An overview of investment types, trends and performance Basic Investment Concepts C09-0223-007...

67

An overview of investment types, trends and performance Basic Investment Concepts C09-0223-007 (3/09)

-

Upload

rosa-black -

Category

Documents

-

view

215 -

download

0

Transcript of An overview of investment types, trends and performance Basic Investment Concepts C09-0223-007...

An overview of investment types, trends and performance

Basic Investment Concepts

C09-0223-007 (3/09)

You should consider the investment objectives, risks, charges and expenses of the investment options carefully before investing. The prospectuses/prospectus summaries/information booklets containing this and other information can be obtained by contacting your local representative. Please read the information carefully before investing.

Insurance products, annuities and funding agreements issued by ING Life Insurance and Annuity Company (“ILIAC”) One Orange Way, Windsor, CT 06095 , which is solely responsible for meeting its obligations. Plan administrative services provided by ILIAC or ING Institutional Plan Services, LLC. All companies are members of the ING family of companies. Securities distributed by or offered through ING Financial Advisers, LLC (member SIPC) or other broker-dealers with which it has a selling agreement.

Agenda

Investment Types Stocks

Bonds

Mutual Funds

Market Trends and Investment Concepts

Investment Types

Represent ownership in a corporation

Potentially make money for investors by: Paying dividends Rising in value

Corporations come in a variety of sizes large medium small

Stocks

Number of shares outstanding x price per share

Indication of firm size Large cap - Over $3.3 billion (+/-)

(e.g., Microsoft, Wal-Mart, G.E.)

Mid cap - $750 million to $3.3 billion (+/-) (e.g., 3Com Corporation, Tupperware Brands Corp., Tootsie Roll)

Small cap - $200 million to 1 billion (+/-) (e.g., LA-Z-Boy, Swift Energy, LoJack Corp.)

Market Capitalization

As of 1/26/09. Market capitalization for Large Cap is represented by the S&P 500 Index; Mid Cap by the S&P 400 Index; Small Cap by the S&P 600 Index.

Source: Standard & Poor’s

Wilshire 5000

Russell 2000

Standard & Poor’s® Small Cap 600

Standard & Poor’s® Mid Cap 400

Standard & Poor’s® 500

- S&P® 500 Growth- S&P® 500 Value

Dow Jones Industrial Average

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Major Domestic Market Indices

??Supply and

Demand Company

Performance

Industry IssuesEconomic, Social and

Political Factors

What affects stock prices?

1976-2008 Average Annualized Rate of Return = 10.22%

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company; Standard & Poor’s 500 Index Composite Total Return as of 12/31/2008

Year

Ret

urn

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

'76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08

Stock Market Performance Over Time

Average Annualized Returns as of 12/31/08

1 Yr. 5 Yrs. 10 Yrs.

-37.00% -2.19% -1.38%

-33.79% -0.93% 3.02%

Ret

urn

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

S&P 500 21.05% -9.11% -11.88% -22.10% 28.69% 10.87% 4.89% 15.80% 5.49% -37.00%

Russell 2000 21.26% -3.15% 2.48% -20.48% 47.25% 18.32% 4.55% 18.35% -1.57% -33.79%

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Large Cap vs. Small Cap

Growth stocks: Exhibit faster than expected gains in earnings

Expected to continue to show high levels of profit growth

Characterized by high P/E ratios and below average dividends

Value stocks: Deemed to be undervalued in price; could eventually have their worth

recognized by the market

Characterized by low P/E ratios, below average earnings growth rate forecasts, and above average dividends

Growth vs. Value

Growth vs. Value

Average Annualized Returns as of 12/31/08

1 Yr. 5 Yrs. 10 Yrs.

-34.92% -3.13% -3.15%

-39.22% -1.31% -0.25%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

S&P 500 Grow th 28.26% -22.08% -12.73% -23.59% 25.68% 6.14% 3.47% 11.01% 9.13% -34.92%

S&P 500 Value 12.72% 6.08% -11.71% -20.86% 31.80% 15.71% 6.34% 20.80% 1.99% -39.22%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Ret

urn

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Diversify by Style: Large Cap

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

S&P 600 12.40% 11.80% 6.54% -14.63% 38.80% 22.65% 7.68% 15.12% -0.30% -31.07%

S&P MidCap 400 14.72% 17.51% -0.61% -14.51% 35.64% 16.50% 12.55% 10.32% 7.98% -36.23%

