AMICE Slides Universitat de Barcelona - UB · dssolfdeoh wr erqgv dqg ordqv iru zklfk qr fuhglw...

31

Workshop Insurance and Pensions, University of Barcelona 14 July 2017 Solvency II Review Standard Formula

Transcript of AMICE Slides Universitat de Barcelona - UB · dssolfdeoh wr erqgv dqg ordqv iru zklfk qr fuhglw...

Workshop Insurance and Pensions, University of Barcelona

14 July 2017

Solvency II Review Standard Formula

Solvency II Live

• First live submissions under Solvency II• Firms were requested to submit Day-one Reporting in January 2016 and

quarterly reporting templates in March, June September and December 2016

• First set of annual templates and First SFCR and First RSR have been submitted in May 2017

• EIOPA has just published its first statistics which are based on Q3 2016 data. As from now on the EIOPA statistics will be published on a quarterly basis and include aggregated country-level information on the following information submitted by more than 3000 firms:

• Balance Sheet, • Own Funds,• Capital Requirements / SCR & MCR ratios per country,• Premiums, • Claims and Expenses

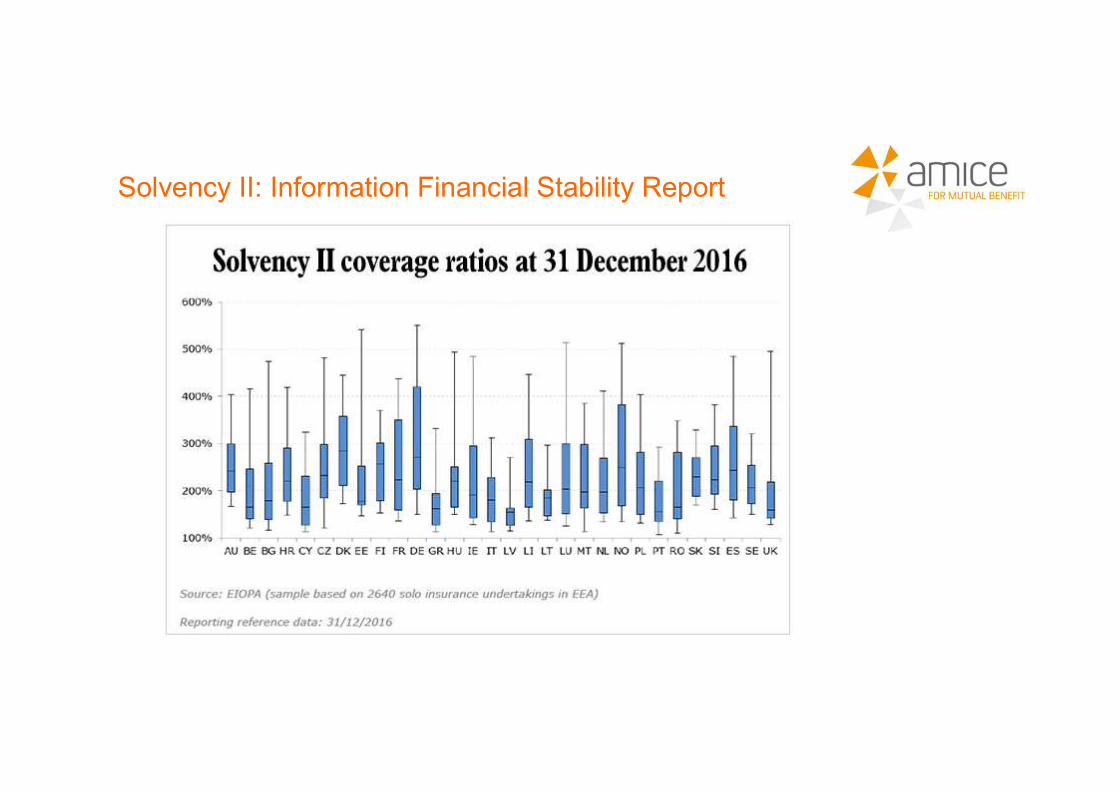

Solvency II: Information Financial Stability Report

2 Reviews

• 2018 Review Delegated Regulation: the Commission will methods, assumptions and standard parameters used in the market risk module including a review of the standard parameters for fixed-income securities and long-term infrastructure, the standard parameters for premium and reserve risk, the standard parameters for mortality risk, as well as the subset of standard parameters that may be replaced by undertaking-specific parameters and the standardised methods to calculate these parameters

• 2020 Review Solvency II Directive, the Commission shall make an assessment of the appropriateness of the methods, assumptions and standard parameters used when calculating the Solvency Capital Requirement standard formula.

