AHM Governance and Regulation

469

AHM 510 : Health Plans : Governance and Regulation AHM 510 Health Plans: Governance and Regulation Page 1 of 469

-

Upload

senthilj82 -

Category

Documents

-

view

51 -

download

6

Transcript of AHM Governance and Regulation

AHM 510 : Health Plans : Governance and Regulation

AHM 510 Health Plans: Governance and Regulation

Page 1 of 469

AHM 510 : Health Plans : Governance and Regulation

AHM 510: Syllabus

AHM 510 describes the formation, types, and structure of health plans. It also addresses the role of health plans in government-sponsored programs, the impact of fraud and abuse, how health plans make decisions about their purpose and overall direction, and the role of public policy in health plans today.

Assignment 1: Environmental ForcesReading A Environmental Forces

Assignment 2: Legal Organization of health plansReading A Legal Organization of health plans

Assignment 3: Formation and Structure of health plansReading A Corporate Restructuring and Corporate TransactionsReading B Health Plan Structures and Arrangements

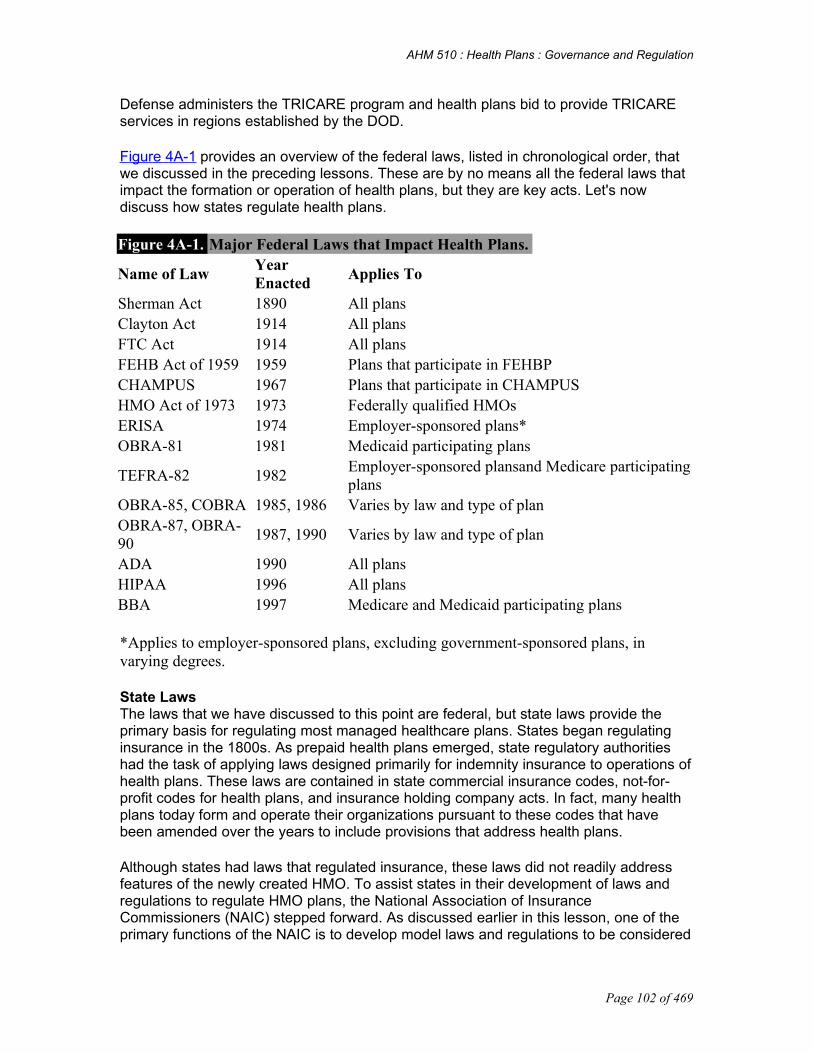

Assignment 4: Overview of Laws and RegulationsReading A Perspective and Overview of State and Federal LawsReading B Regulatory Agencies and health plan

Assignment 5: State Regulation of Health Plans: Part 1Reading A State HMO and Other Types of Health Plan LawsReading B State Mandates and Regulation of the Health Plan-Provider Relationship

Assignment 6: State Regulation of Health Plans: Part 2Reading A Other Laws That Apply to Health PlansReading B Workers' Compensation ProgramsReading C Pharmacy Laws and Legal IssuesReading D Market Conduct Examinations and Mechanisms for Enforcement

Assignment 7: Federal Regulation of Health PlansReading A Federal Regulation of Health PlansReading B Antitrust Concerns and Health PlansReading C ERISA and Health Plans

Assignment 8: Federal Government as PurchaserReading A Federal Government as Purchaser: Overview, TRICARE, and FEHBPReading B Medicare and Health PlansReading C Joint Federal-State Healthcare Programs (Medicaid, Programs of AllInclusive Care for the Elderly, and the State Children's Health Insurance Program)

Page 2 of 469

AHM 510 : Health Plans : Governance and Regulation

Assignment 9: Fraud and AbuseReading A Fraud and Abuse

Assignment 10: Governance: Structure and StrategyReading A The Components of Governance in a Health PlanReading B Strategic Planning in Health PlansReading C Key Strategic Issues for Health Plans

Assignment 11: Governance: Accountability and LeadershipReading A Governance: Accountability and Leadership

Assignment 12: Key Legal Issues in Health PlanReading A Key Legal Issues in Health Plan

Assignment 13: Public Policy and Changing EnvironmentReading A Public Policy from the Health Plan PerspectiveReading B Changing Environment and Emerging Trends in Health Plan Industry

Page 3 of 469

AHM 510 : Health Plans : Governance and Regulation

AHM 510: Course Objectives

This course describes the formation, types, and structure of MCOs. It addresses the role of health plans in government-sponsored pro-grams, the impact of fraud and abuse, how the purpose of an individual health plan is determined, and the role of public policy in the health plan industry. You will learn:

Assignment 1: Environmental Forces

Reading 1A: Environmental Forces

• Name and describe several major factors shaping the environment of health plans • Describe the players in health plan and how their interests affect the way they influence the healthcare environment • Explain the influences accreditation organizations and the media exert over the financing and delivery of healthcare • Describe several possible governance responses that health plans make to deal with their changing environment

Assignment 2: Legal Organization of Health Plans

Reading 2A: Legal Organization of Health Plans

• Explain the distinguishing features of a corporation and a limited liability company • Describe the key features and differences between a for-profit company and a not-for-profit company • Describe the differences between a publicly traded stock company and a privately held stock company • Describe the key features and differences between a stock company and a mutual company

Assignment 3: Formation and Structure of health plans

Reading 3A: Corporate Restructuring and Corporate Transactions

• Describe the options available to mutual companies seeking access to capital, strategic partnerships, and other corporate transactions • Describe the issues that a not-for-profit entity must address when converting to for-profit status or when engaging in other transactions with for-profit entities • Explain how health plans use reorganization and reengineering to improve performance • Distinguish between strategic partnerships, joint ventures, acquisitions, and mergers

Reading 3B: Health Plan Structures and Arrangements

• Identify and describe the various types of sponsors of health plans

Page 4 of 469

AHM 510 : Health Plans : Governance and Regulation

• Discuss the objectives of providers in health plan structures and arrangements • Discuss the impact of changes in health plan structures and arrangements on regulation • Differentiate between horizontal, vertical, and conglomerate integration • Differentiate between structural, virtual, and operational integration • Explain how strategic, marketplace, and regulatory issues can shape health plan structures and arrangements • Describe various arrangements employers use to provide healthcare benefit plans for their employees

