ALXN Buy Recommendation

19

Eric Ebersole This report is published for educational purposes by students competing in the CFA Society of Florida Investment Research Challenge, part of CFA Institute Global Investment Research Challenge. Important disclosures appear at the back of this report Industry: Biotechnology Sector: Healthcare Ticker: ALXN (NASDAQ) Recommendation: Buy Price: $ 190.55 (as of 10/27/14) Price Target: $215.11 Undervalued by: 11.95% Earnings/Share Mar. Jun. Sep. Dec. Year P/E Ratio 2011 $.30 $0.29 $0.37 $0.36 $1.32 75.02 2012 0.45 0.47 0.60 0.60 2.12 73.37 2013 0.65 0.73 0.83 0.87 3.08 95.03 2014E* 1.53 1.12 1.27 1.23 5.07 32.83 2015E* 1.23 1.32 1.44 1.51 5.17 28.25 *Bolded/italicized figures are team estimates Highlights Continued Soliris Success: Soliris is the only market approved product currently being sold by Alexion, however, it continues to increase in sales every quarter. On average, growth year on year has been 43.11% while quarter on quarter growth on average totals 10.5%. As Soliris increases market acceptance and continues to receive various government approvals and subsidies, the revenue generated will continue to increase. Superior Market Positioning: Alexion has positioned themselves into a market in which no other competitor exists. By targeting ultra-rare diseases Alexion is able to capture one hundred percent of the revenue from the patients receiving treatment for each particular disease. While the total patients diagnosed with these diseases are slim, Alexion has removed a key risk factor which almost all business are exposed to, competition. Alexion looks to continue this tactic moving forward as they have begun development of products targeting multiple other ultra-rare diseases. If Alexion continues to receive patent protection and approvals, their complete market share will be protected. International Penetration: Alexion diversifies its revenue through four main geographical groups: United States, Europe, Southeast Asia (Mainly Japan), and other countries such as Australia. In 2013 sixty-seven percent of sales were generated outside of the United States. This diversification helps to reduce domestic market risk and provide stable revenues if a country were to reduce subsidization or deny patent extension. Also, by implementing an international focus, countries belonging to alliances such as the European Union allow for smoother entrances and may create a more welcoming attitude for necessary government action with multiple countries allowing operation and sale of the product in each country. Stock Valuation: Due to Soliris’ continued market success, superior market positioning, and international penetration alongside strong government relations, Alexion’s stock has an expected return of 22.55%. Further, Alexion is undervalued by 13.55% with a fair value of $215.11. The total return suggests that it is an attractive buy. Source: Thomson Baseline Date: 10/28/2014 Source: Yahoo! Finance

-

Upload

eric-ebersole -

Category

Documents

-

view

133 -

download

2

Transcript of ALXN Buy Recommendation

Eric Ebersole This report is published for educational

purposes by students competing in the CFA

Society of Florida Investment Research

Challenge, part of CFA Institute Global

Investment Research Challenge.

Important disclosures appear at the back of this report

Industry: Biotechnology

Sector: Healthcare

Ticker: ALXN (NASDAQ) Recommendation: Buy

Price: $ 190.55 (as of 10/27/14)

Price Target: $215.11

Undervalued by: 11.95%

Earnings/Share Mar. Jun. Sep. Dec. Year P/E Ratio

2011 $.30 $0.29 $0.37 $0.36 $1.32 75.02

2012 0.45 0.47 0.60 0.60 2.12

73.37

2013 0.65 0.73 0.83 0.87 3.08 95.03

2014E* 1.53 1.12 1.27 1.23 5.07 32.83

2015E* 1.23 1.32 1.44 1.51 5.17 28.25

*Bolded/italicized figures are team estimates

Highlights

Continued Soliris Success: Soliris is the only market approved product currently being sold by Alexion,

however, it continues to increase in sales every quarter. On average, growth year on year has been

43.11% while quarter on quarter growth on average totals 10.5%. As Soliris increases market acceptance

and continues to receive various government approvals and subsidies, the revenue generated will continue

to increase.

Superior Market Positioning: Alexion has positioned themselves into a market in which no other

competitor exists. By targeting ultra-rare diseases Alexion is able to capture one hundred percent of the

revenue from the patients receiving treatment for each particular disease. While the total patients

diagnosed with these diseases are slim, Alexion has removed a key risk factor which almost all business

are exposed to, competition. Alexion looks to continue this tactic moving forward as they have begun

development of products targeting multiple other ultra-rare diseases. If Alexion continues to receive

patent protection and approvals, their complete market share will be protected.

International Penetration: Alexion diversifies its revenue through four main geographical groups:

United States, Europe, Southeast Asia (Mainly Japan), and other countries such as Australia. In 2013

sixty-seven percent of sales were generated outside of the United States. This diversification helps to

reduce domestic market risk and provide stable revenues if a country were to reduce subsidization or

deny patent extension. Also, by implementing an international focus, countries belonging to alliances

such as the European Union allow for smoother entrances and may create a more welcoming attitude for

necessary government action with multiple countries allowing operation and sale of the product in each

country.

Stock Valuation: Due to Soliris’ continued market success, superior market positioning, and

international penetration alongside strong government relations, Alexion’s stock has an expected return of

22.55%. Further, Alexion is undervalued by 13.55% with a fair value of $215.11. The total return

suggests that it is an attractive buy.

Source: Thomson Baseline

Date: 10/28/2014

Source: Yahoo! Finance

CFA Society of Orlando

Stetson University Student Research 7/13/2015

2

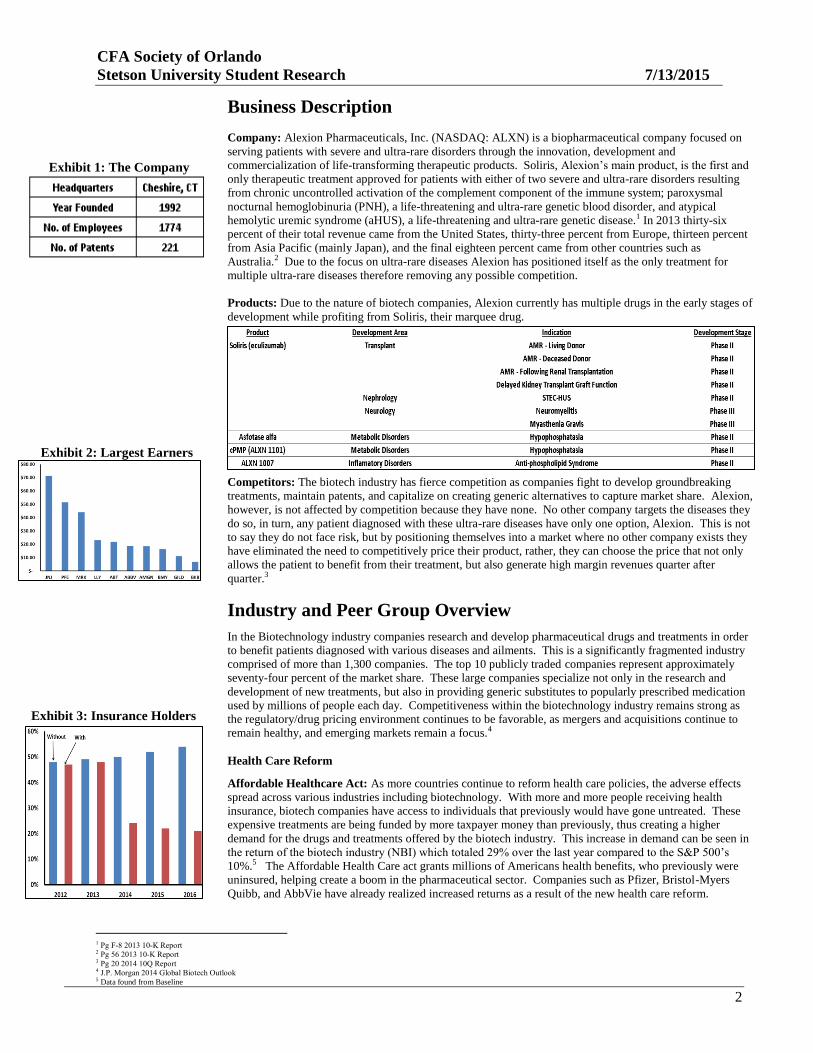

Business Description

Company: Alexion Pharmaceuticals, Inc. (NASDAQ: ALXN) is a biopharmaceutical company focused on

serving patients with severe and ultra-rare disorders through the innovation, development and

commercialization of life-transforming therapeutic products. Soliris, Alexion’s main product, is the first and

only therapeutic treatment approved for patients with either of two severe and ultra-rare disorders resulting

from chronic uncontrolled activation of the complement component of the immune system; paroxysmal

nocturnal hemoglobinuria (PNH), a life-threatening and ultra-rare genetic blood disorder, and atypical

hemolytic uremic syndrome (aHUS), a life-threatening and ultra-rare genetic disease.1 In 2013 thirty-six

percent of their total revenue came from the United States, thirty-three percent from Europe, thirteen percent

from Asia Pacific (mainly Japan), and the final eighteen percent came from other countries such as

Australia.2 Due to the focus on ultra-rare diseases Alexion has positioned itself as the only treatment for

multiple ultra-rare diseases therefore removing any possible competition.

