ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014 July 10, 2014 © Economic Laws Practice 2014.

21

ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014 July 10, 2014 © Economic Laws Practice 2014

-

Upload

sybil-parks -

Category

Documents

-

view

220 -

download

3

Transcript of ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014 July 10, 2014 © Economic Laws Practice 2014.

ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014

July 10, 2014

© Economic Laws Practice 2014

2© Economic Laws Practice 2014

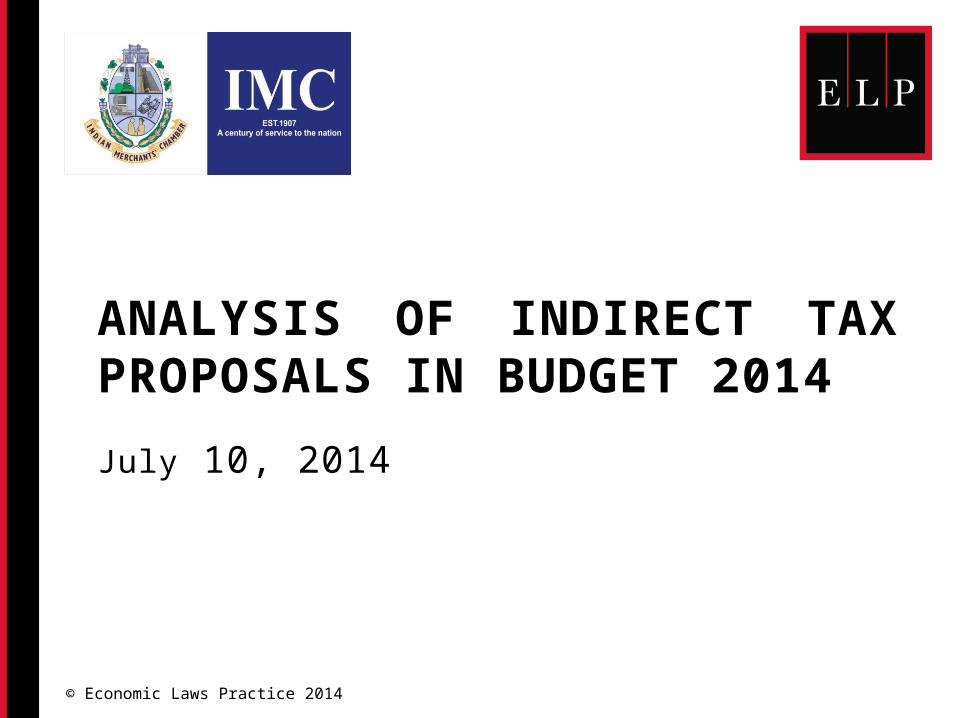

Key issues Pre-Budget Definitive path and time lines for GST

Retrospective amendments

Adoption of DTC

Dealing with culture of Tax Terrorism

Measures to catalyse the manufacturing sector

Measures to enthuse domestic and foreign investment

Curtailing the exponential growth of tax litigation

INDIRECT TAXES

3

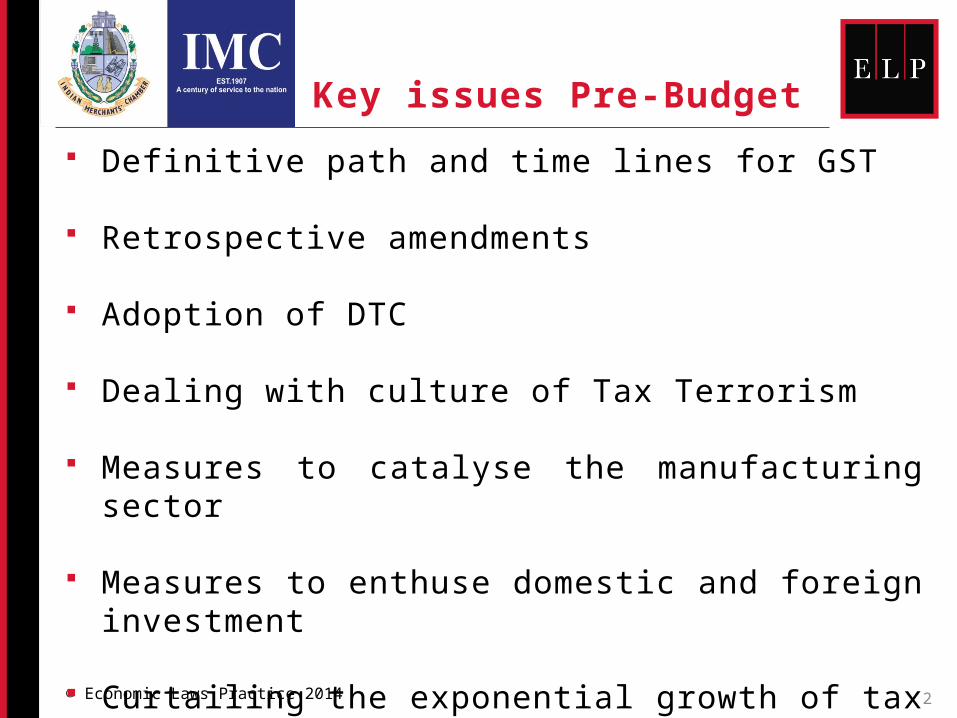

Service tax –Negative List

4© Economic Laws Practice 2014

Negative list to exclude “online and mobile advertising” Earlier list covered selling of space or time slot for advertisement

