AkzoNobel Strategy Update 2013 Tcm9-78275

87

Leading market positions delivering leading performance Ton Büchner & Keith Nichols February 20, 2013

-

Upload

waqas-sherwani -

Category

Documents

-

view

8 -

download

1

description

ok

Transcript of AkzoNobel Strategy Update 2013 Tcm9-78275

Leading market positions delivering leading performance

Ton Büchner & Keith Nichols

February 20, 2013

2 Strategy Update 2013

1. Introduction

2. Market environment

3. Group strategic update

4. Business Areas

Coffee break

5. Financial implications

6. Summary and conclusion Questions

Agenda

1. Introduction

2. Market environment

3. Group strategic update

4. Business areas

5. Financial implications

6. Summary and conclusion

1. Introduction

3 Strategy Update 2013

Our proposition: Leading market

positions delivering leading performance

4

AkzoNobel has gone through a significant amount of

strategic change over the past five years

Today, the company has

• Excellent portfolio of businesses

• Good long term growth potential on the basis of end-user segment growth

• Strong positions in high growth markets (44% of revenue)

• Leadership positions in many markets

• Clear leader in sustainability

• Track record of delivering sustainable innovations and products

• Strong brands, both in consumer and industrial markets

Clear focus to deliver on our significant potential

• Improved returns and cash flow

• Leveraging scale

• Simplification and standardization

• Continued innovation

Strategy Update 2013

5 Strategy Update 2013

AkzoNobel strategy

8.9

14.0

0

4

8

12

16

2012 2015

Return on sales

(Operating income/revenue)

%

6

Return on investment

(Operating income/average

12 months invested capital)

%

Strategy Update 2013

Net debt/EBITDA

x

New and realistic 2015 financial targets focused on quality of earnings and value creation

Assumes sales growth (CAGR) for the period of 4%

*2012 excluding impairment (€2.1 billion) and after IAS19

5.9

9.0

0

4

8

12

2012 2015

1.4

2.0

0

1

2

3

2012 2015

* * <

AkzoNobel today

7 Strategy Update 2013

• Revenue €15.4 billion

• 50,610 employees

• 44% of revenue from high growth markets

• Major producer of Paints, Coatings and

Specialty Chemicals

• Leadership positions in many markets

*2012 excluding impairment (€2.1 billion) **New definition including incidentals and after IAS19

38%

15%

47%

Performance Coatings

Decorative Paints

Specialty Chemicals

48%

8%

44% 37%

27%

36%

Revenue by

Business Area

Operating income*

by Business Area

EBITDA** by

Business Area

5.4%

Growth

2012 vs. 2011

5.9%

Return on sales

(operating income/revenue)

10.4%

EBITDA/revenue

8 Strategy Update 2013

2012 showed challenging market

conditions in most end-user segments

and geographical end markets

Key developments in 2012:

• Divestment of Decorative Paints North America

announced

• Impairment of €2.1 billion on

continued operations

• Exceeded Performance Improvement

Program intermediate targets

2013 market conditions are not expected

to improve significantly

• Focus will be on:

– Organic growth

– Operating income

– Return on capital

– Operating cash flow

• Management remuneration has been

adapted accordingly

• Continue building on our end-user segments

and strong high growth market positions

• Key management changes

2013 market conditions not expected

to improve significantly

1. Introduction

2. Market environment

3. Group strategic update

4. Business Areas

5. Financial implications

6. Summary and conclusion

2. Market environment

9 Strategy Update 2013

10 Strategy Update 2013

~43% of revenues

New Build Projects

Maintenance, Renovation and Repair

Building Products and Components

~16% of revenues

Automotive OEM, Parts and Assembly

Automotive Repair

Marine and Air Transport

~16% of revenues

Consumer Durables

Consumer Packaged Goods

~25% of revenues

Natural Resource and Energy Industries

Process Industries

Total market maintenance

and repair

$ billion, output

New non-residential

construction

$ billion, output

Residential housing

completions

Thousand units

2011 12 13 14 15 16 2011 12 13 14 15 16 2011 12 13 14 15 16

11 Strategy Update 2013

In Buildings and Infrastructure, our main market is in renovation and repair

BRIC

CAGR 13.3%

EUR & US

CAGR 3.1%

2011 = 1,557

2011 = 1,075

BRIC

CAGR 12.3%

EUR & US

CAGR 4.2%

2011 = 410

2011 = 1,222

BRIC

CAGR 0.0%

EUR & US

CAGR 0.4%

2011 = 11,845

2011 = 3,943

Source: IHS / Construction IC Source: Euromonitor International Source: IHS / Construction IC

Buildings and Infrastructure trends and implications for strategy and actions

12 Strategy Update 2013

Recent trends

Impact on strategy and

actions going forward

• Invest further in our strong positions in the

high growth markets

• Restructure proactively in mature markets,

primarily Europe

• Build re-paint culture in high growth markets

• Continuously innovate to improve

sustainability for

– Product itself

– Application

– End-use

• Market contraction

• Limited recovery

• Mortgage markets restricted

• Fewer house purchases

• High growth market outlook positive

• Lower growth in the future

• Increased demand for improved

sustainability in housing

• Some government stimulus packages

for infrastructure

2011 12 13 14 15 16

Light vehicle production

and sales

Million units

Vehicle (car) miles driven

Billion car kilometers

13 Strategy Update 2013

In Transportation, our main markets are vehicle refinish and marine

Production 2011 = 77, CAGR 4.8%

Sales 2011 = 76, CAGR 4.9%

Freight rates

ClarkSea* index $ earnings/day

2011 12 13 14 15 16

2012 avg = $9,945

West Europe 2011 = 2,741

growth 2012 = -0.3%

China 2011 = 1,120

growth 2012 = 10.2%

US 2011 = 2,550

growth 2012 = -0.7%

2006 08 10 12 14 16

Source: Historical data (through 2012) IRF / Euromonitor

International; management estimates for forward

looking data

* Weighted average of tanker, bulk carrier, container-

ship and gas carrier earnings

Source: Historical data (through 2012) Clarkson

Research Services Limited; management estimates

for forward looking data

Source: IHS

Transportation trends and implications for strategy and actions

14 Strategy Update 2013

Recent trends

Impact on strategy and

actions going forward

• Adapt value proposition and distribution

models for high growth market success

• Restructure and reconfigure in contracting

segments and geographies

• Innovate to improve functionality,

sustainability and margins

• Strengthen business models to support

our customers on the maintenance aspects

• Continued growth

• Shift to Asia in automotive

manufacture and demand

• Increasing use of lighter/

different materials

• Vehicle car park increasing,

but repair rate decreasing

• Considerable reduction in new

ship building

• Reduced maintenance spend as

shipping rates fell

• Airplane miles continuing to increase

after recession

Consumer Goods trends and implications for strategy and actions

15 Strategy Update 2013

Recent trends

Impact on strategy and

actions going forward

• Ensure both production and design presence

in high growth countries

• Manage margins and/or restructure in

lower value segments

• Improve multi-level relationships

(e.g. OEM, ODM)

• Differentiate through color, design,

and customer process improvement

• Continued growth

• Geographic shift to Asia in demand,

production and design

• Significant drop in demand in mature

markets during the recession

• Recovery muted thus far

• Different types of demand

• „Vanishing middle‟ in mature markets

• Affordable products are the focus for

growth elsewhere

Industrial trends and implications for strategy and actions

16 Strategy Update 2013

Recent trends

Impact on strategy and

actions going forward

• Adapt our structure in mature markets

• Expand production and sales force in the

high-growth markets

• Increase focus and investment in more

differentiated products

• Innovate for additional functionality and

sustainability

• Manage margins as raw materials fluctuate

Cyclical sectors but AkzoNobel

segments are on different cycles

Recession impact muted due to

strong demand in high growth countries

Particularly strong growth in oil and gas

due to high prices and feedstock shifts

Government encouragement of

investment in (renewable) energy

Pulp and paper lower growth but

more stable

High growth markets are 44% of revenue and their importance will increase

17 Strategy Update 2013

Our goal: Greater than 50% of revenues from high growth markets

% of 2012 revenue, excluding Decorative Paints North America

38%

Mature Europe

26%

Asia Pacific 2%

Middle East

and Africa

11%

Latin America

15%

North America

8%

Emerging Europe 0%

3%

6%

9%

UK Eurozone USA Latin America

China Developing Asia

2013 2014 2015

*Source: EIU: GDP year on year growth in local currency at constant prices

Three year GDP growth*

Capital expenditure

2012, 100% = €826 million (5.4% of revenue)

