The duration gap model and clumping Session 2 Andrea Sironi Mafinrisk – 2010 Market Risk.

Upload

sarahi-turbevilleCategory

view

219download

2

ALM and Internal Transfer Rates

Session 3Andrea Sironi

MAFINRISK 2010Market Risk

2

Agenda

Objectives of a ITR system An example Gross and net ITR How to determine ITRs? Transactions with implicit options The ideal features of a ITR system

3

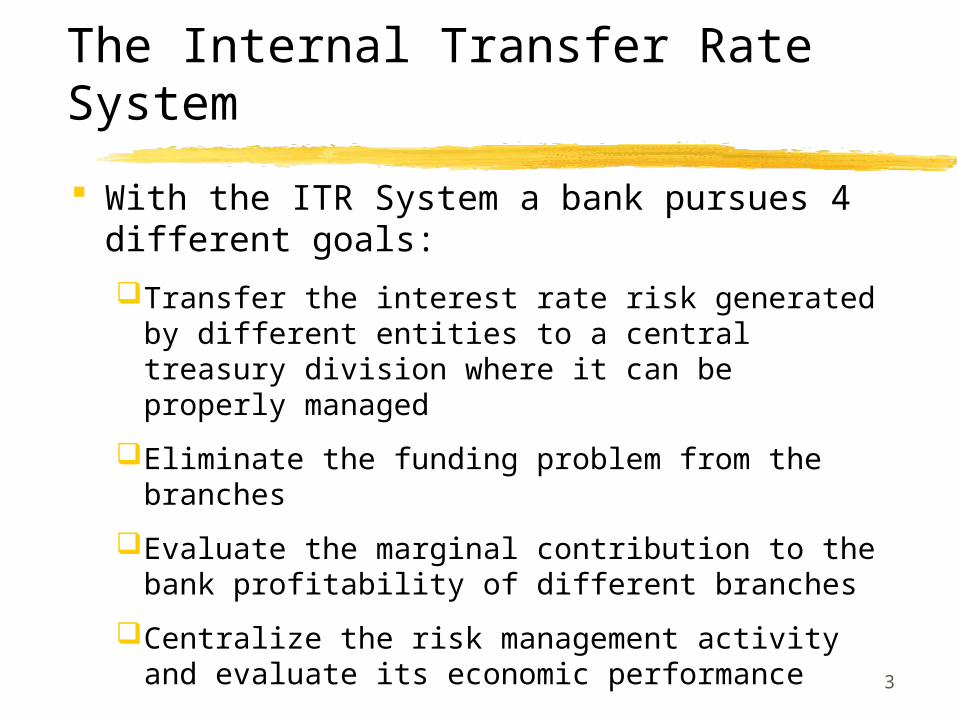

The Internal Transfer Rate System

With the ITR System a bank pursues 4 different goals:

Transfer the interest rate risk generated by different entities to a central treasury division where it can be properly managed

Eliminate the funding problem from the branches

Evaluate the marginal contribution to the bank profitability of different branches

Centralize the risk management activity and evaluate its economic performance

4

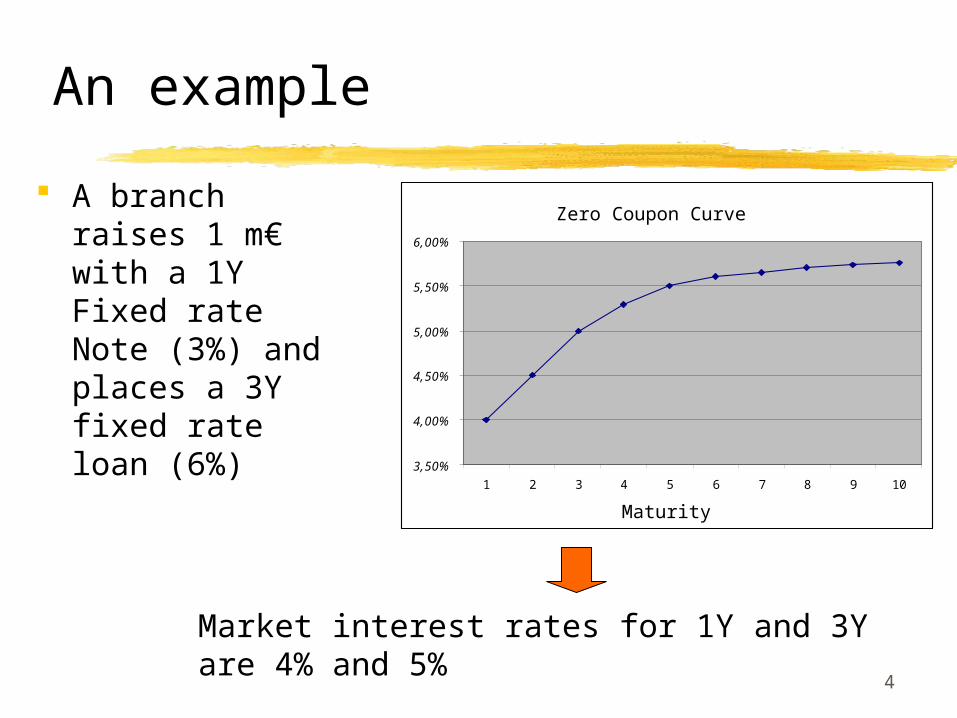

An example

A branch raises 1 m€ with a 1Y Fixed rate Note (3%) and places a 3Y fixed rate loan (6%)

Market interest rates for 1Y and 3Y are 4% and 5%

Curva dei tassi zero-coupon

3,50%

4,00%

4,50%

5,00%

5,50%

6,00%

1 2 3 4 5 6 7 8 9 10

Scadenza (anni)

Zero Coupon Curve

Maturity

5

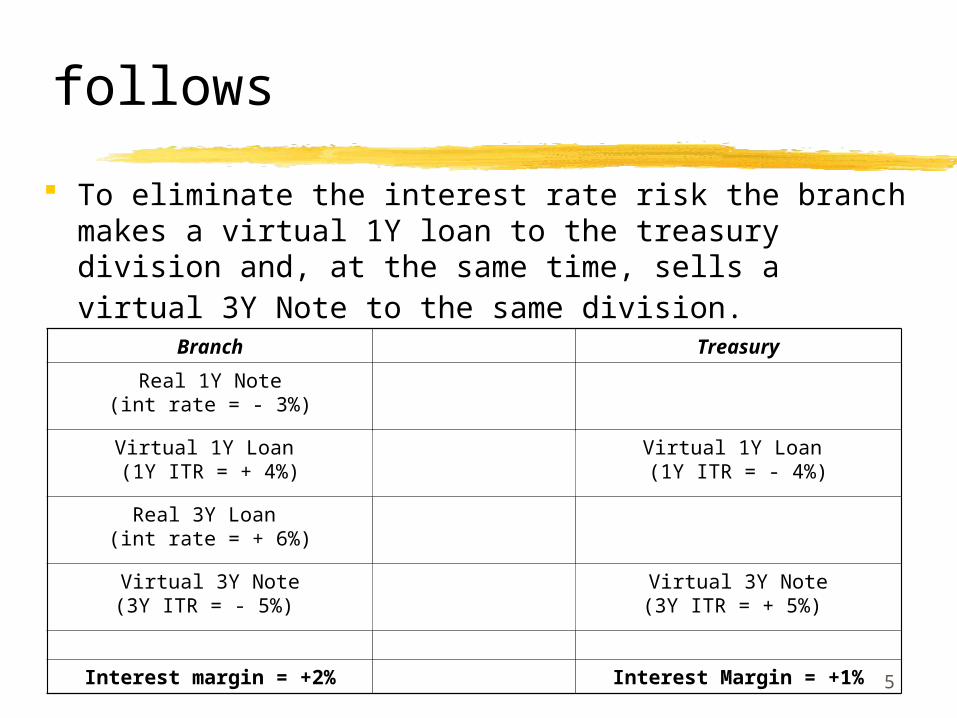

follows

To eliminate the interest rate risk the branch makes a virtual 1Y loan to the treasury division and, at the same time, sells a virtual 3Y Note to the same division.

