Afghanistan Economic Update - World Banksiteresources.worldbank.org/.../AFGEconUpdate2011.pdf ·...

19

October 2011 Poverty Reduction, and Economic Management, South Asia Region The World Bank Afghanistan Economic Update

Transcript of Afghanistan Economic Update - World Banksiteresources.worldbank.org/.../AFGEconUpdate2011.pdf ·...

September 2011

Poverty Reduction, and Economic Management, South Asia Region

The World Bank

Afghanistan Economic Update

October 2011

Poverty Reduction, and Economic Management, South Asia Region

The World Bank

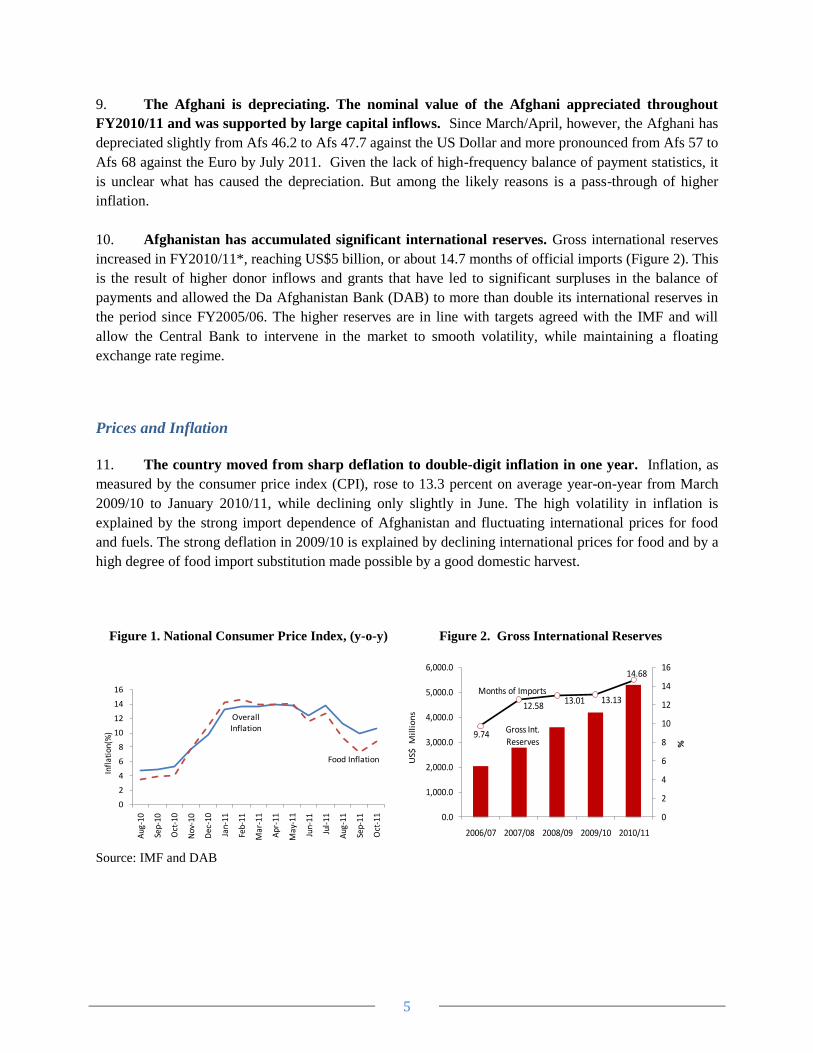

Afghanistan Economic Update

1

Afghanistan Economic Update October 2011

Overview1

Afghanistan’s economy is growing strongly. The growth drivers in recent years have been above-

average agricultural production, strong growth in construction and transportation, and security

spending enabled by large aid flows, especially in FY2009/10. Real GDP growth reached 8.4

percent in FY2010/11.

The Kabul Bank crisis has over-shadowed the dialogue between the Government and its

development partners in the last several months. Satisfactory resolution of Kabul Bank’s

problems is a critical condition for the IMF-supported Extended Credit Facility (ECF) and, the

lack of a resolution has had a negative impact on multi-donor assistance particularly through the

Afghanistan Reconstruction Trust Fund (ARTF). Lately, there has been progress on the

implementation of the resolution plan and indications are now very good for an agreement

between the Government and the IMF by October/November. This agreement, when reached,

will relieve much of the uncertainty regarding donor commitments in the coming period. Donors

have begun to fund again the ARTF investment window in the short-term and are expected to

return to more normal contributions once the agreement with the IMF is in place.

Afghanistan’s fiscal position is strengthening. In the last three years revenues grew by an

average of 34 percent p.a., thanks to improvements in customs and tax administration. Larger

increases are expected once mining operations begin in Aynak and Hajigak and with the

introduction of a value-added tax in FY2014/15. However, government expenditures will also

increase in the coming years due to higher security spending, the roll out of pay-and-grading

reforms for the civil service, rising recurrent obligations from large donor-supported projects

(including those financed outside of the core budget) and the fiscal costs of the Kabul Bank bail-

out.

The country moved from sharp deflation to double-digit inflation in one year. The strong inflation

trend is mainly explained by a increase for prices in food, electricity and fuels and reflect

international price trends, disruptions in trade flows with Iran and Pakistan over the past year as

well as a bad harvest in the 2Q2011 which limits the possibilities for food import substitution by

households.

Medium-term prospects are moderately good and will depend on the Government’s ability to

successfully manage the transfer of security control from international to national forces, and

ensure political stability and fiscal sustainability. Long-term growth prospects will depend on the

extent to which mining can be used to foster development in agriculture and services, which are

crucial to food security, employment and poverty-reduction, and export revenue.

1 This update was prepared by Claudia Nassif and Camilo Gomez Osorio with inputs from Amna Saeed,

Guillemette Jaffrin and Abdul Raouf Zia.

