AlphaImpactRx Barclays Oncology Webinar 1 Dec 2015

68

Immuno-Oncology and Emerging Market Dynamics AlphaImpactRx – Barclays Webinar December 1, 2015

-

Upload

lesley-bailey -

Category

Health & Medicine

-

view

1.119 -

download

1

Transcript of AlphaImpactRx Barclays Oncology Webinar 1 Dec 2015

Immuno-Oncology and Emerging

Market Dynamics AlphaImpactRx – Barclays Webinar

December 1, 2015

Introductions and Objective

Webinar Moderator: Stacy Mecham

Senior Vice President,

Oncology Franchise,

AlphaImpactRx

Objective

• To share our unique perspective on the dynamics of today’s oncology marketplace.

• To advance your understanding of the unprecedented changes emerging across

promotion, treatment and testing - and to provide a view into how 2016 is shaping

up.

2

Featured Presenter: Mark Purcell Managing Director and Head of Global Pharmaceutical Equity Research Coverage, Barclays

Our Agenda

3

• A snapshot of the current Oncology Promotional Landscape

• The I/O Battlefield

NSCLC

Melanoma

PD-L1 Testing

• Preparing for ASH and San Antonio Breast Cancer Conferences

Breast Cancer

CLL

• Q&A

…and once earned, you need to make the most of it.

The battle to earn the Oncologist’s attention is becoming more challenging...

4

Novartis is emerging as the leader within a crowded oncology

promotional landscape.

n=Total sales representative product details BrandImpact Oncology panel had ~ 450 physicians in October 2015

Sh

are

of

Deta

ils

Source: BrandImpact

0%

2%

4%

6%

8%

10%

12%

14%

2010 2011 2012 2013 2014 2015 (Jan-Oct)

Novartis GSK Genentech BMS Merck Celgene

Pfizer Boehringer Ing. Lilly Bayer Janssen Amgen

Eisai Pharmacyclics Medivation Millennium Sanofi Teva

Onyx Incyte AstraZeneca

n=35,979 n=33,970 n=34,408 n=31,103 n=30,028 n=28,498

Share of Attention – Company Level Detailing - Oncology (2010-2015)

March ‘15: Novartis

acquires Oncology

franchise from GSK

5

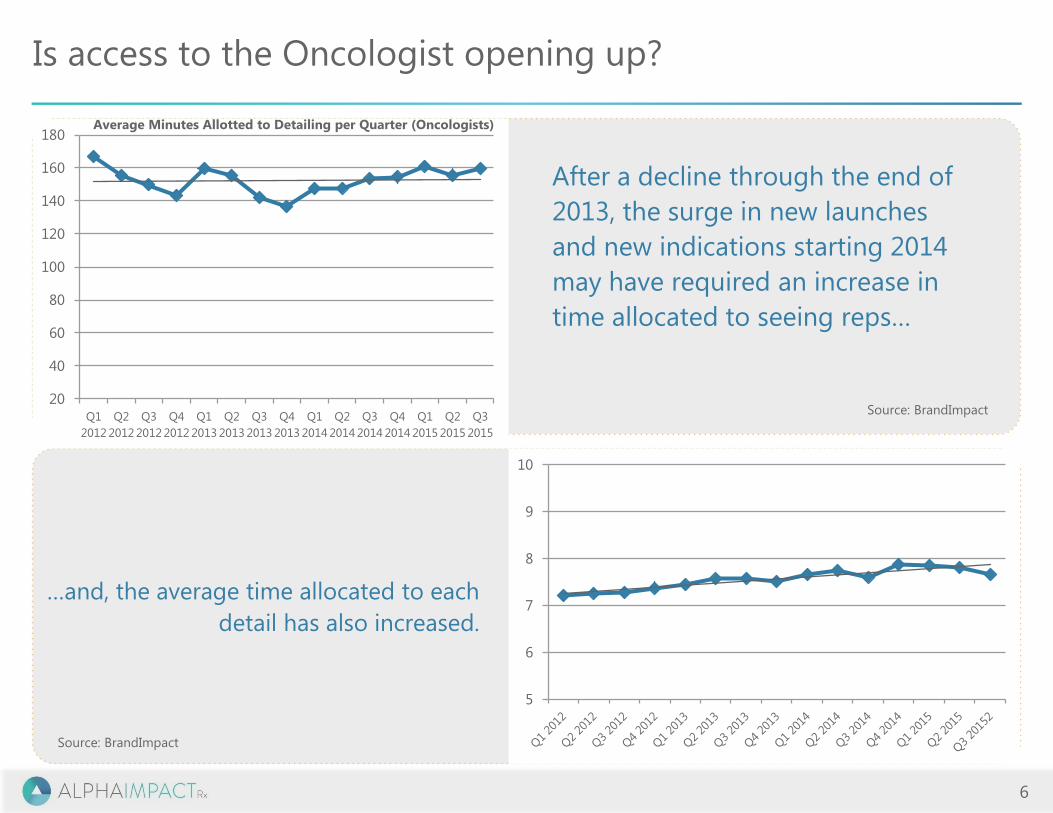

Is access to the Oncologist opening up?

6

After a decline through the end of

2013, the surge in new launches

and new indications starting 2014

may have required an increase in

time allocated to seeing reps…

…and, the average time allocated to each

detail has also increased.

20

40

60

80

100

120

140

160

180

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

5

6

7

8

9

10

Source: BrandImpact

Average Minutes Allotted to Detailing per Quarter (Oncologists)

Source: BrandImpact

Source: BrandImpact

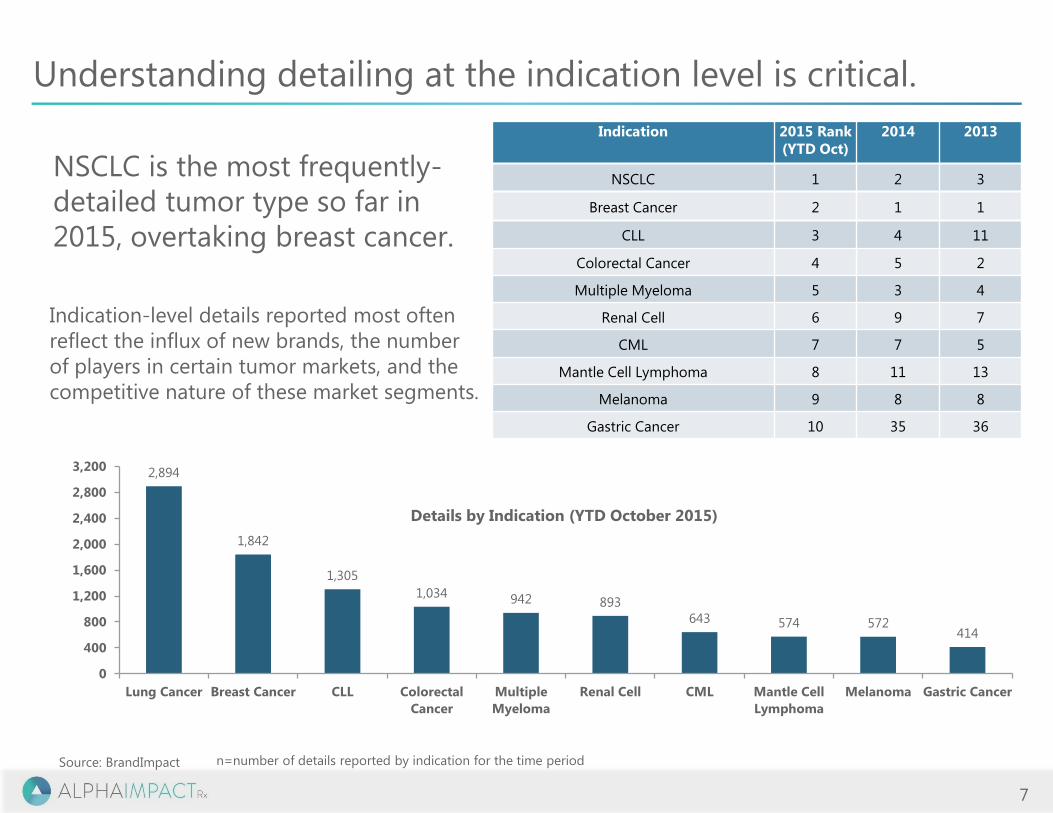

7

2,894

1,842

1,305

1,034 942 893

643 574 572 414

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

Lung Cancer Breast Cancer CLL Colorectal

Cancer

Multiple

Myeloma

Renal Cell CML Mantle Cell

Lymphoma

Melanoma Gastric Cancer

Details by Indication (YTD October 2015)

Indication-level details reported most often

reflect the influx of new brands, the number

of players in certain tumor markets, and the

competitive nature of these market segments.

n=number of details reported by indication for the time period

NSCLC is the most frequently-

detailed tumor type so far in

2015, overtaking breast cancer.

Indication 2015 Rank (YTD Oct)

2014 2013

NSCLC 1 2 3

Breast Cancer 2 1 1

CLL 3 4 11

Colorectal Cancer 4 5 2

Multiple Myeloma 5 3 4

Renal Cell 6 9 7

CML 7 7 5

Mantle Cell Lymphoma 8 11 13

Melanoma 9 8 8

Gastric Cancer 10 35 36

Understanding detailing at the indication level is critical.

Source: BrandImpact

8

Measuring details at the brand level is no longer enough.

Top 10 Detailed Brands

2015 Rank (YTD Oct)

Opdivo 1

Afinitor 2

Imbruvica 3

Keytruda 4

Avastin 5

Cyramza 6

Ibrance 7

Revlimid 8

Xtandi 9

Neulasta 10

Top 10 Detailed Brands by Ind

Indication 2015 Rank (YTD Oct)

Opdivo NSCLC 1

Afinitor Breast Cancer 3

Ibrance Breast Cancer 3

Imbruvica CLL 4

Keytruda Melanoma 5

Xtandi Prostate Cancer 6

Neulasta Neutropenia 7

Gazyva CLL 8

Cyramza NSCLC 9

Kyprolis Multiple Myeloma 10

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with companies covered in its research reports. As a result, investors should be

aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their investment decision.

This research report has been prepared in whole or in part by equity research analysts based outside the US who are not registered/qualified as research analysts

with FINRA.

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 52.

Equity Research

Barclays Global Pharmaceuticals

Mark Purcell

Barclays, UK

+44 203 1347189

Thinking ahead in oncology An analyst’s perspective 1 December 2015

• Introduction

• Lung cancer – Opdivo versus the competition

• Key questions / perspectives in an increasingly crowded indication; 1L data in 2016

• Melanoma battleground

• Opdivo vs Keytruda; Immunotherapy versus targeted treatments; emerging combos

• Breast cancer

• Ibrance launch perspectives in HER2-ve patients

• Perjeta perspectives –a race against time

• Chronic Lymphocytic Leukemia

• Where next for Imbruvica?

Thinking ahead in oncology

Overview

December 1, 2015 10

Source: Barclays Research

Introduction

December 1, 2015 11

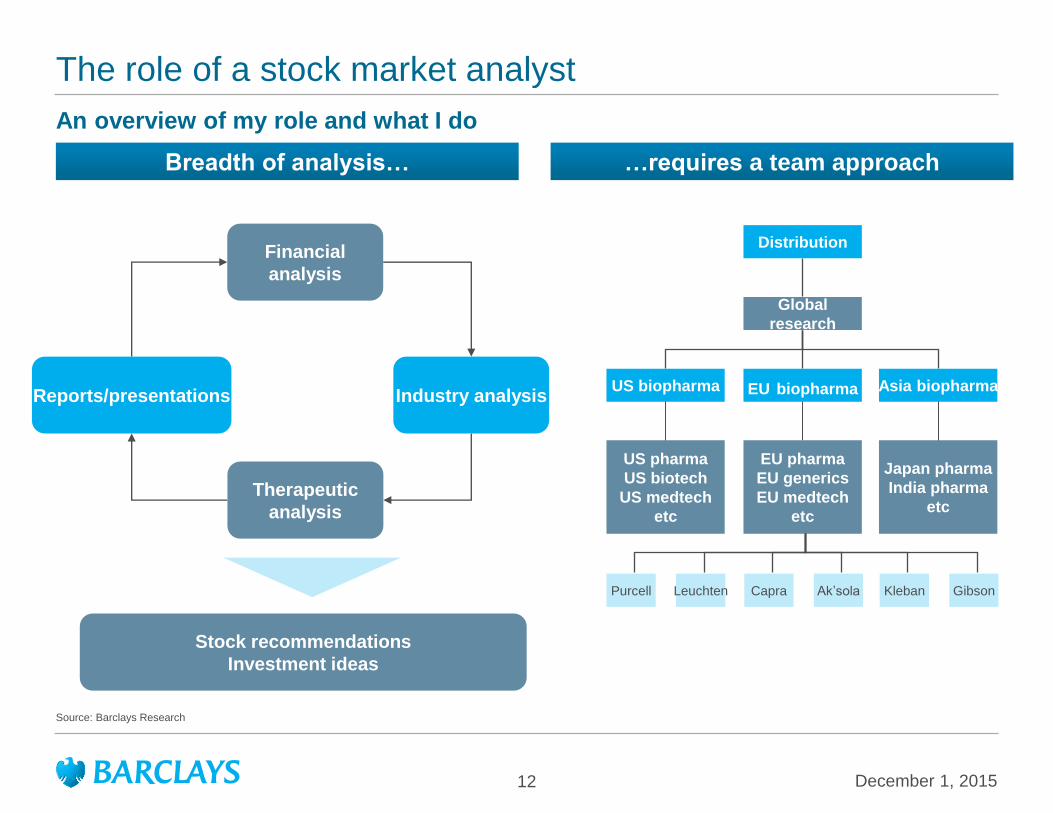

The role of a stock market analyst

An overview of my role and what I do

Source: Barclays Research

December 1, 2015 12

Financial

analysis

Therapeutic

analysis

Industry analysis Reports/presentations

Breadth of analysis… …requires a team approach

Stock recommendations

Investment ideas

US pharma

US biotech

US medtech

etc

Japan pharma

India pharma

etc

Global

research

US biopharma Asia biopharma

Distribution

EU pharma

EU generics

EU medtech

etc

EU biopharma

Gibson Purcell Capra Ak’sola Kleban Leuchten

December 1, 2015 13

Therapeutic market analysis

• Prescription data

• IMS Smart Solutions (US), MIDAS (global), NPA (US)

• AlphaImpactRx (US)

• Customer perspectives

• KOL calls/surveys; conference feedback

• PBM/managed care (US); NICE/IQWIG assessment (EU)

• Company reports and meetings

• Quarterly earnings releases and conference calls

• Analyst meetings; company field trips

Market data

Physician /

payor feedback

Company

perspective

Which data sources do we use?

Source: Barclays Research

December 1, 2015 14

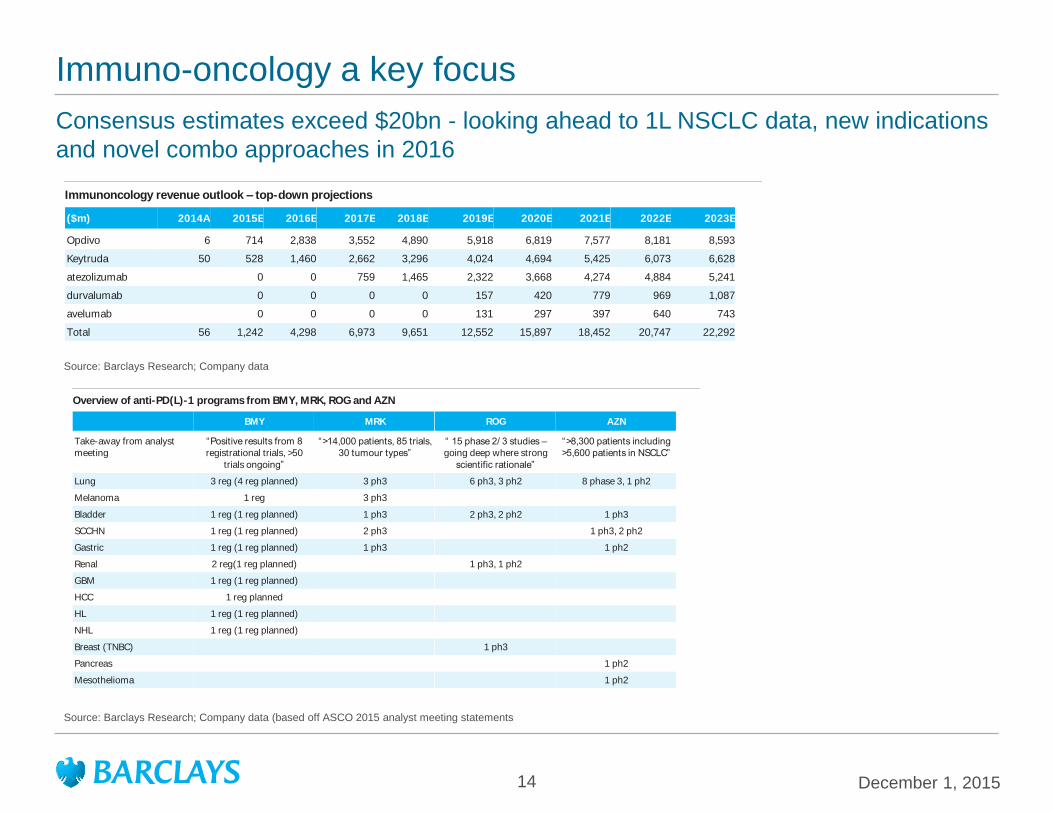

Immuno-oncology a key focus

Consensus estimates exceed $20bn - looking ahead to 1L NSCLC data, new indications

and novel combo approaches in 2016

Source: Barclays Research; Company data (based off ASCO 2015 analyst meeting statements

Overview of anti-PD(L)-1 programs from BMY, MRK, ROG and AZN

BMY MRK ROG AZN

Take-away from analyst

meeting

“Positive results from 8

registrational trials, >50

trials ongoing”

“>14,000 patients, 85 trials,

30 tumour types”

“ 15 phase 2/ 3 studies –

going deep where strong

scientific rationale”

“>8,300 patients including

>5,600 patients in NSCLC”

Lung 3 reg (4 reg planned) 3 ph3 6 ph3, 3 ph2 8 phase 3, 1 ph2

Melanoma 1 reg 3 ph3

Bladder 1 reg (1 reg planned) 1 ph3 2 ph3, 2 ph2 1 ph3

SCCHN 1 reg (1 reg planned) 2 ph3 1 ph3, 2 ph2

Gastric 1 reg (1 reg planned) 1 ph3 1 ph2

Renal 2 reg(1 reg planned) 1 ph3, 1 ph2

GBM 1 reg (1 reg planned)

HCC 1 reg planned

HL 1 reg (1 reg planned)

NHL 1 reg (1 reg planned)

Breast (TNBC) 1 ph3

Pancreas 1 ph2

Mesothelioma 1 ph2

Immunoncology revenue outlook – top-down projections

($m) 2014A 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

Opdivo 6 714 2,838 3,552 4,890 5,918 6,819 7,577 8,181 8,593

Keytruda 50 528 1,460 2,662 3,296 4,024 4,694 5,425 6,073 6,628

atezolizumab 0 0 759 1,465 2,322 3,668 4,274 4,884 5,241

durvalumab 0 0 0 0 157 420 779 969 1,087

avelumab 0 0 0 0 131 297 397 640 743

Total 56 1,242 4,298 6,973 9,651 12,552 15,897 18,452 20,747 22,292

Source: Barclays Research; Company data

December 1, 2015 15

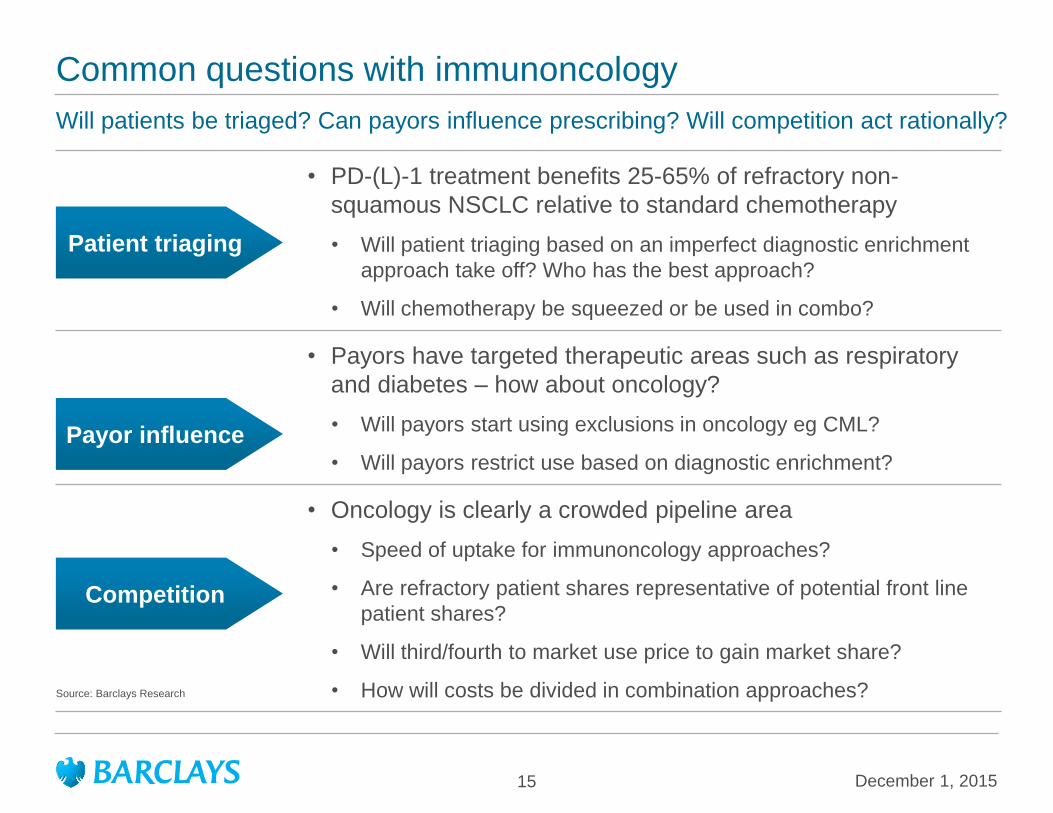

Common questions with immunoncology

• PD-(L)-1 treatment benefits 25-65% of refractory non-

squamous NSCLC relative to standard chemotherapy

• Will patient triaging based on an imperfect diagnostic enrichment

approach take off? Who has the best approach?