Branch Treasury

Real 1Y Note(int rate = - 3%)

Virtual 1Y Loan (1Y ITR = + 4%)

Virtual 1Y Loan (1Y ITR = - 4%)

Real 3Y Loan (int rate = + 6%)

Virtual 3Y Note(3Y ITR = - 5%)

Virtual 3Y Note(3Y ITR = + 5%)

Interest margin = +2% Interest Margin = +1%

6

follows

Figure 2 – Example of how an ITR system works

Treasury Department

1 mln €1 year

4%

depositsloans

1 mln €3 years

5%

=20,000

Branch

1 mln €1 year

3%

depositsloans

1 mln €3 years

6%

+30,000

1 mln €1 year

4%

1 mln €3 years

5%

+10,000

-10,000

real deals fictitious deals profits/losses

Legend:

7

follows

The treasury receives an ex-ante interest margin of 1% (5% - 4%)

The treasury, in order to hedge the interest rate risk, should issue a 3Y note at the 5% market rate and make a 1Y loan at the 4% market rate. In this way the interest risk is hedged but the profit has gone.

Even if the treasury does not hedge the interest rate risk the interest margin of the operative branch is fixed. The risk has been transferred to the treasury division.

8

An example (continues)

If the yield curve were negatively sloped, the treasury margin would be negative treasury could realize hedging transactions aimed at eliminating risk and cancel the negative margin

The negative slope would reflect the interest rates decrease expectations if treasury does not hedge it would benefit from future interest rate changes

The branch would have a guaranteed 2% margin, which could in turn be divided into two components:

A positive margin given by the liability side (1% = 4%-3%), guaranteed for a one year time period A positive margin given by the asset side (1% = 6%-5%), guaranteed for a three years time period

9

Gross and net internal transfer rates

Internal transfer of gross cash flows every single cash inflow is virtually sent to the treasury division and every single cash outflow is virtually generated by the treasury division. The financial statement of the branches is perfectly hedged, only the treasury division bears some interest rate risk.

Internal transfer of net cash flows only the net cash flow of every operative branch is transferred to the treasury division. Part of the ALM is performed by the branches.

10

follows

A system based on the internal transfer of gross cash flows is usually preferred because:

A system based on the internal transfer of net cash flows uses a single transfer rate for cash flows at different maturities

A system based on the transfer of net cash flows leaves part of the interest rate risk to the branches

The interest rate risk of the bank is different form the sum of the exposures of the various branches.

11

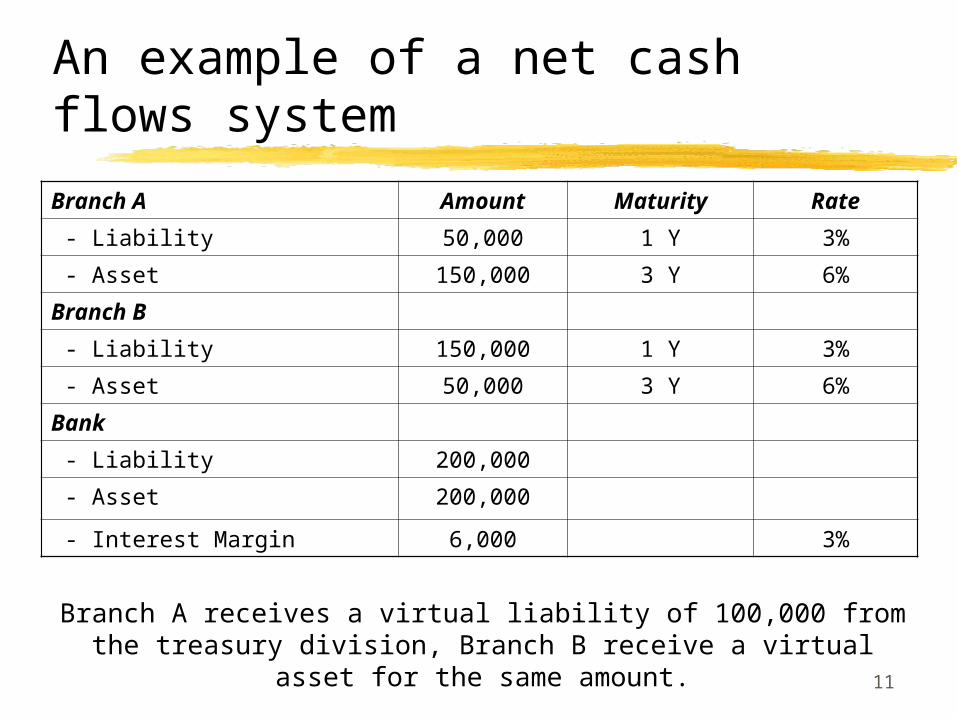

An example of a net cash flows system

Branch A receives a virtual liability of 100,000 from the treasury division, Branch B receive a virtual asset for the same

amount.

Branch A Amount Maturity Rate

- Liability 50,000 1 Y 3%

- Asset 150,000 3 Y 6%

Branch B

- Liability 150,000 1 Y 3%

- Asset 50,000 3 Y 6%

Bank

- Liability 200,000

- Asset 200,000

- Interest Margin 6,000 3%

12

follows

ITR= 1Y rate (4%) ITR= 2Y rate (4,5%) ITR= 3Y rate (5%)

Branch A Amount Maturity Rate Amount Maturity Rate Amount Maturity Rate

- Virtual liability 100,000 1 Y 4.00% 100,000 2 Y 4.50% 100,000 3 Y 5.00%

- Interest Margin 3,500 3,000 2,500

Branch B

- Virtual Asset 100,000 1 Y 4.00% 100,000 2 Y 4.50% 100,000 3 Y 5.00%

- Interest Margin 2,500 3,000 3,500

Treasury

- Virtual liability to A 100,000 1 Y 4.00% 100,000 2 Y 4.50% 100,000 3 Y 5.00%

- Virtual Asset from B 100,000 1 Y 4.00% 100,000 2 Y 4.50% 100,000 3 Y 5.00%

- Interest Margin 0 0.00% 0 0.00% 0 0.00%

interest margins 6,000 6,000 6.000

13

Net ITR

•We obtain different margins for the different branches depending on the ITR (1, 2 or 3 year maturity) we choose

•If 1 year ITR branch A, having funded a 3 year asset (150,000 euro) with a 1 year liability, is exposed to an increase in interest rates

•Branch B, having used part of its 1 year liabilities to fund a 3 year loan (50,000 euro), is exposed to a reduction of interest rates

