A.M. Best Market Briefing at the EAIC 2018 · purchase, sell or hold any securities, insurance...

37

A.M. Best Market Briefing at the EAIC 2018

Transcript of A.M. Best Market Briefing at the EAIC 2018 · purchase, sell or hold any securities, insurance...

A.M. Best Market Briefing

at the EAIC 2018

Agenda

2

Perspectives on the

Global Reinsurance Market

Stefan Holzberger

Chief Rating Officer

7 May 2018

© AM Best Company, Inc. (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN ISPROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED,REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FORSUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANSWHATSOEVER, BY ANY PERSON WITHOUT AMB’s PRIOR WRITTEN CONSENT. All information contained herein is obtained by AMB fromsources believed by it to be accurate and reliable. AMB does not audit or otherwise independently verify the accuracy or reliability of informationreceived or otherwise used and therefore all information contained herein is provided “AS IS” without warranty of any kind. Under nocircumstances shall AMB have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, orrelating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of AMB or any of its directors,officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication ordelivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (includingwithout limitation, lost profits), even if AMB is advised in advance of the possibility of such damages, resulting from the use of or inability to use,any such information. The credit ratings, financial reporting analysis, projections, and other observations, if any, constituting part of theinformation contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations topurchase, sell or hold any securities, insurance policies, contracts or any other financial obligations, nor does it address the suitability of anyparticular financial obligation for a specific purpose or purchaser. Credit risk is the risk that an entity may not meet its contractual, financialobligations as they come due. Credit ratings do not address any other risk, including but not limited to, liquidity risk, market value risk or pricevolatility of rated securities. AMB is not an investment advisor and does not offer consulting or advisory services, nor does the company or itsrating analysts offer any form of structuring or financial advice. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY,TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OROTHER OPINION OR INFORMATION IS GIVEN OR MADE BY AMB IN ANY FORM OR MANNER WHATSOEVER. Each credit rating or otheropinion must be weighed solely as one factor in any investment or purchasing decision made by or on behalf of any user of the informationcontained herein, and each such user must accordingly make its own study and evaluation of each security or other financial obligation and ofeach issuer and guarantor of, and each provider of credit support for, each security or other financial obligation that it may consider purchasing,holding or selling.

4

Reinsurance Market Dynamics

Outlook ?

Convergence Capital

Intense Competition

Earnings Strained

Excess Capital

Inflation Potential

Low Investment

Yields

4

6

Global Reinsurance

Performance Results & Trends

Total Economic and Insured Losses

7

*Due to rounding, numbers do not sumSource: Swiss Re Institute

2017 2016Annual

Change (%)10-Year Average

Economic LossesUSD

Billions

USD

Billions

USD

Billions

Nat Cat 330 171 93% 178Man-made 7 10 -22% 12

Total 337 180* 87% 190

Insured LossesNat Cat 138 48 190% 50Man-made 6 8 -25% 7

Total 144 56 158% 58*

6

Global Combined Ratio

8

Source: A.M. Best data and research

55.9% 56.2% 56.2% 60.6%

76.5%

61.1%

31.9% 33.5% 34.2%34.7%

33.6%

33.6%

5.8% 5.4% 6.0% 5.8%

4.0%5.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0%

20%

40%

60%

80%

100%

120%

2013 2014 2015 2016 2017 5yr Avg

Expense Ratio Loss Ratio Loss Reserve Development

110.1%

89.7% 90.4%95.2%

87.9%94.7%

7

Global Return on Equity

9

Source: A.M. Best data and research

13.0%

11.6%

9.5%

8.3%

-0.3%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2013 2014 2015 2016 2017

Return on Equity Five-Year Average

2018 Insurance

Market Briefing -

3 April 2018 10

Source: A.M. Best data and research

8.4%

4.5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Five -Year Average Return on Equity Five -Year Average Return on Equity Excluding LossReserve Development