other than advertisement broadcast by radio or television New levy extends to advertisements in internet websites, out-of-

home media, on fi lm screen in theatres, bill boards, conveyances, buildings, cell phones, Automated Teller Machines, tickets, commercial publications, aerial advertising, etc.

Sale of space for advertisements in print media, would continue to be in the negative list and hence remain excluded from service tax

Negative list modified to exclude Radio Taxis Abetment scheme similar to rent a cab made available to radio taxis Definition of ‘Radio taxi’ introduced to include radio cab having two

way radio communication and GPS/GPRS enabled tracking

5© Economic Laws Practice 2014

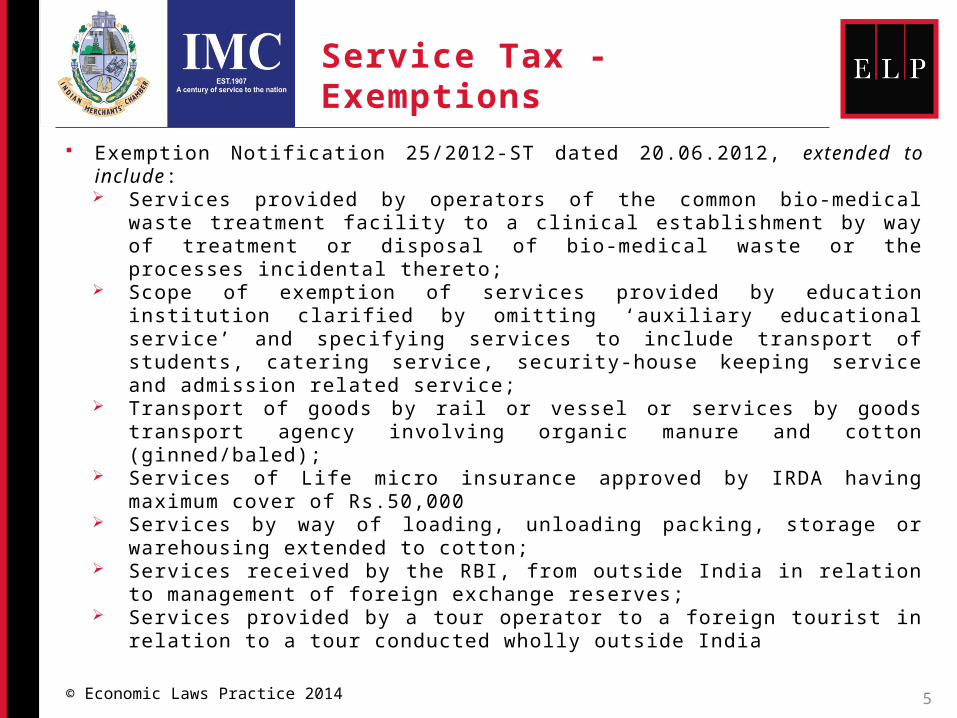

Service Tax - Exemptions Exemption Notifi cation 25/2012-ST dated 20.06.2012, extended to include:

Services provided by operators of the common bio-medical waste treatment facility to a clinical establishment by way of treatment or disposal of bio-medical waste or the processes incidental thereto;

Scope of exemption of services provided by education institution clarified by omitti ng ‘auxiliary educational service’ and specifying services to include transport of students, catering service, security-house keeping service and admission related service;

Transport of goods by rail or vessel or services by goods transport agency involving organic manure and cott on (ginned/baled);

Services of Life micro insurance approved by IRDA having maximum cover of Rs.50,000

Services by way of loading, unloading packing, storage or warehousing extended to cott on;

Services received by the RBI, from outside India in relation to management of foreign exchange reserves;

Services provided by a tour operator to a foreign tourist in relation to a tour conducted wholly outside India

