AKPK Power - Chapter 5 - Buying A House

23

Published by:

-

Upload

encik-anif -

Category

Documents

-

view

221 -

download

0

Transcript of AKPK Power - Chapter 5 - Buying A House

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 1/22

Published by:

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 2/22

Agensi Kaunseling dan Pengurusan Kredit

Aras 8, Maju Junction Mall

1001, Jalan Sultan Ismail50250 Kuala Lumpur

Fax : 03-2616 7601 E-mail: [email protected]

© AKPK

First Edition 2011

The copyright o this book belongs to Agensi Kaunseling

dan Pengurusan Kredit (AKPK). This book or parts thereo,

may be reproduced, translated, or transmitted in any orm

with prior written permission rom AKPK only or the sole

purpose o education. No monetary gain in any orm should

be made or derived, whether direct or indirect rom such

reproduction.

ISBN 978-983-44004-2-2

Disclaimer:

The inormation contained in this book is solely or educational purpose. It is notintended as a substitute or any advice you may receive rom a proessional fnancialadvisor.

Agensi Kaunseling dan Pengurusan Kredit (AKPK) disclaims all and any liability to anyperson using the inormation in this book as a basis or making or taking an action.

While all eorts have been made to make the inormation contained in this bookaccurate, AKPK seeks your understanding or any errors or omission.

The names and details o individuals in the real lie cases have been changed toprotect their identities.

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 3/22

Chper

5BUying

a hOUsE

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 4/22

74

Buying a house is an exciting event,

especially i it is your rst home. A

house may probably be the biggest

purchase you will make and perhapsone o the most crucial inancial

decision you will make as an adult.

To nance the purchase o a house,

you will need to irst source or

a housing loan. Understanding

the steps involved in securing a

housing loan will help you save

time, avoid uncertainties and reduce

unnecessary stress.

This chapter will provide you with

insights on various issues with

regards to buying and nancing the

purchase o a house.

tO BUy OR REnt?

Owning your own home gives you a sense o pride, accomplishment

and security o having a permanent roo over your head.

When you buy a house, you get to increase your net worth as

you pay down the loan. Each monthly payment you make reduces

the outstanding and increases the equity on your house. Paying

down your mortgage will also allow you to renance your house

i you have a need or it in the uture. Renancing should only be

considered i you have sucient equity on your house, a good

purpose and a need or the additional loan.

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 5/22

75

While rental rates can increase rom year to year, the principal

on your mortgage goes down with each payment you make. In

addition, as the housing market grows, the value o your house

appreciates, particularly i it is in a good location.

Although buying a house sounds great, it may not be aordable

or everyone. These are some commitments that may come with

the purchase o a house:

• Owning a house may take up a lot of your time as you

have to handle repairs and the general upkeep o thehouse

• Many small improvements you make to your house can add

up to your expenses. I you rent, maintenance expenses

are usually covered by the landlord

• You are in fact tied down to your house, unlike a tenant

who has the reedom to move about

• If you are not happy with your new neighbourhood, you

may find yourself ‘stuck’ until the value of your house

appreciates beore you can sell it

• Many things can happen unexpectedly to bring down the

value o your house. For instance, the area may be proneto foods or the access to your house may be aected by

a new development

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 6/22

76

o whe ou hould re

• When you cannot afford

the installments or down

payment

• When you expect the

property market to soten

• When you are scouting for

a suitable location to buy a

house

• When you do not want to

worry about maintenance

and repair costs

Renting a house gives you the reedom o

movement

Owning a house gives you a sense o fnancial

reedom

gude

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 7/22

77

BUying FOR inVEstMEnt

Investing in property can be a powerul wealth-building tool. This

is especially true i you are considering becoming a landlord

through a house purchase.

Here are some questions to consider when buying a house for

investment:

• What type of property will increase my nancial worth?

• How much rental income can I expect from my property?

• Will I be able to handle long-term ownership and

maintenance o the property, even i my cash fow is not

consistent (especially when my property is not tenanted)?