S&P 500 21.05% -9.11% -11.88% -22.10% 28.69% 10.87% 4.89% 15.80% 5.49% -37.00%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Small vs. Mid vs. Large

Average Annualized Returns as of 12/31/08

1 Yr. 5 Yrs. 10 Yrs.

-31.07% 0.88% 5.18%

-36.23% -0.08% 4.46%

-37.00% -2.19% -1.38%

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Ret

urn

Diversify by Market Cap

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

S&P 600 Grow th 19.58% 0.57% -1.18% -15.36% 37.32% 22.01% 8.97% 10.54% 5.60% -32.94%

S&P 600 Value 3.03% 20.86% 13.10% -14.47% 40.05% 23.23% 6.44% 19.57% -5.54% -29.51%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Growth vs. Value

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Average Annualized Returns as of 12/31/08

1 Yr. 5 Yrs. 10 Yrs.

-32.94% 0.85% 4.81%

-29.51% 0.88% 5.35%

Ret

urn

Diversify by Style: Small Cap

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

S&P 400 Grow th 27.37% 9.16% -7.97% -19.17% 30.96% 14.01% 13.42% 5.81% 13.50% -37.61%

S&P 400 Value 2.33% 27.84% 7.14% -10.11% 40.22% 18.92% 11.60% 14.62% 2.65% -34.87%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Growth vs. Value

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Average Annualized Returns as of 12/31/08

1 Yr. 5 Yrs. 10 Yrs.

-37.61% -0.15% 5.33%

-34.87 -0.11% 3.59%

Ret

urn

Diversify by Style: Mid Cap

IOU’s

Certify the lending of money to a government or corporation and describe the terms of the loan

Potentially generate money for investors by: Interest payments

Rising in value

Issued by many different entities

Come in a variety of qualities and maturities

Bonds

Government– Treasuries– Agencies– Municipals

Corporate– Investment Grade – Junk (High Yield)

(Higher Risk)

Types of Bonds

Please note, bonds offered by government chartered corporations carry more risk than U.S. Treasury securities.

Moody’s

Aaa

AaABaaBaBCaaCaC-

S&P

AAAAAABBBBBBCCCCCCD

Definition

Highest qualityHigh qualityFavorable attributesMedium qualitySpeculative elementsSmall assurancePoor standingHighly speculativeVery poor prospectsIn default

Bond Ratings

Please note, bond ratings are subject to change and may be downgraded any time by the ratings agency.

– Changes in fundamentals of issuer

– Changes in interest rates

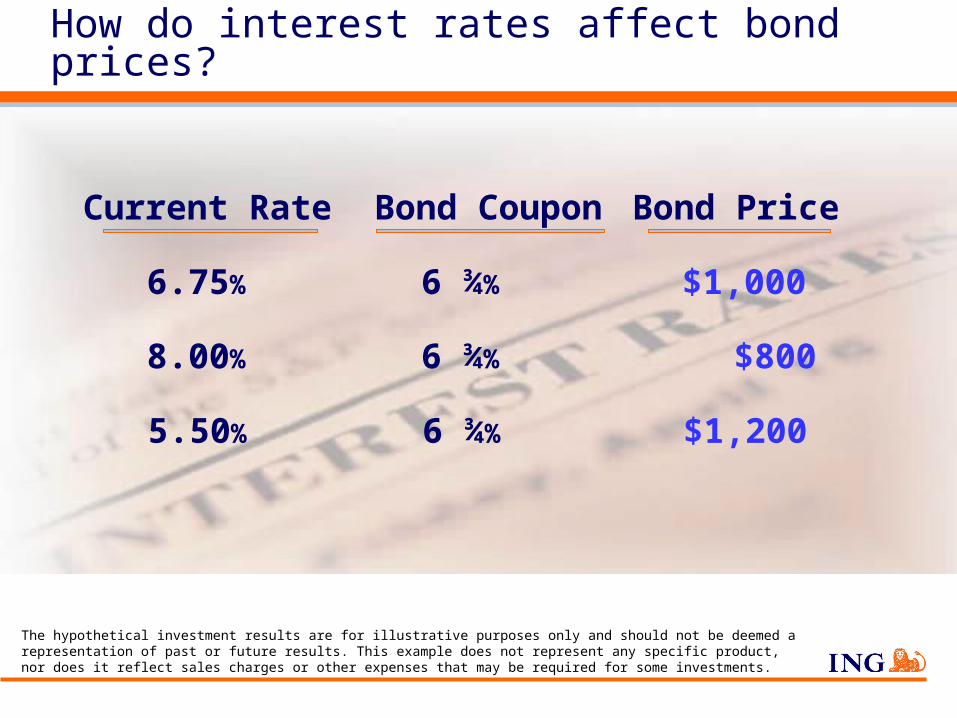

Why do bond prices change?