Assignment 4: Overview of Laws and Regulations

Reading 4A: Perspective and Overview of State and Federal Laws

• Describe the sources of law in the United States • Explain the significance of the HMO Act of 1973 in the development of managed care • Name the federal laws that stimulated health plan participation in Medicare and Medicaid • Describe the provisions of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) of major interest to health plans • Describe the aspects of a health plan on which state regulations usually focus

Reading 4B: Regulatory Agencies and Health Plan

• Explain the role of HCFA in regulating healthcare • Describe the role of the Department of Labor in regulating health plans • Explain the methods states use to delegate regulatory authority for health plans to state agencies

Assignment 5: State Regulation of Health Plans: Part I

Reading 5A: State HMO and Other Types of Health Plan Laws

• Describe the major provisions of the NAIC HMO Model Act • Describe the types of state regulation that apply to PPO, URO, TPA, PSO, and POS products • Explain the need for the Risk-Based Capital for Health Organizations Model Act and the risk-based capital formula

Reading 5B: State Mandates and Regulation of the MCO-Provider Relationship

• Describe the difference between a mandated benefit and a mandated provider law • Give examples and explain the purpose of several mandated benefit laws • Describe the problems with applying any willing provider laws to certain types of health plans • Explain why state mandates often increase the cost of healthcare services provided by health plans

Page 5 of 469

AHM 510 : Health Plans : Governance and Regulation

Assignment 6: State Regulation of Health Plans: Part II

Reading 6A: Other Laws That Apply to Health Plans

• Describe the various types of state laws, other than HMO and insurance laws, that apply to health plan products • Explain how states regulate agent licensing, marketing activities, and advertising • Describe common types of general insurance laws that apply to health plans

Reading 6B: Workers' Compensation Programs

• Describe the kinds of benefits injured employees receive under workers' compensation • List several ways in which workers' compensation differs from other types of healthcare coverage • Describe how state laws can limit the use of health plan to provide workers' compensation benefits • Describe some of the common features of workers' compensation managed care plans • Describe the features of an integrated health and disability plan

Reading 6C: Pharmacy Laws and Legal Issues

• Describe the various types of open pharmacy laws • Describe how states regulate mail-order/ mail service pharmacy programs • Describe how states regulate use of formularies and generic substitution • Explain the benefit exclusions for an experimental drug, an investigational drug, and the off-label use of a drug • Describe how the Nonprofit Institutions Act applies to prescription drug pricing • Describe how states regulate an health plan's use of drug utilization review programs

Reading 6D: Market Conduct Examinations and Mechanisms for Enforcement

• List the operations that a state insurance department reviews in conducting a market conduct examination • Describe the enforcement mechanisms available to states to address violations of law

Assignment 7: Federal Regulation of Health Plans

Reading 7A: Federal Regulation of Health Plans

• Describe some of the operational and quality requirements that federally qualified HMOs must meet • Explain some of the administrative burdens that the Health Insurance Portability and Accountability Act of 1996 (HIPAA) imposes on health plans • Describe the general provisions of the Mental Health Parity Act of 1996 and the Newborns' and Mothers' Health Protection Act of 1996

Page 6 of 469

AHM 510 : Health Plans : Governance and Regulation

• Explain several typical applications to health plan of the Americans with Disabilities Act

Reading 7B: Antitrust Concerns and Health Plans

• Describe the three major federal laws that regulate business activities to prevent antitrust actions • Describe the difference between the per se rule and the rule of reason • Explain the applications of antitrust law in health plan-provider contracting • Explain the relevance of antitrust in mergers and acquisitions • Identify the issues that the 1994 DOJ and FTC guidelines addressed • Explain the procedures the DOJ and FTC follow for their enforcement proceedings

Reading 7C: ERISA and Health Plans

• Describe ERISA's documentation, reporting, and disclosure requirements • Describe the minimum standards of conduct (the fiduciary duties) applicable to ERISA plan fiduciaries • Describe the claims procedures required under ERISA and the standards of review that courts apply in deciding disputed claims • Describe how ERISA preemption has been applied by the courts to: utilization review and credentialing decisions made by health plans; mistaken verification of eligibility by an employer or health plan to a healthcare provider; entities that perform administrative functions under an ASO contract; and provider networks that contract to provide healthcare services to either health plans or self-funded employers on a capitated basis

Assignment 8: Federal Government as Purchaser

Reading 8A: Federal Government as Purchaser: Overview, TRICARE, and FEHBP

• Explain the government's dual role as purchaser and regulator of healthcare services • Describe the evolution of the military health services system from CHAMPUS to TRICARE, and describe TRICARE's triple benefit structure • List the primary features of the Federal Employees Health Benefits Program (FEHBP) • Describe how actions taken by the Office of Personnel Management (OPM) have a positive influence on FEHBP

Reading 8B: Medicare and health plan

• Describe the types of Medicare health plan contracts • Explain the certification process for a Medicare PSO • List the three ways that payment rates will be determined for health plans under Medicare + Choice • Explain how a Medicare Medical Savings Account works • Describe health plan contracting standards under the Medicare + Choice program

Page 7 of 469

AHM 510 : Health Plans : Governance and Regulation

• Provide examples of Medicare marketing restrictions

Reading 8C: Joint Federal-State Healthcare Programs

• Explain the roles of the federal and state governments in the operation of the Medicaid program • Describe the Medicaid services mandated by the federal government • Describe effects of the Balanced Budget Act 1997on regulation and operation of Medicaid managed care programs • Name the types of managed care entities that can contract to provide Medicaid services • Explain the purpose of Section 1915(b) and Section 1115 waivers • Explain how states can mandate Medicaid managed care without obtaining a waiver • Explain the role of Programs of All-Inclusive Care for the Elderly (PACE) • Discuss the purpose and options for implementation of the State Children's Health Insurance Program (SCHIP)

Assignment 9: Fraud and Abuse

Reading 9A: Fraud and Abuse

• Define the terms fraud and abuse • Describe how different types of compensation arrangements can lead to different kinds of fraud and abuse • List and describe the federal laws that regulate healthcare fraud and abuse, and identify the federal agency responsible for enforcing them • Describe the penalties that may be imposed for violating the federal fraud and abuse laws • Discuss some of the steps health plans can take to reduce fraud and abuse

Assignment 10: Governance: Structure and Strategy

Reading 10A: The Components of Governance in a Health Plan

• Explain the purpose of governance in a health plan • Describe the roles and responsibilities of the board of directors • Explain how organizational variations affect board structure and operation • List the three steps in a board risk management program • Describe the roles of shareholders/members and providers in governance • Discuss the roles and responsibilities of the CEO and other senior management

Reading 10B: Strategic Planning in Health Plans

• Define strategic planning • Explain why strategic planning is important to a health plan • Describe the four primary activities in strategic planning • Explain the importance of input and ownership in strategic planning

Reading 10C: Key Strategic Issues for Health Plans

Page 8 of 469

AHM 510 : Health Plans : Governance and Regulation

• Identify and describe the key strategic issues faced by health plans • Give examples of how key strategic issues are interrelated in the strategic planning process

Assignment 11: Governance: Accountability and Leadership

Reading 11A: Governance: Accountability and Leadership

• Discuss accountability among the stakeholders in managed care • Explain several implications of accountability on health plan leadership and governance • Describe the essential elements of an effective health plan compliance plan • Define medical necessity and describe how health plans address related governance issues • Describe quality and ethics programs and ombudsman programs

