AN OPTIMAL PRICING STRATEGY FOR A SOLAR MOBILE CHARGING SYSTEM IN...

110

CELL CHARGING CHALLENGES: AN OPTIMAL PRICING STRATEGY FOR A SOLAR MOBILE CHARGING SYSTEM IN AFRICA MEGAN J. WONG PROFESSOR WARREN B. POWELL SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF BACHELOR OF SCIENCE IN ENGINEERING DEPARTMENT OF OPERATIONS RESEARCH AND FINANCIAL ENGINEERING PRINCETON UNIVERSITY JUNE 2011

Transcript of AN OPTIMAL PRICING STRATEGY FOR A SOLAR MOBILE CHARGING SYSTEM IN...

CELL CHARGING CHALLENGES: AN OPTIMAL PRICING STRATEGY FOR A

SOLAR MOBILE CHARGING SYSTEM IN AFRICA

MEGAN J. WONG

PROFESSOR WARREN B. POWELL

SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF

BACHELOR OF SCIENCE IN ENGINEERING DEPARTMENT OF OPERATIONS RESEARCH AND FINANCIAL ENGINEERING

PRINCETON UNIVERSITY

JUNE 2011

ii

I hereby declare that I am the sole author of this thesis.

I authorize Princeton University to lend this thesis to other institutions or individuals for the purpose of scholarly research.

_________________________

Megan Wong

I further authorize Princeton University to reproduce this thesis by photocopying or by other means, in total or in part, at the request of other institutions or individuals for the purpose of scholarly research.

_________________________

Megan Wong

iii

ABSTRACT

Inspired by the possibility of integrating solar energy into the existing African mobile

charging industry for both personal profit and societal change, we examine aspects of

entrepreneurship from mathematical and business perspectives. We construct a prior belief from

current market estimates of costs and revenues in the solar industry and in Bababé, Mauritania,

respectively, and propose a Bayesian correlated linear belief structure for revenue as a function of

price. On the basis of profit-maximization, we compare myopic, value function approximation,

and look-ahead policies seeking to find the optimal price for a cell phone charge. A business

discussion with two contemporary case studies concludes the work.

iv

ACKNOWLEDGMENTS

My first and foremost thanks to Professor Powell who not only planted the first seed of

this idea but also never failed to share his enthusiasm for my project and encouragement to

“pretend you’re actually in Africa!” His patience, dedication, and creativity for senior theses are

really quite superhuman.

Thanks also to Mohsin Sohani and Ibrahima Ba at Hip Consult for the practical

motivation for my thesis as well as the numerous emails and Skype calls from Africa. This work

is only as important as it incorporates and affects real people and real lives, and I am incredibly

grateful for their practical insight and willingness to work together on this project.

Erik Limpaecher of Princeton Power Systems was also an inspiring example of Princeton

entrepreneurship in a similar field of solar innovation. Many thanks for an informative peek into

the “real engineering” aspect of solar energy and wisdom on the challenges of developing

applications in Africa in his tour and email correspondence.

For bringing me to where I am today, I am indebted to more people than I know. To the

Jack Kent Cooke Foundation which has opened a world of opportunity for me, to my friends who

have encouraged me daily, to my family who has taught me visibly what love is , and to Him who

is able to do more than immeasurably more than all we ask or imagine, thank you.

Soli Deo Gloria.

M.J.W.

v

CONTENTS

ABSTRACT ........................................................................................................................ iii

ACKNOWLEDGMENTS ......................................................................................................iv

FIGURES ............................................................................................................................vii

TABLES ............................................................................................................................ viii

CHAPTER 1 Introduction ......................................................................................................1

1.1 Mobiles Transforming Africa ...................................................................................2

1.2 The Challenge of Electricity .....................................................................................6

1.3 Existing Solutions ....................................................................................................8

1.4 Overview ..............................................................................................................10

CHAPTER 2 Cost and Revenue Assumptions........................................................................12

2.1 Cost Assumptions ..................................................................................................13

2.1.1 Solar Technology ...........................................................................................13

2.1.2 Current Market Analysis .................................................................................15

2.2 Revenue Assumptions ............................................................................................19

2.2.1 Bababé, Mauritania.........................................................................................20

2.2.2 Demand .........................................................................................................21

CHAPTER 3 Model.............................................................................................................23

3.1 Linear Belief Structure ...........................................................................................23

3.2 Specifying a Prior and a Truth Distribution..............................................................27

3.2.1 Truth Mean ....................................................................................................27

3.2.2 Truth Covariance ............................................................................................29

3.2.3 Prior Mean .....................................................................................................30

3.2.4 Prior Covariance.............................................................................................31

3.3 Mathematical Model ..............................................................................................32

3.3.1 State Variable .................................................................................................32

3.3.2 Exogenous Information ...................................................................................33

3.4.3 Decision.........................................................................................................33

3.3.4 Transition Function.........................................................................................33

3.3.5 Contribution Function .....................................................................................34

CHAPTER 4 Policy Optimization Overview .........................................................................35

vi

4.1 Pure Exploitation ...................................................................................................37

4.2 Boltzmann Exploration...........................................................................................38

4.3 Interval Estimation (IE) ..........................................................................................38

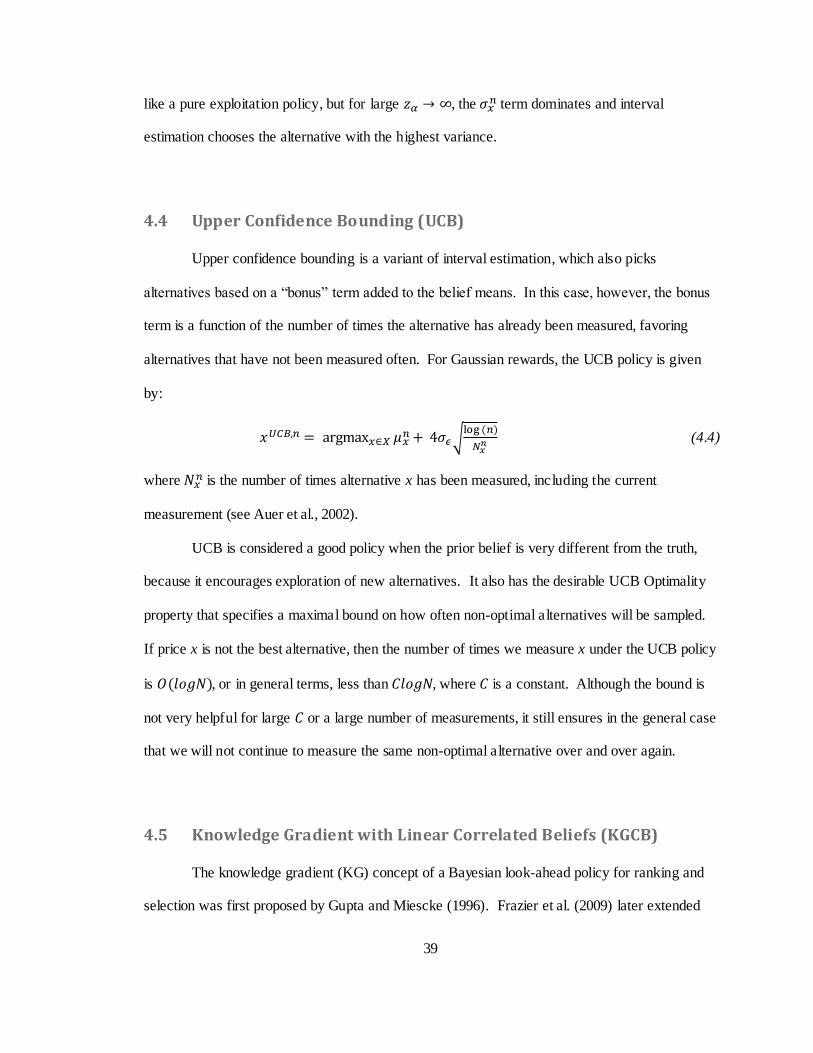

4.4 Upper Confidence Bounding (UCB)........................................................................39

4.5 Knowledge Gradient with Linear Correlated Beliefs (KGCB) ...................................39

4.6 Decision Tree (DT) ................................................................................................41

4.7 Restricted Pricing ..................................................................................................46

CHAPTER 5 Policy Optimization Analysis ...........................................................................51

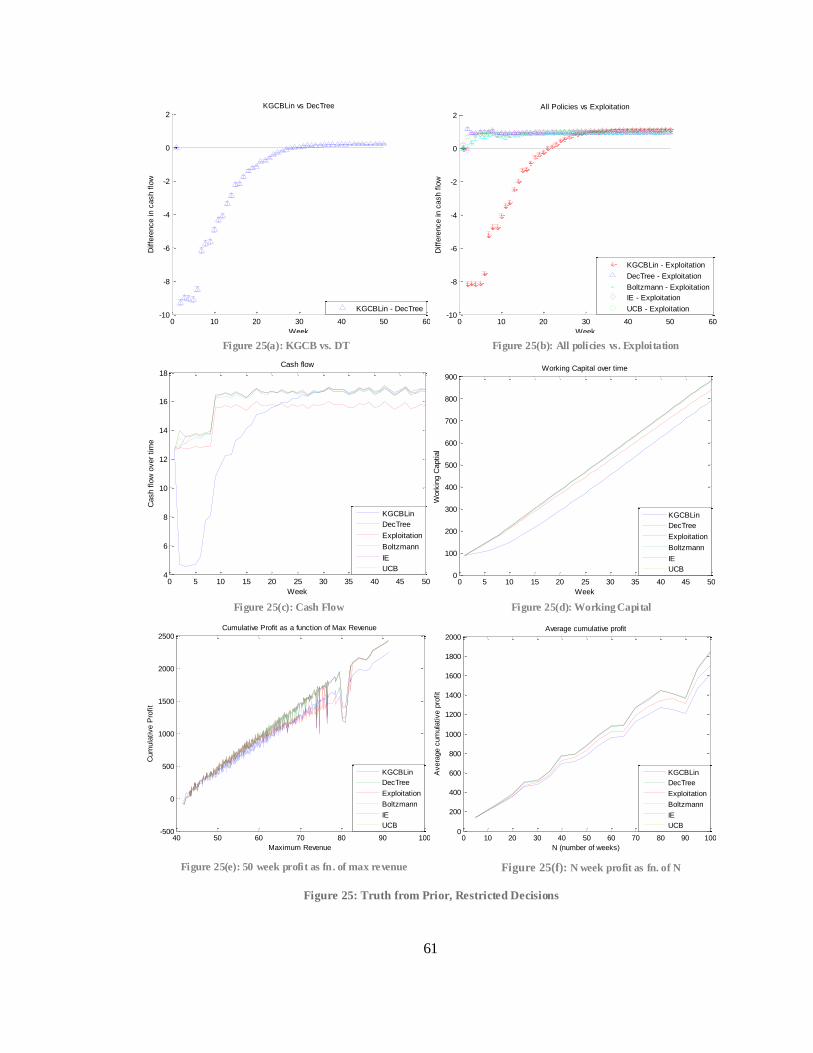

5.1 Worst Case Analysis ..............................................................................................52

5.2 Average Case Policy Comparison with Different Priors ............................................56

5.2.1 When the Truth Comes From the Prior Distribution ..........................................58

5.2.2 When the Prior is Overly Optimistic ................................................................63

5.2.3 Value Function Approximation vs. Look-ahead Policies....................................69

CHAPTER 6 Business Considerations ..................................................................................70