Products: Due to the nature of biotech companies, Alexion currently has multiple drugs in the early stages of

development while profiting from Soliris, their marquee drug.

Competitors: The biotech industry has fierce competition as companies fight to develop groundbreaking

treatments, maintain patents, and capitalize on creating generic alternatives to capture market share. Alexion,

however, is not affected by competition because they have none. No other company targets the diseases they

do so, in turn, any patient diagnosed with these ultra-rare diseases have only one option, Alexion. This is not

to say they do not face risk, but by positioning themselves into a market where no other company exists they

have eliminated the need to competitively price their product, rather, they can choose the price that not only

allows the patient to benefit from their treatment, but also generate high margin revenues quarter after

quarter.3

Industry and Peer Group Overview

In the Biotechnology industry companies research and develop pharmaceutical drugs and treatments in order

to benefit patients diagnosed with various diseases and ailments. This is a significantly fragmented industry

comprised of more than 1,300 companies. The top 10 publicly traded companies represent approximately

seventy-four percent of the market share. These large companies specialize not only in the research and

development of new treatments, but also in providing generic substitutes to popularly prescribed medication

used by millions of people each day. Competitiveness within the biotechnology industry remains strong as

the regulatory/drug pricing environment continues to be favorable, as mergers and acquisitions continue to

remain healthy, and emerging markets remain a focus.4

Health Care Reform

Affordable Healthcare Act: As more countries continue to reform health care policies, the adverse effects

spread across various industries including biotechnology. With more and more people receiving health

insurance, biotech companies have access to individuals that previously would have gone untreated. These

expensive treatments are being funded by more taxpayer money than previously, thus creating a higher

demand for the drugs and treatments offered by the biotech industry. This increase in demand can be seen in

the return of the biotech industry (NBI) which totaled 29% over the last year compared to the S&P 500’s

10%.5 The Affordable Health Care act grants millions of Americans health benefits, who previously were

uninsured, helping create a boom in the pharmaceutical sector. Companies such as Pfizer, Bristol-Myers

Quibb, and AbbVie have already realized increased returns as a result of the new health care reform.

1 Pg F-8 2013 10-K Report 2 Pg 56 2013 10-K Report 3 Pg 20 2014 10Q Report 4 J.P. Morgan 2014 Global Biotech Outlook 5 Data found from Baseline

Exhibit 1: The Company

Exhibit 3: Insurance Holders

Exhibit 2: Largest Earners

CFA Society of Orlando

Stetson University Student Research 7/13/2015

3

Analysts believe that profits for biotechs will increase from $359 billion in 2013 to $476 billion in 2020.6

Obamacare will pave the way for a major rebound in sales with an estimated $115 billion in new business

over a 10-year period. Enrollment in the Medical health insurance program alone is expected to increase by

about 19.5 million people, according to a study conducted by GlobalData. Because pharmaceutical

companies were among the largest supporters of the Affordable Care Act they were able to implement

changes to the legislation in order to create beneficial reforms by implementing new rebates to provide higher

profit potential. This increase in profitability has brought new companies into the market as seen by the more

than thirty IPOs last year in the biotech industry.

European Healthcare Reform: Alexion will not reap as many of these benefits because they are focused on

such a small segment of the market, however, this also means they have minimal exposure to the negative

effects. Unfortunately, health care reform will have its drawbacks that could include cuts in subsidies and

tax credits to competing companies who are researching the same drug or treatment. Luckily, Alexion is the

only company researching and developing treatments for various ultra-rare drugs and has a proven track

record to receive approvals, subsidies, and tax credits from the FDA, EC, and other government agencies.

Countries such as Spain, France, Italy, and Germany are progressing towards new health care acts. These

provisions could lead to a decline in Alexion’s profits if controlled pricing were determined. However,

subsidization would most likely continue due to the political risks of cutting payments for a small

population’s treatments that could lead to death. While Europe has not concluded with a new healthcare act,

each government is determining its own plan to implement the changes seen in the United States. The biotech

industry will be affected by these factors but the positives outweigh the negatives. Short-run costs will be

experienced, but long-run profits will be realized in the future.

Competitive Positioning

Strong Consumer Relationships

Alexion has established itself as a business to business vendor who relies on targeting the large distributors

rather than advertising and marketing itself towards individual patients. Other drugs, such as Tylenol or

Advil, exist in a homogenous market segment thus creating the need to differentiate themselves from the

competition through advertising. Because Alexion treats ultra-rare diseases it is more important that they

target large distributors as well as health care professionals so that once a diagnosis is made those in a

position to do so look to Alexion to benefit their patients. Physician awareness of the options to help patients

diagnosed with the ultra-rare diseases Alexion targets ensures that they will recommend drugs such as Soliris.

Because Alexion’s product is not sold directly sold to consumers over the counter, physicians are one of the

only parties that are able to inform patients of the possibility of Alexion’s treatments. Due to the nature of

these ultra-rare diseases physicians’ knowledge of these ailments is limited. Informing doctors of the

benefits, cost, and process of the treatment allows for not only the doctors to be more informed, but also the

patients because they will be receiving a better explanation. As more physicians become aware and educated

on Alexion’s products the revenues will increase as a result of more physicians prescribing the treatment to

their patients.

Brand Value and Selling Price Premium

In the pharmaceutical industry physicians and their patients care more about cost-efficiency than

differentiation of the brand. Biotech companies build their brand value by ensuring a cost efficient product

that creates the best benefit for the patient. Alexion increases brand value through establishing itself as a

takeover target, drug research, international penetration, and corporate social responsibility that can be seen

in its unit sales growth year after year. Because Alexion has no direct competitors, they must ensure

effective, cost efficient treatments in order to build their brand as beneficial to customers. Consumers are

purchasing a product that significantly increases their chance to combat the deadly illness they have and

Alexion is able to charge a premium. Alexion does not only charge a premium due to its health benefits, but

also because of the continued government subsidization products such as Soliris receive. Alexion’s strong

brand value has enabled them to become highly profitable throughout the last eight years and will continue to

grow moving forward.

Growth Strategies

Alexion currently has three growth strategies they focus on in order to create high shareholder value and

increase top line, as well as bottom line growth: Becoming a Takeover Target, Drug Research, and

International Penetration.

6 http://www.forbes.com/sites/brucejapsen/2013/05/25/obamacare-will-bring-drug-industry-35-billion-in-profits/

CFA Society of Orlando

Stetson University Student Research 7/13/2015

4

Becoming a Takeover Target: Alexion’s high growth and brand value has created takeover value for larger

companies examining acquisition opportunities. The biotech industry is very aggressive in takeovers, which

Alexion has been a part of. The recession caused a slight decrease in mergers and acquisitions within the

biotech industry but has seen a recovery over the last couple of years. Merger and acquisition exits have

remained steady throughout the last five years, even through the economic downturn in 2008. Merger and

acquisition exits were at its highest level since 2007 in 2012 and continue to increase year over year.

Companies like Johnson & Johnson have the potential to acquire Alexion to broaden their research and

development segment, while also profiting from Soliris. Currently, Alexion has no acquisition bids but with

the release of Asfotase Alfa beginning to become a closer reality, potential buyers will start to evaluate the

company. Alexion will most likely take the purchase price so long as a high enough premium is paid and

they are able to function as they did previously. With its financial stability and continued growth, Alexion

will be able to choose from the pool of buyers because they are not in need of capital. Companies such as

Amgen, Allergan, and AstraZeneca saw buying premiums of 89%, 60%, and 88% premarket speculation

respectively. Alexion will be able to see similar premiums and an acquisition would help to significantly

increase the stock price creating great potential returns for shareholders.

Drug Research: Alexion has four drugs that it currently has in the development/trial phase that will help to

improve brand value:

Soliris (eculizumab): Eculizumab is currently being marketed by Alexion to those suffering from PNH

and aHUS. However, research has shown that it has a statistically significant impact upon Acute

Antibody Mediated Rejection (AMR) in both living and deceased donor scenarios. Moreover, it was also

concluded that it help patients with AMR following renal Transplantation. These three treatments are

currently in Phase II of development meaning it is being testing on over 100 participants in order to test

the drug’s efficacy and safety. Soliris has been granted orphan drug designation for the prevention of

graft rejection, kidney transplant graft function, prevention of DGF, neuromyelitis optics, and myasthenia

gravis.

Asfotase Alfa: Asfotase Alfa is a target enzyme replacement therapy in Phase II clinical trials for patients

with Hypophosphatasia, a life-threatening metabolic disease characterized by impaired phosphate and

calcium regulation, leading to progressive damage to multiple vital organs. Interim results of the trial

were presented at the European Society of Pediatric Endocrinology meeting held in September 2013.

