Affinity 02

16

FALL 2008 Managing Your Money in a Changing Economy

-

Upload

shibu-lawrence -

Category

Documents

-

view

243 -

download

0

description

Economy Managing Your Money in a F A L L 2 0 0 8

Transcript of Affinity 02

F A L L 2 0 0 8

Managing YourMoney in aChanging

Economy

Surviving a Challenging Economy.......................................... 2– A Prudent Approach to Your Balance Sheet

Increase Your Personal Bottom Line...................................... 5– Changing Your Behavior to Save Money

Come On Down!....................................................................... 7– Great Opportunities for Car Buyers

Debt Management................................................................... 9– What You Need to Know

Holiday Shopping....................................................................10– Why Wait Until December?

Is Your Insurance Expendable?..............................................11– Ways to Save and Stay Covered

Your Financial Records............................................................12– How Long Should You Keep Them?

AFFINITY NEWS....................................................................13

WELCOME NEW SEGs .....................................................14– Thank You for Choosing Affinity

IN EVERY ISSUE

I N T H I S

I S S U E

7

10Dear Affinity Member,

If you were a business owner in today’s challengingeconomy, you’d be looking for ways to increaseprofitability by reducing expenses, as well as raisingrevenues. This issue of Affinity Connections isdedicated to helping you do just that.

Our lead article, “Surviving a Challenging Economy,”contains a number of ideas to help you reduceongoing expenses, particularly debt, while positioningyour investment portfolio to withstand today’s volatilemarkets. We also explore strategies to pay less at thegas pumps, including taking a closer look at the wayyou drive and maintain your vehicle.

With gas prices at historic highs, many people arewondering if their next car should be a hybrid. Welook at the advantages and disadvantages and reviewa variety of other important issues to consider whenbuying a new or used car.

Of course, soaring gas prices influence other costs likefood prices and we discuss whether shopping in bulkat places like Sam’s Club® and Costco® really makesmore sense than patronizing your local supermarket.And we even focus on one important expense thatyou probably shouldn’t try to eliminate, no matterhow tempting—your insurance premiums. But thatdoesn’t mean we don’t offer ways to reduce them.

Finally, we provide advice on a variety of other topics,including debt management, a service that seems tobe advertised everywhere these days, and the benefitsof doing your holiday shopping now. As you can see,we’ve packed this issue with information you canuse to make the best of our current economy. Takeadvantage of the opportunities it offers and improveyour personal bottom line.

Best regards,

John T. FentonPresident and CEO

11

1 Affinity Connections | FALL 2008

5

2 Affinity Connections | FALL 2008

This newsletter is distributed with the understanding that it does not constitute legal, accounting or other professional advice. Neither Affinity nor any other partywill assume liability for loss or damageas a result of this material. Appropriate legal or accounting advice should be sought from a competent professional. Affinity is not responsible for typographic or inadvertent errors. Affinity FinancialServices is a wholly owned subsidiary of Affinity Federal Credit Union. © 2008 Affinity Federal Credit Union.

Today’s economy is difficult, if not

daunting, for many consumers.

Rising energy and food costs are

taking a bigger bite out of cash flow.

Inflation is up, home prices are

down and many home owners have

been limited in their ability to sell

their property. Investing has become

increasingly challenging with volatile

markets and interest rates lower

than they’ve been in years.

We can’t promise that by following themeasures listed below, you’ll bringprosperity to your life, but we can assureyou that by adopting a prudent, commonsense approach to both sides of yourpersonal balance sheet, you’ll be betterpositioned to withstand the pressures oftoday’s lackluster economy and takeadvantage of whatever opportunities itmight offer.

REDUCING EXPENSES

The right side of your balance sheetrepresents expenses. And while payingless for goods that are increasing in priceis by no means a simple task, it might bepossible if you follow the strategiesdiscussed in our article on pages 5 and 6entitled, “More Ways to Increase YourPersonal Bottom Line.”

One of the most important steps you cantake to reduce expenses is to decrease oreliminate debt. Before you say youcouldn’t possibly do such a thing withoutputting a sizable dent in your savings, let’stake a closer look at the types of debt youmight be carrying.

Surviving aChallengingEconomy

• Credit cards

Do you pay your balances everymonth? Or do you only submit partialpayments and incur finance chargesthat may be as high as 21%?

What makes more sense—to eliminatethese charges or to continue payingthem while your assets earn 2-4% in aCD or money market fund? Use assetsgenerating a low rate of return to payoff high interest debt. And try to limityour impulse buying, so you don’tgenerate new debt.

• Car loans

Unless you’re taking advantage of the0% financing offers that car companiesmake from time to time, take a closerlook at the rate you’re paying. Howdoes it compare to the rates offered byhome equity loans or lines of credit?Generally, home equity loans chargelower rates and the interest you paymay be tax deductible. The key is tofind a home equity loan that allowsyou to pay off your balance in thesame period of time as your car loan.You don’t want to finance a short-termpurchase with long-term debt.

• Mortgages

Rates are low and refinancing yourmortgage can conceivably save youhundreds of dollars a month. Pointsand closing costs are a consideration,so make sure you factor them in whencalculating your overall payments.Also, don’t step backward by takingout a 30-year mortgage when you onlyhave a few years left to pay on yourcurrent loan.

Other debt-related strategies

• You may want to think about makingextra principal payments on your

mortgage. Again, taking money out ofa 2-4% interest bearing account to payfor a 6-8% mortgage makes a lot ofsense. And you’ll reduce your overallinterest payments by thousands ofdollars over the term of your mortgage.

