Agenda Item 6 - DCF

20

Agenda Item 6 IVSC Professional Board Meeting 17 March 2012 Attached is the proposed TIP No 1 Discounted Cash Flow which has been prepared by the working group. The Board is requested to: a. Discuss the difference of view that has arisen between the members of the working group highlighted below and decide which it supports. b. Subject to any amendments to reflect the above, approve the document for publication.* Point for decision by Board: Para 27 sets out a method for calculating the cost of equity using the CAPM. As drafted this includes “alpha”, the risk specific to the company. It has been argued that, in practice, this is not always appropriate. The arguments for and against each approach will be presented at the meeting. * Note: If approved the paper will be put into production which will involve copy editing, design, formatting and pagination prior to printing.

-

Upload

ernest-randall -

Category

Documents

-

view

17 -

download

2

description

exposure draft

Transcript of Agenda Item 6 - DCF

Agenda Item 6

IVSC Professional Board Meeting

17 March 2012

Attached is the proposed TIP No 1 Discounted Cash Flow which has been prepared by the

working group. The Board is requested to:

a. Discuss the difference of view that has arisen between the members of the working

group highlighted below and decide which it supports.

b. Subject to any amendments to reflect the above, approve the document for

publication.*

Point for decision by Board:

Para 27 sets out a method for calculating the cost of equity using the CAPM. As

drafted this includes “alpha”, the risk specific to the company. It has been argued that,

in practice, this is not always appropriate. The arguments for and against each

approach will be presented at the meeting.

* Note: If approved the paper will be put into production which will involve copy editing, design, formatting and

pagination prior to printing.

ii

dcf tip post consult v9

Technical Information Paper 1

Discounted Cash Flow

Copyright © 2012 International Valuation Standards Council. All rights reserved. No part of this Exposure Draft

may be translated, reprinted or reproduced or utilised in any form either in whole or in part or by any electronic,

mechanical or other means, now known or hereafter invented, including photocopying and recording, or in any

information storage and retrieval system, without permission in writing from the International Valuation Standards

Council. Please address publication and copyright matters to:

International Valuation Standards Council

41 Moorgate

LONDON EC2R 6PP

United Kingdom

Email: [email protected]

www.ivsc.org

iii

dcf tip post consult v9

Technical Information Paper 1

Discounted Cash Flow

Technical Information Papers

An IVSC Technical Information Paper (TIP) provides guidance on different valuation topics and is designed to be

of assistance to valuation professionals and informed users of valuations alike. A TIP may:

• provide information that is helpful to valuation professionals in exercising the judgements they are required to make during the valuation process;

• give indications and examples of generally accepted best practice, including appropriate valuation methods and criteria for their use; and

• provide additional information to assist in the application of an International Valuation Standard (IVS).

A TIP does not:

• provide valuation training or instruction; or

• direct that a particular approach or method should or should not be used in any specific situation.

The contents of a TIP are not intended to be mandatory. Responsibility for choosing the most appropriate

valuation methods is the responsibility of the valuer based on the facts of each valuation task.

The guidance in this paper presumes that the reader is familiar with the International Valuation Standards (IVS).

Of particular relevance are the concepts and principles discussed the IVS Framework and the provisions of IVS

200 Businesses and Business Interests and IVS 230 Real Property Interests.

iv

dcf tip post consult v9

Contents

Paragraph page

Introduction 1-2 #

Definitions 3 #

When to Use DCF 4-5 #

Overview 6-8 #

Explicit Forecast Period 9-10 #

Cash Flow Forecasts 11-15 #

Terminal Value 16-22 #

Discount Rate 23-29 #

Internal Rate of Return 30 #

Bases of Value 31-36 #

Consistent Inputs 37-40 #

Reporting 41-44 #

Illustrative Examples 1 – Real Property Valuation #

Illustrative Examples 2 – Business Valuation

Illustrative Examples 3 – WACC calculation

#

#

1

Introduction

1. The discounted cash flow (DCF) method is a valuation method falling under the income approach as

defined in the IVS Framework1. The objective of this TIP is to describe the principles of the DCF method

and provide high level examples of its application. The DCF method can be applied to a wide range of

different asset types. The examples in this TIP are of its application to business interests and investment

property. Although the principles discussed in this TIP may be applied to other assets, the application of

various methods, including DCF to intangible assets is specifically discussed in IVSC TIP 3 The Valuation

of Intangible Assets and to financial instruments in a TIP that is currently undergoing development.

2. Properly applied, the DCF method can provide an appropriate measure for different bases of value. This

TIP illustrates inputs that may be appropriate when estimating market value and investment value.

However, the techniques examined may be applied to estimate other bases of value, for example fair value

or value in use under International Financial Reporting Standards. For more information on these two bases

see IVS 300 Valuations for Financial Reporting.

Definitions

3. The following defined words and terms have particular relevance to the discounted cash flow method and

appear in this TIP. Other words and terms that are also defined in the IVS Glossary may be used but are

not listed below in the interests of brevity.

Term Proposed Definition

Capitalisation Factor The multiple applied to a representative single period income to convert it into a capital value.