Review Solvency II Framework

• The EC has simplified the definition for Infrastructure Corporates to ensure consistency with Infrastructure Projects;

• The definition of Infrastructure Project Entities has been extended to include Project-like Corporates;

• Infrastructure Corporate Debt: 25% reduction in debt calibration and unrated debt treated at par with BBB rated debt

• Infrastructure Corporate Equity: reduction from the existing level of 39% (or 49%) to 36% for all infrastructure corporate equities, listed and unlisted. This compares with 30% for infrastructure projects which includes unlisted equity.

Solvency II: New Set of Delegated Acts

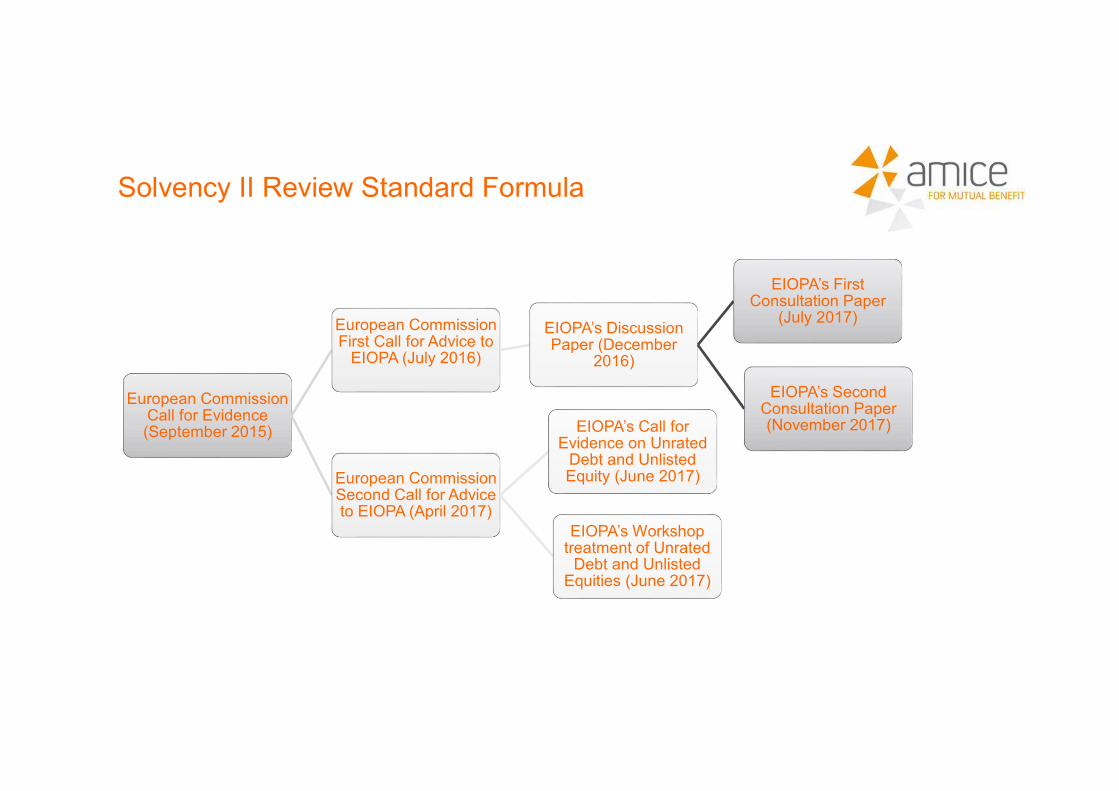

Solvency II Review Standard Formula

European Commission Call for Evidence (September 2015)

European Commission First Call for Advice to

EIOPA (July 2016)

EIOPA’s Discussion Paper (December

2016)

EIOPA’s First Consultation Paper

(July 2017)

EIOPA’s Second Consultation Paper (November 2017)

European Commission Second Call for Advice to EIOPA (April 2017)

EIOPA’s Call for Evidence on Unrated

Debt and Unlisted Equity (June 2017)

EIOPA’s Workshop treatment of Unrated

Debt and UnlistedEquities (June 2017)

• In January 2017, the industry replies to EC Call for evidence on EU Financial Services

• In July 2016, the EC launched the First Call for Advice on the review of the Solvency II Standard Formula.

• In December 2016, EIOPA published a Discussion Paper which consisted of 21 areas subject to the review, three of which are the result of AMICE’s advocacy positions.

• EIOPA’s Discussion Paper has been splitted in two consultations papers

• First consultation paper launched in July 2017. Deadline August 2017. Advice to be delivered to EC in October 2017.

• Second consultation paper to be launched in November 2017. Deadline January 2018. Advice to be delivered to EC in February 2018.

