Alternaty Hotels + Resort Newsletter Nha Trang December 2012

10

Nha Trang Hotel Market Overview Vietnam Hotels + Resorts Newsletter Table of Contents Nha Trang Hotel Market Overview Vietnam Economics Update Regional News Update Feature Article: Branded Residences HICAP 2012 Roundup South East Asia Property Awards 2012 Roundup Investment Opportunities About Us 1 6 7 8 9 9 10 10 December 2012 Nha Trang City is located within the South Central Region of Vietnam, a strip of prov- inces that runs along the coast of Vietnam and includes other resort locations such as Da Nang and Mui Ne. The capital city of Khanh Hoa Province, Nha Trang is 448 km north of HCMC and 1,280 km south of Ha- noi. The latest official population estimate of Nha Trang is 361,454 (2009) and its area is Location 251 km 2 with a 17 km coastline. Nha Trang Bay has 19 islands including the largest island, Hon Tre, with 3,250 ha and home to Vinpearl Resort (Nha Trang’s largest resort with 485 rooms) and Vinpearl Luxury which opened in Q2 of 2011. The island is connect- ed with the mainland by a cable car system that can conveniently ferry tourists between the island and the mainland. Nha Trang City was chosen as this edition’s feature location because the City’s hotel market is poised to enter into a new era as both the supply of and demand for accom- modation is about to make a significant leap forward. In terms of demand, November marked the start of the high season for Rus- sian tourists and with a major tour operator having tentatively entered the market last year, it is about to ramp up tourist arrivals this coming season via charter flights in a big way. On the other hand a wave of new supply is about to hit the market, so it will be interesting to see which side, demand or supply will tip the scales over the coming year. — Alternaty Updates W e attended HICAP in Hong Kong on 10th - 12th October, 2012 and were selected to partic- ipate as a panellist for the HICAP Update 2013 in Singapore in March, 2013. See roundup on page 9. We were a speaker at the 2nd An- nual Hospitality Management Con- ference 2012 held at the Legend Saigon on 15th November 2012. See our website to download our presentation on fractional sale. We assisted in the property inspec- tions and judging process for the South East Asia Property Awards 2012 and presented the awards for Vietnam at the gala dinner in Singapore on 21st November, 2012. See page 9 for the winners. Access Most arrivals to Nha Trang are by a short flight from HCMC or Hanoi. Cam Ranh International Airport was upgraded with a new terminal in 2007 and remains one of the newest and best airports in Vietnam with ample capacity to meet current and expected future demand. The airport is 28 km south of Nha Trang City which translates into a 40 minute taxi ride from the airport at a cost of approximately US$20 for the one way journey. Unfortunately, as is all too com- mon at most airports in Vietnam, there is an army of unscrupulous taxi operators eagerly awaiting to scam vulnerable tourists.

description

The Alternaty Vietnam Hotels + Resorts Newsletter is designed to keep you informed about the hospitality market in Vietnam and Indochina. Our aim is to keep you updated on the latest news and market events and present fresh investment opportunities. In this issue we have analyzed the Nha Trang Hotel Market and provided a review of Branded Residences. You will also find a summary of HICAP as well as the announcement of the Vietnam winners of the South East Asia Property Awards recently held in Singapore.For further information about Alternaty please visit our website www.alternaty.com and follow us on Twitter, LinkedIn or Facebook to receive the latest updates and opportunities as they become available.

Transcript of Alternaty Hotels + Resort Newsletter Nha Trang December 2012

Nha Trang Hotel Market Overview

Vietnam Hotels + Resorts Newsletter

Table of ContentsNha Trang Hotel Market OverviewVietnam Economics Update Regional News UpdateFeature Article: Branded ResidencesHICAP 2012 RoundupSouth East Asia Property Awards 2012 RoundupInvestment OpportunitiesAbout Us

1678991010

December 2012

Nha Trang City is located within the South Central Region of Vietnam, a strip of prov-inces that runs along the coast of Vietnam and includes other resort locations such as Da Nang and Mui Ne. The capital city of Khanh Hoa Province, Nha Trang is 448 km north of HCMC and 1,280 km south of Ha-noi. The latest official population estimate of Nha Trang is 361,454 (2009) and its area is

Location

251 km2 with a 17 km coastline. Nha Trang Bay has 19 islands including the largest island, Hon Tre, with 3,250 ha and home to Vinpearl Resort (Nha Trang’s largest resort with 485 rooms) and Vinpearl Luxury which opened in Q2 of 2011. The island is connect-ed with the mainland by a cable car system that can conveniently ferry tourists between the island and the mainland.

Nha Trang City was chosen as this edition’s feature location because the City’s hotel market is poised to enter into a new era as both the supply of and demand for accom-modation is about to make a significant leap forward. In terms of demand, November marked the start of the high season for Rus-sian tourists and with a major tour operator having tentatively entered the market last year, it is about to ramp up tourist arrivals this coming season via charter flights in a big way. On the other hand a wave of new supply is about to hit the market, so it will be interesting to see which side, demand or supply will tip the scales over the coming year.

— Alternaty Updates

We attended HICAP in Hong Kong on 10th - 12th October,

2012 and were selected to partic-ipate as a panellist for the HICAP Update 2013 in Singapore in March, 2013. See roundup on page 9.