Capital allocation policy is focused on high growth markets and efficiency

18 Strategy Update 2013

15%

25% 58%

2%

Performance Coatings Decorative Paints

Specialty Chemicals Other

• Capital expenditure will be around 4% of revenues

going forward

• 40-50% growth related

Business

Area

Investment

project

2012 2013 2014 2015

Performance

Coatings

China

expansion

Decorative

Paints

UK

megaplant

Decorative

Paints

China

expansion

Specialty

Chemicals

Ningbo

multisite

Specialty

Chemicals

Frankfurt

membrane

Specialty

Chemicals

Brazil

Eldorado

Specialty

Chemicals

Brazil

Suzano

Major projects underway and timing of spend

121 111 108

89 87 80 79 76

52

0

25

50

75

100

125

150

India Brazil China US Germany Sweden UK Netherlands France

Consumer confidence impacts three of our segments

19 Strategy Update 2013

Consumer confidence

Q4 2012

Source: Nielsen, Consumer confidence figures below 100 demonstrate some degree of pessimism

Recent trends

20 Strategy Update 2013

Purchase Managers’ Index (PMI) shows a clear change in trend in Q4 2011

Source: JP Morgan

PMI

40

45

50

55

60

Dec-09 Dec-10 Dec-11 Dec-12

Global Eurozone US China Brazil

• US, China, India

and Brazil indicate

expansion of

manufacturing

• Eurozone indicates

further contraction

• PMI is a good

indicator for our

Industrial segment

AkzoNobel benefits from its broad end-user segmentation and geographical presence

21 Strategy Update 2013

• AkzoNobel’s four end-user segments show a

mixed picture for future development

– Buildings and Infrastructure faces challenges, especially in Europe

– Marine transportation shows reduced activity levels

– Consumer Goods, Industrial, automotive and air transport are

reasonably robust

• High growth markets show stronger demand developments in virtually

all segments

• North America shows earlier signs of recovery compared to Europe

• Consumer confidence varies strongly per region and has a clear influence

on significant end user buying decisions (housing, cars, furniture, etc.)

• The optimism levels reflected in the Purchasing Managers‟ Index (PMI)

will have a positive impact on our Industrial segments

1. Introduction

2. Market environment

3. Group strategic update

4. Business Areas

5. Financial implications

6. Summary and conclusion

3. Group strategic update

22 Strategy Update 2013

The vision and new targets

23

Vision: Leading market positions delivering leading performance

To be a leader in:

• Operating efficiency and customer service

• Innovation

• Sustainability

New targets

• Return on sales (ROS, operating income/revenue)

• Return on investment (ROI, operating income/average 12 months invested capital)

• Carbon emissions across the value chain

• Eco-premium products

Strategy Update 2013

24 Strategy Update 2013

AkzoNobel strategy

25 Strategy Update 2013

We will drive five strategic focus areas

1. Care for the customer

3. Focus on cash and return on investment

4. Embedded safety and sustainability

5. Diverse and inclusive talent development

1. Care for the customer

2. Reduction of product

and process complexity

3. Cash and return

on investment

4. Embedded safety

and sustainability

5. Diverse and inclusive

talent development

26 Strategy Update 2013

Core processes Process owner

The company core processes will support our strategic focus areas

Integrated Supply Chain (HSE)

CEO/CFO

Integrated Supply Chain

(Operations)

RDI

Integrated Supply Chain

(Procurement)

HR

Behavior-based and process safety

Operational control cycle

Continuous improvement

Innovation

Procurement

Talent management

27 Strategy Update 2013

Actions

> Grow organically

> Innovate

> Standardize

> Simplify

> Continuously improve

> Deliver dependably

28 Strategy Update 2013

Strategy on a page

Strategic focus areas

• Care for the customer

• Reduction of product

and process complexity

• Cash and return on

investment

• Embedded safety

and sustainability

• Diverse and inclusive

talent development

Processes

• Behavior-based

and process safety

• Operational

control cycle

• Continuous

improvement

• Innovation

• Procurement

• Talent management

Actions

• Deliver dependably

• Grow organically

• Innovate

• Simplify

• Standardize

• Continuously

improve

End-user segmentation

• Buildings and

Infrastructure

• Transportation

• Consumer Goods

• Industrial

Our sustainability strategy: Creating more value with fewer resources

29 Strategy Update 2013 29

More customer value in our end-user segmentation

Resource scarcity across the value chain will create opportunities

Scope 3 upstream

Raw materials

Scope 1 and 2

Own operations,

including energy use

Scope 3 downstream

Customer operations End-user End of life

Scope 4 Energy/ resource benefits in use

30 Strategy Update 2013

• „Downstream eco-premium solutions’:

20% of our revenues by 2020

We will increase the revenue from solutions

that generate direct resource and energy benefits

for our customers, consumers and users

• Reduction of carbon emissions

25-30% reduction per ton by 2020 (2012 base)

We will reduce our carbon emissions through the value chain

• Resource efficiency

As of 2014 AkzoNobel will report on an innovative new index

measuring how we improve resource efficiency across the

full value chain - compared to the value we generate

Sustainability is business; Business is sustainability

31 Strategy Update 2013

End-user segment trends, combined with sustainability, direct our innovation spend

End-user segments

Sustainability

Sustainability = Business

Business = Sustainability

Direction of

innovation

spend (2.5% of 2012 revenue)

32 Strategy update 2013

AkzoNobel delivers innovation

Buildings and

Infrastructure

Dulux Guardian

A premium, low-VOC

and low-odor soft-sheen

emulsion for interior walls

Transportation

Aerobase

Coating System

A consistently

performing OEM-approved

low VOC base coat/clear

coat system for aerospace

Industrial

Monochloroacetic

acid (MCA)

An asset-light approach

to sustainable chemical

production using proprietary

hydrogenation technology

Consumer goods

Biostyle™ CGP

A range of sustainable

hybrid polymers for

consumer applications

33 Strategy Update 2013

2013 Plan

• Accelerate delivery of recurring €500 million

EBITDA gain in 2013, which was originally

intended in 2014

• Associated cost is estimated at €205 million

• Guidance of €500 million remains even though

North America Decorative Paints will be

divested

• Added measures included

Performance Improvement Program to deliver €500 million in 2013, one year earlier than planned

