Agência Nacional de Saúde – ANS Federal Regulatory Agency for Health Plans and Health Insurance...

18

Agência Nacional de Agência Nacional de Saúde – ANS Saúde – ANS Federal Regulatory Agency for Federal Regulatory Agency for Health Plans and Health Insurance Health Plans and Health Insurance Renata Gasparello – Regulation Renata Gasparello – Regulation Specialist -Actuary Specialist -Actuary IAIS – Solvency and Actuarial Issues IAIS – Solvency and Actuarial Issues Subcommitte Subcommitte Regional Information Session Regional Information Session Santiago – Chile – April 2009 Santiago – Chile – April 2009

-

Upload

darcy-cooper -

Category

Documents

-

view

215 -

download

0

Transcript of Agência Nacional de Saúde – ANS Federal Regulatory Agency for Health Plans and Health Insurance...

Agência Nacional de Saúde – ANSAgência Nacional de Saúde – ANS

Federal Regulatory Agency for Health Plans and Federal Regulatory Agency for Health Plans and Health InsuranceHealth Insurance

Renata Gasparello – Regulation Specialist -Renata Gasparello – Regulation Specialist -ActuaryActuary

IAIS – Solvency and Actuarial Issues SubcommitteIAIS – Solvency and Actuarial Issues Subcommitte Regional Information SessionRegional Information SessionSantiago – Chile – April 2009Santiago – Chile – April 2009

2

AgendaAgenda

• Brazilian Health System

• Background – Brazilian Private Health System

• ANS

• Brazilian Health Plans Market

• Solvency Requirements

• Internal Models

• Challenges

• Expectations and Future

3

Brazilian Health SystemBrazilian Health System

• Brazilian Federal Constitution (1988) states that complete health assitance must be provided to all brazilian citizens.

• Private health systems works in parallel and supplementary with the public system.

4

Background - Brazilian Private Health SystemBackground - Brazilian Private Health System

• Untill 1998 - Heterogeneous market : Companies organized in several structures, including among others insurance companies, all of them offering different and restricted coverages.

• Before 1998 only insurance companies were regulated !

5

• 1998 – Passed a new law (9656 act or “private health plan act”) that provides mainly:

• unlimited admission;

• prohibiting the unilateral rescission of individual contracts (noncancellable policy);

• establishing minimum coverage - no financial limits.

• 2000 - ANS was created;

• 2001 - Insurance companies had to split into new companies to operate exclusively health plans.

Background - Brazilian Private Health SystemBackground - Brazilian Private Health System

6

• Institutional objective:

Promote public interest in supplementary assistance to health, regulating the health plans companies, including their relationships with providers and consumers, contributing to the development of the health actions in Brazil.

Health

Companies

Service

Providers

Consumers

ANSANS

7

• Since 2001 ANS has been regulating structural aspects of this market – e.g:

• health assistance quality standards;

• minimum accounting standards;

• requirements for senior management and board of directors;

• licensing and liquidation of health companies;

• pricing control for individual policies;

• mergers and acquisitions need the ANS’ approval;

• portfolio transfer;

• minimum solvency and actuarial requirements;

• liquidity and financial aspects.

• In 2005 ANS acquired a definitive staff.

