Alternative Tax Apportionment Issues Confronting Multistate Companies

27

1 Alternative Tax Apportionment Issues Confronting Multistate Companies

Transcript of Alternative Tax Apportionment Issues Confronting Multistate Companies

1

Alternative Tax Apportionment Issues Confronting Multistate Companies

Alternative Tax Apportionment Issues Confronting Multistate Companies

2

BACKGROUND

Historically, states used separate accounting to determine in-state income

Apportionment was adopted as separate; accounting was time-consuming and unreliable

Initial formulas were for property tax purposes and relied solely on a property factor

Alternative Tax Apportionment Issues Confronting Multistate Companies

3

PURPOSE OF APPORTIONMENT

Fictional approximation of income earned in a taxable jurisdiction

– Property

– Payroll

– Sales

Tax planner’s role is to determine if the approximation is appropriate

Alternative Tax Apportionment Issues Confronting Multistate Companies

4

CONSTITUTIONAL OVERVIEW

Due Process requirements

– States may only tax the income earned within their borders

– The tax must be fairly related to the services derived from the state Wisconsin v. J.C. Penney Co., 311 U.S. 435

Commerce Clause requirements

– Tax must be fairly apportioned Container Corp. of America v. FTB, SCt, 463 US 159 (1983)

» Internal consistency test—If every state has the same tax and applied it the same way, no multiple taxation would occur.

» External consistency test—The apportionment formula must actually reflect how income is generated.

Alternative Tax Apportionment Issues Confronting Multistate Companies

5

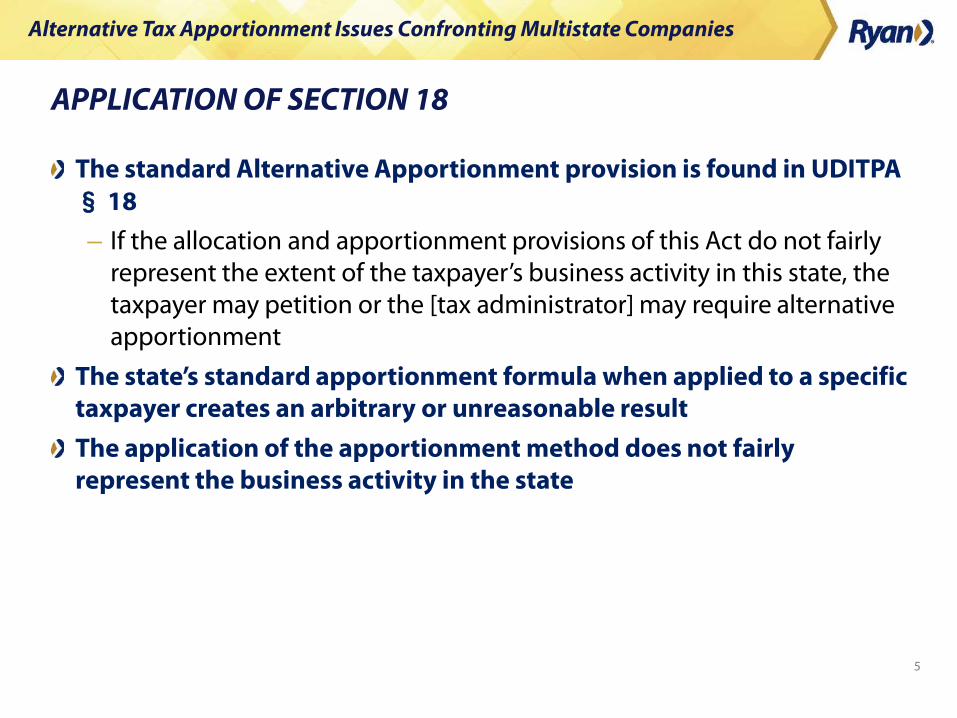

APPLICATION OF SECTION 18

The standard Alternative Apportionment provision is found in UDITPA § 18

– If the allocation and apportionment provisions of this Act do not fairly represent the extent of the taxpayer’s business activity in this state, the taxpayer may petition or the [tax administrator] may require alternative apportionment

The state’s standard apportionment formula when applied to a specific taxpayer creates an arbitrary or unreasonable result

The application of the apportionment method does not fairly represent the business activity in the state

