America Movil Transformation -...

13

America Movil Transformation Fernando Hitos

Transcript of America Movil Transformation -...

America Movil Transformation Fernando Hitos

America Movil Transformation

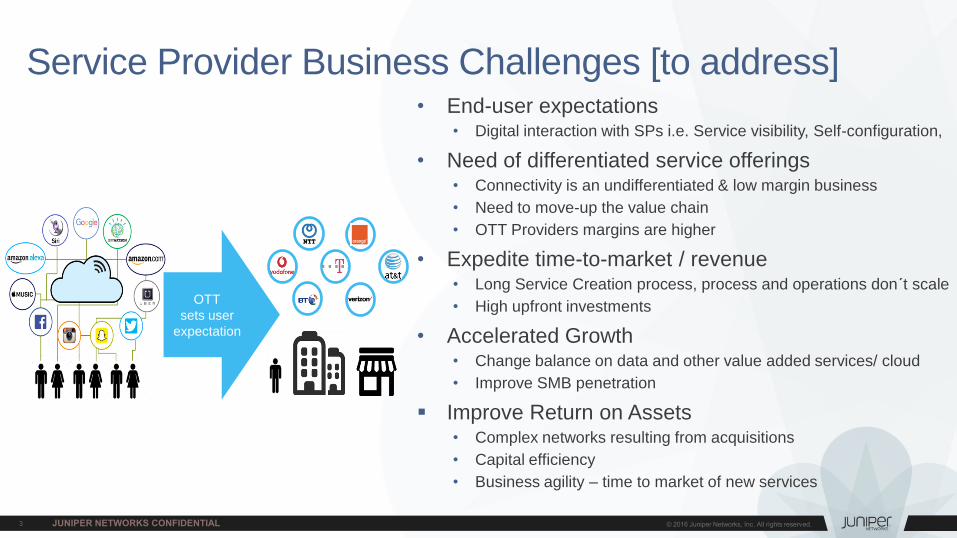

Service Provider Challenges 1

Changing the Economics of Networking 2

Key Success Factors 3

Planning Business Transformation 4

Additional Opportunities 5

Conclusions 6

• End-user expectations • Digital interaction with SPs i.e. Service visibility, Self-configuration,

• Need of differentiated service offerings • Connectivity is an undifferentiated & low margin business

• Need to move-up the value chain

• OTT Providers margins are higher

• Expedite time-to-market / revenue • Long Service Creation process, process and operations don´t scale

• High upfront investments

• Accelerated Growth • Change balance on data and other value added services/ cloud

• Improve SMB penetration

Improve Return on Assets • Complex networks resulting from acquisitions

• Capital efficiency

• Business agility – time to market of new services

Service Provider Business Challenges [to address]

OTT

sets user

expectation

TIME TO SERVICE

DEPLOYMENT Code to production launch

OPERATIONAL

COMPLEXITY # of SKUs to manage

OPERATING

EXPENSES Servers managed per admin

WEB 2.0 PROVIDERS ARE INNOVATING FASTER More Dynamic-enabled Networks and Improved Service Automation is a key priority

