Valuation: Packet 2 Relative Valuation, Asset-based valuation and Private Company Valuation

1 | P a g e

An Equity Valuation and Analysis of Havertys Furniture Companies, Inc.

Casey Noble [email protected]

Joel Dunn [email protected]

Kimberly Edge [email protected]

Lauren Heine [email protected]

2 | P a g e

Table of Contents Executive Summary………………………………………………………………………………3

Business & Industry Analysis…………………………………………………………………8

Company Overview…………………………………………………………………….8

Industry Overview………………………………………………………………………9

Five Forces Model…………………………………………………………………………………11

Rivalry Among Existing Firms……………………………………………………….12

Threat of New Entrants……………………………………………………………….17

Threat of Substitute Products………………………………………………………23

Bargaining Input and Output Markets…………………………………………..25

Bargaining Power of Customers………………………………………….25

Bargaining Power of Suppliers……………………………………………29

Value Chain Analysis…………………………………………………………………………….33

Firm Competitive Analysis……………………………………………………………………..38

Accounting Analysis………………………………………………………………………………43

Key Accounting Policies……………………………………………………………….43

Accounting Flexibility………………………………………………………………….49

Actual Accounting Policy……………………………………………………………..51

Quality of Disclosure…………………………………………………………………..54

Quantitative Analysis of Disclosure……………………………………………….55

Sales Manipulation Diagnostic……………………………………………56

Expense Manipulation Diagnostic……………………………………….61

Potential Red Flags……………………………………………………………………..68

Undo Accounting Distortions……………………………………………………….70

Financial Analysis, Financial Forecasts, and Cost of Capital Estimation………71

Financial Ratio Analysis……………………………………………………………….71

Liquidity Analysis………………………………………………………………………..71

Profitability Analysis……………………………………………………………………78

3 | P a g e

Capital Structure Analysis…………………………………………………………….86

Growth Rate Analysis…………………………………………………………………..92

Internal Growth Rate…………………………………………………………92

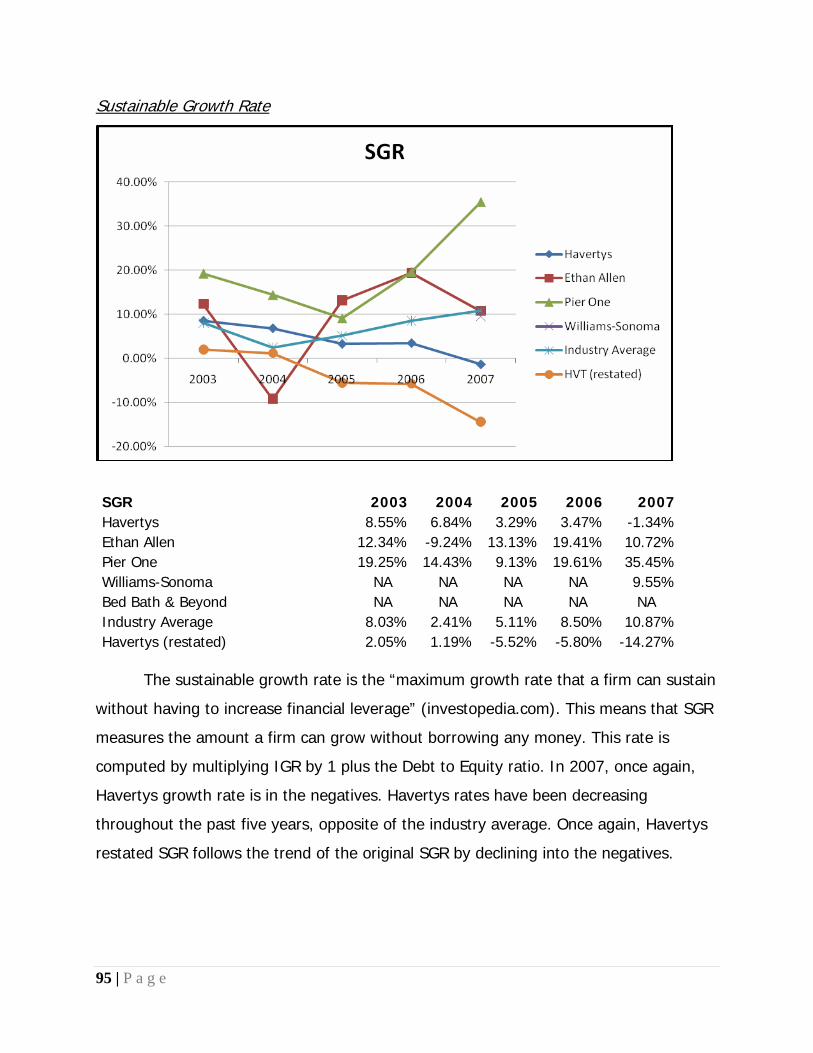

Sustainable Growth Rate……………………………………………………93

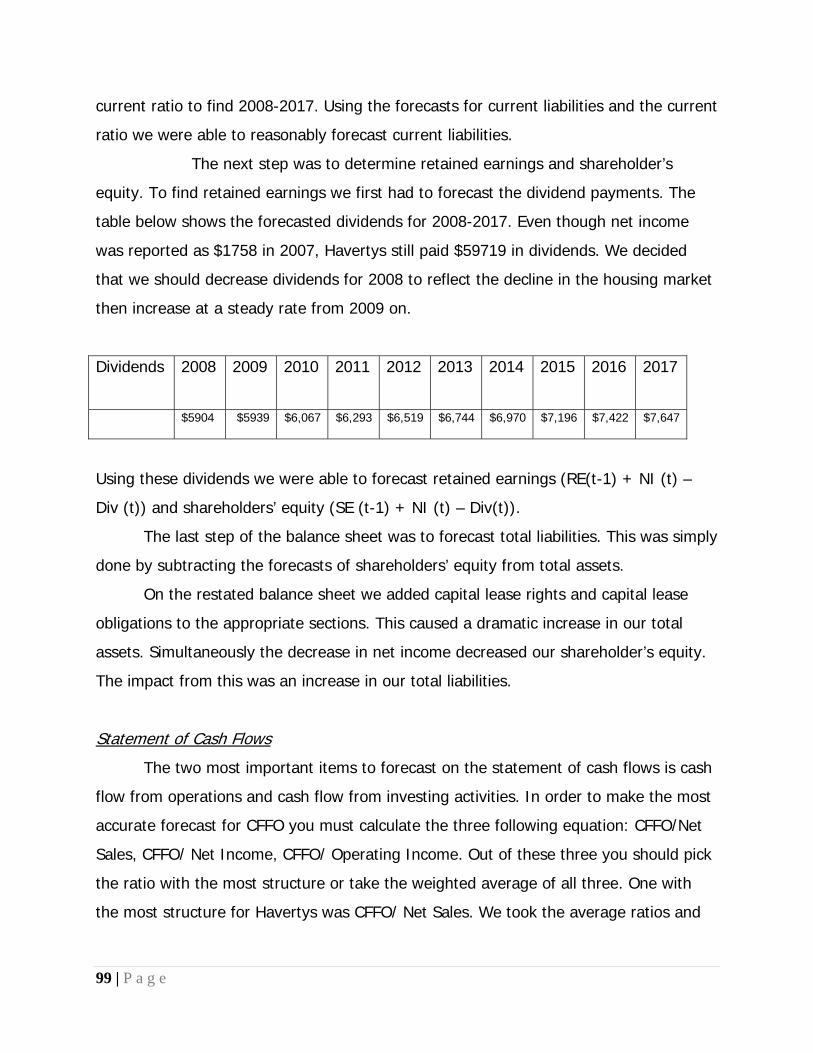

Financial Statement Forecasting…………………………………………………..94

Cost of Capital Estimation……………………………………………………………98

Cost of Equity…………………………………………………………………..98

Cost of Debt……………………………………………………………………..99

Weighted Average Cost of Capital………………………………………100

Equity Valuations………………………………………………………………………………….101

Methods of Comparable………………………………………………………………101

Intrinsic Values…………………………………………………………………………………….106

Discount Dividend Model……………………………………………………………..107

Free Cash Flow Model…………………………………………………………………109

Residual Income Model……………………………………………………………….110

Long Run Return on Equity Residual Income Model……………………….113

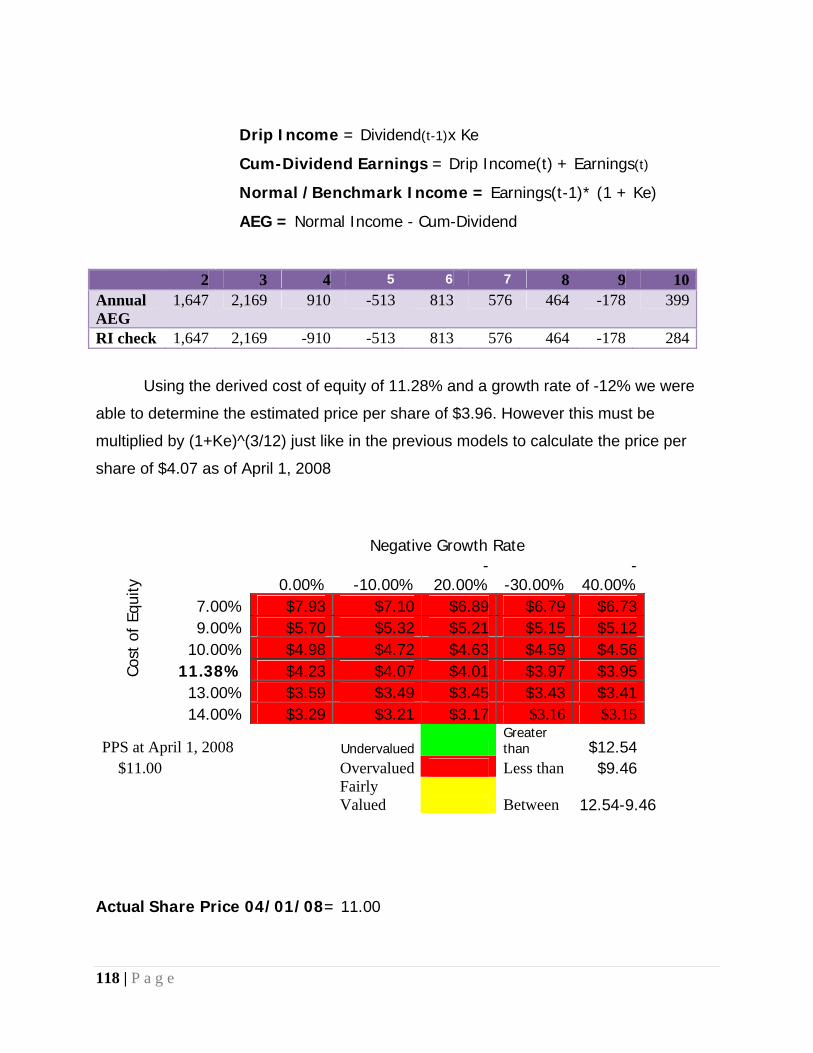

Abnormal Earnings Growth Model………………………………………………..115

Analyst Recommendation……………………………………………………………………..118

Appendix…………………………………………………………………………………………….120

Reference Page……………………………………………………………………………………157

4 | P a g e

Executive Summary

HVT: NYSE (4/01/2008) $11.00 Altman's Z-score

52 week range $7.21 - $13.53 2002 2003 2004 2005 2006

Revenue $787.06 M 3.84 3.7 3.72 3.84 3.96 Market Capitalization $202.2 M Shares Outstanding $22.328M Valuation Estimates Book Value Per Share 13.003 Actual Price (4/01/2008)- $11 Institutional Ownership (%) 114.90% Financial Based Valuations

ROE 0.60% Trailing P/E: $1.13

ROE (restated) -13.71% Forward P/E:

$17.02

ROA 0.37% P.E.G:

$10.98

ROA (restated) -7.36% P/B:

$34.43

P/EBITDA:

$2.23 Back Door Cost of Capital Method P/FCF:

$25.59

Cost of Equity 11.38% EV/EBITDA:

$144.60

Cost of Debt 4.74% Dividend Yield:

$12.36 Weighted Average Cost of Capital 8.62% Intrinsic Valuations:

Published Beta -0.74% Discounted Dividends:

$3.39

Free Cash Flow:

$26.84

Residual income:

$5.28

Abnormal earnings growth:

$4.07

LR ROE:

$2.74

5 | P a g e

Industry Analysis

Havertys Furniture Companies Inc. (HTV) is one of the top home furnishing

retailers in the nation. Today, there are over 120 stores throughout 17 states and they

sustain continued success. Havertys sells residential furniture, accessories, and bedding

and maintains a wide selection of products and breadth of styles in the middle to upper-

middle price ranges. In 2005, Havertys introduced a Havertys brand furniture line by

outsourcing many foreign and exotic materials. Now, nearly all the merchandise offered

is Havertys brand product. Havertys initial direct competitors included Ethan Allen, Pier

One, Bed Bath and Beyond, and William-Sonoma. The home furnishing industry is

highly fragmented. The 25 largest furniture store retailers only account for 22% of the

industry’s sales and 50 of the largest companies only account for around 30% of the

market (First Research). Due to this vast segmentation we had to reevaluate our

competitors. Stores like Dillards and Bed Bath and Beyond sell more than just furniture.

When comparing these types of firms to Havertys we found that we often