Alternative Tax Apportionment Issues Confronting Multistate Companies

6

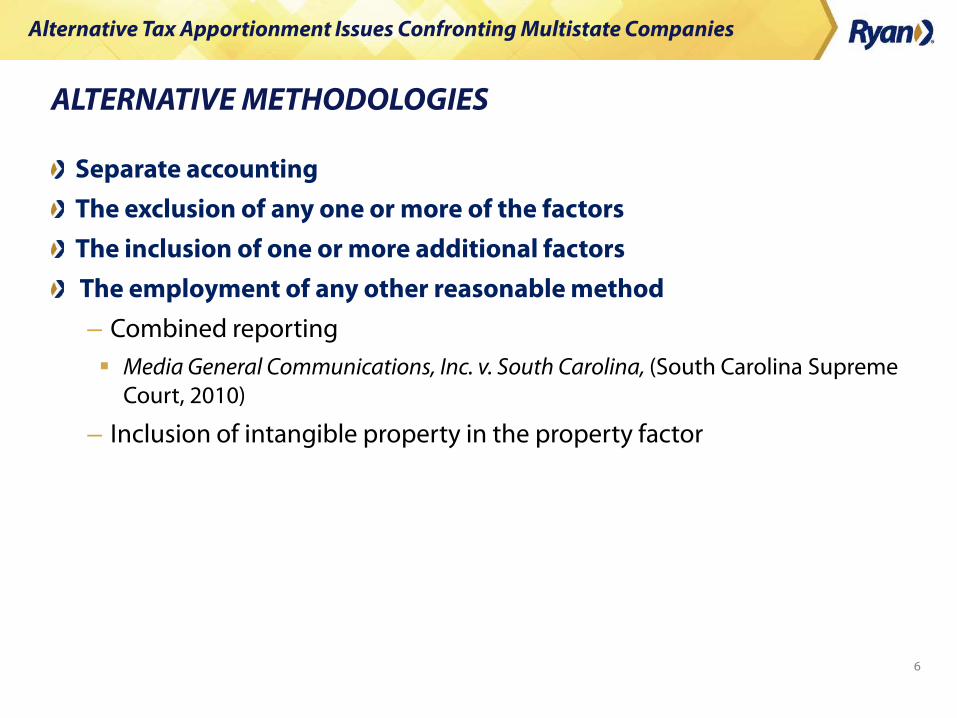

ALTERNATIVE METHODOLOGIES

Separate accounting

The exclusion of any one or more of the factors

The inclusion of one or more additional factors

The employment of any other reasonable method

– Combined reporting Media General Communications, Inc. v. South Carolina, (South Carolina Supreme

Court, 2010)

– Inclusion of intangible property in the property factor

Alternative Tax Apportionment Issues Confronting Multistate Companies

7

STATUTORY ALTERNATIVE APPORTIONMENT

Industry-specific Alternatives

– Construction

– Transportation

– Financial Services

– Media

Alternative Tax Apportionment Issues Confronting Multistate Companies

8

INVOKING ALTERNATIVE APPORTIONMENT

Who may invoke alternative apportionment?

– The state may require the use of an alternative apportionment formula

– The taxpayer may request the use of an alternative apportionment factor

Who has the burden of proof?

– Generally, the party seeking alternative apportionment has the burden of proof

– Consider: Does the burden of proof differ depending on the party seeking a change?

What impact does the deemed correctness of an assessment have on the burden of proof?