• Will chemotherapy be squeezed or be used in combo?

• Payors have targeted therapeutic areas such as respiratory

and diabetes – how about oncology?

• Will payors start using exclusions in oncology eg CML?

• Will payors restrict use based on diagnostic enrichment?

• Oncology is clearly a crowded pipeline area

• Speed of uptake for immunoncology approaches?

• Are refractory patient shares representative of potential front line

patient shares?

• Will third/fourth to market use price to gain market share?

• How will costs be divided in combination approaches?

Patient triaging

Payor influence

Competition

Will patients be triaged? Can payors influence prescribing? Will competition act rationally?

Source: Barclays Research

Comparative Testing Rates for PD-L1 and Established Biomarkers in mNSCLC and mM

Source: Barclays Research; BrandImpact / BrandImpactDx ;

December 1, 2015 16

December 1, 2015 17

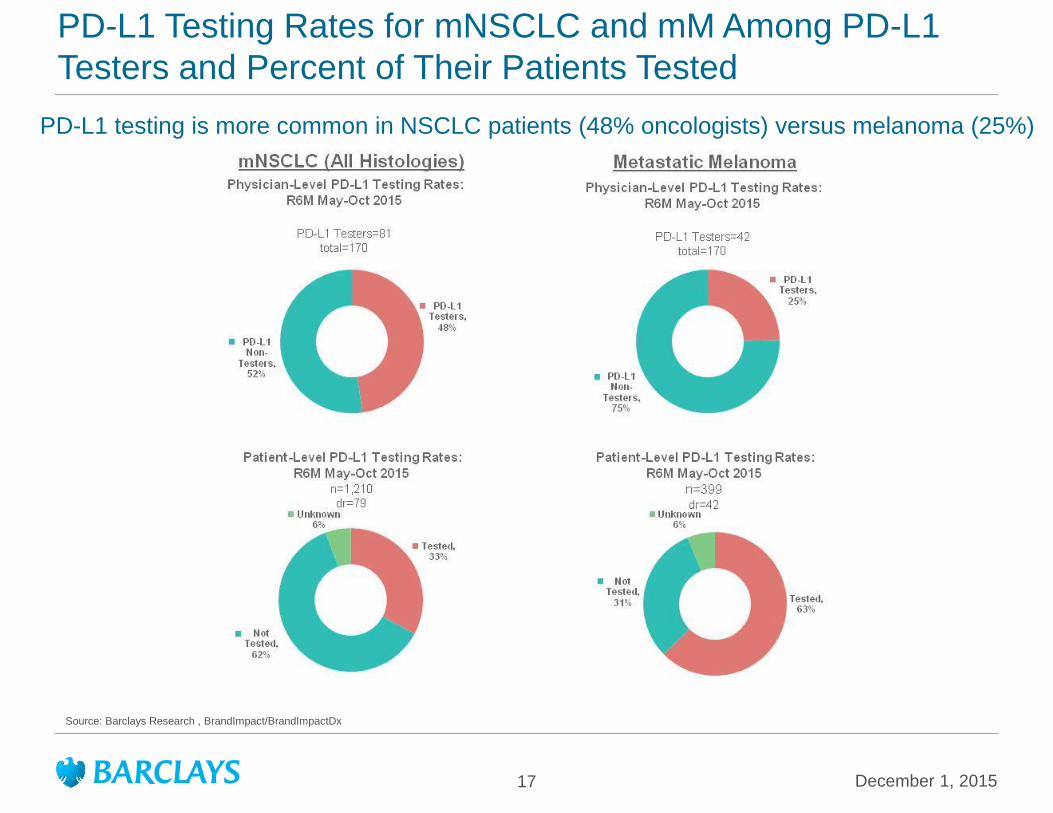

PD-L1 Testing Rates for mNSCLC and mM Among PD-L1

Testers and Percent of Their Patients Tested

Source: Barclays Research , BrandImpact/BrandImpactDx

PD-L1 testing is more common in NSCLC patients (48% oncologists) versus melanoma (25%)

Lung cancer

December 1, 2015 18

December 1, 2015 19

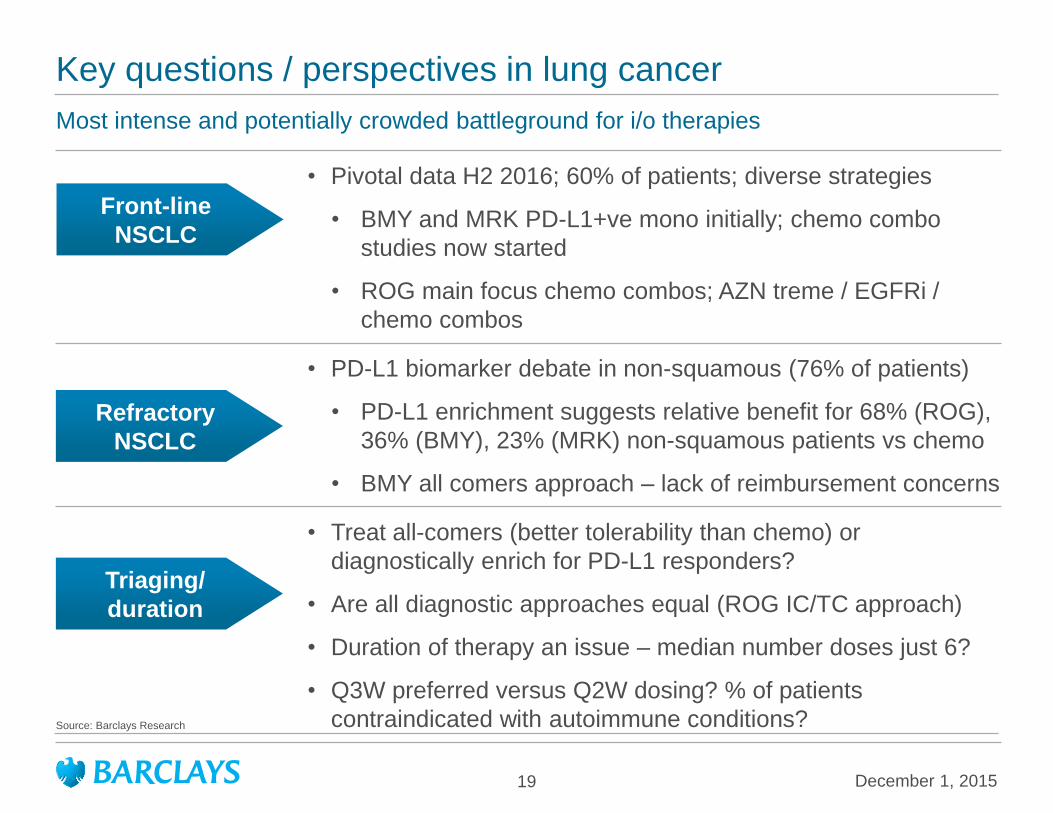

Key questions / perspectives in lung cancer

• Pivotal data H2 2016; 60% of patients; diverse strategies

• BMY and MRK PD-L1+ve mono initially; chemo combo

studies now started

• ROG main focus chemo combos; AZN treme / EGFRi /

chemo combos

• PD-L1 biomarker debate in non-squamous (76% of patients)

• PD-L1 enrichment suggests relative benefit for 68% (ROG),

36% (BMY), 23% (MRK) non-squamous patients vs chemo

• BMY all comers approach – lack of reimbursement concerns

• Treat all-comers (better tolerability than chemo) or

diagnostically enrich for PD-L1 responders?

• Are all diagnostic approaches equal (ROG IC/TC approach)

• Duration of therapy an issue – median number doses just 6?

• Q3W preferred versus Q2W dosing? % of patients

contraindicated with autoimmune conditions?

Front-line

NSCLC

Refractory

NSCLC

Triaging/

duration

Most intense and potentially crowded battleground for i/o therapies

Source: Barclays Research

NSCLC Market Shares Based on PD-L1 Status (squamous)

December 1, 2015 20

Opdivo treated patients – 46% untested, 33% PD-L1 –ve, 20% PD-L1 +ve

Keytruda – approved for PD-L1 +ve patients only

Only 20% of PD-L1 testing occurs in the 2L+ setting

PD-L1 Positive: R6M May-Oct 2015 n=217

dr=28

PD-L1 Negative/Other: R6M May-Oct 2015 n=517

dr=70

Untested Patients: R6M May-Oct 2015 n=757

dr=99

PD-L1 Tested Patients Untested Patients

Keytruda, 1%

Tarceva, 1%

Cyramza, 1%

Opdivo, 49%

Abraxane, 10%

Other Chemo,

35%

Untreated, 4%

Tarceva, 1% Cyramza,

2%

Opdivo, 32%

Abraxane, 13%

Other Chemo,

39%

Untreated, 11%

Tarceva, 2% Cyramza,

1%

Opdivo, 34%

Abraxane, 15%

Other Chemo,

39%

Untreated, 9%

Overall mNSCLC Shares (R6M Through October 2015)

Source: Barclays Research , AlphaImpactRx

Report Definition: (n = number of Patient Visits diagnosed and receiving systemic therapy; dr = number of physicians

reporting,

based on a sample of 170 oncologists, of whom 81(43%) have tested for PD-L1 in some patients).

“Other Chemo’ includes Gemzar, Navelbine, Taxol, and Taxotere. Results may vary from 100% due to rounding.

“PD-L1 Negative/Other” includes patients where the results are negative, pending or inconclusive.

Overall shares include all patients, treated and untreated, and excludes patients on maintenance therapy.

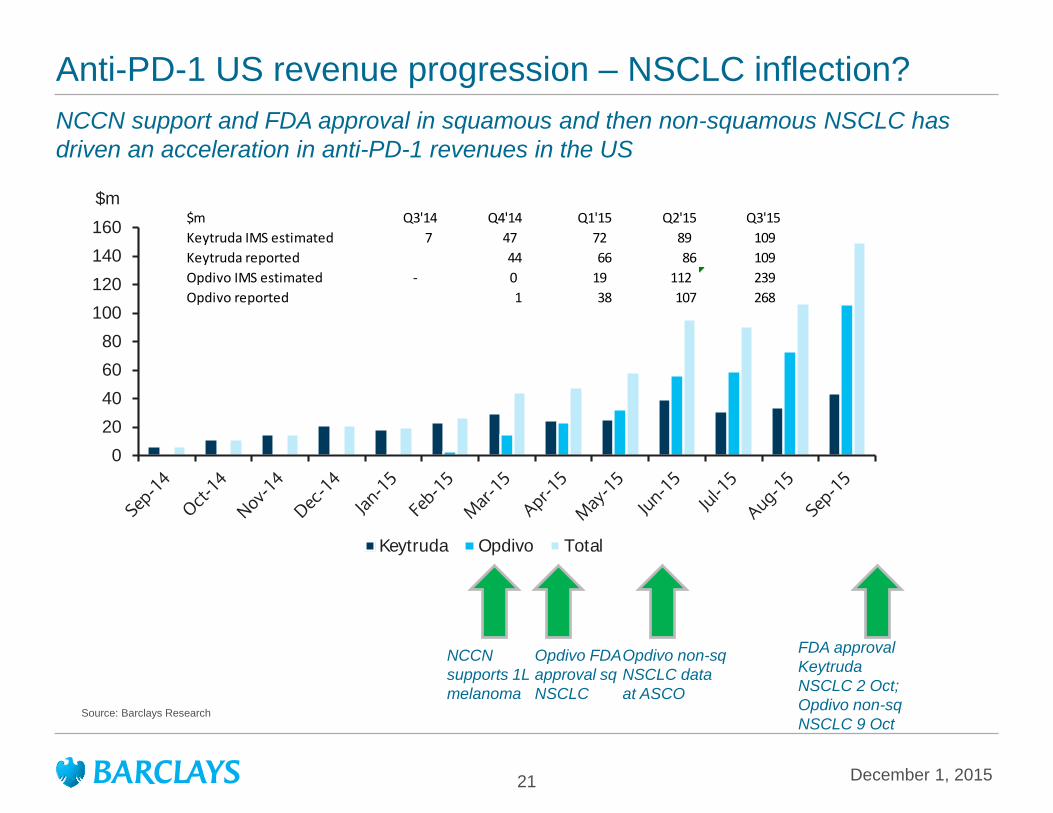

Anti-PD-1 US revenue progression – NSCLC inflection?

December 1, 2015 21

NCCN support and FDA approval in squamous and then non-squamous NSCLC has

driven an acceleration in anti-PD-1 revenues in the US

Source: Barclays Research

NCCN

supports 1L

melanoma

Opdivo FDA

approval sq

NSCLC

0

20

40

60

80

100

120

140

160

$m

Keytruda Opdivo Total

FDA approval

Keytruda

NSCLC 2 Oct;

Opdivo non-sq

NSCLC 9 Oct

$m Q3'14 Q4'14 Q1'15 Q2'15 Q3'15

Keytruda IMS estimated 7 47 72 89 109

Keytruda reported 44 66 86 109

Opdivo IMS estimated - 0 19 112 239

Opdivo reported 1 38 107 268

Opdivo non-sq

NSCLC data

at ASCO

December 1, 2015 22

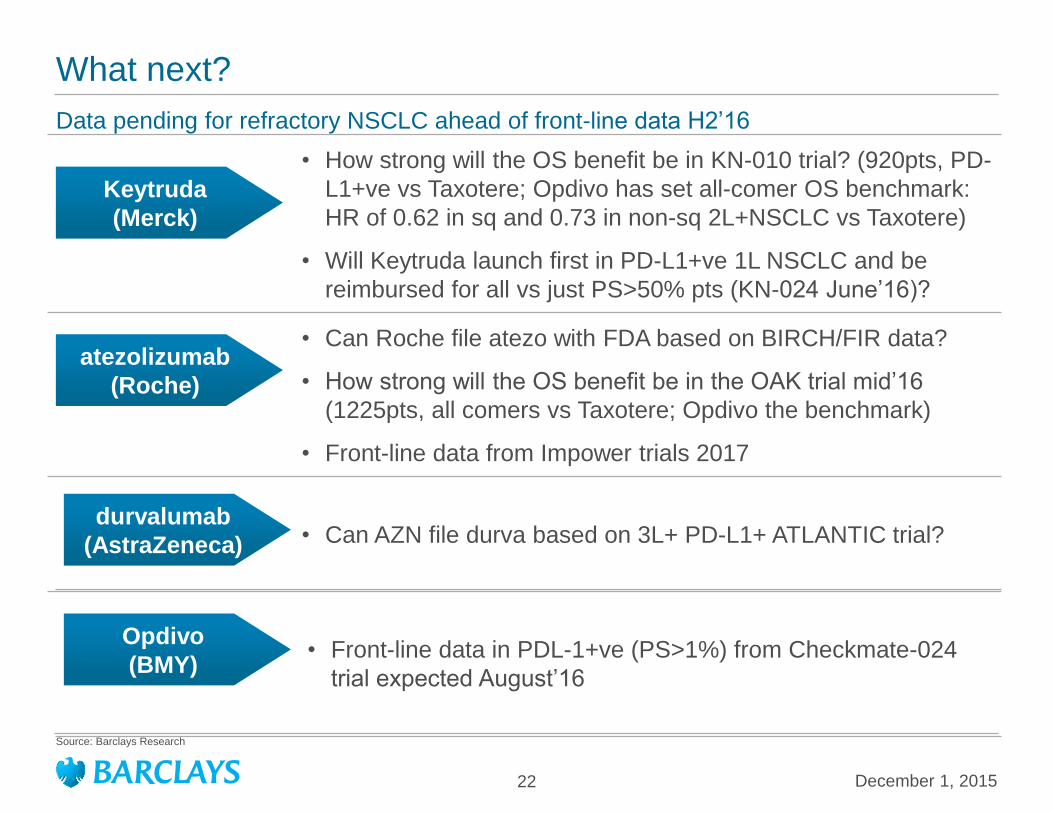

What next?

• How strong will the OS benefit be in KN-010 trial? (920pts, PD-

L1+ve vs Taxotere; Opdivo has set all-comer OS benchmark:

HR of 0.62 in sq and 0.73 in non-sq 2L+NSCLC vs Taxotere)

• Will Keytruda launch first in PD-L1+ve 1L NSCLC and be

reimbursed for all vs just PS>50% pts (KN-024 June’16)?

• Can Roche file atezo with FDA based on BIRCH/FIR data?

• How strong will the OS benefit be in the OAK trial mid’16

(1225pts, all comers vs Taxotere; Opdivo the benchmark)

• Front-line data from Impower trials 2017

• Can AZN file durva based on 3L+ PD-L1+ ATLANTIC trial?