Results of 15 enrolled and treated patients representing a range of HPP characteristics were summarized,

showing that the primary efficacy endpoint was achieved with a high degree of clinical and statistical

significance. In 2013, Asfotase alfa received Breakthrough Therapy Designation from the FDA.7

cPMP (ALXN 1101): ALXN 1101 targets MoCD Type A, a rare metabolic disorder characterized by

severe and rapidly progressive neurologic damage and death in newborns which results from a genetic

deficiency in cyclic Pyranopterin Monophosphate (cPMP). There has been some early clinical experience

with cPMP replacement therapy, but no approved therapy available for MoCD Type A. In October 2013,

cPMP received Breakthrough Therapy Designation from the FDA for the treatment of patients with

MoCD Type A. cPMP has finished Phase I of development and is currently transitioning into Phase II.8

ALXN 1007: ALXN 1007 is designed to target rare and severe inflammatory disorders and is a product

of proprietary antibody discovery technologies. Results from Phase I were collected and after an FDA

review Alexion has moved into Phase II of development in which they will begin a study with patients

suffering from anti-phospholipid syndrome, a severe life-threatening and ultra-rare disorder. This study

began in the second quarter of 2014 and during the second half of the year they are expecting to start a

second proof-of-concept study in another severe life-threatening and ultra-rare disorder

International Penetration: Presently, Alexion generates over sixty percent of its revenues from

international sales. While more than thirty percent of revenues are generated domestically, Alexion has seen

great growth and acceptance in international markets. Alexion has continued to focus on entering

international markets since the approval of Soliris for sale in the United States and multiple countries in

Europe. The most recent development of international penetration can be seen in Alexion’s focus on Japan.

Japan’s government is reviewing Asfotase alfa in order to decide its potential benefits to determine whether

they wish to grant Alexion subsidization. As more treatments finish Phase II and III Alexion will submit

approval documents to try to gain subsidization in countries where Soliris already receives these benefits.

7 Pg 23 2014 Q2 10Q Report 8 Pg 23-24 2014 Q2 10Q Report

Exhibit 4: Mergers & Acquisitions

Exhibit 6: International Revenues

Exhibit 5: Pipeline

18%

13%

33%

36%

CFA Society of Orlando

Stetson University Student Research 7/13/2015

5

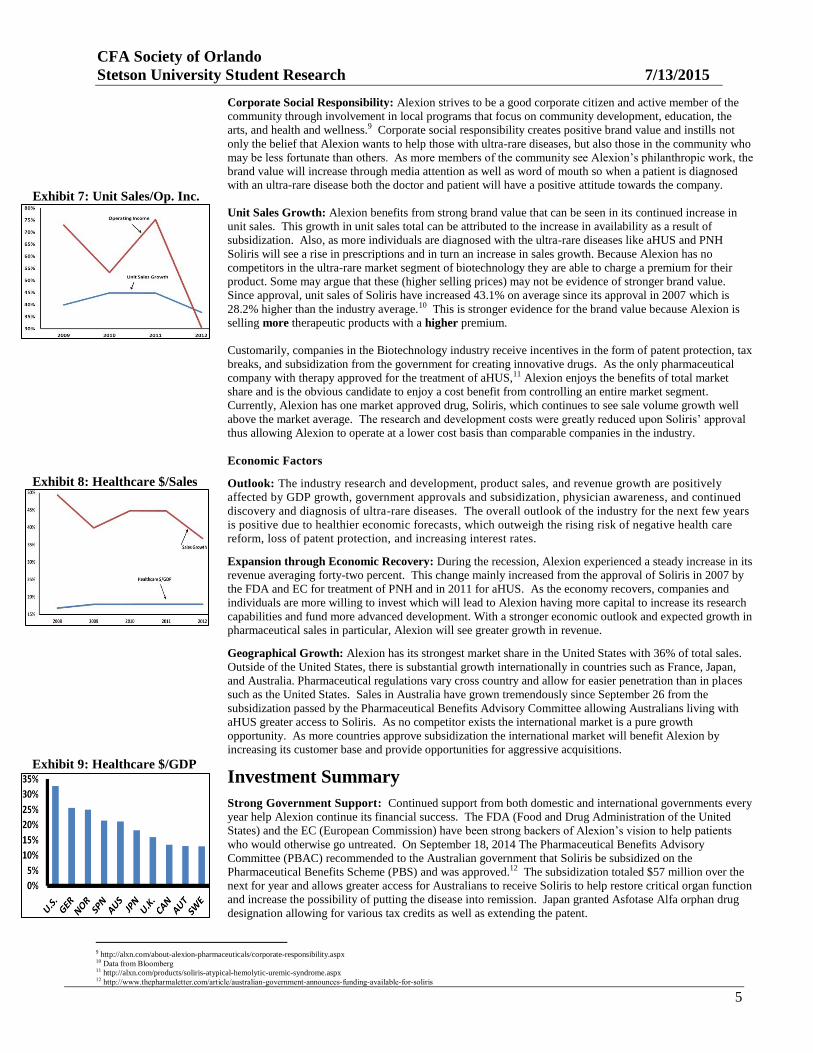

Corporate Social Responsibility: Alexion strives to be a good corporate citizen and active member of the

community through involvement in local programs that focus on community development, education, the

arts, and health and wellness.9 Corporate social responsibility creates positive brand value and instills not

only the belief that Alexion wants to help those with ultra-rare diseases, but also those in the community who

may be less fortunate than others. As more members of the community see Alexion’s philanthropic work, the

brand value will increase through media attention as well as word of mouth so when a patient is diagnosed

with an ultra-rare disease both the doctor and patient will have a positive attitude towards the company.

Unit Sales Growth: Alexion benefits from strong brand value that can be seen in its continued increase in

unit sales. This growth in unit sales total can be attributed to the increase in availability as a result of

subsidization. Also, as more individuals are diagnosed with the ultra-rare diseases like aHUS and PNH

Soliris will see a rise in prescriptions and in turn an increase in sales growth. Because Alexion has no

competitors in the ultra-rare market segment of biotechnology they are able to charge a premium for their

product. Some may argue that these (higher selling prices) may not be evidence of stronger brand value.

Since approval, unit sales of Soliris have increased 43.1% on average since its approval in 2007 which is

28.2% higher than the industry average.10 This is stronger evidence for the brand value because Alexion is

selling more therapeutic products with a higher premium.

Customarily, companies in the Biotechnology industry receive incentives in the form of patent protection, tax

breaks, and subsidization from the government for creating innovative drugs. As the only pharmaceutical

company with therapy approved for the treatment of aHUS,11 Alexion enjoys the benefits of total market

share and is the obvious candidate to enjoy a cost benefit from controlling an entire market segment.

Currently, Alexion has one market approved drug, Soliris, which continues to see sale volume growth well

above the market average. The research and development costs were greatly reduced upon Soliris’ approval

thus allowing Alexion to operate at a lower cost basis than comparable companies in the industry.

Economic Factors

Outlook: The industry research and development, product sales, and revenue growth are positively

affected by GDP growth, government approvals and subsidization, physician awareness, and continued

discovery and diagnosis of ultra-rare diseases. The overall outlook of the industry for the next few years

is positive due to healthier economic forecasts, which outweigh the rising risk of negative health care

reform, loss of patent protection, and increasing interest rates.

Expansion through Economic Recovery: During the recession, Alexion experienced a steady increase in its

revenue averaging forty-two percent. This change mainly increased from the approval of Soliris in 2007 by

the FDA and EC for treatment of PNH and in 2011 for aHUS. As the economy recovers, companies and

individuals are more willing to invest which will lead to Alexion having more capital to increase its research

capabilities and fund more advanced development. With a stronger economic outlook and expected growth in

pharmaceutical sales in particular, Alexion will see greater growth in revenue.

Geographical Growth: Alexion has its strongest market share in the United States with 36% of total sales.

Outside of the United States, there is substantial growth internationally in countries such as France, Japan,

and Australia. Pharmaceutical regulations vary cross country and allow for easier penetration than in places

such as the United States. Sales in Australia have grown tremendously since September 26 from the

subsidization passed by the Pharmaceutical Benefits Advisory Committee allowing Australians living with

aHUS greater access to Soliris. As no competitor exists the international market is a pure growth

opportunity. As more countries approve subsidization the international market will benefit Alexion by

increasing its customer base and provide opportunities for aggressive acquisitions.

Investment Summary

Strong Government Support: Continued support from both domestic and international governments every

year help Alexion continue its financial success. The FDA (Food and Drug Administration of the United

States) and the EC (European Commission) have been strong backers of Alexion’s vision to help patients

who would otherwise go untreated. On September 18, 2014 The Pharmaceutical Benefits Advisory

Committee (PBAC) recommended to the Australian government that Soliris be subsidized on the

Pharmaceutical Benefits Scheme (PBS) and was approved.12 The subsidization totaled $57 million over the

next for year and allows greater access for Australians to receive Soliris to help restore critical organ function

and increase the possibility of putting the disease into remission. Japan granted Asfotase Alfa orphan drug

designation allowing for various tax credits as well as extending the patent.