6.1 People: Who is involved.........................................................................................71

6.2 Opportunity: Customer, Market, and Competition ....................................................72

6.3 Context: African Entrepreneurship ..........................................................................78

6.4 Deal: Financing Decisions ......................................................................................79

6.5 Two Case Studies ..................................................................................................81

6.5.1 Bababé Entrepreneur.......................................................................................81

6.5.2 Energy For Opportunity ..................................................................................84

CHAPTER 7 Conclusion......................................................................................................86

7.1 Main Findings .......................................................................................................87

7.2 Assumptions Revisited and Future Research ............................................................88

7.3 Final Thoughts.......................................................................................................90

WORKS CITED...................................................................................................................92

APPENDIX .........................................................................................................................96

Appendix 1 Linear Prior ................................................................................................97

Appendix 2 Pessimistic Prior .........................................................................................99

vii

FIGURES

Figure 1: Mobiles in Africa (Ewing/Bloomberg Businessweek, 2007) ........................................1

Figure 2: African Mobile Market Growth (Africa & The Middle East Telecom, 2010) ................3

Figure 3: Sub-Saharan Africa Statistics (World Bank, 2008)......................................................4

Figure 4: Fisherman in Chenai, India (©AP images/ America.gov, 2007) ...................................5

Figure 5: Earth at Night (NASA, 2009) ....................................................................................6

Figure 6: Charging Shop in Kiberia, Kenya (GSMA) ................................................................7

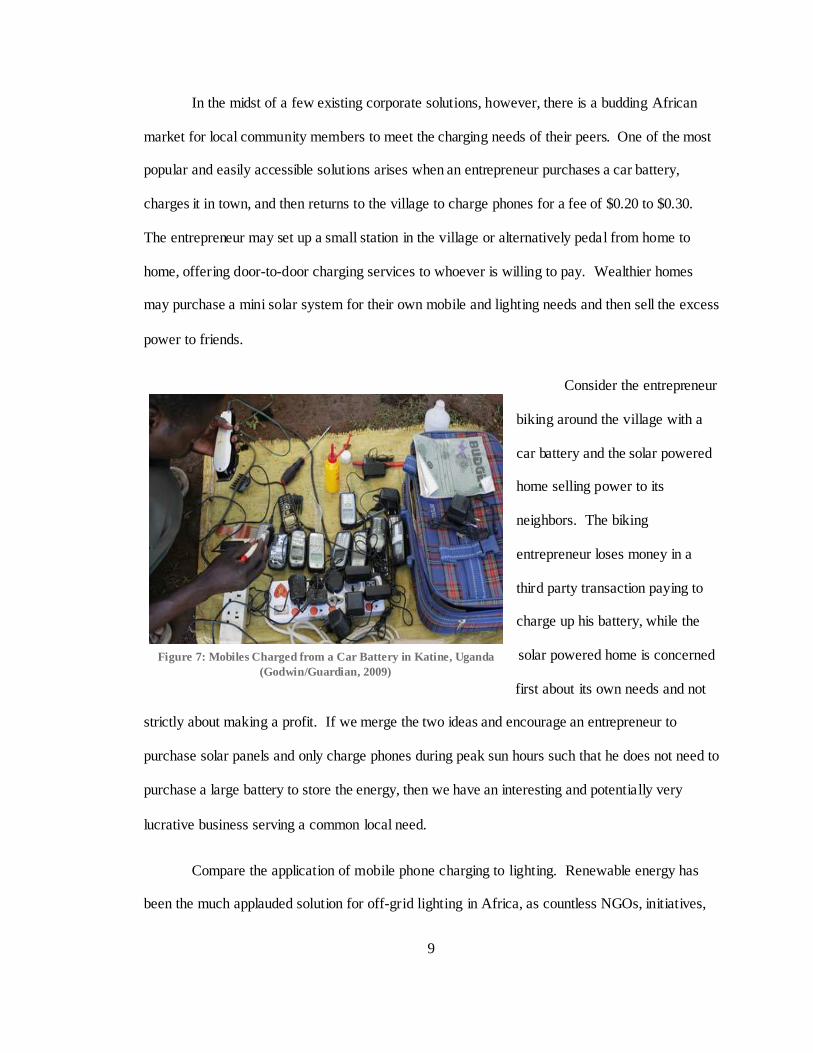

Figure 7: Mobiles Charged from a Car Battery in Katine, Uganda (Godwin/Guardian, 2009) .......9

Figure 8: Solar Cell Diagram (NASA, 2002) ..........................................................................13

Figure 9: How Solar Works (Young/QualityPoint Technologies, 2010) ....................................14

Figure 10: Solar Cost Breakdown (Frost & Sullivan, 2009) .....................................................15

Figure 11: Solar Module Prices..............................................................................................16

Figure 12: Estimated Solar Module Price with 95% Confidence Interval ..................................17

Figure 13: Map of Mauritania (Geographic Guide: Maps of Africa) .........................................20

Figure 14: Point Estimates for True Demand Means................................................................28

Figure 15: 99 Generated Truths .............................................................................................30

Figure 16: Truths and Priors for Weekly Revenue ...................................................................31

Figure 17: Decision Tree (Initial) ...........................................................................................43

Figure 18: Sample Decision Tree (One Iteration Back)............................................................45

Figure 19: Sample Decision Tree (Two Iterations Back)..........................................................46

Figure 20: Decision Tree Algorithm.......................................................................................50

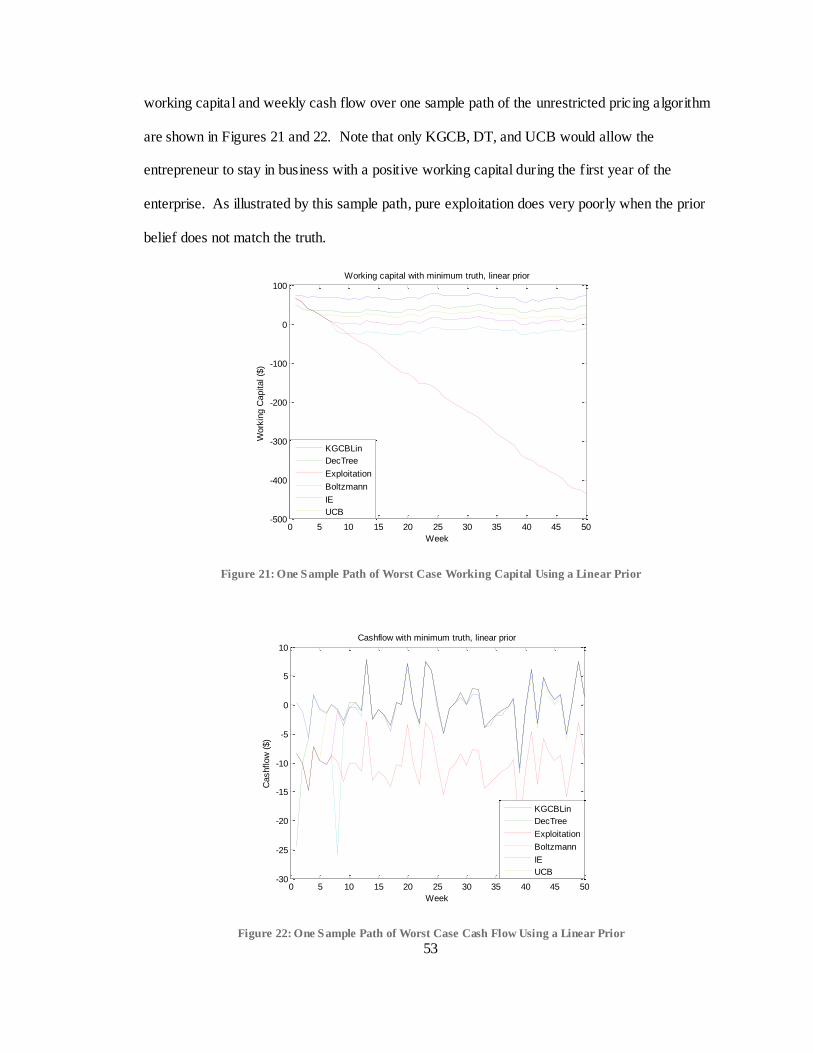

Figure 21: One Sample Path of Worst Case Working Capital Using a Linear Prior ....................53

Figure 22: One Sample Path of Worst Case Cash Flow Using a Linear Prior ............................53

Figure 23: Algorithm Choices for Worst Case Sample with a Linear Prior ................................55

Figure 24: Truth from Prior, Unrestricted Decisions................................................................60

Figure 25: Truth from Prior, Restricted Decisions ...................................................................61

Figure 26: Overly Optimistic Prior, Unrestricted Decisions .....................................................64

Figure 27: Overly Optimistic Prior, Restricted Decisions .........................................................67

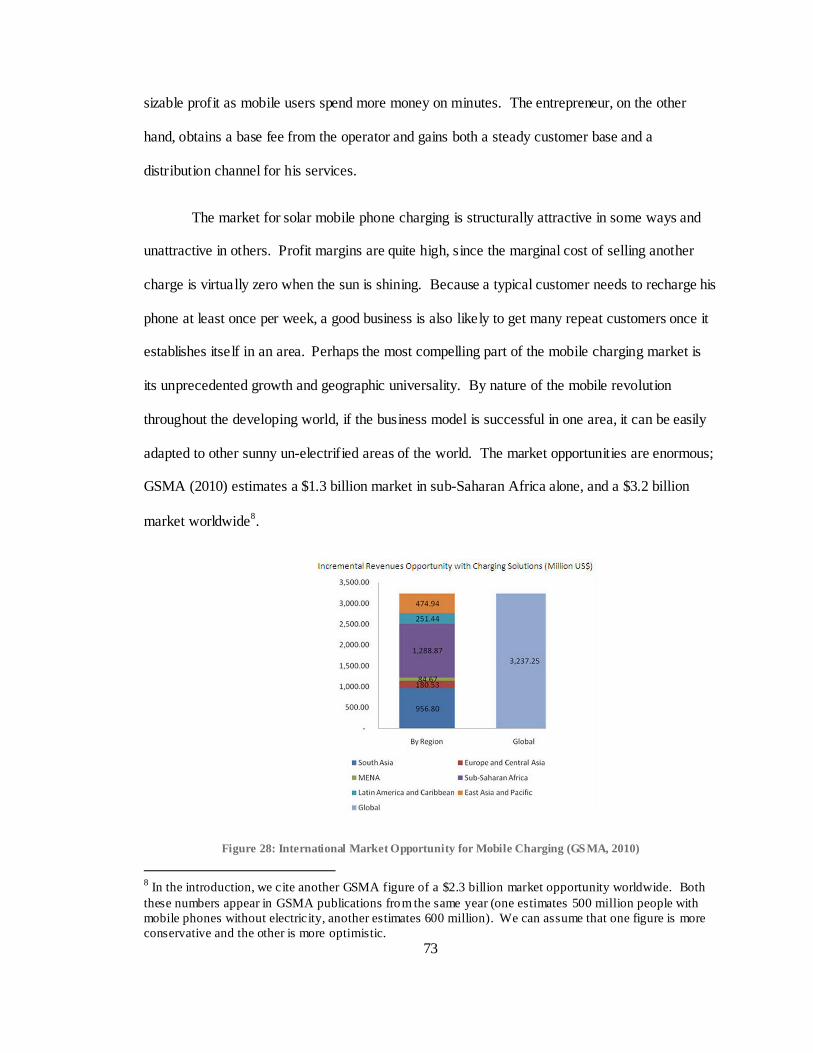

Figure 28: International Market Opportunity for Mobile Charging (GSMA, 2010) ....................73

