Alamos corp presentation March 2017

41

March 2017 Corporate Presentation

-

Upload

alamosgoldinc -

Category

Investor Relations

-

view

152 -

download

1

Transcript of Alamos corp presentation March 2017

March 2017 Corporate Presentation

2

Cautionary Notes

No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein.

Certain statements in this presentation are “forward-looking statements”, including within the meaning of the United States Securities Exchange Act of 1934, as amended. All statements other than statements of historical

fact included in this presentation, including without limitation statements regarding forecast gold production, gold grades, recoveries, waste-to-ore ratios, total cash costs, potential mineralization and reserves, exploration

results, and future plans and objectives of Alamos, are forward-looking statements based on forecasts of future operational or financial results, estimates of amounts not yet determinable and assumptions of management

that involve various risks and uncertainties. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance

(often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results

“may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be “forward-looking statements.” Alamos cautions that forward-looking information involves known and

unknown risks, uncertainties and other factors that may cause Alamos' actual results, performance or achievements to be materially different from those expressed or implied by such information, including, but not limited

to, gold and silver price volatility; fluctuations in foreign exchange rates and interest rates; the impact of any hedging activities; discrepancies between actual and estimated production, between actual and estimated

reserves and resources or between actual and estimated metallurgical recoveries; costs of production; capital expenditure requirements; the costs and timing of construction and development of new deposits; and the

success of exploration and permitting activities. In addition, the factors described or referred to in the section entitled “Risk Factors” in both Alamos Gold Inc.’s Annual Information Form for the year ended December 31,

2015 along with subsequent public filings available on the SEDAR website at www.sedar.com, should be reviewed in conjunction with the information found in this presentation. Although Alamos has attempted to identify

important factors that could cause actual results, performance or achievements to differ materially from those contained in forward-looking information, there can be other factors that cause results, performance or

achievements not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate or that management’s expectations or estimates of future developments,

circumstances or results will materialize. Accordingly, readers should not place undue reliance on forward-looking information.

Note to U.S. Investors

Alamos prepares its disclosure in accordance with the requirements of securities laws in effect in Canada, which differ from the requirements of U.S. securities laws. Terms relating to mineral resources in this presentation

are defined in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects under the guidelines set out in the Canadian Institute of Mining, Metallurgy, and Petroleum Standards on Mineral

Resources and Mineral Reserves. The United States Securities and Exchange Commission (the “SEC”) permits mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can

economically and legally extract or produce. Alamos may use certain terms, such as “measured mineral resources”, “indicated mineral resources”, “inferred mineral resources” and “probable mineral reserves” that the SEC

does not recognize (these terms may be used in this presentation and are included in the public filings of Alamos, which have been filed with the SEC and the securities commissions or similar authorities in Canada).

Cautionary non-GAAP Measures and Additional GAAP Measures

Note that for purposes of this section, GAAP refers to IFRS. The Company believes that investors use certain non-GAAP and additional GAAP measures as indicators to assess gold mining companies. They are intended to

provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared with GAAP.

“Cash flow from operating activities before changes in non-cash working capital” is a non-GAAP performance measure that could provide an indication of the Company’s ability to generate cash flows from operations, and is

calculated by adding back the change in non-cash working capital to “Cash provided by (used in) operating activities” as presented on the Company’s consolidated statements of cash flows. “Free cash flow” is a non-GAAP

performance measure that is calculated as cash flows from operations net of cash flows invested in mineral property, plant and equipment and exploration and evaluation assets as presented on the Company’s consolidated

statements of cash flows and that would provide an indication of the Company’s ability to generate cash flows from its mineral projects. “Mine site free cash flow” is a non-GAAP measure which includes cash flow from

operating activities at, less capital expenditures at each mine site. Return on Equity is defined as Earnings from Continuing Operations divided by the average Total Equity for the current and previous year. “Mining cost per

tonne of ore” and “Cost per tonne of ore” are non-GAAP performance measures that could provide an indication of the mining and processing efficiency and effectiveness of the mine. These measures are calculated by

dividing the relevant mining and processing costs and total costs by the tonnes of ore processed in the period. “Cost per tonne of ore” is usually affected by operating efficiencies and waste-to-ore ratios in the period. “Total

cash costs per ounce”, “all-in sustaining costs per ounce”, and “mine-site all-in sustaining costs” as used in this analysis are non-GAAP terms typically used by gold mining companies to assess the level of gross margin

available to the Company by subtracting these costs from the unit price realized during the period. These non-GAAP terms are also used to assess the ability of a mining company to generate cash flow from operations.

There may be some variation in the method of computation of these metrics as determined by the Company compared with other mining companies. In this context, “total cash costs” reflects mining and processing costs

allocated from in-process and dore inventory associated and associated royalties with ounces of gold sold in the period. Total cash costs per ounce are exclusive of exploration costs. “All-in sustaining costs per ounce”

include total cash costs, exploration, corporate and administrative, share based compensation and sustaining capital costs. “Mine-site all-in sustaining costs” include total cash costs, exploration, and sustaining capital costs

for the mine-site, but exclude an allocation of corporate and administrative and share based compensation.

Additional GAAP measures that are presented on the face of the Company’s consolidated statements of comprehensive income and are not meant to be a substitute for other subtotals or totals presented in accordance

with IFRS, but rather should be evaluated in conjunction with such IFRS measures. This includes “Earnings from operations”, which is intended to provide an indication of the Company’s operating performance, and

represents the amount of earnings before net finance income/expense, foreign exchange gain/loss, other income/loss, and income tax expense. Non-GAAP and additional GAAP measures do not have a standardized

meaning prescribed under IFRS and therefore may not be comparable to similar measures presented by other companies. A reconciliation of historical non-GAAP and additional GAAP measures are available at

www.alamosgold.com.

Technical Information

Except as otherwise noted herein, Chris Bostwick, FAusIMM, Alamos Gold’s Vice President, Technical Services, has reviewed and approved the scientific and technical information contained in this presentation. Chris

Bostwick is a Qualified Person within the meaning of Canadian Securities Administrator’s National Instrument 43-101. For more information, please refer to the Alamos Gold Inc. 2015 Annual Information Form and the

technical reports referenced therein and in this presentation, available on SEDAR (www.sedar.com).

All figures in US$ unless otherwise indicated.

Cautionary Notes

3

1 Based on 2017 Guidance2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Includes cash as of December 31, 2016 and $240 million net proceeds from equity offering completed February 9, 2017.

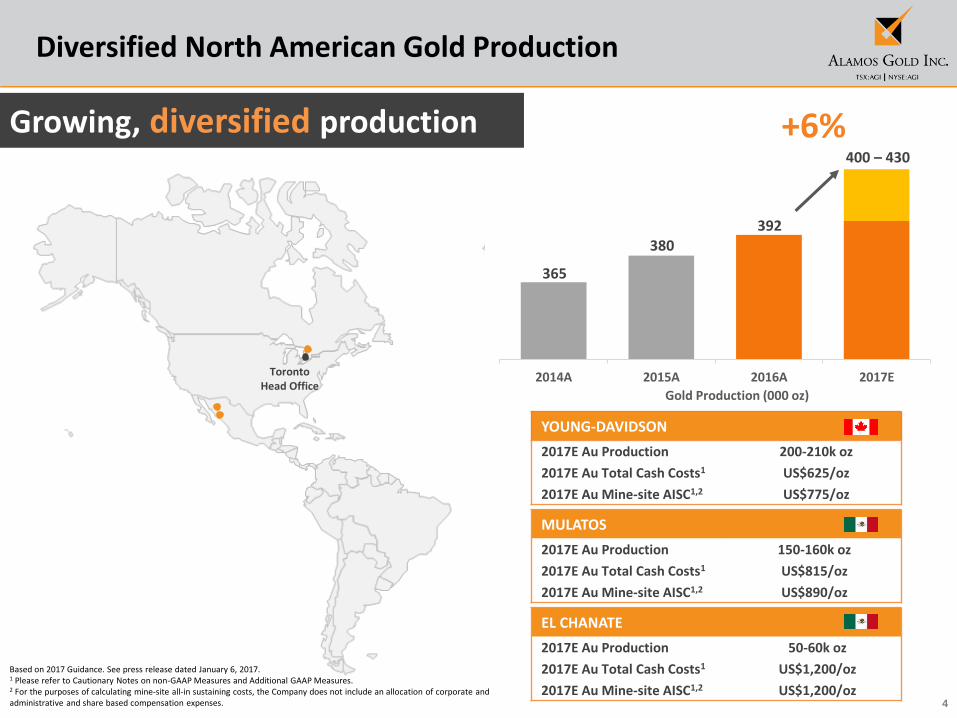

Strong Platform for Delivering Long Term Value

Diversified gold production

400,000 – 430,000 oz from three North American mines1

Expanding margins

$940/oz AISC, an expected 7% decrease from 20161,2

Peer leading growth

Portfolio of 6 low-cost development projects

Strong balance sheet

$492m pro-forma cash3 to support internal growth & debt retirement

Track record of delivering

shareholder value

4

2014A 2015A 2016A 2017E

Gold Production (000 oz)

TorontoHead Office

Diversified North American Gold Production

Based on 2017 Guidance. See press release dated January 6, 2017.1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.2 For the purposes of calculating mine-site all-in sustaining costs, the Company does not include an allocation of corporate and administrative and share based compensation expenses.

Growing, diversified production

380392

400 – 430

+6%

MULATOS

2017E Au Production 150-160k oz

2017E Au Total Cash Costs1 US$815/oz

2017E Au Mine-site AISC1,2 US$890/oz

EL CHANATE

2017E Au Production 50-60k oz

2017E Au Total Cash Costs1 US$1,200/oz

2017E Au Mine-site AISC1,2 US$1,200/oz

YOUNG-DAVIDSON

2017E Au Production 200-210k oz

2017E Au Total Cash Costs1 US$625/oz

2017E Au Mine-site AISC1,2 US$775/oz

365

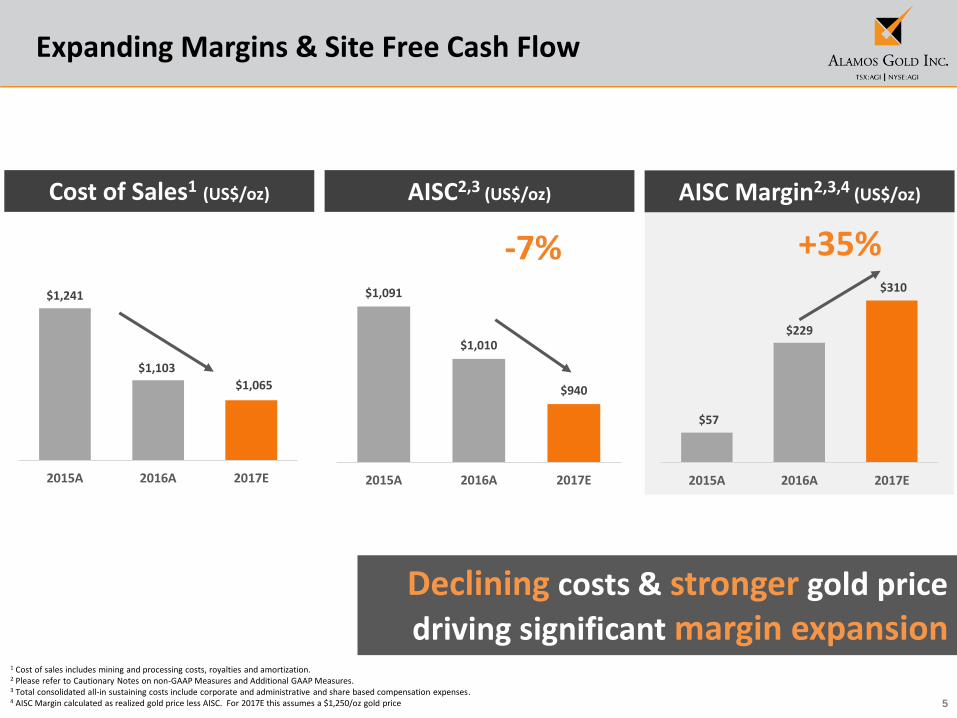

5

$57

$229

$310

2015A 2016A 2017E

$1,091

$1,010

$940

2015A 2016A 2017E

$1,241

$1,103

$1,065

2015A 2016A 2017E

Expanding Margins & Site Free Cash Flow

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Total consolidated all-in sustaining costs include corporate and administrative and share based compensation expenses.4 AISC Margin calculated as realized gold price less AISC. For 2017E this assumes a $1,250/oz gold price