2

Recent Security Developments

1. The first phase of the handover of security responsibilities to Afghan national security

forces in six locations has been completed. The international forces under the International Security

Assistance Force (ISAF) handed over responsibilities for security in seven locations including Bamiyan,

Parwan, Herat city and province, Mehterlam city, Laskargar city, and Panjshir. The transfers are the first

phase of a plan that will place the country’s security under Afghan control in the next three years. All

international combat troops are scheduled to leave Afghanistan by the end of 2014.

2. Preparations are underway for a major international conference in Bonn on December 5,

2011. The conference will give prominence to the shift of security and development authority to the

Government of Afghanistan and commitment by the international community to stay engaged in support

of Afghanistan’s long-term development and security needs. The discussions will take place in a

challenging environment: the security situation remains extremely difficult and questions continue to be

raised about the readiness of the Government to take responsibility after 2014 for providing security and

governing the country, and lead donor countries are facing problems domestically with continued

economic assistance to Afghanistan.

Recent Economic Developments

Real Sector

3. Preliminary estimates suggest that Afghanistan’s GDP growth rate has dropped from a

very high and unsustainable 21.0 percent in FY2009/10 to 8.4 percent in FY2010/11*.2 Since

FY2003/04, the country has seen average growth rates in the double digits (9.1% on average), but with

high levels of volatility due to the prominence of the agriculture sector, which is subject to weather

fluctuations (Figure A). While last year’s GDP growth was exceptionally high due to a record harvest and

a large increase in on- and off-budget donor grants, preliminary data suggest that this year’s return to the

lower, but still strong, pre-FY2009/10 levels is due to the continued expansion of services.

4. On the supply side, the services sector continues to lead the way. In FY2010/11*, as in the

past five years, services accounted for about half of output (Figure B). The most dynamic services

subsectors were communications (65 percent annual growth), transport (23.1 percent) and finance &

insurance (14.3 percent) whereas wholesale and retail trade grew at only 5.3 percent. Services sector was

followed by agriculture which contributed 2.0 percentage points to GDP growth this year. The sector’s

output has been volatile because Afghanistan’s arable land and most irrigation systems depend heavily on

seasonal rain and snow. Overall, industry grew by 6.3 percent from last year. This was largely due to the

expanding mining sector which grew sharply by 43 percent. On the other hand, subsectors such as

construction and manufacturing which have larger contribution to GDP growth, showed modest annual

growth of 7.7 percent and 3.8 percent respectively.

5. On the demand side, private consumption has been fueling the growth of the Afghan

economy. In the past half-decade, on average it has contributed over 9 percentage points to real GDP

growth (excluding FY2008/09 – Figure C). Growth in the security economy underpins the demand for

2 The symbol * refers to initial estimates.

3

goods and services, equipment and operations and maintenance of the national army. Higher non-security

spending by donors is another factor, including their large off-budget contributions. In FY2010/11,

private consumption contributed 6.9 percentage points of the 8.4 percent real growth. Investment has

shown moderate growth over the years and contributing around 2.2 percentage points to GDP growth,

mostly from the external-budget capital spending and private investment in the security economy.

Government spending has contributed relatively little to GDP; just 2.8 percentage points. The

contribution of net exports was negative at – 3.6 percentage points.

6. Opium crop production decreased substantially in 2010, mainly due to a plant disease which

nearly halved crop production. However, this year, yields were back to around 45kg per hectare which

might raise opium production to 5,800 tons. Buoyed by higher speculative prices arising from volatile

security conditions, the farm gate income of opium farmers increased significantly. Estimates by UNODC

suggest that the farm gate value of opium will reach $1.4 billion in 2011 (8% of GDP). Farm gate

production accounts for roughly 20 percent of the opium value chain. About 78 percent of cultivation is

concentrated in southern provinces such as Helmand, Kandahar, Uruzgan and Day Kundi.

External Sector

7. The current account deficit narrowed in FY2010/11 because of an improving trade balance.

While overall trade has declined relative to GDP from 91 to 75 percent, mainly due to blockages at the

Pakistani border, imports fell more than exports (Figure D). Over the past 5 years imports (about $9.2

billion) have been three to four times the size of exports (about $2.8 billion). It should be noted, however,

that official export figures are underestimated and do not account for opium. Along these lines, the deficit

in the current account narrowed from 51.3 to 39.8 percent of GDP. Continued inflows of grants ensured

the financing of the current account deficit and a surplus in the capital and financial accounts of around 4

percent of GDP.

8. The implementation of the Afghanistan-Pakistan Transit Trade Agreement (APTTA)

continues to face difficulties. In October 2010, the countries concluded the APTTA negotiations aimed

at enabling Afghan goods greater access to the port of Karachi and the Wagah border with India (Indian

exports to Afghanistan are still excluded). This agreement is central for Afghanistan’s trade, as it aims to

take advantage of preferential tariffs with India scheduled over the next five years. However, substantial

differences between the Afghan and Pakistan governments regarding the interpretation of the agreement

have resulted in trade blockages over the first eight months since signing of the agreement at the Karachi

port. The areas of contention are bank guarantees, international requirements for sealed trucks, biometric

systems for customs verification and security, and the installation of tracking systems. A two-month

waiver given by Pakistan finally allowed the first Afghan trucks to travel across Pakistan on June 12th.

However, the waiver will expire in September and a final resolution has not yet been reached.

4

The Afghan Economy at a Glance

Strong, but volatile real GDP growth… … driven by the services sector and fluctuating agriculture output.

Figure A Figure B: Contribution to Real GDP Growth(%)

Source: IMF Source: IMF

Private consumption is the motor of growth

from donor inflows and the security economy... … but trade is declining,

Figure C Figure D

Source:IMF Source: IMF

… the current account deficit reduced, which is financed by donor grants. The Afghani is depreciating.