Assignment 12: Key Legal Issues in Managed Care

Reading 12A: Key Legal Issues in Managed Care

• Define breach of contract, negligence, medical malpractice, and punitive damages • Discuss the obligations that health plans owe to plan members in conducting utilization management activities • Describe the standard of care health plans must meet when they credential plan providers • Discuss two theories of liability that may make health plans liable for the medical malpractice of plan providers • Describe how ERISA affects the ability of plan members to bring legal actions against health plans • Identify and describe some legal issues that may arise between health plans and plan providers • Discuss some of the federal and state laws that regulate the business conduct of health plans

Assignment 13: Public Policy and Changing Environment

Reading 13A: Public Policy from the Health Plan Perspective

• Explain some of the ways that health plans influence public policy • Identify primary interest groups in each of the major healthcare sectors that participate in efforts to affect health plan public policy • Describe several types of advocacy and political activities undertaken by interest groups in the health plan policy debate • Discuss the role of litigation in determining health plan public policy • Describe several techniques interest groups use to affect public opinion

Reading 13B: Changing Environment and Emerging Trends in the Health Plan Industry

• Identify several key environmental factors that affect health plans

Page 9 of 469

AHM 510 : Health Plans : Governance and Regulation

• Describe the underlying tension between universal healthcare coverage and comprehensive healthcare benefits • Explain how marketplace reform and regulatory reform have brought about change in the health plan industry

Page 10 of 469

AHM 510 : Health Plans : Governance and Regulation

Chapter 1 A : Environmental Forces

To operate their businesses, health plans must navigate through a complex environment. "Major players move into new markets in a matter of days. Market segments unheard of just a few years ago-such as physician practicemanagement- get major infusions of Wall Street capital and become forces to reckon with overnight. Changes in policy emphasis from Washington create new forms of competition, such as Medicare and Medicaid health plans."¹

Today, health plans must focus on raising capital, addressing competition, and helping to shape or respond to healthcare public policy. In addition, health plans must cope with a rapidly changing market that is regional and national as well as local in nature. Mergers, acquisitions, and business alliances among health plan players who were once avid competitors further complicate the environment. The increase in government mandates dictating the healthcare services that must be covered by health plans drives up costs for health plans. And these are just a few of the environmental forces present in the industry today.

After completing this lesson, you should be able to:

• Name and describe several major factors shaping the environment of managed healthcare

• Describe the players in health plan and how their interests affect the way they influence the healthcare environment

• Explain the influences accreditation organizations and the media exert over the financing and delivery of healthcare

• Describe several possible governance responses that health plans make to deal with their changing environment

The board of directors and senior management of health plans must develop plans to operate their businesses within this constantly changing environment. Business practices that worked well yesterday may not be sufficient today. Healthcare public policy in the form of regulation often impacts and sometimes constricts a health plan's business plan for its operations. For example, health plans must meet state minimum capital requirements in establishing and maintaining their business. In this way, state and federal regulation affects executive management decisions concerning virtually all aspects of a health plan. In addition, business decisions made by health plans may trigger the enactment of new regulations to address new forms of business or new business practices.

Governance is the vehicle health plans use to make decisions about the overall direction or purpose of a company. In this course, we will define governance as the efforts by the health plan's board of directors or other governing body, in conjunction with senior management, to develop corporate policy, to create a corporate mission statement and vision, and to develop strategies in order to achieve the organization's goals and mission. We will discuss corporate vision and mission statements later in this lesson.

Page 11 of 469

AHM 510 : Health Plans : Governance and Regulation

Because regulation and health plan governance decisions share an interdependent relationship, this course combines the presentation of governance issues faced and managed by health plans and the regulations with which health plans must comply.

The environments in which health plans operate can be described as external or internal as discussed in Figure 1A-1. In this lesson, we will discuss the factors that influence the external environment of health plans and the internal responses that health plans make to changes in the environment. Because the health plans' internal responses are covered later in this course, this lesson focuses largely on the external environment affecting health plans.

The Evolving Health Plan MarketThe factors that drive the rapid change and shape the environment in the health plan industry include:

• Extent and level of regulation and legislation (e.g., healthcare reform bills)

• Status of the economy

• Pace and number of mergers and acquisitions

• Changing structure of the health plan market

• Changing demographics (e.g., aging population)

• Consumer expectations for availability of and demand for new and better products and services

• Entrepreneurial and technological innovation (e.g., advances in medical technology including devices, surgical procedures and new pharmaceuticals)

• Politics and election cycles

• Media coverage

• Litigation developments and trends

• Changing interests or needs of the various health plab players (i.e., consumers, competitors, purchasers, providers, payors, etc.) in the marketplace

Page 12 of 469

AHM 510 : Health Plans : Governance and Regulation

All the factors in the preceding list affect a health plan's business decisions and many impact decisions related to formation, organization, and governance of the health plan. In the following sections and throughout this lesson, we will examine how these factors exert influence in the health plan marketplace.

Extent and Level of Regulation and LegislationThe health plan market is unique compared to many other business markets because of the extent to which healthcare is regulated in the United States. For example, few other industries are required to submit quality assurance plans with their applications to operate in a particular state. In addition, few other industries must comply with state and federal requirements regarding the minimum services a company must offer to its customers. Ensuring compliance with regulations requires an allocation of resources and capital to functional areas that would not otherwise need those resources and capital, from a purely business operations standpoint.

Political pressures greatly impact both the regulatory and the legislative processes. In addition, regulation is often the result of legislation. In recent years, the number of health plan bills in the state and federal legislatures has dramatically increased. Legislators have responded to their constituents' healthcare coverage concerns by proposing both benefit mandates for specific healthcare services (e.g., maternity length-of-stay mandates) and comprehensive bills that address numerous concerns (e.g., network adequacy, mental health parity, external review, etc.).

Health plans have a great interest in legislation because of the impact it has on their businesses. Each new mandate and administrative rule or regulation for coverage adds to the health plan's costs for delivering and financing healthcare. These increased costs may make premium hikes a necessity or cause the health plan to discontinue its coverage of some of the "extras" (e.g., vision care or prescription programs) that make health plans attractive to purchasers and consumers.

Status of the EconomyThe state of the economy has a tremendous impact on the formation and operations of health plans. Factors that reflect the state of the economy include the rate of a nation's growth, employment levels, interest rates, spending, production, prices, housing starts, and the money supply.

For health plans, economic factors can influence:

1. The availability of capital for business start-ups or expansions 2. The demand for healthcare services, or the type or amount of those services

desired 3. The accessibility of healthcare coverage

For example, as the United States comes closer to having full employment, the overall population has greater access to healthcare coverage since most coverage is provided through employment relationships. However, an increase in the number of mandates or economic downturns can have a negative effect on the amount of employer-sponsored

Page 13 of 469

AHM 510 : Health Plans : Governance and Regulation

healthcare coverage because employers may buy less healthcare coverage in a period of increased costs or economic instability.

Inflation also plays a role in the health plan environment by influencing the prices of healthcare services, supplies, and coverage.

During an inflationary period, consumers may have less purchasing power because the prices of goods and services increase more quickly than income. Economic factors also influence employers' willingness to purchase coverage for employees and the amount of the premium that employers are willing to pay. If the economy is experiencing increased inflation, consumers and purchasers may choose not to purchase healthcare coverage. During periods of inflation, costs for health plans usually increase more rapidly than the health plan can increase premiums for purchasers to balance the increased costs. The resulting downturn in premium revenue may cause health plans to cut back on employment and/or to reduce expenses by cutting back on employment and/or offering fewer services.