We were a speaker at the 2nd An-nual Hospitality Management Con-ference 2012 held at the Legend Saigon on 15th November 2012. See our website to download our presentation on fractional sale.

We assisted in the property inspec-tions and judging process for the South East Asia Property Awards 2012 and presented the awards for Vietnam at the gala dinner in Singapore on 21st November, 2012. See page 9 for the winners.

Access

Most arrivals to Nha Trang are by a short flight from HCMC or Hanoi. Cam Ranh International Airport was upgraded with a new terminal in 2007 and remains one of the newest and best airports in Vietnam with ample capacity to meet current and expected future demand. The airport is 28 km south of Nha Trang City which translates into a 40 minute taxi ride from the airport at a cost of approximately US$20 for the one way journey. Unfortunately, as is all too com-mon at most airports in Vietnam, there is an army of unscrupulous taxi operators eagerly awaiting to scam vulnerable tourists.

2 Nha Trang Hotel Market Overview

Alternaty® Vietnam Hotels + Resorts Newsletter alternaty.com

In total, there are approximately 78 sched-uled flights per week to Nha Trang which translates to a maximum capacity of 12,600 passengers per week or 655,200 per annum. This does not include charter flights, which over the last year has rapidly grown to become a significant source of international arrivals, especially from Russia with the arriv-al of the tour operator Pegas Touristik.

Nha Trang also welcomes tourist arriv-ing from cruise ships. In 2011, Nha Trang welcomed 35 cruise ships with more than 35,000 tourist arrivals, including the Queen Mary II – one of the world’s largest cruise ships.

Supply

Largest Hotels in Nha TrangFigure 1

Source: Alternaty

Of the 250 accommodation establishments in Nha Trang supplying approximately 5,000 rooms in total, 25 properties are rated 3 - 5 stars by the Vietnam National Administration of Tourism (VNAT) comprising of five prop-erties that are rated 5-star, four properties that are rated 4-star and the remaining properties are rated 3-stars. As is usually the case in Vietnam, a number of properties exist which are officially unrated, yet they would certainly be of an international 4 or 5 star standard. These tend to be the new properties which are yet to reach full scale operational status or due to their boutique nature do not conform to the rigid star rating criteria. What sets Nha Trang apart is the availability of a broad range of hotel management formats and brands with the

ability to satisfy a diverse mix of travellers, catering for a wide range of budgets and accommodation needs. These include local guesthouses, modern city hotels, beachfront resorts, island destinations as well as remote hideaway properties. For this reason, Nha Trang is chosen by the local Vietnamese and expat market (e.g. Mia Resort, Novotel, Sher-aton, Best Western Hon Tam Island, Sunrise Beach Hotel, Vinpearl Luxury), as well as Western backpackers (e.g. local guesthouses and family run hotels), Russians (e.g. Vinpearl Island Resort, Diamond Bay Resort), as well as Europeans, Koreans and Japanese seeking peaceful hideaways (e.g. An Lam Ninh Van Bay, Six Senses Ninh Van Bay, Ana Mandara).

Selected Future Supply in Nha Trang and Cam RanhTable 1

Project Name

The Costa Nha Trang

Nha Trang Centre

Hyatt Regency Cam Ranh

Best Western Premier

Marriott Nha Trang

Russian Cam Ranh Resort

Developer

TD Group

Hoan Cau/Thanh Yen

Kien A Corporation

Hai Van Nam JSC

Sao Sang Nha Trang

Russian Cam Ranh Dev. Corp.

Source: Alternaty

Scale (rooms)

308

140 Apartments

>1,000 (condotel)

250

Operator

IHG

Formerly in talks with an international upscale brand

Hyatt

Best Western

Marriott

Langham

— Alternaty Opinion

Although Nha Trang is served by a modern airport with plenty of

capacity and ability to handle inter-national flights and mid-sized jets, its distance from the city adds a significant cost to the journey, more so in terms of time and transfers than money. In this regard it is less competitive compared to its resort destination peers Da Nang and Phu Quoc where the airports are locat-ed closer to the main beach areas.

© 2012 Bing

Nha TrangKhanh Hoa Province

Crowne Plaza

Hyatt Regency

Best Western Premier

Marriott

Langham Place

Brand

0

100

200

300

400

500

600

Vinp

earl

Diam

ond

Bay

Sher

aton

Yasa

ka S

aigon

Mich

elia

Hot

elVi

en D

ong

Hote

lN

ovot

elLo

dge

Sunr

ise B

each

Orie

ntAs

ia Pa

radi

seLu

xury

Nha

Tra

ngHa

i Yen

Happ

y Lig

htTh

e Su

mm

erVi

npea

rl Lu

xury

Nha

Tra

ngBe

st W

este

rn H

on T

am S

ea &

Sun

Nha

t Tha

nhEv

ason

Ana

Man

dara

Six S

ense

s Nin

h Va

n Ba

yW

hite

San

d Do

clet

Mia

Reso

rtBe

st W

este

rn B

huva

na H

on T

am R

esor

tAn

Lam

Nin

h Va

n Ba

y Re

sort

200

3Nha Trang Hotel Market Overview

Alternaty® Vietnam Hotels + Resorts Newsletteralternaty.com

December 2012

Since the Novotel opened in the fourth quarter of 2008, the number and diversity of rooms supplied has increased dramatically with the opening of the Sheraton (Q4/2010, 284 hotel keys), Michelia (Q1/2011, 201 hotel keys), Vinpearl Luxury (Q2/2011, 84 resort keys), An Lam (Q2/2011, 35 resort keys) and most recently Mia (Q3/2011, 50 resort keys). This pace of increase in supply is set to con-tinue with several large scale properties due to come on line in the near future.