Figure 29: Changes in Demand and Supply in the Market for Cell Phone Charging...................82

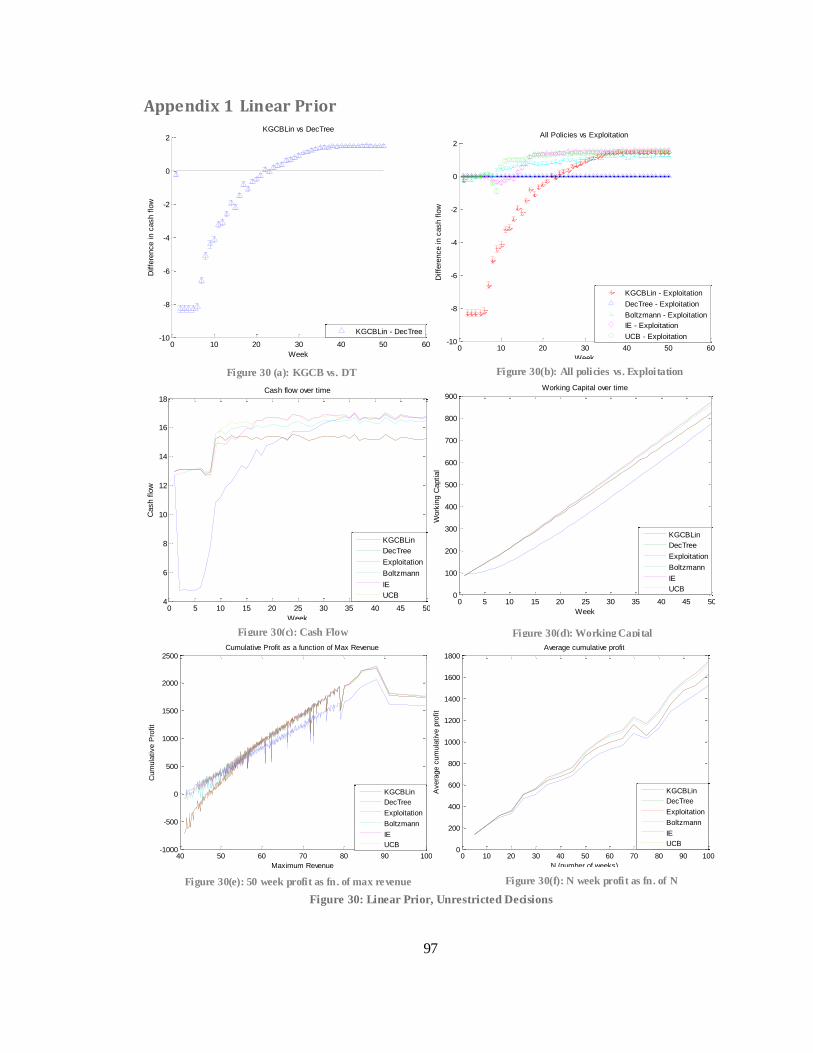

Figure 30: Linear Prior, Unrestricted Decisions ......................................................................97

Figure 31: Linear Prior, Restricted Decisions ..........................................................................98

Figure 32: Pessimistic Prior, Unrestricted Decisions ...............................................................99

Figure 33: Pessimistic Prior, Restricted Decisions ................................................................. 101

viii

TABLES

Table 1: Initial Capital Expenditures ......................................................................................17

Table 2: Weekly Operating Costs...........................................................................................19

Table 3: Summary of Supply and Demand Assumptions .........................................................22

Table 4: Estimates for True Demand at Various Prices ............................................................28

Table 5: Theta Estimates for True Demand.............................................................................28

Table 6: Worst Case Truth and Linear Belief Means ...............................................................52

Table 7: Solar vs. Battery vs. Generator Assumptions .............................................................76

Table 8: Solar vs. Battery vs. Generator Comparison...............................................................77

Table 9: Loan Options...........................................................................................................80

CHAPTER 1 Introduction

Figure 1: Mobiles in Africa (Ewing/Bloomberg Businessweek, 2007)

She pounds grain with a mortar and pestle. She uses kerosene lanterns for lighting, a

wood stove for cooking, and a machete for cutting grass. Her small mud home houses herself,

her husband, and her six children. She is without electricity, refrigeration, education, or sizeable

income, and yet - her family owns a cell phone.

Paradoxical though it seems, this description is becoming more and more common

throughout the developing world. On an international scale, mobile phones have bridged the

divide between rich and poor with greater speed and ubiquity than landline phones, radios,

2

computers, cars, and even electricity. Three inherent features of cell phones enable rapid

adoption and expansion. First, unlike cars or computers, a basic mobile phone can be purchased

for a reasonable price in Africa; $20 for a new phone and much less for a used phone (Ewing,

2007). In a developing society, low initial and maintenance costs are particularly vital to wide

consumer adoption. Second, mobile expansion requires minimal infrastructure needs. While

fixed line phones and computers require a constant supply of energy, mobile phones do not

necessitate connection to the grid. Finally, mobile phones are prime candidates for innovative

and diverse applications across regions. Providing a unique mix of practicality for the

businessman making a sale and of entertainment for the student chatting with a friend, mobile

phones stand as a symbol of globalization and an end to economic isolation in today’s world.

In this introduction, we discuss the obstacle of charging a phone in an un-electrified

village and consequent opportunities for an entrepreneur. In a village where lack of electricity

and telephone wires still prevents the advent of fixed lines, how do mobile phone users find an

energy source to charge their cell phones regularly? Can an entrepreneur start a profitable

business selling phone charging services to an off-grid village? The scarcity of infrastructure

coupled with the flexibility of both cell phone technology and individual charging needs lend

themselves well towards renewable energy and unconventional means of energy distribution.

1.1 Mobiles Transforming Africa

"The cell phone is the single most transformative technology for development."

– Jeffrey Sachs, Columbia University (Bloomberg Businessweek, 2007)

3

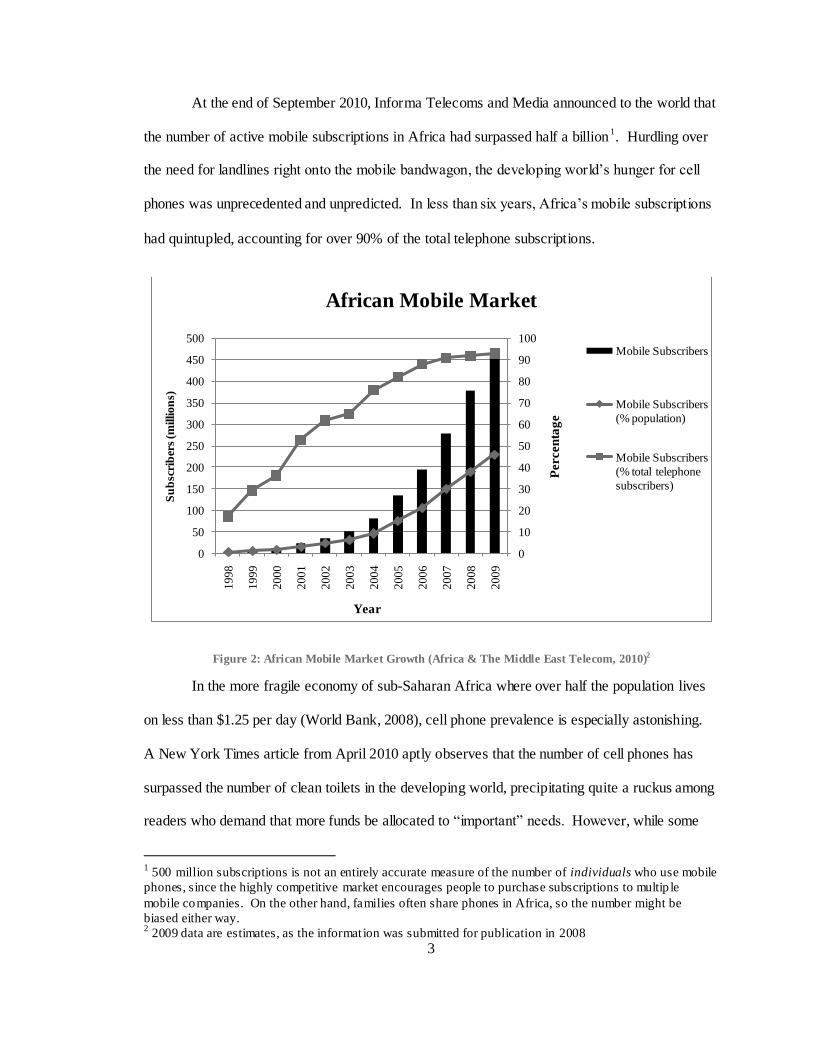

At the end of September 2010, Informa Telecoms and Media announced to the world that

the number of active mobile subscriptions in Africa had surpassed half a billion1. Hurdling over

the need for landlines right onto the mobile bandwagon, the developing world’s hunger for cell

phones was unprecedented and unpredicted. In less than six years, Africa’s mobile subscriptions

had quintupled, accounting for over 90% of the total telephone subscriptions.

Figure 2: African Mobile Market Growth (Africa & The Middle East Telecom, 2010)2

In the more fragile economy of sub-Saharan Africa where over half the population lives

on less than $1.25 per day (World Bank, 2008), cell phone prevalence is especially astonishing.

