac

p.a. for others.

o Income eligibility: As

per latest salary slip or

Form 16

o Employment: Minimum

2 yrs of continuous

employment

o Minimum age of

applicant : 21 years

o Maximum age of

applicant at loan

maturity : 65 years

o Income: Minimum Net

Annual Business

income of Rs. 1.5 Lac

p.a. for selected models

and Rs. 2.5 Lac p.a. for

others

o Income eligibility – As

per latest ITR and

computation of income

o Employment :

Minimum 3 yrs in same

line of business.

o Minimum age of

applicant: 21 years

o Maximum age of

applicant at loan

maturity: 60 years

o Income: Minimum Net

Annual Salary of Rs. 1.5

Lac p.a. for selected

models and Rs. 2.5 Lac

p.a. for others.

o Income eligibility: As

per latest salary slip or

Form 16

o Employment: Minimum

2 yrs of continuous

employment

o For Cat A and Cat B

cars the account must

have an AQB of Rs. 1

Lac for last 4

completed quarters.

o For Cat C cars the

account must have an

AQB of Rs. 2.5 Lac

for last 4 completed

quarters.

o For Cat D cars the

account must have an

AQB of Rs. 5 Lac for

last 4 completed

quarters.

o Maximum loan

amount restricted to 3

times the AQB in the

last 4 quarters

SOURCE: axis.co.in

Page | 29

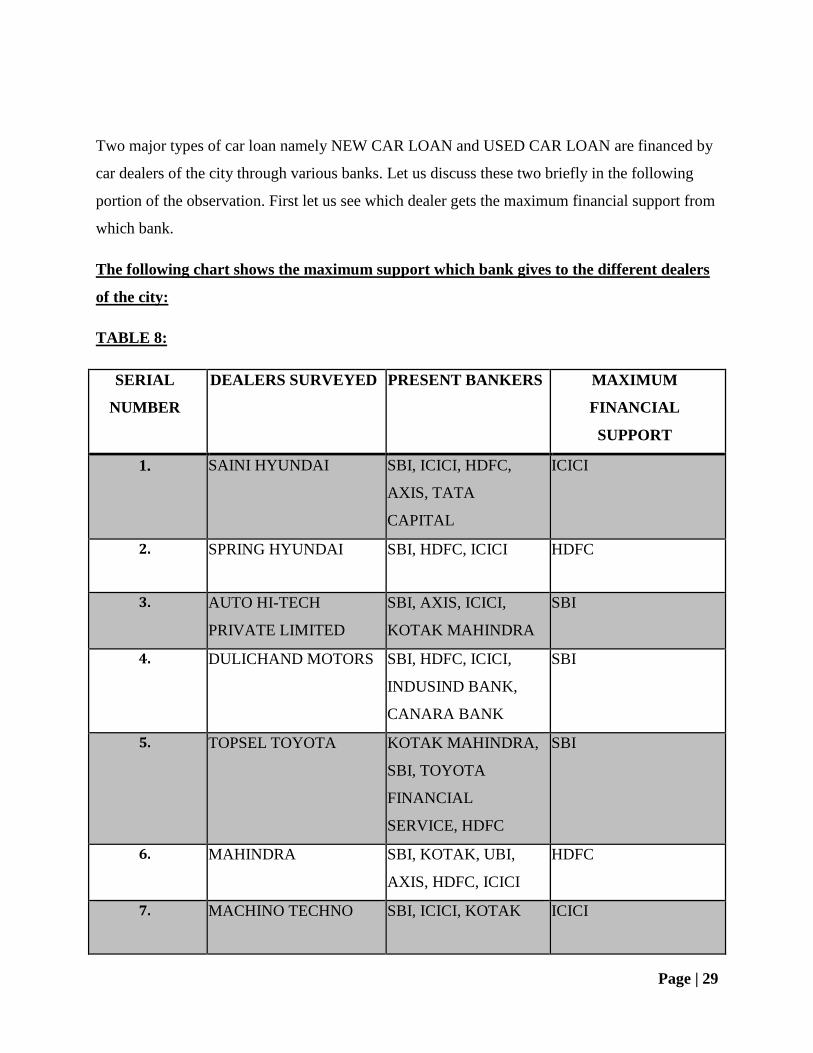

Two major types of car loan namely NEW CAR LOAN and USED CAR LOAN are financed by

car dealers of the city through various banks. Let us discuss these two briefly in the following

portion of the observation. First let us see which dealer gets the maximum financial support from

which bank.

The following chart shows the maximum support which bank gives to the different dealers

of the city:

TABLE 8:

SERIAL

NUMBER

DEALERS SURVEYED PRESENT BANKERS MAXIMUM

FINANCIAL

SUPPORT

1. SAINI HYUNDAI SBI, ICICI, HDFC,

AXIS, TATA

CAPITAL

ICICI

2. SPRING HYUNDAI SBI, HDFC, ICICI HDFC

3. AUTO HI-TECH

PRIVATE LIMITED

SBI, AXIS, ICICI,

KOTAK MAHINDRA

SBI

4. DULICHAND MOTORS SBI, HDFC, ICICI,

INDUSIND BANK,

CANARA BANK

SBI

5. TOPSEL TOYOTA KOTAK MAHINDRA,

SBI, TOYOTA

FINANCIAL

SERVICE, HDFC

SBI

6. MAHINDRA SBI, KOTAK, UBI,

AXIS, HDFC, ICICI

HDFC

7. MACHINO TECHNO SBI, ICICI, KOTAK ICICI

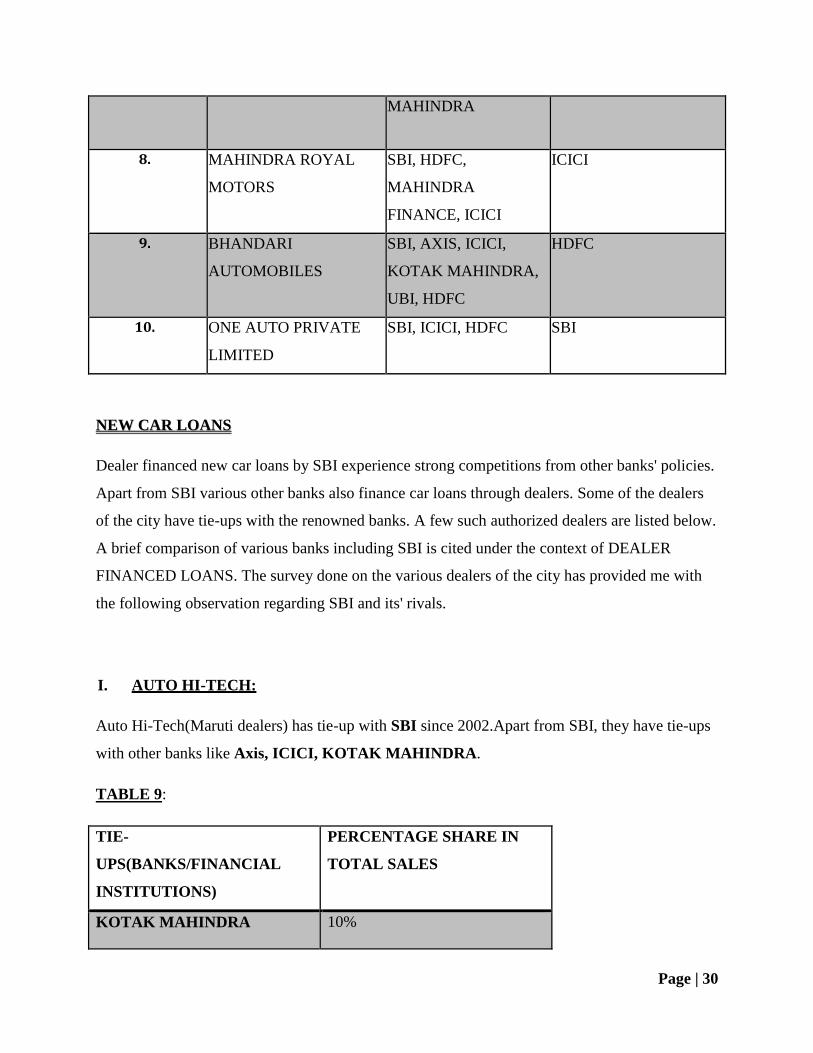

Page | 30

MAHINDRA

8. MAHINDRA ROYAL

MOTORS

SBI, HDFC,

MAHINDRA

FINANCE, ICICI

ICICI

9. BHANDARI

AUTOMOBILES

SBI, AXIS, ICICI,

KOTAK MAHINDRA,

UBI, HDFC

HDFC

10. ONE AUTO PRIVATE

LIMITED

SBI, ICICI, HDFC SBI

NNEEWW CCAARR LLOOAANNSS

Dealer financed new car loans by SBI experience strong competitions from other banks' policies.

Apart from SBI various other banks also finance car loans through dealers. Some of the dealers

of the city have tie-ups with the renowned banks. A few such authorized dealers are listed below.

A brief comparison of various banks including SBI is cited under the context of DEALER

FINANCED LOANS. The survey done on the various dealers of the city has provided me with

the following observation regarding SBI and its' rivals.

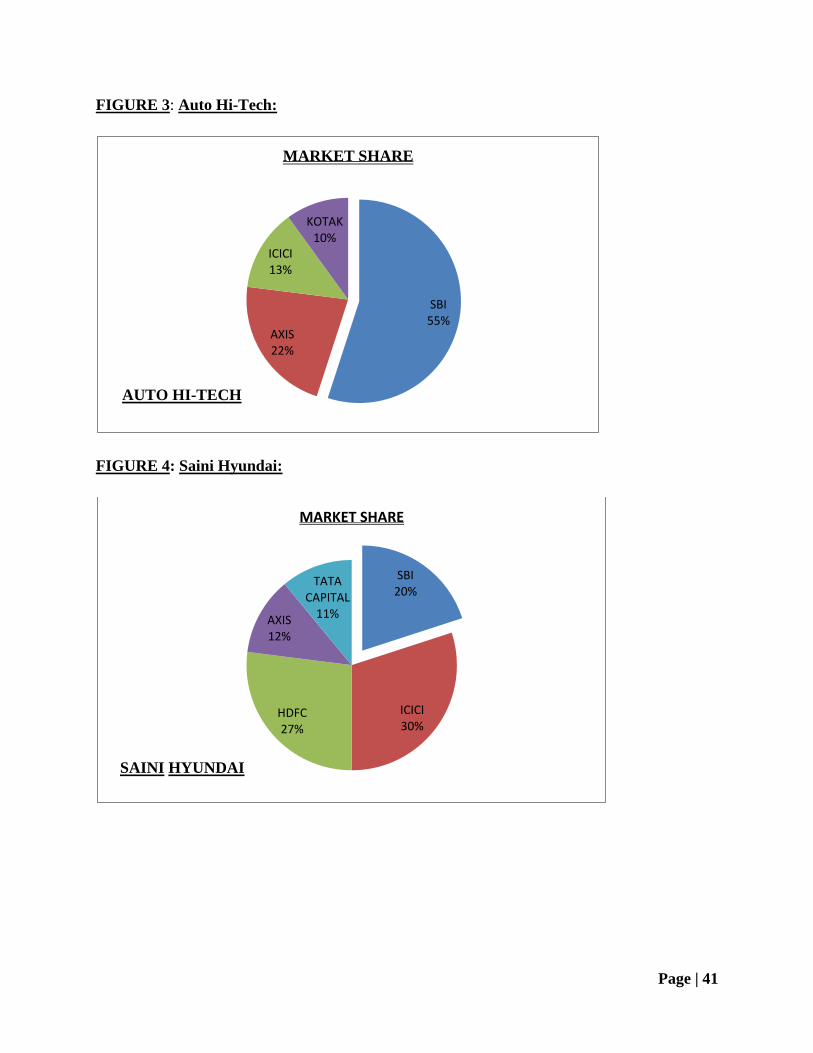

I. AUTO HI-TECH:

Auto Hi-Tech(Maruti dealers) has tie-up with SBI since 2002.Apart from SBI, they have tie-ups

with other banks like Axis, ICICI, KOTAK MAHINDRA.