Fast Definition

Economic environment includes all the elements affecting the production, distribution, and consumption of goods and services. 2

Fast Definition

Inflation-a prolonged rise in the average level of prices in an economy

Review Question

In the paragraph below, a statement contains two pairs of terms enclosed in parentheses. Determine which term in each pair correctly completes the statement. Then select the answer choice containing the two terms that you have chosen.

Inflation plays a role in the health plan environment by influencing the prices of healthcare services, supplies, and coverage. During an inflationary period, consumers typically have (more / less) purchasing power because the prices of goods and services increase (more / less) quickly than income.

more / more

more / less

less / more

less / less

Incorrect. Because inflation increases the costs of goods and services, consumers do not have more purchasing power.

Page 14 of 469

AHM 510 : Health Plans : Governance and Regulation

Incorrect. Because inflation increases the costs of goods and services, consumers do not have more purchasing power.

Correct. Inflation typically increases costs, and reduces consumer purchasing power

Incorrect. In an inflationary period, consumers have less purchasing power because inflation increases the costs of goods and services, and consumers do not have more purchasing power.

Mergers and AcquisitionsMergers and acquisitions occur in almost every industry as companies identify business opportunities that will enhance their market position. In the last few years, however, the health plan industry has experienced a large proportion of mergers and acquisitions that have changed the landscape of the market. On one hand, some industry observers express concern that if the pace of consolidations continues there will be a substantial lessening of competition in the health plan industry. For example, when two health plans merge, the result may be a lessening of competition in some of the affected national, regional, state, or local markets for managed healthcare. In addition, a merger may give the newly formed health plan more market power than each participant had individually prior to the merger. Each phenomenon raises antitrust issues.

On the other hand, a merger may result in a health plan being able to realize operational synergies, reduce administrative costs, and expand and develop a better quality provider network. However, health plans typically consider mergers with care because integration of two formerly separate businesses requires a substantial amount of financial and other resources.

Changing Market StructureThe geographical area of the health plan market has changed from a mostly local market structure to a structure that frequently requires local, regional, and national market presence. Employers with operations in multiple locations in different states or regions often want to negotiate and enter into agreements with only one health plan that will handle the financing and delivery of healthcare in all the employer's business locations. Although enrollment in health plans has surged over the last 10 years, the rate of growth varies among different geographical markets, and the strategies that work in one market do not necessarily work in others.

Market maturity also affects business decisions. Market maturity is a measure of the growth or development of a market in terms of the number and types of players present, the relationships among those players, the products available, and consumer acceptance of the products. Market maturity can affect how receptive consumers and providers are to health plan programs, the extent to which employer healthcare purchasing coalitions are present, the types of products the market demands, and the level of competition among health plans in an area. For example, a health plan that operates in a large metropolitan area may have to offer additional services to compete with other health plans in that market. A health plan that is the only health plan available in a rural community might not face the same market challenges. It is not necessarily easy to assess market maturity in managed healthcare markets. Certain aspects of a market may be in more mature phases than other aspects of the market. For example,

Page 15 of 469

AHM 510 : Health Plans : Governance and Regulation

there may be several health plan competitors in a market but the provider networks for one or more of those competitors may be in the initial stages of development. Health plans, therefore, must constantly assess each of the aspects of the market separately and make business decisions based on the level of maturity of each market aspect.

Changing Demographics

Baby boomers are aging, and as they age they will require more healthcare services. As a significant portion of the American population becomes eligible for Medicare, opportunities for health plans to tap into this demographic market will grow. Recent federal legislation expanded the types of health plans that can contract to serve the healthcare needs of the Medicare population.

The increase in the U.S. population of members of certain ethnic groups or races is another demographic factor that presents challenges and opportunities for health plans. For example, some health plans are pursuing marketing programs that are targeted to reach non-English-speaking potential enrollees. Other health plans are creating disease management programs directed to age-based ethnic groups with a high incidence of certain diseases.

Several health plans offer open access plans that allow members to choose in-network coverage for a small copayment or out-of-network coverage that is generally more expensive. In general, such plans are targeted to economically prosperous baby boomers. In addition, women's healthcare issues and special needs have been the focus of some purchasers, and legislative initiatives such as maternity length-of-stay laws and mandated direct access to obstetricians/gynecologists reflect this concern. Health plans may need to reassess their product and service offerings in light of these demographic and associated regulatory changes.

Consumer DemandThe expectations of today's consumers continue to grow- and consumers are clamoring for new and better healthcare products and services. Among these demands are:

• Direct access to specialists

• Increased efforts to ensure the delivery of quality healthcare (e.g., By obtaining more information about plans and their providers)

• Coverage for more and different types of treatment (e.g., Experimental treatments, alternative medicine, etc.)

• Free and open exchange about healthcare treatment options between physicians and other medical personnel and the consumer

• Grievance and appeals procedures for claim denials, and health plan liability for "bad outcomes"

• Convenience in the delivery of healthcare

Consumer demand has a significant effect on healthcare legislation. It also has an impact on health plan operations. For example, most health plans use primary care providers (PCPs) to manage and coordinate care. PCPs also act as conduits to specialists to coordinate patient care and manage healthcare costs by eliminating

Page 16 of 469

AHM 510 : Health Plans : Governance and Regulation

unnecessary visits to specialists. Allowing consumers direct access to specialists requires some modification in a health plan's procedures.

For example, in a direct access plan, usually the primary care provider (PCP) is still responsible for coordinating patient care and monitoring the patient's health. A health plan may notify (or regulators may require that the plan notify) the PCP about care from specialists received without the PCP's knowledge. This notification may increase costs by adding to administrative procedures, and if state-mandated, may subject a plan to monetary or other penalties for noncompliance

Entrepreneurial and Technological InnovationEntrepreneurs can claim credit for many of the innovations that exist in health plans today. By identifying a market need, and finding a way to address that need, entrepreneurs have established new standard industry practices or developed alternative methods for providing healthcare. For example, entrepreneurs created the concept of physician-hospital organizations, physician practice management companies, and firms that offer disease management programs. Entrepreneurs change the way healthcare is financed and delivered by creating new ways of fulfilling needs and providing services. One way that entrepreneurs affect health plans is through the establishment of unique strategic business alliances. We discuss strategic partnerships in Formation and Structure of Health Plans.

Technological innovation is thriving on several fronts. From a clinical standpoint, advances in healthcare abound- from the application of gene research in treating diseases to breakthroughs in the early detection and treatment of certain forms of cancer. New medical devices and new drugs have been created to treat illness and disease.

From an information management standpoint, change is also flourishing. For example, efforts by health plans to involve physicians in managing health risks require a great deal of information technology support. In addition, recently enacted federal legislation requires the Department of Health and Human Services to develop national standards for the electronic transmission of health data. Information technology plays a pivotal role in the maturation of health plans. Health plans are spending money to apply the findings of outcomes research and evidenced-based medicine. Health plans that do not invest in information technology find themselves at a competitive disadvantage.

Entrepreneurs in health plans have also had an impact on marketing. For example, pharmaceutical companies now market new drugs directly to the consumer through television, magazines, and other forms of advertising.

