Electronic Warfare - Emerging Trends, Approaches, Key issues and Investment Outlook

Agricultural Trade Policy Outlook: Emerging Trends and Research Topics

Robert Johansson

Selected Paper prepared for presentation at the International Agricultural Trade Research Consortium’s (IATRC’s) 2015 Annual Meeting: Trade and Societal Well-Being, December 13-15, 2015, Clearwater Beach, FL. Copyright 2015 by Robert Johansson. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided that this copyright notice appears on all such copies.

AGRICULTURAL TRADE

POLICY OUTLOOK: EMERGING TRENDS AND

RESEARCH TOPICS

Robert Johansson

Chief Economist, USDA

International Agricultural Trade Research Consortium --- 12/13/15

1

Recent Developments

• Free Trade Agreement Negotiations

• Trans Pacific Partnership (TPP)

• Transatlantic Trade and Investment Partnership (TTIP)

• World Trade Organization

• Ministerial Conference/DDA

• Dispute Settlement

• Other

• Animal/crop diseases

• Climate change

• Economic outlook / U.S. competitiveness

2

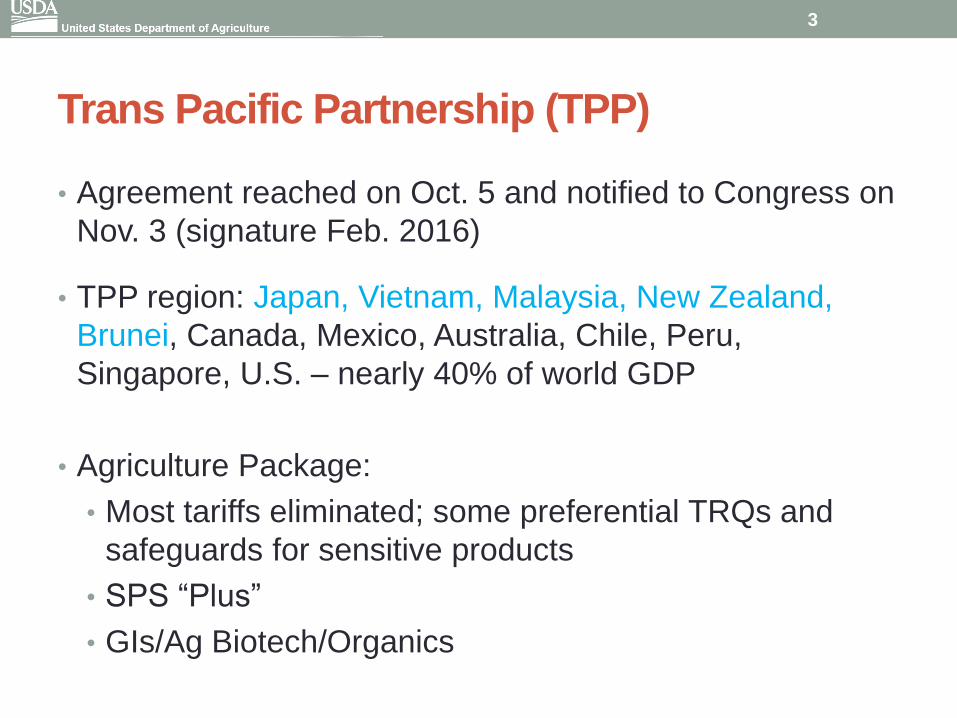

Trans Pacific Partnership (TPP)

• Agreement reached on Oct. 5 and notified to Congress on

Nov. 3 (signature Feb. 2016)

• TPP region: Japan, Vietnam, Malaysia, New Zealand,

Brunei, Canada, Mexico, Australia, Chile, Peru,

Singapore, U.S. – nearly 40% of world GDP

• Agriculture Package:

• Most tariffs eliminated; some preferential TRQs and

safeguards for sensitive products

• SPS “Plus”

• GIs/Ag Biotech/Organics

3

U.S. Agricultural Exports

TPP accounts for 40-50% of total

0

20

40

60

80

100

120

140

160

TPP

$billion

4

Importance of FTAs to U.S. Trade: The

TPP and Asia-Pacific Integration

0

1

1

2

2

3

3

4

North America Asia Pacific

Billi

on

s o

f P

eo

ple

2009 2030

0

5

10

15

20

25

30

35

North America Asia Pacific

Tri

llio

ns

, 2

00

5 P

PP

$

2009 2030

Asia’s middle class is the

fastest growing market in the

world…

…And will drive global middle

class demand in the coming

decades.