9 http://alxn.com/about-alexion-pharmaceuticals/corporate-responsibility.aspx 10 Data from Bloomberg 11 http://alxn.com/products/soliris-atypical-hemolytic-uremic-syndrome.aspx 12 http://www.thepharmaletter.com/article/australian-government-announces-funding-available-for-soliris

Exhibit 9: Healthcare $/GDP

Exhibit 8: Healthcare $/Sales

Exhibit 7: Unit Sales/Op. Inc.

CFA Society of Orlando

Stetson University Student Research 7/13/2015

6

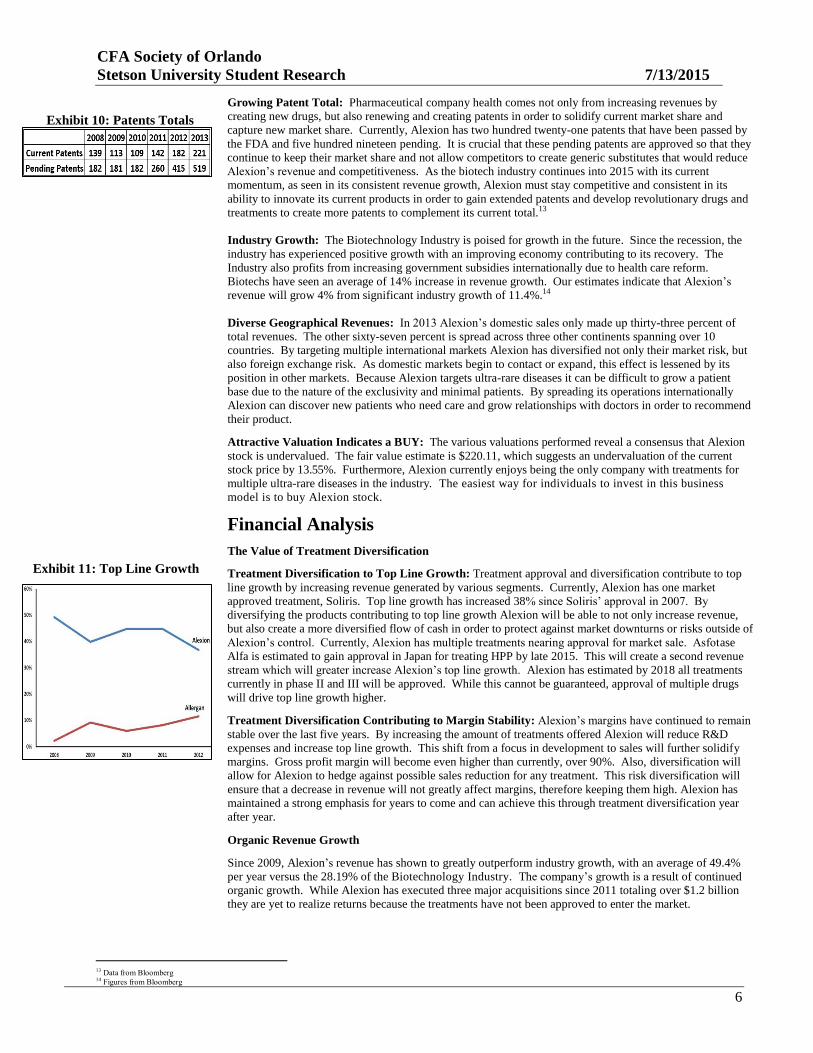

Growing Patent Total: Pharmaceutical company health comes not only from increasing revenues by

creating new drugs, but also renewing and creating patents in order to solidify current market share and

capture new market share. Currently, Alexion has two hundred twenty-one patents that have been passed by

the FDA and five hundred nineteen pending. It is crucial that these pending patents are approved so that they

continue to keep their market share and not allow competitors to create generic substitutes that would reduce

Alexion’s revenue and competitiveness. As the biotech industry continues into 2015 with its current

momentum, as seen in its consistent revenue growth, Alexion must stay competitive and consistent in its

ability to innovate its current products in order to gain extended patents and develop revolutionary drugs and

treatments to create more patents to complement its current total.13

Industry Growth: The Biotechnology Industry is poised for growth in the future. Since the recession, the

industry has experienced positive growth with an improving economy contributing to its recovery. The

Industry also profits from increasing government subsidies internationally due to health care reform.

Biotechs have seen an average of 14% increase in revenue growth. Our estimates indicate that Alexion’s

revenue will grow 4% from significant industry growth of 11.4%.14

Diverse Geographical Revenues: In 2013 Alexion’s domestic sales only made up thirty-three percent of

total revenues. The other sixty-seven percent is spread across three other continents spanning over 10

countries. By targeting multiple international markets Alexion has diversified not only their market risk, but

also foreign exchange risk. As domestic markets begin to contact or expand, this effect is lessened by its

position in other markets. Because Alexion targets ultra-rare diseases it can be difficult to grow a patient

base due to the nature of the exclusivity and minimal patients. By spreading its operations internationally

Alexion can discover new patients who need care and grow relationships with doctors in order to recommend

their product.

Attractive Valuation Indicates a BUY: The various valuations performed reveal a consensus that Alexion

stock is undervalued. The fair value estimate is $220.11, which suggests an undervaluation of the current

stock price by 13.55%. Furthermore, Alexion currently enjoys being the only company with treatments for

multiple ultra-rare diseases in the industry. The easiest way for individuals to invest in this business

model is to buy Alexion stock.

Financial Analysis

The Value of Treatment Diversification

Treatment Diversification to Top Line Growth: Treatment approval and diversification contribute to top

line growth by increasing revenue generated by various segments. Currently, Alexion has one market

approved treatment, Soliris. Top line growth has increased 38% since Soliris’ approval in 2007. By

diversifying the products contributing to top line growth Alexion will be able to not only increase revenue,

but also create a more diversified flow of cash in order to protect against market downturns or risks outside of

Alexion’s control. Currently, Alexion has multiple treatments nearing approval for market sale. Asfotase

Alfa is estimated to gain approval in Japan for treating HPP by late 2015. This will create a second revenue

stream which will greater increase Alexion’s top line growth. Alexion has estimated by 2018 all treatments

currently in phase II and III will be approved. While this cannot be guaranteed, approval of multiple drugs

will drive top line growth higher. Treatment Diversification Contributing to Margin Stability: Alexion’s margins have continued to remain

stable over the last five years. By increasing the amount of treatments offered Alexion will reduce R&D

expenses and increase top line growth. This shift from a focus in development to sales will further solidify

margins. Gross profit margin will become even higher than currently, over 90%. Also, diversification will

allow for Alexion to hedge against possible sales reduction for any treatment. This risk diversification will

ensure that a decrease in revenue will not greatly affect margins, therefore keeping them high. Alexion has

maintained a strong emphasis for years to come and can achieve this through treatment diversification year

after year.

Organic Revenue Growth

Since 2009, Alexion’s revenue has shown to greatly outperform industry growth, with an average of 49.4%

per year versus the 28.19% of the Biotechnology Industry. The company’s growth is a result of continued

organic growth. While Alexion has executed three major acquisitions since 2011 totaling over $1.2 billion

they are yet to realize returns because the treatments have not been approved to enter the market.

13 Data from Bloomberg 14 Figures from Bloomberg

Exhibit 10: Patents Totals

Exhibit 11: Top Line Growth

[

T

y

p

e

a

q

u

o

t

e

f

r

o

m

CFA Society of Orlando

Stetson University Student Research 7/13/2015

7

Looking forward, company revenue organic growth estimates are broken into three categories: (1)

Economic/industry growth, (2) approval of treatments in final stages of development,

and (3) continued government support.

Economic/Industry Effects: Current economic conditions, such as healthcare reform and recession

recovery, have enabled the biotech industry to thrive. Since 2009 the biotech industry has seen

28.19% growth. Alexion has greatly benefited from these effects and will continue to through 2015.

These benefits will continue to drive organic growth as more patients are diagnosed with the ultra-rare

diseases and are able to elect treatment. As the economy continues there will be an increase in capital

investment leading to higher organic growth through Alexion allocating these funds towards

increasing drug development and in turn improving organic growth. Alexion must take international

economic factors into account as they continue their focus on international penetration. International

economic uncertainty may take away organic growth as Alexion may choose to delay entrance into

countries in order to focus on stable markets they are currently operating in.

Approval of Treatments in Final Stages of Development: Alexion has multiple treatments in the

final stages of development and will see a significant increase in profits upon approval. By continui ng

to push treatments through the necessary phases Alexion can grow closer to gaining market approval

for these treatments. Upon market approval Alexion’s organic growth will improve greatly as the R&D

allocated to these treatments will greatly decrease and will begin to generate revenues. Currently,

Asfotase Alfa is the closest of these treatments and is scheduled to gain market approval in the latter

half of 2015.