Evidence based medicine the conscientious, explicit, and judicious use of current best evidence in making decisions about the care of individual patients.5

Politics and Election CyclesBecause our legislative representatives are elected every two years, healthcare is a public policy issue raised every two years in connection with political election campaigns. Although voters do not vote on the issues considered by legislatures, they do elect the representatives who vote on such matters. The elected representatives usually feel compelled to try to implement into law the wants and needs of their

Page 17 of 469

AHM 510 : Health Plans : Governance and Regulation

constituents. As evidenced by the Clinton administration's healthcare reform proposal of 1992 and various patient bills of rights currently under consideration in the House, Senate, and state legislatures, healthcare is an issue of some concern to legislators and the voting public.

Litigation Developments and TrendsIn addition to legislative and regulatory activity, court activity and decisions also impact health plans. For example, consumers are bringing lawsuits against health plans as well as providers for treatment decisions that result in bad outcomes. Court rulings often result in precedents being set that are followed in subsequent court decisions. We discuss key legal issues that impact health plans in Key Legal Issues in Health Plans.

Changing Interests of the PlayersThe main players in health plans are the consumers (the end users of the health plan products and services), the purchasers (employers, unions, purchasing coalitions, other large groups, government programs, and individuals), the providers (physicians, hospitals, and other healthcare professionals), and the payors (health plans, insurance companies, and certain self-funded employer groups).

The players in helath plans have diverse and sometimes conflicting interests. For example, the payors and purchasers want to manage costs and deliver quality healthcare, while the end-user consumers are usually concerned with obtaining the best medical care without focusing on the cost. Physicians often want unlimited authority to make decisions concerning patient care, while health plans must maintain utilization management and quality assurance systems. For example, physicians who refer health plan members to an out-of-network provider without obtaining plan approval may undermine the plan's credentialing and quality programs and hamper the health plan's ability to manage costs. In the following sections, we discuss the interests of the major players and how they influence health plans. We will also discuss other stakeholders in the health plan marketplace, such as vendors, the community, and patient advocacy groups.

ConsumersAmericans see healthcare as a social good and expect it to be available to all individuals, whenever it is needed and in whatever quantity it is needed. In this way, healthcare differs from almost every other product or service. Other products and services are generally available only to those consumers who are able to pay for them. Consumer expectations for healthcare services place burdens and unique responsibilities on the suppliers or providers of such services. They also necessitate the involvement of public policy in setting standards for the provision of healthcare services to populations that are unable to pay the market price or even make any contribution to the payment for those services. We will discuss the impact of the uninsured and underserved populations later in this lesson. Let's now consider the end users who are consuming health plan products and services and explore their impact on the health insurance plan environment.

Consumers want affordable, quality healthcare available-where they need it, when they need it. The influence of consumers can be seen in the number of legislative bills concerning healthcare. For example, many states are considering mandating external review for health plan decisions regarding exclusions from coverage to ensure protection

Page 18 of 469

AHM 510 : Health Plans : Governance and Regulation

of members' interests. Consumers are taking a more active role in their personal health. In the past, a consumer may have hesitated to question the diagnosis or treatment prescribed by a provider, but today such interaction is much more common. Consumers are voicing and demonstrating their desires that certain aspects of healthcare be available to them. The demand for greater choice of providers has encouraged health plans to develop direct access plans. The increased interest in alternative medicine has led some health plans to offer coverage for "non-traditional" providers and treatments.

Today's commercial health plan consumers are better educated and have higher disposable incomes and higher standards of living than their predecessors. Employers and other purchasers that buy the healthcare for these consumers are more attuned to the consumer's needs and desires. In a booming economy with unemployment at a low level, offering a generous package of healthcare benefits may make the difference between hiring the candidate of choice or a less qualified substitute.

PurchasersEmployers and other purchasing groups have exerted tremendous influence on the products and services offered by health plans. Employer initiatives that are shaping health plans include an increased focus on quality as well as cost, as evidenced by the formation of organizations such as the Foundation for Accountability (FACCT). FACCT is a coalition of purchasers (mostly large employers) and consumer organizations founded to make an outcome-oriented assessment of health plans' treatment of medical conditions or diseases. Largely as a result of employers' focus on quality, there has been an increase in the number of health plans that seek accreditation from nationally recognized accreditation organizations. To prove that employers' dollars are being well spent, health plans have begun devoting more time and money to outcomes research and other quality-ensuring initiatives. Additionally, employers' efforts to curb the costs of healthcare coverage, such as the establishment of on-site clinics for employees and the creation of wellness programs, have caused health plans to innovate and expand their product and service offerings.

ProvidersSince providers actually supply the healthcare services that health plans deliver to their customers, they are a crucial component of a health plan. A health plan must employ or recruit and contract with many different types of providers for the provision of healthcare services to the health plan's members. Health plans that strive to develop a relationship with providers based on the exchange of mutual expertise are likely to be more successful than health plans that have a less flexible approach. Providers' concerns about the continued growth of health plans usually center on compensation and autonomy issues. Because some physicians have concerns about losing their decision-making autonomy to health plans, a number of physicians have joined physician groups or created alliances with other providers to establish their own health plans, such as physician-hospital organizations or provider-sponsored organizations. These organizations sometimes become competitors of established health plans or insurance companies by contracting directly with a purchaser and bypassing the health plan entirely. Alternatively, they may present a different type of entity with which a health plan or insurance company must negotiate to obtain provider services in a market. Health plans that maintain strong and positive locally based relationships with providers are more likely to prosper in today's environment. For example, providers have the clinical expertise and supporting clinical data that health plans need to demonstrate to

Page 19 of 469

AHM 510 : Health Plans : Governance and Regulation

purchasers their commitment to quality. In addition, providers usually have great influence with their patients. When these patients are members of a health plan, their satisfaction is of prime importance to that health plan.

PayorsInsurance companies that offer a full range of healthcare products, including indemnity products, compete with health plans. These same insurance companies are health plans if they offer health plan products such as health maintenance organizations (HMOs), preferred provider organizations (PPOs), POS options, etc. In certain instances, an insurance company may have a slight advantage in establishing certain types of managed healthcare product offerings. For example, an insurance company that forms an HMO and also has experience in the fee-for-service arena may have an easier time beginning a PPO or offering a POS option than an HMO that is not affiliated with an indemnity insurer, because the indemnity insurer has the experience and ability to process out-of-network claims and more accurately determine premium rates. The HMO can build or acquire these assets and capabilities, but may take more time and use substantial financial resources to do so.

Other StakeholdersIn the preceding sections, we have discussed some of the main players in the managed healthcare marketplace; however, these are not the only participants in this market. The community in which a health plan operates, the uninsured or underserved populations, vendors, academic medical centers, patient advocacy groups, and the federal and state government are also stakeholders in the health plan marketplace. Each of these stakeholders is discussed in the following sections.

The Community

Although the markets for health plans may be expanding to regional or national markets, most health plans are initially established to serve a local community. In addition, the articles of incorporation and the mission statements of not-for-profits, established for charitable purposes, reflect their commitment to provide benefits to the community. Some state laws require community representation on the board of directors for health plans.

Certain not-for-profit organizations are required to serve their community by making membership available to individuals and small employers; by making services available to low-income, high-risk, medically underserved, and elderly populations; and by using community rating to determine their premiums. Other ways that health plans serve their communities include: teaming up with community public health organizations to provide demand management and health promotion activities, joining forces with academic medical centers to perform education and research, and sponsoring community health projects such as childhood immunization initiatives and health fairs. For example, some health plans are partnering with community public health agencies to educate health plan enrollees about the dangers of substance abuse or obesity. Since community public health agencies often are already doing some of the promotion activities that a health plan wishes to provide, a partnership between these two entities makes sense. In some situations, the promotional activities of the public health agency are tailored for the

Page 20 of 469

AHM 510 : Health Plans : Governance and Regulation

health plan enrollee population; in others, the promotion is aimed at the geographic population (which includes health plan enrollees) at large.

