African Stock Market Integration - African … process has attracted the attention of fund managers...

31

Transcript of African Stock Market Integration - African … process has attracted the attention of fund managers...

African Stock Market Integration:Implications for Portfolio

Diversification and InternationalRisk Sharing

Paul ALAGIDEDE1

Abstract

This paper addresses integration of African stock markets into the globalfinancial system and the implications for investment analysis and risk sharing.First, we show that African stock markets are not well integrated with eachother, raising important questions about the quest for a pan-Africanexchange. Second, we find weak stochastic trends between African marketsand the rest of the world, indicating that Africa’s markets tend to respond tolocal rather than global information. Although the weak trends uncoveredpresent an opportunity to diversify portfolio into African markets, we arguethat risk perception and institutional underdevelopment remain obstacles tothe development of Africa’s emerging equity markets. Thus lessening politicaland economic policy risk, and / or reducing existing barriers to movement offinancial resources are sine qua non to integration and deepening of Africa’scapital markets.

Keywords: Integration, Diversification, Convergence, Interdependenceand African Stock Markets

1. Introduction

The rapid integration of financial markets over the past four decades hasmade capital flows across national boundaries easier and faster. This pheno-menon, produced by the relaxation of controls on capital movements andforeign exchange transactions, deregulation and elimination of restrictions onbanking and securities dealings, and communications and technologicalchanges that have occurred in the world economy, have increased cross-border investment activity and accelerated the flow of resources among natio-nal economies. The increasing importance of developing countries in the

1. Stirling Management School, Division of Economics, University of Stirling, Stirling, FK9 4LA, [email protected]

globalisation process has attracted the attention of fund managers as anopportunity for portfolio diversification, particularly in the light of the intro-duction of financial products such as American Depository Receipts (ADRs)and Country Funds.

Equity market integration has become an important concept in our daysas it plays a key role in economic development. Theory suggests that integra-ted stock markets tend to be more efficient than segmented markets. Assetpricing models also predict that integrated markets respond more to globalevents than to local factors, although the reverse is also true (see Errunza andLosq, 1985). Evidence by Obstfeld (1995), Bracker et al (1999) and Stulz(1999), among others, shows that, by dismantling investment restrictions,integration allows for international risk sharing, which can affect long-termeconomic growth by altering resource allocation and savings rates. Bekaert(1995), Bekaert and Harvey (1995, 2000) and Kim and Singal (2000) arguethat a higher degree of market segmentation will increase the level of risk, andthis will inevitably affect the local cost of capital, with ramifications forcompany financing and, hence, economic growth.

Although a number of papers have investigated the dynamic interdepen-dence of equity markets worldwide, the emphasis has often been on develo-ped economies and the emerging markets of Asia and Latin America. Suchneglect is far from surprising: Africa’s markets are perceived as being excessi-vely risky, for instance they are highly illiquid and the institutional environ-ments in which they operate are underdeveloped. Political strife and econo-mic instability has plagued many African countries (Kenyan post electioncrises in 2007/2008, Nigeria’s marred transition in 2008 and currently Zim-babwe’s economic meltdown) continue to pose a threat to foreign invest-ments. With the exception of South Africa, no African country has emergedas an economic power. This might partly explain the lack of academicresearch on the capital markets of Africa. Yet, there is no justification for thisstate of affair, particularly, given that Africa has recently witnessed significanteconomic and financial development, with good growth prospect.

This paper contributes to the literature on global financial integration byinvestigating the dynamic interdependence of the major equity markets inAfrica (South Africa, Egypt, Nigeria and Kenya). The study is unique for anumber of reasons.

First, the four countries represent the largest markets on the Africancontinent and have common colonial experience. The markets are workingtowards a pan-African stock exchange through the African Stock ExchangesAssociation (ASEA) and integration with the world economy. All markets areopen to foreign investments and, have implemented free market reforms.There have been various common policies, such as harmonising tradingpractices, encouraging cross-border listing of shares, developing computerisedtrading systems and promoting greater inter and intra regional trade. Theseefforts, benign as they may be, have important implications for market effi-ciency, risk diversification and asset allocation.

26 / Proceedings of the African Economic Conference 2008

Second, this paper analyses not only the linkages that exist among Africancountries, but also those between African markets and the rest of the world.We study both long-run relationships and short-term dynamics. The formeris achieved through cointegration. Following Engle and Granger (1987) andJohansen (1991, 1995), cointegration has been widely used to explore long-run relationships between markets. A priori, one would expect that the remo-val of restrictions on the movement of capital around the world would bringnational economies together. Moreover, if stock prices are cointegrated, theunderlying fundamentals may equally be cointegrated (see Kasa, 1992, andalso Engsted and Lund, 1997).

Thirdly, geographical proximity, international trade agreements and/orhistorical ties tend to drive markets together (see Portes and Rey, 2002).

Our results indicate that the average monthly stock return correlationbetween Africa and the developed countries is 14% (this is similar to theevidence reported by Harvey, 1995); that between Africa and the emergingmarkets (in Latin America and Asia) is only 13%. Through cointegrationanalysis, African markets share weak stochastic trends with both the rest ofthe world and with each other. With the exception of South Africa, theAfrican markets in our sample appear almost completely segmented, and tendto respond more to local information than global events. Although Africancountries have made efforts to attract portfolio capital, the response of theinternational investor community has been less enthusiastic. This, in turn,could be attributed to a myriad of factors: home bias attitude of foreigninvestors, lack of information on African companies, poor accounting andauditing standards, minimal investor protection and perceptions of excessiverisk in African markets. Policy response through the deepening of economicties, lessening the impediments to the flow of financial capital and policycoordination will not only improve the efficiency of the markets but also givemeaning to the ideals of a pan-African exchange.

The rest of the paper is organised as follows: we outline the cointegrationmethodology in section 2. The data and their time series properties arecovered in section 3. Section 4 examines the empirical results. The short-rundynamics of our model are presented in section 5.

2. Equity Market Integration

Integration may be loosely referred to the extent to which financialmarkets are connected (Kenen, 1976). Financial markets may, however, beconnected both vertically (through the term structure of interest rates) andhorizontally across a number of geographically distinct markets at each matu-rity. The dynamics of asset returns across both classes and internationalmarkets is essential for the functions of everyday financial management, frommanaging asset allocation and assessing risk, to calculating hedge ratios, orpricing derivative instruments. The empirical approach to modelling integra-

Chapter 2 - African Stock Market Integration... / 27

tion range from, but not limited to structural and time series models. In thispaper, we make use of cointegration (see Johansen, 1990, 1991). The Johan-sen maximum likelihood procedure provides a unified framework for theestimation of multivariate cointegrating systems based on the error correctionmechanism of the VAR(k) model with Gaussian errors and its usefulness inthe analysis of convergence issues would be described as follows:

Define Xt as a set of I (1) variables consisting of n stock indices. AVAR(k) model, can be expressed as

Xt = µ + A1Xt-1 + A2Xt-2 + ... + AkXt-k + et (1)

where Ak is an n × n coefficient matrix, t = 1,2,...,T and et is a random errorterm. Equation (1) may be reformulated into an error correction model as

DXt = µ + Rk-1

i=1CiDXt-i + PiXt-k + et (2)

where D is the first difference operator, C is an n × n coefficient matrix,defined as Ci = -(I – A1 - ... -Ai), which represents the short-run dynamics,and P is an n × n matrix defined as P = -(I - A1 - ... - Ak), where I is anidentity matrix, whose rank determines the number of distinct cointegratingvectors. The usefulness of this methodology in the current analysis essenti-ally comes down to determining the rank of the matrix P. If P has rank r,then there are r cointegrating relationships between the Xt or n - r commonstochastic trends. The number of cointegrating vectors reveals the extent ofintegration across stock markets. If n - r = 0 (r = n) (full rank), we have theabsence of any stochastic trends, with all elements in Xt being stationary[I(0)] and cointegration is not defined. If n - r = n (r = 0) there are nostationary long-run relationships among the elements of Xt. This latterstatement has implications for diversification across international equitymarkets, since a common trend implies relatively high cross-market correla-tion, thereby diluting any potential diversification benefit over the long-run.Reduced rank (n > n-r > 0) implies the existence of at least one commonstochastic trend, and there will then exist n × r matrices � and b such thatP = �b’. The b matrix gives the cointegrating vectors, while � gives theamount of each cointegrating vector entering each equation of the VECM,also known as the adjustment matrix. A finding of reduced rank wouldimply that, while long-run integration is not complete, the convergenceprocess is underway, with the number of independent stochastic trendsreflecting the extent of this convergence and any diversification and institu-tional issues arising from this.