Current Rate Bond Coupon Bond Price

6.75% 6 ¾% $1,000

8.00% 6 ¾% $800

5.50% 6 ¾% $1,200

The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments.

How do interest rates affect bond prices?

Collections of stocks, bonds, and other securities

Managed by a professional investment company

Come in a wide variety of types

Have stated investment objectives, policies and philosophies

Have administrative and investment management fees

Mutual Funds

Types of Mutual Funds/Investment Objectives

Equity Aggressive Growth

Growth

Growth & Income

Sector

International Foreign

Worldwide

Emerging Markets

Fixed Income (short long, intermediate)

Government

Corporate

High Yield

Foreign

Municipal

Combination Balanced

Asset Allocation

Money Market *

* An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in money market funds.

Size

Style

OtherGrowth Value

Blend

Small Cap

Mid Cap

Large Cap

Quantitative vs. Fundamental

Top-down vs. Bottom-up

Equity Mutual Funds and Management Style

Market Trends and Investment Concepts

Aggressive Portfolio

Moderately Aggressive

Portfolio

Moderate Portfolio

Moderately Conservative

Portfolio

Conservative Portfolio

Portfolios reflect a varying mix of equity vs. fixed investments based on different investor profiles

Portfolios are illustrative only and are not intended to be specific recommendations. You have to decide what’s best for your risk tolerance level.

0

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Allo

cati

on Fixed

Investments

Equity Investments

Sample Model Portfolio Allocations

Portfolio Diversification

When two investments exhibit parallel movement, the returns move up and down at the same time and to the same degree.

Risk: Not reduced in a portfolio with no diversification.

Investment A

Investment B

Portfolio 1

No Diversification

Source: SunGard® Online Investment Systems

Portfolio Diversification

When there is some similarity in movement among the returns of two investments, risk is partially reduced when combined into a portfolio.

Investment EPortfolio 2

Investment F

Some Diversification

Source: SunGard® Online Investment Systems

Portfolio Diversification

When two investments move in opposite directions, the strongest diversification effect will be produced.

Risk: Greatly reduced when both investments are represented in a portfolio, without substantially reducing portfolio expected return.

Investment C

Investment D

Portfolio 3

Complete Diversification

Source: SunGard® Online Investment Systems

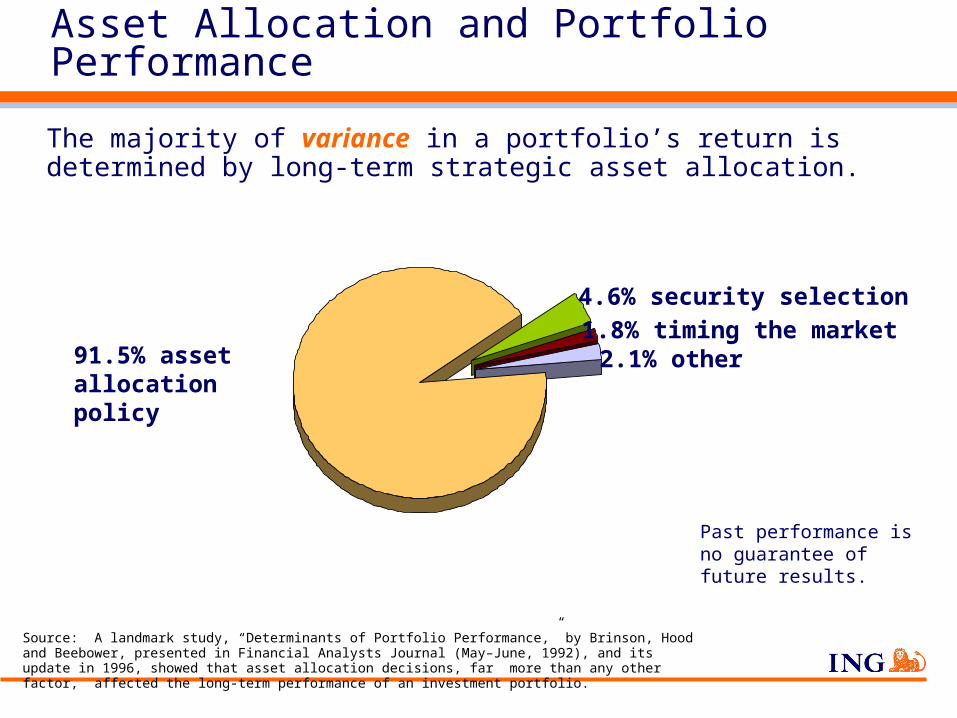

Diversify Between Asset Classes

An asset class is a category of funds with similar investment objectives and risk profiles.