Global Return on Equity – Five-Year Average

11

Market Capacity

Top 10 Largest Reinsurance Groups

10 September 2017 12

Reinsurance WP Total

Life & Non-Life Shareholders’(USD Millions) Gross Net Funds

Swiss Re 35,622 33,570 35,716

Munich Re 33,154 31,891 33,493

Hannover Ruck 17,232 15,192 10,264

SCOR 14,569 13,238 7,055

Berkshire Hathaway 12,709 12,709 286,359

Lloyd's 11,576 8,694 34,101

RGA 10,107 9,249 7,093

China Re 7,857 7,517 10,384

Great West Lifeco 6,195 6,112 13,857

Korean Re 5,554 3,903 1,755

Source: A.M. Best data and research. Ranked by unaffiliated gross premium written in 2016

Estimate for Dedicated Reinsurance Capacity

13

320 340 332

345 345

48

60 68

75 82

0

50

100

150

200

250

300

350

400

450

2013 2014 2015 2016 2017

Convergence Capacity

Traditional Capacity

* ForecastSource: A.M. Best and Guy Carpenter

(US

D B

illio

ns)

Convergence Capacity

14

Source: A.M. Best and Guy Carpenter

4 3 4 5 5

25

34

41

4952

19

23

23

22

25

0

10

20

30

40

50

60

70

80

90

2013 2014 2015 2016 2017E*

ILW Collateralized Re Catastrophe Bonds

*Forecasted

0

10

20

30

40

50

60

70

0

2

4

6

8

10

12

14

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Num

ber o

f Deals

CAT Bonds Issued Number of Deals

CAT BondsConvergence Capacity

Source: A.M. Best and Artemis

15

Market Strategies & Opportunities

Global Market Strategies

16

Client Agent & Broker

Primary Insurance Company

Reinsurance Broker

Reinsurance Company

Convergence Capital

In A.M. Best’s opinion…

The market will continue to

become more efficient as all

players strive to become closer to

the client

Opportunities for the Reinsurance Sector

17

Cyber Insurance

Flood Mortgage Terrorism InsurTech

Global Reinsurance Outlook

Headwinds

Intense competition

Incr. interest from 3rd party capital

Earnings under pressure

Excess capacity hinders improvement

Potential for increased inflation

Although capitalization remains strong and rate deterioration halted, pressure on margins continues. Over the intermediate term, returns for some reinsurers will fall short on a risk-adjusted basis.

Maintain negative outlook.