Demand

Tourist Arrivals to Khanh HoaProvince

Figure 2

Domestic Arrival

International Arrival

Source: Khanh Hoa Department of Culture, Sports and Tourism

Total tourist arrivals to Khanh Hoa Province in 2011 was a record 2.18 million, up by a sig-nificant 18.5% compared to the 1.84 million visitors received in 2010. Domestic arrivals accounted for 80% (1.74 million arrivals) of the total and increased by 20% compared to 2010 while international arrivals accounted for 20% (440,000 arrivals) and increased by only 13.7% compared to the previous year.

In the first 9 months of 2012, total arrivals were 1.75 million, 5.7% higher compared to the same period in 2011 however the 27.4% growth of international arrivals comfortably outpaced the 0.9% growth in domestic arriv-als. In terms of absolute numbers, in the first 9 months of 2012, domestic arrivals to Khanh Hoa Province increased by 11,500 to 1.36 million and international arrivals increased by 82,500 to 383,500 arrivals compared to the same period in 2011.

Nhat Minh International Travel Company in 2010 partnered with Russia’s Vladivostok In-ternational Airport, operating two flights per month from the Russian city of Khabarovsk to the Cam Ranh International Airport in late 2010. The truly game changing event was in late 2011 when the mammoth Pegas Touristik partnered with Anh Duong Company to offer 1 charter flight per day. The partnership has already sent well over 50,000 Russian tourists to Nha Trang from 9 cities in Eastern

Europe and has recently boosted capacity to 3 charter flights per day as they expect to double arrivals this coming season. No doubt the unrest in the Middle East played a key role in channelling a new wave of Russian tourists towards Asia.

The average length of stay in Nha Trang is only several days because the usual package tour to Vietnam tends to include a visit to Hanoi and Ho Chi Minh City packaged with a short beach stay in between either in Nha Trang or Da Nang.

The average length of stay in the city hotels tends to be 3 days and 2 nights for Viet-namese guests, who tend to come for the weekend, while international guests, such as Russians tend to come in groups and stay up to a week in these properties.

The resorts have a longer average length of stay, in the range of 4 to 6 nights, however this varies significantly depending on the nationality of the guest. Vietnamese guests who stay in the resorts tend to book for 2 – 4 nights including the weekend. Europeans tend to stay 1 – 2 weeks with some up to 4 weeks, especially from Germany. The aver-age length of stay of visitors from Australia and the US is 4 – 5 days. Meanwhile, resort guests from Russia stay 4 – 7 nights on aver-age as the tours from Russia tend to be 12

It is clear that the Russian market has become the engine of arrivals growth in Nha Trang and just a cursory look at the way the Russian market has trans-

formed the Thai tourism industry is all that is required to realise that Nha Trang is now at the very cusp of an imminent boom in arrivals. Total Russian tourist arrivals to Thailand in 2011 was just over 1 million, while in 2010, Nha Trang city received a mere 28,000 Russian arrivals. This doubled to 60,000 in 2011.

— Alternaty Opinion

days and include a resort stay plus short tours of other locations in Vietnam. Japanese visitors are a significant source of guests for Ana Mandara Nha Trang and Six Senses Ninh Van Bay as both of these resorts have a native Japanese guest relations officer and their average length of stay tends to be relatively short at just 2 - 3 nights.

0200400600800

100012001400160018002000

4 Nha Trang Hotel Market Overview

Alternaty® Vietnam Hotels + Resorts Newsletter alternaty.com

December 2012

Seasonality

Nha Trang’s major strength as a resort destination is its ideal climate with 10 months of the year being conducive for tourists while only 2 months of the year are charac-terised by heavy rain, storms and flooding. These two months, October and November, alone account for almost 80% of the annual rainfall.

Nha Trang has a tropical climate with two seasons and an average annual temperature of 27 degrees celcius. The dry season lasts from January to August with only 27mm of rainfall per month. The average annual temperature during the local summer and high season months of May to August is 29 degrees. Meanwhile the monsoon season, which coincides with the local winter, is from September to December, with the wettest months being October and November with 250mm of rainfall per month on average.

The diversity of tourist arrivals to Nha Trang means that despite the weather in Nha

Hotel Performance

The abundance of small sized family run mini hotels at the budget end of the spec-trum means that Nha Trang has a fiercely competitive hotel market, making it a diffi-cult task for hoteliers to bring profits. These hotels and guesthouses with zero to 3 stars offer value for money by providing a decent product at a very low price point and they make it extremely difficult for the upscale segment to justify their room rate premium. With room rates in the range of $20 - $40 per night, these hotels have been in business for a long time, so they know their customer needs and they know how to meet these needs at minimum cost.

