Agility Emerging Markets- Logistics- Index 2016

84

Agility Emerging Markets Logistics Index 2016

-

Upload

red-fox-communications -

Category

Investor Relations

-

view

346 -

download

2

Transcript of Agility Emerging Markets- Logistics- Index 2016

Agility Emerging Markets Logistics Index2016

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

2

Section 1: The Agility Emerging Markets Logistics Index 4

Section 2: Sources 6

Section 3: Methodology 7

Section 4: Key Findings 9

EmergingMarkets:HowLogisticsExecutivesSeeThem 9

MarketsontheMove 11

TradeLanes 13

Section 5: Overview & Outlook 14

Section 6: The 2016 Agility Emerging Markets Logistics Index 18

TheTop10 18

ChangesoutsidetheTop10 20

The2016Index 23

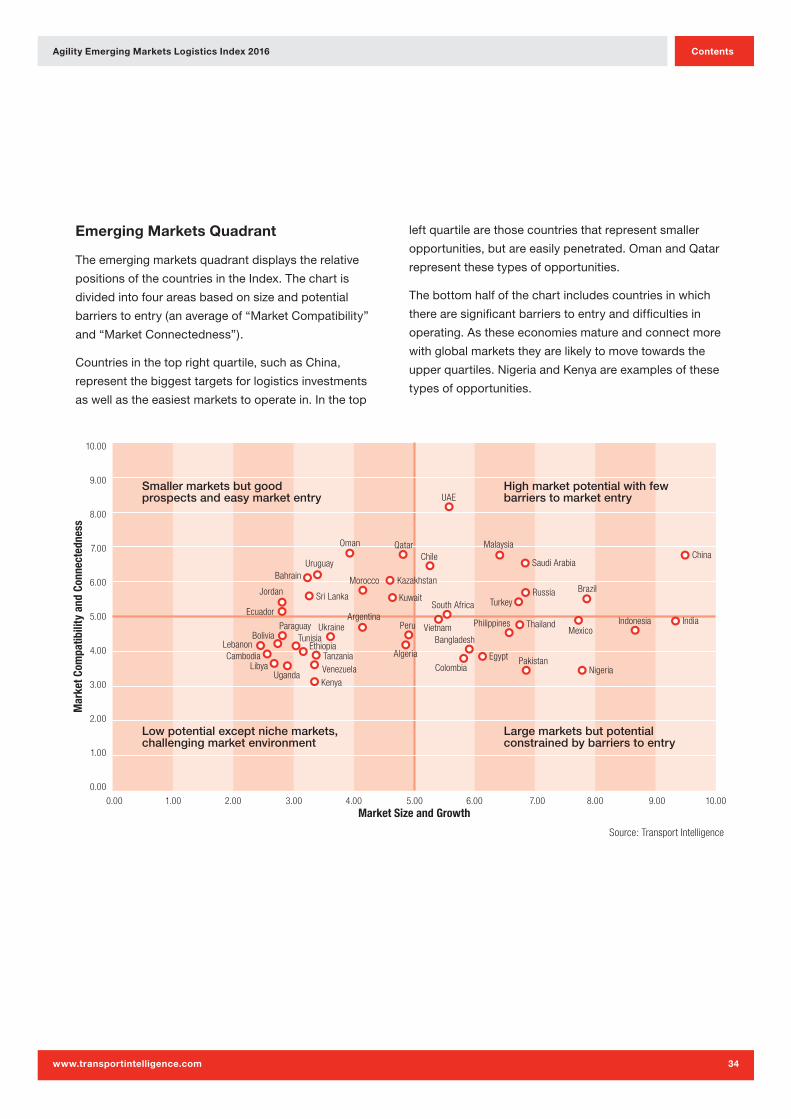

EmergingMarketsQuadrant 34

Section 7: Emerging Market Trade Lanes 35

TradebyAir 38

TradebySea 46

Section 8: The 2016 Agility Emerging Markets Logistics Survey 54

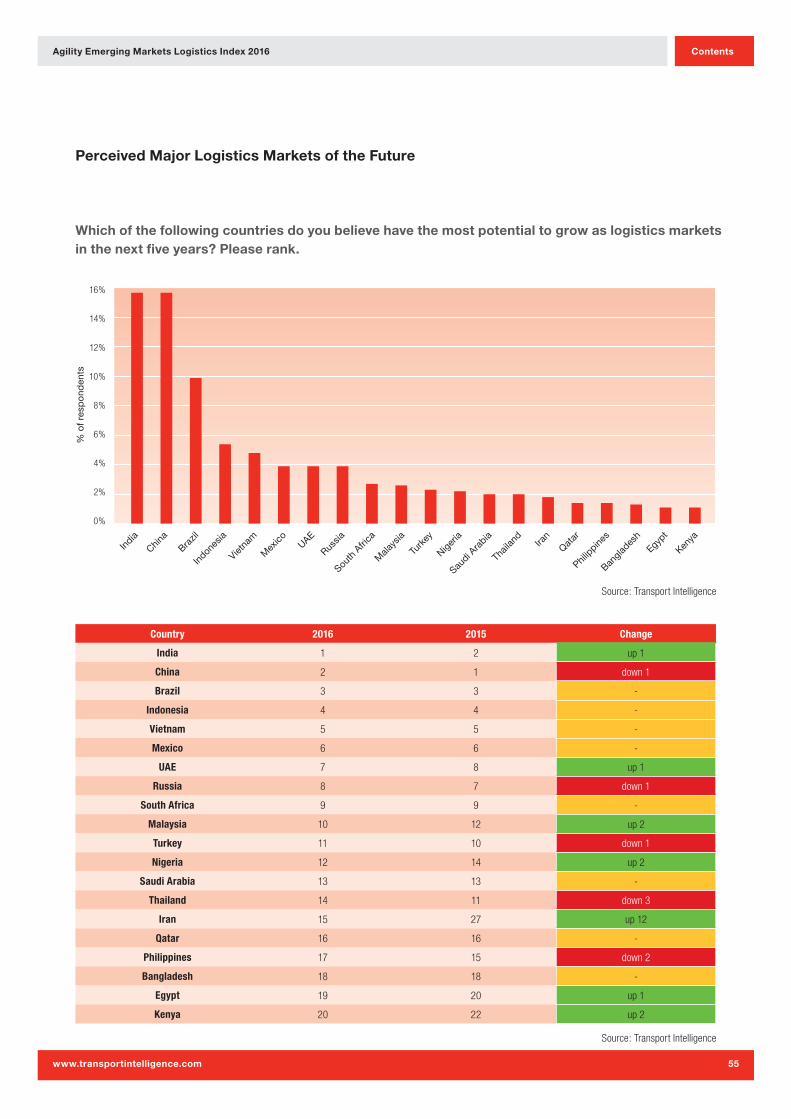

PerceivedMajorLogisticsMarketsoftheFuture 55

FactorsbehindthePotentialEmergenceofMarkets 57

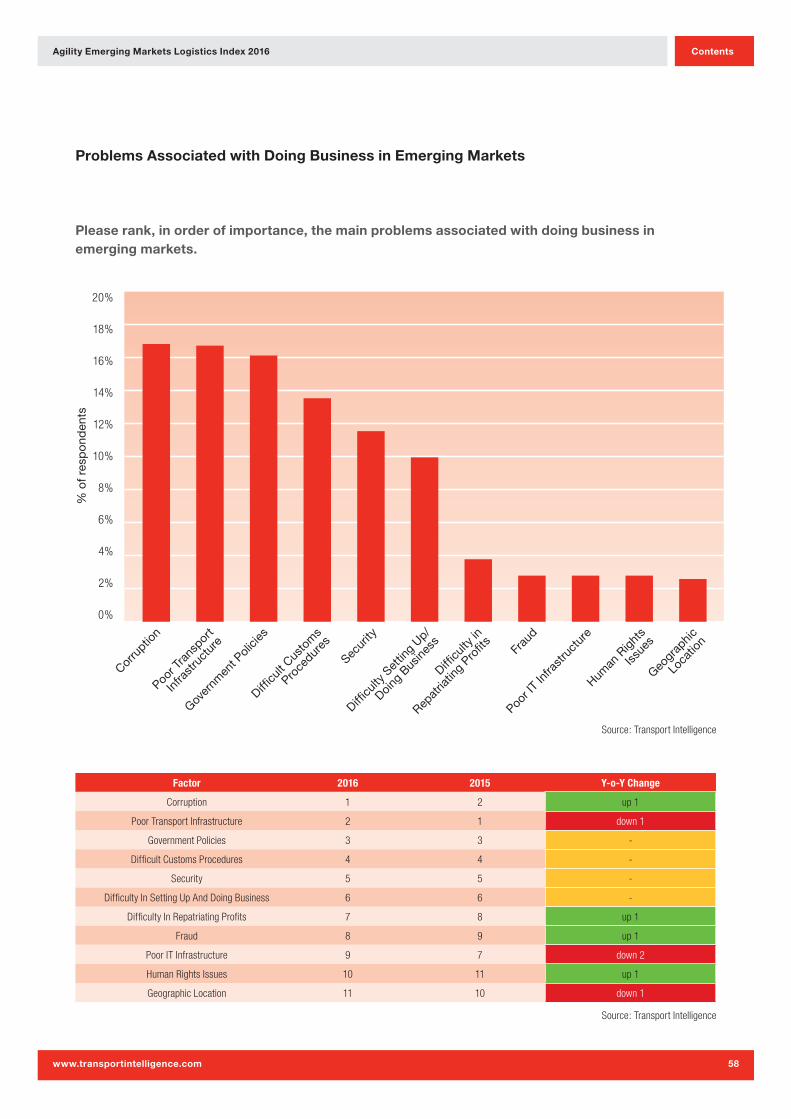

ProblemsAssociatedwithDoingBusinessinEmergingMarkets 58

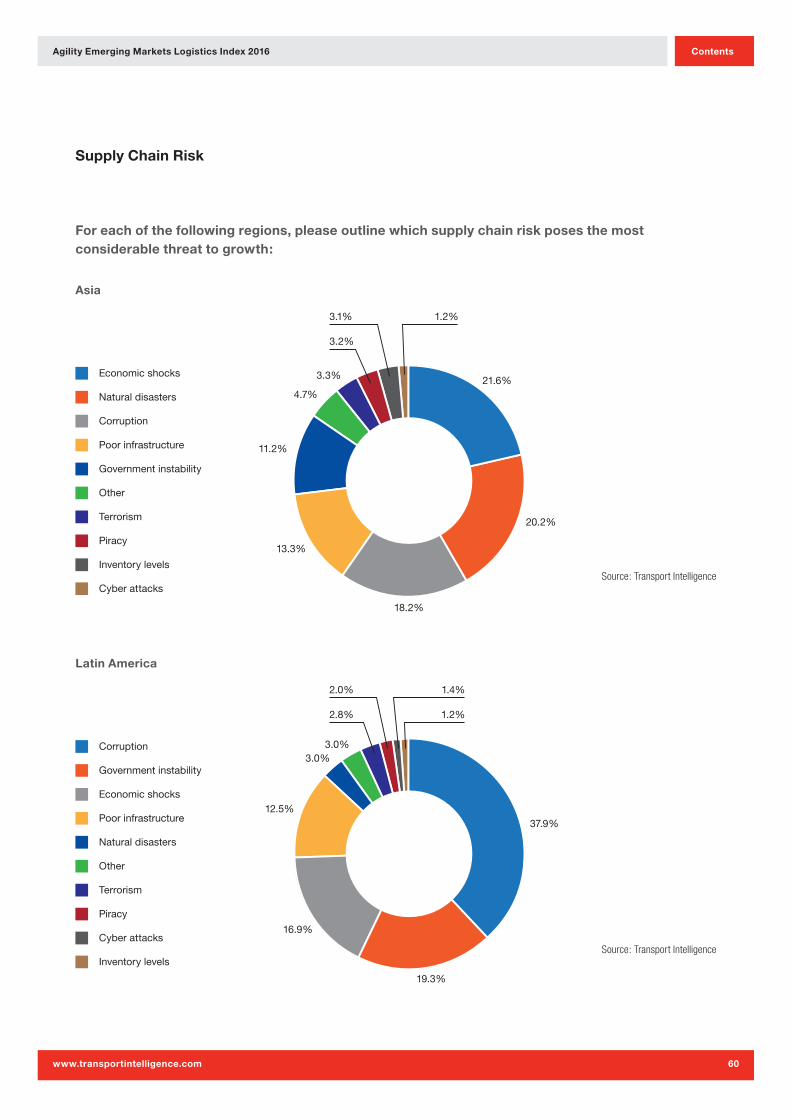

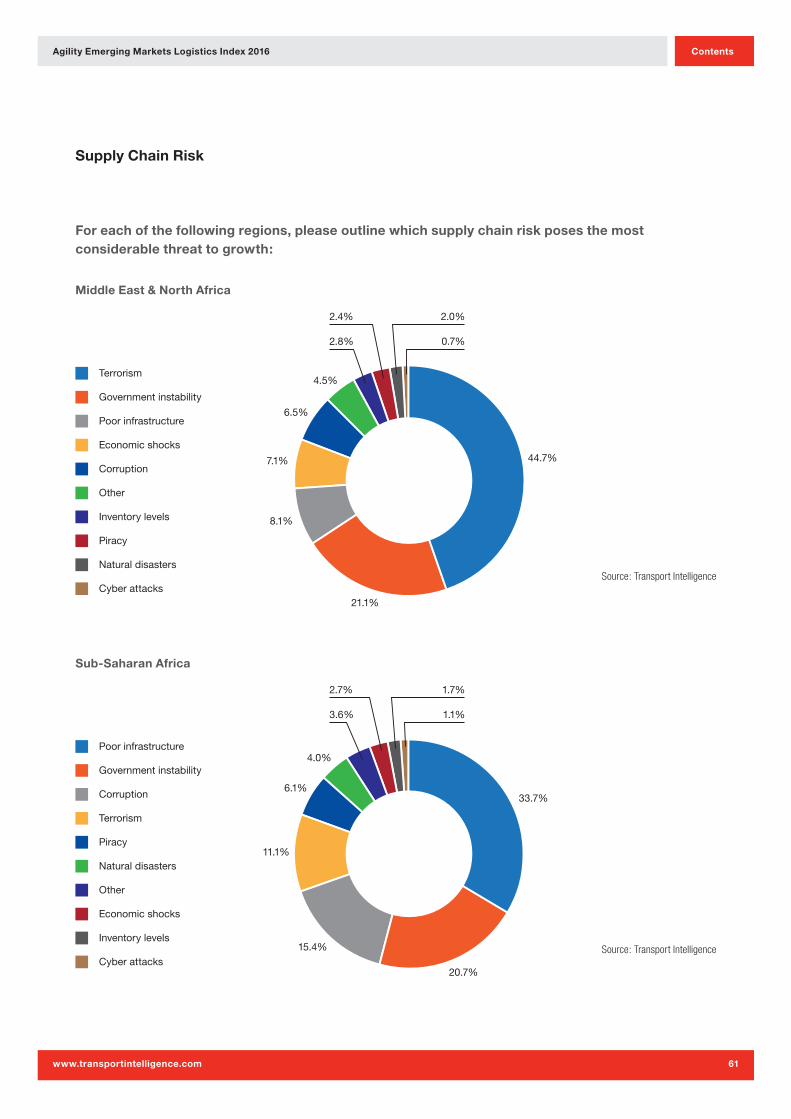

SupplyChainRisk 60

LeastAttractiveEmergingLogisticsMarkets 63

ProspectsforEmergingTradeLanes 65

Contents

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

3

Contents

VerticalSectors 66

MarketsforPotentialInvestmentovertheNextFiveYears 69

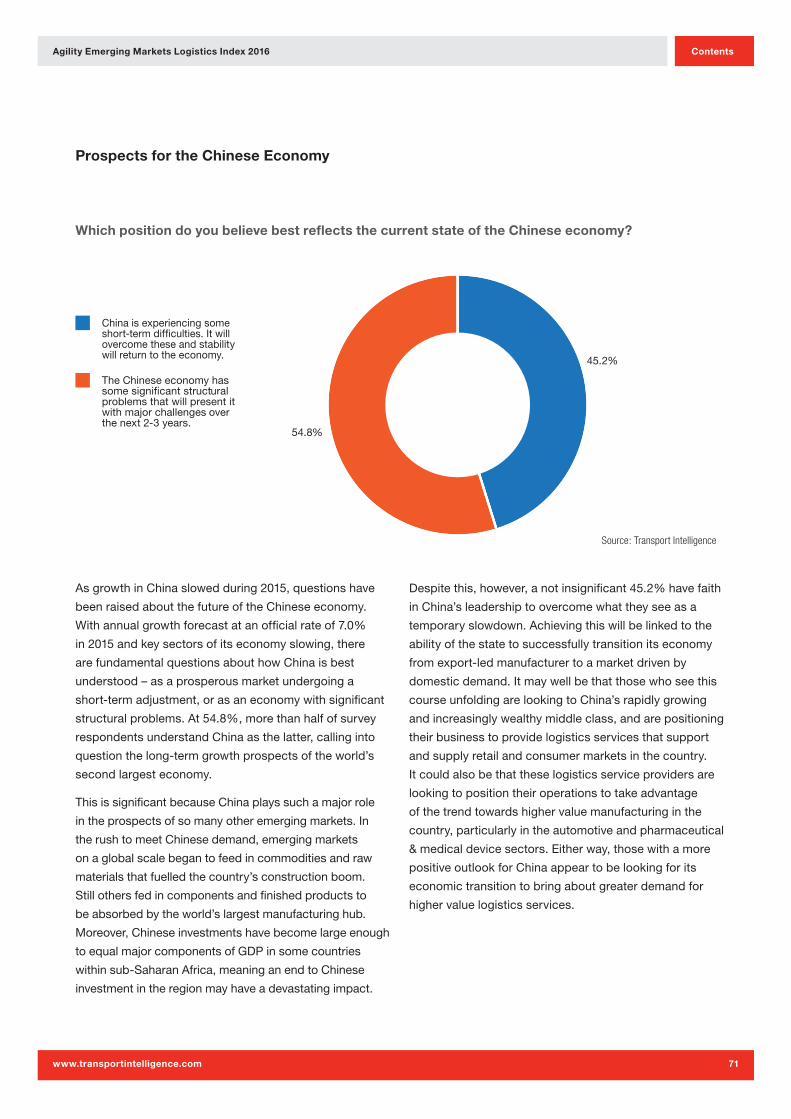

ProspectsfortheChineseEconomy 71

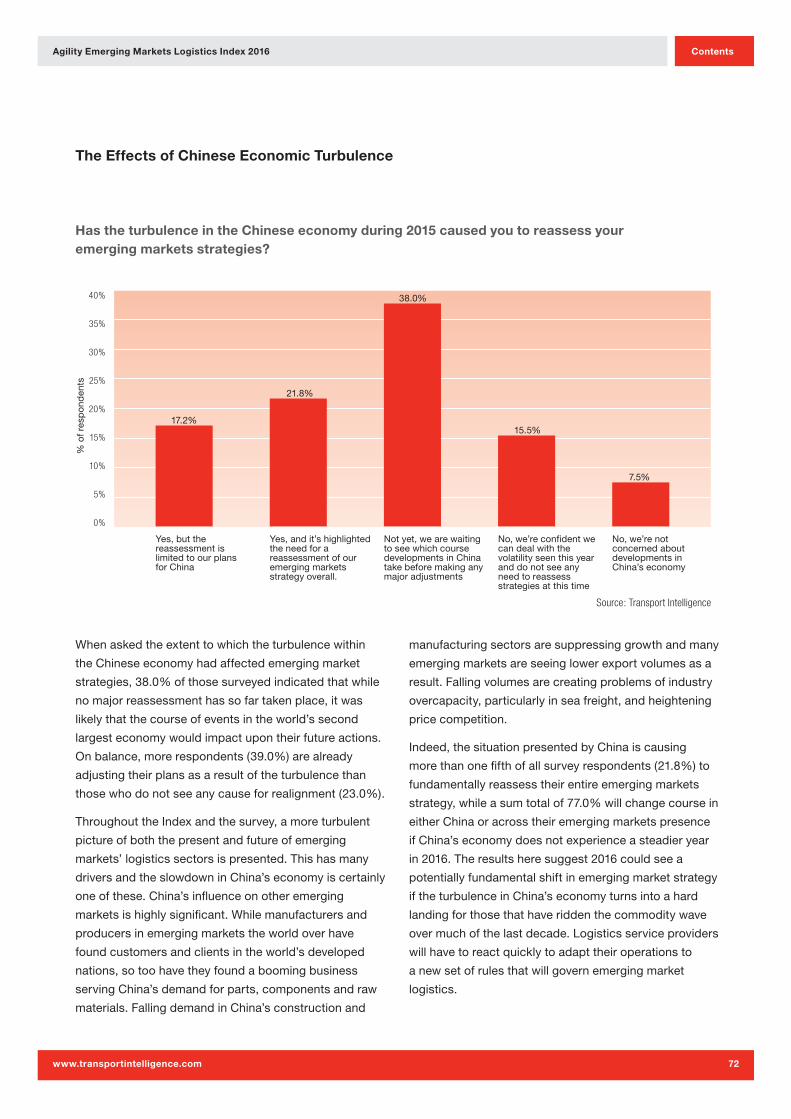

TheEffectsofChineseEconomicTurbulence 72

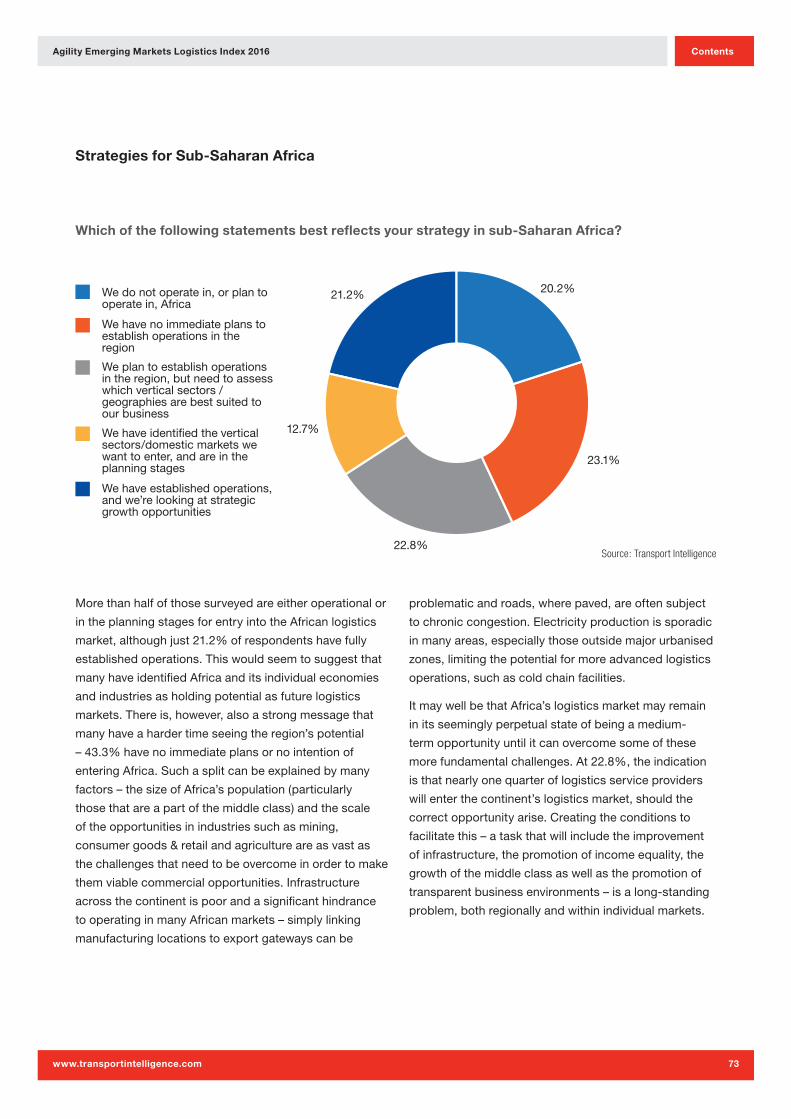

StrategiesforSub-SaharanAfrica 73

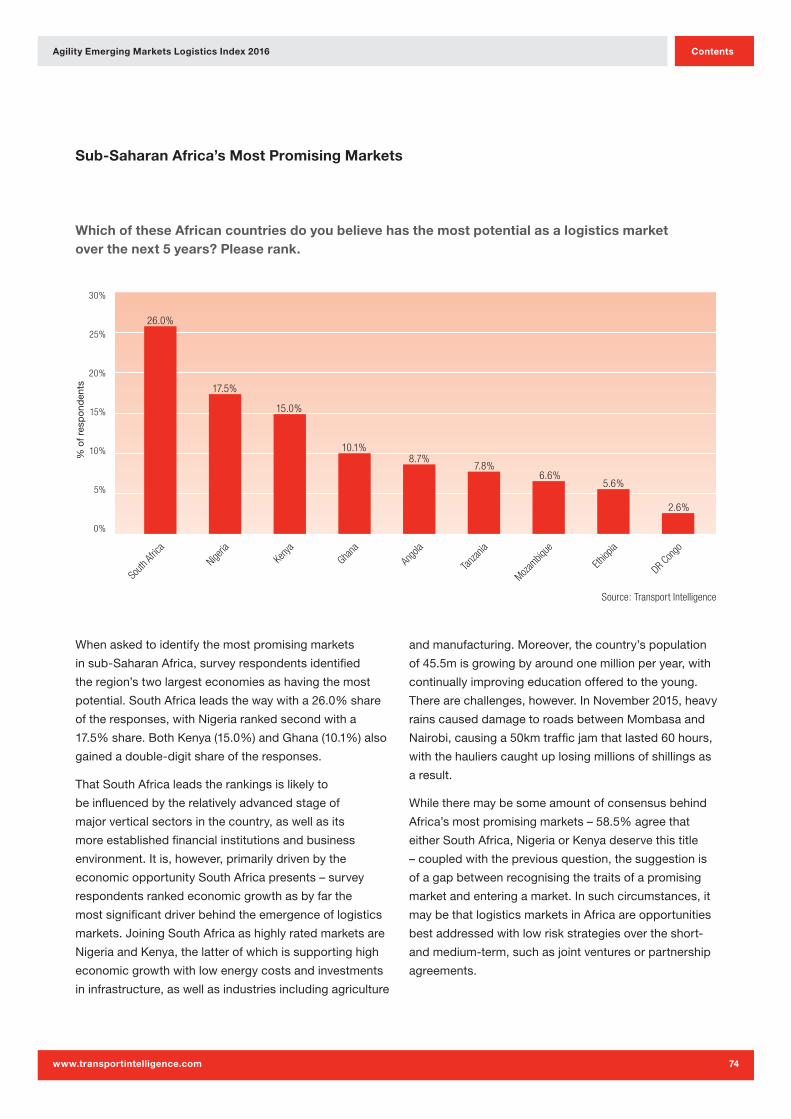

Sub-SaharanAfrica’sMostPromisingMarkets 74

DriversbehindtheEmergenceofSub-SaharanAfrica’sEmergingMarkets 75

ProspectsfortheBRICS 77

BarrierstoGrowthinBrazil 78

TheFutureofGrowthinIndia 79

Expectationsfor2016 80

MostSignificantDriversintheGlobalEconomy 81

ProspectsforEmergingMarketGrowth 82

Section 9: About Agility and Transport Intelligence 83

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

4

The Agility Emerging Markets Logistics Index

Essa Al-Saleh, CEO & President Agility Global Integrated Logistics (GIL)

NationalReviewmagazinerecentlynotedthatforthefirst

timeinhistorylessthan10%oftheworld’spopulation

livesinextremepoverty,currentlydefinedassubsistence

on$1.90adayorless.Forcontext,in1990,37.1%of

theworld’speoplelivedinextremepoverty.Emerging

marketswere–andstillare–hometothemostofthe

world’spoor,butthepaceofchangeandprogressin

thosecountrieshasbeennothingshortofbreathtaking

overthepast25years.That’simportanttoremember

afterayearlike2015,whichwascharacterizedby

fallingtradevolumes,depressedcommoditypricesand

geopoliticalinstabilitythatcombinedtoslowgrowth

inemerginganddevelopedmarketsalike.Emerging

marketsgrowth,4.6%in2014,slowedto4.2%in2015,

accordingtotheInternationalMonetaryFund.TheIMF

forecastsapickup–to4.7%–in2016.

In2015,thelonebrightspotamongthelargestemerging

markets,theso-calledBRICS,wasIndia.India,which

tookinitialstepstoenactlong-promisedreformssuchas

taxsimplificationandregulatorystreamlining,overtook

John Manners-Bell, CEO Transport Intelligence

Theworld’seconomyisstillrivenbyinstability,as

marketscometotermswiththehangoverleftbythe

globalfinancialcrisisof2008-9andthesubsequent

downturnwhichencompassedEurozoneeconomies.

Emergingmarketshavenotbeenimmunetotheworld’s

economicmalaise,withChinainparticulardowngrading

itseconomicgrowthprospectsascommodityprices

slumpandexportsstagnate.WithChinasuffering,its

tradingpartnersacrosstheregionarealsoaffected.On

topofthisastrongerUSeconomyhasmeantaflightof

capitalfromEasttoWest,whichhasledmanyemerging

countriestoincreasetheirinterestrates,dampening

domesticgrowthfurther.

Theunderlyingeconomicproblemshavehad

consequencesfortheinternationalfreightsector.Air

andseavolumeshavebeenweakduetotheslowdown

ininternationaltrade.ShippinglineMaersknowexpects

globaldemandforseabornecontainertransportation

toincreaseby1-3%in2015,downfromitsprevious

expectationof3-5%announcedinitsQ12015report.

One

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

5

Chinaastheworld’sfastest-growingeconomy.Russia

andBrazilexperiencedsharpcontractions.Asagroup,

countriesinSub-SaharanAfricalostmomentumafter

severalyearsofstronggrowth,despitevitalityinEthiopia,

IvoryCoastandTanzania.Theyear-longpersistence

ofcheapenergypricesamountedtoa$450billion-

plustransferofwealthfromproducingcountriesto

consumingeconomies,anenormousboontoconsumers.

Butlowpricesalsostalledambitiousenergyprojects,

particularlyinAfrica,whereoilandgasfindshavethe

potentialtoacceleratedevelopmentandbringdramatic

improvementsinlivingstandards.

Theglobaleconomyrodethecoattailsofemerging

marketsgrowthforadecadeormoreaheadofthe

2008crisis.Withtheslowdowningrowthin2015,some

economistsexpressedconcernthatemergingmarkets,

52%ofglobalGDPinpurchasingpowerterms,could

becomeadragontheworldeconomy.Thatdoesnot

havetobethecase.Billionsofpeoplelivinginemerging

marketscountriescontinuetoworktheirwayinto

theglobalmiddleclass.Theirdesireforbetterjobs,

healthcare,high-qualityeducationandelevatedliving

standardsshouldcontinuetopropelgrowthinemerging

markets,especiallythosecountrieswithyounger

populations.Wherepolicymakerstakestepstoenhance

tradeandimprovethebusinessclimate–streamlining

regulations,protectinginvestors,attackingcorruption,

strengtheningcontractlawandpropertyrights,easing

capitalrestrictions,andnurturingentrepreneursand

smallbusiness–prosperitywilltakerootandemerging

marketscountrieswillbevital,durablelinksinregional

andglobalvaluechains.

Perhapsmostworryinglyofall,theOECD’slatest

economicoutlookwarnsthatglobaltradegrowthwillbe

just2%in2015,downfrom3.4%in2014.

However,itisnotallbadnews.Chinaismuchmore

resilientthanmanywouldbelieve.Ithastheeconomic

resourcestobeabletorideoutthetransientproblems

whichitcurrentlyfaces.Althoughtherewillbea

slowdowningrowth,thechancesofafull-scalerecession

seemoverblown.

Otheremergingmarketsmaynotbesolucky.Brazil,for

example,isnotnearlyasrobustasChinaandissuffering

substantiallyfromaneconomywhichhasnevermaterially

diversifiedfromitsrelianceonnaturalresources.

Transportinfrastructureisweak,againincontrastwith

China,andbusinessishamstrungbycorruptionand

bureaucracy.

Smalleremergingmarketsalsohavesystemicfiscal

problems.Malaysia,forexample,issufferingfromsevere

indebtedness.Russiaisstrugglingduetolowcommodity

pricesandtheeffectsoftradesanctionsimposedby