The main advantage of Johansen’s vector autoregressive estimation pro-cedure is, however, in the testing and estimation of the multiple long-runequilibrium relationships. In addition, the testing of various economic hypo-theses via linear restrictions in the cointegration space is possible when usingJohansen’s estimation method (e.g., Johansen and Juselius, 1990).

28 / Proceedings of the African Economic Conference 2008

3. The Data and their Time Series Properties

The sample is made up of four African stock markets, which satisfy thedefinition of ’emerging market’ (South Africa, Egypt, Nigeria and Kenya)2;first the data in these countries is well reported and readily available. Second,these four countries represent the largest stock markets and could proxy forstock market movements in the rest of the African continent. We have twoLatin American countries (Brazil and Mexico); one Asian economy (India)and three industrialized economies (United States, Japan and the UnitedKingdom). The data consist of monthly closing prices for all countries fromJanuary 1997 to February 2006. The data for Brazil, Mexico, India, Egyptand South Africa is the Morgan Stanley Capital International (MSCI) Index.

The MSCI is designed to be directly comparable across national exchan-ges and is compiled on a value-weighted basis for freely investable shares. ForKenya and Nigeria, the MSCI is unavailable, so we utilise the Standards andPoor (S&P) and International Finance Corporation Global Indices (IFCG).The present coverage of the IFCG Index exceeds 75% of total market capita-lisation, drawing on stocks in order of their liquidity. For the developedcountries, we used the widely available stock indices, i.e., FTSE100 for UK,S&P 500 for US and Nikkei 225 for Japan. All the data are reported in USdollars. Calculating the returns in US dollars eliminates location inflation andthus makes the results more comparable. It also eliminates exchange rate riskand other trading costs associated with investing in developing economies,which may be overlooked when using local currency returns. Monthly data isused to circumvent the problem of non-synchronous trading, so common inemerging markets, and to avoid the possible effects of ’autocorrelation involatility’, a feature of high frequency data such as daily or weekly prices. Allthe indices were obtained from DataStream. Figure 1 presents each of thestock market series in their natural logarithm form. The exchanges of thethree developed markets (UK, US and Japan) are the most advanced stockmarkets in the world and tend to move in response to events within the globaleconomy. One can see the impact of the 2000 dotcom bubble on the threeindices around 2000/2001, as shown in Figure 1. Mexico, South Africa, Indiaand Brazil experienced a downward spike in their indices around 1998, withvarying degrees of intensity. Egypt, Kenya and Nigeria appear to followsimilar trends. After initial low values, the Egyptian and Kenyan indicesbegan an upward trend in late 2003; Nigeria from 2001. In general, the trendin all markets seems to be upward after 2004.

2. The Standards and Poor’s Emerging Market Database classifies a stock market as ’emerging’ if (i) it islocated in a low or middle income economy (which, according to the World Bank high incomeeconomies, are those with Gross National Income (GNI) greater than $9,386 as of 2003);(ii) itsinvestable market capitalisation is low relative to its most recent GNI figures, see S&P (2005 p. 70).This definition effectively puts all the African, Asian and Latin American markets in our sample into thecategory of emerging market economies.

Chapter 2 - African Stock Market Integration... / 29

Figure 1. Logarithms of Monthly Stock Prices

30 / Proceedings of the African Economic Conference 2008

Table 1 presents key valuation measures for the markets examined in thispaper. These include market capitalisation, turn over ratio, dividend yieldsand price/earning ratios. The table shows that, using annual trading value andstock market capitalisation, the African countries (except South Africa) per-form the worst. For instance, the turn over ratio for Kenya, Nigeria and Egyptin 2004 was 8.2%, 13.7% and 17.3% respectively. While these are compara-ble to India (10.3%), they are far less than their Latin American counterpartsare: Mexico (29%) and Brazil (34.9%). South Africa is an exception, with aturn over ratio surpassed only by the developed economies. In terms of marketcapitalisation, outside South Africa, African markets are small compared totheir counterparts in Asia and Latin America (see column 4).

Interestingly, Table 1 reveals that, ranked in terms of key parameters,such as dividend yields, price-earning ratios and price-book value ratios,African markets compare very well with their counterparts elsewhere. Withthe exception of Kenya, the evidence in Table 1 (last column) indicatespositive returns on all indices in 2004. Price/earning ratios for Nigeria(23.5%) and Egypt (21.8%) exceed those of Brazil, Mexico, and the develo-ped markets (except Japan). Dividend yields have also been higher for Africanmarkets as of 2004.

In addition to Table 1, since 1995 African stock indices have gainedabout 40%, with the value of stocks on the Nigerian stock market registeringover a 100% increase in dollar terms3. These facts indicate that investing indeveloping countries could provide high returns and thus aid in portfoliodiversification, an issue we shall turn to shortly. Table 2 present summarystatistics of the markets.

The evidence from Table 2 shows that mean monthly returns during thesample period have been high for the emerging economies. The emergingprocess is always accompanied by high returns. Overall, mean monthlyreturns are highest for Nigeria, Kenya, India and Mexico. The averagemonthly return for these countries is estimated to be 1.2%. This is higherthan the corresponding average for the three developed economies (0.23%)over the same period. This finding indicates that holding the four emergingmarkets stocks over the period July 1997 to February 2006 paid returns of97%, higher than the developed countries in our sample. However, Table 2also indicates that emerging markets are relatively risky (for instance, theycarry additional political, economic and currency risks). The standard devia-tion, which is a crude measure of risk, is highest for Brazil and lowest for UK.For the four emerging markets with the highest mean, the average standarddeviation is 0.07, while that of the three advanced economies is estimated tobe 0.05. An investor in emerging markets should therefore be willing toaccept volatile returns, i.e., there is a chance for large profits at the riskof large losses.

3. It must be emphasized however, that the spill over of the credit crunch has taken a toll on markets suchas Nigeria with the share price index almost near crush levels

Chapter 2 - African Stock Market Integration... / 31

Tab

le1.

Co

mp

arat

ive

Val

uat

ion

Num

ber

ofC

ompa

nies

Tur

nove

rR

atio

Cap

ital

isat

ion

(mill

ion$

)P

/E

Rat

ioP

/BV

Rat

ioD

ivid

end

Yie

ldC

hang

ein

Inde

x(%

)

1995

2004

1995

2004

1995

2004

1995

2004

1995

2004

1995

2004

1995

2004

Ken

ya56

472.

88.

218

8638

91-

19-

3.4

-4.

9-

-10

Nig

eria

181

207

0.8

13.7

2033

1446

412

.523

.53.

63.

25.

63.

7-2

0.9

27.6

Egy

pt74

679

210

.917

.380

8838

515

-21

.8-

4.4

-1.

5-

114.

0

S.A

fric

a64

040

36.

547

.428

052

4555

3618

.816

.22.

52.

52.

33.

117

.855

.9

Bra

zil

543

357

47.9

34.9

1476

3633

0347

20.6

10.6

0.5

2.0

3.8

4.1

-18.

640

.3

Mex

ico

185

152

33.0

29.4

90,6

4917

1940

26.7

15.5

1.8

2.5

1.1

1.8

-26.

051

.4

Indi

a55

5347

3016

.110

.326

6443

3878

5118

.018

.94.

03.

71.

71.

6-2

.28.

9

Japa

n22

6332

2033

.310

5.1

3667

292

3678

262

139.

129

.22.

31.

60.

71.

1-1

.016

.9

UK

2078

2486

39.0

142.

214

0773

728

1592

816

.023

.82.

42.

34.

23.

123

.221

.3

US

7671

5231

85.7

126.

668

5762

216

3237

2618

.720

.72.

93.

02.

31.