AISC2,3 (US$/oz)

-7%

Cost of Sales1 (US$/oz)

+35%

AISC Margin2,3,4 (US$/oz)

Declining costs & stronger gold price

driving significant margin expansion

6

Leading development pipelineGrowth at existing

operations

ESPERANZA

Peer Leading Low-Cost Growth Profile

Controlled, disciplined, multi-stage growth

Advanced exploration

AĞI DAĞI

KIRAZLI

ÇAMYURT

QUARTZ MOUNTAIN

LYNN LAKE

MULATOS DISTRICT

Producing Assets

Development/Exploration Assets

YOUNG-DAVIDSONRAMP-UP

MULATOS: LA YAQUI & CERRO PELON

7

Strong Balance Sheet

1 Unaudited management estimate as of December 31, 2016 2 Pro-forma cash includes cash as of December 31, 2016 plus $240 million net proceeds of equity financing completed February 9, 20173 Available liquidity includes pro-forma cash and undrawn $150m credit facility4As of March 2, 2017

Balance Sheet

Pro-forma Cash1,2 US$492 million

Available Liquidity3 US$642 million

Total Debt1 US$315 million

Capital Structure

Shares Outstanding 298.7 million

Warrants 11.8 million

Employee Options 9.0 million

Fully Diluted 322.2 million

Recent Share Price (TSX)4 C$9.20

Market Capitalization ~C$2.7 billion

2

$492m Pro-forma cash following equity financing

$24m Annual interest savings; $70m over remaining term

$252$315

$240

Pro-forma Cash Debt

as of December 31, 2016

$315m High yield notes to be retired in April 2017

$492m

$315m

1,2

8

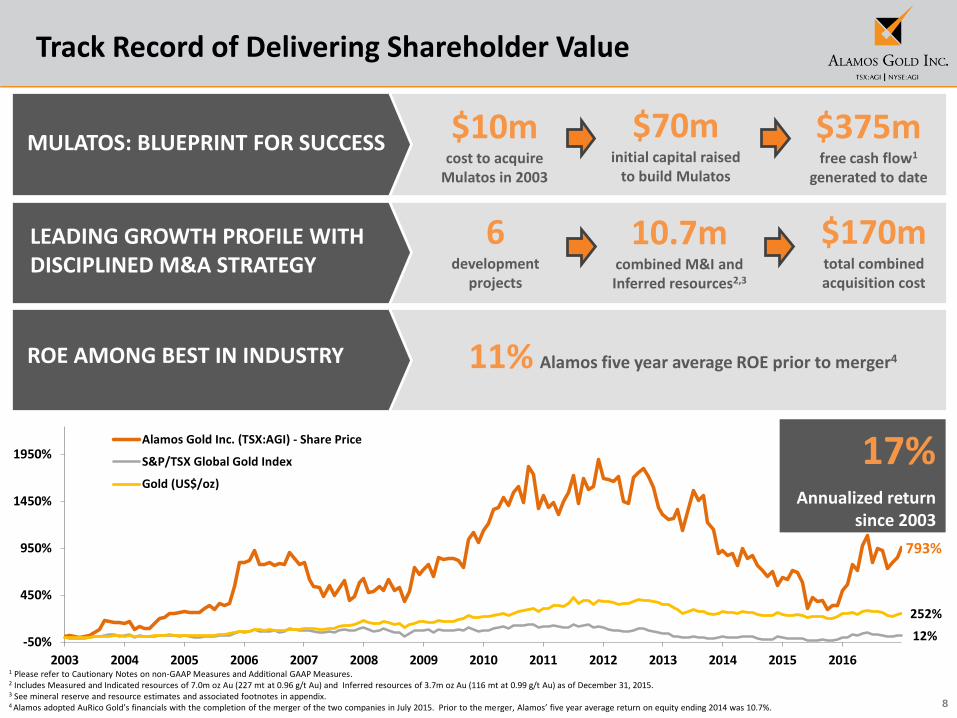

793%

12%

252%

-50%

450%

950%

1450%

1950%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Alamos Gold Inc. (TSX:AGI) - Share Price

S&P/TSX Global Gold Index

Gold (US$/oz)

Track Record of Delivering Shareholder Value

17%Annualized return

since 2003

MULATOS: BLUEPRINT FOR SUCCESS

LEADING GROWTH PROFILE WITH DISCIPLINED M&A STRATEGY

ROE AMONG BEST IN INDUSTRY 11% Alamos five year average ROE prior to merger4

$10mcost to acquire

Mulatos in 2003

$375mfree cash flow1

generated to date

$70minitial capital raised

to build Mulatos

6development

projects

$170mtotal combined acquisition cost

10.7mcombined M&I and Inferred resources2,3

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.2 Includes Measured and Indicated resources of 7.0m oz Au (227 mt at 0.96 g/t Au) and Inferred resources of 3.7m oz Au (116 mt at 0.99 g/t Au) as of December 31, 2015.3 See mineral reserve and resource estimates and associated footnotes in appendix.4 Alamos adopted AuRico Gold’s financials with the completion of the merger of the two companies in July 2015. Prior to the merger, Alamos’ five year average return on equity ending 2014 was 10.7%.

9

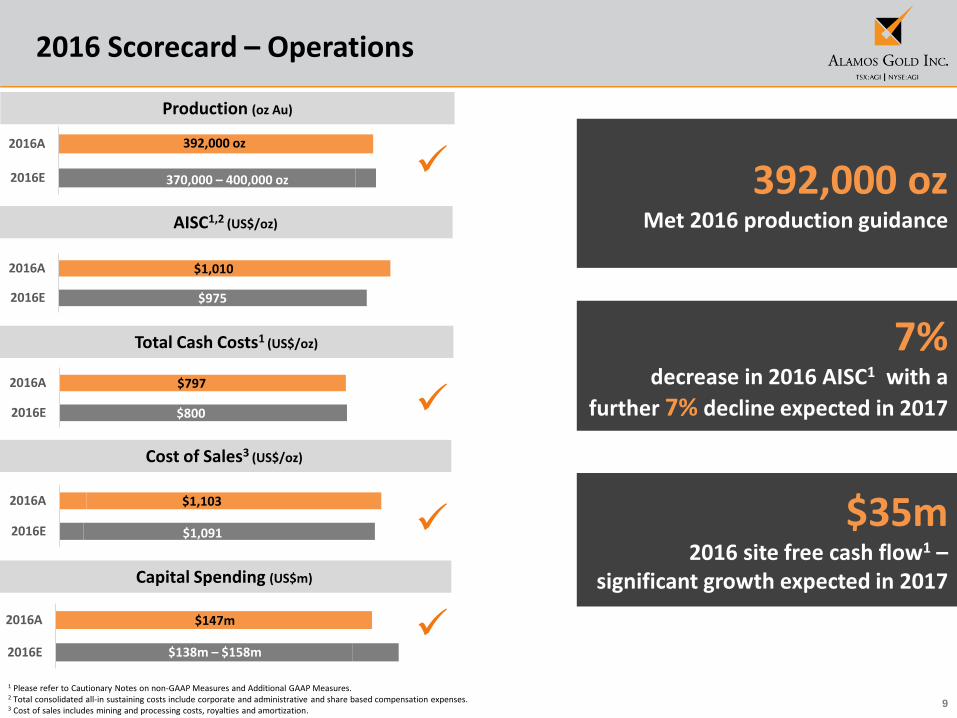

2016 Scorecard – Operations

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 2 Total consolidated all-in sustaining costs include corporate and administrative and share based compensation expenses. 3 Cost of sales includes mining and processing costs, royalties and amortization.

7%decrease in 2016 AISC1 with a

further 7% decline expected in 2017

Production (oz Au)

Capital Spending (US$m)

AISC1,2 (US$/oz)

$35m 2016 site free cash flow1 –

significant growth expected in 2017

392,000 ozMet 2016 production guidance

Cost of Sales3 (US$/oz)

Total Cash Costs1 (US$/oz)

2016E

2016A

$975

$1,010

2016E

2016A

$800

$797

2016E

2016A

$1,091

$1,103

2016E

2016A

2016E

2016A

370,000 – 400,000 oz

392,000 oz

$147m

$138m – $158m

10

Development Pipeline – Surfacing Value – La Yaqui Phase I

1.4 g/t Au

Reserve grade1 68% above Mulatos 2017 budget

H2-2017 Initial production - Phase I

development on track

~$400/oz2017 total cash costs1, 50%

below Mulatos budget

1 See mineral reserve and resource estimates and associated footnotes in appendix.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

11

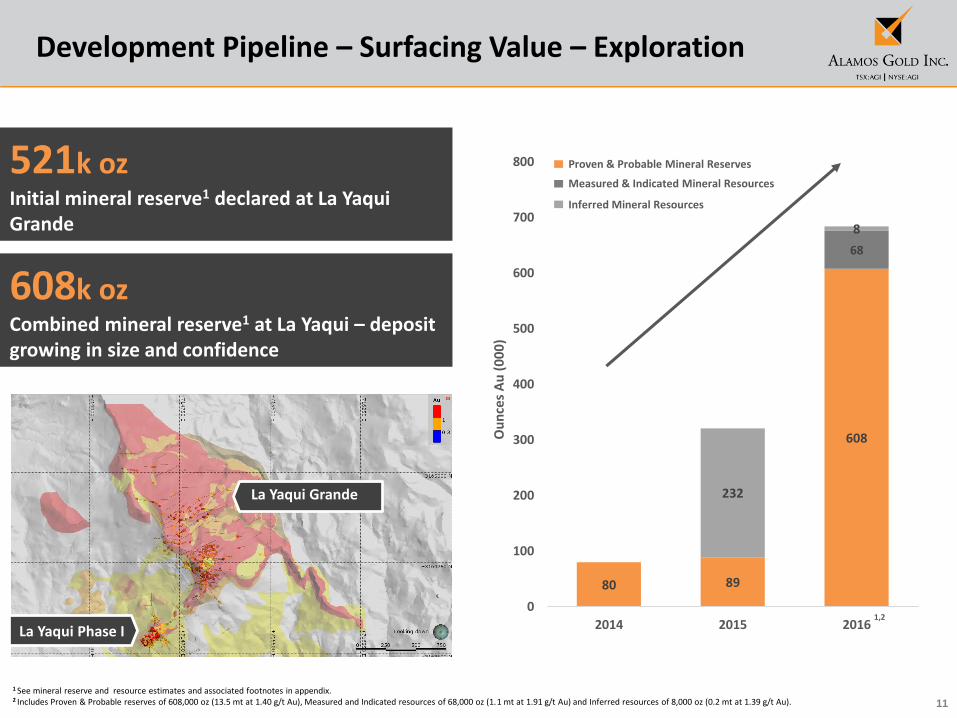

80 89

608

68

232

8

0

100

200

300

400

500

600

700

800

2014 2015 2016

Ou

nce

s A

u (

00

0)

Development Pipeline – Surfacing Value – Exploration

1 See mineral reserve and resource estimates and associated footnotes in appendix.2 Includes Proven & Probable reserves of 608,000 oz (13.5 mt at 1.40 g/t Au), Measured and Indicated resources of 68,000 oz (1.1 mt at 1.91 g/t Au) and Inferred resources of 8,000 oz (0.2 mt at 1.39 g/t Au).

