All tied up MENA - Building a better working world - EY · PDF fileAll tied up MENA. Working...

20

All tied up MENA Working capital management report 2017

Transcript of All tied up MENA - Building a better working world - EY · PDF fileAll tied up MENA. Working...

All tied up MENAWorking capital management report 2017

ForewordAll tied up MENA: working capital report 2017 is part of a series of working capital (WC) management reports based on EY research, reviewing the WC performance of the world’s largest companies.

WC involves Account receivables — Account payables + inventory

Total sales decreased by

Cash opportunity of

Total net working capital (NWC) increased by

Cash-to-cash (C2C) cycle increased by

in FY16 compared with FY15

was identified in FY16.

in FY16 compared with FY15

days in FY16 compared with FY15

All tied up MENA: working capital report 2017 is the first of the reports in the series, focusing on the Middle East and North Africa (MENA) region. The survey focuses on the top 326 companies in the MENA region, examining their WC performance at the company, regional, industry and country levels. In addition, this report sets out the findings of a review comparing the WC performance of small, medium and large companies with that of very large companies.

The analysis in this report can be useful to benchmark your performance with the industry averages and the upper quartiles.

The analysis also provides insights into the trends of various companies and their WC behavior over a period.

Key findings

4.1%

US$29.8b

2.0% 8

2 | All tied up MENA

ContentsExecutive summary 4

MENA companies overview 6

WC performance — by industry 10

WC performance — by size 12

Top vs. bottom WC performers 14

WC performance — by geography 15

WC self-diagnostic 16

How EY can help 17

Methodology and glossary 19

There was an increase in WC metrics compared with 2013The WC Cash to Cash (C2C) increased by 15 days to 116 days in 2016 from 101 days in 2013. The increase was primarily due to an increase in days sales outstanding (DSO) in 2016 by 13 days compared with 2013.

Very large companies (by size) manage WC more efficiently than mid- and small-sized companiesOverall, the larger companies have managed to improve their WC in 2015 compared with small- and mid-sized companies. The average NWC by sales percentage for very large companies decreased to 7% in 2016 from 10% in 2013. The average NWC by sales percentage for small companies was 35% in 2016.

What influences WC?Middle East (MENA) companies have not been proactive in managing WC in 2016. The following economic situations resulted in WC deterioration in 2016:

• Sales decrease • Volatile oil prices• Rising interest rates• Decrease in banks’ lending appetite

Is it more than just negotiating power?The common misconception is that improvements are related only to payment terms. However, in reality, there are many different levers to pull in trade and non-trade WC, such as order processing time, invoice processing timeline, invoice trigger date, invoice delivery timeline and dispute management.

The key aspect that drives WC reduction for very large companies is their investment in people, policies, processes and infrastructure. Discipline in creating and adhering to smart WC processes helps release cash trapped in the business because of process inefficiencies.

Executive summary

4 | All tied up MENA

Themes Key questions to think about

WC top performers operate better across all the metricsOn the basis of the study, top WC performers, on average, show better financial metrics, such as earnings before interest, taxes, depreciation and amortization (EBITDA), return on equity (ROE), and return on capital employed (ROCE), compared with WC performers at the bottom of the scale. They also have more spare cash toward capital expenditure (capex) compared with poor performers.

There are good performers in every industryOn the basis of the study, every industry has exeptional WC improvement. Out of the top 15 industries, four have seen improvement in WC metrics for 50% or more of the companies.

What is the link?There are multiple strategic advantages of WC improvements, such as:

• Creating investment capacity• De-leveraging the business or improving

shareholder yield• Dividend payments • Lower interest income

What can be learnt from them?There are a number of companies improving their WC performance in every industry. The sectors with the largest variance are building materials, chemicals, food producers and distributors, among others.

5 All tied up MENA |

Themes Key questions to think about

MENA companies overview

Reduced sales growth and cash on hand

In FY16, the sales for MENA companies declined by 4.1% compared with FY15. This was primarily because of subdued industrial activity, weak investment environment and low oil prices. The key sectors with maximum sales drop are household durable products, entertainment industry, oil and gas, and industrial and packing material.

Cash on hand for the MENA companies went down by 2.7% in FY16. This may be because of increased WC metrics; and thereby, excess cash unnecessarily being tied up in the business.

Source: EY analysis, based on publicly available annual financial statements Source: EY analysis, based on publicly available annual financial statements

“ In a tough economic environment, it is important to focus on efficiencies and maintain an optimal capital structure. WC optimization can help support the capital structure by releasing excess cash, which can be effectively utilized elsewhere.”

Hani BisharaEY MENA Debt Advisory, Working Capital and Restructuring Leader

53,653

59,208

52,164 50,776

46,000

48,000

50,000

52,000

54,000

56,000

58,000

60,000

FY13 FY14 FY15 FY16

US$

m

Chart 1: Overall trend of sales over historical period Chart 2: Cash balances over historical period

2,55,787

2,69,975

2,57,111

2,46,638

2,30,0002,35,0002,40,0002,45,0002,50,0002,55,0002,60,0002,65,0002,70,0002,75,000

FY13 FY14 FY15 FY16

US$

m

6 | All tied up MENA

Source: EY analysis, based on publicly available annual financial statements

Source: EY analysis, based on publicly available annual financial statements

Source: EY analysis, based on publicly available annual financial statements

Source: EY analysis, based on publicly available annual financial statements

Increase in short-term borrowings and reduction in total debt compared with 2015

A review of the total debt and short-term borrowings indicate that total debt and short-term borrowings increased by 2.5% and 12.0% respectively in 2016. This indicates the need for increased WC

investment required by companies. The total debt increased by 17.0% between 2013 and 2016.