• As properties are not liquid and cannot be sold quickly, will

this be a problem for me when there is a need for cash?

Are you willing to deal with the responsibilities of being a landlord?

It is not an easy task. You will have to collect rent and there

might be instances when the rent is delayed or not paid. You

may not be happy with your tenant and may have to evict them.

Furthermore, there will be repair works, tenancy agreements,income or deductions to be declared and taxes to be paid. O

course, you can engage proessionals to take care o these

matters or you – but that comes with a cost!

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 8/22

78

i ou re bu proper d pl o

ell ler, keep md h ou m be

subjected to Real Property Gains Tax (RPGT)o he rom he le o our proper

1location of

the popety

– location!

location!

location!

When purchasing a house either or investment or residential

purpose, location should be your main consideration. A good

location helps you attract tenants, get the rental income you want

and increase the value o your house.

FaCtORs tO COnsiDER

There are two aspects to consider beore buying a house. These

can be classied as non-nancial and nancial aspects.

no-fcl pec

You need to decide where you

would want to live and the kind

o neighbourhood that suits your

needs. There are many actors

that may infuence your choice o

location. Some o them are:

• basic amenities like shops,banks, post oice, schools,

hospitals, recreational parks and

the general neighbourhood

• availability of public

transportation

• proximity to your work place

• trafc condition

• security

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 9/22

79

2

3Type of

owneship

– freehold or

leasehold

The main types o properties are

landed and high-rise. Landed

properties generally cost more,

especially the ones nearer to

cities. High-rise condominiums and

apartments on the other hand are

normally more aordable. Landed

properties also tend to appreciate

more than high-rise properties

When you buy a reehold property,

you get to own the property or

an indeinite period. A leasehold

property on the other hand, lets you

own the property only or the lease

period, normally up to a period o

99 years. Ater the lease period isover, the property reverts to the

state authority, unless the lease

is renewed (which when done, a

premium (cost) needs to be paid).

Due to this, a reehold property

tends to command a higher price

over a leasehold property

Type of

popety

– landed or

high-rise

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 10/22

80

A title proves your ownership over

a property. You will be issued an

individual title or landed properties,

while a strata title will be given

or condominiums or apartments.

You need to check if there are

encumbrances or restrictions in

interest on the property you are

buying. These restrictions may aect

the transerability or saleability o

the property. It is best to get a

lawyer or someone amiliar with this

matter to advise you beore paying

any deposit or the purchase

Most developers o a new project

adopt a sell-then-build approach.Thereore i you are buying a new

house, you will initially not be able

to see what you are paying for. Here

the track record o the developer

becomes important. Assess their

previous projects to see i they

keep to their promises. Check:

• if they deliver properties on

time

• the quality of their work

• if they provide all the amenities

as promised in the brochure

4

Avaiabiity

of tite

– individual or

strata

5reputation

of deveope

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 11/22

81

• if their previous customers were

satisied with their purchase

upon receiving their units

• if a project is abandoned, you

are liable or all disbursements

made by the bank although

you do not get delivery o the

house

Note that reputable developers

normally charge a premium on theirproperties

Fcl pec

ae our ordbl

Assess your cash fow and net worth position to determine your

inancial standing. These statements serve as your inancialscorecards that should be used as a reerence when you make

money-related decisions.

Basically there are two main aordability issues to consider:

Dow pme d oher reled co

A good estimate or a down payment on a house would be about

10% to 20% of the purchase price. You would also need to setaside another 5% to 10% for related costs, such as legal fees

and stamp duties.

Please refer to Appendix 5.1 for details.

To pay or the above costs, common options are:

Perol v or veme Use your savings or investments to pay for your down payment.

