Analysing the link between CEO remuneration and performance

59

1 The University of Nottingham Analysing the link between CEO remuneration and performance: A stochastic frontier approach Ahmed Mir Finance and Investment MSc

Transcript of Analysing the link between CEO remuneration and performance

1

The University of Nottingham

Analysing the link between CEO remuneration and performance: A

stochastic frontier approach

Ahmed Mir

Finance and Investment MSc

2

Abstract1:

This study utilises an unbalanced panel data set of 41 U.K building societies from 1998 to

2011, examining the relationship between cost efficiency and CEO salary. Using maximum-

likelihood I estimate the parameters of a stochastic cost frontier under a transcendental

logarithmic functional form. The stochastic frontier analysis finds that on average building

societies in the sample operate with a mean cost inefficiency of 18%. The latter stages of

the investigation involve a regression analysis, which estimates the correlation between

the cost efficiency of a smaller sample of building societies and CEO salary. Ultimately, the

evidence presented in this paper finds that efficiency does not have a statistically

significant impact on CEO remuneration but firm size has a substantial influence on

executive pay levels.

1 I would like to thank Dev Vencappa, my supervisor for this project, for his support and

guidance; especially regarding the econometric analysis. In addition, I would like to thank

the University of Nottingham for providing the opportunity to complete the degree of

Finance and Investment MSc

3

Contents Page

1. Introduction .................................................................................................................................. 4

2. Review of the Literature ............................................................................................................... 6

2.1 Data Envelopment Analysis and Stochastic Frontier Analysis .................................................... 6

2.2 Executive Compensation ............................................................................................................. 8

2.3 Previous Studies Exploring Efficiency: Building Societies .......................................................... 11

2.4 Other Mutual Organisations ..................................................................................................... 17

2.5 Banks ......................................................................................................................................... 18

2.6 Determinants of Executive Compensation ................................................................................ 19

2.7 Remarks Regarding the Previous Litreature ............................................................................. 22

3. Methodology and Data ............................................................................................................... 23

3.1 Stochastic Frontier Modelling ................................................................................................... 24

3.2 The Cost Function ...................................................................................................................... 25

3.3 Maximum-Likelihood Estimation and the Half Normal Model ................................................. 26

3.4 The Stochastic Cost Frontier ...................................................................................................... 30

3.5 Input and Output Choice ........................................................................................................... 31

3.6 Cost Function Formulation ........................................................................................................ 34

3.7 CEO Compensation and Efficiency ............................................................................................ 35

4. Empirical Results ......................................................................................................................... 39

4.1 Efficiency and CEO Remuneration ............................................................................................. 44

4.2 Discussion .................................................................................................................................. 46

5. Concluding Remarks .................................................................................................................... 47

7. Appendix ......................................................................................................................................... 50

8. Bibliography ................................................................................................................................ 54

4

1. Introduction

For decades economists have queried the implications of inefficiency on profitability.

Competitive pressure across the financial services industry hand in hand with new and

more stringent economic regulation has reinforced the strategic requirement of efficiency.

Early on, Demsetz (1973) defined the relationship between efficiency and performance,

describing that more productively efficient firms hold a competitive advantage over their

rivals, often resulting in a higher level of profitability. More recently, academia has applied

various models to estimate efficiency on both a firm and industry level. However, the

majority of this research has still failed to analyse mutual firms such as building societies.

Conversely, the diverse level of research examining the compensation top level executives

has publicised the sometimes absurdly high pay packets of executive management. The

debate has been further amplified by economic crises such as the financial crisis of the last

decade and the now long running Eurozone crisis; spotlighting inflated director pay. For

years policymakers, practitioners and academics alike have questioned if the increasing

disparity between executive remuneration and the average wage are in line with owner

interests. Over the years theorists have attempted to explain the phenomenon of

executive remuneration, where classical economists favour the theory of profit

maximisation and on the other hand managerialists support the theory of corporate

growth (Ciscel & Carrol, 1980). Given that chief executive posts on average require high

levels of experience, and with many chief executive officers (CEOs) holding a professional

qualification to supplement their experience it is understandable that they are

compensated beyond the level of an average employee. However, current evidence

suggests that a CEOs in the FTSE 100 index (UK) can expect on average to receive a

5

remuneration package of in excess £4 million in 2010; a growth of over 400 % since 1998

(The Economist, 2012). The implications of such exorbitant pay packages are not merely a

moral issue but can be considered an economic problem, with high levels of compensation

becoming common place it is important to examine if pay is at all linked to firm

performance. Although, the debate regarding the pay to performance relationship was

popularised over two decades ago, research tackling the relationship between efficiency

and executive compensation is relatively limited to banks and other large public limited

companies.

This paper seeks to add to the current literature by providing an in depth focus on the

relationship between cost efficiency and CEO compensation in the UK building society

sector. By using stochastic frontier analysis this paper will evaluate the cost efficiency of UK

building societies; employing a pooled unbalanced panel data set of up to 13 years on a

sample of 41 building societies; originating from bankscope data. Panel data will provide in

depth evidence in regards to performance, permitting for the tracking of efficiency across

different firms in different years; unlike cross sectional data which only provides a

snapshot (Kumbhakar and Lovell, 2000).

This paper is structured as follows. The next section reviews relevant literature, followed

by a section explaining the methodology used in this paper and discussing data

requirements. Thereafter the paper discusses the estimated cost efficiency scores found

by the econometric analysis and ultimately discussing relationship between cost efficiency

and CEO salary.

6

2. Review of the Literature

Modern microeconomic theory treats producers as successful optimisers, producing the

maximum level of outputs from a given set of inputs. However, it is important to note that

many producers may attempt to minimise input to output ratios, but most do not succeed

in being completely efficient (Kumbhakar and Lovell, 2000). To understand inefficiency

and the theory of production there has been an inflow of methods analysing the

relationship between the inputs and outputs of a firm.

Academia has analysed the subject of executive compensation since the early 1990s with

Jensen and Murphy (1990a) providing one of the most influential studies at the time in

regard to CEO pay. Much of this work has focused on how total CEO compensation is

correlated to firm performance. There are various different proxies for performance,

financial ratios for example; such as return on assets, return on equity and net interest

margin. On the other hand, empirical applications to frontier techniques analysing the

efficiency of firms can also be considered as performance measurement (Baten and Kamil,

2010).

2.1 Data Envelopment Analysis and Stochastic Frontier Analysis

The most popular methods used in efficiency analysis today are extensions of the work

carried out by Farrell (1957), where his ground-breaking research employed linear

programming methods generating a measure for productive efficiency, in addition to

providing a definition for a production frontier. The work by Farrell (1957) was the

foundation upon which Charnes et al (1978) formed the non-parametric technique, Data

Envelopment Analysis (DEA). This technique uses the ratio of inputs to outputs to plot an

7

efficient frontier, which illustrates the most efficient allocation of x inputs to produce y

outputs; where the closer an observation is to the frontier the more efficient it is.

However, DEA fails to observe random events which can impact on the efficiency of a firm,

for example insufficient rain in the right season can reduce a paddy farmers harvest; this is

out of the producers control and not as a result of inefficiency. However, DEA does not

recognise the difference between random noise and inefficiency as it is a deterministic

frontier method and as such any deviation from the efficient frontier is considered as

inefficiency.

Aigner et al, 1977; Meeusen et al 1977 proposed an alternative technique, Stochastic

Frontier Analysis (SFA). This method has the ability to differentiate random errors from

inefficiency is now widely accepted as the benchmarked econometric alternative. It

consists of the estimation of a stochastic frontier, where output is bound by a function of

known inputs, inefficiency and a random error; this is usually in order to plot a cost or

production function (Battese & Coelli, 1995). Similarly to DEA the objective is for firms to

reside as close to or on the given frontier as possible. Although, whilst SFA can separate

genuine inefficiency from random noise DEA has the advantage of requiring no functional

form to estimate the frontier, mitigating the possibility that a functional form may be

unwarranted or too simple. However, the deterministic nature of DEA consequently results

in the failure to allow for statistical inference. Nonetheless, DEA is still a popular method

of efficiency measurement in management science (Kumbhakar and Lovell, 2000).