A New York Times article from April 2010 aptly observes that the number of cell phones has

surpassed the number of clean toilets in the developing world, precipitating quite a ruckus among

readers who demand that more funds be allocated to “important” needs. However, while some

1 500 million subscriptions is not an entirely accurate measure of the number of individuals who use mobile

phones, since the highly competitive market encourages people to purchase subscriptions to multip le

mobile companies. On the other hand, families often share phones in Africa, so the number might be

biased either way. 2 2009 data are estimates, as the informat ion was submitted for publication in 2008

0

10

20

30

40

50

60

70

80

90

100

0

50

100

150

200

250

300

350

400

450

500

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Percen

tag

e

Su

bsc

rib

ers

(million

s)

Year

African Mobile Market

Mobile Subscribers

Mobile Subscribers

(% population)

Mobile Subscribers

(% total telephone

subscribers)

4

may complain that the modern focus misplaced on mobile phones above more imminent

necessities like clean water, adequate sanitation, and paved roads implies a gross caricature of

today’s obsession with technology, the reality is that mobile phones have revolutionized the

African economy. Though phone minutes and charging sometimes cost over half a family’s daily

wages, there are direct economic explanations for this widespread mobile popularity.

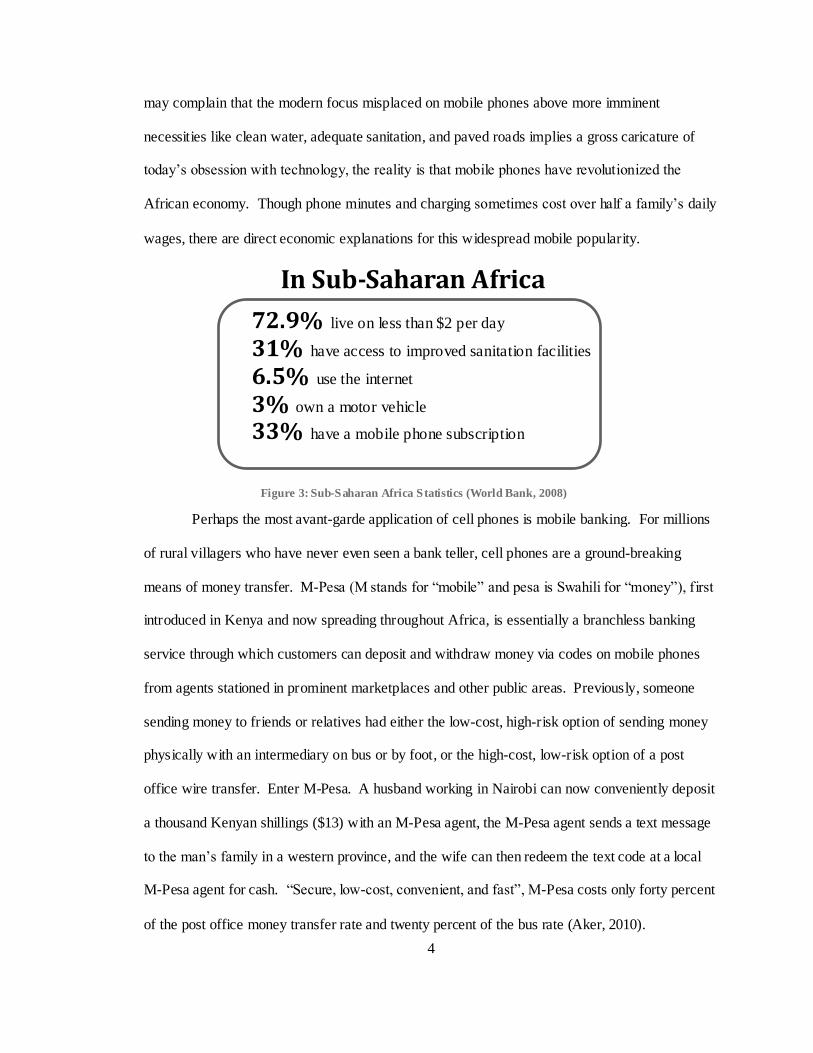

Perhaps the most avant-garde application of cell phones is mobile banking. For millions

of rural villagers who have never even seen a bank teller, cell phones are a ground-breaking

means of money transfer. M-Pesa (M stands for “mobile” and pesa is Swahili for “money”), first

introduced in Kenya and now spreading throughout Africa, is essentially a branchless banking

service through which customers can deposit and withdraw money via codes on mobile phones

from agents stationed in prominent marketplaces and other public areas. Previously, someone

sending money to friends or relatives had either the low-cost, high-risk option of sending money

physically with an intermediary on bus or by foot, or the high-cost, low-risk option of a post

office wire transfer. Enter M-Pesa. A husband working in Nairobi can now conveniently deposit

a thousand Kenyan shillings ($13) with an M-Pesa agent, the M-Pesa agent sends a text message

to the man’s family in a western province, and the wife can then redeem the text code at a local

M-Pesa agent for cash. “Secure, low-cost, convenient, and fast”, M-Pesa costs only forty percent

of the post office money transfer rate and twenty percent of the bus rate (Aker, 2010).

Figure 3: Sub-Saharan Africa Statistics (World Bank, 2008)

In Sub-Saharan Africa

72.9% live on less than $2 per day

31% have access to improved sanitation facilities

6.5% use the internet

3% own a motor vehicle

33% have a mobile phone subscription

5

Increased communication also leads to increased market transparency and fewer third

party inefficiencies. The age when farmers and fishermen paid outside dealers a small sum to

learn crop and fish prices at the market is becoming obsolete; local artisans can now text a market

salesman in the morning, learn the going prices

for the day, and then bring the most sought-after

products to the market in the evening. This

system not only decreases product waste and

increases profits, but also reduces variation

among salespeople and results in a better price

for households. Robert Jensen at Harvard

University estimates that in a small South Indian coastal city between 1997 and 2001, the time

period capturing the first introduction of phones to 60% penetration levels among fishermen and

market salesmen, violations of the Law of One Price decreased from 50-60% of market pairs to

essentially zero. As prices converge, arbitrage opportunities decrease and the net result is

positive for almost all parties. Jensen observes that “fishermen’s profits increased on average by

8 percent while the consumer price declined by 4 percent and consumer surplus in sardine

consumption increased by 6 percent.” Not only do people benefit from a monetary gain, but they

also save time as the consumer no longer has to shop between multiple vendors to get a fair price

and the fisherman no longer has to travel and find a physical third party to acquire market

information.

Without the aid of governments or subsidies or NGOs, the theoretical benefits of the

positive externality of mobile phones seem to materialize clearly in Africa and the rest of the

developed world. MIT studies claim that “adding an additional ten mobile phones per 100 people

boosts a typical developing country’s GDP growth by 0.6 percent” (EPROM, 2009). As

entrepreneurs innovate, regional-specific applications like M-Pesa emerge to serve a local need.

Figure 4: Fisherman in Chenai, India (©AP images/

America.gov, 2007)

6

As information becomes more readily available, market prices become more uniform and people

gain time and money on the whole. As communication is simplified, the burdens of finding

customers for a small business, organizing large numbers of volunteers for a service project, and

calling hospitals during an emergency are simultaneously alleviated.

1.2 The Challenge of Electricity

Pervasive and influential though mobile phones are, they may not be the “silver bullet” of

African development that some authors have proposed. There are significant obstacles for both

the provider and the consumer inherent to Africa’s long history of development and lack of

infrastructure.

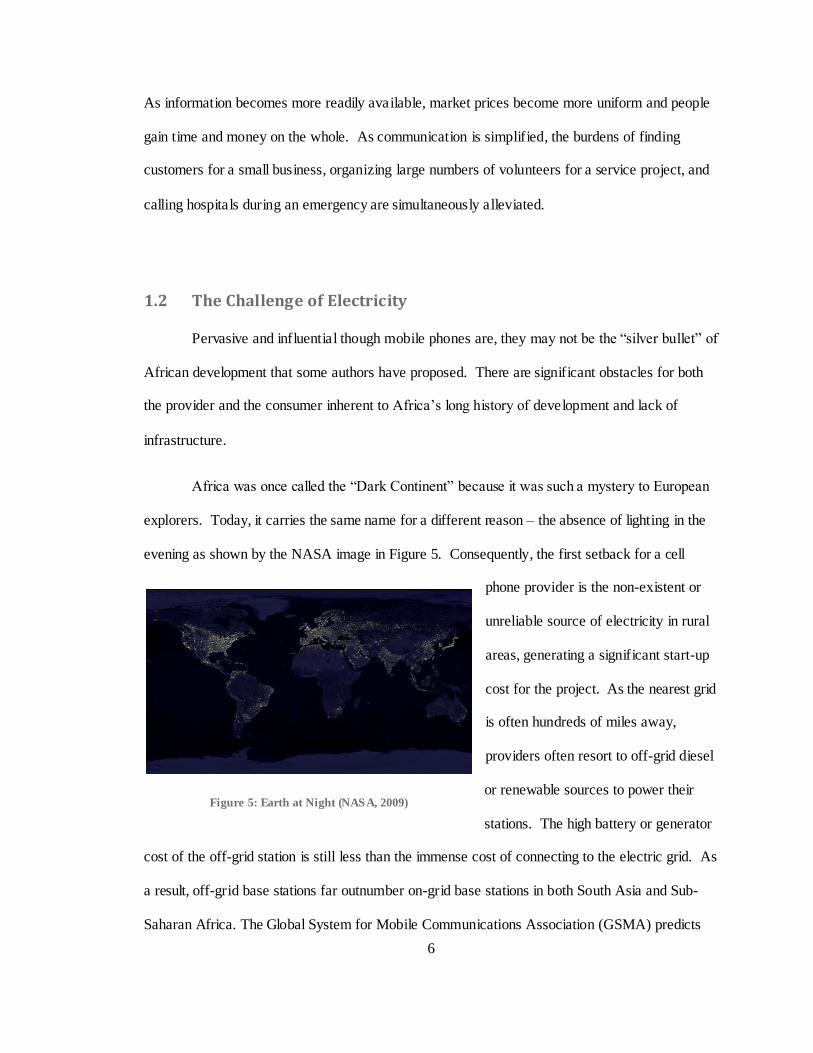

Africa was once called the “Dark Continent” because it was such a mystery to European

explorers. Today, it carries the same name for a different reason – the absence of lighting in the

evening as shown by the NASA image in Figure 5. Consequently, the first setback for a cell

phone provider is the non-existent or

unreliable source of electricity in rural

areas, generating a significant start-up

cost for the project. As the nearest grid

is often hundreds of miles away,

providers often resort to off-grid diesel

or renewable sources to power their

stations. The high battery or generator

cost of the off-grid station is still less than the immense cost of connecting to the electric grid. As

a result, off-grid base stations far outnumber on-grid base stations in both South Asia and Sub-

Saharan Africa. The Global System for Mobile Communications Association (GSMA) predicts

Figure 5: Earth at Night (NASA, 2009)

7

that there will be 639,000 off-grid base stations in the developing world by 2012 (Taverner,

2010). While off-grid is not necessarily a negative aspect, renewable sources in particular

introduce added unpredictability. If a village has a week of cloudy or windless days, the tower

may well be out of service after the reserve battery life is drained.