1,64,919

1,81,595 1,84,928

1,92,949

1,50,0001,55,0001,60,0001,65,0001,70,0001,75,0001,80,0001,85,0001,90,0001,95,0002,00,000

FY13 FY14 FY15 FY16

US$

m

US$m

101 102

108

116

90

95

100

105

110

115

120

2013 2014 2015 2016

Day

s

2013 2014 2015 201665

70

75

80

85

90

Day

s

72 72

78

85

15,640

12,955 13,036 14,733

FY13 FY14 FY15 FY16

US$

m

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

Chart 3: Overall trend in total debt

Chart 5: Overall C2C trend over historical period

Chart 6: Overall DSO trend over historical period

Chart 4: Overall trend in short-term borrowings

The cash to cash cycle for the region increased by eight days to 116 days in 2016 (2013: 101 days). This was primarily because of a significant increase in DSO.

Our study shows that MENA companies are collecting their dues seven days slower in 2016 compared to 2015. There may be multiple drivers, such as increase in credit period, weaker collections process and liquidity issues for a few customers. However, an interesting aspect is the percentage overdue of total receivables and its movement across years. The health of receivables can be ascertained by analyzing the movement of overdue percentage over the period.

7 All tied up MENA |

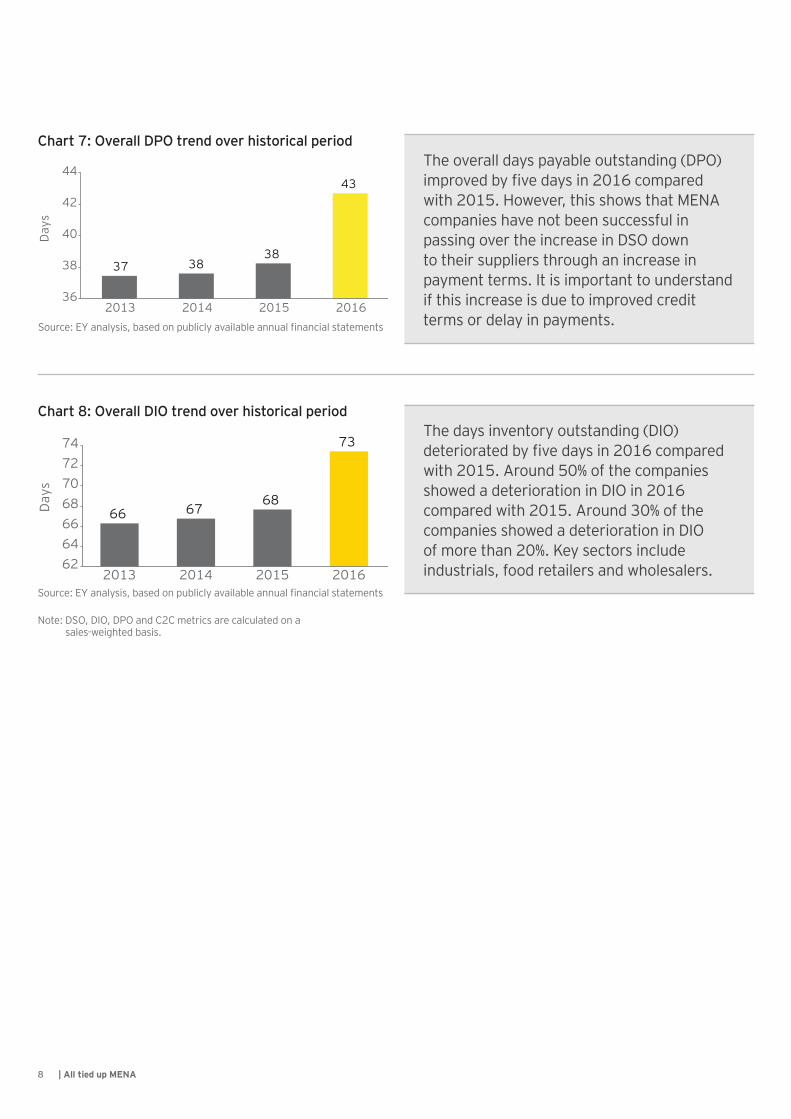

The overall days payable outstanding (DPO) improved by five days in 2016 compared with 2015. However, this shows that MENA companies have not been successful in passing over the increase in DSO down to their suppliers through an increase in payment terms. It is important to understand if this increase is due to improved credit terms or delay in payments.

Chart 7: Overall DPO trend over historical period

Chart 8: Overall DIO trend over historical period

Source: EY analysis, based on publicly available annual financial statements

Source: EY analysis, based on publicly available annual financial statements

Note: DSO, DIO, DPO and C2C metrics are calculated on a sales-weighted basis.

37 38 38

43

36

38

40

42

44

2013 2014 2015 2016

Day

s

66 67 68

73

62646668707274

2013 2014 2015 2016

Day

s

The days inventory outstanding (DIO) deteriorated by five days in 2016 compared with 2015. Around 50% of the companies showed a deterioration in DIO in 2016 compared with 2015. Around 30% of the companies showed a deterioration in DIO of more than 20%. Key sectors include industrials, food retailers and wholesalers.

