Affiliate Monitor€¦ · products, lead generation and paid-for betting tips, onto separate sites....

22

Affiliate Monitor October 2019 Written by Clear Concise Media for iGB

Transcript of Affiliate Monitor€¦ · products, lead generation and paid-for betting tips, onto separate sites....

Affiliate MonitorOctober 2019

Written by Clear Concise Media

for iGB

Published October 2019

© 2019 iGaming Business Ltd

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without the permission of the publisher.

The information contained in this publication is believed to be correct at the time of going to press. While care has been taken to ensure that the information is accurate, the publishers can accept no responsibility for any errors or omissions or for changes to the details given.

Readers are cautioned that forward–looking statements including forecasts are not guarantees of future performance or results and involve risks and uncertainties that cannot be predicted or quantified and, consequently, the actual performance of companies mentioned in this report and the industry as a whole may differ materially from those expressed or implied by such forward–looking statements.

Author: Scott Longley

Editor: Stephen Carter, Joanne Christie

Typesetting: Character Design

Published by iGaming Business part of Clarion Events.

Registered office: Fulham Green Bedford House 69–79 Fulham High Street London SW6 3JW

Tel: +44 (0) 207 384 7763

Registered number: 3934419

iGaming Business • Affiliate Monitor • October 2019 iii

Contents

Editor’s letter .................................................................................................................... 1

Executive summary .................................................................................................... 2

Part 1Analysis of second quarter results .............................................................................3

Part 2: The US affiliate opportunity ..........................................................................................9

Part 3: RAIG and the regulatory push and pull plus Portugal opportunity ..........12

Part 4: M&A update .........................................................................................................................16

iGaming Business • Affiliate Monitor • October 2019 1

Editors Letter

Editor’s letter

The headline development this quarter is that Better Collective’s

stronger momentum in acquiring NDCs, as predicted in our last

report, has seen it overhaul Catena Media in this crucial KPI.

Catena is still the largest performance marketer among its listed peers

based on the headline metrics of revenue and EBITDA, but quarterly

NDC volumes have clearly been tailing off since it took its foot off the

consolidation pedal.

CEO Per Hellberg subsequently announced a number of SEO-focused

turnaround measures designed to address a situation the company is

‘clearly not happy’ about and promised analysts they will do better in H2.

The Catena boss also revealed the direction of travel in terms of value

per individual NDC was in the opposite direction to volume, up to €235 in 2Q19 from €170 in 4Q18.

With regulation continuing to subdue performance in markets such as Sweden, Spain, France and

Italy, geographic expansion was also a common theme of the Q2 earnings releases and analyst calls,

with the likes of Latam, Japan and India – and of course the US – all figuring.

In the US, affiliates of course face several hurdles on top of the state-by-state rollout, not least the

huge DFS player databases of FanDuel and DraftKings reducing these brands’ need for affiliates and the

absence of online operations in the initial launch phase in some states.

Gambling.com Group’s Charles Gillespie also makes the point that US regulators prioritising

‘suitability’ above black and white rules on advertising and problem gambling controls could

conceivably see the sector run into the same problems as we are now seeing in the UK and Sweden.

We hope you enjoy this report and find it useful. Should you have any suggestions or feedback please

don’t hesitate to email me at [email protected]

Stephen CarterEditorial director, iGaming Business

iGaming Business • Affiliate Monitor • October 2019 2

Executive summary

Executive summary

The big news from the second quarter

results from the listed affiliates is the

change at the top in the key metric of new

depositing customers (NDCs). Better Collective

has taken top spot from Catena Media with an

NDC count of 111,000 in the three months to June,

compared with just under 100,000 for its rival

over the same period.

It is, of course, only one metric; Catena Media

still leads the sector in terms of revenues with

€23.7m in the second quarter versus €15.8m over

at Better Collective. It is also ahead on EBITDA

with €9.4m versus €7.0m.