The other setbacks for mobile operators in the developing world are more subtle with less

direct solutions. Imagine receiving a call to service a cell phone tower miles away on unpaved

roads or arriving at a station one morning to find the generator stolen and wires snipped. There

are obstacles both in the undeveloped environment itself and in impoverished populations that

always house a few desperate individuals willing to do anything for money. Customers often

bear this cost, resulting in higher per-minute charges in rural areas than urban areas. In Kenya,

Safaricom loses a vehicle a month on unpaved roads

and some mobile companies resort to armed guards to

protect their fuel, generators, and other equipment

from widespread theft (Ewing, 2007). Establishing a

new business in any area is difficult; with the

additional challenges of rampant theft and vandalism,

operators face unique maintenance hurdles.

In un-electrified areas, the primary obstacle

for the mobile consumer lies in the regular charging

of the cell battery. The NY Times featured an article

describing one Kenyan woman’s plight:

Every week, Ms. Ruto walked two miles to hire a motorcycle taxi for the three-hour ride to Mogotio, the nearest town with electricity. There, she dropped off her cell phone at a store that recharges phones for 30 cents. Yet the service was in such demand that she had

to leave it behind for three full days before returning (Rosenthal, 2010).

Figure 6: Charging Shop in Kiberia, Kenya

(GSMA)

8

Ms. Ruto is one of 500 million mobile users around the world without direct access to electricity,

according to GSMA and Wireless Intelligence research. These users typically pay per charge at a

local shop every week or every day, depending on their phone usage. In Kenya, it is estimated

that one-third of the mobile operating costs go to power instead of airtime (GSMA, 2010),

encouraging users to text rather than call whenever possible. More and more studies are being

conducted regarding off-grid mobile phone charging as companies grasp the magnitude of such a

market. When an individual gains access to a steady charging source, field studies suggest that

the mobile operator’s ARPU (average revenue per user) increases by at least ten percent because

the consumer feels comfortable making more calls. With 500 million customers, this

accumulates to a $2.3 billion market opportunity for network operators (GSMA, 2010).

1.3 Existing Solutions

Where there is an opportunity for profit, corporations and individuals will certainly rise to

the challenge. Digicel, Safaricom, and other mobile companies have already introduced solar

phones with miniature solar panels and batteries built into the back of the phone, allowing users

to leave their phone out during the day to charge. Safaricom and Ericsson have opened village

mobile charging stations in select areas monitored by a guard or other personnel, where people

can plug their phones into the charging dock for a small fee (GSMA, 2010). Since February

2009, GSMA, in partnership with mobile operators and manufacturers, has pioneered the

Universal Charging Solution initiative in hopes of standardizing all mobile chargers with an

energy-efficient micro-USB by 2012. Opening the possibility of a world without duplicate

chargers and with a 50% energy reduction in phone usage, this solution has garnered much

attention and many awards in the last two years.

9

In the midst of a few existing corporate solutions, however, there is a budding African

market for local community members to meet the charging needs of their peers. One of the most

popular and easily accessible solutions arises when an entrepreneur purchases a car battery,

charges it in town, and then returns to the village to charge phones for a fee of $0.20 to $0.30.

The entrepreneur may set up a small station in the village or alternatively pedal from home to

home, offering door-to-door charging services to whoever is willing to pay. Wealthier homes

may purchase a mini solar system for their own mobile and lighting needs and then sell the excess

power to friends.

Consider the entrepreneur

biking around the village with a

car battery and the solar powered

home selling power to its

neighbors. The biking

entrepreneur loses money in a

third party transaction paying to

charge up his battery, while the

solar powered home is concerned

first about its own needs and not

strictly about making a profit. If we merge the two ideas and encourage an entrepreneur to

purchase solar panels and only charge phones during peak sun hours such that he does not need to

purchase a large battery to store the energy, then we have an interesting and potentially very

lucrative business serving a common local need.

Compare the application of mobile phone charging to lighting. Renewable energy has

been the much applauded solution for off-grid lighting in Africa, as countless NGOs, initiatives,

Figure 7: Mobiles Charged from a Car Battery in Katine, Uganda

(Godwin/Guardian, 2009)

10

and applications have been created for this specific purpose. However, by their intermittent

charging nature and existing technological structure, mobile phones, a much less-researched

topic, are even more conducive to renewable energy than lighting. Compared to lighting which

requires energy every evening after sundown, mobile phone charging is far more adaptable to the

individual. If the user knows he needs to make a long call the next day, he can prepare in

advance and fully charge his phone the day before. The time between charges is variable and

highly dependent on user behavior and decision-making. A prudent user, alerted by the

remaining battery life of his device, can plan his calls and charge accordingly to make the most

important calls at the best times. While renewable energy lighting requires an expensive battery

to store energy collected during the day, batteries are inherent to cell phones and entail no

additional investment. Thus, Africa, a continent latent with solar energy, coupled with mobile

phone charging and local entrepreneurship bridges a broad span of potential.

1.4 Overview

In this thesis, we examine the profitability of a small scale enterprise charging cell

phones from a solar module. Although there are many factors that affect profitability, we choose

to study the optimal pricing problem in depth, as this is the most salient numerical factor an

entrepreneur can control. Given prior intuition about the revenue generated using a discretized

set of prices, we seek to understand how the entrepreneur might logically develop pricing

strategies that utilize his prior belief, but also explore new prices. In Chapter 2, we gather market

information to specify cost and revenue assumptions in the particular context of Bababé,

Mauritania. This will be used as the basis of our prior belief on revenue in Chapter 3, where we

introduce the relevant notation and mathematical framework to use a correlated linear belief

structure in which the entrepreneur believes that revenue is a polynomial function of price.

11

In Chapter 4, we propose various policies to discover the optimal revenue. Representing

a diverse range of strategies, these policies fall into the main categories of myopic policies, value

function approximation policies, and look-ahead policies. Given these policies, we examine

worst case performance and average case performance with different prior beliefs in Chapter 5.

We investigate how the policies compare not only when the prior belief is close to the true

revenue distribution, but also when the entrepreneur has been overly optimistic or pessimistic in

his projections.

We provide a broad business framework in Chapter 6 to account for other aspects of the

enterprise besides optimal pricing. Supplemented by case studies with recent examples of a small

business and a large NGO’s successful use of solar power to charge phones and other applications,

the analysis is highly qualitative and discusses the cell phone charging market, customer, and

competition in more detail. The narrow view of Chapters 4 and 5 broadens to a wider scope in

Chapter 6 as we discuss the competitive advantage of a solar charging system and present ways to

improve the entrepreneur’s business model to minimize exogenous risk.

In the conclusion, we summarize the work to draw broad lessons and propose areas for

future research. In particular, we identify the key assumptions that are too restrictive and suggest

alternative approaches to the optimal pricing problem.

12

CHAPTER 2 Cost and Revenue Assumptions

Although business success is dependent on many factors, technical details aside, the most

important numerical factor an entrepreneur can control is price. If he believes that revenue is a

function of the price he charges, how does he choose the price that maximizes revenue? In reality,

the entrepreneur has a prior notion of the revenue he can garner at any given price and a strategy

to utilize his prior belief. He may, for example, take a game theoretical approach and just try to

undercut the price that his competitors at charging shops have set for a cell phone charge.

However, he is not sure that this is the true profit-maximizing price.

To clearly formulate the entrepreneur’s question, we first establish the macro

assumptions necessary to determine cost and revenue estimates. This entails current research on

both the solar industry on the cost side and the potential market of choice on the revenue side.

Note that although we have to make several assumptions about the true cost and revenue

distributions in a particular setting, this approach is easy to adapt to new situations when the truth

does not exactly mirror the suppositions proposed in this chapter.

13

2.1 Cost Assumptions

To estimate the entrepreneur’s initial capital expenditures at the onset of this start-up, we

must understand the fundamentals of solar technology and what traditional parts are necessary in

this context. Then we can study current market prices for various parts and obtain a basic cost

model for the solar module and other physical assets.

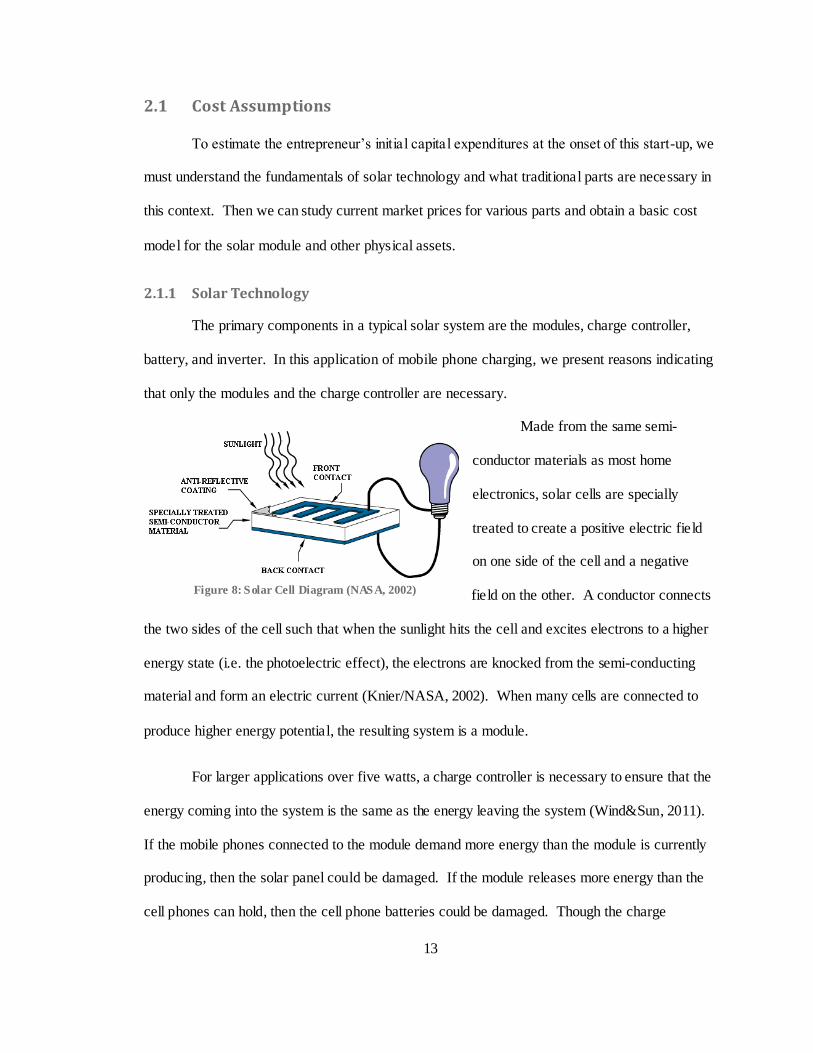

2.1.1 Solar Technology

The primary components in a typical solar system are the modules, charge controller,

battery, and inverter. In this application of mobile phone charging, we present reasons indicating

that only the modules and the charge controller are necessary.

Made from the same semi-

conductor materials as most home

electronics, solar cells are specially

treated to create a positive electric field

on one side of the cell and a negative

field on the other. A conductor connects

the two sides of the cell such that when the sunlight hits the cell and excites electrons to a higher

energy state (i.e. the photoelectric effect), the electrons are knocked from the semi-conducting

material and form an electric current (Knier/NASA, 2002). When many cells are connected to

produce higher energy potential, the resulting system is a module.