8 | All tied up MENA

9 All tied up MENA |

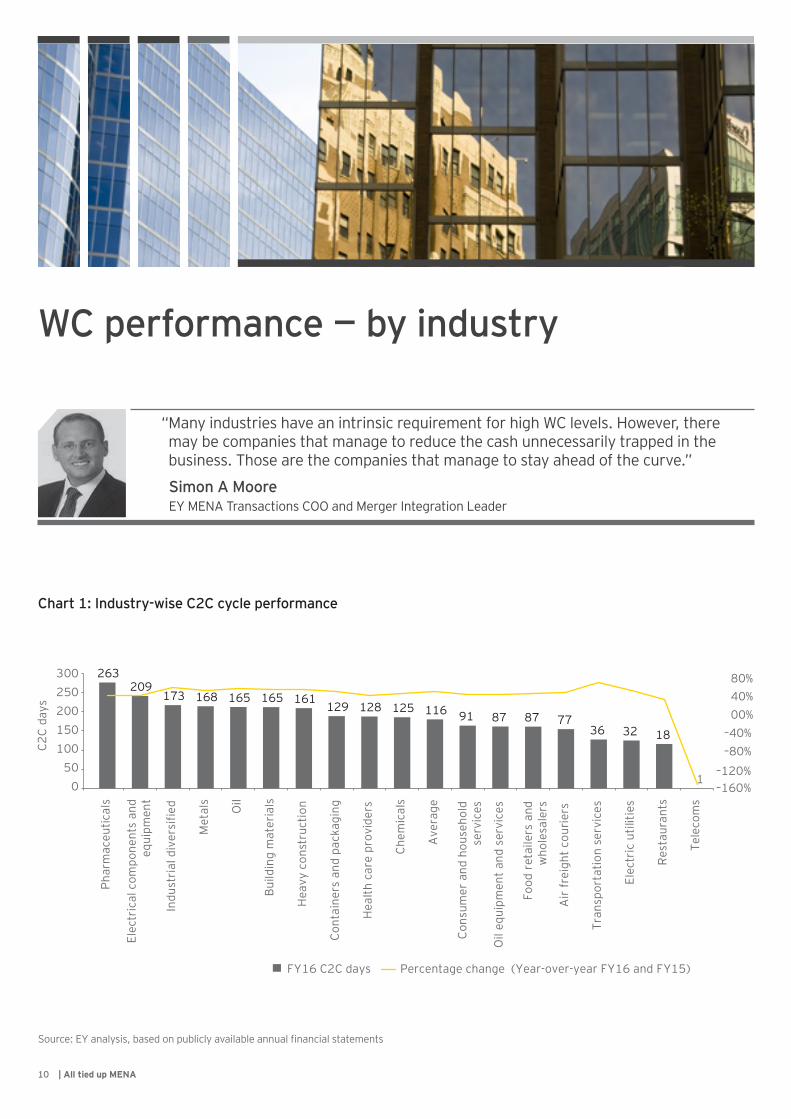

WC performance — by industry

“ Many industries have an intrinsic requirement for high WC levels. However, there may be companies that manage to reduce the cash unnecessarily trapped in the business. Those are the companies that manage to stay ahead of the curve.”

Simon A MooreEY MENA Transactions COO and Merger Integration Leader

Chart 1: Industry-wise C2C cycle performance

Source: EY analysis, based on publicly available annual financial statements

263 209

173 168 165 165 161 129 128 125 116 91 87 87 77

36 32 18

1 –160%–120%

–80%–40%

00%40%80%

050

100150200250300

Phar

mac

eutic

als

Indu

stri

al d

iver

sifie

d

Met

als

Oil

Build

ing

mat

eria

ls

Hea

vy c

onst

ruct

ion

Cont

aine

rs a

nd p

acka

ging

Hea

lth c

are

prov

ider

s

Chem

ical

s

Ave

rage

Air

frei

ght c

ourie

rs

Tran

spor

tatio

n se

rvic

es

Elec

tric

util

ities

Res

taur

ants

Tele

com

s

C2C

days

FY16 C2C days Percentage change (Year-over-year FY16 and FY15)

Oil

equi

pmen

t and

ser

vice

s

Cons

umer

and

hou

seho

ldse

rvic

es

Food

ret

aile

rs a

ndw

hole

sale

rs

Elec

tric

al c

ompo

nent

s an

deq

uipm

ent

10 | All tied up MENA

Chart 2: Industry-wise improvers and non-improvers

Source : EY analysis, based on publicly available annual financial statements

2

2

1 13

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Improved Worsened

12

5

5

4

19

4

8

7

5

12

8

8

9

7

37

12

9

7

29

6

11

8

5

12

6

2

RestaurantsElectrical components

And equipment

Chemicals

Electric utilities

Health care providers

Telecoms

Heavy construction

Containers and packaging

Industrial diversified

Consumer and household services

Food retailers and wholesalers

Building materials

Transportation services

Oil

Metals

Our study shows that the top industries with the highest WC days (C2C) are the pharmaceuticals, electrical components and equipment, and other diversified industrials sectors. The C2C days for pharmaceuticals, and electrical components and equipment decreased by 4.9% and 6.2%, respectively, in FY16. The main reason for the increase in C2C days was decline in inventory days.