• When you’re contemplating whichaccounts you should tap to pay offdebt, eliminate your IRA or 401(k)from consideration. Assets withdrawnfrom these accounts are subject toincome tax at your tax rate, plus a10% penalty if you’re under age 591⁄2.Besides, these accounts are earmarkedfor your retirement. And with manyretirements lasting 20-30 years orlonger, you’re going to need all theassets you can accumulate.

• Resist the temptation to ignore yourbills or postpone payments until youcan better afford them. You’ll onlyincur finance charges and suffer a blowto your credit rating. Most credit cardcompanies and other creditors willwork with you to establish a paymentschedule that you can manage.

INCREASING ASSETS

Like a business, you have two ways toachieve profitability—reduce expensesand increase revenue. For individuals,revenue comes primarily from your joband your investments. As for your job,now is the time to buckle down andmake yourself indispensable—theunemployment rate may not be upappreciably over the past several years,but clearly, we’re living in an uncertainenvironment. As for your investments, it’stempting to alter your strategy. After all,today’s volatile markets can mean potentiallosses or possible opportunities for gains,depending on your point of view.

In times like these, however, staying thecourse is often the smartest strategy.That’s because the individual investmentsyou select for your portfolio don’tcontribute nearly as much to your overallreturn as the way in which you allocateyour assets across the three major assetclasses—stocks, bonds and cash.

3 Affinity Connections | FALL 2008

The high cost ofstock market jitters

Before today’s market uncertainties compel you toabandon your equity investments in favor of saferalternatives, consider the chart on the right. It showshow a $10,000 investment would have been affectedby missing the market’s top-performing days over the10-year period from December 31, 1997 to December31, 2007. For example, an individual who remainedinvested for the entire time period would haveaccumulated $17,758, while an investor who missedjust 15 of the top-performing days during that periodwould have accumulated only $9,246.

Source: Standard & Poor’s. Stocks are represented by Standard & Poor’sComposite Index of 500 Stocks, an unmanaged index that is generallyconsidered representative of the U.S. stock market. Past performance isno guarantee of future results.

The chart below illustrates the results of awell known financial study that wasconducted in 1986 and updated five yearslater. The study concludes that 91.5% of aportfolio’s return is attributable to assetallocation, while only 4.6% is attributableto stock selection.

The right allocation for one person,however, may be totally wrong foranother. Your allocation should be areflection of your objectives, time horizon,need for liquidity, risk tolerance and otherfactors. To develop it, you should consultwith your financial advisor or use the freeanalytical tools available at websites suchas www.mint.com or www.kiplinger.com.

Once you arrive at an appropriateallocation, you should diversify yourholdings within each asset class. Forexample, stocks or mutual funds thatinvest in stocks may be diversified bymarket capitalization, geographic locationand investment style. Bonds, CDs andother fixed income investments shouldvary by maturity. In fact, many astute

fixed income investors ladder theirportfolios with securities that matureseveral months (or years) apart in order toprotect themselves against unpredictableinterest rate fluctuations.

THE KEY TO ANY ECONOMY . . .

. . . is to adopt a consistent approach toboth debt and investment management.The best approach enables you to takeadvantage of potential opportunitiesand avoid unnecessary risk. The currenteconomy is challenging, but by reducingdebt, controlling expenses and diversifyingyour investments, you’ll not only survive it,but position yourself for the upturn whenit finally does occur.

4 Affinity Connections | FALL 2008

What Can You Doto Increase Your

Bottom Line?

Affinity’s Financial Advisors can help you review strategiesto improve your investment return. Call 800-325-0808 or visitwww.affinityfcu.org.

StayInvested

MissTop5 Days

MissTop

10 Days

MissTop

15 Days

MissTop

20 Days

MissTop

25 Days

MissTop

30 Days

$20,000

$15,000

$10,000

$5,000

$0

$17,758

$13,782

$11,189

$9,246

$7,745

$6,547$5,587

Stock Selection4.6%

Other2.0%

Market Timing1.8%

Asset Allocation Decisions91.5%

Source: Brinson, Singer & Beebower

Securities offered by Affinity Investment Services, LLC, 73 Mountain View Boulevard, Basking Ridge, NJ 07920, member FINRA/SIPC. Investments offered by AffinityInvestment Services are not deposits or obligations of Affinity Federal Credit Union. They are NOT NCUA INSURED and NOT GUARANTEED by Affinity Federal CreditUnion or any governmental agency and are subject to INVESTMENT RISK, including LOSS of PRINCIPAL. Investments may lose value. Affinity Investment Services, LLCis a wholly owned subsidiary of Affinity Federal Credit Union.

5 Affinity Connections | FALL 2008

Notice something about today’s gas

prices other than the fact that

they’re skyrocketing?

They’re beginning to change

people’s behavior.

Maybe you simply don’t drive as much asyou did before or at least think twicebefore you turn the ignition. Maybe youfind yourself buying $20-$30 worth of gasbecause you somehow feel it’s lessupsetting than spending $60-$70 to fillthe tank. Or perhaps you’re starting to

wonder if your next car should be ahybrid or at least something other thanan SUV.

There are ways to reduce not only yourgas costs but the costs of the goods thathave risen because of increased gas prices.

Let’s start with your behavior at the pump:

• Do you really need premium?

What does your owner’s manual say?Some automobile manufacturers requirehigh octane gas for certain models,while others only recommend it.

If high octane gas is required for yourcar, bite the bullet and pay the extramoney. Failure to do so may damageyour engine. However, if high octanegas is only recommended, you have adecision to make.

