Allied Bank

175

BRANCHES & ATMS Online Banking facilities are available to customers maintaining accounts at all online branches across the country. Following facilities are available Cash Deposit for immediate credit to a remote branch. Remote Cheque Encashment from any online branch. Instant Funds Transfer between any 2 online branches. Remote Balance Inquiry and Statement of Account. Additionally, account holders of all online branches can obtain Allied Cash+Shop Visa Debit Card for use at ATMs as well as at POS terminals. Click Here to view the List of Branches Open on Saturdays. Home Business Banking Home Remittances To Pakistan o Business Banking Corporate and Investment Banking Transaction and Business Accounts

-

Upload

tabeena-noor -

Category

Documents

-

view

76 -

download

0

Transcript of Allied Bank

BRANCHES & ATMS

Online Banking facilities are available to customers maintaining accounts at all online branches across the country. Following facilities are available

Cash Deposit for immediate credit to a remote branch.

Remote Cheque Encashment from any online branch.

Instant Funds Transfer between any 2 online branches.

Remote Balance Inquiry and Statement of Account.

Additionally, account holders of all online branches can obtain Allied Cash+Shop Visa Debit Card for use

at ATMs as well as at POS terminals.

Click Here to view the List of Branches Open on Saturdays.

Home

Business Banking

Home Remittances To Pakistan

o Business Banking Corporate and Investment Banking Transaction and Business Accounts Home Remittances to Pakistan Savings & Term Deposits Cash Management Solutions

Trade Services SME Financing Agriculture Financing

HOME REMITTANCES TO PAKISTAN

Allied Express – Home Remittance Distribution Service

ABL has been significantly important in helping the growth of home remittances to Pakistan through its

streamlined and trusted services. We are working continuously to develop innovative ideas into service

features that allow us to process and payout remittances even faster resulting in greater customer

satisfaction.

ABL’s real-time online branch network – one of the largest networks in Pakistan, consists of over 830

branches in 300 cities and town, providing comprehensive domestic distribution of remittances to

Beneficiaries across Pakistan.

A host of renowned international banks, exchange houses and money transfer companies from across

the world, including the Middle East, Europe, Asia-Pacific and North America, have been using our

services with utmost trust and satisfaction.

A number of options are available to non-resident Pakistanis through our service, including Direct Credit

to Account, Cash Payment over the Counter and issuance of Allied Express cheques, a payment

instrument that is honored across the entire ABL network of branches.

Please contact us to explore the ABL home remittances value proposition on +92-21-35301043

or [email protected]. For a more detailed review of what we do and how we do it, you may

download the presentation from this link.

Allied ExpressPDFDownload

o Allied Direct

o Remittance Tracker

o Newsletter

o Download

o Contact

Subscribe to Our Email Newsletter

YOU MAY ALSO BE INTERESTED

o Write to Us o Download our Annual Reports o Switch Kit

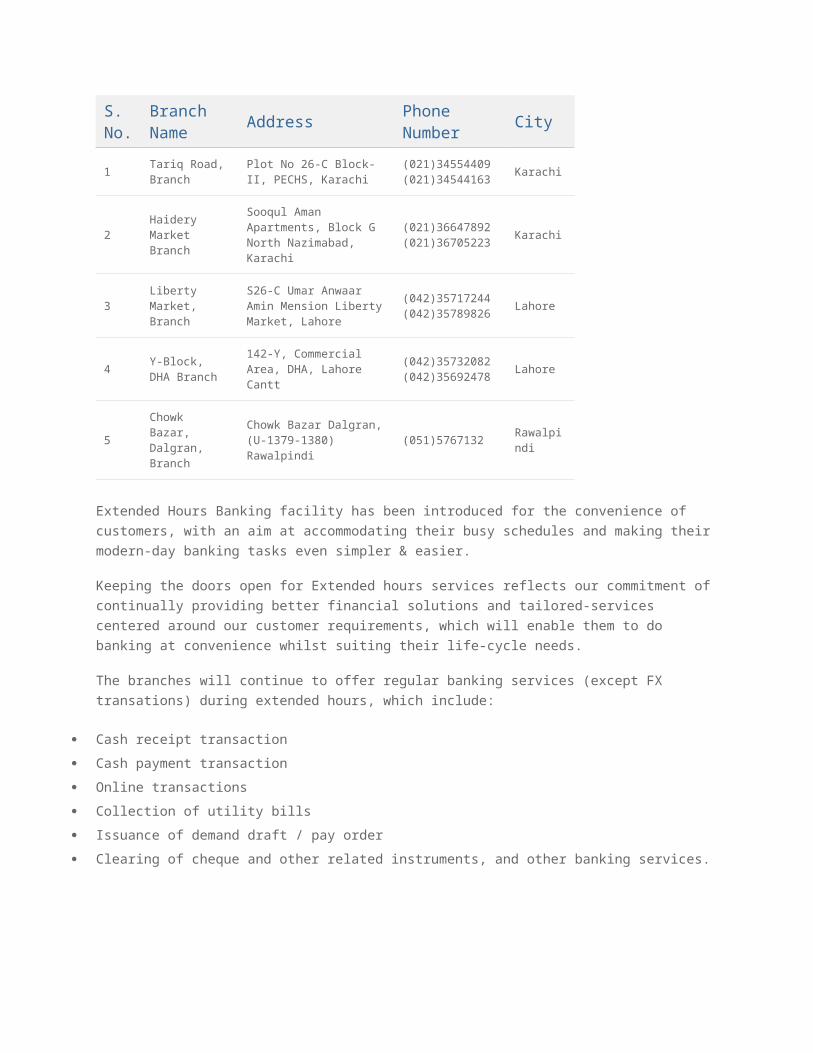

EXTENDED HOURS BANKING

Helping Customers Do Their Banking by Extending Our Branch Business Hours

ABL is pleased to offer Extended Hours Banking Services for its valued customers.

The following selected branches will remain open from 9:00am to 8:00pm from (Monday to Friday) and

from 9:00am to 5:00pm on Saturdays:

S. No.

Branch Name

AddressPhone Number

City

1Tariq Road, Branch

Plot No 26-C Block-II, PECHS, Karachi

(021)34554409 (021)34544163

Karachi

2Haidery Market Branch

Sooqul Aman Apartments, Block G North Nazimabad, Karachi

(021)36647892 (021)36705223

Karachi

3Liberty Market, Branch

S26-C Umar Anwaar Amin Mension Liberty Market, Lahore

(042)35717244 (042)35789826

Lahore

GO

4Y-Block, DHA Branch

142-Y, Commercial Area, DHA, Lahore Cantt

(042)35732082 (042)35692478

Lahore

5Chowk Bazar, Dalgran, Branch

Chowk Bazar Dalgran, (U-1379-1380) Rawalpindi

(051)5767132 Rawalpindi

Extended Hours Banking facility has been introduced for the convenience of customers, with an aim at

accommodating their busy schedules and making their modern-day banking tasks even simpler & easier.

Keeping the doors open for Extended hours services reflects our commitment of continually providing

better financial solutions and tailored-services centered around our customer requirements, which will

enable them to do banking at convenience whilst suiting their life-cycle needs.

The branches will continue to offer regular banking services (except FX transations) during extended

hours, which include:

Cash receipt transaction

Cash payment transaction

Online transactions

Collection of utility bills

Issuance of demand draft / pay order

Clearing of cheque and other related instruments, and other banking services.

ONLINE BANKING

Enjoy Real-time Online Banking service at any Allied Bank Branch. Allied Bank is the only bank in Pakistan offering 100% online branch network. Wherever you go around the country, you can access and do transaction through your ABL bank account from any Allied Bank Branch.

Deposit Cash for instant credit into the account

Withdraw Cash through cheque from any ABL Branch

Make Balance Enquiry and get Account Statement from any Allied Bank Branch

Transfer funds from one ABL account to any other ABL account across the country

Maximize the productivity of your business or financial management with Allied Bank’s Online Banking

facilities. It is a secure, efficient and convenient way to collect your payments faster, optimize the timing of

disbursement of funds, and maintain better control over your funds.

CUSTOMER SUPPORT

The better we treat our customers, the more we do for them, the better relationship we enjoy with them.

At Allied Bank, we give our customers diversified options to interact with us and let them experience the

joy of banking with us, every time they contact us through any of our touchpoints.

Interact with Allied Bank for information, queries, suggestions, complaints because we love to learn from

our customers

Email us

General Info: [email protected]

Human Resource: [email protected]

Complaint Management Unit: [email protected]

Call us

0800-22522 – Allied Phone Banking

Security Center

Confidentiality of our customers is foremost at Allied Bank.

We adopt multi-faceted approach to security and ensure the provision of safety patches and responsible

awareness to our customers to fight off any possible threats.

The advance of web technologies has brought the society countless advantages, but the cyber world also

provides opportunity to a sinister side as well. As technology became more and more integrated in our

lives, the potential risk has also grown in parallel, be it from hacked computers or harvested personal

information.

At Allied Bank’s Security Center, you can read about latest fraud alerts, preventive measures and

information on how to remain protected from all potential threats.

DOWNLOADS

In this section you will find the various documents released by Allied Bank. All documents are available in PDF format.

