akk.docx

37

20 Student: _______________________________________________________________________________________ 1. A bonus usually differs from a salary in terms of: A. Amount and timing. B. Base, timing, and financial statement effect. C. Tax implications. D. Motivation effects. E. Base, pool, and payment terms. 2. Of the three basic forms of management compensation (salary, bonus, benefits), the fastest growing part of total compensation is: A. Salary. B. Bonus. C. Benefits. D. Salary and bonus. 3. As a firm's strategy changes to respond to different stages of a product's life cycle, compensation: A. Can be affected. B. Is affected, but only to a very limited extent. C. Should change in response to the new strategy. D. Should increase. E. Should decrease. 4. Risk aversion by managers should be recognized when revising compensation plans because: A. Compensation mix (salary, bonus) can influence a manager's risk aversion. B. Most companies want risk averse managers. C. Most companies want risk taking managers. D. It costs less to pay risk averse managers. 5. Due in part to the failure of many banks in 2008, executive compensation is getting increased oversight by: A. Audit committees of corporate boards B. Top management C. Compensation committees of corporate boards D. Banking regulators and corporate compensation committees E. Banking regulators such as the SEC 6. Any system of compensation: A. May encourage unethical behavior. B. Must be approved by the appropriate regulatory authority. C. Should be designed by top management. D. Must be approved by the auditor. 7. The objectives of management compensation, when compared to the objectives used to develop performance measurement systems, are: A. More numerous. B. Less specific. C. Consistent in content. D. Significantly broader in scope. E. More specific. 8. In developing compensation plans, the management accountant works to achieve fairness by making the plan: A. Precise, comprehensive and directive. B. Simple, clear and consistent. C. Attractive. D. Rewarding. E. Selective. 9. Bases for management bonus compensation often include:

-

Upload

michael-johnson -

Category

Documents

-

view

11 -

download

0

Transcript of akk.docx

20Student: _______________________________________________________________________________________

1. A bonus usually differs from a salary in terms of:

A. Amount and timing. B. Base, timing, and financial statement effect. C. Tax implications. D. Motivation effects. E. Base, pool, and payment terms.

2. Of the three basic forms of management compensation (salary, bonus, benefits), the fastest growing part of total compensation is:

A. Salary. B. Bonus. C. Benefits. D. Salary and bonus.

3. As a firm's strategy changes to respond to different stages of a product's life cycle, compensation:

A. Can be affected. B. Is affected, but only to a very limited extent. C. Should change in response to the new strategy. D. Should increase. E. Should decrease.

4. Risk aversion by managers should be recognized when revising compensation plans because:

A. Compensation mix (salary, bonus) can influence a manager's risk aversion. B. Most companies want risk averse managers. C. Most companies want risk taking managers. D. It costs less to pay risk averse managers.

5. Due in part to the failure of many banks in 2008, executive compensation is getting increased oversight by:

A. Audit committees of corporate boards B. Top management C. Compensation committees of corporate boards D. Banking regulators and corporate compensation committees E. Banking regulators such as the SEC

6. Any system of compensation:

A. May encourage unethical behavior. B. Must be approved by the appropriate regulatory authority. C. Should be designed by top management. D. Must be approved by the auditor.

7. The objectives of management compensation, when compared to the objectives used to develop performance measurement systems, are:

A. More numerous. B. Less specific. C. Consistent in content. D. Significantly broader in scope. E. More specific.

8. In developing compensation plans, the management accountant works to achieve fairness by making the plan:

A. Precise, comprehensive and directive. B. Simple, clear and consistent. C. Attractive. D. Rewarding. E. Selective.

9. Bases for management bonus compensation often include:

A. Stock price performance. B. Percentage of salary. C. Achievement of break-even sales. D. Percentage of firm-wide net income.

10. When strategic performance measures or critical success factors are used to determine bonus compensation, the bonus will usually depend either on the amount of improvement in the measure or on:

A. Maintaining the current level. B. Achieving a predetermined goal. C. Quality of work completed. D. Intensity of effort expended.

11. Bonus plans should be tied to variable cost income which is not affected by inventory level changes, rather than the conventional:

A. Tax-based net income. B. Marginal cost income. C. Full cost income. D. Operating income.

12. The balanced scorecard critical success factors (CSFs) provide strong motivation in bonus compensation plans if the non-controllable factors are:

A. Emphasized. B. Separated. C. Recognized. D. Excluded. E. Controlled.

13. If fairness only is considered, unit managers prefer:

A. Not to be evaluated. B. A subjective measure. C. A single, objective measure. D. A firm-wide pool over a unit-based pool. E. A unit-based pool over a firm-wide pool.

14. Generally, the current and deferred types of bonus payment options currently in use tend to focus the manager's attention on short-term performance measures, most commonly:

A. Division profit. B. After tax corporate profit. C. Cash flow. D. Growth in firm value. E. Stock price.

15. The stock option form of bonus payments to managers usually:

A. Motivates well even in extended market downturns. B. Can lose some motivation because of the delay in reward. C. Focuses on the short-term. D. Is not consistent with shareholder interests. E. Has less risk than other types of bonus payment plans.

16. The ideal compensation plan would make all company contributions to the plan immediately tax-deductible and all tax consequences for managers:

A. Insignificant. B. Deferred or avoidable. C. Limited, but current. D. Limited, but pre-paid.

17. In management compensation, the use of the balanced scorecard achieves:

A. Fairness. B. Alignment of manager's incentives and the organization's strategy. C. The desired ethical environment. D. Revenue generation and cost control. E. A specific non-financial measurement.