The Novotel, having entered the market back in 2008 and being the only interna-tional 4 star product at this time, has so far succeeded in justifying its price premium over the local products and is favoured by

both local and international guests. However it is no easy task to cover the cost of services and amenities provided and to push rates much above/ towards $100 per night. At the top end of the range for city hotels which is currently dominated by Sheraton, the task of justifying room rates to cover the costs of providing full services and multiple F&B outlets is even more difficult. It will certainly be interesting to see how room rates and performances are affected with the opening of Crowne Plaza and Best Western Premier.

In terms of average room rates the interna-tionally managed and high end boutique resorts are achieving ARR’s in the range of $250 - $300 while the ARR of the interna-tionally managed upscale city hotels are in the range of $90 - $110.

Trang, there are arrivals at all times of the year whatever the season whether that be Europeans, Americans, Russian, Asians or local Vietnamese. In Vietnam, the summer lasts from May to August, which coincides with the school holidays, hence it is the peak season for Vietnamese tourists. Europeans tend to come during their winter months from November to February, as do the Rus-sians and Americans.

Rainfall & Average TemperatureFigure 3

Having interviewed several of the top tier hotels and resorts in Nha Trang, one of the interesting insights that emerged was the stark

contrast in guest segmentation between properties within the same competitor set. Each property has a unique segmentation in terms of lo-cal vs foreign guest, couple vs family and mix of nationalities that varies throughout the year. This makes it a very challenging task for the opera-tors to satisfy a wide range of needs which are often conflicting yet need to be satisf ied concurrently.

— Alternaty Opinion

The recently opened boutique resorts have impressed the mar-

ket not only in terms of the quality of the products delivered but also in terms of the quality of services offered. This has been reflected in their operating performance, reach-ing profitability within 12 months of operation, as well as in terms of cus-tomer reviews, having raced to the top of hotel user review rankings at the online hotel booking sites. What they have proven is that the Nha Trang market has the capacity to easily absorb new supply, provid-ed that the product is thoughtfully conceived and precisely designed with the target market in mind.

— Alternaty Opinion

20

22

24

26

28

30

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

c Tem

pera

ture

(°C

)

Rain

fall (

mm

)

050

100150200250300

Rainfall

Average Temperature

Source: Khanh Hoa Department of Culture, Sports and Tourism

5Nha Trang Hotel Market Overview

Alternaty® Vietnam Hotels + Resorts Newsletteralternaty.com

December 2012

Nha Trang hoteliers enjoy a relatively long trading history compared to other resort destinations in Vietnam as Nha Trang was among the first to develop its tourism sector. This is a considerable advantage in terms of budgeting for and controlling hotel oper-ating costs. Also, staff availably and level of skill as well as experience is above average compared to other locations however the steady increase in rooms supply means there

is always fierce competition for trained and skilled labour which puts an upward pressure on labour costs. Labour costs also tend to have a strong correlation with the number of expatriates among the hotel staff.

That being said, the hideaway style resorts in remote locations, especially those that can only be accessed by boat, such as Six Sens-es, An Lam and Hon Tam have a much more

challenging task of controlling costs, as they have a significant added cost in terms of fuel for the power generators and shuttle boats. This has encouraged the use of alternative energy solutions such as using solar power for the water heating. Another extra cost for these resorts is the on-site staff accommo-dation in some cases.