6© Economic Laws Practice 2014

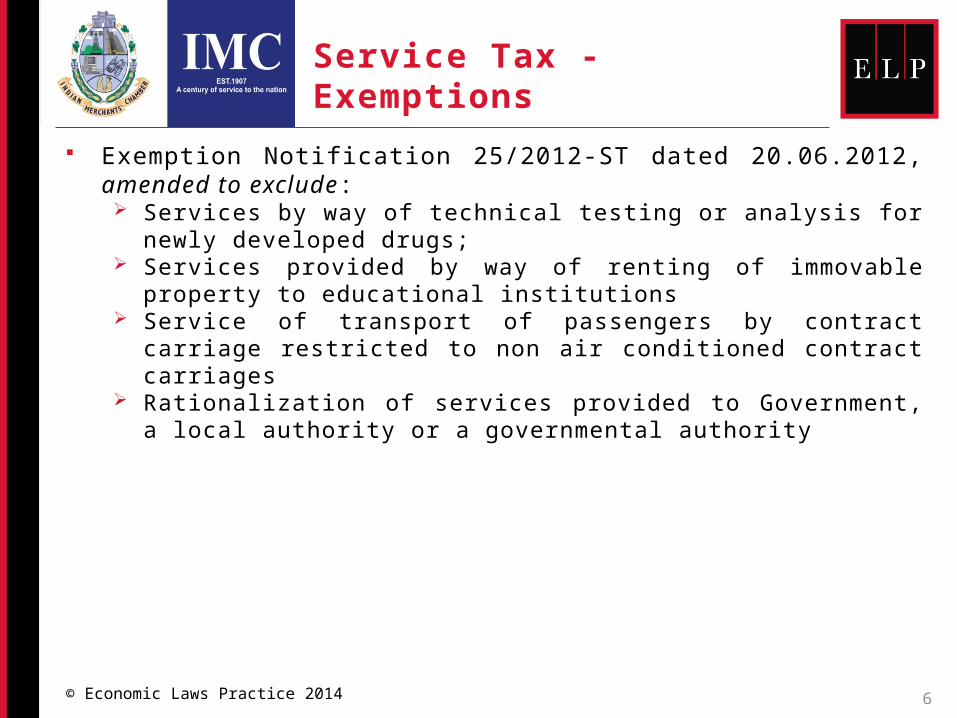

Service Tax - Exemptions Exemption Notifi cation 25/2012-ST dated 20.06.2012, amended to exclude:

Services by way of technical testi ng or analysis for newly developed drugs; Services provided by way of renti ng of immovable property to educati onal

insti tuti ons Service of transport of passengers by contract carriage restricted to non

air conditi oned contract carriages Rati onalizati on of services provided to Government, a local authority or a

governmental authority

7© Economic Laws Practice 2014

Service Tax – Other Legislati ve Changes

Interest rates for delay beyond six months increased slab wise (effective October 2014)

Sr. No Period of Delay Rate of Simple Interest

1 Upto 6 months 18%

2 > 6 months – 1 year 18% - 1st 6 months24% - > 6 months

3 > 1 year 18% - 1st 6 months24% - 6 months - 1 year30% - > 1 year

8© Economic Laws Practice 2014

Service Tax Rules

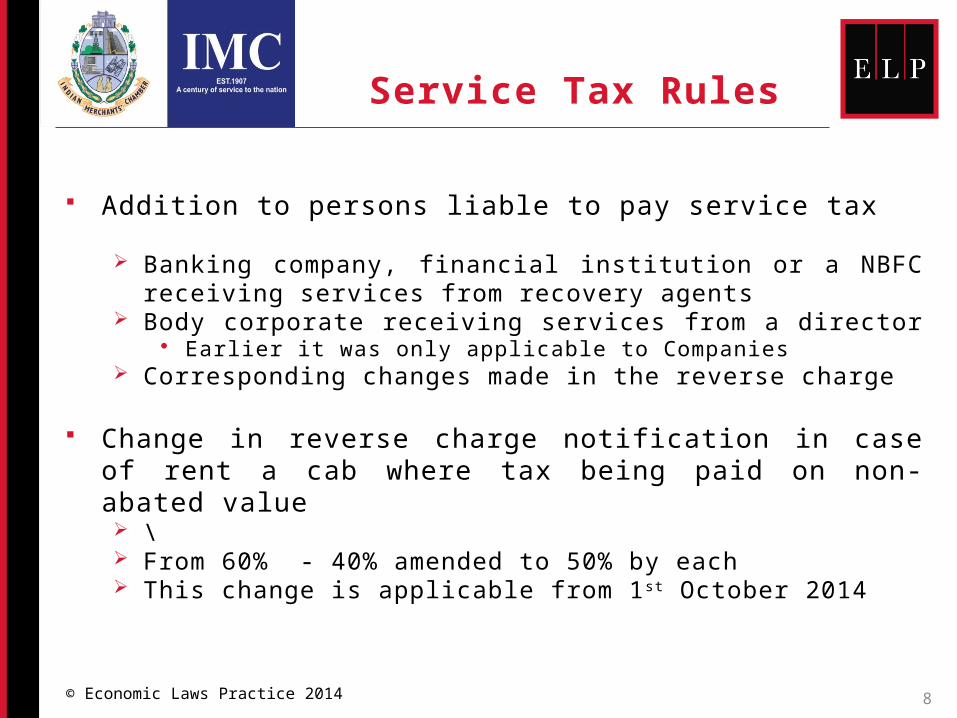

Addition to persons liable to pay service tax

Banking company, fi nancial institution or a NBFC receiving services from recovery agents

