Affordable Care Act Marketplace Implementation Briefing PA Refugee Resettlement Program Annual...

22

Affordable Care Act Affordable Care Act Marketplace Implementation Briefing Marketplace Implementation Briefing PA Refugee Resettlement Program Annual PA Refugee Resettlement Program Annual Meeting Meeting June 11, 2013 June 11, 2013 HEALTHCARE.GOV Aryanna Abouzari, Esq. Aryanna Abouzari, Esq. Executive Officer Executive Officer U.S. Department of Health & Human U.S. Department of Health & Human Services, Region III Services, Region III Pennsylvania, Delaware, District of Pennsylvania, Delaware, District of Columbia, Maryland, Virginia, West Columbia, Maryland, Virginia, West Virginia Virginia

-

Upload

lilian-hutchinson -

Category

Documents

-

view

216 -

download

2

Transcript of Affordable Care Act Marketplace Implementation Briefing PA Refugee Resettlement Program Annual...

Affordable Care ActAffordable Care ActMarketplace Implementation Briefing Marketplace Implementation Briefing

PA Refugee Resettlement Program PA Refugee Resettlement Program Annual MeetingAnnual Meeting

June 11, 2013June 11, 2013

HEALTHCARE.GOV

Aryanna Abouzari, Esq.Aryanna Abouzari, Esq.Executive OfficerExecutive Officer

U.S. Department of Health & Human U.S. Department of Health & Human Services, Region III Services, Region III

Pennsylvania, Delaware, District of Columbia, Pennsylvania, Delaware, District of Columbia, Maryland, Virginia, West VirginiaMaryland, Virginia, West Virginia

Critical Need for Health ReformCritical Need for Health Reform

48.6 million uninsured Americans 48.6 million uninsured Americans

$3 trillion spent annually on healthcare$3 trillion spent annually on healthcare

17.9 % of our economic output tied up 17.9 % of our economic output tied up in the health care system in the health care system

Without reform, by 2040, 1/3 of Without reform, by 2040, 1/3 of economic output tied up in health careeconomic output tied up in health care

Affordable Care Act OverviewAffordable Care Act Overview Creates Consumer ProtectionsCreates Consumer Protections

Prevents denials of coverage for pre-existing Prevents denials of coverage for pre-existing conditionsconditions

Make health insurance more affordable for Make health insurance more affordable for middle class families and small businesses middle class families and small businesses with tax creditswith tax credits

Expands access to care through Marketplaces Expands access to care through Marketplaces and Medicaid expansionand Medicaid expansion

Health Insurance MarketplaceHealth Insurance Marketplace

Sometimes called “Exchanges,” the Sometimes called “Exchanges,” the Marketplace is required by the ACA to be Marketplace is required by the ACA to be created by January 1, 2014created by January 1, 2014

New “marketplace” where small businesses and New “marketplace” where small businesses and individuals can select and enroll in a private individuals can select and enroll in a private health insurance plan health insurance plan

Consumers will have Consumers will have • the same level of benefits and coverage the same level of benefits and coverage

available to members of Congressavailable to members of Congress• more choice and selection in health plansmore choice and selection in health plans

Three models availableThree models available State-BasedState-Based Federal-State PartnershipFederal-State Partnership Federally-FacilitatedFederally-Facilitated

States can apply for Marketplace States can apply for Marketplace establishment funding at any time and be establishment funding at any time and be awarded grants through 2014 awarded grants through 2014

HHS to operate marketplaces for States HHS to operate marketplaces for States that have not elected to do so that have not elected to do so