In 2030: 66% of the world’s

middle class will be in Asia In 2030: 59% of the world’s

middle class consumption will

be in Asia Source: OECD

5

Transatlantic Trade and Investment

Partnership

• To date, eleven negotiating rounds. Next round is in Feb.

2016

• Key issues for agriculture:

• Tariffs (13.7% simple average for US exports to EU vs.

4.7% for EU export to US) (ERS, 2015)

• Nontariff measures (SPS, TBT, GIs, licensing)

• Beef, pork, poultry, dairy, grains, oilseeds, processed

products

6

Transatlantic Trade and Investment

Partnership

-10

-5

0

5

10

15

20

25

US exports to EU EU exports to US Balance

$billion

7

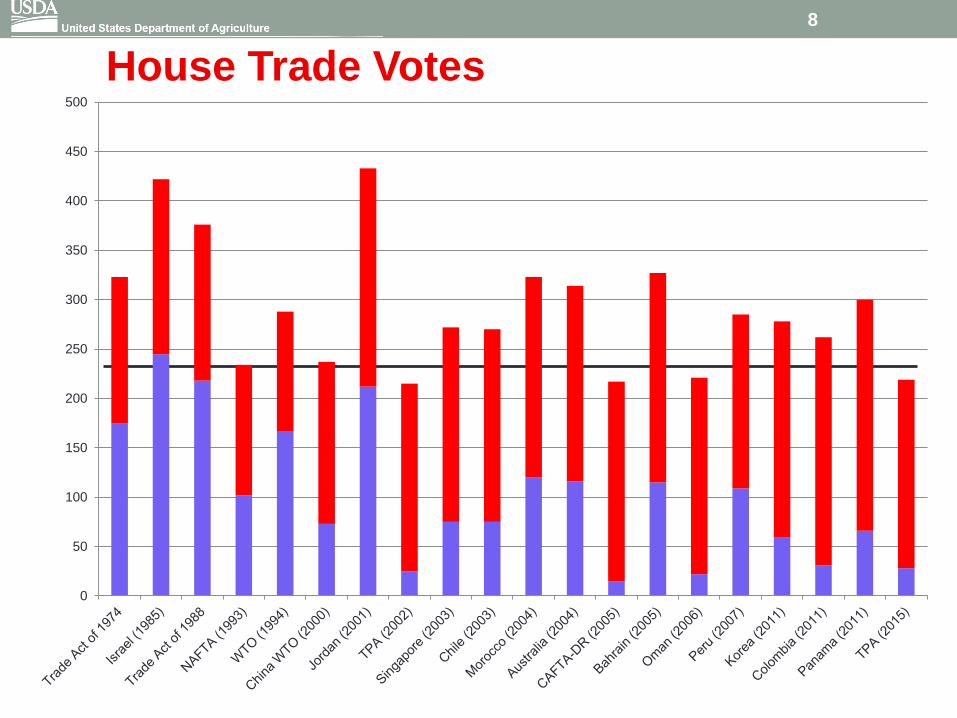

House Trade Votes

0

50

100

150

200

250

300

350

400

450

500

8

World Trade Organization

• 10th Ministerial, Nairobi, Kenya (Dec. 15-18)

• Possible outcome on export competition for agriculture

• Developing countries pushing for safeguards and public

stockholding flexibility (e.g., price supports)

• Other issues (ecommerce, TRIPs, SVEs, LDCs,

accessions of Afghanistan and Liberia)

9

World Trade Organization

• Dispute Settlement Cases

• 500 cases (as of October 2015)

• In comparison, around 300 cases during the 47 years of the

GATT

• Most cases concern trade remedies / nonag

• 6 new ag panels in 2015:

• US – Chinese export subsidies for ag/non-ag enterprises

• EU – Russian tariffs on ag and non-ag products

• China – EU modification of poultry tariff concessions

• US/NZ – Indonesia ag import restrictions

• Japan – Korean ag import restrictions

• Brazil – Indonesian poultry import restrictions

10

World Trade Organization

Country of Origin Labeling (COOL)

• Started in December 2008

• Final AB report (compliance) in May 2015

• Arbitration began in June 2015

• Arbitration report issued December 7

• Canada: $781 million (requested $2.3 bil.)

• Mexico: $228 million (requested $713 mil.)