Body corporate receiving services from a director Earlier it was only applicable to Companies

Corresponding changes made in the reverse charge

Change in reverse charge notification in case of rent a cab where tax being paid on non-abated value \ From 60% - 40% amended to 50% by each This change is applicable from 1 st October 2014

9© Economic Laws Practice 2014

Point of Taxation Rules

In respect of cases where Service tax is to be paid by the receiver, the point of taxation will be

the date of payment, or the day aft er 3 months from the date of invoice, whichever is earlier

The above change is effective for invoices issued aft er 1 st October 2014.

For invoices before 1 st October but no payments made (interim period) new Rule inserted (Rule 10)

Invoice issued before 1 st October 2014 but payments not made: Situati on 1 – if payment made within 6 months, date of payment Situati on 2 – if payment is not made within 6 months, then accrual basis

10© Economic Laws Practice 2014

Place of Provision of Services Rules

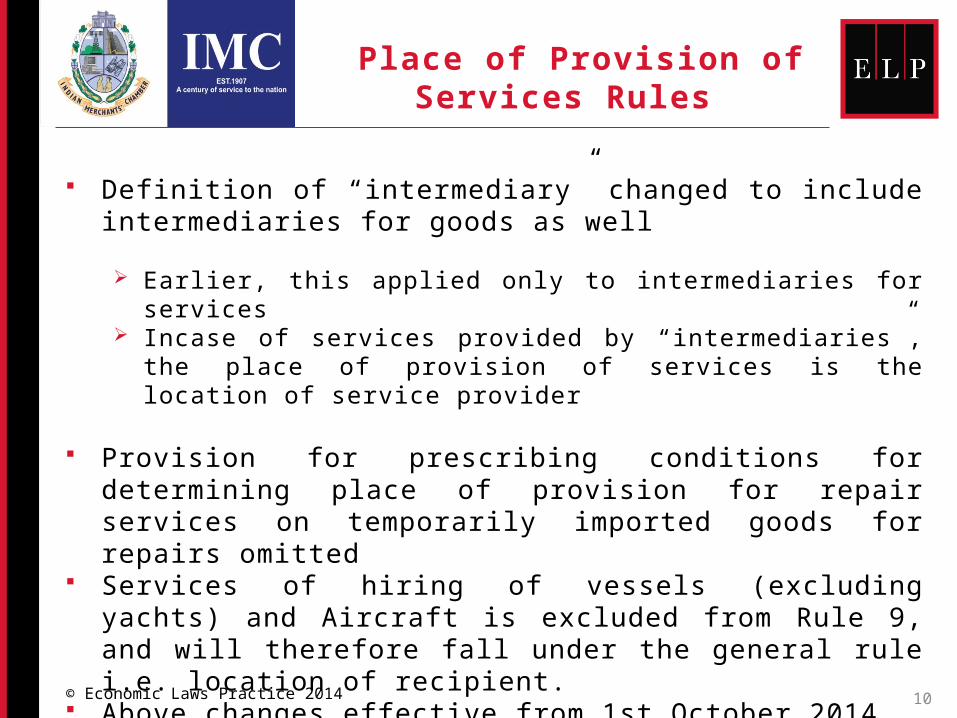

Definition of “intermediary” changed to include intermediaries for goods as well

Earlier, this applied only to intermediaries for services Incase of services provided by “intermediaries”, the place of provision

of services is the location of service provider

Provision for prescribing conditions for determining place of provision for repair services on temporarily imported goods for repairs omitted

Services of hiring of vessels (excluding yachts) and Aircraft is excluded from Rule 9, and will therefore fall under the general rule i.e. location of recipient.