18. The balanced scorecard evaluation of the firm is an especially strong financial tool because of its:

A. Use of qualitative measures. B. Use of quantitative measures. C. Simplicity in use. D. Ability to predict change. E. Use of multiple critical success factors (CSFs).

19. The receivables turnover ratio is a measure of:

A. Asset value. B. Leverage. C. Sales performance. D. Profitability. E. Liquidity.

20. Market value of equity is an objective measure which clearly shows what:

A. The firm's financial statements show the firm's value to be. B. Investors think is the firm value. C. Stock analysts calculate as the firm's value. D. Is the sales value of the firm.E. Is the liquidation value of the firm.

21. Analysts prefer the following three valuation methods over all others:

A. EVA, cash flow multiplier and sales multiplier

B. Enterprise value, discounted cash flow, and sales multiple C. Sales multiple, earnings multiple, and discounted cash flow D. EVA, return on equity and discounted cash flow E. Enterprise value, earnings multiple, and sales multiple

22. Since it is based on cash flows, the discounted cash flow (DCF) method of valuation has the added advantage that it is not subject to the bias of different:

A. Discount rates. B. Internal rates of return. C. Monetary systems. D. Accounting policies for determining total assets and net income.

23. The multiplier used in an earnings-based method of valuation of a firm is often estimated from the price-to-earnings ratios of the stocks of comparable:

A. Taxable entities. B. Industries. C. Firms. D. For-profit firms. E. Publicly-held firms.

24. Which one of the following items is not a measure of a company's liquidity?

A. Accounts receivable turnover. B. Return on equity. C. Quick ratio. D. Cash flow ratio. E. Day's sales in inventory.

25. Which one of the following forms of compensation is a based upon the achievement of performance goals for current the period?

A. Perk. B. Stock option. C. Performance shares. D. Bonus. E. Salary.

26. Which one of the following forms of compensation includes special services and benefits for the employee?

A. Perk. B. Stock option. C. Performance shares. D. Bonus. E. Salary.

27. A method for determining a bonus based upon the performance of the unit is a(n):

A. Segment-based pool. B. Unit-based pool. C. Firm-based pool. D. Activity-based pool. E. Function-based pool.

28. A method for determining a bonus based upon the performance of the firm is a(n):

A. Segment-based pool. B. Unit-based pool. C. Firm-based pool. D. Activity-based pool. E. Volume-based pool.

29. All of the following are listed as common payment options for bonus compensation plans except:

A. Performance shares. B. Current bonus. C. Deferred bonus. D. Preferred bonus. E. Stock options.

30. The profit multiplier is used to measure:

A. Efficiency. B. Effectiveness. C. Net revenue. D. Collectability. E. Accountability.

31. Each one of the following is a method for directly measuring the value of a firm's equity except:

A. The discounted cash flow method. B. Market value.

C. Sales multiple. D. Earnings-based valuation. E. Enterprise value.

32. Which one of the following refers to the firm's ability to pay its current operating expenses and maturing debt?

A. Discounted cash flow. B. Liquidity. C. Earnings base. D. Profitability. E. Purchasing power.

33. Which one of the following develops the value of the firm as the discounted present value of the firm's net free cash flows?

A. Discounted cash flow method. B. Liquidity method. C. Multiples-based method. D. Profitability method. E. Purchasing power method.

34. A deferred bonus consists of:

A. Cash only. B. Stock only. C. Cash and/or stock. D. Membership in a fitness club.

35. Which one of the following computes value based on annual earnings?

A. Discounted cash flow method. B. Liquidity method. C. Multiples-based method. D. Profitability method. E. Market value method.

36. Jackson Supply Company has a 2 to 1 current ratio. This ratio would increase to more than 2 to 1 if the company:

A. Purchased a marketable security for cash. B. Wrote off an uncollectible receivable. C. Sold merchandise on account that earned a normal gross margin. D. Purchased inventory on account.

37. Benefits include all of the following except:

A. Travel. B. Life insurance. C. Medical benefits. D. Membership in a fitness club. E. Performance shares.

38. A current bonus consists of:

A. Cash only. B. Stock only. C. Cash and/or stock. D. Membership in a fitness club.

39. In service firms, improvement in long term profitability is best measured by all the following except:

A. Staff utilization. B. Net revenues. C. Collections of customer accounts. D. Materials usage.

40.