Marketplace Implementation Marketplace Implementation

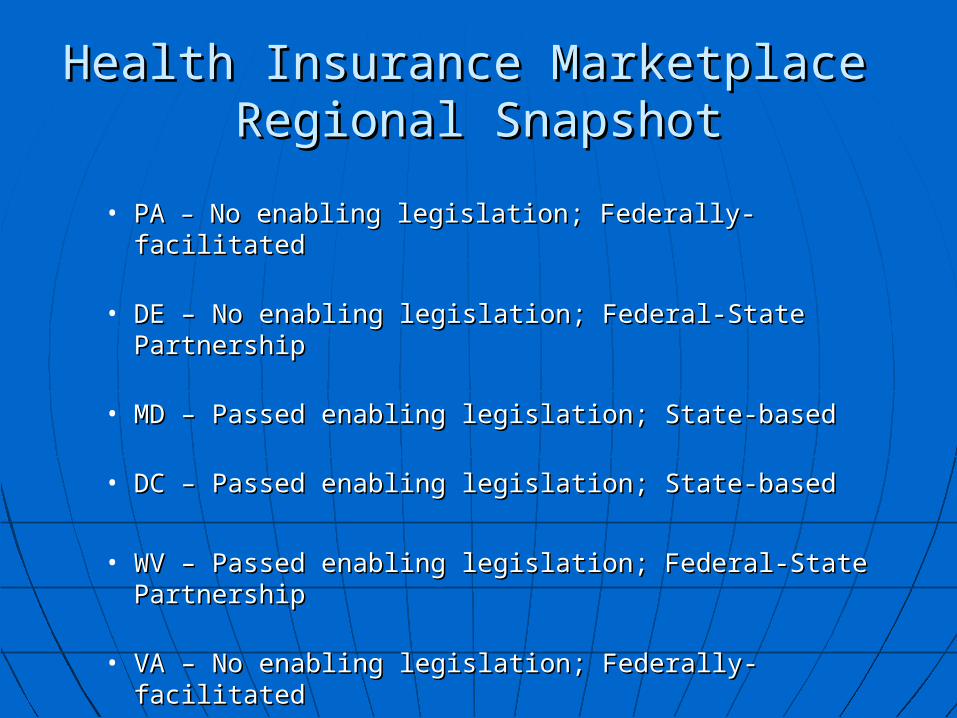

Health Insurance Marketplace Health Insurance Marketplace Regional SnapshotRegional Snapshot

• PAPA – – No enabling legislation; Federally-facilitated No enabling legislation; Federally-facilitated

• DE – No enabling legislation; Federal-State PartnershipDE – No enabling legislation; Federal-State Partnership

• MD – Passed enabling legislation; State-based MD – Passed enabling legislation; State-based

• DC – Passed enabling legislation; State-basedDC – Passed enabling legislation; State-based

• WV – Passed enabling legislation; Federal-State WV – Passed enabling legislation; Federal-State Partnership Partnership

• VA – No enabling legislation; Federally-facilitatedVA – No enabling legislation; Federally-facilitated

Marketplace EligibilityMarketplace Eligibility

Marketplace eligibility requires Marketplace eligibility requires • You live in the service area, You live in the service area, • Are a U.S. citizen or national, or Are a U.S. citizen or national, or • Are a non-citizen who is lawfully Are a non-citizen who is lawfully

present in the U.S. for the entire present in the U.S. for the entire period for which enrollment is soughtperiod for which enrollment is sought

• Are not incarcerated Are not incarcerated

Financial AssistanceFinancial Assistance

Premium tax creditsPremium tax credits• Will reduce the premium amount the consumer Will reduce the premium amount the consumer

owes each monthowes each month• Available to eligible consumers with household Available to eligible consumers with household

incomes between 100% and 400% of the FPL incomes between 100% and 400% of the FPL ($44,680 for an individual and $92,200 for a family ($44,680 for an individual and $92,200 for a family of 4 in 2012), and who don’t qualify for other health of 4 in 2012), and who don’t qualify for other health insurance coverageinsurance coverage

• Based on household income and family size for the Based on household income and family size for the taxable yeartaxable year