Tailwinds

Cession rates increasing

Cat losses temporarily stabilize rates

Favorable reserve development

Strong risk-adjusted capital

Increase in interest rates

M&A

17

Credit Ratings and Market Update

in China

Christie Lee

Head of Analytics, Northeast Asia

7 May 2018

4%

16%

42%

34%

4%0%

4%

15%

44%

33%

2% 2%

A + + A + A A - B + + B +

FSR at Mar 30, 2017 FSR at Mar 30, 2018

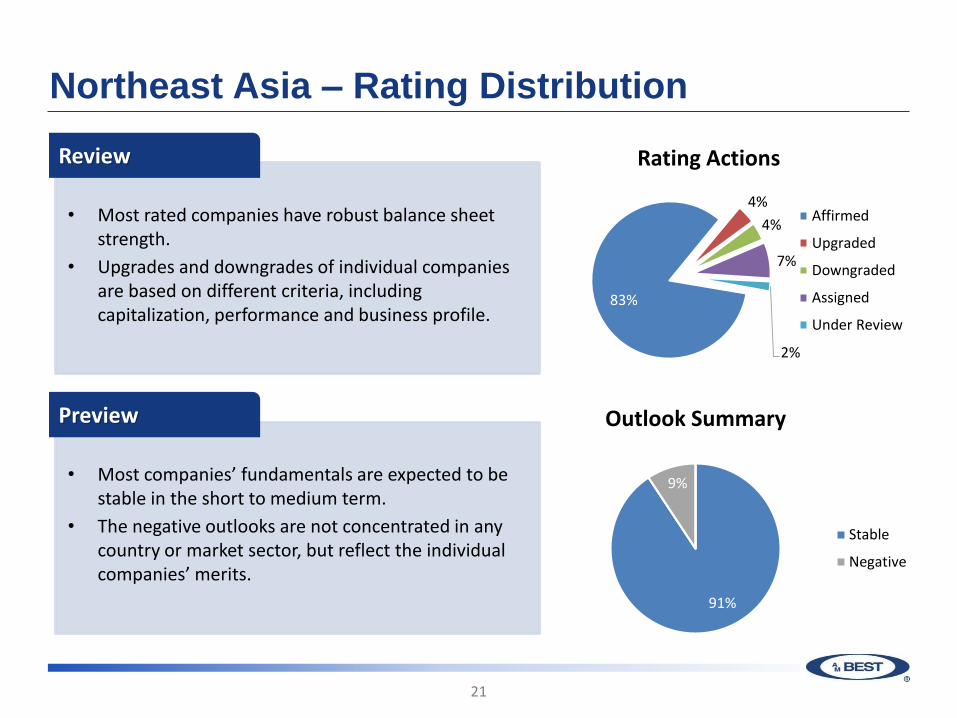

Northeast Asia – Rating Distribution

20

• High growth

• Heavily weighted to Motor line

• Marginal underwriting results

• Japan: Slow domestic growth and overseas expansion

• Korea: Raising capital to get prepared for IFRS 17 and K-ICS in 2021

China Japan/ Korea

Key Market Characteristics

Northeast Asia – Rating Distribution

21

83%

4%

4%

7%

2%

Rating Actions

Affirmed

Upgraded

Downgraded

Assigned

Under Review

• Most rated companies have robust balance sheet strength.

• Upgrades and downgrades of individual companies are based on different criteria, including capitalization, performance and business profile.

Review

• Most companies’ fundamentals are expected to be stable in the short to medium term.

• The negative outlooks are not concentrated in any country or market sector, but reflect the individual companies’ merits.

Preview

91%

0%9%

0%

Outlook Summary

Stable

Negative

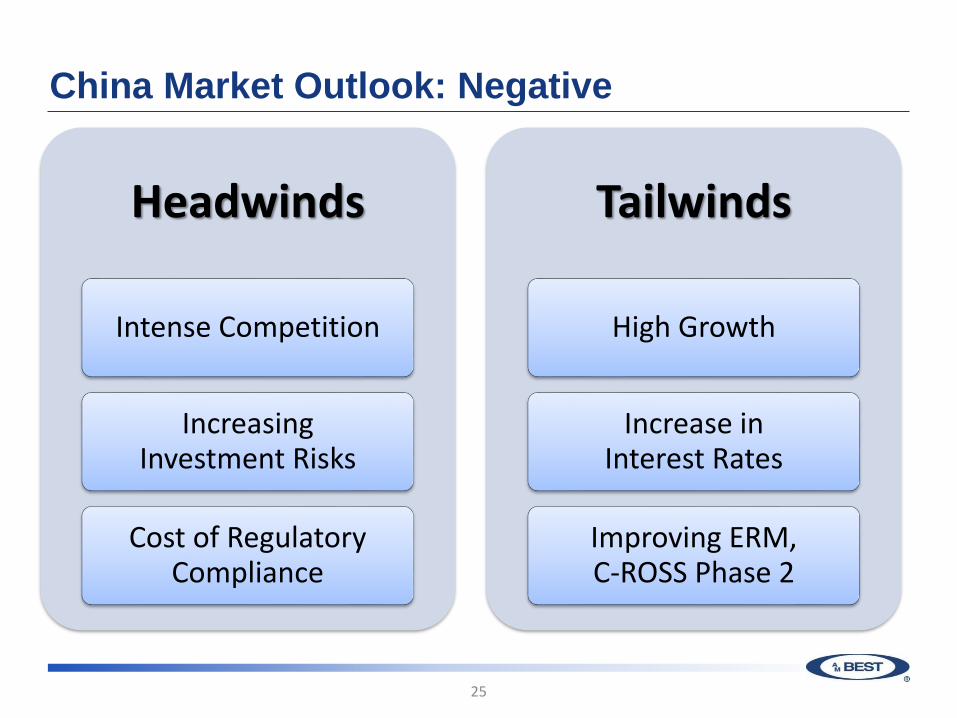

China Market Outlook: Negative

Headwinds

Intense Competition

Increasing Investment Risks

Cost of Regulatory Compliance

Tailwinds

High Growth

Increase in Interest Rates

Improving ERM, C-ROSS Phase 2

22

97.8% 98.0% 97.6%

106.4%108.3% 108.8%

2015 2016 2017 2015 2016 2017

China

23

Non-Life Real Premium Growth (2016)

