Africa – The last great emerging market Australia Africa Business Council (NSW) 21 September 2011.

18

Africa – The last great emerging market Australia Africa Business Council (NSW) 21 September 2011

-

date post

20-Dec-2015 -

Category

Documents

-

view

219 -

download

3

Transcript of Africa – The last great emerging market Australia Africa Business Council (NSW) 21 September 2011.

Africa – The last great emerging market

Australia Africa Business Council (NSW)

21 September 2011

Africa Today

US$1.6 trillion Africa’s GDP in 2008, approximately equal to Brazil or

Russia

US$860 billion Africa’s combined consumer spending in 2008

316 million New mobile phone subscribers signed up in Africa since

2000

60% Africa’s share of the world’s total uncultivated, arable land

52 Number of African cities with more than 1 million people

20 Number of African companies with annual revenues in excess of US$3

billionSource: McKinsey Global Institute

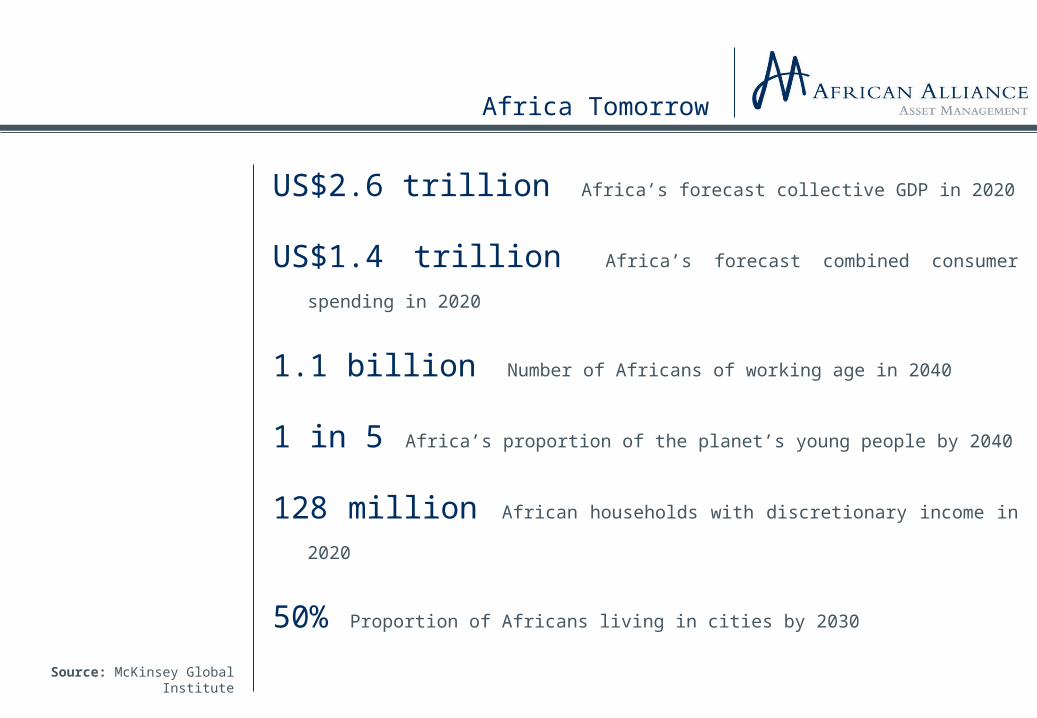

Africa Tomorrow

US$2.6 trillion Africa’s forecast collective GDP in 2020

US$1.4 trillion Africa’s forecast combined consumer spending in

2020

1.1 billion Number of Africans of working age in 2040

1 in 5 Africa’s proportion of the planet’s young people by 2040

128 million African households with discretionary income in 2020

50% Proportion of Africans living in cities by 2030

Source: McKinsey Global Institute