Above changes effective from 1st October 2014

11© Economic Laws Practice 2014

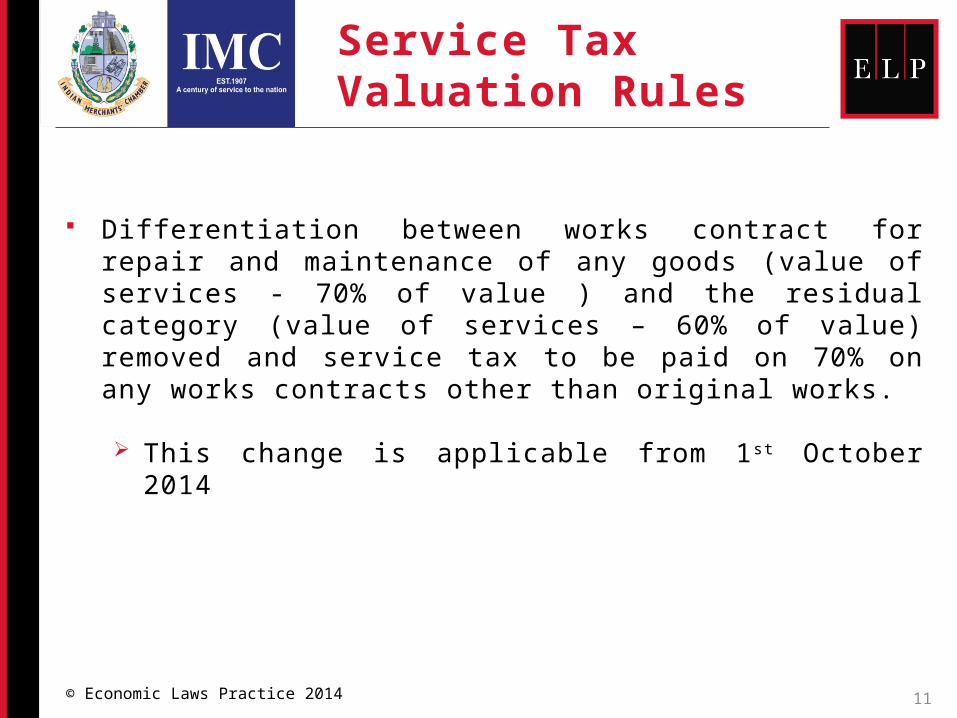

Service Tax Valuation Rules

Differentiation between works contract for repair and maintenance of any goods (value of services - 70% of value ) and the residual category (value of services – 60% of value) removed and service tax to be paid on 70% on any works contracts other than original works.

This change is applicable from 1 st October 2014

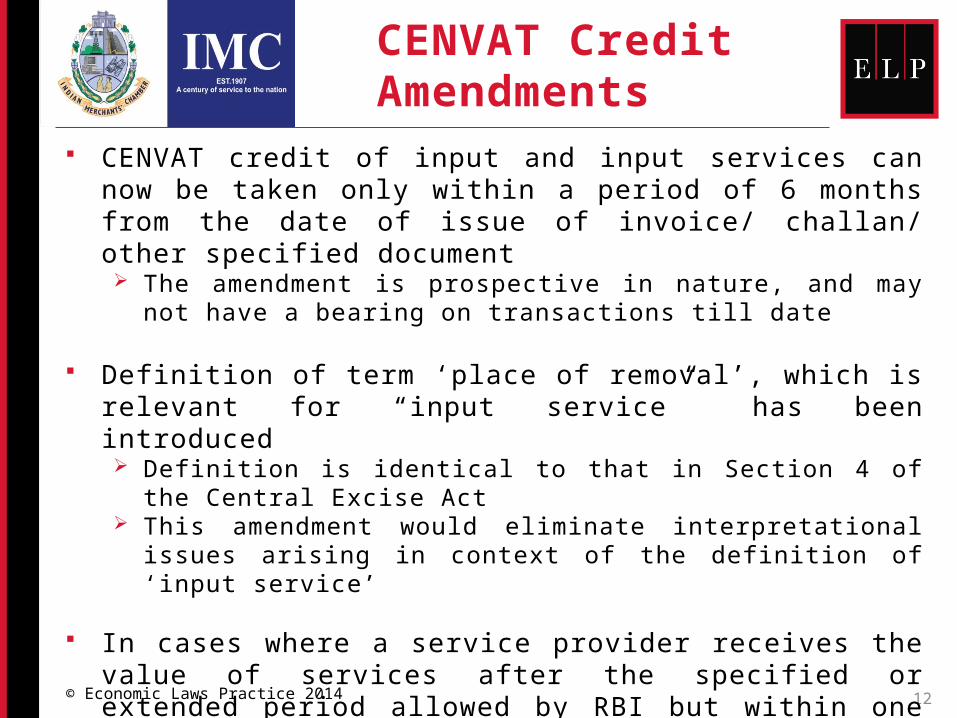

CENVAT Credit Amendments

12© Economic Laws Practice 2014

CENVAT credit of input and input services can now be taken only within a period of 6 months from the date of issue of invoice/ challan/ other specified document The amendment is prospective in nature, and may not have a bearing

on transactions ti ll date

Definition of term ‘place of removal’, which is relevant for “input service” has been introduced Definition is identical to that in Section 4 of the Central Excise Act This amendment would eliminate interpretational issues arising in

context of the defi nition of ‘input service’ In cases where a service provider receives the value of services

aft er the specified or extended period allowed by RBI but within one year from such period shall be entitle to credit previously paid in terms of Rule 6

CENVAT Credit Amendments

13© Economic Laws Practice 2014

CENVAT credit in respect of input services received from vendors where service tax is payable under reverse charge mechanism has been given differential treatment as under:

A Large Taxpayer Unit is disallowed from transferring CENVAT credit from one of its manufacturing unit to another prospectively This amendment is restricted to credit arising in relation to a

manufacturing unit and not premises engaged in rendition of service.