underperformed. However, when compared to firms that just sold furniture like Ethan

Allen and PierOne Imports we were more on par with the industry average. Because the

industry is far from homogeneous, it is a mixed industry, competing on both cost

leadership and differentiation strategies. Havertys competitive advantages include

6 | P a g e

brand image, customer service, and distribution which lends itself to competing mostly

on a differentiation strategy. The home furnishings industry has high industry

competition, high rivalry among existing firms, high threat of new entrants, and a

moderate threat of substitutes. The industry also has high bargaining power of both

customers and suppliers. As mentioned before, the home furnishing industry’s key

success factors are cost leadership and differentiation. Slight differences in competition

strategies can positively or negatively affect the success of a firm. The goal of each firm

is to increase product differentiation while keeping costs at a minimum. In doing this, a

firm is able to grab a larger share of the home furnishings industry.

Accounting Analysis

Analysis of accounting policies and procedures is done to establish the flexibility

of accounting policies, to establish and critique key accounting policies, and to scrutinize

the level of disclosure. This process is aimed at pinpointing the any possible distortions

caused by accounting procedures, as well as assess the quality of disclosure of the

government required annual disclosure. The source used in this process is the 10-k.

Specifically, the balance sheet, income statement, statement of cash flows, and finally,

any footnotes having to do with accounting policy. In the end key accounting policies

should be aligned with the firm’s key success factors in order to create value. The

flexible accounting policies for Havertys, as with most firms in the home furnishings

industry, revolve primarily around operating leases. The showrooms these firms need

are very large and often firms in this industry use operating leases. However, Havertys

operating leases are significant enough that their financials should be restated to

capitalize their operating leases. This discrepancy, when adjusted, can impact their

financial statements greatly. After our restatements you can see vast changes in:

assets, liabilities, stockholder’s equity, retained earnings and net income. By capitalizing

these leases an investor will get a better picture of the firm. Another major flexibility for

firms in the industry is post retirement benefit plans. Because the firm chooses the

7 | P a g e

discount rate to use when estimating the plans, potential error loom in the distance.

Just one percent off on a discount rate can cost the firm upwards of $1.5 million,

severely impairing a firm’s ability to pay its plan expense (Haverty’s 10-k). Another

accounting flexibility is the firm’s ability to choose a defined benefit or a defined

contribution retirement plan to its employees. A defined benefit plan can cripple a firm

if the proper discount rate is not used when calculating returns. The degree to which

Havertys discloses information on decisions it makes to come up with its calculations is

high. They do a good job describing how they calculate their number so the investor

can understand how the company makes money. The footnotes and the appendices

give ample amounts of information on how they came up with their numbers. Havertys

is a transparent company, which is beneficial with flexibility in their leases and

retirement plans.

Financial Analysis, Forecast Financials, and Cost of Capital

The financial analysis consists of financial ratios used to evaluate the liquidity,

profitability, and capital structure of a company. Investors and Analysts use these ratios

to help compare a firm to its competitors and help in forecasting the firm’s financial

statements. Ratios are the key tools used when evaluating a firm’s profitability and

growth to find its value. Liquidity ratios measure the firm’s liquid assets used to help

pay-off the firms current liabilities. The liquidity ratios are composed of the current

ratio, the quick asset ratio, the inventory ratio, the days inventory ratio, and the

working capital turnover. Havertys seems to maintain a healthy liquidity with a few

problems in operating efficiency, but its moving in the right direction. There are six

profitability ratios: gross profit margin, operating income margin net profit margin,

asset turnover, return on equity, and return on assets. We used these ratios to

determine that Havertys will struggle to have positive growth rates and profitability. The

capital structure ratios consist of; debt to equity ratio, times interest earned, and debt

service margin. These ratios show how firms raise funds for capital expenditures.