•The interest rate risk is still within the branches

14

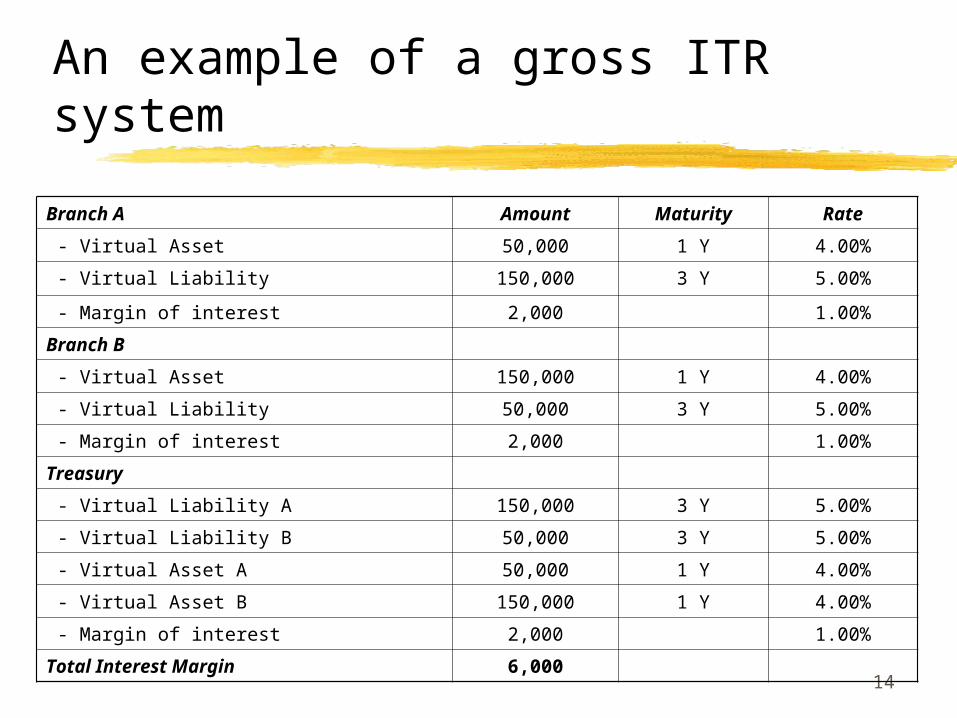

An example of a gross ITR system

Branch A Amount Maturity Rate

- Virtual Asset 50,000 1 Y 4.00%

- Virtual Liability 150,000 3 Y 5.00%

- Margin of interest 2,000 1.00%

Branch B

- Virtual Asset 150,000 1 Y 4.00%

- Virtual Liability 50,000 3 Y 5.00%

- Margin of interest 2,000 1.00%

Treasury

- Virtual Liability A 150,000 3 Y 5.00%

- Virtual Liability B 50,000 3 Y 5.00%

- Virtual Asset A 50,000 1 Y 4.00%

- Virtual Asset B 150,000 1 Y 4.00%

- Margin of interest 2,000 1.00%

Total Interest Margin 6,000

15

Gross ITR

• In this case all cash flows are transferred to the treasury at the conditions corresponding to their maturities

Multiple ITR

• The two branches economic results are equivalent (2,000 euro) and immunized from interest rate changes

• Interest rate risk is entirely transfered to the treasury

• If treasury wants to keep this interest rate risk, it would receive a 2,000 euro remuneration

16

The choice of the Internal Transfer Rates

The choice of the ITR should:

Be grounded on market rates (the rates should be representative of real investment/financing opportunities)

Distinguish between bid and ask rates. For a virtual liability we should use an ask rate, for a virtual asset a bid rate is the correct choice.

Consider every single cash flow as a separate operation.

17

The choice for a fixed rate operation

For a fixed rate operation the ITR is chosen only once at the very beginning of the operation.

Figure 3 – ITR for a fixed-rate transaction

5,000 – 4,000 = 1,000

Mortgage Internal debt

100,000 100,00010 years 10 years5% 4%

BranchMortgage Internal debt

100,000 100,00010 years 10 years5% 4%

Branch

Internal loan

100,00010 years5%

Treasury Dept.Internal loan

100,00010 years5%

Treasury Dept.Branch profit:

18

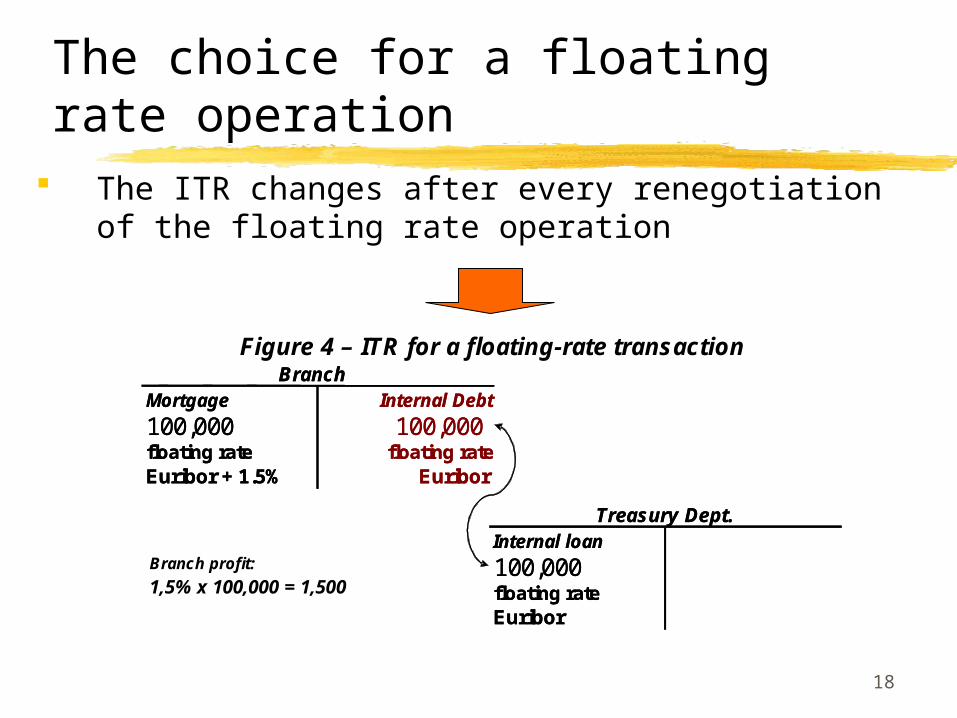

The choice for a floating rate operation

The ITR changes after every renegotiation of the floating rate operation

Figure 4 – ITR for a floating-rate transaction

1,5% x 100,000 = 1,500Branch profit:

Mortgage Internal Debt

100,000 100,000floating rate floating rateEuribor + 1.5% Euribor

BranchMortgage Internal Debt

100,000 100,000floating rate floating rateEuribor + 1.5% Euribor

Branch

Internal loan

100,000floating rateEuribor

Treasury Dept.Internal loan

100,000floating rateEuribor

Treasury Dept.

19

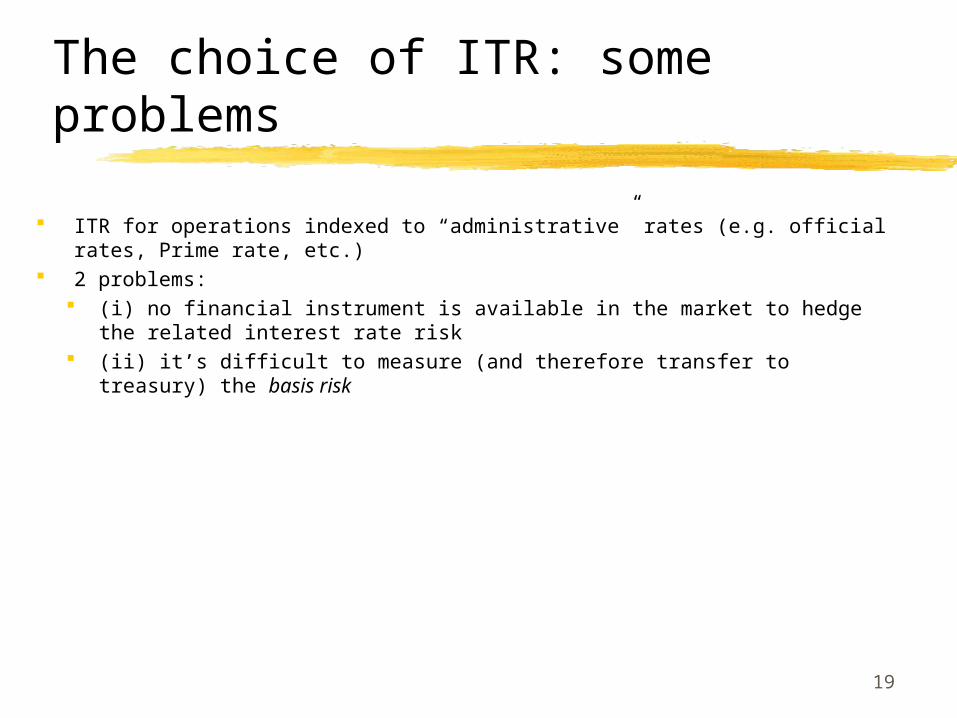

The choice of ITR: some problems

ITR for operations indexed to “administrative” rates (e.g. official rates, Prime rate, etc.)