• Paid each month to the insurerPaid each month to the insurer

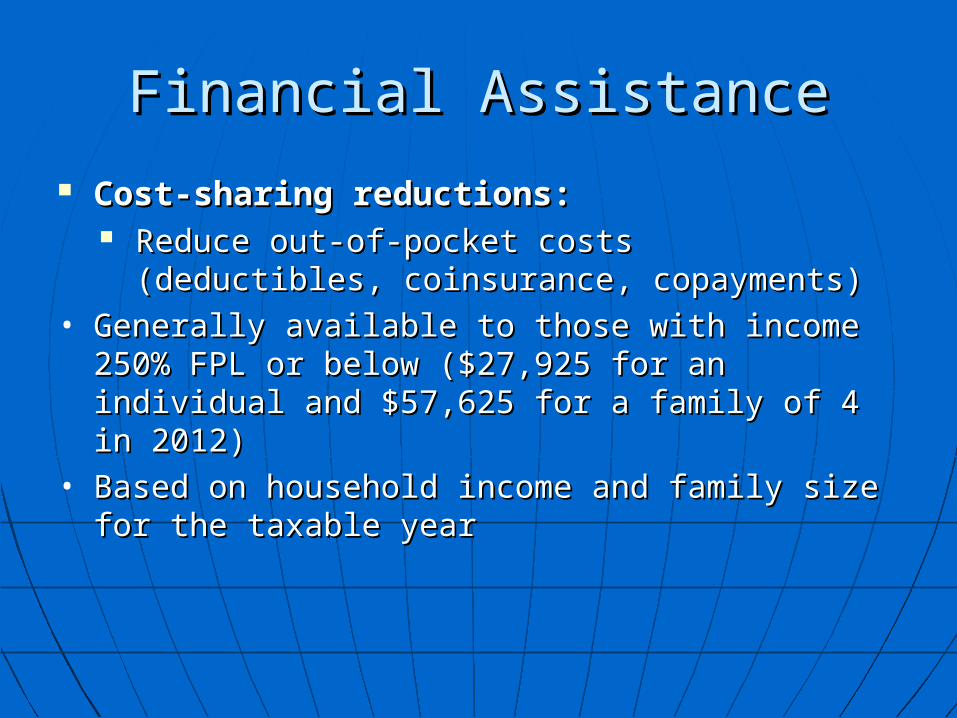

Financial AssistanceFinancial Assistance

Cost-sharing reductions:Cost-sharing reductions: Reduce out-of-pocket costs (deductibles, Reduce out-of-pocket costs (deductibles,

coinsurance, copayments)coinsurance, copayments)• Generally available to those with income 250% Generally available to those with income 250%

FPL or below (FPL or below ($27,925 for an individual and $27,925 for an individual and $57,625 for a family of 4 in 2012)$57,625 for a family of 4 in 2012)

• Based on household income and family size for Based on household income and family size for the taxable yearthe taxable year

Quality InsuranceQuality Insurance The ACA requires plans inside the Marketplace The ACA requires plans inside the Marketplace

to meet particular actuarial value (AV) targetsto meet particular actuarial value (AV) targets• Bronze = 60% AVBronze = 60% AV• Silver = 70% AVSilver = 70% AV• Gold = 80% AVGold = 80% AV• Platinum = 90% AVPlatinum = 90% AV

““Metal Levels” will enable consumers to Metal Levels” will enable consumers to compare plans with similar levels of coverage, compare plans with similar levels of coverage, promote competition on premiums, and allow promote competition on premiums, and allow plans flexibility to design cost sharing plans flexibility to design cost sharing structuresstructures

Essential Health BenefitsEssential Health Benefits• Ambulatory patient servicesAmbulatory patient services• Emergency servicesEmergency services• HospitalizationHospitalization• Maternity and newborn careMaternity and newborn care• Mental health and substance use disorder Mental health and substance use disorder

services, including behavioral health treatmentservices, including behavioral health treatment• Prescription drugsPrescription drugs• Rehabilitative and habilitative services/devicesRehabilitative and habilitative services/devices• Laboratory servicesLaboratory services• Preventive and wellness services and chronic Preventive and wellness services and chronic

disease managementdisease management• Pediatric services, including oral and vision Pediatric services, including oral and vision

carecare

Quality InsuranceQuality Insurance

Marketplace for Small BusinessMarketplace for Small Business

Starting in 2014, a Small Business Health Options Starting in 2014, a Small Business Health Options Program (SHOP) will be available in each state Program (SHOP) will be available in each state

To enroll, employers must To enroll, employers must • have fewer than 100 employees; a state SHOP have fewer than 100 employees; a state SHOP

may limit eligibility to employers with 50 or less may limit eligibility to employers with 50 or less employees for the first two yearsemployees for the first two years

• have an office within the service area of the have an office within the service area of the SHOPSHOP

• offer SHOP coverage to all full-time employeesoffer SHOP coverage to all full-time employees Sole proprietors must purchase through the Sole proprietors must purchase through the