theEUandUS,andTurkeyhashighinflationandlarge

foreigndebts.

However,lookingtothelongerterm,thingsarenotasbad

astheymayatfirstseem.Althoughlowoilpriceshavea

detrimentalimpactonmanyproducersinthedeveloping

world,theyalsospurgrowthintheWest.According

totheIMF,worldGDPwillactuallygrowby3.6%in

2016.Thisissignificant,albeitlowerthanbeforethe

2008financialcrisis.Indiaisexpectedtogrowby7.3%,

takingoverthemantlefromChinaastheworld’sfastest

growinglargeeconomy,helpedbythefactthatitisa

consumerratherthanproducerofoil.Mexicoisalsoina

muchbetterpositionthanmanyotheremergingmarkets,

notleastbecauseofitsstrongtieswiththeUSandthe

benefitsitisgainingfromthenear-sourcingstrategiesof

USmanufacturers.

Morethanever,itseems,investorsinemergingmarkets

havetobediscerning.WhenTiestablishedtheAgility

EmergingMarketsLogisticsIndexin2010,itspurpose

wastodifferentiatebetweencountrieswhichofferedthe

bestopportunitiesduetotheirfarsightednessintermsof

infrastructureinvestment,security,growthprospectsand

businessenvironment,andthosewhichlaggedbehind.

ThebasisfortheIndexremainsasrelevantnowasitwas

then,providingclarityinaconfusingandcomplexworld.

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

6

Sources

TheAgilityEmergingMarketsLogisticsIndexhasthree

maincomponents–theIndexcountryrankings,major

tradelanesbyvolumeandmodeoftransport,anda

surveyoftradeandlogisticsprofessionals.

DatafortheIndexcountryrankingscomesfromthe

InternationalMonetaryFund,OrganizationofEconomic

CooperationandDevelopment,WorldBank,government

statisticalagencies,UnitedNationsandUNagencies,

WorldEconomicForum,InternationalTradeCentreand

InternationalAirTransportAssociation.

TradelanedatacomesfromtheUnitedStatesCensus

BureauandEurostat.

Two

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

7

Methodology

Definition of ‘Emerging Markets’

Theterm‘emergingmarkets’wasfirstcoinedbythe

WorldBank’sInternationalFinanceCorporation(IFC)in

1981.Accordingtoitsdefinition,anemergingmarketis

acountrymakinganefforttoimproveitseconomywith

theaimofreachingthesamelevelofsophisticationas

nationsdefinedas‘developed’.Anemergingmarketis

furthercharacterisedbytheIFCasmeetingatleastone

ofthetwofollowingcriteria:

1.Itisalowormiddleincomeeconomy,asdefinedby

theWorldBank

2.Itsinvestablemarketcapitalisation(IMC)islowrelative

toitsmostrecentGrossDomesticProduct(GDP).

The Agility Emerging Markets Logistics Index

TheAgilityEmergingMarketsLogisticsIndexusesthree

metricstoassessandrank45emergingmarkets.The

metricsmeasurethecountries’:

•Marketsizeandgrowthattractiveness(50%ofoverall

Indexscore)

•Marketcompatibility(25%ofscore)

•Marketconnectedness(25%ofscore).

Market size and growth attractiveness(MSGA)rates

acountry’seconomicoutput,itsprojectedgrowthrate,

financialstabilityandpopulationsize.

Market compatibilityratesemergingmarketsaccording

totheirmarketaccessibilityandbusinessregulation,

foreigndirectinvestment(FDI),marketriskandsecurity

threats,aswellastheleveloflikelydemandforlogistics

servicesbasedonthecountry’seconomicdevelopment.

Marketcompatibilityisablendof:

•Acountry’sdevelopmentthroughtheimportanceofits

servicesector–indicativeofthelevelofoutsourcingof

logisticsservices

Thre

e

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

8

•Urbanisationofpopulation–adriverofmanufacturers’

centraliseddistributionstrategiesandthelikely

consolidationofretailing

•Distributionofwealththroughoutthepopulation–

indicativeofthewidespreadneedforhighervalue

goodsoftenproducedbyinternationalmanufacturers,

asmeasuredbytheGiniIndex

•ForeignDirectInvestment(FDI)–anindicatorofthe

penetrationofaneconomybyinternationalcompanies

•Marketaccessibility–howeasyitisforforeign

companiestoenterthemarketanddealwithexisting

bureaucracyandregulation

•Security–thismeasurestherisktocompanies’

operationsfromthreatssuchastheft,piracyand

terrorism.

Market connectednessassessesacountry’sdomestic

andinternationaltransportinfrastructureandhowwell

theyconnect.

Specifically,thisinvolves:

•Thefrequencyandrangeofdestinationsofitsliner

shippingconnections

•Thelevelofairportinfrastructurerelativetothemarket’s

size

•Aratingofitsoveralltransportinfrastructure

•Aratingoftheefficiencyofitscustomsandborder

controls.

The Agility Emerging Markets Logistics Index for Countries with GDP more/less than US$300bn

GDPismeasuredincurrentUS$.GDPdatahasbeen

obtainedfromtheWorldBank.

Trade Lanes

Thetradelanesectionmeasuresthevolumeofgoods

shippedbyairandseabetweentheemergingmarkets

includedintheIndexandtheUS/EU.Thetradelane

sectionincludestwoparts:

1. Top 10 Trade Lanes – Air and Sea, Import/Export

Alistoftradelaneswiththehighestvolumes,as

measuredbytons,splitbyairandsea,andbyimport

andexport(fromemergingmarketstotheEU/USandto

emergingmarketsfromtheEU/US).

2. Fastest Growing Trade Lanes – Air and Sea, Import/Export

Forairandsea,byimportsandexports,thefastest25

growingtradelanesforeachcasehavebeenranked

bytheirgrowthin2015.Inaddition,anindexhasbeen

calculatedwithabaseyearof2005toofferalong-term

perspectiveoneachtradelane’sperformance.

2005-2014dataare‘actual’figures,whereas2015data

areforecastfiguresbasedonactualmonthlydatafrom

January-August2015.Aforecastmodelwhichaccounts

forseasonalityhasbeenappliedtoestimatefull-year2015

figures.Forseafreight,tonnagerelatingtoHS2product

group27“mineralfuels,mineraloilsandproductsoftheir

distillation;bituminoussubstances;mineralwaxes”has

beensubtractedfromtotalfigures.Noproductgroups

areexcludedfromairfreightfigures.Toqualifyasoneof

the25fastestgrowingtradelanes,acertainvolumemust

bereached.Forseafreighttradelanesthisthresholdis

1milliontonnes.Forairfreight,itis10,000tonnes.This

preventsrelativelyinsignificanttradelanesenteringthe

rankings.

CAGRshavebeenusedtomeasureeachtradelane’s

performance.CAGRstandsforCompoundAnnualGrowth

Rate.Itmeasurestheconstantannualpercentagegrowth

rateofatimeseriesbetweenaparticularstartandend

point.WhileCAGRscanbeaquickandusefulwayto

analysemediumandlong-runperformance,cautionshould

betakenastheycanoftendisguisevolatility.Inspectionof

eachyear’sindexvalueovertimerevealsvolatility.

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

9

Key Findings

Emerging Markets: How Logistics Executives See Them

Nearly 1,200 supply chain and logistics executives

worldwide shared their views on the 2016 global

economic outlook, prospects for emerging markets, key

growth drivers and trends affecting emerging markets

countries.

•Thesupplychainindustryisbracingformorevolatility

intheglobaleconomy.Alargemajorityofindustry

executives(61%)areunclearonthedirectionofthe

worldeconomyorindicatetheyexpectmoreturbulence.