ANSANS

8

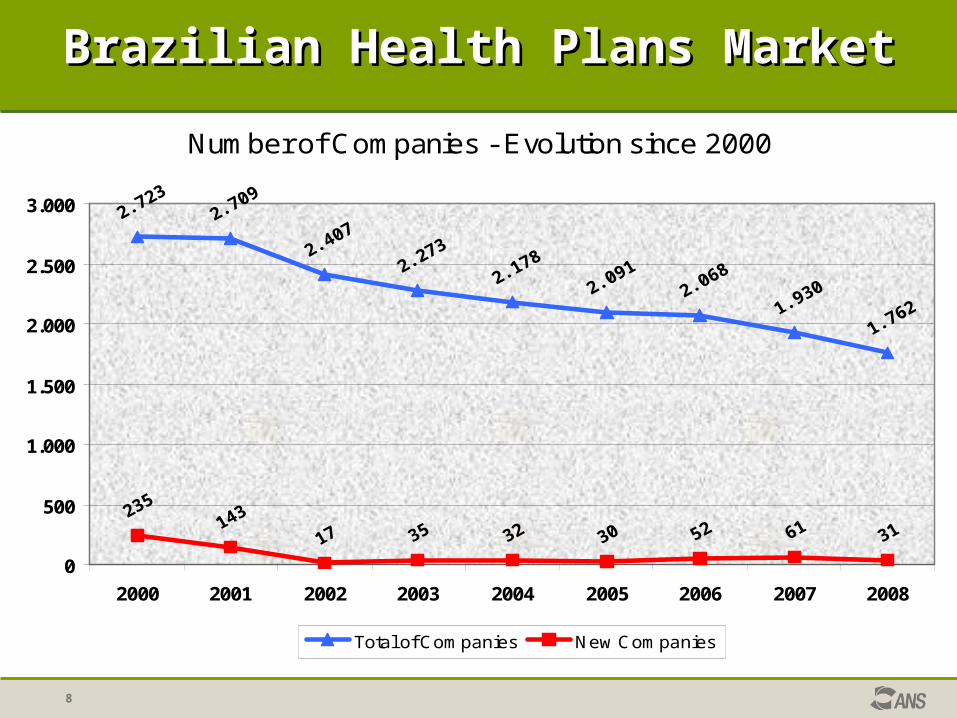

Number of Companies - Evolution since 2000

0

500

1.000

1.500

2.000

2.500

3.000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Total of Companies New Companies

Brazilian Health Plans MarketBrazilian Health Plans Market

9

Brazilian Health Plans MarketBrazilian Health Plans Market

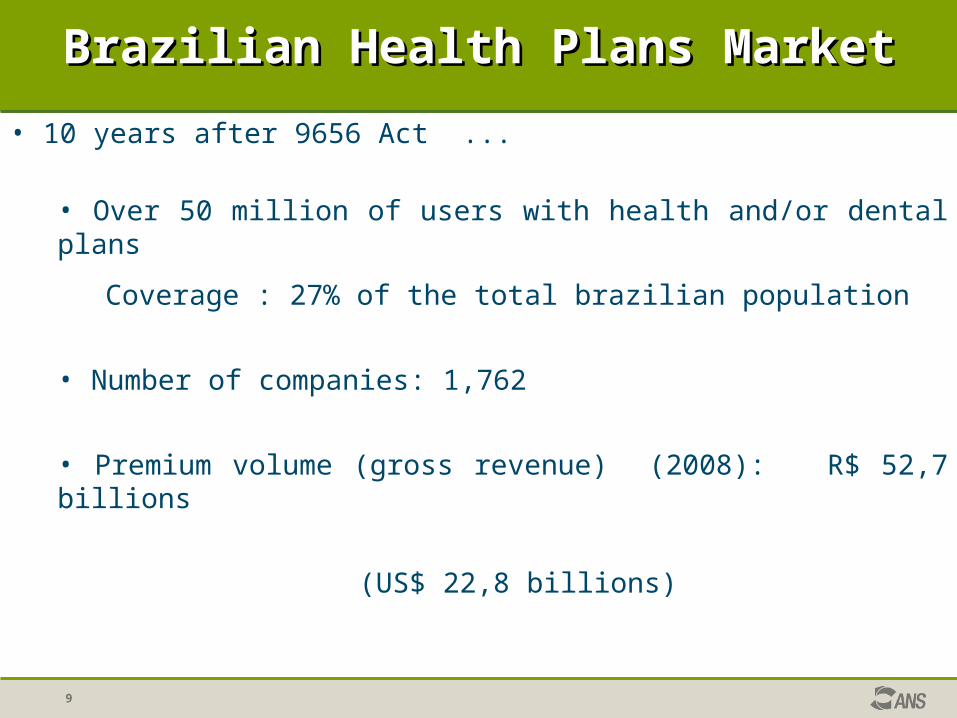

• 10 years after 9656 Act ...