Scenario ImpactIn cases where 100% of the service tax liability is to be paid by the service recipient

CENVAT credit can be availed after payment of Service tax by the service recipient, without payment of value of service

In case the service tax liability is partially to be paid by the service recipient

CENVAT credit can be availed after payment of value of services and Service tax by the service recipient.

14© Economic Laws Practice 2014

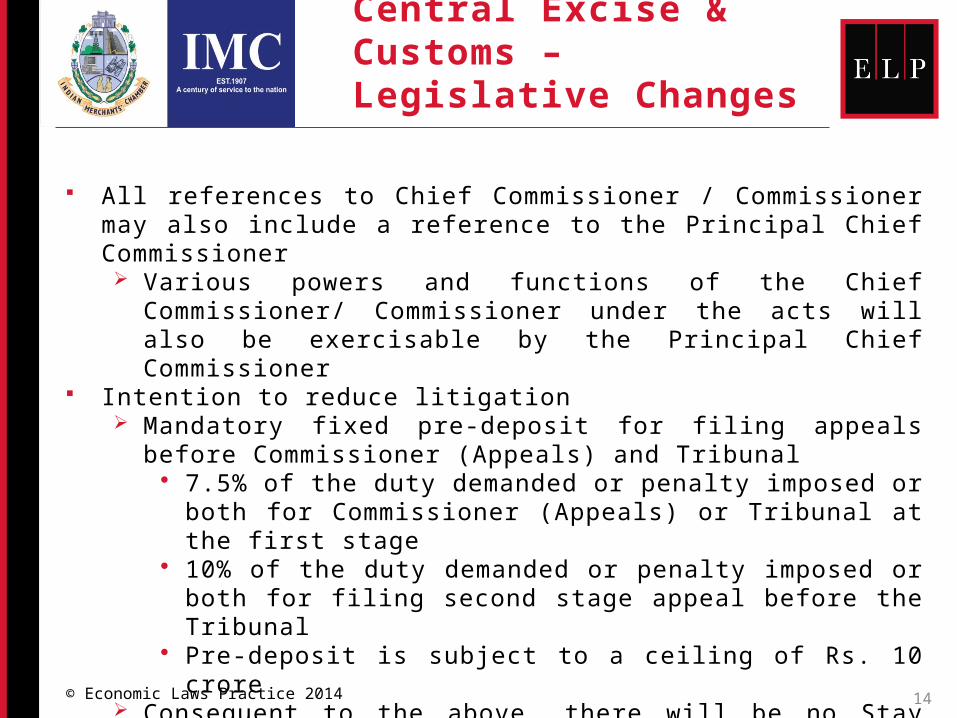

Central Excise & Customs – Legislati ve Changes

All references to Chief Commissioner / Commissioner may also include a reference to the Principal Chief Commissioner Various powers and functions of the Chief Commissioner/

Commissioner under the acts will also be exercisable by the Principal Chief Commissioner

Intention to reduce litigation Mandatory fi xed pre-deposit for fi ling appeals before Commissioner

(Appeals) and Tribunal 7.5% of the duty demanded or penalty imposed or both for

Commissioner (Appeals) or Tribunal at the fi rst stage 10% of the duty demanded or penalty imposed or both for fi ling

second stage appeal before the Tribunal Pre-deposit is subject to a ceiling of Rs. 10 crore

Consequent to the above, there will be no Stay hearing All issues on extension of stay and consequent recoveries go away

15© Economic Laws Practice 2014

Central Excise & Customs – Legislative Changes

Commissioner (Appeals) permitt ed to take into consideration a particular order cited as a precedent decision having not been appealed against for reasons of low amount

Expansion in scope of cases which can be taken up by Sett lement Commission:

Customs: Cases where a Bill of Export, Baggage Declaration, Label or Declaration accompanying the goods effected through Post or Courier have been fi led

Excise: where the assesse has not fi led a return under Excise Concealment of particulars of duty liability from the Customs/ Excise

offi cer (and not from the Sett lement Commission) is a bar on making a subsequent application to the Sett lement Commission

Discretionary powers of the Tribunal to refuse admission of appeal increased from Rs.50,000 to Rs.2 lakh.