• DSB will meet on December 18

11

Post Mortem

• How do Economists present sophisticated modeling

(econometric / PE / GE) to a relatively unsophisticated

audience?

• The lawyers understand Econ 101 yet we are using

relatively sophisticated econometric and modeling

techniques that are not easy for non-economists to grasp.

• Some post-mortem critique of that case is needed from

objective researchers.

• Lots of material out there to sift through.

12

Other Trade Issues

Economic Factors Affecting U.S. Trade

• Sluggish global economic growth

• Strong U.S. dollar

• Lower commodity prices

• Other countries’ economic situation and policies (China,

India, Brazil, Russia)

13

Other Trade Issues

• Livestock / Crop Disease Outbreaks

• HPAI/BSE – looking at effects on trade

• Citrus plant diseases and impact on citrus products

• Climate change

• COP 21

• USDA report --- Food Security and Climate Change

• Improved trade will reduce impacts of climate related

supply shocks.

14

China Falls to Number Two for U.S. Agricultural

Exports, Canada Returns to Top Spot

0

5

10

15

20

25

30

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016forecast

China

Canada

Mexico

Billion dollars

Source: USDA (ERS-FAS) Outlook for U.S. Agricultural Trade, USDA Global Agriculture Trade System

15

Monthly Chinese Corn/Barley/Sorghum

Imports by Origin

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.010

/20

10

12

/20

10

02

/20

11

04

/20

11

06

/20

11

08

/20

11

10

/20

11

12

/20

11

02

/20

12

04

/20

12

06/2

012

08

/20

12

10

/20

12

12

/20

12

02

/20

13

04

/20

13

06

/20

13

08

/20

13

10

/20

13

12

/20

13

02

/20

14

04

/20

14

06

/20

14

08

/20

14

10

/20

14

12

/20

14

2/2

01

5

4/2

01

5

6/2

01

5

8/2

01

5

Milli

on

Metr

ic T

on

s

US-CORN US-SORGHUM US-DDG

Ukraine-CORN Thailand/Burma/Laos-CORN Other-CORN

BARLEY Other-SORGHUM Other-DDG

Source: Global Trade Information Services (GTIS)

16

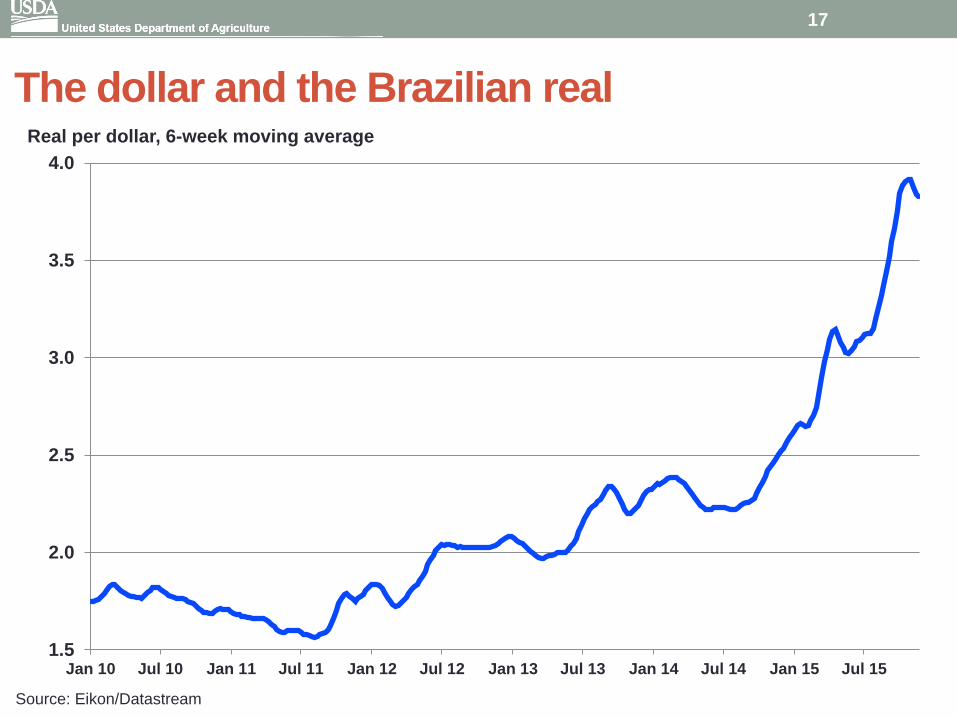

The dollar and the Brazilian real

1.5

2.0

2.5

3.0

3.5

4.0

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15 Jul 15

Real per dollar, 6-week moving average

Source: Eikon/Datastream

17

The price of corn* in dollars and real

5

7

9

11

13

15

17

2.5

3.5

4.5

5.5

6.5

7.5

8.5

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15 Jul 15

Dollars per bushel, 6-week moving average

Reals per bushel, 6-week moving average

Price in real

(right axis)