Alternative Tax Apportionment Issues Confronting Multistate Companies

9

INVOKING ALTERNATIVE APPORTIONMENT

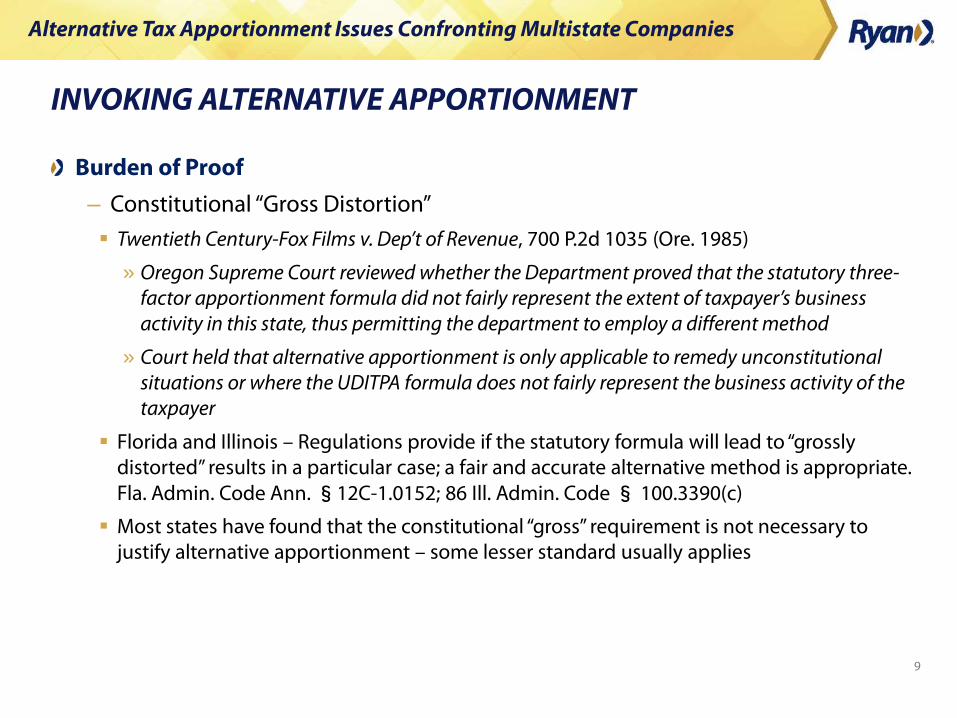

Burden of Proof

– Constitutional “Gross Distortion”

Twentieth Century-Fox Films v. Dep’t of Revenue, 700 P.2d 1035 (Ore. 1985)

» Oregon Supreme Court reviewed whether the Department proved that the statutory three-factor apportionment formula did not fairly represent the extent of taxpayer’s business activity in this state, thus permitting the department to employ a different method

» Court held that alternative apportionment is only applicable to remedy unconstitutional situations or where the UDITPA formula does not fairly represent the business activity of the taxpayer

Florida and Illinois – Regulations provide if the statutory formula will lead to “grossly distorted” results in a particular case; a fair and accurate alternative method is appropriate. Fla. Admin. Code Ann. §12C-1.0152; 86 Ill. Admin. Code § 100.3390(c)

Most states have found that the constitutional “gross” requirement is not necessary to justify alternative apportionment – some lesser standard usually applies

Alternative Tax Apportionment Issues Confronting Multistate Companies

10

INVOKING ALTERNATIVE APPORTIONMENT

Preponderance of the evidence, slightly more evidence in support than against it, >50%

Clear and Convincing/Cogent Evidence. Somewhere between preponderance of evidence and beyond a reasonable doubt , highly probable. Between 75 and 80% likely

– Moorman Manufacturing Co. v. Blair, 437 U.S. 267

– California – Microsoft v. Franchise Tax Board, 139 P.3d 1169 (Cal. 2006). The party invoking the alternative formula must prove by clear and convincing evidence that the statutory formula is not a fair representation. In so holding, the court adopted a quantitative and qualitative test

– New York – British Land (Maryland) Inc. v. N.Y. Tax App. Trib., 85 N.Y.2d 139, 147-48 (N.Y. Ct. App. 1995). Must demonstrate by clear and cogent evidence that the standard apportionment formula does not properly reflect a taxpayer’s presence