Combined Ratio: China Non-Life Insurers

Large Insurers (Motor Focus)

S/M Insurers (Motor Focus)

Growth Opportunities Results in Intense Competition:

• China non-life market’s growth is almost equal to that of North America and Western Europe combined.

• In 2017, China’s non-life gross premium written grew to RMB 1 trillion (USD 160 billion), a 13.8% increase over 2016.

• Motor still accounts for over 70% of the market portfolio.

• Motor detariffication has intensified competition.

2018 EAIC 7 May 2018

China

24

• Overall operating results are highly reliant on investment returns.

• Investment returns are subject to domestic market volatility.

• Insurers have been increasing their allocations to other investments.

0

10

20

30

40

50

60

2013 2014 2015 2016 2017

RM

B (

Bri

llio

n)

Net Profit before Tax (Top 5)

Underwriting Investment

9.9% 11.7% 15.6% 18.3% 24.7% 27.4%

2012 2013 2014 2015 2016 2017

Investment Allocation (Top 5)

Cash & cash equivalents Bonds Equities and funds Long-term equities Other Investments

China Market Outlook: Negative

Headwinds

Intense Competition

Increasing Investment Risks

Cost of Regulatory Compliance

Tailwinds

High Growth

Increase in Interest Rates

Improving ERM, C-ROSS Phase 2

25

China - Opportunities

High growth and profitable lines - Liabilities, Credit & Surety, Personal Accident

Inward Reinsurance - Diversified the portfolio

Belt and Road – Collaborations between domestic and foreign insurers

Technology- Distribution, operational efficiencies, innovative products

26

Credit Ratings and Market Update in

Southeast Asia

Chi-Yeung Lok

Head of Analytics, Southeast Asia

and Australasia

7 May 2018

Overview

28

Introduction

Rating Distribution and Actions

Trends

Headwinds & Tailwinds

South East Asia – A.M. Best Rated Markets

29

South East Asia – Rating Distribution

30

Key Market Characteristics

Growth MarketsMature Markets

• Slowdown in growth

• Less commercial fire

• Small markets

• Still growing

• More commercial, fire

• Small markets – other than India

3%

15%

38%

33%

10%

3%

16%

39%

32%

11%

A+ A A- B++ B+

FSR as at Mar 17 FSR as at Mar 18

Source: A.M. Best

87%

2%

8%

3%

Rating Actions

Affirmed

Upgraded

Downgraded

Initial

79%

5%

16%

Outlooks

Stable

Positive

Negative

South East Asia – Rating Actions and Outlooks

31

• Most companies have solid risk-adjusted capitalization

• Downgrades / outlook changes

• Performance issues

• Reserving issues

Review

• Underwriting margins still positive in most South East

Asian markets – but becoming slimmer

• Ability to adapt to low growth environment and shift to

personal lines

• Relevance of technology in terms of channels,

efficiency, risk management?

Preview

Source: A.M. Best

Premium Growth Trends

32

0%

5%

10%

15%

20%

2012 2013 2014 2015 2016 2017

Vietnam

0%

5%

10%

15%

20%

2012 2013 2014 2015 2016 2017

Indonesia

-5%

0%

5%

10%

15%

2012 2013 2014 2015 2016 2017

Singapore

-5%

0%

5%

10%

15%

2012 2013 2014 2015 2016 2017

Thailand

• Growth in mature markets slowing more significantly

• Shift to retail in growth markets

• Slow rollout of government initiatives – fire and commercial growing slower than expected