Accurately forecasting a firm’s financial statements is important because it will enable

you to get a glimpse of what the structure of that firm may look like in the future. Most

forecasts are done by using industry averages or ratios derived from a firm’s past

8 | P a g e

financial statements. A few forecasted ratios that we derived are; CFFO/net Sales ratio

of 5.98%, current ratio of 1.71, asset turnover rate of 1.78 (steady in 2010). To

estimate the cost of capital we first computed the cost of equity (11.38%). There are

two different method used to compute the cost of equity- the Regression Analysis and

the Back Door Method. We initially tried to estimate it by running regressions, but this

proved to give us inadequate information for calculating the cost of equity. We then

turned to the Back Door Method, which proved to be sufficient. Next, we calculated the

weighted average cost of debt (4.47%). To achieve this, we multiplied the short term

and long term debt of the company by appropriate interest rates. Once we had both the

cost of equity and the cost of debt, we could compute the Weighted Average Cost of

Capital (8.62%) by plugging these two factors into the WACC formula.

Valuation

After the industry analysis, accounting policies, and financial ratios are examined,

an analyst can determine a firm’s share price through equity valuations. Using the

method of comparables and various intrinsic models of valuations an analyst can

conclude if a firm share price is fairly valued, undervalued, or overvalued. The first

valuation model used to formulate a share price for Havertys was the method of

comparables. The Method of Comparables utilizes ratios that are then compared to

ratios of firms throughout the industry. Using comparable ratios is an easy way to place

a firm within an industry, but it lacks explanatory power and intellectual value is difficult

to add. However, these ratios did not reveal whether or not Havertys is fairly valued or

not. Only the PEG and dividend Yield models suggest that Havertys is fairly valued,

while Price to Book, Enterprise Value to EBITDA, Forward P/E, and the Price to Free

Cash Flow show Havertys to be undervalued. Still, Trailing price to Earnings and Price to

EBITDA show Havertys to be overvalued. In order to get a more accurate valuation we

needed to calculate a second set of valuation models. The second set of valuation

models we used were the intrinsic valuation models. These models include the Dividend

Discount Model, Free Cash Flow Model, Residual Income Model, Long Run Residual

Income Model, and the Abnormal Earnings Growth Model. These models range in

9 | P a g e

degrees of reliability based on the sensitivity they have to errors in growth rates,

WACCBT, and cost of equity. The free cash flow model and the dividend discount model

are especially sensitive and should not always be relied upon. However, the residual

income model, the long run residual income model, and the abnormal earnings growth

model are used by most analysts because of their liability. They are less sensitive to

errors in the estimated growth rates and cost of equity. In order to run these models

we assumed a cost of capital of 11.28%, a WACCBT of 8.62%, and a cost of debt of

4.47%. Using these rates we were able to determine that the price per share for

Havertys is overvalued. The Free Cash Flow Model was the only intrinsic model to show

that Havertys stock price was undervalued. However, as we mentioned before this

model is not very reliable and sensitive to error. For this reason we based our decision

off of the other four models to conclude that Havertys is overvalued.

Business and Industry Analysis

Company Overview

Havertys Furniture Companies Inc. (HTV) is one of the top home furnishing

retailers in the nation. Over 120 years ago, J.J.Haverty founded Haverty Furniture

Collection in downtown Atlanta, Georgia. A few years later the firm spread throughout

the South and Midwest and in 1929 they became publicly traded. Today there are over

120 stores throughout 17 states and they sustain continued success. Havertys also

provides its customers a, “revolving charge credit plan with credit limits determined

through our on-line credit approval system and an additional credit program outsourced

to a third party finance company” (Havertys 10K). Havertys headquarters remains in

Atlanta, Georgia.

Havertys sells residential furniture, accessories, and bedding and maintains a

wide selection of products and breadth of styles in the middle to upper-middle price

ranges. With the introduction of the Havertys Collections in 2005, nearly all the

merchandise offered is Havertys brand product. The graph below shows the breakdown

of revenue generated from the different products sold in 2006.

10 | P a g e

Industry Overview

The home furnishing industry is highly fragmented. The 25 largest furniture store

retailers only account for 22% of the industry’s sales and 50 of the largest companies

only account for around 30% of the market (First Research). Several of the larger home

furnishing retailers include Havertys, Ethan Allen, and Pier One, with most of them

grossing less than $1 million in a year.

In the beginning of this valuation project we included Dillards, Bed, Bath &

Beyond, Williams-Sonoma, PierOne Imports, and Ethan Allen as competitors in our

industry. However, throughout our evaluation of Havertys we concluded that not all of

the companies are actually direct competitors of Havertys. Stores like Dillards and Bed

Bath and Beyond sell more than just furniture. When comparing these types of firms to

Havertys we found that we often underperformed. However, when compared to firms

that just sold furniture like Ethan Allen and PierOne Imports we were more on par with

the industry average.

Many retailers within this industry operate similarly. Like Havertys, the typical

furniture store includes living room, bedroom, kitchen and office furniture, with a

possible mattress and children’s section. The industry considers these “case goods.”

11 | P a g e

“Most store operations include sales management, merchandising, inventory

management, and credit financing” (First Research).

Most profit within the home furnishing industry comes from merchandising and

marketing. Many firms rely on discounts, special offers, and sales to boost revenue

since furniture is not a necessary good, but a specialty good. This also causes home

furnishings sales to be highly sensitive to economic changes. Home furnishing sales are

known to be strongly associated with sales in the housing market. Their has recently

been a weakness in the housing industry, which in turn is putting a noticeable strain on

home furnishing retailers, causing many to go bankrupt. Kathy Shwiff of the Wall Street

Journal writes explaining the recent fall in house prices. “These are tough times for U.S.

homeowners... The decline was the largest since April 1991; prices have dipped for 23

consecutive months” (Home Prices Fall. Homeowners in a bind).

One way in which home furnishing retailers are combating this problem is

through purchasing cheaper imported goods, which has caused a major influx of these

imports into the market. Also, many retailers are turning to in-store brands and internet

retailing, which allow them to “price-down” their merchandise and increase growth. The

adoption of two competitive advantage strategies; cost leadership and differentiation,

are also allowing firms to keep afloat during this economic downturn.

12 | P a g e

Five Forces Model The Five Forces model is an implement that forms an industry and investigates

its profitability. These competitive forces help illustrate the industry’s strengths and

weaknesses. The forces can be classified into two categories: the degree of actual and

potential competition, and the bargaining power in input and output markets. The first

category includes the rivalry among existing firms, the threat of new entrants, and the

threat of substitutes. The second category consists of the bargaining power of

customers and the bargaining power of suppliers. The purpose of this section is to

depict the furniture industry’s structure and profitability.

Havertys Furniture Companies, Inc. Home Furnishing Industry

Industry Competition HIGH

Rivalry Among Existing Firms HIGH

Threat of New Entrance HIGH

Threat of Substitute Products MODERATE

Bargaining Power of Customers HIGH

13 | P a g e

Rivalry among Existing Firms

It is extremely important to evaluate the rivalry among existing firms when

investigating an industry’s profitability. The furniture industry is a highly competitive

and sensitive market. Rivalry among existing firms has many factors affecting it, such

as industry growth, level of concentration, differentiation, economies of scale, fixed and

variable costs, excess capacity, and exit barriers.

Industry Growth:

The first step to measuring the rivalry among existing firms is to determine the

industry’s growth rate. The furniture industry currently includes nearly 20,000

companies. Due to the fact that this industry relies heavily on economic conditions, the

furniture industry has a slow growth rate. The growth rate has been unstable

throughout the last five years (as indicated in the graph below). When the growth rate

is unstable or slow, it is more difficult for a company to obtain the limited market share.

The low level of growth rate highly increases the amount of competition in existing

firms. Some firms have been forced to turn to bankruptcy from the unstable economic

conditions.