Alternative Tax Apportionment Issues Confronting Multistate Companies

11

ELEMENTS TO BE PROVEN

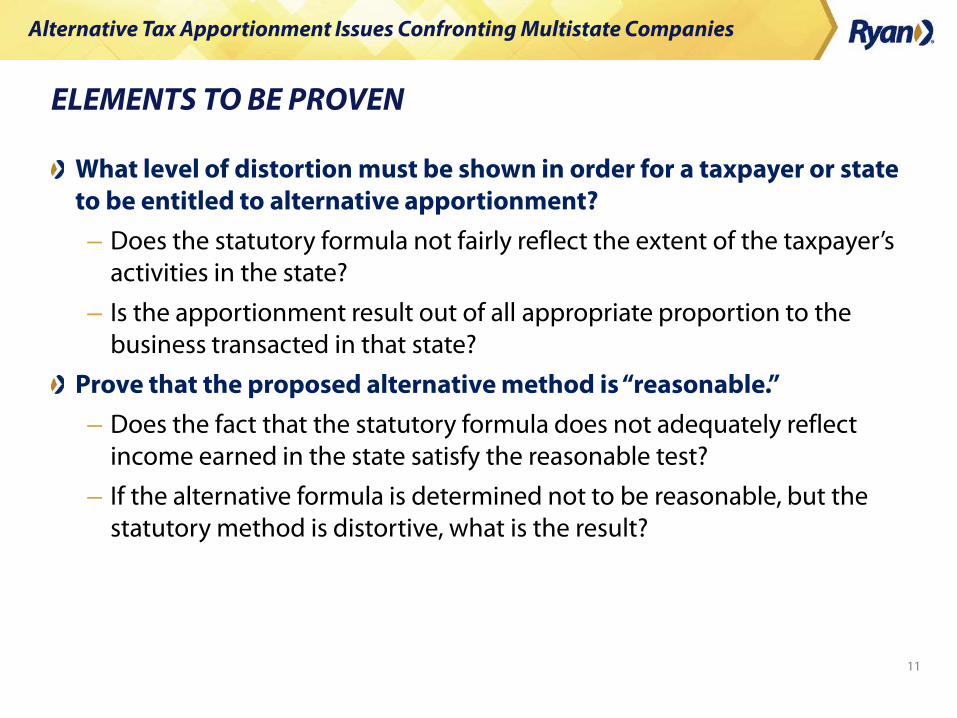

What level of distortion must be shown in order for a taxpayer or state to be entitled to alternative apportionment?

– Does the statutory formula not fairly reflect the extent of the taxpayer’s activities in the state?

– Is the apportionment result out of all appropriate proportion to the business transacted in that state?

Prove that the proposed alternative method is “reasonable.”

– Does the fact that the statutory formula does not adequately reflect income earned in the state satisfy the reasonable test?

– If the alternative formula is determined not to be reasonable, but the statutory method is distortive, what is the result?

Alternative Tax Apportionment Issues Confronting Multistate Companies

12

INDICATIONS OF UNFAIR APPORTIONMENT

Use of separate accounting

– Hans Rees’ Sons

– Moorman Mfg. Co.

– Rejected in Exxon and Mobil

Separate accounting alone will not support alternative apportionment, as this was the method withdrawn in favor of formulary apportionment

– In re: Appeal of Crista Corp. (California State Board of Equalization, No. 2002-SBE-004, June 20, 2002)

Alternative Tax Apportionment Issues Confronting Multistate Companies

13

INDICATIONS OF UNFAIR APPORTIONMENT

Factor does not represent income earned in the state

– Treasury receipts

Microsoft v. FTB, (California Supreme Court, 2006)

Missing factor

– Inventory

Georgia v. Coca-Cola Bottling Co. (GA Supreme Court, 1956)

– Intangibles

Microsoft v. FTB, (San Francisco Superior Court Case No. CGC08471260, 3/21/11, case appealed to the California Court of Appeals)

– Futures contracts

General Mills Inc., v. FTB, 208 Cal. App. 4th 1290 (2012). In determining whether the receipts from hedging transactions should be included in the computation of the receipts factor, the Appellate Court concluded that the FTB did not have to prove the reasonableness of only one alternative but may, if reasonable, apply any “method that is reasonable to effectuate an equitable allocation and apportionment of the taxpayer’s income.”

Alternative Tax Apportionment Issues Confronting Multistate Companies

14

UNREASONABLE APPORTIONMENT

Application of the Three-Factor Formula

– Application of the traditional UDITPA three-factor formula can result in an inaccurate reflection of a taxpayer’s income

– An in-state company with significant property and payroll sourced to the state can benefit from an equally weighted three-factor apportionment formula

– In contrast, multistate businesses with little or no payroll or property to offset their receipts are often at a disadvantage

Alternative Tax Apportionment Issues Confronting Multistate Companies

15

UNREASONABLE APPORTIONMENT

Is the inclusion of foreign-source dividend, interest, and royalty income without appropriate factor representation unconstitutional?

