Air Lease Corporation · ALC is one of the premier aircraft lessors in the marketplace ... plus...

33

Air Lease Corporation Q2 2017 Investor Presentation

-

Upload

truongdang -

Category

Documents

-

view

215 -

download

0

Transcript of Air Lease Corporation · ALC is one of the premier aircraft lessors in the marketplace ... plus...

Air Lease Corporation

Q2 2017 Investor Presentation

Forward Looking Statements & Non-GAAP Measures

Statements in this presentation that are not historical facts are hereby identified as “forward-looking statements,” including any statements about our expectations, beliefs, plans, predictions, forecasts, objectives, assumptions or future events or performance that are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends” and similar words or phrases. Accordingly, these statements are only predictions and involve estimates, known and unknown risks, assumptions and uncertainties that could cause actual results to differ materially from those expressed in them. We wish to caution you that our actual results could differ materially from those anticipated in such forward-looking statements as a result of several factors, including the following:

• our inability to make acquisitions of, or lease, aircraft on favorable terms; • our inability to sell aircraft on favorable terms; • our inability to obtain additional financing on favorable terms, if required, to complete the acquisition of sufficient aircraft as currently contemplated or to

fund the operations and growth of our business; • our inability to obtain refinancing prior to the time our debt matures; • impaired financial condition and liquidity of our lessees; • deterioration of economic conditions in the commercial aviation industry generally; • increased maintenance, operating or other expenses or changes in the timing thereof; • changes in the regulatory environment; and • potential natural disasters and terrorist attacks and the amount of our insurance coverage, if any, relating thereto. We also refer you to the documents the Company files from time to time with the Securities and Exchange Commission (“SEC”), specifically the Company’s

Annual Report on Form 10-K for the year ended December 31, 2016, which contains and identifies important factors that could cause the actual results for the Company on a consolidated basis to differ materially from expectations and any subsequent documents the Company files with the SEC. All forward-looking statements are necessarily only estimates of future results, and there can be no assurance that actual results will not differ materially from expectations, and, therefore, you are cautioned not to place undue reliance on such statements. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. If any such risks or uncertainties develop, our business, results of operation and financial condition could be adversely affected. You may obtain copies of the Company’s most recent Annual Report on Form 10-K and the other documents it files with the SEC for free by visiting EDGAR on the SEC website at www.sec.gov.

In addition to financial results prepared in accordance with U.S. generally accepted accounting principles, or GAAP, this presentation contains certain non-GAAP financial measures. Management believes that in addition to using GAAP results in evaluating our business, it can also be useful to measure results using certain non-GAAP financial measures. Investors and potential investors are encouraged to review the reconciliation of non-GAAP financial measures with their most direct comparable GAAP financial results set forth in the Appendix section.

2

ALC is one of the premier aircraft lessors in the marketplace

One of the world’s largest customers for new commercial jet aircraft

Globally diversified customer base

Positive long term industry fundamentals for growth and replacement of aging aircraft

Strong funding profile and credit metrics

Highest rated standalone aircraft lessor

Executive Summary

3

Ended the second quarter with $12.7 billion1 in aircraft after adding 14 aircraft with a cost of $637 million

• Young aircraft (3.6 years2) on long leases (6.9 years2) with a stable lease yield3

• Minimum future contracted rentals for our current and future fleet are $23.9 billion

• 90% of our order book placed on long-term leases for aircraft delivering through 2019

Expanded management business from 31 to 48 aircraft with the sale of 17 aircraft into Thunderbolt and Blackbird Capital I

• Also announced launch of Blackbird Capital II in August 2017

Entered into agreements with Boeing and Airbus to purchase 28 additional aircraft

Issued a total of $600 million senior unsecured notes at 2.625% in June 2017

Highlights for 2Q17

AIRCRAFT FLEET4

$12.7 billion1

240 owned / 48 managed

2Q17 REVENUES $381 million

+8.8% vs. 2Q16

2Q17 PRE-TAX PROFIT MARGIN

40.9%

PRE-TAX ROE5

17.3%

4

1 Aggregate fleet net book value

2 Weighted average age based on net book value of ALC owned fleet 3 Calculated as rental of flight equipment revenue, excluding overhaul revenue, divided by average net book value 4 As of June 30, 2017 5TTM ended June 30, 2017