• Over 50 million of users with health and/or dental plans

Coverage : 27% of the total brazilian population

• Number of companies: 1,762

• Premium volume (gross revenue) (2008): R$ 52,7 billions

(US$ 22,8 billions)

10

Brazilian Health Plans MarketBrazilian Health Plans Market

% Companies x % Premiums by type of organization (2008)

0,7%

30,2%

19,7%21,4%

28,0%

20,9%

31,1%

12,5%

1,8%

33,7%

0%

5%

10%

15%

20%

25%

30%

35%

Health Insurance Medicine Group (prepaidgroup practices)

Medical Cooperatives Nonprofit companies Deltal Health PlansCompanies

% Companies % Premiums

Insurance companies Other companies

Unearned premium reserve Unearned premium reserve

Reported but not paid loss reserve Reported but not paid loss reserve

IBNR IBNR (scale of 6 years for full adaptation beginning in 2008)

Minimum Capital Minimum Capital

Solvency MarginSolvency Margin (scale of 6 years for

full adaptation beginning in 2008)

Technical Provisions

Capital Requirements

Solvency RequirementsSolvency Requirements

11

• Minimum actuarial requirements for technical provisions;

• Solvency margin requirements – standard formula calculated as a % of either Premiums or Claims (fixed ratio model);

• The standard formula to be replaced by internal models previously approved by ANS;

• Requirements regarding the admissible types of assets to cover technical provisions (asset mix and diversification).

• Quarterly Monitoring :

• Financial analisys – financial ratios (emphasis on liquidity assessment);

• On-site inspections.

Solvency RequirementsSolvency Requirements

12

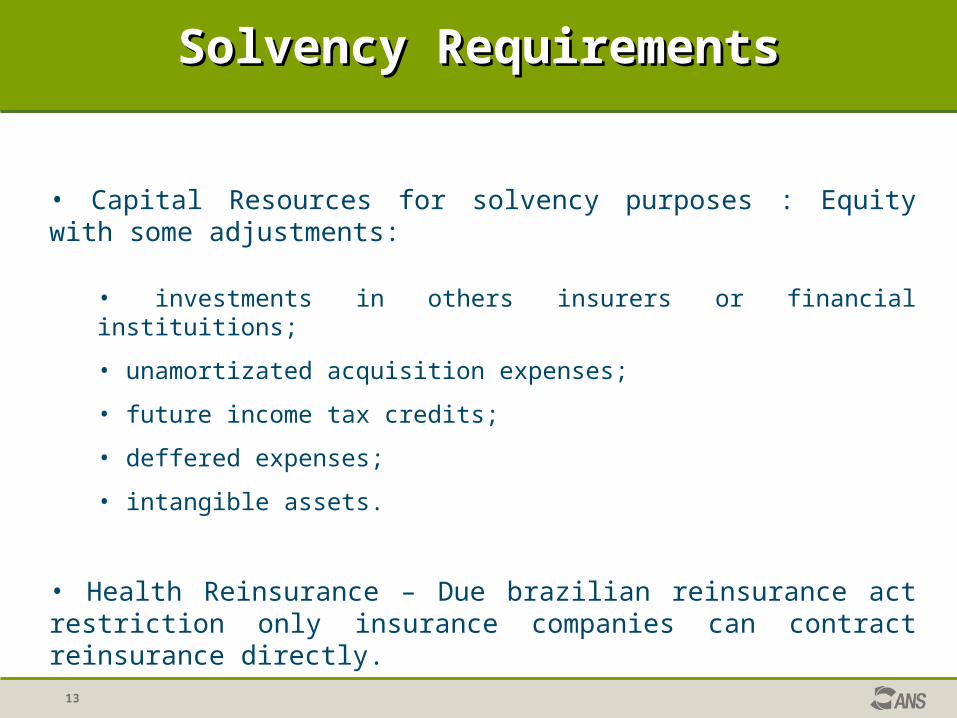

• Capital Resources for solvency purposes : Equity with some adjustments:

• investments in others insurers or financial instituitions;

• unamortizated acquisition expenses;

• future income tax credits;

• deffered expenses;

• intangible assets.

• Health Reinsurance – Due brazilian reinsurance act restriction only insurance companies can contract reinsurance directly.

