ALPHA FINANCE ROMANIA S.A. FINANCE ROMANIA S.A. Consolidated Financial Statements as of and for the...

21

ALPHA FINANCE ROMANIA S.A. Consolidated Financial Statements as of and for the year ended 31 December 2005 Prepared in accordance with International Financial Reporting Standards

Transcript of ALPHA FINANCE ROMANIA S.A. FINANCE ROMANIA S.A. Consolidated Financial Statements as of and for the...

ALPHA FINANCE ROMANIA S.A. Consolidated Financial Statements as of and for the year ended 31 December 2005 Prepared in accordance with International Financial Reporting Standards

S.C. ALPHA FINANCE ROMANIA S.A. Financial Statements

as of and for the year ended 31 December 2005

1

CONTENTS: Consolidated balance sheet 2 Consolidated statement of income 3 Consolidated statement of change in equity 4 Consolidated statement of cash flows 5 Notes to the consolidated financial statements 6

S.C. ALPHA FINANCE ROMANIA S.A. Consolidated balance sheet as of 31 December 2005

(All amounts in RON unless otherwise indicated)

The accompanying notes are an integral part of these financial statements 2

Note 2005 2004 ASSETS Non-current assets Investments 7 314,601 45,209Property and equipment, net 9 2,216,621 1,891,941Intangible assets, net 10 14,348 13,156 2,545,570 1,950,306Current assets Cash and cash equivalents 3 9,209,180 4,271,330Short-term deposits 4 253,863 -Trading securities, net 5 119,193 162,704Bonds, held for trading - 1,775,751Due from customers, net 6 10,269 11,846Other assets 8 212,764 191,362

9,805,269 6,412,992

TOTAL ASSETS 12,350,839 8,363,298

LIABILITIES AND SHAREHOLDERS' EQUITY

LIABILITIES Non-current liabilities Lease payables 13 27,214 41,622Deferred tax liability, net 19 69,079 108,901 96,293 150,523Current liabilities Accrued expenses and other liabilities 12 1,216,172 42,199Bank borrowings 14 159,160 1,973,617Due to customers 11 3,233,199 680,689Deferred income Lease payables

19 13

31,784 14,408

-13,297

4,654,723 2,709,802

SHAREHOLDERS' EQUITY Share capital 15 4,652,151 4,652,151Share premium 67,987 67,987Revaluation surplus 918,197 633,466Retained earnings 1,961,488 149,370 21 7,599,823 5,502,973

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 12,350,839 8,363,298 These financial statements have been approved by the Board of Directors on 13 April 2006 and signed on its behalf by: Dimitris Tamvakas Florin Aldea Managing Director Administrator

S.C. ALPHA FINANCE ROMANIA S.A. Consolidated statement of income for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

The accompanying notes are an integral part of these financial statements 3

Note 2005 2004

Corporate finance income 950,694 1,510,392Commission income 4,488,782 2,987,510Net trading income on securities 16 370,006 (309,159)Other operating revenues 218,810 125,317Operating income 6,028,292 4,314,061

Financial income, net 17 444,180 554,301Operating expenses, net 18 (4,362,579) (3,377,270)Income before income tax expense 2,109,893 1,491,092

Current income tax (390,154) (420,389)Deferred income tax 72,854 78,549 Income tax expense 19 (317,300) (341,840)

Net income for the year 1,792,593 1,149,252

S.C. ALPHA FINANCE ROMANIA S.A. Consolidated statement of change in equity for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

The accompanying notes are an integral part of these financial statements 4

Share Capital Share Premium

Revaluation surplus

Retained earnings (deficit)

Total

Shareholders’ Equity

Balances as of 31 December 2003 4,652,151 67,987 647,801 (1,014,216) 4,353,723 Depreciation of revaluation surplus - - (14,333) 14,333 -Net profit for the year ended 31 December 2004 - - - 1,149,252 1,149,252 Balances as of 31 December 2004 4,652,151 67,987 633,468 149,370 5,502,976 Reevaluation of building 337,287 337,287Deferred taxation on revaluation of building (33,033) (33,033)Depreciation of revaluation surplus (19,525) 19,525 - Net profit for the year ended 31 December 2005 1,792,593 1,792,593 Balances as of 31 December 2005 4,652,151 67,987 918,197 1,961,488 7,599,823