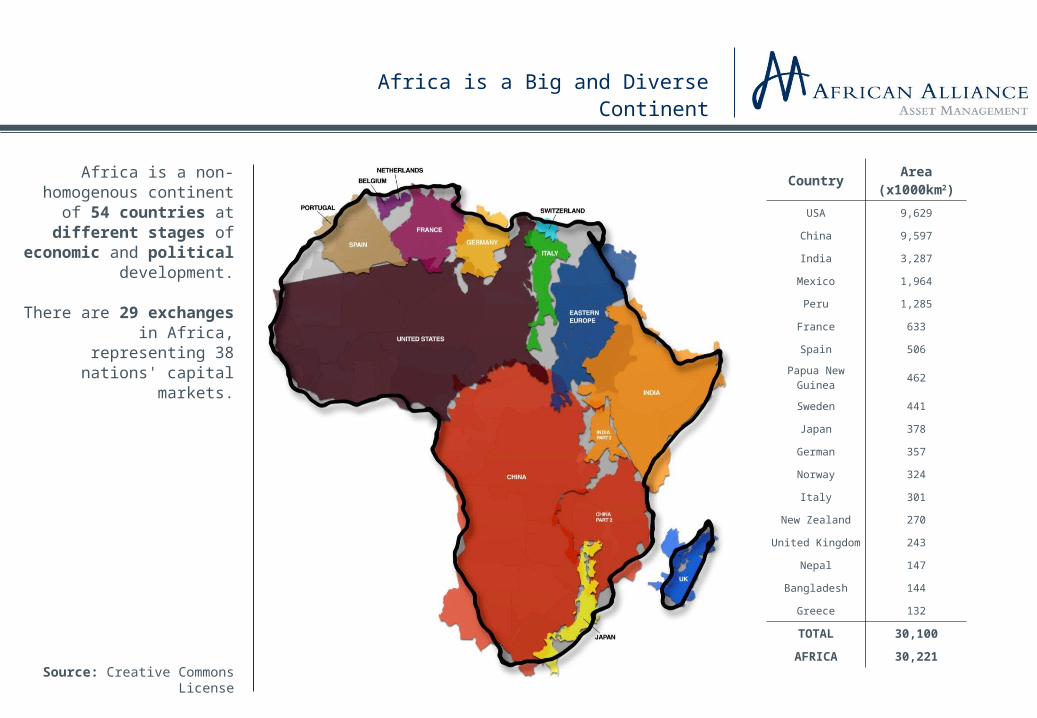

Africa is a Big and Diverse Continent

Africa is a non-homogenous continent of

54 countries at different stages of

economic and political development.

There are 29 exchanges in Africa, representing 38 nations' capital markets.

Source: Creative Commons License

Country Area (x1000km2)

USA 9,629

China 9,597

India 3,287

Mexico 1,964

Peru 1,285

France 633

Spain 506

Papua New Guinea 462

Sweden 441

Japan 378

German 357

Norway 324

Italy 301

New Zealand 270

United Kingdom 243

Nepal 147

Bangladesh 144

Greece 132

TOTAL 30,100

AFRICA 30,221

1. Improved Macroeconomic Stability…

Improved macroeconomic

stability across the African continent has been

achieved by (amongst others):

- Reducing the collective inflation rate from 22

percent in the 1990s to 8 percent after 2000.

- Shrinking budget deficits from 4.6

percent of GDP to 1.6 percent of GDP.

- Reducing the combined foreign debt from 82 percent of GDP to 59

percent of GDP.

- Adopting policies aimed at energizing markets

(privatisations, business competition, open trade,

lower taxes, strengthened regulatory and legal

systems).

1990s 2000s0

5

10

15

20

25

22

8

Inflation(% Per Annum)

1990s 2000s0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

81.9

59.0

Government Debt(% of GDP)

1990s 2000s

-5

-4

-3

-2

-1

0

-4.6

-1.6

Budget Deficit(% of GDP)