Solvency RequirementsSolvency Requirements

13

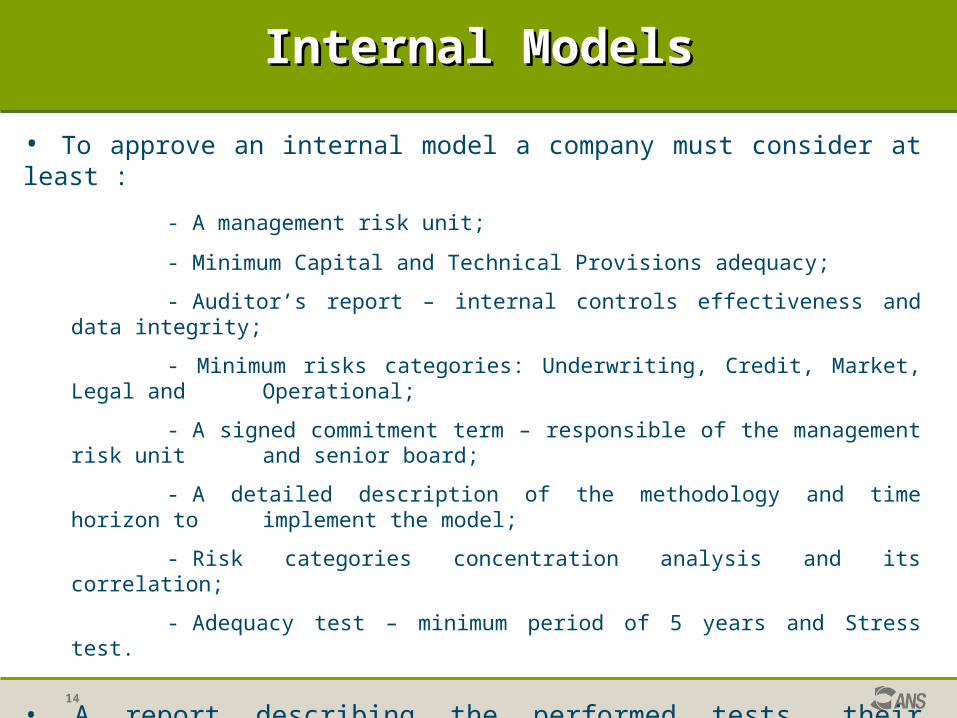

• To approve an internal model a company must consider at least :

- A management risk unit;

- Minimum Capital and Technical Provisions adequacy;

- Auditor’s report – internal controls effectiveness and data integrity;

- Minimum risks categories: Underwriting, Credit, Market, Legal and Operational;

- A signed commitment term – responsible of the management risk unit and senior board;

- A detailed description of the methodology and time horizon to implement the model;

- Risk categories concentration analysis and its correlation;

- Adequacy test – minimum period of 5 years and Stress test.

• A report describing the performed tests, their reliability and assuring that the model is adequated to the company’s reality.