Capitalisation Rate The return represented by the income produced by an investment, expressed as a percentage.

Cash Flow Cash that is generated over a period of time by an asset, group of assets, or business enterprise.

Discount Rate A rate of return used to convert a future monetary sum or cash flow into present value.

Discounted Cash Flow Method

A method within the income approach in which a discount rate is applied to all future expected income streams to estimate the present value.

Enterprise Value The total value of the equity in a business plus the value of its debt or debt-related

liabilities, minus any cash or cash equivalents available to meet those liabilities.

Free Cash Flows to Equity

Cash flows available to pay out to equity owners after funding operations of the business, making necessary capital investments, and increasing or decreasing debt financing.

1 IVS Framework 2011 paras 59-62

2

Term Proposed Definition

Free Cash Flows to the

Firm

Cash flows available to pay out to equity holders and debt investors (in the form of

principal and interest) after funding operations of the business enterprise and

making necessary capital investments.

Income Approach A valuation approach that provides an indication of value by converting future cash flows to a single current capital value.

Initial Yield The initial income from an investment divided by the price paid for the investment

expressed as a percentage.

Internal Rate of Return The discount rate at which the present value of the future cash flows of the

investment equals the acquisition cost of the investment.

Investment Property

Property that is land or a building, or part of a building, or both, held by the owner

to earn rentals or for capital appreciation, or both.

Investment Value The value of an asset to the owner or a prospective owner for individual investment or operational objectives.

Market Risk Risk that affects an entire market not just specific participants or assets. Market Risk cannot be diversified. Also referred to as systematic risk.

Market Value The estimated amount for which an asset should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion.

Net Present Value The value, as of a specified date, of future cash inflows less all cash outflows (including the cost of investment) calculated using an appropriate discount rate.

Nominal Cash Flows Cash flows expressed in monetary terms in a given period or series of periods.

Present Value The value of a future payment or series of future payments discounted to the Valuation Date or to time period zero.

Prospective Financial Information

Forecast financial data used to estimate cash flows in a discounted cash flow model.

Rate of Return An amount of income (loss) and/or change in value realised or anticipated on an investment, expressed as a percentage of that investment.

Real Cash Flows Nominal cash flows adjusted to exclude the effect of price changes over time.

Risk Free Rate The rate of return available in the market on an investment free of default risk.

Risk Premium The rate of return in excess of the risk-free rate that an investment is expected to return to reflect the default risk associated with an investment.

Systematic Risk Risk that affects an entire market and not just specific participants or assets. Systematic Risk cannot be diversified. Also referred to as market risk.

3

Term Proposed Definition

Terminal Value The continuing value at the end of the explicit period over which cash flows are projected in a discounted cash flow analysis.

Unsystematic Risk Risk that is specific to an entity or asset or group of assets. Can be diversified.

Weighted Average Cost of Capital

A discount rate determined by the weighted average, at market value, of the cost of all financing sources in a business enterprise’s capital structure.

Yield The return on an investment. Usually expressed annually as a percentage based on an investment's cost, its current market value or its face (par) value. Often used with a qualifying word or phrase.

When to use the DCF Method

4. The DCF method can be used to value most assets that generate cash flows. It may provide a better

indication of value than other methods where:

• the asset or business is experiencing significant growth or has yet to reach a mature level of

operations, eg a new business venture or an investment property under construction;

• cash flows are likely to fluctuate from period to period in the short term, eg fluctuations to rental income

generated by an investment property due to leasing terms and conditions or to a business’s income

because of cyclical changes in demand for its products; or

• the asset has a limited life, eg assets and businesses in the energy and natural resource sector.

Overview

5. The value of any asset is a reflection of the present value of the net benefits derived from that asset.

Although there are distinct terms and inputs used when applying the DCF method to valuations of real

property and businesses, the basic principles of the method are the same.

6. The DCF method results in an indication of value whereby forecast cash flows are discounted back to the

Valuation Date, resulting in a present value for the cash flow stream of the asset or business. A terminal

value at the end of the explicit forecast period is then determined and that value is also discounted back to

the Valuation Date to give an overall value for the asset or business.

The following key inputs are required for the DCF method:

a. determination of the period over which the cash flows will be forecast;

b. explicit cash flow forecasts for that period;

c. the asset or business value at the end of the forecast period, ie the terminal value; and

d. an appropriate discount rate to apply to the future cash flows, including the terminal value.

Explicit Forecast Period

4

7. The duration of the explicit forecast period requires careful consideration and is normally determined by one

of the following criteria:

a. where cash flows are likely to fluctuate, the length of time for which changes in the cash flows can

be reasonably predicted;

b. the length of time to enable the business or asset to achieve a stabilised level of earnings;

c. the life of the asset; or

d. the intended hold period of the asset.

8. The selection criteria will depend upon the purpose of the valuation, the nature of the asset, the information

available and the required bases of value. For an asset with a short life it is more likely to be both possible

and relevant to project cash flows over its entire life. For some assets there may be an accepted norm

among market participants for the length of forecast period and this would need to be taken into account if

the basis required is market value. The period over which an asset is intended to be held may be the most

appropriate factor in determining the explicit forecast period if the objective of the valuation is to determine

its investment value.