SCR Review Standard Formula

• First Consultation Paper (July 2017 – August 2017)• Simplified calculations

• Reducing the reliance on ECAIs

• Treatment of guarantees, exposure guaranteed by a third party and exposures to RGLA

• Risk-mitigation techniques

• Undertaking specific parameters

• Look-through approach to investment related undertakings

• Information on LAC DT

SCR Review Standard Formula

• Second Consultation Paper (Nov 2017 – Dec 2017)• Volume measure for premium risk

• Recalibration Standard Parameters Non-life Premium and Reserve Risk

• Natural Catastrophe Risk

• Man-made Catastrophe Risk

• Health Catastrophe Risk

• Interest rate risk sub-module

• Calibration mortality and longevity risk

• Risk Margin

• Comparison Own Funds Insurance and Banking Sectors

SCR Review Standard Formula

Second Call for Advice• Methods and assumptions to assess the credit risk in calculating the spread risk

submodule for certain unrated bonds and loans: EIOPA is asked to provide criteria applicable to bonds and loans for which no credit assessment by a nominated ECAI is available.

• Methods and assumptions to be used when calculating the equity risk submodule, with respect to criteria that could be used to identify certain portfolios of unlisted equity: EIOPA is asked to provide criteria applicable to portfolios of equity from the European Economic Area (EEA) which are not listed in order to identify which instruments could benefit from the same risk factor as listed equity.

• Methods and assumptions to be used when calculating the equity risk submodule with respect to strategic equity investments.

SCR Review Standard Formula

SCR Review Standard Formula

• Simplifications• SLT & life lapse: introduction of a simplification to be based on the same

homogeneous risk groups that are used for the calculation of the Best Estimate, however subject to restrictions around the grouping of policies. Firms should demonstrate that the particular grouping used for calculating the best estimate does not allow for material compensations between policies in case of lapse events.

• NSLT & Non-life lapse: introduction of a simplification, however subject to restrictions around the grouping of policies (see above).

SCR Review Standard Formula

• Simplifications• Mortality risk: Modification of the simplification. The formula provided by this

simplified calculation assumes that the total capital at risk CAR does not vary over time. An adjustment of this simplified calculation would easily allow to take into account situations where this is not the case.

• Spread & Market concentration: simplification to be discussed in “reducing reliance on ECAIs.

• Look-through: simplification to be introduced in the autumn consultation.

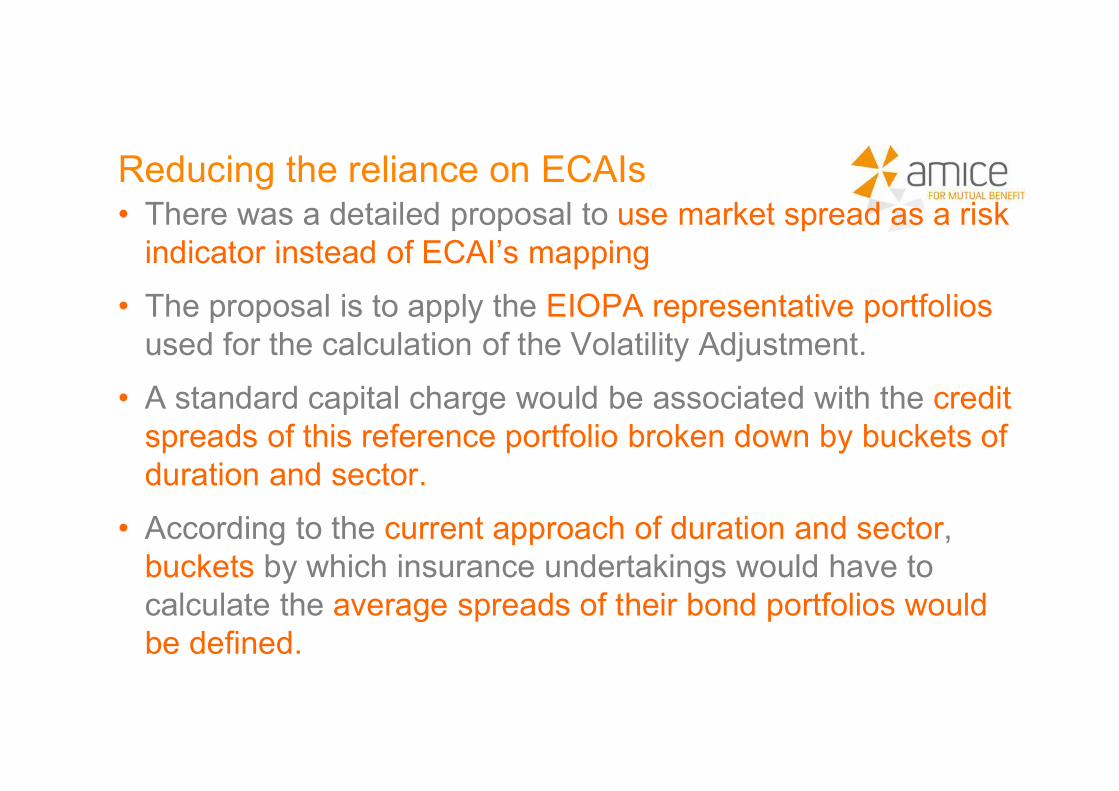

Reducing the reliance on ECAIs • There was a detailed proposal to use market spread as a risk

indicator instead of ECAI’s mapping

• The proposal is to apply the EIOPA representative portfolios used for the calculation of the Volatility Adjustment.