Figure E Figure F: Nominal Exchange Rates, to Afs (Index Mar,22, 2009=100)

Source: IMF Source:DAB

Note: The symbol * refers to initial estimates

Agricultural GDP Growth

Overall GDP

Growth

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

10.45.1

11.7

3.1

17.5

6.9

4.3

2.3

6.5

1.6

8.2

2.9

5.2

2.4

5.6

1.3

6.7

2.2

-8.7-4.3

-10.0-2.3

-11.4

-3.6

-15

-10

-5

0

5

10

15

20

25

30

35

2005/06 2006/07 2007/08 2008/09 2009/10 2010/11*

Pvt Consumption Govt. Consumption

Investment (Gross Dom. Fixed) Net Exports

Real GDP Growth

3.41.5

3.7

0.8

5.7

2.0

4.6

2.3

6.0

1.7

9.8

4.3

1.9

0.9

2.1

0.6

2.8

1.1

1.2

0.8

1.8

0.5

2.6

1.0

0

3

6

9

12

15

18

21

2005/06 2006/07 2007/08 2008/09 2009/10 2010/11*

Agriculture ServicesMining ManufacturingConstruction Industry - others

26%Exports, 21%

24%20% 18%

96%89%

Imports, 85%

71%

57%

0%

20%

40%

60%

80%

100%

120%

2006/07 2007/08 2008/09 2009/10 2010/11

f.o

.b in

% o

f GD

P

Capital and

Financial Account

Current account (excl. grants)

Overall Balance

Current account

(incl. grants)

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

2006/07 2007/08 2008/09 2009/10 2010/11

In %

of G

DP

Pakistani Rupee

Euro

Dollar

70

75

80

85

90

95

100

105

110

115

Apr

-09

Jun

-09

Au

g-0

9

Oct

-09

Dec

-09

Feb-

10

Ap

r-1

0

Jun

-10

Au

g-1

0

Oct

-10

Dec

-10

Feb-

11

Ap

r-1

1

Jun

-11

Aug

-11

Oct

-11

5

9. The Afghani is depreciating. The nominal value of the Afghani appreciated throughout

FY2010/11 and was supported by large capital inflows. Since March/April, however, the Afghani has

depreciated slightly from Afs 46.2 to Afs 47.7 against the US Dollar and more pronounced from Afs 57 to

Afs 68 against the Euro by July 2011. Given the lack of high-frequency balance of payment statistics, it

is unclear what has caused the depreciation. But among the likely reasons is a pass-through of higher

inflation.

10. Afghanistan has accumulated significant international reserves. Gross international reserves

increased in FY2010/11*, reaching US$5 billion, or about 14.7 months of official imports (Figure 2). This

is the result of higher donor inflows and grants that have led to significant surpluses in the balance of

payments and allowed the Da Afghanistan Bank (DAB) to more than double its international reserves in

the period since FY2005/06. The higher reserves are in line with targets agreed with the IMF and will

allow the Central Bank to intervene in the market to smooth volatility, while maintaining a floating

exchange rate regime.

Prices and Inflation

11. The country moved from sharp deflation to double-digit inflation in one year. Inflation, as

measured by the consumer price index (CPI), rose to 13.3 percent on average year-on-year from March

2009/10 to January 2010/11, while declining only slightly in June. The high volatility in inflation is

explained by the strong import dependence of Afghanistan and fluctuating international prices for food

and fuels. The strong deflation in 2009/10 is explained by declining international prices for food and by a

high degree of food import substitution made possible by a good domestic harvest.

Figure 1. National Consumer Price Index, (y-o-y)

Figure 2. Gross International Reserves

Source: IMF and DAB

Overall Inflation

Food Inflation

0

2

4

6

8

10

12

14

16

Aug

-10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-

11

Aug

-11

Sep-

11

Oct

-11

Infl

atio

n(%

) Gross Int. Reserves

9.74

12.5813.01 13.13

14.68

0

2

4

6

8

10

12

14

16

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

2006/07 2007/08 2008/09 2009/10 2010/11

%

US$

Mil

lio

ns

Months of Imports

6

12. Changes in food, electricity and fuel prices account for much of the increase in the CPI.

Food prices rose by 12.7 percent by July 2011 (y-o-y). On average households spend around 60 percent

of their income on food. Since Afghanistan is a net food importing country, high and fluctuating food

prices are related to higher international food prices. The price indices for electricity and fuel rose sharply

by 15.2 percent since July 2010 (year on year), partly due to the increase in international fuel and

petroleum prices and partly to the disruption oil imports from Iran. Food and fuel prices also reflect an

increase in the price of transportation (20.1 percent), due to the deteriorating security situation and delays

in the implementation of the Afghanistan-Pakistan Transit Trade Agreement.

Poverty

13. Estimates indicate that 36 percent of the Afghan population is poor, meaning that

approximately 9 million Afghans are unable to meet their minimum basic needs4. Based on the National

Risk and Vulnerability Assessment (NRVA, 2007/08) data, a recent poverty assessment suggests figures

are even higher for vulnerable groups, such as the Kuchis, at 54 percent poor. Similarly, a large share of

the population is vulnerable to negative shocks (over half of the population consumes at less than 20

3 D’Souza and Jolliffe 2010, “Price Shocks, Food Security, and Coping Mechanisms: Household Evidence from Afghanistan,”

(forthcoming). 4 World Bank and Ministry of Economy 2010, Poverty Status in Afghanistan.

Box 1: Food Crisis Update

In a typical year, Afghanistan's total wheat production comes 2/3 from irrigated land and 1/3 from rain-fed areas.