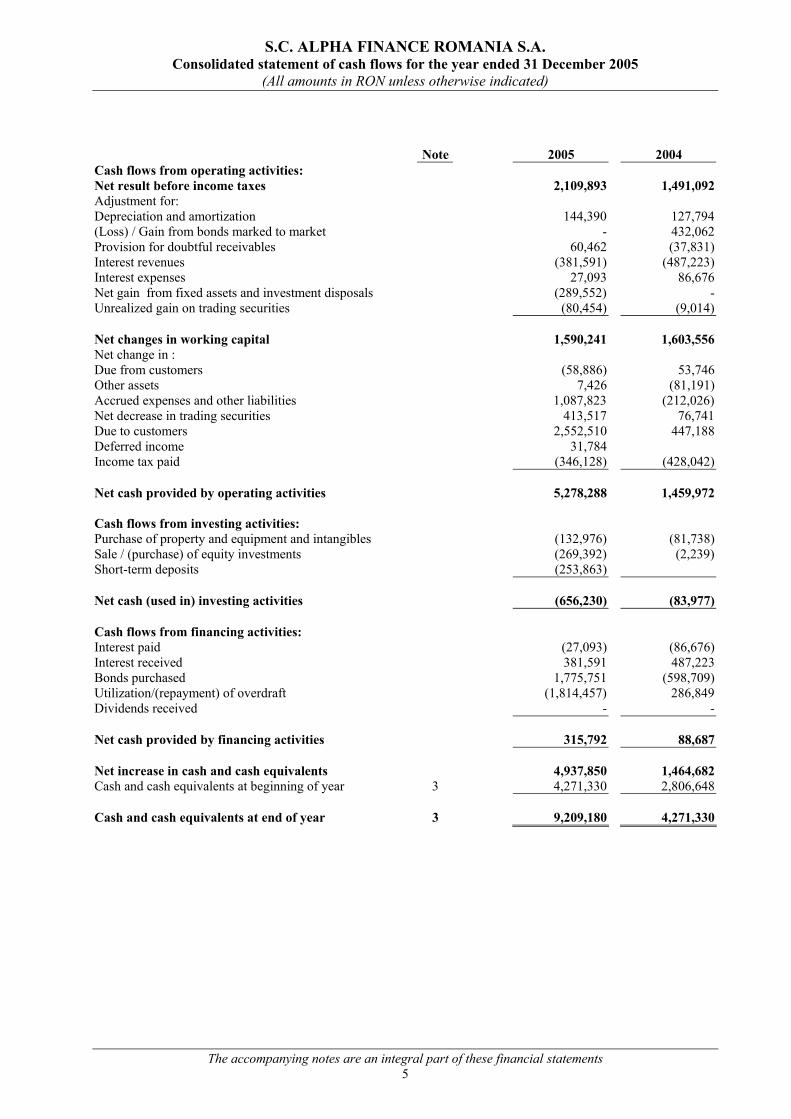

S.C. ALPHA FINANCE ROMANIA S.A. Consolidated statement of cash flows for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

The accompanying notes are an integral part of these financial statements 5

Note 2005 2004

Cash flows from operating activities: Net result before income taxes 2,109,893 1,491,092Adjustment for: Depreciation and amortization 144,390 127,794(Loss) / Gain from bonds marked to market - 432,062Provision for doubtful receivables 60,462 (37,831)Interest revenues (381,591) (487,223)Interest expenses 27,093 86,676Net gain from fixed assets and investment disposals (289,552) -Unrealized gain on trading securities (80,454) (9,014) Net changes in working capital 1,590,241 1,603,556Net change in : Due from customers (58,886) 53,746Other assets 7,426 (81,191)Accrued expenses and other liabilities 1,087,823 (212,026)Net decrease in trading securities 413,517 76,741Due to customers 2,552,510 447,188Deferred income 31,784 Income tax paid (346,128) (428,042) Net cash provided by operating activities

5,278,288

1,459,972

Cash flows from investing activities:

Purchase of property and equipment and intangibles (132,976) (81,738)Sale / (purchase) of equity investments (269,392) (2,239)Short-term deposits (253,863) Net cash (used in) investing activities

(656,230)

(83,977)

Cash flows from financing activities:

Interest paid (27,093) (86,676)Interest received 381,591 487,223Bonds purchased 1,775,751 (598,709)Utilization/(repayment) of overdraft (1,814,457) 286,849Dividends received - - Net cash provided by financing activities

315,792

88,687

Net increase in cash and cash equivalents

4,937,850

1,464,682

Cash and cash equivalents at beginning of year 3 4,271,330 2,806,648 Cash and cash equivalents at end of year

3

9,209,180

4,271,330

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

6

1. Background and general information S.C. ALPHA FINANCE ROMANIA S.A. (the “Company”), whose registered office is at 237B Dorobantilor Street, Bucharest, Romania, was registered as a stock company at the Chamber for Industry and Commerce of Bucharest in 1994 under its initial name Bucharest Investment Group Brokerage S.A. The name was changed in May 2000 to S.C. ALPHA FINANCE ROMANIA S.A. The Company’s main activity is to provide brokerage, corporate finance and advisory services to investors. The Company operates on the Bucharest Stock Exchange (“BSE”). As of 31 December 2005, the Company held 100% (2004 – 100%) of S.C. ALPHA ADVISORY ROMANIA S.R.L. Accordingly, these financial statements represent the consolidated financial statements of the Company and its subsidiary. S.C. ALPHA ADVISORY ROMANIA S.R.L., whose registered office is at 237B Dorobantilor Street, Bucharest, Romania, is a stock company established in 1998. The main activity of S.C. ALPHA ADVISORY ROMANIA S.R.L is consulting and market research. The Company’s shareholders structure at 31 December 2005 was as follows:

2005 Percentage holding (%)

2004 Percentage holding (%)

Alpha Bank (Greece) 45.68% 45.68 % Alpha Finance Axepey 29.59% 29.59 % Alpha Bank (Romania) 15.00% 24.73 % Alpha Investments Services Aepey 0.0062% 0.0062 % Alpha Asset Management A.E. 0.0062% 0.0062 % Alpha Leasing Romania 9.73% 0.0062% Total 100.00% 100.00 % 2. Summary of significant accounting policies a) General The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”), which comprise standards and interpretations approved by the IASB and Standing Interpretations Committee interpretations approved by the IASC that remain in effect. The preparation of consolidated financial statements in conformity with IFRS requires management to make estimates and assumptions that affect reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. These estimates are reviewed periodically and changes in estimates are recognized in the periods in which they become known. The consolidated financial statements have been prepared on an historical cost basis, except for the revaluation of tangible fixed assets and the mark-to-market of trading securities. b) Basis of accounting The consolidated financial statements are presented in Romanian Leu (“RON”), the Company’s functional currency and reflect certain adjustments and reclassifications, not recorded in the accounting records and statutory financial statements of the Company, which are prepared in accordance with Minister of Public Finance Order 1742/106/2002. These adjustments were made in order to conform the statutory balances with IFRS.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