Industry Update Industry Update

Air Lease Update

Portfolio Detail

Capital Structure

Summary

Appendix

Airline Productivity Measures

6

Growing, efficient and profitable utilization of fleets and capacity

Traffic: +7.9% 1st half of 2017

Load factors: ~81% globally

Aircraft utilization at ten year high

Stable aircraft demand environment

Profits: $36 billion in 2016

Parked fleet: ~3%1

Source: IATA June 2017, Boeing 2017 and Deutsche Bank Securities Inc. Research July 2017

1. Aircraft less than 20 years old

Historically, global airline traffic has doubled every 15 years and is projected to grow 5% annually over the next 5 years

Large airline fleet replacement cycle will benefit ALC’s business strategy

More than 95% of ALC’s customer base is outside of the United States1

North America Europe Asia/Pacific Latin America Middle East Africa World

3.5% 4.1%

6.4%

4.2%

5.7%

7.9%

4.9%

7

Global Market Outlook

Forecasted Passenger Volume CAGR by Major Region 2015-2020

Source: IATA October 2016 Economic Report 1 Based on each airline’s principal place of business

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Airline passenger traffic is the ultimate underlying demand for our aircraft

As long as passenger traffic is healthy, we believe there will be demand for the broadly operated aircraft models in our fleet

Resilient, Growing Market Expected to Continue

RPKs (trillions)

Gulf Crisis

Asian Crisis 9/11 SARS

Financial Crisis

4 Recessions

2 Financial crises

2 Gulf wars

1 Oil shock

1 Near pandemic (SARS)

9/11 Attack

Trend

Source: Boeing and ICAO scheduled traffic (September 2015) & IATA Jan 2017 Note: RPKs = Revenue Passenger Kilometers 8

2x

2x

Replacement Market Continues to Grow

ALC’s Target Replacement Market World’s Aging Fleet (Aircraft between 10-25 years over the next decade)

Airc

raft

9 Source: Ascend as of March 2017 and OEM literature

More than 40% of the world’s fleet is between 10-25 years of age

ALC’s target replacement market is aircraft over 10 years of age

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Current 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

8,307 9,045

9,738 10,510

11,378 12,221

12,958 13,555

14,220 15,327

16,471

Less than 10 10-25 25+

ALC estimates an industry capital requirement of $790 billion for new aircraft delivering between 2017 and 2021

10

Increasing Role of Leasing

Less Cash & Financing Required

Fleet Flexibility

Key Delivery Positions

Eliminate Residual Value Risk

Why Lease? Lessor Fleet Ownership

Source: Boeing; Data as of December 31, 2016

1970 1980 1990 2000 2016

17 leased

100 leased

9,771 leased

1,343 leased

3,715 leased

3,722 aircraft 6,037 aircraft 9,160 aircraft 15,032 aircraft 25,122 aircraft

14.7% 24.7%

~39%

1.7% 0.5%

Air Lease Update Industry Update

Air Lease Update

Portfolio Detail

Capital Structure

Summary

Appendix

2012 2013 2014 2015 2016 Q1 2017

$7.3

$9.2

$10.7

$12.4

$14.0$14.9

Consistent Asset Growth ($ in billions)

Fleet Count: 155 193 213

Solid Balance Sheet growth has supported consistent revenue growth

240

2012 2013 2014 2015

12

Q2 2017

240 237

2016

2012 2013 2014 2015 2016 Q2 2017

$4.3

$6.5

$8.6

$10.6

$12.3$13.3

Consistent Unencumbered Asset Growth ($ in billions)

We have focused on financing the business on an unsecured basis

We have grown our unencumbered assets1 to $13.3 billion, providing a solid foundation for our investment grade credit ratings