Frontier functions estimate the maximum possible output given a set of inputs, or the

minimum cost of a set out outputs; usually to estimate production or cost functions. From

the perspective of producers this is crucial to estimate how much output can be produced

8

given an amount of inputs; where production functions mathematically define this

relationship in order to specify the various technical possibilities which are open to

producers (Heathfield & Wibe, 1987). It is recognised that efficiency measures which

employ frontier techniques have advantages over the alternative of accounting ratios

(Beccalli et al, 2006). For example, financial ratios do not consider inputs and the

combination of outputs (Berger & Humphrey, 1992). In addition, a frontier method

provides a concise and clear numerical score complete with ranking (Berger & Humphrey,

1997). Nonetheless, these topics will be discussed in further detail in the methodology

section of this paper.

2.2 Executive Compensation

Academia has attempted to explain the concepts behind CEO remuneration by proposing

different theories and hypothesising various assumptions. This sub-section reviews some

of the many theories documented in the wider literature. These include neo-classical

theory of the firm, the principal agent model, managerial power theory, human capital

theory, tournament theory, social comparison models and information processing theory.

Although, in respect to performance the majority of research focuses on the pioneering

work of Jensen and Meckling (1976) which aggregated the issues identified by previous

researchers to suggest their theory of the firm by defining agency theory; also known as

the principal agent model.

According to neo-classical economic theory the primary objective of a firm is to profit

maximise, consequently maximising the return for the owners. However, due to

constraints in corporate governance often managers maximise their own utility rather than

that of owners (Williamson, 1986). In contrast, work by Festinger (1954) describes a

9

theory of social comparison to explain the determination of executive pay. Where pay for

top level management is benchmarked to compensation levels for comparable positions at

other firms. This prospective utilises consistent peer group comparisons to ensure that pay

is kept in line with competitors. O'Rielly III et al (1988) argue that such relative comparison

is possible as some members of remuneration committees for one company may be

corporate executives of other companies. Their results are consistent with social

comparison theory as their research concludes that CEO compensation is positively related

to the pay of the members of the remuneration committee.

Another hypothesis is the corporate growth theory, which suggests that the size of the

company has a larger impact on executive salary than the profitability of that company.

Cosh (1975) supports this suggestion, documenting that size has a larger impact than

profitability for determining pay. In contrast, Meek and Whittington (1975) argue that

profitability and growth are equal determinants of executive remuneration. Conversely,

the human capital model (Becker, 1975) suggests that executive compensation is

determined by personal factors such as qualifications, age, experience and training. Under

this theory any differentials in pay between executives is down to observed differences in

their personal attributes which impact upon their ability (Shiwakoti et al, 2004).

Tournament theory proposed by Lazear and Rosen in 1981, suggests that the pay structure

of a CEO is not based not upon firm or individual performance but by the position of the

executive in the firms’ hierarchy. Suggesting that the compensation a CEO receives may

surpass the pay his marginal product warrants but still be considered economically

efficient (Main et al, 1993). Such a theory works on the premise that those lower down the

ladder command a lower wage than their marginal product of labour, this disparity in

10

salary provides incentives for employees to compete for promotion to positions of higher

responsibility such as chief executive; which are seen as prizes for long term commitment

(Lazear and Rosen, 1981).

The last but probably most researched theory is the agency problem. The foundations of

agency theory are defined by a simple relationship between two parties, where one party

(the principal) delegates tasks to another party (the agent), who then carries out these

tasks. The principal agent model attempts to resolve conflicts of interest between these

two parties in terms of employment contracts (Jensen and Meckling, 1976). It seeks to

understand how to create a partnership between the two parties to ensure that the

objectives set by the principal are met by offering the agent incentives to ensure that the

agents personal objectives do not hinder the goals of the principal. For example, in public

limited companies it is a common problem that managerial objectives may vary from

shareholder objectives, creating a conflict of interest. The influential paper by Jensen and

Meckling (1976) discusses how ownership and control are separated; an issue which

underpins the classical agency model. In the words of Shleifer and Vishny (1997) managers

may use their power in order to personally benefit themselves, for example managers may

wish to build their own empire (a common topic in M&A) or follow entrenchment

strategies which do not maximise shareholder wealth. In order to ensure this is not the

case, the principal is required to set incentives which ensure the agent does not divert to

peruse goals which maximise his own utility rather than that of the owners. This is in the

form of a contract, designed to optimally maximise the combined utility of both the agent

and principal; this is by ensuring that the maximisation of shareholder objectives coincide

with incentives that will maximise the agents’ utility. Whatever the case, it is a

11

requirement that the agent is monitored beyond simply reviewing performance targets,

but by setting restrictions on executable actions by the agent (Jensen and Meckling, 1976).

2.3 Previous Studies Exploring Efficiency: Building Societies

As mentioned earlier, the concept of efficiency measurement can be attributed to Farrell

(1957) where his non parametric approach defined the estimation of productive efficiency

as the calculation of the maximum amount of outputs a firm can produce from the least

amount of inputs (technical efficiency), and by using inputs in optimal proportions; in other

words producing to where the marginal benefit of a good equals the marginal cost of

production (allocative efficiency). Since Farrell (1957) a large variety of studies have

explored the efficiency of firms and industries, ranging from scale efficiency to economic

efficiency2. However, examples of studies exploring the mutual organisations sector,

especially building societies are relatively limited. Nonetheless, table 1 provides a summary

of studies within this sector.

2 A firm is said to be economically efficient if it is both technically and allocatively efficient

(Kumbhakar and Lovell, 2000)

12

Author(s) Research Title Sample Technique Type of Efficiency Measured

Inputs and Outputs Specified Research Conclusions

Field (1990) Production efficiency of British building societies.

71 U.K building societies, cross sectional data – 1981.

DEA Technical and scale

Full-time labour, equipment value and the number of offices. value of deposits and newly or previously advanced mortgages

Significant negative relationship between size and technical efficiency. Estimated 14 percent of firms in the sample productively efficient and 61 percent of the sample operating inefficiently as a result of scale inefficiency.

Drake and Weyman-Jones (1992)

Technical and scale efficiency in UK building societies.

76 U.K building societies, cross sectional data – 1988.

DEA Technical and scale

Average employee wage and capital input price (expenditure of equipment and buildings divided by mean asset value), and the price of leverage (interest paid divided by the total leverage value). Total assets (consumer and commercial loans, mortgage sales, mortgages and mortgage servicing) and operating income

41 percent of firms scale efficient, whereas 61 percent of sample technically efficient.

Mckillop and Glass (1994)

A cost model of Building Societies, Producers of Mortgage and Non-Mortgage Products.

89 U.K building societies, cross sectional data – 1991.

SFA Cost Capital input price (expenditure on premises and equipment divided by mean value of assets), Labour input price (average employee wage) and the price of borrowed funds (interest expenses divided by value of borrowed funds). Outstanding mortgages and other commercial assets.

Evidence of significant augmented economies of scale for local and national building societies. Whereas constant returns to scale for building societies operating regionally. Overall, varying deviations in cost efficiency across mortgage and non-mortgage products in local, regional and national building societies.

Table 1: A Summary of Studies Analysing the Efficiency of Building Societies

13

Author(s) Research Title Sample Technique Type of Efficiency Measured

Inputs and outputs Research Conclusions

Piesse and Townsend (1995)

The Measurement of Productive efficiency in UK building societies.

57 U.K building societies, cross sectional data – 1992.

DEA Productive Tangible fixed assets, management expenses, number of branches, number of full time equivalent staff, interest paid on non-retail capital and interest paid on retail capital Number of depositors, number of borrowers, profit, interest earned from liquid assets and interest earned from mortgages

Diseconomies of scale present in larger firms, with only six building societies on the efficient frontier. 77 percent of sample operating with diseconomies of scale.

Drake and Weyman-Jones (1996)

Productive and allocative inefficiencies in U.K. building societies: A comparison of non-parametric and stochastic frontier techniques.

48 U.K building societies, cross sectional data – 1988.

DEA and SFA

Productive and allocative

The price of labour, the value of retail funds and deposits, the value of non - retail funds and deposits, the price of funds (interest payments divided by the book value of the sum of retail and wholesale funds) and the price of capital (administration and office expenses divided by total assets). Value of mortgage loans, commercial assets and liquid asset holdings beyond capital requirements.

DEA estimated overall mean inefficiency score of between 12 and 13 percent, where most of this inefficiency consisted of allocative inefficiencies. SFA score supplemented the DEA score and ultimately indicated that there was a negative relationship between size and technical and scale efficiency.

14

Author(s) Research Title Sample Technique Type of Efficiency Measured

Inputs and outputs Research Conclusions

Esho and Sharpe (1996)

X-efficiency of Australian permanent building socities.