7

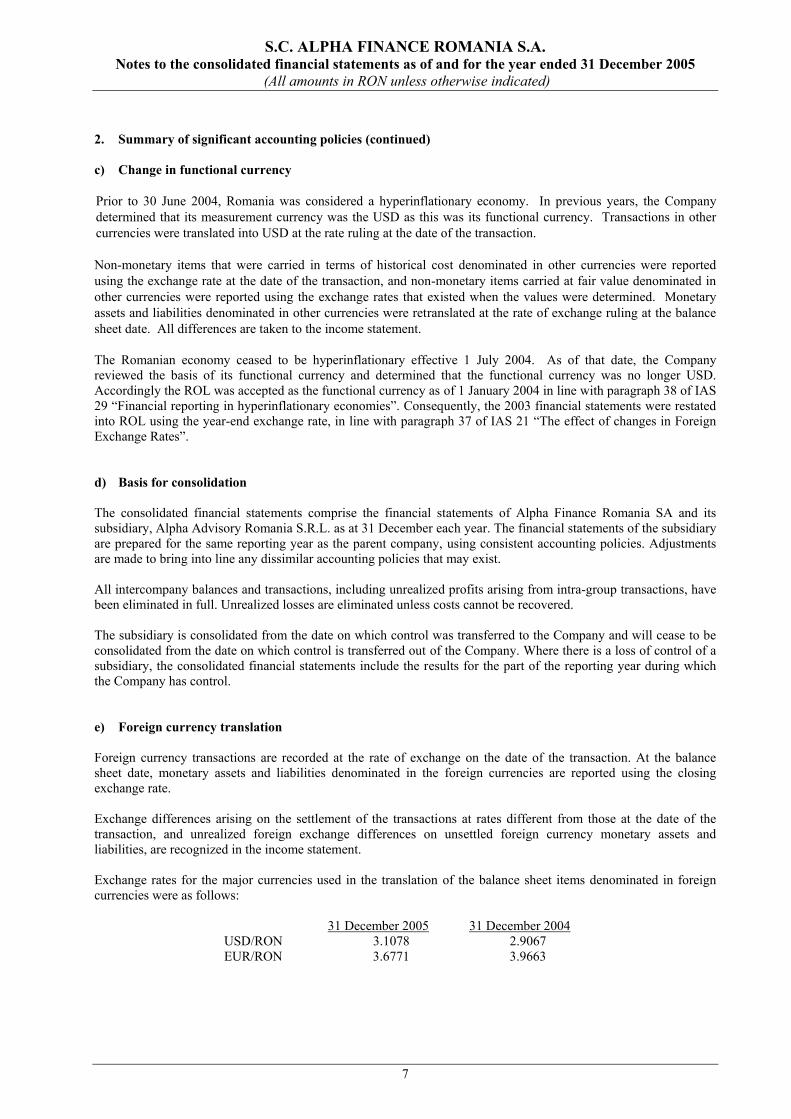

2. Summary of significant accounting policies (continued) c) Change in functional currency Prior to 30 June 2004, Romania was considered a hyperinflationary economy. In previous years, the Company determined that its measurement currency was the USD as this was its functional currency. Transactions in other currencies were translated into USD at the rate ruling at the date of the transaction. Non-monetary items that were carried in terms of historical cost denominated in other currencies were reported using the exchange rate at the date of the transaction, and non-monetary items carried at fair value denominated in other currencies were reported using the exchange rates that existed when the values were determined. Monetary assets and liabilities denominated in other currencies were retranslated at the rate of exchange ruling at the balance sheet date. All differences are taken to the income statement. The Romanian economy ceased to be hyperinflationary effective 1 July 2004. As of that date, the Company reviewed the basis of its functional currency and determined that the functional currency was no longer USD. Accordingly the ROL was accepted as the functional currency as of 1 January 2004 in line with paragraph 38 of IAS 29 “Financial reporting in hyperinflationary economies”. Consequently, the 2003 financial statements were restated into ROL using the year-end exchange rate, in line with paragraph 37 of IAS 21 “The effect of changes in Foreign Exchange Rates”. d) Basis for consolidation The consolidated financial statements comprise the financial statements of Alpha Finance Romania SA and its subsidiary, Alpha Advisory Romania S.R.L. as at 31 December each year. The financial statements of the subsidiary are prepared for the same reporting year as the parent company, using consistent accounting policies. Adjustments are made to bring into line any dissimilar accounting policies that may exist. All intercompany balances and transactions, including unrealized profits arising from intra-group transactions, have been eliminated in full. Unrealized losses are eliminated unless costs cannot be recovered. The subsidiary is consolidated from the date on which control was transferred to the Company and will cease to be consolidated from the date on which control is transferred out of the Company. Where there is a loss of control of a subsidiary, the consolidated financial statements include the results for the part of the reporting year during which the Company has control. e) Foreign currency translation Foreign currency transactions are recorded at the rate of exchange on the date of the transaction. At the balance sheet date, monetary assets and liabilities denominated in the foreign currencies are reported using the closing exchange rate. Exchange differences arising on the settlement of the transactions at rates different from those at the date of the transaction, and unrealized foreign exchange differences on unsettled foreign currency monetary assets and liabilities, are recognized in the income statement. Exchange rates for the major currencies used in the translation of the balance sheet items denominated in foreign currencies were as follows:

31 December 2005 31 December 2004 USD/RON 3.1078 2.9067 EUR/RON 3.6771 3.9663

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

8

2. Summary of significant accounting policies (continued) f) Revenue and expense recognition

Commissions for brokerage activities are charged to customers and credited to income at the time the transactions are performed. Advisory fees are credited to income and invoiced to the client when a distinct phase of a project is completed. In case of consulting services provided over a period of time, those fees are recognized and billed over the period of the agreement in accordance with contract clauses. Brokerage fees are recognized and charged at the transactions date performed for clients on the market (BSE), in accordance with local settlement house regulations. g) Cash and cash equivalents Cash and cash equivalents include cash on hand and cash with banks. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash with original maturity of three months or less and that are subject to an insignificant risk of change in value. In the balance sheet, bank overdrafts are included in the borrowings within current liabilities. h) Short term deposits The Company classifies deposits with maturity term between 3 months and 1 year as being short-term deposits. Short-term deposits are expressed at amortized cost, including the related receivable interest. i) Intangible assets The intangible assets, consisting of software programs, are included in the balance sheet at historical cost and are amortized over 2 years.

j) Tangible fixed assets The tangible fixed assets, except for buildings, are included in the balance sheet at historical cost, including related costs of transportation and custom duties. The building owned by Alpha Finance and Alpha Advisory was revaluated in 2005 for both IFRS and statutory purposes. The appraisal was performed by an independent evaluator, ANEVAR member. As the last revaluation was made in 2002, the benefit of the revaluation is reduction of property tax obligations of the Company from 5% to 1.5% from net book value. The revaluation was approved by the Administration Council and was booked as of 30 April 2005. Depreciation is computed over the estimated economic useful lives of the assets, on the straight-line basis method, as follows: Buildings 50 years Motor vehicles 5 years Computers and other equipment 3-15 years Maintenance and repairs are expensed when incurred and improvements are capitalized.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