Operating Costs

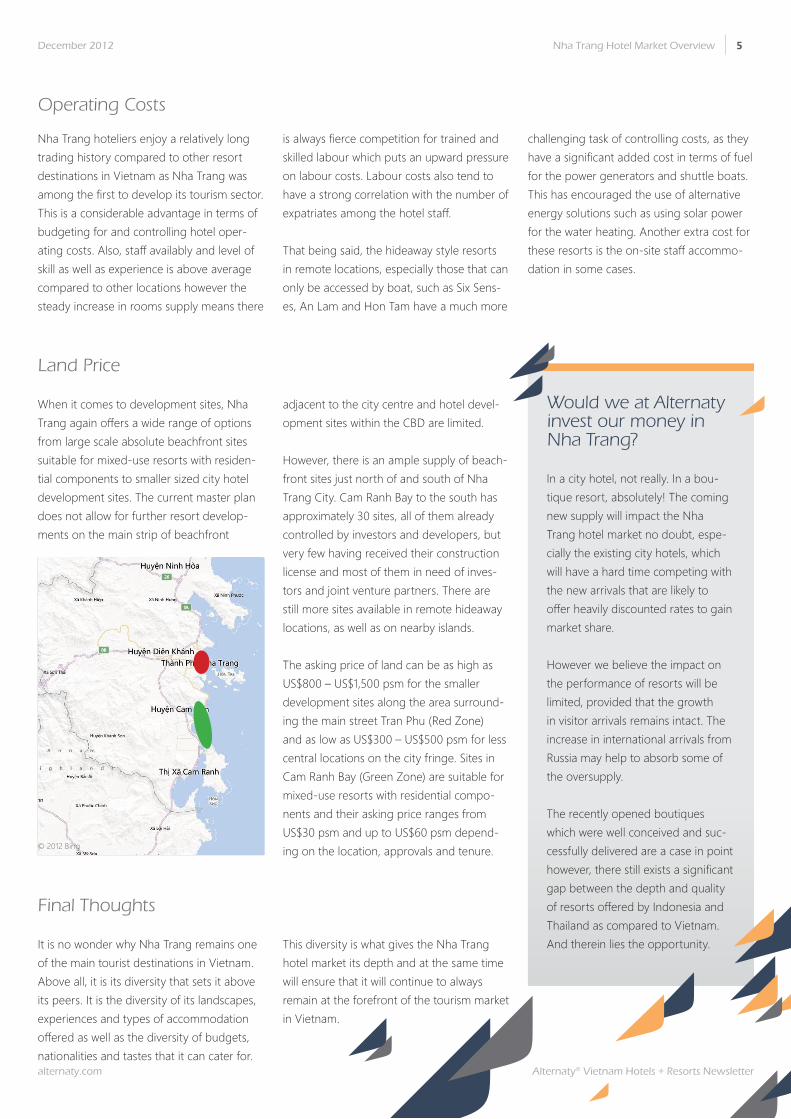

When it comes to development sites, Nha Trang again offers a wide range of options from large scale absolute beachfront sites suitable for mixed-use resorts with residen-tial components to smaller sized city hotel development sites. The current master plan does not allow for further resort develop-ments on the main strip of beachfront

Land Price

© 2012 Bing

Final Thoughts

It is no wonder why Nha Trang remains one of the main tourist destinations in Vietnam. Above all, it is its diversity that sets it above its peers. It is the diversity of its landscapes, experiences and types of accommodation offered as well as the diversity of budgets, nationalities and tastes that it can cater for.

This diversity is what gives the Nha Trang hotel market its depth and at the same time will ensure that it will continue to always remain at the forefront of the tourism market in Vietnam.

In a city hotel, not really. In a bou-tique resort, absolutely! The coming new supply will impact the Nha Trang hotel market no doubt, espe-cially the existing city hotels, which will have a hard time competing with the new arrivals that are likely to offer heavily discounted rates to gain market share.

However we believe the impact on the performance of resorts will be limited, provided that the growth in visitor arrivals remains intact. The increase in international arrivals from Russia may help to absorb some of the oversupply.

The recently opened boutiques which were well conceived and suc-cessfully delivered are a case in point however, there still exists a significant gap between the depth and quality of resorts offered by Indonesia and Thailand as compared to Vietnam. And therein lies the opportunity.

Would we at Alternaty invest our money in Nha Trang?

adjacent to the city centre and hotel devel-opment sites within the CBD are limited.

However, there is an ample supply of beach-front sites just north of and south of Nha Trang City. Cam Ranh Bay to the south has approximately 30 sites, all of them already controlled by investors and developers, but very few having received their construction license and most of them in need of inves-tors and joint venture partners. There are still more sites available in remote hideaway locations, as well as on nearby islands.

The asking price of land can be as high as US$800 – US$1,500 psm for the smaller development sites along the area surround-ing the main street Tran Phu (Red Zone) and as low as US$300 – US$500 psm for less central locations on the city fringe. Sites in Cam Ranh Bay (Green Zone) are suitable for mixed-use resorts with residential compo-nents and their asking price ranges from US$30 psm and up to US$60 psm depend-ing on the location, approvals and tenure.

6 Vietnam Economics Update

Alternaty® Vietnam Hotels + Resorts Newsletter alternaty.com

December 2012

Source: General Statistics Office of Vietnam

VietnamEconomics Update

In the first 11 months of 2012, implemented FDI was US$10 billion, only 0.5% short of the figure achieved during the same period in 2011. On the other hand, newly registered capital was US$7.26 billion, equivalent to only 60.38% of the amount registered in 2011. Real estate ranks second in terms of at-tracting FDI with 9 newly registered projects, with total registered and additional capital of US$1.85 billion or 15.1% of total FDI.

Foreign Direct Investment

Inflation

November CPI came in at 7.08% y-o-y while the m-o-m figure was up 0.47% which was much lower than the 2.2% m-o-m increase in September and 0.85% increase in October. The CPI increase in November was mainly attributed to the 5.16% increase in medicine and healthcare. The food and

foodstuff component, which accounts for 40% in the goods basket, decreased 0.08% compared to October. The government CPI target of 8% for 2012 seems within sight if December’s CPI continues to be under control.

Economic Growth

GDP in the first 9 months stood at 4.73% compared to the figure of 5.77% in the same period of 2011. GDP growth in Q3 was up 5.35% and the highest quarterly result so far this year however it still seems that the 5.2% government GDP target for 2012 will be out of reach.

Interest Rates

According to Ministry of Planning and In-vestment and despite the government’s best efforts to spur lending, in the first 9 months of 2012 credit growth was only 2.35%. On 28th September, 2012 S&P raised its ratings of Vietnam’s banking system to B+ from B in recognition of the government’s efforts to stabilize the economy.

On the other hand, Moody’s on the same day downgraded Vietnam’s foreign and

local currency denominated Government bond ratings to B2 from B1 citing higher risks to the government’s balance sheet due to the continuing weaknesses in the bank-ing system and the expectation of lower medium-term economic growth prospects. Interest rates currently stand at 9% for the base rate (unchanged since November 2010) and 8% for the discount rate (unchanged since July 2012).