For larger applications over five watts, a charge controller is necessary to ensure that the

energy coming into the system is the same as the energy leaving the system (Wind&Sun, 2011).

If the mobile phones connected to the module demand more energy than the module is currently

producing, then the solar panel could be damaged. If the module releases more energy than the

cell phones can hold, then the cell phone batteries could be damaged. Though the charge

Figure 8: Solar Cell Diagram (NASA, 2002)

14

controller prevents both of these undesirable situations, Hankins in his guide Solar Electric

Systems for Africa reports that only half of the solar systems in Kenya took this precaution in

1995. Although people looking to make a quick profit may be frugal on up-front costs, their lack

of foresight ultimately has long term consequences as the life of the system is significantly

compromised. Improper care of photovoltaic systems has given solar a rather poor reputation in

Africa in past years, but with the correct maintenance and the more robust parts sold today, solar

is an exceedingly viable option as an off-grid power source.

A battery is necessary for most applications when the energy is not used as it is produced.

In lighting applications, for example, batteries store energy collected from the sun during the day

and release energy for lighting at night. In this entrepreneurial setting, a battery storage system is

redundant because we plan to only charge phones when the sun is shining. If there is a stretch of

cloudy days, it is assumed that customers will know that they cannot charge their phones until the

sun shines again, and will either find an alternative charging method or adjust their calling needs

appropriately.

Because electrons only travel one

direction in a module, solar applications usually

require an inverter to convert the direct current

(DC) energy collected from the sun into

alternating current (AC) energy required for most

home applications. Since cell phones are always

charged with direct current, the entrepreneur

has no need for an inverter unless he uses the

panel to charge other devices. In general, alternating current is used for most appliances because

it is easy to change voltage using a transformer. With alternating current, a power company can

Figure 9: How Solar Works (Young/QualityPoint

Technologies, 2010)

15

send electricity over long distances to homes using various voltages for safety and money-saving

reasons. Although low current allows electric companies to use smaller wires, high voltages are

also extremely dangerous. Thus, alternating current enables companies to exploit the tradeoff

between safety and speed in different areas.

For the entrepreneur in question, we only need to consider the solar module, charge

controller (for applications above five watts), and installation and set-up costs which include a

power strip to charge multiple phones at once.

2.1.2 Current Market Analysis

By examining current market prices for various solar components, we estimate the initial

cost for an entrepreneur setting up a solar micro-grid to charge phones. The most significant

upfront expense is the solar module, which consists of just over half the cost of the entire system,

as shown in the Frost & Sullivan breakdown in Figure 10. Because solar module prices are more

readily available than controller or

installation costs for the small applications

we evaluate for mobile charging3, we

estimate the controller and installation

costs as percentages of the module price.

To make the cost predictions as

general as possible, we approximate the

price of a solar module for a variety of

sizes. The power output is the most reliable indicator of price, since a compact, heavy solar panel

may have the same wattage as a large, light solar panel. Thus, by “size” we refer to wattage,

3 The average American home uses 11,040 kWh per year (US Energy In formation Admin istration, 2008),

or roughly 30 kWh per day. We are only considering s mall portable systems under 250W, the size o f a

small PV system used for camping or other s mall off-grid purposes.

Figure 10: Solar Cost Breakdown (Frost & Sullivan, 2009)

16

since weight and physical size are usually just indicators of the value of materials or the particular

design application, not necessarily indicators of price. The potential output of a solar module is

given by its power, measured in watts or watt-peak. Watt-peak is the output of a module under

standard conditions of 1000 watts per square meter of solar irradiance, but most literature uses the

term “watt” loosely to mean watt or watt-peak.

Although there is some variation in price per watt of various companies’ solar panels,

after combining the product information from nearly a hundred modules from various online solar

stores4, we observe a general economies of scale effect. The price graph is concave while the

price per watt graph is decreasing, indicating that the manufacturing cost per watt decreases as the

size of the system increases.

Figure 11: Solar Module Prices

We run a linear regression on the logarithm of price vs. the logarithm of watts to obtain

an exponential model for the cost of a solar module with x watts of the form:

The estimated coefficients a and b for the regression and their 95% confidence intervals are

shown in Figure 12. The confidence interval is computed by taking the standard error of the

residuals from the linear regression and transforming the coefficients into exponential form.

4 www.solar-for-energy.com, www.siliconsolar.com, www.wholesalesolar.com in January, 2011

$0

$200

$400

$600

$800

$1,000

-50 50 150 250

Pri

ce

Watts

Solar Module Price

$0.00

$5.00

$10.00

$15.00

0 50 100 150 200 250

Pri

ce p

er w

att

Watts

Solar Module Price Per Watt

17

Variability in the per-watt price is generally a result of differences in the quality of materials or in

the particular application for the solar panel. Panels created for frequent transportation or easy

portability are generally more expensive than typical modules.

Figure 12: Estimated Solar Module Price with 95% Confidence Interval

We use the exponential equations given in Figure 12 to estimate the total initial cost for

the entrepreneur. Assuming that the cost of a charge controller is roughly 20% of the cost of the

solar module itself and installation costs are slightly higher to include a power strip to charge

multiple phones simultaneously; we obtain a final estimate for the initial capital expenditures of

the entrepreneur:

Initial Capital Expenditures

Solar Modules (250W) $775.00

Charge Controller $150.00

Installation and Power Strip $200.00 Table 1: Initial Capital Expenditures

$0.00

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

0 50 100 150 200 250

Pri

ce

Watts

Estimated Solar Module Price

Original Data

Estimated

Upper Bound, with 95% Confidence

Lower Bound, with 95% Confidence

M(x) = 10.3391x0.8464

M(x) = 7.4654x0.7766

M(x) = 8.785x0.8115

18

Let us confirm that 250W is the maximum size necessary for this micro-enterprise.

Assuming a mobile phone takes 11.2Wh to charge5, a 250W module with five hours of sunshine

6

produces enough power to charge over 110 phones per day. In the revenue analysis to follow, we

see that this is the maximal size necessary for the entrepreneur who should only expect on

average 70 customers per day at low prices. In general, an entrepreneur can always add more

solar modules to his system, but he will probably only buy them in increments less than 250W

because of the high capital cost.

We must also estimate the weekly operating costs of the entrepreneur. Assume the

entrepreneur funds the entire project from a microfinance lender. Other options such as personal

savings or a loan from family or friends could also provide the initial capital needed, but we will

begin by assuming the higher interest rate and regular pay-back schedule of a microfinance loan,

leaving the discussion of other financing options to Chapter 6. Microfinance lending rates are

traditionally high because lenders cannot benefit from the economies of scale of large banks. The

microfinance process furthermore requires significant human capital costs to hire specialists to

train entrepreneurs and check up regularly on sma ll businesses. Accounting for high costs to

obtain small sums of money, the possibility of loan defaults, and high transaction costs, current

microfinance interest rates are close to 30% and sometimes as high as 40-50% (KIVA, 2011).

Solar is applauded for its low maintenance fees, so we set aside 0.1% of the initial cost of

the modules for maintenance each week. To garner business in the early weeks of the enterprise,

assume the entrepreneur hires an employee on commission for $0.01 per customer each day. He

then pays $0.01D(p) each week, where D(p) represents the weekly demand for phone charges at a

set price p. This advertising scheme is necessary for the first eight weeks, and then the

entrepreneur will be well-known enough to attract his own customers. And finally, the

5 7V and 0.8A over 2 hours charges a typical American phone (cellphoneshop.net, 2011)

6 Mauritania’s eastern neighbor Mali gets 5-7 peak watt hours per day (areed.org). Conservatively, we can

expect 5 peak watt hours per day for Mauritania.

19

entrepreneur must sustain his family. Assuming he takes $10 per week as pay and saves the rest

to invest in the business later, this yields the following estimate for weekly operating cost:

Operating Costs (weekly)

Loan Pay-back $31.20

Salary $10.00

Advertising (for the first 8 weeks) $0.01D(p)

Maintenance $0.78 Table 2: Weekly Operating Costs

2.2 Revenue Assumptions

Since revenue can be represented as revenue per customer times the number of customers,

an assumption about revenue implicitly includes an assumption about the number of customers

who will purchase charges at different prices, or in economic terms, the price elasticity of demand.

Mobile phone charging strikes an interesting balance between an inelastic and an elastic demand.

On one hand, no matter what the customer’s income or mobile phone usage patterns, he must find

a way to charge his phone. Whether in the city or in the local village, with a car battery or with a

generator, from a friend or from a stranger, the mobile phone battery must be charged. Perhaps

this is why the price of a charge is so high, forcing users to choose between charging their phones

and purchasing air-time. On the other hand, cell phone needs in Africa vary in degrees of urgency.

Some calls must be made right away, yet others can wait a few days or even be entirely forgone.

A prudent user knows how to juggle his needs to stretch his remaining battery life for a given

amount of time. Thus, while all phones must eventually be charged, customers have some control

over how often they want to charge their phones. Therefore, we expect a demand curve that is

neither perfectly inelastic nor perfectly elastic.

Revenue is a function of the price, but also a function of the population of the area and

the maximal market share. Though this analysis is fairly universal, it is helpful to contextualize

20

the entrepreneur and pick one specific area to study. We first provide an overview of a village in

Mauritania with high potential for solar energy and then discuss how to build a prior belief about

demand and revenue as a function of price in the following chapter. From the entrepreneur’s

perspective, we approximate the market demand for mobile phone charging, erring on the

conservative side for all numerical estimates.

2.2.1 Bababé, Mauritania

One of the poorest countries in Africa, Mauritania is a large, sparsely populated country

bordering the Atlantic Ocean, with population 3.3 million and annual GDP per capita $921 (USD).

A significant portion of Mauritania’s population live

on less than $1 a day, less than 50% have access to

an improved water source, and less than 25% have

access to improved sanitation. Poverty, as usual, is

most stark in rural communities (World Bank, 2011).

Although roughly three-quarters of the

country is desert, Mauritania is rich in natural

resources, as mining and iron ore account for nearly

half of the country’s exports. A historically nomadic

country, Mauritania’s main industries include

agriculture, livestock, and fishing. Severe droughts in the 1970’s greatly affected the country as a

result of heavy dependence on crops, accumulating much of the debt that still remains today.

Plagued historically by ethnic schisms and an entrenched practice of slavery, their recently-turned

republic has had a shaky start. President Taya was overthrown by a military coup in 2005 after

twenty years of authoritarian rule, shortly to be followed by another military coup in 2008.

Figure 13: Map of Mauritania (Geographic

Guide: Maps of Africa)

Bababé

21

The village of Bababé in the southwest corner of Mauritania has roughly 10,000 residents.

Households are fairly large in Mauritania since a typical family unit is built around the male head,

including his wives, children, parents, and unmarried sisters.