Internal ModelsInternal Models

14

15

ChallengesChallenges

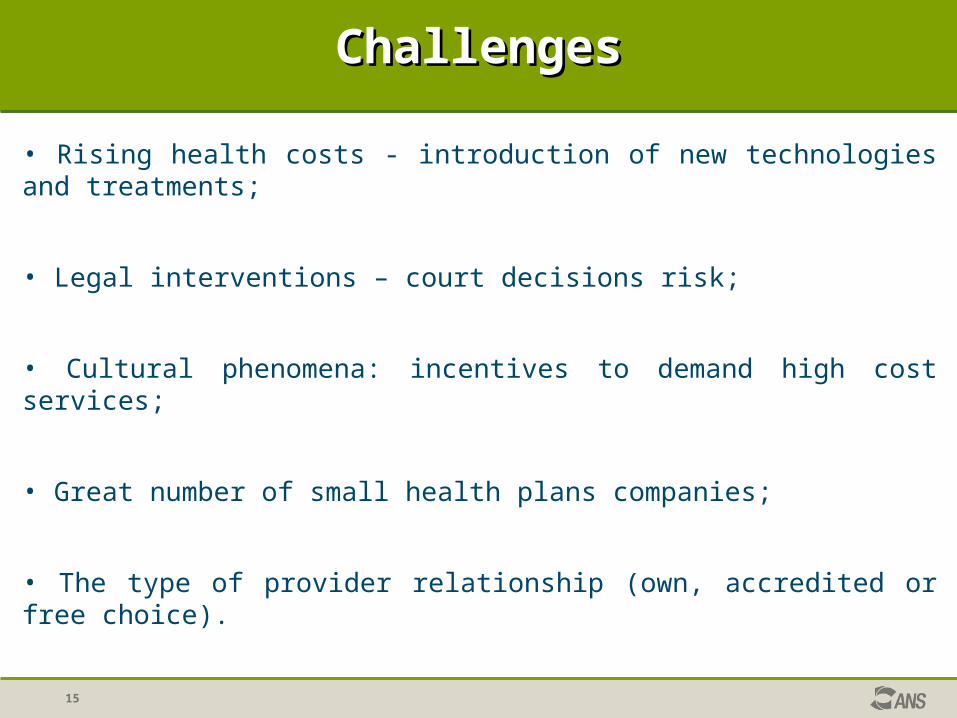

• Rising health costs - introduction of new technologies and treatments;

• Legal interventions – court decisions risk;

• Cultural phenomena: incentives to demand high cost services;

• Great number of small health plans companies;

• The type of provider relationship (own, accredited or free choice).

16

ChallengesChallenges

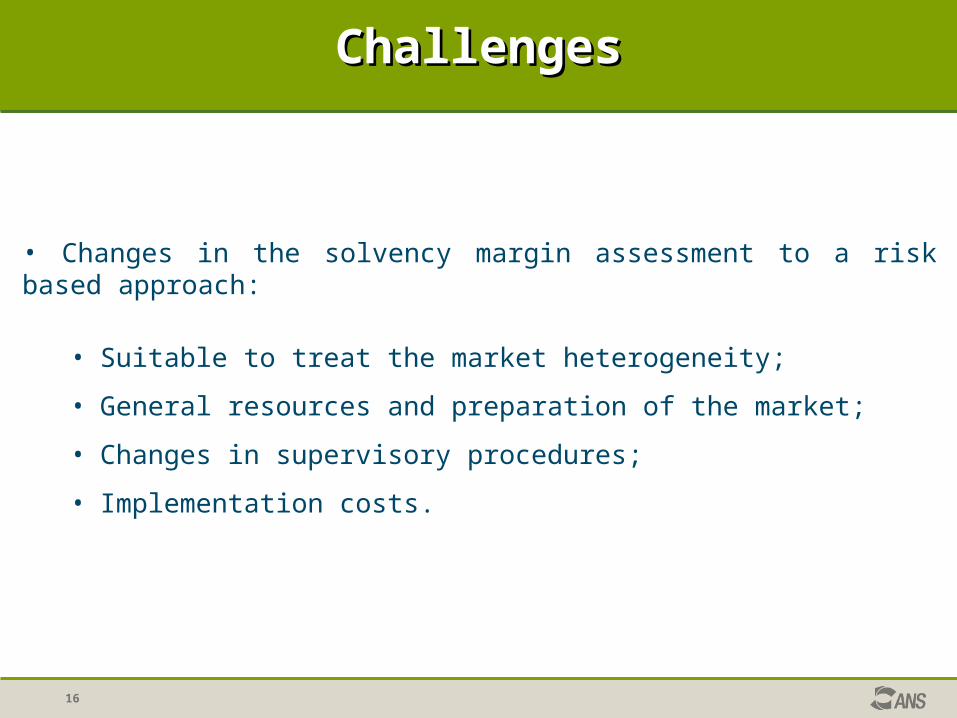

• Changes in the solvency margin assessment to a risk based approach:

• Suitable to treat the market heterogeneity;

• General resources and preparation of the market;

• Changes in supervisory procedures;

• Implementation costs.

17

Expectations and Future Expectations and Future

• Reduction of the number of companies;

• Increasing industry maturity;

• Changes of accounting standards – IFRS;

• Development of Corporate Governance and ERM requirements;

• Portability – competition increasing;

• Development of group solvency assessment with SUSEP.