Financial ReportsDownload and view latest Financial Reports of the Bank

Schedule of ChargesDownload our latest Schedule of Bank Charges applicable to the current half of the year

PublicationsRead all about our products, services and events by downloading our latest publications

Forms and CollateralThese include all the Forms and Collateral of our launch till date.

Knowledge BankingIn depth insights into your host of subjects and case studies, helping you to develop great ideas and

nurture them to fruition.

Articles and MagazinesA selection of recorded articles and magazines covering a wide range of topics of interests

Profit RatesDownload the latest Profit Rates of the deposit products

OTHER SERVICES AT ALLIED BANK

Hajj Services

Hajj Service at Allied Bank is available to all pilgrims. The forms and other related services are provided

by the Bank. Hajj applications are available with all branches during Hajj season, immediately after the

Hajj policy is announced by the Government of Pakistan

Demand Draft

Demand draft is a popular banking instrument in the trade circles to transfer funds from one place to

another. Allied Bank offers speedy issuance and payment of drafts at the branches.

Pay Order

Our customers can walk-in to any Allied Bank branch and make Pay Order to transact payment to a

named payee.

HOME REMITTANCES TO PAKISTAN

Allied Express – Home Remittance Distribution Service

ABL has been significantly important in helping the growth of home remittances to Pakistan through its

streamlined and trusted services. We are working continuously to develop innovative ideas into service

features that allow us to process and payout remittances even faster resulting in greater customer

satisfaction.

ABL’s real-time online branch network – one of the largest networks in Pakistan, consists of over 830

branches in 300 cities and town, providing comprehensive domestic distribution of remittances to

Beneficiaries across Pakistan.

A host of renowned international banks, exchange houses and money transfer companies from across

the world, including the Middle East, Europe, Asia-Pacific and North America, have been using our

services with utmost trust and satisfaction.

A number of options are available to non-resident Pakistanis through our service, including Direct Credit

to Account, Cash Payment over the Counter and issuance of Allied Express cheques, a payment

instrument that is honored across the entire ABL network of branches.

Please contact us to explore the ABL home remittances value proposition on +92-21-35301043

or [email protected]. For a more detailed review of what we do and how we do it, you may

download the presentation from this link.

SAFE DEPOSIT LOCKERS

Allied Bank’s Safe Deposit Lockers Safeguard Your Valuables to Assure Your Peace of Mind & Confidence.

Lockers are available at Allied Bank’s branches for all our account holders with singly as well as joint

operating instructions. As an additional security and track recording, whenever our account holders visit

their locker, they are supervised by our cordial staff along with the verification of signatures to ensure

safe, verified and vigilant entry.

If you are an Allied Bank Account holder, contact your branch and avail the locker facility now.

Some key features and charges of Allied Bank’s safe deposit lockers are,

Key features

Wide Availability

Lockers are insured according to their size.

Privacy and comfort to operate lockers

Lockers available in various sizes. i.e. Small, Medium , Large and Extra Large with flexible rental fee.

Lockers are rented out for a minimum period of one year.

The rent will be recovered from your deposit account maintained with us.

Direct debits for locker rentals from your account provides convenience and hassle-free payment of

annual fee.

Charges

S. # Locker SizeAnnual Locker Rent (Current)

Security Deposit

1. Small Rs.2,000/- Rs.25,000/-

2. Medium Rs.3,000/- Rs.50,000/-

3. Large Rs.4,000/- Rs.75,000/-

4. Extra Large Rs.5,500/- Rs.1,00,000/-

NOTE: Security Deposit is Refundable at the Time of Vacation of Locker.

To check availability of a locker at your nearest ABL branch, please download the “List of Branches with

Lockers” below:

AGRICULTURE FINANCING

The Bank, under the guidelines of the State Bank of Pakistan, extends short, medium and long term

Agriculture credit facilities to farming community of Pakistan on easy terms to increase the credit flow to

Farm and Non-Farm segments of Agriculture sector.

Farm credit is extended for the purpose of production of crops to meet working capital expenses and

Development of Agri land.

Non-Farm Credit facilities are offered for Livestock (Cow, Buffaloe, Goats, and Sheep etc.), Poultry

(Eggs, Day Old Chicks, Layer, Broiler, Hatchery) and fisheries (inland and marine, excluding deep sea

fishing).

Farm Loans

Production Loans

Inputs like seeds, fertilizers, pesticides, weedicides, herbicides, labour charges, water charges,

vegetables, floriculture, forestry etc.

Working capital finance to meet various farming expenses.

Development Loans

Improvement of agricultural land, orchards, etc.

Construction of Godowns

Purchase of Tractors, Machinery & other equipments

Installation of Tube wells

Farm Transportation, etc.

Non-Farm Loans

Livestock

Working Capital

Purchase of animal fodder and feeds, Vaccinations, Vitamins and other medications for animals including

artificial insemination

Overhead expenses i.e. labor, fuel, electricity etc.

Term Loan

Purchase of mature milk yielding buffaloes/cows, Purchase of Young animals for rearing for dairy farming

Purchase of Milk storage chilling tanks and milk carrying containers, feed grinders, tokas, feed mixing

machines and feed/milk containers etc.

Construction/Procurement of permanent sheds, water tanks, water pumps etc.

Poultry

Working Capital

Purchase of Eggs, Birds / Day old chicks, bird feed and feed raw material and vaccination

Overhead expenses i.e. labor, utility bills, Cost of fuel for generators & vehicles, transportation etc.

Term Loan

Purchase of Equipment/Machinery for Broiler/Layer farm & Hatchery

Farm construction for broiler, layer, hatchery and procurement of other items required for the

establishment of poultry farming industry etc.

Agriculture Revolving Credit Scheme

Loan Tenure: 3 Years (Clean up once a year)

One time documentation for 3 years

Loan limit will be based on the Indicative per Acre limit prescribed by ABL/SBP and/or requirement of the

applicant

Development Loans/Finances (Term Loans)

Loan Tenure: up to 7 years

Repayment: Monthly/Quarterly/Bi-Annual/Lump sum

Selection Criteria

Valid CNIC Holder

Preferably be an account holder with ABL

Have a permanent residence and be a self-cultivator

Not be a defaulter of any other Financial Institution/Clean ECIB

Be reputable in the business

Have ‘Repayment Capacity’

Be able to produce proper securities

Click Here to download a list of Designated Branches for flexible agricultural financing solutions.

WOMAN BANKING

Feel the comfort ….while you experience the services at our Women Branches

Allied Bank has introduced exclusive women branches to facilitate women to handle their financial

matters in comfortable homely environment.

Two branches are already opened in Lahore & Faisalabad and more to follow in your cities:

Branch Addresses:

Z-Block, DHA, Lahore

Main Susan Road, Madina Town, Faisalabad

Features:

All female staff

Comfortable environment

Coffee lounge

Kids play area

YOUTH BANKING

A great way for children and youth to get started with saving and lifestyle banking, including free access to ABL Internet Banking!

As a youth or student, you have unique banking needs. Whether you’re looking for value, flexibility or the

ability to save for the future, ABL offers a variety of accounts to help give you what you need. Our

exclusive Youth Branch incorporates a variety of youth-focused activities such as micro-savings, financial

education and entrepreneur development to empower youth in Pakistan.

Why Youth Branch:

Considering there are now over a billion people in the developing world between the ages of 12 and 24,

this is a critical time to harness young people’s capacity for learning and provide them with solid financial

services and understanding that will help lift themselves and their families out of poverty. The Youth

Branch was developed to help financial service providers meet this growing need for products and

services tailored to young people.

The purpose of Allied Bank Youth Banking is:

To secure the provision of opportunities for young people

To make grants to young people to bring about positive change in their own communities

To promote and support high quality learning opportunities

To help young people reach their full potential

To sustain Allied Bank Limited as the leading advocate of young people-led management of resources,

community action and decision-making.

Features:

Cordial Staff

Unique yet Comfortable Ambiance

Internet Facility

Students Area

SAVINGS & TERM DEPOSITS

Manage your funds with us… Meet your financial goals and Grow your Savings!

Have you managed to put aside some cash – What Now?

Your Savings stuffed into a mattress will never grow. But money deposited in a Savings Account or in a

fixed term, works for you by earning interest – and is also a lot safer. The longer that saving stays in your

account, the more you’ll make out of it.

Saving Accounts give you the ability to earn profit along with the flexibility to withdraw funds whenever

you require offsetting a financial emergency or need. The profit is earned as per the mechanics of Saving

Accounts which are mostly on the basis of Minimum Deposit maintained in the account.

Alternatively, investing in a term deposit product gives you a safety of knowing that your profit will not

fluctuate.

Term Deposit Mechanics

Term deposits are investment options offered by banks where you deposit your savings for a certain

‘term’ or period of time – upon which it would earn a particular percentage as profit. Let’s say you decide

to place your deposit for a term of 1 year at Allied Bank. Your deposit will be kept secured till the maturity

date. If you do need to withdraw your funds prior to its maturity date, then there are pre-mature

encashment charges that will apply.

At the maturity date of your term deposit, you may choose,

To withdraw your principal deposit along with the profit that your savings earned or,

You roll over the funds altogether or partially for another term to gain more profit.