Cash Flow Forecasts

9. Cash flows for the explicit forecast period are constructed using prospective financial information, ie

expected income (cash inflows) and expected expenditure (cash outflows). The cash flows are broken

down into suitable periodic intervals, eg monthly, quarterly or annually, with the choice of interval depending

upon the pattern of the cash flows, the data available and the length of the forecast period. The cash flow

model should be constructed so as to adequately capture scheduled future events, eg contract

terminations, contract reviews on the dates on which they fall due, or expected future events that are

expected to trigger changes to the cash inflows and outflows on the dates when they are expected to occur.

10. The prospective financial information may be used to determine the contracted, promised or most likely

future cash flows, or on expected cash flows that are probability weighted. The latter is sometimes known

as the “expected present value” technique. The type of cash flow model used will depend on market

practice for the type of asset or the nature of the prospective financial information available.

11. Forecast cash flow estimates will need to be based on appropriate assumptions. The suitability of these

assumptions will depend upon the purpose of the valuation and the required bases of value. For market

value the cash flows should reflect those that would be anticipated by market participants; in contrast

investment value can be measured using cash flows that are based on the reasonable forecasts of the

particular entity.

12. The cash flows used within the DCF method can be measured on the basis of Free Cash Flows to the Firm

(FCFF) (ie, the cash flow available for distribution to both equity holders and debt investors, after funding

operations of the business and making necessary capital investments), as well as Free Cash Flow to Equity

(FCFE) (ie, the cash flow available for distribution to equity holders after funding operations of the business,

making necessary capital investments and increasing/decreasing debt funding).

5

13. The forecast cash flows may be nominal, ie cash flows reflecting the effects of expected price changes, or

may be real, ie with an adjustment made to remove the effects of price changes over time. The choice will

depend upon the purpose of the valuation, the data available, and market practice.

14. Where prospective financial information for a business is based upon accounting data, adjustments may be

necessary to reconcile profit to cash flow. Non-cash expenses, such as depreciation and amortization are

added back and cash outflows relating to capital expenditure or to changes in working capital are taken out

in translating profit to cash flow.

Terminal Value

15. Where the asset or business is expected to continue beyond the explicit forecast period, it is necessary to

determine the continuing value of the asset or business as at the end of the explicit forecast period. In

calculating this terminal value, regard must be had to the asset or business’ potential for further growth

beyond the explicit forecast period. If the DCF method is being used to estimate market value, the terminal

value can be equated to the price that would be obtained in a hypothetical sale of the asset or business at

the end of the forecast period. For estimating investment value the terminal value will reflect the value to

the entity of continuing to hold the asset indefinitely beyond the end of the forecast period. In certain

circumstances, the terminal value may be a predetermined fixed capital amount, for example a receipt

specified in a contract.

16. Terminal value can be calculated using techniques such as applying a capitalisation factor to the final

explicit period + 1 cash flow or by using a constant growth model. The former is commonly used for valuing

investment property, the latter for valuing businesses. The terminal value can also be derived by

introducing other valuation approaches, such as the market approach using an exit multiple.

17. The capitalisation factor method used to derive the terminal value for real property is normally applied as

follows:

Terminal Value = (NRn+1) x capitalisation factor

Where: NRn = the net rent2 receivable in the final year of the explicit forecast period

18. The constant growth method used to derive the terminal value of a business assumes that the business

grows at a constant rate into perpetuity. It is calculated from a normalised cash flow, which is the free cash

flow of a company at steady state. The formula used is:

Terminal Value = ( FCFn * (1+g) ) / (r-g)

Where:

FCFn = free cash flow of the final year of the explicit forecast period

g = pereptual growth rate

2 The income from the property interest after deduction of all outgoings relating to the property paid by the recipient,(eg repairs,

maintenance, insurance and management), but excluding taxes or debt payable by the recipient.

6

r = discount rate (WACC or cost of equity (Ke))

19. It should be born in mind that the terminal value of some assets may have little or no relationship to the

preceding cash flows. An example would be a wasting asset such as a mine or an oil well.

20. The terminal value determined at the end of the explicit forecast period is then discounted back to the

Valuation Date using the same discount rate applied to the forecast cash flows, unless the risk is

considered to be different to the risk over the explicit forecast period

21. When the forecast period is short the calculation of the terminal value becomes more critical as it

represents a higher proportion of the current value. Where this is the case extra vigilance is required to

ensure that the assumptions made in constructing the cash flow used in the terminal value calculation are

appropriate and that there are no probable changes that would be better reflected by extending the forecast

period to allow them to be explicitly reflected.

Discount Rate

22. The rate at which the forecast cash flows are discounted should reflect not only the time value of money, but

also the risk associated with the asset or business’s future operations. This means that in order for a DCF to

provide a reliable valuation figure, the importance of the quality of the underlying cash flow forecasts is

fundamental.