TABLE 9:

TIE-

UPS(BANKS/FINANCIAL

INSTITUTIONS)

PERCENTAGE SHARE IN

TOTAL SALES

KOTAK MAHINDRA 10%

Page | 31

ICICI 13%

AXIS 22%

SBI 55%

SOURCE: Sales Executive(Auto Hi-tech)

As per the data collected from Auto Hi-Tech, they are satisfied with the services rendered by SBI

but the only problem is associated with the loans for the businessmen. As the loan approval

process in case of businessmen takes huge time( more than 1 month in many cases),there is

always a risk of losing such customer for the dealer.

II. SAINI HYUNDAI:

Saini Hyundai has tie up with SBI since 2007. Along with SBI they have tie ups with

ICICI,HDFC, Tata Capital and recently Axis Bank

TABLE 10:

TIE-UPS(BANKS/FINANCIAL

INSTITUTIONS)

PERCENTAGE SHARE IN TOTAL

SALES

TATA CAPITAL 11%

AXIS 12%

HDFC 27%

SBI 20%

ICICI 30%

SOURCE: Sales Manager(Saini Hyundai)

Maximum amount of loan in case of the above mentioned dealer is financed by HDFC and

ICICI.As per the Sales Manager, there has been large improvement in policies and schemes of

SBI but it still lacks in providing proper customer services. The main constraints faced by the

customers who have applied for SBI car loan are as follows:

Page | 32

Customer Service is not up to the mark.

Lengthy procedure in many case especially in case of businessmen.

In most of the cases the loan approval has to done from Jeevan Deep Branch(and not

from the respective branch), which is often claimed by the customers as huge wastage of

time.

III. BHANDARI AUTOMOBILES:

Bhandari has recent tie up with SBI(since 2011). HDFC, ICICI, Axis, UBI, KOTAK are the

banks with which the dealer has tie ups.SBI provides 10.45% interest rate which is lower

compared to other banks.

TABLE 11:

TIE-UPS(BANKS/FINANCIAL

INSTITUTIONS)

PERCENTAGE SHARE IN

TOTAL SALES

KOTAK 8%

UBI 15%

ICICI 24%

HDFC 28%

AXIS 15%

SBI 10%

SOURCE: Sales Executive(Bhandari Automobiles)

As per the information given by the Sales Manager, they are satisfied with the financial

assistance given by SBI. But same as Saini Hyundai the complains are:

Delay in processing in loan sanction

Lack of proper customer services

Page | 33

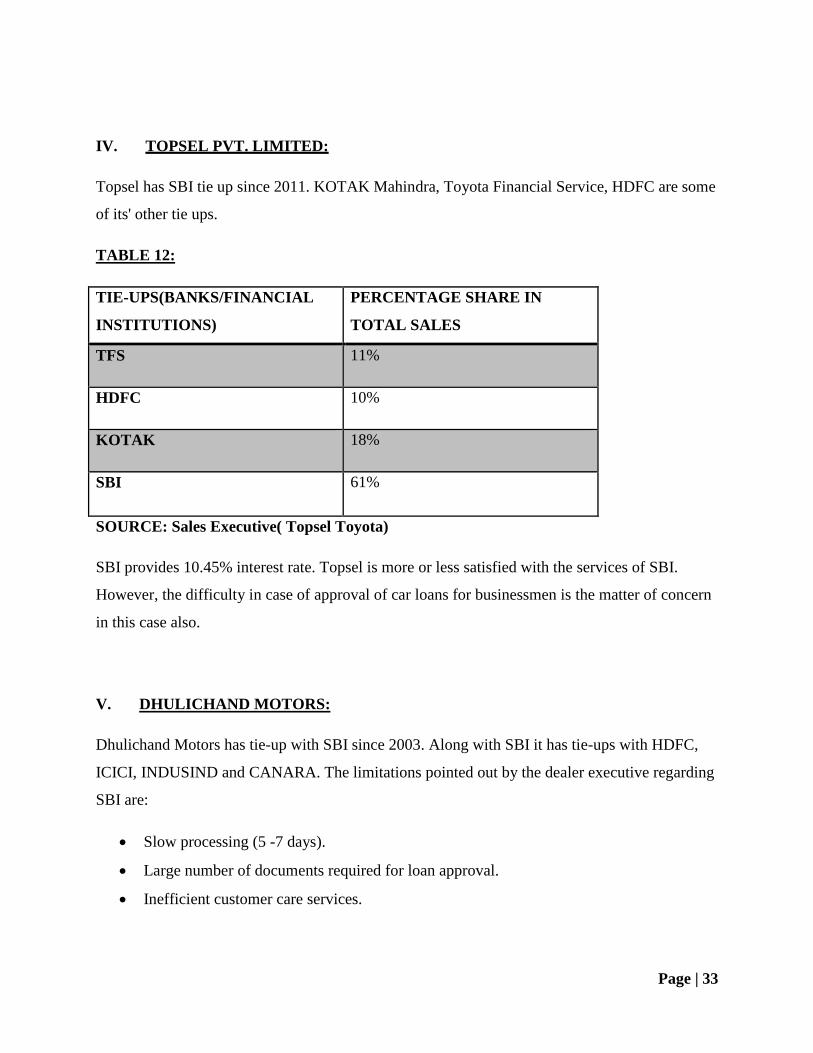

IV. TOPSEL PVT. LIMITED:

Topsel has SBI tie up since 2011. KOTAK Mahindra, Toyota Financial Service, HDFC are some

of its' other tie ups.

TABLE 12:

TIE-UPS(BANKS/FINANCIAL

INSTITUTIONS)

PERCENTAGE SHARE IN

TOTAL SALES

TFS 11%

HDFC 10%

KOTAK 18%

SBI 61%

SOURCE: Sales Executive( Topsel Toyota)

SBI provides 10.45% interest rate. Topsel is more or less satisfied with the services of SBI.

However, the difficulty in case of approval of car loans for businessmen is the matter of concern

in this case also.