Asset class diversification attempts to reduce risk and/ or improve return.

Over time, the variance of returns within an investor’s portfolio primarily depend on the invested asset classes vs. individual fund selection.

Source: A landmark study, “Determinants of Portfolio Performance,” by Brinson, Hood and Beebower, presented in Financial Analysts Journal (May–June, 1992), and its update in 1996, showed that asset allocation decisions, far more than any other factor, affected the long-term performance of an investment portfolio.

Source: A landmark study, “Determinants of Portfolio Performance,” by Brinson, Hood and Beebower, presented in Financial Analysts Journal (May–June, 1992), and its update in 1996, showed that asset allocation decisions, far more than any other factor, affected the long-term performance of an investment portfolio.

Past performance is no guarantee of future results.

4.6% security selection

2.1% other1.8% timing the market

Asset Allocation and Portfolio Performance

The majority of variance in a portfolio’s return is determined by long-term strategic asset allocation.

91.5% asset allocation policy

Relative Return/Risk Continuum

Each sample asset class has its own investment return/risk characteristics.

Risk

This illustration is hypothetical and is not intended to represent the performance of any specific asset class.

Ret

urn

Stability of Principal

Large Cap Growth

Small/Mid/Specialty

Global/International

Income

Large Cap Value

Balanced

HIGHESTRETURN

LOWESTRETURN

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

LargeStocks

LargeStocks

LargeStocks

LargeStocks

LargeStocks

SmallStocks

SmallStocks

SmallStocks

SmallStocks

SmallStocks

Int’lStocks

Int’lStocks

Int’lStocks

Int’lStocks

Int’lStocks

LT Gov’tBonds

LT Gov’tBonds

LT Gov’tBonds

LT Gov’tBonds

LT Gov’tBonds

LargeStocks

30 DayT-Bills

30 DayT-Bills

30 DayT-Bills

30 DayT-Bills

LT Gov’tBonds

SmallStocks

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

LT Gov’tBonds

30 DayT-Bills

SmallStocks

LargeStocks

Int’lStocks

Asset Class Winners and Losers

Potential Benefits of Diversification

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Annual Returns for 2004 - 2008