Operational

Excellence

Functional

Excellence

Business Unit

Adaptations

Key summary to date

• Gains of €250 million,

excluding Decorative Paints North America

• Costs of €292 million,

excluding Decorative Paints North America

• Pulled actions and associated costs forward

• Added measures (including European Decorative

Paints) with additional cost in 2012

Performance Improvement Program

34 Strategy Update 2013

• Product and margin management

• Consolidation of RD&I

• Logistic and warehouse optimization

Operational

Excellence

Functional

Excellence

Business Unit

Adaptations

• IT infrastructure simplification

• HR shared service model

• Finance shared service centers

• Organizational redesign of Marine and Protective

Coatings, Wood Finishes and Adhesives, and

• Pulp and Performance Chemicals

• Additional restructuring of Decorative Paints Europe

During 2013, we will embed

continuous improvement

in our businesses Embedding

Moving from project based to continuous improvement will be core in 2013

35 Strategy Update 2013

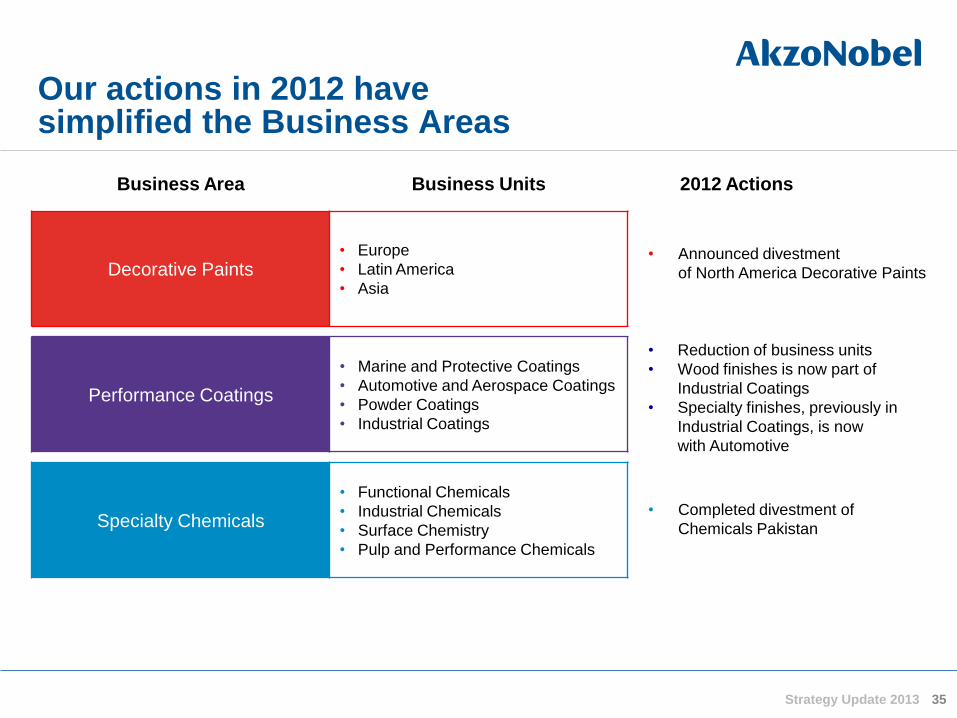

Our actions in 2012 have simplified the Business Areas

Business Area Business Units

Decorative Paints • Europe

• Latin America

• Asia

Performance Coatings

• Marine and Protective Coatings

• Automotive and Aerospace Coatings

• Powder Coatings

• Industrial Coatings

Specialty Chemicals

• Functional Chemicals

• Industrial Chemicals

• Surface Chemistry

• Pulp and Performance Chemicals

2012 Actions

• Completed divestment of

Chemicals Pakistan

• Reduction of business units

• Wood finishes is now part of

Industrial Coatings

• Specialty finishes, previously in

Industrial Coatings, is now

with Automotive

• Announced divestment

of North America Decorative Paints

36 Strategy Update 2013

AkzoNobel strategy

1. Introduction

2. Market environment

3. Group strategic update

4. Business Areas

5. Financial implications

6. Summary and conclusion

4. Business Areas

37 Strategy Update 2013

By end-user segment

2011, 100% = €75 billion

38 Strategy Update 2013

The global paints and coatings market is around €75 billion

By market sector

2011, 100% = €75 billion

Decorative

Paints

(43%)

Automotive

OEM

Protective

Vehicle

Refinish

Performance

Coatings

(57%)

General

Industrial

Powder

Wood

Marine Coil

Packaging

Aerospace Yacht

Source: Orr & Boss; management analysis

Buildings and

Infrastructure

Transportation

Consumer

Goods

Industrial

AkzoNobel has many leading market positions

39 Strategy Update 2013

No.1 Position Other key players

Decorative

Multiple regions

outside North

America

PPG, regional players

North America* Sherwin-Williams PPG, regional players

Protective Sherwin-Williams, Jotun

Powder Axalta, Jotun, regional players

Auto refinish Axalta PPG, AkzoNobel

Wood Sherwin-Williams, Valspar

Marine Jotun, Chugoku

Coil PPG, Beckers

* AkzoNobel not present with North America divestment to PPG

40 Strategy Update 2013

BA-level core processes and capabilities

• Branding

• Distributor, wholesaler, retail management

• Understanding and serving professional painters

• Consumer inspiration

• Quality management, including product portfolio management

Revenue by geographic region

Decorative Paints overview

€ million 2012*

Revenue 4,297

EBITDA 284

Operating income 94

Return on sales 2.2%

Return on investment 3.0%

# Employees 17,020

Revenue by end-user

sub-segment

*After the divestment of Decorative Paints North America, excluding impairment (€2.1 billion)

Decorative Paints key figures (new definition)

49%

25%

14%

8%4% Mature Europe

Asia Pacif ic

Latin America

Emerging Europe

Other regions84%

16% Maintenance,

renovation and repair

New build projects

62%14%

24%Europe

Latin America

Asia

End-user

sub-segment

Geographic region Forward

looking trends

New build

projects

Europe

North America

Asia

Latin America

Maintenance,

renovation and

repair

Europe

North America

Asia

Latin America

41 Strategy Update 2013

Decorative Paints sees limited overall market sector growth in the near future

Expected market growth for the

market sectors relevant to

AkzoNobel: 3-4%

Revenue by Business Unit

42 Strategy Update 2013

Europe

• European organization de-layered

• Better proximity to customers

• Implemented standard processes and merged

ERP system to one

• Implementing a single business entity

• Restructuring cost and benefits for 2013 included

in Performance Improvement Program

• Additional costs are expected in 2014; total

recurring operational benefits of €100 million

will be realized by end of 2014

High growth markets

• Additional investment in China

• Continuously expanding the franchise network

in China, India, and South East Asia

• Stronger focus on Eastern Europe,

Middle East and Africa

• Expansion of activities in Latin America

After the divestment of North America, our focus is on adapting Europe, and investing in high growth markets

Decorative Paints strategic direction

43 Strategy Update 2013

Noteworthy events 2012

• Launched “Let‟s Color” brand and

campaign globally

• Global campaigns to inspire customers

• Expanded store network in China and India

• Announcement divestment of Decorative

Paints North America

• Realigning and restructuring European

business

Actions going forward

• Expand manufacturing capacity in

China and India

• Expand market presence in

emerging Europe and the Middle East

• Complete the divestment of North America

• Launch new products for the

high growth markets

• Deliver on the realignment of the European

organization

Expected 2015 financial outcomes

• Organic revenue growth: 5%

• Return on sales: 7.5%

• Return on investment : 12%

27%

20%30%

11%

8%4%

Mature Europe

North America

Asia Pacific

Emerging EuropeLatin America

Other regions

36%

27%

23%

14%Transportation

Consumer Goods

Buildings and Infrastructure

Industrial

44 Strategy Update 2013

Performance Coatings overview

Performance Coatings

key figures (new definition)

Revenue by end-user segment Revenue by geographic region

€ million 2012

Revenue 5,702

EBITDA 673

Operating income 542

Return on sales 9.5%

Return on investment 21.7%

# Employees 21,310

BA-level core processes and capabilities

• Industrial key account management

• Technical support and service

• Design, color and color matching

• Continuous innovation in functionality and

ease-of-use

• Sustainable, safe solutions

End-user

segment

Performance Coatings

market sectors serving

the segment

Forward looking

trends

Transportation Automotive and air

Marine transport

Consumer

Goods

Powder and packaging

coatings, wood and

specialty plastic finishes

Buildings and

Infrastructure

Protective, coil and

powder coatings, wood

finishes

Industrial Protective and powder

coatings

45 Strategy Update 2013

Expected market growth for the

market sectors relevant to

AkzoNobel: 4%

Performance Coatings sees growth in several key market sectors

*AkzoNobel has a limited position in Automotive OEM coatings

28%

23%17%

32%

Marine and Protective Coatings

Automotive and Aerospace Coatings

Powder Coatings

Industrial Coatings

Revenue by Business Unit

Performance Coatings strategic direction

46 Strategy Update 2013

Noteworthy events 2012

• Schramm acquisition integration on track

• Opened a new manufacturing facility in Vietnam

• Multiple sport stadium contracts for

London Olympics and Brazil‟s future events

• McLaren partnership expanded

• Realigned organization to four Business Units

(from five)

• Reorganized Europe for multiple Business Units

(Wood, Marine, Automotive)

Actions going forward

• Complete manufacturing expansion for

automotive refinish in China

• Complete Schramm integration

• Product and margin management

• Continue product line rationalization

• Continue ERP consolidation

Expected 2015 financial outcomes

• Organic revenue growth: 5%

• Return on sales: 12%

• Return on investment: 25%

47 Strategy Update 2013

Specialty Chemicals overview

Specialty Chemicals key figures

(new definition)