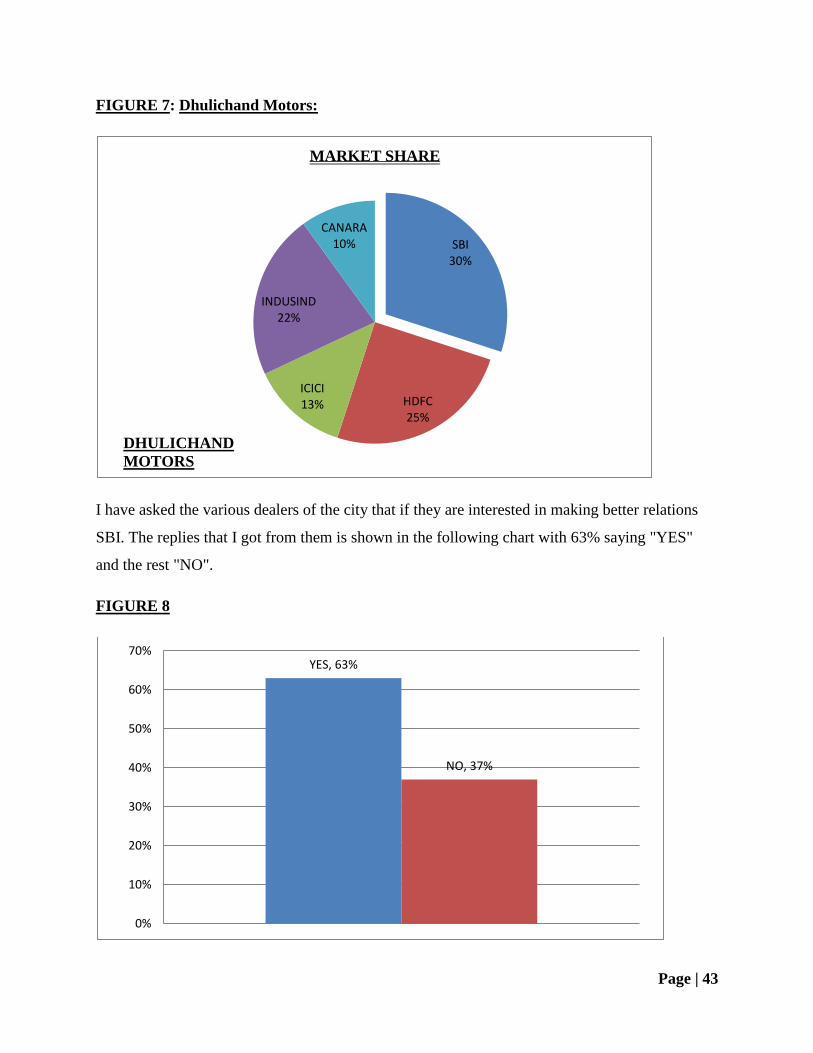

V. DHULICHAND MOTORS:

Dhulichand Motors has tie-up with SBI since 2003. Along with SBI it has tie-ups with HDFC,

ICICI, INDUSIND and CANARA. The limitations pointed out by the dealer executive regarding

SBI are:

Slow processing (5 -7 days).

Large number of documents required for loan approval.

Inefficient customer care services.

Page | 34

TABLE 13:

TIE-UPS(BANKS/FINANCIAL

INSTITUTIONS)

PERCENTAGE SHARE IN TOTAL

SALES

CANARA 10%

INDUSIND 22%

ICICI 13%

HDFC 25%

SBI 30%

SOURCE: Sales Manager(Dhulichand motors)

Here it can be seen that SBI holds a higher share of market. The reason for this can be it has the

oldest tie-up with SBI (Since 2003).

UUSSEEDD CCAARR LLOOAANNSS

SBI and other private and public banks provide various schemes for loans granted for used cars.

My analysis also focuses on used car loans of SBI and its competitors. The used car loan scheme

of SBI is given below:

Tenure Rate of Interest

Up to 3 years 7.25% above Base Rate i.e. 16.95%

p.a.

Above 3 yrs 7.50% above Base Rate i.e. 17.20%

p.a.

Page | 35

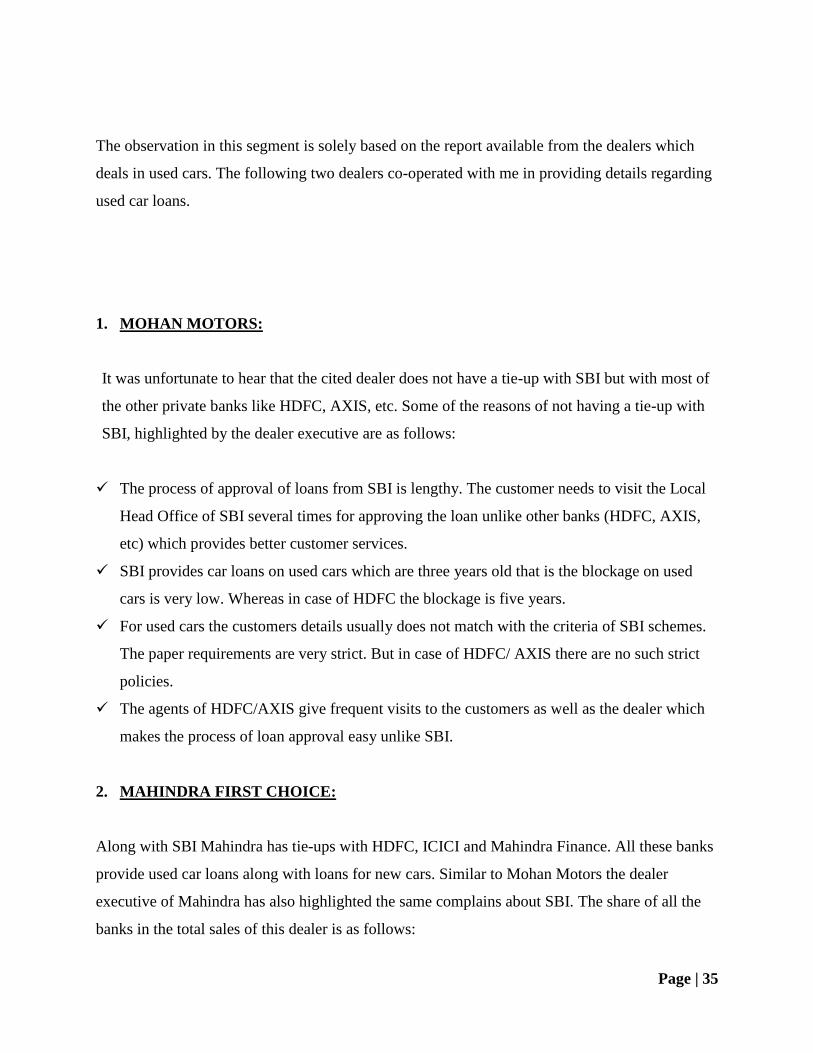

The observation in this segment is solely based on the report available from the dealers which

deals in used cars. The following two dealers co-operated with me in providing details regarding

used car loans.