1 Comprised of unrestricted cash plus unencumbered flight equipment (calculated as flight equipment subject to operating leases less accumulated depreciation less net book value of aircraft pledged as collateral) plus deposits on flight equipment purchases plus certain other assets. 13

2012 2013 2014 2015 Q2 2017

2016

2012 2013 2014 2015 2016 Q2 2016 Q2 2017

$656

$859

$1,050

$1,223

$1,419

$350 $381

Consistent Revenue Growth ($ in millions)

The expansion of our fleet has driven consistent revenue growth and cash generation

Portfolio lease rates have remained consistent during this period

14

2012 2013 2014 2015 2016 Q2 2016 Q2 2017

2012 2013 2014 2015 2016 Q2 2016 Q2 2017

$253

$339

$439

$508

$623

$152 $167

Adjusted Net Income Before Income Taxes ($ in millions)

38.5

2.40

39.4

3.16

41.8

4.03

Reinvesting our earnings has built shareholders’ equity and strengthened our high quality balance sheet

Adj. margin before income taxes (%):

Adj. diluted EPS before income taxes ($):

15

41.7

4.64

2012 2013 2014 2015 2016

44.1

5.67

Adjusted Net Income Before Income Taxes, Adjusted Margin Before Income Taxes, and Adjusted Diluted Earnings Per Share Before Income Taxes are non-GAAP financial measures. See appendix for reconciliations to their most directly comparable GAAP measures.

Q2 2016 Q2 2017

43.9

1.51

43.7

1.39

2012 2013 2014 2015 2016 Q2 2017 LTM

11.2%

13.9%

16.6%17.5%

19.5%18.7%

Adjusted Return on Equity Before Income Taxes1

Strong adjusted ROE generated by the steady execution of our business strategy

16

2012 2013 2014 2015 2016

1 Adjusted Return on Equity Before Income Taxes is calculated as the trailing twelve month Adjusted Net Income Before Income Taxes divided by average shareholders’ equity. Adjusted Net Income Before Income Taxes is a non-GAAP financial measure. See appendix for a reconciliation to its most directly comparable GAAP measure.

Q2 2017 LTM

Portfolio Detail Industry Update

Air Lease Update

Portfolio Detail

Capital Structure

Summary

Appendix

ALC seeks to hold an aircraft for the first 1/3 of its useful life

ALC has a balanced asset mix

• Airframe manufacturers including Airbus and Boeing

• Engine manufacturers including General Electric, CFM, Pratt & Whitney, Rolls Royce, and

International Aero Engines

• Twin-aisle and single-aisle aircraft

ALC has a diversified global customer base with 88 airlines across 54 countries as of June 30, 2017

ALC closely monitors customer receivables to assure problems are proactively addressed

Staggered and balanced lease maturities by year

Flexibility in airframe purchase agreements

Portfolio Risk Management

18

Long term asset acquisition strategy focused on the most in demand, widely distributed, modern single- and twin-aisle commercial aircraft

19

Aircraft Strategy

737-800 & 737 MAX7/8/9

787-9/10 (787-10 Launch Customer)

A330-900NEO (Launch Customer)

A320/321/321LR/NEO (A321LRNEO Launch Customer)

A350-900/1000

The broad installed operator base of our aircraft assets are the basis of our asset liquidity

The lengthy manufacturer backlog increases the value of ALC’s order book

ALC Invests in the Most Liquid Aircraft Types

8.8 years 8.9 years 9.0 years

4.9 years

Bac

klog

2 O

pera

tors

1

343 482 42 70

A320 Family 737 Family A350 Family 787 Family

# To

tal I

n S

ervi

ce1

6,972 7,127 780* 1,069*

20

5.0 years

118

A330 Family

1,223

Source: 1 Ascend as of May 2017. 2 Airbus and Boeing published data 2017 (calculated as backlog divided by production rate). A320 and A350 backlog calculated using average of current and planned production rates. *In service and on order.