23. The discount rate applied is dependent on the basis of value required, the type of asset or the cash flows

utilised. Where the objective of valuation is to estimate market value, the discount rate should reflect market

participants’ view of risk. If the objective is to estimate investment value, the discount rate will reflect the

target rate of return that a specific investor requires having regard to the risks inherent in asset.

24. The discount rate used should also reflect the nature of the cash flows. For example, a discount rate that

reflects expectations about future defaults is appropriate if using contractual, promised or most likely cash

flows (ie a discount rate adjustment technique). That same rate should not be used if using expected (ie

probability-weighted) cash flows (ie an expected present value technique) because the expected cash flows

already reflect assumptions about future defaults; instead, a discount rate that is commensurate with the risk

inherent in the expected cash flows shall be used.

25. For business entities the cash flows are normally discounted using either the weighted average cost of

capital (WACC) or the cost of equity. FCFF are discounted using a WACC (which reflects an optimal, as

opposed to actual) financing structure (adjustments to arrive at the optimal structure may be necessary,

where appropriate), and results in an Enterprise Value for the business. Alternatively, a cost of equity

approach can be applied to the Free Cash Flows to Equity to derive the Equity Value for the business. An

Equity Value reflects the value that accrues to the equity holders. Alternatively, to arrive at Equity Value, the

market value of net debt must be deducted from the Enterprise Value. If applied correctly, both approaches

will yield the same result.

26. The WACC is the rate of return market participants would require to invest in a given investment and is

calculated as set out below:

7

WACC = Ke * (E/(D+E)) + Kd * (1-T) * (D/(D+E))

Where:

Ke = cost of equity;

E = market value of equity;

Kd = cost of debt;

D = market value of debt; and

T = the corporate taxation rate.

27. The cost of equity represents an investor’s expected rate of return from equity. The cost of equity is not

readily observable in the market. There are several models for estimating the cost of equity, with the most

common method being the Capital Asset Pricing Model (“CAPM”) approach. Under CAPM, the cost of

equity is calculated as follows:

Ke = Rf + β * (Rm – Rf) + α

Where:

Rf = risk free rate – the current rate of return on risk free assets;

Rm = the expected return of the market;

(Rm - Rf) = the risk premium above the risk free rate that a ‘market’ portfolio of assets is

earning;

β = the beta factor, being the measure of systematic (or undiversifiable) risk of a particular asset

relative to the risk of a portfolio of all risky assets; and

α = the alpha factor, being the company specific risk (ie which may reflect country, company and

size risk premium)*

* An adjustment may also be made for this risk through the beta factor.

28. An interest in real property can be, and often is, transferred independently of the owning entity. In active

markets there is normally sufficient data from transactions of interests in similar property that can be

analysed to determine the discount rate that a market participant would require after taking into account

factors such as the quality of the building, the quality of the lessee and the length and other terms of the

lease. This market data is normally the most relevant source for determining the discount rate when the

required basis is market value. Where there is insufficient market data to reliably determine a discount rate,

a rate may be estimated using a “build up” approach.

29. The build up approach to determining a discount rate involves determining the appropriate risk free rate,

normally based on a long dated government bond, and then calculating the additional risk premium to reflect

market risks and asset specific risks. The risk premium for real property will reflect factors such as the

investment risks associated with the real property market compared to the risk free investment and risks

specific to the particular property and property interest. The latter typically will include consideration of the

certainty and security of the income and expenditure that will be incurred by an owner, and the certainty of

the timing of future changes to the cash flows. Factors such as the quality of the building and its location,

the quality of the tenant and the terms of the lease all impact on the risk premium.

Internal Rate of Return

30. A DCF model can also be used to calculate the internal rate of return (“IRR”) of an investment. The IRR is

the discount rate at which the net present value of all the cash flows, including the cost of acquisition equals

8

zero. The IRR may be used to evaluate an investment in terms of the company’s own hurdle rate or cost of

capital. .

Bases of Value

31. The DCF method can be used to determine different bases of value, for example market value and

investment value as defined in IVS or fair value for use in financial reporting as defined in IFRS 133 The

nature of the inputs used will vary depending upon the required basis.

32. The use of the DCF method to determine market value or any similar basis should make use of available

market evidence. As far as possible all inputs should be based on market derived data. Where there is

insufficient market data the inputs should reflect the thought processes, expectations, and perceptions of

investors and other market participants as best as they can be understood. As a technique, the DCF

method should not be judged on the basis of whether expected future income is proven to be correct or not

after the event but rather on the degree of market support for the expectation at the time the valuation is

prepared.

33. If a cash flow forecast provided by a particular owner or prospective owner is to be used in estimating

market value, it should be tested against market evidence and expectations. Assumptions of growth or

decline in income would normally be premised on analysis of economic and market conditions and

discussions with management about the expectation for the asset or business performance. Changes in

operating expenses should reflect all expense trends and specific trends for significant expense items. If the

forecast provided differs from market expectations it cannot be used to derive an indication of market value.

34. All valuation inputs and assumptions should have regard to the conceptual framework for market value in

the International Valuation Standards.4

Sufficient research should be undertaken to ensure that cash flow

projections or expectations and the assumptions that are the basis for the DCF method are appropriate,

likely and reasonable for the subject market.