1. MOHAN MOTORS:

It was unfortunate to hear that the cited dealer does not have a tie-up with SBI but with most of

the other private banks like HDFC, AXIS, etc. Some of the reasons of not having a tie-up with

SBI, highlighted by the dealer executive are as follows:

The process of approval of loans from SBI is lengthy. The customer needs to visit the Local

Head Office of SBI several times for approving the loan unlike other banks (HDFC, AXIS,

etc) which provides better customer services.

SBI provides car loans on used cars which are three years old that is the blockage on used

cars is very low. Whereas in case of HDFC the blockage is five years.

For used cars the customers details usually does not match with the criteria of SBI schemes.

The paper requirements are very strict. But in case of HDFC/ AXIS there are no such strict

policies.

The agents of HDFC/AXIS give frequent visits to the customers as well as the dealer which

makes the process of loan approval easy unlike SBI.

2. MAHINDRA FIRST CHOICE:

Along with SBI Mahindra has tie-ups with HDFC, ICICI and Mahindra Finance. All these banks

provide used car loans along with loans for new cars. Similar to Mohan Motors the dealer

executive of Mahindra has also highlighted the same complains about SBI. The share of all the

banks in the total sales of this dealer is as follows:

Page | 36

TABLE 14:

TIE-UPS(BANKS/FINANCIAL

INSTITUTIONS)

PERCENTAGE SHARE IN TOTAL

SALES

SBI 24%

HDFC 28%

ICICI 30%

MAHINDRA FINANCE 18%

SOURCE: Sales Manager(Mahindra First Choice)

I convey my special thanks to the Bakultala Branch SBI for providing me with the data which

gave me the details of the loans those are being sourced and sanctioned from the branch. Here is

shortlisted the number of loans sourced/sanctioned and the amount of loans sourced/sanctioned.

The data obtained is of the last financial year. The tables showing the data sheet are as follows.

TABLE 15: Amount Of Loan Being Sourced At The Bakultala Branch In The Last

Financial Year

MONTH

SOURCING

NUMBER AMOUNT(IN LACS)

APRIL 2O12 9 34.74

MAY 2012 4 15.00

JUNE 2012 5 11.25

JULY 2012

3 14.10

AUGUST 2012 12 46.90

SEPTEMBER 2012 9 18.90

Page | 37

OCTOBER 2012 8 29.73

NOVEMBER 2012 10 31.32

DECEMBER 2012 13 46.00

JANUARY 2013 15 58.55

FEBRUARY 2013 11 49.55

MARCH 2013 21 71.65

SOURCE: SBI (Bakultala Branch)

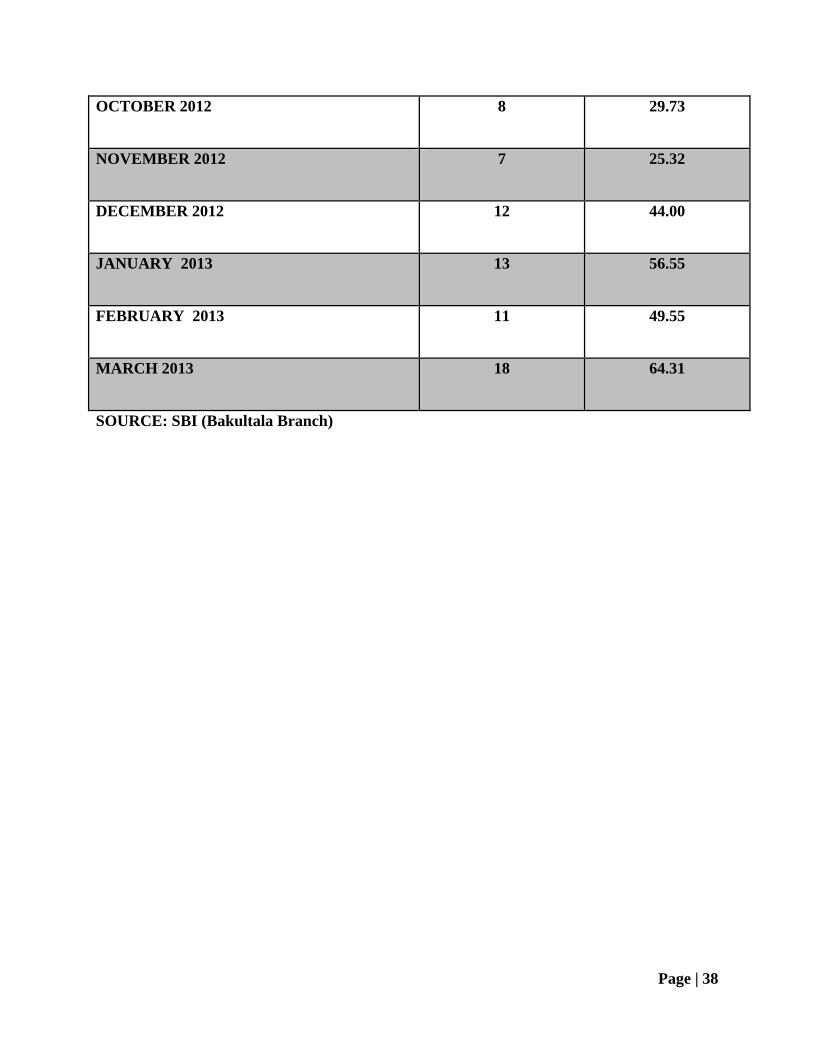

TABLE 16: Amount Of Loan Being Sanctioned At The Bakultala Branch In The Last

Financial Year

MONTH

SANCTION

NUMBERS AMOUNT(IN LACS)

APRIL 2012 8 29.12

MAY 2012 3 14.00

JUNE 2012 3 7.50

JULY 2012 3 14.10

AUGUST 2012 10 34.38

SEPTEMBER 2012 5 12.90

Page | 38

OCTOBER 2012 8 29.73

NOVEMBER 2012 7 25.32

DECEMBER 2012 12 44.00

JANUARY 2013 13 56.55

FEBRUARY 2013 11 49.55

MARCH 2013 18 64.31

SOURCE: SBI (Bakultala Branch)

Page | 39

ANALYSIS:

As per the reports observed from the net and the survey on various dealers and individuals I have

come to a conclusion that SBI offers the lowest interest rates among the major banks of the city.