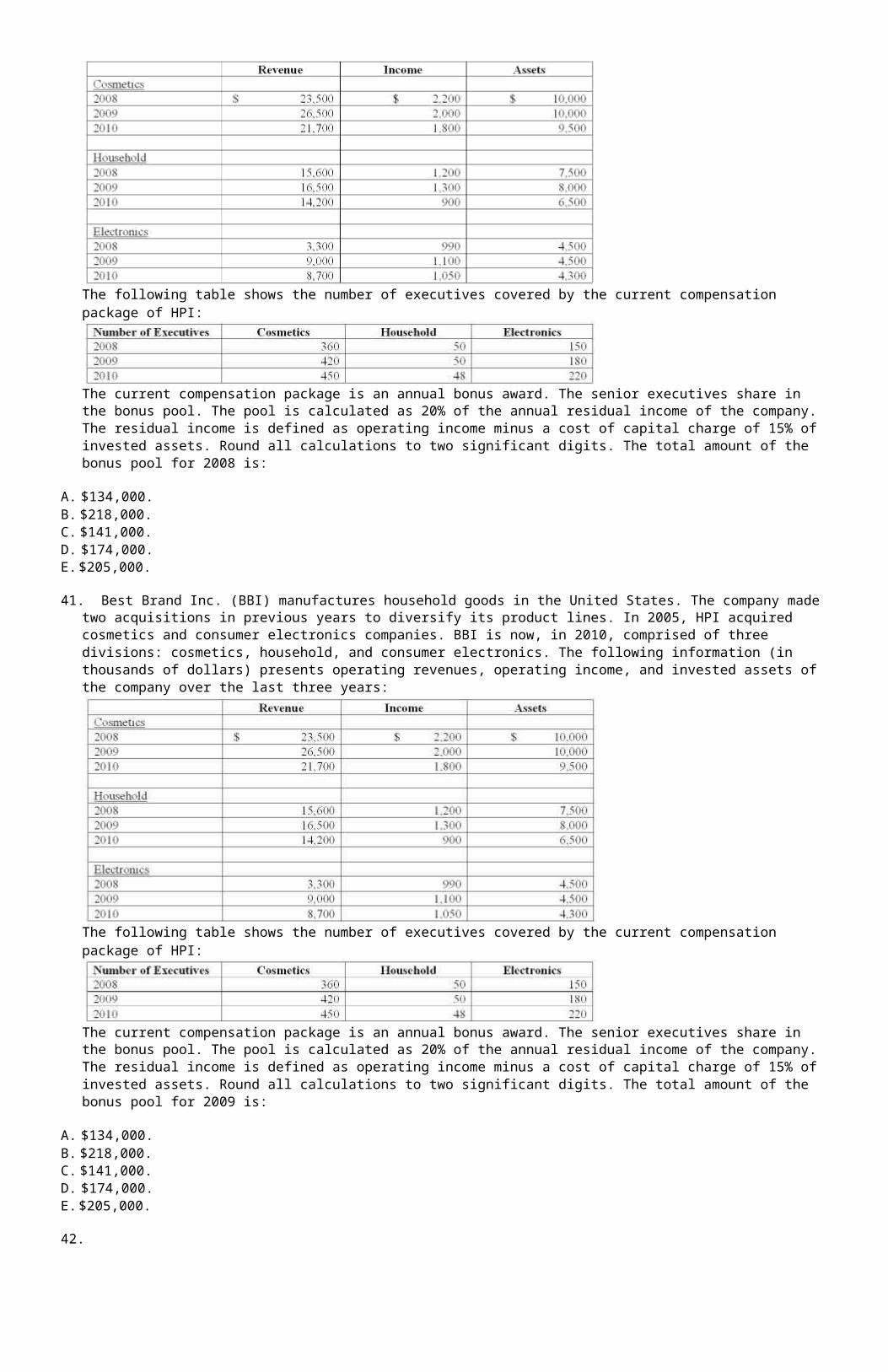

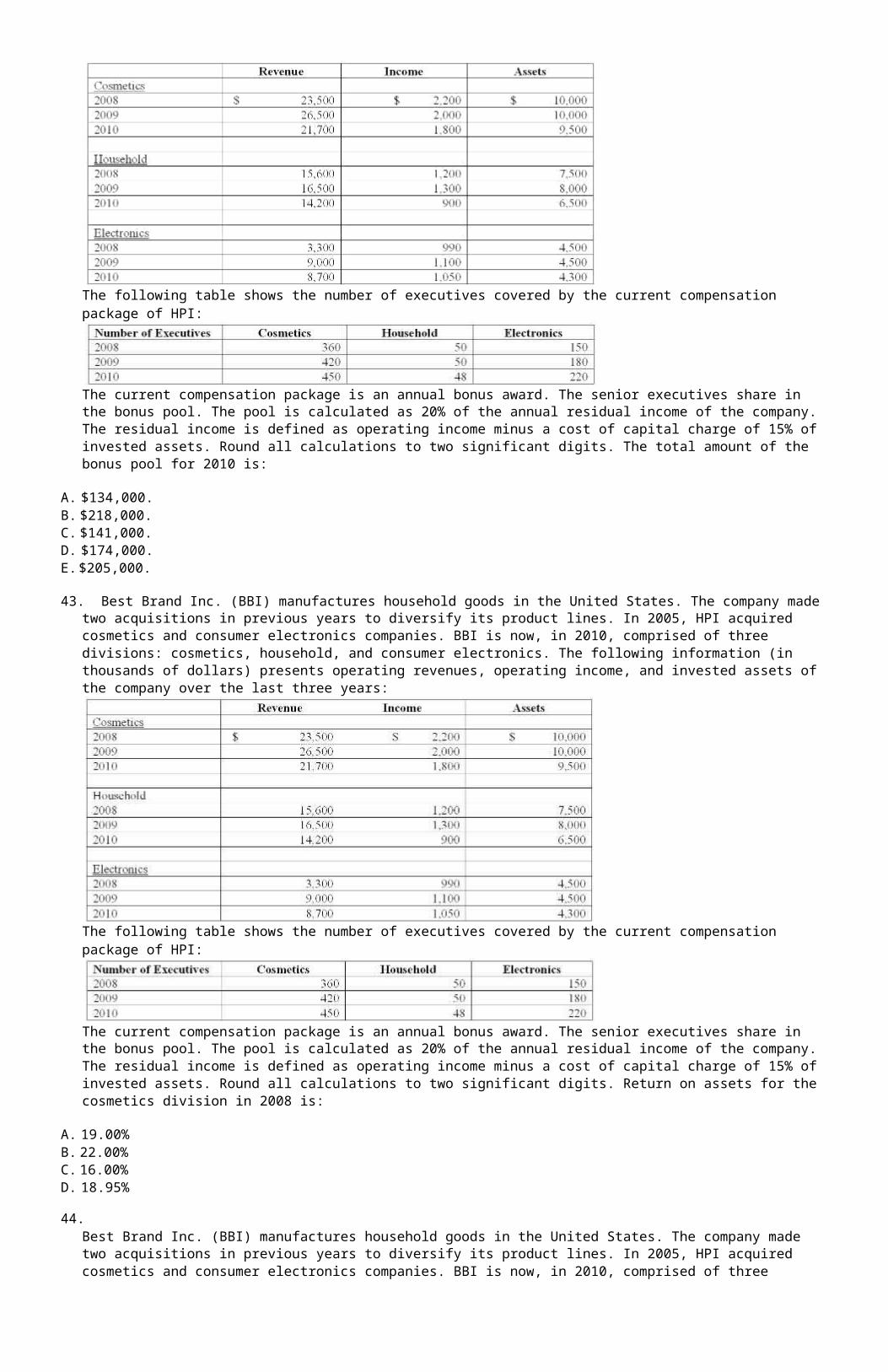

Best Brand Inc. (BBI) manufactures household goods in the United States. The company made two acquisitions in previous years to diversify its product lines. In 2005, HPI acquired cosmetics and consumer electronics companies. BBI is now, in 2010, comprised of three divisions: cosmetics, household, and consumer electronics. The following information (in thousands of dollars) presents operating revenues, operating income, and invested assets of the company over the last three years:

The following table shows the number of executives covered by the current compensation package of HPI:

The current compensation package is an annual bonus award. The senior executives share in the bonus pool. The pool is calculated as 20% of the annual residual income of the company. The residual income is defined as operating income minus a cost of capital charge of 15% of invested assets. Round all calculations to two significant digits. The total amount of the bonus pool for 2008 is:

A. $134,000. B. $218,000. C. $141,000. D. $174,000. E. $205,000.

41. Best Brand Inc. (BBI) manufactures household goods in the United States. The company made two acquisitions in previous years to diversify its product lines. In 2005, HPI acquired cosmetics and consumer electronics companies. BBI is now, in 2010, comprised of three divisions: cosmetics, household, and consumer electronics. The following information (in thousands of dollars) presents operating revenues, operating income, and invested assets of the company over the last three years:

The following table shows the number of executives covered by the current compensation package of HPI:

The current compensation package is an annual bonus award. The senior executives share in the bonus pool. The pool is calculated as 20% of the annual residual income of the company. The residual income is defined as operating income minus a cost of capital charge of 15% of invested assets. Round all calculations to two significant digits. The total amount of the bonus pool for 2009 is:

A. $134,000. B. $218,000. C. $141,000. D. $174,000. E. $205,000.

42.

Best Brand Inc. (BBI) manufactures household goods in the United States. The company made two acquisitions in previous years to diversify its product lines. In 2005, HPI acquired cosmetics and consumer electronics companies. BBI is now, in 2010, comprised of three divisions: cosmetics, household, and consumer electronics. The following information (in thousands of dollars) presents operating revenues, operating income, and invested assets of the company over the last three years:

The following table shows the number of executives covered by the current compensation package of HPI:

The current compensation package is an annual bonus award. The senior executives share in the bonus pool. The pool is calculated as 20% of the annual residual income of the company. The residual income is defined as operating income minus a cost of capital charge of 15% of invested assets. Round all calculations to two significant digits. The total amount of the bonus pool for 2010 is:

A. $134,000. B. $218,000. C. $141,000. D. $174,000. E. $205,000.

43. Best Brand Inc. (BBI) manufactures household goods in the United States. The company made two acquisitions in previous years to diversify its product lines. In 2005, HPI acquired cosmetics and consumer electronics companies. BBI is now, in 2010, comprised of three divisions: cosmetics, household, and consumer electronics. The following information (in thousands of dollars) presents operating revenues, operating income, and invested assets of the company over the last three years:

The following table shows the number of executives covered by the current compensation package of HPI:

The current compensation package is an annual bonus award. The senior executives share in the bonus pool. The pool is calculated as 20% of the annual residual income of the company. The residual income is defined as operating income minus a cost of capital charge of 15% of invested assets. Round all calculations to two significant digits. Return on assets for the cosmetics division in 2008 is:

A. 19.00% B. 22.00% C. 16.00% D. 18.95%

44.Best Brand Inc. (BBI) manufactures household goods in the United States. The company made two acquisitions in previous years to diversify its product lines. In 2005, HPI acquired cosmetics and consumer electronics companies. BBI is now, in 2010, comprised of three divisions: cosmetics, household, and consumer electronics. The following information (in thousands of dollars) presents operating revenues, operating income, and invested assets of the company over the last three years:

The following table shows the number of executives covered by the current compensation package of HPI:

The current compensation package is an annual bonus award. The senior executives share in the bonus pool. The pool is calculated as 20% of the annual residual income of the company. The residual income is defined as operating income minus a cost of capital charge of 15% of invested assets. Round all calculations to two significant digits. Return on sales in the household division in 2009 is (rounded):