Fifteen to twenty years ago, fueling ahigh performance car with regular gascaused engine knock and vibration.Today, however, computerized sensorstypically adjust your engine’s timing forthe type of fuel you use. The result? Noknocks, but possibly a slight reductionin performance and fuel economy. If this

More Ways toIncreaseYour Personal Bottom Line

by Decreasing Day-to-Day Expenses

6 Affinity Connections | FALL 2008

Make More MoneyWhile You Save

Increase your earnings with Affinity Green Rewards Checking.Good for you, good for the environment too!Visit www.affinity.fcu.org/greenrewards or call 800-325-0808 today.

is unacceptable to you, buy the gasrecommended by your car manufacturer.If not, fill ‘er up with regular.

One more thing—there are absolutelyno benefits to be derived from usinghigh octane gas in a car that doesn’trequire it. You might as well be burningthe additional money you spend.

• Can you buy no-name gas?

Gas is a fungible commodity. Thatmeans it doesn’t differ regardless ofwhere you purchase it. However, majoroil companies often add a detergent totheir gas that may have a positiveimpact on engine deposits. If you’replanning to keep your car for a longtime, you may want to take advantageof these benefits and limit no-namegas purchases to every second orthird fill-up.

• What about once you leave the gasstation? What else can you do?

The way you drive and maintain yourcar can have a major impact on howmuch gas it uses. For example:

• Keeping your engine tuned canincrease gas mileage by an averageof 4%.

• Replacing clogged air filters canincrease gas mileage by up to 10%.

• Removing 100 lbs. of the junk you’veallowed to accumulate in your trunkcan increase gas mileage by 2%.

• Keeping your tires properly inflatedand aligned can increase gas mileageby up to 3%.

• Obeying posted speed limits canreally save you money. Driving at55 mph can actually increase fueleconomy by 21% versus drivingat 70 mph.

There—we just increased your fueleconomy by 40%. And that’s not evencounting no-brainers like avoidingunnecessary idling while you’re waitingfor someone.

BEYOND GAS SAVINGS

The high cost of fuel has impacted thecost of manufacturing and deliveringgoods. These higher costs have beenpassed on to you. What can you doabout them?

Many people have begun relying on storeslike Costco and Sam’s Club that sell bulkitems, reducing the number of trips to thelocal grocery store. Is the savings worththe effort?

Maybe.

Buying vegetable oil in mammothcontainers and 10 packs of aluminum foilmay add up to hundreds of dollars insavings a year. But depending on thegoods involved, you may actually dobetter at your local supermarket oroffice supply store.

The key is looking at per unitcost—how much do the goodscost per ounce, pound or otherbasic measure. Surprisingly,bulk is not always going tobe the best, although often itcan be.

In addition, you shouldthink about whether youwill actually use suchlarge quantities of whatmight be perishablegoods before theirexpiration date.

And, of course, there’s the question ofstorage. Do you have enough room tokeep bulk items where you can accessthem conveniently?

Finally, once you bring bulk items home,use them to generate even more costsavings. Drop the tall skim latte habit infavor of brewing your own coffee at homeand bringing it with you. Dip into yourstash of 500 paper bags to brown bagyour lunch. Freeze chicken or beef indinner-size packets. The possibilitiesare endless!

Source: www.edmunds.com

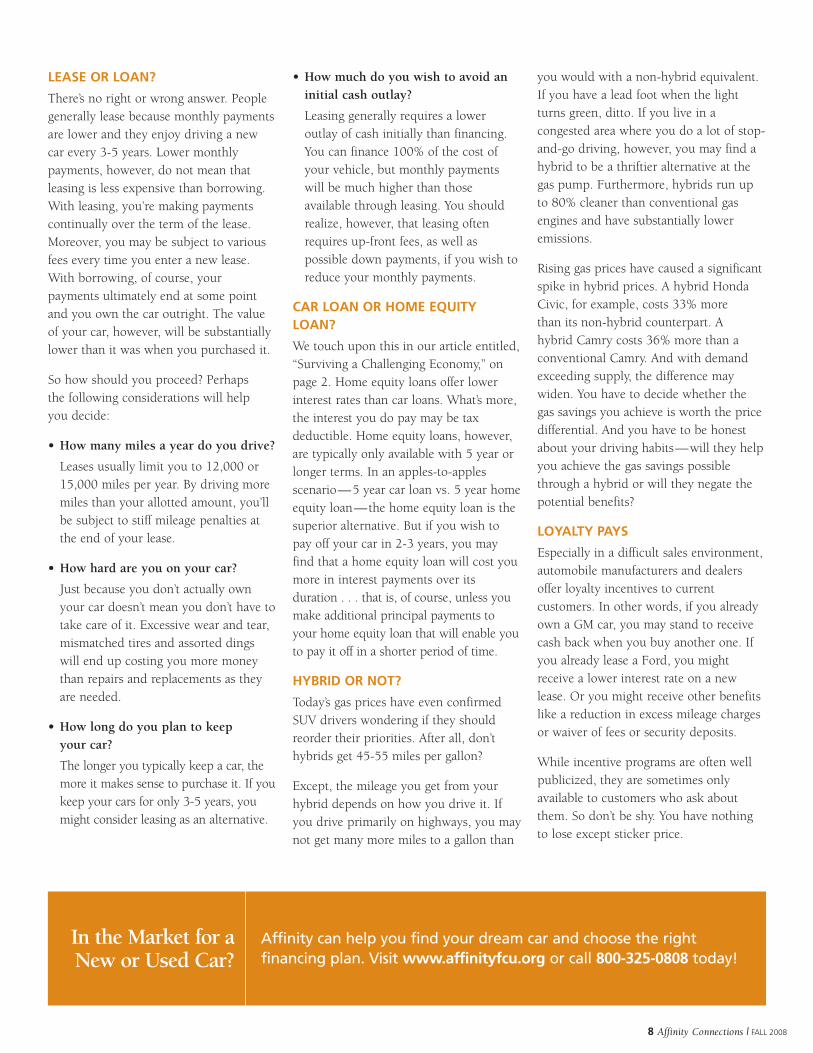

The combination of rising gas

prices and a sagging economy has

slowed car sales to a point that

dealers are offering a wide variety

of rebates, financing arrangements

and other incentives. Should you

take advantage of them?