Consumer Price IndexFigure 4

Consumer Price Index (Y-o-Y) Housing and Construction Materials

Foreign Direct InvestmentFigure 7

Gross Domestic ProductFigure 5

Real GDP annual growth rate (%)Nominal GDP

Committed Capital

Implemented Capital

Source: General Statistics Office of Vietnam

Source: Foreign Investment Agency

State Bank of Vietnam Interest Rates Figure 6

Source: State Bank of Vietnam

Base Discount Rate Refinancing Rate

0

20

40

Y-o-

Y Pr

ice In

dex (

%)

0

5

10

15

20

Inte

rest

Rate

s (%

)

020406080

100120140

Real

GDP

annu

al gr

owth

rate

(%)

Nor

min

al GD

P (U

S$

billio

n)

0

20

40

60

80

FDI (

US$

billio

n)

7Regional News Update

Alternaty® Vietnam Hotels + Resorts Newsletteralternaty.com

December 2012

Regional NewsUpdate

Vietnam News

CBRE Vietnam acquired by CBRE IncCB Richard Ellis (Vietnam) Co., Ltd has been acquired by CBRE Group Inc after 10 years operating as an affiliate. Mr Marc Townsend and Mr Richard Leech will continue to lead the entity in Vietnam.

Kinh Do shelves Lavenue CrownKinh Do Corporation has decided to put Lavenue Crown, a five star hotel, commercial centre and serviced apartment project in HCMC’s CBD on hold and also suspended other real estate projects to focus on its core business in the food sector.

Vietnam on target to achieve 6.5 million international tourist arrivalsAccording to VNAT, international tourist ar-rivals to Vietnam reached 6.036 million in the first 11 months of 2012, up 11.4% compared to the same period of 2011. In November, this number reached 656,000. With this growth rate, the target of 6.5 million interna-tional arrivals for 2012 will be achieved.

Euromonitor forecasts Vietnam to lead hotel sector growth in AsiaAccording to a report released by Euromon-itor International, the hotel sector in Asia is expected to grow by a compounded annual growth rate (CAGR) of 7% during 2012 – 2016 while Vietnam is expected to top the growth rate in the region with an expected CAGR of up to 15% during the same period, followed by the Philippines, China, Malaysia, Uzbekistan, India and South Korea.

Capri by Fraser to debut in HCMC by the end of this yearThe Capri by Fraser, a serviced residence project which is under construction in Dis-trict 7, HCMC, will be managed by Frasers Hospitality Pte Ltd and is scheduled to open late this year. The development consists of 175 units and will be the third Capri by Fraser in SE Asia (others in Singapore and Kuala Lumpur).

ZETA Group (South Korea) an-nounces MOU with Quang Binh GovernmentZETA Group Holding, a real estate invest-ment firm from the Republic of Korea has signed an MoU with the government of Quang Binh, a province in the North Central Region of Vietnam to invest in a US$4 billion development including hotels, urban facilities, casino and outdoor entertainment activities.

C.T. Group nearing completion of new golf course in Cu Chi District, HCMCThe first 18 holes as well as a 10,000 sm club house of the CT Sphinx Golf Club and Residences is expected to be put into operation in Q3, 2013. The project comprises of a 36-hole golf course, a club house and 200 luxury villas over 200 hectares and was acquired from Korean firm GS Engineering & Construction last year by CT Group for US$24 million.

Da Phuoc International Township scraps golf courseDaewon Cantavil, developer of the Da Phuoc project has received permission from the Danang People’s Committee to convert the 66ha golf course forming part of the project into landed houses and high rise buildings. The project comprises of 8,500 apartments, 5-star hotels and a 60 storey office build-ing with total investment capital of US$300 million.

Regional News

Wyndham debuts new brand in IndonesiaWyndham Hotel Group announced the launch of its Howard Johnson brand in Indo-nesia with three properties (in Bali, Surabaya and Makassar) as well as the opening of the fourth Ramada in the country.

Myanmar to establish two hotel zonesThe Myanmar government is planning to establish two hotel zones next year to help combat the severe hotel room shortage brought about by the recent spike in tourist arrivals. One hotel zone will be located with-in the major tourist destination in the Inlay region in Shan State Northern Myanmar while the another zone will be located near Mount Popa, 50km Southeast of Bagan.

Qatar Airways to provide daily flights to Phnom PenhQatar Airways is asserting it aggressive ex-pansion to South East Asia with the launch of daily flights to Phnom Penh early next year, becoming the only Middle Eastern carrier to operate in Cambodia. The Doha - Phnom Penh route will operate with a capacity of 284 seats per day.

Aston launches new select service brand in IndonesiaAston International has launched a new select service brand called Hotel Neo by Aston, which is designed to appeal to the budget traveller with well-designed layouts and four star facilities. The first property is scheduled to open in Bali with a further 20 Hotel Neo’s in the pipeline.

8 Feature Article: Branded Residences

Alternaty® Vietnam Hotels + Resorts Newsletter alternaty.com

December 2012

Feature Article:Branded Residences

Would a residential component be a good option for my resort project?It is certainly worth considering, however each developer has different financing and ROI targets and it is important to be aware that in some cases the inclusion of a residential component may increase costs but not necessary increase the overall return.

Can I sign a management agreement for my mixed-use residential project? This is possible in some cases, but the majority of the inter-national operators would not allow developers to sell residen-tial products that are branded with their name.

What other management op-tions do I have? There are several smaller in-ternational operators that may consider such a project or you can create your own manage-ment and brand but make sure it is done properly from the very beginning.