At the other end of the spectrum, telecoms, food and beverage, utilities, and transportation services enjoy a low C2C cycle. However, the sectors saw an increase in the C2C cycle in FY16 compared with FY15. The main reasons for the low C2C cycle for telecoms and restaurants were the high payable days coupled with medium receivable days and extremely low inventory days.

Average NWC by industry in FY16 shows wide variance in WC performance between industries.The differences primarily arise because of differences in operating models, supplier and customer mix, procurement strategies, and overall industry drivers.

11 All tied up MENA |

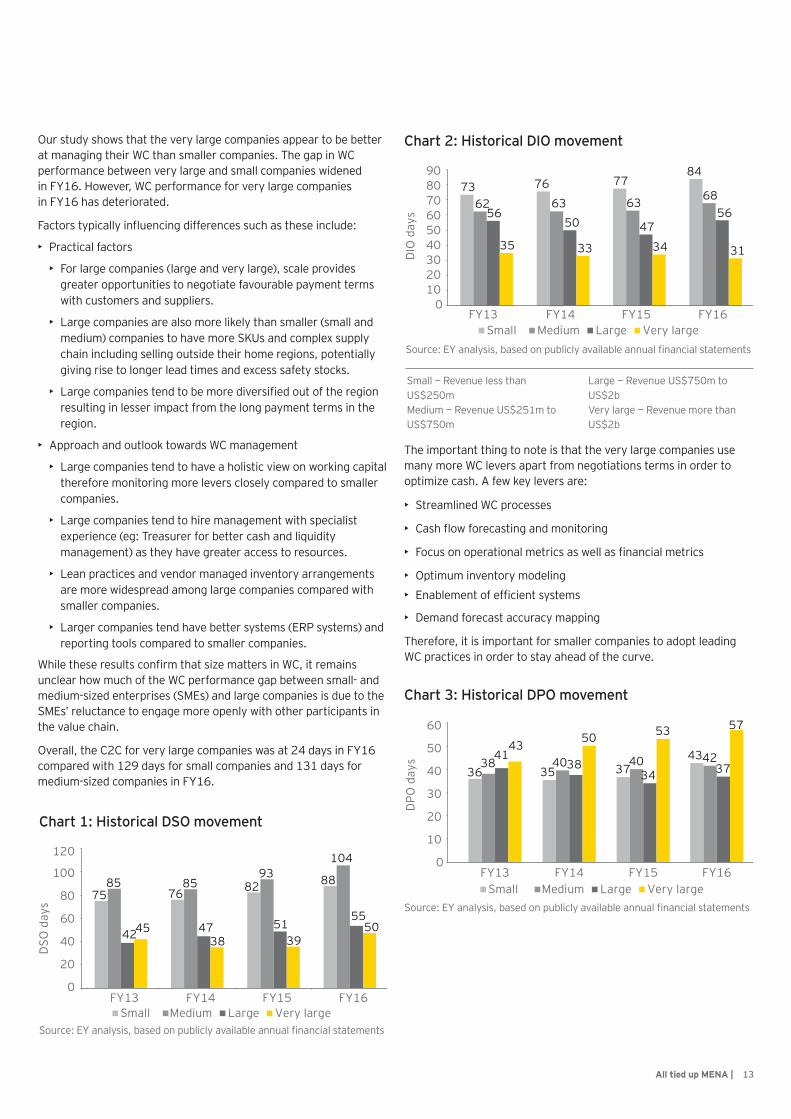

The gap in WC performance between small, medium, large and very large companies increased in FY16, continuing from previous years.

Source: EY analysis, based on publicly available annual financial statements

Chart 1: Size-wise C2C cycle performance

Table 2: Movement between FY16 and FY15

Company size DSO DPO DIO C2C

Small 6% 16% 8% 4%

Medium 12% 4% 7% 11%

Large 9% 8% 16% 15%

Very large 29% 7% -8% 19%

Small — Revenue less than US$250mMedium — Revenue US$251m to US$750m

Large — Revenue US$750m to US$2bVery large — Revenue more than US$2b

WC performance — by size

C2C

days

Small Medium Large Very large

0204060

80

100120140

FY13 FY14 FY15 FY16

57 59 64

75

110 108 116 131

113 117 123 129

36 21 20 24

“ WC management appears to be a key area of concern for many companies in the region. It is important for MENA companies across sizes to move from an only P&L-focused organization to P&L and cash-focused organization.”

Phil Gandier EY MENA TAS Leader

12 | All tied up MENA

Source: EY analysis, based on publicly available annual financial statements

Chart 2: Historical DIO movement

The important thing to note is that the very large companies use many more WC levers apart from negotiations terms in order to optimize cash. A few key levers are:

• Streamlined WC processes

• Cash flow forecasting and monitoring

• Focus on operational metrics as well as financial metrics

• Optimum inventory modeling• Enablement of efficient systems

• Demand forecast accuracy mapping

Therefore, it is important for smaller companies to adopt leading WC practices in order to stay ahead of the curve.

Small — Revenue less than US$250mMedium — Revenue US$251m to US$750m

Large — Revenue US$750m to US$2bVery large — Revenue more than US$2b

73 62

56

35

76 63

50

33

77

63

47

34

84

68 56

31 DIO

day

s

Small Medium Large Very large

0102030405060708090

FY13 FY14 FY15 FY16

Our study shows that the very large companies appear to be better at managing their WC than smaller companies. The gap in WC performance between very large and small companies widened in FY16. However, WC performance for very large companies in FY16 has deteriorated.