Health plans that are active participants in their local communities can gain many benefits. From a public relations perspective, providing additional or tailored services to meet needs in the local community can reap great rewards from increased enrollment in plans to availability of funding sources for expansions. Additionally, individuals, the community, and health plans all reap rewards when health plans participate in activities to improve the health of their members.

Uninsured and Underserved PopulationsThe uninsured population in the United States is a significant social policy concern. Federal and state governments often implement plans to extend insurance coverage or health plan enrollment as an option for these populations. As we will discuss later in this course, major reform initiatives to guarantee insurance for all citizens have not been successful.

The uninsured population has a tremendous impact on the cost of healthcare services in this country. Emergency-room treatment of conditions that would be better served by a primary care provider costs a great deal. Costs of the uninsured cannot always be expressed in monetary terms. For example, no amount of money can compensate the parent of a child who dies after contracting a disease that could have been prevented by an immunization. The basic tenets of health plan education and preventive services- are a natural fit for this population; however, finding the public funding to finance such endeavors is a challenge.

Recently enacted legislation (i.e., the Health Insurance Portability and Accountability Act of 1996), which was intended to make great strides in guaranteeing access to health insurance for some members of the uninsured population, does not seem to be achieving that goal because the cost of coverage is being passed on to individuals. For example, a recently released General Accounting Office report noted that individuals in some states are paying premium rates 140% to 600% higher than standard premiums for individual healthcare products.6

Additional legislation to address this issue at either the state or federal level (or both) is likely. Such legislation can sometimes increase a health plan's costs of providing coverage to members. Health plans that remain active in this public policy debate may be able to suggest solutions that benefit all the participants in this dilemma.

The underserved population in both rural and urban areas presents a somewhat different problem than the uninsured population. Low-income residents in outlying rural communities often suffer from lack of access to healthcare. There may be no hospital and may be only one physician or other healthcare professional that visits such communities once a week as part of a government outreach program. Sometimes, a health plan or insurance company refrains from entering a rural market because there are not enough potential members to make the market a viable business undertaking. Additionally, health plans that desire to enter rural markets may meet resistance from the local physicians or hospitals in those communities. Addressing the needs of underserved markets is not an easy task, yet some health plan innovators have developed methods of serving at least some of the underserved populations in rural areas. One health plan

Page 21 of 469

AHM 510 : Health Plans : Governance and Regulation

builds networks for medium-to-large employers with operations in rural areas across broad geographic regions that allow the health plan to have a large enough potential enrollee market to make the venture worthwhile. Although such a solution does not address the communities where no healthcare facilities are available, it is a step toward making health plans more accessible to a larger portion of the population. In addition, a number of PPOs operate in rural markets.

In metropolitan or urban areas, meeting the needs of the underserved population is also a challenge. For example, many urban Medicaid programs must address transportation issues, lack of providers willing to serve this population, and long waits for care. Finding ways to meet the needs of the uninsured and underserved populations is a responsibility that health plans share with others in the healthcare industry and our country in general.

VendorsVendors, such as organizations that provide billing or other administrative services, can play a significant role in the healthcare market. Companies that produce software for contract or claims management or premium billing are essential to the operation of a health plan. In addition, vendors may provide or manage clinical services such as radiology, and disease management programs targeted to specific diseases such as diabetes. Vendors may also arrange for and administer the provision of carve-out healthcare services such as behavioral healthcare, radiology, chiropractic, oncology, etc. In fact, some health plans have outsourced to vendors their entire information technology function. A vendor often has expertise in a particular area that the health plan has not developed or for which the cost of developing such expertise is not practical. In the managed healthcare industry, there is increasing use of vendors to provide services that are not cost-effective for the health plan to provide. For example, one health plan has outsourced to a vendor its call center for customer service. As another example, an HMO with little expertise in claim processing for a point-of-service product might outsource this activity to a vendor.

As vendors become even more prevalent, they may impact the health plan market in new ways. For example, there are increasing numbers of software firms that want to meet the information needs of all stakeholders in the managed healthcare market. Employers that self-fund their plans already use vendors to perform many functions that are not cost-effective for the employer to undertake. Often the "vendor" to an employer is a health plan; however, as more enterprising firms create market niches for their services some health plans may lose some of their vendor contracts with employers. For example, pharmacy benefit managers (PBMs) act as vendors to employers for pharmaceutical products and services.

Academic Medical CentersAnother stakeholder in the health plan industry is the academic medical center. Academic medical centers (AMCs), also known as academic health centers, are healthcare institutions that offer physician residency programs and include medical schools and other professional healthcare schools such as nursing and dental programs. These institutions train healthcare professionals and perform various clinical and other types of healthcare-related research. Teaching hospitals are usually part of an AMC. Teaching hospitals are institutions that offer physician residency programs. In the past, academic medical centers have had concerns about the growth of health plans. Some of the reasons for this concern are as follows:

Page 22 of 469

AHM 510 : Health Plans : Governance and Regulation

• Often the physician billing practices of AMCs may not mesh with health plan payment structures

• Lack of primary care providers on the staffs of AMCs (usually staffed by specialists) may make such institutions unlikely candidates for health plan approaches

At most teaching hospitals, the physician who supervises the resident bills for his or her services, although it is the resident who provides all or some of the services. In addition, the fee-for-service side of Medicare has largely subsidized AMCs. The proliferation of Medicare health plans may eliminate some of that funding for AMCs. Also, policymakers and legislators are reviewing many aspects of Medicare, including the fee-for-service aspects, and have curbed some of the additional funds that were previously funneled into AMCs.

The environmental pressures that have caused dramatic change in the health plan industry are also impacting AMCs. Some AMCs have merged with other teaching institutions or have entered into relationships with other hospital systems. Other AMCs are beginning to enter into formal relationships with health plans. AMCs are purchasing physician practices to gain access to patients, contracting with non-teaching hospitals to become participants in Integrated Delivery Systems (IDS), or entering into partnerships as providers with HMOs. Some AMCs are even becoming owners/investors in health plans. AMCs can bring unique capabilities and resources to a health plan relationship. Their expertise in education and research is a valuable tool in an era when the health plan market focuses on information. Medical outcomes research and evidence-based medicine are two areas in which AMCs may be able to help health plans.

Review Question

The Sawgrass Health Center is an institution that trains healthcare professionals and performs various clinical and other types of healthcare-related research. Because Sawgrass receives government funding, it is required to provide medical care for the poor. Of the following types of health plans, Sawgrass can best be described as:

a medical foundation

an academic medical center (AMC)

a healthcare cooperative

a community health center (CHC)

Incorrect. A medical foundation is an entity that owns and manages all purchased assets of physician practices, you will read more about this arrangement in the lesson Health Plan Structure and Arrangements.

Correct. An academic medical center is an institution that trains healthcare professionals, performs clinical and other types of healthcare-related research and is required to provide medical care for the poor.

Page 23 of 469

AHM 510 : Health Plans : Governance and Regulation

Incorrect. A healthcare cooperative is a consumer-sponsored, physician-operated medical facility that provides prepaid healthcare to members. You will read more about this arrangement in the lesson Health Plan Structure and Arrangements.

Incorrect. A community health center is a medical facility that recieves federal, state and private grant funding to provide primary care for medically underserved populations. You will read more about this arrangement in the lesson Health Plan Structure and Arrangements.