ALC’s management team has helped launch a number of aircraft types and associated engine designs

ALC is able to drive cost advantages by negotiating with manufacturers for high quality products and competitive pricing

Strength in Manufacturer Relationships

21

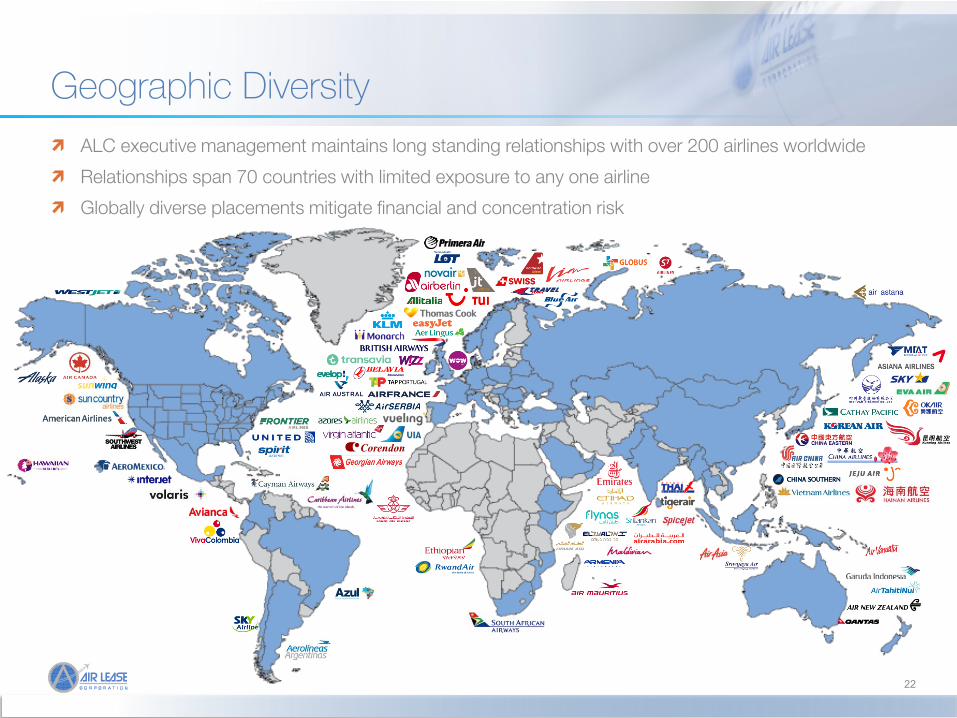

ALC executive management maintains long standing relationships with over 200 airlines worldwide

Relationships span 70 countries with limited exposure to any one airline

Globally diverse placements mitigate financial and concentration risk

Geographic Diversity

22

Europe, 33%

China, 21% Asia (ex. China),

21%

Middle East and Africa, 8%

Latin America, 8%

Pacific, Australia, New Zealand, 4% U.S. and

Canada, 5%

Boeing, 58% Airbus, 42%

Embraer, <1%

Single-Aisle, 78%

Twin-Aisle, 22%

Fleet Overview

240 owned aircraft and 48 managed aircraft

$12.7 billion aggregate fleet net book value

3.6 years weighted average fleet age2

6.9 years weighted average remaining lease term2

$23.9 billion in contracted minimum rentals

Diversified customer base with 88 airlines in 54

countries

1 As of June 30, 2017, except otherwise noted 2 Weighted average based on net book value of ALC’s owned fleet 3 Shown by net book value as of June 30, 2017, may not total to 100% due to rounding 4 Shown by number of aircraft as of June 30, 2017, may not total to 100% due to rounding

Region3

Manufacturers4 Aircraft Size4

23

Fleet Metrics1

2017 2018 2019 2020 2021 Therafter

5 17

32 26 22

44 7

5 5

5

5

2

4

2 7

9

2

12

26 28 35

27

3

7

12 9 7

8

Boeing 787-9/10

Boeing 737 Family

Airbus A350-900/1000

Airbus A330 Family

Airbus A320 Family

Order Book Provides Flexible Growth and a Strategic Advantage

We believe the order book is a source of value and provides visibility into the future and the opportunity to

double in size in 5 years

We believe our coveted delivery positions give us a competitive advantage with current and potential customers