2 problems: (i) no financial instrument is available in the market to hedge the related

interest rate risk (ii) it’s difficult to measure (and therefore transfer to treasury) the basis risk

20

The choice of ITR: some problems

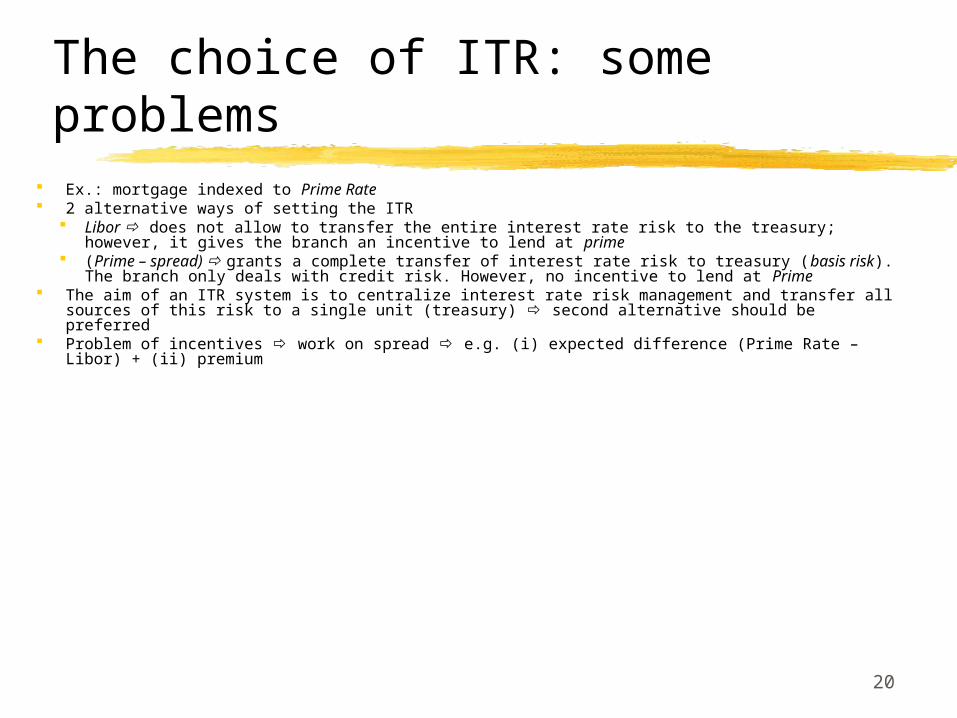

Ex.: mortgage indexed to Prime Rate 2 alternative ways of setting the ITR

Libor does not allow to transfer the entire interest rate risk to the treasury; however, it gives the branch an incentive to lend at prime

(Prime – spread) grants a complete transfer of interest rate risk to treasury (basis risk). The branch only deals with credit risk. However, no incentive to lend at Prime

The aim of an ITR system is to centralize interest rate risk management and transfer all sources of this risk to a single unit (treasury) second alternative should be preferred

Problem of incentives work on spread e.g. (i) expected difference (Prime Rate – Libor) + (ii) premium

21

The choice of ITR: some problems

Example 1 A branch grants a mortgage indexed to Prime

Rate + 0.25% Based on historical data, the bank estimates that:

Prime Rate = Libor + 2% ITR is not set as “Prime Rate - 2%”, but rather as:

Prime Rate - (2%+k)

Branch result 2.25%+k k is included in order to give the branch an

incentive to lend at a favourable rate Prime rate tends to decrease at a slower pace when market rates decrease and viceversa

22

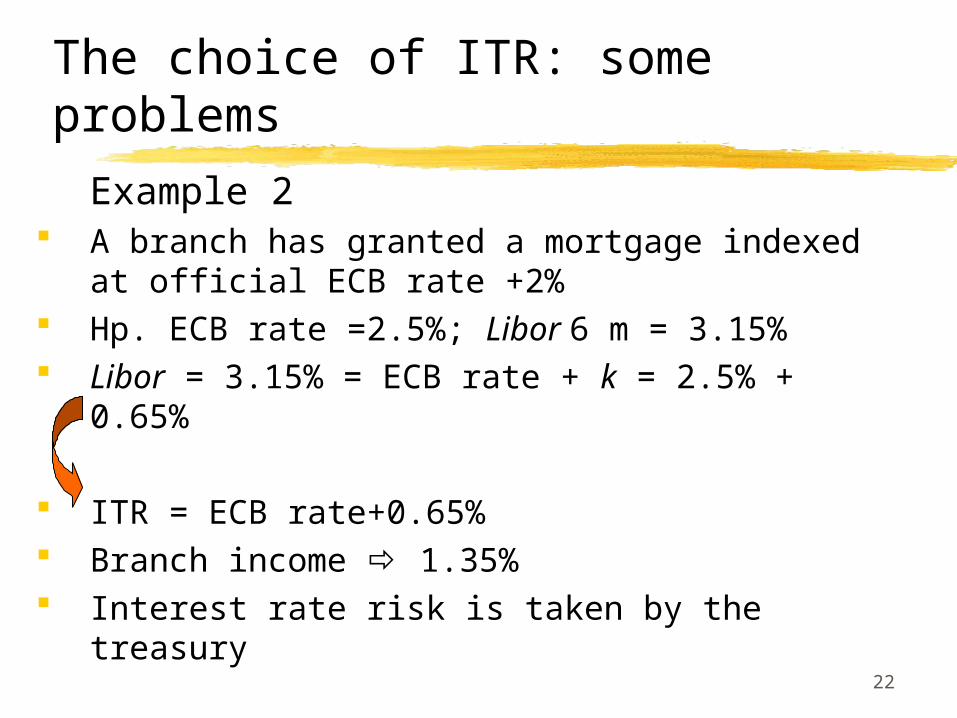

The choice of ITR: some problems

Example 2 A branch has granted a mortgage indexed

at official ECB rate +2% Hp. ECB rate =2.5%; Libor 6 m = 3.15% Libor = 3.15% = ECB rate + k = 2.5% +

0.65%

ITR = ECB rate+0.65% Branch income 1.35% Interest rate risk is taken by the treasury

23

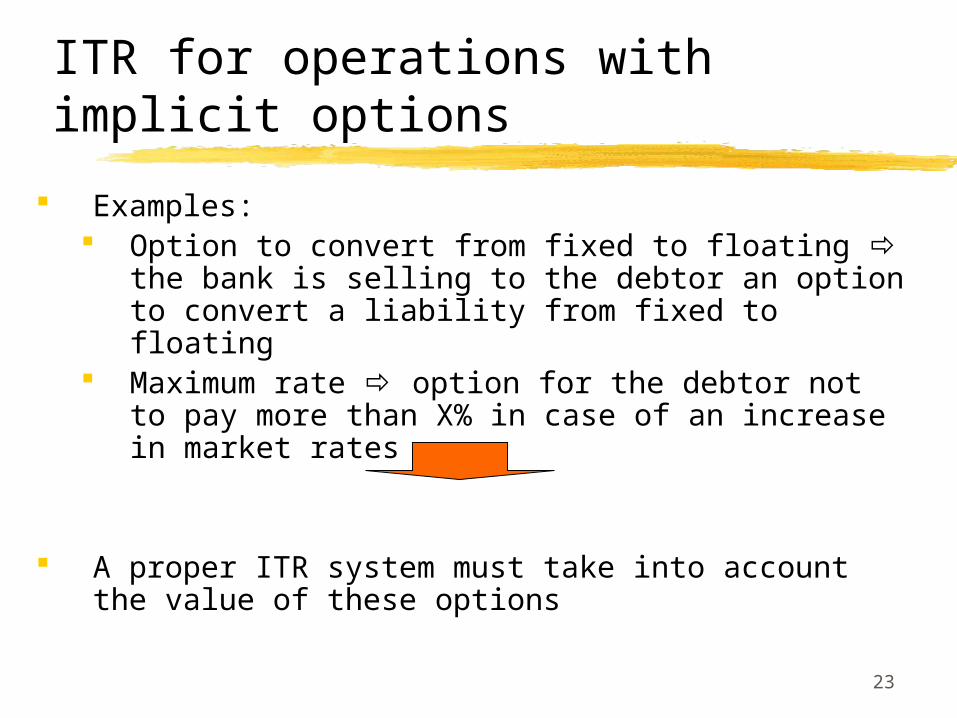

ITR for operations with implicit options

Examples: Option to convert from fixed to floating the

bank is selling to the debtor an option to convert a liability from fixed to floating