937

.012

.5

Sour

ce:A

llcu

rren

cyun

its

are

inU

Sdo

llars

.Sou

rce

ofda

tais

S&P

(200

5)G

loba

lSto

ckM

arke

tFa

ctbo

ok.P

/Eis

pric

e-ea

rnin

gra

tio;

P/B

Vis

the

pric

eto

book

valu

era

tio.

For

the

deve

lope

dm

arke

tsth

ese

are

calc

ulat

edus

ing

S&P

Cit

igro

upIn

dex

whi

lefo

rth

eem

ergi

ngm

arke

ts,t

heS&

P/IF

CG

inde

xis

used

.

32 / Proceedings of the African Economic Conference 2008

Tab

le2.

Su

mm

ary

Sta

tist

ics

of

Sto

ckR

etu

rns:

July

1997

toF

ebru

ary

2006

Egy

ptK

enya

Nig

eria

S.A

fric

aB

razi

lM

exic

oIn

dia

Japa

nU

KU

S

Mea

n0.

005

0.01

30.

012

0.00

30.

007

0.01

20.

011

-0.0

010.

003

0.00

5

Max

imum

0.29

70.

228

0.24

30.

233

0.20

40.

301

0.42

60.

195

0.12

80.

173

Min

imum

-0.1

98-0

.249

-0.2

48-0

.422

-0.4

17-0

.280

-0.4

01-0

.158

-0.1

19-0

.114

Std.

Dev

.0.

086

0.07

90.

073

0.08

90.

112

0.09

80.

102

0.06

00.

044

0.04

7

Skew

ness

0.73

80.

061

0.23

9-1

.195

-1.1

45-0

.679

-0.4

070.

295

-0.3

080.

093

Kur

tosi

s3.

884.

934.

266.

724.

673.

996.

733.

353.

613.

79

JB13

.42*

*18

.38*

*8.

92**

94.4

**36

.412

.8**

66.4

**2.

333.

673.

267

Prob

0.00

10.

000

0.01

150.

000

0.00

00.

001

0.00

00.

3118

0.15

920.

195

Chapter 2 - African Stock Market Integration... / 33

The return distribution of the developing African and Asian countries isleptokurtic, with too many large returns to be consistent with a normaldistribution. However, as the Jacque–Bera (J.B) statistics show, the returncharacteristics of the developed markets in Table 2 show less extreme beha-viour.

3.1. Africa’s Correlations with the World

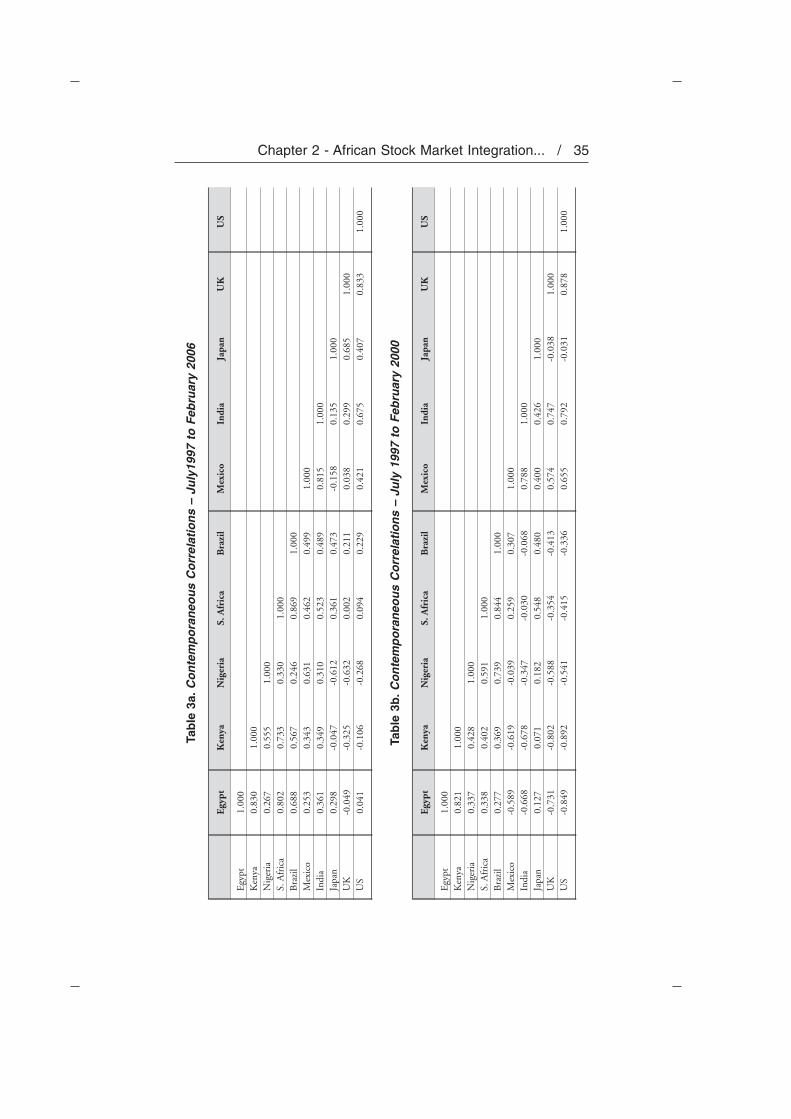

One of the benefits of investing in emerging markets is that the securityreturns in these markets are not highly correlated with the returns of thedeveloped markets (see Harvey, 1995). Therefore, adding emerging marketsecurities to portfolios containing only securities from developed markets canreduce overall portfolio risk, even though securities from emerging marketsare characterised by higher expected risk than developed markets. To addressthis we calculate the return correlations between each of the markets in oursample (see Table 3). Table 3 divides the sample into two. Table 3a shows thereturn correlations for the entire sample July 1997 to February 2006. Therationale for dividing the sample is two fold: first, to see whether the correla-tions between each pair of markets have changed over the ten year period and,second, to take into account any breaks in the series that could have occurredover the period.

For instance, the decade under investigation witnessed the Far East finan-cial crisis (following the speculative attack on the Thai baht in 1997). By1998 the contagion had spread to other emerging markets, such as Brazil andSouth Africa, with attendant depreciation of their currencies and dips in stockprices (see Figure 1 for evidence); hence the choice of the first sub-samplefrom July 1997 to February 2000. The second event is the dot com bubble inearly 2000, mainly in developed countries. Given the links that exist betweennations through trade, technology transfer and other forms of mutual agree-ments, these events are expected to have an impact on the extent to whichcountries interact through trade networks and technology diffusion; thus thesecond sub-sample from March 2000 to February 2006.

The returns of African markets show varying degrees of correlation witheach other and with the emerging and developed markets. The return correla-tion between the markets was weaker during the period July 1997 toFebruary 2000 than from March 2000 to February 2006. Table 3b showsthat the returns from African markets typically had low or negative correla-tions with US and UK stock returns. During this period, Egypt had a returncorrelation of 0.13 with Japan, and was negatively correlated with the UKand US. Negative correlations with the developed and other emerging mar-kets also appear for Kenya, Nigeria and South Africa. During the periodMarch 2000 to February 2006 (Table 3c), the correlations between each pairof markets have been positive throughout. Several major changes occurredover time between each pair of markets. For example, as Table 3c shows, thecorrelation between the Egyptian market and the S&P index is 0.4, compared

34 / Proceedings of the African Economic Conference 2008

Tab

le3a

.Co

nte

mp

ora

neo

us

Co

rrel

atio

ns

–Ju

ly19

97to

Feb

ruar

y20

06

Egy

ptK

enya

Nig

eria

S.A

fric

aB

razi

lM

exic

oIn

dia

Japa

nU

KU

S

Egy

pt1.

000

Ken

ya0.

830

1.00

0N

iger

ia0.

267

0.55

51.

000

S.A

fric

a0.

802

0.73

30.

330

1.00

0B

razi

l0.

688

0.56

70.

246

0.86

91.

000

Mex

ico

0.25

30.

343

0.63

10.

462

0.49

91.

000

Indi

a0.

361

0.34

90.

310

0.52

30.

489

0.81

51.

000

Japa

n0.