La Yaqui Grande

La Yaqui Phase I

Proven & Probable Mineral Reserves

Inferred Mineral Resources

Measured & Indicated Mineral Resources521k ozInitial mineral reserve1 declared at La Yaqui Grande

608k ozCombined mineral reserve1 at La Yaqui – deposit growing in size and confidence

1,2

12

14.2

18.5

0

5

10

15

20

2015 2016

5.9

7.7

0

2

4

6

8

10

2015 2016

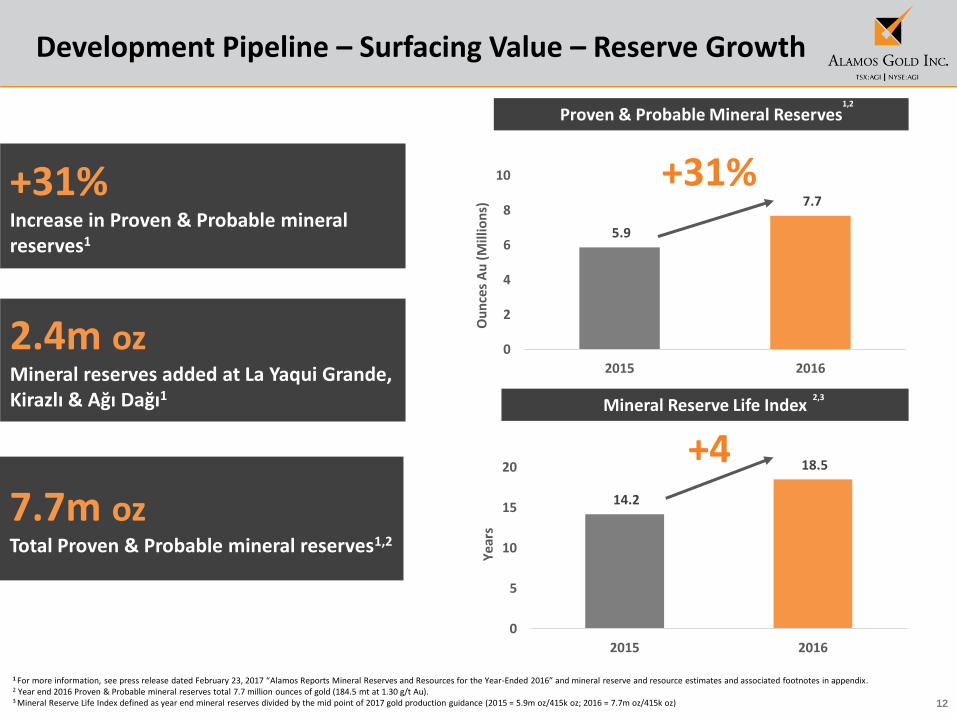

Development Pipeline – Surfacing Value – Reserve Growth

+31%

1 For more information, see press release dated February 23, 2017 “Alamos Reports Mineral Reserves and Resources for the Year-Ended 2016” and mineral reserve and resource estimates and associated footnotes in appendix.2 Year end 2016 Proven & Probable mineral reserves total 7.7 million ounces of gold (184.5 mt at 1.30 g/t Au).3 Mineral Reserve Life Index defined as year end mineral reserves divided by the mid point of 2017 gold production guidance (2015 = 5.9m oz/415k oz; 2016 = 7.7m oz/415k oz)

+31%Increase in Proven & Probable mineral reserves1

7.7m ozTotal Proven & Probable mineral reserves1,2

2.4m ozMineral reserves added at La Yaqui Grande, Kirazlı & Ağı Dağı1

+4O

un

ces

Au

(M

illio

ns)

Ye

ars

Proven & Probable Mineral Reserves

Mineral Reserve Life Index2,3

1,2

13

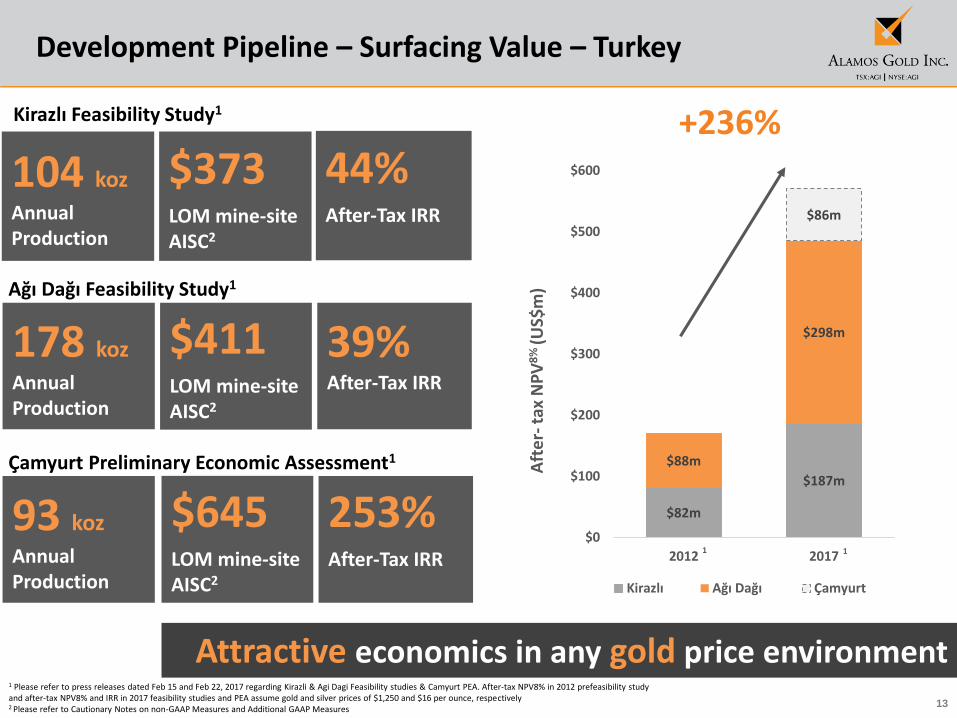

Development Pipeline – Surfacing Value – Turkey

Aft

er-

tax

NP

V8

% (U

S$m

)

$82m

$187m

$88m

$298m

$86m

$0

$100

$200

$300

$400

$500

$600

2012 2017

Kirazlı Ağı Dağı Çamyurt

+236%

104 koz

Annual Production

$373LOM mine-site AISC2

44%After-Tax IRR

Kirazlı Feasibility Study1

178 koz

Annual Production

$411LOM mine-site AISC2

39%After-Tax IRR

Ağı Dağı Feasibility Study1

93 koz

Annual Production

$645LOM mine-site AISC2

253%After-Tax IRR

Çamyurt Preliminary Economic Assessment1

Attractive economics in any gold price environment1 Please refer to press releases dated Feb 15 and Feb 22, 2017 regarding Kirazli & Agi Dagi Feasibility studies & Camyurt PEA. After-tax NPV8% in 2012 prefeasibility study and after-tax NPV8% and IRR in 2017 feasibility studies and PEA assume gold and silver prices of $1,250 and $16 per ounce, respectively 2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures

11

14

$1,091

$1,010$940

2015A 2016A 2017E2015A 2016A 2017E

$1,241

$1,103$1,065

2015A 2016A 2017E 2015A 2016A 2017E

2017 Guidance – Growing Production, Declining Costs

Gold Production (000 oz) AISC1,2 (US$/oz)

-7%

Total Capital Spending (US$m)

$147m$140-157m

Cost of Sales3 (US$/oz)

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 2 Total consolidated all-in sustaining costs include corporate and administrative and share based compensation expenses. 3 Cost of sales includes mining and processing costs, royalties and amortization.4 Total capital spending for Alamos has been included for the periods prior to July 2, 2015 for comparative purposes only.

392

400 – 430

+6%

380

$190m4

15

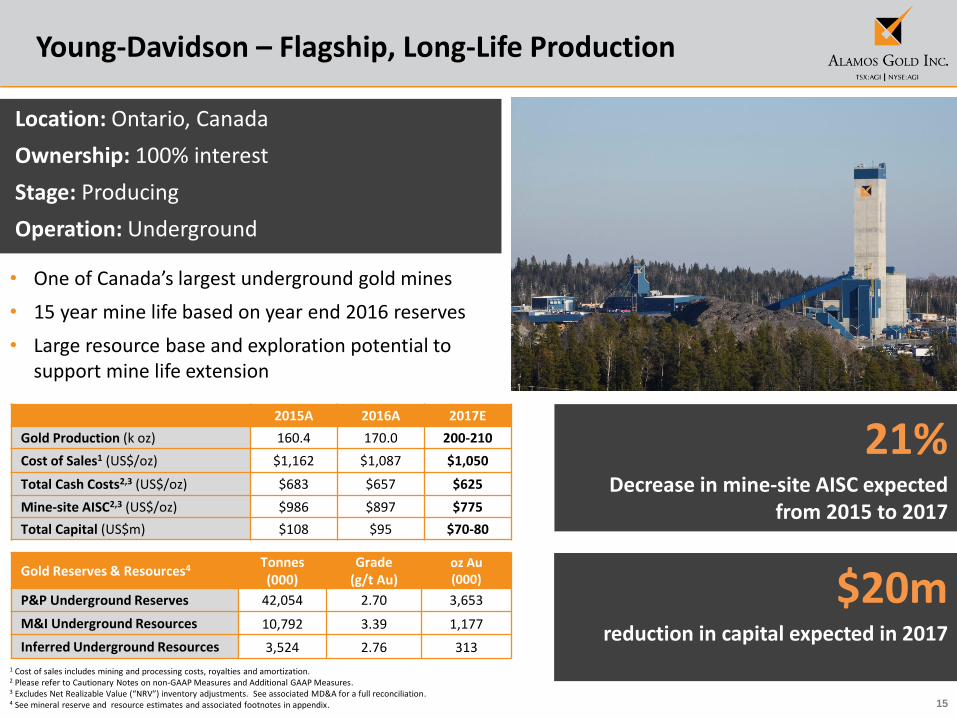

Young-Davidson – Flagship, Long-Life Production

Location: Ontario, Canada

Ownership: 100% interest

Stage: Producing

Operation: Underground

• One of Canada’s largest underground gold mines

• 15 year mine life based on year end 2016 reserves

• Large resource base and exploration potential to support mine life extension

Gold Reserves & Resources4 Tonnes (000)

Grade (g/t Au)

oz Au (000)

P&P Underground Reserves 42,054 2.70 3,653

M&I Underground Resources 10,792 3.39 1,177

Inferred Underground Resources 3,524 2.76 313

$20mreduction in capital expected in 2017

21%Decrease in mine-site AISC expected

from 2015 to 2017

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Excludes Net Realizable Value (“NRV”) inventory adjustments. See associated MD&A for a full reconciliation.4 See mineral reserve and resource estimates and associated footnotes in appendix.

