AG - Prime Academyprimeacademy.com/questions/model/26msugpeiig1.pdf · Sundry Crcdito; 's 20,000...

45

Prime / April 08 Model Exam. 1 AG No.of Question : 8 Total Marks : 100 No of Pages printed: 4 Time Allowed : 3 Hours 1. Amar. Babu and Chander \vere partners in business, sharing profits and losses in the ratio 2 : 1: 1. Their Balance sheet as at 31-3-07 is as follows: BALANCE SHEET As at 31.3.07 (Figures in Rs.’000) Liabilities Rs. Assets Rs. Fixed Capital : Amar 200 Fixed Asets 300 Babu 100 Investment 50 Chander 100 400 Current assets: Stock 100 Current Accounts: Amar 40 Debtors 60 Babu 20 60 Cash and Bank 150 310 Unsecured Loans 200 . 660 660 On 1.4.07, it is agreed among the partners that BC(P) Ltd., a newly formed company with Babu and Chander having each taken up 100 shares ofRs.l 0 each will take over the firm as a going concern including good\yill but excluding cash and bank balances. The following points are also agreed upon . a. Goodwill will be vellued at 3 years' purchase of super profits. b. The actual profit for the purpose of goodwill valuation will be Rs. 1,00,000. c. Normal rate ofrctum will be 15% on fixed capital. d. All other 2ssctS and ktbilities will be taken over at book values. e. The purchase consideration will be payable partly in shares ofRs. 10 each and partly in cash. Payment in cash being to meet the requirement to discharge Amar, who has agreed to retire.. f. Babu and Chander arc to acquire equal interest in the new company. g. Expenses of liquidation Rs. 40.000. You are required to prepare the necessary Ledger Accounts. (20 marks) 2. Mohan of Agra comrnenced business on 1 51 April, 2003 with a capital ofRs. 33,000. He drew on the average Rs. 3.000 per year. His profits for 3 years were Rs. 7,000; he did not prepare proper 2ccounts for the next two ycnrs. On 31 51 March, 2008 an adjudication order was made against him. He submiTS the following information from which his Statement of Affairs and Deficiency Account ere to be prepared :- Rs Sundry Crcdito;'s 20,000 Mortgage on freehold property 4,000 Creditors secured by Life Policy estimated to be worth Rs. 4,000 12,000 Landlord -- 2 months' rent 200

Transcript of AG - Prime Academyprimeacademy.com/questions/model/26msugpeiig1.pdf · Sundry Crcdito; 's 20,000...

Prime / April 08 Model Exam. 1

AG No.of Question : 8 Total Marks : 100 No of Pages printed: 4 Time Allowed : 3 Hours

1. Amar. Babu and Chander \vere partners in business, sharing profits and losses in the ratio 2 : 1: 1. Their Balance sheet as at 31-3-07 is as follows:

BALANCE SHEET

As at 31.3.07 (Figures in Rs.’000) Liabilities Rs. Assets Rs. Fixed Capital :

Amar 200 Fixed Asets 300 Babu 100 Investment 50 Chander 100 400 Current assets:

Stock 100 Current Accounts: Amar 40 Debtors 60

Babu 20 60 Cash and Bank 150 310 Unsecured Loans 200 .

660 660

On 1.4.07, it is agreed among the partners that BC(P) Ltd., a newly formed company with Babu and Chander having each taken up 100 shares ofRs.l 0 each will take over the firm as a going concern including good\yill but excluding cash and bank balances. The following points are also agreed upon .

a. Goodwill will be vellued at 3 years' purchase of super profits. b. The actual profit for the purpose of goodwill valuation will be Rs. 1,00,000. c. Normal rate ofrctum will be 15% on fixed capital. d. All other 2ssctS and ktbilities will be taken over at book values. e. The purchase consideration will be payable partly in shares ofRs. 10 each and partly in cash.

Payment in cash being to meet the requirement to discharge Amar, who has agreed to retire.. f. Babu and Chander arc to acquire equal interest in the new company. g. Expenses of liquidation Rs. 40.000.

You are required to prepare the necessary Ledger Accounts. (20 marks)

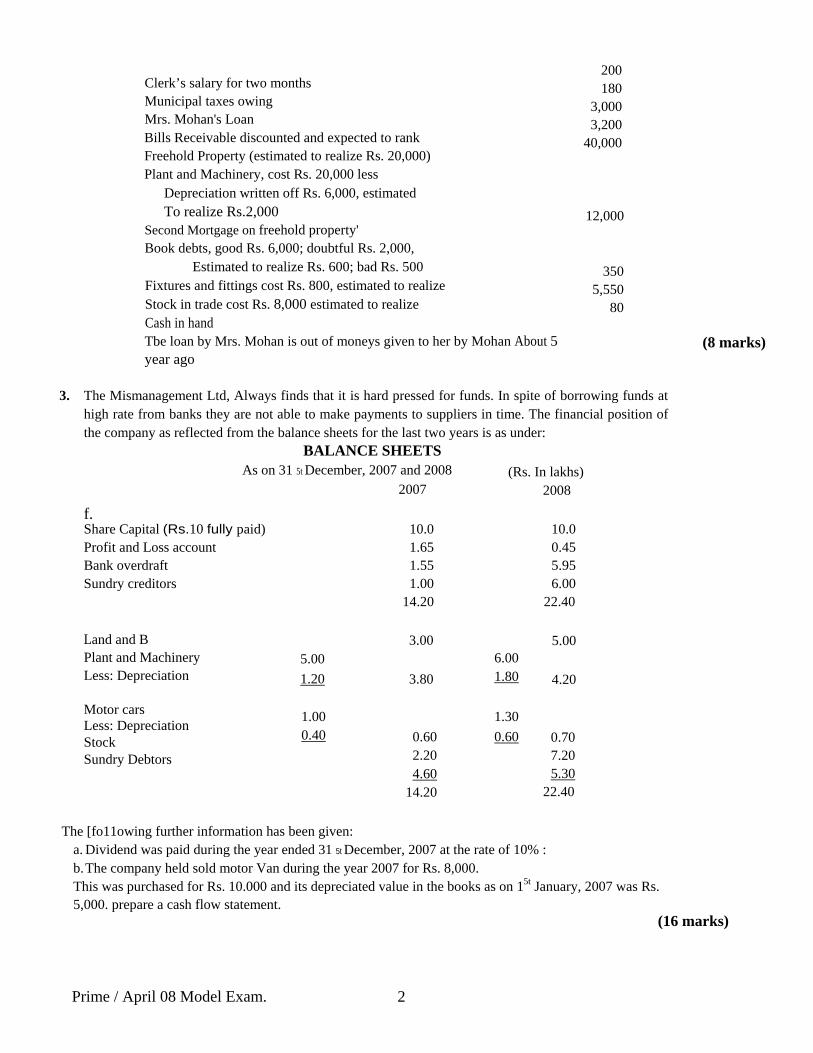

2. Mohan of Agra comrnenced business on 151 April, 2003 with a capital ofRs. 33,000. He drew on the average Rs. 3.000 per year. His profits for 3 years were Rs. 7,000; he did not prepare proper 2ccounts for the next two ycnrs. On 3151 March, 2008 an adjudication order was made against him. He submiTS the following information from which his Statement of Affairs and

Deficiency Account ere to be prepared :- Rs Sundry Crcdito;'s 20,000 Mortgage on freehold property 4,000 Creditors secured by Life Policy estimated to be worth Rs. 4,000 12,000 Landlord -- 2 months' rent 200

Prime / April 08 Model Exam. 2

Clerk’s salary for two months Municipal taxes owing Mrs. Mohan's Loan Bills Receivable discounted and expected to rank Freehold Property (estimated to realize Rs. 20,000) Plant and Machinery, cost Rs. 20,000 less

Depreciation written off Rs. 6,000, estimated To realize Rs.2,000

Second Mortgage on freehold property' Book debts, good Rs. 6,000; doubtful Rs. 2,000,

Estimated to realize Rs. 600; bad Rs. 500 Fixtures and fittings cost Rs. 800, estimated to realize Stock in trade cost Rs. 8,000 estimated to realize Cash in hand Tbe loan by Mrs. Mohan is out of moneys given to her by Mohan About 5 year ago

200 180

3,000 3,200

40,000

12,000

350 5,550 ….80

(8 marks)

3. The Mismanagement Ltd, Always finds that it is hard pressed for funds. In spite of borrowing funds at

high rate from banks they are not able to make payments to suppliers in time. The financial position of the company as reflected from the balance sheets for the last two years is as under:

BALANCE SHEETS As on 31 5t December, 2007 and 2008

2007

(Rs. In lakhs) 2008

f. Share Capital (Rs.10 fully paid) Profit and Loss account Bank overdraft Sundry creditors Land and B Plant and Machinery Less: Depreciation

Motor cars Less: Depreciation Stock Sundry Debtors

5.00 1.20

1.00 0.40

10.0 1.65 1.55 1.00

14.20

3.00

3.80

0.60 2.20 4.60

14.20

6.00 1.80

1.30 0.60

10.0 0.45 5.95 6.00

22.40

5.00

4.20

0.70 7.20 5.30

22.40

The [fo11owing further information has been given: a. Dividend was paid during the year ended 31 5t December, 2007 at the rate of 10% : b. The company held sold motor Van during the year 2007 for Rs. 8,000. This was purchased for Rs. 10.000 and its depreciated value in the books as on 15t January, 2007 was Rs. 5,000. prepare a cash flow statement.

(16 marks)

Prime / April 08 Model Exam. 3

315t March, 2008 of X Ltcl. And Y Ltd. Are as under: X Ltd

Rs. Assets Fixed assets Buildings Machineries Furniture Current assets: Stock Debtors Cash in hand Bank balances

4. The balance sheets as on

Liabilities Share capital: Authorised and subscribed: 60,000 equity shares of Rs.100 each fully paid Reserves and Surplus: General Reserve Profit and Loss Account Current Liabilities and provisions: Creditors

Liabilities Share capital: Authorised and subscribed: 20,000 equity shares of Rs.100 each fully paid Reserves and Surplus: Capital Reserve General reserve Profit and Loss Account Unsecured loan: 12% Debentures Current liabilities and provisions: Creditors

60,00,000

8,00,000 4,80,000

9,60,000

82,40,000

Y Rs.