Committ ee in relation to fi ling of Department appeals before Tribunal can be constituted by an order of the CBEC, and would not require a notifi cation published in the Offi cial Gazett e

Scheme of Advance Ruling extended to resident private limited companies

16© Economic Laws Practice 2014

Central Excise – Other Changes

Key measure for sharing of information Provision to require submission of a return/ information to an

authority or agency, including by assessees, Income Tax Authorities, State Electricity Boards, VAT or Sales Tax Authorities, Registrar of Companies etc in order to identify tax evaders or recover confi rmed dues

Penalty may be imposed on failure to provide the information Clarification under Section 35L that that determination of disputes

relating to taxability or excisability of goods is covered under the term “determination of any question having a relation to rate of duty” The proposed amendment is as per the line of decisions including

Commissioner of Service Tax vs. Ernst And Young Pvt Ltd [2014-TIOL-263-HC-DEL-ST] and Commissioner of Service Tax vs. Delhi Gymkhana Club Ltd. [2009 (16) STR 129]

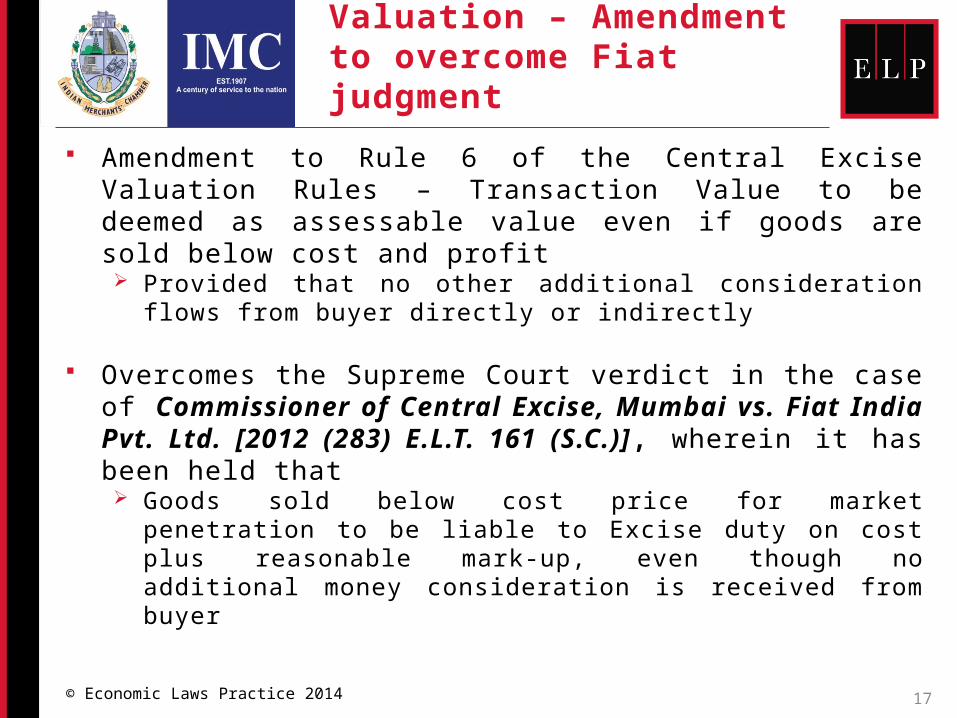

Central Excise Valuati on – Amendment to overcome Fiat judgment

17© Economic Laws Practice 2014

Amendment to Rule 6 of the Central Excise Valuation Rules – Transaction Value to be deemed as assessable value even if goods are sold below cost and profit Provided that no other additional consideration flows from buyer

directly or indirectly

Overcomes the Supreme Court verdict in the case of Commissioner of Central Excise, Mumbai vs. Fiat India Pvt. Ltd. [2012 (283) E.L.T. 161 (S.C.)], wherein it has been held that Goods sold below cost price for market penetration to be liable to

Excise duty on cost plus reasonable mark-up, even though no additional money consideration is received from buyer

18© Economic Laws Practice 2014

ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014

ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014ANALYSIS OF INDIRECT TAX PROPOSALS IN BUDGET 2014

Goods and services tax (GST)

GST

19© Economic Laws Practice 2014

GST part of the manifesto of the newly elected Government and flagged as priority; however no concrete path paved in Budget

FM expressed hope to find a solution to GST in a year and approve legislative scheme for its introduction GST to result into higher tax collection for Centre and States Ease in Tax administration and avoidance of harassment to

business Promise to crack a fair deal with States

Following areas identified as key to GST implementation Compensation for phasing out CST Outlining the State tax jurisdiction

While Economic Survey 2013-14 indicated possibility of phased introduction by way of CenGST, no mention in Budget