2015A 2016A 2017E

Gold Production (k oz) 160.4 170.0 200-210

Cost of Sales1 (US$/oz) $1,162 $1,087 $1,050

Total Cash Costs2,3 (US$/oz) $683 $657 $625

Mine-site AISC2,3 (US$/oz) $986 $897 $775

Total Capital (US$m) $108 $95 $70-80

16

Growing production; declining costs; declining capital intensity

6,675 tpdaverage underground mining rate

in Q4 2016

Young-Davidson – Ramp up of Underground Mining

Owner developmenttransition completed in April 2016

>7,000 tpdachieved 2016 year-end

underground mining rate target

Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Q1

/13

Q2

/13

Q3

/13

Q4

/13

Q1

/14

Q2

/14

Q3

/14

Q4

/14

Q1

/15

Q2

/15

Q3

/15

Q4

/15

Q1

/16

Q2

/16

Q3

/16

Q4

/16

Mill TPD Underground TPD

6,500 - 7,500 tpdunderground mining rate

expected in 2017

17

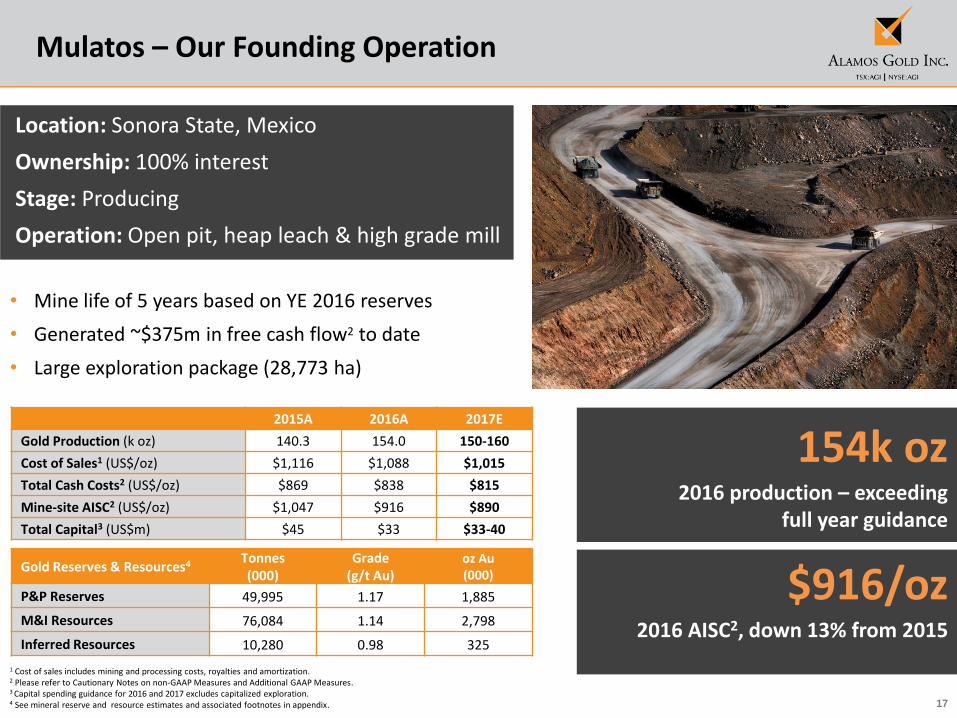

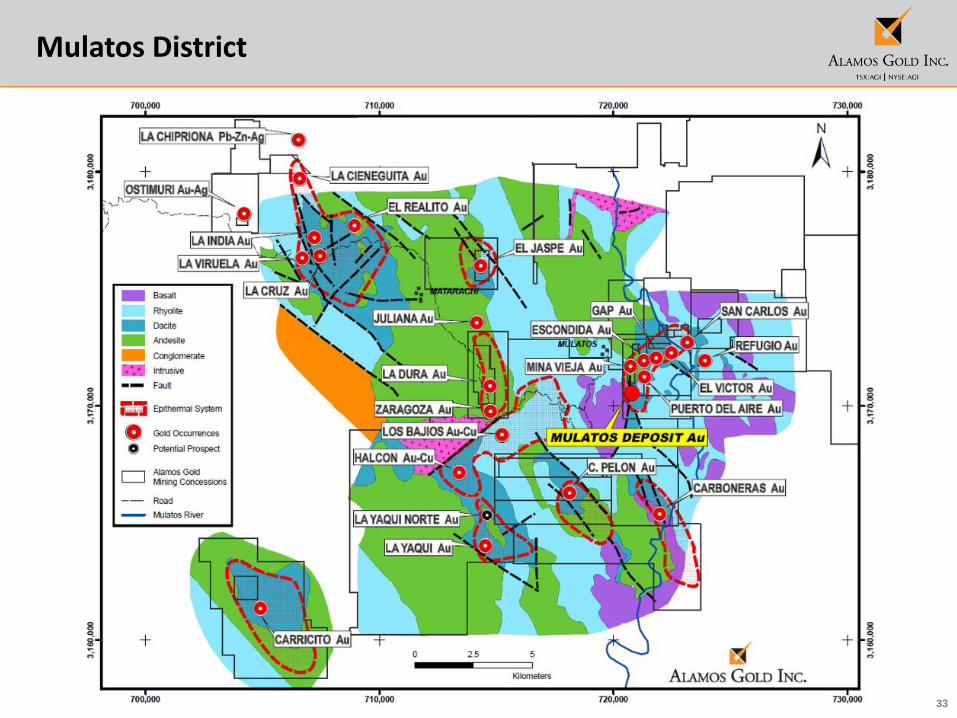

Mulatos – Our Founding Operation

Location: Sonora State, Mexico

Ownership: 100% interest

Stage: Producing

Operation: Open pit, heap leach & high grade mill

• Mine life of 5 years based on YE 2016 reserves

• Generated ~$375m in free cash flow2 to date

• Large exploration package (28,773 ha)

Gold Reserves & Resources4 Tonnes (000)

Grade (g/t Au)

oz Au(000)

P&P Reserves 49,995 1.17 1,885

M&I Resources 76,084 1.14 2,798

Inferred Resources 10,280 0.98 325

$916/oz2016 AISC2, down 13% from 2015

154k oz2016 production – exceeding

full year guidance

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Capital spending guidance for 2016 and 2017 excludes capitalized exploration.4 See mineral reserve and resource estimates and associated footnotes in appendix.

2015A 2016A 2017E

Gold Production (k oz) 140.3 154.0 150-160

Cost of Sales1 (US$/oz) $1,116 $1,088 $1,015

Total Cash Costs2 (US$/oz) $869 $838 $815

Mine-site AISC2 (US$/oz) $1,047 $916 $890

Total Capital3 (US$m) $45 $33 $33-40

18

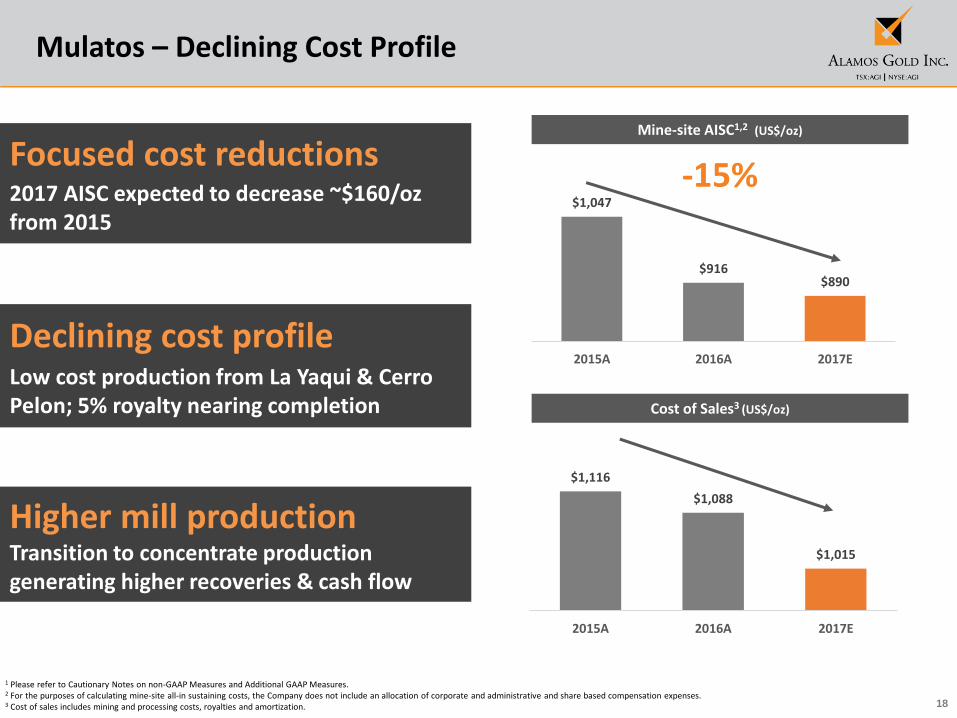

$1,047

$916$890

2015A 2016A 2017E

Focused cost reductions2017 AISC expected to decrease ~$160/oz from 2015

Higher mill productionTransition to concentrate production generating higher recoveries & cash flow

Declining cost profileLow cost production from La Yaqui & Cerro Pelon; 5% royalty nearing completion

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 2 For the purposes of calculating mine-site all-in sustaining costs, the Company does not include an allocation of corporate and administrative and share based compensation expenses.3 Cost of sales includes mining and processing costs, royalties and amortization.

Mine-site AISC1,2 (US$/oz)

Cost of Sales3 (US$/oz)

-15%

$1,116

$1,088

$1,015

2015A 2016A 2017E

Mulatos – Declining Cost Profile

19

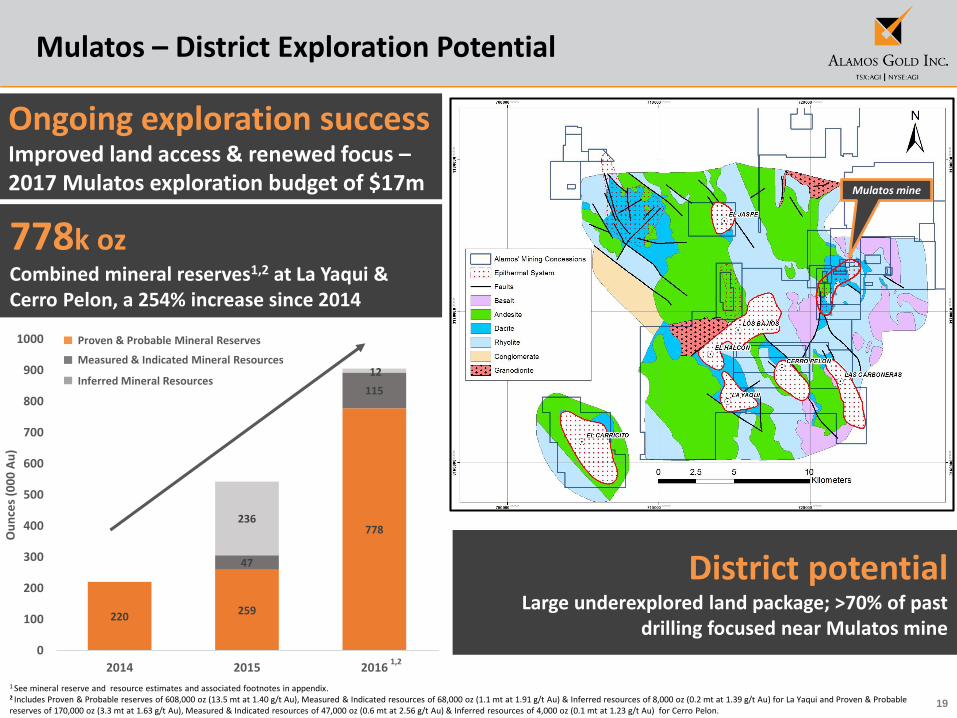

Mulatos – District Exploration Potential

1 See mineral reserve and resource estimates and associated footnotes in appendix.2 Includes Proven & Probable reserves of 608,000 oz (13.5 mt at 1.40 g/t Au), Measured & Indicated resources of 68,000 oz (1.1 mt at 1.91 g/t Au) & Inferred resources of 8,000 oz (0.2 mt at 1.39 g/t Au) for La Yaqui and Proven & Probable reserves of 170,000 oz (3.3 mt at 1.63 g/t Au), Measured & Indicated resources of 47,000 oz (0.6 mt at 2.56 g/t Au) & Inferred resources of 4,000 oz (0.1 mt at 1.23 g/t Au) for Cerro Pelon.