20,00,000

2,00,000 1,00,000 1,40,000

12,00,000

3,80,000 40,20,000

Ltd. Assets Fixed assets Goodwill Machineries Furniture Current assets: Stock Debtors Cash in hand Bank balances Expenditure on new project

Rs.

20,00,000 26,00,000

40,000

16,00,000 9,20,000 2,80,000 8,00,000

82,40,000

Rs.

4,00,000 16,80,000

20,000

7,20,000 7,20,000

20,000 1,60,000 3,00,000

40,20,000

Y Ltd. \vas absorbed by X Ltd, On 15t April, 2008, on the following terms: a. Fixed assets other than Good will to be valued at Rs. 20,00,000 including Rs. 24,000 for furniture. b. Stock to be reduced by Rs. 80,000 and Debtors by 5%. c. X Ltd. to assume liabilities and to discharge the 12% Debentures by issue of 11 % Debentures of the

same value and in addition a premium of 6% was paid in cash. d. The new project to be valued at Rs. 3,80,000. e. The share holders of Y Ltd. to receive cash payment ofRs. 30 per share plus four equity shares in X

Ltd. For every five shares held in Y Ltd. f. Both the companies to declare and pay dividend 0[6% prior to absorption. g. Expenses of liquidation of y Ltd. are to be reimbursed by X Ltd.

Prepare the Balance Sheet of X Ltd. after absorption assuming that X Ltd's authorized capital has been increased to Rs. 80,00,000.

(16 marks)

Prime / April 08 Model Exam. 4

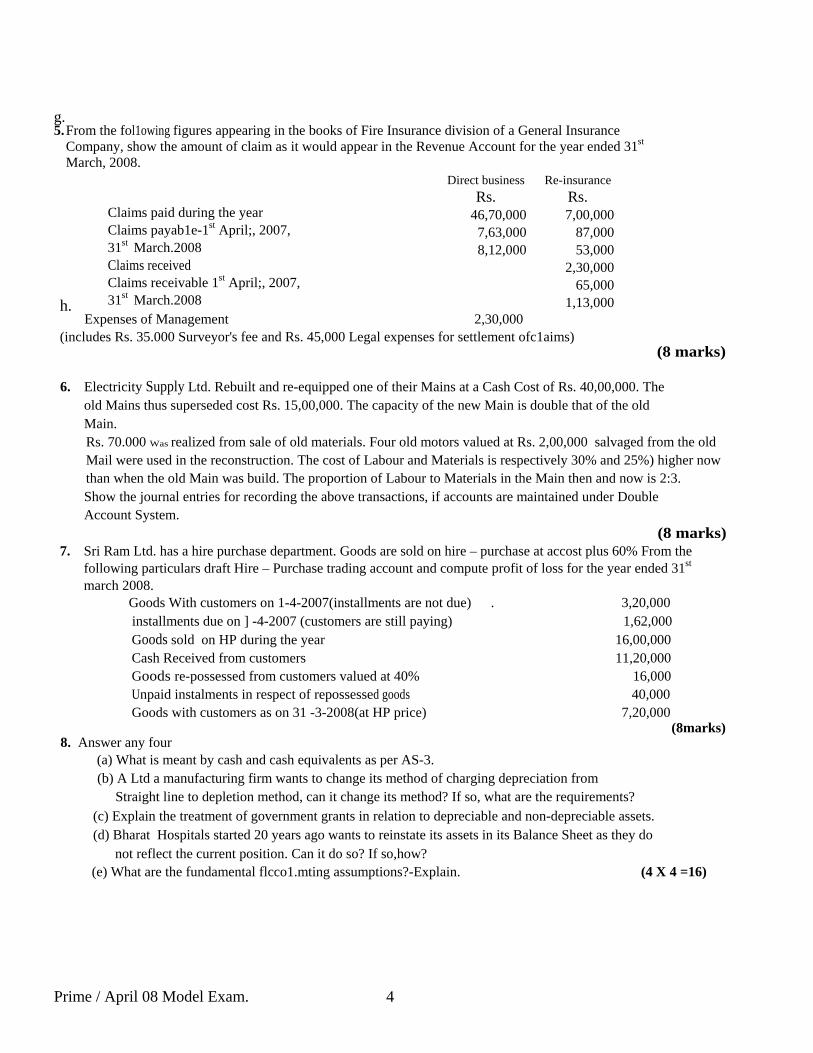

g. 5. From the fol1owing figures appearing in the books of Fire Insurance division of a General Insurance

Company, show the amount of claim as it would appear in the Revenue Account for the year ended 31st March, 2008.

Claims paid during the year Claims payab1e-1st April;, 2007, 31st March.2008 Claims received Claims receivable 1st April;, 2007, 31st March.2008

Direct business Rs.

46,70,000 7,63,000 8,12,000

Re-insurance Rs. 7,00,000

87,000 53,000

2,30,000 65,000

1,13,000 h. Expenses of Management 2,30,000 (includes Rs. 35.000 Surveyor's fee and Rs. 45,000 Legal expenses for settlement ofc1aims)

(8 marks)

6. Electricity Supply Ltd. Rebuilt and re-equipped one of their Mains at a Cash Cost of Rs. 40,00,000. The old Mains thus superseded cost Rs. 15,00,000. The capacity of the new Main is double that of the old Main. Rs. 70.000 Was realized from sale of old materials. Four old motors valued at Rs. 2,00,000 salvaged from the old Mail were used in the reconstruction. The cost of Labour and Materials is respectively 30% and 25%) higher now than when the old Main was build. The proportion of Labour to Materials in the Main then and now is 2:3. Show the journal entries for recording the above transactions, if accounts are maintained under Double Account System.

(8 marks) 7. Sri Ram Ltd. has a hire purchase department. Goods are sold on hire – purchase at accost plus 60% From the

following particulars draft Hire – Purchase trading account and compute profit of loss for the year ended 31st march 2008.

Goods With customers on 1-4-2007(installments are not due) . 3,20,000 installments due on ] -4-2007 (customers are still paying) 1,62,000 Goods sold on HP during the year 16,00,000 Cash Received from customers 11,20,000 Goods re-possessed from customers valued at 40% 16,000 Unpaid instalments in respect of repossessed goods 40,000 Goods with customers as on 31 -3-2008(at HP price) 7,20,000

(8marks) 8. Answer any four

(a) What is meant by cash and cash equivalents as per AS-3. (b) A Ltd a manufacturing firm wants to change its method of charging depreciation from

Straight line to depletion method, can it change its method? If so, what are the requirements? (c) Explain the treatment of government grants in relation to depreciable and non-depreciable assets. (d) Bharat Hospitals started 20 years ago wants to reinstate its assets in its Balance Sheet as they do

not reflect the current position. Can it do so? If so,how? (e) What are the fundamental flcco1.mting assumptions?-Explain. (4 X 4 =16)

Prime / April 08 Model Exam. 5

PRIME ACADEMY 26TH SESSION MODEL EXAM

PE II – ACCOUNTING - (ANSWERS) Basic calculations :

1. Computation of Goodwill : Rs. Weighted average of Actual Profits 1,00,000 Less: Normal profits at 15% of fixed capital employed Of Rs. 4,00,000 60,000 Super profits 40,000 Goodwill at 3 years’ purchase,i.e. 40,000 * 3 1,20,000

2.Computation of purchase consideration : Total assets as per balance sheet 6,60,000 Less : cash and Bank Balances 1,50,000 5,10,000 Add : Goodwill 1,20,000 6,30,000 Less: unsecured loans 2,00,000 Purchase consideration 4,30,000

Ledger Accounts Realisation account Particulars Rs. Particulars Rs. To sundry assets 5,10,000 By unsecured loans 2,00,000 To goodwill 1,20,000 By BC(P) Ltd. 4,30,000 To Bank(Expenses) 40,000 By capital accounts : Amar 20,000 Babu 10,000 Chander 10,000 40,000 6,70,000 6,70,000 Capital Accounts Particulars Amar Babu Chander Particulars Amar Babu Chander To realisa- By bal. c/d 2,00,000 1,00,000 1,00,000 Tion 20,000 10,000 10,000 To cash 2,80,000 By cur. a/c 40,000 20,000 To C (capital By goodwill 60,000 30,000 30,000 adjustment) 10,000 By B(capital adjustment) To shares in BC(P)Ltd 1,30,000 1,30,000 3,00,000 1,50,000 1,40,000 3,00,000 1,50,000 1,40,000

Prime / April 08 Model Exam. 6

Cash and Bank account To Balance b/d 1,50,000 By realization A/c(expenses) 40,000 To BC(P)Ltd.(Bal. figure) 1,70,000 By A’s Capital A/c 2,80,000 3,20,000 3,20,000 BC(P)Ltd. To realization A/c 4,30,000 By cash 1,70,000 By equity shares (Bal. Figure) 2,60,000 (26,000 shares of Rs.10

each) 4,30,000 4,30,000

2. Since accounts were not prepared for 2006-07 and 2007-08 it is necessary to ascertain profit or loss incurred in there two years. Hence, the following trial balance with book figures.

Dr. trial balance Cr. Free hold property 40,000 Capital:introduced 33,000 Plant and Machinery 20,000 Add profit for 3 years 7,000 Less depreciation 6,000 14,000 40,000 Book debts-Good 6,000 Doubtful 2,000 less drawings for 5 years 15,000 25,000 Bad 500 8,500 Sundry creditors 20,000 Fixtures and fittings 800 Mortgage on freehold Property 4,000 Stock in trade 8,000 Creditors secured by policy 12,000 Cash in hand 80 Creditors for expenses - Loss(balancing figure) 5,200 Landlord 200 Salary 200 Taxes 180 580 Mrs. Mohan’s Loan 3,000 Second Mortgage on Free hold property 12,000 76,580 76,580 The trial balance reveals that a total loss of Rs. 5,200 has been incurred during the last two years for which proper accounts were not prepared. Statement of Affairs of Mohan as on March, 31, 1990 Gross Expected Book Estimated Liabilities Liabilities Assets to produce 26,580 unsecured creditors Property as per as per list A 23,580 list E, viz. cash in hand 80 80

Prime / April 08 Model Exam. 7

16,000 creditors fully sec- stock in trade 8,000 5,550 ured as per list Rs. Plant and machinery 14,000 2,000 B 16,000 fixtures and fittings 800 350 Estimated values Book debts as per Of securities 20,000 List F, viz.- Good 6,000 6,000 Surplus to contra 4,000 doubtful 2,000 Bad 500 12,000 creditors partly secured as per estimated to realize 600 list C 12,000 surplus from estimated value securities in the hands securities 4,000 8,000 of creditors fully secured 4,000 200 Creditors for 31,380 18,580 taxes,wages,etc. deduct creditors for being payable in taxes, wages,etc., as full as per list D 200 per list D 200 18,380 deducted as deficiency as per contra 200 explained in list H 13,200 54,780 31,580 31,580 Note : The unsecured creditors in this case will be as follows :- Sundry creditors 20,000 Landlord 200 Salary to clerk 180 Mrs. Mohan’s loan(since moneys were provided by Mohan) nil Bills discounted 3,200 23,580 Deficiency account (list H) Rs. Rs. Excess of assets over liabilities on net loss arising from 1st April, 2003 33,000 carrying on of business from 1st April, 2003 to date of adjudication 5,200 Net profit arising from carrying on Bad debts as per list F 1,900 Of business from 1st April, 2003 to Expenses incurred since Date of adjudication after meeting 1st, April, 2003 other than Usual trade expenses 7,000 usual business expenses, Viz.,household expenses 15,000 Income or profit from other sources Other losses :- Since 1st April 2003-private Loss on realization of : Rs.