Bargaining Power of Suppliers HIGH

Competitive Advantage BRAND, IMAGE, CUSTOMER SERVICE, & DISTRIBUTION

14 | P a g e

*Information from First Research

As Shown in the graph above, the highest peak of furniture sales was in 2004

and lowest in 2003. The graph includes all members of the furniture industry; including

stores such as Havertys, JC Pennys, Dillards, Crate & Barrel, Sears, Ethan Allen, Wal-

Mart, and private “mom and pop” stores. Household furniture sales are closely linked to

home sales, and office furniture sales are closely linked to the employment rate and the

development of new businesses. The industry forecast for the next five years is

expected to grow at an annual compounded rate of five percent (firstresearch.com).

Furniture Store Net Sales

2002 2003 2004 2005 2006

Havertys 703,959 744,635 784,162 827,658 859,101

Bed Bath &

Beyond

2,927,962 3,665,164 4,477,981 5,147,678 5,809,562

Pier One 1,548,556 1,754,867 1,868,243 1,897,853 1,776,701

Ethan Allen 907,264 955,107 949,012 1,066,390 1,005,312

Measured in Thousands ($)

* Information provided Company’s 10-K

15 | P a g e

The chart above shows the publicly traded stores that are strictly related to

furniture. By comparing the two charts above to each other, you’ll see how the net

sales of the stores that are strictly related to furniture compare to the growth rate of

the entire industry. The chart below compares the sales growth between Ethan Allen

and Havertys. Ethan Allen is Havertys most direct competitor.

Sales Growth (%)

2002 2003 2004 2005 2006

Havertys 3.80% 5.78% 5.31% 5.55% 3.80%

Ethan Allen 0.35% 5.27% -0.64% 12.37% -5.73%

Concentration:

Since the furniture industry has numerous firms and is price aggressive, it is a

low concentrated industry. A low concentrated industry increases the level of

competition between the existing firms. There are a total 20,000 firms in the United

States furniture retailing industry. The 50 largest companies hold only 30 percent of

market share, making it a highly fragmented industry (firstresearch.com). The large

majority of companies operate a single store. The most commonly known large

companies include Bed Bath & Beyond, Pier 1 Imports, Ethan Allen, and Havertys.

16 | P a g e

*Information provided by Company’s 10-K

The chart above provides three of the top fifty firm’s market share over the past

five years. Pier One consists most of the market, while Havertys consumes the least

amount the market share. The market share is derived for each of the company’s net

sales.

Differentiation:

There is no brand loyalty in the furniture industry, so firm’s have to differentiate

themselves from other’s to make profit and decrease the competiveness. Firms can

achieve this by having a specialty store, specialty products, high or low prices, or

certain styles or trends that attract consumers. Chains, such as Ikea, Dillard’s and Crate

& Barrel, have grown as companies because they emphasized on style rather than

price. Nearly 10 percent of the firms have license agreements to use famous names

(firstresearch.com). Firms often use these licenses or specialty products to gain profits.

House plans over the next few years are expected to include more multi-purpose

17 | P a g e

rooms, such as media rooms and exercise rooms. To decrease competiveness, firms are

deciding to specialize in a particular type of furniture. Pottery Barn has opened a

Pottery Barn Kids. This is a specialty store that obtains only to children’s needs. There

are not as many Furniture stores directly for children, so by doing this they have

differentiated themselves from other furniture stores.

Switching Costs:

Switching costs are known as the “negative costs that a consumer incurs as a

result of changing suppliers, brands or products” (investopedia.com). Switching costs

are mainly due to monetary reasons, but also can be based upon psychological and

time issues. Customers are willing to take their business to different companies, making

the furniture industry have low switching costs.

Economies of Scale:

Economies of scale is the increase in the size of a firm, which in turn decreases

the average cost of each unit of production. There are two different types of economies

of scale: external and internal. External economies of scale is when the cost per unit

depends on the industry as a whole. Internal economies of scale is when the cost per

unit depends on the firm as an individual (ivestopedia.com). An industry with high

economies of scale is highly competitive. In many industries, the size of the firm

establishes its success and profitability. In the furniture retailing industry, only 30

percent of the market share belongs to the top 50 firms, leaving 70 percent to the

smaller companies. This makes it to where smaller companies can co-exist and compete

with large firms. The furniture industry has high economies of scale and is exceedingly

competitive.

Fixed-Variable Costs:

Variable costs and fixed costs can impact the level of competition in an industry.

The furniture industry has high fixed costs. The cost of selling furniture is high itself.

Firms can experience different degrees of variable costs. The type of variable costs you

18 | P a g e

will find in this industry is things involved with the inventory, such as cost of goods sold

and gross profit. The fixed costs that you will find involved in this industry are the

operating leases and inventory. The inventory remained a consistent average 24% for

Havertys throughout 2002 to 2006. Due to the fact that most furniture stores own

distribution centers, the fixed costs increase in this industry.

Excess Capacity:

Excess capacity occurs when consumer demand is less than the supply. When

this happens, firms are recommended to cut their product prices to fill capacity. Due to

the low real estate demand, there is an excess capacity in the furniture industry. The

large quantity of stores and small demand of furniture products is also a causing factor.

This increases the level of competition in the furniture industry among all the

companies.

Sales Growth (%)

2002 2003 2004 2005 2006

Havertys 3.80% 5.78% 5.31% 5.55% 3.80%

Ethan Allen 0.35% 5.27% -0.64% 12.37% -5.73%

Pier One Imports 9.71% 13.32% 6.46% 1.58% -6.34%

Bed Bath & Beyond 22.17% 25.18% 22.19% 14.96% 12.86%

*Information provided by Company’s 10-K

The chart above shows the growth rate of the firm’s net sales. If a firm’s sales

are declining, it means that the demand is less than the supply, which creates excess

capacity. In 2005, the net sales begin to decline and continue in 2006. In cases like

this, the firms are recommended to have a sale to increase their net sales. Due to the

lack of demand, the furniture industry has high excess capacity.

Exit Barriers:

Exit barriers make it difficult to exit an industry and make it risky to enter. This

happens when companies have high cost or specialized assets that make it difficult to

19 | P a g e

leave. The furniture retailing industry does not face high exit barriers, although it is

much easier for a smaller firm to leave the industry than it is for a large firm to leave.

In September 2007, the Texas-based home furnishing chain Bombay Co, filed for

Chapter 11 bankruptcy protection (firstresearch.com). Many other small Furniture stores

have been forced to follow this trend due to the downward consistency in the Real

Estate market. Due to the fact that so many companies are going bankrupt, this shows

that the furniture industry has low exit barriers.

Conclusion:

In the furniture industry, there is a high rate of rivalry among existing firms. The

industry is extremely competitive and sensitive. The existing firms are experiencing slow

growth rate, low concentration, difficulty differentiating their products, decreases in

demand, high economies of scale, and high fixed costs.

Threat of New Entrants

The threat of new entrants is degree of harm potential firms can cause by

entering an industry. It is exceptionally high when an industry illustrates a history of

substantial profits. Firms will scramble to penetrate a high profit industry in hopes of

gaining a portion of those profits and market share. However, there are a few things

firms must consider before deciding to enter an industry. In order to gain market share,

new entrants will have to overcome many barriers of entry including: Economies of

Scale, First Mover Advantage, Access to Channels of Distribution, Relationships and

Legal Barriers. Fortunately, for those interested in the 85.3 billion dollar home

furnishings industry, there are very few barriers to entry. Although this means a

possible easy entrance for potential firms, it also results in existing firms having a high

risk of diminishing revenues and profits.

Economies of Scale

20 | P a g e

Economies of scale involve the increase in the size of a firm which in turn

decreases the average cost of each unit of production. In an industry with large

economies of scale and high competition, potential firms may not have what it takes to

compete. The furniture industry has both high economies of scale, intensely

competitive, and vastly segmented. Many firms are included under the home

furnishings industry including: Dillard’s, Ethan Allen, Havertys, CostCo and Pier One

Imports. However, not all of these firms sell just furniture causing major differences in

the amount of total assets each firm holds. However, being this segmented does break

down a barrier to entry for potential firms especially because major players in the

industry only hold a total 30% of the market share. That leaves 70% to smaller

economies of scale firms that new entrants can take advantage of.