Price in US dollars

(left axis)

*Central Illinois, from USDA Agricultural Marketing Service

18

The price of soybeans* in dollars and real

13

16

19

22

25

28

31

34

37

40

8.5

9.5

10.5

11.5

12.5

13.5

14.5

15.5

16.5

17.5

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15 Jul 15

Dollars per bushel, 6-week moving average

Reals per bushel, 6-week moving average

Price in real

(right axis)

Price in US dollars

(left axis)

*Central Illinois , from USDA Agricultural Marketing Service

19

Dollar strengthens, exports falling below trend

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

70

75

80

85

90

95

100

105

110

115

120

1998 2000 2002 2004 2006 2008 2010 2012 2014

Monthly Agriculture Exports

(right axis)

Strength of US dollar

(left axis)

2000 = 100 Billion dollars

(nominal)

Source: Eikon/Datastream, USDA Global Agricultural Trade System

20

Dollar strengthens, imports rise

$0

$2

$4

$6

$8

$10

$12

70

75

80

85

90

95

100

105

110

115

120

1998 2000 2002 2004 2006 2008 2010 2012 2014

Monthly Agricultural Imports

(right axis)

Strength of US dollar

(left axis)

2000 = 100 Billion dollars

(nominal)

Source: Eikon/Datastream, USDA Global Agricultural Trade System

21

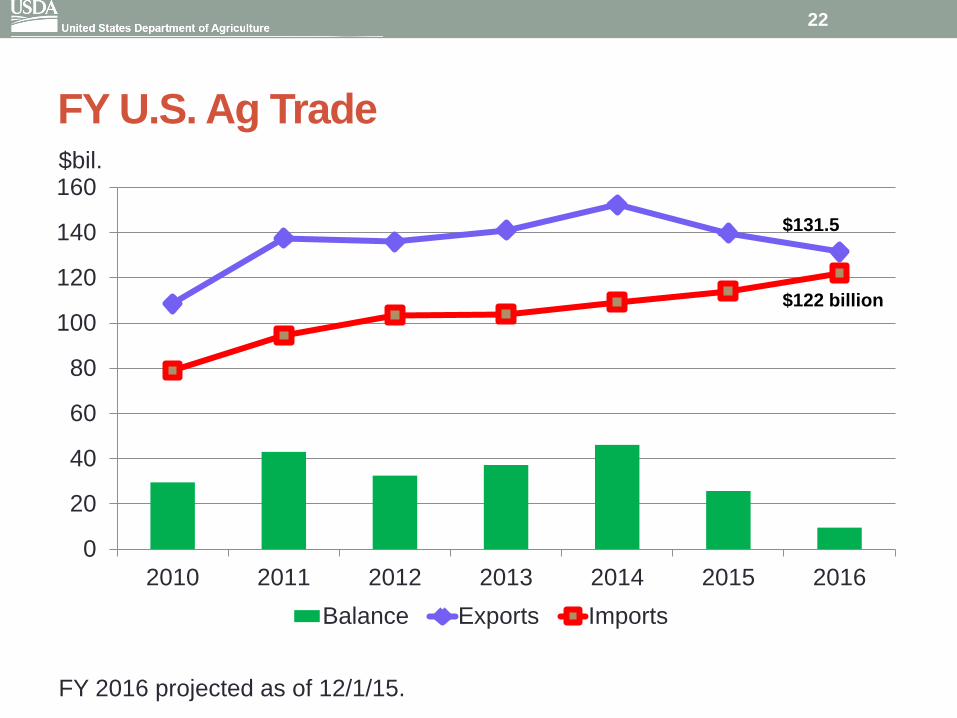

FY U.S. Ag Trade

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015 2016

Balance Exports Imports

$122 billion

$131.5

$bil.

FY 2016 projected as of 12/1/15.