Prime / April 08 Model Exam. 8

Life policy 4,000 stock in trade 2,450 Loan from Mrs. Mohan, being not freehold property 20,000 Payable 3,000 Plant and Machinery 12,000 Deficiency as per statement fixtures and fittings 450 Of affairs 13,200 loss on payment of bills Discounted 3,200 38,100 60,200 60,200

3. CASH FLOW STATEMENT For the year ending 31st December 2008

(ii) CASH FROM OPERATIONS Funds from operations Rs. 62,000 Add: Increase in creditors 5, 00,000 5, 62,000 Less: Increase in stock 5, 00,000 Increase in debtors 70,000 5, 70,000 Cash outflow on account of operations (8,000) Cash flow from investing activity: Sale of car 8,000 Purchase of Land and buildings (2, 00,000) Purchase of plant and machinery (1, 00,000) Purchase of motor car (40,000) Cash flow from investing activity (3, 32,000) Cash flow from financing activity Dividend paid (1, 00,000) (1, 00,000) Net decrease in cash and cash equivalents (4, 40,000) Reconciliation Bank overdraft as on 31-12-2008 (5, 95,000) Bank overdraft as on 1-1-2008 (1, 55,000) Increase in overdraft (4, 40,000) Working notes: ADJUSTED P. & L. ACCOUNT To dividend paid 1, 00,000 By balance b/d 1, 65,000 To depreciation on By profit on sale of Car 3,000 Plant and machinery 60,000 By funds from operations To depreciation on (bal. fig.) 62,000 Motor car 25,000 To balance C/D 45,000 2, 30,000 2, 30,000

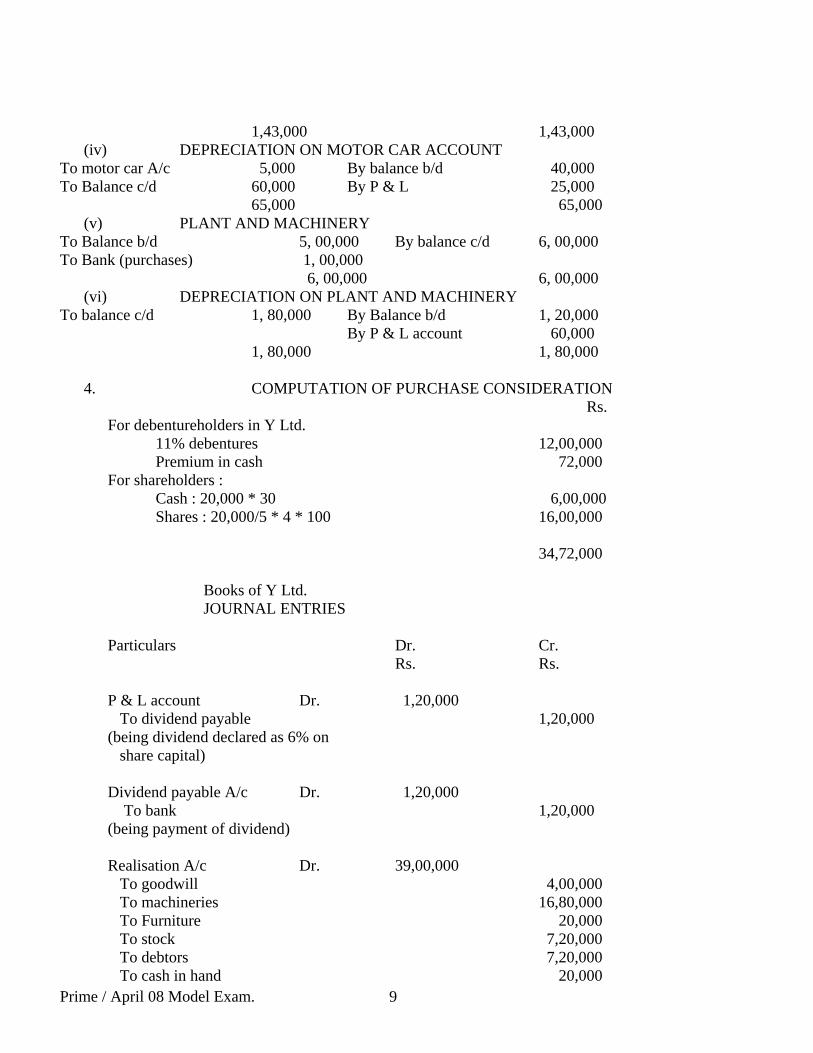

(iii) MOTOR CAR ACCOUNT To Balance b/d 1, 00,000 By bank 8,000 To P & L (profit transferred) 3,000 By depreciation 5,000 To Bank(purchase bal figure) 40,000 By balance c/d 1,30,000

Prime / April 08 Model Exam. 9

1,43,000 1,43,000 (iv) DEPRECIATION ON MOTOR CAR ACCOUNT

To motor car A/c 5,000 By balance b/d 40,000 To Balance c/d 60,000 By P & L 25,000 65,000 65,000

(v) PLANT AND MACHINERY To Balance b/d 5, 00,000 By balance c/d 6, 00,000 To Bank (purchases) 1, 00,000 6, 00,000 6, 00,000

(vi) DEPRECIATION ON PLANT AND MACHINERY To balance c/d 1, 80,000 By Balance b/d 1, 20,000 By P & L account 60,000 1, 80,000 1, 80,000

4. COMPUTATION OF PURCHASE CONSIDERATION Rs.

For debentureholders in Y Ltd. 11% debentures 12,00,000 Premium in cash 72,000 For shareholders : Cash : 20,000 * 30 6,00,000 Shares : 20,000/5 * 4 * 100 16,00,000 34,72,000 Books of Y Ltd. JOURNAL ENTRIES Particulars Dr. Cr. Rs. Rs. P & L account Dr. 1,20,000 To dividend payable 1,20,000 (being dividend declared as 6% on share capital) Dividend payable A/c Dr. 1,20,000 To bank 1,20,000 (being payment of dividend) Realisation A/c Dr. 39,00,000 To goodwill 4,00,000 To machineries 16,80,000 To Furniture 20,000 To stock 7,20,000 To debtors 7,20,000 To cash in hand 20,000

Prime / April 08 Model Exam. 10

To bank 40,000 To Exp. On new project 3,00,000 (being transfer of assets to realization A/c) Creditors Dr. 3,80,000 To realization A/c 3,80,000 (being transfer of creditors to realization A/c) X Ltd. Dr. 34,72,000 To realization A/c 34,72,000 (being purchase consideration due by Y Ltd.) Bank A/c Dr. 6,72,000 11% debentures in X Ltd. Dr. 12,00,000 Shares in X Ltd. Dr. 16,00,000 To Y Ltd. 34,72,000 (being receipt of purchase consideration) 12% debentures A/c Dr. 12,00,000 Realisation A/c Dr 6,72,000

To 12% debenture holders A/c 18,72,000 (being amount due to debentureholders including premium) 12% debentureholders A/c Dr 18,72,000 To 11% debentures in X Ltd. 12,00,000 To Bank 6,72,000 (being payment to debenture holders) Realisation A/c Dr. 4,000 X Ltd. Dr. 20,000 To Bank 24,000 (being liquidation expenses Rs.24,000, X Ltd. To Reimburse Rs. 20,000) Bank Dr. 20,000 To X Ltd. 20,000 (being reimbursement of

Prime / April 08 Model Exam. 11

liquidation expenses) Shareholders A/c Dr. 1,24,000 To realization A/c 1,24,000 (being loss on realization) Share capital A/c Dr. 20,00,000 Capital reserve Dr. 2,00,000 General reserve Dr. 1,00,000 Profit and loss A/c Dr. 20,000 To shareholders A/c 23,20,000 (being share capital, reserves etc. transferred to shareholders account Shareholders A/c Dr. 21,96,000 To bank 5,96,000 To shares in X Ltd. 16,00,000 (being payment to shareholders) working notes : (i) REALISATION ACCOUNT

Particulars Rs. Particulars Rs. To sundry assets 39, 00,000 By creditors 3, 80,000 To 12% debenture holders 72,000 By X Ltd. 34, 72,000 To Bank 4,000 By shareholders A/c (loss) 1, 24,000 39, 76,000 39, 76,000 (ii) SHAREHOLDERS ACCOUNT Particulars Rs. Particulars Rs. To realization A/c 1, 24,000 By share capital 20, 00,000 To shares in X Ltd. 16, 00,000 By capital reserve 2, 00,000 To bank 5, 96,000 By P & L Account 20,000 23, 20,000 23, 20,000 (iii)The actual liquidation expenses of X Ltd. Are Rs. 24,000 while X Ltd. is reimbursing only Rs. 20,000, hence loss of Rs. 4,000 has to be borne by the share holders. The cash payment to them has therefore been reduced by Rs.4, 000.