=

21 | P a g e

The above graphs illustrate the range of total assets over the past five years of

top companies in the highly segmented furniture company. The first graph shows the

total assets of department stores, wholesale clubs and large retail chains. The second

shows total assets of retailers who only sell furniture. These graphs show that

companies with assets in the billions can coexist and successfully compete with firms

who have much smaller amounts of assets. When potential new entrants evaluate

economies of scale they would not find it difficult to compete due to the vast range of

total assets shown by existing competitors. Although the may not be able to compete

with department stores and large chains who have assets in the billions, they could

successfully take on smaller chains and local retailers.

First Mover Advantage

First mover advantage is the “advantage gained by the initial occupant of a

market segment” (about.com). The first firm to enter an industry can gain control of

resources that followers may not be able to match. This can include the ability to set

industry standards and establish exclusive selling agreements with suppliers. This could

22 | P a g e

not only lead to extreme brand loyalty with suppliers but with consumers as well. In the

past, being a first mover would not have given you a tremendous advantage in the

home furnishings industry. Consumers did not show extreme loyalty to one store or

another because not one furniture store had everything they needed. It would not be

unusual for consumers to visit multiple stores in search of the cheapest prices and the

exact style they are looking for. However, stores like Furniture Row are now gaining

notice from consumers for consolidating all types of furnishing in to one giant mega

store. Furniture Row understands that consumers don’t have time to shop for

furnishings piece by piece so they have combined specialty home furnishings, mattress

and linens all under one roof (FurnitureRow.com). Not only is this one-stop shopping for

consumers but companies like Furniture Row have tremendous buying power which

allows them to offer products at a cheaper rate. These first mover firms have the

potential to take a large portion of the market share and establish brand loyalty with

suppliers and consumers.

Channels of Distribution

Historically the high cost of developing a new channel of distribution would be a

challenge that potential entrants to the industry would have to face. However, with the

furniture industry experiencing major changes it is not impossible for potential firms to

compete. The furniture industry is showing an increased trend of shifting to the internet

to distribute their product. “Internet sales, although a still a small fraction of total sales,

are increasing rapidly because prices are discounted by 30 to 40 percent”

(firstresearch.com). These discounts are due to the elimination of showrooms and sales

staff. Acquiring stores in high traffic areas, advertising, and paying employees

commission create high operating costs for firms. The graph below shows the average

salary a firms pays to employees per hour.

Average Hourly Earnings & Annual Wage Increase

Bureau of Labor Statistics

23 | P a g e

*Provided by FirstResearch.com

Although slowly increasing employee wages is a huge operating cost firms must

face. Employees must be trained and very knowledgeable hence their almost $15.00 an

hour wage. Internet companies on the other hand, can get away with paying

employees minimum wage because consumers only contact them in the case of a

problem with an order. The high cost of a physical showroom is also eliminated in favor

of a virtual showroom for employees to browse. Overall, this new channel of distribution

opens the door for new entrants to easily gain market share.

Another factor for potential new entrants to consider is the location of their

distribution channels. Furniture companies usually offer same day or next day delivery

service. It is really important to have strategically placed distribution centers so firms

can keep costs low. Haverty’s for example just recently reconfigured their distribution

channel to a combination of three distribution centers, three home delivery centers and

approximately 14 local market cross-docks (Havertys 10k). This has significantly

decreased the cost and time involved in home deliveries of furniture. It has allowed for

lower inventory levels, less warehouse space, fewer workers, and the ability to enter

new markets without adding local market warehouses (Havertys 10K). Potential new

entrants would need to have well placed distribution centers so they can not only

significantly cut costs but compete with other firms who can ship their merchandise

quickly.

24 | P a g e

Relationships

New entrants to the home furnishing industry will not find it to difficult to create

relationships that will help them gain market share. It is undeniable that many

companies like Havertys with over 100 years of experience have an overwhelming

advantage. Over time they have been able to establish strong relationships with

manufacturers and create customer loyalty. In the past these relationships allowed

firms immense buying power and the ability to lower prices. However, with the industry

moving in to newly chartered waters such as importing goods and internet sales,

existing and potential firms will both have to create new relationships with

manufacturers.

Legal Barriers

Potential new firms must also consider the legal barriers of an industry before

trying to enter. Fortunately for firms looking to enter the home furnishings industry it is

thus far unregulated. Although, for companies who offer credit financing standard state

and federal regulations against deceptive sales practices and laws that regulate the use

of credit financing can be an issue (Firstresearch.com). Also with the industry importing

more and more goods there is a possibility of import policy having a bigger impact on

retailers in the future.

Conclusion

The threat of new entrants in to the home furnishings industry is very high

because there are very few barriers to entry. In this industry large firms can coexist

with smaller ones due to the fact that companies can be profitable without a large

amount of assets and a significant initial investment. There is also potential for new

firms to enter without worrying about not having established relationships with

suppliers and not being the first mover in the industry. There is also room for new firms

to create a channel of distribution. However, firms might have to watch out for legal

barriers in the future. Overall, the threat of new entrants is high and existing firms have

a high risk of diminishing revenues.

25 | P a g e

Threat of Substitute Products

Substitute products can be an intimidating threat to any company because it

increases the company’s susceptibility to decreased profits. Once you know the threat

of substitute products, you are able to more effectively compete in the market.

Relative Price and Performance

The threat of a substitute within an industry is determined by the similarity of

pricing and the function it serves. Within the home furnishings industry, the threat of

substitutes is moderate because all furniture generally serves the same purpose, yet it

has a wide range of pricing.

There are many specialty furniture stores which charge a hefty price tag;

however, the 25 largest retail furniture companies only account for 22% of the

industry’s total sales. The remaining 78% of the industry belongs to mixed market

companies including, “individual local market retailers, larger multiple market

operations, department stores, manufacturers’ stores, ‘lifestyle’ retailers, and wholesale

clubs” (Havertys 10-K). So why do these mixed market retailers carry the majority of

the market? Most of these mixed market companies are able to price their items at a

discount. Also, a customer shopping for shoes may not have to even go to another

store to buy that table they have been looking for.

Buyers’ Willingness to Switch

A customer’s willingness to switch depends on what the individual values. Many

of these incentives include customer service, product quality, range of styles, price,

ease of purchase, the overall experience, and special promotions. Because of the lower

price and ease of purchase, a customer’s willingness to switch among mixed market

retailers which carry furniture is high. However, the small percentage of the industry

which includes the 25 largest furniture retailers heavily depends on the repeat

customer, making their customer’s willingness to switch low. Because these furniture

26 | P a g e

retailers do not dabble in a mixed market, they are firmly established and are able to

offer their customer a quality, style, customer service, and experience which cannot be

found in many mixed market retailers. Between the 25 largest furniture retailers and

the mixed market retailers, the customer’s willingness to switch is moderate.

Conclusion

The way a firm competes is ultimately what determines the resulting danger of

substitute products. There are two ways a firm can compete in the market, low cost

leadership and differentiation. When describing their competition, Havertys explains

that their merchandise, “appeals to customers who are somewhat more affluent than

those of most other competitive price-oriented furniture store chains” (Havertys 10K).

While Havertys competes through low cost leadership, with its integrity of “everyday

low pricing”, it heavily relies on their customer service and brand name to obtain a

competitive edge. Havertys prides itself on having friendly and knowledgeable

employees, accessible financing, and easy and prompt delivery. Havertys also recently

introduced the Havertys Collections brand which carries one-of-a-kind products. This

customer service and brand name is what allows Havertys to obtain a niche within the

industry with which it can overcome the threat of substitutes.

Bargaining Power in Input and Output Markets

While the competition within an industry establishes the possibility and degree of

a firm within that specific industry to experience atypical earnings, markets determine

profitability in the industry. The bargaining power of the industry itself with respect to

the entities supplying goods and services, and the customers purchasing the finished

product are the other factors contributing to buying power. This power to bargain is the

fundamental aspect of the industry’s potential to continue to generate profits. The

home furnishings industry does not stray from this model, but depending on firm’s

place, philosophy, and target market within the industry, the route taken to generating

profits varies immensely. The furniture retailing industry generates massive amounts of

27 | P a g e

revenue $45 billion, spread among 20,000 companies nation wide.

(www.firstresearch.com)

Bargaining Power of Customers

Bargaining power of customers is the power that consumers have over firms as

far as price is concerned. It is important because if the customers of an industry have a

lot of bargaining power, they can set the price and make it hard for firms to turn a

profit. A major goal of the home furnishings industry must be to gain an accurate view

of its customer’s power over the industry as a whole. But in order to obtain an

understanding of customer’s power, the industry must know the demographics of its

customers in order to better understand their tendencies. Without a thorough

understanding of who purchases an industry’s products, the industry is helpless in

determining what customers want, as well as who they are, and what they can afford.