20 Australian building societies, panel data from 1974 to 1990.

SFA X-Inefficiency

Cost of funds and a wage index (similar to the price of labour). Average house loans, average deposits, total government and other securities, other loans and fixed assets.

High levels of estimated X – inefficiency across the sample and larger organisations exhibit cost savings from economies of scale.

Ashton (1997)

Cost efficiency and UK building societies. An econometric panel-data study employing a flexible Fourier functional form.

99 U.K building societies, panel data from 1990 to 1995.

SFA Cost Price of labour (total wage divided by the number of full time employees), price of capital (aggregation of property and equipment rentals and depreciation divided by the quantity of physical capital), price of deposits (total interest payable divided by the quantity of deposits including retain and non-retail costs). Mortgage loans and non-mortgage advances.

Mean efficiency estimated at 76 percent using flexible Flourier form, whereas 72.2 percent using translog form.

15

Author(s) Research Title Sample Technique Type of Efficiency Measured

Inputs and outputs Research Conclusions

Worthington (1998)

Efficiency in Australian building societies: An econometric cost function approach using panel data.

22 Australian building societies, panel data from 1992 to 1995.

SFA Cost Price of physical capital (sum of physical capital expenditures divided by the book value of net total office premises and equipment). Price of deposits (total interest expense divided by total deposits and other borrowings). Price of labour (total expenditures on employees divided by the number of full-time employees). Personal loans, property loans, commercial loans and other securities.

Mean inefficiency score of 21 percent. Branch or agency networks have a large impact on overall efficiency; where an extensive branch network diminishes the ability of the head office to ensure cost efficiency.

16

Table one outlined studies which analyse the efficiency of building societies and although

each study focused on the same industry there was a variety of approaches taken to input

and output specification. Given the large variety of literature on the subject of efficiency it

is puzzling that there is no widely accepted consensus on input and output choice.

Previously, the majority of studies which focus on building society efficiency have adopted

the intermediation approach (Hardwick, 1990; Drake & Weyman-Jones, 1996; Ashton,

1997). The intermedation approach (Sealey & Lindley, 1976) views financial institutions as

the intermediatory in between the supply and demand of funds (Casu & Molyneux, 2003).

Here, inputs are usually labour and capital costs, interest expenses on total funds

(including customer accounts) and output is measured by loans and assets.

Although not as popular as the intermediation method, other approaches also exist. For

example, the production approach (Piesse and Townsend, 1995), where deposit taking

institutions are assumed to keep customer deposits, issue mortgages and other loans, in

addition to managing other financial assets and overseeing customer transactions (Berg et

al, 1993). Less empirically tested specifications, include the asset approach (Drake and

Weyman-Jones, 1992) and the value added approach. The asset approach is similar to the

intermediation approach but outputs are specified in terms of loan assets, the latter

identifies inputs and outputs in terms of their value added to the firm.

Ultimately, the intermediation approach dominates the non-bank financial institution

literature. This is usually the result of problems collecting accurate (sensitive) data, which

are associated with the other approaches (Worthington, 1999). Although in terms of

mutual organisations it is important to note that building societies which operate as a

mutual service provider the behavioural assumption of profit maximisation (which is

17

associated with the intermediation approach) may no longer apply, as the objective of a

mutual can be recognised as maximising the services provided to its members (Fried et al,

1993)

2.4 Other Mutual Organisations

Other mutually run firms such as mutual credit unions and savings and loans associations

(S&Ls) have also been investigated for inefficiencies; although in this section we only

provide a limited summary (for a review of the current literature see Worthington, 2011).

For example, Mester (1993) applied SFA to analyse the efficiency of a large sample set of

over 1,000 S&Ls. This large study used the wage rate (labour expenses divided by number

of full time employees), price of deposits (interest expense divided by the total value of

deposits) and price of physical capital (office occupancy and equipment expense divided by

total office assets) as inputs. Output parameters were specified as mortgages, securities

and other investments, commercial and consumer loans. The study concluded that publicly

owned S&Ls are less efficient than mutually operated S&Ls. Additionally, Mester (1993)

notes that there is a correlation between a higher capital asset ratio and greater efficiency.

Similarly, Worthington (1999) utilised a stochastic frontier approach to analyse the

efficiency of 150 Australian credit unions. In this study inputs were defined as the price of

physical capital (total outlay on office and equipment divided by the book value of office

premises and equipment), and the price of labour (total outlay on employees divided by

the number of full time employees). Output was measured by deposit securities and other

investments, personal, property and commercial loans. His research indicated that a large,

financially stable credit union with a small number of branches is more efficient than

smaller credit unions. This result provides a stark contrast from previous research by

18

Cebenoyan et al (1993) in which the coefficient for the number of branches was found to

be insignificant on efficiency.

2.5 Banks

Banks have received widespread criticism in regard to their recent handling of the financial

crisis and the high level of bonuses which are associated with the banking industry,

especially investment banks. As banks operate in the same market as building societies

but simply undertake more risky activity it is essential to provide some of the current

literature around the topic.

Since the single market initiative the European banking industry has undergone major

changes in an effort to conform to a more efficient benchmark (Altunbas et al, 2001).

Altunbas et al (2001) used a stochastic frontier model to investigate the efficiency of the

European banking industry, their research focused on estimating scale economies, X-

inefficiencies and technical change from 1989 to 1997 for a large sample of European

banks. This study used the price of labour, price of funds and the price of physical capital as

banking inputs. As is the usual method with other similar studies which use Bankscope for

data collection this research used a proxy for the number of employees as total assets,

where the cost of labour was measured as total personnel expenses divided by total assets.

Their analysis concluded that typically, scale economies are between the 5% to 7% mark,

whereas X-inefficiencies are much larger, between the 20% and 25% mark. Although, X-

inefficiencies appear to vary with the size and market of the bank; suggesting that banks of

all sizes can achieve a more efficient standard through reducing the reported inefficiencies.

19

The evaluation of efficiency has also proved popular among academics in the United

States. For example, Berger & Mester (1997) analysed the differences in the efficiencies

across the US banking industry, examining three concepts in efficiency; cost, alternative

profit and standard profit efficiency. Their research indicated that there are scale

economies for banks with a much larger size than indicated in the previous literature.

This section has only provided a limited summary in respect to banking efficiency, for a

further in depth analysis on banking efficiency see Berger et al, 1993, 2000; Resti, 1997 and

Vander Vennet, 2002.

2.6 Determinants of Executive Compensation

“There is a strong prima facie case that inappropriate incentive structures played a role in

encouraging behaviour which contributed to the financial crisis” (Turner, 2010, p. 80).

The issue of executive compensation is a controversial and a highly documented topic in

previous academic literature; with a variety of research based upon companies in the UK

(Cosh, 1975; Conyon, 1995, 1997, Ingham and Thompson, 1993; 1995 and McKnight,

1996). Across the wider literature there is a large focus on the sensitivity to firm

performance (for example Shiwakoti et al 2004;Gregg et al 2005; Ozkan, 2007; Nourayi and

Mintz, 2008). Even still, research examining the pay to performance relationship across

mutual organisations has been far from rigorous. Notably, two studies by Ingham and

Thompson (1993) and (1995) examined the determinants of CEO compensation in the UK

building society sector. The earlier paper employed a sample of 52 building societies across

two years, concluding that firm size (proxied by total assets) is the most influential

component determining CEO salary. Their more recent paper found evidence of only a

20

weak positive relationship between performance and executive remuneration, suggesting

that age has a larger impact on pay. In addition, their work indicated a negative

relationship between the size of the mutual and performance; Ingham and Roberts (1995)

put this down to deregulation within the industry. Their research concluded that as a

mutual company who do not issue shares they face weaker market controls, which causes

a misalignment of owner and CEO interests.

Understanding the empirical relationship between pay to performance can be accredited

to research by Jensen and Murphy (1990a), their influential paper used a sample of over

2500 CEOs across a fourteen year time period; documented that the pay to performance

sensitivity3 (PPS) had weakened over the last sixty years or so. Jensen and Murphy (1990b)

argued that “in most publicly held companies, the compensation of top executives is

virtually independent of performance” (Jensen & Murphy, 1990b, p. 138). Their work

suggested that companies which exhibit a higher sensitivity of pay to performance perform

better overall than those with a lower elasticity of pay to performance (Jensen & Murphy,

1990b). More recent UK studies by Gregg et al (1993) and Conyon (1995) have reinforced

earlier findings by Jensen and Murphy (1990a). With Gregg et al (1993) concluding that

there is a weak positive link between executive remuneration and corporate performance.