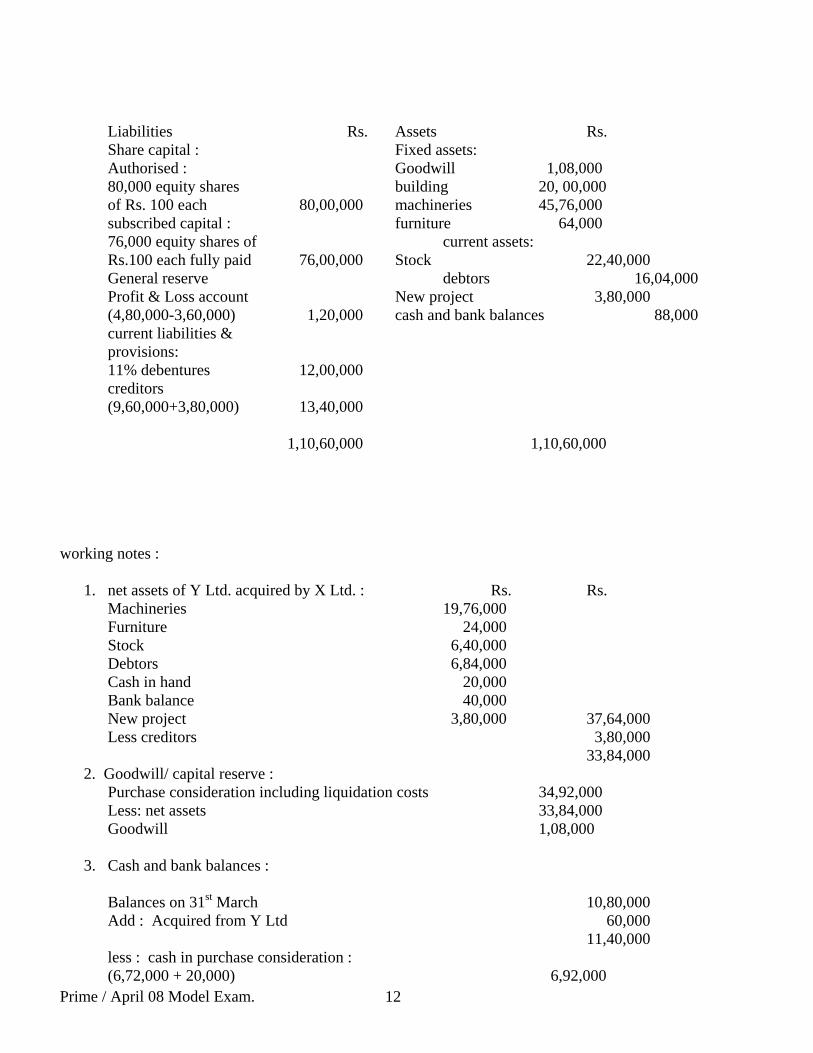

X Ltd. BALANCE SHEET (AFTER ABSORPTION)

Prime / April 08 Model Exam. 12

Liabilities Rs. Assets Rs. Share capital : Fixed assets: Authorised : Goodwill 1,08,000 80,000 equity shares building 20, 00,000 of Rs. 100 each 80,00,000 machineries 45,76,000 subscribed capital : furniture 64,000 76,000 equity shares of current assets: Rs.100 each fully paid 76,00,000 Stock 22,40,000 General reserve debtors 16,04,000 Profit & Loss account New project 3,80,000 (4,80,000-3,60,000) 1,20,000 cash and bank balances 88,000 current liabilities & provisions: 11% debentures 12,00,000 creditors (9,60,000+3,80,000) 13,40,000 1,10,60,000 1,10,60,000 working notes :

1. net assets of Y Ltd. acquired by X Ltd. : Rs. Rs. Machineries 19,76,000 Furniture 24,000 Stock 6,40,000 Debtors 6,84,000 Cash in hand 20,000 Bank balance 40,000 New project 3,80,000 37,64,000 Less creditors 3,80,000 33,84,000

2. Goodwill/ capital reserve : Purchase consideration including liquidation costs 34,92,000 Less: net assets 33,84,000 Goodwill 1,08,000

3. Cash and bank balances :

Balances on 31st March 10,80,000 Add : Acquired from Y Ltd 60,000 11,40,000 less : cash in purchase consideration : (6,72,000 + 20,000) 6,92,000

Prime / April 08 Model Exam. 13

4,48,000 less: dividend paid 3,60,000 88,000 5. General Insurance Company

FIRE REVENUE ACCOUNT (EXTRACTS) For the year ended 31st March, 2008 (In thousand rupees)

Schedule Claim incurred 2 51, 87 SCHEDULE 2 CLAIMS INCURRED NET (in thousand rupees) To claims less re-insurances: 52, 20 Add: Outstanding Claims at the end of the year 7, 52 59, 72 Less: outstanding claims at the beginning Of the year 7, 85 51,87 Working notes:

1. Claims paid during the year : Direct Business 46, 70 Re-insurance 7, 00 53, 70 Add: Surveyor’s fee 35 Legal expenses 45 80 54, 50 Less: Claims received from Re-insurers 2, 30 52, 20

2. Claims outstanding on 31st March, 2008: Direct business 8, 12 Re-insurance 53 8, 65 Less: claims received from re-insurers 1, 13 7, 52

3.Claims Outstanding on 1st April,2007 Direct Business 7,63 Re-insurance 87 8,50

Prime / April 08 Model Exam. 14

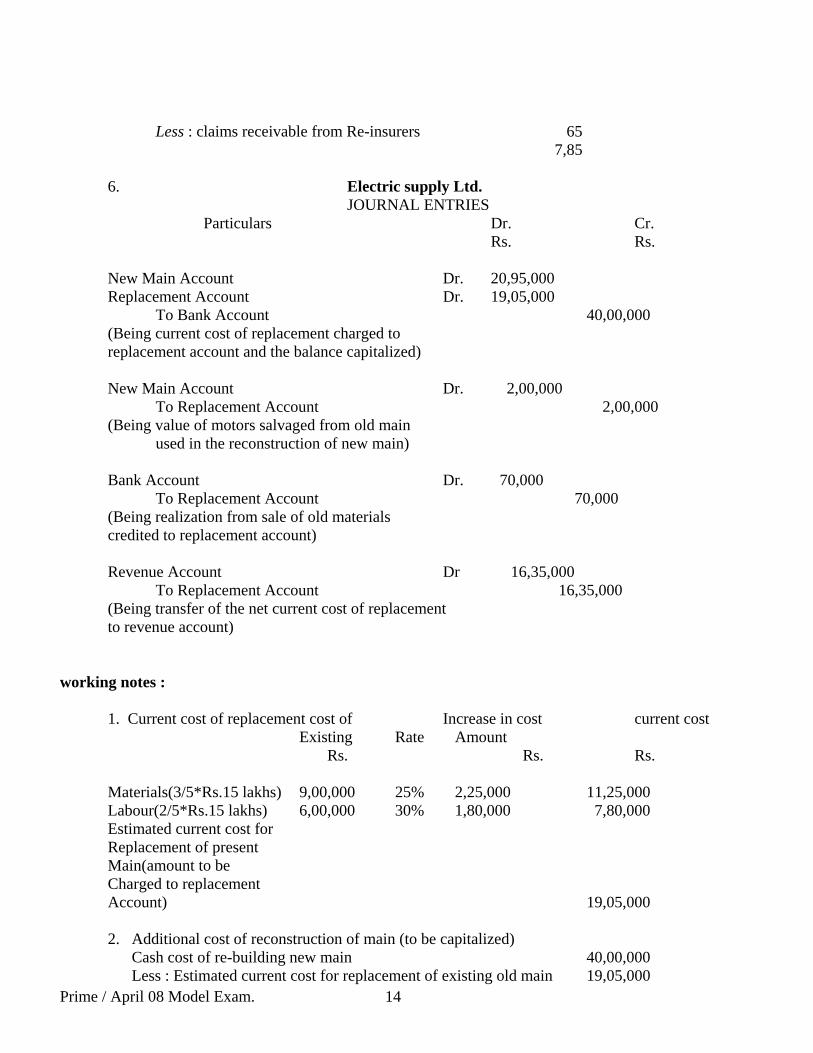

Less : claims receivable from Re-insurers 65 7,85 6. Electric supply Ltd.

JOURNAL ENTRIES Particulars Dr. Cr. Rs. Rs. New Main Account Dr. 20,95,000 Replacement Account Dr. 19,05,000 To Bank Account 40,00,000 (Being current cost of replacement charged to replacement account and the balance capitalized) New Main Account Dr. 2,00,000 To Replacement Account 2,00,000 (Being value of motors salvaged from old main used in the reconstruction of new main) Bank Account Dr. 70,000 To Replacement Account 70,000 (Being realization from sale of old materials credited to replacement account) Revenue Account Dr 16,35,000 To Replacement Account 16,35,000 (Being transfer of the net current cost of replacement to revenue account) working notes : 1. Current cost of replacement cost of Increase in cost current cost Existing Rate Amount Rs. Rs. Rs. Materials(3/5*Rs.15 lakhs) 9,00,000 25% 2,25,000 11,25,000 Labour(2/5*Rs.15 lakhs) 6,00,000 30% 1,80,000 7,80,000 Estimated current cost for Replacement of present Main(amount to be Charged to replacement Account) 19,05,000

2. Additional cost of reconstruction of main (to be capitalized) Cash cost of re-building new main 40,00,000 Less : Estimated current cost for replacement of existing old main 19,05,000

Prime / April 08 Model Exam. 15

Additional cost of new main to be capitalized(exclusive old Motors used) 20,95,000

3. Dr. REPLACEMENT ACCOUNT Cr. Particulars Rs. Particulars Rs. To Bank A/c 19,05,000 By New Main A/c 2,00,000 By Bank A/c 70,000 By Revenue A/c (balancing figure) 16,35,000 19,05,000 19,05,000 7. In the books of S Ltd. Hire purchase Trading account for the year ended om 31-12-2008 To Hire purchase Stock3,20,000 By HP Stock Reserve 1,20,000 To installments due 20,000 By Bank 11,20,000 To goods sold on HP 16,00,000 By goods repossessed 16,000 To HP Stock Reserve 2,70,000 By goods sold on HP 6,00,000 To Profit and loss a/c 4,26,000 By HP stock 7,20,000 By installments due 60,000. 26,36,000 26,36,000 Working notes: 1.Opening stock Reserve 3,20,000*60/160 =1,20,000 2.Loading on goods sold on HP 16,00,000*60/160=6,00,000. 3.Closing stock reserve 7,20,000*60/160=2,70,000 4.Calculation of installments due at the end of the year Opening HP stock +Opening installments due+HP sales during the year (3,20,000+20,000+16,00,000) 19,40,000 Less: Cash received from customers 11,20,000 Installments unpaid for repossessed goods 40,000 Closing balance of HP stock 7,20,000 18,80,000 Closing installments due 60,000 8.(a)As per AS-3 Cash comprises of cash on hand and demand deposits with banks. Cash equivalents are short-term ,highly liquid investments that are reaadily convertible into known amounts of cash and which are subject to insignificant risk of change in value. (b)AS per AS-6 " Depreciation accounting" para 15