22

Outlook

• Regional trade agreements will continue to flourish in absence of multilateral reform

• WTO largely becoming a dispute settlement body, unless the Ministerial sets a new course

• Developing country policies increasingly important in terms of global market distortions

• “Wild card” issues: livestock/plant disease outbreaks, climate change/natural disasters, transportation, economic outlook

23

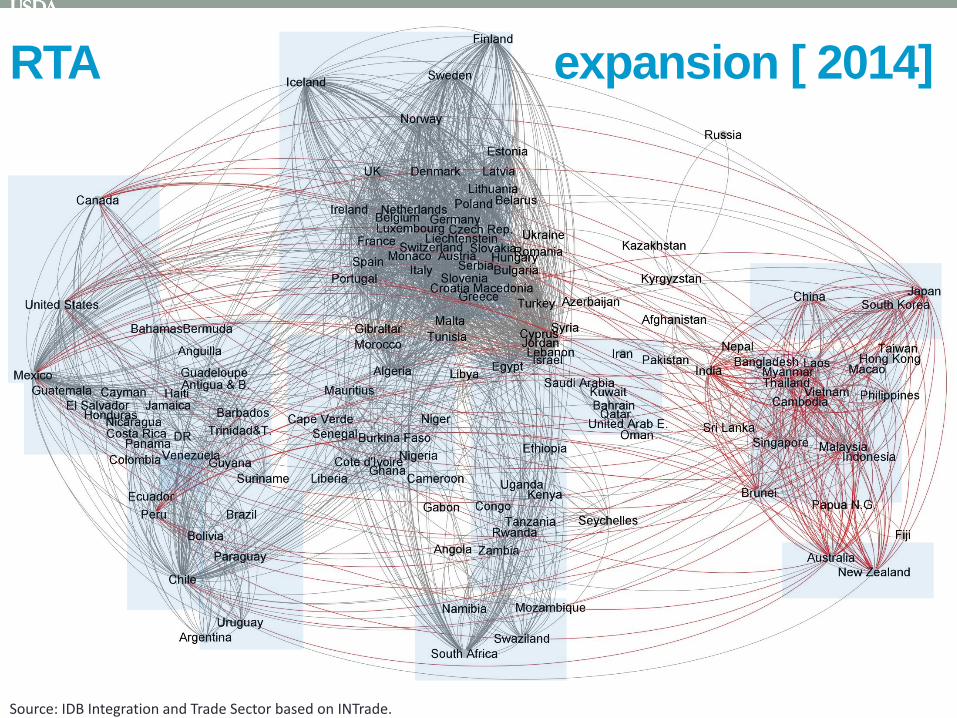

Source: IDB Integration and Trade Sector based on INTrade.

RTA expansion [ 1975] 24

Source: IDB Integration and Trade Sector based on INTrade.

RTA expansion [ 1995] 25

Source: IDB Integration and Trade Sector based on INTrade.

RTA expansion [ 2014] 26

Trans Pacific Partnership Japan – U.S. Tariff Comparison

0

100

200

300

400

500

600

700

800

Japan U.S.

%

Simple average, using DDA ad valorem equivalents

27

TPP Illustration (Japan Beef Tariff)

0

5

10

15

20

25

30

35

40

45

50

0 1 2 3 4 5 6 7 8 9 101112131415

Tari

ff R

ate

(%

)