298

-0.0

47-0

.612

0.36

10.

473

-0.1

580.

135

1.00

0U

K-0

.049

-0.3

25-0

.632

0.00

20.

211

0.03

80.

299

0.68

51.

000

US

0.04

1-0

.106

-0.2

680.

094

0.22

90.

421

0.67

50.

407

0.83

31.

000

Tab

le3b

.Co

nte

mp

ora

neo

us

Co

rrel

atio

ns

–Ju

ly19

97to

Feb

ruar

y20

00

Egy

ptK

enya

Nig

eria

S.A

fric

aB

razi

lM

exic

oIn

dia

Japa

nU

KU

S

Egy

pt1.

000

Ken

ya0.

821

1.00

0N

iger

ia0.

337

0.42

81.

000

S.A

fric

a0.

338

0.40

20.

591

1.00

0B

razi

l0.

277

0.36

90.

739

0.84

41.

000

Mex

ico

-0.5

89-0

.619

-0.0

390.

259

0.30

71.

000

Indi

a-0

.668

-0.6

78-0

.347

-0.0

30-0

.068

0.78

81.

000

Japa

n0.

127

0.07

10.

182

0.54

80.

480

0.40

00.

426

1.00

0U

K-0

.731

-0.8

02-0

.588

-0.3

54-0

.413

0.57

40.

747

-0.0

381.

000

US

-0.8

49-0

.892

-0.5

41-0

.415

-0.3

360.

655

0.79

2-0

.031

0.87

81.

000

Chapter 2 - African Stock Market Integration... / 35

Tab

le3c

.Co

nte

mp

ora

neo

us

Co

rrel

atio

ns

–M

arch

2000

toF

ebru

ary

2006

Egy

ptK

enya

Nig

eria

S.A

fric

aB

razi

lM

exic

oIn

dia

Japa

nU

KU

S

Egy

pt1.

000

Ken

ya0.

924

1.00

0N

iger

ia0.

821

0.83

31.

000

S.A

fric

a0.

910

0.89

60.

811

1.00

0B

razi

l0.

774

0.79

80.

654

0.86

51.

000

Mex

ico

0.74

00.

739

0.74

90.

828

0.91

31.

000

Indi

a0.

813

0.82

20.

739

0.87

70.

925

0.92

01.

000

Japa

n0.

310

0.35

80.

260

0.47

30.

728

0.66

70.

585

1.00

0U

K0.

103

0.17

20.

000

0.22

10.

601

0.50

60.

432

0.80

11.

000

US

0.40

30.

451

0.26

30.

513

0.81

00.

721

0.69

10.

876

0.86

71.

000

36 / Proceedings of the African Economic Conference 2008

to -0.85 in Table 3b. This indicates that the Egyptian market has becomemore related to the US market, probably because of market reforms takingroot during this period. The change from negative to positive correlation inTable 3c shows how volatile the relationship of emerging markets to develo-ped markets can be.

For the entire sample (Table 3a), the average correlation among Africanstock markets is 0.58. This compares favourably with the average correlationof the three developed markets of 0.64, and emerging India and Latin Ame-rica of 0.6. Thus, we observe quite strong correlations between African mar-kets during the period July 1997 to February 2006. This is particularly thecase for South Africa, Egypt and Kenya, which are strongly correlated. Thesecorrelations appear quite close to their counterparts in developed and emer-ging markets. However, when one compares Africa and the rest of the world,a different picture emerges. The average return correlation between Africaand the developed countries is 0.14, while that between Africa and emergingIndia and the Latin American markets is only 0.13. On a pair wise basis,African markets show weak correlations with each other.

While the correlation coefficients presented in Table 3 provide somepreliminary insight into the interdependence of the markets examined, itmust be emphasized that these are static measures and, as such, do not reflectthe dynamic relationships between the markets.

4. Stationarity and Cointegration

The empirical investigation of the relationship between African equitymarkets and the rest of the world begins with testing for the presence of unitroots. Three unit roots test are employed: ADF, PP and Breitung. The resultssuggest that all prices are I (1), evidence consistent with Figure 1(resultsavailable upon request). Thus, cointegration analysis is a valid method ofexploring the stochastic trends in the system, or any pair of the series. Theevidence here is based on the Johansen (1991, 1995) cointegration test toinvestigate the degree of linkage among the ten markets.

Intuitively, if financial markets share a common trend, then there shouldbe no long-term gains to international diversification. We consider all Africancountries as a system; Africa and emerging markets as another system, andlastly Africa and the developed markets. The intuition is straightforward: wewish to examine how integrated African stock markets are with each other(regional integration), and to assess the trends between African markets andthe rest of the world (global integration). The lag length was determined bySchwartz (SIC) and Akaike (AIC) Information Criterion using 10 lags in thegeneral VAR model. The objective is to choose the number of parameters,which minimizes the value of the information criteria. The SIC has thetendency to underestimate the lag order, while adding more lags increases thepenalty for the loss of degrees of freedom. However, since we are interested in

Chapter 2 - African Stock Market Integration... / 37

making sure that there is no remaining autocorrelation in the VAR model, weshall adopt the AIC (column 10 of Table 4 shows the lag length selected.Detailed results available on request).

Having selected the appropriate lags, we apply the Johansen cointegra-tion approach. The coefficient for the deterministic trend in our data isrestricted to zero. An intercept and no trend are specified for the cointegra-ting equation. We report the trace and max test statistics and their correspon-ding p-values from Doornik (1998) for the null and alternative hypothesis inTable 4 and 5.

The null hypothesis r=0 gives a trace statistic of 73.24 for African coun-tries, which is significant at the 1% level. The max statistics has a value of44.26, which also corresponds to the 1% level of significance. Using the smallsample corrections the trace and max statistic are still significant at the 5%and 1% levels respectively.

The evidence for African and emerging markets indicates seven cointe-grating vectors. With the AIC selecting, a lag length of 10 we find strongevidence of cointegration between African and emerging markets. However,applying the small sample corrections, the hypothesis that r=0 cannot berejected using the trace and max test statistics.

The results presented in the last panel of Table 4 suggest that African anddeveloped countries appear to have seven cointegrating relationships. Howe-ver, the small sample corrections indicate just one cointegrating vector.

It is evident from Table 4 that the Johansen test is susceptible to smallsample bias. In a Monte Carlo study, Cheung and Lai (1993) find that, insmall samples, the Johansen tests are biased more often than what asymptotictheory suggests. In a simulation study, Godbout and van Norden (1997) findconsiderable size distortions in the Johansen test for cointegration, especiallyin VAR models with many lagged variables. Our results suggest that the laglength of 10 for African/Emerging markets, and Africa/developed marketsmay affect the empirical distribution of the test statistics. To this end, weconcentrate on the results based on the small sample corrections.

The results from Table 4 suggest that there are no independent linearcombinations of the vector of stock price series, Xt, that are stationary for theset of African and emerging countries that we examine during the period1997 to 2006. Concerning African markets and their developed counterparts,one stochastic trend in a system of seven countries is found for the entiresample. There is one cointegrating vector binding the African countries inour sample.

We use the evidence presented in Table 4 to address whether marketconvergence is occurring between Africa and the rest of the world. Further,we also address the issue of portfolio diversification within the cointegrationliterature. In developing stochastic definitions of convergence and commontrends based on cointegration analysis, Bernard (1991) argues that a necessary(but not sufficient) condition for multi-country convergence is that there aren-1 cointegrating vectors for n countries. For time series data, this notion of

38 / Proceedings of the African Economic Conference 2008

Tab

le4.

Mu

ltiv

aria

teJo

han

sen

test

Ran

kT

race

test

[P

rob]

Max

test

[P

rob]

Tra

cete

st(T

-nm

)M

axte

st(T

-nm

)L

AG

SL

M(q

)

Afr

ica

073

.24

[0.0

06]*

*44

.26

[0.0

00]*

**64

.45

[0.0

43]*

*38

.95

[0.0

04]*

**2

1.17

7[0.

242]

128

.97

[0.5

69]

15.0

9[0

.637

]25

.49

[0.7

64]

13.2

8[0

.783

]2

13.8

8[0

.671

]9.