There is a core principle that relates to the term deposit i.e. The longer the period of time for which you

are prepared to commit your funds with the bank, the better will be the rate and greater will be the income

Our Term Deposits can help you reach your savings goal.

CREDIT & DEBIT CARDS

Range of payment instruments and channels offered by Allied Bank has significantly contributed to service our customers.

A decade ago, it wasn’t all that unusual to be out for dinner or at the cash counter at a grocery store and

suddenly realize that you don’t have enough cash to cover the bill.

Today, we can conveniently pull out a debit or credit card and settle the bill electronically there and then.

It is difficult now to imagine a time when the card-based payment option were not available.

Debit cards are issued with a bank account so the money spent or withdrawn, is automatically deducted

from the account. It is a convenient alternate to cash, especially when it is directly used for shopping at

merchant locations on their POS (Point of Sale) machines.

With Credit Card, you can spend more than you have, or leveraging the credit balance, you can

reschedule your payments as per your convenience and typically get better rewards and better insurance

protection. Credit cards allow spending while paying the money back later.

Our customers using debit and credit cards enjoy the convenience that these cards bring in, for improved

financial management.

DOMESTIC REMITTANCE – PAY ANYONE

Around 2,000 Pay Anyone transactions are carried out every month!

Domestic Remittance is a significant financial service and a need for many people across Pakistan. It is

important for families, friends or acquaintances to have a convenient banking channel for remitting money

that is safe, fast and reliable. Our new addition on Allied Direct platform is the service called “Pay Anyone”

through which our customers can send/pay money to anyone in Pakistan.

How does it work

Allied Direct customers will be able to remit money from their accounts via 2 modes of payments,

Through Cash to be collected from any Allied Bank Branch all over Pakistan

Through a banker’s cheque (Allied Express Cheque) delivered to the specified beneficiary’s address and

payable at any branch of ABL.

BANCASSURANCE

“Investments and Protection plans at Allied Bank” Dreams.. worth saving for!

Alsurance

Il’m

Anmol Rishtey

ALSURANCE

Your Future Secured, Your Responsibilities Fulfilled

Overview

Because life is so unpredictable accidents can happen when you least expect them. An accident can

have a serious financial impact and we may have never thought about the financial consequences to us

and our family if we were involved in a serious accident.

Allied Bank and New Hampshire Insurance Company introduces Alsurance, a unique and exclusive

product that provides financial assistance to you and your family from accidents and incidents that, God

forbid, befall you.

Features:

Lowest ever premium: Rs. 6 per day

Highest protection up to: Rs. 7,500,000

14-day free trial period.

No medical tests required.

Covers your entire family.

Expenses for accident or terrorism related injuries covered

Why?

We are always concerned about the welfare of our children, our parents, and our family. Although, we

cannot prevent any incident or accident from happening, we can at least provide some solace in the form

of monetary relief, so that financial obligations can be met in the event a calamity may occur.

ABL as a responsible financial partner remains committed not only to your financial well being but also to

obligations that you or your family may face unexpectedly in the event of such an incident.

Product Benefits

Low Minimum Premium

Alsurance provides great benefits for as low as Rs. 2,160 per annum, which is Rs. 6 a day.

Lump Sum Payment

In case of an Accidental Death or Disability, the claim is paid out lump sum basis so that your family can

maintain their lifestyle and take care of any immediate financial responsibilities.

Family Coverage

Alsurance provides flexible plans for individuals as well as for families – which include spouse and

children.

Reimbursement for accidental or terrorism related injuries

In the event of an accidental or terrorism related injuries, your expenses for medical care are reimbursed.

Ease of Payment

Alsurance offers you both annual payment and monthly payment option, so you can choose a payment

plan that suits you best.

Plans

Silver GoldPlatinum

Diamond

Accidental or Terrorism Related

Death or Permanent Total Disability

Rs.1,500,000Rs.3,000,000

Rs.5,000,000 Rs.7,500,000

Medical Expense Reimbursement

Rs.300,000 Rs.500,000 Rs.750,000 Rs.1,000,000

Policy TypePremium Amount

Individual Annual Rs.2,160 Rs.4,080 Rs.6,720 Rs.9,90

Family Annual Rs.4,440 Rs.8,760 Rs.14,016 Rs.20,520

IL’M

Your Child Education Assured

Your Child’s Future is Precious

Be it an aspiring lawyer, a caring doctor or a skilled engineer – whatever your child aspires to become

tomorrow, we make sure it comes true. ILM (Child Education Plan) ensures your promise of better

education gets fulfilled no matter what the future holds for you

Allied Bank, with EFU Life Assurance Ltd, introduces “IL’M”, a savings plan that helps you meet your

child’s future education expenses.

Features:

Education Bonus

Freedom to customize

14 Day Free-Look Period

Fund Acceleration Premium (FAP)

Built-in Benefits:

Accidental Death and Disability Benefit upto Rs. 5,000,000

Continuation Benefit

Regular Education Fund Benefit

Why?

Education costs that are already exorbitant will further soar because of uncontrollable inflation. Saving

adequately and then prudentially investing those savings will give you the financial ability to fulfill the

promise of a better education to your children, even if you are not around to see it.

When Should You Start?

The earlier you start saving the better your child’s future will be. So build a steady saving from as low as

Rs.6,000 per annum with ILM After all, you work hard to earn your money; it’s only fair that your money

should work hard for you in return.

Milestones to Look-out for

School Fees: Rs. 70,000-Rs. 100,000 per year

University Education: Rs. 300,000-Rs. 500,000

These are approximate costs for good local schools and universities. These costs are substantially high

right now and will be even higher by the time your child reaches these milestones.

Product Features and Benefits:

Low Minimum Premium

I’LM gives you the opportunity to start saving for your child with as low asRs. 6000 per annum, which is

less than Rs. 20 a day.

Built-in Accidental Death and Disability Cover

The plan provides immediate funds in case the assured parent dies due to an accidental cause or suffers

permanent disability. The amount of payout is equal to 10 times the basic annual premium with a

maximum payout limited to Rs. 5 million.

Regular Education Fund Benefit

Withdrawals linked to key education related events can be made. They are allowed after completion of 5

policy years and a maximum 10% of the fund value at each time can be withdrawn.

Education Bonus

The plan provides valuable education bonuses during the plan term to boost the fund accumulation.

Starting from the 11th policy year, a bonus is allocated as a percentage of the average Basic Plan

contribution paid.

The extra unit allocation, in addition to the basic plan contribution, is as follows:

Applicable in Policy Year Extra Unit Allocation

11 25%

16 40%

21 60%

Fund Withdrawal Option

At maturity, the plan provides the accumulated fund value, which can either be taken in a lump sum or in

2, 3 or 4 equal annual installments.

Continuation Benefit

In the unfortunate event of death of the assured parent during the savings term, EFU Life continues to

make the contributions towards the plan so that the future planning of the child is not affected and the

targeted funds are available when needed.

Optional Benefits

Income Benefit

Waiver of Premium

Illustration

Plan with a 25 year term: For a 35 year old male, an annual premium of Rs. 15,000 and a built-in

Accidental Death and Disability benefit (providing sum assured of Rs. 147,400), the expected cash values

would be as follows:

Policy Year

Return On Investment

@ 6% p.a.unit @ 8% p.a.unit @ 10% p.a.unit

growth rate growth rate growth rate

1 3,485* 3,550* 3,616*

2 14,581 14,927 15,276

3 29,290 30,216 31,159

4 44,858 46,705 48,607

5 61,336 64,488 67,775

10 159,437 176,784 196,103

15 294,524 345,996 407,431

20 477,484 597,038 750,438

25 728,356 972,393 1,309,840

The policy cannot be surrendered until two full years premiums have been paid.

A portion of premium is invested in earlier years.

If the policyholder chooses the optional rider i.e. Income benefit, for an annual premium of Rs.945, a

regular quarterly income of Rs. 3,750 will be given to the family to meet the recurring child expenses in

case of death of the parent during the plan term.

Accessibility

In case higher funds are needed, the client has the flexibility to fully or partially withdraw the accumulated

fund value anytime after two full years premiums have been paid.

Unit Accumulation and Investment Fund

Every contribution paid towards the plan is invested in an internal investment fund of EFU Life called the

“EFU Managed Growth Fund”. The objective of the Fund is to maximize capital growth by investing in a

balanced portfolio spread across a wide range of shares, government and other fixed interest securities

and cash.

Fund Acceleration Premium (FAP)

You can make an additional lump sum contribution to the plan besides your regular Premium, to enhance

its cash value, at any time during the policy term.

Applicable Ages and Terms

The plan is available to individuals of 18 years to 60 years of age. The minimum savings term available is

10 years while the maximum is 25 years. The savings term has to be selected in such a way that the

maximum age of the customer at the end of the savings term is not more than 70 years.

Disclaimer

This product is underwritten by EFU Life. It is not guaranteed or insured by Allied Bank or its affiliates and

is not an Allied Bank product.

EFU Life is registered and supervised by Securities and Exchange Commission of Pakistan.

The contributions in the plan are invested in EFU Managed Growth Fund.

The cash values have been worked out at assumed growth rates of 6%, 8% and 10% per annum.

Depending upon the performance of the underlying investments in the EFU Managed Growth Fund, the

actual values may be higher or lower than the ones shown in the table.