In contrast, a UK study by McKnight (1996) suggested that the relationship between

executive compensation and firm performance is a positive one that is stronger than

implied by previous work.

3 The impact of a one dollar change in shareholder wealth on the wealth of the chief

executive officer (Jensen & Murphy, 1990a)

21

This is now the wider consensus across academia, as evidence indicates that the

association between performance and executive pay is a weak one, where factors other

than performance are more highly correlated to pay. For example, Gomez-Mejia et al

(1987) document that after controlling for size, researchers have found the relationship

between CEO pay and performance to be weaker and less consistent than predicted by

economic theory. Nourayi and Mintz (2008) indicate that firm performance is a significant

determinant of executive cash compensation for the first three years as CEO, but when

tenure is longer than fifteen years than performance is not a significant determinant of

salary.

Stathopoulos et al (2005) provides an interesting summary of the issue:

“The overall impression one gains from this vast body of work is that a link between

executive pay (including stock option payoffs) and corporate performance does exist.

However, the link is quite weak, statistically significant, but far from compelling”

(Stathopoulos et al, 2005, p.91).

Researchers have noted that industry can enforce differentials in executive pay across top

level management (O'Rielly III et al , 1988). Possibly, because of the variations in the level

of strategic compeition and consequently the need for innovative dominance flunctuates

across industires; where employees in more competitive and innovative sectors could

demand higher salaries.

Various scholars have attempted to explain the relationship between firm size and

executive pay (Simon, 1957; Lydall, 1968, Rosen, 1990, Boyd, 1994 and Schaefer, 1998).

Simon (1957) finds that executive pay and size are positively correlated, finding that the

22

pay of senior managers such as CEOs can be written as a function of the number of

employees they supervise, either directly or indirectly (Kubo, 2000). Research by Boyd

(1994) found a weak relationship between CEO pay and firm size4, although some studies

have documeted a strong relationship between executive pay and firm size5 (Deckop,

1998; Jones & Kato, 1996). Rossen (1990) disputed that in equilibrium, the most capable

executives occupy top positions in the largest firms, where their marginal productivity is

amplified across the people below the CEO. Schaefer (1998) discussed how the marginal

marginal productivity of executives flunctuates with firm size, with larger firms paying

more with an expectation of more effort . More recently, Chalmers et al (2006) concluded

that firm size, when measured by total assets is the strongest determinant of CEO

compensation; arguing that CEOs in larger firms usually have a higher skill set and

qualifications realitive to their counterparts in smaller organisations. Lastly, Nourayi and

Mintz (2008) argued that firm size is a signifcant indactor of salary regardless of the tenure

of a CEO.

2.7 Remarks Regarding the Previous Litreature

Given the variety of previous studies it is clear that there is no definitive approach to

efficiency measurement or the evaluation of executive compensation. Surprisingly, even

forty years since its inception, there is still no widely accepted consensus in regard to the

input and output specification required for frontier analysis. Nonetheless, the succession

4 Log of net sales served as a proxy for size.

5 Number of sales is used as a proxy for size.

23

of innovative research around the topic of efficiency over the last 30 years has ensured the

development of the paradigm beyond its original framework.

3. Methodology and Data

In this section we discuss cost efficiency and the stochastic frontier model. Defining how

the model employed in this paper measures inefficiency, originating from the firms cost

function and how the model distinguishes between random noise and inefficiency.

Consequently, we compute a maximum likelihood model which is used to estimate the

parameters of the stochastic frontier. Where the data used for this section of the paper

originates from the Bankscope database, which contains the balance sheets and income

statements of all the building societies in the sample.

In order to analyse the performance of CEOs in the UK building society sector we use

annual reports published by the firms in the sample, containing the total remuneration

package of its current chief executive. We use data covering 2010 to 2011 for a sample of

33 CEOs (66 observations) in combination with a scoring for efficiency obtained using

stochastic frontier analysis. As such we hypothesise an econometric function which will

provide the basis for understanding the relationship between efficiency and executive pay.

As discussed by Varian (1990) the principles of economic theory are bound by optimising

behaviour. This rests on the assumption that firms minimise costs, whereas consumers

maximise utility. Varian (1984) documents the Weak Axiom of Cost Minimisation (WACM),

where the cost of planned production must be less than or equal to any other production

plan which yields the same amount of output. Similarly, cost efficient firms minimise costs,

where relative cost efficiency can be defined as “the ratio between the minimum cost at

24

which it is possible to attain a given volume of production and the cost actually incurred.”

(Maudos et al, 2002, p.7).

3.1 Stochastic Frontier Modelling

The stochastic frontier model uses a hypothesised function to estimate the relative

efficiencies of decision making units (DMUs), where a DMU can be anything in which

output is measurable (for example a person, firm or industry). It estimates the maxima or

minima of a dependent variable given explanatory variables, usually to estimate

production (maxima) or cost (minima) functions. Such a methodology assumes that the

production of a firm is limited by the sum of a parametric function of known inputs, and a

random error; which is associated with uncontrollable factors or model misspecification

(Worthington, 1998). Providing the necessary tools for a two component error structure,

where one measures random6 factors which affect output and the second measures

individual firm deviation from the efficient frontier which is within the organisations

control (Worthington, 1998). The relative efficiency of a DMU within the SFA framework is

defined as the ratio of multiple weighted inputs to multiple weighted outputs, where the

weight is chosen such that it maximises the efficiency for a DMU. These relative ratios

combine to create a production (cost) frontier, outlining the most efficient possibilities and

the closer a DMU is to this curve the more efficient it is. In the case of productive

efficiency all observations are found inside or on the stochastic production frontier, in

respect to cost efficiency, all observations lie outside or on the stochastic cost frontier.

6 Random shocks which are beyond the control of a firm can impact output, for example

weather (Kumbhakar and Lovell, 2000)

25

Where any deviation from the frontier has two potential sources: input allocative

inefficiency and input-orientated technical inefficiency (Kumbhakar and Lovell, 2000).

3.2 The Cost Function

A review7 of the optimisation problem stochastic frontier analysis tackles in its most basic

form presents the following cost function:

(2.1)

Where describes the scalar total cost of firm I at time t and represents the

cost function for firm i at time t. Where is a vector of explanatory variables which

include input prices and measures of output for firm i at time t, whereas represents a

vector of unknown parameters yet to be estimated.

Now if we assume that firms are not completely efficient we have the following equation:

(2.2)

Where Describes the efficiency of firm i at time t, where must be between 0 and 1.

If then the firm is fully efficient and is producing the optimal amount of outputs

from the given inputs, whereas when firm i is said to be inefficient to some degree.

Under this specification the cost function contains is split into two: a deterministic element

which is common among all producers [ and an element for producer specific

random shocks which can impact the output of a firm [ ; such that

7 This section is provided using the detailed analysis carried out in Kumbhakar and Lovell

(2000)

26

(2.3)

In order to interpret the inefficiency as a percentage deviation from the efficient frontier

we take the natural log of both sides:

{ } { } (2.4)

For simplicity we further assume that the cost function takes the log linear Cobb-Douglas

form and that there are k inputs, generating:

∑ ( ) (2.5)

For a detailed derivation see Kumbhakar and Lovell (2000).

3.3 Maximum-Likelihood Estimation and the Half Normal Model

Maximum-likelihood is a statistical technique of deriving estimates for the parameters of a

model given an observed set of data. Maximum-likelihood uses mathematical iteration to

estimate a maximised function where using some values of the parameters to be

maximised MLE adjusts the estimates iteratively until it estimates values of the parameters

which are considered to be the most likely maximum for a given set of data. Kumbhakar

and Lovell (2000) comment that if we can make distributional assumptions about and

MLE techniques should provide a more efficient prediction of the models parameters

than other estimation methods8. This is supported by Greene (2011) who notes that in

respect to stochastic frontier estimation, least square estimation is unbiased and

consistent, however the maximum likelihood estimator is non-linear and is more efficient

than least squares.

8 GLS or LSDV for more see Kumbhakar and Lovell (2000)

27

The results obtained from equation (1.1) are highly dependent on the assumed variables

and assumptions underlying the model. The majority of studies exploring the stochastic

frontier model have made various distributional assumptions of the error term following

either a half normal, exponential or gamma distribution. In the following section we

discuss one of the most commonly assumed (and the one assumed in this paper)

distributions (half-normal).