This change at the top on NDCs comes at an

important stage of development for the sector

as a whole. The opening up of the US sports

betting market has presented the affiliate

sector with a huge new potential opportunity

and the sector leaders have not been slow to

make their moves.

Catena Media had already bought its way into

the US prior to the repeal of PASPA and now

Better Collective has made its own move, buying

first a 60% stake in the RotoGrinders Network for

$21m (with an option to buy the remaining 40% in

three to five years) and then following it up with

the VegasInsider.com and ScoresandOdds.com

buyout in July for $20m.

These are big statements on intent and taken

with the other moves in the US from Catena and

the rest, it is fair to say the largest companies

in the sector have pivoted towards the sports

opportunity in the US. Whether they will succeed

is a question that will – as with the operators –

take some time to answer.

The timing of the US opportunity could not

have been better given the extent to which the

regulatory pressure in Europe continues to be

ratcheted up on affiliates as much as operators.

References to issues in the UK, Sweden, Spain,

France and Italy pepper the results statements

of the listed firms and all go to illustrate the

degree to which the regulatory embrace now fully

encompasses the affiliate sector.

In response, three leading names within the

affiliate space have launched a new organisation

called Responsible Affiliates in Gambling (RAIG),

with which they hope to encourage best practice

in the sector while also providing it with a voice

for the first time.

How the sector evolves from this point will be

of interest to the operators as much as to those

involved in the affiliate space. As ever it should

be noted that the listed firms that this report

concentrates on are not the whole market, but

together they provide an informative straw in the

wind and help provide an understanding of the

market as a whole.