Keytruda

(Merck)

atezolizumab

(Roche)

durvalumab

(AstraZeneca)

Data pending for refractory NSCLC ahead of front-line data H2’16

Source: Barclays Research

• Front-line data in PDL-1+ve (PS>1%) from Checkmate-024

trial expected August’16

Opdivo

(BMY)

December 1, 2015 23

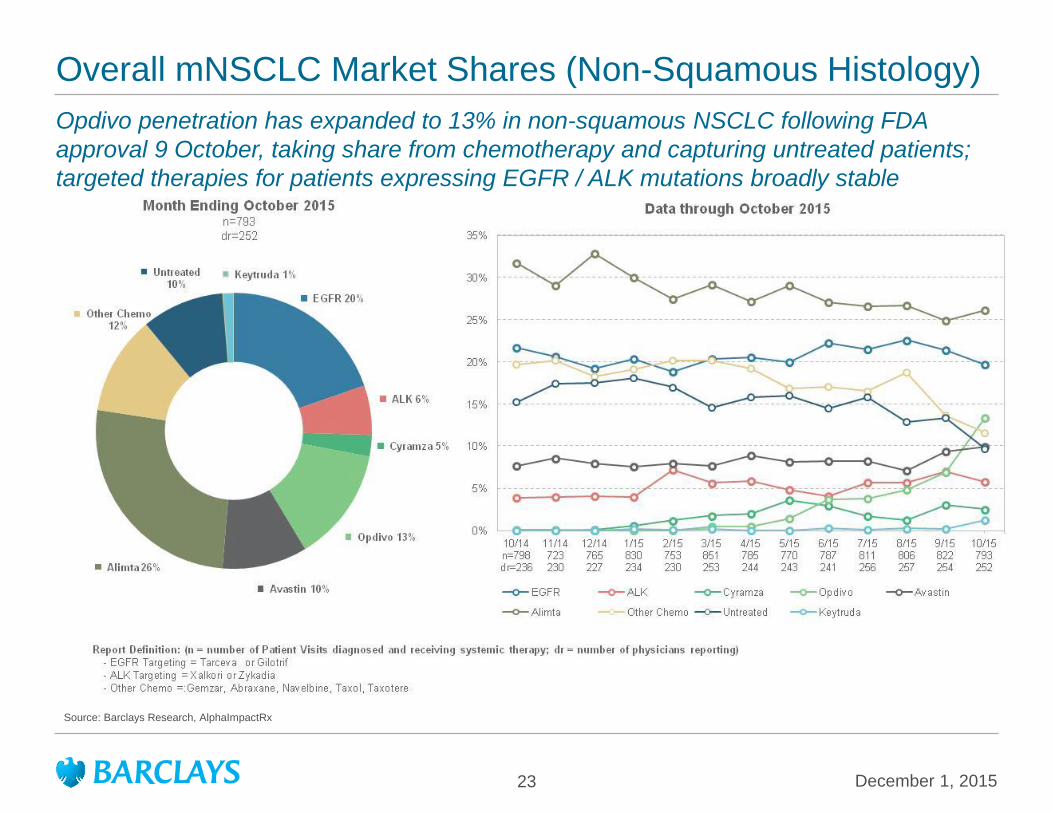

Overall mNSCLC Market Shares (Non-Squamous Histology)

Opdivo penetration has expanded to 13% in non-squamous NSCLC following FDA

approval 9 October, taking share from chemotherapy and capturing untreated patients;

targeted therapies for patients expressing EGFR / ALK mutations broadly stable

Source: Barclays Research, AlphaImpactRx

December 1, 2015 24

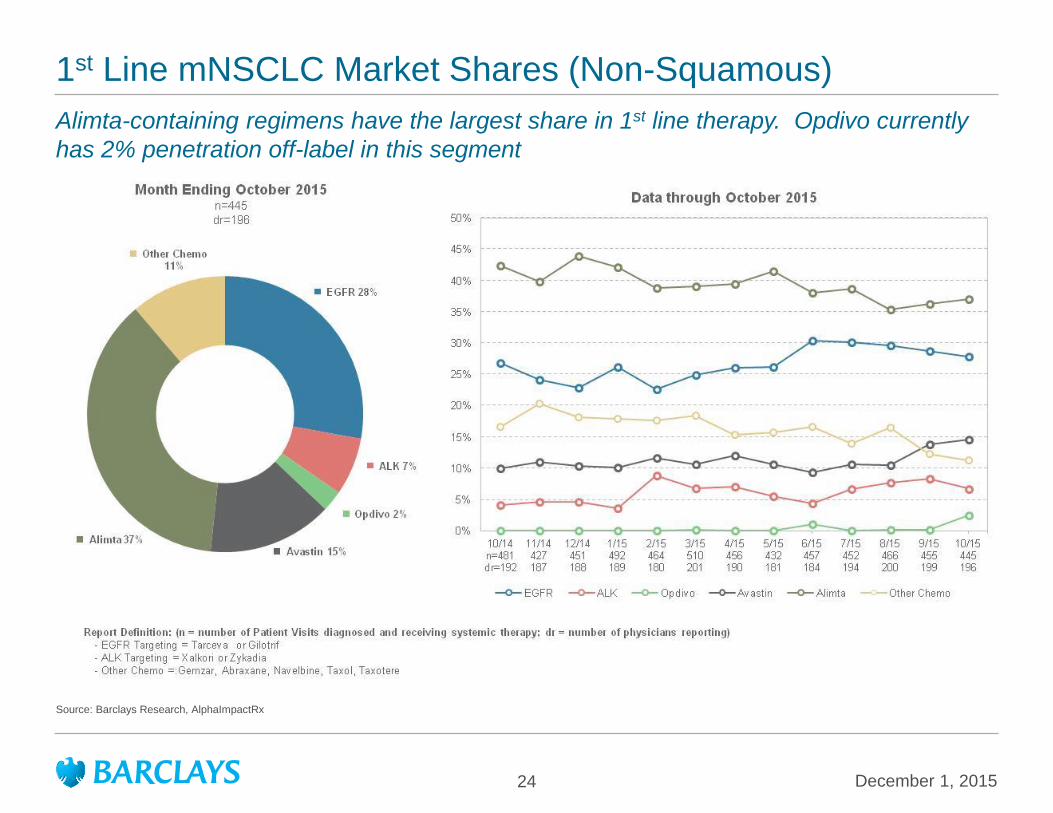

1st Line mNSCLC Market Shares (Non-Squamous)

Alimta-containing regimens have the largest share in 1st line therapy. Opdivo currently

has 2% penetration off-label in this segment

Source: Barclays Research, AlphaImpactRx

December 1, 2015 25

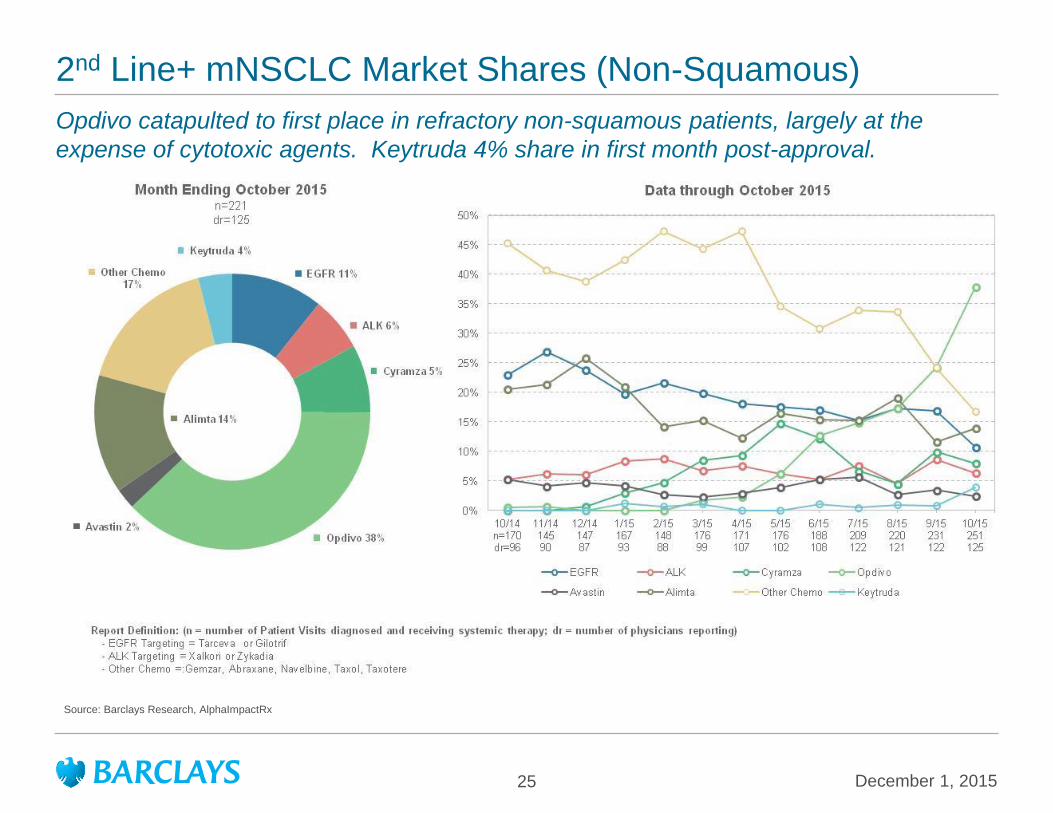

2nd Line+ mNSCLC Market Shares (Non-Squamous)

Opdivo catapulted to first place in refractory non-squamous patients, largely at the

expense of cytotoxic agents. Keytruda 4% share in first month post-approval.

Source: Barclays Research, AlphaImpactRx

December 1, 2015 26

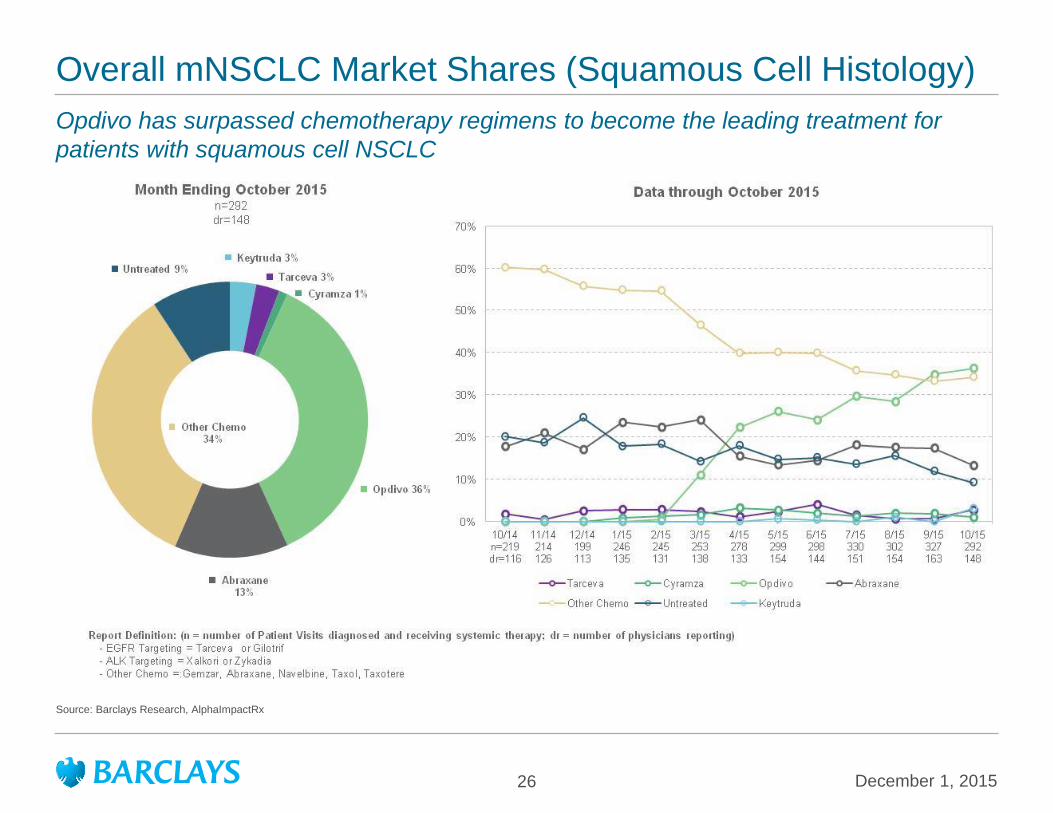

Overall mNSCLC Market Shares (Squamous Cell Histology)

Opdivo has surpassed chemotherapy regimens to become the leading treatment for

patients with squamous cell NSCLC

Source: Barclays Research, AlphaImpactRx

December 1, 2015 27

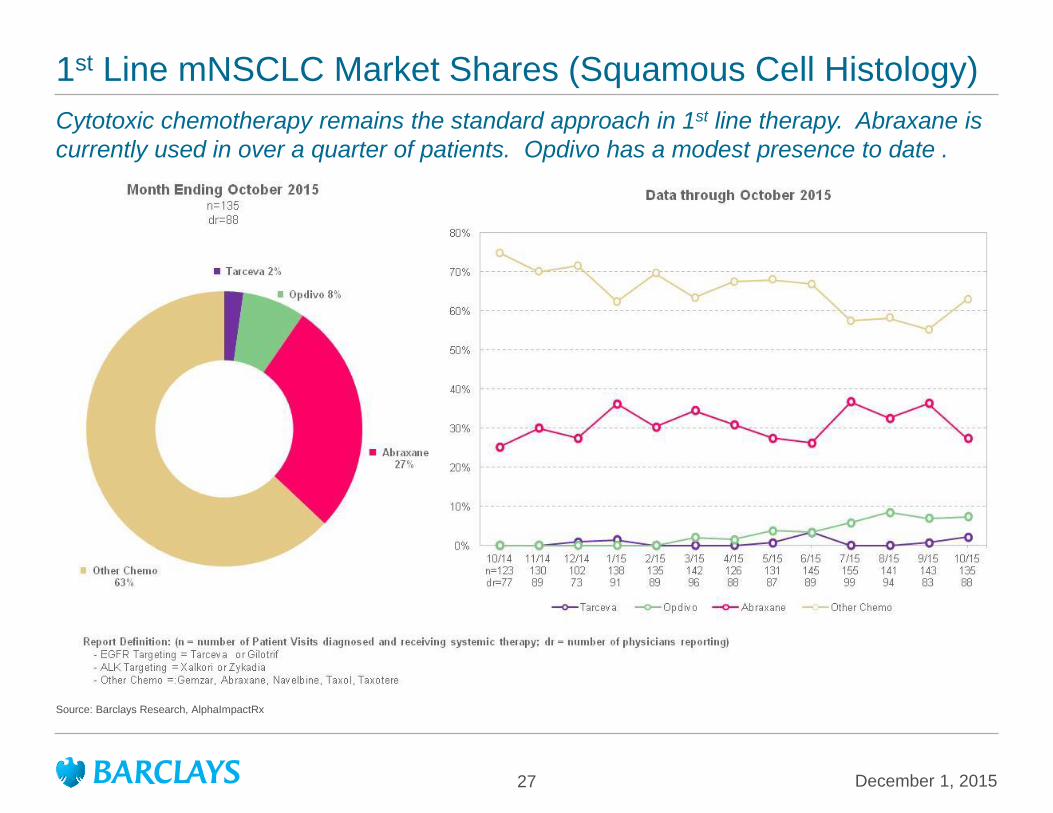

1st Line mNSCLC Market Shares (Squamous Cell Histology)

Cytotoxic chemotherapy remains the standard approach in 1st line therapy. Abraxane is

currently used in over a quarter of patients. Opdivo has a modest presence to date .

Source: Barclays Research, AlphaImpactRx

December 1, 2015 28

2nd Line+ mNSCLC Market Shares (Squamous Cell Histology)

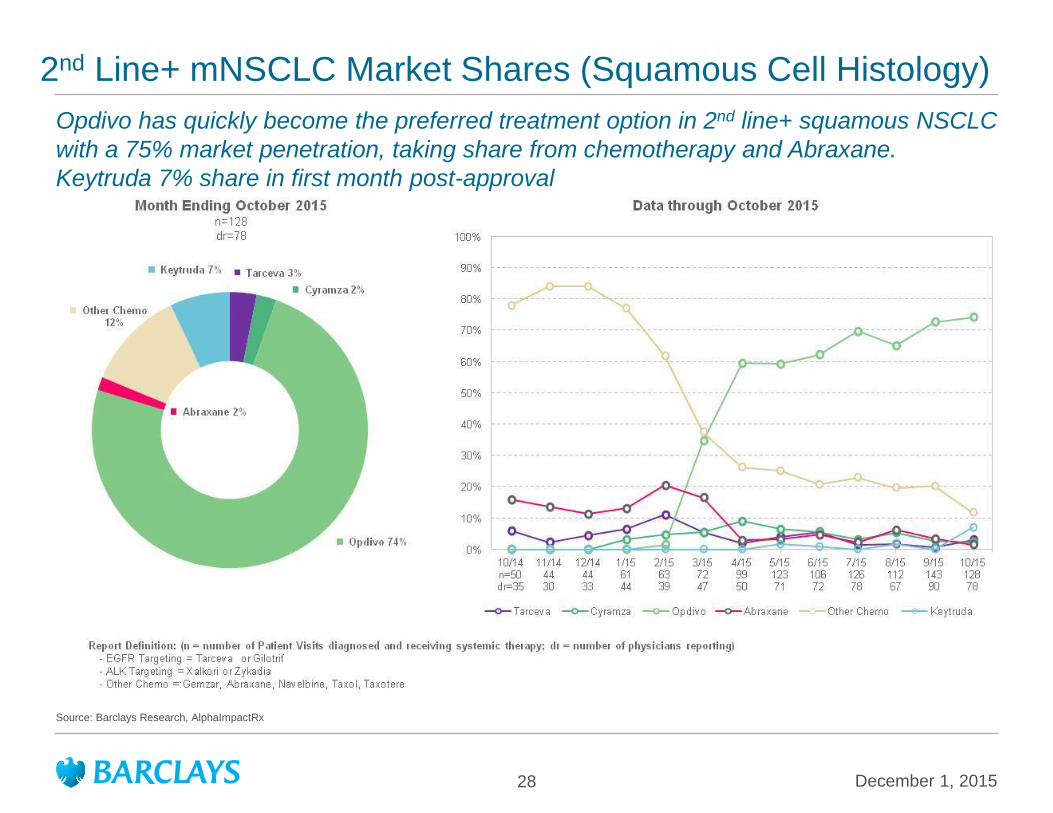

Opdivo has quickly become the preferred treatment option in 2nd line+ squamous NSCLC

with a 75% market penetration, taking share from chemotherapy and Abraxane.

Keytruda 7% share in first month post-approval

Source: Barclays Research, AlphaImpactRx

Melanoma

December 1, 2015 29

December 1, 2015 30

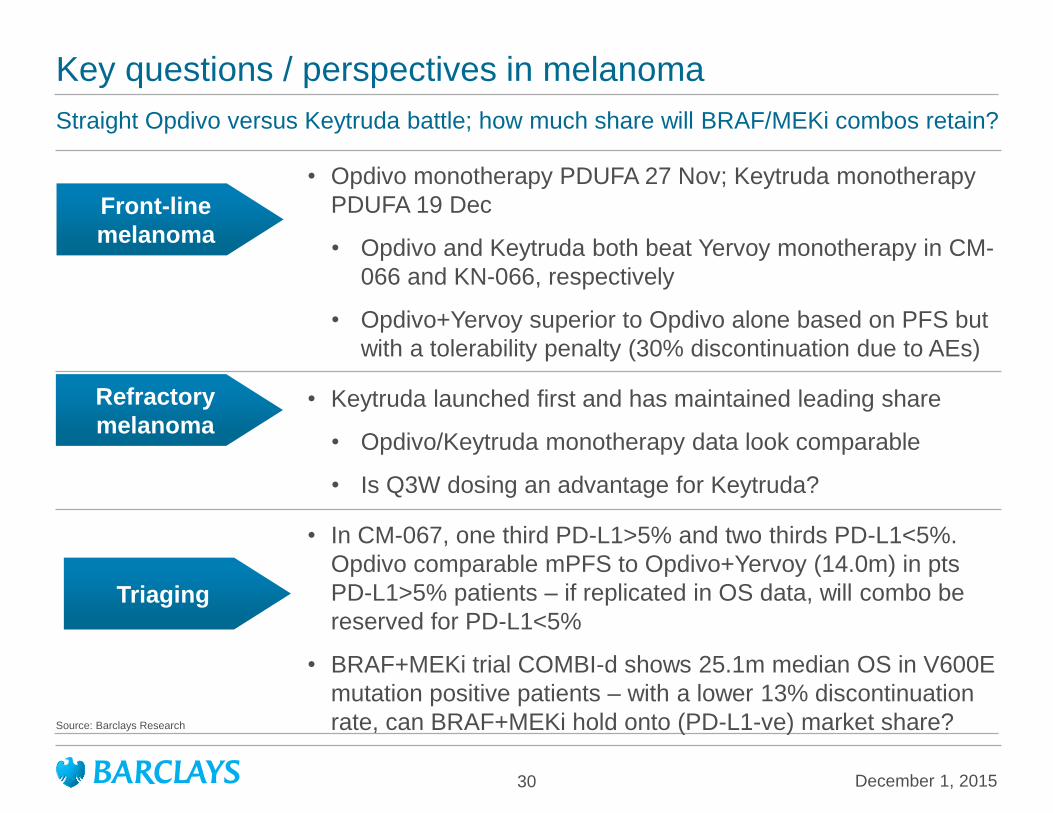

Key questions / perspectives in melanoma

• Opdivo monotherapy PDUFA 27 Nov; Keytruda monotherapy

PDUFA 19 Dec

• Opdivo and Keytruda both beat Yervoy monotherapy in CM-

066 and KN-066, respectively

• Opdivo+Yervoy superior to Opdivo alone based on PFS but

with a tolerability penalty (30% discontinuation due to AEs)

• Keytruda launched first and has maintained leading share

• Opdivo/Keytruda monotherapy data look comparable

• Is Q3W dosing an advantage for Keytruda?