Source: World Bank Development Indicators,

Political Risk Services, McKinsey Global Institute

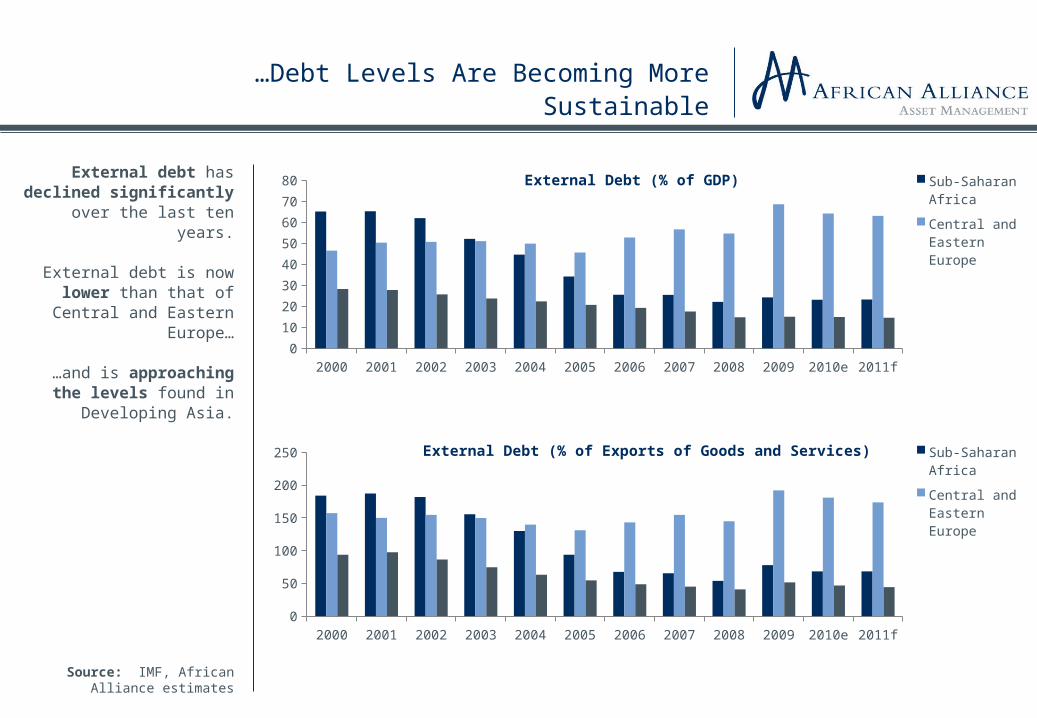

…Debt Levels Are Becoming More Sustainable

External debt has declined significantly over the last ten years.

External debt is now lower than that of Central

and Eastern Europe…

…and is approaching the levels found in

Developing Asia. 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010e 2011f0

10

20

30

40

50

60

70

80 External Debt (% of GDP) Sub-Saharan Africa

Central and Eastern Europe

Developing Asia

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010e 2011f0

50

100

150

200

250 External Debt (% of Exports of Goods and Services) Sub-Saharan Africa

Central and Eastern Europe

Developing Asia

Source: IMF, African Alliance estimates

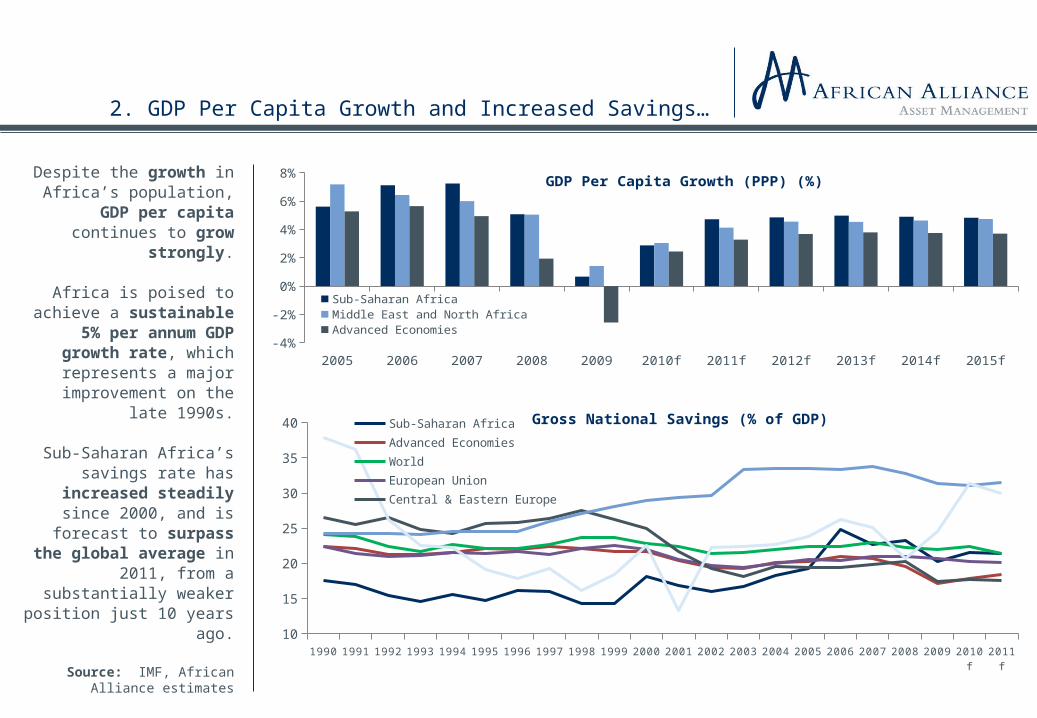

2. GDP Per Capita Growth and Increased Savings…

Despite the growth in Africa’s population, GDP per capita continues to

grow strongly.