Prime / April 08 Model Exam. 16

The method of depreciation is applied consistently to provide comparability of the results of the operation of the enterprise from period to period.A change from one method of providing depreciation to another is made only if the adoption of the new method is required by statue or for compliance with an accounting standard or if it is considered that the change would result in a more appropriate preparation or presentation of the financial statements of an enterprise.When such a change in the method of depreciation is made,depreciation is recalculated in accordance with the new method from the date of the asset coming into use.The deficiency or surplus arising from retrospective recomputation of depreciation in accordance with the new method is adjusted in the year in which the method of depreciation is changed.In case the change in the method results in deficiency in depreciation in respect of past years,the deficiency is charged to the statement of profit and loss .In case the change in the method results in a surplus,the surplus is credited to the statement of profit and loss . Such a change is treated as a change in accounting policy and its effect is quantified and disclosed. (c)As per AS-12 "Accounting for Government Grants" para 8there are two methods of presentaion of grants in the finacial staements: Under one method,the grant is shown as a deduction from the gross value of the asset concerned in arriving at its book value.The grant is thus recognised in the profit and loss staement over the useful life of a depreciable asset by way of a reduced depreciation charge.Where the grant equals the whole ,or virtually the whole,of the cost of the asset,the asset is shown in the balance sheet at a nominal value. Under the othe rmethod, grants relating to depreciable assets are treated as deffered income which is recognised in the profit and loss statement on a systematic and rational basis over the useful life of the asset. Such allocation to income is usually made over the periods and in the proportions in which the depreciation on related assets is charged.Grants related to non depreciable assets are credited to capital reserve under this method,as there is usually no charge to income in respect of such assets. However, if the grant related to a non-depreciable asset requires the fulfillment of certain obligations,the grant is credited to income over the same period over which the cost of meeting such obligations is charged to income.The deferred income is suitably disclosed in the balance sheet pending its apportionment to profit and loss account.For example in a company ,it is shown after "Resrves ans Surplus" but before "Secured loans" with a suitable description eg."Deferred government grants" (d) Refer to AS -10 "Accounting for fixed Assets" para13. Answer found in page 60 of the book "First Lessons on Accounting Standards" by Mr.M.P.Vijay Kumar (e)Refer to AS-1 "Disclosure of Accounting Policies"para 10 Answer found in page 2 of the book "First Lessons on Accounting Standards" by Mr.M.P.Vijay Kumar

Prime / April 08 Model Exam. 17

AU No of Questions: 8 Total Marks: 100 No of Pages Printed: 2 Time Allowed: 3 Hours

Answer Question 1 & 2 and answer any four from the rest

1. As an auditor Comment on the following Situations/Statements

a) A ltd has its registered office at New Delhi. During the current accounting year it has shifted its corporate

head Office to Indore though it gas retained the registered office at new Delhi. The managing Director of the Company wants to shift its books to Indore from New Delhi as he feels there is no legal bar in doing so.

(5 Marks) b) The board of Directors of a company have filed a Complaint with the Institute of Chartered Accountants

of India against their statutory auditors for their failing to attend Annual General meeting of the shareholders in which audited accounts were considered

(5 Marks) c) The Management tells you that WIP is not valued since it is difficult to know the same in view of multiple

processes involved and in any case opening and closing WIP will be more or less the same (4 Marks) d) The auditor of a company wanted to see the minutes book of Directors’ meetings. The Chairman of the

company refused for the same on the ground that matters of Confidential nature were contained therein.

(4 Marks)

2. (a) Managing Director of PQR Ltd. Himself wants Shri G a practicing Chartered Accountant as first auditor of the company. Comment on the proposed action of the Managing Director

(4 Marks)

(b) A ltd has received Rs. 50 lacs as grant from the State Government towards the part cost of a specific machinery. The company credited the above sum of Rs. 50 lacs as income in its profit and loss account for the year. What are your views on the accounting treatment of the above receipt of Rs. 50 lacs

(4 Marks)

(c) XYZ Ltd a pharmaceutical company while valuing its finished stock at the year end wants to include interest bank overdraft as an element of cost for the reason that overdraft has been taken specifically for the purpose of financing current assets like inventory and for meeting day to day working expenses

(4 Marks)

(d) Audit of expenditure is one other major components of Government audit. In this connection, Write in brief what do you understand by:

a. Audit against rules and orders b. Audit of sanctions c. Propriety audit (6 Marks)

3. (a) What are the basic principles laid down in AAS1. Explain in brief (10 Marks)

Prime / April 08 Model Exam. 18

(b) What do you understand by internal check (6 Marks)

4. How will you verify or vouch the following:

a. Sales commission expenditure (4 Marks) b. Stocks lying with third party (4 Marks) c. Purchase of Motor Car (4 Marks) d. Sales return (4 Marks)

5. (a) State the matters to be specified in Auditors report in terms of provisions of section 227(3) of the

companies Act 1956 (8 Marks)

(b) What are the reporting requirements in companies (auditor’s report)order, 2003 in respect of money

raised in public issues (8 Marks)

6. (a) State the matters to be specified in Auditor’s report in terms of provisions of section 227(3) of the Companies Act 1956

(8 Marks)

(b) Mention any points which you would look into as an auditor while auditing a Partnership firm (8 Marks)

7. W rite Short notes on the following

a) Disclaimer of Opinion (4 Marks) b) Cut-off arrangement (4 Marks) c) Sweat Equity shares (4 Marks) d) Disclosure of accounting policies (4 Marks)

8. (a) Explain the term Auditor’s Lien (8 Marks)

(b) Discuss the concept of “True and Fair” (8 Marks)

Prime / April 08 Model Exam. 19

Suggested Answers to PE-II/ AUDITING -APRIL 2008 Answer Question 1 & 2 and answer any four from the rest

Total Marks –100

9. As an auditor Comment on the following Situations/Statements

a. A ltd has its registered office at New Delhi. During the current accounting year it has shifted its corporate head Office to Indore though it gas retained the registered office at new Delhi. The managing Director of the Company wants to shift its books to Indore from New Delhi as he feels there is no legal bar in doing so. 5 marks Place of Books of Account: Section 209 of the Companies Act, 1956 states that every company shall keep at its registered office proper books of account with respect to all sums of money received and spent, all sales and purchases of goods, all assets and liabilities of the company, and the required cost records.

However, all or any of such books of account aforesaid may be kept at any other place in India as the Board of Directors may decide, and if so, the company shall within seven days of the decision file with the Registrar a notice in Form 23 AA in writing giving the full address of that other place.

Therefore, for shifting the books from Delhi to Indore, the Board’s Resolution has to be passed, and notice is to be given to the Registrar of Companies within the specified time. The auditor may, accordingly, inform the Managing Director that his contention is not in accordance with the legal provisions.

b. The board of Directors of a company have filed a Complaint with the Institute of

Chartered Accountants of India against their statutory auditors for their failing to attend Annual General meeting of the shareholders in which audited accounts were considered 5 marks Auditor’s Attendance at Annual General Meeting: Section 231 of the Companies Act, 1956 confers right on the auditor to attend the general meeting. The said section provides that all notices and other communications relating to any general meeting of a company which any member of the company is entitled to have are also to be forwarded to the auditor. Further, it has been provided that the auditor shall be entitled to attend any general meeting and to be heard at any general meeting which he attends on any part of the business which concerns him as an auditor. Therefore, the section does not cast any duty on the auditor to attend the annual general meeting. The law only confers right on the auditor to receive notices and also attend the meeting if he so desires. Therefore, the complaint filed by the Board of Directors is based on mis-conception of the law.

c. The Management tells you that WIP is not valued since it is difficult to know the same in view of multiple processes involved and in any case opening and closing WIP will be more or less the same 4 marks AS-2 prescribes the valuation of inventories, The word inventories includes any item held in the process of production. Production process is going on but final product has not come out before the end of accounting year. This is known as WIP and company will have to find out the stage of completion of products. It has to decide and find out the process at which the said stock is lying at the end of the year and value the same. In certain cases due to nature of the product and the manufacturing process involved, physical verification of WIP may be impracticable. But in such cases, if necessary the advice of an expert can be taken

Prime / April 08 Model Exam. 20

in he matter, The value of such WIP is normally done by taking the basic raw material cost and adding thereto the proportionate factory overhead cost incurred upto the stage of completion. WIP is an item of manufacturing, trading and profit and loss account and also forming part of current assets is relevant and can not be ignored. Omitting WIP will result in under or over statement of profit and current assets. Part II of Schedule VI to the companies Act also prescribes that the figures of opening and closing balances of stock and WIP be disclosed in the profit and loss account. Part I of the same schedule requires that the mode of valuation of stock be shown in the balance sheet. The argument of the management that the opening and closing WIP would be more or less the same is not justified because the cost incurred for raw materials and overhead would be different and would give different value of opening and closing WIP. Taking into consideration all the above aspects, management is wrong and if WIP is not valued or taken into consideration he should qualify his report.

d. The auditor of a company wanted to see the minutes book of Directors’ meetings. The Chairman of the company refused for the same on the ground that matters of Confidential nature were contained therein. 4 marks

Right of Access to Board’s Minutes: Under section 227(1) of the Companies Act, 1956, the auditor of a company has the right of access at all times to books and accounts and vouchers of the company whether kept at the head office of the company or elsewhere. Further, he is also entitled to require from the officers of the company such information and explanations which he considers necessary for the proper performance of his duties. Therefore, he has a statutory right to inspect the directors’ minutes book. The refusal by Chairman to provide access to Directors’ Minutes Book shall constitute limitation of scope as far as the auditor’s duties are concerned. The auditor may examine whether by performing alternative procedures, the auditor can substantiate the assertions or else he shall have to either qualify the report or give a disclaimer of opinion

10. (a) Managing Director of PQR Ltd. Himself wants Shri G a practicing Chartered Accountant as first auditor of the company. Comment on the proposed action of the Managing Director

4 marks Appointment of First Auditor of company: As per section 224(5) of the companies Act 1956 the first auditor of a company can be appointed by the board of directors within one month of the date of registration of the company. If the board fails to appoint the first auditor or auditors the company in general meeting is empowered to make such appointment. This authority is not available to the Managing director of the company himself, Such appointment should be made through board of Directors or by share holders in the general meeting. In view of the above provision, managing director is advised not to appoint first auditors himself and let the board to take decision in this regard. It will be considered as a violation of section 224(5) of the companies Act 1956

(c) A ltd has received Rs. 50 lacs as grant from the State Government towards the part cost of a specific machinery. The company credited the above sum of Rs. 50 lacs as income in its profit and loss account for the year. What are your views on the accounting treatment of the above receipt of Rs. 50 lacs 4 marks Accounting for Grants(AS_12): Grants or subsidy related to specific fixed assets are government grants whose primary condition is that an organization qualifying for such grant should either purchase construct or otherwise acquire such assets. Besides Govt., may specity the type or location of the assets or the periods during which they are to be acquired or held. For accounting treatment the following basis should be taken into consideration: (i) Grant to be shown as a deduction from gross value of assets concerned in arriving at its book value.