Questions + Answers

Q

Hotel and resort developers are constantly seeking innovative ways to shorten their payback period and increase the overall return on their investment. The last few years have seen an increase in the num-ber of hotel and resort projects that have incorporated residential components in a bid to increase profits. By combining residential products with professionally managed hotel and resort components developers are able to rely on an additional source of financing

through presales of the residential products. These mixed-use projects are developed in the belief that second home buyers would appreciate the opportunity to not only own property but also to enjoy the use of a lifestyle product with the added benefit of some potential rental returns. Owners of branded residences have full access to all the amenities and services that form part of the hotel or resort complex thereby enjoying the full brand experience.

Some things that you should be aware of before consider-ing to develop branded residences

International hotel management companies prefer to stay well away from them due to their management implications.

Ensure that the marketing agent or sales team does not over promise to buyers. They only deal with the buyers until the sale is made, while you will have to deal with them for the life of your development.

Do not underestimate the importance of a finely balanced maintenance fee and think again before proposing to have it fixed - it can end up being a very painful decision once the resort ages.

The maintenance fee is one of the most common reasons for litigation with the owners. Ensure that the calculation methodology is completely transparent.

Set up an independent body corporate structure for the individual owners and ensure that the accounting systems of the resort and residential components are completed separated.

A

Q

A

Q

A

Be aware that your hotel or resort will decrease in value once you sign with a management company or if you have a residential component

Consider to create a fractional structure as part of the residential sales but seek expert advice before doing so.

Allow the owners to join an internation-al and local exchange system.

Do not allow the owners to publically rent their units in the open market at a self determined price. This can be extremely damaging to the marketing image and financial performance of the whole complex.

In the case of branded residences, do not promise to owners a specific brand and a specific brand should not be named in the sales contract. Always reserve the right to terminate the man-agement company and have the ability to change to an equivalent substitute.

Finally, seeks expert advice before embarking upon mixed-use branded residences.

9HICAP 2012 Roundup

Alternaty® Vietnam Hotels + Resorts Newsletteralternaty.com

December 2012

HICAP 2012Roundup

The Hotel Investment Conference Asia Pacific (HICAP), held annually since 1989, is the most established conferences for the hotel investment and development community in Asia Pacific. Unsurprisingly, at this year's event held in Hong Kong on 10 - 12 October, Alternaty was one of only a few attending companies representing Vietnam. There was a much lower attendance of Vietnamese companies compared to previous years and instead there was a much higher partici-pation from countries that were previously underrepresented namely the Philippines, Myanmar and Indonesia.

Attention is clearly moving towards newly accessible destinations such as Myanmar and Sri Lanka, both of which seem to be among the top emerging hotel and resort markets in Asia. The two countries were often men-tioned by panellists throughout the confer-ence and especially during the “Investment Outlook” session where they were identified as highly targeted investment destinations. Indonesia is still experiencing very strong growth and destinations such as Bali and Jakarta have the close attention of Singapor-ean, Hong Kong and Australian investors. However, the rapid growth seems to be headed towards oversupply in the resort

destinations, especially for products with residential components.

Myanmar was the hottest topic in every investment discussion and many investors are currently considering to explore oppor-tunities for development or acquisition of existing buildings to convert into hotels.The next conference in the series will be the HICAP Update which will be held in Singapore on 12 - 13 March 2013. For this conference Alternaty has been selected to participate in the panel discussion focusing on hotel development and investment op-portunities and challenges in Vietnam.