72[0

.655

]12

.22

[0.7

96]

8.56

[0.7

68]

34.

16[0

.720

]4.

16[0

.721

]3.

66[0

.786

]3.

66[0

.788

]A

fric

a/E

mer

ging

040

5.42

[0.0

00]*

**10

9.11

[0.0

00]*

**12

1.62

[0.6

36]

32.7

3[0

.831

]10

0.98

7[0.

523]

129

6.31

[0.0

00]*

**82

.59

[0.0

00]*

**88

.89

[0.7

37]

24.7

8[0

.932

]2

213.

72[0

.000

]***

69.2

8[0

.000

]***

64.1

2[0

.730

]20

.78

[0.9

04]

314

4.45

[0.0

00]*

**49

.74

[0.0

00]*

**43

.33

[0.7

22]

14.9

2[0

.940

]4

94.7

1[0

.000

]***

45.5

8[0

.000

]***

28.4

1[0

.602

]13

.67

[0.7

53]

549

.13

[0.0

00]*

**33

.67

[0.0

00]*

**14

.74

[0.6

03]

10.1

[0.6

16]

615

.46

[0.0

14]*

*15

.46

[0.0

14]*

*4.

64[0

.654

]4.

64[0

.655

]A

fric

a/D

evel

oped

043

8.19

[0.0

00]*

**15

7.66

[0.0

00]*

**13

1.46

[0.0

76]*

47.3

[0.0

43]*

*10

0.85

7[0.

756]

128

0.53

[0.0

00]*

**10

2.14

[0.0

00]*

**84

.16

[0.4

78]

30.6

4[0

.454

]2

178.

39[0

.000

]***

77.2

3[0

.000

]***

53.5

2[0

.741

]23

.17

[0.5

97]

310

1.16

[0.0

00]*

**40

.6[0

.000

]***

30.3

5[0

.897

]12

.18

[0.9

46]

460

.55

[0.0

00]*

**35

.77

[0.0

00]*

**18

.17

[0.8

28]

10.7

3[0

.772

]5

24.7

8[0

.010

]***

13.2

1[0

.128

]7.

43[0

.863

]3.

96[0

.948

]6

11.5

7[0

.016

]**

11.5

7[0

.016

]**

3.47

[0.5

08]

3.47

[0.5

07]

Not

e:p-

valu

esar

eba

sed

onD

oorn

ik(1

998)

;*,

**,

***

deno

tes

sign

ifica

nce

ofth

ete

stst

atis

tic

atth

e10

%,

5%an

d1%

leve

lre

spec

tive

ly.

LM(q

)de

note

sth

eLa

gran

geM

ulti

plie

rte

sts

for

resi

dual

auto

corr

elat

ion

ofor

der

q.(T

-nm

)ar

eth

esm

alls

ampl

eco

rrec

tion

s.

Chapter 2 - African Stock Market Integration... / 39

Tab

le5.

Biv

aria

teJo

han

sen

Test

Tra

cete

st[

Pro

b]T

race

test

[P

rob]

Max

test

[P

rob]

H0:

rank

<0H

0:ra

nk<1

H0:

rank

<0H

0:ra

nk<1

LAG

SLM

(q)

Sout

hA

fric

a/E

gypt

29.5

1[0

.015

]**

7.49

[0.3

05]

22.0

2[0

.017

]**

7.49

[0.3

06]

40.

288

[0.9

6]So

uth

Afr

ica/

Ken

ya18

.79

[0.3

00]

7.25

[0.3

29]

11.5

4[0

.472

]7.

25[0

.330

]2

0.28

8[0

.96]

Sout

hA

fric

a/N

iger

ia17

.45

[0.3

90]

3.58

[0.7

96]

13.8

7[0

.273

]3.

58[0

.798

]2

1.27

4[0

.259

]So

uth

Afr

ica/

Bra

zil

19.7

8[0

.242

]8.

27[0

.238

]11

.51

[0.4

74]

8.27

[0.2

38]

21.

354[

0.21

9]So

uth

Afr

ica/

Mex

ico

11.8

9[0

.817

]4.

38[0

.689

]7.

51[0

.855

]4.

38[0

.690

]3

0.66

6[0

.721

]So

uth

Afr

ica/

Indi

a7.

93[0

.827

]1.

26[0

.900

]6.

67[0

.712

]1.

26[0

.899

]2

0.43

3[0

.896

]So

uth

Afr

ica/

Japa

n14

.09

[0.6

55]

3.77

[0.7

72]

10.3

2[0

.594

]3.

77[0

.774

]2

0.72

7[0

.667

]So

uth

Afr

ica/

UK

26.3

4[0

.042

]**

6.58

[0.4

01]

19.7

6[0

.041

]**

6.58

[0.4

02]

21.

125

[0.3

49]

Sout

hA

fric

a/U

S16

.73

[0.4

44]

4.11

[0.7

26]

12.6

1[0

.372

]4.

11[0

.727

]3

0.92

0[0

.501

]E

gypt

/Ken

ya22

.33

[0.1

30]

7.85

[0.2

72]

14.4

9[0

.230

]7.

85[0

.273

]2

0.87

8[0

.535

]E

gypt

/Nig

eria

26.5

[0.0

40]*

*8.

06[0

.254

]18

.44

[0.0

66]*

8.06

[0.2

54]

30.

727

[0.6

67]

Egy

pt/B

razi

l21

.96

[0.1

43]

3.03

[0.8

62]

18.9

3[0

.056

]*3.

03[0

.863

]2

1.55

9[0

.140

]E

gypt

/Mex

ico

18.6

2[0

.310

]2.

13[0

.945

]16

.48

[0.1

27]

2.13

[0.9

46]

21.

432

[0.1

85]

Egy

pt/I

ndia

19[0

.287

]3.

71[0

.779

]15

.29

[0.1

83]

3.71

[0.7

81]

30.

685

[0.7

04]

Egy

pt/J

apan

19.2

4[0

.273

]4.

2[0

.714

]15

.04

[0.1

97]

4.2

[0.7

16]

21.

379

[0.2

08]

Egy

pt/U

K25

.61

[0.0

52]*

7.96

[0.2

63]

17.6

5[0

.087

]*7.

96[0

.263

]2

1.63

8[0

.116

]E

gypt

/US

23.2

4[0

.102

]8.

7[0

.205

]14

.54

[0.2

27]

8.7

[0.2

05]

21.

075

[0.3

82]

Ken

ya/N

iger

ia18

.35

[0.3

28]

2.12

[0.9

46]

16.2

3[0

.138

]2.

12[0

.947

]2

1.03

1[0

.414

]K

enya

/Jap

an21

.22

[0.1

72]

8.48

[0.2

21]

12.7

4[0

.361

]8.

48[0

.221

]2

1.05

76[0

.395

]K

enya

/UK

26.5

2[0

.039

]**

9.09

[0.1

79]

17.4

3[0

.094

]*9.

09[0

.179

]2

0.36

0[0

.939

]K

enya

/US

24.8

1[0

.066

]*9.

09[0

.179

]15

.72

[0.1

61]

9.09

[0.1

79]

40.

751

[0.6

45]

Not

e:p-

valu

esar

eba

sed

onD

oorn

ik(1

998)

;*,

**,

***

deno

tes

sign

ifica

nce

ofth

ete

stst

atis

tic

atth

e10

%,

5%an

d1%

leve

lre

spec

tive

ly.

LM(q

)de

note

sth

eB

reus

ch-G

odfr

eyte

stfo

rre

sidu

alau

toco

rrel

atio

nof

orde

rq

base

don

the

Lagr

ange

Mul

tipl

ier.

40 / Proceedings of the African Economic Conference 2008

Tab

le5.

Biv

aria

teJo

han

sen

Test

(co

nti

nu

ed)

Tra

cete

st[

Pro

b]T

race

test

[P

rob]

Max

test

[P

rob]

H0:

rank

<0H

0:ra

nk<1

H0:

rank

<0H

0:ra

nk<1

LAG

SLM

(q)

Ken

ya/B

razi

l18

.02

[0.3

50]

3.71

[0.7

80]

14.3

1[0

.242

]3.