The home furnishings industry is an industry has two primary target markets.

According to www.firstreseacrch.com they are the Baby Boomers (ages 40-55), and

their children. The industry explains its focus on the Baby Boomers because they are

said to be at “peak earnings and have paid off their mortgages”. Likewise, their children

are a target of the home furnishings industry because they have a large proportion of

discretionary income and relatively few financial obligations (www.firstresearch.com).

Therefore any change in the economy in a downward trend would severely impair this

industry’s ability to make a profit. Also, one of their target markets, the Baby Boomers

is getting older and during this stage, fewer will continue to buy new furniture. This

could hurt the industry’s profits as well and could cause them to look elsewhere for a

new market.

There are two main aspects of the bargaining power of customers that unite to

establish the power of customers with respect to the industry. These factors are

expressed by: price sensitivity, and relative bargaining power. In the case of the U.S.

furniture retailing industry, it experiences pressure from and extends pressure to

customers. Industry analysis done by First Research® on the furniture retail industry

suggests that gross margins with respect to profit are “high” nearing 50 percent. This

28 | P a g e

suggests that customers have little power over firms on price (www.firstresearch.com).

However, many firms in the industry have chosen to enter into the market that has little

differentiation in order to compete on a low cost approach. This is an interesting

strategy because the selling expenses in the industry are extremely high due to the

amount of space needed to showcase the product, and the cost of paying sales people.

It is estimated that net income as a percentage of sales in the furniture retail

industry ranges between zero and 5 percent (www.firstresearch.com). This is true for

Havertys as well as most of its competitors. Thus, firms in this particular industry have

such a small margin for error, that selling undifferentiated products as a low cost

provider is extremely risky and requires precise and well researched financial decisions.

This approach could mean that bargaining power is slowly changing hands to the

customers and firms in this industry are risking it all in order to meet those new

demands. Or it could mean that firms in the industry are breaking the mold of the

classic furniture retailing business which involved locally owned businesses. Because

furniture sales are connected tremendously to home sales, one might contend that

customers as a whole do have some bargaining power, but that power comes at a cost

to everyone, since both are affected by the stability or the lack of stability of the

economy.

Price Sensitivity

Price sensitivity is the first factor that determines the customers bargaining

power. It is characterized by the degree to which customers will be willing to negotiate

on price. Price sensitivity occurs primarily within markets that the Industry’s products

have become undifferentiated and the switching costs for the customers are nominal.

For the firms in the home furnishings industry that sell the higher end merchandise,

price sensitivity is fairly low. However, firms in the industry that sell low end

merchandise experience relatively high price sensitivity. As stated previously, the

industry gross margin, according to www.firstresearch.com, is almost 50 percent,

primarily to cover the enormous cost of selling these items, including showroom space,

and advertising, as well as low inventory turnover. At first glance, this might seem like

29 | P a g e

price sensitivity would be low, but with further investigation it appears that firms in the

industry, especially the firm’s aspiring to be low cost leaders where brand loyalty

disappears, fight it out over price and credit terms. Furniture is a fairly big ticket item

and for companies like Havertys and Ethan Allan rely on brand loyalty and customer

service rather than pricing. Conversely, with firms such as Ikea and Bed Bath and

Beyond, price sensitivity does come into play. Therefore, price sensitivity of customers

does play a major role in this particular industry since the 50 largest firms in the

industry only account for approximately 30 percent of the revenue according to the

industry analysis done by First Research (www.firstresearch.com). A majority of the

sales are fought out by locally owned furniture stores that are trying to appeal provide

low cost leadership.

Relative Bargaining Power

Relative bargaining power may be realized only when customers of a product can

obtain a strong bargaining position against firms in an industry. This bargaining position

is established by the number of patrons relative to the firms in that specific industry.

Other factors can include, but are not limited to, volume of purchases made by a sole

client, switching costs, and the quantity of alternative products obtainable by the client.

This relative bargaining power is split between patrons and firms within the

home furnishings industry. There are over 20,000 firms competing in this industry, and

most of them are small, single store operations. Customers have many choices when

choosing furniture, but prices in general must go up across time. This is due to the

nature of the products sold in this industry. The primary raw material used in the

creation of the finished product is and will most likely continue to be wood. Moreover,

forest reserves are declining. The rate at which they can be re-planted and harvested

again cannot keep up with ever increasing demand. Thus, wood laminates and other

alternatives are becoming more prevalent because they are less costly, less harmful in

terms of the environment. This trend to be green could be a way for firms in the

industry to find cheaper, less damaging materials.

30 | P a g e

Switching costs are low for consumers, but can be high for firms, especially ones

that focus on one brand or style. However, these firms are usually insulated from price

sensitivity because of the higher end merchandise they sell. Relative bargaining power

within this industry, especially in the near future will be overshadowed by the

continuing sub-prime mortgage defaults, and the ever decreasing home sales. In the

long run relative bargaining power of customers within this industry will be fairly high

primarily due to their lower switching costs. The implications of this for firms are very

important as far as their profit drivers are concerned because the more power the

customer has, the less a firm can charge. Firms in the industry will have to take

opportunities when they present themselves and find them when they don’t in order to

be profitable in this industry.

Conclusion

Although there are a multitude of factors that effect different ends of the home

furnishings industry, it appears that the power of the buyer has become an increasingly

large factor in the industry. Firms in this industry must regain power over their buyers

to be able to withstand an economic downturn like the one being experienced right

now.

Bargaining Power of Suppliers

The home furnishings industry is supplied by a few recognizable brand names

like Havertys and Ethan Allan, and an large amount of low cost furniture producers like

Ikea. Together they make up the home furnishing industry’s suppliers. These suppliers

have gone the way of many industry suppliers over the past few years, and the

suppliers with well recognized names are attempting to enter the industry themselves.

These companies are attempting to cut out the middle man in an attempt to make

higher profits and over power smaller entities within the industry to gain market share.

31 | P a g e

In order to turn a profit, an industry must haggle with suppliers that the firm

must acquire its raw materials, labor, finances, and other miscellaneous elements.

Understanding whether the industry has the power over its suppliers, as is the case for

much of the large retail industry, is fundamental to valuing actual realizable profit

growth for the industry. The better the industry can haggle over prices, the better the

potential for higher profits industry wide. As stated previously, the buyers of the home

furnishings industry have a substantial amount of power, therefore firms in the industry

need to have power over suppliers in order to be very profitable. Unfortunately for the

firms in the industry, suppliers are deciding to enter the industry themselves. By doing

this, the suppliers are positioning themselves in direct competition to their old clients,

and are forcing them to go elsewhere for product.

Bargaining power of the supplier is considered high when there are few

companies in an industry and they have few substitutes, or because their product is

highly differentiated. Subsequently, suppliers can actually control industry prices and

possibly manipulate distribution agendas to maintain dominance. Conversely, if there

are many suppliers with low product differentiation, the firms of an industry can have

power over its suppliers. In the home furnishings industry, there are many suppliers for

low end furniture, but few for higher end merchandise. Therefore, depending on what

type of furniture a firm sells, it could experience high bargaining power, or low

bargaining power.

Within the home furnishings industry, firms are subject to the power of suppliers

like Thomasville and Stickley. There are relatively few suppliers of high quality furniture

and brand image can be very important to the customer that can afford such items.

Also, suppliers have an edge because many of the big suppliers like Ethan Allan have

decided to open their own showrooms and sell their furniture directly to the public,

effectively bypassing the middle man and driving costs down while they enjoy a much

larger profit; this new phenomenon, however, primarily only affects the higher end

furniture merchandisers.

Price Sensitivity

32 | P a g e

In this part of the model price sensitivity is again a factor that can attribute

bargaining power to one entity or the other. In this case it is suppliers and the home

furnishings industry. Price sensitivity can be very high in this industry especially with

respect to the low cost leadership side. Switching costs are low for the firms in this

arena, and that gives them power over the suppliers.

However, at the higher end side of the industry where brand name matters,

firms can have little power over their suppliers. This is especially true over the past

couple of years since the manufacturers them selves have begun to market their

products including the afore mentioned Ethan Allan example. This has hurt some

companies and caused them to think outside the box. Companies like Havertys foresaw

this phenomenon, according to their 10-K, and created their own brand name.