Patient Advocacy GroupsPatient Advocacy groups are consumer organizations that may provide patient education, coordinate the delivery of or provide care, and/or represent the general political interests of patients or those with certain illnesses. In addition, patient advocacy groups often pursue legislation designed to further the interests of the patients in the group (e.g., mandated coverage of benefits for experimental cancer drugs).

In the past, health plans' relationships with patient advocacy groups have sometimes been adversarial. Health plans often only interacted with a patient advocacy group when the health plan denied coverage for a treatment needed by a member the advocacy group represented. Today, some health plans are partnering with patient advocacy groups to provide certain aspects care. Some patient advocacy groups provide psychosocial or holistic care in partnership with a health plan. A health plan may benefit from such a partnership in several ways, including establishing a better reputation among patients and actually lowering the long term cost of certain treatments by providing care that more closely monitors and treats a patient's condition and over all health.

Federal and State GovernmentsAs we will describe throughout this course, federal and state governments exert tremendous influence over a health plan's formation, operations, and governance. These governments are stakeholders in the managed healthcare industry in two important ways. First, such governments enact and enforce laws to protect and preserve the public's interests.

The second way in which governments act as stakeholders is through their roles as purchasers of healthcare services for government employees and government-sponsored healthcare programs. From this perspective, their needs and concerns more closely parallel those of purchasers described earlier. Governments, through their dual roles as purchasers and regulators, affect the types of laws or regulations enacted or the standards to compete in the marketplace. We will discuss governments' roles as purchasers in more detail in Federal Government as Purchaser.

Review Question

Page 24 of 469

AHM 510 : Health Plans : Governance and Regulation

Regulatory and legislative bodies are among the important environmental forces in the health plan industry. The following statements are about such regulation and legislation. Select the answer choice that contains the correct statement.

Federal guidelines exist to direct health plans on compliance issues when a health plan encounters conflicting state laws in a given service area. Administrative rules and regulations do not carry the force of law.

As stakeholders in the health plan industry, federal and state governments exert tremendous influence over a health plan's formation and operations. In recent years, the number of health plan bills in the state and the federal legislatures has decreased.

Incorrect. Healtrh plans often have to comply with multiple state laws while trying to meet the needs of a single market.

Incorrect. Administrative rules and regulations, prescribed by a federal or state administrative agency, carry the force of law.

Correct. Federal and state governments exert tremendous influence over health plans' formation, operations and governance

Incorrect. In recent years the number of health plan bills in the state and federal legislatures has increased.

Other Environmental ForcesIn addition to the direct environmental forces that impact the market that we have just discussed, other forces also shape health plans. Governments' roles as purchasers, conflicting state and federal regulations, the increasing use of accreditation, and the media all have an impact on health plans and their operations. We briefly discuss each of these below.

1. Governments

2. Accreditation

3. The Media

We mentioned earlier that governments' dual roles as purchasers and regulators sometimes affect the laws or regulations that impact managed healthcare. The dual roles of governments sometimes affect the market in ways not necessarily intended. For example, if the federal agency responsible for purchasing healthcare for federal employees sets a standard that potential contractors must meet to be eligible for consideration as a health plan for those employees, other purchasers in the industry may demand a similar minimum threshold for the health plans with which they contract.

Governments also affect the managed healthcare regulatory environment in other unintended ways. A health plan that serves a multistate community such as Memphis,

Page 25 of 469

AHM 510 : Health Plans : Governance and Regulation

Tennessee (portions of the Memphis metropolitan area are also in the states of Mississippi and Arkansas), may be subject to several sets of state laws that sometimes conflict. Offering the same product in the entire metropolitan area may become a regulatory challenge since there are no guidelines for a health plan to follow to comply with conflicting state laws in a service area. The health plan and its legal counsel must comply with the laws of multiple states while trying to meet the needs of a single market. In addition, there can be conflicts between state and federal laws. For example, a health plan may have to meet a minimum federal standard for the provision of some aspect of healthcare services, such as mental health in accordance with the federal Mental Health Parity Act that we will discuss in Federal Regulation of Health Plans, and meet additional requirements of a state that has regulations affecting the coverage for mental health services.

Complying with regulations requires an allocation of time and money from a health plan. The more complicated or burdensome the laws and regulations become, the more time and resources are required to comply with such laws and regulations. Eventually, these increased costs to the health plan are passed on to the purchaser in the form of increased premiums.

Increased demands by purchasers and consumers for accountability in managed healthcare have spurred growth of a competitive industry for accrediting health plans, the health plans they sponsor, and the separate providers of specialized care within health plans. Accreditation programs develop standards for health plan performance; conduct reviews of the organization, its policies, and procedures; and gather data to determine the extent to which the organizations meet the standards. Most accreditation programs were initially developed by the providers in the industry they accredit in response to pressure for accountability and the need for an independent third-party review. The major accrediting programs for healthcare are now sponsored by independent not-for-profit entities. These entities are governed by boards of directors with a broad representation of providers, insurers, purchasers (private and public), and consumers to help ensure independence, credibility, and responsiveness to the needs of major stakeholders. Accrediting programs confer an accreditation status following their review but generally do not attempt to establish rankings that directly compare health plans, their health plans, or parts of their plans. 7

Many employers will not consider entering into a contract with a health plan that has not been accredited by a nationally recognized accreditation program. In addition, some state governments are requiring health plans to obtain accreditation from a nationally recognized accreditation organization as a condition of licensure in a state. Other states may not require accreditation for licensure but allow accreditation to suffice in place of a mandatory external review for quality.

Today, it is hard to pick up any newspaper or magazine or to tune into network television and not see managed healthcare mentioned. All too often, the articles are not positive. The media has significant influence on public opinion in the choice of topics that it covers and the manner in which the stories are covered. Since public opinion can have an impact on a health plan's business, health plans must consider media coverage as a

Page 26 of 469

AHM 510 : Health Plans : Governance and Regulation

factor in their environment. Insight 1A-3 provides a brief overview of health plan's relationship with the media.

Insight 1A-3. Does the media fuel health plan backlash?

A new survey on media coverage of health plan by the Kaiser Family Foundation points to a significant increase in coverage of health plan issues over the past decade, much of it critical of health plans. The study, which was published in the January/February 1998 issue of Health Affairs, finds that most, two-thirds, of 2,100 news stories that have appeared in newspapers, business publications, and on network television since 1990 are largely neutral in their coverage of health plan. A quarter were critical, whereas 11% praised the system.

However, the more highly visible stories on network TV and in special newspaper series have been much more negative, particularly in the last four years. Coverage involving health plan in the early 1990s tended to emphasize the benefits of this emerging system and its potential to reduce high healthcare costs. During the health reform debate of 1993 to 1994, health plan was the "savior," recalled reporter Susan Dentzer at a Kaiser forum on media coverage of health plan. Competing health plans were going to improve quality and lower costs.

More recently the media has highlighted patient "horror stories" and "high-drama" anecdotes, particularly on TV and in newspaper series. Journalists acknowledge a "herd instinct" among reporters in covering such issues as "drive-through deliveries" and gag clauses. And some have found that editors are interested only in stories with health plan victims and villains. To gain more balance, reporters cited a need for better data and hard information on costs, enrollment, and benefits.

Health Plan Responses to Environmental ForcesWe've discussed many of the external environmental forces at work in the health plan industry and stated that health plans must make business decisions taking these factors and forces into account. Now we'll briefly mention some ways health plans are responding to the various forces in the health plan environment.