9

2. Summary of significant accounting policies (continued) k) Impairment of assets Fixed assets and intangible assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Whenever the carrying amount of an asset exceeds its recoverable amount, an impairment loss is recognized in income for items carried at cost and treated as a revaluation decrease for assets that are carried at revalued amounts to the extent that the impairment loss does not exceed the amount held in the revaluation surplus for the same asset. The recoverable amount is the higher of an asset’s net selling price and value in use. The net selling price is the amount obtainable from the sale of an asset in an arm’s length transaction while value in use is the present value of estimated future cash flows expected to arise from the continuing use of an asset and from its disposal at the end of its useful life. Recoverable amounts are estimated for individual assets or, if it is not possible, for the cash-generating unit. Reversal of impairment losses recognized in prior years is recorded when there is an indication that the impairment losses recognized for the asset no longer exist or has decreased. The reversal is recorded in income or as a revaluation increase, as appropriate. l) Investments All investments are initially recognized at fair value, being the fair value of the consideration given and including acquisition charges associated with the investment. The income statement reflects income from the investment only to the extent that the investor receives dividends from the investee. The Company’s investments in entities which have no quoted market price are carried at restated cost less an estimate for impairment. These financial investments generally represent equity in companies for which there is no reliable comparative information for estimating market value. m) Trading securities and bonds held for trading Trading securities actively traded in organized financial markets are stated at fair value determined by reference to Stock Exchange quoted market bid prices at the close of business on the balance sheet date. All gains and losses arising from trading securities are reported in net trading gains or losses in the income statement. Interest earned whilst holding interest-bearing trading securities is reported as interest income. Dividends received are included in other operating revenues. n) Trade and other receivables and payables

Trade and other receivables originated by the enterprise are initially recognized at fair value and carried at amortized cost, net of any estimated reserves for impairment. Due to their short-term nature and low transaction costs, the cost is deemed to approximate their fair value. Trade and other payables as well as bank loans are stated at amortized cost. Due to their short-term nature and their immaterial transaction costs their amortized cost is deemed to approximate their fair value.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

10

2. Summary of significant accounting policies (continued) o) Income taxes Current taxation The current tax is the amount of income taxes payable in respect of the statutory taxable profit, computed in accordance with Romanian tax rules and accrued for in the period to which it relates. Current income taxes are provided on statutory income, as adjusted for certain items by the tax legislation, at a rate of 16%. Deferred taxation Deferred income tax is provided, using the liability method, on all temporary differences at the balance sheet date between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Deferred income tax liabilities are recognized for all taxable temporary differences. Deferred income tax assets are recognized for all deductible temporary differences and unused tax losses, to the extent that it is probable that taxable profit will be available against which the deductible temporary differences and unused tax assets and unused tax losses can be utilized. Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the balance sheet date. p) Legal reserves Legal reserves are created in accordance with requirements of Romanian laws and regulations and include annual allocations of 5% of Company's net earnings for investing activity purposes. According to Romanian law, the legal reserve cannot exceed 20% of share capital. q) Pensions and other retirement benefits Short-term employee benefits: Short-term employee benefits include wages, salaries and social security contributions. Short-term employee benefits are recognized as expenses as services are rendered. Post-employment benefits: Both the Company and its employees are legally obliged to make defined contributions (included in the social security contributions) to the National Pension Fund, managed by the Romanian State Social Security (a defined contribution plan financed on a pay-as-you-go basis). As such, the Company has no legal or constructive obligation to pay future benefits. Its only obligation is to pay the contributions as they fall due. If the Company ceases to employ members of the Romanian State Social Security plan, it will have no obligation to pay the benefits earned by its own employees in previous years. The Company’s contributions relating to defined contribution plans are charged to income in the year to which they relate. Termination benefits Expenses related to termination indemnities are accrued when management decides to adopt a plan that will result in future payments of termination benefits and either starts to implement the restructuring plan or communicates the restructuring plan to those affected by it in a sufficiently specific manner to raise a valid expectation that the Company will carry out the restructuring. No such expenses were incurred or planned for 2006.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

