Affordable Care Act ACA Reporting. Two Types of Reporting 6056 Reporting (1095-C and 1094-C) –...

24

Affordable Care Act ACA Reporting

-

Upload

bathsheba-johns -

Category

Documents

-

view

216 -

download

0

Transcript of Affordable Care Act ACA Reporting. Two Types of Reporting 6056 Reporting (1095-C and 1094-C) –...

Affordable Care Act

ACAReporting

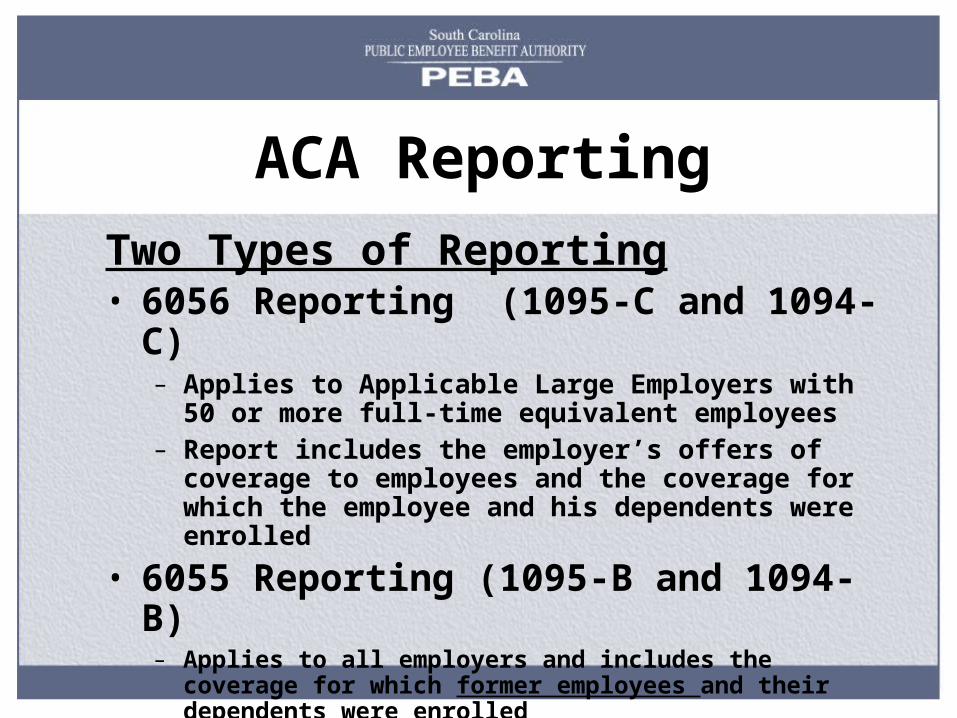

Two Types of Reporting• 6056 Reporting (1095-C and 1094-C)

– Applies to Applicable Large Employers with 50 or more full-time equivalent employees

– Report includes the employer’s offers of coverage to employees and the coverage for which the employee and his dependents were enrolled

• 6055 Reporting (1095-B and 1094-B)– Applies to all employers and includes the coverage for which former

employees and their dependents were enrolled– Employers with fewer than 50 full-time equivalent employees will also

use these forms to report coverage for their active employees

ACA Reporting

For employees:• Each employer will be responsible for filing forms

for any individual employed with them at any time during the preceding calendar year.

• For state agencies or divisions that collectively make up the ALE member that is “The State” (payroll processed by the CG), only one consolidated report for active employees of the State will be submitted to the IRS. The reporting entity has not been identified yet.

ACA Reporting

For non-employees:• PEBA will be responsible for making the returns

and statements required for non-Medicare eligible retirees, COBRA subscribers and survivors of “The State”.

• A list of state agencies and divisions that collectively make up the ALE member that is “The State” will be published on our website.

ACA Reporting

For non-employees:• Other employers that participate in the State

Health Plan pursuant to S.C. Code Ann § 1-11-710 (technical colleges, public universities, public school districts and certain public corporations) may designate PEBA as its Designated Governmental Entity (DGE) for making the returns and statements required for its non-Medicare eligible retirees, COBRA subscribers and survivors.

ACA Reporting

For non-employees:• PEBA will not permit employers that participate in

the State Health Plan pursuant to S.C. Code Ann § 1-11-720 (local subdivisions) to designate PEBA to report.

• Participants in the State Health Plan pursuant to S.C. Code Ann § 1-11-720 will be provided coverage information from PEBA.