This can be seen from the following column diagram which shows the interest rates of the six

major rivals of STATE BANK of INDIA.

FIGURE 1

The above diagram shows the interest rates on new cars. Apart from new cars SBI and other

banks also provide loans on used cars on which the rate of interest charged is different from the

above. In this segment CANARA BANK has the edge over SBI. SBI charges one of the highest

interest rates in used car loans. It is evident from the following table and the column diagram.

TABLE 17:

BANKS

INTEREST

RATES(USED

CARS)

SBI 16.95%

UBI

13.55%

HDFC 17.75%

0.00%

5.00%

10.00%

15.00%

RATE OF INTEREST

RATE OF INTEREST

Page | 40

ICICI 16.50%

CANARA 10.45%

FIGURE 2

SBI enjoys fruitful market condition with some of the dealers the city. From the above

observations it is quite evident that SBI has good market share with few dealers. But in some

cases the rivals have an upper-hand in the market. Though SBI offers the lowest interest rates in

the market it lacks in customer service facilities which pushes it back in the competition with

other banks. Other banks provide various facilities which makes it less hectic for the customers

to get approval for the loan. Hence even if the cost is high customers do want a hastle free

journey to a new car. This makes SBI lag behind its competitors in some cases. This state of the

multinational bank can be quite clear from its' share in total sales of the five dealers of the city.

This can be shown with the help of a pie-chart. In the next segment of the project is shown the

market share of different banks for the different dealers of the city.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

SBI UBI HDFC ICICI CANARA

INTEREST RATES OF USED CARS

INTEREST RATES OF USEDCARS

Page | 41

FIGURE 3: Auto Hi-Tech:

FIGURE 4: Saini Hyundai:

SBI55%

AXIS22%

ICICI13%

KOTAK10%

MARKET SHARE

AUTO HI-TECH

SBI20%

ICICI30%

HDFC27%

AXIS12%

TATA CAPITAL

11%

MARKET SHARE

SAINI HYUNDAI

Page | 42

FIGURE 5: Bhandari Automobiles:

FIGYRE 6: Topsel Pvt. Ltd:

SBI10%

AXIS15%

HDFC28%

ICICI24%

UBI15%

KOTAK8%

MARKET SHARE

BHANDARI

SBI61%

KOTAK18%

HDFC10%

TFS11%

MARKET SHARE

TOPSEL TOYOTA

Page | 43

FIGURE 7: Dhulichand Motors:

I have asked the various dealers of the city that if they are interested in making better relations

SBI. The replies that I got from them is shown in the following chart with 63% saying "YES"

and the rest "NO".

FIGURE 8

SBI30%

HDFC25%

ICICI13%

INDUSIND22%

CANARA10%

MARKET SHARE

DHULICHAND

MOTORS

YES, 63%

NO, 37%

0%

10%

20%

30%

40%

50%

60%

70%

Page | 44

Whatever the banks be most of the dealers had reports against it. So overall not many are

satisfied with the services of the banks. Hence it is a good opportunity for SBI to capitalize this

situation and analyze the market to make some attractive deals for the customers. This will draw

in a huge amount of revenue and will take SBI way ahead of its' competitors. The reports of the

various dealers are cited below in the pie-chart.