Diversifying Across Asset Classes

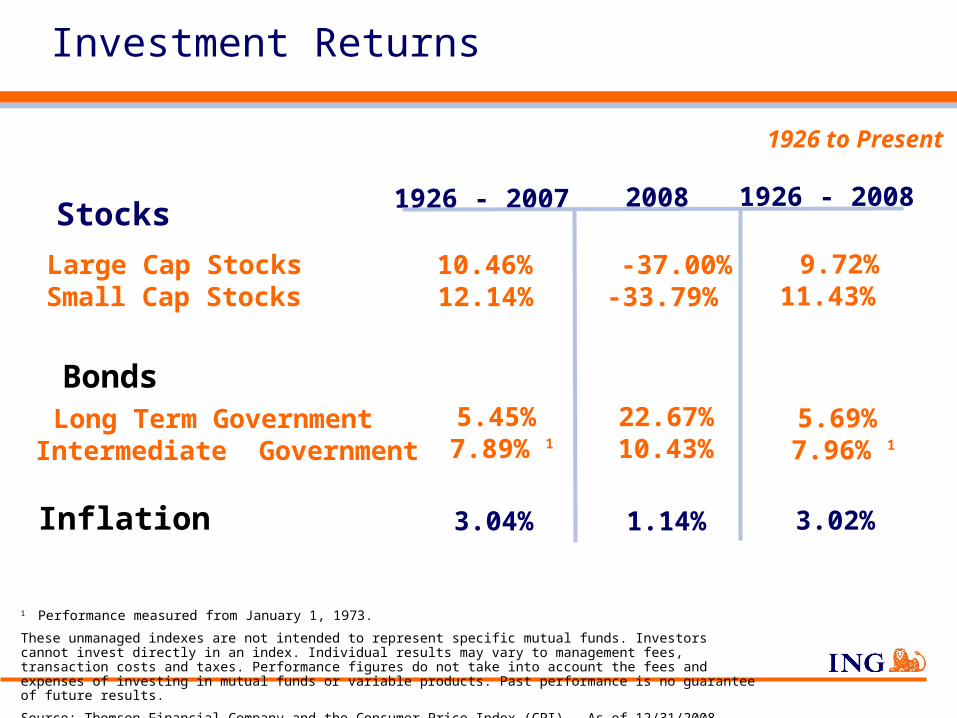

Stocks

Large Cap StocksSmall Cap Stocks

Long Term GovernmentIntermediate Government

Inflation

2008

-37.00%-33.79%

22.67%10.43%

1.14%

1926 - 2007

10.46%12.14%

5.45%7.89% 1

3.04%

Bonds

1926 - 2008

9.72%11.43%

5.69%7.96% 1

3.02%

1 Performance measured from January 1, 1973.

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company and the Consumer Price Index (CPI). As of 12/31/2008.

1926 to Present

Investment Returns

10.74%9.83%

10.52%8.44%

3.58%

10.76%10.80%

9.31%7.96%

1

4.53%

7.32%7.43%

9.32%6.74%

2.78%

Stocks

Large Cap StocksSmall Cap Stocks

Long Term GovernmentIntermediate Government

Inflation

Bonds

1980 - 2008 1970 - 2008 1990 - 2008

1 Performance measured from January 1, 1973.

These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company and the Consumer Price Index (CPI). As of 12/31/2008.

1970, 1980, 1990 to Present

Investment Returns

The Importance of Diversification

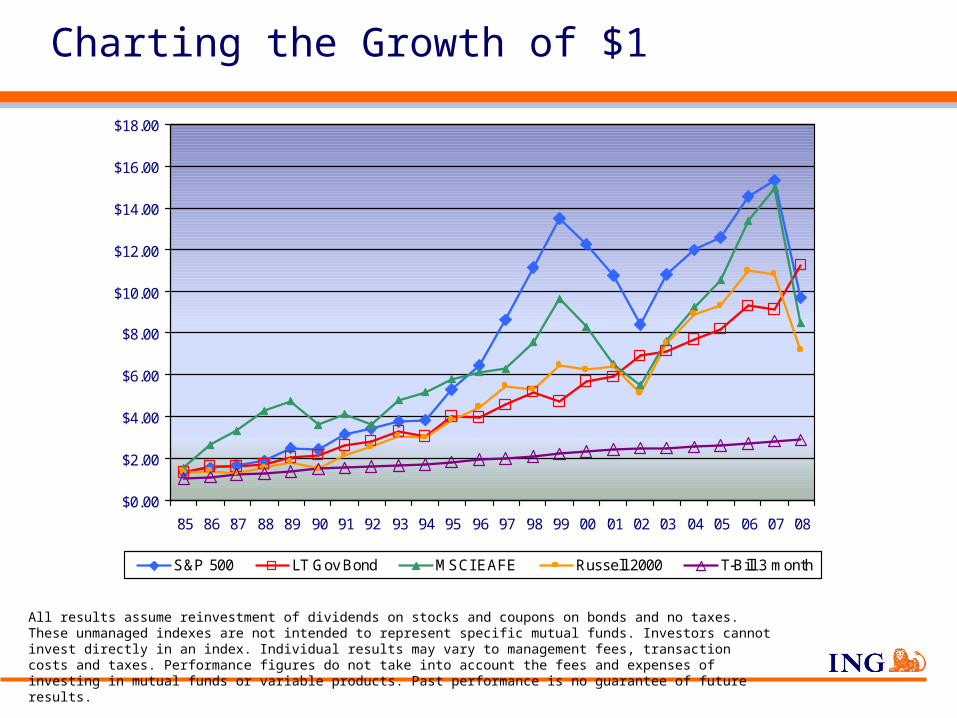

Small Stocks - 5 Years(Russell 2000)

Sector leaders are based on annual index returns with dividends reinvested (1980 - 2008)

Source: Thomson Financial Company

International Stocks - 11 Years(MSCI EAFE)

Large Stocks - 6 Years(S&P 500)

Bonds - 7 Years(Barclays Capital Credit Bond Index)

All results assume reinvestment of dividends on stocks and coupons on bonds and no taxes. These unmanaged indexes are not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company. Period 1/1/1985 – 12/31/2008.

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

'85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08

S&P 500 LT Gov Bond MSCI EAFE Russell 2000 T-Bill 3 month

Charting the Growth of $1

Both John and Barbara saw their $10,000 investment in common stocks drop to $7,846 in the month of October 1987.