71[0

.782

]3

1.60

3[0

.126

]K

enya

/Ind

ia15

.96

[0.5

04]

3.95

[0.7

48]

12.0

1[0

.427

]3.

95[0

.749

]2

1.30

6[0

.242

]K

enya

/Mex

ico

20.0

9[0

.225

]3.

25[0

.836

]16

.84

[0.1

14]

3.25

[0.8

38]

20.

805

[0.5

98]

Nig

eria

/Jap

an15

.47

[0.5

43]

2.01

[0.9

54]

13.4

5[0

.303

]2.

01[0

.955

]2

0.39

1[0

.923

]N

iger

ia/U

K15

.62

[0.5

31]

2.74

[0.8

93]

12.8

8[0

.349

]2.

74[0

.894

]2

0.50

7[0

.849

]N

iger

ia/U

S17

.17

[0.4

10]

4.58

[0.6

62]

12.6

[0.3

74]

4.58

[0.6

64]

20.

912

[0.5

02]

Nig

eria

/Bra

zil

6.97

[0.8

93]

2.29

[0.7

20]

4.68

[0.9

03]

2.29

[0.7

19]

51.

449

[0.1

79]

Nig

eria

/Ind

ia22

.46

[0.1

26]

4.89

[0.6

18]

17.5

7[0

.089

]*4.

89[0

.619

]3

1.19

2[0

.306

]N

iger

ia/M

exic

o18

.73

[0.3

03]

2.5

[0.9

16]

16.2

2[0

.138

]2.

5[0

.917

]2

0.48

2[0

.867

]

Not

e:p-

valu

esar

eba

sed

onD

oorn

ik(1

998)

;*,

**,

***

deno

tes

sign

ifica

nce

ofth

ete

stst

atis

tic

atth

e10

%,

5%an

d1%

leve

lre

spec

tive

ly.

LM(q

)de

note

sth

eB

reus

ch-G

odfr

eyte

stfo

rre

sidu

alau

toco

rrel

atio

nof

orde

rq

base

don

the

Lagr

ange

Mul

tipl

ier.

Chapter 2 - African Stock Market Integration... / 41

convergence requires that, the expected difference between the series becomearbitrarily small (or converges on some constant as time elapses. In the case ofintegrated series, stochastic convergence can be defined in terms of the diffe-rences between the series being of a lower order of integration than theoriginal series). Clearly, from Table 4, this condition fails to hold for oursample. From these results, we can argue that there is some transmission ofstock market shocks across the countries, but the rate of stock market perfor-mance has not been equalised through time.

A potential problem in interpreting the results presented in Tables 4 isthat we cannot isolate the impact of cointegration on the various pairs ofcountries in our sample. We therefore investigate the issue on a pair-wisebasis. With 10 countries in our sample, there can be 45 pairings. However,our interest is in the trends that exist between African countries and theemerging Asian and Latin American countries, and the developed markets.To this end, we present 30 pairings in Table 5.

The evidence from Table 5 fails to reject the null hypothesis of nocointegration for the vast majority of the pairings. Out of 30 pairings, 22pairs are non-cointegrated. The max test is not rejected marginally for thefollowing pairs: Egypt/Brazil, Nigeria/India and Kenya/US. However, wecannot reject the existence of long-run relations between the following pairsat the 5% level using the trace test: South Africa/Egypt, South Africa/UK,Nigeria/Egypt, and Kenya/UK.

The most interesting finding from Table 5 is that none of the Africancountries shares common trends with Mexico and Japan. There appear to bestrong links between African markets and the UK, rather than with the US.This might be due to historical links and colonial ties with the former.

4.1. Implications for Regional and Global Integration

The cointegration test results can be used to address the issue of whetherregional integration is occurring, and/or whether African countries are inte-grated globally. The evidence from Table 4 indicates that African markets arenot integrated regionally. The evidence of a single stochastic trend suggeststhat the pace of integration is slow and at best driven only by the biggermarkets. Thus, even in an economic sense, integration may be occurring butis not yet complete. It is tempting to conclude that geographical proximity isneither a necessary nor a sufficient condition for African stock markets to beintegrated. This would further suggest that efforts at integrating African stockmarkets remain largely futile to date.

Globally, the evidence suggests that African markets remain segmented.As shown in Table 4, the rate of convergence between Africa and the develo-ped markets has not equalized over time. The significant relationships thatexist seem to be driven largely by South Africa and Egypt. The fundamentalquestion is why is it that foreign investors shy away from the emergingmarkets in Africa? One may argue that foreign investors are not responding

42 / Proceedings of the African Economic Conference 2008

rationally to the continent’s investment opportunities because of some hur-dle: home bias or other concerns, such as lack of information on companies,poor auditing and accounting standards, minimal degree of investor protec-tion and emerging markets specific risks (political, currency or macroecono-mic policy risks, see Bekaert, 1995), systematically discourage investors frombringing their capital into Africa.

Second, one can also argue that liquidity or market size present an entrybarrier to African markets. This is more compelling given that, with theexception of South Africa and Egypt, African markets are small compared totheir emerging counterparts elsewhere. Evidence indicates that alternativeroutes to African markets through American Drawing Receipts (ADRs) andcountry funds are sometimes non-existent. A glance through the 94 globalemerging market funds for which data are available shows that they all investin South Africa, but almost none invest elsewhere on the continent (see Mosset al, 2007).

4.2. Implications for Portfolio Diversification

The lack of strong links among African markets, and between Africanmarkets and their counterparts in developed economies and Latin Americaand Asia, present an opportunity for portfolio diversification. With the excep-tion of South Africa/Egypt and Nigeria/Egypt (Table 5), none of the Africanpairs is cointegrated. The practical implication for investors on the continentof Africa is that they can gain by holding portfolios from different countries.For instance, our results suggest the possibility of Kenyan investors being ableto reduce portfolio risk by investing in South Africa, Nigeria or Egypt. Forthe international investor, the evidence shows that including African assets ina portfolio should significantly reduce risk. This is particularly useful in thecontext of the earlier finding of negative or low correlation between Africanmarkets and the developed countries (see Table 3). Not only are there lowand sometimes negative correlations, but also African markets have shownincreasing good performance compared to their counterparts in Asia andLatin America (Table 1).

To throw more light on the results in Table 4, we carried out recursiveestimation. Recursive estimation provides a valuable tool for assessing cons-tancy in the cointegrated models. The left hand side graphs of Figure 2A showthe linear combinations ∫b≠ Xt, t he next four graphs on the right hand side plotthe long-run fitted and actual values. Two of the cointegration vectors lookstationary, with the fitted and actual tracking each other reasonably closely.The other two look less stationary, with not much relationship between fittedand actual. Figure 2B shows the recursively estimated eigenvalues4.

4. We used the R-representation (fixing the short run dynamics at their full sample values) for the recursiveestimation (see Doornik and Henry, 1995).

Chapter 2 - African Stock Market Integration... / 43

The eigenvalues are relatively constant, the first three at non-zero values,and the fourth much smaller but visibly closer to zero throughout. ForAfrican/developed countries (Figure 3A), only one (perhaps two) of the coin-tegration vectors look stationary, with the fitted and actual values being quite

Figure 2A. Unrestricted RelationsAfrican Countries

Figure 2B. Recursive EigenvaluesAfrican Countries

44 / Proceedings of the African Economic Conference 2008

close. The wide gap between actual and fitted for the rest of the countries inFigure 3A could provide supporting evidence to the finding of relative weakcointegration between African and developed markets when we employ thesmall sample corrections to our data.

Figure 3A. Unrestricted RelationsAfrica/Developed

Figure 3B. Recursive EigenvaluesAfrica/Developed

Chapter 2 - African Stock Market Integration... / 45

5. Are African Stock Markets isolated from the restof the World?

An important question worth addressing is whether African markets arecompletely segmented. To investigate further the dynamic relationshipbetween African markets and the rest of the world, we estimate a VAR in firstdifferences for the non-cointegrated markets (see Table 5). The advantage ofusing this model is that it estimates the dependence among the markets, andallows shocking a particular market and analysing how shocks perpetuatethemselves through impulse responses.