Maximum rate option for the debtor not to pay more than X% in case of an increase in market rates

A proper ITR system must take into account the value of these options

24

ITR for operations with implicit options Mortgage with the option to convert from fixed to

floating (or viceversa) is equivalent to a loan + sale of a swaption the buyer gets the right but not the obligation to buy at a future date and at predefined conditions (fixed rate and maturity) an Interest Rate Swap

Table 6 – Example of a loan converted from a fixed to a floating rate Date Interest on the

loan Interest Rate Swap flows

(from when the swaption is exercised)

Final net flows

+ 1 year -7% (not available) -7% + 2 years -7% +7% -(Libor+s) -(Libor+s) + 3 years -7% +7% -(Libor+s) -(Libor+s)

25

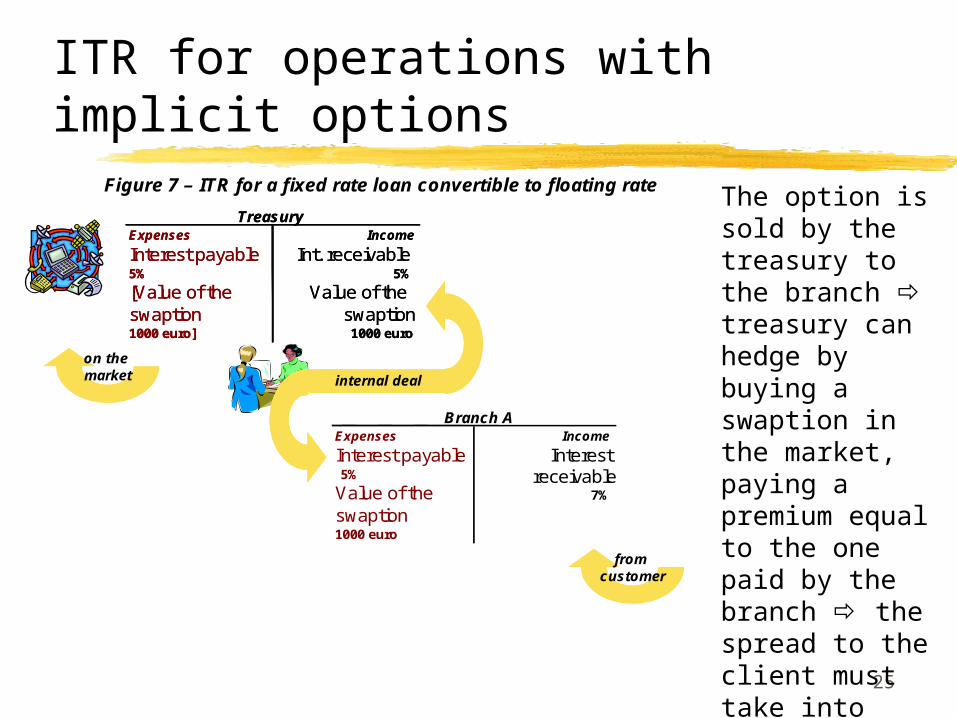

ITR for operations with implicit options

Figure 7 – ITR for a fixed rate loan convertible to floating rate

on the market

fromcustomer

Expenses Income

Interest payable Interest receivable5%

7%Value of the swaption1000 euro

Branch A

Expenses Income

Interest payable Int. receivable5% 5%

[Value of theswaption

Value of theswaption

1000 euro] 1000 euro

TreasuryExpenses Income

Interest payable Int. receivable5% 5%

[Value of theswaption

Value of theswaption

1000 euro] 1000 euro

Treasury

internal deal

The option is sold by the treasury to the branch treasury can hedge by buying a swaption in the market, paying a premium equal to the one paid by the branch the spread to the client must take into account the cost of the swaption

26

ITR for operations with implicit options Maximum rate the bank has sold to the client an

interest rate cap the implicit option must be paid by the customer

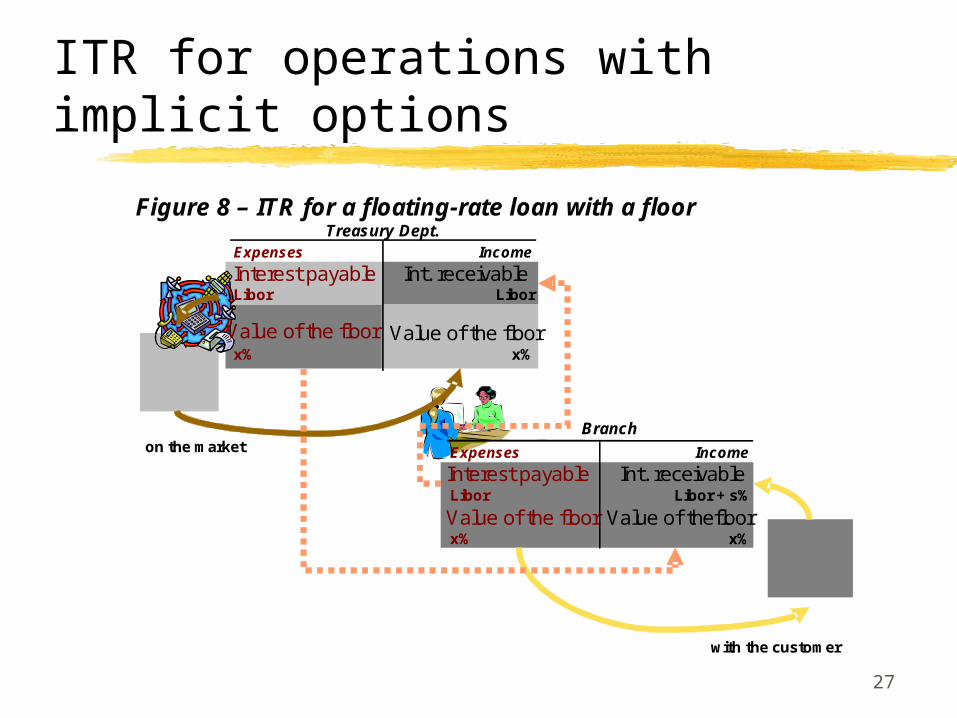

Minimum rate the bank has bought an interest rate floor from the client the branch sells the floor to the treasury

27

ITR for operations with implicit options

Figure 8 – ITR for a floating-rate loan with a floor

Expenses Income

Interest payable Int. receivableLibor Libor

Value of the floor Value of the floorx% x%

Treasury Dept.