• A standard capital charge would be associated with the credit spreads of this reference portfolio broken down by buckets of duration and sector.

• According to the current approach of duration and sector, buckets by which insurance undertakings would have to calculate the average spreads of their bond portfolios would be defined.

Reducing the reliance on ECAIs

• The new spread risk sub-module would provide an adjustment factor according to the size of the difference between an entity specific average spread per bucket and the reference portfolio spread provided by EIOPA.

• Volatility may be smoothed by using a rolling average of the portfolio’s spread.

SCR Review Standard Formula

• USPs • USP for non-proportional reinsurance: introduction of a USP method that caters for

stop loss reinsurance programs.

• Lapse risk: EIOPA invites stakeholders to provide more methods for consideration that fulfil the criterion of a “permanent and maturity independent bidirectional shock that satisfies the 99.5% VaR calibration”.

• USPs for nat cat: will be investigated by EIOPA Cat WS once simplification and recalibration works are over.

• USPs for longevity and mortality: will be investigated at a later stage, once the calibration of mortality and longevity shocks are over.

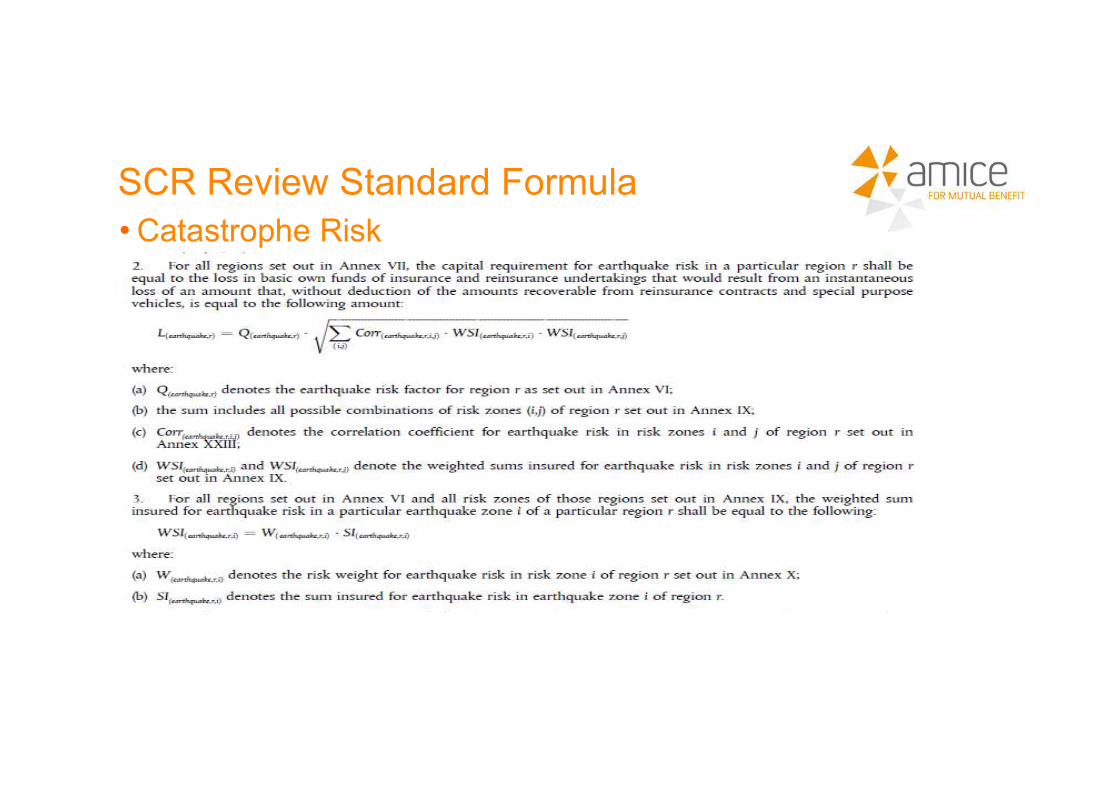

SCR Review Standard Formula• Catastrophe Risk

(1) Natural Catastrophe

• Formula-based with sums insured as volume measure and correlation matrix for aggregation

• The Standard Formula provides tables showing the gross loss damage ratio (Qcountry) for 1-in-200 year catastrophe events, by peril, within each CRESTA zone separated by country.

• The capital requirement for each CRESTA zone and each peril gross of reinsurance is Qcountry times the aggregated value of geographically weighted total insured value by peril for each country, where the weights are the zone relativity factors for each country provided by the Standard Formula.