A. 6.34% B. 7.69% C. 7.88% D. 8.54%

45. Best Brand Inc. (BBI) manufactures household goods in the United States. The company made two acquisitions in previous years to diversify its product lines. In 2005, HPI acquired cosmetics and consumer electronics companies. BBI is now, in 2010, comprised of three divisions: cosmetics, household, and consumer electronics. The following information (in thousands of dollars) presents operating revenues, operating income, and invested assets of the company over the last three years:

The following table shows the number of executives covered by the current compensation package of HPI:

The current compensation package is an annual bonus award. The senior executives share in the bonus pool. The pool is calculated as 20% of the annual residual income of the company. The residual income is defined as operating income minus a cost of capital charge of 15% of invested assets. Round all calculations to two significant digits. Asset turnover in the electronics division in 2010 is (rounded):

A. 1.82 B. 2.02 C. .733 D. 2.31

46. An increase in the market price of a company's common stock will immediately affect its:

A. Stock return. B. Debt to equity ratio. C. Earnings per share. D. Economic value added. E. Return on common stockholders' equity.

47. Compensation plans for high-level managers and executives are usually explained in the firm's:

A. Management Discussion and Analysis (MD&A). B. Income Statement. C. Notes to the Financial Statements. D. Proxy Statement.

48. In service firms, financial results can be measured by all the following except:

A. Staff utilization. B. The profit multiplier. C. Collections of accounts. D. Throughput.

49. Which of the following aspects would not play a strategic role in management compensation?

A. Ethical issues. B. Strategic conditions facing the firm. C. The effect of comparable positions within the industry. D. The effect of risk aversion on managers' decision making.

50. Which one of the following has been the most common payment option for bonus compensation in recent years?

A. Vacation time. B. Stock options. C. Increased benefits. D. Salary increase.

51. Common bases of bonus compensation include:

A. A B. B C. C D. D E. E

52. Which of the following would explain why a manager would elect to defer bonus compensation to future years?

A. Interest rates are expected to decrease. B. The firm will be issuing an initial public offering in the near future. C. To show dedication to the company. D. To avoid or defer taxes.

53. Firms typically provide benefits (perks) to employees to enhance motivation. Which of the following would not be an example of a perk?

A. Company car. B. Country club membership. C. Stock options. D. Executive life insurance.

54. The commonly used approaches for business valuation include:

A. A B. B C. C D. D E. E

55. Which of the following is a liquidity ratio?

A. Gross margin ratio. B. Return on Assets ratio. C. Quick ratio. D. Earnings per share.

56. EVA is the acronym for:

A. Extra Value Assets. B. Economic Volume Analysis. C. Efficiency Volume Analysis. D. Economic Value Added.

57. EVA is calculated as:

A. EVA Net Income - (Cost of Capital x EVA Invested Capital). B. Total Net Income - (Cost of Capital x Invested Capital). C. Gross Income - Cost of Capital. D. Total Net Income - EVA Net Income. E. Accounting earnings adjusted for EVA.

58. Methods for directly valuing a firm include:

A. A B. B C. C D. D E. E

59. There is a common concern today that executive compensation in the U. S. is:

A. Not adequately linked to strategic performance measures B. Ineffective as a performance incentive C. Not properly disclosed to the IRS D. Varies too greatly from industry to industry

60. Salary is:

A. A fixed payment that includes a bonus. B. A fixed payment that includes benefits. C. A benefit that includes a bonus. D. A fixed payment.

61. Economic value added is calculated from:

A. Average total assets, current liabilities, net income, and the cost of capital. B. EVA net income and EVA invested capital. C. Net income, cost of capital, and net assets. D. Net income and the cost of capital. E. EVA net income, the cost of capital, and EVA invested capital.

62. Performance shares grant stock for achieving certain performance goals:

A. In the following year. B. In two years or more. C. In the current period. D. When stock prices improve.

63. There is a current tax deduction for the firm for which of the following types of compensation?

A. Qualified stock options. B. Nonqualified stock options. C. Deferred bonus. D. Current bonus. E. Performance shares.

64. There is a current tax for the manager when which of the following types of compensation is received?

A. Qualified stock options B. Nonqualified stock options C. Deferred bonus D. Current bonus E. Performance shares

65. Which of the following types of compensation does not provide a deduction to the firm for tax purposes?

A. Perks B. Qualified stock options C. Retirement plans D. Current bonus E. Performance shares

66. Bonus payment options include all of the following except:

A. Perks. B. Current bonus. C. Deferred bonus. D. Stock options. E. Performance shares.

67. A CFO whose compensation plan may have had the effect of creating an incentive for unethical actions includes:

A. Kenneth Lay B. Scott Sullivan C. Bernie Madoff D. Dennis Kozlowski

68.

The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The accounts receivable turnover ratio for 2010 is:

A. 11.2 B. 12.7 C. 13.7 D. 14.9

69. The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The inventory turnover ratio for 2010 is (rounded):

A. 11.2 B. 12.7 C. 13.7 D. 14.9

70.

The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The current ratio for 2010 is:

A. 1.8 B. 2.0 C. 3.9 D. 4.7

71. The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The gross margin percentage for 2010 is (rounded):

A. 11.2% B. 12.7% C. 13.7% D. 14.9%

72.

The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

Return on assets for 2010 is:

A. 9.2% B. 16.4% C. 13.7% D. 19.2%

73. The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

Return on equity for 2010 is (rounded):

A. 11.6% B. 14.6% C. 15.5% D. 18.9%

74.