TheirtoptwoconcernsareoilpricesandChina’s

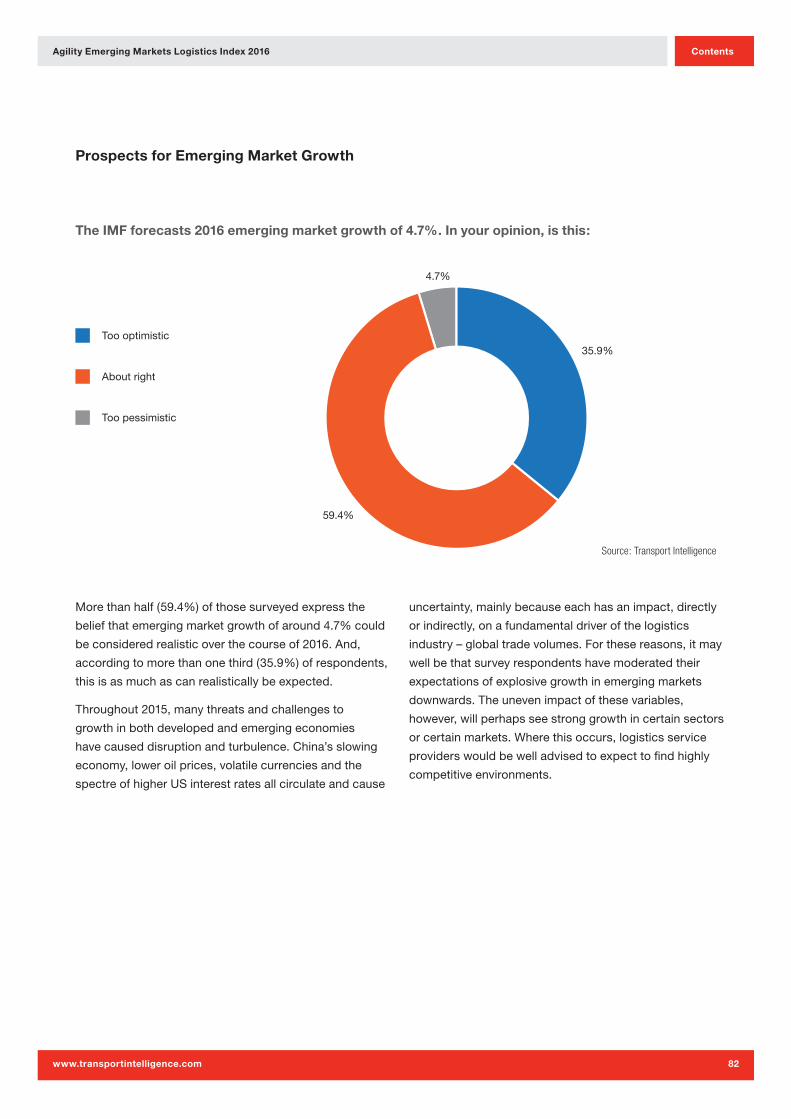

economichealth.Atthesametime,most(59.4%)feel

theIMFwas“aboutright”inforecasting4.7%growthfor

emergingmarketsin2016

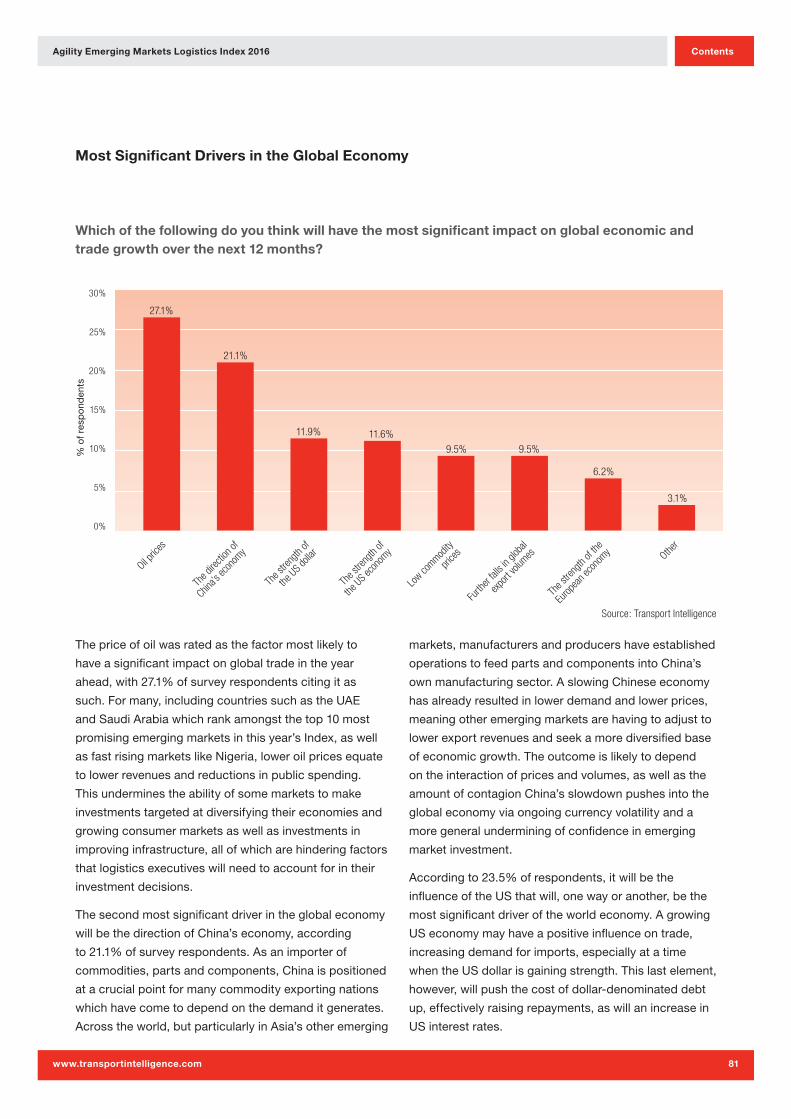

•Globaleconomicprospectsin2016areheavily

dependentontheUnited States,intheviewofindustry

executives.AfteroilpricesandChineseeconomic

vitality,respondentssaidthemostsignificantdriversof

theglobaleconomywillbethestrengthofthedollarand

thehealthoftheUSeconomy

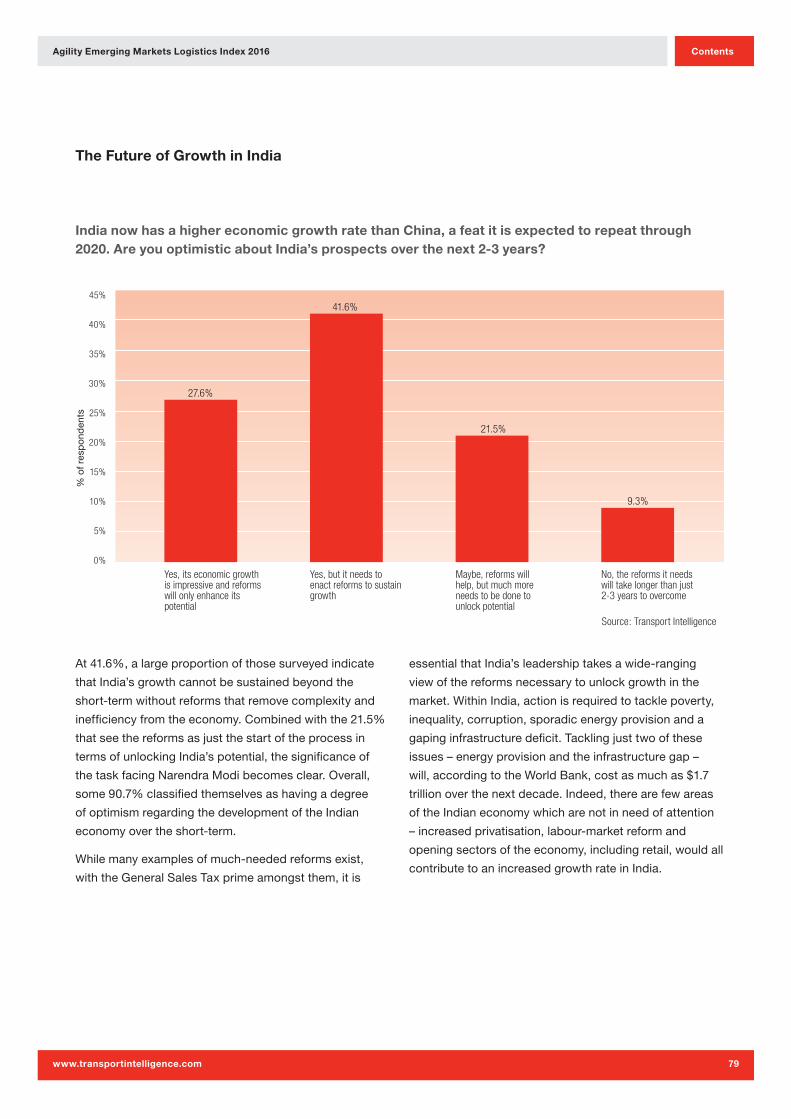

•Forthefirsttime,supplychainindustryprofessionals

seeIndiaastheemergingmarketscountrywith“the

mostpotentialtogrow”asalogisticsmarketoverthe

nextfiveyears.IndiaedgedoutChina,whichwasseen

asthemarketwiththemostpotentialinpastsurveys.

Indiaalsoclimbedtwospotsto3rd,behindChina

andUAE,inthedata-drivenAgilityEmergingMarkets

LogisticsIndex.Itsrisewaspropelledbyaninitial

roundofeconomicreformsandasurgingeconomy.

Whileoptimistic,logisticsprofessionalsalsoremain

cautiousaboutIndia.Nearly42%saidIndianeedsmore

structuralreformtosustainitscurrentgrowthandmore

than21%saidthecountryneedsmorethaneconomic

reformifitistounlockitspotential

•LogisticsexecutivesareintriguedbyIran’semergence

frominternationalisolationandanticipateopportunity

andgrowthwiththephasedliftingofmosteconomic

sanctions.Inthe2016survey,Iranmovesup12spots

(from27thto15th),asapotentialmajorlogisticsmarket

overthenextfiveyears.Iranalsoleaptfrom35thto

16th,amongmarketsforpotentialinvestmentoverthe

nextfiveyears

Four

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

10

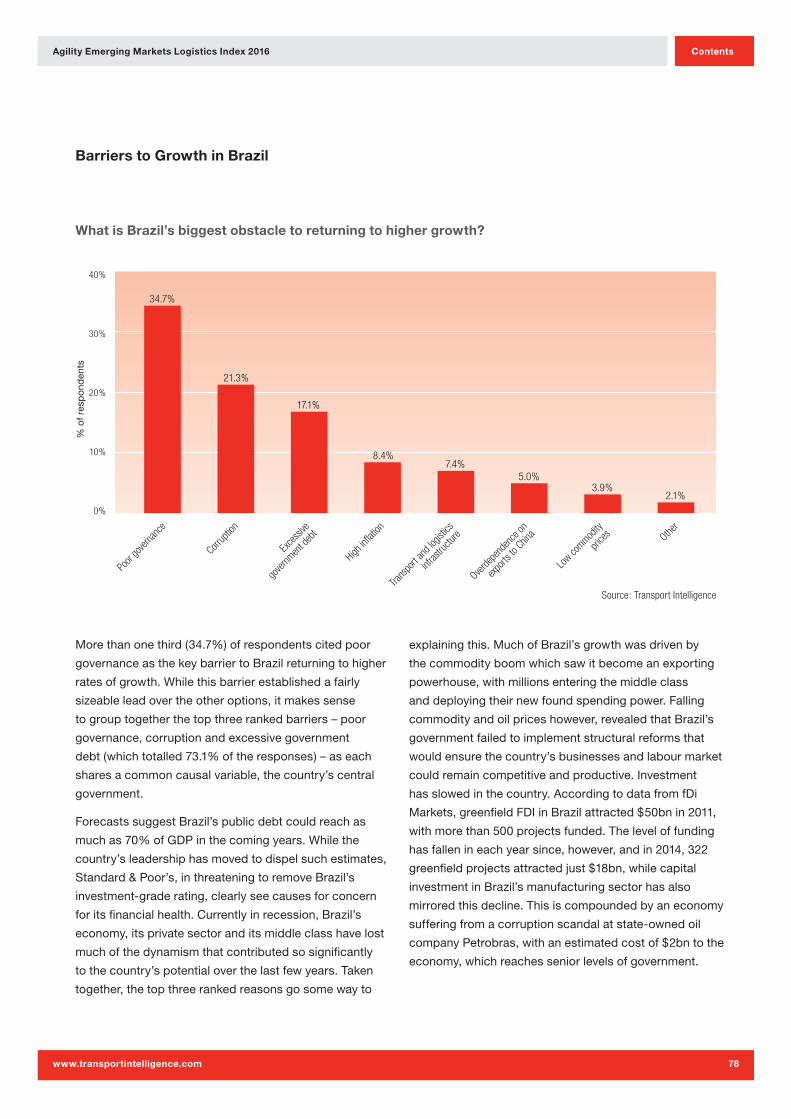

• Brazilremainsanappealinglogisticsmarkettoalarge

percentageofindustryexecutives,againrankingas

thethirdmostattractiveemergingmarketamongthose

surveyed.Butsentimenthassouredamongsome,

whoputBrazil17thamongemergingmarketswith

theleastpotentialasamajorlogisticsmarket.Nearly

35%ofsurveyrespondentscitedpoorgovernance

asthekeybarriertoBrazil’sreturntohighergrowth

rates.Takentogether,thetopthreebarriers–poor

governance,corruptionandexcessivegovernmentdebt

–drew73.1%ofresponses,anindicationthatindustry

executivespinblameforBrazil’scurrentrecession

mainlyonthecentralgovernment

•Economicgrowthratesareagain,byfar,theleading

choiceasthe“keydriver”thatmakesacountryan

importantemergingmarket(30%).Foreigndirect

investmentwaspickedasthe2ndmostsignificantdriver

andgrowingtradevolumeswere3rd.Atthebottomofa

12-itemlistweretheabilitytobeanear-sourcingmarket,

lackofcorruptionandstrongsecurity

•Industryprofessionalsseecorruptionasthebiggest

problemassociatedwithdoingbusinessinemerging

markets,eventhoughtheydon’tconsider“lackof

corruption”tobeakeydriverthatmakesacountryan

importantemergingmarket.Thissuggeststhatindustry

professionalsunderstandthattheywillencounter

corruptioninemergingmarketsandhavestrategiesto

dealwithit

•Forthefirsttime,logisticsprofessionalsseeeconomic

shockastheleadingsupplychainriskinAsiaPacific,

reflectingconcernabouttheeffectofaslowingChinese

economyandthepotentialforarippleeffectinthe

region.Inthepast,industryprofessionalsviewed

naturaldisastersandcorruptionandthetopthreatsto

Asia’ssupplychains.Morethanhalf(54.8%)oflogistics

professionalsnowbelievetheChineseeconomyfaces

majorchallengesoverthenexttwotothreeyears.

Asignificantpercentage(38%)isreassessingits

Chinastrategy,asaresult.SluggishnessinChinahas

prompted22%tore-examinetheirbroaderemerging

marketsstrategy

•Logisticsprofessionalsbelievethatsupplychainrisks

varybyregion,althoughgovernmentinstabilityisnear

thetopofthelistinmostregions.InLatinAmerica,

corruptionremainsthetoprisk.IntheMiddleEastand

NorthAfrica,terrorismisthebiggestconcern.InSub-

SaharanAfrica,poorinfrastructuretopsthelist

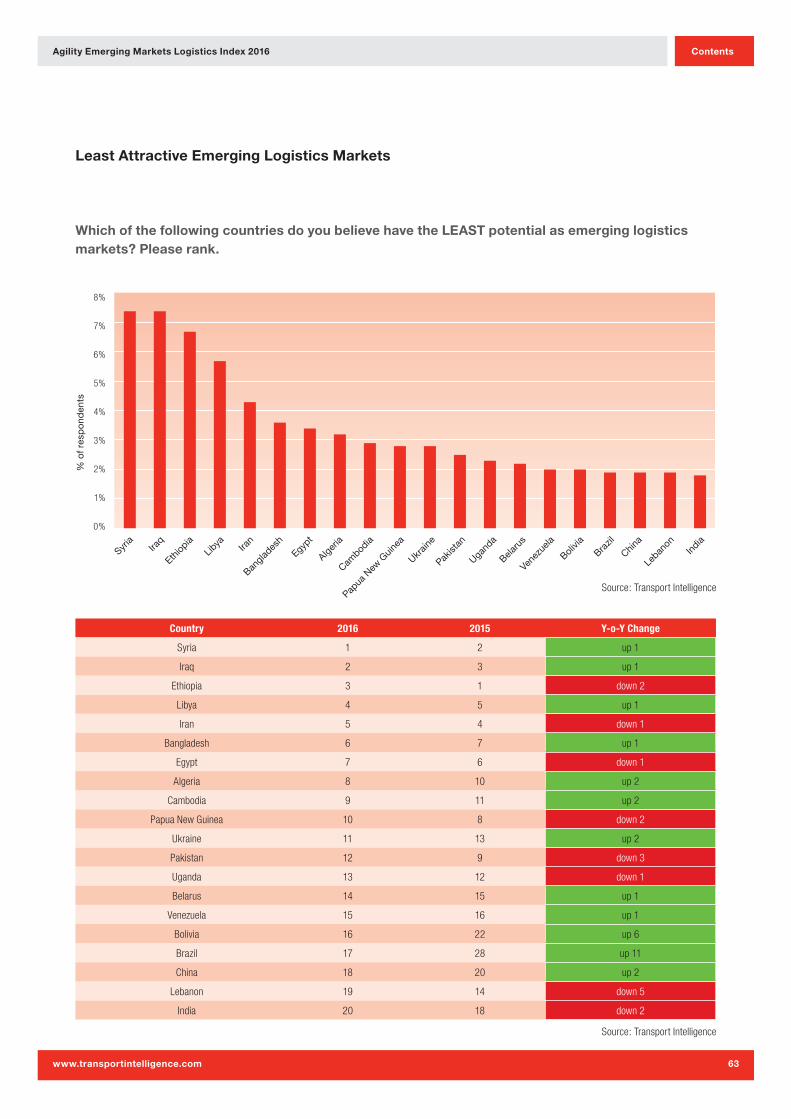

•Notsurprisingly,countriesgrippedbywar,sectarian

conflict,politicalinstabilityorinternationaleconomic

sanctionswereidentifiedbysurveyrespondentsas

havingtheleastpotentialasemerginglogisticsmarkets:

Syria(1st),Iraq(2nd),Libya(4th)andIran(5th).There

werethreenotableexceptionsamongthe20countries

identifiedastheleastattractivemarkets:Ethiopia(3rd)

isridinganexportboombutisalsosufferingitsworst

droughtindecadesandfacingpowercuts.Bolivia(up

sixspotsto16th)wasjarredbytheannouncementthat

PresidentEvoMoraleswantstochangetheconstitution

inordertoseekre-electionandstayinpoweruntil2025.

Brazil(up11spotsto17th)isinthemidstofarecession

andexperiencinghighunemploymentandinflation.

PresidentDilmaRousseff,whowantstoraisetaxes

andcutspending,isentangledinamassivecorruption

scandal

•TradeflowsbetweenAsianmarketsremainthemost

promisingintheeyesoflogisticsprofessionals.Atthe

sametime,theyshowedincreasedoptimismabout

prospectsforgrowthalongotherkeyAsiantrade

routes:Asia-NorthAmerica,Asia-AfricaandAsia-

MiddleEast.SentimentaboutAsia-SouthAmericatrade

andSouthAmerica-NorthAmericatradeslippedfroma

yearago

•Industryprofessionalscontinuetoviewthebiggest

emergingmarkets(China,IndiaandBrazil)asripestfor

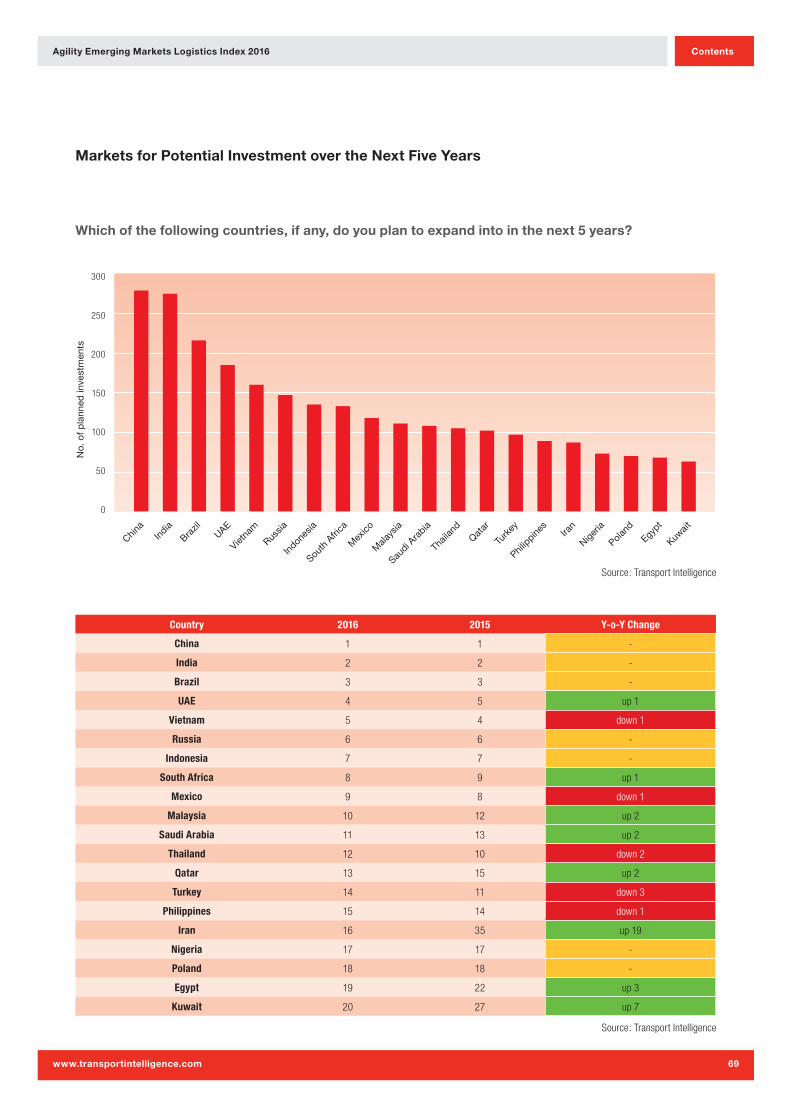

investmentoverthenextfiveyears.Butmanyareclearly

intriguedbyIran.Iranleapt19spotsto16th,among

marketswiththebiggestinvestmentpotential.Turkey,hit

byslowinggrowth,fallingexportsandinstabilityalongits

southernborder,droppedthreespots,to14th.Kuwait,

whichcontinuestoinchtowardsprivatisationofkey

state-ownedenterprises,climbedsevenspotsto20th

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

11

•Inspiteofrecentgrowthandsurgingforeigninvestment,

Sub-SaharanAfricaremainstheemergingmarkets

frontier,aplacewhereonlytheboldarepreparedtodo

business.Just21.2%ofrespondentsindicatedthey

haveestablishedoperationsinSub-SaharanAfrica.