If we assume that is half normal we have the following assumptions:

)

(ii)

(iii) and are distributed independent of each other and the regressors.

Assume we wanted to estimate +

Given the independence of the error terms and as follows a half normal

distribution then the density function of is given by:

√ exp

(1.2)

Whereas the density function of is given by:

√ exp -

(1.3)

Given assumption (iii) the joint density function of and is given by the product of (1.2)

and (1.3) such that:

28

√ exp -

-

(1.4)

Given that obtain:

exp -

-

(1.5)

In order to obtain the marginal density function of we must integrate out of

generating:

∫

=

. [ (

)].exp -

=

. ϕ (

). (

)

For a stochastic cost frontier

. ϕ (

). (

) (1.6)

Where:

√

, ⁄ , standard normal cumulative distribution

function and standard normal density function.

Using equation (1.6) the log likelihood function for I producers is:

∑ (

)

∑ (1.7)

29

Equation (1.7) can be maximised with respect to the parameters to be estimated in order

to obtain maximum likelihood estimates for all parameters; where the estimates are

consistent as long as I tends to +

Now we have the estimated joint residuals , in order to derive the value of we use the

Jondrow et al (1982) estimator of individual technical efficiency, where:

Given that ⁄ ) is distributed as the mean or the mode can be used as a

point estimator for which is given by the following:

⁄ + [

⁄

⁄

]

= [

(

)] (2.0)

and

⁄ =

(2.1)

Where

= ⁄ and

⁄

Once the estimates in (2) or (2.1) are obtained individual producer technical efficiency is

calculated by:

(2.2)

Where: is ⁄ or ⁄

Estimations of individual firm specific efficiency as per the Jondrow et al (1982) method

take a value between 0 and 1, where the closer to 1 the firm is the more efficient it is.

30

Although, it is important to note that although the Jondrow et al (1982) point estimator is

unbiased but it does not consistently measure technical efficiency as

- (Coelli, 1995).

3.4 The Stochastic Cost Frontier

We express the frontier as a single equation cost function such that:

∑ i =1….N and t=1….N (3.1)

i =1….N and t=1….N (3.2)

Where ln denotes the natural logarithm of total cost for firm i at time t. is a (K x 1)

vector of input price ratios (P) and outputs (Q) for firm i at time t. The disturbance term

consists of two variables, where we assume the half normal assumptions outlined earlier in

the paper (assumption i to iii).

Following the conditional distribution approach outlined by Jondrow et al (1982) we

decompose the error term for a half normal distribution, providing an unbiased estimation

of cost inefficiency. As discussed in the previous section, we argued that using MLE was

more efficient than alternative methods. In order to obtain the estimates for equation (2)

we must first use MLE to obtain estimates of (3.1) for the stochastic cost frontier.

However, prior to obtaining estimates for (2) and (3.1) we need identify the vector of input

prices and outputs, in addition to specifying a cost function, these are the steps outlined in

the next two sections.

31

3.5 Input and Output Choice

Apart from adopting a parametric or non-parametric approach researchers have previously

employed differing choices to input and output specification. We follow the production

approach as previously outlined earlier in the paper. Where we use input price ratios

consisting of the cost of physical capital9 measured by total non-interest expenses divided

by fixed assets and cost of labour10, measured by personnel expenses divided by total

assets respectively. Outputs are measured by residential mortgage loans, total deposits

and other earning assets. A summary of the statistics in regard to variables used and a

description of the variables are provided in tables 2 and 3.

The input and output choice is illustrated below:

9 As per the specification used by Maudos et al (2002)

10 Ideally, we would like to measure the cost of labour by total personnel expenses divided

by the number of employees. However, due to the lack of data in bankscope for the

number of employees of a firm we follow a method employed by other researchers using

Bankscope and use total assets as a proxy for the number of employees (Molyneux et al,

1994; Bikker and Groeneveld, 2000)

Building Society

OEA

RML

Cost of Capital

Cost of Labour

Total Deposits

Cost of Funds

INPUTS OUTPUTS

32

Where RML = Residential mortgage loans, Total Deposits = all deposits including customer,

retail and non-retail deposits. OEA = Other earning assets (assets which earn a return apart

from deposits and loans),

Whilst there is no widely accepted consensus on input and output specification we have

decided to peruse the production approach as it provides a method commonly overlooked

in the literature and as such exploring this approach may provide a different outlook on

the efficiency of mutual organisations (Worthington, 1998)

33

Table 3: Descriptive Statistics

Variable Mean Std. Dev. Minimum Maximum

Total Cost (000’s) £246,000 £1,053,000 £1,000 £9,744,000

Cost of Capital (ratio) £2.1 £2 £0.52 £24.5

Cost of Labour (ratio) £0.0053 £0.0024 £0.0003 £0.0221

Cost of Funds (ratio) £0.0127 £0.0130 £0.0043 £0.1597

Total Deposits (000’s) £4,575,000 £20,052,000 £14,400 £169,866,000

Residential Mortgage Loans (000’s)

£4,033,000 £19,324,000 £15,400 £155,939,000

Other Earning Assets (000’s) £4,367,000 £4,596,000 £5,600 £155,469,000

Variable Variable Name Description (for firm i at time t)

C Total Cost Total non-interest expense + total interest expenses

Cost of Labour Total personnel expenses divided by total assets

Cost of Capital Total non-interest expenses divided by fixed assets

Cost of Funds Total interest expense divided by total deposits

Total Deposits Total customer, retail and other deposits

Residential Mortgages

Total residential mortgages

Other Earning Assets

Other assets which are not loans which earn a return

Table 2: Dependent Variable, Inputs and Outputs

34

3.6 Cost Function Formulation

In the previous literature there are two dominating cost functions, these are the Cobb-

Douglas and the translog (transcendental logarithmic) functional form. The Cobb-Douglas

is a linear in logs model, which is easy to estimate and requires few parameters. However

being a simplistic functional form it assumes that each firm has the same production

elasticity and an elasticity of substitution equal to 1. In contrast, translog is quadratic in

logs, providing a much more flexible functional form, applying firstly no a priori restrictions

on substitution or production elasticities, and secondly, permitting economies of scale to

vary across firms (Worthington, 1998).

Consequently, in this paper we adopt the translog specification, where the error term

is composed of two components, and . We assume this error term follows a normal-

half normal distribution where ),

, in addition and

are distributed independent of each other and the regressors. In order to estimate

equation (3.1) we specify the following multi output translog cost equation:

(

) (

) (

) +

(

) + (

) + + +

+ + +

+ + + (4.1)

35

In order to ensure linear homogeneity in input prices we follow Worthington (1998) and

Fiorentino et al (2006) by normalising total costs and all input prices by one selected input

price (in this case the cost of capital), as such the cost of capital disappears as the cost of

capital divided by the cost of capital equals zero.

In respect to equation (4.1): lnTC denotes the natural logarithm of total cost11 (total non-

interest expense + total interest expenses + personnel expenses) divided by the cost of

capital. refers to the natural logarithm of outputs (total deposits, residential

mortgage loans and other earning assets). is the natural logarithm of input prices

normalised by dividing against the cost of labour (the cost of capital divided by the cost of

labour and the cost of funds divided by the cost of labour).Furthermore as described

earlier following the execution of the translog cost frontier (4.1) we estimate the

conditional expectation of given as per the Jondrow et al (1982) firm specific

efficiency specification (2.1).

3.7 CEO Compensation and Efficiency

As the aim of this paper is not to solely examine efficiency but to understand the impact of

changes in CEO salary in tandem with efficiency scoring we must regress the efficiency

scores provided by the translog cost frontier in the previous section to the CEO salary for

each executive; providing us with a hypothesised function, which will serve to predict the

relationship between CEO salary and firm efficiency. This is by regressing firm level CEO

compensation levels for a smaller sample set of 33 building societies across two years

(2010 and 2011) against the efficiency score found by the frontier analysis. In addition, we

11

We follow the same definition of total costs as Casu & Molyneux (2010)

36

carry out two separate cross sectional regressions (for the years 2010 and 2011) to

understand any yearly changes in cost efficiency and the impact of this on yearly CEO

salary. We will use the following pooled model12 for the regressions:

(5.1)

Where:

= Total compensation by CEO of firm i in year t

= Total assets13 of firm i at time t

, Coefficients yet to be estimated

= SFA score of CEO of firm i in year t

= error term

We hypothesise that more efficient CEOs gain a higher level of compensation as such we

expect > 0 (positive relationship). Moreover, we suspect that CEOs who are more

efficient are rewarded with a higher total compensation (ceteris paribus), consequently we

expect as we expect compensation to be positively related to the size of the firm.