The past performance of EFU Managed Growth Fund is not necessarily a guide to future performance.

Any forecast made is not necessarily indicative of future or likely performance of the funds and neither

EFU Life nor Allied Bank will incur any liability for the same.

A personalized illustration of benefits will be provided to you by our sales representative. Please refer to

the notes in the illustration for detailed understanding of the various Terms and Conditions.

Service charges and taxes will be applicable as per the Bank’s “Schedule of Charges” and taxation laws

as stipulated by the relevant authorities.

A description of how the contract works is given in the policy provisions and conditions. This product

brochure only gives a general outline of the product features and benefits and the figures used above are

indicative and for illustration purposes only.

Contact Information:

EFU Life Assurance Ltd

Main Office: 37-K, Block 6, PECHS Karachi-75400, Pakistan

Tel: (021) 111-EFU-111 Fax: (021) 4535079 Toll Free: 0800-33800

E-Mail: [email protected] Website: www.efulife.com

Allied Bank Limited

Bancassurance Department (CRBG)

ABL Head Office, 3 Tipu Block, New Garden Town, Lahore.

Contact No: 042-35880043 – Ext. 32102

Email: [email protected]

ANMOL RISHTEY

Your Biggest Responsibility Assured

Dreams are Very Precious

You have provided for the best possible education, a virtuous upbringing and fulfilled your child’s dreams

so far. You aspire to give them the best when it’s time for their wedding and like every parent, you also

desire to fulfill their most cherished dream.

Allied Bank, with EFU Life Assurance Ltd, introduces “Anmol Rishtey”, a Marriage Savings Plan that helps

you meet the expenses of your child’s most important day.

Features:

Marriage Support Bonus

Freedom to customize

14 Day Free-Look Period

Fund Acceleration Premium (FAP)

Built-in Benefits:

Accidental Death and Disability Benefit upto Rs.5,000,000

Continuation Benefit

Engagement Bonus

Will your Savings Suffice?

You are a loving and responsible parent but are you sure your savings for her big day will suffice? Is your

hard earned money working as hard as you? Are you sure that with the rising inflation and living costs

your savings will meet the expenses when the wedding day arrives?

What Should you Do?

You can start as early as when your child is born or when your daughter is in her teens. The earlier you

start saving, the more easily you will be able to meet the expenses of her big day. So build a steady

saving from as low as Rs. 6,000 per annum with AnmolRishtey. After all, you work hard to earn your

money; it’s only fair that your money should work hard for you in return.

Product Features and Benefits

Low Minimum Premium

AnmolRishtey gives you the opportunity to start saving for your child with as low as Rs. 6000 per annum,

which is less than Rs. 20 a day.

Built-in Accidental Death and Disability Cover

The plan provides immediate funds in case the assured parent dies due to an accidental cause or suffers

permanent disability. The amount of payout is equal to 10 times the basic annual premium with a

maximum payout limited to Rs. 5 million.

Engagement Bonus

At the end of 15 years, EFU Life will add an “Engagement Bonus” to the plan equal to 20% of the average

basic plan premium paid.

Marriage Support Bonus

The plan provides valuable Marriage Support bonuses during the plan term to boost the fund

accumulation. Starting from the 11th policy year, a bonus is allocated as a percentage of the average

basic plan contribution paid.

The extra unit allocation, in addition to the basic plan contribution, is as follows:

In Policy Year Extra Unit Allocation

11 20%

16 30%

21 50%

Continuation Benefit

In the unfortunate event of death of the assured parent during the savings term, EFU Life continues to

make the contributions towards the plan so that the future planning of the child is not affected and the

targeted funds are available when needed.

Plan Maturity

At maturity, the plan provides the accumulated fund value, which can either be taken in lump sum or be

left to accumulate with EFU Life for a maximum period of 1 year.

At the end of the one-year period, EFU Life pays the accumulated value and a “Maturity Investment

Bonus” of 20% of the annual average premium.

Access to savings at all times

The plan provides complete access to the accumulated fund value at all times. After the contributions

have been paid for two full years, the fund can be withdrawn for its full or partial value.

Unit Accumulation and Investment Fund

Every contribution paid towards the plan is invested in an internal investment fund of EFU Life called the

“EFU Managed Growth Fund”. The objective of the Fund is to maximize capital growth by investing in a

balanced portfolio spread across a wide range of shares, government and other fixed interest securities

and cash.

Fund Acceleration Premium (FAP)

You can make an additional lump sum contribution to the plan besides your regular Premium, to enhance

its cash value, at any time during the policy term.

Applicable Ages and Terms

The plan is available to individuals of 18 years to 60 years of age. The minimum savings term available is

10 years while the maximum is 25 years. The savings term has to be selected in such a way that the

maximum age of the customer at the end of the savings term is not more than 70 years.

Optional Benefits

Income Benefit

Waiver of Premium

Illustration

For a 35 year old male, AnmolRishtey plan with a 25 year term, an annual premium of Rs. 15,000 and a

built-in Accidental Death and Disability benefit (providing sum assured of Rs. 147,400), the expected cash

values would be as follows:

Policy Year

Return On Investment

@ 6% p.a.unit growth rate

@ 8% p.a.unit growth rate

@ 10% p.a.unit growth rate

1 3,485* 3,550* 3,616*

2 14,581 14,927 15,276

3 29,290 30,216 31,159

4 44,858 46,705 48,607

5 61,336 64,488 67,775

10 159,437 176,784 196,103

15 294,524 345,996 407,431

20 477,484 597,038 750,438

25 728,356 972,393 1,309,840

*The policy cannot be surrendered until two full years premiums have been paid.A portion of premium is

invested in earlier years.

If the policyholder chooses the optional rider of Income benefit, for an annual premium of Rs.945, a

regular quarterly income of Rs. 3750 will be given to the family to meet the child expenses incase of death

of the parent during the plan term.

Disclaimer

This product is underwritten by EFU Life. It is not guaranteed or insured by Allied Bank or its affiliates and

is not an Allied Bank product.

EFU Life is registered and supervised by Securities and Exchange Commission of Pakistan.

The contributions in the plan are invested in EFU Managed Growth Fund.

The cash values have been worked out at assumed growth rates of 6%, 8% and 10% per annum.

Depending upon the performance of the underlying investments in the EFU Managed Growth Fund, the

actual values may be higher or lower than the ones shown in the table.

The past performance of EFU Managed Growth Fund is not necessarily a guide to future performance.

Any forecast made is not necessarily indicative of future or likely performance of the funds and neither

EFU Life nor Allied Bank will incur any liability for the same.

A personalized illustration of benefits will be provided to you by our sales representative. Please refer to

the notes in the illustration for detailed understanding of the various Terms and Conditions.

Service charges and taxes will be applicable as per the Bank’s “Schedule of Charges” and taxation laws

as stipulated by the relevant authorities.

A description of how the contract works is given in the policy provisions and conditions. This product

brochure only gives a general outline of the product features and benefits and the figures used above are

indicative and for illustration purposes only.

E-BANKING SERVICES

“Electronic touchpoints to do banking round the clock” Banking on your fingertips!

As customers become more technology literate, Allied Bank delivers services that fit customers’ lifestyles

and offer more choice as to where, when and how they conduct transaction. Our customers are digitally

enabled and have less time to connect, interact and transact.

We, at Allied Bank differentiate ourselves not just by offering multi-dimensional channels to our customer

but also by enhancing their experience of utilizing those channels and find them convenient and familiar.

Our e-Banking services make us well positioned in creating better everyday life for our customers. We

have gathered a wealth of experience and expertise in providing electronic transactions to our individual

and corporate clients. We handle more than 23 Million electronic transactions annually.

‘Security’, ‘Speed’ and ‘Ease of use’ are the principles of e-banking infrastructure. At Allied Bank, we are

committed to our ability to speed our customers through to a successful transaction and improve their

efficiency levels while carrying out their financial decisions. Electronic services vary domestically as well

as globally but the challenge resides in delivering solutions that are efficient, providing customers with the

convenience and confidence they require in performing transactions.

ALLIED DIRECT – INTERNET BANKING

“Over 120,000 satisfied customers have registered for Allied Direct – Internet Banking”

Banking is now at your fingertips! Allied Direct Internet Banking offers you the convenience to manage

and control your banking and finances – when you want, where you want! It’s Simple, Convenient, Secure

and Faster.

Why Use Allied Direct – Internet Banking:

Allied Direct – Internet Banking gives customers 24-hour access to their Nationwide accounts. Here are

some of the services that will help save time and effort:

View and manage your account whenever and wherever you like.

Set up, manage and pay your bills.

Transfer money between your Nationwide accounts instantly.

Faster payments.

Top-up your mobile phone numbers

Go paperless, as you can view statements online.

Be up to do your banking, including paying bills and more, any day, any time, all from the privacy of your

own home, office or anywhere you have an internet connection. Sign-In or Sign-Up Now!

For Help and Support, please call the ABL Customer Center on: 0800-22522.

How to Sign Up for Allied Direct – Internet Banking

It only takes a few minutes to register. Please follow the steps, if you already have an account and ATM /

Debit Card; and start banking online:

Register yourself on Allied Direct website using the online registration process. A confirmation will be sent

to your given email addresses on registration and after approval of your request for using this service.