35. When the DCF method is being used to estimate investment value the inputs used such as the discount

rate, discount period and cash flow assumptions may differ from those that would be used by a market

participant.

36. The cash flows may reflect the expectation of market participants or be specific to the present owner or a

prospective owner. The discount rate used will normally be determined by entity specific criteria, e.g. a

target or hurdle rate of return, an opportunity cost or the entity’s WACC rate. An example could be where a

DCF model is used to calculate the investment value to a prospective buyer of a business. The prospective

buyer may wish to determine the level of cash flows that would be needed for the potential target to

generate its required target rate of return before entering the market.

Consistent inputs.

3 IFRS 13 published by IFRS Foundation, see also IVS 300 Valuations for Financial Reporting

4 IVS Framework paras 30 – 35

9

37. As indicated in paras 12 and 13 cash flows may be fixed or variable, gross or net of tax, gross or net of debt

finance costs or reflective or non-reflective of anticipated inflation or deflation. It is important that the cash

flows and discount rates are internally consistent.

38. The decision as to whether it is better to use a DCF model based on nominal or real cash flows, or pre-tax

or post-tax cash flows, will depend upon the facts and circumstances of the asset being valued, the data

that is available and the practice in the relevant market. If the evidence in the market was based on pre-tax

cash flows and pre-tax discount rates, it would normally be inappropriate to adjust that evidence to create

post-tax equivalents if the objective was to estimate market value, although such adjustments might be

appropriate if investment value was required.

39. Similarly, if nominal cash flows are used, care should be taken to ensure that any discount rate derived from

analysis of comparable companies or investment properties are also based on nominal cash flows. If

properly applied, either approach should result in the same answer.

40. Using inputs that differ from the norms in the relevant market increases the probability of error in the

valuation. Cash flows for investment property, ie rents, and discount rates are customarily quoted on a pre-

tax basis. Conversely, discount rate data for businesses is normally quoted on a post-tax basis. Adjusting

between pre-tax and post-tax rates can be complex and prone to error and needs to be approached with

caution.

Reporting

41. IVS 101 Scope of Work and IVS 103 Reporting require all assumptions that are to be made in the course of

a valuation assignment to be recorded. IVS 103 additionally requires the valuation approach to be

identified, the key inputs used and the principal reasons for the conclusion reached to be included in the

report.

42. The extent of the information to enable users of valuations to properly understand the valuation will vary

depending upon the nature of the asset, the purpose of the valuation and the intended recipient. In order to

comply with the reporting requirements of IVS 103 it is recommended that where a DCF method is used to

determine the valuation the following matters be considered for inclusion:

The nature and source of information relied upon (IVS 103 5(h))

• the source of the prospective financial information used to construct the cash flows

Valuation approach and reasoning (IVS 103 5 (l))

• the explicit forecast period including the commencement date of the cash flow and the number,

frequency and term of the periods employed;

• the components of cash inflow and cash outflow grouped by category and the rationale behind their

selection;

• the derivation of, or rationale for, the discount rate;

• the basis of the terminal value calculation;

10

43. It is recommended that the report comment on the possible impact of any changes to the assumptions

made about key inputs to the calculation on the valuation result. This may take the form of a sensitivity

analysis.

44. When another valuation method is used as well as DCF, it is recommended that the report contain either a

reconciliation between the result obtained in the DCF and the result obtained by the other method, or a

clear rationale provided for preferring one or other of the methods as the better indicator of value.

11

Illustrative Examples

IE 1 Real Property

Scenario

The task is to calculate the market value of an office building. The building is about 20 years old. Following substantial expenditure on upgrading the upper floors of the building two years ago, Floors 2-5 were let to a single tenant. The lease of Floor 1 will expire in 18 months and in order to maximise the letting potential and future income, the owner needs to upgrade that accommodation as well. The details of each lease are:

• Floor 1 is 400 m2 and the current rent is CU40,000 pa. T.

• Floors 2 – 5 are 1,600m2 in total and the current rent is CU240,000 pa. The lease commenced 18 months

ago ad expires in 18½ years. The lease provides for the rent to be increased at the end of the 5th year to

CU280,000 pa and at 5 yearly intervals thereafter by the rate of inflation over the preceding five years measured by a government index.

• Both leases require the tenant to contribute a proportionate cost of routine building maintenance, security and cleaning by way of a service charge. This is currently CU20,000 per annum.

The current market rent for the upgraded accommodation assuming a lease for a term of at least five years with a six month initial rent free period is:

• Floor 1: CU80,000

• Floors 2-5: CU280,000

The owner can expect to suffer a loss on income when the lease expires on Floor 1, during the time required to undertake the upgrading works and also during the time that will be required after completion of the works for finding a new tenant and the initial rent free period that is customary to give to incoming tenants in the local market. It is estimated that:

• the upgrading work will be complete in 9 months,

• that a further 3 months will be required after completion of the work to secure a new tenant and

• the new tenant would negotiate a 6 month initial rent free period in line with current market norms.