Revenue by end-user segment

Revenue by geographic spread

€ million 2012

Revenue 5,543

EBITDA 830

Operating income 500

Return on sales 9.0%

Return on investment 13.6%

# Employees 10,750

18%

6%

18%58%

Buildings and

Infrastructure

Transportation

Consumer

Goods

Industrial

40%

21%

22%

10%4%3% Mature Europe

North America

Asia Pacific

Latin America

Emerging Europe

Other regions

BA-level core processes and capabilities

• Management of integrated value chains

• Continuous technological advancement

• Engineering and project management

• Process safety

• Product and margin management

• Managing capital intensive businesses and expansions

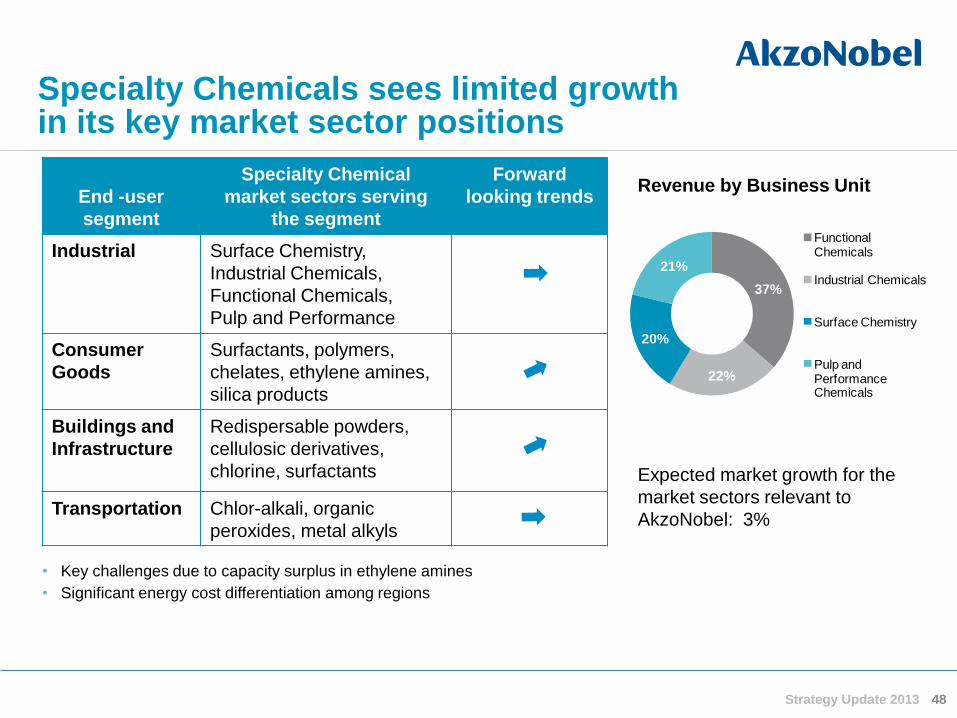

End -user

segment

Specialty Chemical

market sectors serving

the segment

Forward

looking trends

Industrial Surface Chemistry,

Industrial Chemicals,

Functional Chemicals,

Pulp and Performance

Consumer

Goods

Surfactants, polymers,

chelates, ethylene amines,

silica products

Buildings and

Infrastructure

Redispersable powders,

cellulosic derivatives,

chlorine, surfactants

Transportation Chlor-alkali, organic

peroxides, metal alkyls

48 Strategy Update 2013

Specialty Chemicals sees limited growth in its key market sector positions

Expected market growth for the

market sectors relevant to

AkzoNobel: 3%

Revenue by Business Unit

37%

22%

20%

21%

Functional Chemicals

Industrial Chemicals

Surface Chemistry

Pulp and Performance Chemicals

• Key challenges due to capacity surplus in ethylene amines

• Significant energy cost differentiation among regions

Specialty Chemicals strategic direction

49 Strategy Update 2013

Noteworthy events 2012

• Acquired Boxing Oleochemicals, China

• Further expansion in Ningbo, China multisite

• MCA expansion in Taixing, China

• Opened bleaching chemical Island in Brazil

and further investment in another site

• Demerger and sales of Chemicals Pakistan

Actions going forward

• Further integrate and grow Boxing

• Benefit from capacity expansions in Taixing,

Brazil and Germany

• Generate growth from new products

• Further rationalize and consolidate

ERP systems

Expected 2015 financial outcomes

• Organic revenue growth: 3%

• Return on sales: 12%

• Return on investment: 15%

2.2

9.5 9.0 7.5

12.0 12.0

0

4

8

12

16

Decorative Paints Performance Coatings Specialty Chemicals

3.0

21.7

13.6 12.0

25.0

15.0

0

8

16

24

32

Decorative Paints Performance Coatings Specialty Chemicals

5.0 5.0

3.0

0

4

8

Decorative Paints Performance Coatings Specialty Chemicals

Realistic expected 2015 outcomes

50 Strategy Update 2013

Return

on

sales

Return

on

investment

2012

2015

Assumption: Revenue growth

3 year CAGR

%

%

%

Expected Outcomes

1. Introduction

2. Market environment

3. Group strategic update

4. Business Areas

5. Financial implications

6. Summary and conclusion

5. Financial implications

51 Strategy Update 2013

Historical EBITDA profitability shows stable results in challenging economic times

52 Strategy Update 2013

EBITDA as reported* € billion

0.0

0.5

1.0

1.5

2.0

0

2

4

6

8

10

12

14

2012

1.9

2011

1.8

2010

2.0

2009

1.7

2008

1.8

EBITDA EBITDA margin

EBITDA margin %

*All years excluding National Starch

0

53 Strategy Update 2013

Cash flow sources and uses

€ million

2011 2012

Source Use Source Use

• We are not generating enough cash from

operations to adequately meet our needs

• Restructuring and pension top-ups consume a

significant proportion of cash

• We have been borrowing to pay dividends

• Need to generate more cash from better

performance

• Remuneration metrics have been adjusted to

include cash generation

AkzoNobel sources and uses of cash remains a key challenge we are addressing

Capital expenditures

Pensions

Operating working capital

EBITA

Dividends

Provision

Targets for 2015 are focused on increased cash generation and value creation

54 Strategy Update 2013

New targets Old targets Change driver

Increase return on sales (ROS,

operating income/ revenue)

to 9%

Grow to €20 billion revenues • Increased focus on delivery of

operating profit after incidentals

Achieve return on investment

(ROI) to 14%

Increase EBITDA each year,

maintaining 13-15% margin

• Ultimate driver of value creation

• Deliver returns above the cost

of capital

Net debt/EBITDA <2.0 times Reduce OWC/revenues by

0.5 p.a. towards a 12% level

• Fuller measure of cash

generation; not just one

component

Deadline: end 2015 Deadline: medium term • Shorter term

• Defined point in time

• Increased focus on delivery

and accountability

Incidentals are now included in EBITDA* as part of our ongoing business

55 Strategy Update 2013

• Incidentals are now included in EBITDA

unless genuinely one-off and not related to

normal business

• Restructuring charges are now considered an

ongoing business activity and are not reported

as incidentals

• Performance improvement program

restructuring charges are also now included in

EBITDA

*Restated for IAS19 adjustments which impact the other line

€ million 2010 2011 2012

Incidentals as reported (139) (126) (2,520)

Total restated incidentals

(32) 3 (2,170)

Restated IAS19 incidentals with no impact on EBITDA

0 0 6

Total incidental EBITDA adjustment: (107) (129) (344)

IAS19 EBITDA adjustment 13 12 40

EBITDA as reported

EBITDA %

2,009

14.8%

1,834

12.6%

1,901

12.4%

Restated EBITDA

Restated EBITDA %

1,915

14.1%

1,717

11.8%

1,597

10.4%

0.0

0.5

1.0

1.5

2010 2011 2012*

0%

5%

10%

15%

2010 2011 2012* 2015

Operating income is our new focus: our return on sales target is to deliver 9% in 2015

56 Strategy Update 2013

• Going forward, operating income, after

incidentals, and return on sales (ROS,

operating income/revenue) are key metrics

• This will focus management on delivery and

quality of profits

• Operating income and ROS have not

progressed over the last three years

• Our ROS target is 9%, an increase of 3.1%

percentage points, by 2015

• Absolute operating income is one of the targets

for management remuneration

56 *2012 excluding impairment (€2.1 billion)

Specialty Chemicals

Performance Coatings

Return on sales (ROS) development

Operating income/revenue

AkzoNobel

Decorative Paints

Operating income development

€ billion

Return on investment target is to deliver 14% in 2015

57 Strategy Update 2013

0%

10%

20%

30%

40%

2010 2011 2012* 2015

Return on investment (ROI) development

Operating income/Average 12 month invested capital

Specialty Chemicals Performance Coatings

AkzoNobel Decorative Paints

• Return on investment is another key target for

the group, reflecting our focus on delivering

value through returns in excess of our cost

of capital

• Invested capital defined as total assets

(excluding cash, investments in associates,

pension assets, assets held for sale) less tax

liabilities and other payables

• Return on investment target is 14%,

an increase of 5.1 percentage points, by 2015

• Return on investment is one of the targets for

management remuneration

*2012 excluding impairment (€2.1 billion)

0%

100%

58 Strategy Update 2013

Profit and loss breakdown*

% of total

Variable costs represent 54% of revenue

Decorative

Paints

Performance

Coatings

Specialty

Chemicals

AkzoNobel

Raw materials, energy and other variable costs

Fixed production costs

Selling, advertising, administration, R&D costs

EBIT margin

* Rounded percentages

• Decorative Paints is more driven by

personnel costs in the distribution network,

while Specialty Chemicals has more

production costs

• Operating expense growth is primarily

due to wage inflation

• The performance improvement program

benefits are equally split

between fixed and variable costs

Operating cash flow is a key internal target

59 Strategy Update 2013

1.1 0.9 1.0

0.0

0.5

1.0

1.5

2010 2011 2012*

*2012 excluding impairment (€2.1)

Operating cash flow development

€ billion

• Operating cash flow includes:

– EBITDA (new definition)

– Change in operating working capital

– Capital expenditure

– Incidental costs

• Management remuneration is linked to

delivery of operating cash flow targets

0.0

0.5

1.0

1.5

2010 2011 2012

2015 target is to maintain a net debt to EBITDA ratio of less than two times

60 Strategy Update 2013

Net debt/EBITDA

x

• Maintain investment grade rating of BBB+

• We have a strong liquidity position to support growth

• No immediate refinancing is needed

• Average cost of debt has reduced over the last

three years

* At the end of Q3 2012

Debt maturities

billion

Average cost of long term bonds

%

0

0.3

0.6

0.9

2013 2014 2015 2016 2018 2022

€ bonds $ bonds £ bonds

7.29 6.35 5.62

0

2

4

6

8

2010 2011 2012

IAS 19 pension accounting changes create positive impact on EBITDA and net income

61

• Due to changes in IAS 19, the amortization charges in EBITDA will cease and the charges in financing

expenses are significantly lower

• The changes in IAS 19 no longer permit „corridor accounting‟. The reported funded status deficit excluding

administration costs previously included in the defined benefit obligation (DBO) liability will become the

new balance sheet liability, with an associated deferred tax impact (not shown on this slide).