In our earlier discussion of the market for health plans, we touched upon many of the ways health plans respond to changes in their environment or the market, such as forming strategic business alliances and participating in mergers or acquisitions. To ensure their survival in the rapidly changing health plan environment, health plans are assessing their strategic options by reviewing their organizational structure, their corporate values and mission, their product portfolio and development process, their strategies to remain or become competitive in a particular market, and the way they respond to consumers' demands.

Page 27 of 469

AHM 510 : Health Plans : Governance and Regulation

Most companies develop a corporate vision and a mission statement. Health plans are no exception.

A mission statement is a statement that succinctly sums up the organization's reason for existence and overall purpose. What is changing with health plans is the focus of their corporate vision and mission statements. In the past, health plan mission statements may have mentioned the customer, but meeting the customer's needs was usually not the focus. Health plans now develop mission statements that center on defining and meeting in an ethical and cost-effective manner the needs of the customer and/or the community. To realize this overall goal of addressing the customer's needs, health plans develop strategic plans. Strategic planning is the process of identifying a company's long-term objectives. Companies use corporate strategies to achieve their plans.

Changes in the environment of a health plan sometimes necessitate governance moves that are not in the normal course of business. Occasionally, a change in a health plan's environment makes it necessary for the health plan to restructure or reorganize its business operations to remain competitive, become more competitive, or enter new markets. A corporate reorganization or restructuring is the process of adjusting the internal structure of an organization by changing reporting relationships; adding, eliminating or changing the responsibilities of functional departments; moving from a centralized to a decentralized business structure (or vice versa); or creating a new subsidiary or holding company. For example, an insurance company that enters the health plan arena may create a subsidiary HMO. Or, an existing health plan may change the functional duties of departments or reporting relationships within its organization to streamline its responses to customer needs or to reduce administrative expenses.

Fast Definition Corporate vision an overall view of what the organization should achieve by its existence.

Fast DefinitionCorporate strategies the methods a company plans to use to achieve its long-term objectives.

Other ways that health plans respond to change include leadership changes, converting from a not-for-profit or mutual organization to a for-profit organization, going public, selling portions of their businesses, acquiring new or existing companies, entering new business ventures, getting out of existing business ventures, or making major changes in plan or product offerings. We will discuss each of these responses later in this course. However, let's now consider an example of one of these environmental responses. See Figure 1A-2.

As you can see, a health plan has many internal governance tools it can use to respond to changes in its external environment. Throughout the remainder of this course, we will discuss the legal and regulatory factors in the health plan environment, as well as the governance planning and responses that allow health plans to thrive in the dynamic environment of health plans today.

Figure 1A-2. An example of one health plan's response to its environment.

Page 28 of 469

AHM 510 : Health Plans : Governance and Regulation

After reviewing demographic characteristics and regulatory factors, the Livwel Company, a health plan, identifies a new business opportunity in the Medicare market. This health plan has ready capital, but no expertise in serving this market. The Livwel Company decides to enter into a business venture with another health plan, called Firstline, that has expertise in serving the Medicare market. This type of joint business venture benefits Firstline by providing a ready source of capital, while the Livwel Company gains expertise in serving this new type of market.

Chapter 2 A : Legal Organization of Health Plans

Because of the rapid pace of change in the health plan industry and the need to constantly reassess strategic plans, determining a health plan's legal form is one of the fundamental issues that must be addressed by the company's leaders. In this lesson, we begin with an overview of the basic forms of legal organization available to health plans, with a focus on corporations, the predominant form. We then examine the for-profit health plan, the not-for-profit health plan, and the mutual insurance company. In this discussion, we examine issues such as legal and formal requirements, owners' liability, tax treatment, long-term stability, allocation of profits, and options for raising operating funds.

After completing this lesson, you should be able to:

Explain the distinguishing features of a corporation and a limited liability company Describe the key features and differences between a for-profit company and a not-

for-profit company Describe the differences between a publicly traded stock company and a privately

held stock company Describe the key features and differences between a stock company and a mutual

company

Basic Forms of Legal OrganizationIn the United States today, business entities can be established in any one of a number of legal forms. For instance, most health plans are corporations, and many healthcare providers and other vendors with whom health plans do business are sole proprietorships, partnerships, or professional corporations. Figure 2A-1 provides an overview of several forms of legal organization.

CorporationsHealth plans are typically established as corporations. This legal form affords owners, directors, and executives the greatest protection from individual liability. Also, in the case of for-profit health plans, the corporation is the legal form that provides the greatest flexibility for raising operating funds. In some states, an entity responsible for financing healthcare, such as an insurance company, is required by law to be organized as a corporation. In many states, however, a health plan, such as an HMO, is not required to be a corporation; it can, for instance, be a limited liability company. Also, as we will see later in this lesson, federal law now allows certain types of provider-owned organizations, which are not all corporations, to operate as health plans in the Medicare and Medicaid markets.

Page 29 of 469

AHM 510 : Health Plans : Governance and Regulation

Figure 2A-1. Sole Proprietorships, Partnerships, and Corporations.

Sole Proprietorships

A sole proprietorship is a business owned by one person. All the debts of the business are the debts of the owner. Business profits or losses are treated as individual income for tax purposes. Although the sole proprietor can leave the assets and liabilities of the business to someone else, continuing the operation of a sole proprietorship after the owner's death is often difficult.

Partnerships

A partnership is a business that has many of the same legal characteristics of a sole proprietorship but is owned by two or more persons. The partners can be individuals or legal entities, such as corporations. A partnership can be established by oral agreement or through a formal partnership agreement. All states have laws that spell out the requirements for establishing a partnership. A partnership can take any one of the following legal forms.

A general partnership is owned by two or more general partners who share responsibility for business operations. General partners, when they are individuals, are responsible for the debts of the whole business and declare the appropriate share of their partnership income or losses on their individual tax returns. The partnership itself does not pay federal income tax, although it is required to file a return for information purposes. A general partnership ends with the death or withdrawal of any general partner; the remaining partners must form a new partnership if they want to continue the business.

Partners can limit the liability of certain owner-investors by forming a limited partnership. A limited partnership consists of limited partners and at least one general partner. Limited partners, who cannot participate in the day-to-day management of the organization, are at personal financial risk only for the amount of their investment in the business. The general partners, on the other hand, have full liability, similar to the liability of sole proprietors. Typically, limited partners can enter into and opt out of a limited partnership with much greater freedom than can general partners, which is an advantage for raising operating funds because the partnership can more easily attract limited partners if it needs additional investors.

When the partners in a limited partnership are individuals, the profits and losses of the business are treated as individual income, and the partners each declare the appropriate share of their partnership income on their individual tax returns. The partnership itself does not pay federal or state income tax. However, if the structure of the limited partnership includes more corporate than partnership characteristics, it may be taxed as a corporation.

Generally, a limited partnership continues upon the death or withdrawal of a limited partner, but it ends with the death or withdrawal of a general partner. However, the partnership agreement can place restrictions on a limited partner's right to withdraw, or can allow for the partnership to continue beyond the withdrawal of a general partner.

Page 30 of 469

AHM 510 : Health Plans : Governance and Regulation

Another type of partnership, permitted by enabling statutes in some states, is the registered limited liability partnership (LLP). A registered limited liability partnership agreement eliminates a partner's personal liability for debts and obligations that result from acts committed by another partner or a representative of the partnership while conducting partnership business. A registered limited liability partnership is similar to a general partnership in most other respects.

Corporations

A corporation, as defined in 1819 by U.S. Supreme Court Chief Justice John Marshall, is "an artificial being, invisible, intangible, and existing only in contemplation of the law."