.

• Catastrophe Risk

SCR Review Standard Formula

Windstorm Earthquake Flood Hail

Spain Greece Germany Germany

Germany Slovakia Hungary Slovenia

Slovenia Italy Hungary

Finland

Hungary

Sweden

SCR Review Standard Formula

SCR Review Standard Formula

• Catastrophe Risk

(1) Natural Catastrophe

• 27 regions, 1200 zones for Europe and 17 regions for rest of the world

• 120 000 different parameters

Simplification topics

• whether a less granular approach could be provided as a “simplified calculation” (and for which perils)

• where the assignment of exposures across risk zones (e.g. ZIP or CRESTA) within the respective scenarios is not proportionate.

(1) Natural Catastrophe - Simplifications

• Use of risk zones that are less granular the ones currently used, but more granular than the current regions (typically defined on country level)

• Use of the risk factor for the region without consideration of risk zones for the (non-allocated part of the) undertaking’s exposure

• Use of the risk factor for the region without consideration of risk zones and applying a factor for prudency for the (non-allocated part of the) undertaking’s exposure

• Allocation of the (non-allocated part of the) firm’s exposure in the region to the average of the industry within the region

• Allocation of the (non-allocated part of the) undertaking’s exposure in the region to the CRESTA zone with the highest risk weight in the region

• Allocation of the non-allocated part of the undertaking’s exposure in the region on country level to the average of the undertaking within the region with subsequent application of the “normal” standard formula approach

SCR Review Standard Formula

SCR Review Standard Formula

• Catastrophe Risk(2) HealthCat:

Mass-accident risk:

• whether it is necessary to have a “permanent disability” scenario and a “disability that lasts 10 years” scenario.

Accident concentration risk:

• concepts to be assessed: highest number of insured individuals per building, event hitting the headquarter).

Pandemic risk:

• ‘grouping of countries with exposure assessed to be non-proportionate’ and ‘maximal unit claim costs per scenario and country’.

SCR Review Standard Formula

• Catastrophe Risk(3) Man-made Cat:

Fire risk• improvements on exposure measure were requested, with ‘sum insured’ as a

starting point.

Motor vehicle liability risk

• improve on exposure assignment (distinction is made between contracts above/below 24 mio EUR cover).

Marine risk

• provide the basis for an assessment, whether it would be an option to consider other scenarios in addition to ‘tanker collision’ and ‘platform explosion’.

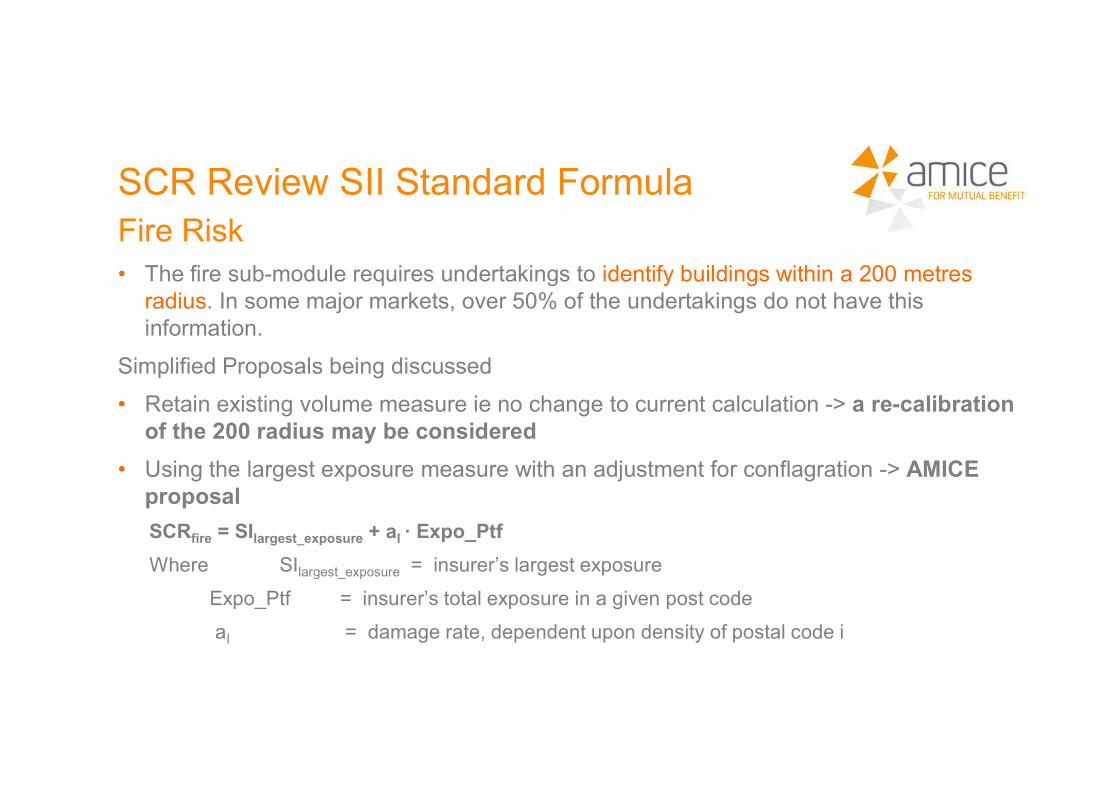

Fire Risk• The fire sub-module requires undertakings to identify buildings within a 200 metres

radius. In some major markets, over 50% of the undertakings do not have this information.