Strategy Update 2013

€ million 2011 IAS19

impact

2012 IAS19

impact

Statement of income

EBITDA 12 40

Incidentals – 6

Financing expenses 25 62

After-tax impact in statement of income 29 77

Balance sheet

Pension net liabilities/(asset) 331 1,486

Other post-retirement liabilities (28) (21)

Post-retirement liabilities/(asset) 303 1,465

Pension cash flow guidance

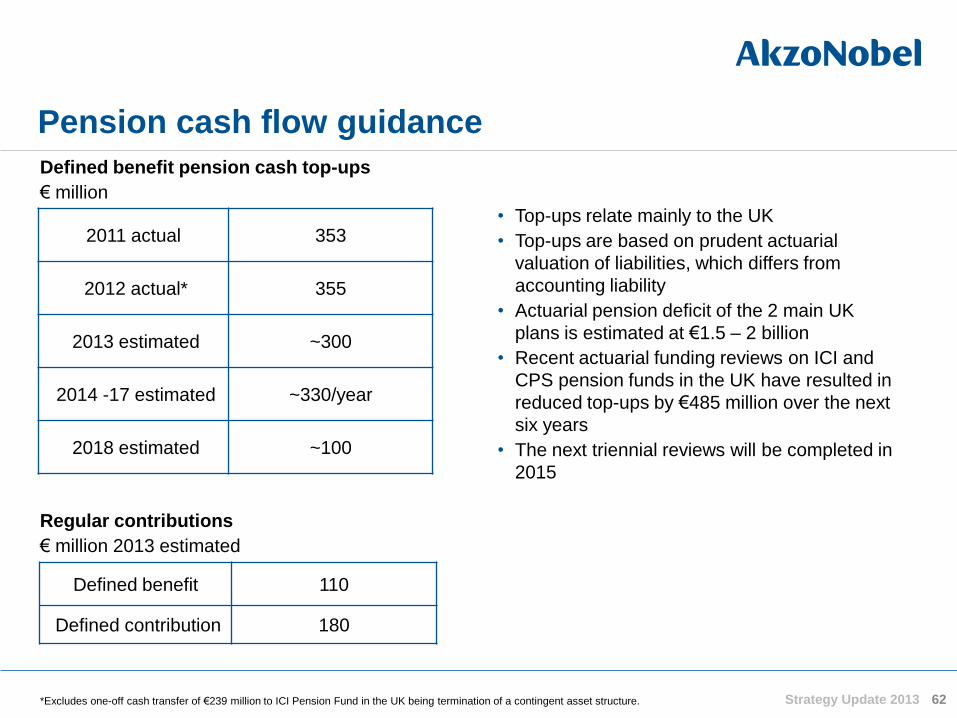

62 Strategy Update 2013

Defined benefit pension cash top-ups

€ million

2011 actual 353

2012 actual* 355

2013 estimated ~300

2014 -17 estimated ~330/year

2018 estimated ~100

• Top-ups relate mainly to the UK

• Top-ups are based on prudent actuarial

valuation of liabilities, which differs from

accounting liability

• Actuarial pension deficit of the 2 main UK

plans is estimated at €1.5 – 2 billion

• Recent actuarial funding reviews on ICI and

CPS pension funds in the UK have resulted in

reduced top-ups by €485 million over the next

six years

• The next triennial reviews will be completed in

2015

Defined benefit 110

Defined contribution 180

Regular contributions

€ million 2013 estimated

*Excludes one-off cash transfer of €239 million to ICI Pension Fund in the UK being termination of a contingent asset structure.

€ million

2010

2011 2012*

2015

Target

Revenue 13,605 14,604 15,390

EBITDA 1,915 1,717 1,597

Depreciation,

amortization (590) (563) (625)

Restated

incidentals (32) 3 (64)

Operating

income 1,293 1,157 908

EBITDA

margin 14.1% 11.8% 10.4%

Return on

sales 9.5% 7.9% 5.9% 9.0%

Invested

capital** 11,467 11,537 10,238

Return on

investment 11.3% 10.0% 8.9% 14.0%

New focus to improve performance and drive value creation

63 Strategy Update 2013

• Benefits of new targets

– Clear focus on value creation

– Linked to remuneration

of senior management

*2012 excluding impairment (€2.1 billion) ** Average 12 month invested capital excluding full year impairment