The owner will therefore face period of 18 months with no income from Floor 1. During this period the owner will need to pay the cost of the upgrading work, the unrecoverable service charge and the costs of marketing and leasing to the new tenant. Forecast Period

The projected income is forecast to be stabilised by Q3 of year 4 after the fixed rental increase on Floors 2-5 to CU280,000 has occurred. Although further index linked increases occur after 10 and 15 years it would be of questionable benefit to extend the explicit income projections beyond December 2015 due to the greater uncertainty of projecting income fluctuations significantly further into the future and because the present value of those fluctuations will also diminish in future periods. A forecast period of 4 years is therefore adopted. Because the rent is received quarterly, the cash flow is analysed on a quarterly basis.

Discount Rate

The cash flows are based on nominal figures. A discount rate of 7% has been adopted, based on analysis of recent market transactions and after making due adjustments for the comparative risks to future income arising from quality of the building and location, the quality of the tenant and the terms of the lease.

12

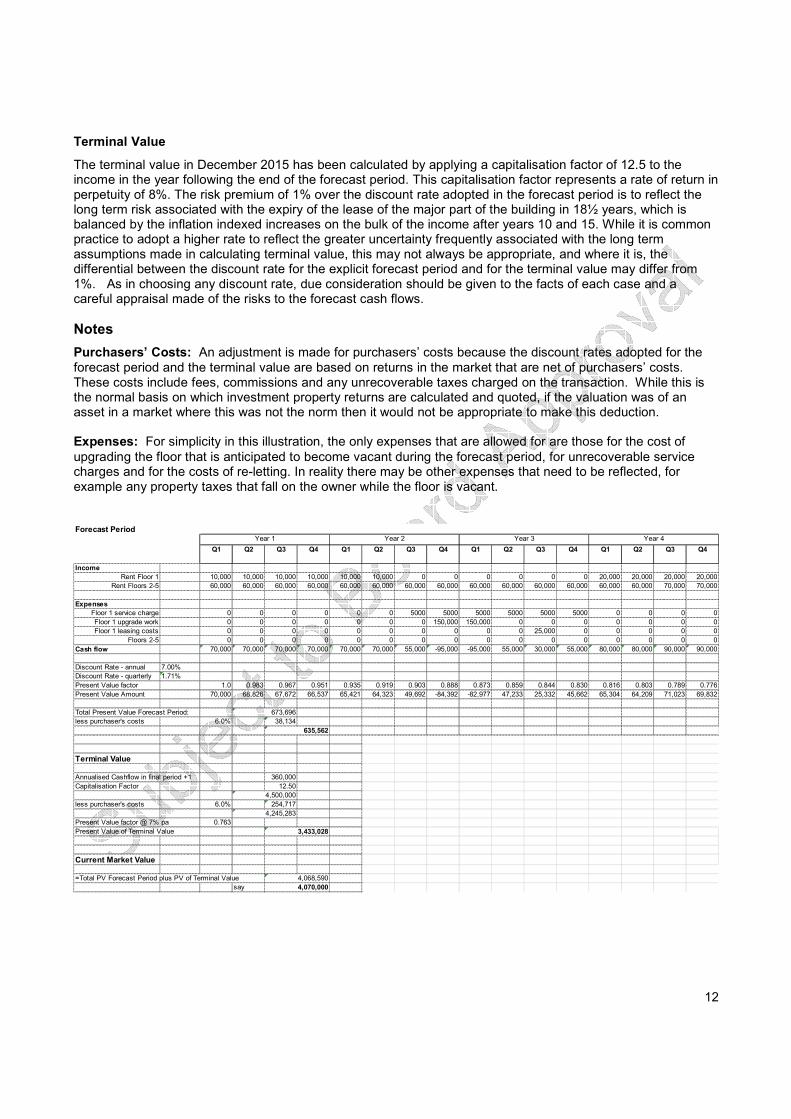

Terminal Value

The terminal value in December 2015 has been calculated by applying a capitalisation factor of 12.5 to the income in the year following the end of the forecast period. This capitalisation factor represents a rate of return in perpetuity of 8%. The risk premium of 1% over the discount rate adopted in the forecast period is to reflect the long term risk associated with the expiry of the lease of the major part of the building in 18½ years, which is balanced by the inflation indexed increases on the bulk of the income after years 10 and 15. While it is common practice to adopt a higher rate to reflect the greater uncertainty frequently associated with the long term assumptions made in calculating terminal value, this may not always be appropriate, and where it is, the differential between the discount rate for the explicit forecast period and for the terminal value may differ from 1%. As in choosing any discount rate, due consideration should be given to the facts of each case and a careful appraisal made of the risks to the forecast cash flows.

Notes

Purchasers’ Costs: An adjustment is made for purchasers’ costs because the discount rates adopted for the

forecast period and the terminal value are based on returns in the market that are net of purchasers’ costs. These costs include fees, commissions and any unrecoverable taxes charged on the transaction. While this is the normal basis on which investment property returns are calculated and quoted, if the valuation was of an asset in a market where this was not the norm then it would not be appropriate to make this deduction. Expenses: For simplicity in this illustration, the only expenses that are allowed for are those for the cost of

upgrading the floor that is anticipated to become vacant during the forecast period, for unrecoverable service charges and for the costs of re-letting. In reality there may be other expenses that need to be reflected, for example any property taxes that fall on the owner while the floor is vacant.