11

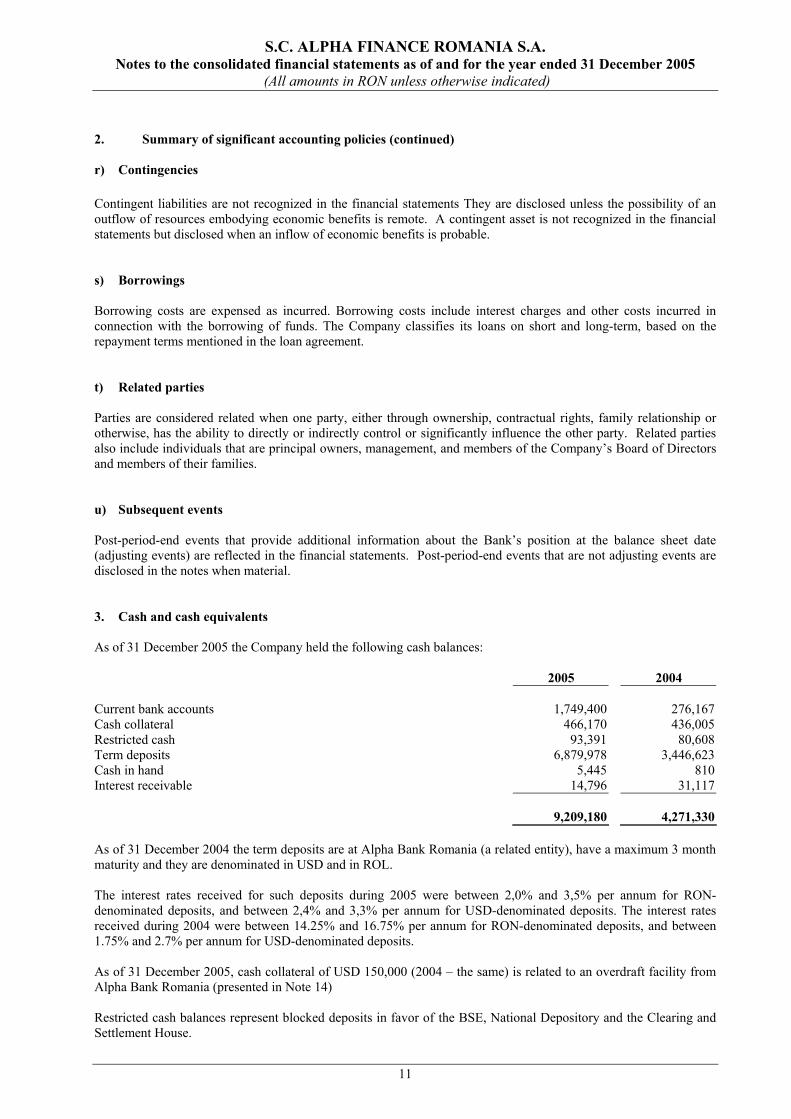

2. Summary of significant accounting policies (continued) r) Contingencies Contingent liabilities are not recognized in the financial statements They are disclosed unless the possibility of an outflow of resources embodying economic benefits is remote. A contingent asset is not recognized in the financial statements but disclosed when an inflow of economic benefits is probable. s) Borrowings Borrowing costs are expensed as incurred. Borrowing costs include interest charges and other costs incurred in connection with the borrowing of funds. The Company classifies its loans on short and long-term, based on the repayment terms mentioned in the loan agreement. t) Related parties Parties are considered related when one party, either through ownership, contractual rights, family relationship or otherwise, has the ability to directly or indirectly control or significantly influence the other party. Related parties also include individuals that are principal owners, management, and members of the Company’s Board of Directors and members of their families. u) Subsequent events Post-period-end events that provide additional information about the Bank’s position at the balance sheet date (adjusting events) are reflected in the financial statements. Post-period-end events that are not adjusting events are disclosed in the notes when material. 3. Cash and cash equivalents As of 31 December 2005 the Company held the following cash balances:

2005 2004 Current bank accounts 1,749,400 276,167Cash collateral 466,170 436,005Restricted cash 93,391 80,608Term deposits 6,879,978 3,446,623Cash in hand 5,445 810Interest receivable 14,796 31,117

9,209,180 4,271,330 As of 31 December 2004 the term deposits are at Alpha Bank Romania (a related entity), have a maximum 3 month maturity and they are denominated in USD and in ROL. The interest rates received for such deposits during 2005 were between 2,0% and 3,5% per annum for RON-denominated deposits, and between 2,4% and 3,3% per annum for USD-denominated deposits. The interest rates received during 2004 were between 14.25% and 16.75% per annum for RON-denominated deposits, and between 1.75% and 2.7% per annum for USD-denominated deposits. As of 31 December 2005, cash collateral of USD 150,000 (2004 – the same) is related to an overdraft facility from Alpha Bank Romania (presented in Note 14) Restricted cash balances represent blocked deposits in favor of the BSE, National Depository and the Clearing and Settlement House.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

12

4. Short-term Deposits As of 31 December 2005 the Company has in balance a 6 months maturity deposit opened with Alpha Bank (a related party) with a principal value of 250,000 RON at a 6% interest rate. 5. Trading securities, net As of 31 December 2005, the Company’s portfolio of trading securities consisted of shares listed on the BSE (2004 BSE and RASDAQ). Their cost and fair values were as follows:

31 December Cost Mark to market Carrying value Fair value

2005

137,944 (18,751) 119,193 119,1932004 153,690 9,014 162,704 162,704

6. Due from customers As of 31 December 2005, due from customers represent receivables for transactions performed on behalf of the clients. As of 31 December 2005 a provision of 60,462 RON was recorded for doubtful debts (2004 – RON 8,408). 7. Investments As of 31 December 2005, the detail of the investments of the Company, all located in Romania, is as follows: 2005 2004 Amount Ownership Principal Amount Ownership Principal Investment 2005 Interest Activities 2004 Interest Activities Alpha Leasing Romania 238,350

5.7%

Leasing 42,727

0.01%

Leasing

Alpha Bank Romania 2,371

Less than 0.01% Bank 872

Less than 0.01% Bank

BVB - 1,48%

Stock Exchange - - -

RASDAQ (merged with BSE) - -

Over the counter 1,000

Less than 0.01%

Over the counter

Romanian Clearing House 9,000 0,37% - Fondul de Compensare al Investitorilor 1,500 1,36% -

610 0.17%

Clearing of transactions

with securities 610 0.17%

Clearing of transactions

with securities

National Clearing Settlement and Depository Institution (“SNCDD”)

Total 251,831 45,209 According to the regulations of the National Commission of Securities, all companies that perform transactions on the secondary market are required to have an investment in SNCDD. During 2005, the Company has been granted free shares in BSE which for statutory reporting purposes were recorded in other reserves and reversed for IFRS reporting purposes, as their value can not be reasonably estimated.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