Depreciation is charged on reduced value of fixed assets. (ii) In case of grants related to non-depreciable assets, the same shall be credited to capital reserve account Taking into consideration the above view, accounting treatment given of the grants received by the organization is not correct. As an auditor it will be advised to correct the wrong treatment given otherwise it is the duty of the auditor to qualify his report.

Prime / April 08 Model Exam. 21

© XYZ Ltd a pharmaceutical company while valuing its finished stock at the year end wants

to include interest bank overdraft as an element of cost for the reason that overdraft has been taken specifically for the purpose of financing current assets like inventory and for meeting day to day working expenses 4marks Cost of Inventories: As per Accounting Standard 2 “Valuation of Inventories”, cost of inventories comprises all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition. However, it makes clear that interest and other borrowing costs are usually not included in the cost of inventories because generally such costs are not related in bringing the inventories to their present location and condition. Therefore, the proposal of CC Ltd. to include interest on bank overdraft as an element of cost is not acceptable because it does not form part of cost of production

(d) Audit of expenditure is one othe major components of Government audit. In this connection, write in brief what do you understand by: 2X3=6 marks a. Audit

against rules and orders The auditor has to see that the expenditure incurred conforms to the relevant provisions of the statutory enactment and is in accordance with the financial rules and regulations framed by the competent authority.

b. Audit of sanctions: The auditor has to ensure that each item of expenditure is covered by an sanction either, general

or special accorded by the competent authority, authorizing such expenditure. c. Propriety audit : It is required to be seen that the expenditure is incurred with due regard to broad and general

principles of financial propriety. The auditors aims to bring out cases of improper, avoidable or infructuous expenditure even though the expenditure has been incurred in conformity with the existing rules and regulations, Audit aims to secure a reasonably high standard of public financial morality by looking into the wisdom, faithfulness and economy of transactions

11. (a) What are the basic principles laid down in AAS1. Explain in brief 10 Basic Principles governing an Audit: Auditing and assurance Standard-1 on Basic principles governing an Audit issued by the ICAI describes the basic principles which govern the auditor’s professional responsibilities and which should be complied with whenever an audit of financial information of any entity is carried out. The basic principles as stated are as under : i) Integrity, objectivity and independence: The auditor should be honest , straightforward and sincere in his approach to his professional work. He must be fair and must not allow prejudice or bias to override his objectivity. He should maintain an impartial attitude and both be and appear to be free of any interest which might be regarded whatever its actual effect, as being incompatible with integrity and objectivity. ii) Confidentiality: The auditor should respect the confidentiality of information acquired in the course of his work and should not disclose any such information to a third part without specific authority or unless there is a legal or professional duty to disclose. iii) Skills and competence: The audit should be performed and the report should be prepared with due professional care by persons who have adequate training experience and competence in auditing. iv) Work performed by others: When the auditor delegates work to assistants or uses work performed by other auditors and experts, he will be entitled to rely on work performed by others provided he exercise adequate skill and care and is not aware of any reasons to believe that he should not have so relied. The auditor should carefully direct supervise and review work delegated to assistants and obtain reasonable assurance v)Documentation: The auditor should document matters which are important in providing evidence that the audit was carried in accordance with the basic principles. vi)Planning: Planning enables the auditor to conduct an effective audit in an efficient and timely manner. Primarily planning should be based on the knowledge of the client’s business. Plans should be further developed and revised as necessary during the course of the audit. vii) Audit evidence: The auditor should obtain sufficient appropriate audit evidence through the performance of compliance and substantive procedures to enable him to draw reasonable conclusions therefrom on which to base his opinion on the financial information.

Prime / April 08 Model Exam. 22

viii) Accounting system and internal control: The auditor should reasonably assure himself that the accounting system is adequate and that all the accounting information which should be recorded has in fact been recorded and internal controls normally contribute to such assurance. ix) Audit conclusion and reporting: The auditor should review and assess the conclusions drawn from the audit evidence obtained and from his knowledge of business of the entity as the basis for the expression of this opinion on the financial information, This review and assessment involves forming an overall conclusion as to whether

i. the financial information has been prepared using acceptable accounting policies which have been consistently applied,

ii. the financial information complies with relevant regulations and statutory requirements iii. there is an adequate disclosure of all material matter relevance to the proper presentation of

the financial information, subject to staturoy requirements where applicable.

(b) What do you understand by internal check 6 marks Internal Check has been defined by the Institute of Chartered Accountants of England and Wales as the checks on day-to-day transactions which operate continuously as part of routine system whereby the work of one person is proved independently or is complementary to the work of another, the object being the prevention or early detection of errors or fraud. Internal check is a part of the overall internal control system and operates as a built in device as far as the staff organization and job allocation aspects of the control system are concerned. A system of internal check in accounting implies organization of system of book keeping and arrangement of staff duties in such a manner that no one person can completely carry through a transaction and record every aspect thereof. The essential elements of a goods system of internal check are :

1) Existence of checks on the day to day transaction 2) Which operate continuously as apart of the routine system 3) Whereby the work of each person is either proved independently or is made complementary to the work of another

Thus the objective is to bring about a speedy detection of frauds , wastes and errors

12. How will you verify or vouch the following: 4 marks each

a. Sales commission expenditure a) Examine the agreement or correspondence and note the rate of commission and other terns and other conditions b) Check the amount of orders received through agents to ensure that commission is paid to them for services

rendered or orders obtained by them c) Ascertain whether sales commission is calculated properly and paid only to authorized agents /dealers/distributors d) Verify computation of commission based on the agreement e) Where commission eligibility is subject of realization of debtors, check the calculations of commission accordingly f) Ensure the payment is properly authorized g) Verify the entry relating to payment in the Bank book and trace the payment in the bank statements h) Verify whether TDS has been deducted at source at the appropriate rates and remitted with the due dates

stipulated under the Income Tax Act i) Verify the acknowledgements or receipt received from agents j) Compute percentage of commission to Total Sales. Compare this with previous years’ figures and obtain

explanations for significant deviations. b. Stocks lying with third party Stocks lying with third parties include

(i) Stocks in pledged godowns, (ii) Stocks in the hands of distributors, dealers or retailers (iii) Stocks with customers to whom goods have been sent on sale or return basis (iv) Stock with transporters

1. Confirmatory certificates shall be received from the above parties to verify the value of stocks 2. Examine that there are separate stock sheets for each of the above item

Prime / April 08 Model Exam. 23

3. In case of goods on consignment and stock on sale or return basis- verify the relevant agreements, proforma invoices and the quantitative details thereof.

4. Verify the reconciliation statements

c. Purchase of Motor Car a) Ascertain the amount at which the asset is capitalized, including all accessories, registration fees, life-time tax, and

other incidental expenses of purchasing the asset b) Verify whether the invoice is made out in the name of the client c) Examine whether the entire consideration has been properly settled d) Where the purchase is of second hand car, confirm whether the receipt contains all relevant details like registration

number, chassis number etc e) Verify the title and in case of bank finance purchase whether hypothecation has been noted properly f) Ascertain whether the asset has been properly insured for the requisite value g) Ascertain whether requisite amount has been paid for the vehicle h) Verify whether the asset acquisition has been duly authorized by competent authority i) Confirm that all costs relating to acquisition have been capitalized j) Confirm that minor repair expenditure have been duly charged to revenue k) Check the computation of depreciation , rate and whether the asset has been properly disclosed

d.Sales return (i) Examine the accounting basis for such transactions with reference to corresponding

debit note to debit note. The relevant correspondence may also be examined (ii) Verify by reference to relevant corresponding record in good inward book or the stores

records. Further the figures in these documentary evidences should be compared with the original invoices for rates and other charges and calculation should also be checked.

(iii) Examine in depth to eliminate the possibility of fictitious sales returns for covering bogus sales recorded earlier when such returns outwards are in substantial figure either at the start or end of the accounting year.

(iv) Cross-check with reference to original invoices any rebates in price or allowances if any given by buyers on strength of their debit notes.

13. (a) State the matters to be specified in Auditors report in terms of provisions of section 227(3) of the companies Act 1956 8 Matters to be reported by auditor under section 227 (3): Under section 227(3) of the Companies Act, 1956, the report of the auditor shall state - (i) Whether he has obtained all the information and explanations which to the best of his knowledge and belief were necessary for the purposes of his audit; (ii) Whether, in his opinion, proper books of accounts as required by law have been kept by the company so far as appears from his examination of those books; whether proper returns adequate for the purposes of his audit have been received from the branches not audited by him; (iii) Whether the report on the accounts of the branches audited by branch auditors under section 228 has been forwarded to him and how he had dealt with the same in preparing the auditor's report; (iv) Whether the company's balance sheet and profit and loss account are in agreement with the books of accounts and returns; (v) Whether in his opinion the profit and loss account and balance sheet comply with the accounting standards referred to in section 211(3C); (vi) In thick type or in italics the observations or comments of auditors which have any adverse effect on the functioning of the company; (vii) Whether any director is disqualified from being appointed as director under section 274(1)(g);

Prime / April 08 Model Exam. 24

(viii) Whether the cess payable under section 441 A had been paid and if not details of amount of cess not so paid.