A higher down payment lowers your cost of borrowing.

reputation of

deveope (continuation)

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 12/22

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 13/22

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 14/22

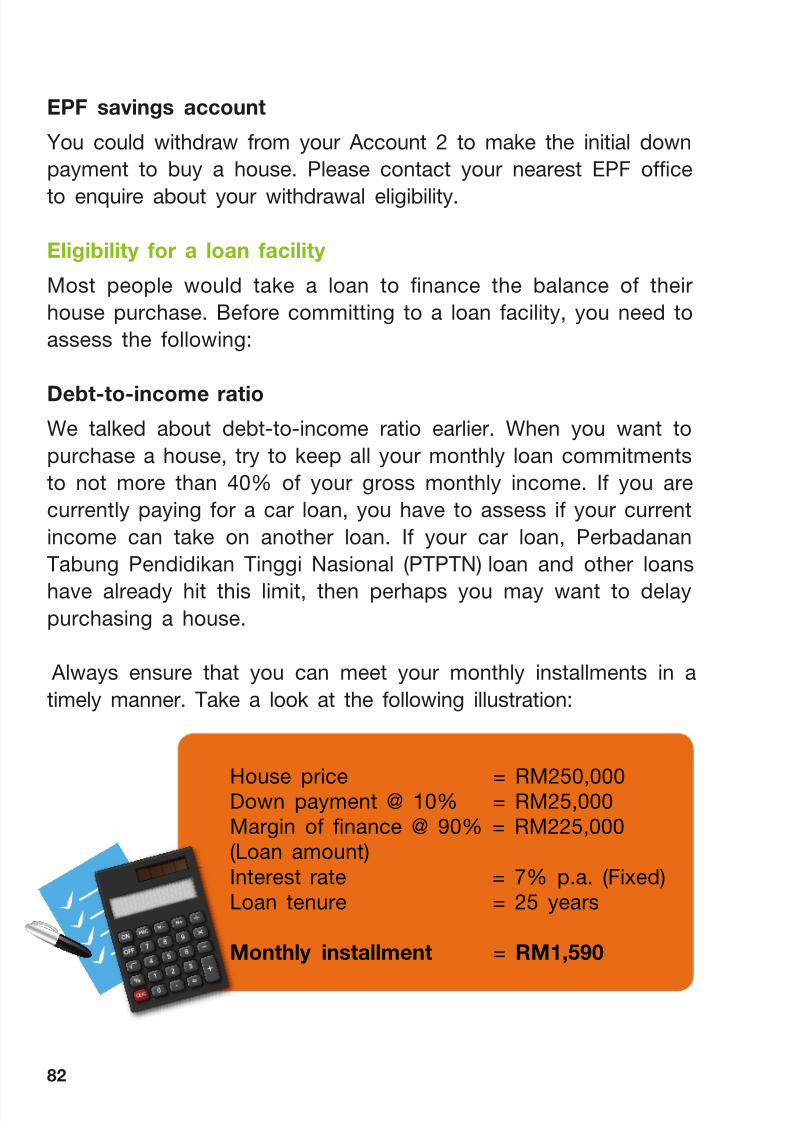

84

Lo-o-vlue ro (LtV)

LTV ratio is also commonly referred to as the margin of nancing.

Typically, banks are willing to lend you up to 90% of the purchase

price. However, the margin of nancing may vary depending onthe type o property, the existing loans and repayment capacity

o the borrower. The dierence between the loan and purchase

price is what you need to pay in cash when buying a house.

For your investment properties, it is best that you keep the LTV

ratio low. This is because, should there be a signicant weakening

o property prices, you may be required by your nancier to eitherreduce your loan outstanding or provide additional security to

maintain the LTV margin set by the nancial institutions.

tyPEs OF LOan

Ater assessing your capacity, check the loan packages that are

available in the market that best suits your requirements.

Here are some of the different types of loan available:

• Conventional loan or Islamic nancing

• Fixed or oating rate

• Term or exi loan

• Level or graduated payment

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 15/22

85

BLR is an interest rate calculated by fnancial

institutions based on a ormula which takes

into account the institution’s cost o unds and

other administrative costs. Any changes to the

BLR will:

a) increase or decrease the amount o repayment; and

b) extend or shorten the tenure

It may seem complicated and conusing at rst but i you take

your time to do your research and know what works best or you,

you should be able to nd the right package. Most loans are tied

to the BLR.