Once your request is approved, an ACTIVATION KEY will be sent to your email address. Use this

Activation Key to activate your account.

Activate your account by visiting your nearest Allied Bank ATM. After entering your ATM PIN Select

“Internet Banking” under “Other Services”. You will need to key in 8 digits Activation Key

received through email. On successful activation, you will get a message on ATM screen as well as on

paper receipt.

Once your Internet Banking is activated, visit our website. After entering the User ID, Activation Key and

other information, you will be required to specify the password to log in to Allied Direct. After the

verification of the information, you will be able to enjoy a host of benefits including Funds Transfer and

Online Bill Payments with few simple clicks.

E-SHOPPING

Shopping is more fun with Allied Bank!

The “e-Shopping” facility at ABL offers online payment facility linked to the online stores serving as a

payment gateway.

Allied Bank’s tie-up with a leading shopping websites facilitates convenient and secure online shopping

for you. Just choose your products online and pay conveniently through Allied Direct – Internet

Banking service.

Steps to Avail “e-Shopping” Service:

Visit the shopping site

Make your desired purchases

Click on “Dues Payment” in the horizontal navigation bar at the top

Enter the following information: Order Number, Description of Purchased Item, Amount, and Financial Pin

Click “Proceed” button

A confirmation screen will appear. Before confirming the transaction, double-check the Order

Number and Amount entered. Click “Confirm” to execute the transaction.

Ratings of Allied Bank Limited

June 30, 2012

The Pakistan Credit Rating Agency (PACRA) has upgraded long-term rating of Allied Bank Limited to

“AA+” (Double A plus) [Previous Rating: “AA”]. The short-term rating of the bank is already at the highest

level i.e. “A1+” (A One plus). The rating of the unsecured, listed and subordinated TFC-II (PKR 3,000

Million) has also been upgraded to “AA” (Double A) [Previous Rating: “AA-”]. The ratings denote a very

low expectation of credit risk emanating from a very strong capacity for timely payment of financial

commitments.

Reply by M.Tariq Malik on December 12, 2011 at 10:43pm

HISTORY OF ALLIED BANK LTDABL is the first Muslim Bank established on territory that later on became Pakistan. It was established on December 3, 1942 as Australasia Bank at Lahore with capital of 0.12 million. At that time the chairman was Kh. Bashir Baksh. ABL’s story was one of the dedication, commitment to professionalism and adaptation to changing environmental changes.

The bank's history is divided into many phases. During 25 years of united Pakistan the bank advanced forward in all areas of its activities. 1970’s were a difficult decade for all Banks of Pakistan. In 1971 East Pakistan was separated and Australasia Bank lost its 50 branches and a lot of capital as well. Nevertheless the growth remained steady.

In 1974 all the Banks were nationalized including Australasia Bank. The small provincial Banks were merged into Australasia Bank. On 1st July 1974 the new entity was renamed as ABL of Pakistan Limited. Then it started its operations as Public sector financial institution.

Different Phases of the Bank Are as Follows:

THE PRE INDEPENDENCE PERIOD (1942-47)

Australasia Bank had the unique distinction of being closely identified with some of the country’s most Prominent leaders of the freedom moment. Such as Mian Mumtaz Daultana (Board of directors), Mian Iftikhar Hussain and Maulana Zafar Ali Khan.

The bank originally started its operation in the garage of Khawaja Bashir Baksh’s bungalow (who was the chairman) near the Lahore Railway Station. But the success of Bank enforced the directors to open its another branch in Anarkali on 1st March 1944. Kh. Bashir was first chief executive. He was the person who was really working in its development. His sincerity of purpose can be judged from his great moments.

Another branch was opened at Amaratsar in 1945. In June 1946, the bank earned the status of scheduled bank. During 1946-47 many other branches were opened at Mcleod Road Lahore, Jallandhar, Ludhiana, Agra and Delhi.

At independence the industrial and commercial sectors were underdeveloped but ABL contributed a lot in the development of these sectors.

AUSTRALASIA BANK IN PRIVATE SECTOR (1947-74)

It was the only full functional Muslim Bank on the land of Pakistan. On August 14, 1947 bank was identified with Pakistan moment. Many of its Board of Directors were prominent Muslim League leaders. Jallandhar and Ludhiana branches were attacked by rioters because of Muslim staff appointed in these branches of bank. But when the Pakistan flags wee hoisted on the branches then all the banks in India were closed down. With this, the bank lost a lot of capital and its deposits and almost 6 branches. During 1948 new branches were opened at Karachi, Rawalpindi, Peshawar, Sialkot, Sargodha, Jhang, Gujranwala and Kasur. But later on its branches were spread to Multan and Quetta. At that time, the bank financed trade in cloth and food grains and thus maintained consumer’s supplies during the riot effected early months of 1948. Australasia Bank made a profit of

50,000/= in 1947-48.

In August 1948, Australasia Bank became the first Pakistani Bank to successfully negotiate and open L/C for a Sialkot based importer of books. So it also made correspondence relations with Midland (UK), Chase Manhattan (USA) and Lloyds (India).

During the treasury functions of Federal Govt. of Pakistan and it also acted as Banker to several local Govt. Bodies and to the Punjab University during this period. Treasury functions were taken by National Bank of Pakistan in 1949.

In 1950-51, Chairman was replaced with his own brother Kh. Sharif Baksh.

During 1955-56, Mr. Naseer A. Sh. became the Chairman of Board and close working relationship was forged between the new Chairman and Managing Director. This partnership proved in modernizing its operations and consolidating its financial position.

In 1963, Bank had 29 branches in various cities. And deposits were 89 million and advances were 66 million. Bank was mainly concerned with general banking and trade financing (including foreign exchange transactions). It helped a lot in development of small and medium sized business houses. These were Nishat, Crescent, Pak Cement, Haroon traders, Takht Bhai Sugar, Insaf, Punjab soap, Pak fruit and Saboor Oil Mills etc.

In 1964, 13 new branches were opened including 3 in East Pakistan. In 1965, 17 new branches were opened and over 83 % of gross profit for the year was earmarked for development expenditure in connection with opening of new branches.

In 1966 bank opened 26 new branches and doubled its reserved funds. For the first time in history, its advances were increased to Rs. 160 million and deposits raised by almost 58 % exceeding Rs. 232 million mark. In 1966, Central Office was built in Karachi but Head Office remaining at Shah Chiragh Building, Lahore.

16 new branches were opened in 1967 and 20 in 1968. Respectively their funds were increased gradually. 21 new branches were opened in 1971. But separation time the 51 branches were lost by the bank which was a big loss.

ALLIED BANK: PUBLIC SECTOR YEARS (1974-91)

Under the Nationalization Act of 1974, 14 scheduled banks were taken over by the Government. Australasia Bank’s Board of Directors was dissolved and the bank was renamed as Allied Bank of Pakistan Limited. Sarhad Bank,

Lahore Commercial Bank and Pakistan Bank Limited were merged into Australasia Bank. At time of merge, ABL was second highest among all the banks Nationalized in 1974.

Allied Bank’s first Executive Board was constituted of Mr. Iqbal A. Rizvi as President, Mr. Ajmal Khalil as Joint President and Mr. Khadim Hussain Siddique as member. In 1974 Mr. I.D. Junejo and Mr. Safdar Abbas Zaidi joined the Board later. 116 new branches were opened in 1974 and it started participation in commodity Operation program of Government.

In 1970’s Bank played an important part of agricultural area loans and other loans. In 1976 Mr. Ajmal replaced Mr. Rizvi as Chief Executive and President. During 1974-77, 361 new branches were opened and 230 of these were located in villages and small towns. It also opened its foreign branch in London, near the Bank of England. In 1980 the Bank of England granted Allied Bank recognition as a full fledge Bank under the U.K. Banking Act.

In 1981, President was changed. In 1984, again new president was come to know. He tries to increase the international business. It also initiated a major counter program. In 1985, mainframe computer was installed and effective management system was developed. During this period profitability was increased. New President Mr. Maqbool introduced different schemes in 1987-88. In 1989, new 13 branches were installed.

Over 1991, 745 branches were there in all over the Pakistan.

Permalink Reply by M.Tariq Malik on December 12, 2011 at 10:43pm

A NEW BEGINNING

In November/ December 1990, the Government announced its commitments to the rapid privatization of the Banking sector. Allied Bank’s management under the leadership of Mr. Khalid Latif decided to react positively to this challenge. In September 1991, ABL entered in a new era of its history as world’s first bank to be owned and managed by its employees. The 850 executives and 7200 staff members spread over 750 branches throughout the Pakistan established a high degree of cooperation and family feelings

After this, it grows more and more, even at present it has 900 branches throughout the country and 4 foreign branches in U.K.

Allied bank Objectives:

Allied bank has following objectives:

i) Main objective of Allied bank is to earn profit.

ii) To provide services to their customers and assistance in the development of commerce and trade.

Allied bank also have another responsibility to give service to their communities. It watches the growth and development of his community especially the commerce and business of the area.