– No – Conoco Inc., v. State of New Mexico, 931 P. 2d 730 (NM 1996)

– Yes – Tambrands, Inc. v. State Tax Assessor, 595 A. 2d 1039 (ME 1991)

– No – E.I. DuPont de Nemours v. State Tax Assessor, 595 A. 2d 1039 (ME 1996), ruling on the “Augusta Formula” which was devised after the Tambrands case The Augusta Formula allows exclusion of 50% of the dividends from foreign

subsidiaries, but without factor relief

Alternative Tax Apportionment Issues Confronting Multistate Companies

16

UNREASONABLE APPORTIONMENT

Taxpayer’s use of the statutory formula

– Use of the statutory cost of performance method Equifax Inc. v. MS DOR, MS S. Ct. (June 20, 2013)

» June 20, 2013, the Mississippi Supreme Court upheld an assessment, including penalties, against Equifax for failure to apportion its income using a sales factor based on its market presence in Mississippi. In that case, the Court did not find it necessary that the Department of Revenue had the burden to prove that the statutory method of apportionment, cost of performance, resulted in distortion.

» H.B. 799, enacted April 10, 2014, effective January 1, 2015, clarifies the ability of the Department of Revenue and taxpayers to utilize alternative apportionment.

» Specifically, the legislation requires the party requesting alternative apportionment show by a preponderance of the evidence that the statutory method of apportionment does not fairly represent the extent of a taxpayer’s Mississippi business activity, and that the proposed method does more fairly represent the activity more than any other reasonable method.

Alternative Tax Apportionment Issues Confronting Multistate Companies

17

UNREASONABLE APPORTIONMENT

Vodafone Americas Holdings, Inc. v. Roberts, No. M2013-00947-COPA-R3-CV TN Ct. App. (6/23/2014)

– June 23, 2014, the Tennessee Court of Appeals upheld a lower court’s and revenue agency’s decision to require Vodafone to use an alternative method of apportionment.

– Vodafone had sourced revenue for the sale of cell phone services to Tennessee based on the statutory cost of performance rule, where services are sourced to a single state in which the bulk of the taxpayer’s cost of performing the service is incurred.

– The Court upheld the Commissioner of Revenue’s decision to use a market-based sourcing rule to report Tennessee receipts.

– The Court found that the Commissioner had shown by clear and cogent evidence that unusual circumstances existed to warrant a deviation from the statutory formula.

Alternative Tax Apportionment Issues Confronting Multistate Companies

18

UNREASONABLE APPORTIONMENT

Trend to more heavily weighted sales factor or single-sales factor formula

– Only eight of 19 MTC member states continue to use the equally weighted three-factor apportionment formula

– Does using a heavily or single weighted sales factor more accurately reflect the activities of taxpayers conducting business within its borders?

The rationale is a weighted sales factor corresponds with the technological advancements (e.g., the generation of sales and other gross receipts does not necessarily depend on having employees, real property , or tangible property within a state)

However a single sales factor only reflects the contribution of the market state

MTC Article III obligates member states to offer their multistate taxpayers the option of using either the Compact’s three-factor formula to apportion and allocate income for state income tax purposes or the state’s own alternative apportionment formula

Due to the adoption of a single sales factor by a number of states, the option to use the standard three-factor apportionment formula becomes an attractive alternative method for out-of-state taxpayers

Alternative Tax Apportionment Issues Confronting Multistate Companies

19

UNREASONABLE APPORTIONMENT

A California taxpayer was permitted to use the equally weighted three-factor MTC apportionment formula to calculate its California franchise tax

– Gillette argued that the state’s mandate of apportionment using double-weighted sales factor violated California’s participation in the MTC

– The California Court of Appeals determined that the Multistate Tax Compact is binding on the signatory states and that it calls for the option, under UDITPA, to apportion income on an equally weighted three-factor basis

– The election is necessary to provide a taxpayer an option for uniformity when there are conflicting state statutes

– The only way for a member state to eliminate this option is to withdraw from the MTC

– Gillette Co. v. Franchise Tax Board, No. A130803, Court of Appeal of California, First District (Oct. 2, 2012)

– CA Supreme Court heard oral arguments on this case on October 6, 2015

Alternative Tax Apportionment Issues Confronting Multistate Companies

20

MICHIGAN

IBM v. Department of Treasury

– July 14, 2014, the Michigan Supreme Court decides (4 to 3) in favor of the taxpayer, allowing the election of an equally weighted three-factor apportionment formula

– September 10, 2014, Legislature approves retroactive repeal of MTC compact. Governor approves and enacts law on September 12, 2014

– To date, the Michigan court of claims and court of appeals have upheld the retroactive repeal of the MTC compact. Most recently in Gillette Commercial Operations N. Am. v. Department of Treasury, MI Ct. App., No. 325258, 9/29/15, the Court upheld the retroactive repeal