FIGURE 9

64%

15%

7%

14%

EXPERIENCE OF DIFFERENT DEALERS WITH THE

PRESENT BANKERS

AVERAGE EXCELLENT GOOD NOT SATISFACTORY

Page | 45

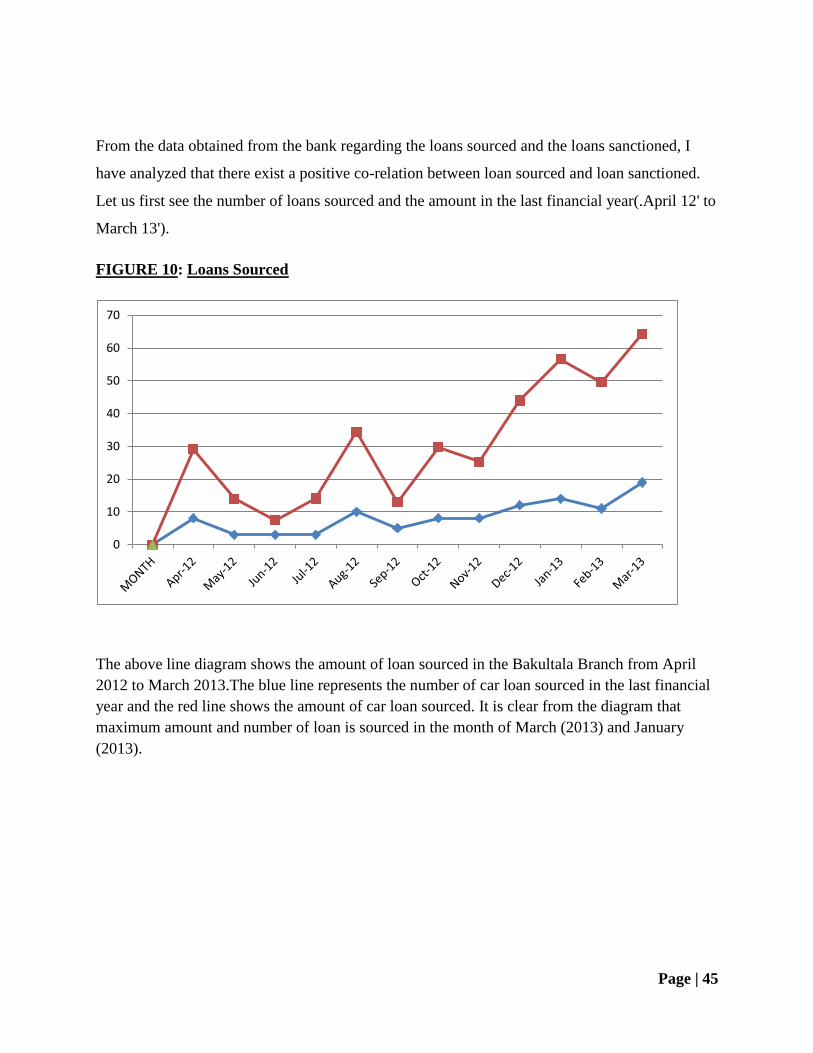

From the data obtained from the bank regarding the loans sourced and the loans sanctioned, I

have analyzed that there exist a positive co-relation between loan sourced and loan sanctioned.

Let us first see the number of loans sourced and the amount in the last financial year(.April 12' to

March 13').

FIGURE 10: Loans Sourced

The above line diagram shows the amount of loan sourced in the Bakultala Branch from April

2012 to March 2013.The blue line represents the number of car loan sourced in the last financial

year and the red line shows the amount of car loan sourced. It is clear from the diagram that

maximum amount and number of loan is sourced in the month of March (2013) and January

(2013).

0

10

20

30

40

50

60

70

Page | 46

Now let us take a look at the number of loans sanctioned and their amounts. Here also we will

see that the amount has been gradually increasing with few sudden decline.

FIGURE 11: Loans Sanctioned

The above line diagram shows the amount of loan sanctioned at the Bakultala branch in the last

financial year that is from April 2012 to March 2013. The blue line shows the number of car

loans sanctioned and the red line shows the amount of car loans sanctioned. It is clear from the

table and the diagram that maximum amount of loan sanctioned is in March and January.

TABLE 18: THE CORRELATION BETWEEN THE AMOUNT OF LOANS SOURCED

AND SANCTIONED

MONTH

SOURCING SANCTION

NUMBER AMOUNT(IN

LACS)

NUMBER AMOUNT (IN

LACS)

APRIL 2012 9 34.74 8 29.12

MAY 2012 4 15.00 3 14.00

JUNE 2012 5 11.25 3 7.50

JULY 2012 3 14.10 3 14.10

0

10

20

30

40

50

60

70

Page | 47

AUGUST 2012 12 46.90 10 34.38

SEPTEMBER 2012 6 18.90 5 12.90

OCTOBER 2012 8 29.73 8 29.73

NOVEMBER 2012 10 31.32 8 25.32

DECEMBER 2012 13 46.00 12 44.00

JANUARY 2013 15 58.55 14 56.55

FEBRUARY 2013 11 49.55 11 49.55

MARCH 2013 21 71.65 19 64.31

SOURCE: SBI (Bakultala Branch)

FIGURE 12: Co-Relation Between Loans Sourced And Loans Sanctioned

The above diagram shows the correlation between the loan sourced and sanction in the last

financial year. It is represented with help of scatter diagram. As we can see there is a positive

correlation between sourcing and sanction of car loan, which is represented by the upward

sloping linear line. This shows that the amount of loans sanctioned is close to the amount of

loans sourced. On an average the amount has increased.

0

10

20

30

40

50

60

70

0 20 40 60 80

SAN

CTI

ON

SOURCING

AMOUNT(IN LACS)

Linear (AMOUNT(IN LACS))

Page | 48

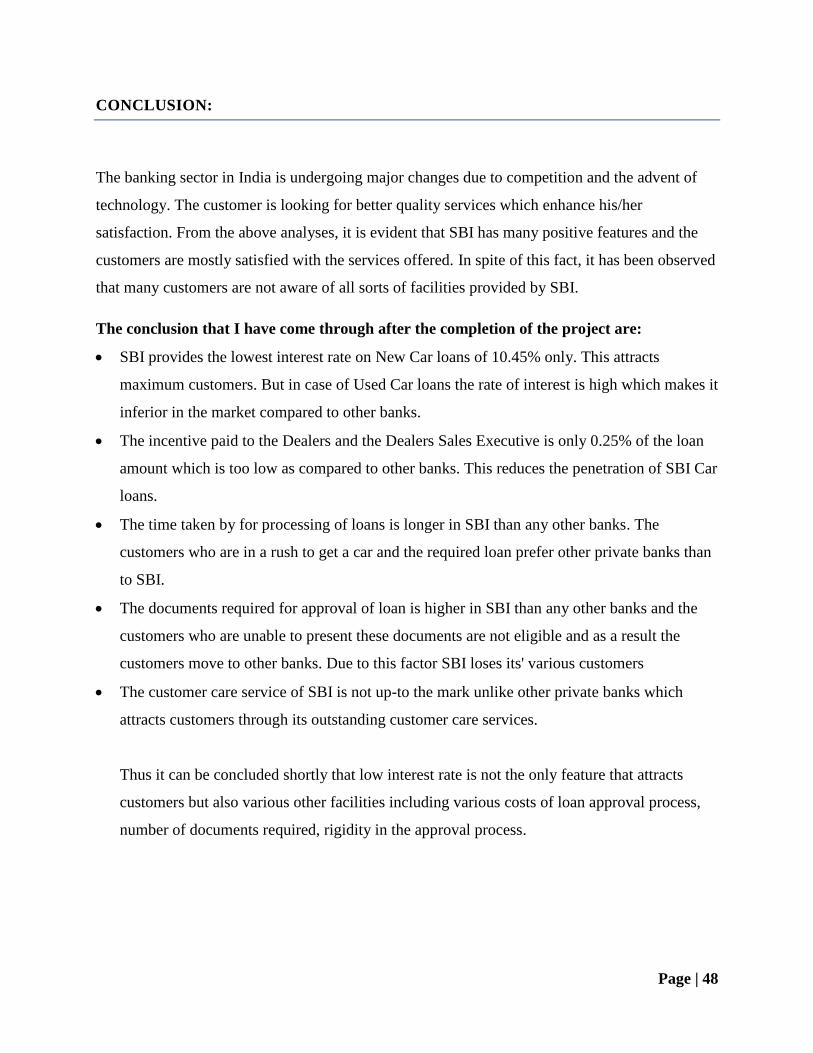

CONCLUSION:

The banking sector in India is undergoing major changes due to competition and the advent of

technology. The customer is looking for better quality services which enhance his/her

satisfaction. From the above analyses, it is evident that SBI has many positive features and the

customers are mostly satisfied with the services offered. In spite of this fact, it has been observed

that many customers are not aware of all sorts of facilities provided by SBI.