If you’ve been thinking about shoppingfor a car, now is a great time. It’s helpful,however, to make certain you’veconsidered the following issues beforeyou begin:

2009 OR 2008?

It depends. Dealers traditionally offerwhatever current year models are left ontheir lot at a substantial discount. Youshould realize, however, that the minuteyou drive out of the lot, your car will beworth considerably less than a 2009model, particularly if the 2009 model haschanged substantially. If you plan to driveyour car “until the wheels fall off,” you maynot be concerned about future trade-in orresale value. But, if you typically buy a carevery 3-5 years, you might think aboutnegotiating a great deal on a 2009 modelto ensure a better trade-in value.

NEW OR USED?

Tough call. The benefits of each areobvious—new car panache vs. used carpracticality. Clearly, a used car costs lessthan a new one, but it may also be poisedfor major unwarrantied repairs,depending on its age and condition. Ifyou go the used car route, make certainyou check its title through a service likeCARFAX (www.carfax.com) to determinewhether the car has ever been:

• Seriously damaged in an accident ornatural disaster

• Repossessed

• Returned as a lemon

Checking the title can also inform youwhether the car’s odometer has ever beenrolled back.

7 Affinity Connections | FALL 2008

Come ondown!

Today’s economy offersgreat opportunities

for car buyers

8 Affinity Connections | FALL 2008

LEASE OR LOAN?

There’s no right or wrong answer. Peoplegenerally lease because monthly paymentsare lower and they enjoy driving a newcar every 3-5 years. Lower monthlypayments, however, do not mean thatleasing is less expensive than borrowing.With leasing, you’re making paymentscontinually over the term of the lease.Moreover, you may be subject to variousfees every time you enter a new lease.With borrowing, of course, yourpayments ultimately end at some pointand you own the car outright. The valueof your car, however, will be substantiallylower than it was when you purchased it.

So how should you proceed? Perhapsthe following considerations will helpyou decide:

• How many miles a year do you drive?

Leases usually limit you to 12,000 or15,000 miles per year. By driving moremiles than your allotted amount, you’llbe subject to stiff mileage penalties atthe end of your lease.

• How hard are you on your car?

Just because you don’t actually ownyour car doesn’t mean you don’t have totake care of it. Excessive wear and tear,mismatched tires and assorted dingswill end up costing you more moneythan repairs and replacements as theyare needed.

• How long do you plan to keepyour car?

The longer you typically keep a car, themore it makes sense to purchase it. If youkeep your cars for only 3-5 years, youmight consider leasing as an alternative.

• How much do you wish to avoid aninitial cash outlay?

Leasing generally requires a loweroutlay of cash initially than financing.You can finance 100% of the cost ofyour vehicle, but monthly paymentswill be much higher than thoseavailable through leasing. You shouldrealize, however, that leasing oftenrequires up-front fees, as well aspossible down payments, if you wish toreduce your monthly payments.

CAR LOAN OR HOME EQUITYLOAN?

We touch upon this in our article entitled,“Surviving a Challenging Economy,” onpage 2. Home equity loans offer lowerinterest rates than car loans. What’s more,the interest you do pay may be taxdeductible. Home equity loans, however,are typically only available with 5 year orlonger terms. In an apples-to-applesscenario—5 year car loan vs. 5 year homeequity loan—the home equity loan is thesuperior alternative. But if you wish topay off your car in 2-3 years, you mayfind that a home equity loan will cost youmore in interest payments over itsduration . . . that is, of course, unless youmake additional principal payments toyour home equity loan that will enable youto pay it off in a shorter period of time.

HYBRID OR NOT?

Today’s gas prices have even confirmedSUV drivers wondering if they shouldreorder their priorities. After all, don’thybrids get 45-55 miles per gallon?

Except, the mileage you get from yourhybrid depends on how you drive it. Ifyou drive primarily on highways, you maynot get many more miles to a gallon than

you would with a non-hybrid equivalent.If you have a lead foot when the lightturns green, ditto. If you live in acongested area where you do a lot of stop-and-go driving, however, you may find ahybrid to be a thriftier alternative at thegas pump. Furthermore, hybrids run upto 80% cleaner than conventional gasengines and have substantially loweremissions.

Rising gas prices have caused a significantspike in hybrid prices. A hybrid HondaCivic, for example, costs 33% morethan its non-hybrid counterpart. Ahybrid Camry costs 36% more than aconventional Camry. And with demandexceeding supply, the difference maywiden. You have to decide whether thegas savings you achieve is worth the pricedifferential. And you have to be honestabout your driving habits—will they helpyou achieve the gas savings possiblethrough a hybrid or will they negate thepotential benefits?

LOYALTY PAYS

Especially in a difficult sales environment,automobile manufacturers and dealersoffer loyalty incentives to currentcustomers. In other words, if you alreadyown a GM car, you may stand to receivecash back when you buy another one. Ifyou already lease a Ford, you mightreceive a lower interest rate on a newlease. Or you might receive other benefitslike a reduction in excess mileage chargesor waiver of fees or security deposits.

While incentive programs are often wellpublicized, they are sometimes onlyavailable to customers who ask aboutthem. So don’t be shy. You have nothingto lose except sticker price.

In the Market for aNew or Used Car?

Affinity can help you find your dream car and choose the rightfinancing plan. Visit www.affinityfcu.org or call 800-325-0808 today!

You knowyou might

need debtmanagement

counseling when youbegin to identify with the people in theTV commercials:

• You’re being harassed by phone callsfrom creditors and collection agencies.