Factors typically influencing differences such as these include:

• Practical factors

• For large companies (large and very large), scale provides greater opportunities to negotiate favourable payment terms with customers and suppliers.

• Large companies are also more likely than smaller (small and medium) companies to have more SKUs and complex supply chain including selling outside their home regions, potentially giving rise to longer lead times and excess safety stocks.

• Large companies tend to be more diversified out of the region resulting in lesser impact from the long payment terms in the region.

• Approach and outlook towards WC management

• Large companies tend to have a holistic view on working capital therefore monitoring more levers closely compared to smaller companies.

• Large companies tend to hire management with specialist experience (eg: Treasurer for better cash and liquidity management) as they have greater access to resources.

• Lean practices and vendor managed inventory arrangements are more widespread among large companies compared with smaller companies.

• Larger companies tend have better systems (ERP systems) and reporting tools compared to smaller companies.

While these results confirm that size matters in WC, it remains unclear how much of the WC performance gap between small- and medium-sized enterprises (SMEs) and large companies is due to the SMEs’ reluctance to engage more openly with other participants in the value chain.

Overall, the C2C for very large companies was at 24 days in FY16 compared with 129 days for small companies and 131 days for medium-sized companies in FY16.

Source: EY analysis, based on publicly available annual financial statements

Chart 1: Historical DSO movement

75 76 82 88 85 85 93

104

42 47 51 55

45 38 39

50

0

20

40

60

80

100

120

FY13 FY14 FY15 FY16

DSO

day

s

Small Medium Large Very large

Source: EY analysis, based on publicly available annual financial statements

Chart 3: Historical DPO movement

DPO

day

s

FY13 FY14 FY15 FY16Small Medium Large Very large

36 35 37 43

38 40 40 42 41 38

34 37

43 50 53 57

0

10

20

30

40

50

60

13 All tied up MENA |

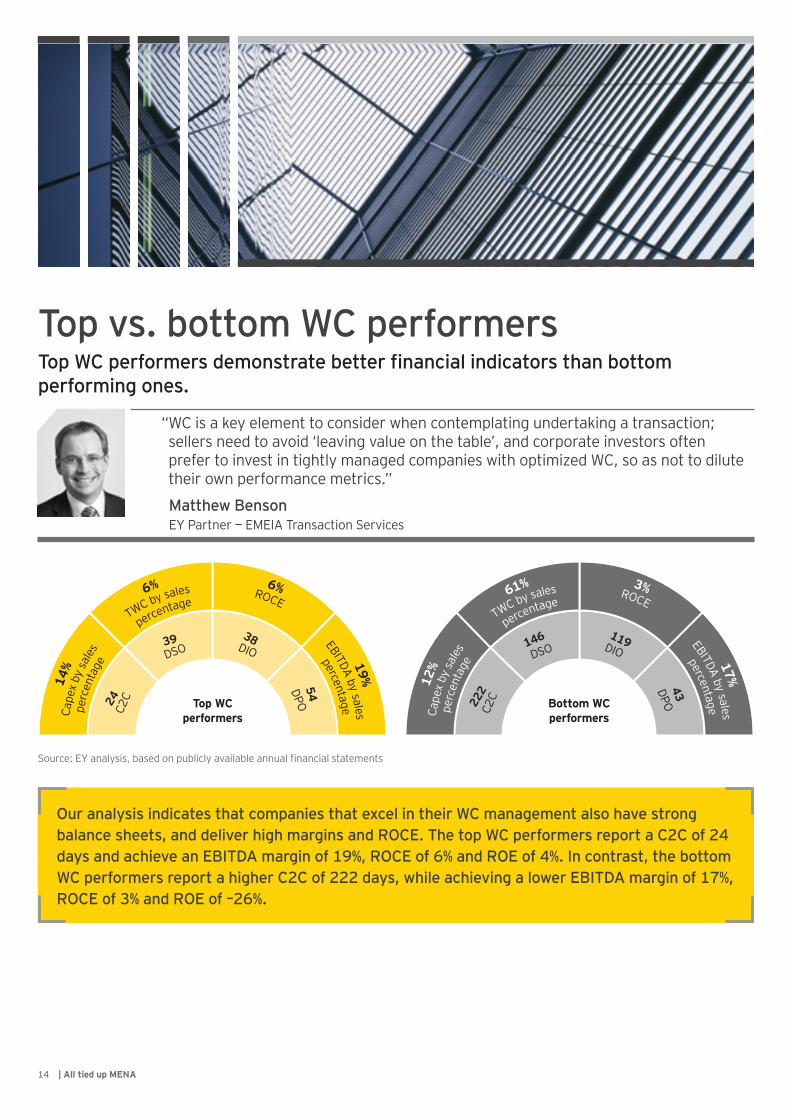

Top WC performers

24C2

C

39DSO

38DIO

54DPO

19%

EBITDA by sales

14%

Cape

x by

sales

perc

enta

ge

6%

TWC by sales

percentage6%ROCE

percentage Bottom WC performers

222

C2C

146DSO

119DIO

43DPO

17%

EBITDA by sales

12%

Cape

x by

sales

perc

enta

ge

61%

TWC by sales

percentage3%ROCE

percentage

Top vs. bottom WC performersTop WC performers demonstrate better financial indicators than bottom performing ones.

“ WC is a key element to consider when contemplating undertaking a transaction; sellers need to avoid ‘leaving value on the table’, and corporate investors often prefer to invest in tightly managed companies with optimized WC, so as not to dilute their own performance metrics.”