ALC can exercise flexibility with delivery position commitments and timing

We typically place aircraft 18-36 months prior to delivery and currently are 90% placed through 2019

Scheduled Aircraft Deliveries1

46

Total Commitments

130

24

27

146

24 1 As of June 30, 2017

12

47

77 75 78

84

Capital Structure Industry Update

Air Lease Update

Portfolio Detail

Capital Structure

Summary

Appendix

Capital Structure & Financing Strategy

2

26

Capitalization – June 30, 2017

1

1 Calculated as: Contracted Minimum Lease Payments / Debt, as of June 30, 2017 2 Calculated as: (Net Flight Equipment – Undiscounted Contracted Minimum Lease Payments) / Equity, as of June 30, 2017

($mm) % of capitalizationUnrestricted cash $240 2%Total assets 14,861 116%

Unsecured debtSenior notes 6,920 54%Revolving credit facility 1,477 11%Term financings 214 2%Convertible senior notes 200 2%

Total unsecured debt 8,811 69%

Secured debtTerm financings 539 4%Export credit financing 48 0%

Total secured debt 588 5%

Less: debt discount (95)Total debt 9,303 72%

Shareholder's equity 3,558 28%

Total capitalization $12,862 100%

Selected credit metricsDebt/Equity 2.61xContracted Cash Flows/Debt1 105%Residual Fleet Value / Equity2 0.83xSecured Debt/Total Assets 4.0%Fixed Rate Debt/Debt 77.5%

Debt to Equity ratio

of 2.5:1

80/20 Fixed to Floating

debt ratio

90/10 Unsecured to Secured debt ratio

Balanced debt

maturity profile

Key Debt Portfolio Targets

Fleet comprised of young, high demand, technologically advanced aircraft with an average age of 3.6 years

Long weighted average remaining lease term of 6.9 years across the fleet

Diversified customer base of 88 airlines in 54 countries

Minimal lease expirations over the next few years $9.8 billion contracted minimum future rentals on our existing fleet

$14.1 billion committed rentals on our order book, for a total of $23.9 billion committed cash flows

Debt : Equity ratio of 2.6 : 1 Conservative debt maturity schedule 77.5% fixed rate debt Strong contracted cash flow coverage relative to debt outstanding at 105%1

Low residual value risk relative to equity at 0.83x2 Highly profitable – 43.9% adjusted margin before income taxes for Q2 20173

ALC Credit Highlights

Conservative Capital Structure

27

Data as of June 30, 2017, unless otherwise noted 1 Calculated as: Contracted Minimum Lease Payments / Debt, as of June 30, 2017 2Calculated as: (Net Flight Equipment – Undiscounted Minimum Lease Payments) / Equity, as of June 30, 2017 3Adjusted margin before income taxes is calculated as adjusted net income before income taxes divided by total revenues, excluding insurance recoveries. Adjusted

margin before income taxes is a non-GAAP financial measure. See appendix for reconciliation to its most directly comparable GAAP measure.

Strong Asset Base

A- Stable

BBB Stable

BBB Stable

Summary Industry Update

Air Lease Update

Portfolio Detail

Capital Structure

Summary

Appendix

Air Lease growth continues while maintaining a conservative capital structure and delivering strong returns to our shareholders

Air Lease Investment Highlights

Contracted Growth

Strong ROE

Conservative Capital

Structure

We believe our order book is a source of value and provides visibility into the future and the opportunity to double in size in 5 years

We have substantial forward cash flow visibility through our lease placements

We are 90% placed through 2019, and currently have $23.9 billion in committed rentals1

We have minimal lease expiries through the next several years, further enhancing visibility