Lastly, as we suspect that that increases in compensation and firm size are non-linear

(compensation does not increase proportional to firm size) we include a square term of

12We use a similar model to Chen et al (2009) except we use SFA instead of DEA for the

efficiency analysis and the cross sectional regressions are simply without the label for time.

13 We use total assets as a proxy for size as used in previous empirical research (Chalmers

et al, 2006)

37

total costs in the regression. Lastly, we hypothesise that there are decreasing returns to

scale in respect to compensation with firm size (ceteris paribus), thus we expect .

Table 5 provides a summary of statistics from the data concerning CEO salary, we note that

the standard deviation is higher than the mean for the year 2010 indicting that the data is

highly skewed, this is complimented by the fact the maximum value is much higher than

the mean.

Variable CEO Pay 2010 CEO Pay 2011

Mean 294 278

Standard Deviation 329 269

Min 80 71

Max 1884 1539

N = 66

Table 5: Summary CEO Salary Descriptive Statistics

38

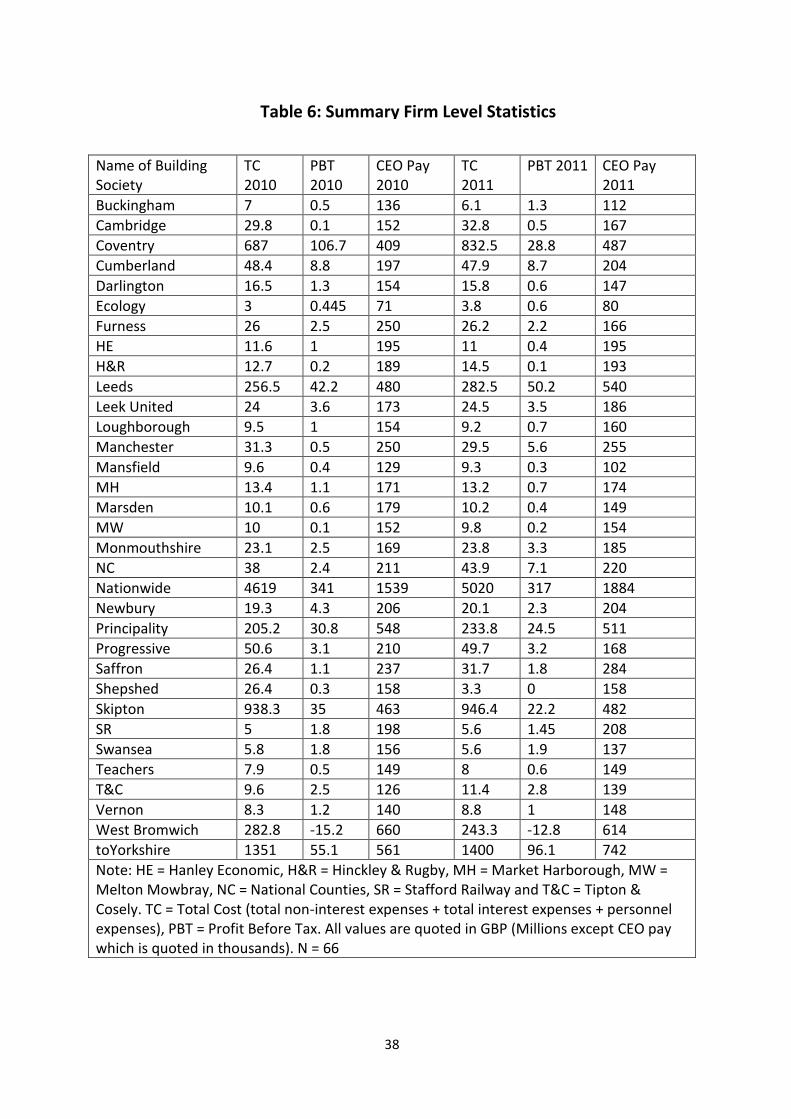

Name of Building Society

TC 2010

PBT 2010

CEO Pay 2010

TC 2011

PBT 2011 CEO Pay 2011

Buckingham 7 0.5 136 6.1 1.3 112

Cambridge 29.8 0.1 152 32.8 0.5 167

Coventry 687 106.7 409 832.5 28.8 487

Cumberland 48.4 8.8 197 47.9 8.7 204

Darlington 16.5 1.3 154 15.8 0.6 147

Ecology 3 0.445 71 3.8 0.6 80

Furness 26 2.5 250 26.2 2.2 166

HE 11.6 1 195 11 0.4 195

H&R 12.7 0.2 189 14.5 0.1 193

Leeds 256.5 42.2 480 282.5 50.2 540

Leek United 24 3.6 173 24.5 3.5 186

Loughborough 9.5 1 154 9.2 0.7 160

Manchester 31.3 0.5 250 29.5 5.6 255

Mansfield 9.6 0.4 129 9.3 0.3 102

MH 13.4 1.1 171 13.2 0.7 174

Marsden 10.1 0.6 179 10.2 0.4 149

MW 10 0.1 152 9.8 0.2 154

Monmouthshire 23.1 2.5 169 23.8 3.3 185

NC 38 2.4 211 43.9 7.1 220

Nationwide 4619 341 1539 5020 317 1884

Newbury 19.3 4.3 206 20.1 2.3 204

Principality 205.2 30.8 548 233.8 24.5 511

Progressive 50.6 3.1 210 49.7 3.2 168

Saffron 26.4 1.1 237 31.7 1.8 284

Shepshed 26.4 0.3 158 3.3 0 158

Skipton 938.3 35 463 946.4 22.2 482

SR 5 1.8 198 5.6 1.45 208

Swansea 5.8 1.8 156 5.6 1.9 137

Teachers 7.9 0.5 149 8 0.6 149

T&C 9.6 2.5 126 11.4 2.8 139

Vernon 8.3 1.2 140 8.8 1 148

West Bromwich 282.8 -15.2 660 243.3 -12.8 614

toYorkshire 1351 55.1 561 1400 96.1 742

Note: HE = Hanley Economic, H&R = Hinckley & Rugby, MH = Market Harborough, MW = Melton Mowbray, NC = National Counties, SR = Stafford Railway and T&C = Tipton & Cosely. TC = Total Cost (total non-interest expenses + total interest expenses + personnel expenses), PBT = Profit Before Tax. All values are quoted in GBP (Millions except CEO pay which is quoted in thousands). N = 66

Table 6: Summary Firm Level Statistics

39

4. Empirical Results

In this section, we discuss the results obtained from the stochastic frontier analysis in

addition to the results from the regressions outlined in the previous section; analysing the

relationship between cost efficiency and CEO salary. The appendix provides individual

efficiency scores obtained for all years from the frontier analysis, however summary

efficiency statistics and a description of the regression coefficients are provided where

required.

Table 7 presents the maximum-likelihood estimates for the parameters of the normalised

translog cost frontier as described in equation (4.1). We reject the null hypothesis of joint

insignificance for the coefficients of the cost function ( = = 0) by using the

log-likelihood ratio test statistic with chi-square distribution. In addition we reject the null

hypothesis of no technical inefficiency ( = 0) as it is true that

. We find that

both error terms are statistically significant, with the inefficiency component significant at

the 99% confidence level and the random noise component significant at the 99.9%

confidence level.

40

Parameter Variable Coefficient Std.Error Parameter Variable Coefficient Std.Error

4.183

(1.91)

2.189 -0.109

(-0.24)

0.454

1.618

(1.05)

1.548 0.544

(0.44)

1.224

-0.298

(-0.19)

1.586 0.527

(-0.93)

1.526

-0.919

(0.45)

2.059 -0.992

(-0.65)

1.494

-0.198

(-0.19)

1.041 -0.582

(-0.39)

0.674

-0.198

(-0.07)

2.661 -0.759

(-1.13)

1.912

0.274

(0.84)

0.325 1.137

(0.59)

0.637

-0.085

(-0.13)

0.673 -0.832

(-1.31)

0.637

2.272

(1.06)

2.144 -1.443

(-0.55)

2.631

0.337

(1.08)

0.311 0.467

(0.59)

0.769

0.989

(0.30)

3.252

-2.743***

(-7.86)

0.349

-2.818**

(-2.69)

1.048

t statistics in parentheses: *p < 0.05, **p < 0.01, ***p < 0.001 : Log-likelihood = -56.31 N = 294

Where: Ln = Natural Logarithm, P1 = Cost of labour, P2 = Cost of funds, P3 = cost of capital, Y1= Residential

mortgage loans, Y2 = Other earning assets, Y3 = Total deposits, P1* = P1/P3, P2* = P2/P3, Variance of two

sided stochastic frontier, = Variance of inefficiency and Total error variance in the model

.