Forecast Period

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Income

Rent Floor 1 10,000 10,000 10,000 10,000 10,000 10,000 0 0 0 0 0 0 20,000 20,000 20,000 20,000

Rent Floors 2-5 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 60,000 70,000 70,000

Expenses

Floor 1 service charge 0 0 0 0 0 0 5000 5000 5000 5000 5000 5000 0 0 0 0

Floor 1 upgrade work 0 0 0 0 0 0 0 150,000 150,000 0 0 0 0 0 0 0

Floor 1 leasing costs 0 0 0 0 0 0 0 0 0 0 25,000 0 0 0 0 0

Floors 2-5 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Cash flow 70,000 70,000 70,000 70,000 70,000 70,000 55,000 -95,000 -95,000 55,000 30,000 55,000 80,000 80,000 90,000 90,000

Discount Rate - annual 7.00%

Discount Rate - quarterly 1.71%

Present Value factor 1.0 0.983 0.967 0.951 0.935 0.919 0.903 0.888 0.873 0.859 0.844 0.830 0.816 0.803 0.789 0.776

Present Value Amount 70,000 68,826 67,672 66,537 65,421 64,323 49,692 -84,392 -82,977 47,233 25,332 45,662 65,304 64,209 71,023 69,832

Total Present Value Forecast Period:

less purchaser's costs 6.0% 38,134

Terminal Value

Annualised Cashflow in final period +1 360,000

Capitalisation Factor 12.50

less purchaser's costs 6.0% 254,717

Present Value factor @ 7% pa 0.763

Present Value of Terminal Value

Current Market Value

=Total PV Forecast Period plus PV of Terminal Value

say 4,070,000

Year 1 Year 2 Year 3 Year 4

4,068,590

673,696

635,562

4,500,000

4,245,283

3,433,028

13

IE 2 Business Valuation

Introduction

The following four simplified examples illustrate how the enterprise value of a business under a DCF method is identical whether the basis on which the cash flow projections are prepared is FCFF, FCFE or based on real or nominal terms. While this illustrates the underlying theory, in practice the type of cash flow used will depend on the nature of the business or the type of asset and the market in which it operates. As indicated in para 40 it is not recommended that information based on one set of data assumptions be adjusted for use with another set of data assumptions. Additionally, the examples consider terminal value based on both a constant growth model as well as assuming an exit multiple.

Scenario

In this scenario the valuer has been engaged to provide an estimate of the market value of a company that distributes

food products. Management has requested that both the Enterprise Value and Equity Value be determined. Management expects revenue of £200m in the first year and to maintain a constant Earnings Before Interest, Tax, Depreciation and Amortisation (“EBITDA”) margin of 20% each year. Revenue is forecast to grow at 4% per annum for the explicit forecast period, which is assumed to last four years, after which the company’s earnings are expected to have stabilised. Depreciation is estimated at 2.5% of revenue, capital investment is assumed to equal depreciation, and working capital is estimated at 2% of revenue. The company operates in the UK and a long term tax rate assumption of 23% has been assumed over the forecast period. The company looks at its forecasts on both a nominal and real basis, with its long term inflation assumption set at 4% per annum. In determining an appropriate terminal value, it would be reasonable to assume a constant growth rate of 4% after the explicit forecast period. The valuer considered through the cycle as well as prospective multiples and considered 12.2x to be an appropriate multiple to apply as an exit multiple. Given that that the value of the company is derived from management’s ability to generate future cash flows from the business, and given that a four year business forecast is available as at the Valuation Date, the valuer considers the DCF approach to be most appropriate in determining the value of the company. As at the Valuation Date, a nominal WACC of 9.5% was determined using the method described in para 26. A detailed calculation to support the WACC is presented in IE 3. This corresponds to a real WACC of 5.5%.

14

Example 1 - FCFF (post-tax / nominal CFs, constant growth TV)

£m

Year 1 2 3 4 Terminal value

Revenue 200.0 208.0 216.3 225.0 234.0

EBITDA 40.0 41.6 43.3 45.0 46.8

Less depreciation (5.0) (5.2) (5.4) (5.6) (5.8)

EBIT 35.0 36.4 37.9 39.4 40.9

Tax (8.1) (8.4) (8.7) (9.1) (9.4)

Add depreciation 5.0 5.2 5.4 5.6 5.8

Capital expenditure (5.0) (5.2) (5.4) (5.6) (5.8)

Working capital movement (0.2) (0.2) (0.2) (0.2) (0.2)

FCFF 26.8 27.9 29.0 30.1 31.3

Terminal value CF 569.4

Discount period 1.0 2.0 3.0 4.0 4.0

Discount factor 0.913 0.834 0.762 0.695 0.695

Present value 24.5 23.2 22.1 21.0 396.0

Enterprise value 486.8

Less debt (243.4)