iGaming Business • Affiliate Monitor • October 2019 3

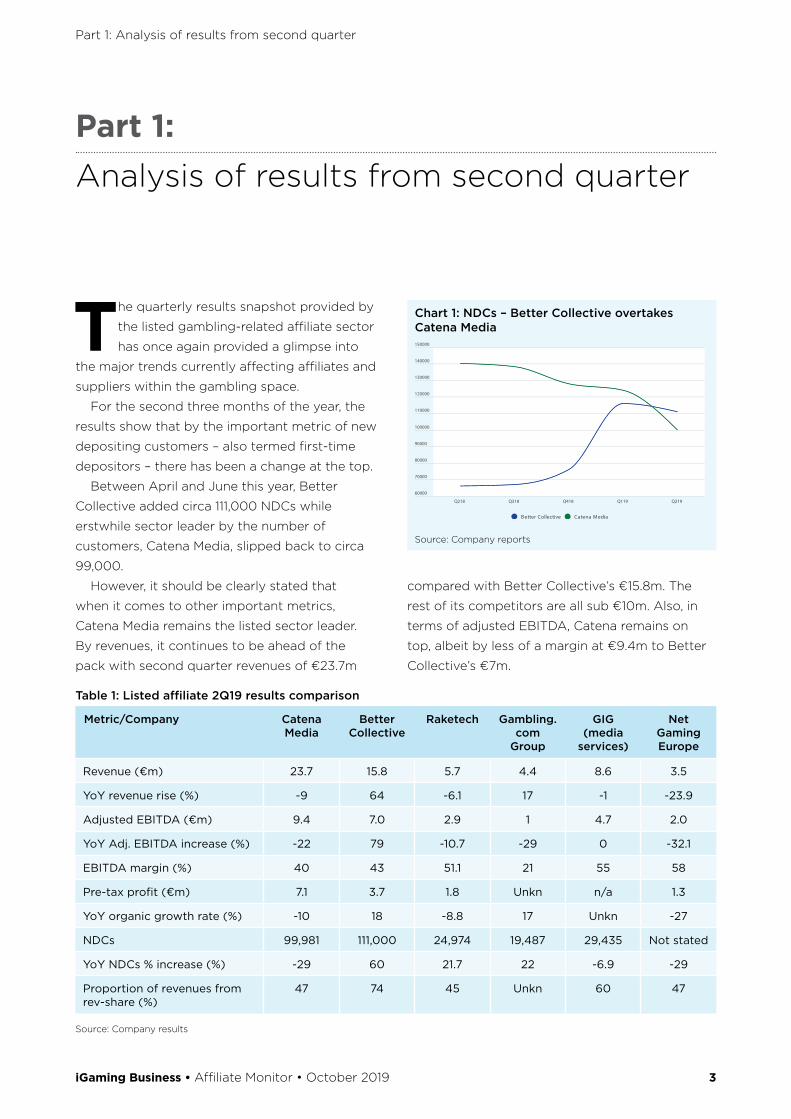

Part 1: Analysis of results from second quarter

compared with Better Collective’s €15.8m. The

rest of its competitors are all sub €10m. Also, in

terms of adjusted EBITDA, Catena remains on

top, albeit by less of a margin at €9.4m to Better

Collective’s €7m.

The quarterly results snapshot provided by

the listed gambling-related affiliate sector

has once again provided a glimpse into

the major trends currently affecting affiliates and

suppliers within the gambling space.

For the second three months of the year, the

results show that by the important metric of new

depositing customers – also termed first-time

depositors – there has been a change at the top.

Between April and June this year, Better

Collective added circa 111,000 NDCs while

erstwhile sector leader by the number of

customers, Catena Media, slipped back to circa

99,000.

However, it should be clearly stated that

when it comes to other important metrics,

Catena Media remains the listed sector leader.

By revenues, it continues to be ahead of the

pack with second quarter revenues of €23.7m

Part 1: Analysis of results from second quarter

Table 1: Listed affiliate 2Q19 results comparison

Metric/Company Catena Media

Better Collective

Raketech Gambling.com

Group

GIG (media

services)

Net Gaming Europe

Revenue (€m) 23.7 15.8 5.7 4.4 8.6 3.5

YoY revenue rise (%) -9 64 -6.1 17 -1 -23.9

Adjusted EBITDA (€m) 9.4 7.0 2.9 1 4.7 2.0

YoY Adj. EBITDA increase (%) -22 79 -10.7 -29 0 -32.1

EBITDA margin (%) 40 43 51.1 21 55 58

Pre-tax profit (€m) 7.1 3.7 1.8 Unkn n/a 1.3

YoY organic growth rate (%) -10 18 -8.8 17 Unkn -27

NDCs 99,981 111,000 24,974 19,487 29,435 Not stated

YoY NDCs % increase (%) -29 60 21.7 22 -6.9 -29

Proportion of revenues from rev-share (%)

47 74 45 Unkn 60 47

Source: Company results

Chart 1: NDCs – Better Collective overtakes Catena Media

60000

70000

80000

90000

100000

110000

120000

130000

140000

150000

Q218 Q318 Q418 Q119 Q219

Better Collective Catena Media

Source: Company reports

iGaming Business • Affiliate Monitor • October 2019 4

Part 1: Analysis of results from second quarter

Yet NDCs are an important measure of the

health of any affiliate organisation and Catena’s

relative decline in this area is worthy of some

analysis.

NDC focusDuring the second quarter results analyst call,

Catena Media repeated the message from its

capital markets presentation from last November

that it was quality rather than quantity that

mattered when it came to NDCs. As chief

executive Per Hellberg stated at the time, the

company “doesn’t talk about NDCs internally” and

“volume is not the key”.

Yet the NDC number still represents as good

a measure as any for the health of any gambling

affiliate’s business. The business is a funnel and

whether the affiliate’s revenues are dependent on

CPA or revenue share, the number of NDCs will be

the determinant for future revenues.

As such, the trend for Catena Media’s NDC

count will likely be the cause of some headaches

within the company.

The company was, of course, built on

acquisitions; as of last November it said it had

completed 34 deals and had collected more than

1,200 website brands. This strategy of pursuing an

affiliate space land-grab had achieved results and

between the first quarter of 2017 to the second

quarter of 2018, NDCs soared 74% from more than

80,000 to about 140,000.