This year's rain-fed harvest, however, was limited with average losses of around 80 percent of output in 14 of the

wheat growing provinces due to drought conditions during the months of April to June. The irrigated wheat

production also declined by about 8-9 percent because of the lower snow levels in the winter of 2011. As a result,

2011 recorded a wheat harvest 25 percent below that of last year and 12 percent below the decade’s average –

leading to flour prices generally 44 percent higher.

The gap between domestic supply and the demand for wheat will be about 1.7 million tons this year, which roughly

doubles the long-term average gap. As always, most it will be served by private sector imports that may not reach

all areas. International prices of wheat remain substantially high and at around 70 percent above last year's prices.

Persistent high food prices pose a risk to groups vulnerable to poverty. If the increase in August 2010 food prices is

sustained, many Afghan households would be at risk of falling into poverty. Preliminary estimates suggest that a

one percent rise in the flour price translates to a 0.21 percent decline in real monthly per-capita food consumption.3

To illustrate the potential effect of such price changes on poverty, a 10 percent increase in wheat prices would push

an additional 377,000 Afghans or 1.3 percent of the population into poverty. This estimation is based on how

households in the NRVA 2007/08 reduced their consumption in response to the food-price shocks of 2008.

Moreover, the data suggests that households trade off quality for quantity as they move towards staple foods and

away from nutrient-rich foods, such as meat and vegetables (given the smaller price elasticity in calorie intake than

in food consumption). Bread and cereals comprise an important share of the poorer households’ consumption

basket, and price volatility directly affects their purchasing power.

WFP and the Ministry of Agriculture, Irrigation and Livestock (MAIL) estimate that the drought might increase the

number of food insecure people by another 2.9 million persons (or about 0.5 million households). The Government,

supported by donors, is planning to increase distribution of food, seed and cattle feed in the drought affected areas.

7

percent above the poverty line). In addition, the mapping of poverty throughout the country shows the

striking finding that the most poverty-afflicted areas are not those in conflict.

Public Finances

Revenue

14. Revenue collection continues growing

strongly by over 20 percent per year. The 2010/11

fiscal year closed with collections at an all time high

of US$ 1.7 billion (10 percent of GDP), exceeding the

IMF target of 9.2 percent of GDP. This is remarkable,

as revenue collection stood at a meager 3 percent of

GDP before 2002/03. Behind these successful

collection efforts is the high growth of tax and

customs duties, which are the drivers of revenue.

During the first quarter of 2011/12, both tax

collection and non tax revenue reached US$490

million (Afs 23.03 billion) and represented 24 percent

of the annual revenue collection target. In

comparison to the same quarter last year, revenues

increased by around 31 percent.5

15. Taxes, especially customs duties, are

driving domestic revenues. Tax collection in

2010/11 grew by 29 percent over those of the previous year. The sales tax (the 2 percent BRT on imports

and the 10 percent BRT on services) was the largest component, reaching an estimated US$347 million;

the income tax (mostly on wages) generated around US$219 million, and fixed taxes (imports by licensed

businesses) were US$193 million. The share of customs revenues rose to 36 percent of total revenues

this year and its collection grew by 27 percent. Overall, more than half of the resources from customs are

attributed to duties on motor vehicles and parts, and fuel imports. In the first quarter of 2011, customs

revenues reached US 266 million (Afs 12.483 billion), which was slightly below its quarterly target (or 11

percent lower than expected.), but still a 16 percent increase over the same quarter last year. Overall,

collection in Q1 closed around 31 percent higher than the same quarter last year and overall collection is

projected to close the year at US$ 2.07 billion (Afs 97.4 billion).

Expenditures

16. The operating budget increased by 26 percent in 2011/12 and the development budget was

cut by a third to approve a more realistic figure. The total core budget for 2011/12 is US$ 4.78 billion

(Afs 224.781 B), of which the operating budget is US$ 3.2 billion (Afs 150.726 billion).

5 Fiscal Bulletin Q1, MOF

Figure 3: Breakdown of Customs Revenue,

2010/11

Source: MOF, Fiscal Bulletin

Motor

vehicles, parts 28%

Minerals

fuels, oils 24%

Milling

products, malt

starch, wheat

gluten 5%

Electric

machinery, equipment

5%

Iron & Steel 5%

Salt, sulfur,

stone 3%

Machinery, mechanical appliances

2%

Beverages,

spirits, vinegar 2%

Other 26%

8

17. Since operating expenditures are growing faster than revenues, fiscal sustainability remains

a challenge. Over the coming years (2015/16 and beyond), there will be large liabilities for recurrent

expenditures arising from: i) increases in the security wage bill in order to recruit and train 352,000

national security troops; ii) the rolling out of the pay & grading reforms and the hiring of new teachers;

and iii) the operation and maintenance costs of assets constructed through development budget spending,

as well as those funded by donors through the external budget. As a result of such needs, domestic

revenues will not be sufficient to cover operational expenditures in the coming years.6 Estimates suggest

that by 2012/13, operational spending will increase to 20 percent of GDP, while revenue collection will

stand at 12 percent of GDP, providing just 60 percent coverage of the operating budget (Figure 5).

18. The largest component of the operational budget in 2010/11 was wages & salaries, which

accounted for 75 percent. (Figure 4) The security wage bill alone represented about two thirds of the

operating budget and 7 percent of GDP. Donors paid 68 percent of last year’s security wage bill.7 A

significant portion of the non security salaries (23 percent) was covered through the Recurrent Cost

window of the Afghanistan Reconstruction Trust Fund (ARTF). The second largest expense was

operations & maintenance, and accounted for 19 percent of operational spending, and 2 percent of GDP

for 2010/11. Finally, a remaining 2 percent of GDP consisted of a combination of pensions, transfers,

capital spending, and interest payments.