778k oz Combined mineral reserves1,2 at La Yaqui & Cerro Pelon, a 254% increase since 2014

District potentialLarge underexplored land package; >70% of past

drilling focused near Mulatos mine

Mulatos District

Mulatos mine

220259

778

47

115

236

12

0

100

200

300

400

500

600

700

800

900

1000

2014 2015 2016

Ou

nce

s (0

00

Au

)

Proven & Probable Mineral Reserves

Inferred Mineral Resources

Measured & Indicated Mineral Resources

1,2

Ongoing exploration success Improved land access & renewed focus –2017 Mulatos exploration budget of $17m

20

El Chanate – Consistent Gold Producer

Location: Sonora State, Mexico

Ownership: 100% interest

Stage: Producing

Operation: Open pit, heap leach

• Positive free cash flow generation in 2016

• Significant free cash flow at end of mine life – low cost production through residual leaching

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Excludes Net Realizable Value (“NRV”) inventory adjustments. See associated MD&A for a full reconciliation.4 See mineral reserve and resource estimates and associated footnotes in appendix.5 ~75% of El Chanate’s 2017 expected production has been hedged through gold collars ensuring minimum gold price of $1,225/oz and participation up to $1,450/oz

Gold Reserves & Resources4 Tonnes (000)

Grade (g/t Au)

oz Au(000)

P&P Reserves – Open Pit 10,812 0.56 193

P&P Reserves – Leach Pad Inventory - - 100

M&I Resources 4,415 0.66 93

~75%2017 production hedged ensuring minimum gold price of $1,225/oz5

$5m Site free cash flow2 generated in 2016

2015A 2016A 2017E

Gold Production (k oz) 79.3 68.0 50-60

Cost of Sales1 (US$/oz) $1,504 $1,177 $1,265

Total Cash Costs2,3 (US$/oz) $808 $1,052 $1,200

Mine-site AISC2,3 (US$/oz) $978 $1,069 $1,200

Total Capital (US$m) $14 $1 $2

21

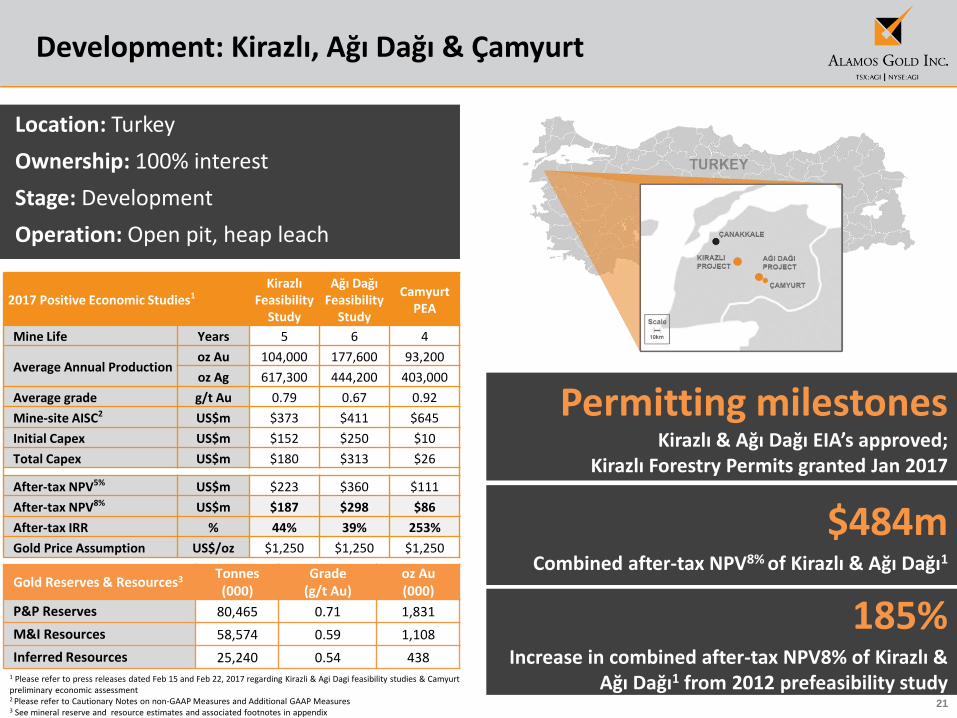

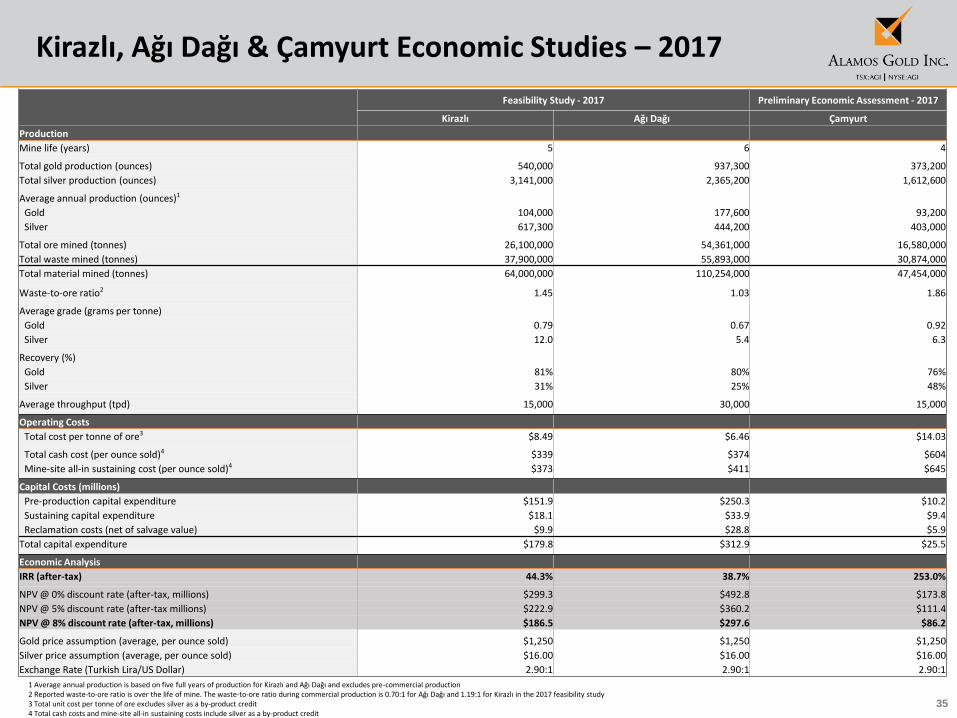

Development: Kirazlı, Ağı Dağı & Çamyurt

1 Please refer to press releases dated Feb 15 and Feb 22, 2017 regarding Kirazli & Agi Dagi feasibility studies & Camyurtpreliminary economic assessment2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures3 See mineral reserve and resource estimates and associated footnotes in appendix

Location: Turkey

Ownership: 100% interest

Stage: Development

Operation: Open pit, heap leach

Permitting milestonesKirazlı & Ağı Dağı EIA’s approved;

Kirazlı Forestry Permits granted Jan 2017

185%Increase in combined after-tax NPV8% of Kirazlı &

Ağı Dağı1 from 2012 prefeasibility study

Gold Reserves & Resources3 Tonnes (000)

Grade (g/t Au)

oz Au(000)

P&P Reserves 80,465 0.71 1,831

M&I Resources 58,574 0.59 1,108

Inferred Resources 25,240 0.54 438

$484mCombined after-tax NPV8% of Kirazlı & Ağı Dağı1

2017 Positive Economic Studies1Kirazlı

Feasibility Study

Ağı Dağı Feasibility

Study

CamyurtPEA

Mine Life Years 5 6 4

Average Annual Productionoz Au 104,000 177,600 93,200

oz Ag 617,300 444,200 403,000

Average grade g/t Au 0.79 0.67 0.92

Mine-site AISC2 US$m $373 $411 $645

Initial Capex US$m $152 $250 $10

Total Capex US$m $180 $313 $26

After-tax NPV5% US$m $223 $360 $111

After-tax NPV8% US$m $187 $298 $86

After-tax IRR % 44% 39% 253%

Gold Price Assumption US$/oz $1,250 $1,250 $1,250

22

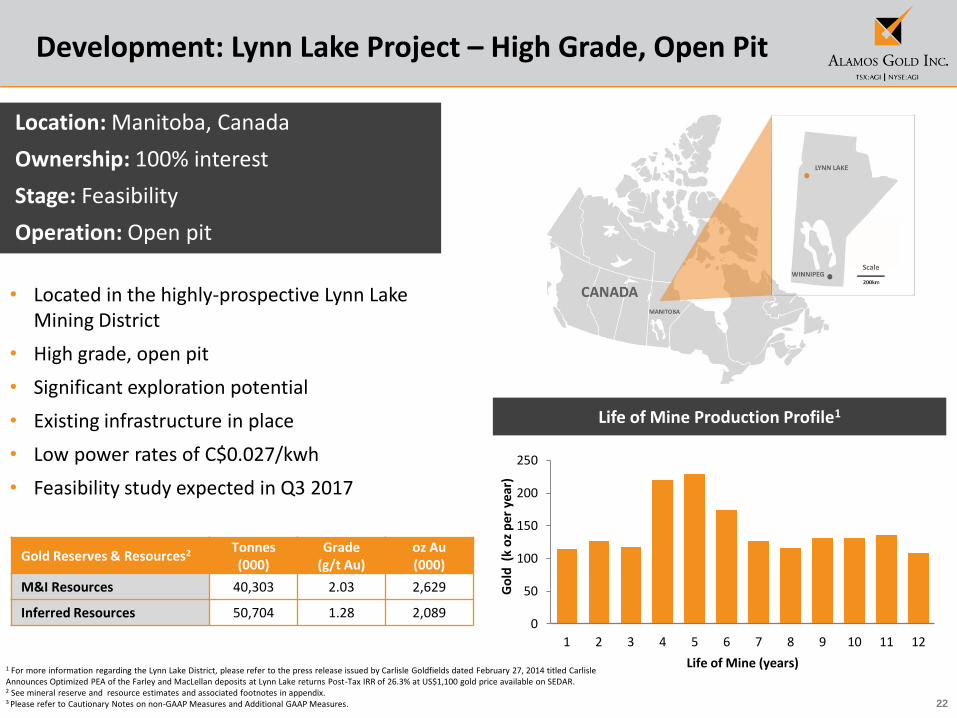

Development: Lynn Lake Project – High Grade, Open Pit

1 For more information regarding the Lynn Lake District, please refer to the press release issued by Carlisle Goldfields dated February 27, 2014 titled Carlisle Announces Optimized PEA of the Farley and MacLellan deposits at Lynn Lake returns Post-Tax IRR of 26.3% at US$1,100 gold price available on SEDAR.2 See mineral reserve and resource estimates and associated footnotes in appendix.3 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

Location: Manitoba, Canada

Ownership: 100% interest

Stage: Feasibility

Operation: Open pit

• Located in the highly-prospective Lynn Lake Mining District

• High grade, open pit

• Significant exploration potential

• Existing infrastructure in place

• Low power rates of C$0.027/kwh

• Feasibility study expected in Q3 2017

Life of Mine Production Profile1

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10 11 12

Go

ld (

k o

z p

er y

ear

)

Life of Mine (years)

Gold Reserves & Resources2 Tonnes (000)

Grade (g/t Au)

oz Au (000)

M&I Resources 40,303 2.03 2,629

Inferred Resources 50,704 1.28 2,089

23

Development: Esperanza & Quartz Mountain

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures2 Historic column recovery tests for gold at Quartz Mountain varied between 74% and 88% for the felsic rock hosted mineralization; see Orsa Ventures press release dated February 12, 20133 See mineral reserve and resource estimates and associated footnotes in appendix.4 Additional C$3m due on completion of feasibility study & C$15m or 2% NSR upon successful permitting

Location: Morelos State, Mexico

Ownership: 100% interest

Stage: Development

Operation: Open pit, heap leach

• Excellent infrastructure; low technical risk

• Low capital intensity and operating costs

• Average annual production potential > 100,000 oz

• All-in sustaining costs expected to be lowest quartile1

Location: Oregon, United States

Ownership: Right to earn a 100% interest4

Stage: Advanced Exploration

• Located on northern extension of prolific Basin & Range

Province of Nevada

• Low strip ratio, favourable metallurgy2

• Acquisition cost $3.5m

Tonnes Grade Contained Ounces

(000) (g/t Au) (g/t Ag) (000 Au) (000 Ag)

Measured & Indicated3 34,352 0.98 8.09 1,083 8,936

Inferred 718 0.80 15.04 18 347

Quartz Butte

Crone Hill

Tonnes Grade Contained Ounces

(000) (g/t Au) (000 Au)