13

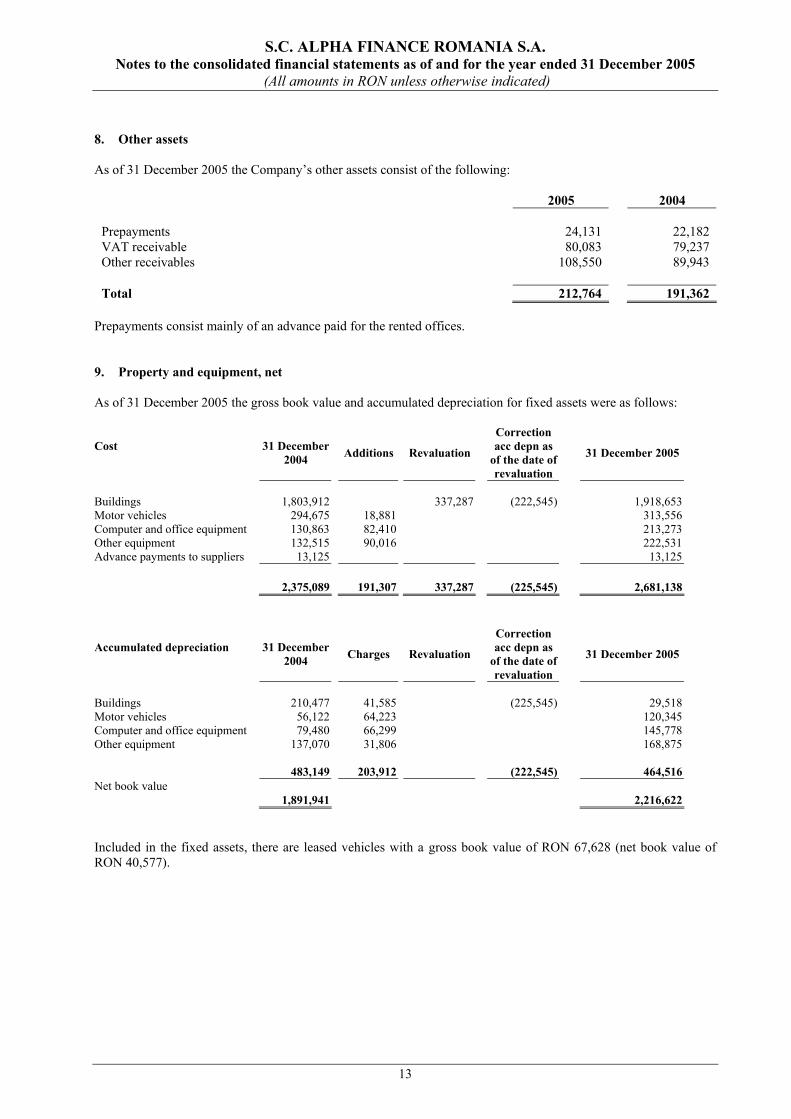

8. Other assets As of 31 December 2005 the Company’s other assets consist of the following:

2005 2004 Prepayments VAT receivable Other receivables

24,131 80,083

108,550

22,182 79,237 89,943

Total 212,764 191,362 Prepayments consist mainly of an advance paid for the rented offices. 9. Property and equipment, net As of 31 December 2005 the gross book value and accumulated depreciation for fixed assets were as follows: Cost 31 December

2004 Additions Revaluation

Correction acc depn as

of the date of revaluation

31 December 2005

Buildings 1,803,912 337,287 (222,545) 1,918,653Motor vehicles 294,675 18,881 313,556Computer and office equipment 130,863 82,410 213,273Other equipment 132,515 90,016 222,531Advance payments to suppliers 13,125 13,125

2,375,089 191,307 337,287 (225,545) 2,681,138

Accumulated depreciation 31 December

2004 Charges Revaluation

Correction acc depn as

of the date of revaluation

31 December 2005

Buildings 210,477 41,585 (225,545) 29,518Motor vehicles 56,122 64,223 120,345Computer and office equipment 79,480 66,299 145,778Other equipment 137,070 31,806 168,875 483,149 203,912 (222,545) 464,516Net book value

1,891,941 2,216,622 Included in the fixed assets, there are leased vehicles with a gross book value of RON 67,628 (net book value of RON 40,577).

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

14

10. Intangible assets, net As of 31 December 2005, the Company’s intangibles comprise of computer software as follows:

31 December 2004

Additions/ Charges Disposals 31 December

2005 Cost

115,074 17,034 - 132,108

Accumulated amortization 101,918 15,843 - 117,760 Net book value 13,156 14,348 11. Due to customers As of 31 December 2005 the amounts due to customers represent advances received for securities purchases. 12. Accrued expenses and other liabilities As of 31 December 2005, the Company’s accrued expenses and other liabilities consist of:

2005 2004 Payables to suppliers Income tax payable Other liabilities

70,537 -

1,145,635

20,2122,529

19,458 Total

1,216,172

42,199

13. Lease payables As of 31 December 2005 the Company’s lease payables consist of:

2005 2004 14,408 13,297Current lease payables

Non-current lease payables 27,214 41,622 Total 41,622 54,919 As of 31 December 2005 the Company has a motor vehicle finance facility for a period of 4 years with Alpha Leasing Romania (a related party).