The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The value of the company, calculated using the earnings multiple for 2010 is:

A. $1,220,000 B. $1,620,000 C. $2,520,000 D. $8,335,000

75. The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The value of the company, calculated using the free cash flow multiple for 2010 is:

A. $1,220,000 B. $1,620,000 C. $2,520,000 D. $8,400,000

76.

The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The value of the company, calculated using the sales multiple for 2010 is:

A. $1,220,000 B. $1,620,000 C. $2,520,000 D. $8,400,000 E. $7,125,000

77. The King Mattress Company had the following operating results for 2009-2010. In addition, the company paid dividends in both 2009 and 2010 of $60,000 per year and made capital expenditures in both years of $30,000 per year. The company's stock price in 2009 was $8 and $7 in 2010. The industry average earnings multiple for the mattress industry was 9 in 2010 and the free cash flow and sales multiples were 18 and 1.5, respectively. The company is publicly owned and has 1,200,000 shares of outstanding stock at the end of 2010.

The market value of the company's equity for 2011 is:

A. $1,220,000 B. $1,620,000 C. $2,520,000 D. $8,400,000 E. $7,125,000

78.

Cost Allocation and Compensation Performance of divisional managers at Leakproof Faucet Corporation is judged by an evaluation ofthe operating incomes of the divisions. Abbreviated income statements for the year ending 2010 are shown below for the three divisions of Leakproof Faucet Corp:

* Total Corporate Overhead is allocated to each division based on the division's proportion of total revenues. The manager of the Newton division, through increases in manufacturing efficiency, created some additional capacity in 2010. The only way he could have utilized this capacity would have been to manufacture a model J-5 faucet, which would have had the following impact on the Newton division: Increase in annual revenues (in thousands) of $750. Increase in cost of goods sold of $600. Increase in divisional overhead of $100. Mr. Garrett, the Newton division manager, chose not to manufacture the J-5 faucets; therefore, the additional capacity went unused. Required: (1) Prepare revised income statements for the three divisions for 2010 assuming that Mr. Garrett had chosen instead to utilizethe additional capacity to manufacture the model J-5. (2) Calculate the contribution margin of the Newton division if J-5 is manufactured and if it is not manufactured. (3) Why did Mr. Garrett choose not to manufacture the J-5? (4) Would Leakproof Faucets have benefited from the manufacture of the J-5? (5) Identify an advantage and a disadvantage of not allocating any corporate overhead to the divisions.

79. Choosing Between Incentive PlansBrogdon is a ski instructor looking for employment in the Oregon mountains. He has received full-time job offers from two ski lodges, and must choose between them. The two jobs seem equally attractive, so Brogdon wants to choose the lodge which will pay him the higher compensation. Running Elk Lodge offers a wage of $8.00 per hour for a 40 hour week, plus 30% of the fees paid by walk-on pupils desiring private lessons, plus 40% of fees from pupils who specifically request a private lesson from Brogdon. Blustery Ridge Lodge offers a wage of only $6.00 per hour, plus 25% of walk-on private fees, 45% of request private fees, and 15% of the fees paid by walk-on groups. Both lodges charge skiers $50 for private lessons and $100 per 5-person group for group lessons. Brogdon's previous experience leads him to expect weekly volume of 15 walk-on privates, 6 request privates, and 20 walk-on groups. Required: Which job should Brogdon accept? What factors should Brogdon consider in making his choice?

80. Compensation; Review of Chapter 19 Products Inc. manufactures furniture and is organized into three large divisions: bedroom, livingroom, and dining room furniture. The following information presents operating revenues, operating incomes and invested assets of the company over the last three years. (all figures in 000s)

The following table shows the number of managers covered by the current compensation package of Products Inc.:

The current compensation package is an annual bonus award. The managers share in the bonus pool. The pool is calculated as 12% of the annual residual income of the company. The residual income is defined as operating income minus an interest charge of 15% of invested assets. Required: (1) Use investment turnover, return on sales, and ROI to explain the differences in profitability of the three divisions.(2) Compute the bonus amount to be paid during each year. Also, compute the (average) individual executive bonus amounts. (3) If the bonus were calculated by divisional residual income what would be the bonus amounts (4) Discuss the benefits and problems of basing the bonus on residual income of a company compared to using divisional residual income.

81. Choosing Bonus Plans Mobile Business Incorporated (MBI) is a worldwide manufacturing company that specializes in high technologyproducts for the aerospace, automotive and plastics industries. The state-of-the-art technology and business innovation have been key to MBI's success over the last ten years. After a meeting of the board of directors, there was some feeling that the company was moving away from its goal of striving to maintain and expand its global position through innovative management teams. One area of concern was with the company's bonus compensation package. The company's current bonus plan focuses on giving reward based on the utilization of capital within the company, i.e. management of inventory, collection of receivables and use of physical assets. Even with such a state-of-the-art bonus plan, the board of directors is concerned with the short-term focus of the compensation package. MBI's basis in current financial standards suggests that the future period consequences of managerial actions will not be reflected when presenting bonus compensation. Required: Help MBI solve the problem of basing bonuses on short-term decisions. Develop a bonus package that takes into consideration the long-term financial position of MBI.