-5%

0%

5%

10%

15%

2012 2013 2014 2015 2016 2017

Malaysia

Source: A.M. Best and regulatory statistics

0%

5%

10%

15%

20%

2013 2014 2015 2016 2017

Philippines

Combined Ratio Trends

33

80%

90%

100%

2012 2013 2014 2015 2016 2017

Vietnam

80%

90%

100%

2012 2013 2014 2015 2016 2017

Indonesia

80%

90%

100%

2012 2013 2014 2015 2016 2017

Malaysia

80%

90%

100%

2012 2013 2014 2015 2016 2017

Singapore

80%

90%

100%

2012 2013 2014 2015 2016 2017

Thailand

90%

100%

110%

2012 2013 2014 2015 2016 2017

Philippines

• Underwriting margins positive but declining

• As premiums are increasing in growth markets, so are combined ratios

• Need to manage quality of growth and expense ratios

Source: A.M. Best and regulatory statistics

UW Margins – South East Asia (2016)

34

48%55%

51%43%

52% 54%

49%40%

43%51%

41%33%

Vietnam Thailand Indonesia Philippines Singapore Malaysia

Loss Ratio Expense Ratio

Source: A.M. Best and regulatory statistics

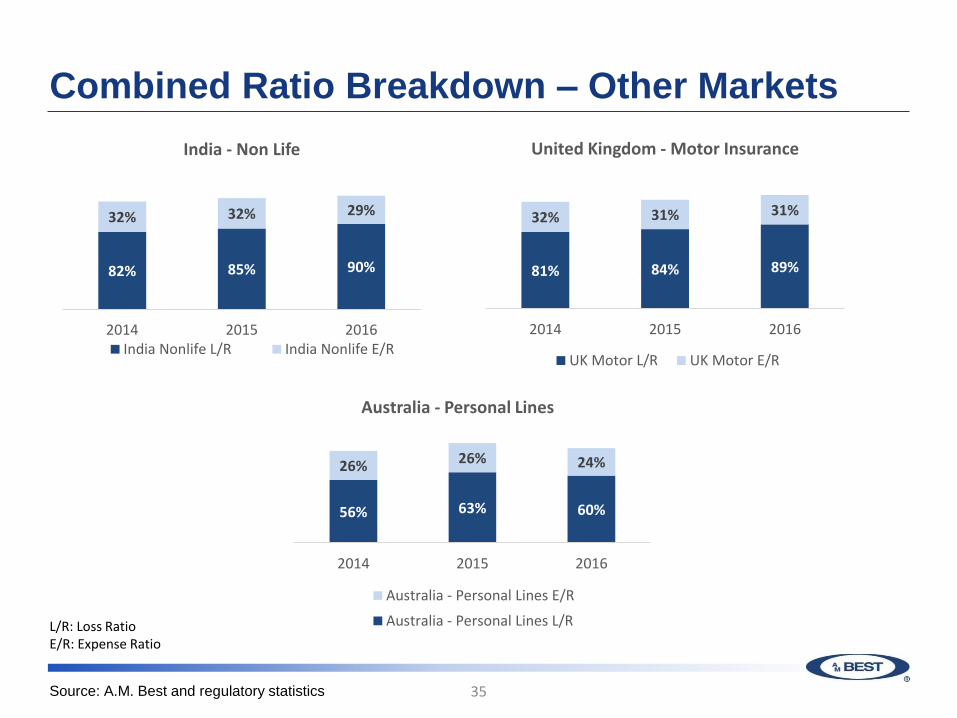

Combined Ratio Breakdown – Other Markets

35

81% 84% 89%

32% 31% 31%

2014 2015 2016

United Kingdom - Motor Insurance

UK Motor L/R UK Motor E/R

82% 85% 90%

32% 32% 29%

2014 2015 2016

India - Non Life

India Nonlife L/R India Nonlife E/R

56% 63% 60%

26% 26% 24%

2014 2015 2016

Australia - Personal Lines

Australia - Personal Lines E/R

Australia - Personal Lines L/RL/R: Loss RatioE/R: Expense Ratio

Source: A.M. Best and regulatory statistics

Conclusion

36

Headwinds

• Stagnant growth

• Quality of growth

• Technical expertise

Tailwinds

• Technology

• Low penetration

• Solid risk-adjusted capitalization

Questions & Answers