According to their 10-K, Havertys has competed with their main competitors by

outsourcing about 60% of the production of their goods to China.

Since the majority of the companies in this industry are small local stores we are

forced to conclude that the home furnishings industry is forced by its suppliers to pay

higher prices because most of these smaller stores can buy in the bulk like a big

corporation could and receive a lower price. Therefore, due to the large number of

small firms in this particular industry, the suppliers tend to have the upper hand and

retain bargaining power over the firms.

Relative Bargaining Power

The relative bargaining power of an industry has the potential of greatly affecting

the final price of goods to the customer. In this time of economic recession, bargaining

power is extremely important, but it is important in any economic situation. For low end

home furnishings retailers relative buying power of the supplier is fairly low because

firms have many sellers to choose from to get essentially the same product. But if a

firm conducts business in a market in which brand name is a major factor, relative

bargaining power for the supplier is high and the firm is subject to the decisions of the

supplier, on price, when getting their product. This has the potential of severely

impairing a firms profits due to the fact that they actually make so little on what they

33 | P a g e

sell. This is particularly true with suppliers who have decided to open their own show

rooms and sell their furniture directly to the customers.

The majority of the merchandise sold in the industry is lower end merchandise,

but the majority of the revenue gained in this industry is realized in high end, low

turnover type merchandise like bedroom sets and china cabinets rather than lamps and

accents. Due to this fact, it is difficult to attribute bargaining power to the industry as a

whole, because the industry is so fragmented between high and low end merchandise.

However, one could feasibly contend that the suppliers have more bargaining power

relative to firms in the home furnishings industry. For retailers focusing on high end

merchandise, switching costs are very high, while undifferentiated merchandise enjoys

low switching costs. Another reason that suppliers have higher relative bargaining

power is that due to retail consolidation, fewer styles are in production. This means that

firms are getting less and less choice in the merchandise they can purchase to sell

unless they design their own, which is impossible for a majority of the small firms who

primarily populate the industry, but lack the ability to produce their own furniture.

Conclusion

The bargaining power of suppliers in the home furnishings industry plays a major

role in the cost structure, and the ability of firms to be profitable organizations. The

furniture retail industry faces fairly high supplier bargaining power due to the fact that

most of the firms in this industry are small single store operations. Recently, suppliers

are beginning to open their own show rooms effectively cutting out the middle man.

When suppliers need the firms in this industry less, firms will be weeded out and many,

if they cannot differentiate themselves could eventually cease to exist. Some firms do

have bargaining power over their suppliers, unfortunately, their sales do not make up a

large enough portion of the revenues created by this industry to warrant it much power

over its suppliers on an industry level. Due to the fragmenting in this industry between

the high and low end furniture sales, one could contend that they make up two distinct

industries. Also, manufacturers that have entered the industry on their own could be

considered to be in their own industry. In subsequent sections the valuation the firm

34 | P a g e

will give a more definitive answer to this idea. However, as the industry is now,

depending on the type of merchandise sold buying power of suppliers will have a

possibly major impact on cost structure and the ability to make a profit.

Value Chain Analysis

The home furnishings industry is highly concentrated, and experiences high

competition among its 20,000 firms. The ability of a firm to characterize itself within the

industry by accurately recognizing its strengths and its deficiencies is crucial to survival

in this particular industry. Success is realized in this industry by a firm playing off its

strengths in order to gain market share in gain a competitive advantage. Finding this

competitive advantage and then sticking with it is the best way to continue growth at

the firm level, as well as at the industry level.

As is the case for most industries, firms in the home furnishings industry will

attempt to gain their competitive advantage by one of two strategies: cost leadership

and differentiation. Although industry tradition has focused on cost leadership, some

firms are now thriving due to their unique abilities to create differentiation even in low

end the lower end merchandising sector of the home furnishings industry. The industry

is highly fragmented, extremely competitive, and includes a diverse group of

competitors ranging from “national department stores, regional or independent

specialty stores, to dedicated franchises of furniture manufacturers” (Havertys 10-K).

35 | P a g e

Cost Leadership

Traditionally, cost leadership has been the focus of most of the home furnishings

industry. Interestingly, the top 50 firms in the industry only account for 30 percent of

the revenues generated (www.firstresearch.com). This discrepancy suggests that no

one company has a majority of the market share, and that competition is exceptionally

fierce in this particular industry. With few entrance barriers, this industry is wide open

to new competitors with new cost-cutting strategies. Moreover, industry suppliers have

noticed the low entrance barriers and concluded the same. Furniture manufacturers

such as Ethan Allan have entered the industry and have the potential to wreak havoc

on smaller firms, as well as retailers who carry their product line.

Now more than ever, cost leadership is a top priority for the home furnishings

industry because of the downturn in the economy. This industry attempts to market

luxury products and is subject to the volatility of the housing market. Thus, times will

be harder.

Low input costs

Input costs include those costs that are associated with the cost of doing

business. For the home furnishings industry, the most notable example of the lowering

of input costs is the internet. Many companies in the industry sell exclusively on the

internet and that significantly reduces costs because they don’t utilize costly showrooms

or warehouses, but order directly from the manufacturer (www.firstresearch.com). Also,

many of the traditional firms in the industry have utilized the internet to gain name

recognition and to display their products with very little cost associated, and virtually

unlimited exposure to their target markets.

Efficient Production

Efficiency has been a focus in American business for a several years, and home

furnishings industry does not break the mold. Efficiency within this industry is

imperative. The gross margin in this industry is close to 50 percent (www.first

36 | P a g e

research.com), but the high costs of maintaining a large showroom, low product

turnover, distribution costs, and advertising expenses soon take up most of the

revenue. That coupled with credit sales on the rise and price cutting to draw customers,

this industry actually has very little margin for managerial error.

Suppliers entering the industry have also done much to spur the focus on

efficient business in the home furnishings industry. Firms like the Havertys Furniture

Companies Inc., according to their 10-K, have been forced to turn to outsourcing the

manufacturing of their products to places like China in order to compete within the

industry. Subsequently, severe changes in exchange rates or tariffs have the potential

to lower gross profit on items received from overseas according to the Havertys 10-K.

Another major aspect of efficient production to be considered, especially in the

U.S., is the ability to obtain cost effective marketable products that comply with

Government standards. According to the article Safety Push Focuses on Retailers, The

Consumer Product Safety Commission is beginning to “shift “its strategy in order to

maintain safe products as the bulk of manufacturing is done overseas. The shift would

be to focusing on the quality and safety of the goods entering the U.S. and causing

firms that outsource manufacturing to be held more accountable for the quality and

safety of their products. This directly effects the home furnishings industry due to the

fact that about 30 percent of its goods are now manufactured in China

(www.firstresearch.com). Another article in the Wall Street Journal entitled Some

Stalled Safety Rules For Products May Be Enacted, suggests that The Product Safety

Commission will make several new safety rules including “tougher flammability

standards for upholstered furniture.” The ability of the industry to efficiently adhere to

the new standards is necessary to maintain profitability.

Low-cost Distribution

In order to obtain low-cost distribution at the industry level, the firms in that

industry must be capable of acquiring sufficient technology systems, supply chains,

labor forces, and warehouse capacity. The home furnishings industry’s profitability relies

much on its ability to distribute its products efficiently and at a low cost. Virtually all of

37 | P a g e

the sales in this industry require the product to be delivered to the customer’s home.

According to the Wall Street Journal, oil prices rose 45.3 percent in 2007 alone. With

demand not decreasing, it is getting harder for firms in the industry that rely so heavily

on distribution to make a profit. Companies will attempt to pass the price increases

along to the customer, but that can last only so long.

Efficient management information systems and Information Technology

infrastructure are another major component of low-cost distribution. Firstly, if the

implementation of an efficient management information system in attainable, it will cut

costs caused by unnecessary wages, and more importantly, human error. Since these

systems are used to monitor point-of-sale, credit operations and distribution systems,

the efficiency, reliability, and sharing capabilities of these systems is of utmost

importance to low-cost distribution.

Differentiation

For a majority of the home furnishings industry, the strategy taken to gain a

competitive advantage is differentiation of their product. Differentiation occurs when a

product is supplied by a single entity that is incomparable and it sold at a lower cost

than the price a premium customer will pay. Differentiation is attempted and achieved

in this particular industry via three strategies, or a combination of them. The three

strategies are Superior customer service, more flexible delivery, and investment in

brand image.