Africa is poised to achieve a sustainable 5% per

annum GDP growth rate, which represents a

major improvement on the late 1990s.

Sub-Saharan Africa’s savings rate has

increased steadily since 2000, and is forecast to

surpass the global average in 2011, from a

substantially weaker position just 10 years ago.

2005 2006 2007 2008 2009 2010f 2011f 2012f 2013f 2014f 2015f-4%

-2%

0%

2%

4%

6%

8% GDP Per Capita Growth (PPP) (%)

Sub-Saharan AfricaMiddle East and North AfricaAdvanced Economies

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010f

2011f

10

15

20

25

30

35

40 Gross National Savings (% of GDP)Sub-Saharan AfricaAdvanced EconomiesWorldEuropean UnionCentral & Eastern EuropeDeveloping AsiaMiddle East & North Africa

Source: IMF, African Alliance estimates

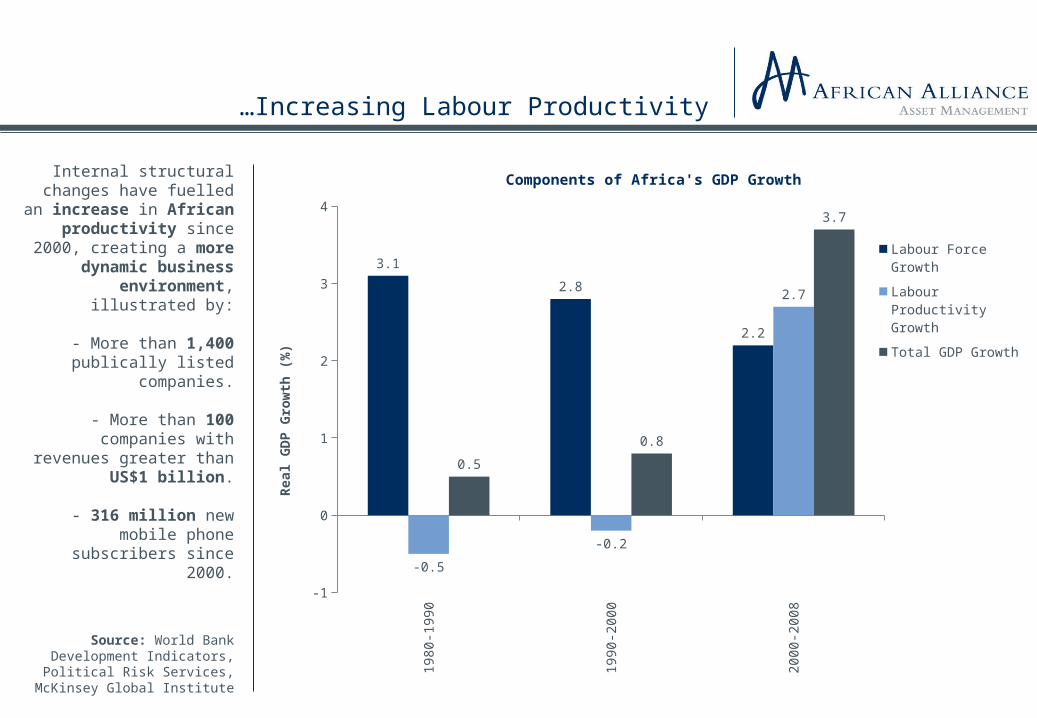

…Increasing Labour Productivity

Internal structural changes have fuelled an

increase in African productivity since 2000,

creating a more dynamic business environment,

illustrated by:

- More than 1,400 publically listed

companies.

- More than 100 companies with revenues

greater than US$1 billion.

- 316 million new mobile phone subscribers since

2000.