In general, a kth order VAR in first differences for a 2x1 vector of jointlydetermined (endogenous) variables Xt is written as

DXt = µ + Rki=1 PiDXt-1 + et (3)

Here, the residual vector et is said to be the innovation (shock) in X thatcannot be predicted from past values of variables in the system. Then, eitherby polynomial lag division or by successive substitution, the correspondingmoving average representation (MAR) is derived from the following equa-tion5:

DXt = P-1(B)et = W(B)et = et + R∞i=1 Wiet-i (4)

where Wi = Rij=1 PjWi-j and W0 = In

In this model, no distinction is made between endogenous and exoge-nous variables, so the Wi matrices can be interpreted as the dynamic multi-pliers of the system, since they represent the model’s response to a unit shockin each of the variables. While the estimated coefficients in the VAR systemprovide very little insight into the dynamic interaction among the series, theMAR presents information equivalent to that contained in the original esti-mates, but allows tracing out the time path of the various shocks on thereturn series (Sims, 1980).

We compute the dynamic response of each market return series to ran-dom shocks in other markets. This shows us how unexpected changes in eachmarket return change the returns of other markets over time. We apply thegeneralised impulse response function (GIRF)

GIRF (n,et,xt-1) = E [Xt+n | ej,t, xt-1] - E [Xt+n | xt-1]t (5)

We follow Pesaran and Shin (1997) by constructing orthogonal sets ofinnovations that do not depend on the VAR ordering. The evidence fromFigure 4 gives the responses resulting from a one standard deviation shock toa pair of the non-cointegrated markets in Table 5 (we produced the impulse

5. As shown by Sims (1980), it is more informative to analyse the system’s reaction to typical randomshocks by tracing out the system’s moving average representation rather than to continue with thecomplicated cross-equation feedbacks involved in the autoregressive representation.

46 / Proceedings of the African Economic Conference 2008

response of all the countries but, for the sake of brevity, we report only theinteresting cases). Monte Carlo constructed 95% confidence bands are provi-ded to judge the statistical significance of the impulse response functions.

From Figure 4, we observe minimal dynamic interactions between themarkets. Indeed, the responses of Egypt and Nigeria to innovations in SouthAfrica are immediate and subside toward zero quickly. The response of theSouth African market to innovations in Egypt is negative, but dies out inabout eight months. The response of Egypt to Kenya and vice versa ispositive. Admittedly, none of the responses is significant. The sensitivity toshocks from other markets is related to the degree of openness and to the levelof macroeconomic coordination between countries. The results of theimpulse response functions give further evidence that African markets do notappear to have strong links.

The responses of the Brazilian market to the South African market appearpositive and significant up to the fourth month. South Africa also respondspositively to innovations in Mexico and vice versa. Given the size of thesemarkets as emerging market economies, one would expect substantial interac-tions between them. The impulse responses between African countries andthe developed countries are minimal and die out in less than six months. Thegeneral trend for the remaining responses is not very different. Evidenceshows that shocks from Japan, UK and US are minimal in explaining shocksin South Africa and vice versa.

These results may be attributed to a low level of policy coordinationamong African countries. Although there have been attempts to encourageequity market integration through the Association of African Stock Exchan-ges, the evidence presented here indicates that the four markets would have toestablish institutional agreements concerning equity markets: the exchangerate mechanism that might increase coordination among these countries hasnot yet been harmonized, and intensive trade and other cooperation amongnational governments is required to remove existing impediments that inhibitthe flow of investment funds across the African continent. The weak linkageamong African markets may also be due to the low proportion of intra-regional trade. Evidence from the WTO statistics indicates that inter Africantrade amounts to only 11% per annum. The direction of trade is highlyinfluenced by colonial ties rather than regional trading blocks such as ECO-WAS or SADC. Thus, not only is equity market integration weak, but alsooverall economic integration remains a dream.

5.1. Independence and Interdependence

To further understand the dynamic relationship between the markets inour sample, we perform Granger causality tests using the VAR model. Causa-lity tests seek to answer the question, do changes in African markets leadchanges in developed and emerging markets in Asia and Latin America (orvice versa)? If this is the case, it follows that African markets must be impor-

Chapter 2 - African Stock Market Integration... / 47

Fig

ure

4.G

ener

alis

edIm

pu

lse

Res

po

nse

s

48 / Proceedings of the African Economic Conference 2008

Fig

ure

4.G

ener

alis

edIm

pu

lse

Res

po

nse

s(c

on

tin

ued

)

Chapter 2 - African Stock Market Integration... / 49

tant in explaining most of the movements in global markets. The evidence isreported in Table 6. Consistent with the results from the impulse responses,there appears to be little feedback between African countries. However, wefind uni-directional causality between the South African market and heremerging counterparts. The evidence from Table 6 shows that the SouthAfrican market significantly influences India, Mexico and Brazil. Given thesize of the Johannesburg stock exchange as the largest emerging market in oursample, one would expect movements in that market to affect movements inother developing stock markets.

Once again, in line with the impulse responses and cointegration tests,very little dynamic interaction is found between African markets, andbetween African markets and their developed counterparts.

6. Summary and Concluding Remarks

Since the late 1980s, a number of African countries have establishedorganised stock exchanges, partly to satisfy their quest for new capital, toencourage indigenisation and to incorporate elements of market capitalisminto their economies. Owing to their small size and low liquidity, significantefforts have been expended in integrating these equity markets. Through theAfrican Stock Exchanges Association (ASEA), closer cooperation among Afri-can stock exchanges has been forged through the existing regional economicblocks. There has also been various policies aimed at integration, such asharmonizing trading practices, encouraging cross border listing of stocks, andpromoting greater inter and intra regional trade. However, there is generally adearth of empirical research on the state of integration of Africa’s markets,both within the continent and with the rest of the world. Little is knownabout the opportunities and threats presented by these emerging markets.Again, little is known about the response of Africa’s markets to global infor-mation factors, and whether disturbances in Africa matter for marketselsewhere.

The theme of this paper centred on equity market integration and itsimplications for market efficiency, portfolio diversification and investmentanalysis. We first examined integration within Africa and then the rela-tionship between African markets and other parts of the world. Our data setincluded four of the most developed African stock markets (South Africa,Nigeria, Egypt and Kenya), two Latin American countries (Brazil andMexico), three developed markets (US, UK and Japan), and finally India. Weemployed cointegration analysis to examine the long-run relationships.Finally, we analysed the short-run dynamics to learn more about the propaga-tion of stock market shocks.

Evidence from cointegration and correlation analysis indicates that Afri-can countries share weak trends with the rest of the world. On the one hand,the evidence suggests that, in spite of many years of collaboration and econo-

50 / Proceedings of the African Economic Conference 2008

Tab

le6.

Gra

ng

erC

ausa

lity

F-st

atis

tic

Pro

bF-

stat

isti

cP

rob

Sout

hA

fric

a–/→

Nig

eria

0.37

40.

689

Egy

pt–/

→K

enya

0.73

10.

484

Nig

eria

–/→

Sout

hA

fric

a1.

310

0.27

4K

enya

–/→

Egy

pt0.

167

0.84

6K

enya

–/→

Sout

hA

fric

a0.

318

0.72

8N

iger

ia–/

→Ja

pan

0.54

50.

461

Sout

hA

fric

a-/K

enya

0.48

50.

617

Japa

n–/→

Nig

eria

0.09

50.

758

Sout

hA

fric

a–/→

Bra

zil

11.7

9**

0.00

0N

iger

ia–/

→U

K1.

048

0.60

4B

razi

l–/→

Sout

hA

fric

a0.

491

0.61

3U

K–/

→N

iger

ia0.

506

0.35

4So

uth

Afr

ica–

/→M

exic

o4.

42**

0.00

6N

iger

ia–/

→U

S2.

113

0.12

6M

exic

o–/→

Sout

hA

fric

a0.

108

0.95

5U

S–/→

Nig

eria

0.09

10.

913

Sout

hA

fric

a–/→

US

1.55

60.

1297

Nig

eria

–/→

Bra

zil

1.29

00.

280

US–

/→So

uth

Afr

ica

0.39

00.

955

Bra

zil–

/→N

iger

ia0.