Superior Customer Service

The home furnishings industry is a customer service oriented industry. From the

research and development of the products, to the sales person on the showroom floor,

to the set-up and delivery crew, all are run with a focus on customer service. One major

way that the home furnishings industry has explicitly show its focus on customer service

emphasis within the differentiation approach is the fact that the industry as a whole is

moving from focus on their product to style (www.firstresearch.com). The industry

tries to provide experienced sales associates to customers by providing competitive

38 | P a g e

wages, schedule flexibility, and good commissions according to

(www.firstresearch.com). The sales associated are also continually trained to offer

patrons advice and accurate information about the products.

More Flexible Delivery

Value in the U.S. is assessed primarily on speed of delivery. Customers of the

home furnishings industry are no different. They require instant gratification. Therefore

many firms in the industry are focused on timely delivery. Some firms like Havertys are

continuing to make that a priority and hopefully an advantage by building more

distribution centers. In 2005 Havertys built a new distribution center effectively

ensuring the capability of overnight delivery of products to its customers (Haverty’s 10-

K). According to a slaes associate here in Lubbock, firms like Bob Mills furniture are

also trying to simplify distribution with Oklahoma City as its hub for supplying Lubbock

and Amarillo instead of trying to get warehouse space in all three cities. In our society

this is a legitimate avenue for competitive advantage and gaining market share.

Investment on Brand Image

Making one’s brand a highly recognizable and desirable one costs a firm time,

money, and marketing skills. Now that manufacturers are entering the industry, brand

image is becoming more important to the industry as a whole. In order to thwart

competitors some firms are opting to create their own brand in order to gain a brand

image advantage. Firms like Havertys, Ethan Allan, and Ashley furniture have created

their own brand to market so as not to support the suppliers who have entered the

industry. As stated previously, the industry trend is moving from emphasis on product

to an emphasis on style. This gives companies with their own brand a special

opportunity to differentiate themselves and possibly gain an advantage over other firms

in the industry.

Conclusion

39 | P a g e

Firms in the home furnishings industry use both cost leadership and

differentiation strategies in order to gain a competitive advantage. In other words this

industry uses a mix of the cost leadership and differentiation strategies. On the cost

leadership side they use lower input costs, efficient production, and low-cost

distribution to gain an advantage. On the differentiation side firms in the industry use

superior customer service, more flexible delivery, and investment in brand image to

create an advantage.

Firm Competitive Advantage Analysis For Havertys to compete in the furniture industry they must achieve and sustain

competitive advantage. To do this they must use two competitive strategies, cost

leadership and differentiation. Cost leadership is the ability of a firm to offer the same

product as its competitors but at a lower cost. Differentiation is directed more towards

providing a distinct product that will set them apart from their competitors. In order for

Havertys to be profitable they must use these strategies to accurately position

themselves in the industry. Like most high end firms in the home furnishings industry,

Havertys tends to rely on differentiation strategies to distinguish themselves. However,

they do still use cost leadership especially now with the economy going towards a

recession.

Cost Leadership

Cost Leadership is the ability of a firm to offer the same product as its

competitors but at lower cost. Firms can do this with efficient production, lower input

costs, and lower cost distribution. In a highly segmented industry, such as the home

furnishing industry, low prices are not always a major competitive advantage. While

firms like Walmart and Ikea market their furniture as good quality at low prices, others

40 | P a g e

such as Pottery Barn and Havertys sell their superior quality furniture for higher prices.

In fact Havertys clearly states that they do not market themselves as a low cost retailer.

Instead they provide their customers with a wide selection of products and styles

primarily in the middle to upper-middle price ranges (Havertys 10K).

However, with the recent changes in the economy many high end retailers will

have to reevaluate their price positions. Furniture is a discretionary spending item which

makes the stability of the economy an important factor in profits. As of now the

economy has suffered a significant downturn and consequently so has the housing

market. According to the Wall Street Journal, “declining home values can put a chill on

consumer spending, which makes up 70% of U.S. economic activity; people feel less

wealthy and spend less, analysts say.” Needless to say this decline in the housing

market has had a huge effect on the home furnishings industry. Havertys will have to

adopt a few cost leadership strategies in order to keep their net sales and profitability

from declining.

Efficient Production

One way Havertys has lowered costs is by focusing their attention on efficient

production. The production of furniture involves many costly aspects such as elaborate

technology systems, labor forces, warehouse space to hold inventory and

transportation. These high costs have led the industry to shift to importing finished

goods. Havertys has also moved toward this trend and is importing to lower their costs

of production. During 2006, approximately 60% of Havertys purchases were for goods

not produced domestically (Havertys 10K). Havertys is able to import the same quality

product at a cheaper price allowing them to price down their merchandise. They are

also currently working with select Asian manufacturers to increase the level of “direct”

import purchases in 2007 (Havertys 10K). They believe that this will allow substantial

cost savings which will be important with the economy moving towards a recession.

Establishing these relationships and using their ability to import wisely will be an

advantage for Havertys to keep their sales afloat.

Lower Input Costs

41 | P a g e

With the industry moving towards selling their merchandise on the internet lower

input costs have become available. Havertys is one of many stores that have utilized

the internet to lower input costs. Although they do not sell their merchandise over the

internet they do have a sort of “virtual showroom” for customers to browse and check if

an item is available at their local Havertys. This has significantly lowered input costs

such as advertising for the firm. Their entire product line is now only a click away for

consumers. The company hopes to bring more functionality to their website in 2008

which will allow even lower input costs (Havertys 10-K).

Low Cost Distribution

Havertys can also cut costs with lowering their cost of distribution. According to

their 10K Havertys has made “significant investments in their distribution infrastructure

by using a combination of three distribution centers, three home delivery centers and

approximately 14 local market cross-docks.” This recent change in their distribution

channel has provided many low cost distribution benefits for Havertys. It has allowed

for lower inventory levels, less warehouse space, fewer workers, and the ability to enter

new markets without adding local market warehouses (Havertys 10K). All of these

things are cost savers for the firm and allow them to be able to price down their

merchandise. This is becoming increasingly important due to the rising prices of oil.

According to an article in the Wall Street Journal, “oil prices surged from just over $10 a

barrel a decade ago to $100 January 2, 2008.” This is why firms find it so important to

strategically place distribution centers around the country. Not only does it allow them

to ship to their customer quickly but cuts down on gas prices for their delivery trucks.

Differentiation

Differentiation is a strategy that is based on the ability of a firm to offer a unique

product that will set them apart from their competitors. The home furnishings industry

creates competitive advantage mainly with the use of differentiation. In order to do this

a firm will have to identify attributes of their product that customers will value, position

themselves to meet their target customer, and achieve differentiation at a cost lower

than what customers will pay for their unique product. Havertys has done this

42 | P a g e

successfully with the use of superior customer service, more flexible delivery, and large

investments in brand image. With the economy nearing a recession retailers are finding

themselves in trouble if they don’t start to focus on competitive advantage strategies

such as differentiation. An article in the Wall Street Journal explains how “Retailers

turned in their worst monthly sales results in nearly five years, and big chains appeared

to be girding themselves for a prolonged slowdown in consumer spending.” This makes

it even more important for retail chains such as Havertys to differentiate their products

from their competitors to keep stores open and sales up.

Superior Customer Service

If Havertys could pick their strongest competitive advantage it would be their

superior customer service. With over 100 years in the industry Havertys has developed

and maintained a very knowledgeable labor force. To attract and retain qualified

personnel Havertys offers competitive salaries and also enrolls employees in their own

training program. These programs include classes on product knowledge, selling and

management skills classes (Havertys 10K). They find this necessary because they

primarily promote internally. For this reason they find that training and assessment of

their associates is essential to their growth (Havertys 10K). Large employee turnover

can be costly for firms especially if put through rigorous training programs. Havertys

has definitely found a way to maintain their labor force and educate them on the

industry and specifically their products. There is no doubt that when shopping at

Havertys customers will have a knowledgeable source available to them to assist in

their purchasing.

More Flexible Delivery

Havertys prides itself on its ability to deliver their furniture to their customers in

a short time frame. This has become increasingly easy with their recent investment in a

new distribution infrastructure. They have recently moved from five regional

warehouses and 46 local market warehouses to a combination of three distribution

centers, three home delivery centers and approximately 14 local market cross-docks

43 | P a g e

(Havertys 10k). This has significantly decreased the cost and time involved in home