Continued Government Support: The third contribution to the company’s revenue growth is derived

from continued government support. As Alexion continues to focus on entering international markets it is

crucial that they are able to gain government support. In order to remain profitable the cost of treatments

must be subsidized by the government in order to make it attainable for patients. If not, it would be

detrimental to organic growth since sales would greatly decrease due to the cost of treatment being high.

Also, Alexion cannot begin selling other treatments until the necessary government approvals have been

attained. Alexion’s relationship with the respective governments of each country they operate in is critical so

that they continue to diversify their cash flow and increase top line and organic growth.

Acquisition Growth

Alexion has made three major acquisitions in the last three years that have led to the continued increase

in organic growth. In quarter one of 2011 Alexion paid $115 million to acquire Taligen. This

acquisition allowed helped to broaden Alexion’s portfolio of preclinical compounds and expand their

capabilities in translational medicine.15 During the same time Alexion acquired Orphatec for $8.2

million in order to profit from their research and development on treatments for molybdenum cofactor

deficiency (MoCD). A year later the company paid $1.1 billion in to acquire Enobia in February 2012

in order to control their premier drug, Asfotase Alfa.16 This was a long-term focused deal that enables

Alexion to profit from Asfotase Alfa when it becomes approved within the next year. Acquisition

growth has complemented organic growth because both rely on researching and developing new

treatments for ultra-rare diseases. Alexion has not realized any return from these acquisitions because

none of the treatments gained through these acquisitions have been approved for sale. However, since

the acquisitions significant progress has been made towards registration. As these treatments begin to

enter the market Alexion will see significant increases in revenue as it did when Soliris finished its

development process and was approved for sale.

Margin Expansions

Gross Margin Improvement: Alexion has continued to keep gross margin extremely high with Q3 2014

reflecting 90.7%. Over the last twelve quarters gross margin, on average, has totaled 89.7%. This margin

stability ensures that a large decrease in revenue or increase in cost will not greatly affect gross profit and in

turn net income. Based on the pro forma estimates, Alexion will continue this trend into the next four

quarters with gross margin amounting to 93.1%, on average. This consistent margin performance indicates

strong financial health and will allow Alexion to continue its growth strategies without fear of risking losses.

Profit Margin Benefitting from R&D Expense Stability: The largest expense for any biotech company is

research and development because all the company’s efforts are devoted to creating innovative drugs. Over the

last 12 quarters Alexion has maintained R&D expense growth of 17.3%. It is crucial that Alexion continues to

increase R&D at a steady rate so that they can continue to create innovative treatments which will continue to

grow its revenues. While R&D is over 30% of total operating expenses, the historic stability of this growth

continues to reflect Alexion’s ability to control costs while increasing revenues. Operating expenses for the next

15 Pg 6 2011 Q1 10Q Report 16 Pg 7 2012 Q1 10Q Report

Exhibit 12: Acquisitions

Exhibit 13: Profit Margin

CFA Society of Orlando

Stetson University Student Research 7/13/2015

8

four quarters show a decrease which is consistent with historical trends.17 Currently, a majority of Alexion’s

R&D expense is focused on finishing Phase II and III trials rather than developing the treatments. Unless

Alexion develops a new drug investors can expect profit margin to benefit from low expense growth. Earnings

Alexion has developed a reputation for regularly beating earnings. Through its acquisitions and organic

growth, Alexion has been able to maintain stable earnings growth year over year coming out of the

Recession. Since 2009, EPS has been growing year over year an average of 26% compared to the industry’s

21%. Looking forward, earnings growth is anticipated continue this trend due to strong expected growth in

the industry and the company’s top line, as well as a reduction in general operating expenses.

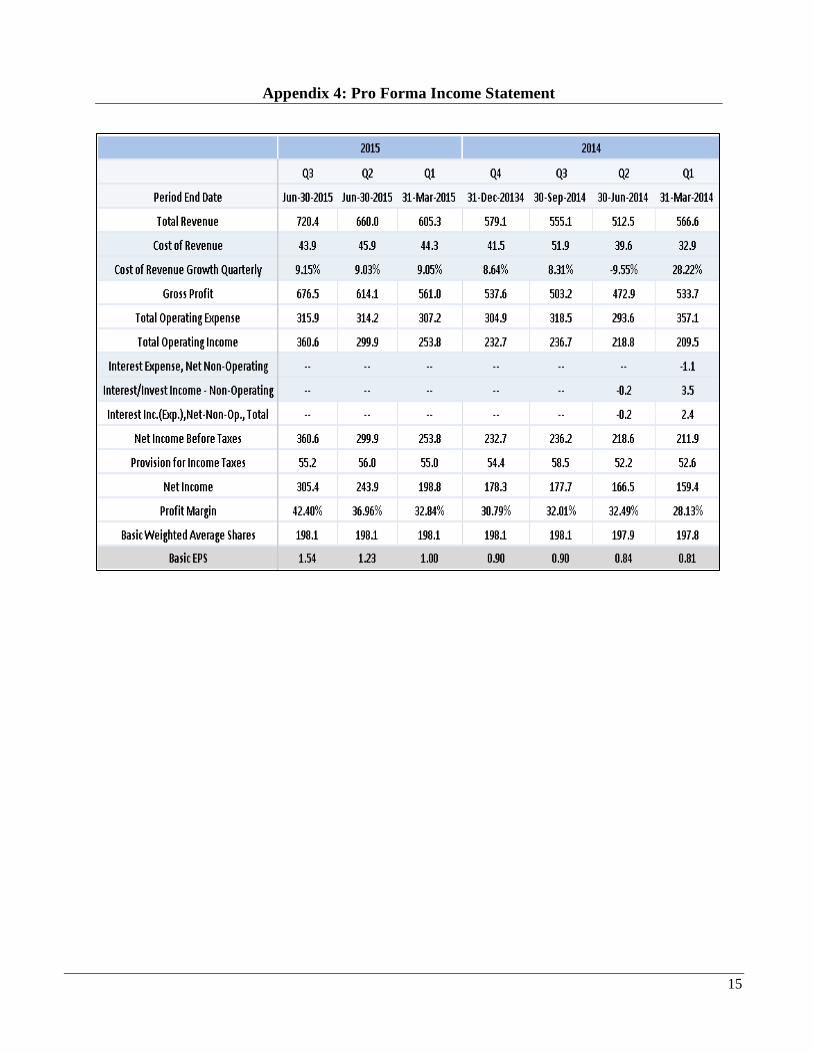

Pro Forma: Based on the assumptions that (1) the company revenue will grow approximately 9% quarterly

for the next year, (2) the gross margin will be between 92-94%, (3) R&D expenses will continue to increase

approximately 17%, the next four quarters EPS are estimated to be $5.17, beating earnings estimates of $5.03

(Appendix 4). For the next four quarters, EPS will see an increase of 111% from the previous four

quarters.18 Keeping with this upward trend, earnings are expected to grow by an average of 19.81% per

quarter in 2015.

Return on Equity

Alexion has a ROE of 34.6% versus Allergan’s 25% and has recently begun outperforming Allergan.

Alexion’s higher ROE is a result of a higher profit margin, higher inventory turnover, and higher leverage.

This pattern of Alexion having better fundamentals seems to hold up over time. Specifically, the constant

growth in profitability during the recession, Alexion has demonstrated an overall superior effectiveness in

operations and continued financial stability. Alexion has a lower (inventory) equity multiplier than Allergan

as of 2013 (1.39 vs. 1.64). This lower equity multiplier indicates Alexion’s state of low asset use to finance

debt compared to its comparable, Allergan.

Efficiency

Sales per R&D: Alexion’s revenue growth is outpacing its research and development expenses, as

demonstrated by its rising sales per R&D dollar. While the Allergan generates $6.04 of revenue for every $1

spent in R&D, Alexion produces $4.89. Historically, Alexion has seen this ratio decrease by 7.3% over the

last two years while Allergan’s sales per R&D has increased .58% over the same time. This difference comes

from Alexion’s increase in developing Asfotase alfa since acquiring Enobia in 2012. This indicates that the

company’s R&D initiative is effective in promoting greater revenue growth. This is a result of Alexion’s

ability to develop new treatments and gain approval quickly in order to begin the Phase II and III testing

process. Currently, Alexion has amount of treatments in testing which reduces expensive enabling Alexion

to further increase financial efficiency. By lowering its R&D costs relative to comparable companies in the

industry, Alexion is able to use its higher efficiency to grow its bottom line.