South East Asia PropertyAwards 2012 Roundup

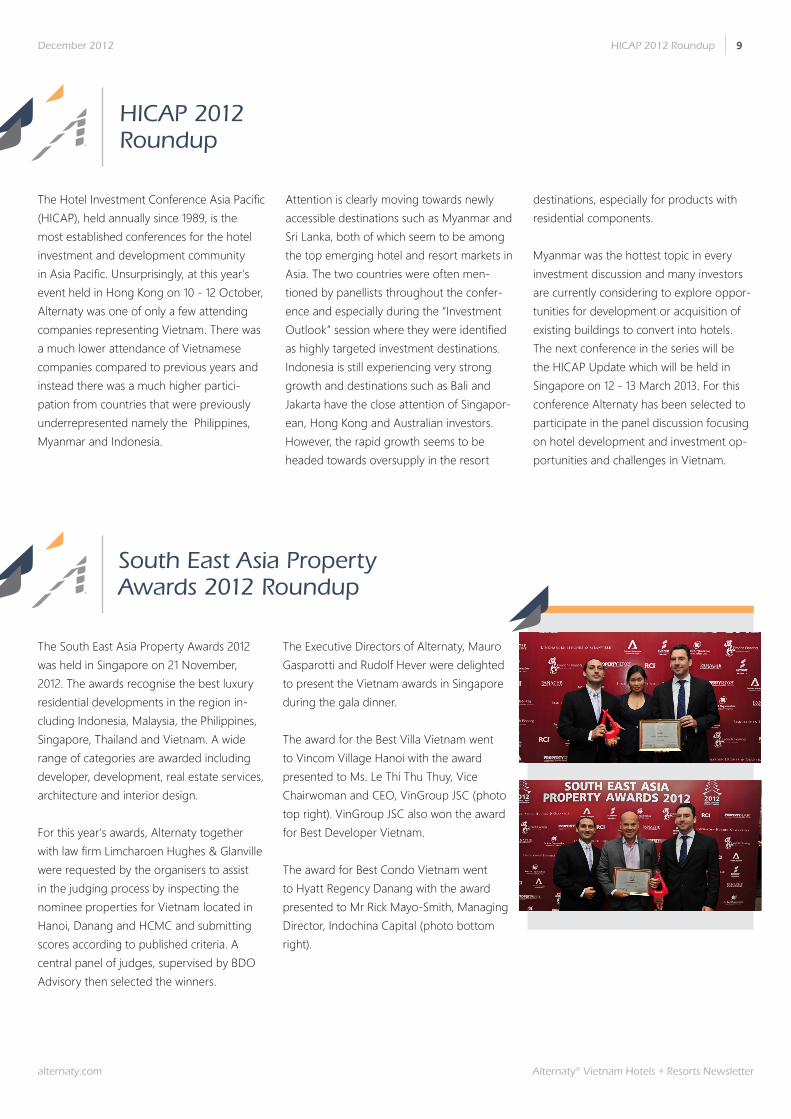

The South East Asia Property Awards 2012 was held in Singapore on 21 November, 2012. The awards recognise the best luxury residential developments in the region in-cluding Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam. A wide range of categories are awarded including developer, development, real estate services, architecture and interior design.

For this year's awards, Alternaty together with law firm Limcharoen Hughes & Glanville were requested by the organisers to assist in the judging process by inspecting the nominee properties for Vietnam located in Hanoi, Danang and HCMC and submitting scores according to published criteria. A central panel of judges, supervised by BDO Advisory then selected the winners.

The Executive Directors of Alternaty, Mauro Gasparotti and Rudolf Hever were delighted to present the Vietnam awards in Singapore during the gala dinner.

The award for the Best Villa Vietnam went to Vincom Village Hanoi with the award presented to Ms. Le Thi Thu Thuy, Vice Chairwoman and CEO, VinGroup JSC (photo top right). VinGroup JSC also won the award for Best Developer Vietnam.

The award for Best Condo Vietnam went to Hyatt Regency Danang with the award presented to Mr Rick Mayo-Smith, Managing Director, Indochina Capital (photo bottom right).

10 Investment Opportunities December 2012

InvestmentOpportunities

+84 933 902 530

Rudolf Hever Executive Director

TE

+84 908 556 492

T

E

Mauro GasparottiExecutive Director

Please don’t hesitate to contact us to discuss any of the contents in this newsletter or for more information on any of the opportunities above. We welcome your comments and suggestions for the next edition. In the meantime, don’t forget to follow us on Twitter, LinkedIn or Face-book to receive the latest updates and opportunities as they become available.

+84 836 028 591

T

E

My NguyenResearch Executive

Hot Properties – See our website for more Hot Properties & Enquiries

Location Phuket, ThailandStatus Operating resortScale 42 keys on 1.5 hectaresDescription Contemporary Thai style villa resort on a cliff with private beach. Some units have a private swimming pool.Investment Options 100% equity stake

Location Bali, IndonesiaStatus Operating resortScale 81 keysDescriptionHigh end villa resort located in Uluwatu with strata title.Investment Options Up to 90% equity stake

Location Chiang Mai, ThailandStatus Operating resortScale 29 keysDescription A boutique resort with a prime location with value-add opportunity to refurbish adjacent buildings to add another 29 keys.Investment Options 100% equity stake, freehold

Location Hoi An, VietnamStatus Construction 93% completed and expected to be operational within 12 weeks.Scale 98 keys comprising of apartments, penthouses and villas on 2.6 hectares.Description A beachfront resort with a mix of unit types including beachfront villas designed in a Mediterranean style.Investment Options 100% equity stake, 59% equity stake or 31.5% equity stake with option to purchase on shore or off shore.

Location HCMC, VietnamStatus Construction 85% completed and expected to be handed over by Q2, 2013.Scale 70 units of serviced apartmentsDescription A mixed-use development comprising of serviced apartment, hotel, retail, office and residential apartment com-ponents in close proximity to the airport.Investment Options Serviced apartment lease or management contract.

Location HCMC, VietnamStatus Operating HotelScale 280 roomsDescription 5 star hotel located on the periphery of the CBD.Investment Options 100% equity stake

About Us

Alternaty is a boutique real estate firm providing specialist advice for hotel, resort and second home proj-ects in Vietnam and the Indochina region.

Our servicesInvestment ConsultingInvestor RepresentationHotel Operator SelectionMarket ResearchFeasibility StudyDevelopment Consulting

We specialise in Alternative OwnershipRental Pool StructuringFractional OwnershipMembership ClubsBranded Residences

Alternaty Vietnam Hotels + Resorts Newsletter, published by Alternative Real Estate Service Co., Ltd. (hereafter “Alternaty”), is a newsletter containing information about the hotel and resort market in Vietnam and Indochina region. It is provided for gener-al information purposes only. Whilst making all reasonable effort to provide correct information, no legal responsibility can be accepted by Alternaty for any loss or damage arising out of the use of or reliance on the contents of this newsletter.

Disclaimer

Unit 23, 26 Ly Tu Trong Street,

District 1, Ho Chi Minh City,

Vietnam

+84 836 028 591

alternaty.com

T

W

Find Us

Regional OpportunitiesVietnam Opportunities