Marketplace, not through SHOPMarketplace, not through SHOP

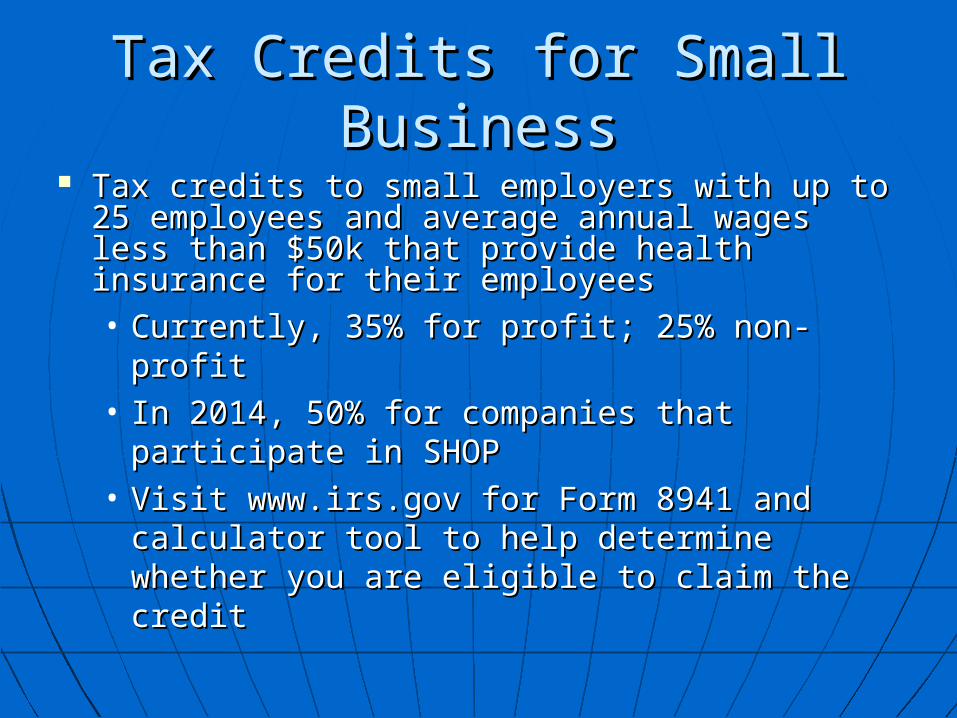

Tax Credits for Small BusinessTax Credits for Small Business Tax credits to small employers with up to 25 Tax credits to small employers with up to 25

employees and average annual wages less employees and average annual wages less than $50k that provide health insurance for than $50k that provide health insurance for their employeestheir employees• Currently, 35% for profit; 25% non-profitCurrently, 35% for profit; 25% non-profit• In 2014, 50% for companies that In 2014, 50% for companies that

participate in SHOPparticipate in SHOP• Visit www.irs.gov for Form 8941 and Visit www.irs.gov for Form 8941 and

calculator tool to help determine whether calculator tool to help determine whether you are eligible to claim the credityou are eligible to claim the credit

Enrollment ProcessEnrollment Process Consumer submits application to the marketplaceConsumer submits application to the marketplace

• OnlineOnline• PhonePhone• MailMail• In PersonIn Person

The marketplace verifies and determines The marketplace verifies and determines eligibility foreligibility for• enrollment in a Qualified Health Plan (QHP)enrollment in a Qualified Health Plan (QHP)• tax credits and cost-sharing reductionstax credits and cost-sharing reductions• Medicaid or CHIPMedicaid or CHIP

Consumer enrolls in a QHP or Medicaid/CHIPConsumer enrolls in a QHP or Medicaid/CHIP• Online plan comparison tool available to inform health plan Online plan comparison tool available to inform health plan

choicechoice• Tax credit is sent to insurer (if eligible) to reduce consumer Tax credit is sent to insurer (if eligible) to reduce consumer