1. Introduction

2. Market environment

3. Group strategic update

4. Business Areas

5. Financial implications

6. Summary and conclusion

6. Summary and conclusion

64 Strategy Update 2013

Dividends

65 Strategy Update 2013

• Our dividend policy is to pay a stable to rising

dividend each year

• An interim and final dividend will be paid in

cash unless shareholders elect to receive a

stock dividend

2012

0.33

1.12

2011

0.33

1.12

2010

0.32

1.08

2009

0.30

1.05

Interim dividend Final dividend

A smaller Executive Committee going forward*

66 Strategy Update 2013 *With effect from the Annual General Meeting on April 26, 2013 **Until June 2013

Spelling and *

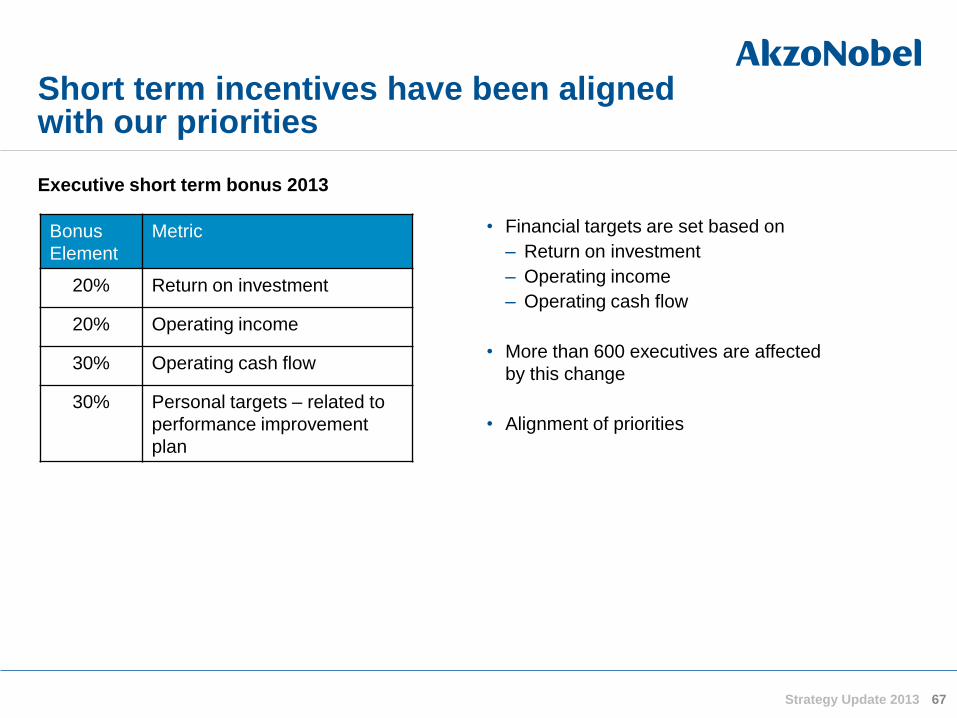

Short term incentives have been aligned with our priorities

67 Strategy Update 2013

• Financial targets are set based on

– Return on investment

– Operating income

– Operating cash flow

• More than 600 executives are affected

by this change

• Alignment of priorities

Executive short term bonus 2013

Bonus

Element

Metric

20% Return on investment

20% Operating income

30% Operating cash flow

30% Personal targets – related to

performance improvement

plan

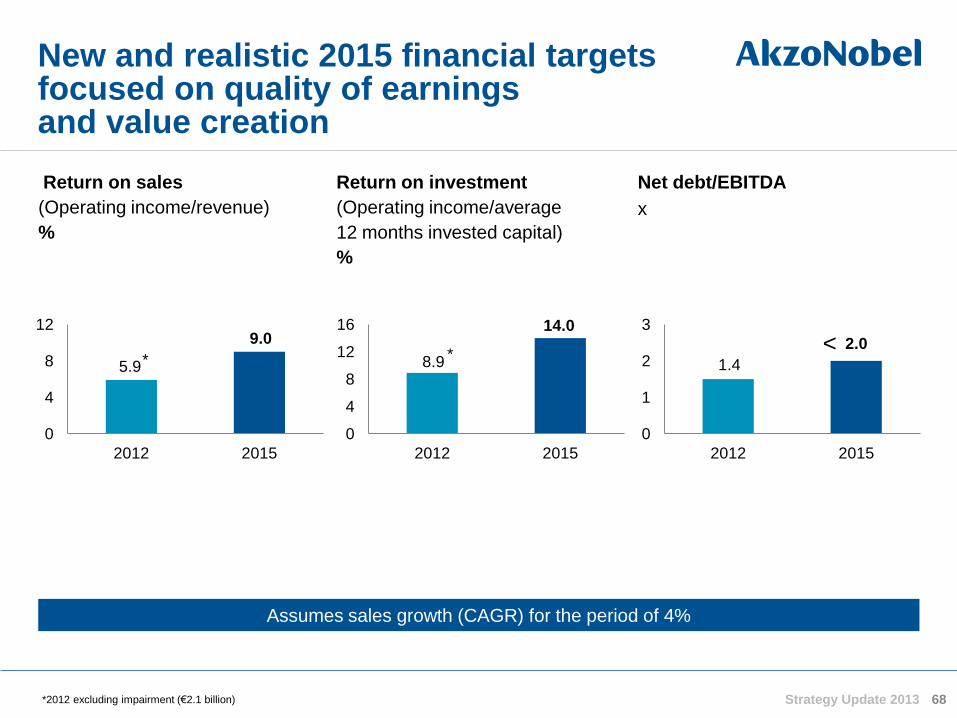

8.9

14.0

0

4

8

12

16

2012 2015

Return on sales

(Operating income/revenue)

%

68

Return on investment

(Operating income/average

12 months invested capital)

%

Strategy Update 2013

Net debt/EBITDA

x

New and realistic 2015 financial targets focused on quality of earnings and value creation

Assumes sales growth (CAGR) for the period of 4%

*2012 excluding impairment (€2.1 billion)

5.9

9.0

0

4

8

12

2012 2015

1.4

2.0

0

1

2

3

2012 2015

* * <

Summary

69 Strategy Update 2013

• Clear end-user segment focus providing forward looking indicators

and direction for our market initiatives and innovation spend

• Challenging market conditions expected in the near future

• Operational strategy on the basis of:

– Well defined strategic focus areas

– Core processes

– Clear set of actions aimed at continuous efficiency improvements

• Clear sustainability strategy and sustainability targets

• Guidance and targets defined

• A number of new management team members

• Focus on operating income, return on investment and cash generation:

remuneration aligned

Leading market positions

delivering leading performance

70

Today, the company has

• Excellent portfolio of businesses

• Good long term growth potential on the basis of end-user segment growth

• Strong positions in high growth markets (44% of revenue)

• Leadership positions in many markets

• Clear leader in sustainability

• Track record of delivering sustainable innovations and products

• Strong brands, both in consumer and industrial markets

Clear focus to deliver on our significant potential

• Improved returns and cash flow

• Leveraging scale

• Simplification and standardization

• Continued innovation

Strategy Update 2013

Thank you for your attention

Safe Harbor Statement

72 Investor update Full-Year 2012 & Q4 results

This presentation contains statements which address such key issues as

AkzoNobel’s growth strategy, future financial results, market positions, product development, products in

the pipeline, and product approvals. Such statements should be carefully considered, and it should be

understood that many factors could cause forecasted and actual results to differ from these statements.

These factors include, but are not limited to, price fluctuations, currency fluctuations, developments in raw

material and personnel costs, pensions, physical and environmental risks, legal issues, and legislative,

fiscal, and other regulatory measures. Stated competitive positions are based on management estimates

supported by information provided by specialized external agencies. For a more comprehensive discussion

of the risk factors affecting our business please see our latest Annual Report, a copy of which can be found

on the company’s corporate website www.akzonobel.com.

Appendices

73 Strategy Update 2013

2011 12 13 14 15 16 2011 12 13 14 15 16

74 Strategy Update 2013

In Consumer Goods, our activities are spread evenly over consumer durables and consumer packaging

Consumer electronics

production

$ billion, value added

2011 = 100

Furniture production

$ billion, value added

2011 = 109

Food and beverage

production

$ billion, value added

2011 = 871

-1.2% +2.2%

+7.9% p.a.

CAGR 2.6%

CAGR 1.8%

2011 12 13 14 15 16

Source: Oxford Economics Source: Oxford Economics Source: Oxford Economics

0

100

2011 12 13 14 15 16 2011 12 13 14 15 16 2011 12 13 14 15 16

75 Strategy Update 2013

In Industrial, our activity is spread across the two sub-segments

Brent crude futures price

$, price per barrel

Annual average spot price

2011 = $111

Energy and utilities

construction

$ billion, output

2011 = 360

Chemical production

$ billion, output

2011 = 690

CAGR

9.4%

CAGR

3.8%

Source: Oxford Economics Source: Business Monitor International Source: Oxford Economics

Scope 3 upstream

Raw materials

Scope 1 and 2

Own operations

Scope 3 downstream

Customer operations End-user End of life

Scope 4

Energy/resource benefits in use

Sustainable

business

Cost savings Cost savings

Improve revenue

and margin

Improve revenue and margin

Resource

efficiency

Reduced material

and energy use

Reduced

energy used

Reduced material

and energy use in

customer processes,

application

Reduced material and energy use

in product use

Capable,

engaged

people

Engaged suppliers Engaged

employees

Engaged customers Engaged customers and users

By focusing on the full value chain, we will drive business, resource and engagement benefits

76 76 Strategy Update 2013

€ million

2010

2011 2012*

2015

Outcome

Revenue 3,933 4,201 4,297

EBITDA 541 389 284

Depreciation,

amortization (205) (152) (176)

Restated

incidentals 0 (2) (14)

Operating

income 336 235 94

EBITDA

margin 13.8% 9.3% 6.6%

Return on

sales 8.5% 5.6% 2.2% 7.5%

Invested

capital** 4,908 5,032 3,121

Return on

investment 6.8% 4.7% 3.0% 12.0%

Decorative Paints restated financials, key assumptions and expected outcomes

77 Strategy Update 2013

• Financials are restated for changes to

incidental treatment and exclusion of the

North American Decorative Paints business

• Expected outcomes

– Return on sales of 7.5% by 2015

– Return on investment of 12% by 2015

• Key assumption

– Revenue CAGR of 5% to 2015

*2012 excluding impairment (€2.1 billion) ** Average 12 month invested capital excluding full year impairment

€ million 2010

2011 2012

2015

Outcome

Revenue 4,786 5,170 5,702

EBITDA 610 572 673

Depreciation,

amortization (107) (116) (131)

Restated

incidentals (16) 2 0

Operating

income 487 458 542

EBITDA

margin 12.7% 11.1% 11.8%

Return on

sales 10.2% 8.9% 9.5% 12.0%

Invested

capital* 2,063 2,267 2,499

Return on

investment 23.6% 20.2% 21.7% 25.0%

Performance Coatings restated financials, key assumptions and expected outcomes

78 Strategy Update 2013

• Financials are restated for changes to

incidental treatment

• Expected outcomes

– Return on sales of 12% by 2015

– Return on investment of 25% by 2015

• Key assumption

– Revenue CAGR of 5% to 2015

*Average 12 month invested capital

€ million

2010

2011 2012

2015

Outcome

Revenue 4.943 5.335 5.543

EBITDA 915 909 830

Depreciation,

amortization (260) (281) (306)

Restated

incidentals (51) (6) (24)

Operating

income 604 622 500

EBITDA

margin 18.5% 17.0% 15.0%

Return on

sales 12.2% 11.7% 9.0% 12.0%

Invested

capital* 3,464 3,406 3,678

Return on

investment 17.4% 18.3% 13.6% 15.0%

Specialty Chemicals restated financials, key assumptions and expected outcomes

79 Strategy Update 2013

• Financials are restated for changes to

incidental treatment

• Expected outcomes

– Return on sales of 12% by 2015

– Return on investment 15% by 2015

• Key assumptions

– Revenue CAGR of 3% to 2015

* New definition **Average 12 month invested capital

Incidentals now included in EBITDA as part of ongoing business

80 Strategy Update 2013

€ million 2010 2011 2012

Restructuring costs (104) (129) (324)