(b) What are the reporting requirements in companies (auditor’s report)order, 2003 in respect of money raised in public issues 8 marks Money raised by Public Issues: Companies (Auditor’s Report) order, 2003 requires that in case the company has made a public issue of any of its securities like shares, preference shares, debentures and other securities, the auditor is required to report upon the disclosure of end-use of the money by the management in the financial statements. The auditor is also required to state whether he has verified the disclosure made by the management in this regard. Schedule VI to the Act requires that only unutilized amount of any public issue made by the company should be disclosed in the financial statements of a company. In the absence of any legal requirement of such disclosure, it appears that the clause envisages that the companies should disclose the end use of money raised by the public issue in the financial statements by way of notes and the auditor should verify the same. Normally, the companies do mention the end-use of the money proposed to be raised through the public issues in the prospectus. An examination of the prospectus would provide the auditor an understanding of the proposed end-use of money raised from public. The auditor should verify that the amount of end-use of money disclosed in the financial statements by the management is not significantly different from the proposed and actual end use. The auditor should obtain a representation from the management as to the completeness of the disclosure with regard to the end-use of money raised by public issues. If the auditor is of the opinion that adequate disclosure with regard to end use of money raised by public issue has not been made in the financial statements, the auditor should state the fact in his audit report. If, for any reason, the auditor is not able to verify the end-use of money raised from public issues, he should state that he is not able to comment upon the disclosure of end-use of money by the company since he could not verify the same. He should also mention the reasons which resulted in the auditor’s inability to verify the disclosure.

6.(a) State the matters to be specified in Auditor’s report in terms of provisions of section 227(3) of the Companies Act 1956 8marks Matters to be reported by auditor under section 227 (3): Under section 227(3) of the Companies Act, 1956, the report of the auditor shall state - (i) Whether he has obtained all the information and explanations which to the best of his knowledge and belief were necessary for the purposes of his audit; (ii) Whether, in his opinion, proper books of accounts as required by law have been kept by the company so far as appears from his examination of those books; whether proper returns adequate for the purposes of his audit have been received from the branches not audited by him; (iii) Whether the report on the accounts of the branches audited by branch auditors under section 228 has been forwarded to him and how he had dealt with the same in preparing the auditor's report; (iv) Whether the company's balance sheet and profit and loss account are in agreement with the books of accounts and returns; (v) Whether in his opinion the profit and loss account and balance sheet comply with the accounting standards referred to in section 211(3C); (vi) In thick type or in italics the observations or comments of auditors which have any adverse effect on the functioning of the company; (vii) Whether any director is disqualified from being appointed as director under section 274(1)(g); (viii) Whether the cess payable under section 441 A had been paid and if not details of amount of cess not so paid.

Prime / April 08 Model Exam. 25

(b) Mention any points which you would look into as an auditor while auditing a Partnership firm 8 marks

Refer Text

7.W rite Short notes on the following 4 marks each

e) Disclaimer of Opinion Refer Text 4 b. Cut-off arrangement

Accounting is a continuous process because the business never comes to halt. It is therefore Necessary that transactions of one period would be separated from those in the ensuing period so that the results of the working of each period can be correctly ascertained. The arrangement that is made for this purpose is technically known as “cut-off arrangement”. It essentially forms part of the internal control system of the organization, Accounts other than sales, purchase and stock are not usually affected by the continuity of the business and therefore this arrangement is generally applied only to sales, purchase and stock. The auditor satisfies by examination and test-checks that the cut-off procedure are adequately followed and ensure that

(i) Goods purchased, property in which passed on to the client have in fact been included in the inventories and that the liability has been provided for n case credit purchase

(ii) Goods sold have been excluded from the inventories and credit has been taken for the sales . If the value of sales is to be received, the concerned party has been debited.

c. Sweat Equity shares

As per the explanation to section 79A, the expression sweat equity shares means equity shares issued by the company to employees or directors at a discount or for consideration other than cash for providing know-how ort making available right in the nature of intellectual property rights or value additions, by whatever name called. The auditor may see that the sweat equity shares issued by the company are of a class of shares already issued and following conditions fulfilled:

d. The issue of sweat equity shares is authorized by a special resolution passed by the company in the general meeting

e. The resolution specifies the number of shares, current market price, considerations and the class or classes of directors or employees to whom such equity share to be issued

f. Not less than one yea has at the date of the issue elapsed since the date on which the company was entitled to commence the business;

g. The sweat equity shares of a company whose equity shares are listed on a recognized stock exchange are issued in accordance with the regulations made the SEBI in this behalf.

Provided that in case of a company whose equity shares are not listed on any recognized stock exchange , the sweat equity shares are issued in accordance with the guidelines as may be prescribed

d .Disclosure of accounting policies The view presented in the financial statements of an enterprise of its state of affairs and of the profit or loss can be significantly affected by the accounting policies followed in the preparation and presentation of the financial statements.

The accounting policies followed vary from enterprise to enterprise. Disclosure of accounting policies followed is necessary if the view presented is to be properly appreciated. The disclosure of some of the accounting policies followed in the preparation and presentation of the financial statements is required by some cases The purpose of AS-1 is to promote better understanding of financial statements establishing through an accounting standard and the disclosure of significant accounting policies and the manner in which such accounting policies are disclosed in the financial statements. Such disclosure would also facilitate a more meaningful comparison between financial statements of different enterprises Any change in accounting policy which has a material effect should be disclosed , the amount of such change and financial impact on the current financial period as also in later period s should be appropriately disclosed.

Prime / April 08 Model Exam. 26

8.a. Auditor’s Lien: Under the general principles of law, if any person has lawful possession of the property of

another person, on which he has worked, he may retain such property for non payment of any amount outstanding in respect of work done on the property. Accordingly, the auditor may exercise lien on the client’s documents in his possession for non payment of fees for work done for the client. As per AAS 3, “Documentation”, the working papers are the property of the auditor. The auditor at his discretion may make extracts from his working papers available to his clients. The auditor should also adopt reasonable procedures for custody and confidentiality of his working papers and should retain them for a period of time sufficient to meet the needs of his practice and satisfy any pertinent and legal or professional requirement of record retention. However, regarding books of account of a company, it may be noted that as per section 209 of the Companies Act, 1956, these must be kept at the registered office of the company. However, all or any of the books of account may be kept at any other place in India pursuant to a Board’s Resolution, and notice must be filed with the Registrar. Thus, as per such a resolution, if the Board of a company hands over the books of account to the auditor, the auditor may exercise his lien for non payment of fees. However, reasonable facilities must be provided for inspection of the books of account by the directors, members and other authorised persons. The auditor needs to observe provisions of the Companies Act, 1956. Further, in respect of auditor exercising the lien, the views of the Institute of Chartered Accountants of England and Wales are worth noting:

(i) Documents must belong to the client who owes the money, and these documents must come to the possession of the auditor on the client’s authority.

(ii) The auditor can retain such documents, only if he has done work on such documents, on which fees have not been paid.

(b) Concept of “True and Fair”: The concept of “true and fair” is a fundamental concept in auditing. The phrase “true and fair” in the auditor’s report signifies that the auditor is required to express his opinion as to whether the state of affairs and the results of the entity as ascertained by him in the course of his audit are truly and fairly represented in the accounts under audit. This requires that the auditor should examine the accounts with a view to verifying that all assets and liabilities, incomes and expenses are stated at the amounts which are in accordance with accounting principles and policies, and no material item has been

Prime / April 08 Model Exam. 27

omitted. What constitutes “true and fair” has not been defined in the legislation. However, section 211(1) and (2) of the Companies Act, 1956 states that every balance sheet of a company shall give a true and fair view of the state of affairs of the company at the end of the financial year and every profit and loss account of a company shall give a true and fair view of the profit or loss of the company for the financial year.

However, section 211(5) of the Companies Act, 1956 states that the balance sheet and profit and loss account of a company shall not be treated as not disclosing a true and fair view of the state of affairs of the company if they do not disclose any matters which are not required to be disclosed by virtue of the provisions of Schedule VI to the Companies Act, 1956, or by virtue of any notification or any order. Therefore the auditor must see that the accounts are drawn up as per requirements of the provisions of Schedule VI, and whether they contain all matters required to be disclosed therein. In case of companies governed by special Acts, say, banking, electricity, etc. the auditor should see, whether the relevant disclosure requirements are complied with. Thus, what constitutes a true and fair view is a matter of the auditor’s judgement in the particular circumstances of the case. In specific terms to ensure truth and fairness, an auditor has to see:

(i) that the assets are neither undervalued or overvalued;

(ii) no material asset is omitted;

(iii) the charge on assets, if any, is disclosed;

(iv) material liabilities should not be omitted, and liabilities are neither undervalued or overvalued;

(v) accounting policies have been followed consistently;

(vi) all unusual, exceptional, non recurring items have been disclosed separately;

(vii) accounts have been drawn as per requirement of Schedule VI to the Companies Act; and

♦ (viii) the accounts have been drawn in compliance to the relevant accounting standards. In case of deviation from accounting standards, disclosure should be made of the reasons for such deviation and financial effects, if any arising due to such deviation.

Prime / April 08 Model Exam. 28

BS No of Questions: 10 Total Marks: 100 No of Pages Printed: 2 Time Allowed: 3 Hours

Question no 1 and 7 are compulsory.

Answer any three questions out of Q. Nos.2, 3,4,5 and 6. Answer any two questions out of Q. Nos. 8, 9 and 10.

1. (a) For the purpose of making uniform for the employees, Ramakrishna brought dark blue colored cloth from CT Cotton

Mills , but Ramakrishna did not disclose the sellers the purpose of the purchase. When uniform were prepared and used by the employees, the cloth was found unfit. However, there was evidence that the cloth was fit for caps and carriage lining. Advise Ramakrishna whether he is entitled to have any remedy.

(b) What are the differences between “negotiability and assign ability”? (c) What are the implied warranties in a contract of sale under the sale of goods Act,1930 (d) Which acts do not fall within the implied authority of a partner under the Indian Partnership Act, 1932? (e) Explain the meaning of “allocable surplus” and available surplus stated in the payment of bonus Act. (f) State the purpose for which the net profit of a multi-state Co-operative society may be utilized under the provisions

of the Multi state co-operative societies Act, 1984. (g) What are the power of an ‘inspector’ under the Employees Provident Funds and Miscellaneous Provisions Act,

1952? (h) Explain the provisions regarding regulation of contribution made by the societies registered under the co-operative

societies Act, 1912. (8x3=24)

2 (a) A passenger deposited a bag in the cloakroom at a Railway Station. Acknowledgement Receipt given to him carried, on the face of it the words “see back”. One condition limited the liability of the Railways for any package to Rs.100. The bag was lost and passenger claimed Rs.200 being its value, pleading he has not read the condition. Whether the Railway has to pay the amount claimed by the passenger.