Measured & Indicated3 12,156 0.87 339

Inferred 39,205 0.91 1,147

Project: Esperanza

Project: Quartz Mountain

24

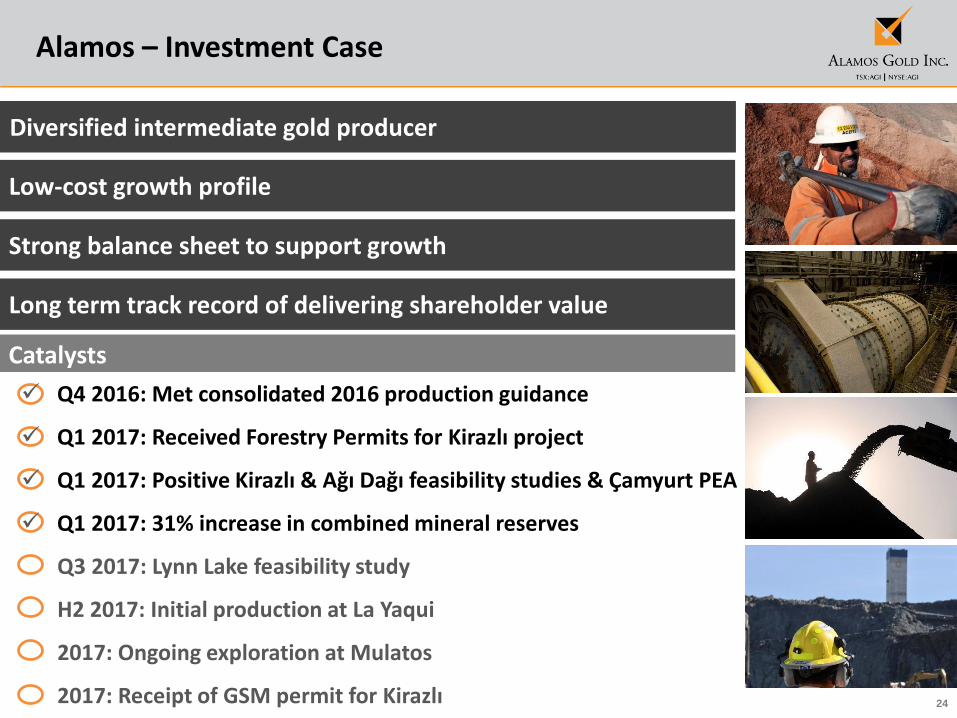

Q4 2016: Met consolidated 2016 production guidance

Q1 2017: Received Forestry Permits for Kirazlı project

Q1 2017: Positive Kirazlı & Ağı Dağı feasibility studies & Çamyurt PEA

Q1 2017: 31% increase in combined mineral reserves

Q3 2017: Lynn Lake feasibility study

H2 2017: Initial production at La Yaqui

2017: Ongoing exploration at Mulatos

2017: Receipt of GSM permit for Kirazlı

Alamos – Investment Case

Diversified intermediate gold producer

Low-cost growth profile

Strong balance sheet to support growth

Long term track record of delivering shareholder value

Catalysts

25

Appendices

26

Board of Directors and Executive and Management Team

Paul J. Murphy Chairman

John A. McCluskey Director

Mark J. Daniel Director

Patrick D. Downey Director

David Fleck Director

David Gower Director

Claire M. C. Kennedy Director

Ronald E. Smith Director

Kenneth Stowe Director

John A. McCluskey President and Chief Executive Officer

Jamie Porter Chief Financial Officer

Peter MacPhail Chief Operating Officer

Christine Barwell Vice President, Human Resources

Chris Bostwick Vice President, Technical Services

Luis Chavez Senior Vice President, Mexico

Andrew Cormier Vice President, Development & Construction

Nils Engelstad Vice President, General Counsel

Greg Fisher Vice President, Finance

Aoife McGrath Vice President, Exploration

Scott Parsons Vice President, Investor Relations

Colin Webster Vice President, Sustainability & External Affairs

Board of Directors Executive and Management Team

27

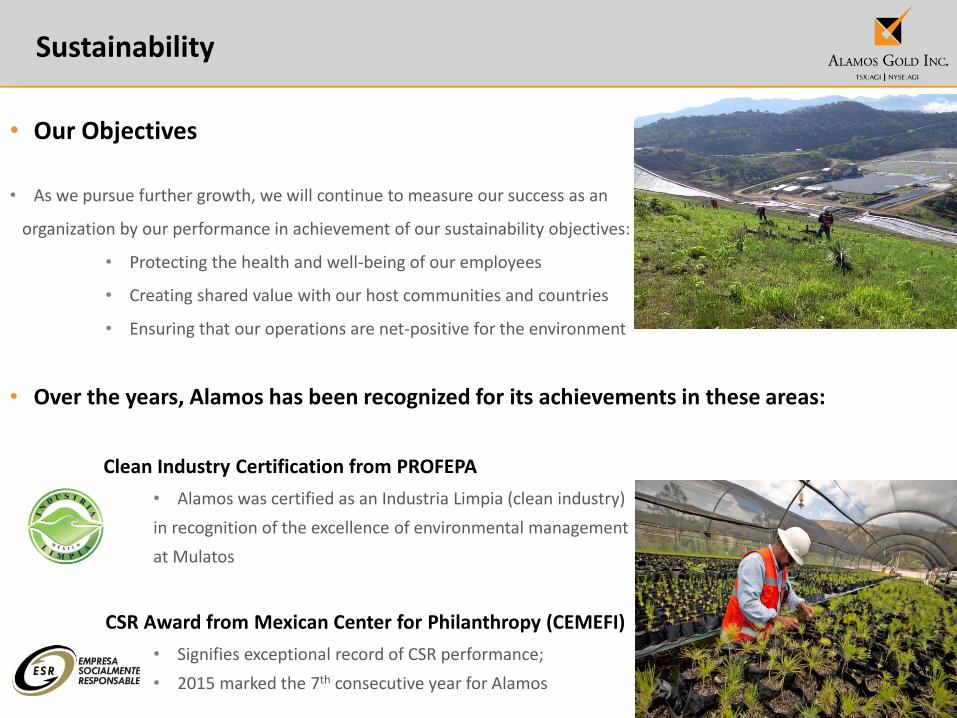

Sustainability

• Our Objectives

• As we pursue further growth, we will continue to measure our success as an

organization by our performance in achievement of our sustainability objectives:

• Protecting the health and well-being of our employees

• Creating shared value with our host communities and countries

• Ensuring that our operations are net-positive for the environment

• Over the years, Alamos has been recognized for its achievements in these areas:

Clean Industry Certification from PROFEPA

• Alamos was certified as an Industria Limpia (clean industry)

in recognition of the excellence of environmental management

at Mulatos

CSR Award from Mexican Center for Philanthropy (CEMEFI)

• Signifies exceptional record of CSR performance;

• 2015 marked the 7th consecutive year for Alamos

28

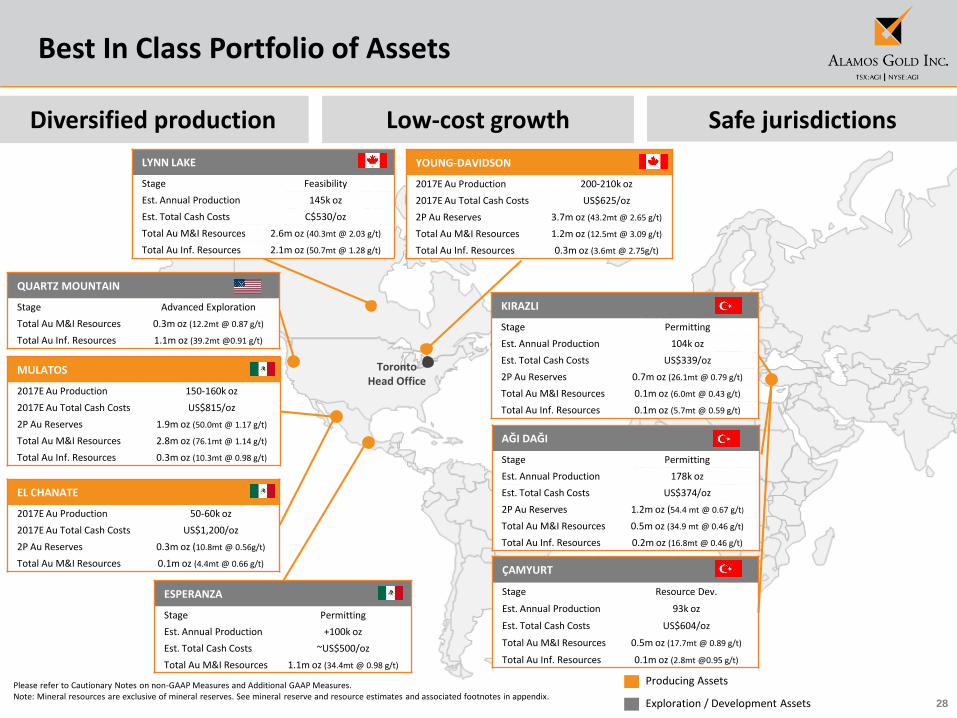

Best In Class Portfolio of Assets

MULATOS

2017E Au Production 150-160k oz

2017E Au Total Cash Costs US$815/oz

2P Au Reserves 1.9m oz (50.0mt @ 1.17 g/t)

Total Au M&I Resources 2.8m oz (76.1mt @ 1.14 g/t)

Total Au Inf. Resources 0.3m oz (10.3mt @ 0.98 g/t)

EL CHANATE

2017E Au Production 50-60k oz

2017E Au Total Cash Costs US$1,200/oz

2P Au Reserves 0.3m oz (10.8mt @ 0.56g/t)

Total Au M&I Resources 0.1m oz (4.4mt @ 0.66 g/t)

QUARTZ MOUNTAIN

Stage Advanced Exploration

Total Au M&I Resources 0.3m oz (12.2mt @ 0.87 g/t)

Total Au Inf. Resources 1.1m oz (39.2mt @0.91 g/t)

YOUNG-DAVIDSON

2017E Au Production 200-210k oz

2017E Au Total Cash Costs US$625/oz

2P Au Reserves 3.7m oz (43.2mt @ 2.65 g/t)

Total Au M&I Resources 1.2m oz (12.5mt @ 3.09 g/t)

Total Au Inf. Resources 0.3m oz (3.6mt @ 2.75g/t)

AĞI DAĞI

Stage Permitting

Est. Annual Production 178k oz

Est. Total Cash Costs US$374/oz

2P Au Reserves 1.2m oz (54.4 mt @ 0.67 g/t)

Total Au M&I Resources 0.5m oz (34.9 mt @ 0.46 g/t)

Total Au Inf. Resources 0.2m oz (16.8mt @ 0.46 g/t)

Producing Assets

Exploration / Development Assets

TorontoHead Office

ESPERANZA

Stage Permitting

Est. Annual Production +100k oz

Est. Total Cash Costs ~US$500/oz

Total Au M&I Resources 1.1m oz (34.4mt @ 0.98 g/t)

KIRAZLI

Stage Permitting

Est. Annual Production 104k oz

Est. Total Cash Costs US$339/oz

2P Au Reserves 0.7m oz (26.1mt @ 0.79 g/t)

Total Au M&I Resources 0.1m oz (6.0mt @ 0.43 g/t)

Total Au Inf. Resources 0.1m oz (5.7mt @ 0.59 g/t)

ÇAMYURT

Stage Resource Dev.

Est. Annual Production 93k oz

Est. Total Cash Costs US$604/oz

Total Au M&I Resources 0.5m oz (17.7mt @ 0.89 g/t)

Total Au Inf. Resources 0.1m oz (2.8mt @0.95 g/t)

LYNN LAKE

Stage Feasibility

Est. Annual Production 145k oz

Est. Total Cash Costs C$530/oz

Total Au M&I Resources 2.6m oz (40.3mt @ 2.03 g/t)

Total Au Inf. Resources 2.1m oz (50.7mt @ 1.28 g/t)

Diversified production Low-cost growth Safe jurisdictions

Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.Note: Mineral resources are exclusive of mineral reserves. See mineral reserve and resource estimates and associated footnotes in appendix.