6 Fiscal sustainability here refers to a narrow concept of the ability to meet operational expenditures from domestic

revenues. However, its standard definition refers to a country’s fiscal balance in a steady state, the ratio of total

public debt and debt servicing to macroeconomic aggregates like GDP, not increasing over time. 7 Contributions are paid into two trust funds, the Combined Security Transition Command CSTC-A at roughly US$

287 million and the Law and Order Trust Fund for Afghanistan (LOTFA) at US$520 million. Source: Fiscal

Bulleting Q4 1389, MOF.

Figure 4. Core Budget Development Figure 5. Fiscal Sustainability Ratio and Operating

Expenditures

Security Wages

Civil Service Wages

O&M

Others

Development

0%

5%

10%

15%

20%

25%

30%

2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

% o

f G

DP

Domestic Revenues

12%

Core Operating Expenditures

20%

38%

Fiscal Sustainability

Ratio

72%

59%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0%

5%

10%

15%

20%

25%

% o

f G

DP

9

19. The Afghan budget continues to rely heavily on external financing. In 2010, of the roughly

US$16.9 billion in total public spending, only US$3.3 billion were channeled through the “core” budget

and was under the control of the government’s PFM systems. In 2011/12, domestic revenues are

budgeted to cover 72 percent of operations and 48 percent of the total core budget, while the remainder

was covered by donor grants, which already account for the bulk of the development spending (or 85

percent of the total development budget).

Figure 6. Public Spending – Core and External Budget 2010/11 (in US$ million)

8

Source: MOF, WB Staff calculations

20. The low rate of execution of the development budget raises concerns about absorptive

capacity. Over the past three years, the Afghan government has only executed about 40 percent of the

development budget (roughly US$ 950 million). Behind these trends are both structural and capacity

issues, as well as an unrealistic budget formulation mechanism. For instance, the budget sometimes

reflects projects for which donor funding has not been fully secured. Projects that are yet to be

implemented or have been stopped are not formally dropped and carried over to the next fiscal year. As a

result, the unspent funds continue to inflate the denominator in the calculation of budget execution. For

2010/11 the size of the carryover accounted for 60 percent of the core development funds. Low execution

rates could undermine the Government’s objective, formulated at the Kabul Conference, to “channel at

least 50 percent of the development aid through the Afghan core budget within two years”.

8 Figures represent actual development budget disbursements, 40 % budget execution rate. The external budget at

US$ 13.6 billion was reported as donor disbursements to World Bank excluding on-budget contributions to the

ARTF, CSTCA and LOTFA trust funds.

Security

$8.6 billion

Non -Security

$ 5.2

billion

10

Figure 7: Core Budget by Sectors, 2011/12

Source: MOF, WB Staff calculations

21. Security spending, mostly salaries, dominates the total core budget in 2010/11. A closer look

at core budget allocations, both operations and development, shows that 40 percent of the on-budget

spending was allocated to security. This share will grow over the coming year when the ANSF will reach

its 352,000 troops target. About a third of the 2010/11 budget was allocated to education (15 percent),

infrastructure, (14 percent) and health (4 percent). The agriculture and rural development sector received

a 9 percent share of the core budget, much of it allocated to the National Solidarity Program.

22. Delays in direct donor contributions resulted in a tight cash position. In response to the

prolonged negotiations over a new IMF supported program, donors withheld their direct budget

contributions. In the case of the ARTF trust fund, this represented a gap of US$ 270 million (US$ 200

million for recurrent expenditure). Other than domestic revenues, these are the only resources over which

the MOF has discretion to finance its deficit. As a way to maintain its cash position until the issue was

resolved, the government under-spent on operations and maintenance throughout 2010/11. However, new

budget estimates suggest that, in the absence of further donor contributions to the operating budget, the

cash balance would fallen to below a month of operating expenditures by early January 2012.

23. The fiscal year 2010/11 has also seen progress with wider public financial management

reform. The Afghanistan Financial Management Information System (AFMIS) is now connecting all

line Ministries and all 34 Provinces. Coverage of the Verified Payroll Program was extended to over

562,000 civil servants, of which 380,000 are currently receiving salaries through direct deposit in their

bank accounts. Finally, the monthly financial statements have been made timely available on the

treasury’s website. Procurement reform also continue to make progress: bidding opportunities and

outcomes of awarded contracts by line ministries are now made publicly available on the website of the

Security39%

Governance6%

Infrastructure14%

Education15%

Health4%

Agriculture & Rural Dev

9%

Social Protection

1%

Economic Governance & Private Sector

4% Contingency8%

11

Public Procurement Unit (PPU). The system is also able to accept data on awarded contracts as well as

bidding opportunities.

Private Sector Development

Investment Climate

24. Given the security situation, doing Business in Afghanistan is more difficult than in other

South Asian countries. The World Bank’s Doing Business Index 2011 ranked Afghanistan lowest in the

region and 167th out of 183 countries surveyed. At a firm-level, Afghan businesses are restrained by red

tape, lack of policy predictability, and corruption. Afghanistan’s regulatory framework is relatively well

ranked on two indicators – Starting a Business (25th) and Paying Taxes (53th). However, it is ranked last

(183th) on three indicators--Protecting Investors, Trading across Borders and Closing a Business (see

table below). In order to address and enhance Afghanistan’s business environment the Ministry of

Commerce and Industries launched an initiative in December 2010 aimed at making improvements in

these areas.9

Figure 9: Doing Business Indicators 2011, Regional Comparison

Source: World Bank, Doing Business 2011

9 The Doing Business survey focuses on regulatory constraints. There are other, and clearly dominant constraints to

the development of the private sector, such as limited access to infrastructure, and security conditions, which ranked

highly in the Investment Climate Assessment (2008).