• In CM-067, one third PD-L1>5% and two thirds PD-L1<5%.

Opdivo comparable mPFS to Opdivo+Yervoy (14.0m) in pts

PD-L1>5% patients – if replicated in OS data, will combo be

reserved for PD-L1<5%

• BRAF+MEKi trial COMBI-d shows 25.1m median OS in V600E

mutation positive patients – with a lower 13% discontinuation

rate, can BRAF+MEKi hold onto (PD-L1-ve) market share?

Front-line

melanoma

Refractory

melanoma

Triaging

Straight Opdivo versus Keytruda battle; how much share will BRAF/MEKi combos retain?

Source: Barclays Research

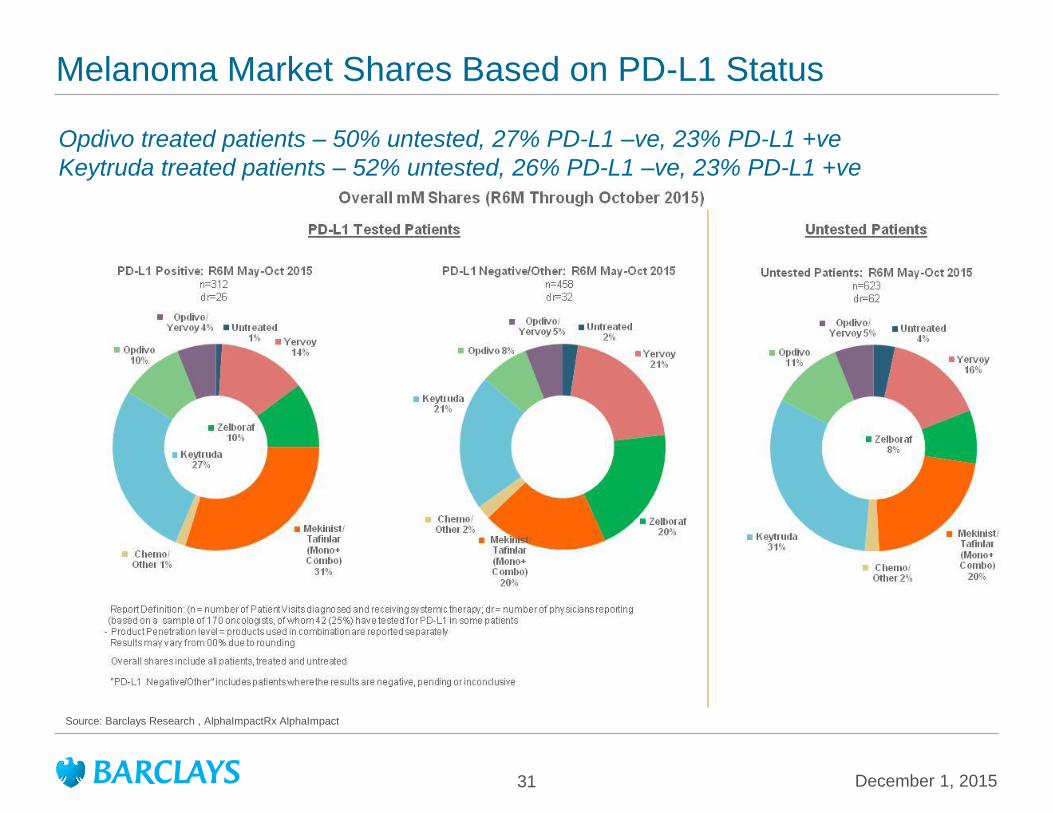

Melanoma Market Shares Based on PD-L1 Status

December 1, 2015 31

Opdivo treated patients – 50% untested, 27% PD-L1 –ve, 23% PD-L1 +ve

Keytruda treated patients – 52% untested, 26% PD-L1 –ve, 23% PD-L1 +ve

Source: Barclays Research , AlphaImpactRx AlphaImpact

December 1, 2015 32

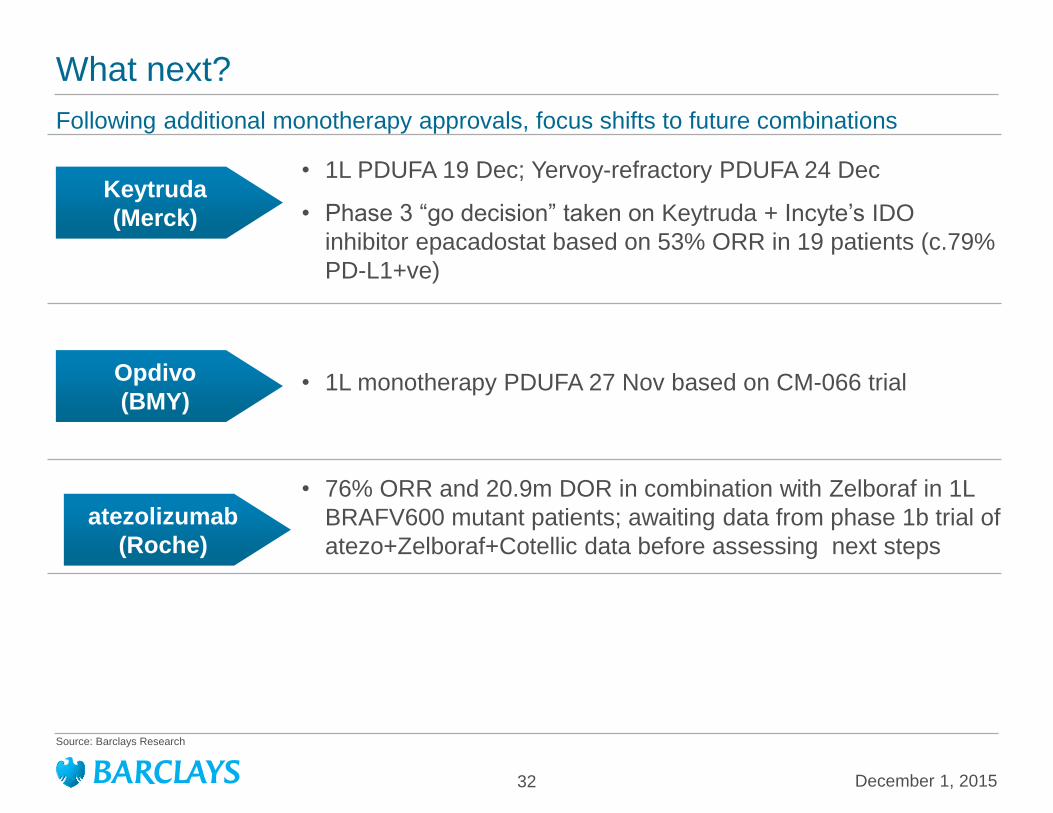

What next?

• 1L PDUFA 19 Dec; Yervoy-refractory PDUFA 24 Dec

• Phase 3 “go decision” taken on Keytruda + Incyte’s IDO

inhibitor epacadostat based on 53% ORR in 19 patients (c.79%

PD-L1+ve)

• 1L monotherapy PDUFA 27 Nov based on CM-066 trial

• 76% ORR and 20.9m DOR in combination with Zelboraf in 1L

BRAFV600 mutant patients; awaiting data from phase 1b trial of

atezo+Zelboraf+Cotellic data before assessing next steps

Keytruda

(Merck)

atezolizumab

(Roche)

Following additional monotherapy approvals, focus shifts to future combinations

Source: Barclays Research

Opdivo

(BMY)

December 1, 2015 33

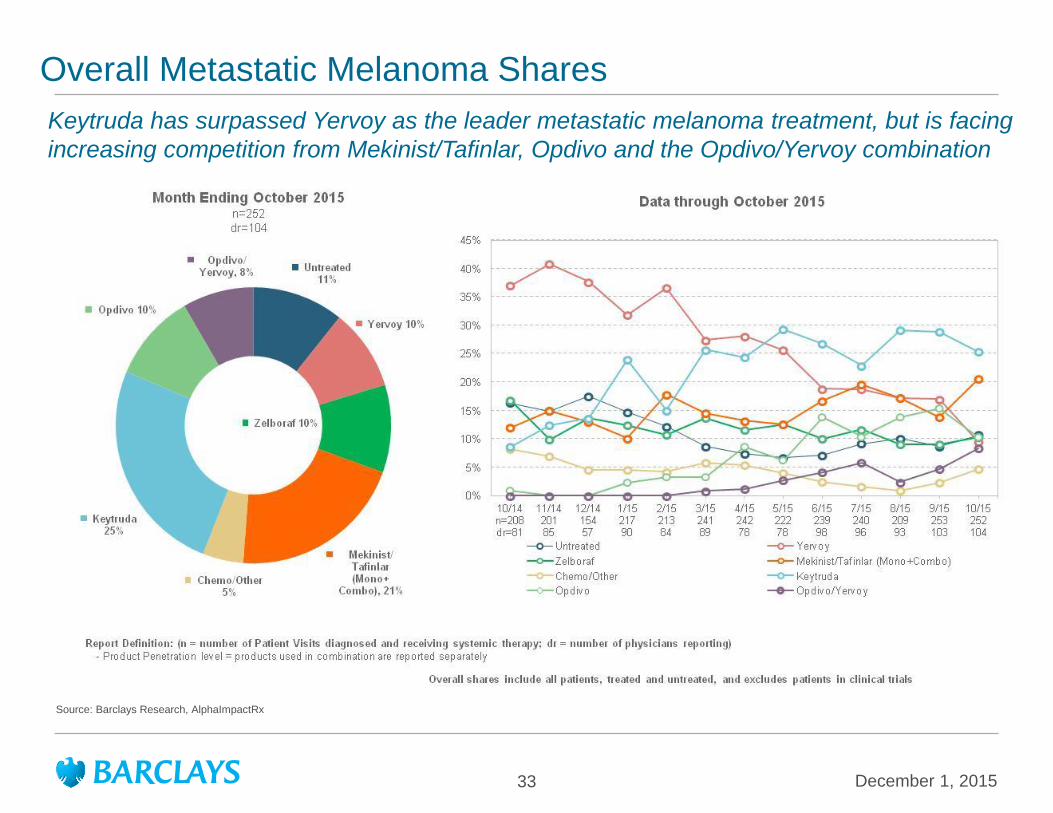

Overall Metastatic Melanoma Shares

Keytruda has surpassed Yervoy as the leader metastatic melanoma treatment, but is facing

increasing competition from Mekinist/Tafinlar, Opdivo and the Opdivo/Yervoy combination

Source: Barclays Research, AlphaImpactRx

December 1, 2015 34

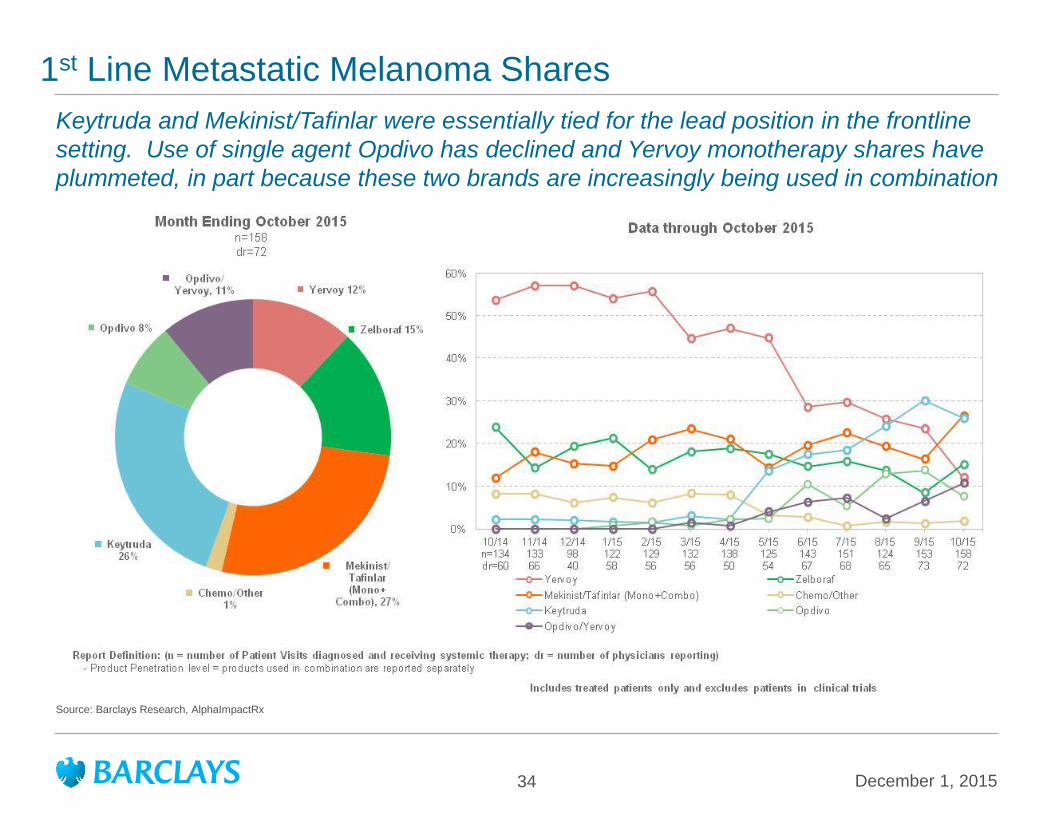

1st Line Metastatic Melanoma Shares

Keytruda and Mekinist/Tafinlar were essentially tied for the lead position in the frontline

setting. Use of single agent Opdivo has declined and Yervoy monotherapy shares have

plummeted, in part because these two brands are increasingly being used in combination

Source: Barclays Research, AlphaImpactRx

December 1, 2015 35

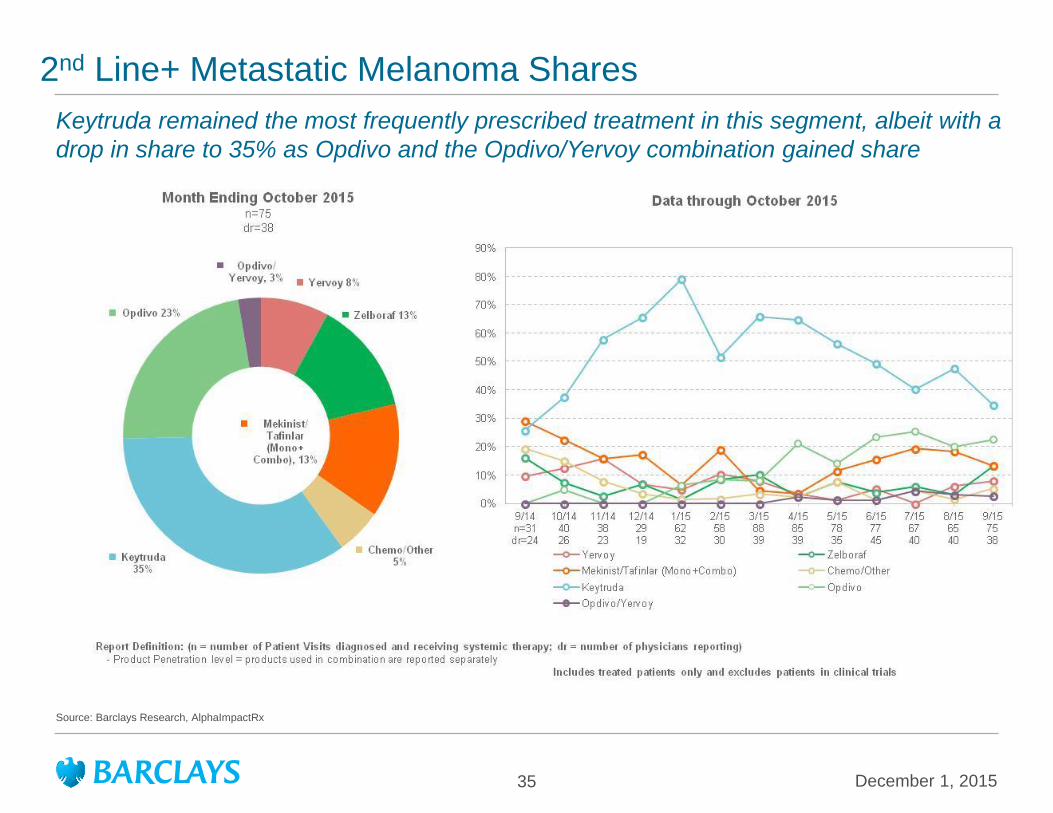

2nd Line+ Metastatic Melanoma Shares

Keytruda remained the most frequently prescribed treatment in this segment, albeit with a

drop in share to 35% as Opdivo and the Opdivo/Yervoy combination gained share

Source: Barclays Research, AlphaImpactRx

December 1, 2015 36

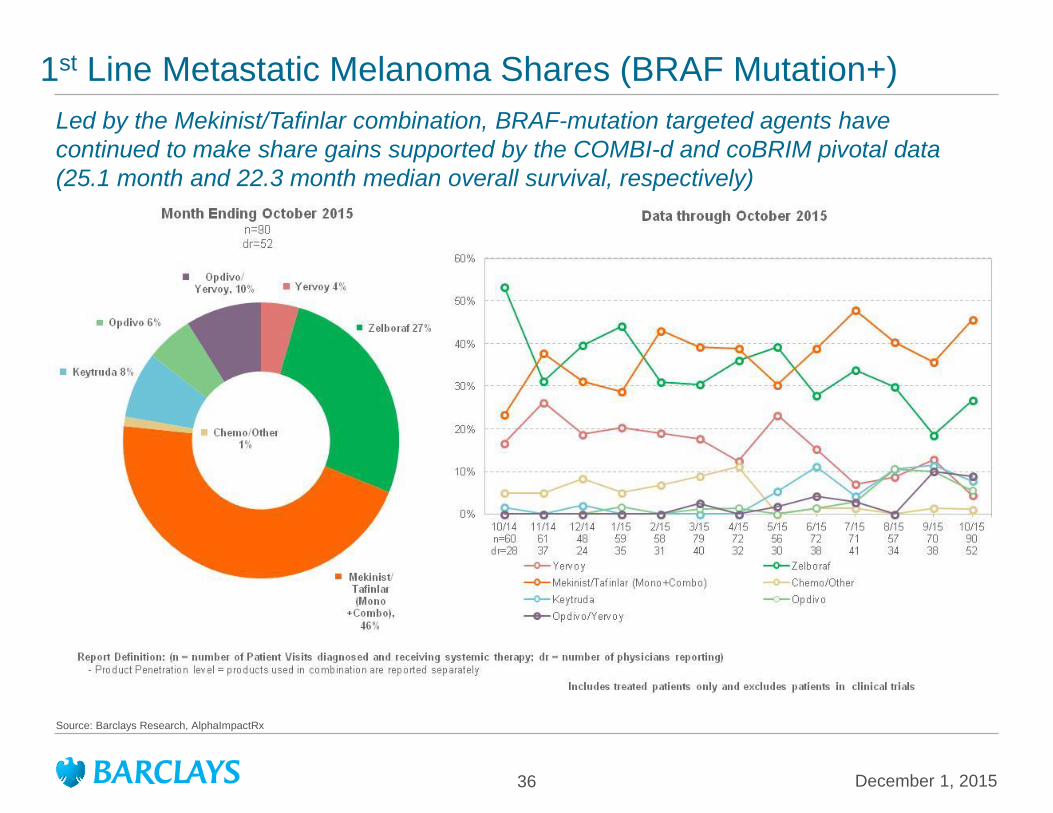

1st Line Metastatic Melanoma Shares (BRAF Mutation+)