We are focused on risk with no single customer greater than 10% of our revenue

We expect further benefits from operating leverage as our fleet grows

We expect to benefit through the refinancing of our remaining high yield debt with investment grade bonds

We expect additional profits from the growth of our management business

We have a strong balance sheet, with substantial liquidity of $2.5 billion

Low Debt/Equity target of 2.5x

Large unencumbered asset base $13.3 billion

77.5% fixed rate debt

Investment grade ratings from three agencies

29 1 Placements and committed rentals as of June 30, 2017 2 Values as of June 30, 2017

2

Appendix Industry Update

Air Lease Update

Portfolio Detail

Capital Structure

Summary

Appendix

Appendix – Non-GAAP Reconciliations

31

(in thousands, except share and per share data) Q2 2017 Q2 2016 2016 2015 2014 2013 2012

Reconciliation of net income to adjusted net incomebefore income taxes:

Net income 100,925$ 91,803$ 374,925$ 253,391$ 255,998$ 190,411$ 131,919$

Amortization of debt discounts and issuance costs 6,437 7,388 30,942 30,507 27,772 23,627 16,994

Stock-based compensation 5,304 4,501 16,941 17,022 16,048 21,614 31,688

Settlement - - - 72,000 - - -

Insurance recovery on settlement (950) (2,000) (5,250) (4,500) - - -

Provision for income taxes 54,944 50,468 205,313 139,562 138,778 103,031 72,054

Adjusted net income before income taxes 166,660$ 152,160$ 622,871$ 507,982$ 438,596$ 338,683$ 252,655$

Assumed conversion of convertible senior notes 1,431 1,455 5,780 5,806 5,811 5,783 5,627

Adjusted net income before income taxes plus assumed conversions 168,091$ 153,615$ 628,651$ 513,788$ 444,407$ 344,466$ 258,282$

Total revenues 380,957$ 350,139$ 1,419,055$ 1,222,840$ 1,050,493$ 858,675$ 655,746$

Weighted-average diluted shares outstanding 111,564,483 110,839,180 110,798,727 110,628,865 110,192,771 108,963,550 107,656,463

Adjusted margin before income taxes1 43.9% 43.7% 44.1% 41.7% 41.8% 39.4% 38.5%

Adjusted diluted earnings per share before income taxes 1.51$ 1.39$ 5.67$ 4.64$ 4.03$ 3.16$ 2.40$

Year Ended December 31,Three Months Ended

1 Adjusted margin before income taxes is adjusted net income before income taxes divided by total revenues, excluding insurance recoveries

Appendix – Non-GAAP Reconciliations

32

(in thousands, except share and per share data) Q2 2017 LTM 2016 2015 2014 2013 2012

Reconciliation of net income to adjusted net incomebefore income taxes:

Net income 376,126$ 374,925$ 253,391$ 255,998$ 190,411$ 131,919$

Amortization of debt discounts and issuance costs 31,822 30,942 30,507 27,772 23,627 16,994

Stock-based compensation 18,278 16,941 17,022 16,048 21,614 31,688

Settlement - - 72,000 - - -

Insurance recovery on settlement (950) (5,250) (4,500) - - -

Provision for income taxes 207,597 205,313 139,562 138,778 103,031 72,054

Adjusted net income before income taxes 632,873$ 622,871$ 507,982$ 438,596$ 338,683$ 252,655$

Average shareholders' equity 3,376,867$ 3,201,050$ 2,895,987$ 2,647,748$ 2,428,028$ 2,254,452$

Adjusted return on equity before income taxes 18.7% 19.5% 17.5% 16.6% 13.9% 11.2%

Year Ended December 31,

Appendix – Cash Flow Coverage Calculations

33

($ in billions) JUNE 30, 2017

Net Book Value of Aircraft A 12,743$

Minimum Future Lease Rentals from Operating Leases B 9,807$

Residual Exposure A - B 2,936$

Shareholders Equity C 3,558$

Residual Value Risk (A-B) / C 0.83x

Total Debt D 9,303$

Contracted Cash Flows / Debt B / D 105%