The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments. Source: Thomson Financial Company.

John: Sold off his stocks and reinvested in 3 month U.S. Treasury Bills.

As of December 31, 2008, his investment reflected:

Average Annual Return

Cumulative ReturnIndex

T-Bill (3 Month Yield) 4.28% 142.71%John

Account Balance

$19,043

Barbara: Held on to her stocks. As of December 31, 2008, her investment reflected:

S&P 500 Composite Total Return 8.66% 480.53%Barbara $45,548

A Tale of Two Investors

Value of $10,000 invested in the securities included in the S&P 500 Index January 1, 1973:

Unlike CDs, which are insured by the FDIC and offer a fixed rate of return, the principal value and investment return for equities will fluctuate with changes in market conditions. All results assume reinvestment of dividends on stocks and coupons on bonds and no taxes. Past performance is no indication of future results. Indices are unmanaged and not available for direct investments.

Source: Thomson Financial Company

$5,000

$5,500

$6,000

$6,500

$7,000

$7,500

$8,000

$8,500

$9,000

$9,500

$10,000

S&P 500 $10,000 $9,514 $8,961 $9,391 $8,520 $5,729

'01/01/733 Months

Later6 Months

Later9 Months

Later1 Year Later

1 Year, 9 Months Later

Continued...Balance after 1 year, 9 months: $5,729

When the Going Gets Tough...

Scenario 1: $5,729 remained invested in securities (represented by the S&P 500)Scenario 2: $5,729 removed from the market and reinvested in an interest-bearing CD at 5%.

$5,000

$10,000

$15,000

$20,000

$25,000

S&P 500 $5,729 $7,704 $7,914 $10,312 $12,408 $24,303

CD at 5% $5,729 $5,870 $6,015 $6,316 $7,312 $9,332

01-Oct-74 6 Months Later 1 Year Later 2 Years Later 5 Years Later 10 Years Later Value as of 12/31/08

$239,486

$30,466

Unlike CDs, which are insured by the FDIC and offer a fixed rate of return, the principal value and investment return for equities will fluctuate with changes in market conditions. All results assume reinvestment of dividends on stocks and coupons on bonds and no taxes. The S&P 500 is an unmanaged index and is not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company.

$24,303

$9,332

When the Going Gets Tough...

Investing in the S&P 500 over a 10-year period ending 12/31/08.

-6% -4% -2% 0%-16% -14% -12% -8%-10%

All Trading Days

Minus 10 Best Days

Minus 20 Best Days

Minus 30 Best Days

Average Annual Return

-7.72%

-1.38%

Stock market performance is represented by price movements of the S&P 500 Index, an unmanaged stock market index that cannot be invested directly. This example assumes the reinvestment of dividends. Past performance is no guarantee of future results.

Source: Bloomberg

What a Difference a Day Makes!

-11.58%

-14.86%

Returns as of 12/31/08. Average Equity Investor returns were calculated by applying the retention rates of investors of mutual funds to the returns of the S&P 500. The S&P 500 is an unmanaged index and is not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Dalbar, 2009 and Thomson Financial Company.

Investment Returns 1989 - 2008

8.43%

1.87%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

S&P 500 Average EquityInvestor

Don’t Get Caught Chasing Returns

Timing the Market and Your Portfolio?

“Emotion is the enemy of all good investors”

“If 7,000 pros on Wall Street can’t do it, someone who (just) learned how a limit order works shouldn’t do it.”

- Ben Utley, certified financial planner and founder of Utley & Associates of Eugene, OR

Responding to market downturns

Don’t lose sight of your long-term objectives: Overall investment strategy Investment horizon timeline (years until retirement) Diversification through asset allocation Disciplined investing through dollar-cost averaging

Rose 936.42 pts, its largest point gain in its history (10/13/2008)

Declined 777.68 pts, its largest point loss in history (9/29/2008)

Rose 889.35 pts, its 2nd largest point gain in its history (10/28/2008)

The Dow Jones Industrial Average (DJIA):

Source: 2009 Dow Jones & Company

Comprehensive study showed that these events did not compel the majority of plan participants to: Withdraw from plan participation Reduce their contribution levels Increase their fund transfer activity

Market Volatility’s Impact on Investor Behavior

Top 10 Retirement Bloopers

1. You aren’t saving at all for retirement.Will Social Security subsidize your retirement needs?

2. You cashed out of your employer-sponsored retirement program or IRA. Did you pay over 35% in taxes including a 10% penalty?