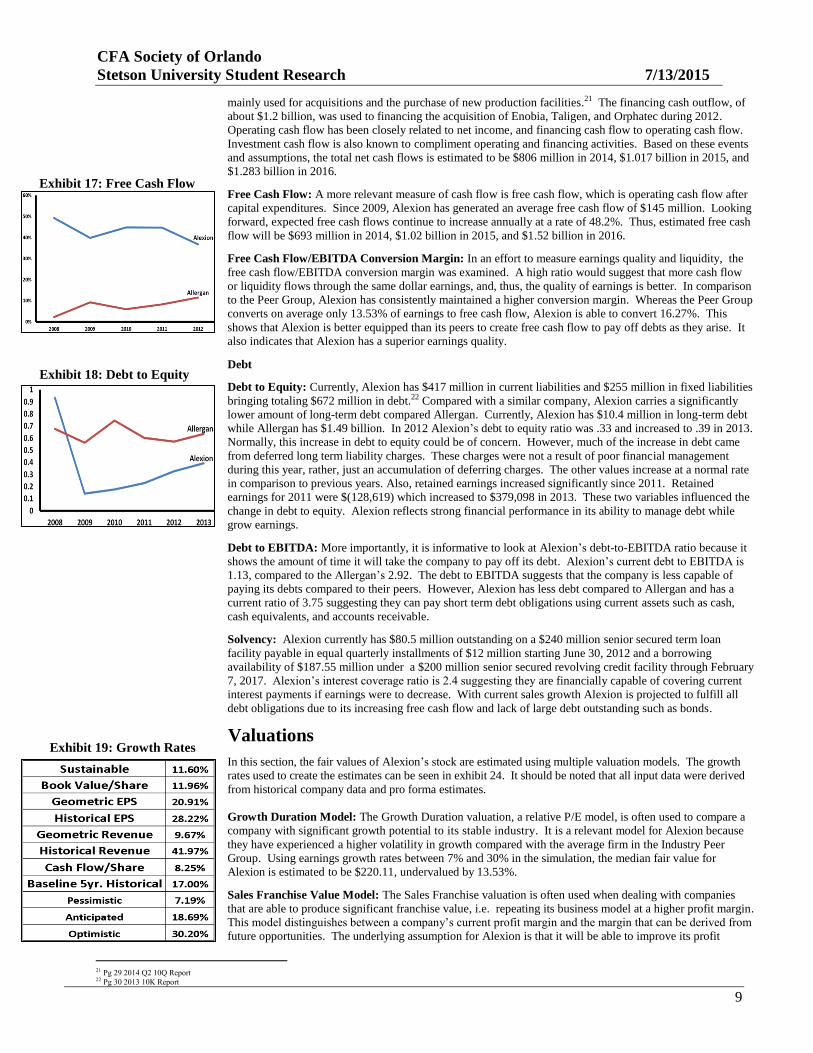

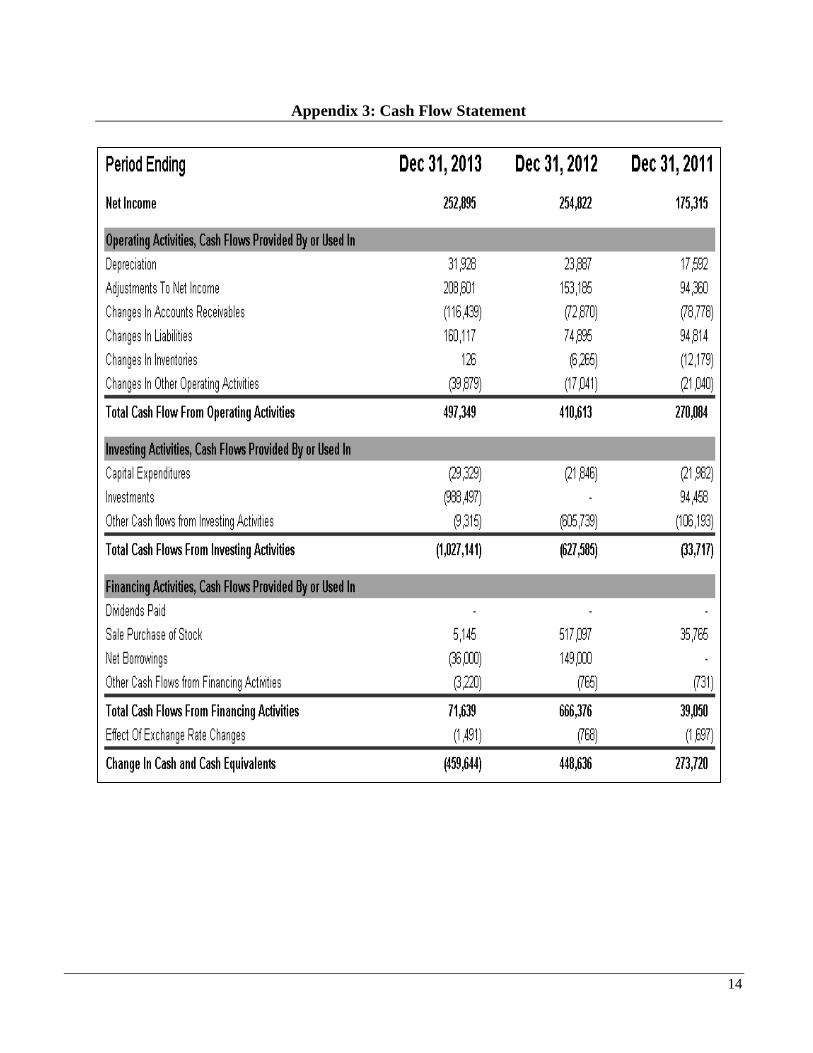

Cash Flow

Total Net Cash Flow: Due to the high research costs of the industry, biotechnology companies place an

emphasis on cash flow. On average, over 60%, or about $290 million, of Alexion’s cash flow comes from

operations.19 The investment cash outflow, which has been around $370 million20 per year on average, was

17 Pro Forma Income Statement 18 This large increase is influenced by a large tax payment incurred in Q4 2013 as a result of deferring taxes 19 Data from Reuters 20 Data from Reuters

Exhibit 14: Earnings per Share

Exhibit 15: Return on Equity

Exhibit 16: Sales per R&D

CFA Society of Orlando

Stetson University Student Research 7/13/2015

9

mainly used for acquisitions and the purchase of new production facilities.21 The financing cash outflow, of

about $1.2 billion, was used to financing the acquisition of Enobia, Taligen, and Orphatec during 2012.

Operating cash flow has been closely related to net income, and financing cash flow to operating cash flow.

Investment cash flow is also known to compliment operating and financing activities. Based on these events

and assumptions, the total net cash flows is estimated to be $806 million in 2014, $1.017 billion in 2015, and

$1.283 billion in 2016.

Free Cash Flow: A more relevant measure of cash flow is free cash flow, which is operating cash flow after

capital expenditures. Since 2009, Alexion has generated an average free cash flow of $145 million. Looking

forward, expected free cash flows continue to increase annually at a rate of 48.2%. Thus, estimated free cash

flow will be $693 million in 2014, $1.02 billion in 2015, and $1.52 billion in 2016.

Free Cash Flow/EBITDA Conversion Margin: In an effort to measure earnings quality and liquidity, the

free cash flow/EBITDA conversion margin was examined. A high ratio would suggest that more cash flow

or liquidity flows through the same dollar earnings, and, thus, the quality of earnings is better. In comparison

to the Peer Group, Alexion has consistently maintained a higher conversion margin. Whereas the Peer Group

converts on average only 13.53% of earnings to free cash flow, Alexion is able to convert 16.27%. This

shows that Alexion is better equipped than its peers to create free cash flow to pay off debts as they arise. It

also indicates that Alexion has a superior earnings quality.