Another12.7%saidtheyareintheplanningstagesto

entermarketsthere.Morethan43%saidtheyhaveno

planstoestablishoperationsinSub-SaharanAfrica

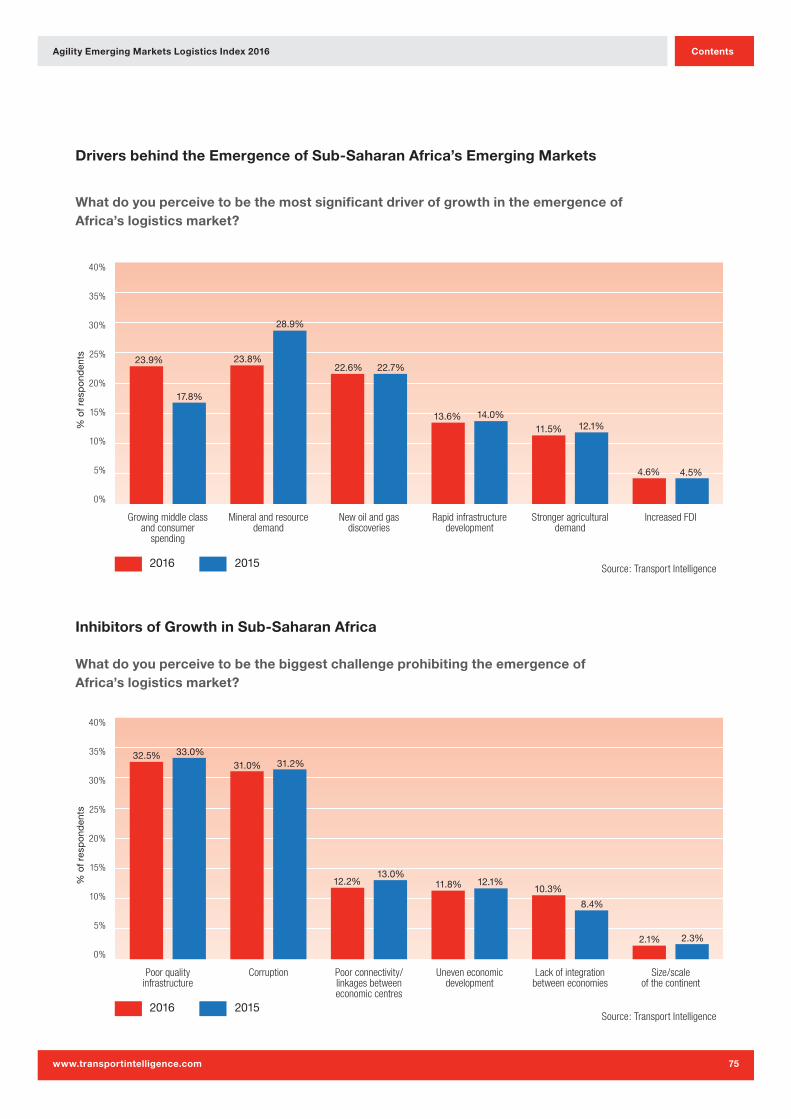

•South AfricaandNigeria,Sub-SaharanAfrica’stwo

largesteconomies,areviewedbylogisticsprofessionals

asthemostpromisingmarkets,followedbyKenyaand

Ghana.Forthefirsttime,industryprofessionalssee

consumerspendingbyAfrica’sgrowingmiddleclass

asamoreimportantdriverofgrowththanmineraland

resourcedemand.Poorinfrastructureandcorruption

remaintheleadinginhibitorstogrowth,survey

respondentssaid.

Markets on the Move

•Volatilityintheglobaleconomywasmirroredinthe2016

AgilityEmergingMarketsLogisticsIndex.Eightofthe

top10emergingmarketseconomiesshiftedplaces.

Chinaremainstheleadingmarketbyalargemargin,in

spiteofthefactthatitseconomyisslowing

•Amongthetop10emergingmarkets,thecountries

takingstepstodiversifyandenacteconomicand

businessreform–UAE(2nd),India(3rd)andMalaysia

(4th)–leapfroggedthecommodity-dependent

economiesofSaudi Arabia(5th),Brazil(6th)and

Indonesia(7th),allofwhichslidthreespots

• Nigeria(17th)andEgypt(22nd)bothjumped10

spots,thelargestimprovementbyanycountrysince

theIndexwasfirstpublishedin2010.Inthecaseof

Nigeria,businessesandinvestorshavebeguntogeta

truerpictureofitsperformanceandpotentialwiththe

recalibrationofitsnationaleconomicstatistics.Ayear

ago,logisticsprofessionalsindicatedtheyweregrowing

moreoptimisticaboutEgypt,eventhoughthecountry

slippedfourspotsinthe2015Index.Inthe2016Index,

Egypt’sperformancehascaughtupwithsentiment,the

resultoffaster-than-expectedgrowthandanimproving

businessclimate.Algeria–upfourplacesto30th–

wastheotherbrightspotinNorthAfrica

•Byfar,theemergingmarketsbestbusinessclimate–or

marketcompatibility–isfoundinUAE.Atthesame

time,theUAEboaststhebest“connectedness”–a

gaugeofinfrastructureandtransportconnections.As

aresult,UAEranksastheworld’s2ndmostpromising

emergingmarket,eventhoughitseconomyisdwarfed

bythatofChina(25timeslarger),India(fivetimeslarger)

andBrazil(sixtimeslarger)

•Amongthesmalleremergingmarketseconomies

(lessthan$300bnGDP),Chilecontinuestobethe

topperformer,basedonitsstrongbusinessclimate,

infrastructureandtransportconnections.Qatarand

Omanscorehighestamongsmallereconomiesfortheir

businessenvironment

•ThepicturewasgloomierinLatinAmerica.SeveralLatin

countriesdroppedsharplyintheIndex.Inadditionto

Brazil(whichfellthreespotsto6th),Uruguaydropped

fourspotsto24th,Colombiaslippedthreespotsto25th,

Peruplungedfiveplacesto28thandArgentinadropped

fivespotsto31st.Venezuelacontinuesitseconomic

freefall.Itdroppedthreespotsto39th.Twenty-three

ofthe29countrieswithsmallereconomiesoutrank

VenezuelaintheIndex.ElsewhereinLatinAmerica,only

Paraguay(upthreeto35th)andBolivia(upthreeto

38th)improvedtheirIndexrankingssignificantly

• Russia,increasinglyisolatedeconomicallysinceit

beganbackingrebelsineasternUkraine,fellfrom7thto

9thintheIndex.Ukrainefellfourspotsto34th.

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

12

BIGGEST MOVERS1 Egypt2 Nigeria3 Algeria4 Malaysia5 UAE6 Bolivia7 Paraguay8 India9 Pakistan10 Sri Lanka

UPBIGGEST MOVERS1 Argentina2 Peru3 Jordan4 Ukraine5 Uruguay6 Brazil7 Indonesia8 Morocco9 Saudi Arabia10 Venezuela

DOWN

1

2

3

4

5

67

8

9

10

8

7

2

6

51

10

9

4

3

Source: Transport Intelligence

Markets on the Move

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

13

Trade Lanes

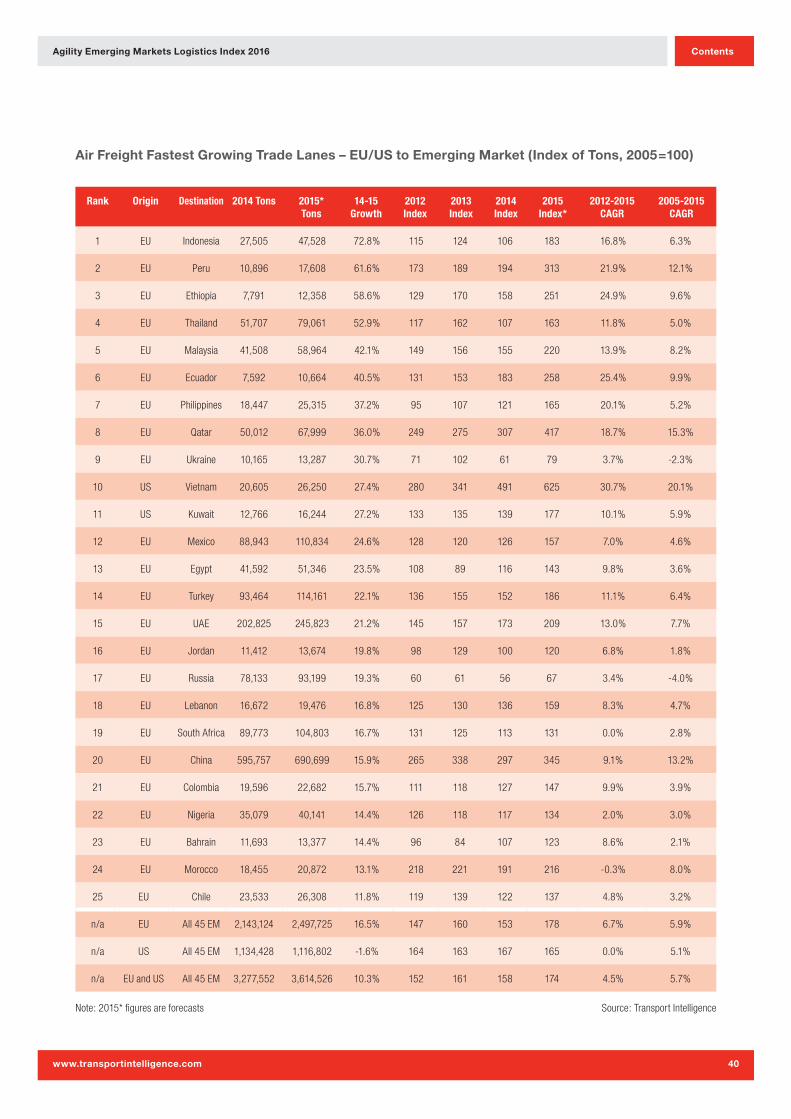

Air Freight to Emerging Markets

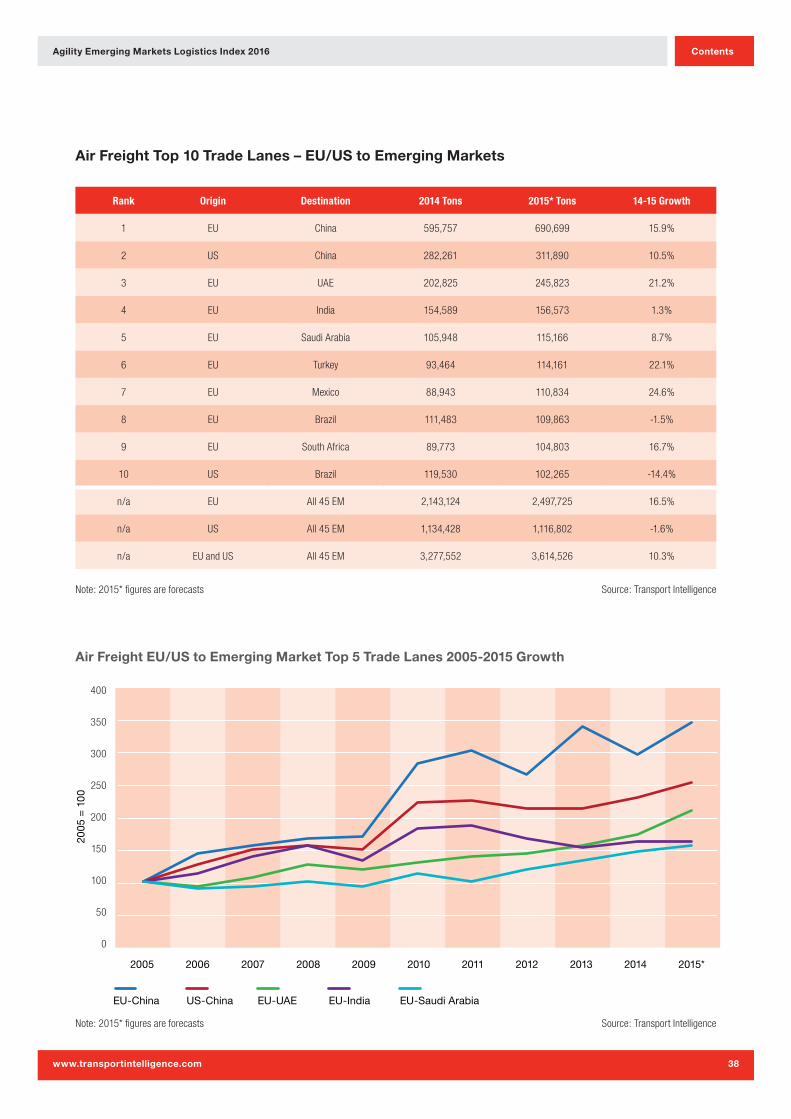

Thebusiestemergingmarketsairfreighttradelanes

originatingintheEUorUStendtoconnecttolarger

marketsintheIndex:China,UAE,India,SaudiArabia,

Turkey,Mexico,BrazilandSouthAfrica.Volumealong

theselanesgrewbydouble-digitmarginsinmanycases.

TheexceptionswereEU-Brazil(down1.5%)andUS-

Brazil(down14.4%).

Theninefastest-growingairlanesinvolveEUorigins.

ThetopfivewereEU-Indonesia(up72.8%),EU-Peru(up

61.6%),EU-Ethiopia(up58.6%),EU-Thailand(up52.9%)

andEU-Malaysia(up42.1%).

EUairshipmentstoemergingmarketsareonpaceto

growby16.5%forfull-year2015,butUSairshipmentsto

thosesamemarketslooksettoshrinkby1.6%.

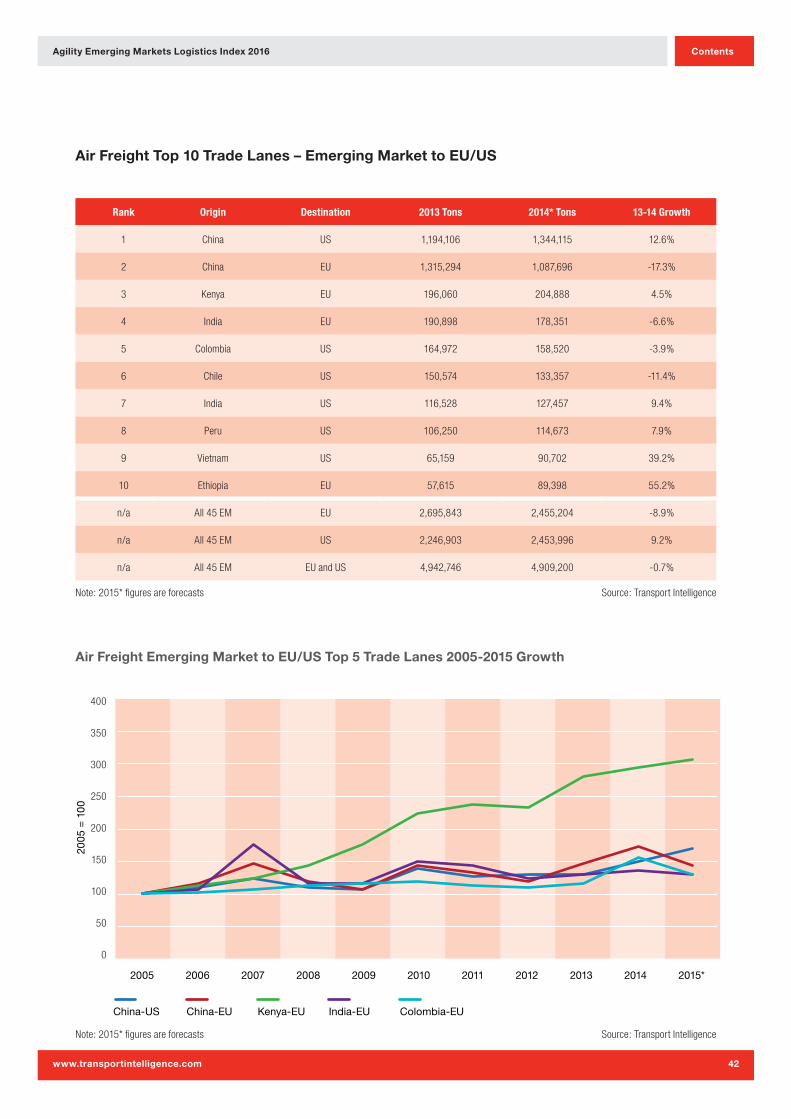

Air Freight from Emerging Markets

Flowingintheotherdirection–fromemergingmarketsto

theEUandUS–thepicturewasmixed.Alongthebusiest

airlane,China-USairfreightgrew12.6%.Volumeon

the2ndlane–China-EU–fell17.3%.Thelargestgains

amongtop10laneswereVietnam-US(up39.2%)and

Ethiopia-EU(up55.2%).

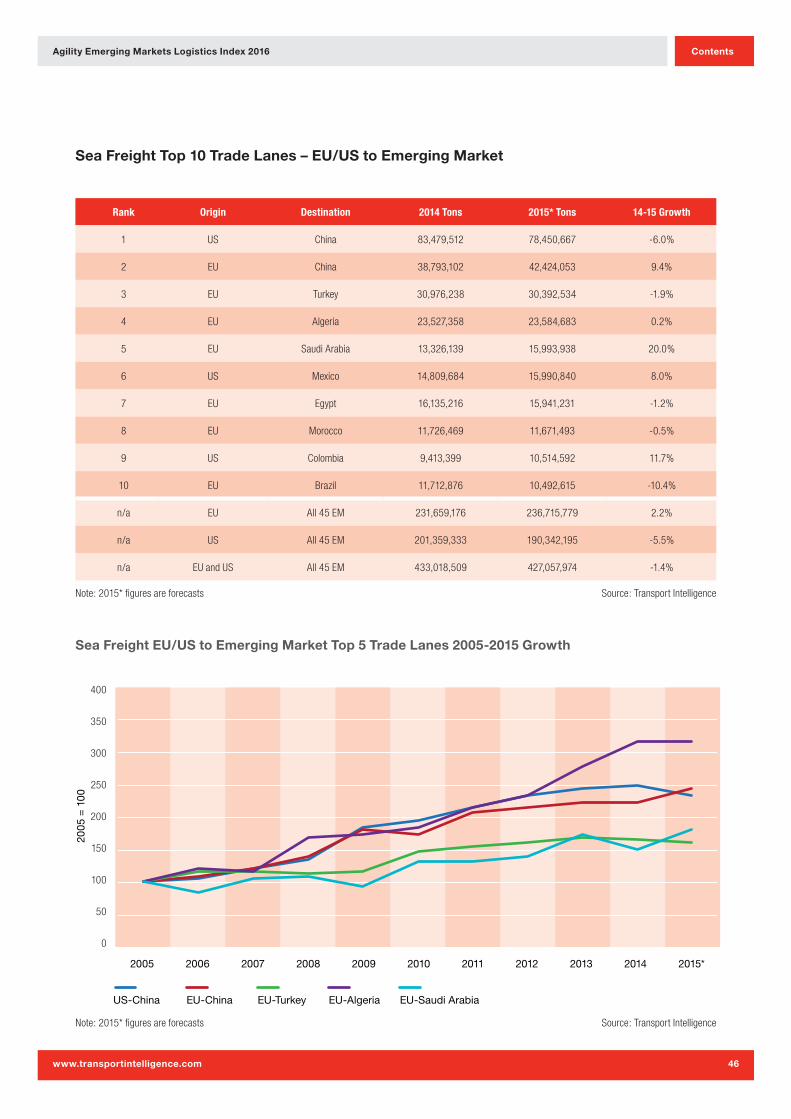

Ocean Freight to Emerging Markets

Inoceanfreight,thelargestlaneconnectsUSoriginswith

destinationsinChina.Tradealongthatlanefell6%.The

EU-Chinaoceanlaneexperienceda9.4%increasein

volume.Elsewhere,EUoceanshipmentstoSaudiArabia

(up20%)andUSshipmentstoColombia(up11.7%)

showedthemostgrowthamongthetop10lanesinvolving

EU/USoriginsandemergingmarketsdestinations.Along

laneswithlessvolume,thebiggestincreasescamein

EU-Bangladesh(up107.4%),US-Pakistan(up76.6%),

EU-Oman(up59.4%)andEU-Kenya(up57.4%).