However, in the four subsequent quarters this

metric has gone into reverse. Since Q318 the

quarter-on-quarter NDC trend has been negative,

with an average decline over the past four

quarters of 8% and a hefty 19% drop between the

first and second quarters of this year. In year-on-

year terms, meanwhile, the drop in the second

quarter is worse at nearly 30%.

The company has cited, variously, the effects

of regulation in key territories including the UK,

Sweden and, perhaps surprisingly France, where it

said the regulator had asked that it separate two

products, lead generation and paid-for betting

tips, onto separate sites.

In the UK, the company said that the KYC

Company “clearly not happy” with NDC numbers and “will do better in second half”Per Hellberg – Catena CEO

Chart 2: Catena Media’s NDCs rise and fall

160000

140000

120000

100000

80000

60000

40000

20000

0

Q117 Q217 Q317 Q417 Q118 Q218 Q318 Q418 Q119 Q219

80421 91222 100741 113258 133322 140154 138194 127805 124007 99981

NDCs

Source: Catena Media

Chart 3: The quarter-on-quarter NDC performance at Catena Media

-20

-15

-10

-5

0

5

10

15

20

25

Q117 Q217 Q317 Q417 Q118 Q218 Q318 Q418 Q119 Q219

%

QUARTERS

Source: Catena Media

iGaming Business • Affiliate Monitor • October 2019 5

Part 1: Analysis of results from second quarter

checks introduced earlier this year were the

source of delays in player activities and sign-ups

in May and June, while in Sweden Catena said

there was “no tangible improvement” due in part

to seasonal lows.

The company also blamed player winnings

which, it said, affected its revenue share

arrangements, particularly for AskGamblers.

During the second quarter results earnings

call, Hellberg said the company was “clearly not

happy” with the situation regarding NDC numbers

even as he repeated the message about quality

over quantity. He also suggested the company

was engaged in various remedial measures to

turn the situation around. These include the hiring

of more than 30 new SEO, product design and

management personnel, plus the hiring of external

agencies. These have been working on what the

company said have been, to date, 24,000 SEO

fixes across its vast website estate. “Our aim is

more NDCs,” he told analysts. “We will do better

in the second half.”

Catena also pointed to the value per NDC

figure, a somewhat newer metric in the affiliate

space. According to a chart produced in the

second quarter presentation, that figure had risen

from circa €170 in the fourth quarter of 2017 to

about €235 in the second quarter of this year.

NDCs comparisonsWhat is obvious from the results elsewhere in

the listed affiliate space is that Catena Media is

not alone in suffering a reverse in new player

numbers. Both the media services division within

Gaming Innovation Group (GIG) and Net Gaming

Europe also suffered year-on-year NDC declines.

Conversely Raketech and Gambling.com Group

– which although not listed has a bond listed on

the corporate bond list at Nasdaq Stockholm and

hence releases quarterly results – each followed

Better Collective’s lead with NDC rises of circa

22% each.

Given the variance in business models and

geographies across the listed affiliates, it is hard

to draw many conclusions from the numbers.

Regulation was cited as a drag also by Net

Gaming Europe and by Gaming Innovation Group,

along with the comparison from last year when

the World Cup took place partly during the

period.

At Raketech, the picture on NDCs was far more

upbeat, even though the company said during its

own earnings call with analysts that in Sweden

– which remains its biggest market – growth

had “stalled”. The Nordic region as a whole

represented nearly 97% of total second quarter

revenues.

We generally have high traffic levels on our sites, but player values remain at the lower levels, which we have noted since the beginning of the year.Michael Holmberg, Raketech

Table 2: Listed affiliates NDC comparison

Metric Catena Media

Better Collective

Raketech Gambling.com

Group

GIG Net Gaming Europe

NDCs Q219 99,981 111,000 24,974 19,487 29,435 Not stated

YoY NDCs % increase (%) -29 60 21.7 22 -6.9 -29

Source: Company reports

iGaming Business • Affiliate Monitor • October 2019 6

Part 1: Analysis of results from second quarter

The US aside, areas cited variously for

expansion include Latin America, with Spanish

and Portuguese language sites very much to the

fore, parts of eastern Europe including Romania,

and Japan and India.