Alternative Tax Apportionment Issues Confronting Multistate Companies

21

MINNESOTA

Kimberly-Clark Corp. v. Commissioner of Revenue, Minnesota Tax Court, File No. 8670-R, June 15, 2015

– Court concluded, without deciding, that the MTC compact created a valid binding contract between Minnesota and the other states that adopted the compact

– However, the compact did not bar the Minnesota Legislature from repealing Articles III and IV, to eliminate the equally weighted three-factor apportionment election

– The court determined that the 1987 repeal of the equally weighted three-factor apportionment election was permitted under the compact, and therefore held for the state

Alternative Tax Apportionment Issues Confronting Multistate Companies

22

OREGON

In an Oregon Tax Court case, an out-of-state taxpayer is asserting that it has a right to elect to apportion its income under the Multistate Tax Compact’s evenly weighted three-factor formula.

The complaint to the tax court’s magistrate division was filed on July 2. The parties met in a case management conference in August, and on Sept. 17 filed for a petition of special designation to bypass the magistrate division and start the proceedings in the regular division. That petition is awaiting a ruling by the judge.

Oregon adopted the compact in 1967 and is still a full member. However, in 1993, the state enacted Revised Statute 314.606, which says that when Oregon enacts an apportionment formula that conflicts with the Multistate Tax Compact election provision, the state statute is controlling.

Oregon currently requires single-sales-factor apportionment.

Health Net, Incorporated and Subsidiaries v. Department of Revenue (Case No. 120649D).

Alternative Tax Apportionment Issues Confronting Multistate Companies

23

TEXAS

In orders released by the Texas Controller of Public Accounts on 9/12/12, 5/16/13, 6/18/13 and 8/14/13, denied the refund claims of three unidentified out-of-state businesses that attempted to elect to apportion their income under the Multistate Tax Compact’s evenly weighted three-factor formula.

In the 6/18/13 case, the taxpayer introduced the CA Gillette win into the record. The Comptroller ruled that no weight can be given to Gillette as it was depublished, and cert was granted by the California Supreme Court.

Texas adopted the Multistate Tax Compact in 1967 and is still a full member, with the compact codified as chapter 141 of the Texas Tax Code. However, Sec. 171.106(a) of the Code requires that a taxable entity’s margin be apportioned to Texas under a single-factor formula based on gross receipts.

Texas is a bit more complex than California, as there is a question as to whether the Texas gross margins tax is an “income tax.”

Alternative Tax Apportionment Issues Confronting Multistate Companies

24

REASONABLENESS OF PROPOSED METHOD

Twentieth Century-Fox Films v. Dep’t of Revenue, 700 P.2d 1035 (Ore. 1985)

– Reasonableness has at least three components 1) the division of income fairly represents business activity and if applied uniformly would result in taxation of no more or no less than 100% of a taxpayer’s income; 2) the division of income does not create or foster lack of uniformity among UDITPA jurisdictions; and 3) the division of income reflects the economic reality of the business activity engaged in by the taxpayer in the state.

Carmax Auto Superstores West Coast, Inc. v. DOR, SC Supreme Court, No. 27474 12/23/2014

– The party seeking to use the alternate formula need only show that its accounting method is reasonable, not that it more fairly represents the taxpayer’s business than any competing method.

Alternative Tax Apportionment Issues Confronting Multistate Companies

25

CONCLUSION

Despite taxpayer setbacks in the MTC cases, Equifax, Vodafone, and others, it is still the taxpayer’s duty to examine the reasonableness of the application of the apportionment formula to its business.

With the increasing reliance on the sales (market) factor as a way to solely source income, many taxpayers may find themselves in situations where the statutory formulas do not reflect a taxpayer’s presence in a particular jurisdiction resulting in a distortion of the income subject to tax by that jurisdiction.

Alternative Tax Apportionment Issues Confronting Multistate Companies

26

Contact Information

Mark L. Nachbar

Principal

Ryan

State Income and Franchise Tax

630.515.0477

27 © 2015 Ryan, LLC. All rights reserved. All logos and trademarks are the property of their respective companies and are used with permission.

This document is presented by Ryan, LLC for general informational purposes only, and is not intended as specific or personalized recommendations or advice. The application and effect of certain laws can vary significantly based on specific facts, and professional advice of any nature should be sought

only from appropriate professional advisors. This document is not intended, and shall not be deemed, to constitute legal, accounting or other professional advice.