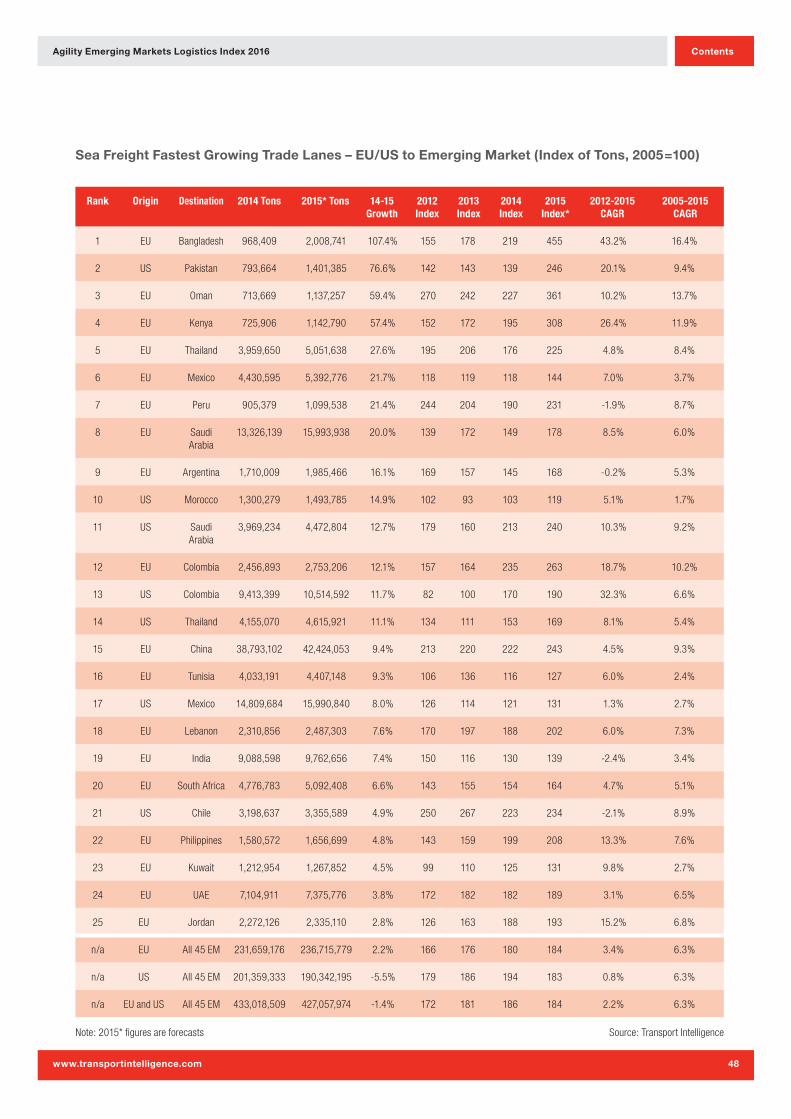

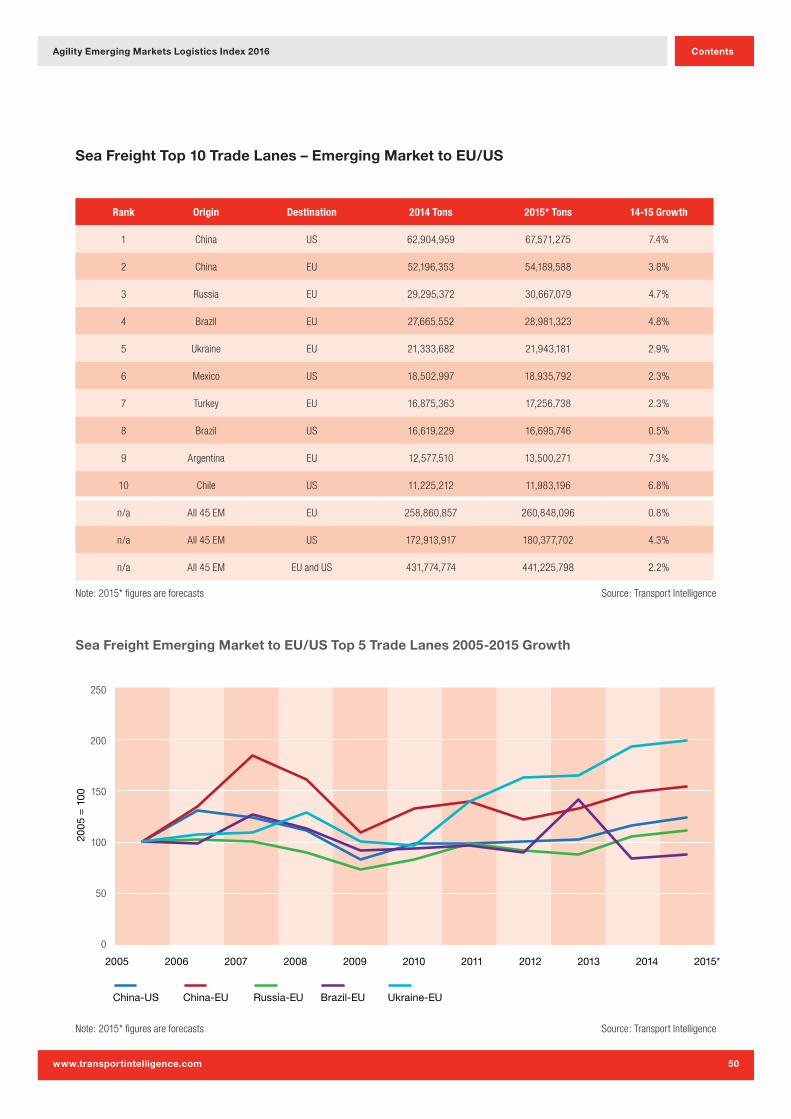

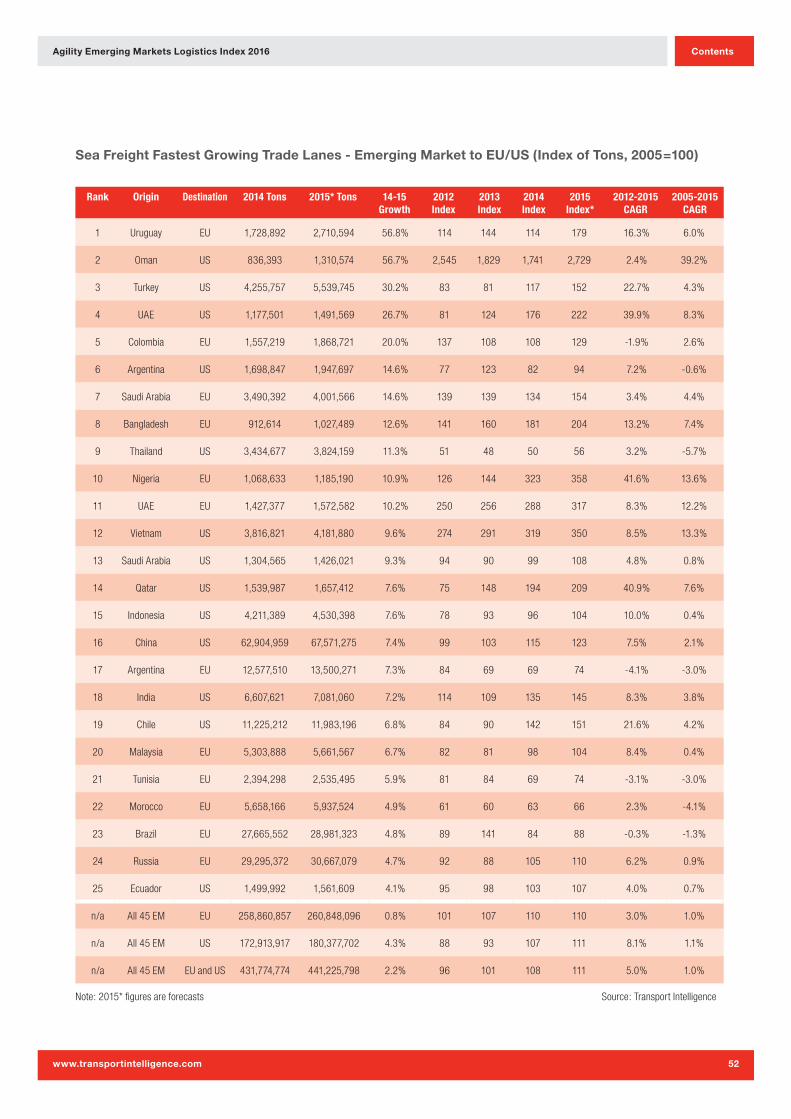

Ocean Freight from Emerging Markets

Alongthetopoceanlanescarryingemergingmarkets

freighttotheEUandUS,growthwasmoremodest.The

biggestgaincameinthebusiestlane:China-USvolume

wasup7.4%.

Anumberoflaneslinkingemergingmarketswiththe

EUandUSgrewspectacularly,butmostgainscameoff

relativelysmallbasevolumes:Uruguay-EU(up56.8%),

Oman-US(up56.7%)andTurkey-US(up30.2%).

EUoceanfreightfromemergingmarketsoriginswasflat

(upamere0.8%).USoceanvolumefromIndexcountries

grew4.3%.

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

14

Overview & Outlook

Emergingmarketshavebecomeincreasinglyimportant

totheworld’seconomy,takingonrolesasmanufacturing

hubs,outsourcingdestinations,transhipmentpoints

betweenproductionandconsumption,andforsome,

aspotentialconsumermarketshometomillionsof

consumersenteringthemiddleclasseachyear.These

rolesbecamevastlymoresignificantfollowingthefinancial

crisisin2008,whichhighlightedthealreadycompelling

commercialopportunitiesandcostadvantagesoffered

tomanufacturers,retailersandlogisticsserviceproviders

inavastarrayofindustriesandsub-sectors.Asweenter

2016,however,apotentmixofeconomicheadwinds,

marketturbulence,andsocialandpoliticalpressureshave

threatenedthecapacityofmanyoftheworld’shighgrowth,

highpotentialemergingmarketstofulfiltheirpromise.

Theyearaheadwillbringwithitnewfounduncertainty

andcomplexityinemergingmarkets,andthoseoperating

inmanyofthesehighlypromisingmarketswillhaveto

navigateathirdphaseofthewiderglobaleconomic

traumathatfirstappearedin2008.AsAndyHaldane,

ChiefEconomistattheBankofEngland,explained,

phaseonecamein2007-2008,whenbankslenttoo

muchwithouttheprotectionofsufficientcollateral.Phase

twooccurredduring2011-2012,withtherealisation

thatlendingintheEurozonewasofferedonthefalse

assumptionthatallcountrieshadequalcapacitytorepay,

culminatingwithmassiveroundsofquantitativeeasing.

Now,weareinwhatcanbecharacterisedasthethird

phase:theneedtoadjusttoaneraoflowertradegrowth,

loweroilandcommodityprices,andaloomingendto

cheapcreditproppinguptheglobaleconomy.

Whileactsoneandtwooftheglobaleconomicturmoil

ledtomanypainfulmoderationsandadjustmentsin

developednations,theybroughtaboutaboomperiodfor

emergingmarkets.China’seconomicoutput,forexample,

totalled$4.56trillionin2008,accordingtoWorldBank

figures.By2014,thatfigurehadskyrocketed127%to

$10.36trillion.Itisgrowthonthisscalethathasproven

soattractivetoinvestors,butaswemoveinto2016,

thetwodecadesofspectaculargrowththatpropelled

Chinatobecometheworld’ssecondlargesteconomy

alreadyseemlikeadistantmemory.Whilethecountry

lookstoreorientitseconomytoplacedomesticdemand

andconsumermarketsatthecentreofitsnextstageof

development,emergingmarketsthatgearedtheirown

developmenttowardsservingChinesedemandforparts,

componentsandcommoditiesmustalsoadjust.

Five

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

15

LowerChinesedemandissignificantforanumberof

reasons,notleastbecauseitlowersthepriceofgoods

andmaterialsthatexport-orientedemergingmarketssell.

Forthesemarkets,lowercommoditypriceshaveresulted

inlowerexportrevenues,lostjobsandcurrencyvolatility.

Onemeasureoftheextentofthecollapseinrawmaterials

pricesinthisdecadecomesfromTheEconomist’s

compositecommodity-priceindex,whichhasplunged

fromafigureofaround240nearthestartof2011,to

just140inthemiddleof2015,implyingadecreaseof

approximately40%overtheperiod.Netoilexporting

countriesareenduringparticularlydifficulttimestoo.At

theendofJune2014,theOPECBasketPriceforcrudeoil

wasaround$110.BytheNovember2015,thepricehad

sunkbelow$40,acrashofaround60%.

Emergingmarketcurrencieshaveenduredatorrid2015,

too,withsubstantialdepreciationsrecordedinalarge

numberofmarkets.AnalysisbytheFinancialTimes

showedthatthecurrenciesofRussia,Colombia,Brazil,

Turkey,MexicoandChilehavelostbetween20%and50%

oftheirvalueagainsttheUSdollar,sinceJune2014.This

hasoccurredforvariousreasons,withtheexpectation

ofaUSinterestratehikeandChina’sdecisiontodevalue

theyuancompoundingtheeffectsofreductionsinthe

quantitydemandedandpricesofcommodities,prime

amongstthem.Thefallingvalueofemergingmarket

currencieshasbeenespeciallydamagingbecause

ratherthanreapportioningafixedleveloftradebetween

winnersandlosers,theFT’sresearchsuggestscurrency

weaknesshasunderminedimports,asonewouldexpect,

buthasnothadanybeneficialimpactonexportvolumes.

Additionally,thefallinthevalueofcurrencyhasmeantthat

foreign-denominateddebtthatemergingmarketsholdhas

suddenlybecomemoreexpensivetoservice.

Debtheldinemergingmarketsisalsopresentinghigh

levelsofrisk.Indeed,theseverityoftheemergingmarket

debtproblemisdifficulttocomprehend.TheIMF’s

October2015GlobalFinancialStabilityReportwarnedthat

corporatedebtofnon-financialfirmsinmajoremerging

marketshasmorethanquadrupled(from$4trilliontoover

$18trillion)from2004to2014,aperiodwhichalsosaw

averageemergingmarketcorporatedebt-to-GDPratios

increaseby26percentagepoints.Suchanexpansion

ofdebtisnotsurprisinggivengrowthinemerging

marketsandthelarge-scaleroundsofquantitative

easingamongstadvancedeconomiesthatcreatedvast

amountsofcheapcreditalliedwithlowinterestrates,

overtheperiod.Buttheobviousriskthispresentsis

whenglobalfinancialconditionsinevitablytighten,as

interestratesrise.Debtservicingcostswillalsorise:a

problemalreadyexacerbatedbydepreciationofemerging

marketcurrencies.Onthisbasis,theIMFhaswarnedthat

emergingmarketsshouldbraceforariseincorporate

failures.Ontheothersideofthecoin,accordingto

researchbyMoody’s,theshareofdebtheldintheworld’s

largestemergingmarketsindomesticcurrencytermshas

jumpedfromjustover50%,tojustunder75%,inthepast

15years.Thiswillhelptoprovideinsulationforexposed

emergingeconomiesandmeans,whiledebtisdefinitelya

problem,itcouldbefarworse.

Thefinalstormthatemergingmarketsareweatheringis

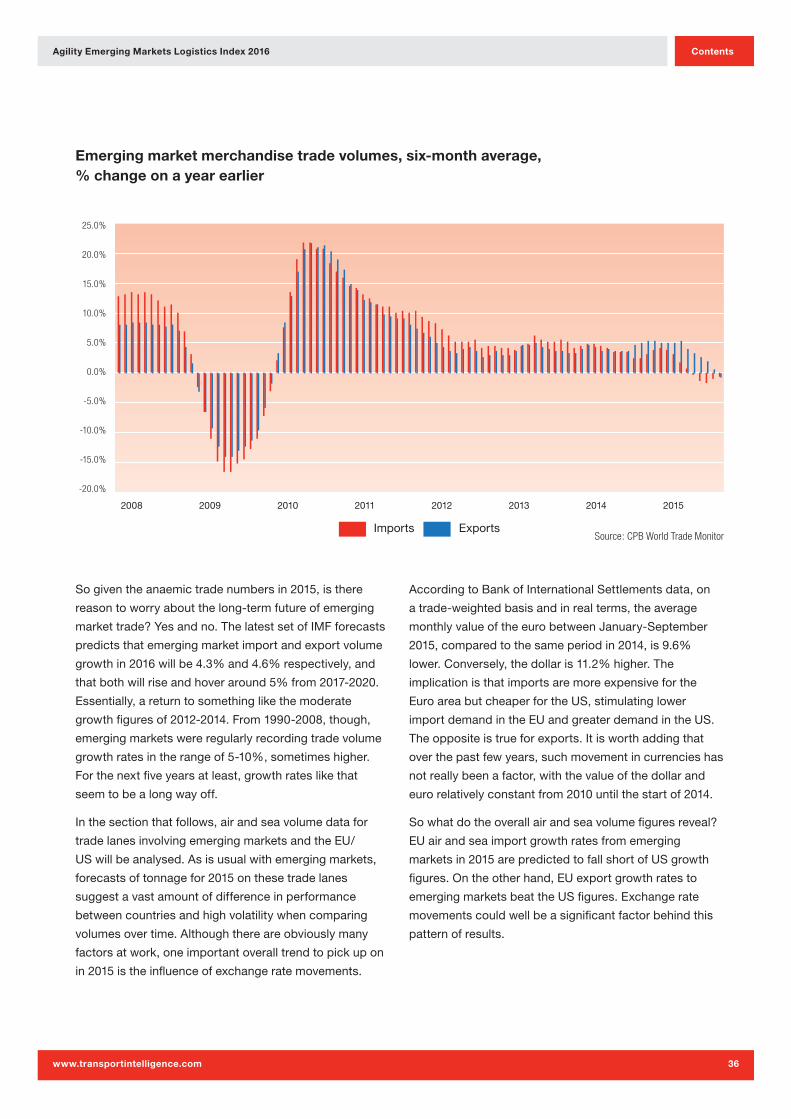

tumblingtradevolumegrowth.For2012to2014,import

andexportvolumegrowthinemergingmarketsaveraged

4.7%and4.2%respectivelyonasix-monthmoving

averagebasis,withrelativelylittlevariationaboveor

belowthosemarks.In2015,year-on-yeargrowthrates

havefallenwellshortofthesefigures,evendippinginto

negativeterritoryattimesinthesecondandthirdquarters

oftheyear.

But,while2015hasundoubtedlybeenachallengingyear,

forecastsfor2016aremorepositive.Themessagetotake

fromtheturmoilisthatthevolatilityandheadwindsof

thelast12monthsareproofoftheresilienceofemerging

markets.Manywillalreadyknowthatthetrendsseenin

2015arebettercharacterisedastornadosratherthan

tsunamis(theeffectsarenotbalanced,thevolatilitynot

universal)andthatrecoveryandsubsequentgrowthis

likelytobejustasuneven.Creatingvalueinthiscontext

requiresnotonlybusinessmodelsthatmanagethe

complexity,butalsomind-setsanddecision-making

modelsthatmanagethestormandempowerthosethat

understandtheuncertainty.

Asia Pacific

AsiaPacificcontinuestodominatethetopendofthe

AgilityEmergingMarketsLogisticsIndexin2016:seven

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

16

oftheregion’s11emergingmarketscoveredbythis

Indexplacewithinthetop20rankingspots.Despitethe

economicturbulenceoriginatingfromChina,onlyoneof

the11–Indonesia–seesitsrankingscorefall.

Theregionremainstheengineroomofglobaleconomic

development,withitsoutputexpectedtogrow6.5%in

2015.AccordingtotheWorldBank,EastAsiawillaccount

foraround40%ofalleconomicgrowthin2015,withthe

sub-region’semergingmarketsgrowing4.6%.Theseare

positivenumbersthatindicatestrongopportunitiesin

servingbothglobalmarketsaswellasdomesticdemand

ineconomieslikeChina,SouthKoreaandSingapore.

Indeed,itmaywellbethoseseekingtofacilitateintra-Asia

tradethatfindthebestopportunities,althoughthiswon’t

bewithoutitschallenges.Thegrowthincontainerisedsea

freightvolumesonintra-Asialaneshasseenanexplosion

ofcompetitionandforcedratesdown.Despitethis,the

outlookremainspositive.MOLLinerexpectsintra-Asia

reefervolumestogrow6%,addingaround1.3mextra

TEUalonetothelanein2015.Whilemoregenerally

costsremainlow,skillsamongsttheregion’slabourforce

areincreasingandsupplychainsarebecomingmore

sophisticated,thereforecreatingopportunitiestooffer

highervalueandhighmarginservices.Growingmiddle

classesamongstAsiaPacific’semergingmarketswill

furtheraddtodemand,aswilltheincreasedfreedomand

efficiencywithwhichASEANmemberstateswillbeable

totrade.

However,whiletheemergingmarketsofAsiaPacific

seemwellplacedtotakeadvantageofsuchtrends,

therearechallengesthatmustbeovercome.Economies

acrosstheregionarehavingtorapidlyadjusttoaslowing

Chineseeconomyandsubsequentfallindemandfor,and

pricesof,commodities.Moreover,theprospectofhigher

interestratesandastrongerUSdollar,especiallyagainst

weakeneddomesticcurrencies,areathreattothosewith

highlevelsofpublicorprivatedebt.Howeffectivelythese

issues,inadditiontoloweroilpricesintheregion’snet

oilexporterssuchasMalaysia,aremanaged,willplay

alargeroleinthefortunesofmarkets,manyofwhich

willbefacingtheirsternesttestsincethe1997-98Asian

FinancialCrisis.Reformsthatemphasisesustainable,

long-termeconomicgrowthmustbebalancedwith

robusteconomicmanagementthataddressesshort-term

challenges,structuralinefficiencyandinequality.