Source: World Bank Development Indicators,

Political Risk Services, McKinsey Global Institute

1980-1

990

1990-2

000

2000-2

008

-1

0

1

2

3

4

3.1

2.8

2.2

-0.5

-0.2

2.7

0.5

0.8

3.7

Components of Africa's GDP Growth

Labour Force Growth

Labour Productivity Growth

Total GDP Growth

Real G

DP

Gro

wth

(%

)

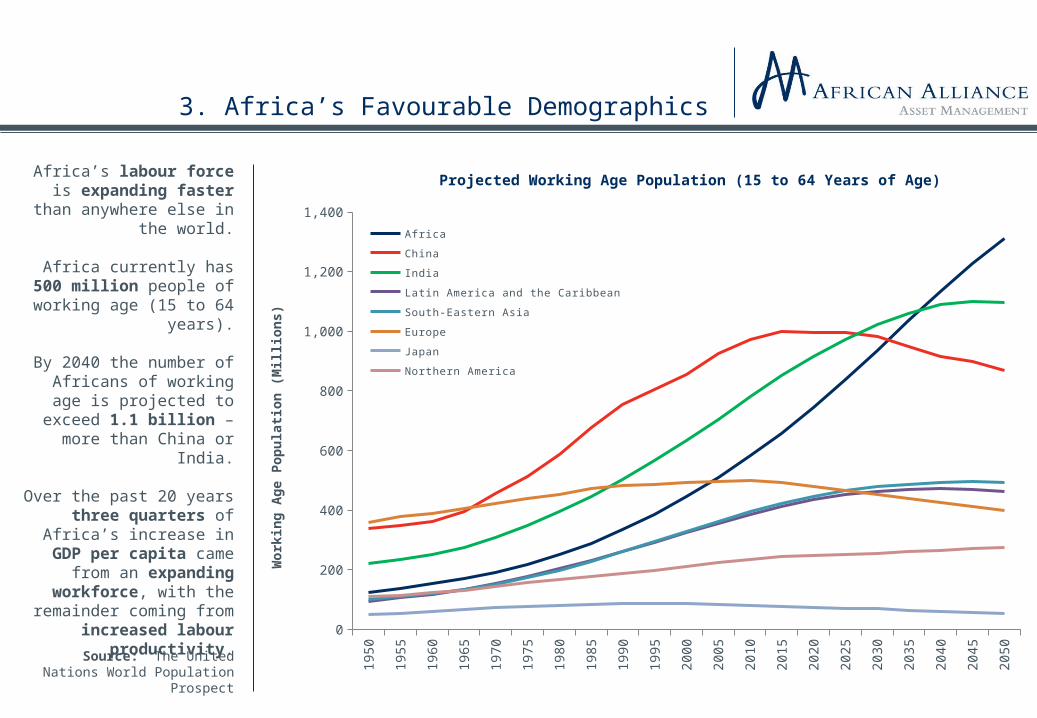

3. Africa’s Favourable Demographics

Africa’s labour force is expanding faster than

anywhere else in the world.

Africa currently has 500 million people of working

age (15 to 64 years).

By 2040 the number of Africans of working age is

projected to exceed 1.1 billion – more than China

or India.

Over the past 20 years three quarters of

Africa’s increase in GDP per capita came from an

expanding workforce, with the remainder

coming from increased labour productivity.

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

0

200

400

600

800

1,000

1,200

1,400

Projected Working Age Population (15 to 64 Years of Age)

Africa

China

India

Latin America and the Caribbean

South-Eastern Asia

Europe

Japan

Northern America

Work

ing A

ge P

opula

tion (

Millions)

Source: The United Nations World Population Prospect

4. Increasingly Diversified Growth

Economic growth has accelerated across the

African continent, in 27 of the 30 largest economies.

Africa’s growth story is only partly explained by the commodities boom.

During the period 2000-2008 natural resources accounted for just 24

percent of Africa’s GDP growth.

Labour productivity has increased by 2.7 percent

annually since 2000.

Africa’s growth surge is a result of improved

political and macroeconomic

stability coupled with microeconomic

reforms.

SectorSector Share of Change

in Real GDP (2002-2007) (%)1

CAGR(%)

Resources 24 7.1

Wholesale and retail 13 6.8

Agriculture 12 5.5

Transport and telecommunications 10 7.8

Manufacturing 9 4.6

Financial intermediation 6 8.0

Public administration 6 3.9

Construction 5 7.5

Real estate and business services 5 5.9

Tourism 2 8.7

Utilities 2 7.3

Other 6 6.9

1 100% = US$235 billion in 2005 dollars

Source: Global Insight, Arab Monetary Fund, African

Development Bank, McKinsey Global Institute

5. A Unique Business Opportunity

Africa’s economic growth is creating substantial

business opportunities for both local and global

companies.