Read more: ALLIED BANK LIMITED – INTERNSHIP REPORT - Virtual University of Pakistan http://vustudents.ning.com/group/fini619internshipreportfinance/forum/topics/allied-bank-limited-internship-report?commentId=3783342%3AComment%3A1010400&groupId=3783342%3AGroup%3A59249#ixzz25CYeD8WP

Reply by M.Tariq Malik on December 12, 2011 at 10:43pm

MANAGEMENT SYSTEM OF ABLSuccessful and profitable banking management depends on two principal factors.

a) The manner in which the functions of banking, that is the acquiring of deposits, the investing or converting such deposits into earning assets, and the servicing of such deposits, are performed.

b) The degree to which officers and employees contribute their talents to the progress and welfare of the bank in discharging duties and responsibilities.

Allied Bank Management

Banks are managed by board of director or similar group of men who are responsible to the owners, creditors, and the government for the well being of their institutions. The government selects all or some of directors of ABL. Management of ABL are given as follows:

Bank’s Information

1. Directors:

Rashid M. Chaudhry is the chairman and Mohammadi Yaqoob is secretary of ABL, are also the board of directors.ABL’s other directors are M. Saleem Shaikh, S. Jauhar Husain, I.A. Usmaini, Raja Raza Arshad, Mohammad Saleem Sethi, Athar Mahmood Khan. Stockholders elect the directors for a term of one year and they are eligible for re-election. Voting is cumulative, that is, each shareholder has the right to vote the member of shares owned by him. The boards may format major policies and select officers to execute them. They may supervise these officers, review their act.

2. Executive Committee

Executive Committee consists of Rashid M. Chaudary (president), M. Salim Shaikh, S. Jauhar Husain, I. A. Usmain, Naveed Masud, Bilal Mustafa, M. Saleem Khan Durrani, Ashfaq Hassan Qureshi, Shariqe Umar Farooqi (secretary).

3. Officers:

Officers are selected by the directors to manage their banks. An officer’s relationship to the board is that of an employee to an employer. Chief Officer (Rashid M. Chaudary) of ABL is known as Chairman, Senior Executive Vice President (M. Saleem Sheikh, S. Jauhar,). They are also members of the board of director and are large shareholders. They are in a position, to dominate the bank's policies as well as its administration.

The Chief duty of the chairman is to lend the bank's funds. This work is often subject to little supervision by the board of directors.

STRUCTURE OF ABL LIMITEDNo bank can be expected to operate efficiently unless all employees with in a department, division or section know:

A) From whom they are to receive the work they are to do.

B) What they are supposed to do with the work after they receive it.

C) How they are supposed to handle the operation of item.

D) When they are supposed to do work, perform the operation.

E) To whom they give the item or function after finishing it.

To perform the functions efficiently the bank has its Head Office in Karachi, which is controlled by the president of the Bank. The bank has regional office under head office in major areas of the country. Regional Chief heads this office. The region Consist of many zonal offices with a zonal chief. There are many branches in a zone to carry

the functions effectively and performing customer services locally.

ABL Ltd. is functionally organized into divisions and divisions are further divided into department and sections. Every province has its own regional office and zonal offices. Executive vice president heads the divisions and departments are further headed by OGI (Officer of Grade I). Manager heads branches.

BRANCH NETWORKThere are Four Provincial Headquarters of Allied Bank Limited situated at Lahore (Punjab), Karachi (Sind), Peshawar (NWFP & Azad Kashmir) and Quetta (Baluchistan).

PROVINCIAL HEADQUARTERSPUNJAB:7E/3, Main Boulevard, Gulberg, Lahore

SINDH:Jubilee Insurance House, I.I. Chundrigar Road, Karachi

NWFP:1st floor, State Life Building, The Mall,

AZAD KASHMIR:Peshawar Cantt.

BALUCHISTAN:C.C. & I Building, Zarghoon Road, Quetta.

CIRCLESThere are 22 circles of ABL through out the country under which 46 zones are present. Their detailed is as follows:

City Circle KarachiZones 3

Branches 36

Sadar Circle KarachiZones 2

Branches 37

Nazimabad Circle KarachiZones 2

Branches 34

City Circle HyderabadZones 2

Branches 34

Commercial Circle HyderabadZones 2

Branches 37

Sukkur CircleZones 2

Branches 33

City Circle LahoreZones 2

Branches 47

Project Circle LahoreZones 2

Branches 29

Gujranawala CircleZones 3

Branches 73

Islamabad CircleZones 2

Branches 27

Rawalpindi CircleZones 2

Branches 43

Jhelum CircleZones 2

Branches 46

Faislabad CircleZones 2

Branches 46

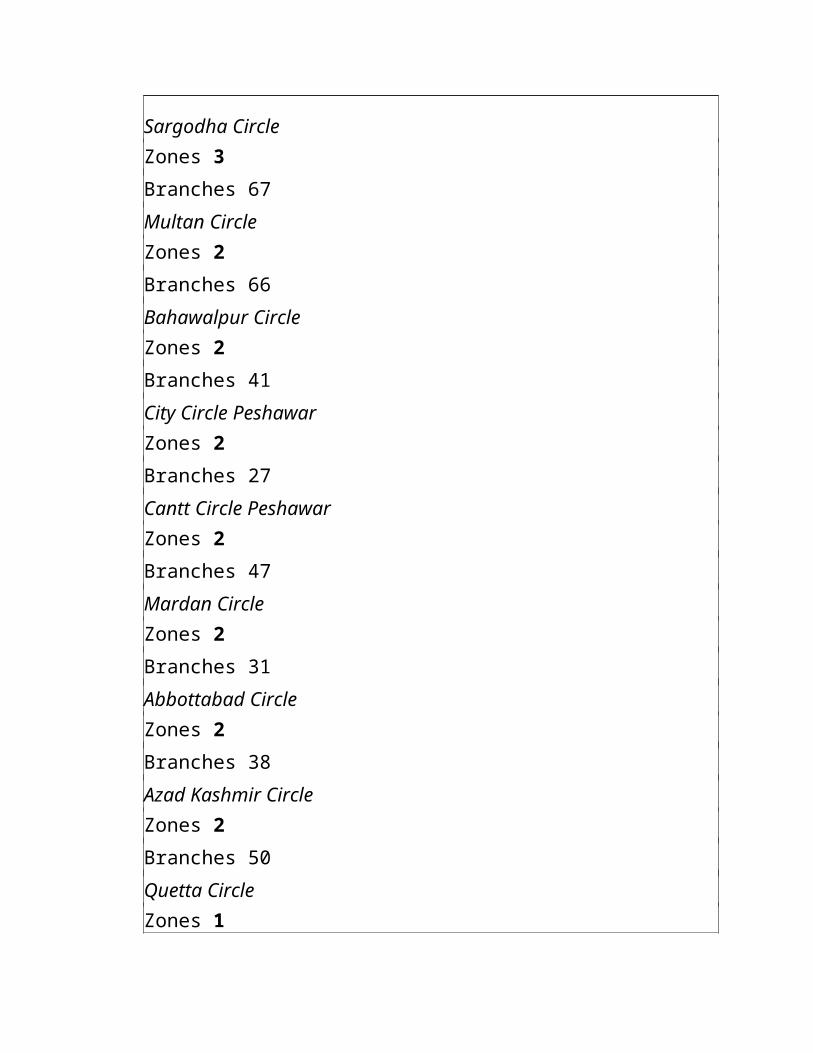

Sargodha CircleZones 3

Branches 67

Multan CircleZones 2

Branches 66

Bahawalpur CircleZones 2

Branches 41

City Circle PeshawarZones 2

Branches 27

Cantt Circle PeshawarZones 2

Branches 47

Mardan CircleZones 2

Branches 31

Abbottabad CircleZones 2

Branches 38

Azad Kashmir CircleZones 2

Branches 50

Quetta CircleZones 1

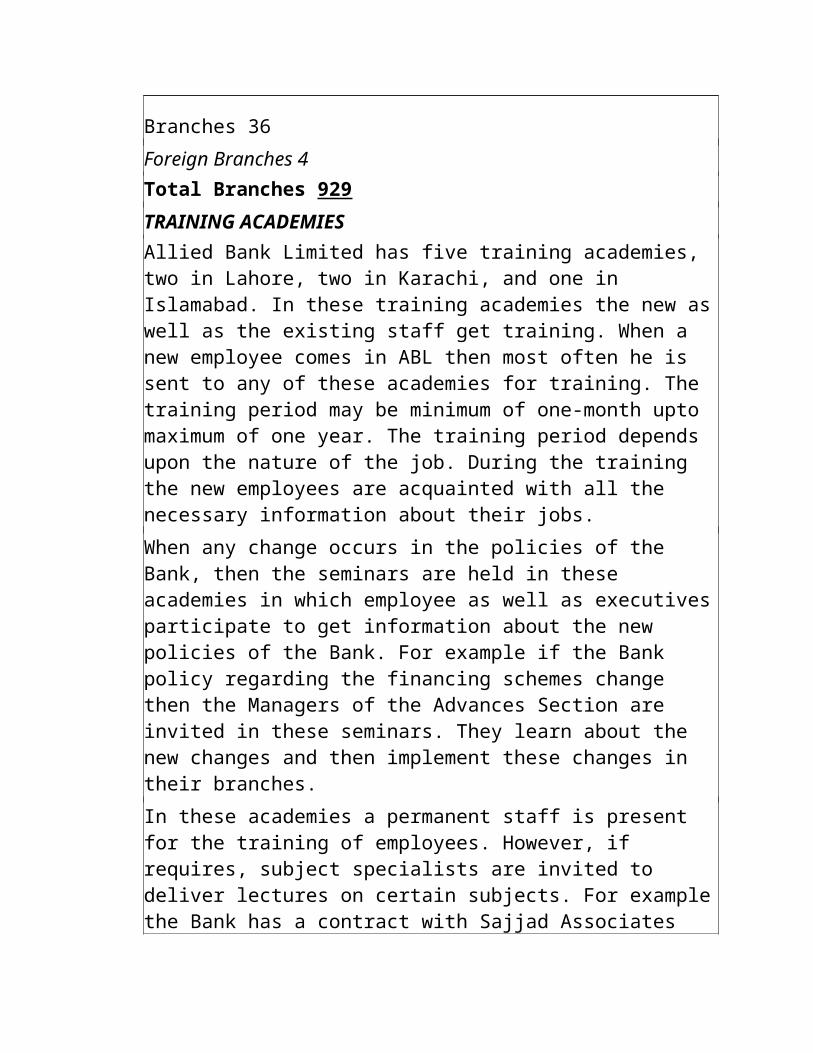

Branches 36

Foreign Branches 4Total Branches 929

TRAINING ACADEMIESAllied Bank Limited has five training academies, two in Lahore, two in Karachi, and one in Islamabad. In these training academies the new as well as the existing staff get training. When a new employee comes in ABL then most often he is sent to any of these academies for training. The training period may be minimum of one-month upto maximum of one year. The training period depends upon the nature of the job. During the training the new employees are acquainted with all the necessary information about their jobs.

When any change occurs in the policies of the Bank, then the seminars are held in these academies in which employee as well as executives participate to get information about the new policies of the Bank. For example if the Bank policy regarding the financing schemes change then the Managers of the Advances Section are invited in these seminars. They learn about the new changes and then implement these changes in their branches.

In these academies a permanent staff is present for the training of employees. However, if requires, subject specialists are invited to deliver lectures on certain subjects. For example the Bank has a contract with Sajjad Associates which send its executives to deliver lectures on project financing. Exams are also held in these training academies.

ORGANIZATIONAL STRUCTURE (MULTAN CIRCLE)

ALLIED BANK OF PAKISTAN

JAHANIAN BRANCH

The Branch of ABL Ltd. is responsible to provide all services to its customer. This branch is located in Jahanian.

FUNCTIONS OF JAHANIAN BRANCH OF ABL LTD

There are following functions which are performed by Allied bank Limited Jahanian Branch.

ACCEPTS DEPOSITS

The Bank provides deposit facility to its customers. The types of deposits are:

a) PLS Saving Account:

In this type, the depositor shares profit and loss with the bank.

b) Fixed Deposits

They bear high profit, but these can only be withdrawn after a fixed period of time

c) Current Accounts

No profit is paid on these deposits but amount could be withdrawn without any restriction.

Branch Setup

REMITTING OF FUNDS

The Bank provides the facility to its customers for remitting large amounts of money in the form of bank drafts, T telegraphic Transfers and Mail Transfers to where ever the customers want.

Permalink Reply by M.Tariq Malik on December 12, 2011 at 10:44pm

The Senior Vice President heads the personnel department. Its head office is at Karachi. All the policies and rules, regulations etc. This department deals about personnel.

HIERARCHY OF POWERSenior Vice President.

Vice President.

Assistant Vice President.

Officer.

CATEGORIES OF WORKERSThe work force in the personnel department is as follows:

Officers

Clerical staff

Non-clerical staff

OFFICERSOfficers are designated according to their grades.

Executive grade.

Sr. grade-I

Sr. grade-II

Sr. grade-III

Officer grade-I

Officer grade-II

Officer grade-III.

CLERICAL STAFFCashiers

Assistants

Senior Assistants

Typists

Steno typists

Steno graphers

Telephone operators

Telex operators

Godown keepers

NON-CLERICAL STAFFDrivers

Messengers

Guards

Godown Chowkidars.

Sweepers

ELIGIBILITY CRITERIA FOR PROMOTIONS

From Clerical to Officers Cadre

QUALIFICATION LENGTH OF SERVICE

Graduate two years

Intermediate four years

Matriculate six years

From Typist and Stenotypist and Stenotypist to Stenographer Cadre

Confirmed staff in clerical cadre.

Required shorthand typing speed.

Stenotypist 80/45 words per minute

Stenographer 120/45 words per minute

From Clerical to Non Clerical Cadre

QUALIFICATION LENGTH OF SERVICE

Intermediate one year

Matriculate two years.

For the purpose of promotion it is important consideration that an employee has rendered service in rural areas.

PROBATIONARY PERIOD

The probation period varies for various posts. It is usually from 1 to 2 years.

CONFIRMATIONS

After the probation period comes the confirmation period. The branch manager refers him/her for confirmation. The confirmation of various post rights rests with the zonal/area chief. For big posts the confirmation is centralized by central office Karachi. Confirmation is made after 1 year of probationary period.

PHYSICAL ACTIVITY

The personnel department also takes case of physical activities of the employees. They encourage the employees in physical games like cricket,

Football, tennis, hockey etc. They hold regional and zonal competitions. For

Publicity purposes the bank also employs famous players to play on behalf of the bank. In this way the bank on the other side provides financial help to our talented boys.

EMPLOYEES MATTERS

ABL policy is very socialistic about its employees, its motto is:

“Every employee is the owner of the bank”

Literally the bank has given power to even an officer to sell the ABL assets; the authority of an employee is unlimited. This attitude encourages the employees to get most involved in to the bank affairs. ABL also provides lot of facilities to the employees. Here is a list of loans and leaves, which can be granted to the employees:

LEAVES

Casual leave

Sick leave

Maternity leave

Disability leave

Privilege leave

Extra ordinary leave

Hajj and Ziarat leave

Leave preparatory leave

CAUSAL LEAVE.

One can take fifteen days causal leave in one year, five days maximum at a time. The unvalued leaves are not granted in coming next year. These leaves should be availed in the respective year.

SICK LEAVE.

There is a criterion for sick leave.

With full pay the staff can take 12-month sick leave in the entire service of his life with out pay the staff can request the sick leave, as he/she requires.

MATERNITY LEAVES.

The maternity leave is granted once in three years. It’s for female employees. It varies from 15 days to three months. The bank gives full pay during the leave.

DISABILITY LEAVES.

The disability leave is conditional to following rules:

The disability is caused during the service of the employee.

It is brought into the notice for prompt action with in three months of its occurrence.

Its period lies between one day to 24 months as recommended by the doctor.

Six month pay is granted and afterwards its half pay.

PRIVILEGE LEAVES.

Privilege leave is granted one per eleven days in a year and accumulated up to 90 days.

EXTRAORDINARY LEAVE.

This leave is with out pay. When sick leave is unsatisfactory or some special occasions occurs, when no leave is due then the extra leave is granted.

HAJJ AND ZIARAT LEAVE.

It is provided after completing five years of the service. Its period extends to one month. It’s on full pay basis.

PREPARATORY AND RETIREMENT LEAVE.

It’s the kind of leave which is allowed to a person retiring from the service for the period of leave earned and due up to 90 days.

· AUTHORITY FOR LEAVE SANCTIONING

Causal and privilege leave or sanctioned by mangers, zonal chief, but all other is dealt in the central office Karachi.

PROMOTION PLANS

OFFICERS.

Normally promotion is done on seniority basis. A promotion is due after a person has completed three years in the same grade.

CLERICAL AND NON CLERICAL STAFF.

It’s on the basis of their length of service and the written tests and qualifications.

QUALIFICATION LENGTH OF SERVICE

Matriculate. Six years service.

Intermediate. Four years service.

Graduate. Two years service.

More over interviews and tests also contribute in promotion.

LOANS FOR EMPLOYEES

Allied Bank has a long list of loans, which it offers to its employees. The hire the post is, the more facilities are given to the employees.

Loans are as follows.

PROVIDENT FUND LOAN.

Provident Fund loan is loan which is given after the retirement of the employees. Its is equal to own contribution plus the interest on the amount. Three basic salaries plus banks own contribution.

OLD OPTION BENEFITS .

In P.F.L a lumps is taken in this case and the pension is not given.

New option benefit.

In case of option pension, loan against general provident fund is allowed equal to own contribution and 3 months basic salaries.

CONVINCE LOANS.

The convince loan include scooter loan, car loan, cycle loan. Etc.

The car loan is equivalent to 12 basic salaries, which is sanctioned to officers, executives drawing basic salary of. RS. 1250. Month. Such loans bear interest of ten 10% pa. They are recoverable in 120 monthly installment

MOTOR CYCLE LOAN.

Such loans are sanctions to lower grade officers and clerical, non-clerical staff. The limit of the loan is not more then Rs. 10,000. It is conditioned that the employees have completed 3 years of service in the bank. Motor Cycle loan is interest free loan.

HOUSE BUILDING LOANS.

This loan is given if the employees have completed of full 5 years of service, as a confirmed officer. It is equal to 80 months salary.