Latin America

ForthefirsttimeeverintheAgilityEmergingMarkets

LogisticsIndex,LatinAmericahasnopresenceinthetop

fiveIndexranking,asBrazilslippedto6thandMexico’s

improvedperformancewasonlystrongenoughtosee

itreach8th.Ofthe11LatinAmericanmarketsinthe

Index,sixfellintheoverallrankings,whiletheaverage

scoreacrossthemarketsdeclined.Allthreeothermajor

regionalgroupingssawanincreaseinaveragescore.

Itshouldperhapsbenosurprisethenthatanexamination

ofLatinAmericarevealsanumberofchallenges,with

lowercommoditypricesprimaryamongstthem.Lessening

Chinesedemandfortheregion’sexportsisamajordriver

ofthelowerprices,whichisfurthercompoundedbylow

oilprices,hittingproducerslikeVenezuelahard.Inthe

early2000s,growthratesofaround5%ormorewere

commonacrosstheregion.However,lowerprices,aswell

ascorruption(estimatedtocostMexicobetween5%-9%

ofGDP),poorinfrastructure(theIMFidentifiedBrazil’s

infrastructureashinderingdomesticintegration,export

performance,productivityandmarketefficiency)and

pooreconomicmanagementinvariousmarketsacross

theregion,havedriventheregion’sgrowthratedownto

around2%-2.5%,inmorerecentyears.Indeed,theIMF

hasevengonesofarastoforecastaslightcontraction

acrosstheregionin2015,withtheregion’slargest

economies–Brazil,VenezuelaandArgentinainparticular–

weighingdownthemorebuoyanteconomies.

Duringthe2000scommodityboom,LatinAmerica’s

middleclassexpandedbynearly50%.Thiscreatedvast

consumermarkets,butthestagnationoftheregion’s

economymeansitisatriskoffallingintoamiddle-

incometrapasrisingwagessapthecompetivenessof

highervalue-addedsectors.Achroniclackofadequate

infrastructureisalsoalimitingfactorintheregion’s

capacitytopropelitselfbacktohighergrowthrates,

asisalackofcompetitivenessandproductivityinkey

industrialsectors.Therearepositives,though.Coldchain

needsaregrowinginColombia,amajorglobalexporter

offlowers,whilethewideningofthePanamaCanalwill

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

17

createopportunitiesfortranshipmentoperationswithin

bothPanamaandsurroundingcountries.Mexico’s

proximitytotheUSanditsmembershipofNAFTAalso

boostitsprospectsastheUSgrows.

Middle East & North Africa

Forthesecondconsecutiveyear,theMENAregionis

representedin2ndsecondplaceintheoverallIndex,

althoughthistimebytheUAE.SaudiArabia,2ndinlast

year’sIndex,slipsthreeplacesto5th.The13MENA

countriesincludedintheIndexarespreadfairlyevenly

throughoutthe45rankingplaces.Thoseintheupper

half,broadlyspeaking,haveresourcewealthandpolitical

stabilityaspillarsofeconomicdevelopment.Progressing

downthelist,however,revealstheeffectsofinstabilityon

performanceasanemerginglogisticsmarket.Jordan(33rd),

Tunisia(36th),Libya(41st)andLebanon(42nd)haveall

seensignificantupheavalinrecentyears,eitherasaresult

oftheArabSpringin2011ortheongoingconflictsinSyria

andIraq.Theregion’smostimprovedperformerisalso

perhapsthemostillustrativeexampleofstability’simpact

onthefortunesofMENA’semerginglogisticsmarkets.

Egypt,havingreached18thpositionbeforetheonsetofthe

ArabSpring,slipped14positionsby2015,asstabilityand

securityacrossthecountryweakened,andconfidencein

thebusinessenvironmenteroded.In2016,though,Egypt

ranks22nd,havingrisen10placesoverthelast12months,

astheruleofGeneralAbdel-Fattahal-Sisihasrestoreda

measureofconfidenceinthemarketanditsgovernance,

evenifprogressinotherareasofsocietyisslow.

ThecontrastingperformanceofMENAcountriescreates

aclearpictureofjusthowsignificantstabilityistothe

emergenceofhighgrowth,highpotentiallogistics

markets.Whileitmaywellbefoundedonabasisof

stabilityassecurity(bothintermsofthephysicalsecurity

andeconomicstabilitythatresultfromstronginstitutions

implementingandenforcingruleoflaw),stabilityhere

alsomeanscontinuityagainstawidersetofthreatsthat

includefallingoilprices,short-termisminpolicymaking

andundiversifiedeconomies.Thosemarketsthathave

takenmeasurestoeitherreducedependenceonresource

wealthbyincentivisingactivityinotherindustrialareas,

astheUAEhas,orhaveimplementedsoundeconomic

managementduringbettertimes,suchasinSaudi

Arabia,arebestpositionedtohandlemorechallenging

conditions.Acrosstheregion,economicgrowthis

expectedtoreach2.9%in2015,solidlybelowthe4%-

5%experiencedbetween2000and2010.

Sub-Saharan Africa

JusttwomarketsfromSub-SaharanAfricareached

thetop20in2016:SouthAfricaandNigeria.Whilethis

performancehighlightsNigeria’sprogress(itmatched

Egyptbyrising10rankingpositions),aswellasthe

potentialoftheregionasalogisticsmarket,sub-Saharan

Africaisstillahighlychallengingenvironmentinwhichto

dobusinessandperformlogisticsservices.Thisismost

clearlydemonstratedbyfouroftheregion’ssixmarkets

occupyingpositionswithinthebottomninerankingspots.

Lowcommodityprices,andespeciallythelowprice

ofoil,arethreatstosub-SaharanAfrica’semerging

markets.Nigeria,amajorexporter,hasindicated

thatcapitalexpenditureswillfallaspartofarevised

budget,threateningthedevelopmentofmuchneeded

infrastructure.AndwhileSouthAfricashouldbea

benefactoroflowoilprices,energyshortagesandweak

investorconfidencehavesappeddynamismfromthe

country’seconomy.Moreover,SouthAfricaisalsofeeling

theeffectsofthefallincommodityprices,withthe

country’sminingsectorlosing23,000jobsbetweenApril

andAugust2015alone.

Toputtheregion’sacuteinfrastructurecrisisinto

perspective,theweightdraggingonproductivityinthe

worstaffectedareasinsomecountriesisestimatedto

reduceoutputbyasmuchas40%,atleastequaltothe

burdenimposedbycorruption,crimeandexcessive

bureaucracy.Providingaconsistentsupplyofpoweris

alsoasignificantchallenge.Indeed,the48countriesthat

makeuptheregionhaveapowergenerationcapacityin

linewiththatofSpain,whichhasapopulationtotalling

roughly5%ofsub-SaharanAfrica’s.Whilethese

challengesandtheireffectsareunevenacrosstheregion,

theydemonstratethescaleandsalienceoftheproblems

sub-SaharanAfrica’semergingmarketshavetosolve.

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

18

The 2016 Agility Emerging Markets Logistics Index

The Top 10

Theupheavalcausedbytheglobalforcesthathave

shapedmuchoftheemergingmarketlandscapeover

thelast12monthsarestarklyillustratedwithinthehigh

degreeoffluctuationseeninthisyear’stop10ranking.

Forseveralyears,thosecountriesrankedattheupper

endoftheIndexlookedtobeslowlyedgingawayfrom

therestofthepack.Theywere,withintheIndexat

least,stableintheirpositionasagroupofemerging

marketsthatappearedtooffertheverybestmixof

economicrobustness,commercialopportunityand

accesstobothdomesticandglobalmarkets.Results

in2016,however,appeartoshowasplitbetweenthese

markets,highlightingthosebestpositionedtomanage

macroeconomicturbulence,andthosemorevulnerableto

globalmarketforcesandeconomicheadwinds.

Fiveofthetop10rankedmarketsmovedbyatleast

threepositions,whilejusttwo–ChinaandTurkey–are

inunchangedpositions.Comparingthefourmarketsthat

rosewiththefourthatsank,thedifferencecanlargely

beattributedtotheeffortsmadetocreatediversified

andmodernisedeconomiesoverthecourseofthe

2000s.TheUAE,whichrosefourpositionstorank2nd

overall,isaprimeexampleofthis.TheEmirates’ability

tobothunderstandandplaytoitsstrengths(primarily

itsgeographicpositionasastrategictransithublinking

eastandwest,itsvasthydrocarbonendowmentand

therevenuesgeneratedtherein,anditsabilitytocreate

abusinessenvironmenthighlyattractivetoforeign

investment)hasbeencentraltoitsabilitytoachieve

thisranking.FormanyorganisationsoperatinginUAE–

includinglogisticsandtransportationserviceprovidersas

wellasmanufacturers–anetworkof34freetradezones

offersfullforeignownership,nodirectbusinesstaxation,

noexchangecontrolsandnolimitsontherepatriation

ofcapital.Whatisthereforeanalreadyhighlyattractive

businessenvironmentisfurthercomplementedwitha

largepoolofmigrantlabour,includingbothskilledand

low-costworkers.Inshort,theUAEhastakensignificant

stepstocreatetheconditionsforlogisticsservice

providers,andtheirclients,tosucceed.

Asimilarpatternofeconomicdiversificationcanbe

seeninMalaysia,anothermarketrisingfourplaces

intheIndextoachieveitshighesteverranking.Once

amarketdominatedbytheexportofrawmaterials,

Six

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

19

Malaysiahastransformedintoanopeneconomyand

becomealeadingglobalexporterofelectricalappliances,

partsandcomponents,aswellaspalmoil.Alsorising,

althoughfollowingastutteringattemptateconomic

diversification,isMexico,whichgainedonepositionto

rank8th.Nationalised75yearsago,Mexico’soilindustry

wasopenedtoprivateinvestmentinmid-2014,justas

oilpricesplunged.TheexpectedfloodofFDIintothe

sectorwasstymiedandthecountry,whichreliesonoil

revenueforaroundonethirdofitsoutlays,islikelytocut

publicspending,includingoninfrastructureprojects,

asaresult.Thecountry,though,isabletoperformwell

becauseithasstrengthsinotherareas.Itsmanufacturing

sectorishighlydevelopedandoffersbothproximityto

theUSandthecapacitytoproducehighvaluegoods

withlabouravailableatbroadlysimilarcoststoChina.

SuchcompetitiveadvantageshaveseenFDIinMexico’s

automotivesectortotal$20bnsince2010,withfDi

MarketsdatashowingthatMexicohasovertakenChina

intermsofmarketshareofinvestmentintheglobal

automotiveindustry.

Thefinaltop10markettoriseisIndia.Itsreturntothe

top3forthefirsttimesince2013demonstratesjusthow

uneventhecountry’sgrowthhasbeen.Attheheartof

theundulationinitsfortunessitsstiflinginefficiency,the

bestexampleofwhichcanbefoundinthedireneedfor

thestill-pendingGoodsandServicesTax(GST).India’s

currenttaxregimeeffectivelycreates29sub-national

marketswithinthecontinent-sizednationandrequires

checkpointsonmajortransportationlanesthatcreate

queuesoftrucksanddelaysintransit,whileeroding

valueandefficiency,andaddingsignificantcomplexity.

EstimatessuggestimplementationoftheGSTalone

wouldinstantlyaddupto2%toIndia’sGDPandfreeup

valuewithinsupplychainsacrossthemarket.Theneed

forsuchreformsismadeallthemorepressingbyIndia’s

potentialasalogisticsmarketprimarilybringdrivenbyits

sizeandstrengthasaconsumption-driveneconomy.

Justasexamplesofweatheringtheglobaleconomic

stormexistamongsttherisingcountries,sotoodo

examplesofvulnerabilitiesamongstthosemarketswhich

slipped.PerhapsthemostnotableoftheseisBrazil,

whichplacedoutsideofthetop3rankingpositionsforthe

firsttimeever.Ridingthecommodityboomofthe2000s

sawmillionsofBraziliansenterthemiddleclassforthe

firsttime,allowingretailersandmanufacturerstofindnew

consumers,asdisposableincomesgrew.SlidingChinese

demand,however,hasseencommoditypricesfall,which

hasresultedinjoblosses.Meanwhilebureaucracy,high

wagesandpoorqualityinfrastructurehaveleftBrazil’s

manufacturersuncompetitive.Addtothemixa$2bn

briberyscandalatstate-ownedoilcompany,Petrobras,

andBrazil’sproblemsarecompoundedbyagovernment

ingridlock,unabletoimplementmuchneededreforms

thatwouldenhanceproductivityandcompetiveness,or

moveaheadwithspendingonprojectstoremedythe

country’schronicinfrastructuredeficit.Withtheeconomy

inrecession,logisticsserviceprovidersfaceyetmore

challengesinBrazil.Russia’sfalloftwopositionsto8th

inthe2016Indexrankingscomesasitdealswithcapital

flight,adevaluationofitscurrencyandrampantinflation,

whichhaverevealedthetrueextentoftheneedforthe

countrytodecreaseitsrelianceontheenergysector.

UndersanctionsfromWesterngovernmentsfollowingits

activitiesinUkraine,economicgrowthisalmostcertainto

remainfragilesolongasacertaindegreeofuncertainty

overRussia’sgeopoliticalambitionsexists.

Alsofallingasaresultoffallingcommodityandoilprices

areSaudiArabiaandIndonesia,rankingthisyearin

5thand7thplaces,respectively.SaudiArabia’sslide

from2ndplacelastyearfollowsafallinoilprices:the

Kingdom’soil&gassectoraccountsforaround50%of

GDPand85%ofexports.Soundeconomicmanagement

duringthe2000slimiteditsfalldowntherankings,but

thereisclearevidenceofSaudiArabia’sneedtodiversify

itseconomy.Stepsarealreadybeingtakentoprivatise

infrastructureassets,shiftingtheinvestmentburden,and

therisk,bothofwhicharenowunsustainableagainsta

backdropofloweroilrevenues.Theprivatisationprocess

islikelytotouchonportsandairports,andwithnew

impetustocompeteagainstregionalrivalssuchasJebel

Ali,couldbringrenewedimpetustoinnovateanddrive

costsdownforshippersandlogisticsserviceproviders.

Indonesia,meanwhile,findsitselfhavingtodealwith

lowercommoditypricesandlowerdemandforits

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

20

exports.Thecountry’sgovernmenthasrespondedwith

legislationdesignedtoimproveitsbusinessenvironment,

butmanyofitsshortcomingsasalogisticsmarketare

linkedtoalackofinfrastructure,poorproceduresand

systems,andcorruption.Domestically,mostkeytrunk

routesandgatewayssufferfromcongestionas,formuch

ofthelastdecade,ports,railways,airportsandroads

havebeenallbutneglected.Thisaddscosttosupply

chains,andunlessreformsandinvestmentsaremade

quicklyandeffectively,Indonesiacouldseeitselfloseout

toneighboursasOEMsseekalternativestoChina.

Thetwomarketswithunchangedrankingsbookendthe

top10thisyear.Forthefourthconsecutiveyear,Turkeyis

positionedin10th,primarilyduetoitspositionasamajor

manufacturinghubforEuropeanandUSbusinesses,

offeringcloseproximitytothegroupof28European

states.SuchFDIhascreatedjobsthatemploymillions

ofthecountry’slabourforceandempoweritsdomestic

consumers.Thecountryhasalsopositioneditselfasa

stableactorinavolatileregion,apillarofitseconomic

attractivenessitwouldbewelladvisedtopreserve.There

arechallenges,however.Lowerglobaltradeisthreatening

thejobscreatedbyforeignmanufacturersandTurkey’s

privatesectorhasborrowedheavilyindollar-denominated

debt,withrepaymentsbecomingmoreexpensiveasthe

USdollargainsstrengthandtheTurkishliralosesvalue.

Thesecondemerginglogisticsmarketwithanunchanged

rankingin2016isChinawhich,havingenteredtheIndex

in2011,hassuccessfullytakenthetopspotineachyear

since.Chinais,though,slowlyregressingtowardsthe

pack.Itsmarginofvictoryhasdecreasedineachyear

since2012anditsscoreintheoverallIndexthisyear

(7.91)representsthefirsttimeithasrecordedafigure

belowthe8.00mark.Thisisbecausegrowthinthe

Chineseeconomyisfaltering,leavingitwithsignificant

questionstoanswer.Havingbeengearedtowardsgrowth

asanexport-ledmanufacturer,China’sproductive

capacityisnowfacingreorientationinordertosmoothly

andrapidlytransitiontheeconomytoaconsumption-

leddomesticmarket.Aspartofthistransition,China

mustactquicklytodiversifyitseconomy,purgeitself

ofcorruptionandintegratethevastpopulationinrural

areasintomoreproductiveeconomicactivity.Thisis

because,putsimply,China’sinternalmarketisnotyet

abletooffsetthefallinexportvolumesquicklyenoughto

makeupfortheshortfallingrowth.Whilethelossof$5

trillionfromitsstockmarketsinJuly2015isanindication

thatconfidenceinthemarketisweakening,thereare

signsofprogress.China’sleadershiprecognisesthat

modernconsumption-driveneconomiesrunonreliable

androbustroads,railways,electricity,telecommunication

networksandinternationalgateways.Investmentsin

suchinfrastructurehavebenefittedvastswathesofthe

population,aswellasChineseindustry.Furthertargeted

infrastructureinvestmentwillbeneededtosupportthe

transitiontoadomesticconsumption-driveneconomy.

ReportsemergedinJanuary2015suggestingan

acceleratedinvestmentprocessacross300infrastructure

projectswithintheenergy,health,transportationand

miningsectors.Thissuggeststheinvestmentistaking

place,butthequestionremainsastowhetherthescale

andspeedrequiredcanbeachieved.

Changes outside the Top 10

Nigeria

Nigeriaranks17thinthe2016Index,movingup10spots

thisyear.Itsscorehasincreasedfrom4.56to5.28.

IntheMarketSizeandGrowthAttractivenesssub-index,

Nigeria’sscorehasrisenfrom6.31to7.79.Thisreflectsthe

country’s‘rebasing’ofitsGDPin2014,whichpromoted

NigeriatothelargesteconomyinAfrica,supplanting

SouthAfrica.Morespecifically,therevisedGDPfigurewas

89%higherthanpreviouslythought.Althoughsceptics

maydoubtthevalidityofthenewnumber,itwasreally

theoldfigurethatwasdubious.AssummarisedbyThe

Economist,“GDPistypicallymeasuredbyreferenceto

theshapeoftheeconomyina‘base’year.Statisticians

samplebusinessesindifferentindustriestoseehowfast

theyaregrowing.Theweighttheygivetoeachsector

dependsonitsimportancetotheeconomyinthebase

year.Astimepassesthefiguresbecomelessandless

accurate.Nigeria’soldGDPdatareliedonahopelessly

datedsnapshotofitseconomyin1990.Thenewfigures

(whichhave2010asthebaseyear)givedueweightto

fast-growingindustriessuchasmobiletelecomsandfilm-

makingthathavesprungupsincethen.”

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

21

TherebasingalsohadasignificantimpactonNigeria’s

Compatibilityscore(3.40comparedto2.46inthe2015

Index),becausethecompositionoftheeconomyisnow

moreorientedtowardslogistics-intensivesectorsthan

previouslythought.ThisbumpedNigeriaupthreespots,

thoughitstillrankspoorlyatjust40thinthissub-index.

Egypt

Egypthasjumped10spotsintheoverallIndexranking,to

22nd.Itsscorehasrisenfrom4.38to4.99.Thisismostly

downtoitsMarketSizeandGrowthAttractivenessscore

increasingfrom4.92to6.12.Theimprovementhasbeen

drivenbysignificantupwardrevisionstoitseconomic

growthforecastsandtheoverallsizeofitseconomy

beingmoreimpressivecomparedtotherestofthepack,

thanlastyear.Post-ArabSpring,Egypthasquietlymade

animpressiverecovery.

Unsurprisingly,therehasalsobeenageneral

improvementinEgypt’sbusinessenvironmentwhich

hasseenitsCompatibilityscorerisefrom2.35to2.85,

thoughthisstillonlyranks43rd.Foreigninvestorsin

particularappeartoberegainingameasureofconfidence

inEgypt.AccordingtofDi,realforeigninvestmentin

Egypt(asmeasuredbytheextentofgreenfieldcapital

investmentprojects)pickedupstronglyin2014,witha

significantnumberoflarge-scaleinvestmentprojects

announced,whichthemselvesfollowtheredevelopment

andwideningoftheSuezCanal.Infact,Egypt’sinward

capitalinvestmentof$18bnin2014wasgreaterthanany

othercountryintheMiddleEastandAfrica.However,this

fundingwasconcentratedinjust51projects,compared

to302($13bn)intheUAEand116($4bn)inSouthAfrica.