Matthew Benson EY Partner — EMEIA Transaction Services

Source: EY analysis, based on publicly available annual financial statements

Our analysis indicates that companies that excel in their WC management also have strong balance sheets, and deliver high margins and ROCE. The top WC performers report a C2C of 24 days and achieve an EBITDA margin of 19%, ROCE of 6% and ROE of 4%. In contrast, the bottom WC performers report a higher C2C of 222 days, while achieving a lower EBITDA margin of 17%, ROCE of 3% and ROE of –26%.

14 | All tied up MENA

WC performance — by geography

Kingdom of Saudi Arabia

87

799240

130

49

1096351

121

38

1286738

157

16

704636

80

49

835137

97

41

587945

93

36

1139854

157

10

753634

77

326

917343

121

Oman Kuwait EgyptUnited Arab

EmiratesJordan Qatar Bahrain Total

Number of companies DSO

DPODIO

C2C

Source: EY analysis, based on publicly available annual financial statements

Source: EY analysis, based on publicly available annual financial statements

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

20% 80%

27% 73%

31% 69%

35% 65%

36% 64%

39% 61%

45% 55%

65% 35%

Percentage of improvers Percentage of non-improvers

Bahrain

Jordan

Qatar

Oman

UAE

KSA

Kuwait

Egypt

Chart 1: Country-wise percentage of improvers vs. non-improvers

“ Liquidity and working capital management have been an important focus area for many global companies over the past few years. There is an opportunity for MENA companies to align their WC performance with that of their global peers.”

Jon Morris EY EMEIA Working Capital Leader

15 All tied up MENA |

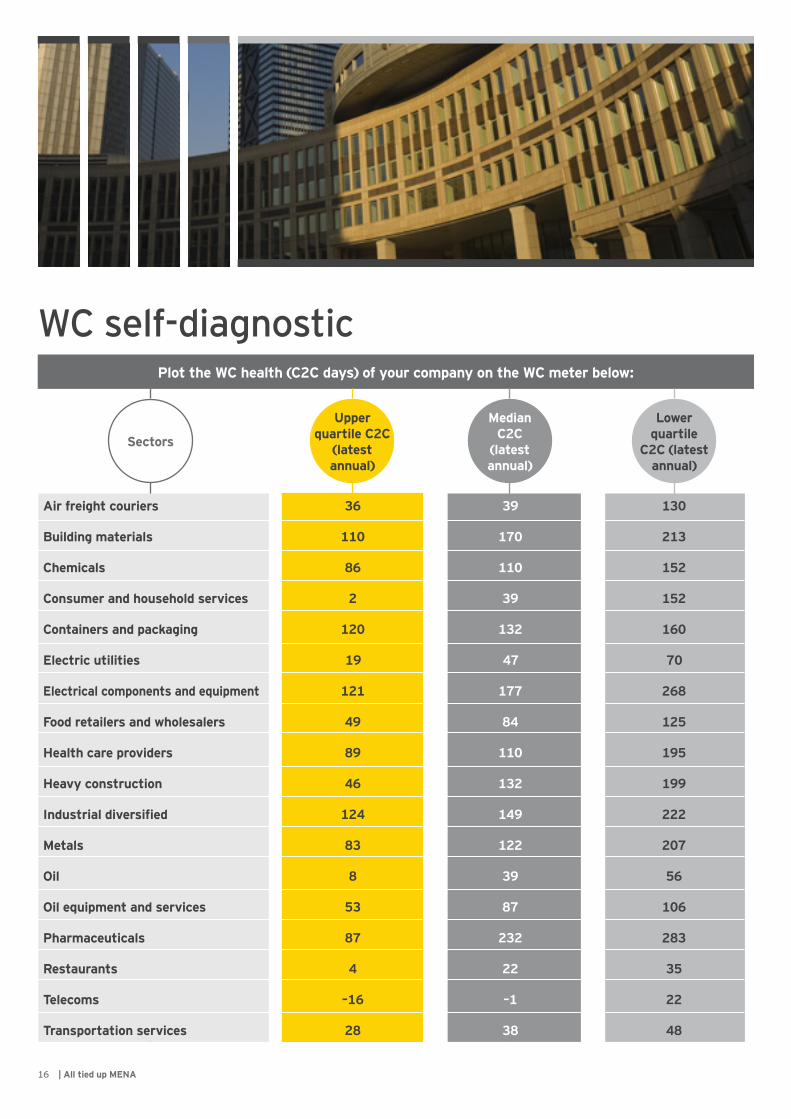

130

Heavy construction

Air freight couriers

Building materials

Chemicals

Consumer and household services

Containers and packaging

Electric utilities

Electrical components and equipment

Food retailers and wholesalers

Health care providers

Industrial diversified

Oil equipment and services

Pharmaceuticals

Restaurants

Telecoms

Transportation services

Metals

Oil

152

152

160

70

268

125

195

199

222

207

56

106

283

22

35

48

39

110

39

132

47

177

84

110

132

149

122

39

87

232

–1

22

38

170 213

36

86

2

120

19

121

49

89

46

124

83

8

53

87

–16

4

28

110

WC self-diagnostic

Sectors

Upper quartile C2C

(latest annual)

Median C2C

(latest annual)

Lower quartile

C2C (latest annual)

Plot the WC health (C2C days) of your company on the WC meter below:

16 | All tied up MENA

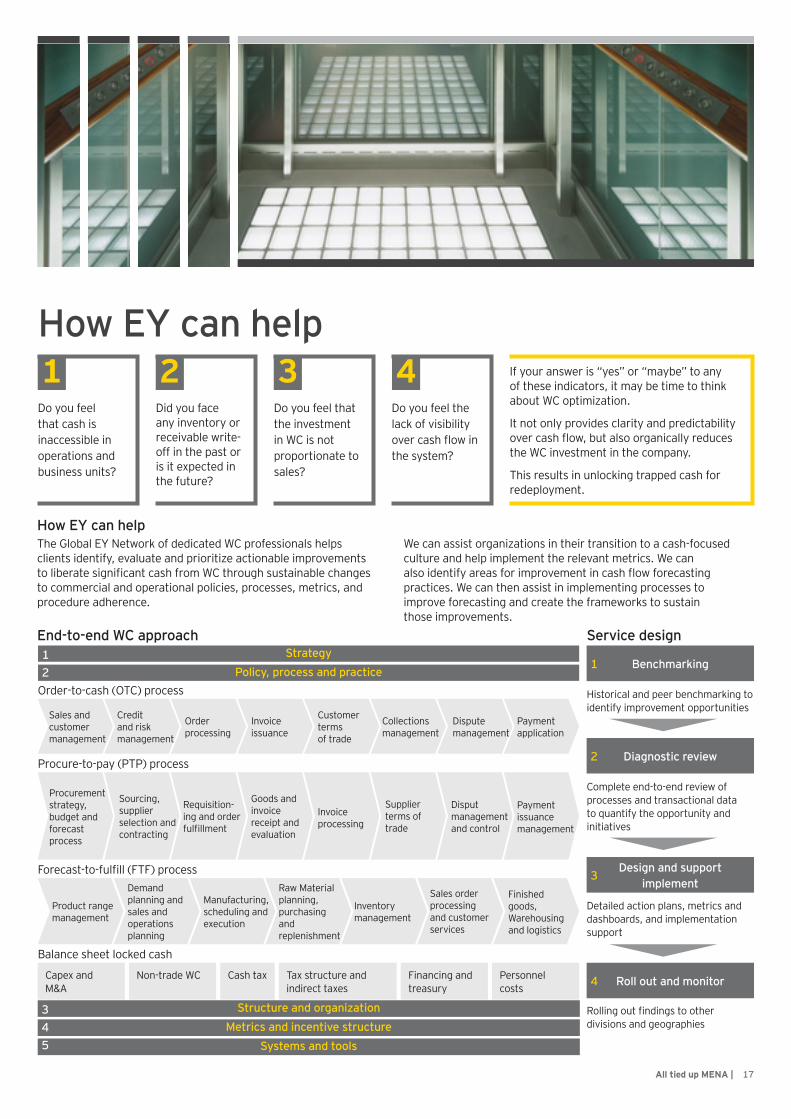

How EY can helpIf your answer is “yes” or “maybe” to any of these indicators, it may be time to think about WC optimization.

It not only provides clarity and predictability over cash flow, but also organically reduces the WC investment in the company.

This results in unlocking trapped cash for redeployment.

How EY can help

End-to-end WC approach Service design

The Global EY Network of dedicated WC professionals helps clients identify, evaluate and prioritize actionable improvements to liberate significant cash from WC through sustainable changes to commercial and operational policies, processes, metrics, and procedure adherence.

We can assist organizations in their transition to a cash-focused culture and help implement the relevant metrics. We can also identify areas for improvement in cash flow forecasting practices. We can then assist in implementing processes to improve forecasting and create the frameworks to sustain those improvements.

Metrics and incentive structureStructure and organization

Systems and tools

StrategyPolicy, process and practice

Order-to-cash (OTC) process

Forecast-to-fulfill (FTF) process

Balance sheet locked cash

Procure-to-pay (PTP) process

Sales and customer management

Product range management

Capex and M&A

Non-trade WC Cash tax Tax structure and indirect taxes

Financing and treasury

Personnel costs

Procurement strategy, budget and forecast process

Credit and risk management

Demand planning and sales and operations planning

Sourcing, supplier selection and contracting

Order processing

Manufacturing, scheduling and execution

Requisition-ing and order fulfillment

Invoice issuance

Raw Material planning, purchasing and replenishment

Goods and invoice receipt and evaluation

Customer terms of trade

Inventory management

Invoice processing

Collections management

Sales order processing and customer services

Supplier terms of trade

Dispute management

Finished goods, Warehousing and logistics

Disput management and control

Payment application

Payment issuance management

1Benchmarking

Historical and peer benchmarking to identify improvement opportunities

1

Diagnostic review

Complete end-to-end review of processes and transactional data to quantify the opportunity and initiatives

2

Design and support implement

Detailed action plans, metrics and dashboards, and implementation support

3

3

2

45

Roll out and monitor

Rolling out findings to other divisions and geographies

4

Do you feel that cash is inaccessible in operations and business units?

1Did you face any inventory or receivable write-off in the past or is it expected in the future?

2Do you feel that the investment in WC is not proportionate to sales?

3Do you feel the lack of visibility over cash flow in the system?