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

15

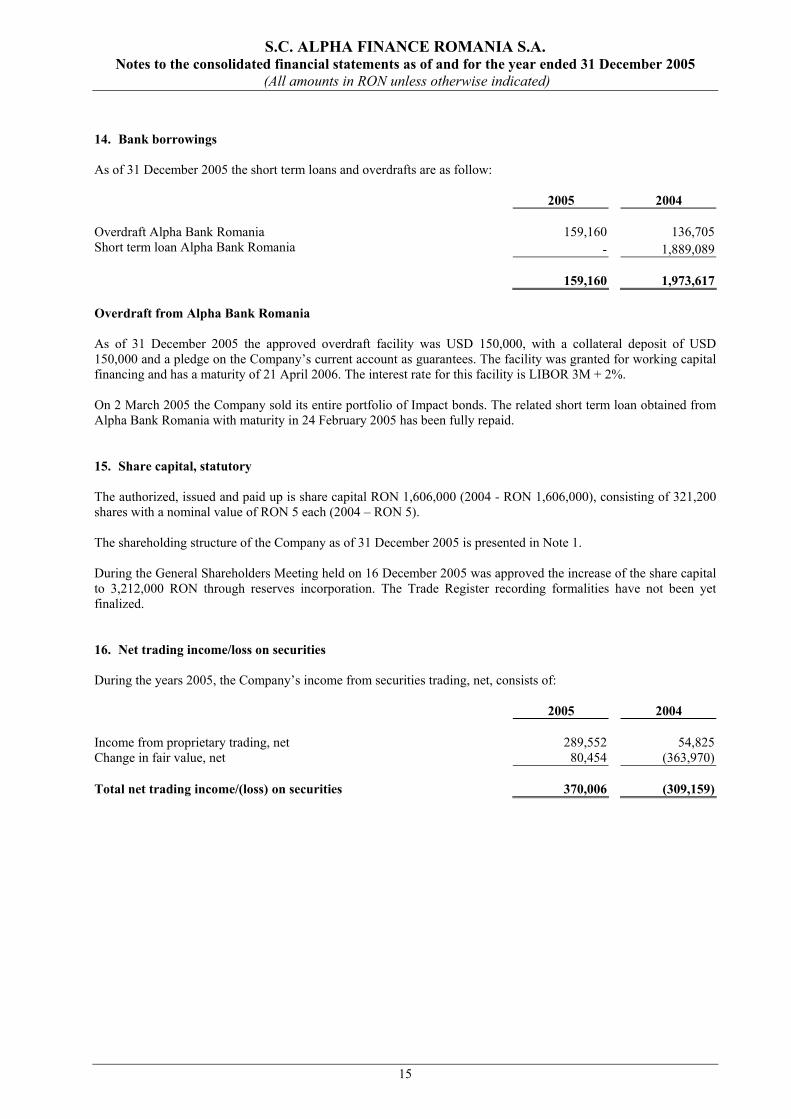

14. Bank borrowings As of 31 December 2005 the short term loans and overdrafts are as follow:

2005 2004 Overdraft Alpha Bank Romania 159,160 136,705Short term loan Alpha Bank Romania - 1,889,089 159,160 1,973,617 Overdraft from Alpha Bank Romania As of 31 December 2005 the approved overdraft facility was USD 150,000, with a collateral deposit of USD 150,000 and a pledge on the Company’s current account as guarantees. The facility was granted for working capital financing and has a maturity of 21 April 2006. The interest rate for this facility is LIBOR 3M + 2%. On 2 March 2005 the Company sold its entire portfolio of Impact bonds. The related short term loan obtained from Alpha Bank Romania with maturity in 24 February 2005 has been fully repaid. 15. Share capital, statutory The authorized, issued and paid up is share capital RON 1,606,000 (2004 - RON 1,606,000), consisting of 321,200 shares with a nominal value of RON 5 each (2004 – RON 5). The shareholding structure of the Company as of 31 December 2005 is presented in Note 1. During the General Shareholders Meeting held on 16 December 2005 was approved the increase of the share capital to 3,212,000 RON through reserves incorporation. The Trade Register recording formalities have not been yet finalized. 16. Net trading income/loss on securities During the years 2005, the Company’s income from securities trading, net, consists of:

2005 2004 Income from proprietary trading, net 289,552 54,825Change in fair value, net 80,454 (363,970) Total net trading income/(loss) on securities 370,006 (309,159)

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

16

17. Financial income, net

2005 2004 Interest income 381,591 487,223Foreign exchange differences, net gain 89,682 153,754Leasing interest to Alpha Leasing (3,670) (5,220)Interest expense (23,423) (81,456) Total financial income, net 444,180 554,301 Interest income represents mainly interest received on time deposits in 2005 (2004 – the same). 18. Operating expenses, net

2005 2004 Wages and salaries and 1,349,142 1,066,725Social insurance contributions 363,898 231,818Office premises rental expenses 331,654 329,208Offices premises expenses related to services from landlord 49,153 76,882Insurance costs 59,234 78,204Post and telecommunication 90,162 108,446Advertising and promotion 45,068 24,542Depreciation and amortization 144,390 127,794Commission and taxes 1,039,437 814,598Bank fees and other commissions 21,419 11,705Provisions for doubtful receivables 60,462 8,408Other administrative expenses 808,560 498,939 Total operating expenses 4,362,579 3,377,270 The average number of employees during 2005 was 22 full-time and 1 part-time (2004 - 18 full-time and 5 part-time) employees.

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

17

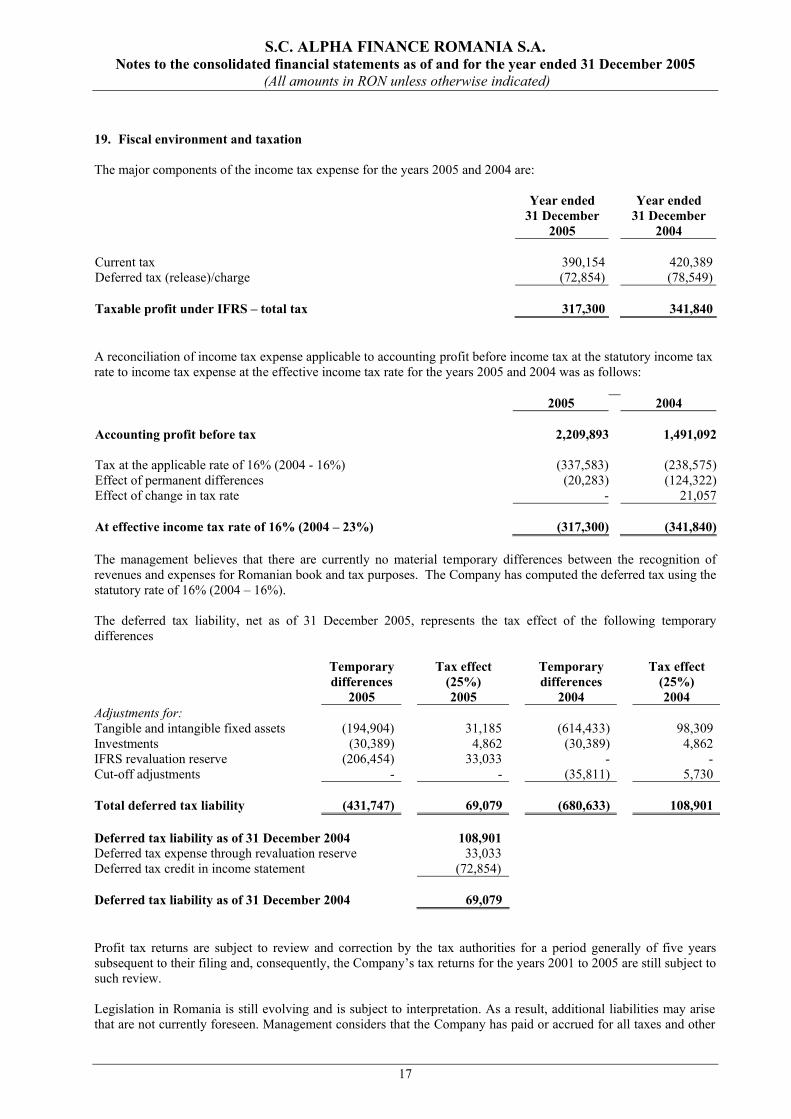

19. Fiscal environment and taxation The major components of the income tax expense for the years 2005 and 2004 are: Year ended

31 December 2005

Year ended 31 December

2004 Current tax 390,154 420,389Deferred tax (release)/charge (72,854) (78,549) Taxable profit under IFRS – total tax 317,300 341,840 A reconciliation of income tax expense applicable to accounting profit before income tax at the statutory income tax rate to income tax expense at the effective income tax rate for the years 2005 and 2004 was as follows: 2005 2004 Accounting profit before tax 2,209,893 1,491,092 Tax at the applicable rate of 16% (2004 - 16%) (337,583) (238,575)Effect of permanent differences (20,283) (124,322)Effect of change in tax rate - 21,057 At effective income tax rate of 16% (2004 – 23%) (317,300) (341,840) The management believes that there are currently no material temporary differences between the recognition of revenues and expenses for Romanian book and tax purposes. The Company has computed the deferred tax using the statutory rate of 16% (2004 – 16%). The deferred tax liability, net as of 31 December 2005, represents the tax effect of the following temporary differences