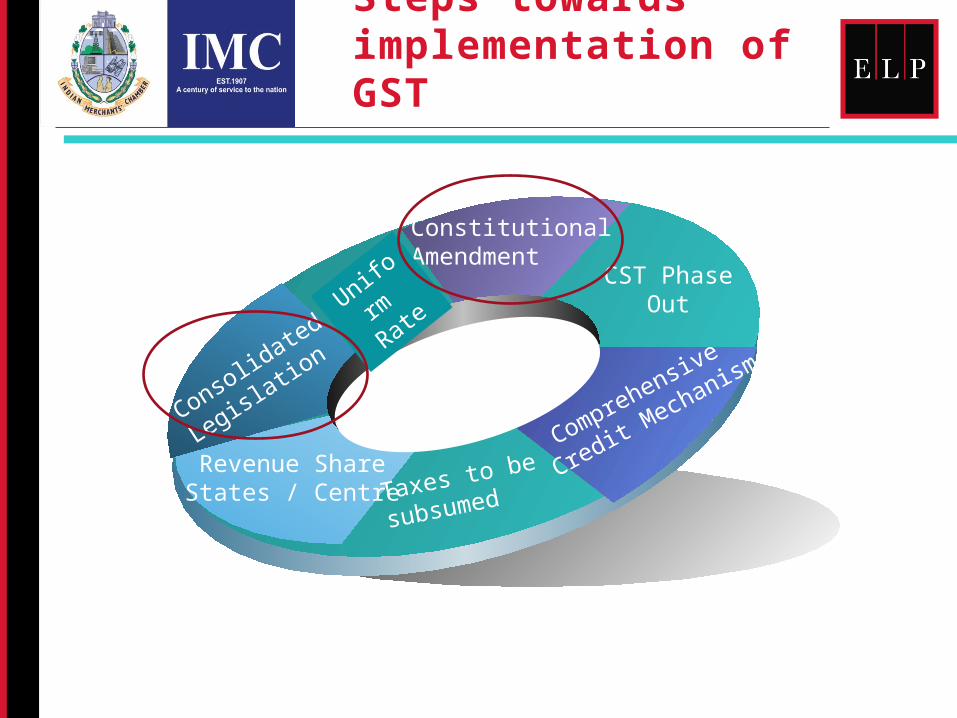

CST Phase Out

Revenue ShareStates / Centre

Consolidated

Legislation

Taxes to be

subsumed

Constitutional Amendment

Comprehensive

Credit Mechanism

Uniform

Rate

Steps towards implementation of GST

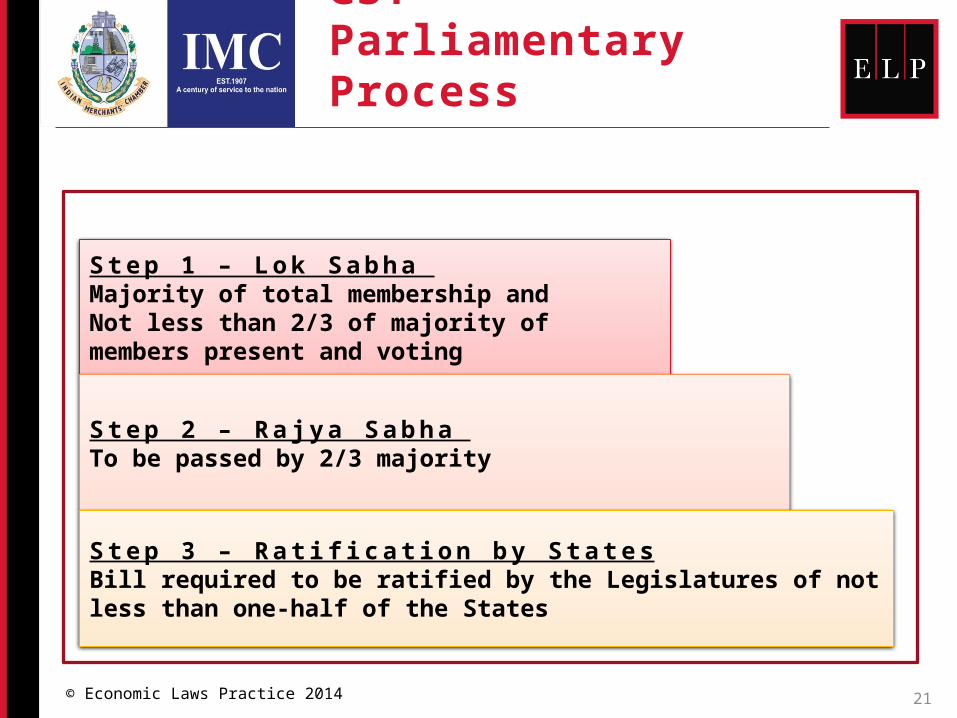

GST – Parliamentary Process

21© Economic Laws Practice 2014

S t e p 1 – L o k S a b h a Majority of total membership and Not less than 2/3 of majority of members present and voting

S t e p 2 – R a j y a S a b h a To be passed by 2/3 majority

S t e p 3 – R a ti fi c a ti o n b y S t a t e sBill required to be ratified by the Legislatures of not less than one-half of the States