12

Financial Sector

25. One year later, financial sector development is still clouded by the implications of the Kabul

Bank crisis. The crisis highlighted the limited capacity of the Central Bank to effectively supervise the

banking sector and enforce regulations. The IMF is therefore discussing with the authorities a satisfactory

resolution of the problem as a critical threshold for the establishment of an Extended Credit Facility. As

of October 2011, no final agreement on a new program was reached, however, progress on the

implementation of the resolution plan moved considerably and recent developments suggest there could

be a program in place over the coming months. Donors have begun to fund again the ARTF investment

window in the short-term and are expected to return to more normal contributions once the agreement

with the IMF is in place.

26. Measures to strengthen the health of the financial sector are underway. The Afghan

authorities have been in intensive discussions with the international community on priority steps to

stabilize the banking sector and lay foundations for a broad banking sector reform. The key short term

priorities are: (i) resolving the Kabul Bank issues and (ii) strengthening banking supervision to re-

establish confidence in the health of the banking sector and avoid similar crises in the future. In this

context, the IMF is providing technical assistance on the resolution of Kabul Bank’s problems. The UK

Department for International Development (DFID) and the World Bank are financing audits across the

banking system. USAID is providing renewed support to the Central Bank via its new Financial Access

for Investing in the Development of Afghanistan (FAIDA) project, notably on mobile banking. As part of

the World Bank Financial Sector Rapid Response Project, approved in August 2011, measures will be

taken to modernize the national payment system which is currently dominated by Kabul Bank.

Natural Resources

27. Hajigak tender enters evaluation stage. The start of mining-related construction at Hajigak

was delayed by the decision to re-launch the tender for the exploration concessions last year in order to

ensure a larger response from international investors. This resulted in strong international interest. The

bids for the tender were opened in September and include six bids from Indian, Iranian and Canadian

companies. It is expected that the contract will be awarded by the end of this year. The mining project at

Hajigak is, by a wide margin, one of the largest investments in the country’s history and will – together

with the large copper mine located in Aynak - play a leading role in the economy in years to come.

Current projections estimate that the two mines could generate up to US$342 million annually in

government revenue until 2015, and up to US$704 million annually in 2016 and beyond. In the medium

term the mining sector could contribute up to 5 percent of annual growth. However, large investments

(US$6-US$15billion) in mining and infrastructure development are needed in the coming years to exploit

the sector’s potential.

28. The extractive industry sector is attracting increasing investments in oil and gold. In the past

nine months, Afghanistan has awarded two contracts for oil extraction in the northern Amu Darya basin.

Reserves are estimated to be a relatively modest 80m barrels. However, the nearby Afghan-Tajik basin is

estimated to hold around 1.5bn barrels of crude oil. Developing these oilfields would help to generate tax

13

revenue and would also help Afghanistan reduce its reliance on foreign fuel. If the six-month pilot is

successful, the Government would extend extraction at the Angot site and permit drilling in four other

fields that could generate US$50m in annual revenue for the government. Earlier this year, the

government signed an agreement with Afghan Krystal Natural Resources, allowing the company to invest

US$50m in Afghanistan's second gold mine, Qara Zaghan. Afghanistan is estimated to have US$25

billion worth of gold deposits. Production is planned to begin in 2013, provided the government can

satisfy the high security needs around the mine.

Infrastructure

29. Afghanistan’s telecommunications industry is growing rapidly. By early 2010, the number of

mobile telephone subscriptions was estimated to be about 13 million with the networks covering about 60

percent of the population. Subscriptions are projected to reach 19 million by end- 2011, of which private

firms will account for 99.2 percent.10

More than half of Afghan households have at least one mobile

telephone. Thus, the private-sector led telecommunications revolution in Afghanistan has been one of the

country’s success stories. At the same time, only 5 percent of the population is believed to use the

internet, with services limited to major urban areas such as: Kabul, Herat, and Mazar-e-Sharif.

30. Freight services have started on Afghanistan’s first major railway. Under a three-year

agreement, Uzbekistan’s national railway company (UTY) is operating the 75 km long gauge line, which

was built at a cost of US$165m and supported by the Asian Development Bank. The line starts at the

Hairatan freight terminal on the Afghan side of the Uzbek border, which handles around half of

Afghanistan’s imports, and ends at a site near Mazar-e-Sharif airport. The freight service is expected to

increase traffic through the Hairatan terminal, which has reached full capacity (4,000 tons of cargo a

month); however, the flow of goods from Central Asia to Afghanistan is projected to rise to 25,000-

40,000 tons a month over the next few years. At a later stage, the railway network will be extended to

Herat in the west and Tajikistan in the east. The railway will primarily service commercial and civilian

cargo.

Economic Growth in the Medium and Long-Term

31. Real GDP growth might slow down in 2011/12, reaching levels lower than the initially

projected 8 percent. The drought between April and June will affect agriculture output which is likely to

be 25% lower than last year’s production. Services will continue to provide much of the growth in the

year, benefiting from higher government and donor spending, and private investments in the mining

sector. The mining sector is expected to grow vigorously, as the construction phase of the Aynak copper

mine intensifies.

32. Stability, continued reform and external aid will determine the success of the transition and

medium-to-long term growth prospects. The transition is likely to be characterized by a slowdown in

economic growth. While more detailed analysis is currently underway, it is reasonable to expect that

Afghanistan will revert to a lower growth trajectory (compared to the recent 10 percent per year).

10 Forecast of Wireless Intelligence, based on data up to Q1 2010.

14

Medium-term growth performance will vary with the speed of the decline in civilian and military aid and

efforts to make aid more effective, for example by concentrating investments in areas that promise high

economic returns and employment opportunities, or by redirecting more funding to local contractors.