• You can barely pay your credit cardminimums.

• You’re constantly late with your invoicepayments.

• You haven’t been able to work out areasonable payment plan with creditors.

Maybe you should do what the commercialsays and call the toll-free number to freeyourself of debt and take steps to restoreyour peace of mind.

Or maybe you shouldn’t.

Debt management counseling has becomea $7 billion industry in the U.S. withbankruptcies high and consumer debt atrecord levels. Not all debt counselors arealike. And some can leave you in evenworse financial shape than you were whenyou made the initial call.

Here’s what you should know before youpick up the phone:

• Counseling is key . . .

Reputable debt counselors should offersuch services as personalized budgetcounseling and courses in savings anddebt management. Counselors should betrained and certified in consumer credit,budgeting and money management. And

they should be willing to meet with youon an individual basis.

• . . . and so is accreditation

A Department of Justice ruling thatanyone planning to file for bankruptcymust first complete a pre-filingcounseling session has given birth to aproliferation of debt managementcompanies. Make sure the companiesyou’re considering meet the standards ofthird party sources like the United StatesTrustee Program (www.usdoj.gov/ust)or the National Foundation for CreditCounseling, a 50-year old organizationwith strict accreditation guidelines(www.debtadvice.com).

• Debt management programs may be aviable solution, but . . .

. . . they shouldn’t be the first and onlyoption offered by the company you’reconsidering. With a debt managementplan, the counseling company negotiateswith your creditors to reduce fees,finance charges and interest rates whilescheduling a repayment plan. Youdeposit money with the counselingcompany every month and thecounseling company pays your creditors.

If you do participate in a debt managementplan make certain you determine:

• How long the plan will be in effect

Many plans take 48 months or more tocomplete and require you to avoid usingor applying for credit. Be wary of open-ended plans. Your counselor should atleast be able to give you an estimate ofyour plan’s duration.

• How much the plan will cost

Debt management plans typically requirea set-up fee and a monthly payment,both of which may range from $10 tounconscionable amounts. The counselingcompany may also receive paymentsfrom your creditors. Make sure you shoparound as fees vary greatly. And, if youare asked for substantial up-front fees,find another counselor.

• If your creditors are really being paid

Check your creditors’ monthlystatements to make certain yourcounseling company is fulfilling itspromises. Also check to determinewhether payments are being made ontime. Late payments, of course, canadversely affect your credit rating.

You should realize that participation in adebt management plan can impact yourcredit rating, even if your plan pays yourcreditors on a timely basis. In addition,some creditors may not want to doadditional business with you after you’vecompleted your plan, but others will.In fact, many believe that debt counselingis a positive sign that a customer is gettinghis or her debts under control. And it iscertainly a less onerous alternative thandeclaring bankruptcy.

The counseling companies advertising onTV and radio aren’t your only options.According to the Federal TradeCommission, many universities, militarybases, credit unions, housing authoritiesand branches of the U.S. CooperativeExtension Service operate non-profit debtmanagement programs. For moreinformation, visit www.ftc.gov.

9 Affinity Connections | FALL 2008

What you should knowbeforeyou call the 800 number

Do You NeedDebt Management

Counseling?

Look to Affinity’s free Budget and Credit Score Enhancement Service(BASES) for the answer. Learn more at www.affinityfcu.org orcall 800-325-0808.

DebtManagement:

10 Affinity Connections | FALL 2008

Securities offered by Affinity Investment Services, LLC, 73 Mountain View Boulevard, Basking Ridge, NJ 07920, member FINRA/SIPC. Investments offered by AffinityInvestment Services are not deposits or obligations of Affinity Federal Credit Union. They are NOT NCUA INSURED and NOT GUARANTEED by Affinity Federal CreditUnion or any governmental agency and are subject to INVESTMENT RISK, including LOSS of PRINCIPAL. Investments may lose value. Affinity Investment Services, LLCis a wholly owned subsidiary of Affinity Federal Credit Union.

Shop Now,Save Now.

With an Affinity Club Account you can save for those holiday purchasesall year long. To find out about our savings accounts call 800-325-0808or visit www.affinityfcu.org.

Whywaituntil December to do yourholiday shopping?

In the past, towns began to decorate

their main streets for the holidays

right after Thanksgiving. Today,

Halloween seems to be the starting

point. But for savvy shoppers,

would you believe Labor Day?

It’s not too early to begin making yourshopping list, checking it twice and loggingonto the Internet to start shopping. Today’sdifficult economy is especially rough onretailers, many of whom have alreadybegun marking down merchandise. To takeadvantage of this environment, here are afew ideas to consider:

• Collect promotional codes forimmediate discounts

How many times have you purchasedsomething online and been asked toprovide a promotional code that youdidn’t have at checkout? The fact thatyou were asked indicates that a code isavailable, but where can you find it?

Next time you’re asked, open upanother window and:

– Check Google

Enter the phrase used by themerchant—promotional code orcoupon, for example—and the nameof the merchant. Chances are, you’llfind codes that can save youmeaningful dollars on the purchaseyou were about to make.

– Check other websites

You might also be able to findcoupons or promotional codes onsites such as www.CouponCabin.com,www.FatWallet.com andwww.Keycode.com. These sitescontain numerous promotional codes,discount coupons and cash-backoffers from a variety of retailers.

• Compare prices without visitingdifferent websites

Are you really getting the lowestprice possible? Instead of shoppingat the websites of individual retailers,why not visit consolidated shoppingsites like www.shopping.msn.com orwww.shopping.yahoo.com? You canview side-by-side comparisons that will

enable you to purchase merchandise fromthe retailer offering the lowest price.