Expenses Income

Interest payable Int. receivableLibor Libor + s%

Value of the floor Value of thefloorx% x%

Branchon the market

with the customer

28

ITR for operations with implicit options

Max and Min rates for a loan When the bank funds a client at floating interest

rate fixing: A maximum rate (the client company will never pay more then a

predefined threshold); A minimum rate (the client company will never pay less then a

predefined threshold);

…the bank is implicitly selling the client an Interest Rate Cap and, at the same time, buying from the client an Interest Rate Floor selling an Interest Rate Collar

the client company must pay a premium for the acquisition of the cap and at the same time receive a premium for the sale of the floor

29

ITR for operations with implicit options

Example: a client gets a loan at “Libor+s” and buys a collar (max rate 7%, min rate 4%) paying a premium (cap value > floor value) treasury sells the collar to the branch; the branch in turn sells the collar to the client

If Libor becomes equal to 3.5%, the client must pay the difference between floor rate and market rate to the branch (0.5%); the same must be done by the branch to the treasury

If Libor goes to 7.5%, the branch must pay to the client the difference between market rate and cap rate; the same must be done by the treasury to the branch

30

ITR for operations with implicit options

Prepayment option The borrower has bought an option to buy back

the loan before maturity This option must be paid by the borrower to

the branch The branch in turn is selling this option to the

treasury If interest rates decrease and the borrower

exercises the option, then the branch would in turn exercise the option with the treasury

31

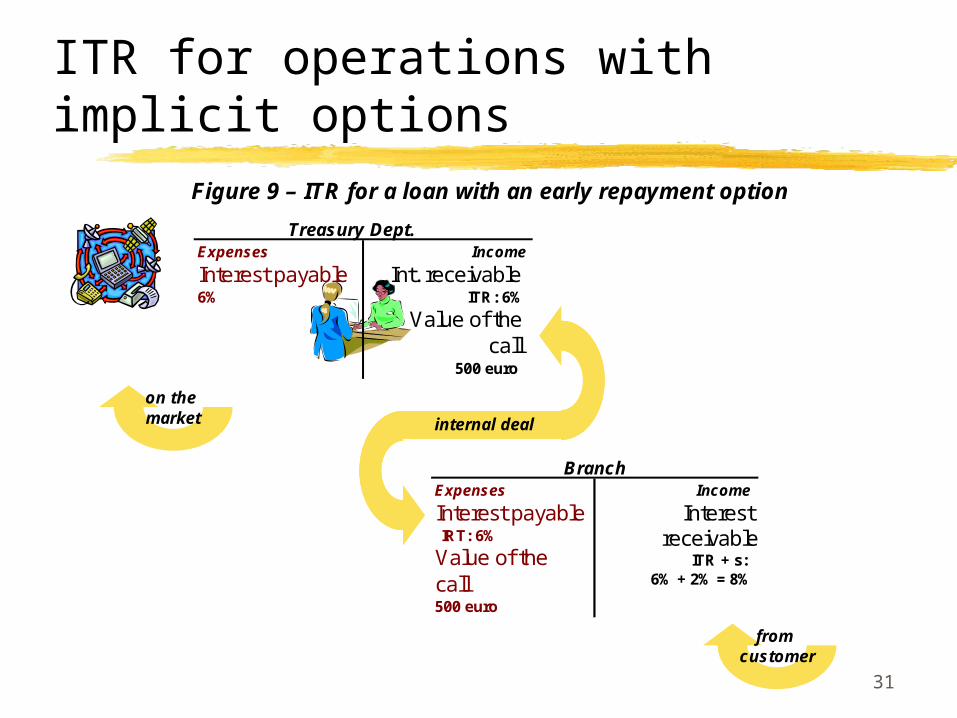

ITR for operations with implicit options

Figure 9 – ITR for a loan with an early repayment option

on the market

fromcustomer

Expenses Income

Interest payable Interest receivableIRT: 6%

ITR + s: 6% + 2% = 8%

Value of the call500 euro

Branch

Expenses Income

Interest payable Int. receivable6% ITR: 6%

Value of thecall

500 euro

Treasury Dept.

internal deal

32

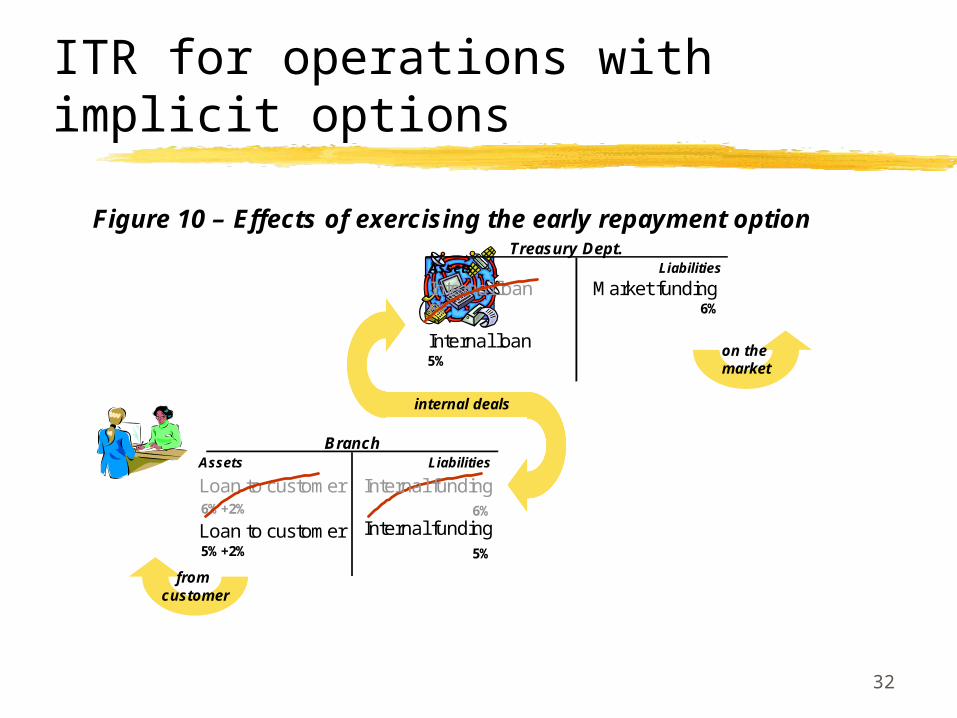

ITR for operations with implicit options

Figure 10 – Effects of exercising the early repayment option

on the market

fromcustomer

Assets Liabilities

Loan to customer Internal funding5%+2% 5%

Branch

Assets Liabilities

Internal loan Market funding6% 6%

Treasury Dept.

internal deals

Internal loan5%

Loan to customer6%+2%

Internal funding6%

33

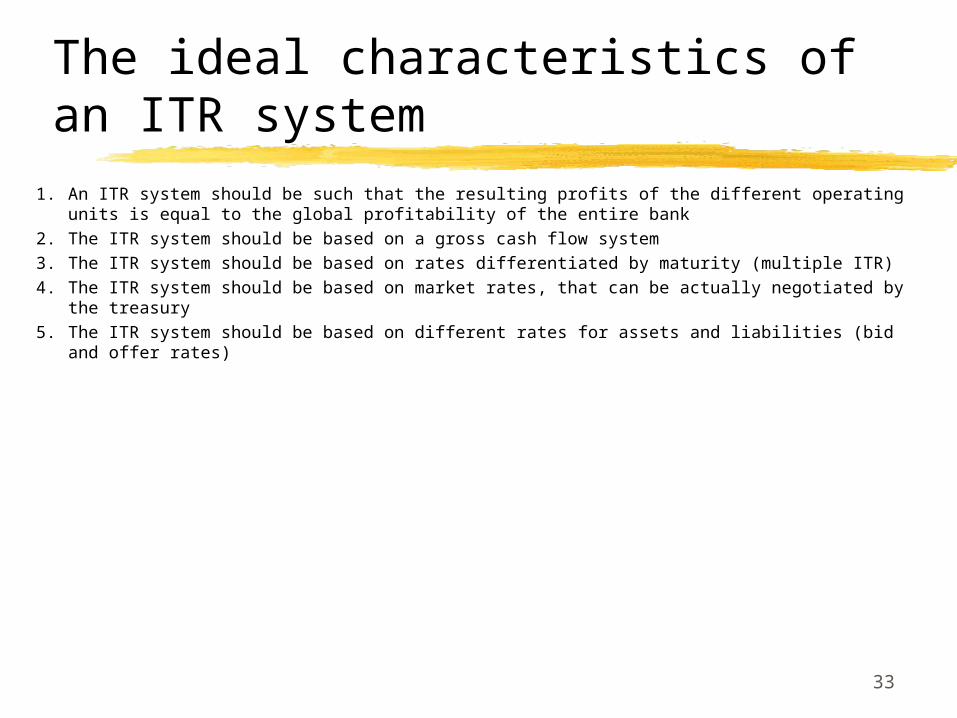

The ideal characteristics of an ITR system

1. An ITR system should be such that the resulting profits of the different operating units is equal to the global profitability of the entire bank