29

1 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures. 2 Excludes capitalized exploration.3 For the purposes of calculating mine-site all-in sustaining costs at individual mine sites, the Company does not include an allocation of corporate and administrative and share based compensation expenses to the mine sites.4 Cost of sales includes mining and processing costs, royalties, and amortization expense

2017 Guidance

2017 Guidance 2016 Actuals

Young-Davidson Mulatos El Chanate Total Total

Gold production (000’s ounces) 200-210 150-160 50-60 400-430 392

Cost of Sales (in millions) (4) $215 $157 $70 $442 $429

Cost of Sales ($/oz) (4) $1,050 $1,015 $1,265 $1,065 $1,103

Total cash costs ($/oz) (1) $625 $815 $1,200 $765 $797

All-in sustaining costs ($/oz) (1) $940 $1,010

Mine-site all-in sustaining costs ($/oz) (1),(3) $775 $890 $1,200 -

Capital expenditures (in millions)

Sustaining capital(1) $30-35 $8-10 $2 $40-47 $49

Growth capital(1) $40-45 $25-30 (2) - $65-75 $97

Total – Operating Mines(1) $70-80 $33-40 $2 $105-122 $128

Total – Development Projects $35 $18

Total Consolidated Budget $140-157 $147

Corporate & Administrative (in millions) $16 $16

30

Young-Davidson – Increasing Grade & Productivity

1 Cost of sales includes mining and processing costs, royalties and amortization.2 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.3 Excludes Net Realizable Value (“NRV”) inventory adjustments. See associated MD&A for a full reconciliation.4 Excludes hydro rebate not attributable to Q4/15

Underground ramp up driving production higher and unit costs lower

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16

Gold ounces produced 28,281 29,252 30,099 33,106 35,104 40,166 40,538 40,945 38,098 39,365 38,201 44,694 39,065 42,644 43,629 44,662

Cost of sales1 (US$/oz) Pre-commercial production $1,677 $1,625 $1,370 $1,211 $1,216 $1,298 $1,165 $986 $1,058 $1,182 $1,032 $1,077

Total cash costs per oz. (2,3) $694 $716 $666 $850 $1,009 $871 $723 $719 $745 $697 $681 $617 $616 $738 $607 $667

Mine-site AISC per oz.(2,3) $1,059 $1,254 $1,357 $1,270 $1,315 $1,144 $959 $912 $987 $1,008 $979 $980 $846 $965 $849 $926

Underground mine

Tonnes mined per day 1,130 1,611 1,417 2,590 2,611 3,595 3,753 4,140 4,130 5,149 5,081 5,911 5,776 6,123 5,467 6,675

Grades (g/t) 2.7 2.5 2.8 3.1 2.8 3.3 3.1 3.0 3.0 2.6 2.6 2.6 2.6 2.4 2.8 2.4

Development metres 1,941 2,445 2,620 2,986 3,772 3,545 3,269 3,438 3,409 3,789 3,619 3,769 3,490 3,168 2,677 3,044

Unit UG mining costs (US$)Pre-commercial production

$46 $45 $41 $39 $39 $33 $32 $294 $31 $34 $34 $32

Unit UG mining costs (CAD$) $51 $49 $45 $44 $48 $41 $41 $384 $42 $44 $45 $42

Mill processing facility

Tonnes processed per day 6,466 7,017 6,747 6,969 7,163 8,230 7,670 7,757 7,186 7,677 7,680 7,630 7,342 7,006 6,833 7,552

Grades (inc. OP stockpile) 1.8 1.7 1.7 2.0 1.8 2.2 1.9 2.0 2.0 2.0 1.9 2.2 2.1 2.1 2.4 2.2

Recoveries (%) 86% 85% 89% 88% 87% 88% 90% 88% 86% 88% 92% 91% 90% 92% 93% 90%

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16

Un

it U

G m

inin

g co

sts

(US$

/t)

Un

de

rgro

un

d T

PD

Underground tonnes mined per day Unit UG mining costs (US$/t)

31

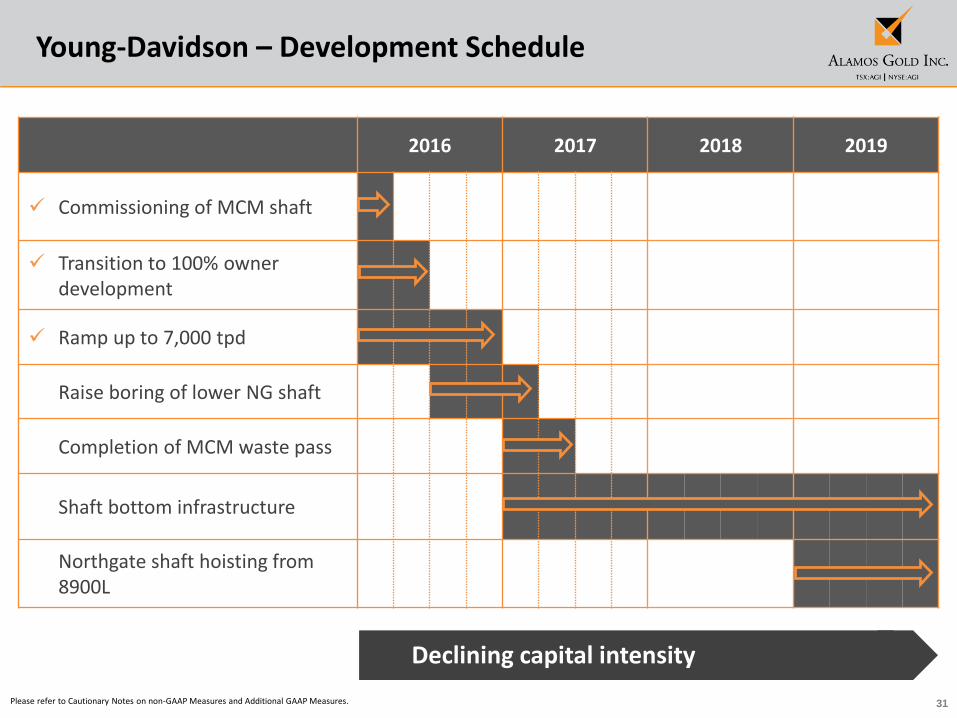

Young-Davidson – Development Schedule

Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures.

Declining capital intensity

2016 2017 2018 2019

Commissioning of MCM shaft

Transition to 100% owner development

Ramp up to 7,000 tpd

• Raise boring of lower NG shaft

• Completion of MCM waste pass

• Shaft bottom infrastructure

• Northgate shaft hoisting from 8900L

32

Young-Davidson – Long Section

Productivity improvements & declining costs

Developing the underground to support ramp up of underground mining

Milled grade higher

Declining capital intensity

Higher underground mining rates driving:

Production growth

33

Mulatos District

34

35

Kirazlı, Ağı Dağı & Çamyurt Economic Studies – 2017

Feasibility Study - 2017 Preliminary Economic Assessment - 2017

Kirazlı Ağı Dağı Çamyurt

Production

Mine life (years) 5 6 4

Total gold production (ounces) 540,000 937,300 373,200

Total silver production (ounces) 3,141,000 2,365,200 1,612,600

Average annual production (ounces)1

Gold 104,000 177,600 93,200

Silver 617,300 444,200 403,000

Total ore mined (tonnes) 26,100,000 54,361,000 16,580,000

Total waste mined (tonnes) 37,900,000 55,893,000 30,874,000

Total material mined (tonnes) 64,000,000 110,254,000 47,454,000

Waste-to-ore ratio2 1.45 1.03 1.86

Average grade (grams per tonne)

Gold 0.79 0.67 0.92

Silver 12.0 5.4 6.3

Recovery (%)

Gold 81% 80% 76%

Silver 31% 25% 48%

Average throughput (tpd) 15,000 30,000 15,000

Operating Costs

Total cost per tonne of ore3 $8.49 $6.46 $14.03

Total cash cost (per ounce sold)4 $339 $374 $604

Mine-site all-in sustaining cost (per ounce sold)4 $373 $411 $645

Capital Costs (millions)

Pre-production capital expenditure $151.9 $250.3 $10.2

Sustaining capital expenditure $18.1 $33.9 $9.4

Reclamation costs (net of salvage value) $9.9 $28.8 $5.9

Total capital expenditure $179.8 $312.9 $25.5

Economic Analysis

IRR (after-tax) 44.3% 38.7% 253.0%

NPV @ 0% discount rate (after-tax, millions) $299.3 $492.8 $173.8

NPV @ 5% discount rate (after-tax millions) $222.9 $360.2 $111.4

NPV @ 8% discount rate (after-tax, millions) $186.5 $297.6 $86.2

Gold price assumption (average, per ounce sold) $1,250 $1,250 $1,250

Silver price assumption (average, per ounce sold) $16.00 $16.00 $16.00

Exchange Rate (Turkish Lira/US Dollar) 2.90:1 2.90:1 2.90:1

1 Average annual production is based on five full years of production for Kirazlı and Ağı Dağı and excludes pre-commercial production2 Reported waste-to-ore ratio is over the life of mine. The waste-to-ore ratio during commercial production is 0.70:1 for Ağı Dağı and 1.19:1 for Kirazlı in the 2017 feasibility study3 Total unit cost per tonne of ore excludes silver as a by-product credit 4 Total cash costs and mine-site all-in sustaining costs include silver as a by-product credit

36

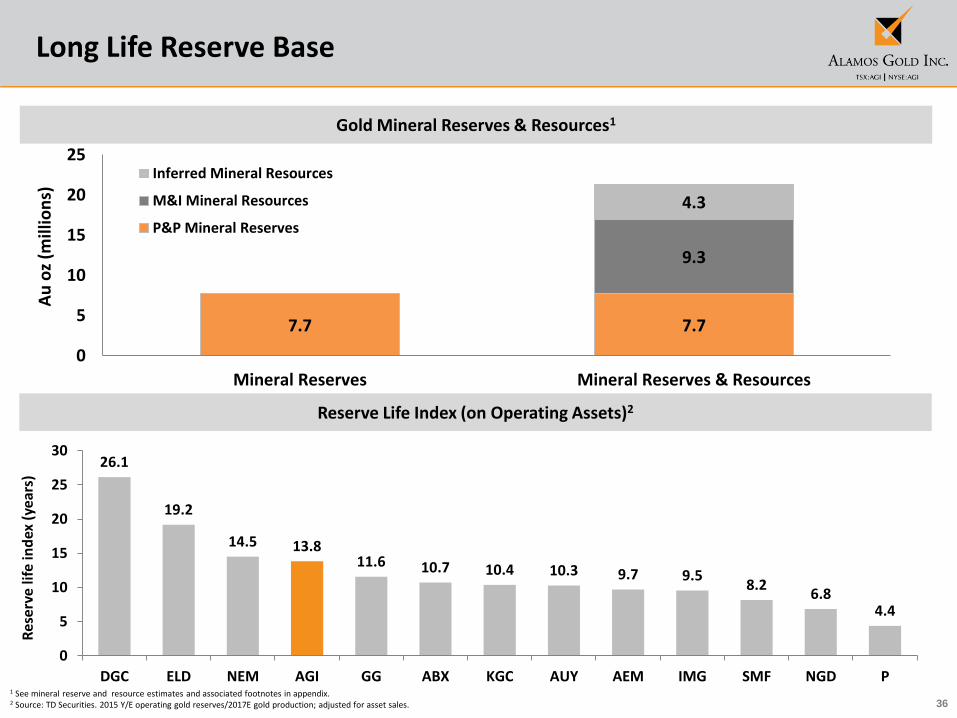

Long Life Reserve Base

Reserve Life Index (on Operating Assets)2

Gold Mineral Reserves & Resources1

1 See mineral reserve and resource estimates and associated footnotes in appendix.2 Source: TD Securities. 2015 Y/E operating gold reserves/2017E gold production; adjusted for asset sales.