3. You aren’t taking advantage of your employer-sponsored retirement program.Will you forgo the potential tax-deferred growth?

4. You don’t know the first thing about IRAs. Do you know IRAs also offer tax-deferred growth?

Top 10 Retirement Bloopers

5. You aren’t diversified.

Have you checked the Top 10 holdings of your investment options?

6. You didn’t learn from the Enron fiasco.

Is it prudent to invest heavily in employer stock?

7. You assume you’ll need less.

Upon reaching retirement, will your lifestyle change?

8. You’re not taking advantage of higher savings limits.

Do you know how Pension Reform affects you?

Top 10 Retirement Bloopers

9. You don’t have a smart withdrawal plan. Will you take a lump sum or opt for a systematic payout option?

10. You borrowed from your retirement plan when it wasn’t really an emergency. Do you know you’re missing out on potential market growthwhile paying yourself back?

Financial Roller Coaster

Is this cause for concern?

A reflection that market volatility is a way of life?

Most likely, a bit of both.

Recent volatility of the Dow Jones Industrial Average:

Don’t “throw in the towel” Some consolation for investors: You

weren’t alone! There’s no “surefire” strategy to

becoming wealthy We need to come to grips with what

happened and plan sensibly for the future

...What should I do?

I lost half my savings in a market slide...

Where within your portfolio did you incur the losses?

Was your account diversified? Did you skip bonds thinking they were too conservative?

Were your stock holdings broadly diversified by: Size? (small-, mid and large-cap stocks)

Style? (value and growth)

Sector? (retail, energy, utilities, etc.)

Gaining insight into why you may have lost so much: Questions to ponder...

How did I get here?

Key factor: After years of a Bull market we were faced with one of the worst Bear markets in history

Did we become conditioned to expect higher returns of the 90’s?

Maybe I shouldn’t I be allocated 100% in stocks. Maybe it’s 80, 70 or 60 percent.

Be careful not to go from one extreme to the next. Don’t allow emotions to drive you out of stocks completely.

After the recent market downswing, how should my money REALLY be diversified?

Where do I go from here?

Check the performance of your investment options Have they measured up to their peers?

Is your portfolio over-weighted in certain areas? Are you only in Large Cap? Have you considered Small Cap or Value

Stocks? Bonds?

Tip: Compare the Top 10 holdings of your investment options Are they similar among your investment options? Are you truly diversified?

Regrouping: Getting Back to Basics

Bear Markets(Decline & Recovery)

Amount of Decline

Aug ‘56 - Sep ‘58

Dec ‘61 - Sep ‘63

Feb ‘66 - May ‘67

Nov ‘68 - Mar ‘72

Jan ‘73 - Jul ‘80

Nov ‘80 - Nov ‘82

Aug ‘87 - Jul ‘89

Mar ‘00 - Sept ‘06

Duration of Bear# of Months

14.9

6.6

8.0

18.1

21.0

20.8

3.4

31.0

21.6%

28.0%

22.2%

36.1%

48.2%

27.1%

33.5%

47.5%

Recovery Period# of Months

11.3

14.5

7.0

21.7

70.5

2.8

20.0

48.0

Source: Neuberger Berman; Standard & Poor’s Corp. Past performance does not guarantee future results.

Oct ‘07 - ? ? ? ?

Bear Markets

The S&P 500 is an unmanaged index and is not intended to represent specific mutual funds. Investors cannot invest directly in an index. Individual results may vary to management fees, transaction costs and taxes. Performance figures do not take into account the fees and expenses of investing in mutual funds or variable products. Past performance is no guarantee of future results.

Source: Thomson Financial Company

Ret

urn

Dec 7, 1941Pearl Harbor

Nov 22, 1963Kennedy

AssassinationAug 2, 1990

Iraq Invades Kuwait

Feb 26, 1993World Trade

Center Bombed

Sep 11, 2001World Trade Center &

Pentagon Attacked

Cumulative Return of the

S&P 500 After Tragic Events

U.S. Market Recovery After Tragedy

Six month returns from start of Post-Crisis period

* Large and small cap are represented by the top and bottom deciles of NYSE based on market cap. Growth and Value are represented by the S&P 500/BARRA Growth and Value indices, respectively.