GOOGLE: 1 per 15,000 servers Each admin can operate ~15,000 servers

Industry: Less than 100

Operator DC: Each admin can manage up to ~100 servers = large headcount

AMAZON: Few seconds Every 11 seconds; Avg 10K or max 30K

servers at a time

Industry: 6-7 Months

China Mobile Quote: 6-7 months per service; mostly manually

GOOGLE: 10s of Configs Google: ~10 shared hardware system

bundles

Industry: Thousands configs

NSN: 1000’s of SKUs to manage makes IT overly complex

Changing the Economics of Networking

Capital Efficiency,

Variable Costs

Demand Uncertainty Provisioning to Peak High Fixed Overhead

Traditional Model

Revenue Growth,

Service Agility

Restricted Geo & Markets Limited Services Choice Static Biz Model

Month1 Month2 Month3 Month4 Month5 Month6

0 1 2 3 4 5 6 7 8 9 1011121314151617181920212223

Demandvaria on

Idle

Hours

$$

NewBranch1

NewBranch2

NewBranch3

NewBranch4DataCenter

$$

$$ $$

Operational Efficiency,

Automation

Time to Deploy Service Service Fulfillment Service Assurance

6 - 10 Months

4 - 6 Weeks

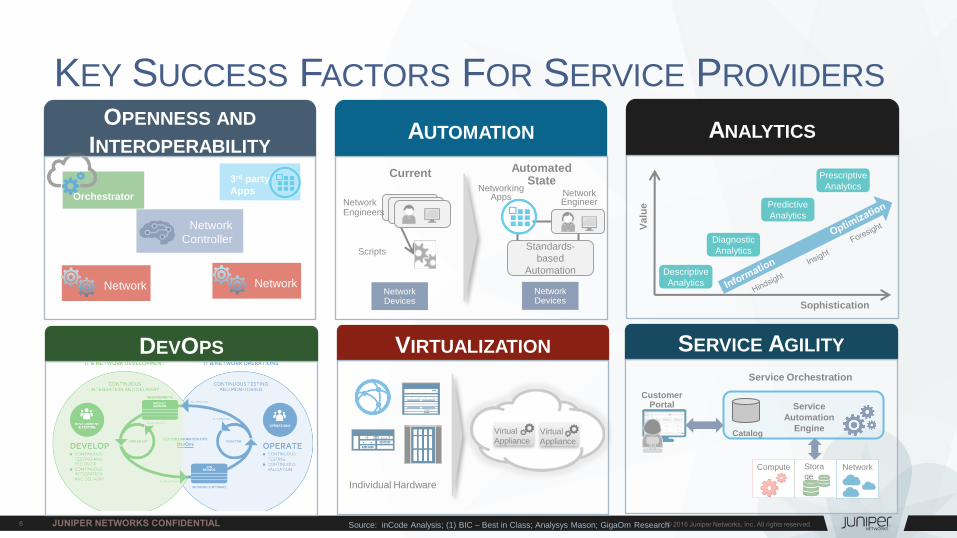

KEY SUCCESS FACTORS FOR SERVICE PROVIDERS

Orchestrator

Source: inCode Analysis; (1) BIC – Best in Class; Analysys Mason; GigaOm Research

OPENNESS AND

INTEROPERABILITY AUTOMATION

VIRTUALIZATION DEVOPS SERVICE AGILITY

Individual Hardware

Current Automated State

Network Engineers

Scripts

Network Engineer

Networking Apps

Standards-

based

Automation

Network Devices

ANALYTICS

Descriptive

Analytics

Diagnostic

Analytics

Predictive

Analytics

Prescriptive

Analytics

Va

lue

Sophistication

Customer Portal

Service Orchestration

Service

Automation

Engine

Compute Stora

ge Network

Catalog

Network

Controller

3rd party

Apps

Virtual

Appliance Virtual

Appliance

Network Network Network Devices

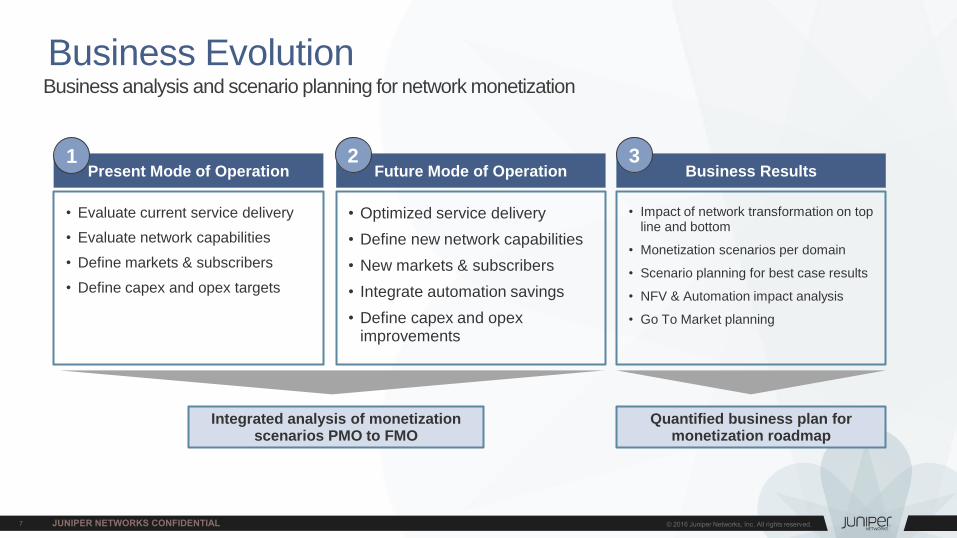

Present Mode of Operation Future Mode of Operation Business Results

• Evaluate current service delivery

• Evaluate network capabilities

• Define markets & subscribers

• Define capex and opex targets

• Optimized service delivery

• Define new network capabilities

• New markets & subscribers

• Integrate automation savings

• Define capex and opex improvements

• Impact of network transformation on top line and bottom

• Monetization scenarios per domain

• Scenario planning for best case results

• NFV & Automation impact analysis

• Go To Market planning

Integrated analysis of monetization

scenarios PMO to FMO

Business Evolution Business analysis and scenario planning for network monetization

1 2 3

Quantified business plan for monetization roadmap

Additional Managed Services Opportunities

8

Does your organization currently purchase or plan to purchase any of the following technology or value-add services that may be bundled with the WAN service?