2. The ITR system should be based on a gross cash flow system3. The ITR system should be based on rates differentiated by maturity (multiple ITR)4. The ITR system should be based on market rates, that can be actually negotiated by the

treasury5. The ITR system should be based on different rates for assets and liabilities (bid and offer

rates)

34

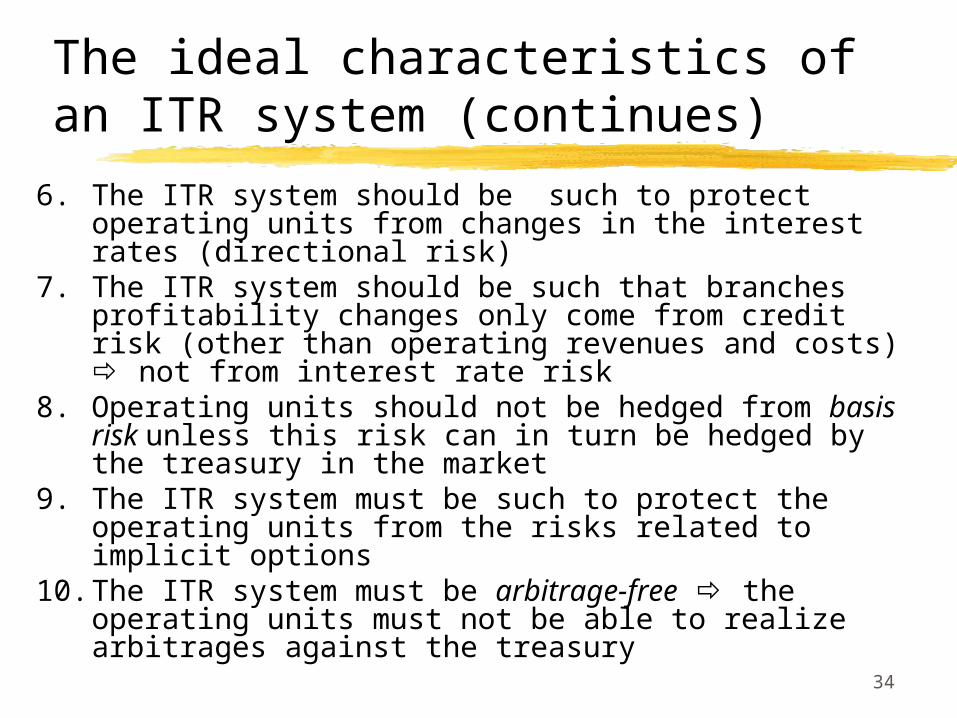

The ideal characteristics of an ITR system (continues)

6. The ITR system should be such to protect operating units from changes in the interest rates (directional risk)

7. The ITR system should be such that branches profitability changes only come from credit risk (other than operating revenues and costs) not from interest rate risk

8. Operating units should not be hedged from basis risk unless this risk can in turn be hedged by the treasury in the market

9. The ITR system must be such to protect the operating units from the risks related to implicit options

10. The ITR system must be arbitrage-free the operating units must not be able to realize arbitrages against the treasury

35

Questions & Exercises

1. Branch A of a bank only has fixed-rate deposits, with a maturity of one year, for 100 million euros; branch B has only fixed-rate loans, for the same amount, with a maturity of 3 years. Market rates, on the 1 and 3 year maturity respectively, currently are 5% and 4%. Consider the following statements:

I. One cannot use market rates as ITRs, as they would lead to a negative margin for the Treasury Unit;

II. 3- and 4-years ITRs must be set exactly at 5% and 4%;III. The Treasury Unit can both hedge interest rate risk and

meanwhile have a positive net income;IV. The Treasury Unit can hedge interest rate risk, but doing so

would bring its net income down to zero.

Which one(s) is (are) correct?A. All four.B. II and IV.C. I and IIID. II and III.

36

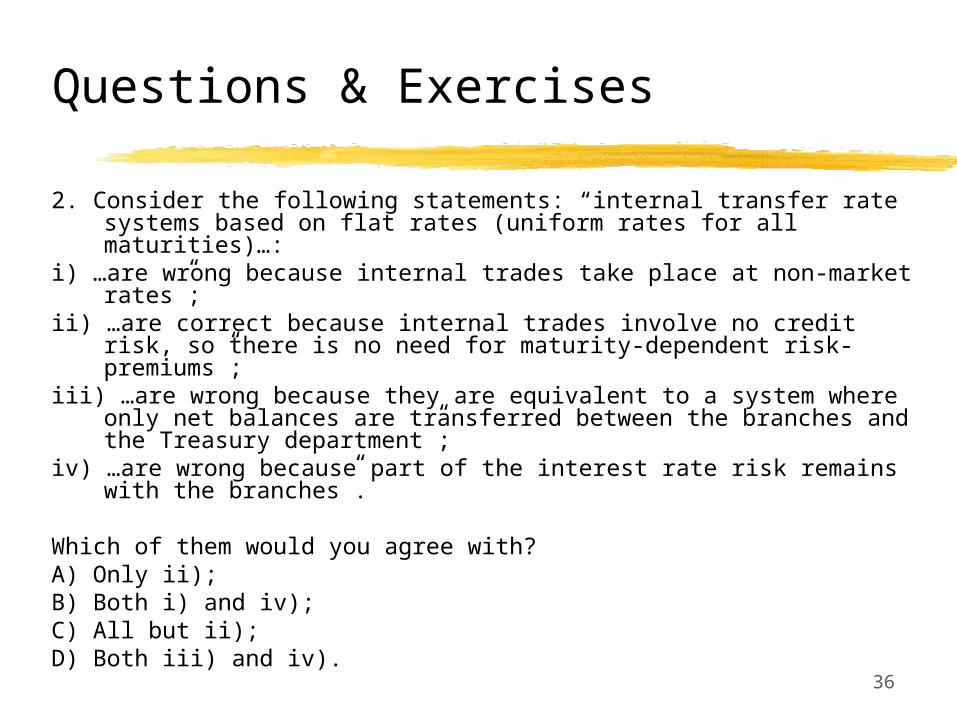

Questions & Exercises

2. Consider the following statements: “internal transfer rate systems based on flat rates (uniform rates for all maturities)…:

i) …are wrong because internal trades take place at non-market rates”;

ii) …are correct because internal trades involve no credit risk, so there is no need for maturity-dependent risk-premiums”;

iii) …are wrong because they are equivalent to a system where only net balances are transferred between the branches and the Treasury department”;

iv) …are wrong because part of the interest rate risk remains with the branches”.

Which of them would you agree with?A) Only ii);B) Both i) and iv);C) All but ii);D) Both iii) and iv).