FACILITIES

MEDICAL FACILITIES

Banks provides medical facilities to its employees. It also has fixed amount, which is limited in order for tremens of employees. The record of medical expenses is maintained at zonal office and monthly statement is sent to central office Karachi.

TRAVELLING ALLOWANCE

There is facility of TA. /DA. For employees who go on official visit out side the city.

EDUCATION ALLOWANCE

Education allowance is given to the children of the employees and employees as well. The maximum allowance for one employee will be RS. 450. App. Per month for maximum three children.

HOUSE ALLOWANCE (RENT)

House rent allowance is upto 90% of basic salary at all stages. The house rent allowance differs according to the areas and its rates.

LOCAL COMPENSATORY ALLOWANCE

Local compensatory allowance is given in accordance with areas of work such as Islamabad and Karachi maximum Rs. 200 and at Lahore, Rawalpindi, Peshawar and Quetta it is Rs.100 per month.

CONVEYANCE ALLOWANCE

The conveyance allowance is given to the employees in accordance of their designation.

DOMESTIC SERVICE

The Allied Bank provides the services to top men in the bank such as Executive Vice President, Sr. Vice President, Vice president and Asst. Vice President etc.

They also provided by Mali/Chowkidar and furnishing the house is also bank facility.

TELEPHONE ALLOWANCE

There is fixed amount of telephone bills for executives/officers, which is paid every month to them.

PENSION/GRATUITY FACILITY

The pension is given when an employee completes his ten years in the bank. The gratuity is given if employee qualify the rules then he can ask for the pension of 15 year at one go.

PROMOTIONS

Upto clerical staff the promotions are on tests and their daily work/efficiency and their length of service. The promotion of officers is with seniority.

RECRUITMENT

After the Privatization of ABL central office at Karachi is dealing with the appointments to different officers posts. And the central office also fills other executive posts. For certain posts the executives also have right to appoint the qualified persons. But the main criteria of appointment are by test and interviews.

Allied Bank has a criteria already prepared for the appointments of employees. the criteria involve:

Academic work.

Extra curricular activities

Working experience.

The candidates must be the citizens of Pakistan and the state of Jammu and Kashmir should not be more than 25 and less than 18. However in certain cases the age can be relaxed. Normally the citizen for under developed areas of Pakistan has the age relaxation. The executives also have the power to employ an over age person etc.

Read more: ALLIED BANK LIMITED – INTERNSHIP REPORT - Virtual University of Pakistan http://vustudents.ning.com/group/fini619internshipreportfinance/forum/topics/allied-bank-limited-internship-report?commentId=3783342%3AComment%3A1010400&groupId=3783342%3AGroup%3A59249#ixzz25CZ5ue00

Reply by M.Tariq Malik on December 12, 2011 at 10:45pm

Advances department of a bank provides many facilities to various individuals and businessmen against charging the interest from them.

It is the usual practice of the back level it examines the perusal characteristics of the borrower and the reputation and scope of the business, he is doing or going to start.

However, there are there ways normally used to seem the account.

1. Pledge

2. Mortgage

3. Hypothecation

1. PLEDGE

Pledge is a contract between the borrower and the back whereby the goods are transferred into the banker's possession while the ownership remains in the possession of the borrower. This possession remains with the bank until the payment of loan is dully made. In case of default, the back can sale the goods after giving the notice.

2. MORTGAGE

Mortgage is a contract whereby the interest in any specified immovable property is transferred to the banker in order to give the security for the payment of debts.

3. HYPOTHECATION

Hypothecation is a term where goods are charged for the purpose of security. But the possession and ownership remains with the owner of the goods.

CATEGORIES OF ADVANCES

The bank can make the advances in the following three ways.

1. Overdraft

2. Loan

3. Cash Credit

1. OVERDRAFT

Under such arrangement the customer is allowed to withdraw the amount excessive from his balance. But the limit of amount is sanctioned by the manager and given for a fixed period.

2. LOAN

When the bank make the advances in a lumpsum, to be repaid in lumpsum or in forms of installments with interest at any future date, is known as loan. These loans may be of short and long term.

3. CASH CREDIT

These advances are made against the security of the goods which may be made like in the form pledge or hypothecation. The bank credits the borrower's account with the amount making as loan. The amount can not be withdrawn in lumpsum. While interest is paid on the amount withdrawn from the bank.

TYPES OF LOANSThe Bank provides the facility of two types of financing.

1. Funds based Financing

2. 2. Non Funds based Financing

FUNDS BASED FINANCINGThe type of Financing in which the funds of the Bank are directly involved is called Funds based Financing.

There are following types of Funds based Financing.

· Running Finance

· Cash Finance

· Demand Finance

· Demand Finance against Foreign Currency Account

· Demand Finance to Staff

· Finance Against Local Manufactured Machinery

· Allied Equity Building Plan

· Unorganized Sector Financing Scheme

· Housing Finance

· Agricultural Finance

· IDA Financing

· Consortium Finance

· Finance Under Small Business and Small Industries

· Overseas Employment Financing Scheme

· Finance Against Trust Receipt

· Term Finance Certificates

· Finance for Government Operations

1. RUNNING FINANCEPURPOSERunning Finance is short-term loan usually given for the working capital management. The running finance is suitable for meeting day to day financial needs of the Business. The running finance account can be operated and daily sale proceeds can be deposited into the account.

SECURITYThe Bank requires following types of securities in running finance.

PRIMARY SECURITYThe primary security requires by the Bank is stock. Bank hypothecates a specific amount of stock, that is, stock remains in the custody of borrower, but the lien is of Bank. The borrower is responsible for keeping and managing the stock well and providing the regular stock reports to the Bank. The Bank advances a certain percentage of the value of the hypothecated stock as loan after keeping some margin.

PERSONAL GUARANTEESUnder the SBP laws, ABL can give the loan to the extent of Rs. 50,000 on two personal guarantees along with the primary security.

PRINCIPLE SECURITYIf the loan required by the borrower is greater than Rs. 50,000 then the Bank requires some collateral security along with the Primary security. The security taken as collateral is usually immovable. However, according to ABL laws, the agricultural land cannot be taken as collateral security. In some rare cases it may also happen that a creditworthy firm may keep some moveable security as collateral but provided that it is very easily encashable, e.g. defense saving certificates etc.

MARK-UPNormally the cost of running finance is 14% but it is negotiable and may vary. 1-% rebate is given to a client who gives three times more business to Bank than his limit. Furthermore, 1% more rebate is given to a client who exports three times more than his limit.

Limit means the maximum amount of finance, which is sectioned from the Bank authorities in favor of client.

PERIODRunning finance is usually given for a period of one or less than one year.

REPAYMENT SCHEDULEThe borrower has to repay the loan on the daily sail proceeds of stock. It is necessary for the borrower to adjust the account on the date of expiry of loan period. However, Bank may give a period of one month after the maturity of loaning period, so that the borrower may repay the loan during this period. This period is called ‘Date of Final Adjustment’.

2. CASH FINANCEINTRODUCTIONCash finance is the account of the Bank. It is like the current account. In this account a certain amount of cash is available for the borrowers at all the times. A limit is first sanctioned to the borrower and then, on his needs, the amount is transfer from cash finance account to the borrower’s current account from where he can withdraw the money. This transfer of cash from the Bank’s cash finance account to the borrower’s current account is just the paper transaction and the borrower takes the finance in no time. The borrower can take finance unto his limit sanctioned by Bank’s authorities. However, the Bank cannot keep the cash finance account greater than 30% of its equity.

PURPOSECash finance is normally giver for seasonal needs e.g. in Cotton season, Rice season etc. But in some cases it can be given for regular needs.

SECURITYFollowing securities are required by the Bank.

PRIMARY SECURITYThe primary security required by the Bank is stocks. But unlike running finance, in which the stock is hypothecated, here the stock is pledged by the Bank. The stock pledged is kept with

the Bank at the cost of the borrower. Usually the stocks are kept at the warehouses of the Borrower Company, but certain representative of Bank as Inspector is always there to keep a check on the stock. The Bank advances certain percentage of the pledge stock after keeping some margin.

PRINCIPLE SECURITYLike running finance, some collateral security is taken as principle security.

MARK-UPThe Mark-up of cash finance is normally 14%, but is negotiable.

PERIODThe maximum period for cash finance is one year.

REPAYMENT SCHEDULERepayment of the loan is made after the completion of loaning period, along with the markup.

3. DEMAND FINANCEPURPOSEDemand finance is usually given for the financing of new Projects. For example, if a person wants to open the Floor mill or textile mill, he can get the demand finance from the Bank.

MODE OF FINANCEDemand finance is given in installments to the borrower. First installment is given to purchase the land, then second installment is given for the construction of building and finally the remaining amount is paid to the supplier to install the Machinery.

SECURITYThe Bank requires the following types of securities.

PRIMARY SECURITYNo primary security is required as the finance is given for the new projects and the Borrower Company has no existing stocks with it.

PRINCIPLE SECURITYLike running and cash finance, some collateral security is required as principle security. This collateral may be land, building or machinery.

MARK-UPNormally 14% but negotiable.

PERIODDemand finance is usually given for the long-term period e.g. for two years, five years or even upto fifteen years.