PAYING FOR YOUR PURCHASES

Whether you shop online or in person,consider paying by credit card. Under theFair Billing Credit Act, purchases made bycredit card offer an added level ofprotection. Specifically:

• You are limited to $50 liability fordisputed or fraudulent charges, withmany credit card providers waiving thismaximum.

• You have the right to withhold paymentwhile charges are being investigated.

• You have the right to deny payment, ifmerchandise shipped to you is defective.

• Many credit cards offer additional buyerprotection benefits such as extendedwarranties and refunds in the event thatpurchases are damaged or stolen withina specified period of time.

So just because the holidays are a fewmonths away, that’s no reason to delaychecking off your shopping list. Your earlyaction can result in substantial savings.

11 Affinity Connections | FALL 2008

Admit it—those insurance

premiums can be an expense that’s

hard to justify in a difficult

economy. And maybe you’ve even

wondered if you should drop your

coverage and pick it up again when

the economy turns around.

Insurance is probably the last expenseyou should give up in a difficult or,for that matter, a thriving economy.However, there might be ways to reduceyour premiums:

LIFE INSURANCE

Life insurance premiums are basedprimarily on age and health. If you dropyour policy today with the intention ofpurchasing another one at some point inthe future, you may find that yourpremiums will be higher, simply becauseyou’re older. Moreover, you may not be ashealthy when you’re ready to resumeyour coverage. Also, depending on thenature of your condition, you will payconsiderably higher premiums or perhapsbe deemed “uninsurable.” This means thatthe insurance company will not assumethe risk of covering you.

If you have whole, universal or variablelife insurance that earns cash value, youmay be able to skip a premium or pay

a lower premium now and then,depending on how much cash is in thepolicy. Or you may consider replacingyour policy with low cost term insurancethat offers protection only without cashvalue accumulation.

AUTO INSURANCE

Clearly, you have no choice but to retainyour auto insurance unless you plan totrade in your car for a skateboard.However, you might be able to reduceyour premiums by:

• Raising deductibles on collision andcomprehensive

According to the Ohio InsuranceInstitute, raising deductibles from $200to $500 can reduce collision andcomprehensive premiums by 15-30%.Raising it to $1000 can reduce premiumsby considerably more.1 And you’ll still beprotected in the event of a major loss.Your insurance company can advise youon the specific savings you may realize.

• Eliminating collision andcomprehensive coverage

Experts suggest that if the cost of yourcollision and comprehensive insurancefor your vehicle is more than 10% of itscurrent value, you’ll pay more to insureit than the amount of money you’llreceive in the event of an accident.2

Check your vehicle’s value with an autodealer or through a third party sourcelike Kelley Blue Book (www.kbb.com).

DISABILITY INSURANCE

Disability insurance can be expensive,especially if you have to purchase it onyour own because you’re not eligible forgroup coverage through your employer.Dropping coverage, however, can becatastrophic if you suddenly becomedisabled and find you need benefits.

If you’re concerned about how you’re goingto afford your disability policy, consider:

• Lowering the monthly benefit youwould receive if you became disabled.

• Increasing the waiting period beforebenefits begin.

• Checking your policy to make certainyou’re not paying for optional coveragesthat would be “nice to have” but aren’treally mandatory.

Remember—you purchased your variousinsurance policies to protect yourself andyour loved ones from the unexpected. Bydropping coverages, you run the very realrisk of placing your family in far greaterjeopardy than they face in a difficulteconomic environment.

Endnotes:

1 Ohio Insurance Facts, 11/2007

2 Smart Money, “How much auto insurance do you need?”

Is Your Insurance

Expendable?

Can YourInsurance

be Improved?

Paying too much? Not protected adequately? Affinity InsuranceSpecialists can help you find out for sure. Visit www.affinityfcu.org orcall 800-325-0808.

12 Affinity Connections | FALL 2008

Want More Detailed Information?

Visit www.bankrate.com to see a comprehensive list of how longyou should keep various records.

How LongShould You StoreYourFinancial Records?

Documents How long should you keep them?

Tax Returns Seven years, to be safe. The IRS has three years to audityour return and six years if it thinks you under-reportedyour gross income by 25% or more.

RetirementPlan/SavingsAccounts

Keep your quarterly statements until you receive yourannual summary, at which point you may shred them. Keepannual summaries until you retire or close the account.

BrokerageStatementsand TradeConfirmations

Keep them at least until you sell the securities. However,you will need records of prices for which you bought andsold securities to determine whether you have capital gainsor losses at tax time. As a result, you may want to keepthis information for as long as you keep your tax returns, incase you are audited by the IRS at some point in the future.

Bank andCredit UnionRecords

Discard cancelled checks that have no long-termimportance, but keep those that represent major, long-term purchases.

Credit CardReceipts andStatements

Keep your original receipts until you receive yourstatement. For tax-related expenses, keep yourstatements for the same seven year period you keepyour tax returns.

Pay Stubs When you receive your W-2 form for taxes, make surethe information matches that which is on your pay stubs.At that point, you can shred the stubs.

Bills Once you receive a cancelled check, you can generallydiscard invoices or bills. However, you should keepinvoices for major purchases, so you have a record oftheir value in the event of loss or damage.

IRAContributions

Permanently. When you take money out of your IRA atretirement, you’ll need to prove whether you’ve alreadypaid tax on contributions you’ve made.

Don’t forget—the same rules apply if you receive your financial statementsand other records online instead of through the mail.

Tax returns, bank and brokerage statements, credit card receipts—Americans are inundated by paper that keeps arriving month after monthand, sooner or later, overwhelms even the most diligent record keepers.