Implementation Year

Japan’s Beef (Chilled/Frozen) Import Tariffs

WTO Bound

MFN Applied

Australia EPA for frozen beef

Failed WTO result

TPP Agreement

28

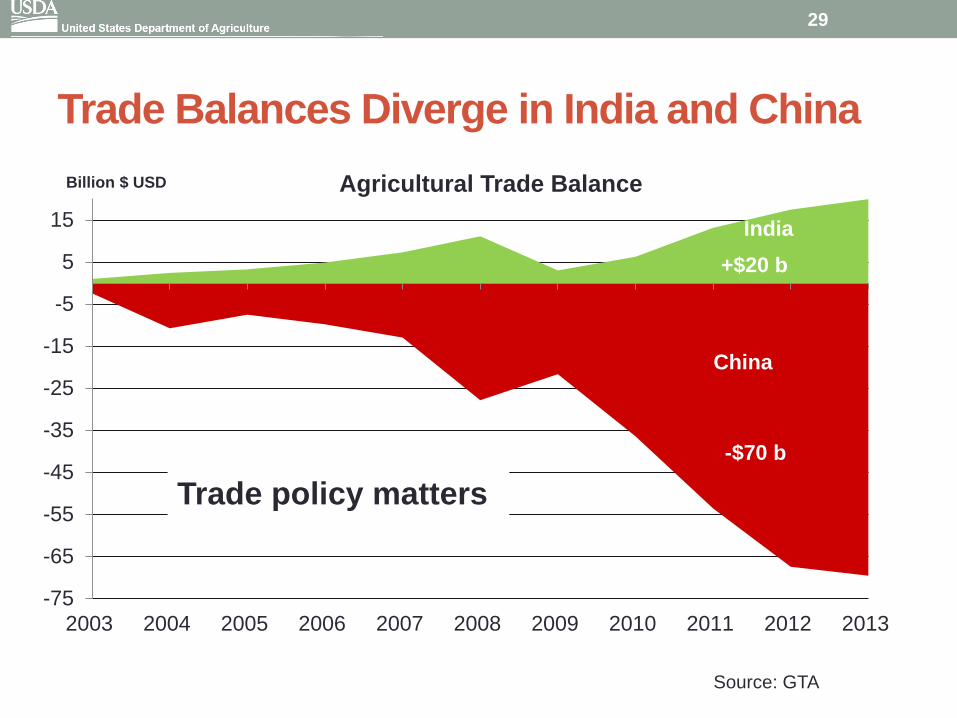

Trade Balances Diverge in India and China

-75

-65

-55

-45

-35

-25

-15

-5

5

15

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Agricultural Trade Balance

+$20 b

Source: GTA

-$70 b

India

China

Billion $ USD

Trade policy matters

29

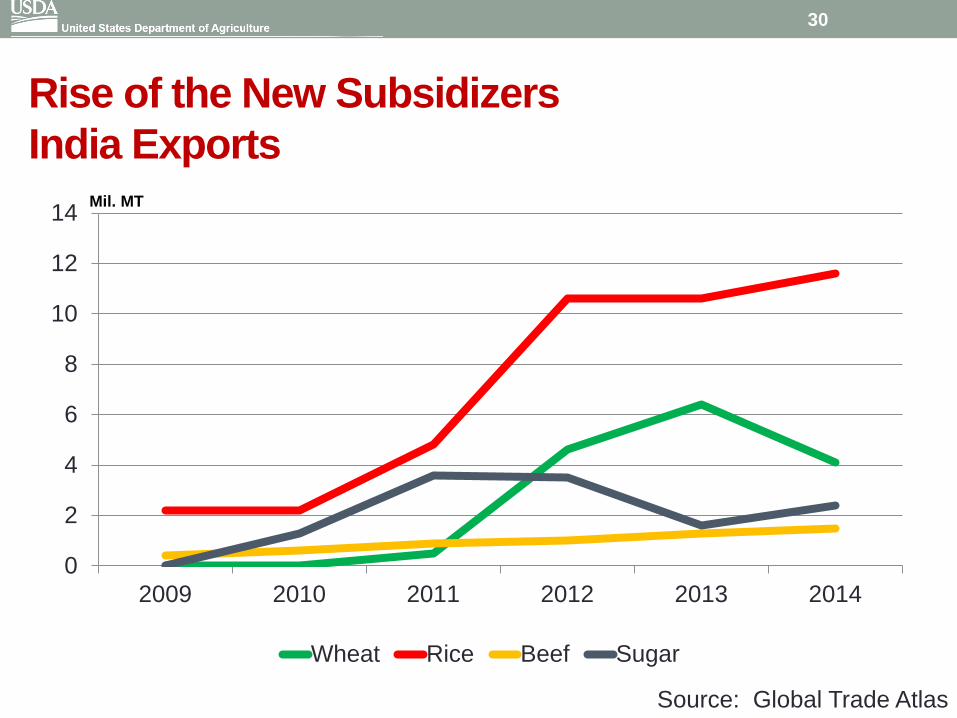

Rise of the New Subsidizers

India Exports

0

2

4

6

8

10

12

14

2009 2010 2011 2012 2013 2014

Wheat Rice Beef Sugar

Mil. MT

Source: Global Trade Atlas

30

Trade Distorting Domestic Support Rising

by Developing Countries

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US$

Mill

ion

s

Total Trade Distoring Domestic Support

India

EU

USA

China

Japan

Russia

Brazil

Canada

Indonesia

Australia

EU

India

US China

Source: Cairns Group & WTO Notifications

31

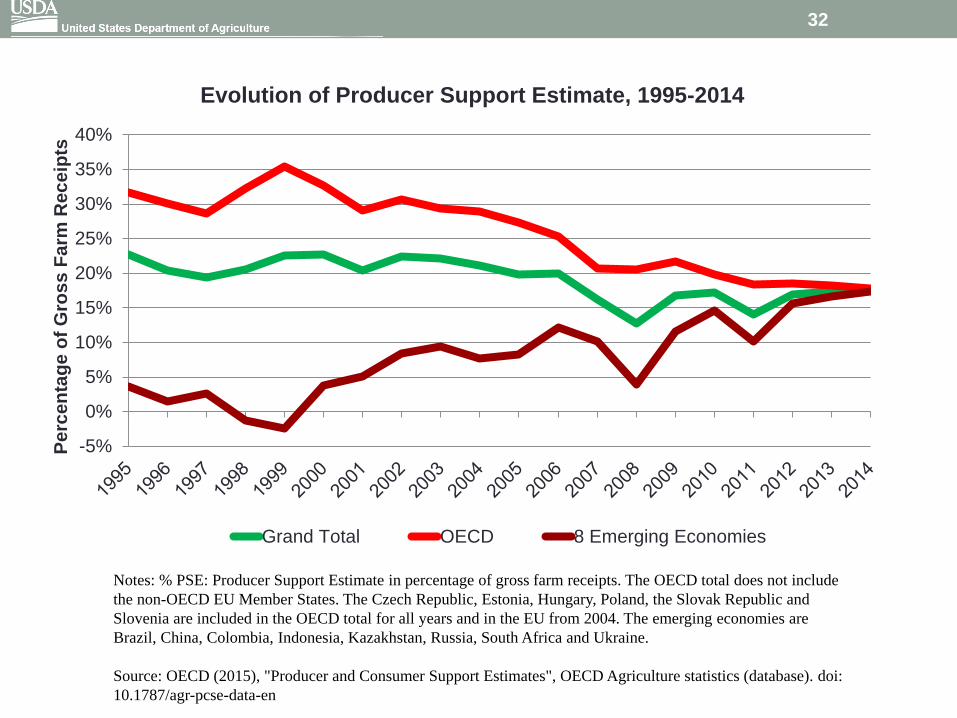

Notes: % PSE: Producer Support Estimate in percentage of gross farm receipts. The OECD total does not include

the non-OECD EU Member States. The Czech Republic, Estonia, Hungary, Poland, the Slovak Republic and

Slovenia are included in the OECD total for all years and in the EU from 2004. The emerging economies are

Brazil, China, Colombia, Indonesia, Kazakhstan, Russia, South Africa and Ukraine.