Four categories of opportunities could be

worth US$2.6 trillion in annual revenues by 2020.

Consumer-facing sectors present the largest

opportunity, and are growing 2-3 times faster

than in OECD countries.

Africa’s projected 5 largest consumer markets in 2020

– Alexandria, Cairo, Cape Town, Johannesburg, and

Lagos – will each have more than US$25 billion

a year in household spending and be

comparable in size to Mumbai and New Delhi.

Industry GroupEstimated Annual Revenue (2020)

(US$ Billion)

Growth (2008-2020)

(US$ Billion)

Compounded Annual Growth

Rate(2008-2020)

(%)

Consumer 1,380 520 4%

Resources 540 110 2%

Agriculture 500 220 5%

Infrastructure 200 130 9%

Total 2,620 980 4%Source: McKinsey Global

Institute

6. The Rise of the African Urban Consumer

Increased urbanization and an expanding

labour force are leading to the rise of the middle-

class African consumer.

In 1980 just 28 percent of Africa’s population lived

in cities – today 40 percent of Africa’s 1

billion inhabitants do.

By 2030 Africa’s top 18 cities could have

combined spending power of US$1.3 trillion.

The number of African households earning

US$5000 or more – the level at which people start

spending roughly half their income on items

other than food – is projected to increase from

85 million today to 128 million by 2020. India Africa China Europe Latin America North America

3040 45

7379 82

7060 55

2721 18

Share of Rural vs. Urban Population by Region (2010) (%)

RuralUrban

Rura

l vs.

Urb

an P

opula

tion

India Africa China Europe Latin AmericaNorth

AmericaPopulation (Millions)

1,219 1,032 1,351 830 594 349

Cities With >1 Million

People48 52 109 52 63 48

Source: United Nations, McKinsey Global Institute

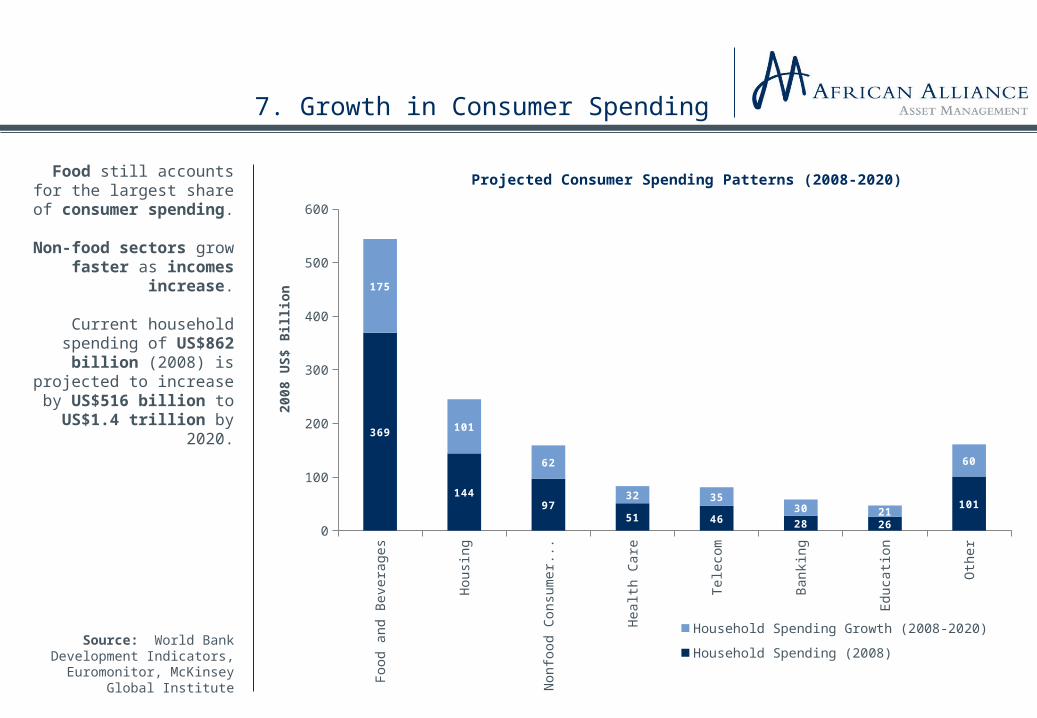

7. Growth in Consumer Spending

Food still accounts for the largest share of

consumer spending.

Non-food sectors grow faster as incomes

increase.