37

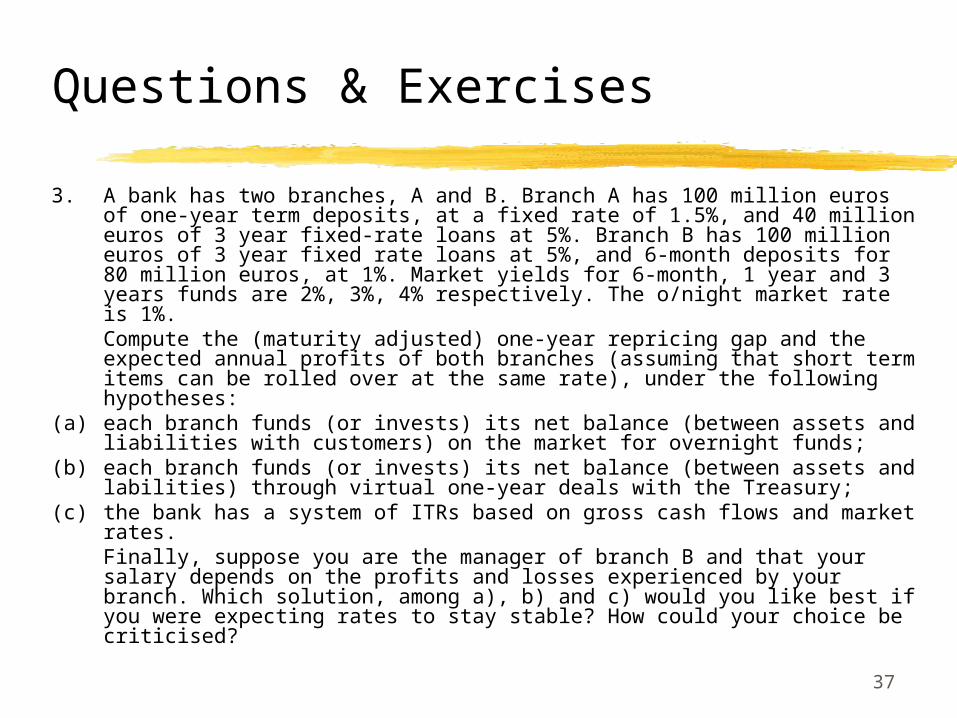

Questions & Exercises

3. A bank has two branches, A and B. Branch A has 100 million euros of one-year term deposits, at a fixed rate of 1.5%, and 40 million euros of 3 year fixed-rate loans at 5%. Branch B has 100 million euros of 3 year fixed rate loans at 5%, and 6-month deposits for 80 million euros, at 1%. Market yields for 6-month, 1 year and 3 years funds are 2%, 3%, 4% respectively. The o/night market rate is 1%.Compute the (maturity adjusted) one-year repricing gap and the expected annual profits of both branches (assuming that short term items can be rolled over at the same rate), under the following hypotheses:

(a) each branch funds (or invests) its net balance (between assets and liabilities with customers) on the market for overnight funds;

(b) each branch funds (or invests) its net balance (between assets and labilities) through virtual one-year deals with the Treasury;

(c) the bank has a system of ITRs based on gross cash flows and market rates.Finally, suppose you are the manager of branch B and that your salary depends on the profits and losses experienced by your branch. Which solution, among a), b) and c) would you like best if you were expecting rates to stay stable? How could your choice be criticised?

38

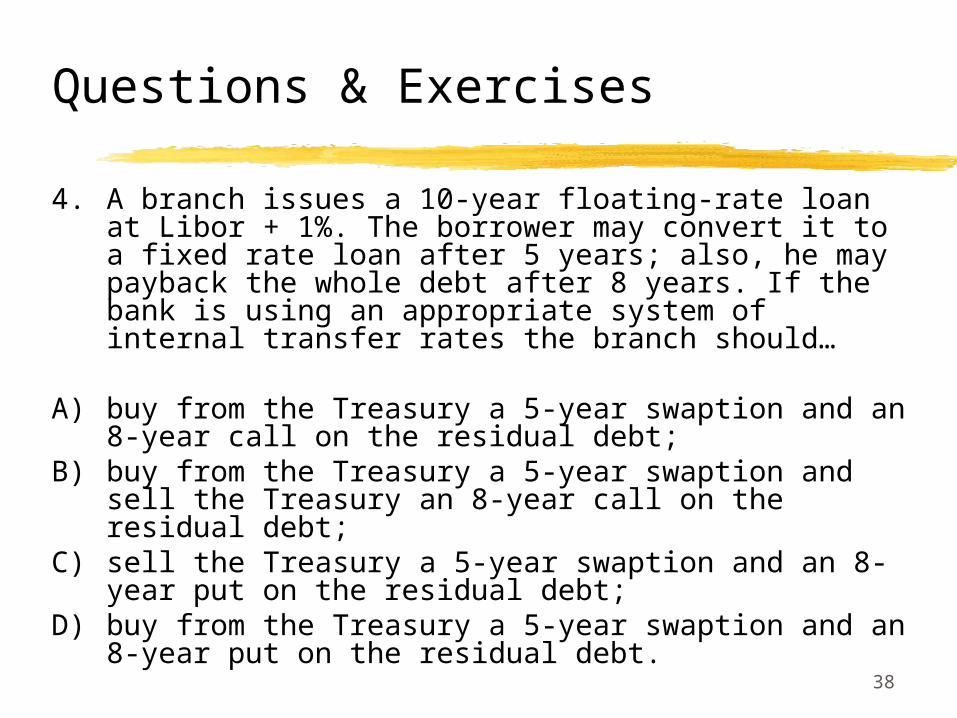

Questions & Exercises

4. A branch issues a 10-year floating-rate loan at Libor + 1%. The borrower may convert it to a fixed rate loan after 5 years; also, he may payback the whole debt after 8 years. If the bank is using an appropriate system of internal transfer rates the branch should…

A) buy from the Treasury a 5-year swaption and an 8-year call on the residual debt;

B) buy from the Treasury a 5-year swaption and sell the Treasury an 8-year call on the residual debt;

C) sell the Treasury a 5-year swaption and an 8-year put on the residual debt;

D) buy from the Treasury a 5-year swaption and an 8-year put on the residual debt.

39

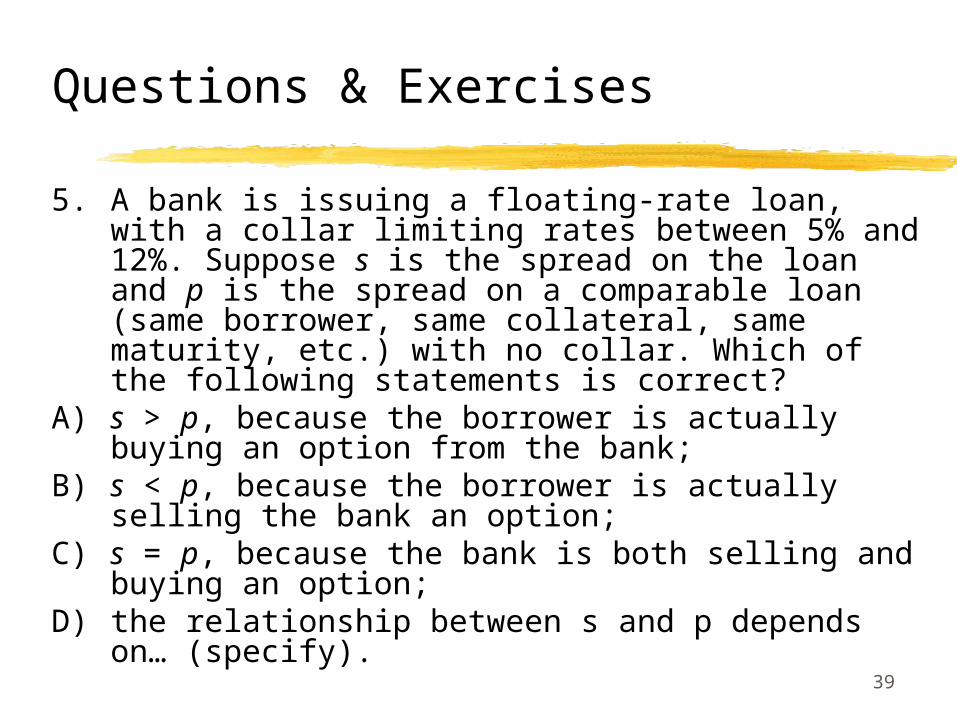

Questions & Exercises

5. A bank is issuing a floating-rate loan, with a collar limiting rates between 5% and 12%. Suppose s is the spread on the loan and p is the spread on a comparable loan (same borrower, same collateral, same maturity, etc.) with no collar. Which of the following statements is correct?

A) s > p, because the borrower is actually buying an option from the bank;

B) s < p, because the borrower is actually selling the bank an option;

C) s = p, because the bank is both selling and buying an option;

D) the relationship between s and p depends on… (specify).