82. Evaluating an Incentive SystemHarold Small joined Morton Electric Company eight months ago as Vice President of PersonnelAdministration. Morton Electric Company is a small regional public utility serving 50,000 customers in three communities and the surrounding rural area. Electricity is generated at a central plant, but each community has a substation and its own work crew. The total labor force at the central plant and three substations, exclusive of administrative and clerical personnel, numbers 180 people. Small designed and introduced a Performance Evaluation and Review System (PERS) shortly after joining Morton. This system was based upon a similar system he had developed and administered in his prior position with a small company. He thought the system had worked well and that it could be easily adapted for use at Morton. The purpose of PERS, as conceived by Small, is to provide a positive feedback system for evaluating employees that would be uniform for each class of employees. Thus, the system would indicate to employees how they were performing on the job and help them correct any shortcomings. The Plant Supervisors and Field Supervisors are responsible for administering the system for the plant workers and the substation crew workers respectively. The General Supervisors are responsible for the Plant/Field Supervisors. Employees get personal PERS Reports monthly informing them of their current status, and there is a review and evaluation every six months. PERS is based on a point system in an attempt to make it uniform for all workers. There are eight categories for evaluation with a maximum number of points for each category and a total of 100 points for the system. The eight categories for the plant and crew workers and the maximum number of points in each category are as follows.

The list of categories used to evaluate the Plant/Field Supervisors is slightly different. Each employee begins the year with 100 points. If an infraction in any of the categories is observed, one to five penalty points can be assessed for each infraction. Notification is given to the employee indicating the infraction and the points to be deducted. A worker who is assessed 25 points in any one month or loses all the points in any category in one month is subject to immediate review. Likewise, anytime an employee drops below 40 points, a review is scheduled. The General Supervisor meets with the individual employee and the employee's Plant/Field Supervisor at this review. If an employee has no infractions during the month, up to 12 points can be restored to the employee's point total - two points each for Categories 1-4 and one point each for Categories 5-8. However, at no time can a worker have more than the maximum allowed in each category or more than 100 points in total. When Small first introduced PERS to the General Supervisors, they were not sure they liked the system. Small told them how well it had worked where he had used it before. Small's enthusiasm for the system and his likeable personality convinced the General Supervisors that the system had merit. There were a few isolated problems with the system in the first two months. However, Ray Meyers, a crew worker, is very unhappy with the new system as evidenced by his conversation with Dan Jenkins, a fellow crew worker. Meyers: "Look at this notice of infraction - I have lost 22 points! I can't believe it!" Jenkins: "How did your supervisor get you for that many points in such a short period?" Required: (1) What are the strengths and weaknesses of the Performance Evaluation and Review system (PERS) in terms of the design for a review and evaluation system and for the expected motivational effects? (2) What problems might occur in the administration of the PERS system?

83. Business Analysis Avantronics is a manufacturer of electronic components and accessories with total assets of $20,000,000. Selectedfinancial ratios for Avantronics and the industry averages for firms of similar size are presented below.

Avantronics is being reviewed by several entities whose interests vary, and the company's financial ratios are a part of the data being considered. Each of the parties listed below must recommend an action based on its evaluation of Avantronics' financial position. • Mid Coastal Bank. The bank is processing Avantronic's application for the new five-year term note. MidCoastal has been Avantronics' banker for several years, but must re-evaluate the company's financial position for each major transaction. • Ozawa Company. Ozawa is a new supplier to Avantronics, and must decide on the appropriate credit terms to extend to the company. • Drucker&Denon. A brokerage firm specializing in the stock of electronics firms that are sold over-the- counter, Drucker&Denon must decide if it will include Avantronics in a new fund being established for sale to Drucker&Denon's clients. • Working Capital Management Committee. This is a committee of

Avantronics' management personnel chaired by the chief operating officer. The committee is charged with the responsibility of periodically reviewing the company's working capital position, comparing actual data against budgets, and recommending changes in strategy as needed. Required: (1) Describe the analytical use of each of the four ratios presented above. (2) For each of the four entities described above, identify one or two financial ratios, from those ratios presented, that would be most valuable as a basis for its decision regarding Avantronics.(3) Discuss what the financial ratios presented in the question reveal about Avantronics. Support your answer by citing specific ratio levels and trends as well as the interrelationships between these ratios.

84. Wilson & Associates is a medium-size marketing organization specializing in professional promotion and publicity services. The firm's top management believes that it provides quality service as evidenced by the high level of customer satisfaction. The organization consists of three departments: print media, audio media, and visual media, each of which has a senior director in charge. The company employs 80 clerical staff who are paid on an hourly basis and 30 professional staff who are salaried. A large majority of the employees have an excellent rating in their job skills, and all employees demonstrate above average performance in their job responsibilities. The employees take pride in their achievements, and morale is very good. Salary ranges are established for different job classifications within the clerical staff (i.e., clerk, clerk typist, secretary, and administrative assistant) and the professional staff (i.e., analyst, manager, and director). A fixed-rate structure is used for all salaries. The company offers no commissions because it does not want its professional staff applying undue sales pressure on its customers. Company management is proud that it does not have to resort to a salary plus commission structure for its professionals to generate sales. Employees are recognized for superior performances through salary increases and promotions. Management believes that salary increases should be based on merit, and open positions are filled from within whenever possible. Top management contends that highly skilled and motivated employees will improve productivity it they are rewarded with annual merit pay raises and if promotions are based on performance. Top management announced in November that the amount available for pay increases would be 10 percent of the actual total salary expenditures for 2011. All salary increases would be effective January 1, 2010. The print media department consists of 20 clerical and eight professional employees on January 1, 2011. Six clerical employees were added during the year at the rate of about one every two months. Two professionals were added, one on March 1 and one on August 1. Three employees were promoted during the year: two secretaries to administrative assistants and one manager to director. The total actual salary expense for the department without regard for employee benefits and employer tax contributions was $548,000. Therefore, the total amount allocated for wage increases for the print media department in 2010 is designated to be $54,800. Shortly after the merit pay program was announced, the print media department employees received their year-end evaluation conducted by the employee's supervisor. The senior director met with each supervisor and received all performance reports and then announced the merit pay increase for each employee. Upon completion of this entire process, several employees complained individually about the inequities of the merit pay program. The senior director was concerned about the employee discontent because the people complaining were some of the highest achievers on the staff. They tended to be at the lower classification levels and were relatively new employees, having been with the company for one to two years. The individuals showed potential and were highly motivated, often working extra hours and assuming additional responsibilities. The new employees' behavior differed slightly from the employees who had been with the department for a longer period of time. Although highly skilled and competent in their jobs, the veteran employees tended to be reluctant to accept additional responsibility or to work extra hours on a regular basis. Required: 1) Review Wilson and Associates' wage and compensation plan. a. Identify and discuss the general strength of the wage and compensation plan. b. Identify and explain the shortcomings in the administration of the merit pay increases that are to become effective in 2010, and discuss what effect these shortcomings could have on the group of discontent employees in the print media department. 2) Explain how this compensation program should be revised, if at all.