Notably, there is a clear move towards

unregulated markets. While the focus for many of

the affiliates’ operator clients will be on regulated

markets, and the risks involved there, the affiliates

themselves will be seeking greener pastures in

markets where the regulatory framework is either

in the process of being built, such as Brazil, or

entirely absent, as in India and Japan.

“We generally have high traffic levels on our

sites, but player values remain at the lower levels,

which we have noted since the beginning of the

year,” chief executive Michael Holmberg told

analysts.

Geographic expansionThe dependence among many affiliates on key

regulated markets across Europe – previously

trumpeted by Catena Media as a strength – is

being addressed to varying degrees across the

listed sector. Of course, the US is already a major

area of activity and this will be dealt with later on

in this report.

Company-by-company results takeaways

Catena Media• Revenues of 23.7m, down 9%

• EBITDA of €9.4m, down 22%

• NDCs down 29% to 99k

The second quarter was one to forget for

Catena Media. The company laid out a host

of reasons for the revenue miss including

seasonality, regulatory pressure in the UK and

France, continuing issues with the Swedish

market, a drop-off in lower-value NDCs and

instances of higher player pay-outs in casino.

EBITDA target of €100m is nixedHaving previously abandoned its EBITDA

target of €100m, chief executive Per Hellberg

had to admit during the earnings call that the

target was “a long way away” at present. “The

ingredients are there to make that happen, but

costs will be a factor,” he said. No new target

date was set.

Geographic expansion plansOne remedy for Catena’s ills comes with

plans for further geographic expansion, with

sports being launched soon in Japan and

sport and casino slated for launch in Romania.

The company also said it would be dipping a

toe in South America with both Spanish and

Portuguese language sites planned.

Third quarter improvementsRemedial actions have taken place within the

past three months or more to improve under-

performing assets and Hellberg said that the

results of this were being seen in third quarter

trading to date.

Italy and FranceWhile discussions with the regulator in Italy are

ongoing, it was notable that Hellberg said that

trading in the market was “more or less dead

in the second quarter”, With Italy now below

10% of total revenues. In France the company

has two products, lead generation and paid-

for professional tips, and Hellberg said the

regulator had instructed these can no longer be

on the same site.

Raketech• Revenue down 6% to €5.7m

• Organic growth down 9%

• Adjusted EBITDA down 10% to €2.9m

• NDCs up 22% to circa 25k

iGaming Business • Affiliate Monitor • October 2019 7

Part 1: Analysis of results from second quarter

Raketech said continuing uncertainties in

Sweden and a tough comparative with last year

due to the World Cup were to blame for the

year-on-year revenue fall. Specifically, Holmberg

suggested the market in Sweden, Raketech’s

largest market, had “stalled”. Looking ahead, he

said early third quarter trends suggested player

values “will not decrease any further”.

Geographic expansionLatin America was again given a mention

and Holmberg also suggested the company

was looking at Spain and Italy. The results

came before the Japanese-facing Casumba

acquisition, which was prefigured by Holmberg

suggesting Raketech was “looking primarily

at Japan and India”. Unlike some of its rivals,

Raketech gave the impression that it was not

entirely convinced by the potential in the US.

“Short-term, we see better growth (prospects)

in other markets,” he told analysts.

Better Collective• Revenue up 64% to €15.8m

• Organic growth of 18%

• EBITA up 77% to €6.8m

• New depositing customers for the quarter at

111,000, up 60%

As the company said, this was a decent

performance given the World Cup comparatives

from last year. The key for Better Collective

will be execution in the US. The company was

more positive than some of its rivals regarding

Sweden, although it too suggested that in the

second quarter revenues had been “lower due

to seasonality”.