The conclusion that I have come through after the completion of the project are:

SBI provides the lowest interest rate on New Car loans of 10.45% only. This attracts

maximum customers. But in case of Used Car loans the rate of interest is high which makes it

inferior in the market compared to other banks.

The incentive paid to the Dealers and the Dealers Sales Executive is only 0.25% of the loan

amount which is too low as compared to other banks. This reduces the penetration of SBI Car

loans.

The time taken by for processing of loans is longer in SBI than any other banks. The

customers who are in a rush to get a car and the required loan prefer other private banks than

to SBI.

The documents required for approval of loan is higher in SBI than any other banks and the

customers who are unable to present these documents are not eligible and as a result the

customers move to other banks. Due to this factor SBI loses its' various customers

The customer care service of SBI is not up-to the mark unlike other private banks which

attracts customers through its outstanding customer care services.

Thus it can be concluded shortly that low interest rate is not the only feature that attracts

customers but also various other facilities including various costs of loan approval process,

number of documents required, rigidity in the approval process.

Page | 49

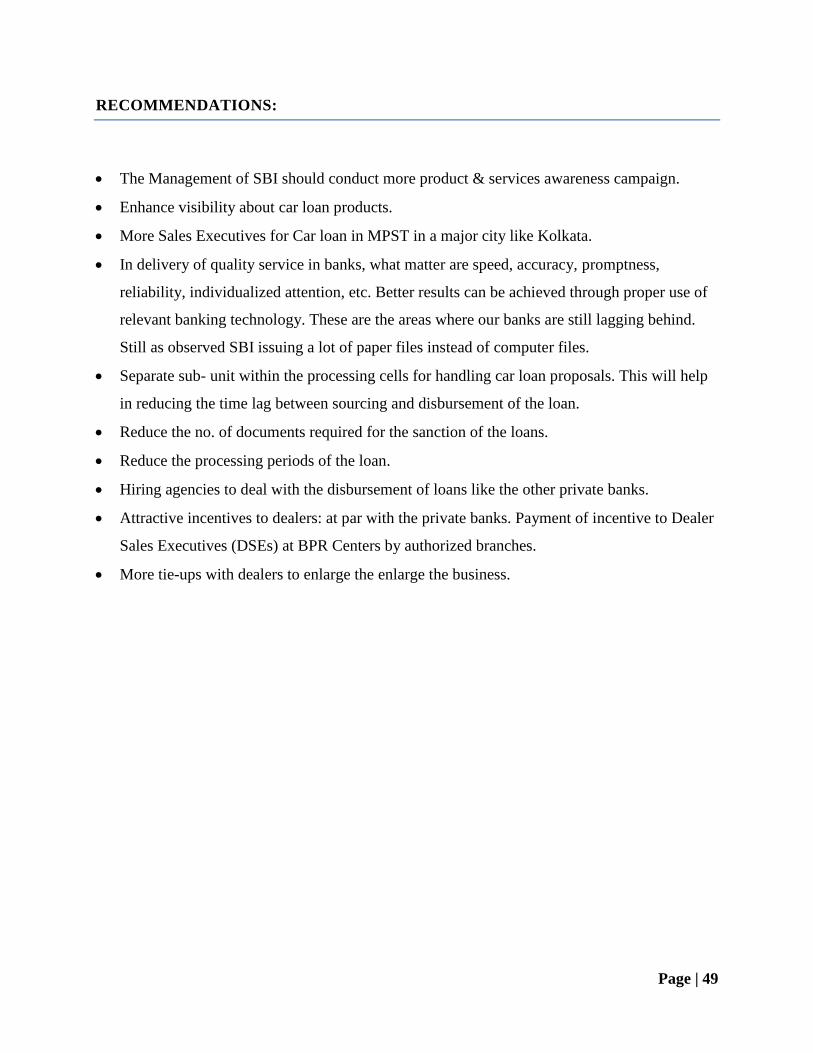

RECOMMENDATIONS:

The Management of SBI should conduct more product & services awareness campaign.

Enhance visibility about car loan products.

More Sales Executives for Car loan in MPST in a major city like Kolkata.

In delivery of quality service in banks, what matter are speed, accuracy, promptness,

reliability, individualized attention, etc. Better results can be achieved through proper use of

relevant banking technology. These are the areas where our banks are still lagging behind.

Still as observed SBI issuing a lot of paper files instead of computer files.

Separate sub- unit within the processing cells for handling car loan proposals. This will help

in reducing the time lag between sourcing and disbursement of the loan.

Reduce the no. of documents required for the sanction of the loans.

Reduce the processing periods of the loan.

Hiring agencies to deal with the disbursement of loans like the other private banks.

Attractive incentives to dealers: at par with the private banks. Payment of incentive to Dealer

Sales Executives (DSEs) at BPR Centers by authorized branches.

More tie-ups with dealers to enlarge the enlarge the business.

Page | 50

BIBLIOGRAPHY

This project was completed with the help of the following journals and websites:

ECONOMIC TIMES, June 2013.

State Bank of India Times

www.google.com

www.icici.co.in

www.axis.co.in

www.hdfc.co.in

www.rupeetimes.com

![EY - Loan portfolio transaction markets this background, this edition of EY’s Loan Portfolio Transaction Markets considers the UK and Irish loan portfolio ljYfkY[lagf eYjc]lk Yf\](https://static.fdocuments.us/doc/165x107/5b1e5c467f8b9a397f8c05ea/ey-loan-portfolio-transaction-this-background-this-edition-of-eys-loan-portfolio.jpg)