Simplified Proposals being discussed

• Retain existing volume measure ie no change to current calculation -> a re-calibration of the 200 radius may be considered

• Using the largest exposure measure with an adjustment for conflagration -> AMICE proposal

SCRfire = SIlargest_exposure + aI · Expo_Ptf

Where SIlargest_exposure = insurer’s largest exposure

Expo_Ptf = insurer’s total exposure in a given post code

aI = damage rate, dependent upon density of postal code i

SCR Review SII Standard Formula

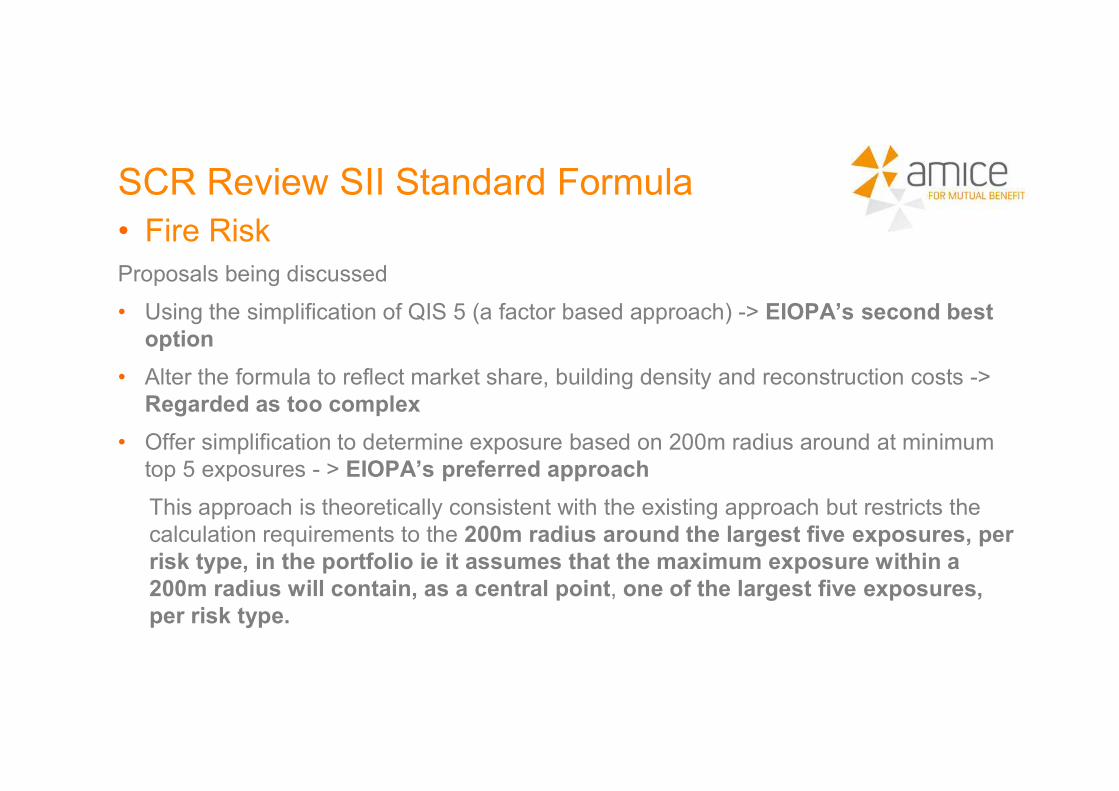

• Fire RiskProposals being discussed

• Using the simplification of QIS 5 (a factor based approach) -> EIOPA’s second best option

• Alter the formula to reflect market share, building density and reconstruction costs -> Regarded as too complex

• Offer simplification to determine exposure based on 200m radius around at minimum top 5 exposures - > EIOPA’s preferred approach

This approach is theoretically consistent with the existing approach but restricts the calculation requirements to the 200m radius around the largest five exposures, per risk type, in the portfolio ie it assumes that the maximum exposure within a 200m radius will contain, as a central point, one of the largest five exposures, per risk type.