Temporary differences

2005

Tax effect (25%) 2005

Temporary differences

2004

Tax effect (25%) 2004

Adjustments for: Tangible and intangible fixed assets (194,904) 31,185 (614,433) 98,309 Investments (30,389) 4,862 (30,389) 4,862 IFRS revaluation reserve (206,454) 33,033 - - Cut-off adjustments - - (35,811) 5,730 Total deferred tax liability (431,747) 69,079 (680,633) 108,901 Deferred tax liability as of 31 December 2004 108,901 Deferred tax expense through revaluation reserve 33,033 Deferred tax credit in income statement (72,854) Deferred tax liability as of 31 December 2004 69,079 Profit tax returns are subject to review and correction by the tax authorities for a period generally of five years subsequent to their filing and, consequently, the Company’s tax returns for the years 2001 to 2005 are still subject to such review. Legislation in Romania is still evolving and is subject to interpretation. As a result, additional liabilities may arise that are not currently foreseen. Management considers that the Company has paid or accrued for all taxes and other

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

18

payments due to the State, that are applicable, in the financial statements as at 31 December 2004 and for the period then ended. However, the risk remains those relevant authorities could take differing positions with regard to interpretative issues and the effect could be significant. 20. Transactions and balances with related parties During 2004, the Company was involved in transactions with the following related parties: Alpha Bank Romania, Alpha Leasing Romania, Alpha Insurance, Alpha Brokerage Assets, and Alpha Finance Axepey. During 2005 the following transactions were carried out: 2005 2004 Expenses Interest charged by Alpha Bank Romania Bank commission expense charged by Alpha Bank Romania

(22,827) (19,295)

(86,739)(10,713)

Leasing interest expense charged by Alpha Leasing Romania (3,698) (5,249)Professional risk insurance premium charged by Alpha Insurance (43,371) (61,958)Consultancy services from Alpha Astika Greece (7,643)

(89,191) (172,302)Revenues Interest income received from Alpha Bank Romania 361,274 378,148Trading commission revenues received from Alpha Equity Fund 120,023 34,562Trading commission revenues received from Alpha Finance Axepay 1,469 29,920Research revenues from Alpha Leasing 20,811 32,700Income from trading commissions Alpha Insurance Romania 823Income from trading commissions Alpha Bank AE Income from trading commissions Alpha Mutual Fund Management Company SA

62,583

1,246

566,159 477,399

The balances with related parties at year-end are as follows: 2005 2004 Assets Term deposits in USD and RON at Alpha Bank Romania, including interest

7,595,139 3,916,053

Current accounts in USD, EUR and RON at Alpha Bank Romania 811,788 192,919Cash collateral for overdraft facility granted by Alpha Bank Romania 466,170 594,945

8,873,097 4,703,917Liabilities Overdraft facility granted by Alpha Bank Romania (159,160) (1,973,617)Lease liability for the financial lease agreement concluded with Alpha Leasing Romania

(36,217)

(45,845)

(195,377) (2,019,462) Directors’ remuneration For the year ended 31 December 2005 management emoluments amounted to RON 521,547 (2004 - RON 495,624).

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

19

21. Effect of adjustments and remeasurements The effect of adjustments and remeasurements of the financial statements prepared under Romanian Accounting Standards to the IFRS financial statements is the following:

Net income 2005

Shareholder’s equity 2005

Net income 2004 Shareholder’s

equity 2004 Balances under statutory financial statements

1,746,530 8,461,251

1,077,071

6,079,447

Adjustments: - Tangibles and intangibles restatement

(26,791) 11,791

5,297

91,990

- Consolidation elimination - (771,733) 38,710 (596,033)- Investments restatement - 30,389 (96,197) 30,389 - Cut-off adjustments - - 45,822 6,081- Reversal of statutory free shares from BSE

- (307,090) - -

- Deferred tax impact of the above 72,854 175,216 78,549 (108,901)

Net effect of adjustments 46,063 (861,428) 72,181 (576,474)

Balance under IFRS 1,792,593 7,599,823 1,149,252 5,502,973 22. Risk management a) Currency risk The Company manages its exposure to movements in exchange rates by modifying its assets and liabilities mix. The aggregated structure of assets and liabilities denominated in RON and foreign currencies (“FCY)”is as follows:

2005 2004 FCY RON FCY RON

Assets Non-current assets - 2,545,570 - 1,950,306Current assets 2,099,250 7,706,019 1,199,195 5,213,797 Total assets 2,099,250 10,251,589 1,199,195 7,164,103 Liabilities Non-current liabilities - 69,079 54,919 108,901Current liabilities 159,160 12,122,600 1,987,637 708,868

Total liabilities 159,160 12,191,679 2,042,556 817,769

S.C. ALPHA FINANCE ROMANIA S.A. Notes to the consolidated financial statements as of and for the year ended 31 December 2005

(All amounts in RON unless otherwise indicated)

20

22. Risk management (continued) b) Interest rate risk The interest rate risk refers to the fluctuation in the value of financial instruments due to the changes in market interest rates. This risk can mainly have a significant adverse effect on highly leveraged businesses, which is not the case of AFR. c) Market risk The Romanian securities market is not yet well developed and this presents a risk for companies with investment portfolios. In order to manage market risk, the Company has established limits on proprietary trading. d) Liquidity risk The liquidity risk is associated either to the difficulty of an enterprise to raise necessary funds in order to meet commitments or to its inability to sell a financial asset quickly at close to its fair value. The Company mitigates the liquidity risk through monitoring of its resources and placements. The Company’s financial assets and liabilities are considered to have no significant transaction costs and therefore their carrying value approximates their fair value. e) Cash flow risk The cash flow risk is deriving primarily from the liquidity risk and secondarily from the interest rate risk and market risk. As discussed in the paragraphs above, the Company is adequately planning and monitoring its cash flows and their influence factors. f) Credit/ Settlement risk The Company’s activity involves the execution, settlement and financing of clients securities transaction. These activities may expose the Company to settlement risk in the event the customer or other counter party is unable to fulfill its contracted obligations and the Company has to buy or sell financial instruments underlying the contract as a loss. 23. Contingencies and commitments Off balance sheet items The Company has powers of attorney over clients’ funds deposited with Alpha Bank Romania. As of 31 December 2005 the total balance on these accounts was of RON 12,642,127 (2004 – RON 8,308,250).