Debt

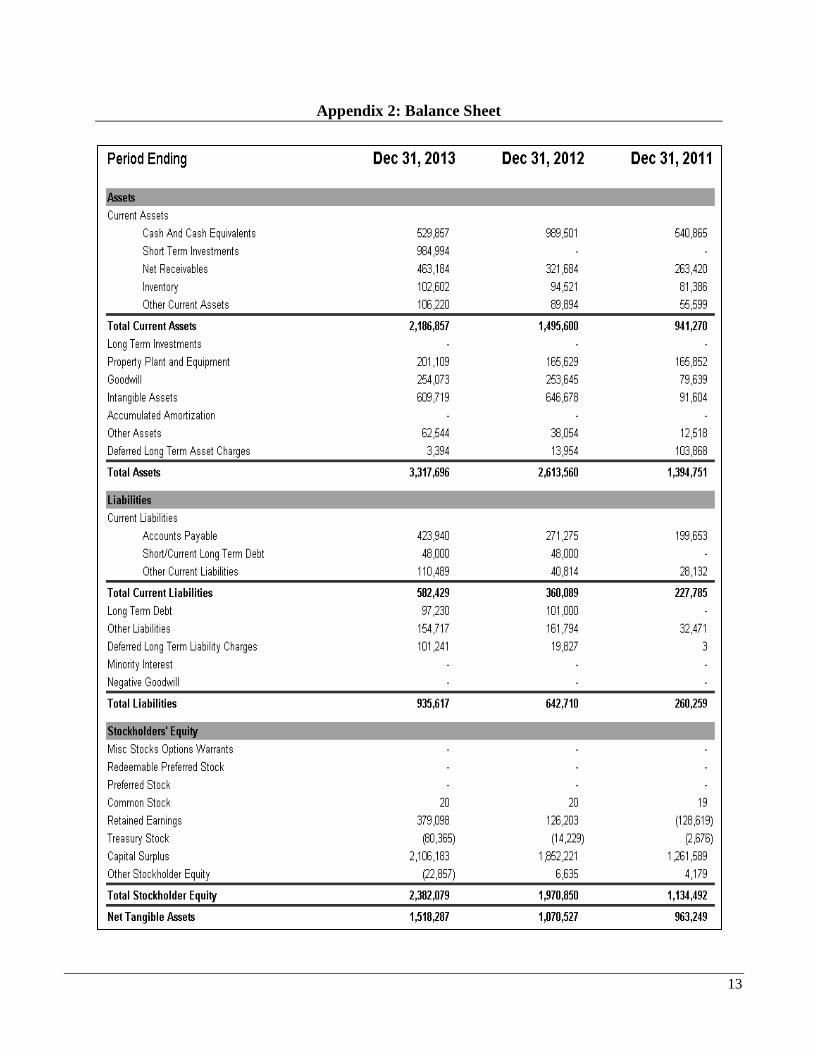

Debt to Equity: Currently, Alexion has $417 million in current liabilities and $255 million in fixed liabilities

bringing totaling $672 million in debt.22 Compared with a similar company, Alexion carries a significantly

lower amount of long-term debt compared Allergan. Currently, Alexion has $10.4 million in long-term debt

while Allergan has $1.49 billion. In 2012 Alexion’s debt to equity ratio was .33 and increased to .39 in 2013.

Normally, this increase in debt to equity could be of concern. However, much of the increase in debt came

from deferred long term liability charges. These charges were not a result of poor financial management

during this year, rather, just an accumulation of deferring charges. The other values increase at a normal rate

in comparison to previous years. Also, retained earnings increased significantly since 2011. Retained

earnings for 2011 were $(128,619) which increased to $379,098 in 2013. These two variables influenced the

change in debt to equity. Alexion reflects strong financial performance in its ability to manage debt while

grow earnings.

Debt to EBITDA: More importantly, it is informative to look at Alexion’s debt-to-EBITDA ratio because it

shows the amount of time it will take the company to pay off its debt. Alexion’s current debt to EBITDA is

1.13, compared to the Allergan’s 2.92. The debt to EBITDA suggests that the company is less capable of

paying its debts compared to their peers. However, Alexion has less debt compared to Allergan and has a

current ratio of 3.75 suggesting they can pay short term debt obligations using current assets such as cash,

cash equivalents, and accounts receivable.

Solvency: Alexion currently has $80.5 million outstanding on a $240 million senior secured term loan

facility payable in equal quarterly installments of $12 million starting June 30, 2012 and a borrowing

availability of $187.55 million under a $200 million senior secured revolving credit facility through February

7, 2017. Alexion’s interest coverage ratio is 2.4 suggesting they are financially capable of covering current

interest payments if earnings were to decrease. With current sales growth Alexion is projected to fulfill all

debt obligations due to its increasing free cash flow and lack of large debt outstanding such as bonds.

Valuations

In this section, the fair values of Alexion’s stock are estimated using multiple valuation models. The growth

rates used to create the estimates can be seen in exhibit 24. It should be noted that all input data were derived

from historical company data and pro forma estimates.

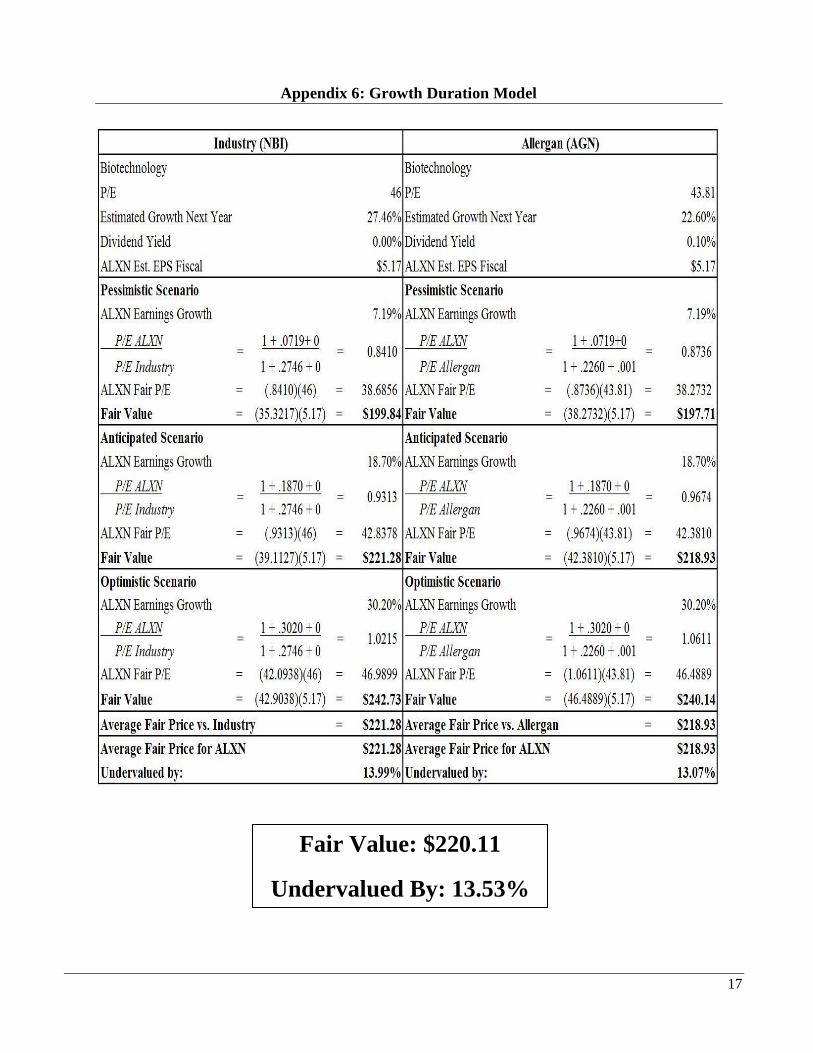

Growth Duration Model: The Growth Duration valuation, a relative P/E model, is often used to compare a

company with significant growth potential to its stable industry. It is a relevant model for Alexion because

they have experienced a higher volatility in growth compared with the average firm in the Industry Peer

Group. Using earnings growth rates between 7% and 30% in the simulation, the median fair value for

Alexion is estimated to be $220.11, undervalued by 13.53%.

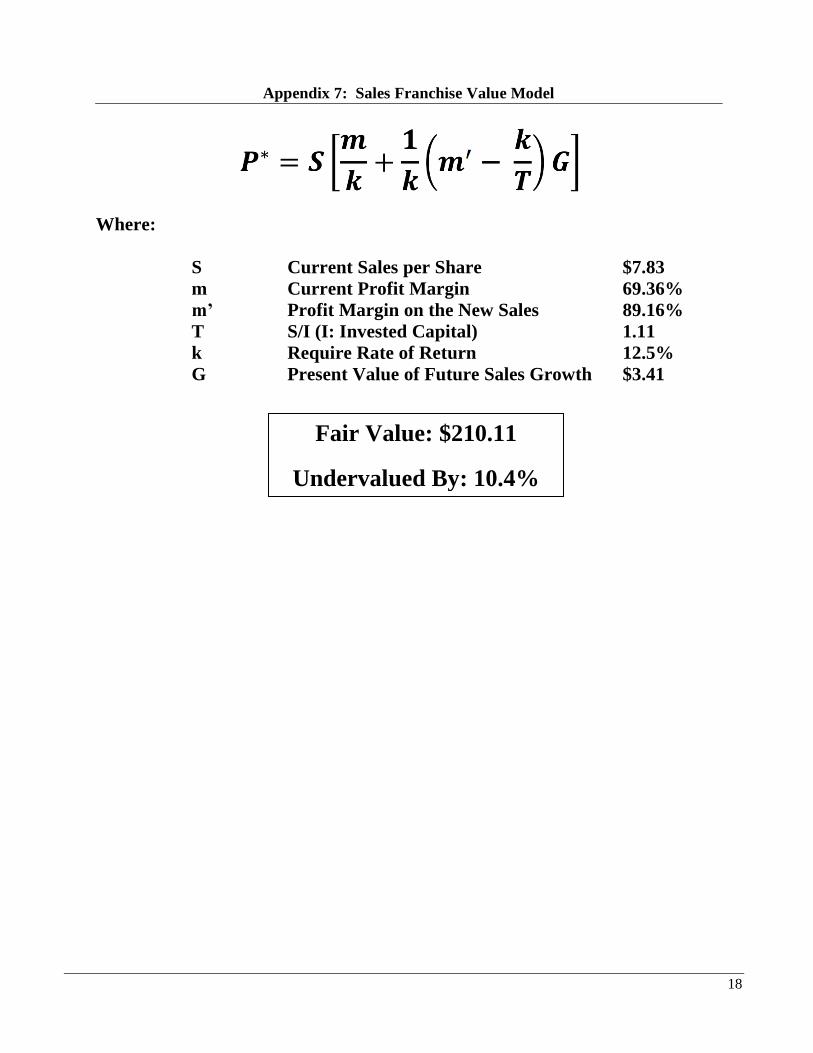

Sales Franchise Value Model: The Sales Franchise valuation is often used when dealing with companies

that are able to produce significant franchise value, i.e. repeating its business model at a higher profit margin.