Regulated by the government through a Public-Private Partnership initiative, two diesel

generators currently provide electricity to 600 households and small businesses in Bababé

(Sohani, 2011). These generators currently run from 10am to 3am, but as the customer base

expands, it will be profitable for the generators to run all day and this will naturally threaten an

entrepreneur’s prospects at a successful solar charging industry.

2.2.2 Demand

We obtain a general approximation for cell phone charging demand in Bababé by

estimating the population of cell phone users without access to electricity. Note that in Africa the

percentage of people with access to electricity is much higher than the percentage that actually

have homes with solar panels or grid connections, since people often charge phones or watch TV

at the homes of friends and relatives. In 2009, there were 66.32 mobile subscriptions for every

100 people in Mauritania (International Telecommunications Union), a higher percentage than

those with improved water source access. Because Bababé is a smaller, more rural part of

Mauritania, we conservatively assume that cell phone coverage is closer to 35 subscriptions per

100 people. With the advent of electric generators, it is estimated that 50% of the population still

do not have access to electricity (Sohani), leaving a market of 1750 mobile users who need a

method to charge their phones. More realistically, the entrepreneur will probably only be able to

garner 10% of this market share even if he charges low prices, because each cell phone user

already has some existing way to charge their phone. Many have probably begun friendly

working relationships with bikers with car batteries and owners of local charging shops, so

convincing these people to switch to new-fangled solar technology may be more difficult than

22

merely charging a lower price. Averaging two cell phone charges a week and assuming the

entrepreneur only works five days per week, we expect the entrepreneur to have up to 70

customers per day for the lowest prices.

ESTIMATED SUPPLY QUANTITIES Low Est Med Est High Est

Solar hours per day (kWh/m2) 4 5 6

Watts produced per day 1000 1250 1500

Max phones can charge per day 89.29 111.61 133.93

ESTIMATED DEMAND QUANTITIES Low Est Med Est High Est

Population 9750 10000 10250

Cell phone users 2925 3500 4100

Cell phone users without electricity 1316.25 1750 2255

Customers per week if charged $.10 per charge 105.30 175 270.60

Customers per day if charged $.10 per charge 40.01 70 113.65

Table 3: Summary of Supply and Demand Assumptions

23

CHAPTER 3 Model

Central to the quantitative study of any real world problem is a clear and succinct

mathematical model that describes how we process relevant information. Given the assumptions

in the previous chapter, we introduce the Bayesian framework and notation necessary to make the

entrepreneur’s pricing decision. After proposing a revenue structure polynomial in price, we

utilize the previous chapter’s cost and revenue assumptions to obtain precise notions of both the

entrepreneur’s belief and the truth about the revenue that any price will generate. Using a

normal-normal model with linear beliefs, this entails specifying a mean and covariance structure

for the linear parameters. The last section of this chapter establishes the mathematical notation

needed to describe the process by which the entrepreneur makes weekly pricing decisions and

updates his belief about revenue with each new observation.

3.1 Linear Belief Structure

To determine an estimate for revenue as a function of price, we must have a notion of the

demand curve, the number of customers who will pay to charge their cell phones at a given price.

Intuitively, we know the demand curve is decreasing, because fewer people will charge their

24

phones at higher prices. From various newspaper articles and reports, we also know that the

going rate in Africa is $0.20 to $0.30 per charge (GSMA, 2010; Rosenthal/NY Times, 2010;

Edwards/Energy for Opportunity, 2011). However, beyond this basic knowledge, we can only

estimate. As we observe real demand values, Bayesian statistics later serves as a powerful tool to

update our prior belief and learn the true demand most efficiently.

Demand (D) and revenue (R) are both functions of price and are related by:

since revenue is simply the number of customers multiplied by the price paid per person. The

most simple and expressive form for the two functions is a polynomial function, linear in

coefficients. We choose a cubic demand model so that we can capture a logistic curve effect

when the demand is not as sensitive to price for extreme high or low prices. Revenue must

consequently be quartic because its degree is one greater than demand’s.

Although demand and revenue are non-linear with respect to price, they are both linear

with respect to the estimated parameters , and so the structure is correctly labeled a linear belief

model. With this structure, the entrepreneur only has to estimate the vector , and not the

individual values of R or D for the discrete set of prices.

In reality, the entrepreneur can only choose from a discrete set of prices, which can be

represented as an M X 1 vector with M alternatives, . Then we represent

the possible prices and corresponding revenues with vectors and R, respectively, and write the

above equation in shorthand:

25

(3.1)

where is an M X K matrix, and K is the number of linear terms in our model. Each row of is

the vector of terms corresponding to the coefficients.

(3.2)

Using a normal prior distribution and a normal sampling distribution, our belief about the

vector can be described by our belief about its mean vector and covariance matrix . We

use a normal-normal model to fully utilize our belief about covariance, the fact that we believe

the values and are related. If we are fairly certain, for example, that demand is

downward sloping and concave, then the linear and quadratic demand terms (corresponding to the

quadratic and cubic revenue terms) will be negatively correlated. For this reason among others,

we see the benefits of an additive linear belief model for demand. In addition to relating beliefs

about the general form of the demand curve, a linear belief structure is far more descriptive than a

regular correlated belief structure where the revenues for various prices are related. Imagine we

observe revenue much higher than what we believe is possible for a given price. The underlying

linear construction allows us to always update our belief about alternatives according to a natural

structure instead of arbitrarily making the belief about revenue for the observed price very high

and leaving the rest of the revenues low. Furthermore, the linear belief model reduces our

updating equations to only a K X K covariance matrix instead of an M X M matrix, and a K X 1

mean matrix instead of a M X 1 mean matrix. For a large number of alternatives, this

computational saving is immense.

The relationship between the mean and covariance of the parameters and the actual

alternatives p is given by simple linear algebra. Let us use the notation that after making n

26

observations of the true revenue, we believe the linear parameters are distributed normally

according to and the revenues are distributed normally according to

. is a K X 1 vector and is an M X 1 vector. It is already clear that =

by our linear assumption on revenue. The covariance between our beliefs at time n regarding two

prices and is given by:

(3.3)

where is the (i, k) entry of X.

Generalizing to matrix form, we can represent the M X M covariance matrix of the

alternatives by:

(3.4)

so that our belief about the alternatives normally distributed according to:

(3.5)

27

3.2 Specifying a Prior and a Truth Distribution

In the Bayesian model, we must specify two probability distributions for the vector.

The first is a distribution from which we generate the truth about revenue, and the second is a

distribution an entrepreneur might use as his initial belief before he begins to discover the truth.

To completely characterize the distribution in a normal-normal model, we must specify a mean

vector and a covariance matrix for both the prior and the truth. In reality, the truth is not

generated from a distribution; it simply exists and people try their best to discover it. However,

in this setting where we do not know the truth, but have an idea of what it might be, it is

necessary to establish a set of truths so we can observe the behavior of learning algorithms in

different states of the world and average them to see the broad behavior of the algorithm.

The learning process involves generating a true revenue curve and then using a learning

algorithm to discover that curve as fast as possible, starting with a prior belief about the revenue

curve. In the following sections, we first propose a truth distribution by doing a cubic regression

on point estimates of demand. Then, we generate a set of truths and determine the best, median,

and worst case scenarios for revenue. To provide a complete framework for the policy

optimization to follow, we finally propose various prior beliefs that an entrepreneur might have.

3.2.1 Truth Mean

Let us begin by assuming a true demand distribution of alternative means, since demand

for various prices is easier to visualize and estimate than revenue as a continuous function of

price. Although the linear belief model is more mathematically descriptive, it is also more

difficult to intuitively think of means and variances for values than it is to think of demand

approximations. After we assume demand point estimates, we use a cubic regression model to

obtain an estimate for the mean and covariance of the truth distribution, and .

28

Using the guidelines assumed earlier – that demand is a decreasing function of price and

less sensitive to price changes at extreme high or low prices, we propose the following numerical

low, medium, and high estimates for how demand should vary with price. Recall that the going

price is generally $0.20 to $0.30 per charge, so demand decreases significantly in this range, as

competition is stronger for these prices. Also, we are more certain about the behavior for extreme

prices, so the three estimates vary less for prices of $0.10 and $0.50 than for prices of $0.20 or

$0.30.

Price Med Est High Est Low Est

$0.10 350 360 340

$0.15 340 360 320

$0.20 300 340 240

$0.25 225 310 140

$0.30 150 250 70

$0.35 100 175 30

$0.40 60 100 15

$0.45 30 50 5

$0.50 10 20 0

Table 4: Estimates for True Demand at

Various Prices

Figure 14: Point Estimates for True Demand

Means

Given these point estimates, we calculate the linear parameters corresponding to our

belief by running cubic regressions on these three curves. The cubic regressions yield the

following results for the three demand estimates:

Estimated

Med 11144.78 -9482.68 1386.75 301.27

High 11750.84 -11984.85 2703.20 192.22

Low 9158.25 -5876.62 -171.92 422.66 Table 5: Theta Estimates for True Demand

0

50

100

150

200

250

300

350

400

0 0.2 0.4 0.6

Cu

sto

mers

per w

eek

Price

Point Estimates for True

Demand

Med

High

Low

29

3.2.2 Truth Covariance

Since estimates for the standard deviation of the values given by the regressions are

extremely high, we use half of the absolute value of an average of the difference of the estimated

’s as proxies for standard deviation. That is,

This can also be viewed as though we want our high and low estimates of the demand to be two

standard deviations above and two standard deviations below our best estimates when we

generate truths. Since the estimates are not exactly centered on the medium estimate, we take an

average of the two differences. This short exercise also makes it clear that for the desired shape

of the demand curve, and are negatively correlated with and . When one group

increases, the other decreases.

With estimates for the standard deviations of each term, we create a covariance matrix

to generate truths. Because a slight change in proportions of the terms yields drastically

different results, we set a very high correlation co-efficient between and , for all

. Then, each element of the covariance matrix for truths is:

Using the mean vector and covariance matrix as described, we produce 99 truths from the

distribution, shown in Figure 15(a).

30

Figure 15: 99 Generated Truths

3.2.3 Prior Mean

Let us now determine reasonable prior beliefs that an entrepreneur might have. Of course,

the entrepreneur could use the mean and covariance matrix we just used to generate the truth, but

he might also have less sophisticated beliefs. We use four prior distributions in the analysis of

Chapter 5:

1. Truth: a prior which is the same as the mean used to generate the truth.

2. Linear: a prior with a linear belief about demand and hence a quadratic belief about

revenue, in which demand decreases linearly from 70 customers per day at $0.10 to 0

customers per day at $0.50.

3. Optimistic: a prior in which the entrepreneur generates $80 in revenue per week,

regardless of the price he sets.

4. Pessimistic: a prior in which the entrepreneur generates $10 in revenue per week,

regardless of the price he sets.