Source: Ned Davis Research, CRISP, Ibbotson

-3.6%-3.4%-3.1%-3.1%Feb ‘94Northridge Earthquake

2.2%5.5%-8.7%-1.3%May ‘86US Bombs Libya

0.3%-10.7%Jan ‘74Oil Embargo

26.5%24.8%Nov ‘62Cuban Missile Crisis

41.3%18.9%Aug ‘50Korean War

29.8%-5.8%Jan ‘42Pearl Harbor

ValueGrowthSmall Cap

Large

Cap *

Start of

Post-CrisisCrisis

Don’t Bet Against America

Sh

are

Pri

ce

$5

$8$8

$6$6

$10

5

10

January$100 10

March$100 16.6

April$100 12.5

May$100 12.5

June$100 16.6

February$100

20

Month:Investment:

Shares:

7

8

6

9

Dollar cost averaging/Systematic Investment plan does not ensure a profit nor guarantee against loss. Investors should consider theirfinancial ability to continue their purchases through periods of low price levels. The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results.

This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments.

Total Investment: $600 Total Shares Purchased: 88.2

Average Cost per Share: $6.80 Average Market Price per Share: $7.16

Investing Through Dollar Cost Averaging

$10

$6Sh

are

Pri

ce

5

10

7

8

6

9

January$600 60

March$0 0

April$0 0

May$0 0

June$0 0

February$0

0

Month:Investment:

Shares:

(from prior example)

Total Investment: $600 Total Shares Purchased: 60

Average Cost per Share: $10.00 Average Market Price per Share: $7.16

Dollar cost averaging/Systematic Investment plan does not ensure a profit nor guarantee against loss. Investors should consider theirfinancial ability to continue their purchases through periods of low price levels. The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results.

This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments.

...vs. Making a One-time Investment

72

average rate of return

=# of years for investment to

double

0% tax on 6% = 6% net

=72

6% net

12 years for investment to

double

Tax-deferred Investment

25% tax on 6% = 4.5% net

=72

4.5% net

16 years for investment to

double

Taxable Investment

Hypothetical example: $10,000 invested at age 20, earning 6% at 25% tax rate*

The Formula for Rule of 72:

* A 25% tax rate and an 6% rate of return are applied for this illustration. Actual rates may be significantly higher or lower which will impact the comparative results. The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments.

How long could it take to double your money?

A Rule to Save By: Rule of 72

Hypothetical example: $10,000 invested at age 20, earning 6% at 25% tax rate*

Tax-deferred Investment

12 years for investment to double

Age 20 $10,00032 20,00044 40,00056 80,00068 160,000

Total $160,000

minus Tax @ 25% 40,000

AFTER TAXES $120,000

Taxable Investment

16 years for investment to double

Age 20 $10,00036 20,00052 40,00068 80,000

Total $80,000

AFTER TAXES $80,000

* A 25% tax rate and an 6% rate of return are applied for this illustration. Actual rates may be significantly higher or lower which will impact the comparative results. The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments.

A Rule to Save By: Rule of 72

Terminology

Load - fee for entering (front-end) or exiting (back-end) a fund

Total fund expenses - annual expense applied to fund for management and administration (Funds ALWAYS have annual expenses, but NOT always loads)

NAV (Net Asset Value):

Price quoted on a daily basis

Is net of fund expenses (tiny fraction assessed daily)

Fund Terminology

Mutual funds: May be offered within a qualified retirement program (custodial account)

Offered at net asset value (NAV): NAV (price) quoted on a daily basis and may be tracked in newspapers

NAV is net of fund expenses: A tiny fraction is assessed daily

Investing in a mutual fund means purchasing shares of that fund

Mutual Fund Terminology

May be offered within a qualified retirement program (e.g., 401(k), 403(b), etc.)

Account values determined on a daily basis

Contributions toward the account purchase “units” of a pooled Separate Account The Separate Account then invests directly into the open market (e.g.,

directly into mutual funds)

AUVs are not tracked in newspapers

Variable Group Annuity Investment Options

Variable Group Annuity Investment Options

Each unit purchased has a value known as the Accumulation Unit Value (AUV)

Number of units owned x AUV = The account balance

Accumulation Unit Values:

Prospectus Each fund has one

Your retirement program has one (sometimes called a “disclosure booklet” or “disclosure information”)

Outlines “ground rules” of fund (e.g., fund objective)

Annual and Semi-Annual Report Each fund has one

Lists ALL fund holdings as of particular date

Provides manager analysis of performance

Statement of Additional Information (SAI) Addendum to prospectus

Fund Reporting/Sources of Information

Several types of stocks, bonds and funds

Different funds/varying investment objectives

Our role defined

Conclusion