ACA Reporting

ACA Reporting

Designated Governmental Entity (DGE)• Eligible employers may submit a DGE form to PEBA

via email at [email protected] • Designation is not accepted until the employer

receives a signed form back from PEBA • PEBA will only report on former non-Medicare

employees, COBRA subscribers, and survivors who have not been employed for any portion of the reporting period

• Copy of signed form will also be placed in imaging

IRS Reporting DeadlinesProvided to covered subscribers by January 31, 2016• 1095-C Employer- Provided Health Insurance Offer and Coverage• 1095-B Health Coverage

Provided to IRS by February 28, 2016 (March 31, 2016 if filing electronically)

• 1094-C Transmittal of Employer –Provided Health Insurance Offer and Coverage Information

• 1094-B Transmittal of Health Coverage

Let’s Look at the Forms

This presentation provides a brief overview of the Affordable Care Act and was current as of March 20, 2015. This presentation does not constitute legal advice. Employers are encouraged to contact their own legal counsel to ensure legal compliance.

The Plan of Benefits documents and Benefits Contracts contain complete descriptions of the Health and Dental Plans and all other insurance benefits. Their terms and conditions govern all benefits offered by or through the South Carolina Public Employee Benefit Authority.

This presentation does not create any contractual rights or entitle ments. The South Carolina Public Employee Benefit Authority reserves the right to revise the content of this presentation, in whole or in part.

Legal Disclaimer

Aggregation of Multiple Employers Control group analysis under IRC 414 also applies to

government entities IRS Presentation – July 24, 2014 (“The Affordable Care

Act’s Employer Shared Responsibility Provisions – What Government Employers Need to Know”) “[The common ownership concept is] kind of an odd concept for

government entities, and that’s been recognized, and so we have not yet developed rules under Section 414 for how a particular government entity determines if it is aggregated with or combined with another government entity for purposes of determining whether they’re a single employer. Instead, we’re just – you can apply any of these rules in reasonable good faith, and so if you apply it reasonably in how you would work it, that will be respected. . . . I would not anticipate any further guidance under Section 414 for government entities for at least the next several years while we’re still defining exactly what a government entity is in certain cases. So this reasonable good faith standard should apply for at least the next several years.”

Aggregation (cont’d) Example in IRS presentation:

School board attempts to treat and test each school it governs as a separate employer, so that each school conveniently falls under the 50-employee threshold (but would be deemed an ALE if tested in the aggregate)

Consider 414(m) – affiliated service group rulesPerforming “management functions” on a

regular and continuing basis

Seasonal Positions and Application of the Employer MandateSeasonal Employees

Must be counted when determining if the employer has 50 full-time employees and FTEs

Seasonal Workers

May be excluded when determining if the employer has 50 full-time employees and FTEs if that number exceeds 50 for 120 days (4 months) or less

Definitions

Seasonal employee: An employee who is hired into a position for which the customary annual employment is six months or less

Seasonal worker: Retail workers employed exclusively during the holidays and workers who performs labor on a seasonal basis in accordance with the following Department of Labor rules:From the nature of the work, employment is

the kind exclusively performed during periods of the year

Examples: agriculture , ski instructors

Seasonal Positions and Treatment under the ACA Seasonal employees may be treated

as variable hour employees for ACA compliance purposes

Transition relief for Small ALEs Remember no 2015 penalties for ALEs with less

than 100 employee? – 1 Catch ALE must certify on its Form 1094-C that it

meets the following eligibility conditions: It employs a limited workforce between 50 and

100 full-time employees (and equivalents) Between Feb. 9, 2014 and Dec. 31, 2014, it does

not reduce the size of its workforce or overall hours of its employees in order to satisfy the workforce size condition; and

ALE does not eliminate or materially reduce the health coverage, if any, offered as of Feb. 9, 2014

IRC 6056 – Simplified Reporting

(1) Qualifying Offers Method For those employees given a qualifying offer to the employee,

spouse, and dependents meeting minimum essential coverage and minimum value standards for all 12 months of the year,

(2) 98% offers method Employer certifies it offered qualifying coverage to at least 98%

of the employees (and their dependents) on whom it is reporting. (3) 2015 Transition Rule

Employer can certify that it made a qualifying offer to at least 95% of all FT EEs, spouses and dependents for each month in 2015. If the employer qualifies to use the 2015 transition method, full/general reporting is not required for any FT EEs.

ACA Reporting

Questions?