Pakistan

Pakistanhasmoveduptwospotsinthisyear’sIndexto

23rd.Itsscorehasimprovedfrom4.77to4.99.

Thisislargelydowntoitseconomicoutlookimproving.For

example,theIMF’slatestiterationofrealGDPforecasts

to2020iscertainlymoreoptimisticthanayearago.

Credit-ratingagenciessuchasMoody’sandStandard&

Poor’shavealsobeensimilarlyupbeat.Bothimproved

theircreditratingoutlookforthecountrytopositive

fromstableinMarch2015andMay2015,respectively.

Standard&Poor’sstated:“Thepositiveoutlookreflects

ourexpectationsofPakistan’simprovedeconomicgrowth

prospects,fiscalandexternalperformance,andthe

supportiverelationshipofexternaldonorsoverthenext

12months.”Theagencyalsoraisedits2015-2017average

growthprojectionto4.6%from3.8%.

However,Pakistanstilllagsbehindseverelyinthe

CompatibilityandConnectednesssub-indices,ranking

42ndand35threspectively,withPakistan’sscorein

bothmeasuresfallingyear-on-year.Onepossibleroad

toimprovementmaycomeintheformofChinese

investment.WhenPresidentXiJinpingvisitedPakistan

inApril2015,Chinapledged$46bnforroad,portsand

powerplants:aplannedinvestmentequaltoalmostthree

timesthetotalFDIthatPakistanhasreceivedoverthe

lastsevenyears.Pakistaniofficialssaymostprojects

willreachcompletioninonetothreeyears,withsome

$15.5bnofcoal,wind,solarandhydroenergyprojectsto

comeonlineby2017.

Peru

Perustruggledinthisyear’sIndex,losingfivespotsto

rank28thoverall.Itsscorehasfallenfrom4.84to4.70.

Thedeclinewaslargelyattributabletoaweakening

ofthecountry’seconomicprospects.WhiletheIMF

hasdowngradeditslongertermoutlookforPeru,its

mostconcerningpieceofdataisthatPeru’srealGDP

growthin2015isnowexpectedtocomeinat2.4%,

downfromitspredictionayearagoof5.1%.Although

expansionaryfiscalpolicyandhigheryear-on-year

miningindustryoutputaresustainingsomemeasureof

growth,lowercommoditypricesarehavingasignificant

adverseimpact.Thepriceofcopper,forinstance,has

fallenbymorethan15%in2015alone.Inaddition,

Peru’smanufacturingandconstructionsectorshave

struggledthisyear,whileinvestmentgrowthisslow,

duetodepressedbusinessconfidence.Asidefromthe

economicdata,Peru’sConnectednessscoreisdown

from4.96to4.84,mainlyasaresultofthecountrybeing

judgedtohavepoorerqualityinfrastructureandmore

inefficientcustomsproceduresyear-on-year.

Amorepositivespinmightbethatoverthelongerterm,

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

22

Peruislikelytobeoneofthebetter-faringcountriesin

LatinAmerica.OutofallSouthAmericancountries,ithas

oneofthebestgrowthoutlooksoverthenextfiveyears,

evenwiththedownwardrevisionsin2015.

Algeria

AlgeriamovedupfourspotsintheoverallIndexrankingto

30thin2016.Itsscorehasincreasedfrom4.10to4.46.

Ithasmademeaningfulgainsacrossallfacetsofthe

Index.ItsMarketSizeandGrowthAttractivenessscoreis

up0.40points,Compatibilityhasincreasedby0.62points

andConnectednessisupby0.21points.MarketSizeand

GrowthAttractivenesshasimprovedlargelybecauseits

economy,asmeasuredbyPPPGDP,madeimpressive

gainsyear-on-year.Compatibilityhasrisenbecause

Algeria’seconomyisnowthoughttobemoreoriented

towardslogisticsintensivesectorsthanbefore,inaddition

tometricsofsecurityimprovingyear-on-year.Finally,

Connectednessisbetterthankstoimprovedcustoms

procedures.

Themajorquestionmarksurroundingthecountryisthe

collapseintheoilpriceandthesubsequentimpactonthe

economy.WithoilresponsibleforalmostallofAlgeria’s

exportrevenues,howthecountryrespondstosuchan

adverseshockwillbecrucial.

ArgentinahasplummetedfivespotstoNo.31inthisyear’s

Index.Itsoverallscorehasdeclinedby0.25pointsto4.42.

Unsurprisingly,giventhecountry’songoingeconomic

difficulties,thedropintheMarketSizeandGrowth

Attractivenesssub-indexwasparticularlysevere(down

from4.78to4.14).Itseconomicoutlookisworsenow

comparedtoayearago,withtheIMFpredictingvirtually

noeconomicgrowthfrom2016-2020.Inflationisaround

25%andcurrencycontrolsandtraderestrictionsinplace

since2011continuetochoketheeconomy.Thisisthe

legacythatPresidentCristinaFernandezdeKirchner

leavesbehind.OnereasonforoptimismisthatArgentina

willbeundernewleadershipwiththeelectionofpro-

businessMauricioMacrifromDecember2015anditis

difficulttoimaginethateconomicpolicygoingforward

couldbeanyworsethanunderthepreviousregime.

Jordan

JordanhasfallenfourspotsintheoverallIndexrankingto

33rd.Itsscoreisdown0.26pointsto4.28.

TheMarketSizeandGrowthAttractivenesssub-index

declinedmoderately,mainlyonaccountofthecountry’s

worseningfinancialstability,butthemainculpritwas

theCompatibilitysub-index,whichscoredjust5.52this

year,downfrom6.51inlastyear’sIndex.Theweightof

instabilitycausedbycrime,violenceandterrorismspilling

overtheborderfromSyriaanditsknock-onimpactwere

primarydriversbehindthis.Apartfromthecatastrophic

humanitarianimpactoftheconflict,theUNhasestimated

thatthetotaleconomiclossfromthewarwillreach

$237bnbytheendof2015.

Ukraine

Ukraineranks34thinthisyear’sIndex,adeclineoffour

placescomparedtothepreviousyear.Itsoverallscore

hascontractedby0.37pointsto4.09.

Thecountryhasbeenenvelopedincrisissince

November2013,withmassunrestplaguingthecountry.

TheprimarilyRussian-speakingeasternandsouthern

regionsofthecountryhavebeenhittheworst.Interms

ofIndexscores,theconflicthastakenitstollonvarious

fronts.ItsMarketSizeandGrowthAttractiveness

sub-indexhascrashedby0.42pointsto3.48.TheIMF

estimatedthatrealGDPgrowthwas-6.8%in2014

andworsestillin2015,at-9.0%.Inaddition,Ukrainian

financialstabilityhastakenabighit.Moreover,the

Compatibilitysub-indexscoreof3.99,downby1.30

points,indicatesthatthebusinessenvironmentin

Ukrainehassufferedseverely.Measuresoftheinstability

areunderstandablyfarworsethanbeforethecrisis

erupted.Furthermore,FDIflowstoUkrainefellby91%to

$410min2014(thelowestlevelin15years),mainlydue

toRussiancapitalabandoningthecountry.

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

23

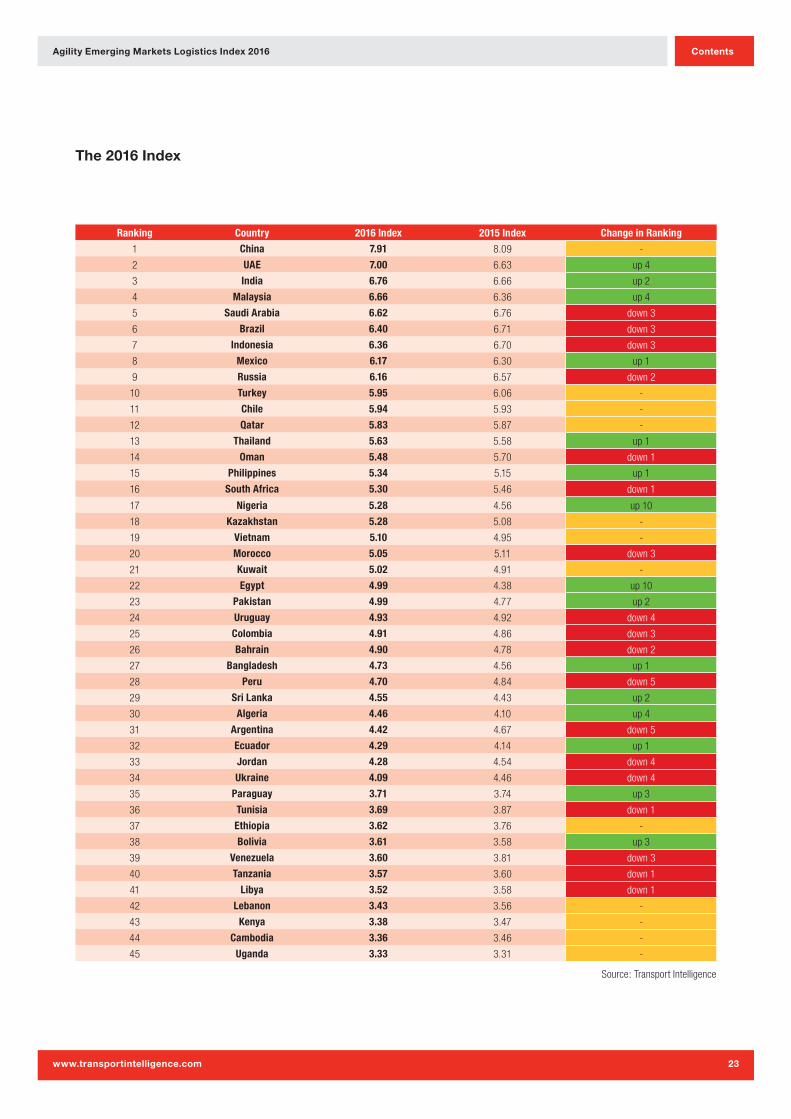

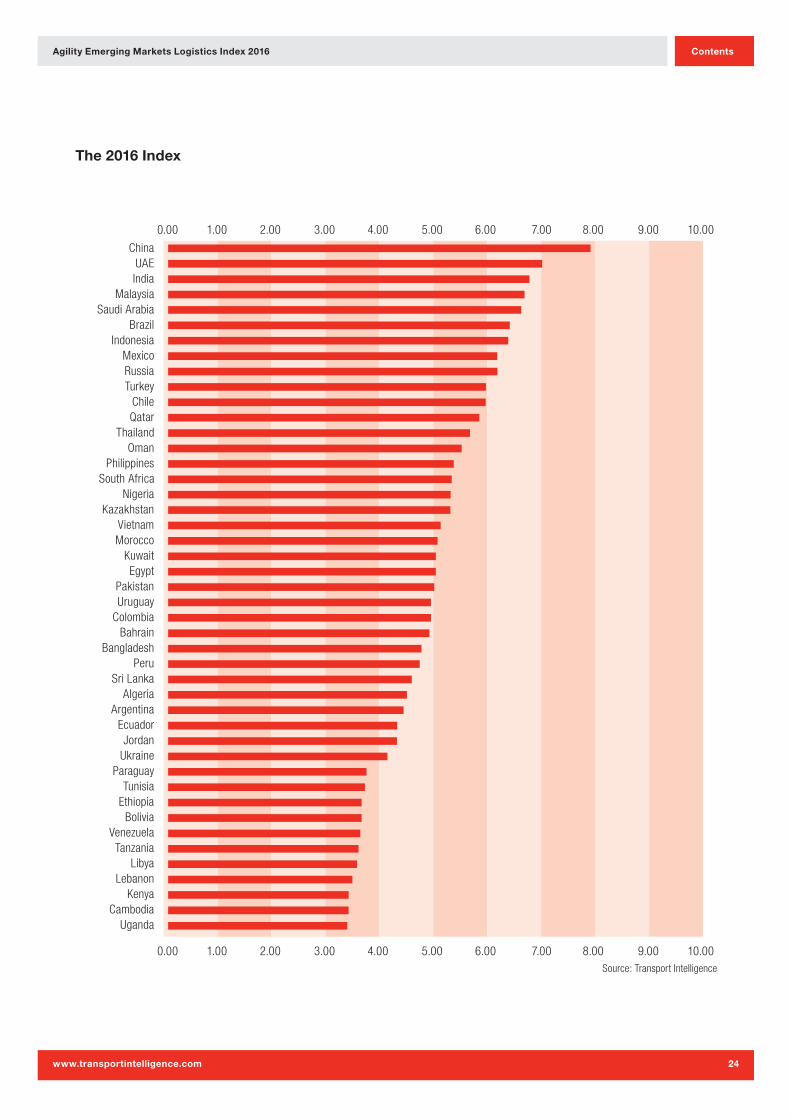

Ranking Country 2016 Index 2015 Index Change in Ranking

1 China 7.91 8.09 -

2 UAE 7.00 6.63 up 4

3 India 6.76 6.66 up 2

4 Malaysia 6.66 6.36 up 4

5 Saudi Arabia 6.62 6.76 down 3

6 Brazil 6.40 6.71 down 3

7 Indonesia 6.36 6.70 down 3

8 Mexico 6.17 6.30 up 1

9 Russia 6.16 6.57 down 2

10 Turkey 5.95 6.06 -

11 Chile 5.94 5.93 -

12 Qatar 5.83 5.87 -

13 Thailand 5.63 5.58 up 1

14 Oman 5.48 5.70 down 1

15 Philippines 5.34 5.15 up 1

16 South Africa 5.30 5.46 down 1

17 Nigeria 5.28 4.56 up 10

18 Kazakhstan 5.28 5.08 -

19 Vietnam 5.10 4.95 -

20 Morocco 5.05 5.11 down 3

21 Kuwait 5.02 4.91 -

22 Egypt 4.99 4.38 up 10

23 Pakistan 4.99 4.77 up 2

24 Uruguay 4.93 4.92 down 4

25 Colombia 4.91 4.86 down 3

26 Bahrain 4.90 4.78 down 2

27 Bangladesh 4.73 4.56 up 1

28 Peru 4.70 4.84 down 5

29 Sri Lanka 4.55 4.43 up 2

30 Algeria 4.46 4.10 up 4

31 Argentina 4.42 4.67 down 5

32 Ecuador 4.29 4.14 up 1

33 Jordan 4.28 4.54 down 4

34 Ukraine 4.09 4.46 down 4

35 Paraguay 3.71 3.74 up 3

36 Tunisia 3.69 3.87 down 1

37 Ethiopia 3.62 3.76 -

38 Bolivia 3.61 3.58 up 3

39 Venezuela 3.60 3.81 down 3

40 Tanzania 3.57 3.60 down 1

41 Libya 3.52 3.58 down 1

42 Lebanon 3.43 3.56 -

43 Kenya 3.38 3.47 -

44 Cambodia 3.36 3.46 -

45 Uganda 3.33 3.31 -

Source: Transport Intelligence

The 2016 Index

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

24

ChinaUAEIndia

MalaysiaSaudi Arabia

BrazilIndonesia

MexicoRussiaTurkey

ChileQatar

ThailandOman

PhilippinesSouth Africa

NigeriaKazakhstan

VietnamMorocco

KuwaitEgypt

PakistanUruguay

ColombiaBahrain

BangladeshPeru

Sri LankaAlgeria

ArgentinaEcuadorJordan

UkraineParaguay

TunisiaEthiopia

BoliviaVenezuela

TanzaniaLibya

LebanonKenya

CambodiaUganda

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00Source: Transport Intelligence

The 2016 Index

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

25

Agility Emerging Markets Logistics Index for Countries with GDP more than US$300bn

The16economieswithGDPabove$300bnremainthe

sameasin2015.Whilethereismovementamongstthe

markets,itistruetosaythatlargeGDPequatestohigh

potentialasanemerginglogisticsmarket.Indeed,thetop

10marketsoverallhaveGDPabovethethreshold.

Todependsolelyonmarketsize,however,wouldpainta

misleadingpictureofwhattruelogisticsmarketpotential

lookslike.UAE,ranked2ndoverallbytheIndex,hasan

economyjust3.9%thesizeof1strankedChina,whilethe

EmiratesoutscoresIndiaandBrazil,despiteitseconomy

equalling19.4%ofIndia’seconomyand17.1%ofBrazil’s.

Ranking Country Market size and growth sub-index

Market compatibility sub-index

Market connected-ness sub-index

Total Index

1 China 9.48 6.79 6.75 7.91

2 UAE 5.58 8.61 7.73 7.00

3 India 9.32 4.80 4.95 6.76

4 Malaysia 6.41 6.56 7.00 6.66

5 Saudi Arabia 6.84 6.89 6.23 6.62

6 Brazil 7.87 6.09 4.91 6.40

7 Indonesia 8.66 4.44 4.81 6.36

8 Mexico 7.73 4.56 5.29 6.17

9 Russia 6.83 5.58 5.72 6.16

10 Turkey 6.74 5.63 5.23 5.95

11 Thailand 6.72 4.33 5.13 5.63

12 South Africa 5.54 4.81 5.31 5.30

13 Nigeria 7.79 3.40 3.50 5.28

14 Colombia 5.88 2.86 4.95 4.91

15 Argentina 4.14 4.99 4.42 4.42

16 Venezuela 3.38 3.69 3.79 3.60

Source: Transport Intelligence

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

26

Agility Emerging Markets Logistics Index for Countries with GDP less than US$300bn

JustasintheoverallIndex,thereturnofameasure

ofstabilitytoEgyptseesitrisethroughtheranking,

movingfrom17thto9th.ThereverseistrueofUkraine,

wheretheongoingconflicthasdetrimentallyaffectedits

prospects:thecountrytookhitstobothitsSize&Growth

AttractivenessscoreanditsCompatibilityscore.

Perhapsthemostsignificantoutcomehere,though,is

thatastaggering23ofthe29countrieswithGDPsbelow

the$300bnthresholdoutrankVenezuelaasanemerging

logisticsmarket.Infact,Chile’soverallscorewould

seeitfinish11thintherankingofcountrieswithGDP

above$300bn.Againstabackdropoflowereconomic

prospectsacrossallemergingmarkets,thisserves

asapotentreminderthatinvestmentdecisionsmust

bebothstrategicandnuanced,reflectingtheunique

characteristicsofthemarketsunderinvestigation.While

forecastssuggest2016willseesomethingofarebound

infortunesforemergingmarkets,thedaysofinvestment

guidedbyheadlinefigures–andindeed,thedaysof

‘investmentbyacronym’–shouldbefullyconsignedto

history.