If your file drawers are already stuffed with documents and you’rewondering where you’re going to file new ones, here are a few tips on howlong you should keep various financial records before shredding them:

13 Affinity Connections | FALL 2008

A F F I N I T Y N EW S

Taking Political Action – Affinity continues tobuild support in order to protect credit unions.

Affinity’s primary focus has always been the financial health andwell-being of our members. This includes protecting yourinterests in the political arena.

Affinity’s Political Action Committee (PAC) and Regulatory andPolitical Issues Committee work together to educate legislatorsabout the benefits of credit unions. We meet with legislatorsto explain what credit unions are, how they differ from banks,and how that difference benefits families across America. As aresult, many legislators have pledged their support for regulatoryrelief, including the retention of the credit union tax exemptstatus. Affinity supports these Congressmen and we urgeyou to consider how their support plays a large role in thecontinuing strength of your rights as a credit union member.

Is your Congressman supporting credit unions? Here are a fewof the New Jersey legislators that do support credit unions:

• Congressman Rob Andrews (D-District 1)

• Congressman Frank LoBiondo (R-District 2)

• Congressman Scott Garrett (R-District 5)

• Congressman Frank Pallone (D-District 6)

• Congressman Michael Ferguson (R-District 7)

• Congressman Bill Pascrell (D-District 8)

• Congressman Steve Rothman (D-District 9)

• Congressman Donald Payne (D-District 10)

• Congressman Rodney Frelinghuysen (R-District 11)

• Congressman Rush Holt (D-District 12)

• Congressman Albio Sires (D-District 13)

Community News

Announcing Affinity’s EasyFLEX Home EquityLine of Credit

Imagine a home equity line of credit so flexible it gives youexactly what you need, when you need it. Like most lines ofcredit, you get immediate access to cash for any purpose.But with EasyFLEX, you can also take out up to three fixed-rate loans at any one time. The only requirement is thatyou stay within your approved EasyFLEX limit.Visit www.affinityfcu.org/easyflex,call 800-325-0808, or visit any Affinity branch.

Congratulations to the 2008 AffinityScholarship Recipients

Jessica DePrima - Basking Ridge, NJ,Monmouth University

Keiona Eady - Cross, SC,Clemson University

Thabo D’Anjou - Scotch Plains, NJ,Howard University

Crystal Himes - Piscataway, NJ,Cornell University

Andy Yuan-Jay Lee - Basking Ridge, NJ,George Washington University

Brian D. Thorne - Lebanon, NJ,Kenyon College

Visit the newest Affinity Branch inFlemington, NJ

Our newest branch is located at 275 Route 202 South/31 South in Flemington, NJ just south of the FlemingtonCircle. The new 4,100 square foot facility features full branchservices, as well as many extras including coffee, safe depositboxes, a children's activity area, an Internet café and a smallmeeting room available for members and communityorganizations to use.

Hours of operation will be 8:30 am to 6:00 pm on Monday,Tuesday, Wednesday and Friday; 8:30 am to 7:00 pm onThursday, and 9:00 am to 1:00 pm on Saturday.

Mark your calendar for these business events:

• Business Networking Event - Wednesday, October 15th at6:30 pm. Make new contacts and learn how Affinity canhelp your business grow.

• Franchise Ownership Workshop - Tuesday, November 11thfrom 6:30 pm - 8:30 pm. Learn the common myths andmisconceptions about franchises, franchise opportunities,legal obligations of owners and financing options.

Stay tuned for information about our Grand Openingcelebration, which will feature special offers and giveaways.For more information on the Affinity Flemington Branch, visitwww.affinityfcu.org/flemington or call 800-325-0808,ext. 3550.

WELCOME

14 Affinity Connections | FALL 2008

AG Transport, LLCAlchemy UnitedAmerica Healthcare Inc.Anderson Ward

Plantscapes, Inc.Andrews Plumbing &

Heating CompanyApplied Retail

Technologies LTDApril's CreationsAtlantic Rheumatology

and OsteoporosisAssociates, P.A.

AUMTECH, Inc.Awl Facility ManagementBernards Sports Chiropractic

& Physical RehabilitationBfade Services, LLCBooks To Books, LLCBorough of Glen GardnerBorough of New ProvidenceBridgewater Veterinary

HospitalBristol Management

Consultants, LLCC. Blue Group, LLCCar Toyz of NYC, LLCCardinal Technology

Solutions, LLCCasa Colombo

Civic AssociationCCW Car Service, LLCCenter for Advanced

Training & StudiesChoice Cuts BarbershopCitizen Scales Inc.Compass Maritime Services, LLCConvenient Power EquipmentDeSantis Construction, Inc.DJ Sweets EntertainmentDocument SolutionsDT General Contracting, LLCDumiec Holdings of

New Jersey, Inc.Edgerton Realty CorpElements of BeautyEquitable Metropolitan

Realty, LLC

Faithful Hands PowerWashing, LLC

Fito's Transport, Inc.Franklin Communication

Strategies, LLCG Lyfe Entertainment, LLCGamma 88 Inc.Garden of Beadin, LLCGEO Services, LLCGlen Gardner Fire CompanyGloriata Clinical Services, LLCGostyla Limited Liability

CompanyGrass Roots Lawncare &

Garden Svc.GuidoliciousHair Affair At The CarterHenry & James Pavenski

Modern Home Const. Co.Holiday CreationsHolly ConsultingHome Décor Designs, LLCHope HouseHorizon Landscape CompanyHunterdon Central Jr. Devils

Youth Football ClubHYJ Partners/DBA MunicaterIndigo Restaurant, Bar CateringIQE RF, LLCITV Ventures ProductsJ.J.L.L., Inc.Joseph's Landscaping, Inc.Kenneth B. Beckman

Dental ClinicKeystone Plastics Inc.KGH Enterprises, LLCKnobbery.Com., LLCKnowlton Construction, LLCLaw and Mediation of