Table 7 – Translog Cost Function

41

Table 8 provides a summary of mean cost efficiency scores on a yearly basis for the whole

sample period. The scores outlined in table 8 each describe how far above the respective

efficient cost frontier each building society is estimated to be. The overall mean efficiency

score was estimated at roughly 0.82, indicating a mean cost inefficiency of 18% across the

sample. We find that the proportion of efficient CEOs has declined from 2003 to 2008 year

on year, interestingly the lowest mean inefficiency (year) score is in 2008, coinciding with

the worldwide financial crisis. The estimated cost efficiencies found in this paper are

consistent with the earlier findings of Worthington (1998), although his study focused on

Australian building societies. It is interesting to see that although we follow a production

approach the mean cost inefficiency score is close to that found by Worthington (1998)

(21%) who employed an intermediation approach.

42

Table 9 summarises the mean firm specific cost efficiency scores estimated by the translog

cost frontier along with a value for average total assets for each mutual, we find that there

is no definitive given relationship between firm size and efficiency.

Year Observations Mean Std. Dev. Minimum Maximum

1998 2 0.8184736 0.0297145 0.7974623 0.8394849

1999 2 0.8451663 0.0080369 0.8394833 0.8394849

2000 3 0.8352573 0.0147830 0.8228537 0.8516154

2001 3 0.8498542 0.0075276 0.8419057 0.8568749

2002 3 0.8186927 0.0414188 0.7742882 0.8562799

2003 6 0.8565482 0.0170381 0.8304076 0.8836235

2004 25 0.8325011 0.0170381 0.8304076 0.8836235

2005 31 0.8051640 0.0511372 0.6971726 0.9164624

2006 31 0.7949433 0.0461719 0.6967176 0.8746896

2007 32 0.7722448 0.0584345 0.6440333 0.8750280

2008 39 0.7565842 0.0650992 0.5897666 0.8827966

2009 39 0.8487659 0.0466377 0.7238307 0.9229753

2010 39 0.8670900 0.0338448 0.7686022 0.9198319

2011 36 0.8710819 0.0303110 0.7943464 0.9176146

1998 - 2011 294 0.8200372 0.0615920 0.5897666 0.9229753

Note: For a detailed description of the efficiency scores associated with the translog cost

frontier (4.1) see Table 10 (appendix).

Table 8: Stochastic Cost Frontier Efficiency Summary

43

Average Total Assets Building Society Average Cost Efficiency

187.1875 Bath Investment 0.863373

145.3125 Beverley 0.750649

149.95 Buckinghamshire 0.830156

926.26 Cambridge 0.864610

32.7125 City of Derry 0.787271

22081.8 Coventry 0.832846

1406.2 Cumberland 0.808606

593.125 Darlington 0.859215

261.7625 Dudley 0.837476

79.976 Ecology 0.852636

814.0875 Furness 0.833676

335.0714 Hanley Economic 0.821982

163.4571 Harpenden 0.817177

647.8125 Hinckley & Rugby 0.850801

415.95 Ipswich 0.851334

20572.25 Leeds 0.777264

732.325 Leek United 0.833798

252.4375 Loughborough 0.816680

892.15 Manchester 0.830574

242.9429 Mansfield 0.836889

404.5875 Market Harborough 0.851513

343.5857 Marsden 0.888486

400.2875 Melton Mowbray 0.815333

569.0875 Monmouthshire 0.755527

1140.85 National Counties 0.750097

169936.5 Nationwide 0.821621

606.3375 Newbury 0.800095

1620.213 Nottingham 0.848758

5770.914 Principality 0.703823

1483.525 Progressive 0.722298

792.9375 Saffron 0.824975

233.2 Scottish 0.872923

86.975 Shepshed 0.860166

13204.28 Skipton 0.907365

154.4668 Stafford Railway 0.776839

136.3875 Swansea 0.799076

251.4625 Teachers 0.797602

304.225 Tipton & Cosely 0.835730

214.3714 Vernon 0.840646

8368.2 West Bromwich 0.789831

25069.87 Yorkshire 0.814842

Table 9: Average Size and Average Cost Efficiency

44

Note: Average total assets (ATA) are used as a proxy for size, similar to table 9. ATA are

measured in millions of GBP (£) and cost efficiency scores can range between 0 and 1.

4.1 Efficiency and CEO Remuneration

We analysed the link between CEO salary and firm efficiency across two years, for

comparison we have provided three different sets of results, with one providing estimates

of a pooled OLS approach on regression analysis for the two year sample of 33 building

societies. Secondly, we split the regression into a cross sectional basis and analyse the

results from 2010 and 2011 separately in order to detect any changes to the relationship

between SFA score and CEO salary, in addition to being able to discuss and evaluate any

skewness in the results. Note that we have multiplied the estimated SFA scores by 100 in

order to be able to analyse a one unit change in efficiency against CEO salary (thus SFA

score in the regressions below is between 0 and 100 instead of 0 and 1).

Examining the relationship between Cost Efficiency and CEO Salary

Variable Pooled 2010 - 2011 2011 Cross Section 2010 Cross Section

Constant 441

(1.45)

594.1

(1.40)

114.9608

(0.17)

SFA Score -2.9

(-0.83)

-4.712

(-0.96)

0.997

(0.13)

Total Assets 0.467***

(7.74)

0.0159**

(5.73)

0.00688**

(2.78)

-0.00000258

(-1.76)

-4.74e-08

(-3.25)

8.79e-09

(0.62)

Adjusted 0.8869 0.8634 0.8280

N 66 33 33

t statistics in parentheses: *p < 0.05, **p < 0.01, ***p < 0.001

Table 10: Efficiency and CEO Salary Regressions

45

The regression analysis summarised in table 10 indicates that overall SFA score is

negatively correlated to CEO salary, the skewness of the results is visible when comparing

the pooled results to the result from the 2010 cross sectional regression. Nonetheless, it is

puzzling as to why the estimated SFA score decreases (on average) with increases to

executive pay; it seems that it is probably a simple issue of a requiring more data to

provide a more accurate description of the relationship between pay and efficiency. In

addition, the magnitude of an increase in efficiency on CEO salary varies across years, with

2011 indicating that the SFA score and CEO pay exhibit a strong negative relationship, on

the other hand the 2010 regression indicates a weak positive relationship between

efficiency and pay, where if we assume efficiency serves as a proxy for performance we

find a weak positive link between pay and performance, in line with previous research by

Jensen and Murphy (1990a) and Gregg et al (2003).

Interestingly, total assets is significant in each estimated regression, varying from being

statistically significant at the 99% confidence level in the cross sectional regressions and at

the 99.9% confidence level in the pooled regression. In all the regressions an increase in

size when measured by total assets has a statistically significant increase in CEO salary;

corresponding with the earlier findings of Chalmers et al (2006).

Earlier we hypothesised that the coefficient for SFA score > 0 as we suspected that more

efficient executives receive a higher level of compensation, given our results we fail to

reject the null hypothesis as we have two out of three regressions in which SFA score is less

than zero. We also suspected the coefficient for total assets would be > 0 as we expected

that CEO salary is positively correlated to firm size. Given the results in table 9 we fail to

reject the null hypothesis as the estimates provided by the regressions indicate that size

46

and salary exhibit a significant positive relationship. Lastly we expected the coefficient of

total-assets² < 0 as we suspected that there are decreasing returns to scale for CEO salary

with respect to firm size, once again we fail to reject the null hypothesis of decreasing

returns to scale; as the regression for the year 2010 has a positive coefficient for total-

assets². Although, overall (pooled regression) there is evidence of decreasing returns to

scale.

4.2 Discussion

Overall we find that firm size is powerful determinant of CEO salary, especially when

compared to the efficiency score. Adjusted R² for all three regressions indicates that we

have explained over 80% of the variation in CEO compensation with the given variables.