Impairment Deco - - (2,106)

Results related to major legal,

anti-trust and environmental cases

Results of acquisitions and divestments 33 10 (45)

Other incidental results (19) 2 (9)

Total Incidentals as reported (139) (126) (2,520)

Restructuring costs - - -

Impairment Deco - - (2,106)

Results related to major legal,

anti-trust and environmental cases

Results of acquisitions and divestments 33 10 (30)

Other incidental results (16) 2 (14)

Total Restated Incidentals (incl IAS 19 impact) (32) 3 (2,170)

Total difference (107) (129) (350)

Of which IAS 19 impact on incidentals - - 6

Remaining difference due to definition change) (107) (129) (344)

EBITDA as reported 2,009 1,834 1,901

EBITDA adjustment due to new definitions (107) (129) (344)

EBITDA adjustment due to IAS 19 impact 13 12 40

Restated EBITDA (IAS 19 impact included) 1,915 1,717 1,597

(9)

(9)

(36)

(20)

(49)

(49)

Variable costs analysis

81 Strategy Update 2013

30%

3%

7%

5% 14%

3%

9%

16%

7%

6%

2012 (excluding Decorative North America)

* Other variable costs include variable selling costs (e.g. freight) and products for resale ** Other raw materials include cardolite, hylar etc.

*** Chemicals and intermediates include caustic soda, acetic acid, tallow, ethylene, ethylene oxide, sulfur, amines etc.

Energy & other variable costs*

Raw materials

Other raw materials**

Titanium

dioxide

Coatings‟ specialties

Resins

Pigments

Additives

Solvents

Packaging

Chemicals and

intermediates***

Debt duration 4.2 years and no refinancing currently planned

82 Strategy Update 2013

Debt maturities*

€ million (nominal amounts)

Strong liquidity position to support growth

• Undrawn revolving credit facility of €1.7 billion (2017) and €0.1 billion (2016)

• €1.5 and $3 billion commercial paper programs, backed by the revolving credit facility

• Net cash and cash equivalents €1.6 billion*

15

825

622

800 750

379

44

306

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

€ bonds $ bonds £ bonds

* At the end of Q4 2012

Financial restatement summary for AkzoNobel Group

Strategy update 2013 83

FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012

Revenues 13.605 14.604 3.707 4.044 3.966 3.673 15.390 - - - - - - - 13.605 14.604 3.707 4.044 3.966 3.673 15.390

EBITDA 2.009 1.834 438 577 523 363 1.901 -94 -117 -28 -23 -95 -158 -304 1.915 1.717 410 554 428 205 1.597

Depreciation -435 -419 -114 -115 -115 -119 -463 - - - - - - - -435 -419 -114 -115 -115 -119 -463

Amortisation -155 -144 -39 -40 -41 -42 -162 - - - - - - - -155 -144 -39 -40 -41 -42 -162

EBIT 1.419 1.271 285 422 367 202 1.276 -94 -117 -28 -23 -95 -158 -304 1.325 1.154 257 399 272 44 972

Incidentals -139 -126 -52 -44 -2.229 -195 -2.520 107 129 31 33 99 187 350 -32 3 -21 -11 -2.130 -8 -2.170

Operating Income 1.280 1.145 233 378 -1.862 7 -1.244 13 12 3 10 4 29 46 1.293 1.157 236 388 -1.858 36 -1.198

Operating Income excl. impaired goodwill 1.280 1.145 233 378 244 7 862 1.293 1.157 236 388 248 36 908

Total Finance Charges -327 -336 -65 -82 -66 -54 -267 -2 25 15 15 16 16 62 -329 -311 -50 -67 -50 -38 -205

Associates 25 24 4 5 5 -1 13 - - - - - - - 25 24 4 5 5 -1 13

Finance Charges & Associates -302 -312 -61 -77 -61 -55 -254 -2 25 15 15 16 16 62 -304 -287 -46 -62 -45 -39 -192

Profit Before Tax 978 833 172 301 -1.923 -48 -1.498 11 37 18 25 20 45 108 989 870 190 326 -1.903 -3 -1.390

Tax -174 -233 -61 -82 -58 29 -172 -2 -8 -5 -7 -6 -13 -31 -176 -241 -66 -89 -64 16 -203

Minorities -83 -64 -14 -22 -9 -18 -63 - - - - - - - -83 -64 -14 -22 -9 -18 -63

Discontinued Income 33 -59 -26 4 -392 -22 -436 25 - - - - - - 58 -59 -26 4 -392 -22 -436

Net Income 754 477 71 201 -2.382 -59 -2.169 34 29 13 18 14 32 77 788 506 84 219 -2.368 -27 -2.092

Adjusted Net Income 912 790 162 259 234 119 774 -66 -157 -10 -7 -57 -95 -169 846 633 152 252 177 24 605

EPS 3,23 2,04 0,30 0,85 -10,00 -0,25 -9,14 0,15 0,12 0,06 0,07 0,06 0,14 0,32 3,38 2,16 0,36 0,92 -9,94 -0,11 -8,82

Adjusted EPS 3,91 3,10 0,69 1,09 0,98 0,50 3,26 -0,28 -0,27 -0,04 -0,03 -0,24 -0,40 -0,71 3,63 2,83 0,65 1,06 0,74 0,10 2,55

EBITDA Margin% 14,8% 12,6% 11,8% 14,3% 13,2% 9,9% 12,4% 14,1% 11,8% 11,1% 13,7% 10,8% 5,6% 10,4%

EBIT Margin % 10,4% 8,7% 7,7% 10,4% 9,3% 5,5% 8,3% 9,7% 7,9% 6,9% 9,9% 6,9% 1,2% 6,3%

Return on Sales % 9,4% 7,8% 6,3% 9,3% -46,9% 0,2% -8,1% 9,5% 7,9% 6,4% 9,6% -46,8% 1,0% -7,8%

Return on Sales % (excl. impaired goodwill) 9,4% 7,8% 6,3% 9,3% 6,2% 0,2% 5,6% 9,5% 7,9% 6,4% 9,6% 6,3% 1,0% 5,9%

Moving Average ROI% 12,1% 10,5% 10,2% 9,9% 9,7% 10,0% 10,0% 11,3% 10,0% 9,4% 8,7% -9,2% -10,1% -10,1%

Moving Average ROI% (excl. impaired goodwill) 11,3% 10,0% 8,9%

Capex 492 658 135 166 195 330 826 - - - - - - - 492 658 135 166 195 330 826

Invested Capital average (12M) 11.721 12.088 12.447 12.882 13.107 12.781 12.781 -254 -551 -642 -763 -865 -964 -964 11.467 11.537 11.805 12.119 12.242 11.817 11.817

Invested Capital average (12M) (excl. impaired goodwill) 11.721 12.088 11.467 11.537 10.238

OWC 1.839 1.891 2.259 2.314 2.178 1.659 1.659 -147 -57 -62 -87 -76 -87 -87 1.692 1.834 2.197 2.227 2.102 1.572 1.572

OWC% 13,5% 13,2% 15,1% 14,1% 13,6% 11,2% 11,2% 12,4% 12,9% 14,8% 13,8% 13,3% 10,7% 10,7%

New FormatRestatements (Incidentals & IAS 19)As Reported (excluding NA Deco)

Financial restatement summary for Decorative Paints

Strategy update 2013 84

FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012

Revenues 3.933 4.201 974 1.187 1.141 995 4.297 - - - - - - - 3.933 4.201 974 1.187 1.141 995 4.297

EBITDA 593 479 90 158 130 47 425 -52 -90 -22 -3 -33 -83 -141 541 389 68 155 97 -36 284

Depreciation -124 -91 -27 -26 -26 -27 -106 - - - - - - - -124 -91 -27 -26 -26 -27 -106

Amortisation -81 -61 -16 -17 -18 -19 -70 - - - - - - - -81 -61 -16 -17 -18 -19 -70

EBIT 388 327 47 115 86 1 249 -52 -90 -22 -3 -33 -83 -141 336 237 25 112 53 -82 108

Incidentals -52 -92 -22 -3 -2.144 -92 -2.261 52 90 22 3 33 83 141 - -2 - - -2.111 -9 -2.120

Operating Income 336 235 25 112 -2.058 -91 -2.012 - - - - - - - 336 235 25 112 -2.058 -91 -2.012