Currently, many inancial institutions oer loans at attractive

rates (below BLR). However, you need to be mindful that most

of these rates come with ‘lock-in’ periods (normally 5 years). If

you redeem the loan within this period, you may be subjected

to a penalty ee.

Browse the website o BNM

www.bko.com.mor urther inormation.

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 16/22

86

Fxed or o re?

With a xed rate loan, the interest remains constant. Thus the

installment remains the same over the tenure

With a loating rate loan, the interest is pegged to BLR.

I the BLR rises, your interest rate will increase and your

monthly repayments will be higher. On the other hand, i the

BLR decreases you will benet rom paying lower monthly

repayments

There are also foating interest rate loans with xed monthly

payments where any changes to the interest rate will either

increase or decrease the loan tenure

Keep up wh our commme After knowing your capabilities and being able to answer ‘yes’ to

the ollowing questions, you are ready to buy a house:

• Am I ready for a long term commitment?

• Can I keep up with the installments?

• If you are buying for investment, can you continue payingthe installments without rental income?

I you are unable to keep up with your housing loan repayments,

you can end up losing your house as well as all the monies you

have paid or the house. I the bank decides to auction your house,

you will be liable or any shortall arising rom the auction.

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 17/22

87

i our pocke deep eouh?

Age : 31 years old

Occupation : Technician

Marital status : Single

Kanesan only had one credit card and a hire purchase

facility of RM50,000. He did not live a lavish lifestyle,

was prudent with his spending and careul with his

credit cards. As the eldest child in his amily, he took

it upon himsel to take care o his parents and siblings,

although his salary as a technician was barely enough to

pay or the household expenses and his hire purchase

commitment.

Ater years o staying in a rented house, his amily

persuaded him to buy a house o his own. They insisted

that through home ownership, he would not lose the

monthly installment paid towards the house as he would

own the property at the end o the loan tenure.

Kanesan was excited with the idea and thought that he

could manage the monthly housing loan installments with

his overtime and extra allowance. He soon agreed to his

amily’s persuasion and took a loan or RM150,000 to

purchase the house.

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 18/22

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 19/22

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 20/22

90

Checkl

Have you done a developer’s background check, if

you are buying a house under construction?

Do you know the encumbrances and restrictions

in interest on the title?Do you have enough money to make the down

payment?

Can you aord to pay the monthly installments

comfortably?

Do you know the incidental ees or costs that

you have to pay?

Is the interest rate xed or pegged to the BLR?

Is there a penalty i you redeem your loan beore

the tenure expires?

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 21/22

91

sELF assEssMEnt

1. When buying a house, you should _________________a. check the background o the developer (i buying a

house under construction)

b. consider the location o the property, in line with yourrequirement

c. consider the monthly loan installments and other relatedcosts, in line with your level o aordability

d. all o the above

2. Generally owning your own home means all of the following,EXCEPT:

a. A sense o pride, accomplishment and security

b. Increasing your net worth

c. Unable to rent out the house

d. Pay quit rent and assessment

3. When you decide to apply or a housing loan, what is themost important factor to be considered?

a. Determine your abil ity to service the monthlyinstallments

b. Ensure that you understand the loan agreement

c. Check your CCRIS

d. Find a suitable location

4. The ollowing are direct and incidental costs usually incurredduring property purchase, EXCEPT:

a. Legal ees or Sales and Purchase Agreement

b. Legal ees or bank loan agreement

c. Real Property Gains Tax

d. Stamp duties on S&P and loan agreement

8/6/2019 AKPK Power - Chapter 5 - Buying A House

http://slidepdf.com/reader/full/akpk-power-chapter-5-buying-a-house 22/22

![Request for Quotation [RFQ] - AKPK](https://static.fdocuments.us/doc/165x107/61cb4938d42d0c5ac76b5ca4/request-for-quotation-rfq-akpk.jpg)