748

0.47

6So

uth

Afr

ica–

/→Ja

pan

1.04

40.

416

Nig

eria

–/→

Mex

ico

1.51

50.

225

Japa

n–/→

Sout

hA

fric

a0.

855

0.57

8M

exic

o–/→

Nig

eria

0.62

40.

538

Sout

hA

fric

a–/→

Indi

a2.

831*

0.09

5N

iger

ia–/

→K

enya

1.89

60.

117

Indi

a–/→

Sout

hA

fric

a1.

548

0.21

6K

enya

–/→

Nig

eria

1.89

50.

117

Egy

pt–/

→U

S1.

216

0.29

4K

enya

–/→

Japa

n0.

399

0.67

2U

S–/→

Egy

pt1.

269

0.26

3Ja

pan–

/→K

enya

1.02

80.

361

Egy

pt–/

→In

dia

0.27

80.

758

Ken

ya–/

→B

razi

l0.

803

0.45

1In

dia–

/→E

gypt

1.59

00.

209

Bra

zil–

/→K

enya

2.31

70.

104

Egy

pt–/

→M

exic

o0.

330

0.72

0K

enya

–/→

Indi

a2.

153

0.12

1M

exic

o–/→

Egy

pt0.

620

0.54

0In

dia–

/→K

enya

0.67

30.

513

Egy

pt–/

→Ja

pan

1.43

80.

179

Ken

ya–/

→M

exic

o0.

029

0.85

6Ja

pan–

/→E

gypt

0.82

70.

604

Mex

ico–

/→K

enya

0.15

50.

972

Not

e:–/

→de

note

sdoe

snot

Gra

nger

caus

e.Fo

rin

stan

ceSo

uth

Afr

ica–

/→N

iger

iaim

plie

stha

tcha

nges

inth

eSo

uth

Afr

ican

mar

ketd

ono

tto

chan

gesi

nN

iger

ia.T

here

vers

ear

eal

sotr

ue.*

,**

indi

cate

sre

ject

ion

atth

e1%

and

5%le

vels

resp

ecti

vely

.The

test

isba

sed

ona

biva

riat

eV

AR

(k)

mod

el.O

ptim

alla

gle

ngth

isba

sed

onth

eA

IC(r

esul

tsav

aila

ble

onre

ques

t).

Chapter 2 - African Stock Market Integration... / 51

mic reforms, the African stock markets are not significantly influenced byeach other or world stock markets. Thus, geographical proximity and/oreconomic ties do not matter for the integration of African markets. Thiswould suggest that increased inter/intra regional trade, greater financial libe-ralisation, freer mobility of capital and more determined macroeconomiccoordination should precede any attempt at stock market regionalism. On theother hand, the overall results indicate that African assets are attractivelyvalued and, given their low correlations and weak trends with the rest of theworld, can play a significant role in international portfolio diversification (i.e.,by widening the investment opportunity set and hence reducing risk).

References

Bernard, A.B (1991), “Empirical Implications of the Convergence Hypothe-sis”, CEPR Publication 239, Centre for Economic Policy Research, Stan-ford University.

Bekeart G., (1995), “Market Integration and Investment Barriers in Emer-ging Equity Markets”, The World Bank Economic Review, 9, 75-107.

Bekeart, G. and Harvey, C (1995), “Time Varying World Market Volatility”Journal of Finance, 43, 29-77.

Bekeart, G. and Harvey, C (1995), “Asymmetric Volatility and Risk inEquity Markets”, Review of Financial Studies, 13, 1-42

Bracker, K., Dockino, G., and Koch, P (1999), “Economic Determinants ofEvolution in International Stock Market Integration”, Journal of Empiri-cal Finance, 6:1-27.

Breitung, J (2002), “Nonparametric Tests for Unit Roots and Cointegra-tion”, Journal of Econometrics, 108, 343-364.

Breitung, J and Taylor, A.M.R (2003), “Corrigendum to NonparametricTests for Unit Roots and Cointegration”, Journal of Econometrics117,401-4.

Cheung Y-W., and Lai, K.S (1993), “Finite sample sizes of the JohansenLikelihood ratio tests for cointegration”, Oxford Bulletin of Economics andStatistics 55, 313-28.

Classens, S and Forbes, K (eds), (2001), International Financial Contagion:How it Spreads and How it can be Stopped. Kluwer Academic Publishers.

Dickey, D.A., and Fuller, W.A (1979), “Distribution of the Estimators forAutoregressive Time Series with a Unit Root”, Journal of the AmericanStatistical Association, 74,427-31.

Doornik, J.A (1998), “Approximations to the asymptotic distribution ofcointegration tests”, Journal of Economic Surveys 12, 573-593

Engle, R. F., Granger, C. W. J., (1987), “Cointegration and Error Correc-tion: Representation, Estimation and Testing”, Econometrica 55,251–276.

52 / Proceedings of the African Economic Conference 2008

Engsted, T and Lund, J (1997), “Common Stochastic Trends in Internatio-nal Stock Prices and Dividends: An Example of Testing OveridentifyingRestrictions on Multiple Cointegrating Vectors”, Applied Financial Eco-nomics 7, 659-665.

Errunza, V and Losq, E (1985), “International Asset Pricing Under MildSegmentation: Theory and Test”, Journal of Finance 40, 105-24.

Harvey, C.R. (1995), “Predictable Risk and Returns in Emerging Markets”,Review of Financial Studies, 9(1), 75-107.

Huang B., Yang C. and Hu J.W (2000), “Causality and Cointegration ofStock markets among the United States, Japan and the South ChinaGrowth Triangle”, International Review of Financial Analysis 9:3 281-297.

Johansen, S (1991), Estimation and Hypothesis testing of cointegration vec-tors in Gaussian Vector Autoregressive Models, Econometrica 59, and1551-1581.

Johansen, S (1995), “Likelihood-based inference in cointegrated vector auto-regressive models”, Oxford University Press, Oxford.

Johansen, S., and Juselius, K., (990), “Maximum likelihood estimation andinference on cointegration with applications to the demand for money”,Oxford Bulletin of Economics and Statistics 52, 169-210

Kamin, S.B (1999), “The Current International Financial Crisis: How Muchis New?” Journal of International Money and Finance 18, 501-14

Kasa, K. (1992), “Common Stochastic Trends in International Stock Mar-kets”, Journal of Monetary Economics, 29, 95-124.

Kenen, P.B. (1976): Capital Mobility and Financial Integration, PrincetonStudies in International Finance, No. 39, Princeton University press,

Princeton, NJKim, J., and Singal, V (2000), “Stock Market Openings: Experience of

Emerging Economies”, Journal of Business, 73, 25-66.MacKinnon, J.G (1991), “Critical Values for Cointegrating tests”, in R.F

Engle and C.W.J Granger (Eds), Long Run Economic Relationships: Rea-dings in Cointegration, Oxford University Press: New York

Moss, T, Ramachandandran, V and Standley, S (2007), “Why doesn’t Africaget more equity investment? Frontier markets, firm size and asset alloca-tions of Global Emerging Markets Funds. Working Paper 112, Centrefor Global Development.

Obstfeld, M (1995), “Risk-Taking, Global Diversification, Growth”, Ameri-can Economic Review, 84:1310-29.

Pesaran, H and Y. Shin (1997), “Generalized Impulse Response Analysis inLinear Multivariate Models”, Economics Letters, 58, 17-29.

Phillips, P.C.B and Perron, P (1988), “Testing a Unit Root in Time SeriesRegression”, Biometrika, 75,335-46.

Portes, R., and Rey, H (2002), “The Determinants of Cross border EquityFlows”, NBER, Working Paper, Cambridge, M.A

Sims, C (1980), “Macroeconomics and Reality”, Econometrica 48, pp. 1-49.

Chapter 2 - African Stock Market Integration... / 53

Singh, A (1999), “Should Africa Promote Stock Market Capitalism?” Journalof International Development, 11,343-365.

Standard and Poor’s (2005), Global Stock Market Factbook; McGraw-Hill,New York.

Stulz, R (1999), “Globalisation of Equity Markets and Cost of Capital”,Working Paper, The Ohio State University.

54 / Proceedings of the African Economic Conference 2008