This model distinguishes between a company’s current profit margin and the margin that can be derived from

future opportunities. The underlying assumption for Alexion is that it will be able to improve its profit

21 Pg 29 2014 Q2 10Q Report 22 Pg 30 2013 10K Report

Exhibit 18: Debt to Equity

Exhibit 17: Free Cash Flow

Exhibit 19: Growth Rates

CFA Society of Orlando

Stetson University Student Research 7/13/2015

10

margin by releasing a new product within the next year while also entering foreign markets. Using its current

profit margin of 69.36% and the expected future profit margin of 89.16%, the median fair value for Alexion

is forecasted to be $210.11, undervalued by 10.4% (Appendix 6).

Average Fair Value: By averaging the valuation models used, the estimated fair value of Alexion is

$215.11, meaning it is undervalued by 11.95%.

Investment Risk

Foreign Currency: As a result of Alexion’s international business model they are exposed to foreign

exchange risk, primarily from the Euro, Japanese Yen, and British Pound against the US Dollar. Alexion

enters into foreign exchange forward contracts, with durations up to 36 months, to hedge exposures resulting

from portions of forecasted revenues that are denominated in currencies other than the U.S. dollar. As of

June 30, 2014 Alexion had open contracts with notional amounts totaling $1,410,389 that qualified for hedge

accounting. The fair value of foreign exchange forward contacts that are not designed as hedging instruments

was zero as of June 30, 2014.23

Uncertainty of Clinical Testing and Approval of Product Candidates: Completion of preclinical studies

or clinical trials does not guarantee that Alexion will be able continue into the next phase of development and

in turn can eliminate the possibility of the product making it to the market. Currently, Soliris is the only

product that has received regulatory approvals, but has not been approved for any indication other than for

the treatment of patients with PNH and aHUS. It is possible that the other products, such as cPMP and

ALXN 1007, may never make it through the entire development process. Due to this possibility, it is crucial

that Soliris continue to gain approval and Asfotase alfa can receive its first secondary approval

Operations: Alexion relies on governments to offer subsidies, patent extension, tax credits, and approvals in

order to continue their current growth and remain profitable. Currently, Alexion has no outstanding bonds

but holds debt in a credit agreement with multiple banks that provide for a $240,000 senior secured term loan

facility payable in equal quarterly installments of $12 million starting June 30, 2012 and a $200 million

senior secured revolving credit facility through February 7, 2017.As of June 30, 2014, the is $81.5 million

outstanding on the term loan, open letters of credit of $12.44 million, and borrowing availability under the

revolving facility of $187.55 million This exposure from debt makes it can difficult to obtain financing for

additional acquisitions and makes Alexion more vulnerable to industry downturns and competitive pressures.

Intellectual Property: Alexion’s business and competitive position will be harmed if they cannot obtain

new patents, maintain our existing patents and protect the confidentiality and proprietary nature of our trade

secrets and other intellectual property, our business and competitive position will be harmed. In the event

Alexion is unable to renew patents a competitor will be able to capitalize on producing and selling the

product cheaper than currently provided. The sensitive nature of the technology used in biotech research

creates exposure wherein competitors could obtain trade secrets through potential collaborations.24

23 Pg 34 2014 Q2 10Q Report 24 Pg 48-50 2014 Q2 10Q Report

Important disclosures appear at the back of this report

Table of Contents

Appendix 1: Income Statement 12

Appendix 2: Balance Sheet 13

Appendix 3: Statement of Cash Flow 14

Appendix 4: Pro Forma Income Statement 15

Appendix 5: Capital Asset Pricing Model 16

Appendix 6: Growth Duration Model 17

Appendix 7: Sales Franchise Value Model 18

12

Appendix 1: Income Statement

13

Appendix 2: Balance Sheet

14

Appendix 3: Cash Flow Statement

15

Appendix 4: Pro Forma Income Statement

16

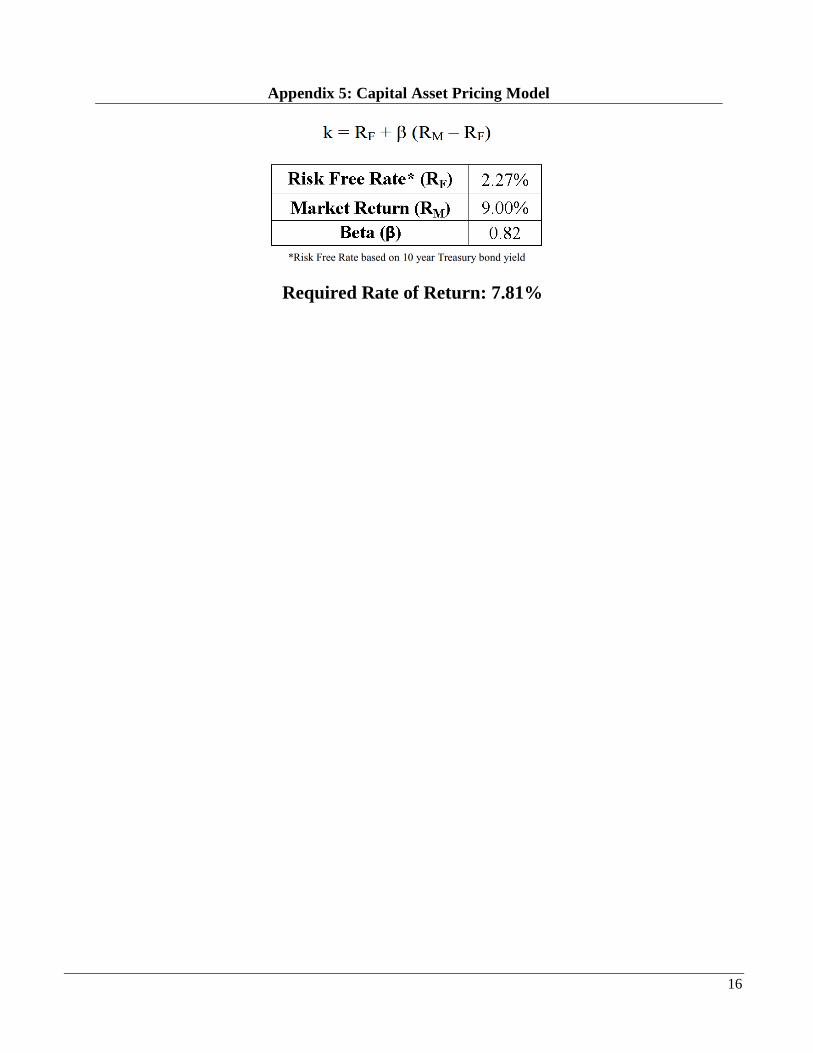

Appendix 5: Capital Asset Pricing Model

Required Rate of Return: 7.81%

17

Appendix 6: Growth Duration Model

Fair Value: $220.11

Undervalued By: 13.53%

18

Appendix 7: Sales Franchise Value Model

Where:

S Current Sales per Share $7.83

m Current Profit Margin 69.36%

m’ Profit Margin on the New Sales 89.16%

T S/I (I: Invested Capital) 1.11

k Require Rate of Return 12.5%

G Present Value of Future Sales Growth $3.41

Fair Value: $210.11

Undervalued By: 10.4%

19

Sources:

Reuters

Baseline

Bloomberg

Morningstar

Yahoo Finance

Google Finance

Alexion 10-Q

Alexion 10-K

Alexion Announcements

Alexion Transcripts

Alexion Conference Calls

J.P. Morgan 2014 Global Biotech Outlook

Forbes

ThePharmaLetter

Disclosures:

Ownership and material conflicts of interest: The author, or a member of their household, of this report does not hold a financial interest in the securities of this company.

The author, or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias

the content or publication of this report.

Receipt of compensation:

Compensation of the author of this report is not based on investment banking revenue.

Position as an officer or director: The author, or a member of their household, does not serve as an officer, director or advisory board member of the subject company.

Market making: The author does not act as a market maker in the subject company’s securities.

Disclaimer: The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author to

be reliable, but the author does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute

investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security.