26.1

19.2

14.5 13.811.6 10.7 10.4 10.3 9.7 9.5

8.26.8

4.4

0

5

10

15

20

25

30

DGC ELD NEM AGI GG ABX KGC AUY AEM IMG SMF NGD P

Res

erv

e lif

e in

dex

(ye

ars)

7.7 7.7

9.3

4.3

0

5

10

15

20

25

Mineral Reserves Mineral Reserves & Resources

Au

oz

(mill

ion

s)

Inferred Mineral Resources

M&I Mineral Resources

P&P Mineral Reserves

37

2016 Proven and Probable Mineral Reserves

PROVEN AND PROBABLE GOLD RESERVES (as at December 31, 2016)

Proven Reserves Probable Reserves Total Proven and Probable

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Au) (000's) (000's) (g/t Au) (000's) (000's) (g/t Au) (000's)

Young-Davidson - Surface 1,165 0.91 34 - - - 1,165 0.91 34

Young-Davidson - Underground 14,851 2.80 1,336 27,203 2.65 2,317 42,054 2.70 3,653

Total Young-Davidson 16,016 2.66 1,370 27,203 2.65 2,317 43,220 2.65 3,687

Mulatos Main Pits 4,173 1.02 137 21,847 0.87 613 26,020 0.90 750

San Carlos Underground 72 13.06 30 34 8.64 9 106 11.65 40

Stockpiles 7,129 1.38 317 - - - 7,129 1.38 317

La Yaqui 470 1.48 22 1,469 1.37 65 1,939 1.40 87

La Yaqui Grande - - - 11,548 1.40 521 11,548 1.40 521

Cerro Pelon 960 1.70 53 2,293 1.59 117 3,253 1.63 170

Total Mulatos 12,804 1.36 559 37,191 1.11 1,325 49,995 1.17 1,885

El Chanate - Open Pit 7,008 0.51 114 3,804 0.65 79 10,812 0.56 193

El Chanate - Leach Pad Inv. - - 100 - - - - - 100

Total El Chanate 7,008 0.95 214 3,804 0.65 79 10,812 0.84 293

Agi Dagi 1,450 0.76 36 52,911 0.66 1,130 54,361 0.67 1,166

Kirazli 700 1.25 28 25,404 0.78 637 26,104 0.79 665

Total Turkey 2,150 0.93 64 78,315 0.70 1,767 80,465 0.71 1,831

Alamos - Total 37,979 1.81 2,208 146,513 1.17 5,488 184,492 1.30 7,696

PROVEN AND PROBABLE SILVER MINERAL RESERVES (as at December 31, 2016)

Proven Reserves Probable Reserves Total Proven and Probable

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's)

La Yaqui 470 7.40 112 1,469 7.19 340 1,939 7.25 452

La Yaqui Grande - - - 11,548 19.94 7,403 11,548 19.94 7,403

Ağı Dağı 1,450 6.22 290 52,911 5.39 9,169 54,361 5.41 9,459

Kirazli 700 15.90 358 25,404 11.90 9,720 26,104 12.01 10,078

Alamos - Total 2,620 9.02 760 91,332 9.07 26,632 93,952 9.07 27,392

38

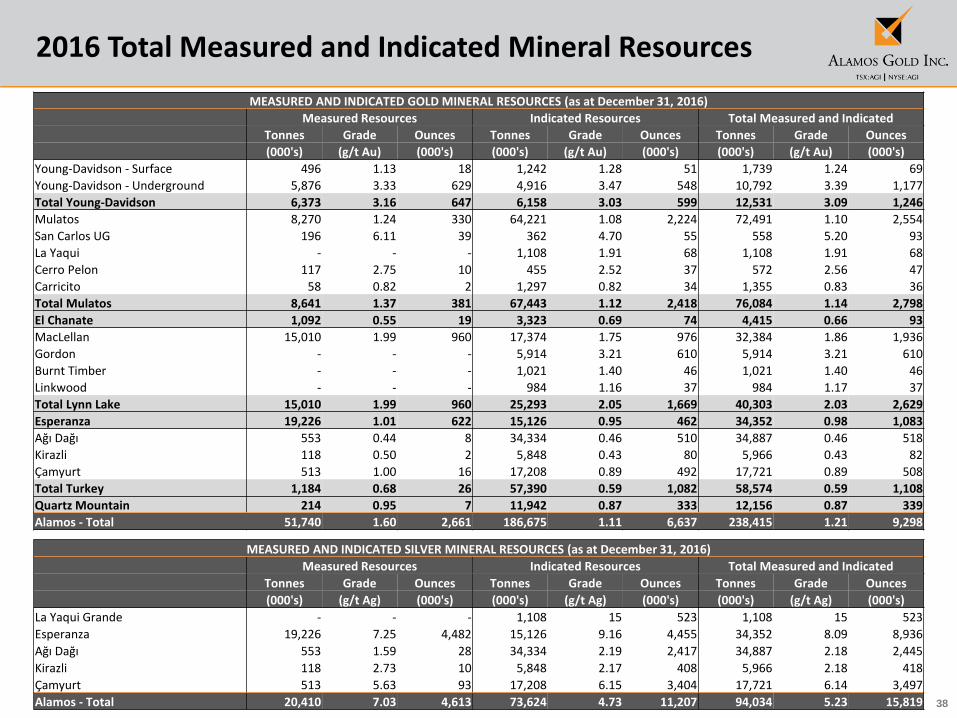

2016 Total Measured and Indicated Mineral Resources

MEASURED AND INDICATED GOLD MINERAL RESOURCES (as at December 31, 2016)

Measured Resources Indicated Resources Total Measured and Indicated

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Au) (000's) (000's) (g/t Au) (000's) (000's) (g/t Au) (000's)

Young-Davidson - Surface 496 1.13 18 1,242 1.28 51 1,739 1.24 69

Young-Davidson - Underground 5,876 3.33 629 4,916 3.47 548 10,792 3.39 1,177

Total Young-Davidson 6,373 3.16 647 6,158 3.03 599 12,531 3.09 1,246

Mulatos 8,270 1.24 330 64,221 1.08 2,224 72,491 1.10 2,554

San Carlos UG 196 6.11 39 362 4.70 55 558 5.20 93

La Yaqui - - - 1,108 1.91 68 1,108 1.91 68

Cerro Pelon 117 2.75 10 455 2.52 37 572 2.56 47

Carricito 58 0.82 2 1,297 0.82 34 1,355 0.83 36

Total Mulatos 8,641 1.37 381 67,443 1.12 2,418 76,084 1.14 2,798

El Chanate 1,092 0.55 19 3,323 0.69 74 4,415 0.66 93

MacLellan 15,010 1.99 960 17,374 1.75 976 32,384 1.86 1,936

Gordon - - - 5,914 3.21 610 5,914 3.21 610

Burnt Timber - - - 1,021 1.40 46 1,021 1.40 46

Linkwood - - - 984 1.16 37 984 1.17 37

Total Lynn Lake 15,010 1.99 960 25,293 2.05 1,669 40,303 2.03 2,629

Esperanza 19,226 1.01 622 15,126 0.95 462 34,352 0.98 1,083

Ağı Dağı 553 0.44 8 34,334 0.46 510 34,887 0.46 518

Kirazli 118 0.50 2 5,848 0.43 80 5,966 0.43 82

Çamyurt 513 1.00 16 17,208 0.89 492 17,721 0.89 508

Total Turkey 1,184 0.68 26 57,390 0.59 1,082 58,574 0.59 1,108

Quartz Mountain 214 0.95 7 11,942 0.87 333 12,156 0.87 339

Alamos - Total 51,740 1.60 2,661 186,675 1.11 6,637 238,415 1.21 9,298

MEASURED AND INDICATED SILVER MINERAL RESOURCES (as at December 31, 2016)

Measured Resources Indicated Resources Total Measured and Indicated

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's) (000's) (g/t Ag) (000's)

La Yaqui Grande - - - 1,108 15 523 1,108 15 523

Esperanza 19,226 7.25 4,482 15,126 9.16 4,455 34,352 8.09 8,936

Ağı Dağı 553 1.59 28 34,334 2.19 2,417 34,887 2.18 2,445

Kirazli 118 2.73 10 5,848 2.17 408 5,966 2.18 418

Çamyurt 513 5.63 93 17,208 6.15 3,404 17,721 6.14 3,497

Alamos - Total 20,410 7.03 4,613 73,624 4.73 11,207 94,034 5.23 15,819

39

2016 Total Inferred Mineral Resources

INFERRED GOLD MINERAL RESOURCES (as at December 31, 2016)

Tonnes Grade Ounces

(000's) (g/t Au) (000's)

Young-Davidson - Surface 31 0.99 1

Young-Davidson - Underground 3,524 2.76 313

Total Young-Davidson 3,555 2.75 314

Mulatos 8,935 0.92 265

San Carlos UG 162 4.93 26

La Yaqui 174 1.39 8

Cerro Pelon 109 1.23 4

Carricito 900 0.74 22

Total Mulatos 10,280 0.98 325

El Chanate 112 0.71 3

MacLellan 1,898 2.01 123

Gordon 4,364 2.87 403

Burnt Timber 23,438 1.04 781

Linkwood 21,004 1.16 783

Total Lynn Lake 50,704 1.28 2,089

Esperanza 718 0.80 18

Ağı Dağı 16,760 0.46 245

Kirazli 5,689 0.59 108

Çamyurt 2,791 0.95 85

Total Turkey 25,240 0.54 438

Quartz Mountain 39,205 0.91 1,147

Alamos - Total 129,815 1.04 4,334

INFERRED SILVER MINERAL RESOURCES (as at December 31, 2016)

Tonnes Grade Ounces

(000's) (g/t Ag) (000's)

La Yaqui Grande 174 5.55 31

Esperanza 718 15.04 347

Ağı Dağı 16,760 2.85 1,534

Kirazli 5,689 8.96 1,638

Çamyurt 2,791 5.77 518

Alamos - Total 26,132 4.84 4,068

40

Notes to Mineral Reserve and Resource Estimates

Notes to Mineral Reserve and Resource Tables:• The Company’s Mineral Reserves and Mineral Resource as at December 31, 2016 are classified in accordance with the Canadian Institute of Mining Metallurgy and Petroleum’s “CIM Standards on Mineral

Resources and Reserves, Definition and Guidelines” as per Canadian Securities Administrator’s NI 43-101 requirements. • Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability.• Mineral Resources are exclusive of Mineral Reserves.• Mineral Reserve cut-off grade for the Mulatos Mine, the Cerro Pelon Pit, the La Yaqui Pit, the Kirazlı Pit and the Ağı Dağı Pit are determined as a net of process value of $0.10 per tonne for each model

block• All Measured, Indicated and Inferred Mineral Resources are pit constrained with the exception of those outside the Mulatos Main Pits on the Mulatos property which have no economic restrictions and

are tabulated by gold cut-off grade.• Mineral Reserve estimates assumed a gold price of $1,250 per ounce and Mineral Resource estimates assumed a gold price of $1,400 per ounce, except as follows: Lynn Lake Mineral Resources assumed a

gold price of $1,550 per ounce with an assumption of the Canadian dollar at parity with the United States dollar. Metal prices, cutoff grades and metallurgical recoveries are set out in the table below.• El Chanate reserve ounces include a December 31, 2016 inventory 99,900 recoverable ounces in the heap leach pad

Qualified Persons:

Chris Bostwick, FAusIMM, Alamos Gold’s Vice President, Technical Services, has reviewed and approved the scientific and technical information contained in this news release. Chris Bostwick is a Qualified Person within the meaning of Canadian Securities Administrator’s National Instrument 43-101 (“NI 43-101”). The Qualified Persons for the National Instrument 43-101 compliant mineral reserve and resource estimates are detailed in the following table.

Mineral ResourcesJeffrey Volk, CPG, FAusIMM Director - Reserves and Resource,

Alamos Gold Inc.Young-Davidson, El Chanate, San Carlos U/G, Lynn Lake

Marc Jutras, P.Eng Principal, Ginto Consulting Inc. Mulatos Pits, Cerro Pelon, La Yaqui, Carricito, Esperanza, Ağı Dağı,Kirazlı, Çamyurt, Quartz Mountain

Mineral ReservesChris Bostwick, FAusIMM VP Technical Services, Alamos Gold Inc. Young-Davidson, El Chanate,

San Carlos UndergroundHerb Welhener, SME-QP VP, Independent Mining Consultants Inc. Mulatos Pits, Cerro Pelon, La Yaqui, Ağı Dağı, Kirazlı

Resources ReservesGold Price Cutoff Gold Price Cutoff Met Recovery

Mulatos:

Mulatos Main Open Pit $1,400 0.5 $1,250 see notes >50%

San Carlos Underground $1,400 2.5 $1,250 3.27 70%

Cerro Pelon $1,400 0.5 $1,250 see notes 75%

La Yaqui $1,400 0.5 $1,250 see notes 75%

Carricito $1,400 0.3 n/a n/a >50%

Young-Davidson - Surface $1,400 0.5 $1,250 0.5 91%

Young-Davidson - Underground $1,400 1.3 $1,250 1.9 91%

El Chanate $1,400 0.15 $1,250 0.15 30-65%

Lynn Lake $1,555 0.4 n/a n/a 89-92%

Esperanza $1,400 0.4 n/a n/a 60-72%

Ağı Dağı $1,400 0.2 $1,250 see notes 80%

Kirazlı $1,400 0.2 $1,250 see notes 81%

Çamyurt $1,400 0.2 n/a n/a 78%

Quartz Mountain $1,400 0.21 Oxide, 0.6 Sulfide n/a n/a 65-80%