Equity value 243.4

Key assumptions

EBITDA margin 20.0%

Tax 23.0%

WACC 9.5%

TV grow th 4.0%

Example 2 - FCFF (post-tax / nominal CFs, capitalisation factor TV)

£m

Year 1 2 3 4 Terminal value

Revenue 200.0 208.0 216.3 225.0 234.0

EBITDA 40.0 41.6 43.3 45.0 46.8

Less depreciation (5.0) (5.2) (5.4) (5.6)

EBIT 35.0 36.4 37.9 39.4

Tax (8.1) (8.4) (8.7) (9.1)

Add depreciation 5.0 5.2 5.4 5.6

Capital expenditure (5.0) (5.2) (5.4) (5.6)

Working capital movement (0.2) (0.2) (0.2) (0.2)

FCFF 26.8 27.9 29.0 30.1

Terminal value CF 569.4

Discount period 1.0 2.0 3.0 4.0 4.0

Discount factor 0.913 0.834 0.762 0.695 0.695

Present value 24.5 23.2 22.1 21.0 396.0

Enterprise value 486.8

Less debt (243.4)

Equity value 243.4

Key assumptions

EBITDA margin 20.0%

Tax 23.0%

WACC 9.5%

TV grow th rate 4.0%

Capitalisation factor (EBITDA) 12.2x

15

Example 3 - FCFF (post-tax / real CFs, constant growth TV)

£m

Year 1 2 3 4 Terminal value

Revenue 200 200 200 200 200

EBITDA 40.0 40.0 40.0 40.0 40.0

Less depreciation (5.0) (5.0) (5.0) (5.0) (5.0)

EBIT 35.0 35.0 35.0 35.0 35.0

Tax (8.1) (8.1) (8.1) (8.1) (8.1)

Add depreciation 5.0 5.0 5.0 5.0 5.0

Capital expenditure (5.0) (5.0) (5.0) (5.0) (5.0)

Working capital movement - - - - 0.0

FCFF 27.0 27.0 27.0 27.0 27.0

Terminal value CF 486.8

Discount period 1.0 2.0 3.0 4.0 4.0

Discount factor 0.948 0.898 0.851 0.806 0.806

Present value 25.5 24.2 22.9 21.7 392.4

Enterprise value 486.8

Less debt (243.4)

Equity value 243.4

Key assumptions

EBITDA margin 20.0%

Tax 23.0%

WACC - real 5.5%

TV grow th - real 0.0%

Example 4 - FCFE (post-tax / nominal CFs, constant growth TV)

£m

Year 1 2 3 4 Terminal value

FCFF 26.8 27.9 29.0 30.1 31.3

Less interest * (1-tax) (18.7) (19.5) (20.3) (21.1) (21.9)

Plus new debt issued 9.7 10.1 10.5 11.0 11.4

FCFE 17.8 18.5 19.2 20.0 20.8

Terminal value CF 284.7

Discount period 1.0 2.0 3.0 4.0 4.0

Discount factor 0.898 0.807 0.725 0.651 0.651

Present value 16.0 14.9 14.0 13.0 185.5

Equity value 243.4

Add debt 243.4

Enterprise value 486.8

Key assumptions

Tax 23.0%

Cost of equity 11.3%

TV grow th rate 4.0%

16

IE 3 WACC calculation The calculation for the WACC applied in IE2 is set out below, with the cost of equity calculated based on the CAPM approach. As at the Valuation Date, the company has a debt level of 50%, which is also consistent with the market, at a pre-tax interest rate of 10% per annum. Current market conditions dictate a nominal risk free rate of 4% with reference to the UK 10 year government bond, market risk premium of 5% and an asset beta based on that observed for market comparables of 0.60. A company specific adjustment of 2% was also considered appropriate following discussions with management to account for forecasting risk. Based on these assumptions, the concluded nominal WACC was 9.5%.

WACC calculation

Comments

Inputs

Asset beta (unlevered) = 0.60 Derived from comparable company analysis

% total debt = 50.0% Based w ith reference to comparable companies in sector

Corporate tax rate = 23.0% Corporation tax rate

Risk free rate = 4.00% Yield on 10 year UK government bond as at the Valuation Date

Market risk premium = 5.0% Regarded as appropriate in the current investment climate for developed countries

Alpha = 2.0% Company specific risk

Capital Asset Pricing Model ('CAPM')

Risk-Free Rate = 4.00% Yield on 10 year UK government bond as at the Valuation Date

Relevered Equity Beta = 1.06 = Asset beta * ( 1 + ((1 - Tax rate) * (debt / equity)))

Market Risk Premium = 5% Regarded as appropriate in the current investment climate for developed countries

Alpha = 2.0% Company specific risk

Required Equity Return = 11.3% = Risk-Free Rate + (Equity Beta x Market Premium) + alpha

WACC

Required Equity Return = 11.3% Calculated above

Pre-tax cost of debt = 10.0% Return on total debt of comparable risk companies

% total debt = 50% Based w ith reference to comparable companies in sector

% total equity = 50% 1 - % total debt

Corporate tax rate = 23.0% Calculated above

WACC = 9.5% = (% equity * required equity return) + (% debt * (1 - Tax rate) * (cost of debt))