85. Topaz Industries operates several large plants that provide the packaging for many consumer products. The company has a progressive compensation system that is market-based and competitive with that of similar companies. Every position within Topaz is assigned a grade level from 1 to 30, with 30 being the company's chairman and 1 the lowest-level unskilled position. In assigning the grade levels, Topaz uses the following methodology: 1. The higher-level positions are classified according to the exact titles used by similar firms. 2. The lower-level positions are classified on the following factors: a. Formal education attained. b. Amount of responsibility. c. Complexity of tasks. d. Effects of mistakes. e. Physical difficulty or amount of effort. 3. Salary ranges increase annually according to the rate of inflation. When Topaz hires employees, they are generally offered a starting salary at the lower end of the position grade level. For an individual with exceptional skills or experience, the offer could be closer to the top of the level. Employees can move through the levels on the basis of performance and merit increases; a promotion moves the employee into a new position level with a higher salary range. Topaz provides various in-house educational programs for its employees and has a tuition reimbursement program. Jill Simon, assistant controller for one of Topaz's plants, was hired a year ago at the top level for her position because of her extensive experience in the field. She has just learned that her annual increase will be 3 percent of her salary, the same percentage used to increase all position levels in the current year. Jill believes that her performance merits a larger increase but knows that as long as she remains an assistant controller at the top level, her future salary increases will be similar. Jon Russell is an administrative secretary reporting to Topaz's treasurer. Jon has been with the company for several years, earning his current position two years ago through above-average performance. Because Jon has proved to be reliable and efficient, his boss has transferred responsibility for many routine tasks to him. Jon believes that his position should be reevaluated because of these increased duties, but he has not received any encouragement from his boss concerning this. Billy Hampton was recently promoted to supervisor in one of the packaging plants, directing the work of 15 employees. He started at Topaz as a shipping clerk after completing high school and has learned the packaging business on the job by holding increasingly important positions over the years. Many of Billy's co-supervisors are better educated than he is, but lack his experience and frequently turn to him for solutions to their problems. Billy knows that these less-experienced supervisors earn more than he does because of their educational qualifications. Although he is confident that his salary will catch up with the others through merit increases, he does not believe that the company has been entirely fair with him. Required: 1) Describe the incentive effects that Topaz Industries' job evaluation and compensation program is likely to have on JillSimon, Jon Russell, and Billy Hampton. 2) Recommend several ways that the firm could improve its evaluation and compensation program to avoid situations similar to those described here. 3) Describe the general conditions that must be present for employees to be motivated to improve their performance under a merit pay system.

86. Boating Inc. manufactures water vessels and is organized into three large divisions: jet skis, fishing boats and yachts. The following information presents operating revenues, operating incomes and invested assets of the company over the last three years:

(All figures in 000s.)

The following table shows the number of managers covered by the current compensation package of Boating Inc.:

The current compensation package is an annual bonus award. The managers share in the bonus pool. The pool is calculated as 10% of the annual residual income of the company. The residual income is defined as operating income minus an interest charge of 14% of invested assets. Required: (1) Compute the bonus amount to be paid during each year. Also, compute the (average) individual executive bonus amounts. (2) If the bonus was calculated by divisional residual income, what would be the bonus amounts?

87.

Ginyard Company has the following financial statements for the year ended December 31, 2010.

Some additional information about 2010 includes:

Required: 1. Complete a business analysis of Ginyard Company for 2010. 2. Complete a business valuation for Ginyard Company for2010.

88. Jackson Manufacturing has the following operating results for 2010.

In addition, the company paid dividends in both 2009 and 2010 of $100,000 per year and made capital expenditures in both years of $45,000 per year. The company's stock price in 2009 was $10 and $12 in 2010. The industry average earnings multiple for the industry was 10 in 2010 and the free cash flow and sales multiples were 20 and 2, respectively. The company is publicly owned and has 1,050,000 shares of outstanding stock at the end of 2010. The industry average ratios for Jackson's industry were as follows in the most recent year. Exhibit A: Industry Ratios for the Jackson Company

Required: 1. Calculate the ratios In Exhibit A for Jackson Company for 2010, group them by category (liquidity, profitability) anddevelop a brief overview for the liquidity and profitability of the Jackson Company at the end of 2010. 2. Complete a Business Valuation for the Jackson Company based on 2010 financial statement information.