Led by the Mekinist/Tafinlar combination, BRAF-mutation targeted agents have

continued to make share gains supported by the COMBI-d and coBRIM pivotal data

(25.1 month and 22.3 month median overall survival, respectively)

Source: Barclays Research, AlphaImpactRx

December 1, 2015 37

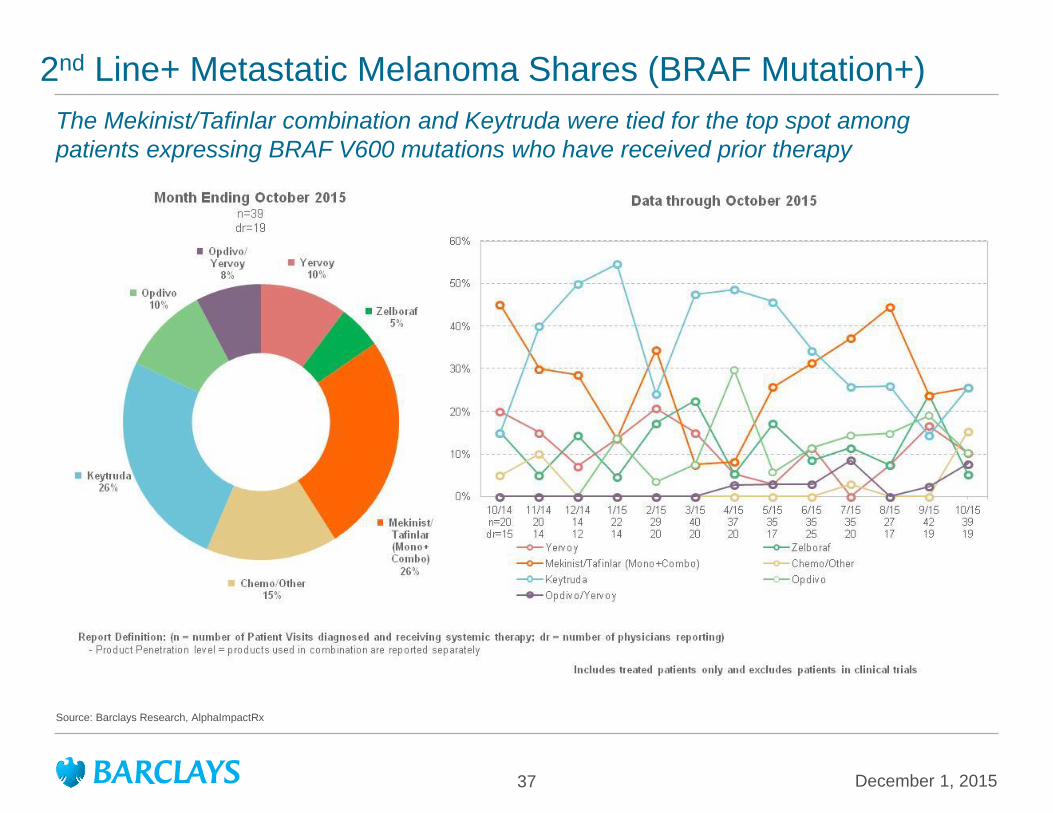

2nd Line+ Metastatic Melanoma Shares (BRAF Mutation+)

The Mekinist/Tafinlar combination and Keytruda were tied for the top spot among

patients expressing BRAF V600 mutations who have received prior therapy

Source: Barclays Research, AlphaImpactRx

Ibrance in breast cancer

December 1, 2015 38

December 1, 2015 39

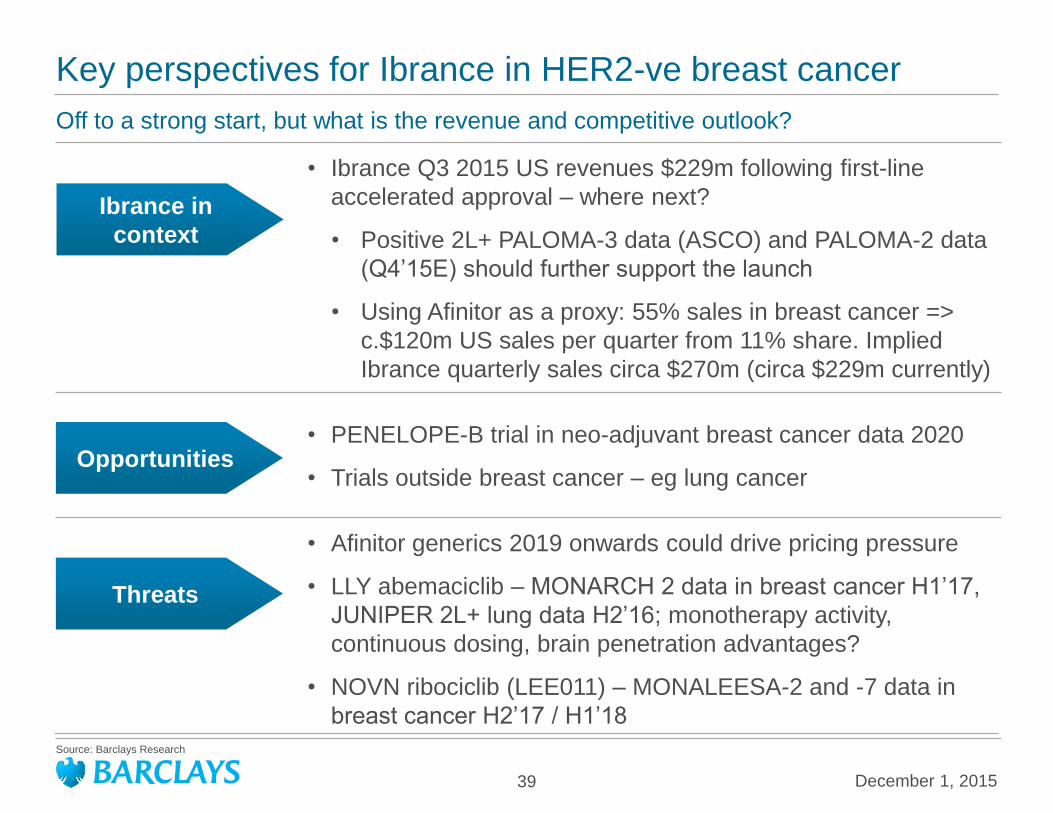

Key perspectives for Ibrance in HER2-ve breast cancer

• Ibrance Q3 2015 US revenues $229m following first-line

accelerated approval – where next?

• Positive 2L+ PALOMA-3 data (ASCO) and PALOMA-2 data

(Q4’15E) should further support the launch

• Using Afinitor as a proxy: 55% sales in breast cancer =>

c.$120m US sales per quarter from 11% share. Implied

Ibrance quarterly sales circa $270m (circa $229m currently)

• PENELOPE-B trial in neo-adjuvant breast cancer data 2020

• Trials outside breast cancer – eg lung cancer

• Afinitor generics 2019 onwards could drive pricing pressure

• LLY abemaciclib – MONARCH 2 data in breast cancer H1’17,

JUNIPER 2L+ lung data H2’16; monotherapy activity,

continuous dosing, brain penetration advantages?

• NOVN ribociclib (LEE011) – MONALEESA-2 and -7 data in

breast cancer H2’17 / H1’18

Ibrance in

context

Opportunities

Threats

Off to a strong start, but what is the revenue and competitive outlook?

Source: Barclays Research

December 1, 2015 40

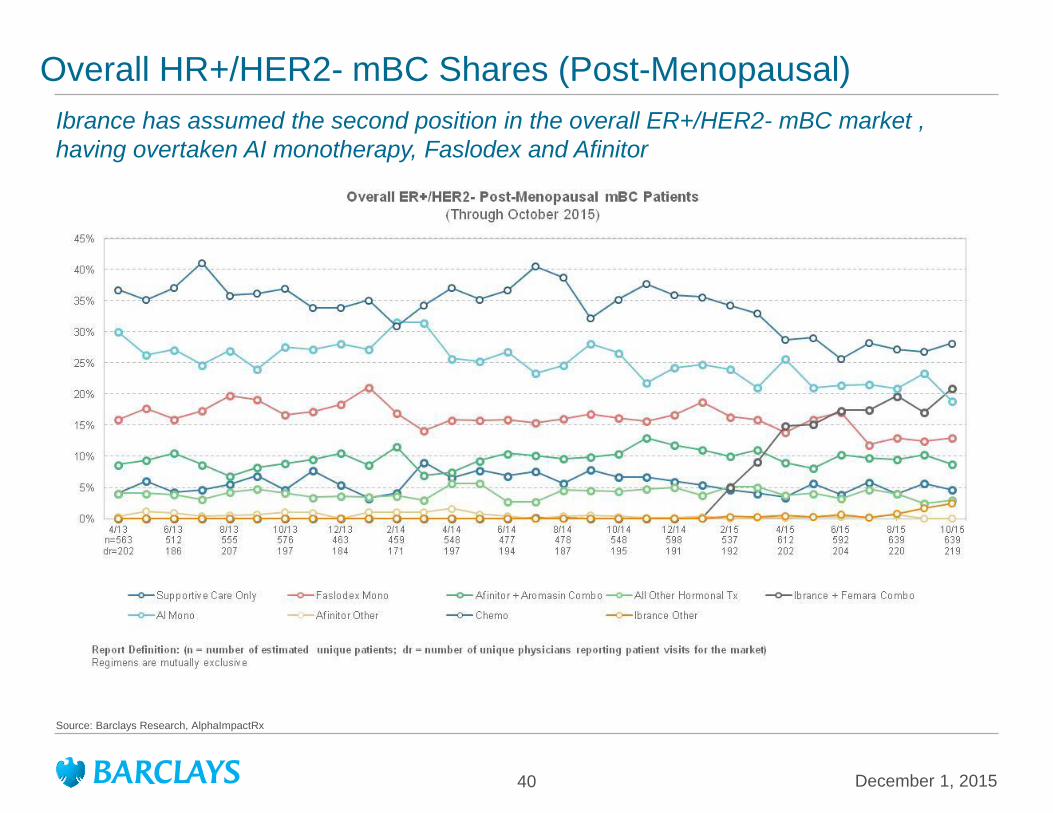

Overall HR+/HER2- mBC Shares (Post-Menopausal)

Ibrance has assumed the second position in the overall ER+/HER2- mBC market ,

having overtaken AI monotherapy, Faslodex and Afinitor

Source: Barclays Research, AlphaImpactRx

December 1, 2015 41

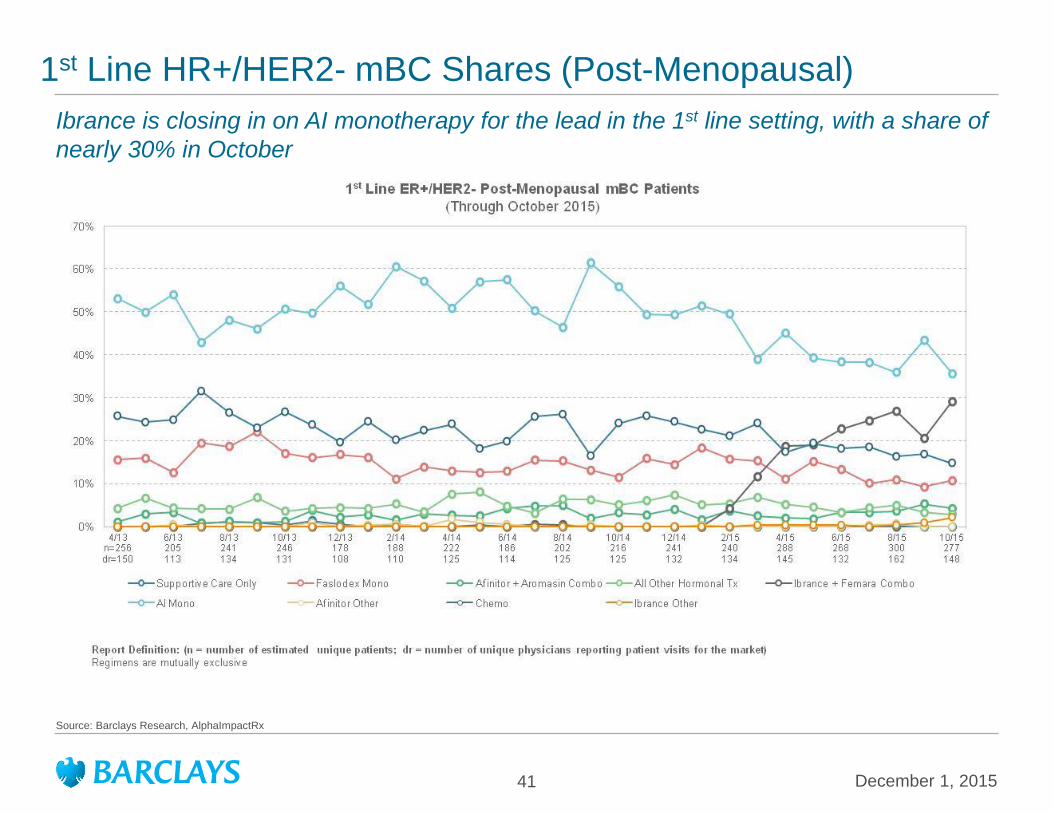

1st Line HR+/HER2- mBC Shares (Post-Menopausal)

Ibrance is closing in on AI monotherapy for the lead in the 1st line setting, with a share of

nearly 30% in October

Source: Barclays Research, AlphaImpactRx

December 1, 2015 42

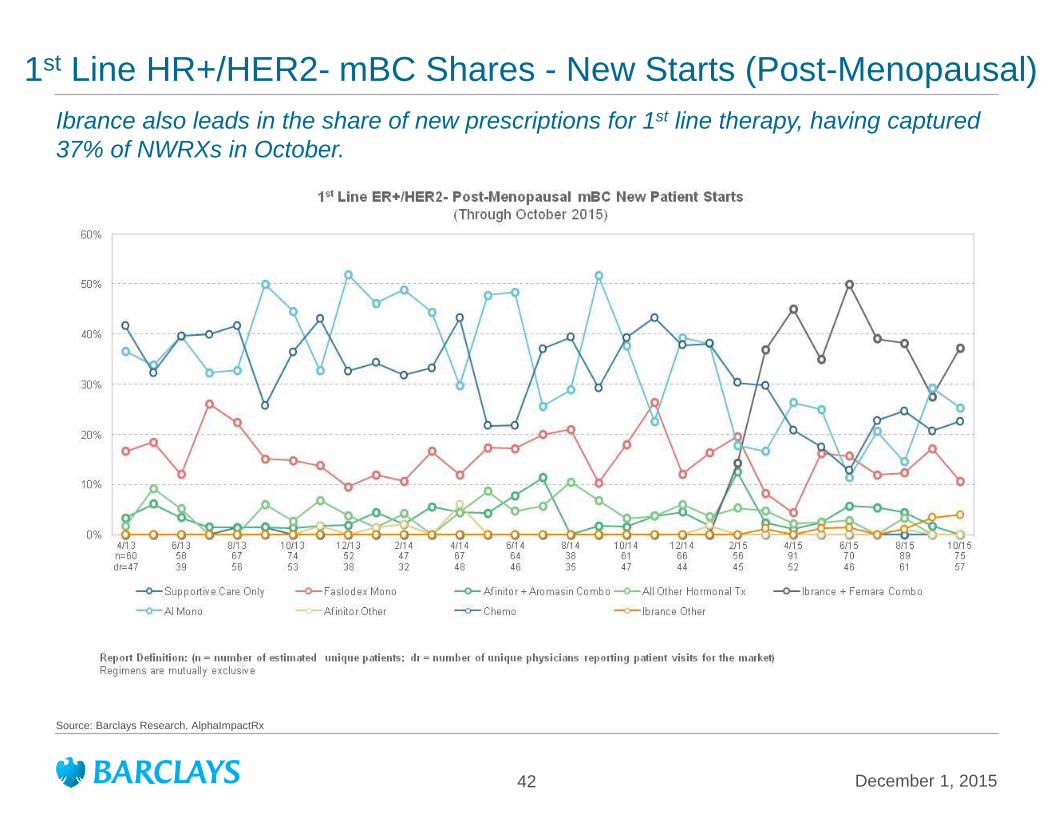

1st Line HR+/HER2- mBC Shares - New Starts (Post-Menopausal)

Ibrance also leads in the share of new prescriptions for 1st line therapy, having captured

37% of NWRXs in October.

Source: Barclays Research, AlphaImpactRx

December 1, 2015 43

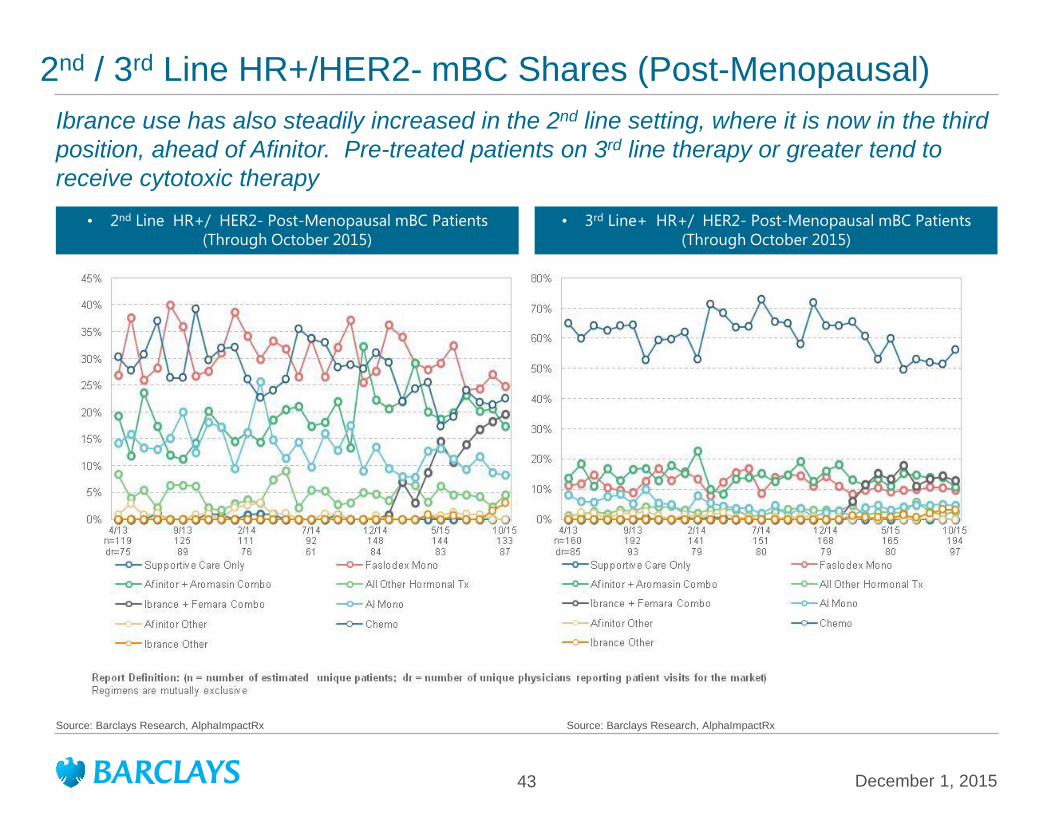

2nd / 3rd Line HR+/HER2- mBC Shares (Post-Menopausal)

Ibrance use has also steadily increased in the 2nd line setting, where it is now in the third

position, ahead of Afinitor. Pre-treated patients on 3rd line therapy or greater tend to

receive cytotoxic therapy

Source: Barclays Research, AlphaImpactRx

Source: Barclays Research, AlphaImpactRx

• 2nd Line HR+/ HER2- Post-Menopausal mBC Patients

(Through October 2015)

• 3rd Line+ HR+/ HER2- Post-Menopausal mBC Patients

(Through October 2015)

Perjeta in breast cancer

December 1, 2015 44

December 1, 2015 45

Protecting Roche’s breast cancer franchise – Perjeta update

• Perjeta and Kadcyla have accelerated revenue growth of

Roche’s HER2 franchise to 19% - however Herceptin remains

68% US / 78% ex-US franchise by value:

• Perjeta penetration >50% on-label (>70% neo-adjuvant)

• Subcutaneous Herceptin >30% conversion

• Kadcyla+Perjeta 1L trial MARIANNE failed

• Perjeta driving Herceptin duration of use

• Perjeta 2L+ PHEREXA trial 2015/16

• Perjeta APHINITY trial H1 2016 (55% of Herceptin use)

• The race against time – Herceptin biosimilars!