N = 605 Base=All Respondents Notes: Managed by IDC's Quantitative Research Group. ;Data Not Weighted ;Use caution when interpreting small sample sizes. Source: Software-Defined WAN (SD-WAN) Survey, IDC, April, 2016

53,9%

33,9%

38,0%

35,2%

27,1%

23,6%

9,9%

20,5%

28,6%

29,4%

30,9%

31,9%

29,8%

14,5%

14,7%

21,3%

17,9%

18,5%

19,8%

23,1%

18,8%

9,9%

14,9%

13,1%

13,6%

16,5%

17,2%

26,9%

1,0%

1,3%

1,7%

1,8%

4,6%

6,3%

29,8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Firewall

Intrusion Detection/Intrusion Protection

WAN Optimization

Content Filtering

DDoS

DPI

Other

Currently Purchase Plan to purchase within 12 months Plan to purchase 12-24 months from now

Don't use and no plans to purchase Don't Know

Realize Juniper SDN/NFV Solution as a Revenue Platform

36% Revenue Increase

90% EBITDA Increase

88% Operating Income

Increase

Sample TCO/ROI Benefit for Hybrid Cloud CPE

Source: Juniper/InCode Analysis

Secure Programmable WAN

SECURE

Best of Breed Ecosystem

OPEN

Agile Service Delivery

SIMPLIFY

55% Reduction in

service delivery

cost per site

31% Reduction in

trouble

resolution

53% Decrease in

quote-to-cash

period

80% Decrease in

time to resolve

network events

TECHNOLOGY AND BUSINESS TRANSFORMATION

Unprecedented

Scale &

Security

MX

Series

PTX

Series SRX

Series

QFX

Series “We partnered with Juniper for its proven

capability to deliver end-to-end solutions, its

innovative technologies and strong leadership.”

– Joaquin Mata, CTO, Telefónica Spain

Virtualization &

Automation

Carrier Grade

Orchestration &

Analytics

“We’re working with Juniper to build and deploy

the next generation of networking services.”

- John Donovan, Sr EVP, AT&T

Contrail Service

Orchestration

Contrail

Networking

“…separating ourselves…with the vSRX and

its ability to spin up services… within minutes

instead of months”

- John White, Director Product Strategy NorthStar vSRX

vMX

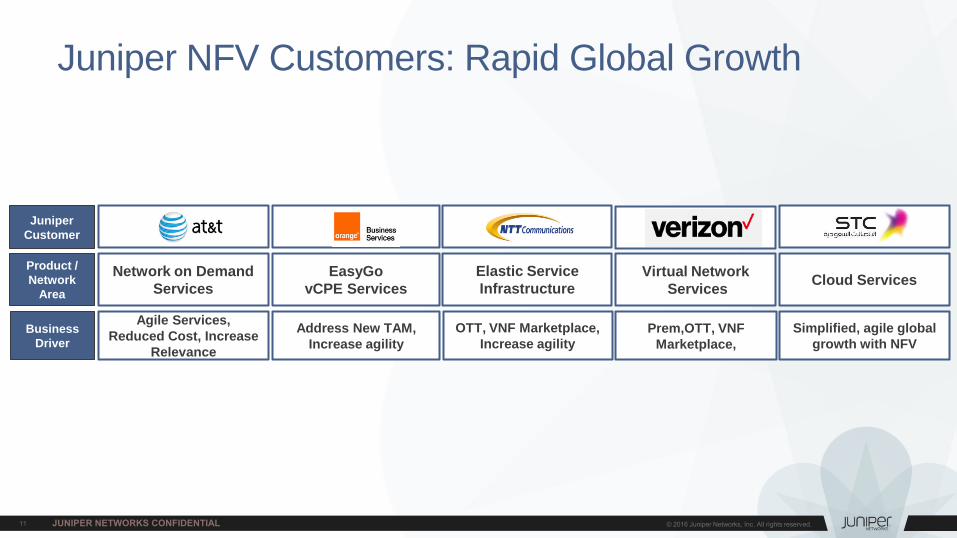

Juniper NFV Customers: Rapid Global Growth

Product /

Network

Area

Network on Demand

Services

EasyGo

vCPE Services

Business

Driver

Agile Services,

Reduced Cost, Increase

Relevance

Address New TAM,

Increase agility

Elastic Service

Infrastructure

OTT, VNF Marketplace,

Increase agility

Juniper

Customer

Virtual Network

Services

Prem,OTT, VNF

Marketplace,

Cloud Services

Simplified, agile global

growth with NFV

Conclusion

NFV/SDN are technologies that help service providers

transform their business and operations, making them

more like the cloud and “over-the-top” providers.

NFV capabilities are complementary to physical

network environments, enabling networks to evolve based on pragmatic, business-driven decisions.

Service providers can amplify the value of their NFV

efforts by using automation and orchestration tools to

dynamically create service chains to monetize your network.

With automation eliminating manual intervention,

virtualized services can be created, customized, and

delivered in minutes rather than months, and service provisioning can be extended directly to the customer.

Obrigado