Operating Income excl. impaired goodwill 336 235 25 112 48 -91 94 336 235 25 112 48 -91 94

EBITDA Margin % 15,1% 11,4% 9,2% 13,3% 11,4% 4,7% 9,9% 13,8% 9,3% 7,0% 13,1% 8,5% -3,6% 6,6%

EBIT Margin % 9,9% 7,8% 4,8% 9,7% 7,5% 0,1% 5,8% 8,5% 5,6% 2,6% 9,4% 4,6% -8,2% 2,5%

Return on Sales % 8,5% 5,6% 2,6% 9,4% -180,4% -9,1% -46,8% 8,5% 5,6% 2,6% 9,4% -180,4% -9,1% -46,8%

Return on Sales % (excl. impaired goodwill) 8,5% 5,6% 2,6% 9,4% 4,2% -9,1% 2,2% 8,5% 5,6% 2,6% 9,4% 4,2% -9,1% 2,2%

Moving average ROI % 7,2% 5,9% 5,9% 5,2% 4,7% 4,8% 4,8% 6,8% 4,7% 4,4% 3,7% -37,4% -42,7% -42,8%

Moving Average ROI% (excl. impaired goodwill) 6,8% 4,7% 3,0%

Capex 127 155 29 41 44 92 206 - - - - - - - 127 155 29 41 44 92 206

Invested Capital average (12M) 5.407 5.500 5.614 5.738 5.658 5.151 5.151 -499 -468 -463 -463 -459 -450 -450 4.908 5.032 5.151 5.275 5.199 4.701 4.701

Invested Capital average (12M) (excl. impaired goodwill) 4.908 5.032 3.121

OWC 474 434 654 661 587 353 353 -71 - - - - - - 403 434 654 661 587 353 353

OWC % 12,7% 11,2% 16,8% 13,9% 12,9% 8,9% 8,9% 10,8% 11,2% 16,8% 13,9% 12,9% 8,9% 8,9%

Number of Employees 16.865 17.120 17.320 17.430 17.220 17.020 17.020 16.685 17.120 17.320 17.430 17.220 17.020 17.020

New FormatAs Reported (excluding NA Deco) Restatements (Incidentals & IAS 19)

Financial restatement summary for Performance Coatings

Strategy update 2013 85

FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012

Revenues 4.786 5.170 1.369 1.472 1.467 1.394 5.702 - - - - - - - 4.786 5.170 1.369 1.472 1.467 1.394 5.702

EBITDA 647 611 164 213 202 190 769 -37 -39 -5 -9 -39 -43 -96 610 572 159 204 163 147 673

Depreciation -81 -86 -23 -25 -23 -24 -95 - - - - - - - -81 -86 -23 -25 -23 -24 -95

Amortisation -26 -30 -9 -8 -10 -9 -36 - - - - - - - -26 -30 -9 -8 -10 -9 -36

EBIT 540 495 132 180 169 157 638 -37 -39 -5 -9 -39 -43 -96 503 456 127 171 130 114 542

Incidentals -53 -37 -5 -9 -39 -43 -96 37 39 5 9 39 43 96 -16 2 - - - - -

Operating Income 487 458 127 171 130 114 542 - - - - - - - 487 458 127 171 130 114 542

EBITDA Margin % 13,5% 11,8% 12,0% 14,5% 13,8% 13,6% 13,5% 12,7% 11,1% 11,6% 13,9% 11,1% 10,5% 11,8%

EBIT Margin % 11,3% 9,6% 9,6% 12,2% 11,5% 11,3% 11,2% 10,5% 8,8% 9,3% 11,6% 8,9% 8,2% 9,5%

Return on Sales % 10,2% 8,9% 9,3% 11,6% 8,9% 8,2% 9,5% 10,2% 8,9% 9,3% 11,6% 8,9% 8,2% 9,5%

Moving average ROI % 26,3% 22,0% 22,0% 22,9% 23,9% 25,6% 25,6% 23,6% 20,2% 20,4% 20,5% 20,6% 21,7% 21,7%

Capex 87 116 18 25 23 57 123 - - - - - - - 87 116 18 25 23 57 123

Invested Capital average (12M) 2.054 2.253 2.326 2.397 2.471 2.488 2.488 9 14 10 9 9 11 11 2.063 2.267 2.336 2.406 2.480 2.499 2.499

OWC 714 772 852 871 857 742 742 -23 - - - - - - 691 772 852 871 857 742 742

OWC % 14,4% 14,6% 15,6% 14,8% 14,6% 13,3% 13,3% 14,0% 14,6% 15,6% 14,8% 14,6% 13,3% 13,3%

Number of Employees 21.020 21.960 21.910 21.920 21.650 21.310 21.310 21.020 21.960 21.910 21.910 21.640 21.310 21.310

As Reported Restatements (Incidentals & IAS 19) New Format

Financial restatement summary for Specialty Chemicals

Strategy update 2013 86

FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012

Revenues 4.943 5.335 1.399 1.431 1.393 1.320 5.543 - - - - - - - 4.943 5.335 1.399 1.431 1.393 1.320 5.543

EBITDA 939 906 235 255 227 172 889 -24 3 - -20 -19 -20 -59 915 909 235 235 208 152 830

Depreciation -214 -228 -61 -63 -62 -65 -251 - - - - - - - -214 -228 -61 -63 -62 -65 -251

Amortisation -46 -53 -13 -15 -13 -14 -55 - - - - - - - -46 -53 -13 -15 -13 -14 -55

EBIT 679 625 161 177 152 93 583 -24 3 - -20 -19 -20 -59 655 628 161 157 133 73 524

Incidentals -75 -3 -21 -23 -19 -20 -83 24 -3 - 20 19 20 59 -51 -6 -21 -3 - - -24

Operating Income 604 622 140 154 133 73 500 - - - - - - - 604 622 140 154 133 73 500

EBITDA Margin % 19,0% 17,0% 16,8% 17,8% 16,3% 13,0% 16,0% 18,5% 17,0% 16,8% 16,4% 14,9% 11,5% 15,0%

EBIT Margin % 13,7% 11,7% 11,5% 12,4% 10,9% 7,0% 10,5% 13,3% 11,8% 11,5% 11,0% 9,5% 5,5% 9,5%

Return on Sales % 12,2% 11,7% 10,0% 10,8% 9,5% 5,5% 9,0% 12,2% 11,7% 10,0% 10,8% 9,5% 5,5% 9,0%

Moving average ROI % 19,2% 17,8% 17,3% 17,6% 16,8% 15,6% 15,6% 17,4% 18,3% 16,9% 16,7% 15,5% 13,6% 13,6%

Capex 273 365 87 95 125 177 484 - - - - - - - 273 365 87 95 125 177 484

Invested Capital average (12M) 3.545 3.521 3.528 3.615 3.693 3.735 3.735 -81 -115 -54 -55 -57 -57 -57 3.464 3.406 3.474 3.560 3.636 3.678 3.678

OWC 651 685 754 783 734 564 564 -14 - - - - - - 637 685 754 783 734 564 564

OWC % 12,9% 13,3% 13,5% 13,7% 13,2% 10,7% 10,7% 12,6% 13,3% 13,5% 13,7% 13,2% 10,7% 10,7%

Number of Employees 11.080 11.510 11.860 11.980 11.950 10.750 10.750 11.080 11.510 11.860 11.980 11.950 10.750 10.750

As Reported Restatements (Incidentals & IAS 19) New Format

Financial restatement summary for Other Activities

Strategy update 2013 87

FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012 FY2010 FY2011 Q1-12 Q2-12 Q3-12 Q4-12 FY2012

Revenues -57 -102 -35 -46 -35 -36 -152 - - - - - - - -57 -102 -35 -46 -35 -36 -152

EBITDA -170 -162 -51 -49 -36 -46 -182 19 9 -1 9 -4 -12 -8 -151 -153 -52 -40 -40 -58 -190

Depreciation -16 -14 -3 -1 -4 -3 -11 - - - - - - - -16 -14 -3 -1 -4 -3 -11

Amortisation -2 - -1 - - - -1 - - - - - - - -2 - -1 - - - -1

EBIT -188 -176 -55 -50 -40 -49 -194 19 9 -1 9 -4 -12 -8 -169 -167 -56 -41 -44 -61 -202

Incidentals 41 6 -4 -9 -27 -40 -80 -6 3 4 1 8 41 54 35 9 - -8 -19 1 -26

Operating Income -147 -170 -59 -59 -67 -89 -274 13 12 3 10 4 29 46 -134 -158 -56 -49 -63 -60 -228

Capex 5 22 1 5 3 4 13 - - - - - - - 5 22 1 5 3 4 13

Restatements (Incidentals & IAS 19) New FormatAs Reported (excluding NA Deco)