The investigation of building society efficiency has yielded results which are in line with

previous empirical research, with a mean building society cost efficiency of 82% the firms

in the sample would have to increase outputs by 18% to be considered completely cost

efficient (ceteris paribus). The efficiency scores provide the basis for which improvements

can be made in order to not only be more cost efficient but as a result more profitable. As

noted earlier in the paper, the lowest mean year efficiency score is estimated for 2008,

around the time of the global financial crisis. We know that building societies given their

conservative attitude to risk were in many ways sheltered from the brunt of the financial

crisis; brought on by mortgage lending and later derivative trading gone into over drive.

However, the results indicate that whatever the reason for the inefficiencies in our sample

the timing of the lowest mean score indicates the financial crisis may have had an impact

on the efficiency of building societies. This is especially important when you consider that

this paper takes a production approach, which depends on deposits as outputs. If we make

47

the assumption that the financial crisis reduced total bank deposits, this would lower

overall cost efficiency as output would decrease relative to previous years (ceteris paribus).

In the last section of the analysis the regressions indicate that there is clear evidence that

CEO salary is correlated to efficiency; however, that said the evidence presented indicates

it is not a statistically significant determinant of CEO salary.

5. Concluding Remarks

Corporate governance and the associated theories have met a recent media backlash as

financial institutions, primarily consisting of banks attempt to explain why executives are

paid such a high salary. This high level of public exposure has not only exposed in many

cases a weak pay to performance relationship but a relationship which by many empirical

accounts has been analysed as statistically non-significant. By utilising an approach usually

overlooked in previous literature the empirical analysis in this paper indicates that the

relationship between efficiency and CEO salary is not as strong as thought in theory and as

indicated in previous research. However, we do find similarities to previous empirical

research in respect of size being a strong determinant of CEO salary; but it would be

interesting to see an analysis of how size determines executive pay when a different proxy

is used other than total assets in combination with a stochastic cost frontier score.

We have established that a statistically significant positive relationship exists between size

and executive salary in the U.K building society sector. But the evidence concerning the

relationship between efficiency and CEO salary is not so clear, as the regressions provide

48

conflicting results. As this paper is the first of its kind14 in respect to examining a stochastic

frontier score in tandem with executive salaries in the mutual organisation sector there are

various ways to extend the analysis in this paper. There is a distinct possibility that a larger

sample set could provide a better overview of the relationship between efficiency and

executive pay, in addition, using different proxies could possible yield differing results.

Moreover, applying a comparatively advanced frontier technique in addition to analysing

more variables in respect to the estimation of the determinants of CEO salary may provide

a different outlook on the subject of efficient CEOs. Lastly, using more consistent and

accurate data which incorporates sensitive data which is currently difficult to obtain such

as the number of employees year on year and the number of employees off sick in a year

may provide an alternative approach which has yet to be fully utilised.

In order to reduce the unexplained variation within the dependent variable a regression

analysis which employs an increased number of independent variables may provide a more

accurate and consistent indication of the correlation between CEO pay and efficiency. For

example, this could be by including variables which account for variations in CEO age,

degree level and if the executive has a family to support.

Ultimately, this study finds that the cost efficiency of U.K building societies is more of less

in line with previous research and that size is a more important determinant of CEO salary

than firm cost efficiency. Consequently, the evidence presented in this paper finds

similarities with Ingham and Thompson (1995), where size has a significant influence on

executive salary. In addition, there are similarities between this study and other that

carried out by Worthington (1998) in respect to cost efficiency estimates. However, the

14 To the knowledge of the author.

49

results obtained from the regressions provide estimates for a relationship (in respect to

using an SFA score) yet to be empirically tackled in the literature. It is evident that a more

detailed evaluation of the subject is required in order to provide evidence which yields a

more accurate description of the correlation between efficiency and CEO salary.

50

Name 1998 1999 2000 2001 2002 2003 2004

Bath Investment - - - - - 0.8836235 0.8982414

Beverley - - - - - - 0.8221018

Buckinghamshire - - - - - 0.8564557 0.8304076

Cambridge - - - - - - -

City of Derry - - - - - 0.82551 0.7426277

Coventry - - - - - - -

Cumberland - - - - - - -

Darlington - - - - - - -

Dudley - - - - - - 0.8815243

Ecology - - - - - - 0.8732530

Furness - - - - - - 0.8287350

Hanley Economic

Harpenden - - - - - - 0.8149030

Hinckley & Rugby - - - - - - 0.8248304

Ipswich - - - - - 0.857098 0.8530745

Leeds - - - - - - -

Leek United - - - - - - 0.8455605

Loughborough - - - - - - 0.8334979

Manchester - - - - - - -

Mansfield - - 0.8516154 0.8507820 0.7742882 - -

Market Harborough - - - - - - 0.8482306

Table 11: Firm Level Cost Efficiency Estimates – Page 1

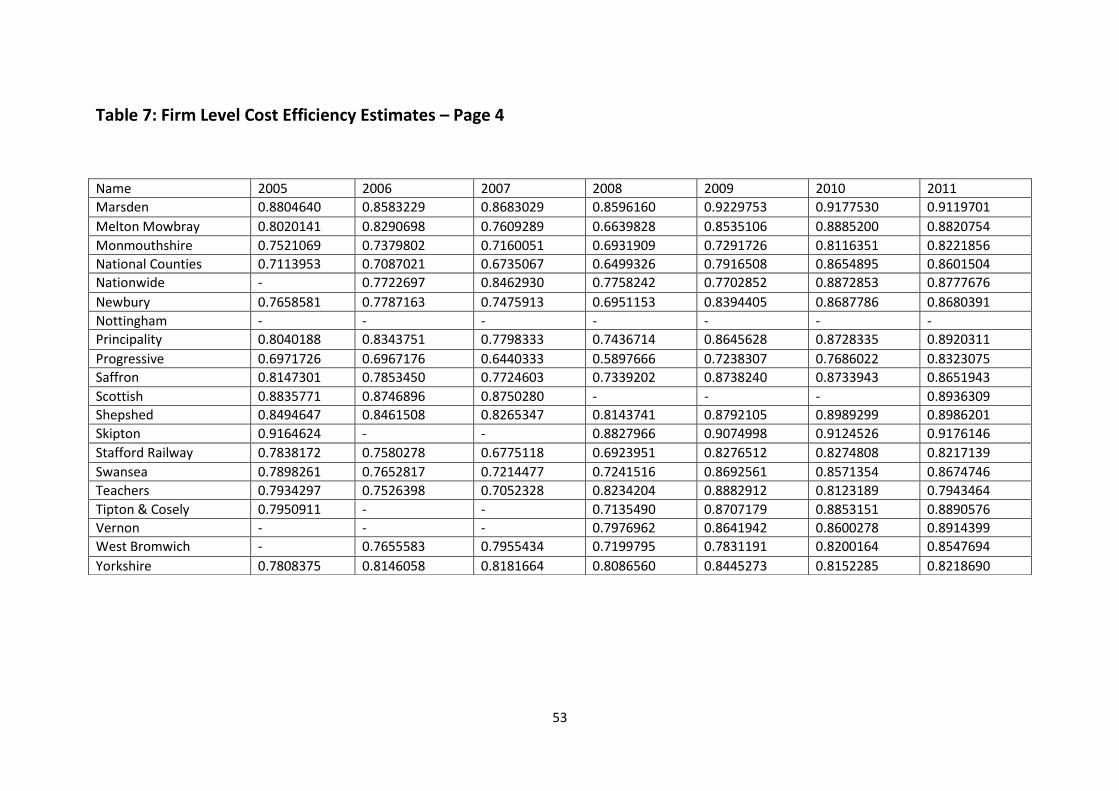

7. Appendix

51

Table 7: Firm Level Cost Efficiency Estimates – Page 2

Name 1998 1999 2000 2001 2002 2003 2004

Marsden - - - - - - -

Melton Mowbray - - - - - - 0.8425618

Monmouthshire - - - - - - 0.7819394

National Counties - - - - - - 0.7399479

Nationwide - - - - - - -

Newbury - - - - - - 0.8372208

Nottingham 0.8394849 0.8394833 0.8313028 0.8419057 0.8562799 0.8599628 0.8728861

Principality - - - - - - -

Progressive - - - - - - 0.8259498

Saffron - - - - - - 0.8809341

Scottish - - - - - - 0.8376894

Shepshed - - - - - - 0.8680426

Skipton - - - - - - -

Stafford Railway - - - - - - 0.8261181

Swansea - - - - - - 0.7980310

Teachers - - - - - - 0.8111342

Tipton & Cosely - - - - 0.8568749 0.8517414 0.8234922

Vernon 0.7974623 0.8508492 0.8228537 - - - -