4

17 All tied up MENA |

TeamsJon MorrisEY EMEIA Working Capital Leader+44 20 7951 [email protected]

Pearce QuinnDirector — WorkingCapital Advisory+971 4701 0707 [email protected]

Karthik VenkatramExecutive — WorkingCapital Advisory+971 4701 2141 [email protected]

Hani is a partner in Dubai and has over 20 years of work experience in several areas, including WC management, turnaround management, M&A, corporate finance, banking, and corporate restructuring.

He has extensive experience in refinancing corporations undergoing capital restructuring, both as an advisor and a banker. He has managed debt restructuring transactions exceeding US$10b.

In his capacity as advisor, he was involved in very complex transactions, supplier and bank negotiations, and management of departments and large groups of staff in day-to-day operations.

Jon is a partner from the EY member firms in UK Working Capital services and leads Working Capital Advisory for the Europe, Middle East, India and Africa Region.

From a background in EY member firm’s Restructuring Services advising stressed and distressed companies, Jon has successfully transferred these techniques to enhance business performance in a wider field.

Jon’s clients predominantly include both FTSE 100 and private equity houses, with a particular emphasis on manufacturing, service, telecommunications, media and technology sectors.

Pearce is a director of EY MENA Transactions Advisory Services team. He has been with EY in the region for eight years.

Pearce is the director spearheading the Working Capital projects in the MENA Region. Pearce has worked on WC projects for a leading petroleum company in the UAE.

He has assisted a large multinational UAE business understand the potential cash release from implementing a WC optimization program.

Karthik is an experienced professional with the working capital team with EY MENA.

Karthik completed his Executive MBA from the Indian School of Business, Hyderabad, India.

Karthik has performed multiple WC cash release projects across sectors, such as services, manufacturing, and oil and gas.

He has evaluated processes and policies across the WC framework, including operating strategy, accounts payable, accounts receivable, inventory, reporting structure, and monitoring metrics and incentives.

He has identified multiple process inefficiencies, and re-engineered the inventory, receivables and payables processes.

Hani BisharaEY MENA Debt Advisory, Working Capital and Restructuring Leader+971 4 312 9290 [email protected]

18 | All tied up MENA

Methodology and glossary

• The report contains the findings of a review of the WC performance of 326 companies in the MENA region. We have considered companies with a revenue of above US$10m in 2016, headquartered in MENA.

• This report also sets out the findings of a review comparing the WC performance of small, medium, large and very large companies, using sales as the indicator of each company’s size. SMEs have been defined in this report as follows:

• Small — less than US$250m

• Medium — US$251m to US$750m

• Large — US$750m to US$2b

• Very large — more than US$2b

• The overall analysis draws on companies’ latest fiscal 2016 reports. Performance comparisons have been made with 2015, 2014 and 2013 for the companies.

• The report is based on the review, which is segmented by region, country, industry and company. It uses metrics to provide a clear picture of the overall WC management and identify the resulting levels of cash opportunity.

• Each of the companies analyzed in this research has been allocated to an industry and to a region or country. Reported global, regional and country numbers are sales-weighted.

• The overall review excludes financial institutions and real estate companies because of the difficulty of assessing its “true” WC performance, given the intertwined nature of its industrial and financial activities.

• The performance trends at the country and industry levels need to be treated with a degree of caution; the approach is based on consolidated numbers in the absence of further local details, with each company being allocated to the location of its headquarters.

• Because of differences in industry weightings and the level of international activity within each economy, an analysis of the WC performance gap across countries in Europe would not have been useful or meaningful.

• The WC performance metrics are calculated from the latest publicly available company annual financial statements. In order to make the figures as comparable and consistent as possible, adjustments (see glossary) have been made to the data to reflect the impact of acquisitions and disposals, and off-balance sheet arrangements.

• DSO: year-end trade receivables net of provisions, including value-added tax (VAT) and adding back securitized and current financial receivables, divided by full-year pro forma sales and multiplied by 365 (expressed as a number of days of sales, unless stated otherwise)

• DIO: year-end inventories net of provisions, divided by full-year pro forma sales and multiplied by 365 (expressed as a number of days of sales, unless stated otherwise)

• DPO: year-end trade payables, including VAT and adding back trade-accrued expenses, divided by full-year pro forma sales and multiplied by 365 (expressed as a number of days of sales, unless stated otherwise)

• C2C: sum of DSO and DIO less DPO (expressed as a number of days of sales, unless stated otherwise)

• Pro forma sales: reported sales net of VAT, and adjusted for acquisitions and disposals where this information was available

• NWC: year-end trade receivables net of provisions, including VAT and adding back securitized and current financial receivables plus year less end inventories net of provisions — year-end trade payables, including VAT and adding back trade-accrued expenses

Met

hodo

logy

Glo

ssar

y

19 All tied up MENA |

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

The MENA practice of EY has been operating in the region since 1923. For more than 90 years, we have grown to more than 6,000 people united across 20 offices and 15 countries, sharing the same values and an unwavering commitment to quality. As an organization, we continue to develop outstanding leaders who deliver exceptional services to our clients and who contribute to our communities. We are proud of our accomplishments over the years, reaffirming our position as the largest and most established professional services organization in the region.

© 2017 EYGM Limited. All Rights Reserved.

EYG no. 06103-172GBL ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com/mena

![[PreMoney MENA 2015] ArabNet >> Omar Christidis, "THE GLOBAL VC: MENA"](https://static.fdocuments.us/doc/165x107/58d198b51a28ab6f6b8b4a09/premoney-mena-2015-arabnet-omar-christidis-the-global-vc-mena.jpg)