premium owed premium owed

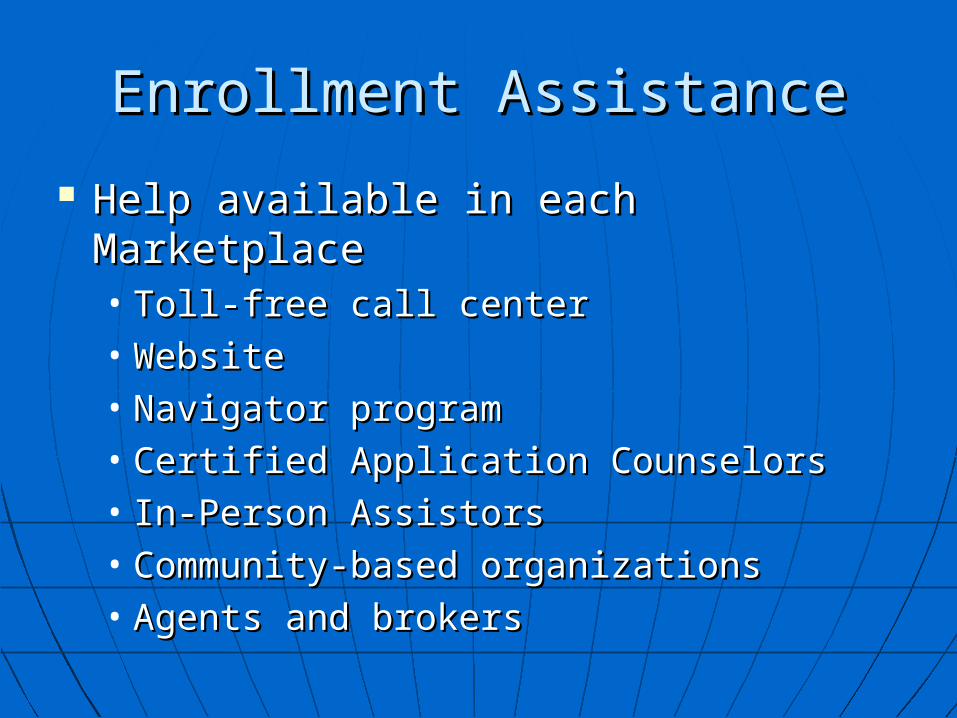

Enrollment AssistanceEnrollment Assistance

Help available in each MarketplaceHelp available in each Marketplace• Toll-free call centerToll-free call center• WebsiteWebsite• Navigator programNavigator program• Certified Application CounselorsCertified Application Counselors• In-Person AssistorsIn-Person Assistors• Community-based organizationsCommunity-based organizations• Agents and brokers Agents and brokers

Marketplace Call CenterMarketplace Call Center

A single 1-800 number for the call centerA single 1-800 number for the call center A single TTY number for hearing impaired A single TTY number for hearing impaired

callerscallers Services will be available in English and SpanishServices will be available in English and Spanish

• A separate language line will be available for A separate language line will be available for translation services (over 150 additional languages translation services (over 150 additional languages available)available)

A special “assistor” phone line to support A special “assistor” phone line to support Navigators, IPAs, and Medicaid OfficesNavigators, IPAs, and Medicaid Offices

June – September 2013: June – September 2013: • The call center will launch in conjunction with The call center will launch in conjunction with

the re-launch of HealthCare.gov the re-launch of HealthCare.gov

Initial Open Enrollment PeriodInitial Open Enrollment Period

October 1, 2013 – March 31, 2014October 1, 2013 – March 31, 2014

Enroll during the Initial Open Enrollment Period

Your coverage is effective*

On or before December 15, 2013

January 1, 2014

Between the 1st and 15th day of January – March

First day of the following month

Between the 16th and the last day of December – March

First day of second following month

Consumers may enroll or change QHP:Consumers may enroll or change QHP:• Within 60 days in individual market and 30 days in small group Within 60 days in individual market and 30 days in small group

market from qualifying event market from qualifying event

Special Enrollment Period Special Enrollment Period Special Enrollment Period Special Enrollment Period

1919

Special Enrollment Period Qualifying EventsLoss of minimum essential coverage

Material contract violations by Qualified Health Plans

Gaining or becoming a dependent

Gaining or losing eligibility for premium tax credits or cost sharing reductions

Gaining lawful presence Relocation resulting in new or different Qualified Health Plan selection

Enrollment errors of the Marketplace

Exceptional circumstances

Medicaid Expansion in PAMedicaid Expansion in PA 650,000 Pennsylvanians will be 650,000 Pennsylvanians will be

eligible for health insurance if eligible for health insurance if Medicaid is expandedMedicaid is expanded

Federal Government pays 100% of Federal Government pays 100% of costs 2014 thru 2016; 90% from costs 2014 thru 2016; 90% from 2020 onwards2020 onwards

PA will receive $17 billion in federal PA will receive $17 billion in federal funding in first six yearsfunding in first six years

Medicaid ExpansionMedicaid Expansion

Resources:

Affordable Care Act website –Affordable Care Act website –www.healthcare.govwww.healthcare.gov

Health Insurance Marketplace –Health Insurance Marketplace –

http://http://marketplace.cms.govmarketplace.cms.gov

Center for Consumer Information & Insurance Center for Consumer Information & Insurance Oversight website – Oversight website –

http://cciio.cms.govhttp://cciio.cms.gov

Affordable Care Act Spanish Affordable Care Act Spanish website website – – www.cuidadodesalud.govwww.cuidadodesalud.gov