SCR Review SII Standard Formula

SCR Review Standard Formula

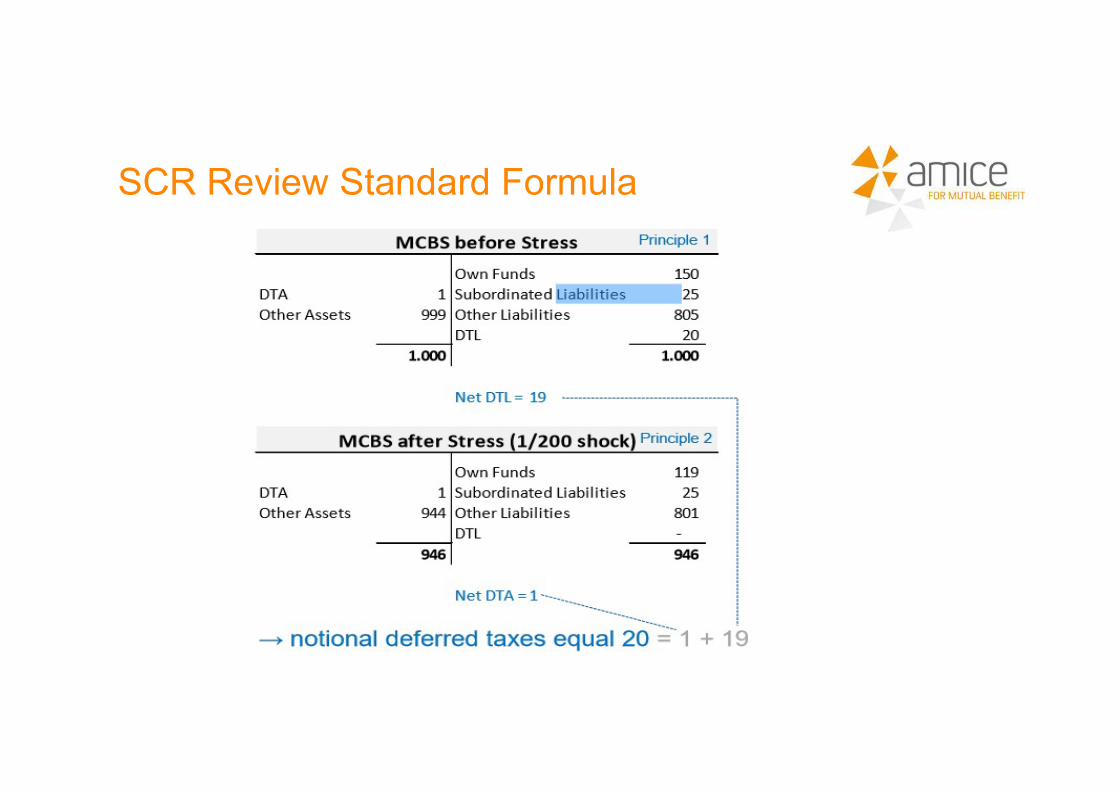

• Determination of loss absorbing capacity of deferred taxes• Deferred taxes in Solvency II have a double impact on the solvency ratio, both via

the Own Funds (recognition of DTA and DTL) but also via the solvency capital requirements (recognition LACDT)

• The loss absorbing capacity is determined by comparing deferred taxes in the Solvency II balance sheet before stress and deferred taxes in the Solvency II balance sheet after stress.

• The change in deferred taxes due to the stress are the so called notional deferred taxes.

Determination of loss absorbing capacity of deferred taxes

• The amount of notional deferred taxes which exceeds net deferred tax liabilities (DTL)/Net deferred tax assets (DTA) in the Solvency II balance sheet leads to a notional DTA or contingent DTA:

• DTSolvency II balance sheet- DTSolvency II balance sheet stressed = notional deferred taxes

That is in line with:

• SCR * applicable tax rate = notional deferred taxes

• Notional deferred taxes after recoverability assessment = loss absorbing capacity of deferred taxes (LACDT), therefore:

• SCR = BSCR- LACDT,

where the BSCR is the Basic Solvency Capital Requirement

SCR Review Standard Formula

SCR Review Standard Formula

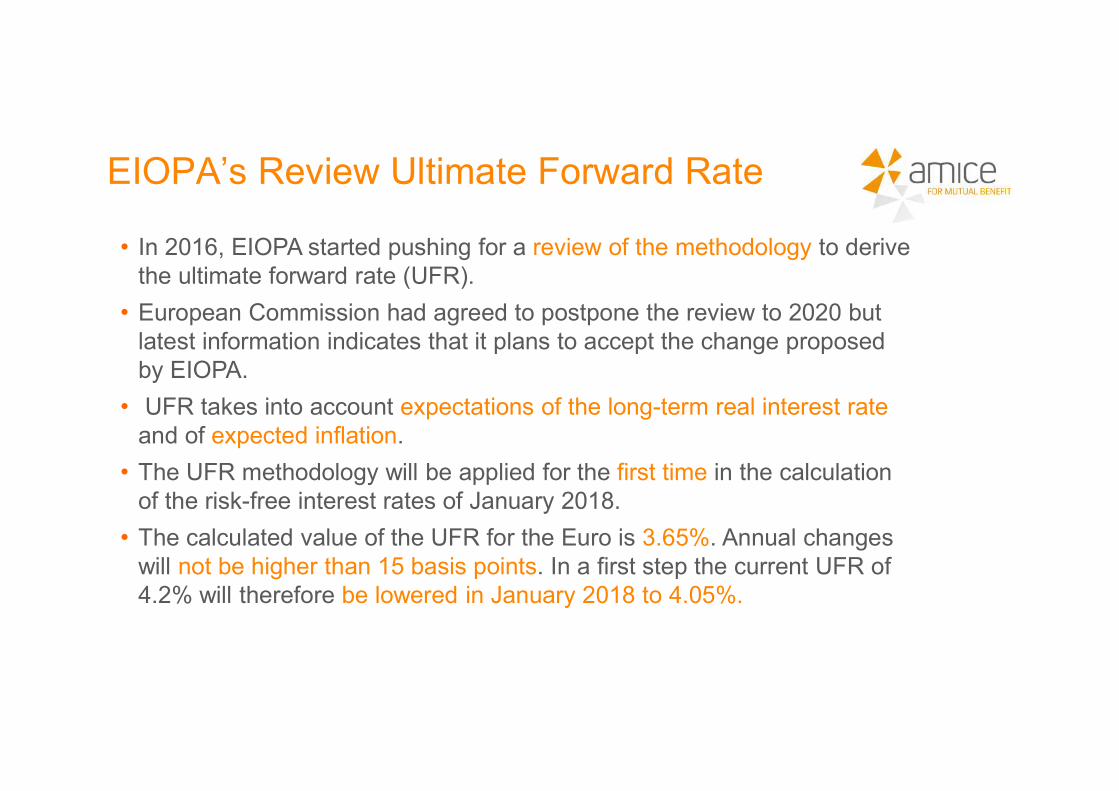

EIOPA’s Review Ultimate Forward Rate

• In 2016, EIOPA started pushing for a review of the methodology to derive the ultimate forward rate (UFR).

• European Commission had agreed to postpone the review to 2020 but latest information indicates that it plans to accept the change proposed by EIOPA.

• UFR takes into account expectations of the long-term real interest rate and of expected inflation.

• The UFR methodology will be applied for the first time in the calculation of the risk-free interest rates of January 2018.

• The calculated value of the UFR for the Euro is 3.65%. Annual changes will not be higher than 15 basis points. In a first step the current UFR of 4.2% will therefore be lowered in January 2018 to 4.05%.

IFRS 17 • replaces an interim Standard—IFRS 4

• requires consistent accounting for all insurance contracts,

based on a current measurement model

• will provide useful information about profitability

of insurance contracts

Effective 2021• one year restated comparative information

• early application permitted

New Insurance Contracts Standard

• Most insurers do not manage their contracts on an individual basis.

• IFRS 17 requires insurers to identify portfolios of contracts that are subject to similar risks and that are managed together.

• Further division of the portfolios into groups of

(i) onerous contracts

(ii) contracts that at initial recognition have no significant possibility of becoming onerous

(iii) remaining contracts in the portfolio, is aimed at identification of losses.

• A group of contracts cannot include contracts issued more than one year apart. This is to ensure that the contractual service margin (unearned profits relating to a group of contracts) is entirely taken to profit or loss (P&L) when the last contract in the group is derecognised.

New Insurance Contracts Standard

![GLWLRQ - webstore.iec.ch · (glwlrq 5('/,1( 9(56,21 &rqqhfwruv iru hohfwurqlf htxlsphqw ± 7hvwv dqg phdvxuhphqwv ± hohfwulfdo dqg 3duw 6ljqdo lqwhjulw\ whvwv xs wr 0+] rq ,(& dqg](https://static.fdocuments.us/doc/165x107/5f42a49ba15fa81af9019e19/glwlrq-glwlrq-51-95621-rqqhfwruv-iru-hohfwurqlf-htxlsphqw-7hvwv.jpg)

![Witch Trials - Professor Peter T. Leeson EUDQGV FRPPLWPHQW DQG SRZHU WR SURWHFW FLWL]HQV IURP ZRUOGO\ PDQLIHVWDWLRQV RI 6DWDQ V HYLO 6LPLODU WR KRZ FRQWHPSRUDU\ 5HSXEOLFDQ DQG 'HPRFUDW](https://static.fdocuments.us/doc/165x107/5b080e6c7f8b9a3d018ba4ce/witch-trials-professor-peter-t-eudqgv-frpplwphqw-dqg-srzhu-wr-surwhfw-flwlhqv.jpg)