33. Afghanistan has substantial untapped mineral deposits, which have the potential to make it

a major exporter. Preliminary analysis suggests that Afghanistan’s combined revenue could reach an

average US$208 million per year over 2011-15. Conservative projections suggest that mining would

increase fiscal revenues annually by 19 percent, and add over 1.1 percent of GDP per year. In more

expansive scenarios, the figures could rise to US$364 million annually. The direct employment effect

could be relatively small but, assuming a reasonable development path, the public service and private

industry sectors could create more than 165,000 additional jobs through up- and down-stream linkages.

34. Development of the mining sector and creation of resource corridors could stimulate rural

development. With appropriate sector policies, mining development would provide benefits in the form

of royalties to the public budget, direct employment and increased private-sector growth, mainly from

backward and forward linkages. However, international experience has shown that even in the best-

performing countries, significant challenges arise from resource-based growth:

Natural resource wealth raises average income, but benefits to the population in general, and

local communities in particular, are not automatic and can only be achieved if appropriate

policies are adopted.

An overreliance on natural resources could make the country more susceptible to external

market fluctuations or erode the competitiveness of other (emerging) tradable sectors as a

result of appreciation of the real exchange rate.

35. The development of a strong and dynamic agriculture sector holds promise for improving

the quality of future growth. Agriculture is by far the largest employer, with approximately 70 percent

of Afghans involved. There is, however, much that can be done to improve the sector’s productivity,

particularly after the losses incurred from years of conflict. In the last 40 years Afghanistan’s agricultural

production has declined, while that of its neighbors, Iran and Pakistan, has increased five-fold. Less than

half of available water is used and only one-third of the 7.5 million hectares available for agriculture are

irrigated. The government has articulated well the agenda for improving farm productivity; the challenge

is implementation. Closely linked is the development of agribusiness that could stimulate downstream

and upstream linkages that foster growth.

36. Mining and agricultural development will not be able to take place without the

simultaneous development of supporting services. The competiveness of both mining and agriculture

depends critically on the provision of low-cost supply-chain services – particularly transportation,

logistics, electricity and irrigation – none of which are currently available in the required quantity or

quality. The challenge in promoting enabling services for mining development lies in the size of the

investments (e.g., railways). The difficulty in agriculture and agribusiness development lies in solving the

complex coordination problems found in modern supply-chain services that must move goods from

production to markets without major post-harvest losses.

15

37. The transition process will pose significant challenges to maintaining fiscal sustainability.

Domestic revenues are expected to grow as the mining sector develops and tax revenues become stronger

with improvements in tax administration and the introduction of VAT in 2014. However, operating

expenditure will grow faster while external support will declines during the transition years and a

revenues from mining activities will only begin to build. In particular, the sustainability of the operating

budget will be pressured by the military transition and pay-and-grading reform, the resolution of Kabul

Bank problems, integrating externally funded technical assistance into the formal civil service system,

and the need for large increases in spending for operations and maintenance. Finally, the implementation

of some of the 22 National Priority Programs will require additional resources, as the bulk of programs

have not secured funding.

38. Financing additional operations and maintenance (O&M) requirements, which are

currently underfunded, will become the main source of fiscal tension. The handover of donor- and

military-funded assets will add significant recurrent liabilities to the government budget if they are to be

maintained. In this context, relatively little is known about the large assets created by the Provincial

Reconstruction Teams (PRT) and other off-budget donor funding. Much of the US Department of

Defense’s Commander’s Emergency Response Program (CERP) budget is spent on development through

either the PRT or directly by the various US regional commands. This has considerably increased the

amount of money available for development at the sub-national level. However, it is questionable if all of

these developments can be sustained by the government in the future.

16

World Bank Assistance to Afghanistan Overview

39. World Bank assistance comprises a portfolio of International Development Association (IDA)

grants and credits as well as the projects it supervises on behalf of the ARTF. Since 2002, IDA has

committed a total of US$2.3 billion in grants (80 percent) and credits (20 percent) in Afghanistan. Thirty-

six development and emergency-reconstruction projects and four budget-support operations have been

committed to date. In addition, the ARTF has committed US$2.3 billion for recurrent costs of government

and US$1.8 billion in ARTF investments in national government programs. At end-August 2011 the

active IDA portfolio was worth US$1.1 billion and the active ARTF investment portfolio was worth

US$899 million.

New Financing in FY2009/10 and FY2010/11

40. In FY2009/10, IDA approved six new grants worth US$197 million. These included US$7.5

million for the Pension Reform Project, US$30 million for the Afghanistan Rural Enterprise Development

Program (AREDP), US$50 million for the Customs Reform and Trade Facilitation project, and US$40

million for the third phase of the National Solidarity Program (NSP III). In addition, the crisis response

window of IDA was utilized to provide an extra US$69 million to critical human development

investments in Afghanistan, including the Strengthening Higher Education Project (SHEP) and the

Strengthening Healthcare for the Rural Poor Project (SHARP). In addition, the ARTF approved US$290

million in recurrent-cost financing (of which US$63.8 million was based on meeting the benchmarks of

the ARTF Incentive Program 1389) and US$196 million for investments, including NSP III, the National

Emergency Rural Access Project (NRAP), SHARP, and the Horticulture and Livestock Project.

41. During FY2010/11, five projects were approved by the World Bank board totaling $261.8

million, ensuring that the full IDA 15 allocation was utilized by the government. The new projects include

the US$40 million additional financing for the National Emergency Rural Access Project (NERAP), the

Sustainable Development of Natural Resources additional financing (US$52m), the ICT Sector

Development Project (US$50m), the Afghanistan New Market Development Program (US$22m), and the

Irrigation Restoration and Development project (US$97.8m). Under the ARTF, new investment financing

of US$554 million was committed in FY 2011/11, of which the substantial part was for co-financing of

the core IDA-financed national programs such as NSP, EQUIP and NRAP, as well as new investments in

agriculture and infrastructure.