• Herceptin COMP 2014 EU (2ndry patents?), 2019 US

• Samsung bioepsis (Jan’16; NA); Amgen ABP-980 (Mar’16;

NA); Celltrion (Dec’16; NA), Pfizer (Oct’16; 1L / Dec’16 NA)

Perjeta in

context

Opportunities

Threats

Off to a strong start, but what is the revenue and competitive outlook?

Source: Barclays Research

December 1, 2015 46

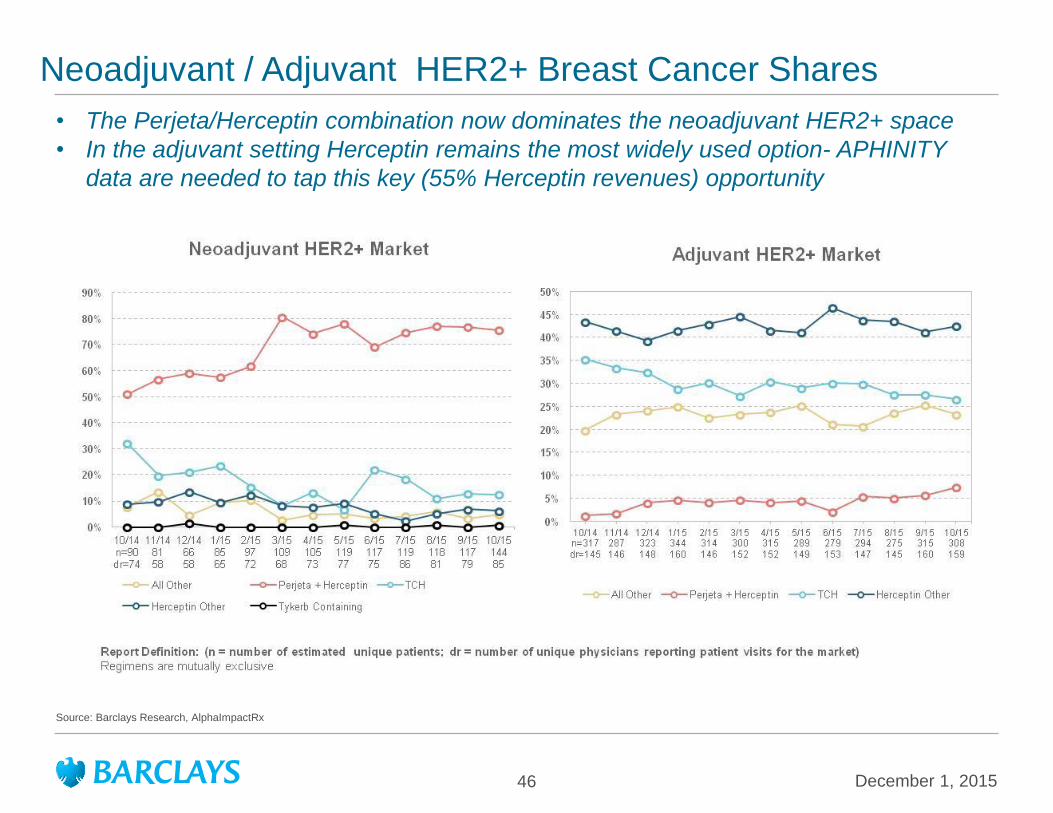

Neoadjuvant / Adjuvant HER2+ Breast Cancer Shares

• The Perjeta/Herceptin combination now dominates the neoadjuvant HER2+ space

• In the adjuvant setting Herceptin remains the most widely used option- APHINITY

data are needed to tap this key (55% Herceptin revenues) opportunity

Source: Barclays Research, AlphaImpactRx

December 1, 2015 47

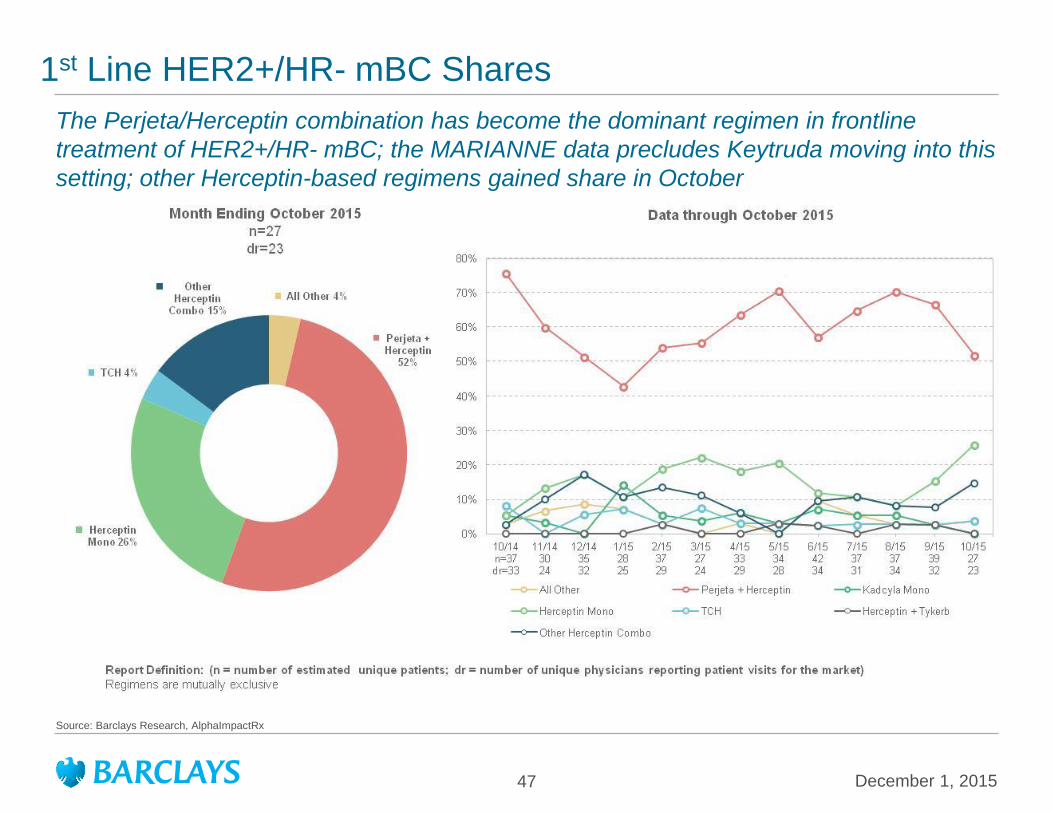

1st Line HER2+/HR- mBC Shares

The Perjeta/Herceptin combination has become the dominant regimen in frontline

treatment of HER2+/HR- mBC; the MARIANNE data precludes Keytruda moving into this

setting; other Herceptin-based regimens gained share in October

Source: Barclays Research, AlphaImpactRx

December 1, 2015 48

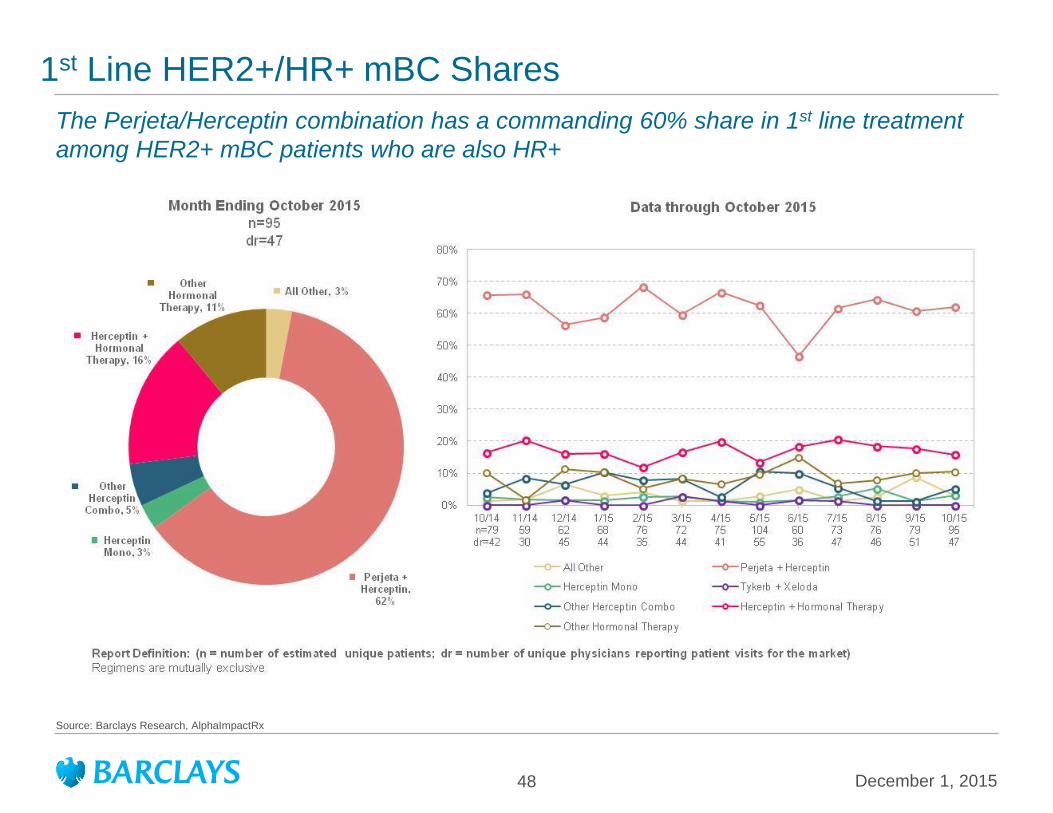

1st Line HER2+/HR+ mBC Shares

The Perjeta/Herceptin combination has a commanding 60% share in 1st line treatment

among HER2+ mBC patients who are also HR+

Source: Barclays Research, AlphaImpactRx

December 1, 2015 49

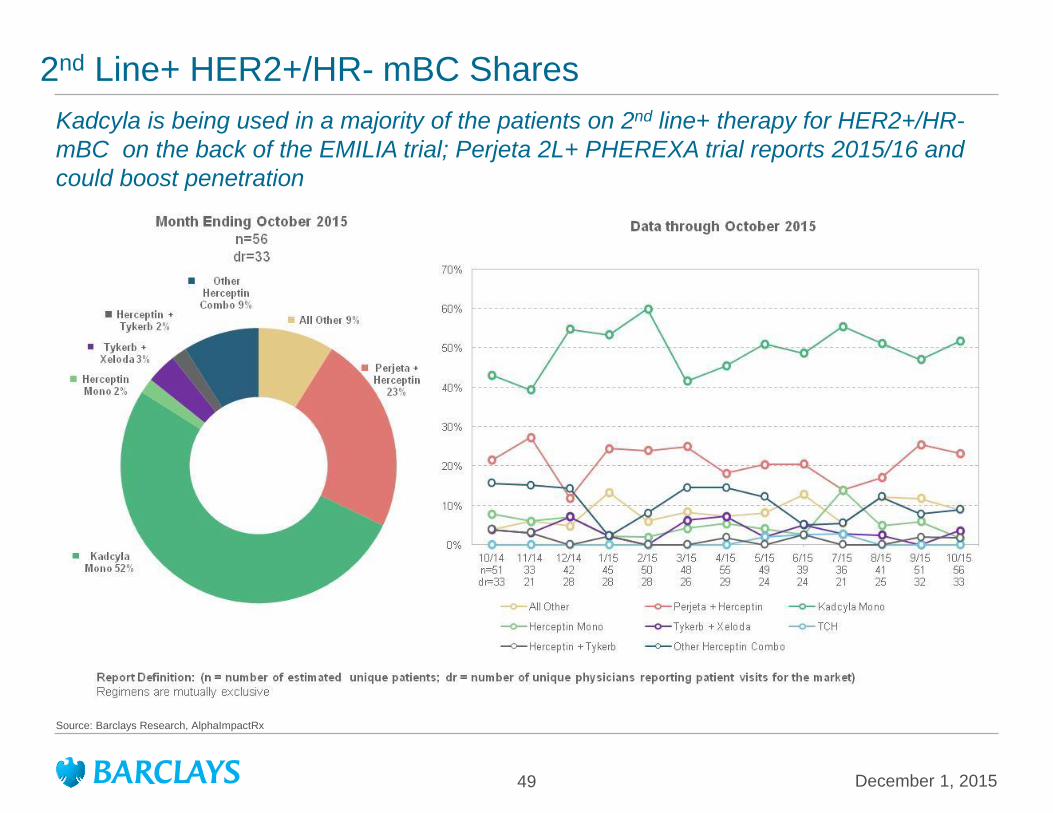

2nd Line+ HER2+/HR- mBC Shares

Kadcyla is being used in a majority of the patients on 2nd line+ therapy for HER2+/HR-

mBC on the back of the EMILIA trial; Perjeta 2L+ PHEREXA trial reports 2015/16 and

could boost penetration

Source: Barclays Research, AlphaImpactRx

December 1, 2015 50

2nd Line+ HER2+/HR+ mBC Shares

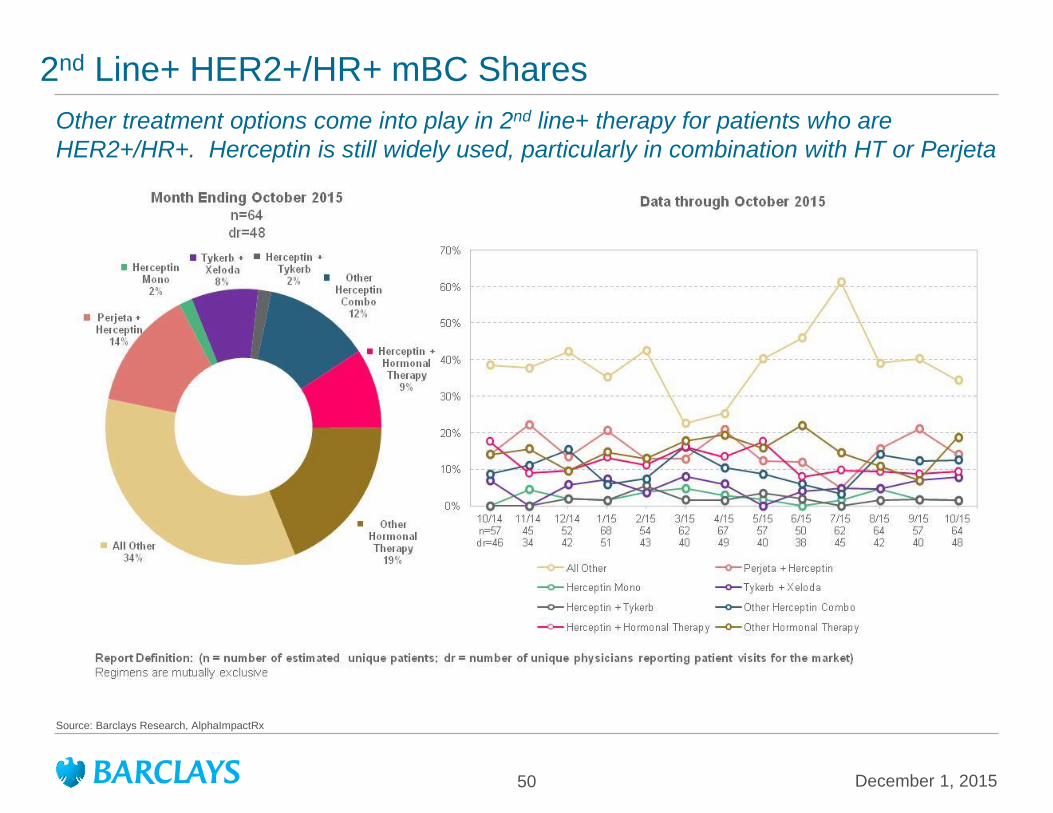

Other treatment options come into play in 2nd line+ therapy for patients who are

HER2+/HR+. Herceptin is still widely used, particularly in combination with HT or Perjeta

Source: Barclays Research, AlphaImpactRx

Imbruvica in CLL

December 1, 2015 51

December 1, 2015 52

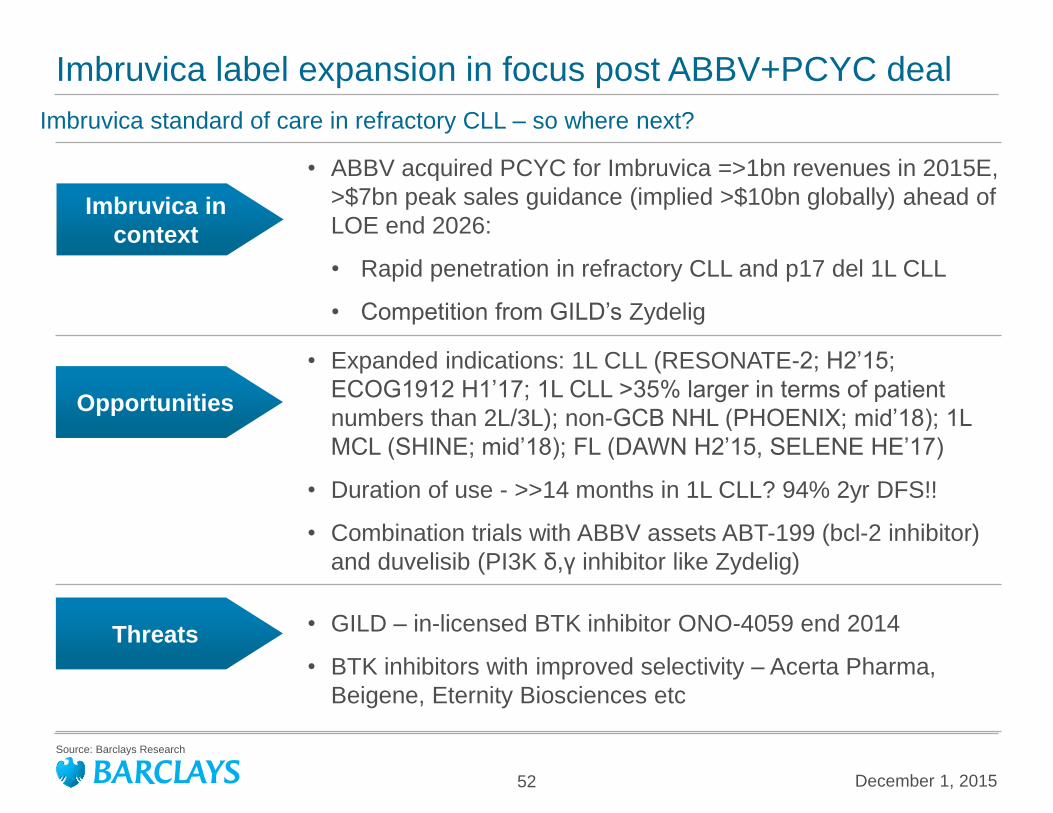

Imbruvica label expansion in focus post ABBV+PCYC deal

• ABBV acquired PCYC for Imbruvica =>1bn revenues in 2015E,

>$7bn peak sales guidance (implied >$10bn globally) ahead of

LOE end 2026:

• Rapid penetration in refractory CLL and p17 del 1L CLL

• Competition from GILD’s Zydelig

• Expanded indications: 1L CLL (RESONATE-2; H2’15;

ECOG1912 H1’17; 1L CLL >35% larger in terms of patient

numbers than 2L/3L); non-GCB NHL (PHOENIX; mid’18); 1L

MCL (SHINE; mid’18); FL (DAWN H2’15, SELENE HE’17)

• Duration of use - >>14 months in 1L CLL? 94% 2yr DFS!!