Source: OECD (2015), "Producer and Consumer Support Estimates", OECD Agriculture statistics (database). doi:

10.1787/agr-pcse-data-en

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Perc

en

tag

e o

f G

ros

s F

arm

Rec

eip

ts

Evolution of Producer Support Estimate, 1995-2014

Grand Total OECD 8 Emerging Economies

32

-20%

-10%

%

10%

20%

30%

40%

50%

Pe

rce

nta

ge

of

Gro

ss

Fa

rm R

ece

ipts

Evolution of Producer Support Estimate, 1995-2014

United States Brazil China European Union (EU-28)

Notes: % PSE: Producer Support Estimate in percentage of gross farm receipts. The Czech Republic, Estonia,

Hungary, Poland, the Slovak Republic and Slovenia are included in the EU from 2004.

Source: OECD (2015), "Producer and Consumer Support Estimates", OECD Agriculture statistics (database). doi:

10.1787/agr-pcse-data-en

33

Net CCC Outlays: Increase Relative to Baseline

2017-20 avg.

6.4

6.6

6.8

7

7.2

7.4

7.6

7.8

8

8.2

8.4

Programs Programs + Crop Ins Programs + Crop Ins +CRP

2014 Farm Bill 2008 Farm Bill

$bil.

Source: FAPRI analysis for OCE

34

Research Outlook

• Quantitative Analysis

• Moving beyond tariffs and the US/EU

• Developing tools to analyze developing country policies and trade/price effects

• NTMs

• Counterfactual: How do we frame the question?

• Sectoral analyses will likely become more important to understand in more granular detail.

• Assessing the “wild cards”

• Economic framework for analyzing non-policy disruptions to trade

35