0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.50

20

40

60

80

100

120

99 truths for revenue

Price to charge one cell phone

Weekly

Revenue (

$)

0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.50

50

100

150

200

250

300

350

400

450

50099 truths for demand

Price to charge one cell phone

Weekly

Dem

and (

custo

mers

)

Figure 15(a): 99 Truths for Revenue Figure 15(a): 99 Truths for Demand

31

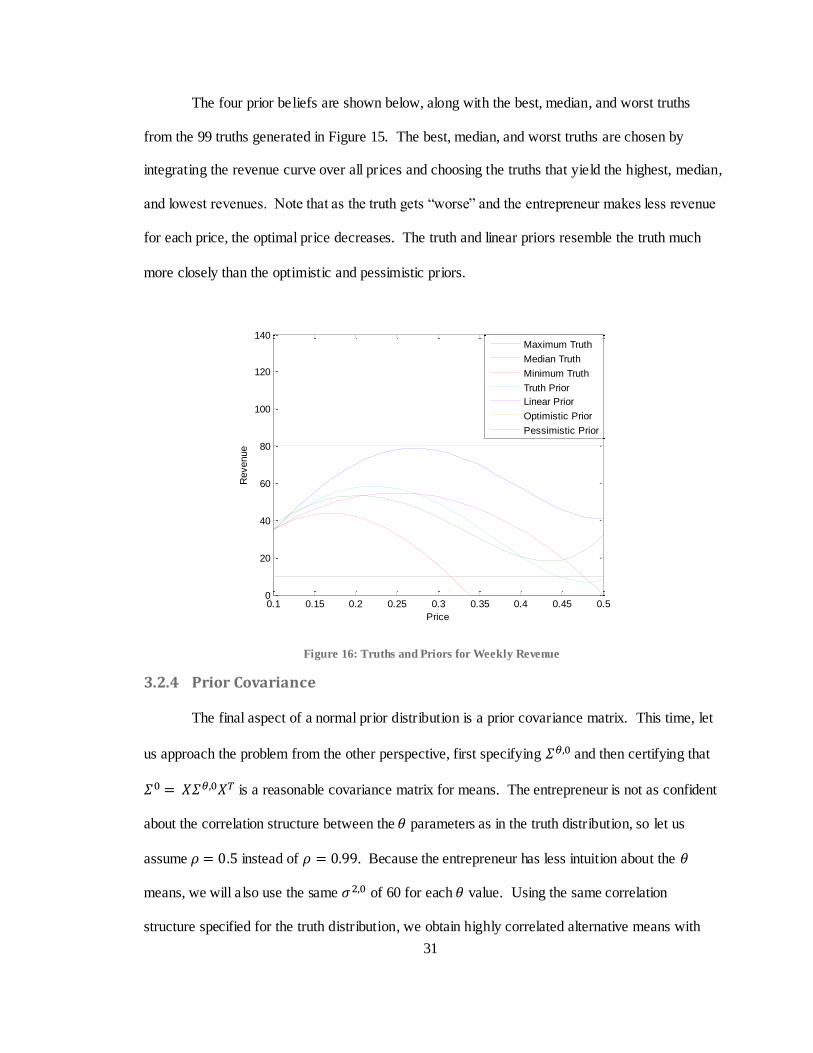

The four prior beliefs are shown below, along with the best, median, and worst truths

from the 99 truths generated in Figure 15. The best, median, and worst truths are chosen by

integrating the revenue curve over all prices and choosing the truths that yield the highest, median,

and lowest revenues. Note that as the truth gets “worse” and the entrepreneur makes less revenue

for each price, the optimal price decreases. The truth and linear priors resemble the truth much

more closely than the optimistic and pessimistic priors.

Figure 16: Truths and Priors for Weekly Revenue

3.2.4 Prior Covariance

The final aspect of a normal prior distribution is a prior covariance matrix. This time, let

us approach the problem from the other perspective, first specifying and then certifying that

is a reasonable covariance matrix for means. The entrepreneur is not as confident

about the correlation structure between the parameters as in the truth distribution, so let us

assume instead of . Because the entrepreneur has less intuition about the

means, we will also use the same of 60 for each value. Using the same correlation

structure specified for the truth distribution, we obtain highly correlated alternative means with

0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.50

20

40

60

80

100

120

140

Price

Revenue

Maximum Truth

Median Truth

Minimum Truth

Truth Prior

Linear Prior

Optimistic Prior

Pessimistic Prior

32

standard deviations of near 60-70. This is reasonable for our entrepreneur, who probably has

little idea what the true revenue for any price is. Now, with a specific set of truth and prior

distributions, we explore which policies are most effective at learning the truth in Chapter 5.

3.3 Mathematical Model

Given a prior belief about the coefficients of a linear model, we describe the revenue

learning process. The entrepreneur makes a pricing decision based on his prior belief, observes a

noisy instance of the true revenue at that price, and updates his linear belief structure using

Bayesian statistics. In this correlated linear belief model, one observation of price changes the

entrepreneur’s belief about all the coefficients in his model. We assume that the entrepreneur

can change price once per week, so time is indexed by n measured in weeks. Using Powell’s

notation (2010) to define the entrepreneur’s pricing problem, we express the entrepreneur’s

process of learning consumer demands by his state variable, exogenous information, decision,

transition function, and contribution.

3.3.1 State Variable

The state variable is defined as “the minimally dimensioned function of history that is

necessary and sufficient to compute the decision function, the transition function, and the

contribution function” (Powell, 2010). Thus, the state variable captures all the knowledge

necessary to the decision-making process. We use the general notation that superscript n

indicates information known at week n, after making n measurements. Any information with

superscript is random at week n, but known at week . The state of the enterprise after n

price measurements includes the entrepreneur’s belief about the mean and covariance of the

coefficients that guide the general revenue equation (3.1). It is written as follows:

33

By convention, the state variable only includes dynamic information that is updated over time.

Other static information necessary for computation are considered parameters, such as the matrix

X and the measurement noise .

3.3.2 Exogenous Information

We know that the true revenue is a function of price, but even with an unchanging truth

we only obtain imperfect observations of revenue because of measurement noise. In this setting,

exogenous information is the random revenue generated from setting a certain price x.

where =

and the measurement noise is normally distributed according to .

3.4.3 Decision

The entrepreneur’s primary decision is which price to set for a mobile phone charge on

week n. In Chapter 4, we propose different policies to make such a pricing decision, but for now,

we write in general notation:

where is the price chosen on week n and is a decision made by using policy from a

given state .

3.3.4 Transition Function

As mentioned before, the power of the Bayesian model lies in the fact that the

entrepreneur updates his belief each time period based on the price he chose and the

corresponding revenue observation. Using the state notation introduced above, the entrepreneur

updates his state based on the model M according to:

34

The recursive updating equations are described more thoroughly in both Powell and Ryzhov

(2010) and Negoescu et al. (2009), but here we present the results without proof. and are

just intermediate calculations used to simplify the notation.

(3.6)

(3.7)

(3.8)

(3.9)

where is a column vector containing the row entries of X corresponding to the price chosen

on week n:

3.3.5 Contribution Function

The entrepreneur’s goal is to maximize his total profit, the difference between revenue

and cost. By the assumptions given in Chapter 2, we give the weekly contribution of making a

particular decision in state as:

(3.10)

where is the cost for the entrepreneur as a function of revenue, since he pays

advertising costs as a portion of revenue in the early weeks of the business. This current profit

for a single period specifies how we determine the efficacy of a policy. By summing the

contribution over each period to obtain cumulative profit, we know which policies are most

effective in profit generation.

CHAPTER 4 Policy Optimization Overview

Posed with the problem of choosing an optimal price, the entrepreneur has several

decision-making options. After checking market prices for mobile charges in comparable

businesses and estimating their weekly demand, he formulates a prior belief in a manner similar

to our analysis in the previous chapter. Recall that a prior distribution includes a belief about the

mean and the covariance of various prices, so the entrepreneur must quantify both his intuition

regarding the revenue that various prices will yield as well as the uncertainty he has for each

estimate. Given this prior belief, the entrepreneur is faced with the classic “exploration-

exploitation” question of decision-making. He must balance exploiting his hunch about the

optimal price and exploring new prices that he is uncertain about, in fear that his original belief

was wrong. If the entrepreneur’s intuition is correct, then an exploitation policy is optimal. Yet

in the more likely event that the entrepreneur’s belief is not entirely correct, the best general

policies allow for a balanced mixture of exploration and exploitation and thus permit the

entrepreneur to learn the best price over time.

In this chapter, we examine several decision-making policies and introduce an additional

pricing restriction to mirror the actual situation more closely. The pricing problem is part of a

widely studied class of ranking and selection problems in which the decision maker must choose

one of many alternatives to measure in each time period, given a measurement budget. In this

36

online context with correlated beliefs, the revenue from each period accumulates over time and

the entrepreneur believes that the revenues from various prices are not independent.

For a summary of correlated belief research in ranking and selection, see Frazier et al.

(2009) and for a description of online policies, see Ryzhov et al. (2010). The most common

solution to the online “multi-armed bandit problem” in which early decisions affect the final

objective function is the Gittins index policy (Gittins (1974)), chosen to be optimal for an infinite

measurement budget with discounted rewards. To avoid the difficult computation of Gittins

indices, the knowledge gradient policy maximizes the value of making an additional

measurement (see Frazier et al. (2009) for initial derivation and Ryzhov et. al (2010) for

extension to the online case).

However, in all the policies mentioned thus far, the problem size is still linear in the

number of alternatives. Because it is ideal to analyze the pricing problem with a continuous

alternative set, we choose to analyze a revenue structure that is linear in its parameters instead,

thus simplifying the problem from an infinite alternative set to a small number of parameters. It

is possible, of course, to use existing policies to choose an alternative and then update the

parameters according to Bayesian updating equations, but few policies exist specifically for this

linear belief framework. In the context of drug discovery, an adaptation of Frazier’s knowledge

gradient policy for an additive linear model is proposed by Negoescu et al. (2009), and we

compare this policy to others in Chapter 5.

To adapt to the entrepreneur’s pricing problem to the ranking and selection framework,

we discretize the alternative set so that the only available prices during any time period are in

increments of $0.05 between $0.10 and $0.50 per cell phone charge. Many simple algorithms for

the ranking and selection problem have been suggested (see Powell and Ryzhov (2010) for more

details), each with favorable qualities and unfavorable shortcomings. The first pure exploitation

policy describes what is most likely to happen in reality as an entrepreneur chooses whatever

37

price he believes at that time will generate optimal revenue. The entrepreneur only takes into

account his profit for the current period in this classic myopic policy. The next three policies,

Boltzmann exploration, interval estimation, and upper confidence bounding are in a class of value

approximation policies that describe metrics for assigning values to alternatives. They seek a

finer balance between exploration and exploitation based on how much better we believe an

alternative is than its peers, how uncertain we are about an alternative, and how many times we

have already measured an alternative. In a different class of look-ahead policies, knowledge

gradient and decision tree resemble a more sophisticated entrepreneur who projects his current

beliefs into the future and makes decisions that maximize reward over a period of time.

4.1 Pure Exploitation

A very confident entrepreneur would use a pure exploitation policy that simply chooses

whatever price he believes is best each week. After observing a price, he updates his belief as