17

Selected Macroeconomic Indicators, 1381 - 1389

Million of Afs, nominal unless stated otherwise

actuals estimated

1381 1382 1383 1384 1385 1386 1387 1388 1389 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

Real Sector

Nominal GDP 185,471 224,696 252,597 311,436 352,308 435,692 533,522 615,082 729,905

GDP (in million US$) 4,142 4,584 5,280 6,272 7,058 8,746 10,471 12,481 15,928

Real GDP (base 2002/03) 185,470 201,132 203,255 225,969 238,520 271,293 281,090 340,176 368,868

Agriculture 70,365 72,335 56,249 66,205 62,823 72,055 61,307 88,627 82,979

Industry 43,373 47,830 56,186 63,485 72,162 77,670 82,130 87,146 92,614

Services 69,162 76,338 85,056 89,656 96,102 114,644 130,484 152,989 180,703

Real GDP growth (%) n.a. 8.4 1.1 11.2 5.6 13.7 3.6 21.0 8.4

GDP per capita 8,135 9,441 10,215 12,122 13,198 15,897 18,810 21,013 24,186

Money and Prices

CPI inflation (average, %) 5.1 24.1 13.2 12.3 5.1 13.0 26.8 -13.2 13.7

Broad money (M2) n.a. n.a. n.a. n.a. n.a. 91,300 119,600 162,500 226,400

Investment and Saving

Gross Domestic Investment 63,096 87,137 119,214 143,627 153,781 176,800 194,232 194,832 191,687

o/w: private 13,659 18,175 24,251 30,957 28,916 37,340 47,869 53,679 61,770

Gross Domestic Savings 56,386 50,077 107,431 135,299 134,125 182,497 198,942 177,720 203,859

o/w: private n.a. -12,089 15,983 19,273 20,164 53,359 74,549 46,125 67,312

Government finance

Domestic Revenue 5,864 10,168 12,812 20,652 28,819 33,579 41,390 63,531 80,384

o/w: tax revenue n.a. 5,176 9,378 14,035 21,893 24,994 28,777 51,532 64,389

Operating Grants 9,430 11,717 14,214 16,878 19,214 23,207 29,507 32,768 54,500

Development Grants n.a. 4,104 12,793 18,292 16,625 33,416 22,733 30,089 26,200

Total Core Expenditure

15,514 30,054 46,039 54,222 78,628 95,770 115,888 135,051 155,098

Operating 15,514 21,972 26,605 31,979 43,448 50,727 69,824 88,072 110,453

Rule of law 1,170 1,595 1,441 3,274 4,291 4,330 14,498 18,287 22,934

Security 6,874 11,745 10,633 14,683 18,843 22,613 30,257 38,165 47,863

Health 940 1,062 1,108 1,222 1,323 1,418 1,473 1,857 2,329

Education 2,490 4,261 6,084 7,344 9,350 9,209 12,795 16,139 20,240

Others 4,040 3,308 7,339 5,457 9,641 13,157 10,801 13,624 17,086

Development n.a. 8,082 19,434 22,243 35,180 45,043 46,065 46,979 44,645

Rule of law n.a. 28 233 436 784 1,254 885 1,365 1,891

Security n.a. 1,045 823 1,367 1,411 1,193 672 1,010 419

Health n.a. 171 1,076 993 2,036 2,593 3,259 3,740 3,143

Education n.a. 177 406 1,217 1,699 4,317 4,149 5,519 5,264

Others n.a. 6,661 16,896 18,231 29,251 35,685 37,101 35,344 33,930

Operating balance -9,650 -11,804 -13,793 -11,327 -14,629 -17,148 -28,434 -24,541 -30,069 Operating balance

(incl. grants) -220 -86 421 5,551 4,585 6,059 1,073 8,227 24,432 Overal Core balance

(excl. grants) -9,650 -19,886 -33,227 -33,570 -49,809 -49,809 -74,498 -71,520 -74,713

Fiscal sustainability ratio (Domestic revenues/

operating exp) 37.8 46.3 48.2 64.6 66.3 66.2 59.3 72.1 72.8

18

External Sector

Current account (incl. grants) -149.8 -756.1 -246.3 -167.7 -393.8 114.4 92.4 -347.2 265.7 Exports FOB (in million US$) 1/ 1,290.6 1,893.6 1,643.0 1,795.0 1,820.0 1,853.5 2,465.0 2,517.2 2,836.3

Imports FOB(in million US$) 2,508.2 4,379.3 5,086.3 6,130.4 6,741.9 7,793.8 8,944.7 8,871.6 9,139.0 Gross reserves

(in million US$) 425 822 1,309 1,661.9 2,039.5 2,784.3 3,591.2 4,208.5 5,321.1

Gross reserves (months of imports GNFS) 2.8 4.9 6.8 7.8 9.7 12.6 13.0 13.1 14.7

Current account balance

(incl. grants, % of GDP) -3.6 -16.5 -4.7 -2.7 -5.6 1.3 0.9 -2.8 1.7

Current account balance (excl. grants, % of GDP) -31.9 -64.1 -67.5 -72.2 -71.1 -68.1 -59.6 -51.3 -39.8

Total External debt

Total debt stock(in million

US$) 539 640 763 11,939 11,971 2,012 2,061 1,147 1,280

Debt-to-GDP Ratio (%) 13.0 14.0 14.5 190.4 169.6 23.0 19.7 9.2 8.0

Memorandum items

Population (in millions) 22.80 23.80 24.73 25.69 26.69 27.41 28.36 29.27 30.18 Exchange rate, average

(Afs/US$) 45 49 48 50 50 50 51 49 47

Source: MOF, IMF, and WB staff calculations

1/ Excludes opium exports and transit trade and includes official recorded exports, estimates of smuggling, reexports and sales to

nonresidents.