Michelle LeonardLink High Tech.Manik Media, Inc.Mayer CateringMcDonald's RockawayMedia Logic, Inc.Millionaire Holdco, LLCMilon Builders, LLC

Mom's Against PredatorsNiros Colonial Corner

Autobody, Inc.Office Solutions, Inc.Pawtastic Pet Sitting, LLCPBR Group, LLCPerfect Storm Apparel, LLCPerfection DetailingPhotografismPlaza Lanes Inc.PRUDENTMDR&N Transport, LLCRevelation Kids, LLCRiverview Lawns, LLCRMKANE Consulting, LLCSam Ash & CompanySandello's Plumbing & HeatingSeaGate International, LLCSincere LegendsSneha Software SolutionsSPG TennisStinky Pete's Grooming

Salon, LLCSTL Systems, LLCStorage Assets, LLC DBA

Lackland Self StorageTaamba Hardware CompanyTents, Chairs & Party

Wares, Inc. T/A AdamsRental & Sales

The Historical Society ofthe Somerset Hills

The Trademark Company, LLCTony R. Construction, Inc.Total Health Physical

Medicine &Rehabilitation Center

Totowa Pediatric GroupTownship Of Mt. OliveTradition Home

RemodelingUnclejesses Travel/

World VenturesVision Systems Group, Inc.Whitlock PackagingCorporationWorld GymZ Mark, LLC

Since the last edition of Affinity Connections, the following companies have joined theAffinity Federal Credit Union family as Select Employee Groups (SEGs). We’d like to thankyou for choosing Affinity. If you know of a business that wishes to take advantage of offeringthe benefit of Affinity membership to their associates, please have them call 800-325-0808.We’ll be happy to talk to them about the Affinity Federal Credit Union difference.

Thank You for Choosing Affinity

73 Mountain View Blvd.Basking Ridge, NJ 07920

C O N TA C T U S O N L I N E O R B Y C A L L I N G O U R M E M B E R S E R V I C E C E N T E R :

Std. Presort

PAIDPermit No. 225Warminster, PA

www.affinityfcu.org | 800-325-0808

F O R Y O U R C O N V E N I E N C E

Cert no. SW-COC-1980

Affinity’s Connections Magazine is printedentirely on Forest Stewardship Councilcertified paper. FSC certification ensures thatthe paper used in this magazine contains fibersfrom well-managed and responsibly harvestedforests that adhere to strict environmental andsocioeconomic standards. Please join Affinity inour commitment to improving the environmentby recycling this magazine.

Printed on recycled paper—50% recycled and 25% post-consumer waste.

Here is a listing of Affinity Public Access Branches and their hours:

Mountain View BranchMountain ViewCorporate Center

73 Mountain View Blvd.Basking Ridge, NJ 07920LobbyMonday-Wednesday, Friday,

8:30-4:00Thursday, 8:30-6:00Saturday, 9:00-1:00

Drive UpMonday-Friday, 8:30-6:00Saturday, 9:00-1:00

Bedminster Branch1520 Route 206 NorthBedminster, NJ 07921LobbyMonday-Wednesday, Friday,

8:30-4:00Thursday, 8:30-6:00Saturday, 9:00-1:00

Drive UpMonday-Friday, 8:30-6:00Saturday, 9:00-1:00

Cedar Knolls BranchMorris County Mall235 Ridgedale Ave.Cedar Knolls, NJ 07927Monday-Friday, 8:30-6:00Saturday, 9:00-1:00

Denville BranchSaint Clare’s Hospital25 Pocono RoadDenville, NJ 07834Monday-Wednesday, Friday,

8:30-4:00Thursday, 8:30-6:00Saturday, 9:00-1:00

Dover BranchSaint Clare’s Hospital400 W. Blackwell StreetDover, NJ 07801Monday-Wednesday, Friday,

8:30-4:00Thursday, 8:30-4:30

Flemington Branch275 Route 202 South/31 South

Flemington, NJ 08822Monday-Wednesday, Friday,

8:30-6:00Thursday, 8:30-7:00Saturday, 9:00-1:00

Hillsborough BranchHillsborough Promenade315 Route 206 NorthHillsborough, NJ 08844Monday-Wednesday, Friday,

8:30-6:00Thursday, 8:30-7:00Saturday, 9:00-1:00

Middletown BranchCountry SquareShopping Center

1860 Route 35 SouthMiddletown, NJ 07748Monday-Friday, 8:30-6:00Saturday, 9:00-1:00

Morristown BranchCountry Mile Village1098 Mt. Kemble Ave.Morristown, NJ 07960LobbyMonday-Thursday,

8:30-4:00Friday, 8:30-5:00Saturday, 9:00-1:00

Drive UpMonday-Friday, 8:30-6:00Saturday, 9:00-1:00

New Providence BranchA&P Shopping Center598 Central Ave.New Providence, NJ 07974Monday-Friday, 8:30-6:00Saturday, 9:00-1:00

Paramus BranchAT&T Wireless15 East Midland Ave.Paramus, NJ 07652Monday-Wednesday, Friday,

8:30-4:00Thursday, 8:30-5:30

Piscataway BranchNext to IHOP1342 Centennial Ave.Piscataway, NJ 08854LobbyMonday-Wednesday, Friday,

8:30-6:00Thursday, 8:30-7:00Saturday, 9:00-1:00

Drive UpMonday-Wednesday, Friday,

8:00-6:00Thursday, 8:00-7:00Saturday, 9:00-1:00

Not near one of these branches? You can also access youraccounts via 50,000 surcharge-free ATMs, 1,700 shared branches,or through Internet Home Banking. For information, visitwww.affinityfcu.org/locator.