(b) Explain the provision of law relating to unpaid seller’s right of lien and distinguish it from the right of stoppage the

goods in transit. (6+6=12)

3 (a)State the grounds upon which a contract may be discharged under the Provisions of Indian Contract Act, 1872.

(b) Whether a minor may be admitted in the business of partnership firm? Explain the rights of a minor in the partnership firm.

(6+6=12)

4 (a) What is a promissory Note’ and what are its elements? A writes “I promise to pay”B” a sum of Rs.500, seven days after my marriage with “C” Is this promissory note?

(b) What is the minimum and maximum amount of bonus payable under the payment of Bonus Act, 1965?

(6+6=12) 5 (a) Point out the classes of those establishments upon which the provisions of Employees provident fund and

miscellaneous provision Act, 1956 does not apply. (b) Describe the procedure of registration of a multistage co-operative Society paid down in the multi state co-

operative Societies Act, 1984 which are the documents required to be filed at the time of registration of such a society.

(6+6=12)

Prime / April 08 Model Exam. 29

6 (a)Discuss the restrictions on the powers of a society registered under the co-operative Societies Act, 1912 to make loan and to contribute charitable purpose

(b) Discuss the circumstances where notice of dishonor is exercised under the NI Act, 1881. (6+6=12)

7. Answer any Four of the following; (a) State the conditions of restrictions with which a private company is incorporated under the companies Act, 1956. (b) Briefly explain the doctrine of ‘ulttra vires’ under the Companies Act, 1956. What are the consequences of ultra

virus Acts of the company? (c) Can a company issue shares at discount? What is the Law, in this relation, laid down in the Companies Act, 1956? (d) ‘Diminution of capital does not constitute reduction of capital within the provisions of the companiesAct, 1956-

comment. (e) The Articles of Association of a liquated company provided that ‘x’ shall be the Law officer of the company and he

shall not be removed except on the ground of proved misconduct. The company removed his even though he was not guilty of misconduct. Decide, whether companies action is valid.

(4x5=20)

8 (a) M/S XYZ Ltd were incorporated on 1-4-2003. No general meeting of the company has been held so far. Explain the

provisions of the companies Act, 1956 regarding the time limit for holding the first Annual General meeting of the company and the power of the registrar to grant extension of time for the first Annual General meeting.

(b) Whether a company can buy back its own shares? Explain in brief the provisions of companies Act, 1956 relating to the source of funds and conditions for buy-back its own shares by the company.

(5+5=10)

9. (a) What is the concept of ‘charge’ under the provisions of the Companies Act, 1956? Point out the circumstances

where under a floating charge becomes a fixed charge. (b) Explain the provisions of the companies Act, 1956 relating to registration of a non-profit organization as a

company, what procedure is required to be adopted for the said purpose? (5+5=10)

0. (a) Advice the board of directors of a public limited company in relation to following matters, under the provisions of the companies Act,1956 (I) Sources out of which the company can declare dividend. II) Transfer of profits to reserves before declaring dividend, for a particular financial year,

(b) Explain the provisions of the companies Act, 1956 relating to establishment of an ‘investors education protection fund’.

(5+5=10)

Prime / April 08 Model Exam. 30

PRIME ACADEMY 26TH SESSION MODEL EXAM

PE II - BUSINESS AND CORPORATE LAWS

1(a) There is no description of the clothes prescribed by the buyer in this contract of sale and there is no breach of implied warranties by the seller in relation to the products which will not make the seller liable for the clothes sold. Hence Ramakrishna shall not be entitled to any remedy in the given situation.

(b)

Basis Negotiation Assignment Notice of Transfer

Not necessary Notice must be served by assignee on his debtor

Consideration for Transfer

Presumed To be proved

Mode Bearer Instruments - Delivery Order Instrument - Endorsement and Delivery

Document to be reduced into writing and signed by transferor

Rights Transferee acquires all rights of a holder in due course

Assignee has only the right, title and interest of the assignor

Title The title of the transferee (i.e. the holder in due course) is better than that of the transferor

The title of the assignee is subject to the defects in the title of the assignor

(c) (i) Warranty of Quiet possession : Sec. 14

Unless contrary intensions appear, it is implied that the buyer shall have and enjoy quiet possession of the goods. Thus, if the right of possession is disturbed by the seller or any other person, the buyer is entitled to sue the seller for damages. Example : X purchased a second hand television from Y who spent Rs.2,500/- on repairs. The television was later seized by the police as it was a stolen one. X filed a suit against Y for recovery of damages for breach of warranty of quiet possession including cost of repairs. X was entitled to recover the same.

(ii) Warranty of freedom from encumbrances : Sec. 14

Means that the goods are free from any charge or encumbrance in favour of a third person, not declared to or known to the buyer

Prime / April 08 Model Exam. 31

Example : X borrowed Rs.5000/- from Y and hypothecated his Television with Y as security. Later X sold this television to Z, who bought in good faith. Hence Z can claim damages from X because his possession is disturbed by Y having a charge.

Prime / April 08 Model Exam. 32

(iii) Warranty of disclosing the dangerous nature of the goods

In case the goods sold are of dangerous nature, the seller must warn the ignorant buyer of the probable danger, failing which the buyer can claim the damages for injuries caused to him. Example : X purchased a tin of pesticides which required to be opened with special care. X’s wife while opening the tin was injured as the powder flew into her eyes. X is entitled to claim from seller for the loss suffered.

(iv) Warranty as to quality or fitness by usage of trade : Sec.160

An implied warranty as to quality or fitness for a particular purpose may be annexed by the usage of trade.

(d) Unless negated by an express agreement, every partner has an implied authority to carry on in the usual way, business of the kind carried on by the firm and thereby bind the firm. A partner’s authority may be express or implied. It is “express” when it is decided between the partners by mutual agreement. The agreement may, however be verbal or written. It is implied, when the law by implication gives certain powers to a partner, i.e the law presumes that every partner has the power to do certain acts unless negated by an express agreement. The implied authority of a partner, thus extends only to such acts : Which are common in the type of business carried on by the firm and Which are done by him in the usual way of carrying on the firm’s business. In connection with a partner’s implied authority, judicial decisions have made a distinction between a trading and a non trading partnership. In the case of a trading firm, a partner can borrow money on behalf of the firm. But in the case of non trading firm, unless the power to borrow is given expressly by the partnership deed, a partner cannot borrow money or pledge property of the firm, on behalf of the firm, so as to bind the firm. In case of trading firm, however the implied authority of a partner extends also to drawing and accepting bills of exchange and making and endorsing promissory notes.

(e) Allocable Surplus : In relation to an employer, being a Company (other than a banking company) which has not made the arrangements prescribed under the Income Tax Act for the declaration and payment within India of the dividend payable out of it profits in accordance with the provisions of Section 194 of the Act, sixty seven percent of the available surplus in an accounting year. In any other case sixty percent of such available surplus. Available Surplus : Surplus computed in the manner prescribed in Section 5 of the Act which provides that available surplus in any accounting year is the Gross Profit for that year after deducting therefrom sums referred in Sec. 6.

Prime / April 08 Model Exam. 33

(f) A society is prohibited from dividing its capital fund by way of bonus, dividend or otherwise. Only profits can be divided and not capital. The dividend shall be paid from the net profit after making the contribution towards reserve fund as below : The Net Profits are to be appropriated in the following manner :

At least 25 % of the net profits of a Society should be transferred to the Reserve Fund. 1 % of the net profits should be credited to the National Cooperative Union of India Ltd. as

contribution to the education fund maintained by the union. Transfer of an amount not less than 10 % to a reserve fund for meeting unforeseen losses.

The net profits remaining after above appropriations may be used for any or al of the following:

a) payment of dividend to the members on their paid up share capital at a rate not exceeding the prescribed limit.

b) constitution of, or contribution to, such special funds including education funds as may be specified

in the bye laws ; c) purpose connected with the development of cooperative movement or charitable purpose as defined

in Section 2 of the Charitable Endowments Act, 1890. d) payment of ex-gratia amount to employees of the Multi-State Cooperative Society to the extent and

in the manner specified in the bye laws.

(g) The appropriate Government may, by notification in the official gazette, appoint Inspectors for the purpose of this Act and Scheme.

Powers of inspectors and as follows : a) Collect information

b) Require an employer or any contractor from whom any amount is recoverable to furnish such

information as he may consider necessary.

c) At any reasonable time, ENTER and SEARCH any establishment or any premises connected therewith.

d) Require any one found in charge thereof to produce before him for examination, any accounts, books, registers and other documents relating to the establishment, whom the inspector has reasonable cause to believe to be or to have been an employee in the establishment.

Prime / April 08 Model Exam. 34

e) Make copies of or take extracts from any book, register or other documents maintained in relation to the establishment.

f) Where he has reason to believe that any offence under this Act has been committed by an employer,

SEIZE with such assistance as he may think fit

(h) A registered society may contribute to any charitable purpose as defined in the Charitable Endowments Act, if the following conditions are fulfilled.

1/4th of the net profits in any year has been carried to a reserve fund. The contribution shall not exceed 10 % of the remaining net profits ; and The sanction of the Registrar shall be obtained.

2 (a) The claim of the Railways shall be restricted to Rs 100 as specified in conditions prescribed in the back of the acknowledgement.

2 (b) Against the goods

1. Lien on the goods: Sec. 47, 48 & 49

The word "lien" means to retain possession. An unpaid seller, who is in possession of the goods, is entitled to retain them until payment or tender of the price in the following cases: (i) Where the goods have been sold without any stipulation as to credit. (ii) Where the goods have been sold on credit, but the term of credit has expired. (iii) Where the buyer becomes insolvent -

Lien can be exercised only for non-payment of the price, and not for any other charges due against the buyer. Where part delivery has been made, he may still exercise his right of lien on the remainder of goods unless he has waived the lien. It is a personal right which can be exercised only by him and not by his assignees or creditors. The unpaid seller can exercise his lien notwithstanding that he is in possession of the goods as agent or bailee for the buyer. Eg : X buys a car from Y and agrees to pay for it later. X leaves the car with Y to be sent to him later. Y shall have lien on the car if in the meantime he learns of X's insolvency.