• Combination trials with ABBV assets ABT-199 (bcl-2 inhibitor)

and duvelisib (PI3K δ,γ inhibitor like Zydelig)

• GILD – in-licensed BTK inhibitor ONO-4059 end 2014

• BTK inhibitors with improved selectivity – Acerta Pharma,

Beigene, Eternity Biosciences etc

Imbruvica in

context

Opportunities

Threats

Imbruvica standard of care in refractory CLL – so where next?

Source: Barclays Research

December 1, 2015 53

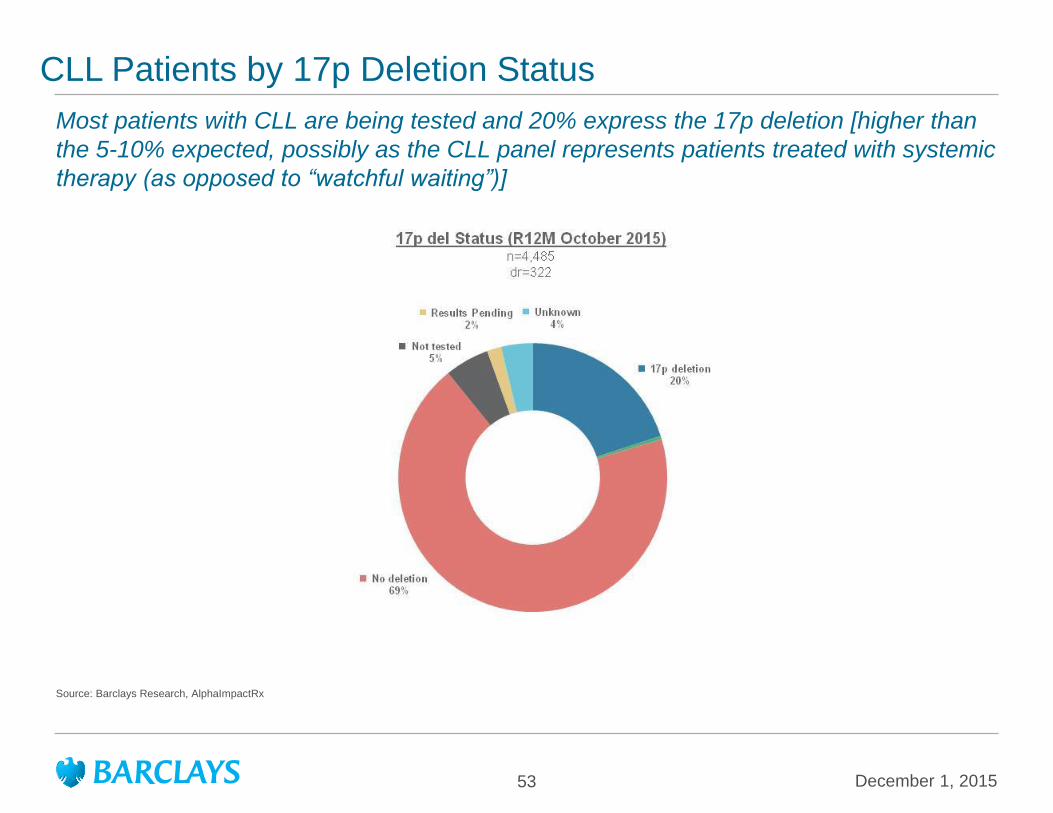

CLL Patients by 17p Deletion Status

Most patients with CLL are being tested and 20% express the 17p deletion [higher than

the 5-10% expected, possibly as the CLL panel represents patients treated with systemic

therapy (as opposed to “watchful waiting”)]

Source: Barclays Research, AlphaImpactRx

December 1, 2015 54

Overall CLL Market Shares

Imbruvica has become the leading therapeutic option within the overall CLL space,

followed in turn by Treanda and Rituxan

Source: Barclays Research, AlphaImpactRx

December 1, 2015 55

CLL Market Shares (1st Line)

Treanda-based treatment held onto the lead position in October, but Imbruvica penetration

continues to rise at the expense of Rituxan-based treatments ahead of RESONATE-2

Source: Barclays Research, AlphaImpactRx

December 1, 2015 56

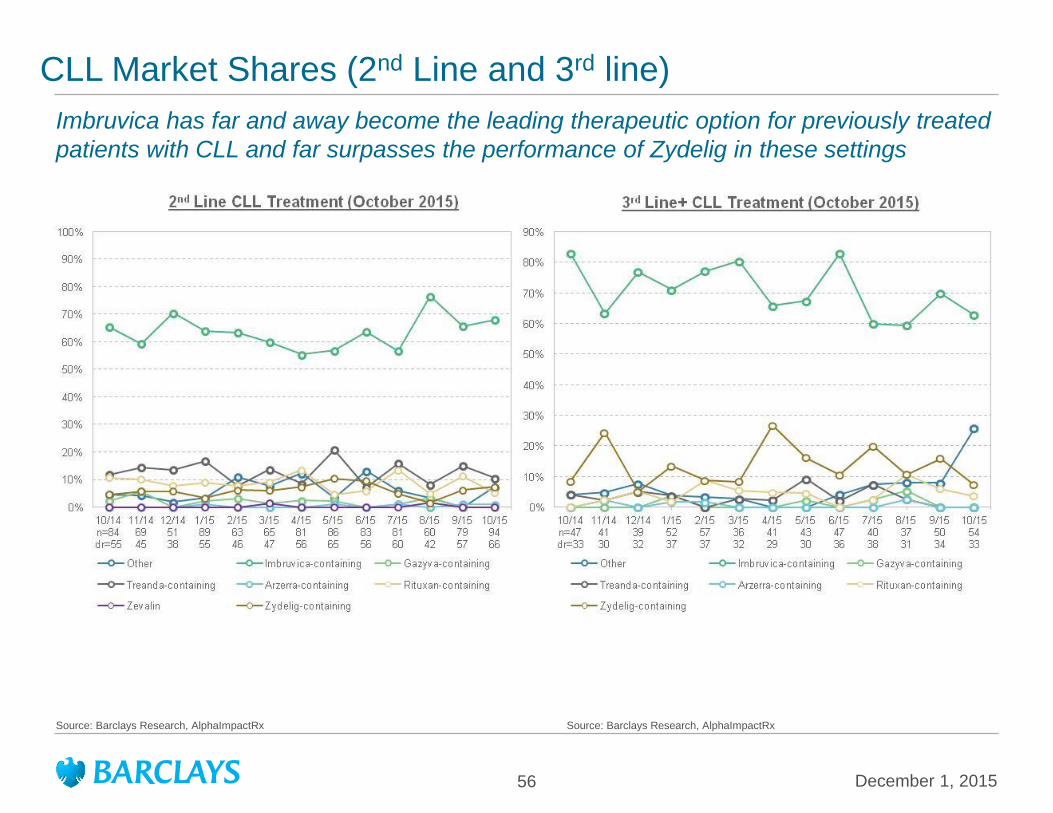

CLL Market Shares (2nd Line and 3rd line)

Imbruvica has far and away become the leading therapeutic option for previously treated

patients with CLL and far surpasses the performance of Zydelig in these settings

Source: Barclays Research, AlphaImpactRx

Source: Barclays Research, AlphaImpactRx

December 1, 2015 57

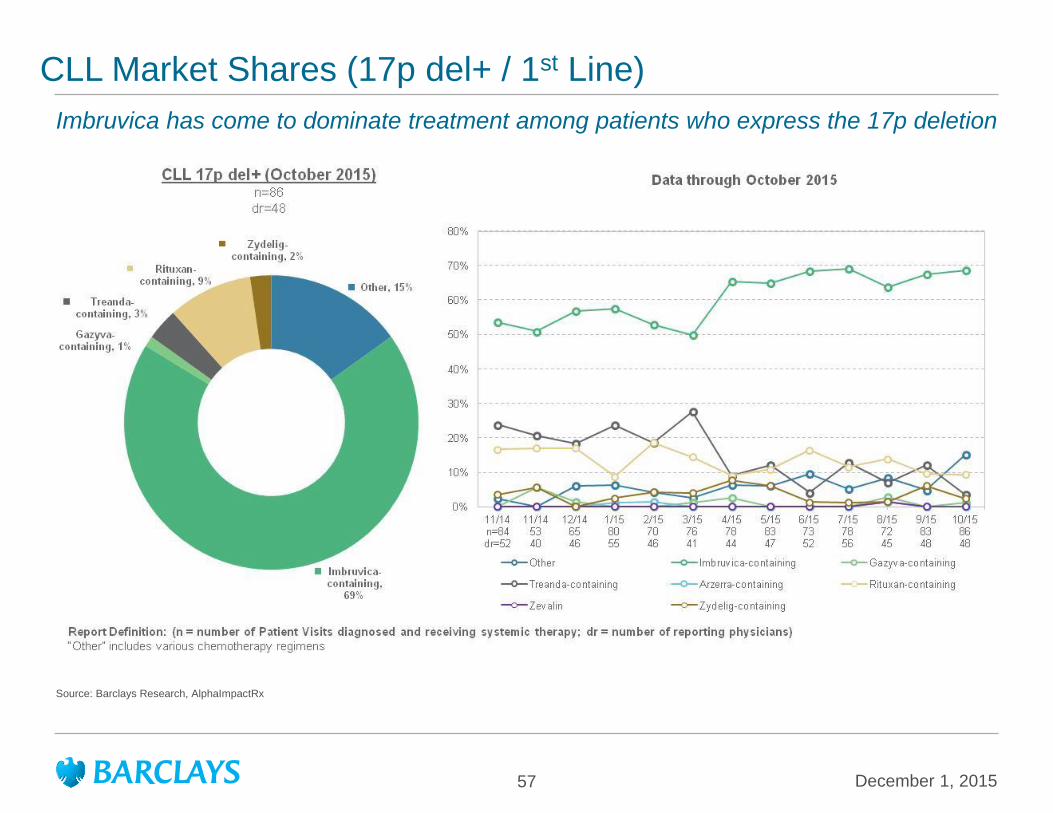

CLL Market Shares (17p del+ / 1st Line)

Imbruvica has come to dominate treatment among patients who express the 17p deletion

Source: Barclays Research, AlphaImpactRx

December 1, 2015 58

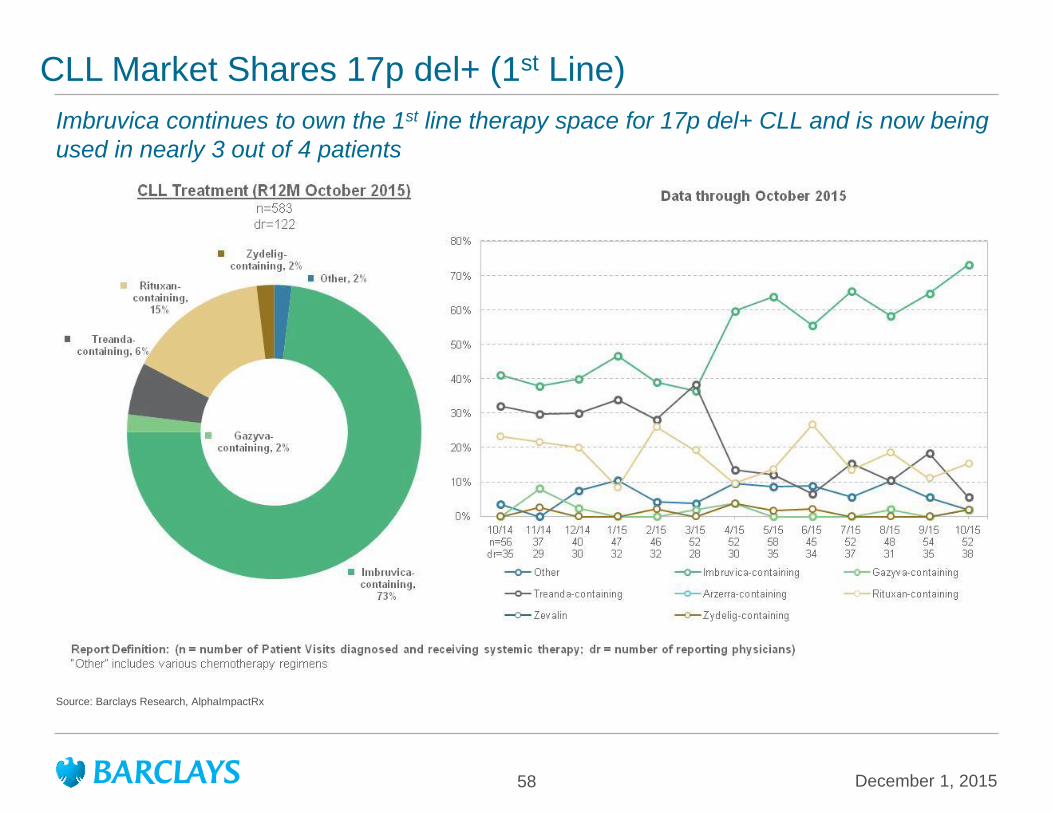

CLL Market Shares 17p del+ (1st Line)

Imbruvica continues to own the 1st line therapy space for 17p del+ CLL and is now being

used in nearly 3 out of 4 patients

Source: Barclays Research, AlphaImpactRx

December 1, 2015 59

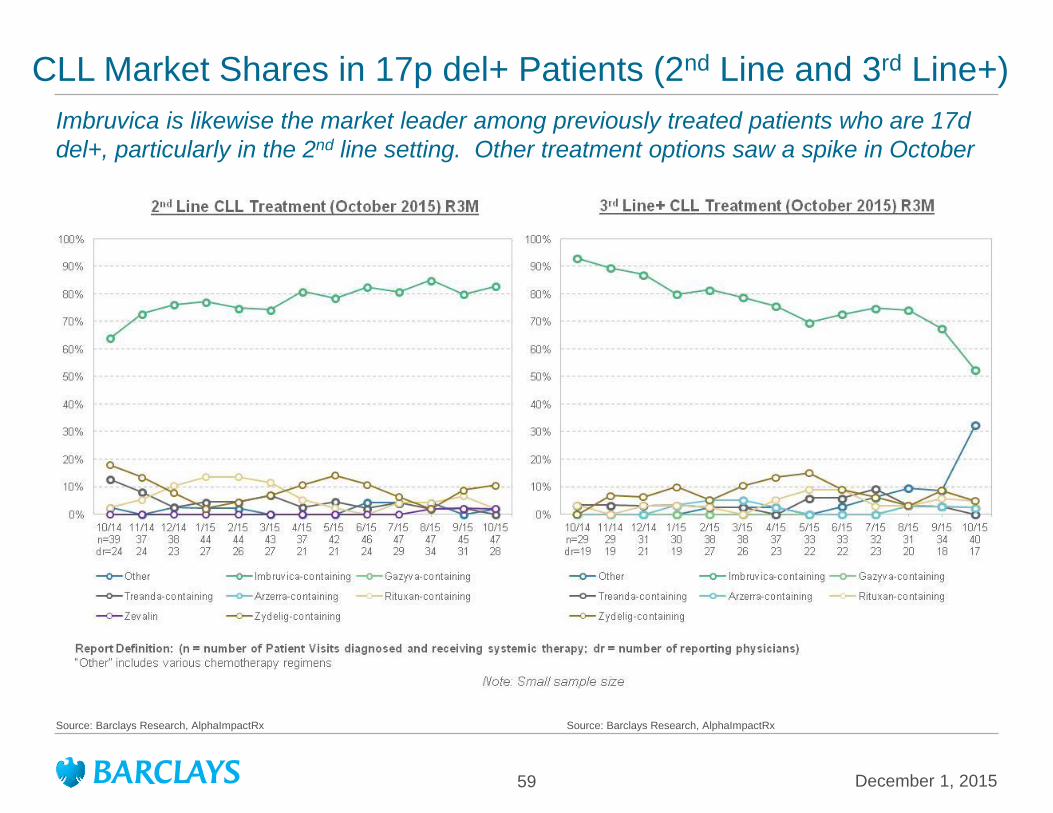

CLL Market Shares in 17p del+ Patients (2nd Line and 3rd Line+)

Imbruvica is likewise the market leader among previously treated patients who are 17d

del+, particularly in the 2nd line setting. Other treatment options saw a spike in October

Source: Barclays Research, AlphaImpactRx

Source: Barclays Research, AlphaImpactRx

December 1, 2015 60

Analyst Certifications and Important Disclosures

Analyst(s) Certification(s):

I, Mark Purcell, hereby certify (1) that the views expressed in this research report accurately reflect my personal views about any or all of the subject securities or

issuers referred to in this research report and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or

views expressed in this research report.

Important Disclosures:

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with companies covered in its research reports. As a result, investors should be

aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their investment decision.

The analysts responsible for preparing this research report have received compensation based upon various factors including the firm's total revenues, a portion

of which is generated by investment banking activities.

This research report has been prepared in whole or in part by equity research analysts based outside the US who are not registered/qualified as research

analysts with FINRA.

Research analysts employed outside the US by affiliates of Barclays Capital Inc. are not registered/qualified as research analysts with FINRA. These analysts

may not be associated persons of the member firm and therefore may not be subject to NASD Rule 2711 and incorporated NYSE Rule 472 restrictions on

communications with a subject company, public appearances and trading securities held by a research analyst’s account.

Analysts regularly conduct site visits to view the material operations of covered companies, but Barclays policy prohibits them from accepting payment or

reimbursement by any covered company of their travel expenses for such visits.

Barclays Research is a part of the Investment Bank of Barclays Bank PLC and its affiliates (collectively and each individually, "Barclays"). Where any companies

are the subject of this research report, for current important disclosures regarding those companies please send a written request to: Barclays Compliance

Department, 745 Seventh Avenue, 13th Floor, New York, NY 10019 or refer to http://publicresearch.barclays.com or call 212-526-1072.

In order to access Barclays Statement regarding Research Dissemination Policies and Procedures, please refer to

https://live.barcap.com/publiccp/RSR/nyfipubs/disclaimer/disclaimer-research-dissemination.html. In order to access Barclays Research Conflict Management

Policy Statement, please refer to: https://live.barcap.com/publiccp/RSR/nyfipubs/disclaimer/disclaimer-conflict-management.html.

The Investment Bank's Research Department produces various types of research including, but not limited to, fundamental analysis, equity-linked analysis,

quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from recommendations contained in other types of

research, whether as a result of differing time horizons, methodologies, or otherwise.

December 1, 2015 61

Important Disclosures (continued)

Risk Disclosure(s)

Master limited partnerships (MLPs) are pass-through entities structured as publicly listed partnerships. For tax purposes, distributions to MLP unit holders may

be treated as a return of principal. Investors should consult their own tax advisors before investing in MLP units.