Ranking Country Market size and growth sub-index

Market compatibility sub-index

Market connected-ness sub-index

Total Index

1 Chile 5.26 6.62 6.32 5.94

2 Qatar 4.83 7.62 5.97 5.83

3 Oman 3.93 7.54 6.11 5.48

4 Philippines 6.56 4.79 4.27 5.34

5 Kazakhstan 4.60 6.94 5.14 5.28

6 Vietnam 5.42 5.15 4.72 5.10

7 Morocco 4.15 6.05 5.52 5.05

8 Kuwait 4.63 6.59 4.59 5.02

9 Egypt 6.12 2.85 4.90 4.99

10 Pakistan 6.85 2.86 4.06 4.99

11 Uruguay 3.38 6.71 5.69 4.93

12 Bahrain 3.27 6.21 6.01 4.90

13 Bangladesh 5.91 4.45 3.56 4.73

14 Peru 4.91 4.03 4.84 4.70

15 Sri Lanka 3.25 5.96 5.26 4.55

16 Algeria 4.87 4.49 3.98 4.46

17 Ecuador 2.80 4.65 5.77 4.29

18 Jordan 2.81 5.52 5.25 4.28

19 Ukraine 3.48 3.99 4.84 4.09

20 Paraguay 2.82 4.76 4.15 3.71

21 Tunisia 3.06 4.18 4.14 3.69

22 Ethiopia 3.37 4.39 3.48 3.62

23 Bolivia 2.76 4.52 4.06 3.61

24 Tanzania 3.15 4.52 3.53 3.57

25 Libya 2.68 2.08 5.25 3.52

26 Lebanon 2.46 4.33 4.04 3.43

27 Kenya 3.34 2.23 4.06 3.38

28 Cambodia 2.53 4.34 3.77 3.36

29 Uganda 2.90 3.48 3.74 3.33

Source: Transport Intelligence

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

27

Source: Transport Intelligence

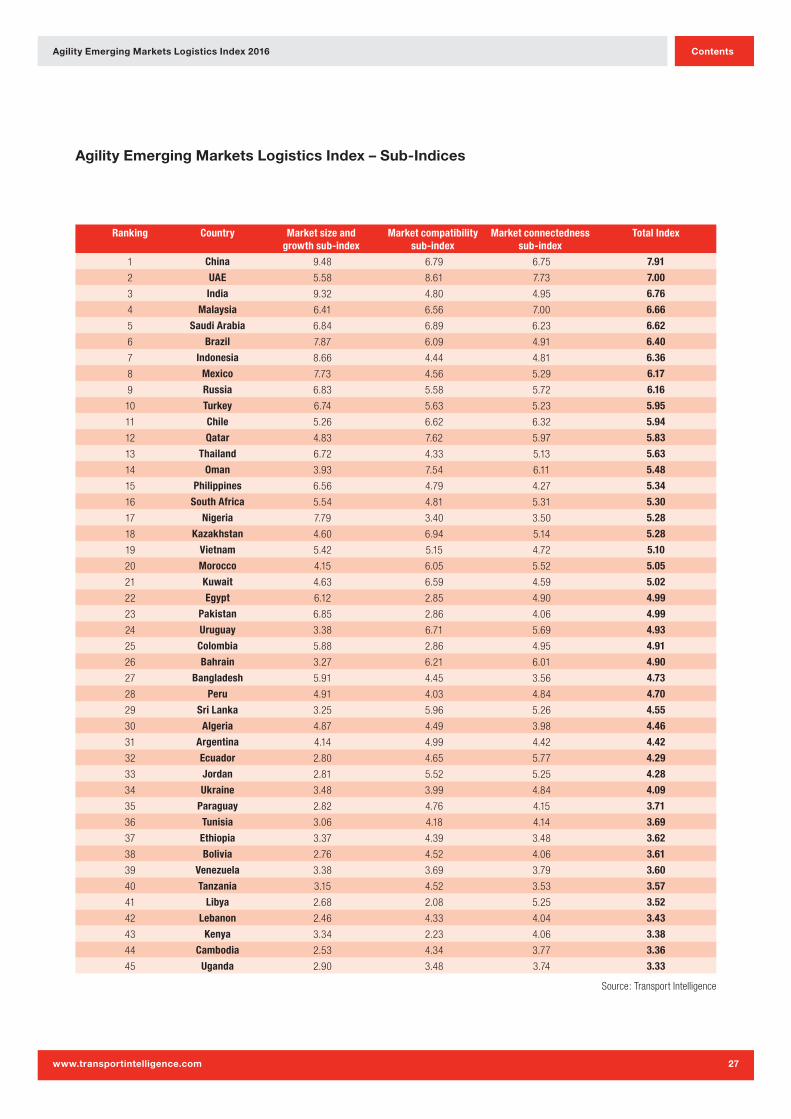

Agility Emerging Markets Logistics Index – Sub-Indices

Ranking Country Market size and growth sub-index

Market compatibility sub-index

Market connectedness sub-index

Total Index

1 China 9.48 6.79 6.75 7.91

2 UAE 5.58 8.61 7.73 7.00

3 India 9.32 4.80 4.95 6.76

4 Malaysia 6.41 6.56 7.00 6.66

5 Saudi Arabia 6.84 6.89 6.23 6.62

6 Brazil 7.87 6.09 4.91 6.40

7 Indonesia 8.66 4.44 4.81 6.36

8 Mexico 7.73 4.56 5.29 6.17

9 Russia 6.83 5.58 5.72 6.16

10 Turkey 6.74 5.63 5.23 5.95

11 Chile 5.26 6.62 6.32 5.94

12 Qatar 4.83 7.62 5.97 5.83

13 Thailand 6.72 4.33 5.13 5.63

14 Oman 3.93 7.54 6.11 5.48

15 Philippines 6.56 4.79 4.27 5.34

16 South Africa 5.54 4.81 5.31 5.30

17 Nigeria 7.79 3.40 3.50 5.28

18 Kazakhstan 4.60 6.94 5.14 5.28

19 Vietnam 5.42 5.15 4.72 5.10

20 Morocco 4.15 6.05 5.52 5.05

21 Kuwait 4.63 6.59 4.59 5.02

22 Egypt 6.12 2.85 4.90 4.99

23 Pakistan 6.85 2.86 4.06 4.99

24 Uruguay 3.38 6.71 5.69 4.93

25 Colombia 5.88 2.86 4.95 4.91

26 Bahrain 3.27 6.21 6.01 4.90

27 Bangladesh 5.91 4.45 3.56 4.73

28 Peru 4.91 4.03 4.84 4.70

29 Sri Lanka 3.25 5.96 5.26 4.55

30 Algeria 4.87 4.49 3.98 4.46

31 Argentina 4.14 4.99 4.42 4.42

32 Ecuador 2.80 4.65 5.77 4.29

33 Jordan 2.81 5.52 5.25 4.28

34 Ukraine 3.48 3.99 4.84 4.09

35 Paraguay 2.82 4.76 4.15 3.71

36 Tunisia 3.06 4.18 4.14 3.69

37 Ethiopia 3.37 4.39 3.48 3.62

38 Bolivia 2.76 4.52 4.06 3.61

39 Venezuela 3.38 3.69 3.79 3.60

40 Tanzania 3.15 4.52 3.53 3.57

41 Libya 2.68 2.08 5.25 3.52

42 Lebanon 2.46 4.33 4.04 3.43

43 Kenya 3.34 2.23 4.06 3.38

44 Cambodia 2.53 4.34 3.77 3.36

45 Uganda 2.90 3.48 3.74 3.33

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

28

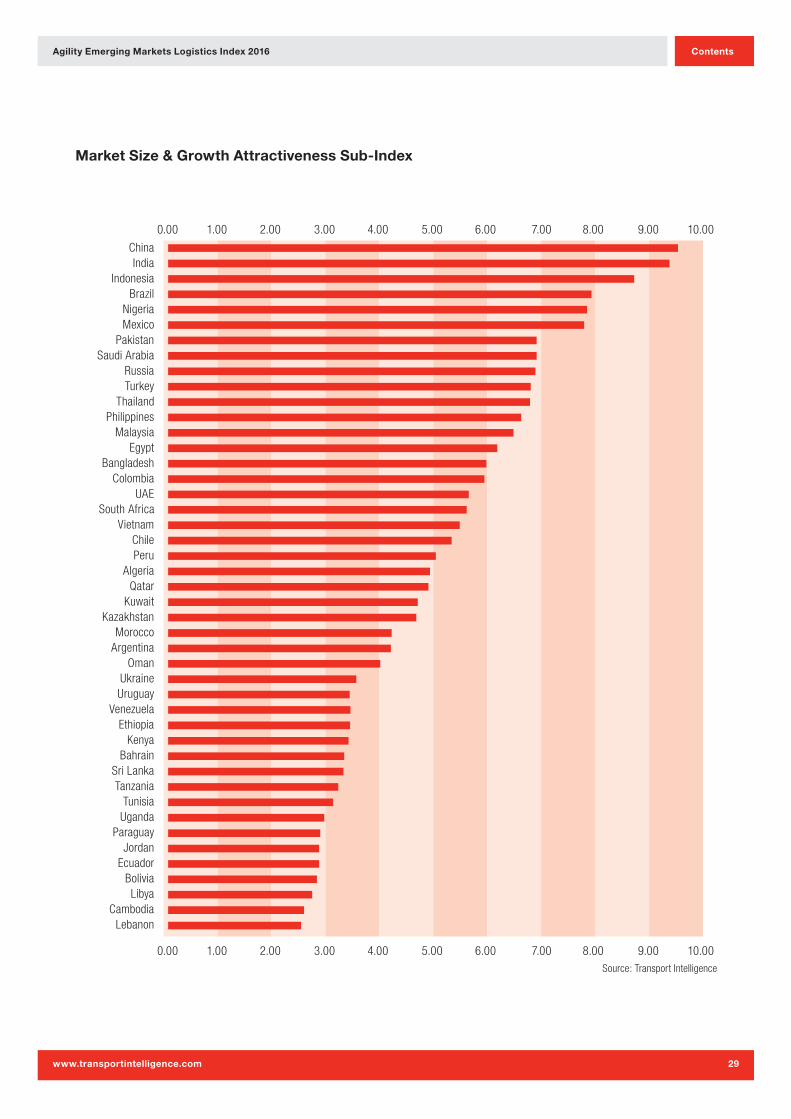

Market Size & Growth Attractiveness

WithintherankingforMarketSize&Growth

Attractiveness,thetopfourrankingmarketsare

unchangedforathirdconsecutiveyear.Nigeriahas

risentotake5thintheranking,whilePakistanjumpedto

7thasaresultofmarkedlybettergrowthprospectsfor

itseconomythanayearago.Russia,however,hasfelt

theimpactofpoorergrowthexpectationsfollowingthe

impositionofEUandUSsanctions,whichhaveseenit

slipto9thinthismeasure.

Atthebottomendofthescale,Cambodia,forthefirst

timesinceitwasaddedtotheIndexin2013,isnotthe

lowestrankedMarketforSize&GrowthAttractiveness.

Paraguay’simprovedoutlookhasseenitrisefromthe

lowestreachesofthismeasuretoo.

Source: Transport Intelligence

Ranking Country Market size and growth sub-index

1 China 9.48

2 India 9.32

3 Indonesia 8.66

4 Brazil 7.87

5 Nigeria 7.79

6 Mexico 7.73

7 Pakistan 6.85

8 Saudi Arabia 6.84

9 Russia 6.83

10 Turkey 6.74

11 Thailand 6.72

12 Philippines 6.56

13 Malaysia 6.41

14 Egypt 6.12

15 Bangladesh 5.91

16 Colombia 5.88

17 UAE 5.58

18 South Africa 5.54

19 Vietnam 5.42

20 Chile 5.26

21 Peru 4.91

22 Algeria 4.87

23 Qatar 4.83

24 Kuwait 4.63

25 Kazakhstan 4.60

26 Morocco 4.15

27 Argentina 4.14

28 Oman 3.93

29 Ukraine 3.48

30 Uruguay 3.38

31 Venezuela 3.38

32 Ethiopia 3.37

33 Kenya 3.34

34 Bahrain 3.27

35 Sri Lanka 3.25

36 Tanzania 3.15

37 Tunisia 3.06

38 Uganda 2.90

39 Paraguay 2.82

40 Jordan 2.81

41 Ecuador 2.80

42 Bolivia 2.76

43 Libya 2.68

44 Cambodia 2.53

45 Lebanon 2.46

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

29

ChinaIndia

IndonesiaBrazil

NigeriaMexico

PakistanSaudi Arabia

RussiaTurkey

ThailandPhilippines

MalaysiaEgypt

BangladeshColombia

UAESouth Africa

VietnamChilePeru

AlgeriaQatar

KuwaitKazakhstan

MoroccoArgentina

OmanUkraineUruguay

VenezuelaEthiopia

KenyaBahrain

Sri LankaTanzania

TunisiaUganda

ParaguayJordan

EcuadorBoliviaLibya

CambodiaLebanon

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00

Market Size & Growth Attractiveness Sub-Index

Source: Transport Intelligence

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

30

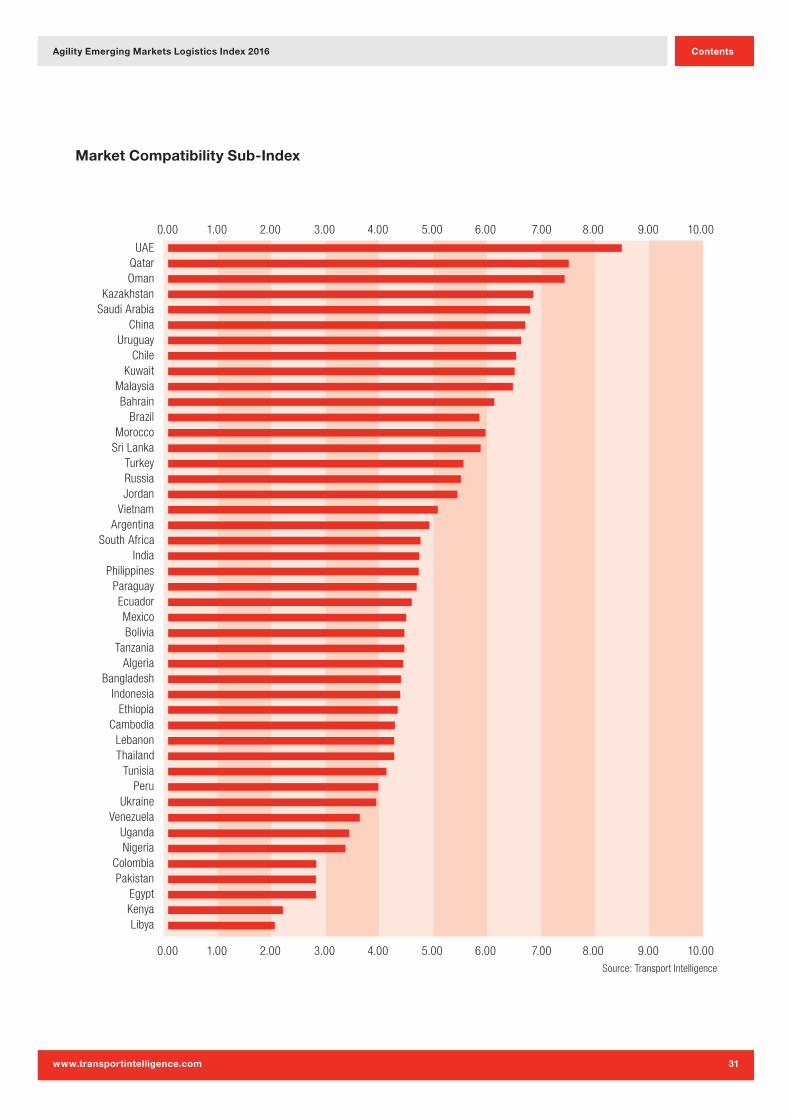

Market Compatibility

Fiveofthetop10rankedmarketsforCompatibilitycome

fromtheMiddleEast&NorthAfricaregion.TheUAE

retainsitspositionatthetopforasecondconsecutive

year,althoughitsscorehasfallen.ThattheUAEistop,

though,isunlikelytobeasurprisetothosewithexposure

tothemarket.Its34freetradezones,non-existent

corporationtaxandtheofferoffullownership,aswellas

unlimitedrepatriationofprofits,makeitahighlyappealing

businessenvironmentforproducersandmanufacturers

alike,aswellastologisticsserviceproviders.

Kazakhstan’sfavourabletaxregimeseesitriseto

becomethe4thhighestrankedmarketforCompatibility

thisyearwhich,combinedwithSaudiArabia’sclimb

to5th,seesChinafalloutofthetop5inthismeasure.

Anothermajoremergingmarkettofalldowntheranking

isRussia,whichslipsthreeplacesto16th,butitis

Ukrainewhichsuffersmostheavilyfollowingtheconflict

betweenthetwo,dropping19spotsfrom18thto37th.

ConflictalsocausedJordan’sslide–havingreached4th

in2014,thecountry’sslidehasacceleratedasitfollowed

afourplacedropin2015withafurthernineposition

lossin2016,toendin17thoverall–asthetroublesin

neighbouringSyriaweighdownitsprospects.

LibyapropsuptheCompatibilityrankingforasecond

year,andwhileEgyptandNigeriawereabletorise,

neithercouldmatchtheirrateofprogressintheSize&

GrowthAttractivenessranking.Despiteitshighoverall

ranking,Indiastilllanguishesasthe21strankedmarket

forCompatibility.Thismayrepresentariseofeight

positions,butitservestohighlightthatthecountry’s

businessenvironmentisstillinneedofsignificantand

rapidimprovement.

Source: Transport Intelligence

Ranking Country Market compatibility sub-index

1 UAE 8.61

2 Qatar 7.62

3 Oman 7.54

4 Kazakhstan 6.94

5 Saudi Arabia 6.89

6 China 6.79

7 Uruguay 6.71

8 Chile 6.62

9 Kuwait 6.59

10 Malaysia 6.56

11 Bahrain 6.21

12 Brazil 6.09

13 Morocco 6.05

14 Sri Lanka 5.96

15 Turkey 5.63

16 Russia 5.58

17 Jordan 5.52

18 Vietnam 5.15

19 Argentina 4.99

20 South Africa 4.81

21 India 4.80

22 Philippines 4.79

23 Paraguay 4.76

24 Ecuador 4.65

25 Mexico 4.56

26 Bolivia 4.52

27 Tanzania 4.52

28 Algeria 4.49

29 Bangladesh 4.45

30 Indonesia 4.44

31 Ethiopia 4.39

32 Cambodia 4.34

33 Lebanon 4.33

34 Thailand 4.33

35 Tunisia 4.18

36 Peru 4.03

37 Ukraine 3.99

38 Venezuela 3.69

39 Uganda 3.48

40 Nigeria 3.40

41 Colombia 2.86

42 Pakistan 2.86

43 Egypt 2.85

44 Kenya 2.23

45 Libya 2.08

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

31

UAEQatarOman

KazakhstanSaudi Arabia

ChinaUruguay

ChileKuwait

MalaysiaBahrain

BrazilMorocco

Sri LankaTurkeyRussiaJordan

VietnamArgentina

South AfricaIndia

PhilippinesParaguayEcuadorMexicoBolivia

TanzaniaAlgeria

BangladeshIndonesia

EthiopiaCambodia

LebanonThailand

TunisiaPeru

UkraineVenezuela

UgandaNigeria

ColombiaPakistan

EgyptKenyaLibya

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00

Market Compatibility Sub-Index

Source: Transport Intelligence

Agility Emerging Markets Logistics Index 2016

www.transportintelligence.com

Contents

32

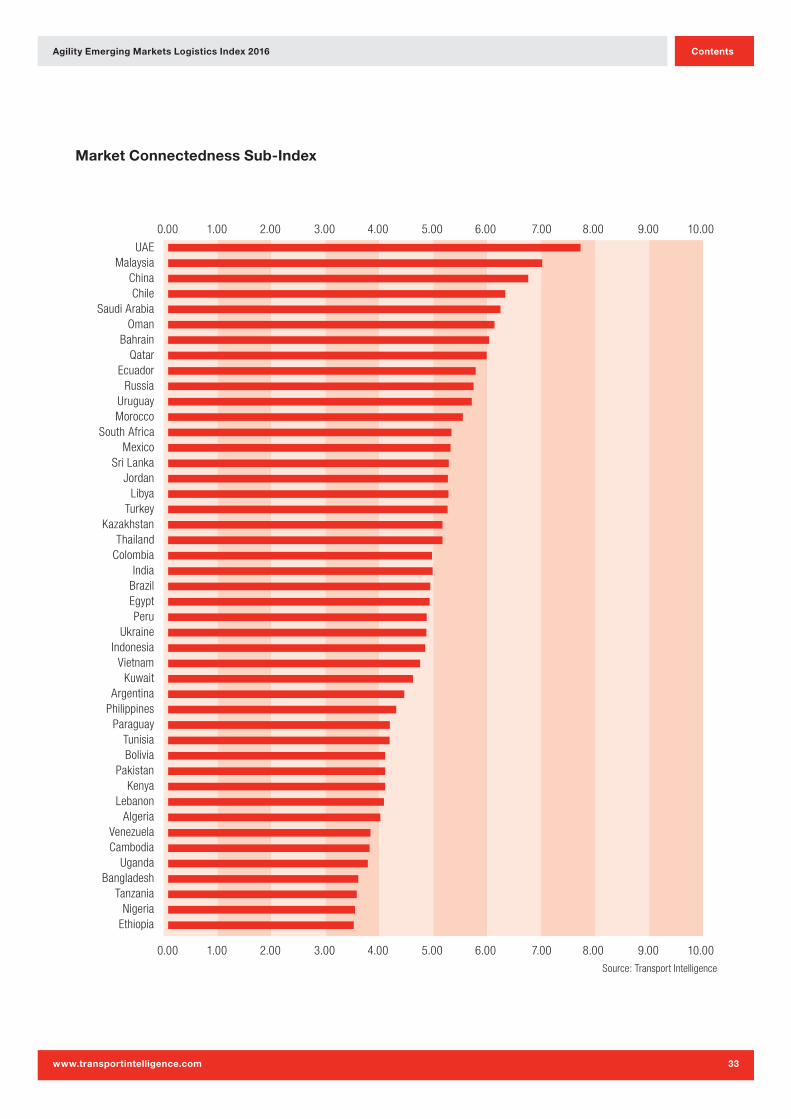

Market Connectedness

Thetop10rankingpositionsforMarketConnectedness

displayedalargeamountofcontinuityyear-on-yearas

themarketstooccupythetopthreepositions–UAE,

MalaysiaandChina–wereunchanged,whilenineofthe

10remainedunchanged.ThecasualtywasSouthAfrica,

whichslidto13thandwasreplacedbyRussia.The

infrastructuredeficitsoftwomajoremergingmarkets–

BrazilandIndia–aresharplyillustratedinthismeasure

ofdomesticandinternationalconnectivity,withboth

languishingindistinctmediocrity.

Overall,theIndexin2016paintsabroadlypositivepicture

ofNigeria’spotentialasanemergingmarket.Havingrisen

10placesinthecombinedranking,itmaywellserveasa

warningtothoseexcitedbythecountry’spotential,that

itsinfrastructureislikelytoseverelylimitgrowthunless

significantprogressismade.Inthismeasure,Nigeria

ranks44thofthe45marketsunderexamination,having

regressedoverthelastyear.

Source: Transport Intelligence

Ranking Country Market connectedness sub-index

1 UAE 7.73

2 Malaysia 7.00