Current household spending of US$862

billion (2008) is projected to increase by US$516

billion to US$1.4 trillion by 2020.

Food a

nd B

evera

ges

Housi

ng

Nonfo

od C

onsu

mer

...

Healt

h C

are

Tele

com

Bankin

g

Educa

tion

Oth

er

0

100

200

300

400

500

600

369

14497

51 46 28 26

101

175

101

62

32 3530 21

60

Projected Consumer Spending Patterns (2008-2020)

Household Spending Growth (2008-2020)

Household Spending (2008)

2008 U

S$ B

illion

Source: World Bank Development Indicators,

Euromonitor, McKinsey Global Institute

8. Africa and the BRICs

BRIC-Africa trade as a proportion of World-Africa trade grew from 4.6% in

1993 to over 19% in 2008.

China-Africa trade increased from US$3.5 billion in 1990 to over

US$100 billion today – two-thirds of Africa’s

total BRIC trade.

In 2008 Africa ran a trade surplus of US$20.2

billion with the BRICs.

The proportion of BRIC-Africa trade held by Sub-

Saharan Africa has increased from 53% in 1980 to 77% in 2008.

Total BRIC-Africa trade is projected to exceed US$4 trillion by 2030, equal to 10% of BRIC-World trade and 45% of Africa-World

trade.

2000 2004 20080

20

40

60

80

100

120

140

160

180 BRIC-Africa Trade (US$ Billions)

China

India

Russia

Brazil

Brazil Russia India China-4

-2

0

2

4

6

8

10

12 Africa's Trade Balance With the BRICs (US$ Billions)1990

1996

2002

2008

Source: IMF, WTO, Standard Bank Group

9. Opportunity for Increased Intra-Regional Trade

Current trade between African countries remains low at just 12 percent of total imports and exports

– less than half the level in other emerging market

regions.

Half of Africa’s intra-regional trade occurs

within the Southern African Development

Community (SADC), in which South Africa trades

with its smaller neighbours.

Expanding Africa’s intra-regional trade could

provide a significant boost to regional growth.

West

ern

Euro

pe

Asi

a-P

aci

fic

East

ern

Euro

pe

Lati

n A

meri

ca

Afr

ica

Mid

dle

East

61

3931

2112 10

39

6169

7988 90

Share of Intra-Regional Trade By Region (%)

Extra-Regional

Intra-Regional

Source: IMF Direction of Trade Statistics, McKinsey Global

Institute

10. African Markets (ex South Africa) Have Been Ignored

Since global market lows in early 2009 African

markets (ex South Africa) have largely been

ignored by international investors.

While emerging markets in general have doubled

over this time period, Africa ex South Africa is

essentially flat.

This has occurred despite continued economic

growth and constantly improving business

fundamentals in these markets.

Source: Bloomberg, African Alliance

Dec

-08

Jan

-09

Feb

-09

Feb

-09

Mar

-09

Ap

r-0

9A

pr-

09

May

-09

Jun

-09

Jun

-09

Jul-0

9Ju

l-09

Au

g-0

9S

ep-0

9S

ep-0

9O

ct-0

9O

ct-0

9N

ov-0

9D

ec-0

9D

ec-0

9Ja

n-1

0Feb

-10

Feb

-10

Mar

-10

Ap

r-1

0A

pr-

10

May

-10

May

-10

Jun

-10

Jul-1

0Ju

l-10

Au

g-1

0A

ug

-10

Sep

-10

Oct

-10

Oct

-10

Nov

-10

Dec

-10

Dec

-10

Jan

-11

Jan

-11

Feb

-11

Mar

-11

Mar

-11

Ap

r-1

1M

ay-1

1M

ay-1

1Ju

n-1

1Ju

l-11

Jul-1

1

0

50

100

150

200

250 Selective Index Comparisons (US$ Returns)

Johannesburg All Share MSCI Emerging Markets MSCI EFM Africa ex SA

Index V

alu

e (

Rebased t

o 1

00)

Period Johannesburg All Share MSCI Emerging Markets MSCI EFM Africa ex SA

FY2009 64.1% 74.5% 3.1%

FY2010 30.1% 16.4% 14.3%

FY2011 YTD (July) -4.5% -1.2% -18.1%

Jan 2009 - Jul 2011 103.9% 100.6% -3.5%

Finally….Some On The Ground Observations

Regionalisation

Social change

Longer-term focus

Expatriate skills

Thank you!

Any questions?