Mentioned Stocks (Ticker, Date, Price)

AbbVie Inc. (ABBV, 25-Nov-2015, USD 60.29), Overweight/Neutral, A/C/D/J/K/L/M/O

AstraZeneca (AZN.L, 26-Nov-2015, GBP 45.20), Underweight/Neutral, C/D/J/K/L/M/N

Bristol-Myers Squibb (BMY, 25-Nov-2015, USD 68.08), Equal Weight/Neutral, A/C/D/J/K/L/M/N

Johnson & Johnson (JNJ, 25-Nov-2015, USD 101.96), Equal Weight/Neutral, C/J/K/M/N

Merck & Co. (MRK, 25-Nov-2015, USD 53.72), Equal Weight/Neutral, C/D/J/K/L/M/N/O

Merck KGaA (MRCG.DE, 26-Nov-2015, EUR 96.46), Equal Weight/Neutral, A/D/E/J/K/L/M/N

Pfizer Inc. (PFE, 25-Nov-2015, USD 32.87), Equal Weight/Neutral, C/D/J/K/L/M/O

Roche (ROG.VX, 26-Nov-2015, CHF 274.00), Overweight/Neutral, A/D/E/J/K/L/M/N

Other Material Conflicts: Barclays Bank and or its affiliate is advising GeneWEAVE BioSciences Inc in relation to their potential acquisition by Roche (SIX:ROG.)

The ratings, price targets and estimates on Roche (SIX:ROG) do not incorporate this transaction.

December 1, 2015 62

Important Disclosures (continued)

Disclosure Legend:

A: Barclays Bank PLC and/or an affiliate has been lead manager or co-lead manager of a publicly disclosed offer of securities of the issuer in the previous 12

months.

B: An employee of Barclays Bank PLC and/or an affiliate is a director of this issuer.

C: Barclays Bank PLC and/or an affiliate is a market-maker in equity securities issued by this issuer.

D: Barclays Bank PLC and/or an affiliate has received compensation for investment banking services from this issuer in the past 12 months.

E: Barclays Bank PLC and/or an affiliate expects to receive or intends to seek compensation for investment banking services from this issuer within the next 3

months.

F: Barclays Bank PLC and/or an affiliate beneficially owned 1% or more of a class of equity securities of the issuer as of the end of the month prior to the

research report's issuance.

G: One of the analysts on the coverage team (or a member of his or her household) owns shares of the common stock of this issuer.

H: This issuer beneficially owns 5% or more of any class of common equity securities of Barclays PLC.

I: Barclays Bank PLC and/or an affiliate has a significant financial interest in the securities of this issuer.

J: Barclays Bank PLC and/or an affiliate is a liquidity provider and/or trades regularly in the securities of this issuer and/or in any related derivatives.

K: Barclays Bank PLC and/or an affiliate has received non-investment banking related compensation (including compensation for brokerage services, if

applicable) from this issuer within the past 12 months.

L: This issuer is, or during the past 12 months has been, an investment banking client of Barclays Bank PLC and/or an affiliate.

M: This issuer is, or during the past 12 months has been, a non-investment banking client (securities related services) of Barclays Bank PLC and/or an affiliate.

N: This issuer is, or during the past 12 months has been, a non-investment banking client (non-securities related services) of Barclays Bank PLC and/or an

affiliate.

O: Barclays Capital Inc., through Barclays Market Makers, is a Designated Market Maker in this issuer's stock, which is listed on the New York Stock Exchange.

At any given time, its associated Designated Market Maker may have "long" or "short" inventory position in the stock; and its associated Designated Market

Maker may be on the opposite side of orders executed on the floor of the New York Stock Exchange in the stock.

P: A partner, director or officer of Barclays Capital Canada Inc. has, during the preceding 12 months, provided services to the subject company for remuneration,

other than normal course investment advisory or trade execution services.

Q: Barclays Bank PLC and/or an affiliate is a Corporate Broker to this issuer.

R: Barclays Capital Canada Inc. and/or an affiliate has received compensation for investment banking services from this issuer in the past 12 months.

S: Barclays Capital Canada Inc. is a market-maker in an equity or equity related security issued by this issuer.

T: Barclays Bank PLC and/or an affiliate is providing equity advisory services to this issuer.

U: The equity securities of this Canadian issuer include subordinate voting restricted shares.

V: The equity securities of this Canadian issuer include non-voting restricted shares.

W: Barclays Bank PLC and/or an affiliate should be assumed to be an actual beneficial owner of 1% or more of all the securities (including debt securities) of this

issuer as of the end of the month prior to the research report's issuance.

December 1, 2015 63

Important Disclosures (continued)

Guide to the Barclays Fundamental Equity Research Rating System:

Our coverage analysts use a relative rating system in which they rate stocks as Overweight, Equal Weight or Underweight (see definitions below) relative to

other companies covered by the analyst or a team of analysts that are deemed to be in the same industry (“the industry coverage universe”). To see a list of

companies that comprise a particular industry coverage universe, please go to http://publicresearch.barclays.com.

In addition to the stock rating, we provide industry views which rate the outlook for the industry coverage universe as Positive, Neutral or Negative (see

definitions below). A rating system using terms such as buy, hold and sell is not the equivalent of our rating system. Investors should carefully read the entire

research report including the definitions of all ratings and not infer its contents from ratings alone.

Stock Rating

Overweight - The stock is expected to outperform the unweighted expected total return of the industry coverage universe over a 12-month investment horizon.

Equal Weight - The stock is expected to perform in line with the unweighted expected total return of the industry coverage universe over a 12-month investment

horizon.

Underweight - The stock is expected to underperform the unweighted expected total return of the industry coverage universe over a 12-month investment

horizon.

Rating Suspended - The rating and target price have been suspended temporarily due to market events that made coverage impracticable or to comply with

applicable regulations and/or firm policies in certain circumstances including where the Investment Bank of Barclays Bank PLC is acting in an advisory capacity

in a merger or strategic transaction involving the company.

Industry View

Positive - industry coverage universe fundamentals/valuations are improving.

Neutral - industry coverage universe fundamentals/valuations are steady, neither improving nor deteriorating.

Negative - industry coverage universe fundamentals/valuations are deteriorating.

Distribution of Ratings:

Barclays Equity Research has 2787 companies under coverage.

42% have been assigned an Overweight rating which, for purposes of mandatory regulatory disclosures, is classified as a Buy rating; 51% of companies with this

rating are investment banking clients of the Firm.

40% have been assigned an Equal Weight rating which, for purposes of mandatory regulatory disclosures, is classified as a Hold rating; 43% of companies with

this rating are investment banking clients of the Firm.

15% have been assigned an Underweight rating which, for purposes of mandatory regulatory disclosures, is classified as a Sell rating; 39% of companies with

this rating are investment banking clients of the Firm.

Guide to the Barclays Research Price Target:

Each analyst has a single price target on the stocks that they cover. The price target represents that analyst's expectation of where the stock will trade in the next

12 months. Upside/downside scenarios, where provided, represent potential upside/potential downside to each analyst's price target over the same 12-month

period.

December 1, 2015 64

Important Disclosures (continued)

Top Picks:

Barclays Equity Research's "Top Picks" represent the single best alpha-generating investment idea within each industry (as defined by the relevant "industry

coverage universe"), taken from among the Overweight-rated stocks within that industry. Barclays Equity Research publishes global and regional "Top Picks"

reports every quarter and analysts may also publish intra-quarter changes to their Top Picks, as necessary. While analysts may highlight other Overweight-rated

stocks in their published research in addition to their Top Pick, there can only be one "Top Pick" for each industry. To view the current list of Top Picks, go to the

Top Picks page on Barclays Live (https://live.barcap.com/go/keyword/TopPicksGlobal).

To see a list of companies that comprise a particular industry coverage universe, please go to http://publicresearch.barclays.com.

Barclays legal entities involved in publishing research:

Barclays Bank PLC (Barclays, UK)

Barclays Capital Inc. (BCI, US)

Barclays Securities Japan Limited (BSJL, Japan)

Barclays Bank PLC, Tokyo branch (Barclays Bank, Japan)

Barclays Bank PLC, Hong Kong branch (Barclays Bank, Hong Kong)

Barclays Capital Canada Inc. (BCCI, Canada)

Absa Bank Limited (Absa, South Africa)

Barclays Bank Mexico, S.A. (BBMX, Mexico)

Barclays Capital Securities Taiwan Limited (BCSTW, Taiwan)

Barclays Capital Securities Limited (BCSL, South Korea)

Barclays Securities (India) Private Limited (BSIPL, India)

Barclays Bank PLC, India branch (Barclays Bank, India)

Barclays Bank PLC, Singapore branch (Barclays Bank, Singapore)

Barclays Bank PLC, Australia branch (Barclays Bank, Australia)

December 1, 2015 65

Disclaimer

Disclaimer:

This publication has been produced by the Investment Bank of Barclays Bank PLC and/or one or more of its affiliates (collectively and each individually,

"Barclays"). It has been distributed by one or more Barclays legal entities that are a part of the Investment Bank as provided below. It is provided to our clients for

information purposes only, and Barclays makes no express or implied warranties, and expressly disclaims all warranties of merchantability or fitness for a

particular purpose or use with respect to any data included in this publication. Barclays will not treat unauthorized recipients of this report as its clients and

accepts no liability for use by them of the contents which may not be suitable for their personal use. Prices shown are indicative and Barclays is not offering to

buy or sell or soliciting offers to buy or sell any financial instrument.

Without limiting any of the foregoing and to the extent permitted by law, in no event shall Barclays, nor any affiliate, nor any of their respective officers, directors,

partners, or employees have any liability for (a) any special, punitive, indirect, or consequential damages; or (b) any lost profits, lost revenue, loss of anticipated

savings or loss of opportunity or other financial loss, even if notified of the possibility of such damages, arising from any use of this publication or its contents.

Other than disclosures relating to Barclays, the information contained in this publication has been obtained from sources that Barclays Research believes to be

reliable, but Barclays does not represent or warrant that it is accurate or complete. Barclays is not responsible for, and makes no warranties whatsoever as to,

the content of any third-party web site accessed via a hyperlink in this publication and such information is not incorporated by reference.

The views in this publication are those of the author(s) and are subject to change, and Barclays has no obligation to update its opinions or the information in this

publication. If this publication contains recommendations, those recommendations reflect solely and exclusively those of the authoring analyst(s), and such

opinions were prepared independently of any other interests, including those of Barclays and/or its affiliates. This publication does not constitute personal

investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not

be suitable for all investors. Barclays recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any

independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant

economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from

those reflected. Past performance is not necessarily indicative of future results.

This document is being distributed (1) only by or with the approval of an authorised person (Barclays Bank PLC) or (2) to, and is directed at (a) persons in the

United Kingdom having professional experience in matters relating to investments and who fall within the definition of "investment professionals" in Article 19(5)

of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Order"); or (b) high net worth companies, unincorporated associations

and partnerships and trustees of high value trusts as described in Article 49(2) of the Order; or (c) other persons to whom it may otherwise lawfully be

communicated (all such persons being ''Relevant Persons''). Any investment or investment activity to which this communication relates is only available to and

will only be engaged in with Relevant Persons. Any other persons who receive this communication should not rely on or act upon it. Barclays Bank PLC is

authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority and is a member of

the London Stock Exchange.

The Investment Bank of Barclays Bank PLC undertakes U.S. securities business in the name of its wholly owned subsidiary Barclays Capital Inc., a FINRA and

SIPC member. Barclays Capital Inc., a U.S. registered broker/dealer, is distributing this material in the United States and, in connection therewith accepts

responsibility for its contents. Any U.S. person wishing to effect a transaction in any security discussed herein should do so only by contacting a representative of

Barclays Capital Inc. in the U.S. at 745 Seventh Avenue, New York, New York 10019.

Non-U.S. persons should contact and execute transactions through a Barclays Bank PLC branch or affiliate in their home jurisdiction unless local regulations

permit otherwise.

December 1, 2015 66

Disclaimer (continued)

Barclays Bank PLC, Paris Branch (registered in France under Paris RCS number 381 066 281) is regulated by the Autorité des marchés financiers and the

Autorité de contrôle prudentiel. Registered office 34/36 Avenue de Friedland 75008 Paris.

This material is distributed in Canada by Barclays Capital Canada Inc., a registered investment dealer, a Dealer Member of IIROC (www.iiroc.ca), and a Member

of the Canadian Investor Protection Fund (CIPF).

Subject to the conditions of this publication as set out above, the Corporate & Investment Banking Division of Absa Bank Limited, an authorised financial

services provider (Registration No.: 1986/004794/06. Registered Credit Provider Reg No NCRCP7), is distributing this material in South Africa. Absa Bank

Limited is regulated by the South African Reserve Bank. This publication is not, nor is it intended to be, advice as defined and/or contemplated in the (South

African) Financial Advisory and Intermediary Services Act, 37 of 2002, or any other financial, investment, trading, tax, legal, accounting, retirement, actuarial or

other professional advice or service whatsoever. Any South African person or entity wishing to effect a transaction in any security discussed herein should do so

only by contacting a representative of the Corporate & Investment Banking Division of Absa Bank Limited in South Africa, 15 Alice Lane, Sandton,

Johannesburg, Gauteng 2196. Absa Bank Limited is a member of the Barclays group.

In Japan, foreign exchange research reports are prepared and distributed by Barclays Bank PLC Tokyo Branch. Other research reports are distributed to

institutional investors in Japan by Barclays Securities Japan Limited. Barclays Securities Japan Limited is a joint-stock company incorporated in Japan with

registered office of 6-10-1 Roppongi, Minato-ku, Tokyo 106-6131, Japan. It is a subsidiary of Barclays Bank PLC and a registered financial instruments firm

regulated by the Financial Services Agency of Japan. Registered Number: Kanto Zaimukyokucho (kinsho) No. 143.

Barclays Bank PLC, Hong Kong Branch is distributing this material in Hong Kong as an authorised institution regulated by the Hong Kong Monetary Authority.

Registered Office: 41/F, Cheung Kong Center, 2 Queen's Road Central, Hong Kong.

Information on securities/instruments that trade in Taiwan or written by a Taiwan-based research analyst is distributed by Barclays Capital Securities Taiwan

Limited to its clients. The material on securities/instruments not traded in Taiwan is not to be construed as 'recommendation' in Taiwan. Barclays Capital

Securities Taiwan Limited does not accept orders from clients to trade in such securities. This material may not be distributed to the public media or used by the

public media without prior written consent of Barclays.

This material is distributed in South Korea by Barclays Capital Securities Limited, Seoul Branch.

All Indian securities-related research and other equity research produced by the Investment Bank are distributed in India by Barclays Securities (India) Private

Limited (BSIPL). BSIPL is a company incorporated under the Companies Act, 1956 having CIN U67120MH2006PTC161063. BSIPL is registered and regulated

by the Securities and Exchange Board of India (SEBI) as a Research Analyst: INH000001519; Portfolio Manager INP000002585; Stock Broker/Trading and

Clearing Member: National Stock Exchange of India Limited (NSE) Capital Market INB231292732, NSE Futures & Options INF231292732, NSE Currency

derivatives INE231450334, Bombay Stock Exchange Limited (BSE) Capital Market INB011292738, BSE Futures & Options INF011292738; Merchant

Banker: INM000011195; Depository Participant (DP) with the National Securities & Depositories Limited (NSDL): DP ID: IN-DP-NSDL-299-2008;

Investment Adviser: INA000000391. The registered office of BSIPL is at 208, Ceejay House, Shivsagar Estate, Dr. A. Besant Road, Worli, Mumbai – 400 018,

India. Telephone No: +91 2267196000. Fax number: +91 22 67196100. Any other reports produced by the Investment Bank are distributed in India by Barclays

Bank PLC, India Branch, an associate of BSIPL in India that is registered with Reserve Bank of India (RBI) as a Banking Company under the provisions of The

Banking Regulation Act, 1949 (Regn No BOM43) and registered with SEBI as Merchant Banker (Regn No INM000002129) and also as Banker to the Issue

(Regn No INBI00000950). Barclays Investments and Loans (India) Limited, registered with RBI as Non Banking Financial Company (Regn No RBI CoR-07-

00258), and Barclays Wealth Trustees (India) Private Limited, registered with Registrar of Companies (CIN U93000MH2008PTC188438), are associates of

BSIPL in India that are not authorised to distribute any reports produced by the Investment Bank.

Barclays Bank PLC Frankfurt Branch distributes this material in Germany under the supervision of Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin).

December 1, 2015 67

Disclaimer (continued)

This material is distributed in Malaysia by Barclays Capital Markets Malaysia Sdn Bhd.

This material is distributed in Brazil by Banco Barclays S.A.

This material is distributed in Mexico by Barclays Bank Mexico, S.A.

Barclays Bank PLC in the Dubai International Financial Centre (Registered No. 0060) is regulated by the Dubai Financial Services Authority (DFSA). Principal

place of business in the Dubai International Financial Centre: The Gate Village, Building 4, Level 4, PO Box 506504, Dubai, United Arab Emirates. Barclays Bank

PLC-DIFC Branch, may only undertake the financial services activities that fall within the scope of its existing DFSA licence. Related financial products or

services are only available to Professional Clients, as defined by the Dubai Financial Services Authority.

Barclays Bank PLC in the UAE is regulated by the Central Bank of the UAE and is licensed to conduct business activities as a branch of a commercial bank

incorporated outside the UAE in Dubai (Licence No.: 13/1844/2008, Registered Office: Building No. 6, Burj Dubai Business Hub, Sheikh Zayed Road, Dubai City)

and Abu Dhabi (Licence No.: 13/952/2008, Registered Office: Al Jazira Towers, Hamdan Street, PO Box 2734, Abu Dhabi).

Barclays Bank PLC in the Qatar Financial Centre (Registered No. 00018) is authorised by the Qatar Financial Centre Regulatory Authority (QFCRA). Barclays

Bank PLC-QFC Branch may only undertake the regulated activities that fall within the scope of its existing QFCRA licence. Principal place of business in Qatar:

Qatar Financial Centre, Office 1002, 10th Floor, QFC Tower, Diplomatic Area, West Bay, PO Box 15891, Doha, Qatar. Related financial products or services are

only available to Business Customers as defined by the Qatar Financial Centre Regulatory Authority.

This material is distributed in the UAE (including the Dubai International Financial Centre) and Qatar by Barclays Bank PLC.

This material is not intended for investors who are not Qualified Investors according to the laws of the Russian Federation as it might contain information about or

description of the features of financial instruments not admitted for public offering and/or circulation in the Russian Federation and thus not eligible for non-

Qualified Investors. If you are not a Qualified Investor according to the laws of the Russian Federation, please dispose of any copy of this material in your

possession.

This material is distributed in Singapore by the Singapore branch of Barclays Bank PLC, a bank licensed in Singapore by the Monetary Authority of Singapore.

For matters in connection with this report, recipients in Singapore may contact the Singapore branch of Barclays Bank PLC, whose registered address is 10

Marina Boulevard, #23-01 Marina Bay Financial Centre Tower 2, Singapore 018983.

Barclays Bank PLC, Australia Branch (ARBN 062 449 585, AFSL 246617) is distributing this material in Australia. It is directed at 'wholesale clients' as defined

by Australian Corporations Act 2001.

IRS Circular 230 Prepared Materials Disclaimer: Barclays does not provide tax advice and nothing contained herein should be construed to be tax advice. Please

be advised that any discussion of U.S. tax matters contained herein (including any attachments) (i) is not intended or written to be used, and cannot be used, by

you for the purpose of avoiding U.S. tax-related penalties; and (ii) was written to support the promotion or marketing of the transactions or other matters

addressed herein. Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor.

© Copyright Barclays Bank PLC (2015). All rights reserved. No part of this publication may be reproduced or redistributed in any manner without the prior written

permission of Barclays. Barclays Bank PLC is registered in England No. 1026167. Registered office 1 Churchill Place, London, E14 5HP. Additional information

regarding this publication will be furnished upon request.

.

Our Agenda

68

• A snapshot of the current Oncology Promotional Landscape

• The I/O Battlefield

NSCLC

Melanoma

PD-L1 Testing

• Preparing for ASH and San Antonio Breast Cancer Conferences

Breast Cancer

CLL

• Q&A