M&AAhead of the acquisition of UK-facing

mybettingsites.co.uk, chief executive Jesper

Søgaard suggested the company had a “good

position in the M&A space”. “We are also

looking at skill sets. And potentially markets or

environments where we feel sports betting is

important.” This pretty much fits the bill of the

mybettingsites.co.uk deal, where the ex-owner

Ian Bowden has remained in situ as the head of

the UK for Better Collective.

Geographic expansionAccording to Søgaard, the company believes

South America represents a “great opportunity”.

“We are already invested in that region; it is

quite high on our agenda.”

GIGB2B media highlights

• Revenues and EBITDA flat – €8.6m against

€8.7m last year and static at €4.7m,

respectively

• Sequentially, revenue down from €9.1m,

EBITDA down from €5.2m

• Revenue share was down to 60%; CPAs up

to 17%

• FTDs down from 31.4k to 29.4k

In his last presentation as CEO Robin Reed said of

the affiliate business that it had a “solid quarter”

given the World Cup comparatives from last year.

Though the media business remains stable, as the

company has noted previously, clearly the issues

going on elsewhere are having an impact on the

organisation as a whole. The flat-lining revenue

performance and slight decline in NDCs will likely

have been concerning to the board given the

business’s reliance on media services revenues.

Expansion plansIn terms of the geographic expansion of

the media division, the company said it had

received a licence to operate its affiliate

business in Romania.

Sale of Highroller.comAhead of the results, GIG announced it had sold

Highroller.com to Ellmount Gaming, an affiliate

business based in Malta.

iGaming Business • Affiliate Monitor • October 2019 8

Part 1: Analysis of results from second quarter

Net Gaming Europe • Revenues down 24% to €3.5m

• EBITDA down 32% to €2.0m

• NDCs down 29%, with casino NDCs down

33%

• 32% decline in US revenues “due to

competition” for PokerListings

Net Gaming Europe blamed its disappointing

performance on the regulatory backdrop

without talking specific countries (though

UK and Sweden are obvious problems). The

company is hoping to transition to more

revenue-share arrangements from CPAs and

said its results were impacted by this move.

However, it is still reliant on casino (69%) and

poker (13%) so no sports revenues as yet. It said

the fall in US revenues is down to competition.

Falling NDCs

CEO Marcus Teilman admitted that the move

to revenue share will hit the top line and the

NDCs figure. “We will get more stable revenues

over time. You can also see the NDCs decline

by 29% and revenues by 24% and that is related

to the difference between revenue share and

CPAs. Over time that will benefit us.”

Gambling.com Group• Revenues up 17% to €4.42m, all organic

• Adjusted EBITDA down to €0.99m from

€1.39m; EBITDA margin also down to 21%

from 37%

• NDCs up 22% to 19.5k

Gambling.com is making a big push in the US –

it has established an office there and launched

the American Gaming Awards – hence the fall in

EBITDA (presumably) due to the investment.

Investor shiftThe big news for the company came

subsequent to the results, however, when it

announced it had secured a $15.5m investment

from private equity firm Edison Partners. In the

press release announcing the deal, Gambling.

com said it believed the US opportunity

would be sizeable and would “grow to rival”

the European market in the coming years.

The press release said Edison is replacing an

existing shareholder at Gambling.com, but iGB

understands that this is not Mark Blandford, the

largest shareholder at the time of the issuing of

the listed bond issue.

iGaming Business • Affiliate Monitor • October 2019 9

Part 2: The US affiliate opportunity

What should we make of the US

opportunity for the affiliate sector

at present? The biggest two in the

sector are now positioned for picking up potential

US growth, yet the figures we have seen to date

suggest it will be a while before we see the

degree to which US sports betting may transform

the gambling affiliate space.

Catena Media is certainly betting that the US

will be central to its business in the years to come,

with chief executive Per Hellberg saying the

question was simply one of quantum and when

the uplift would kick in.

“We expect the higher numbers to come,” he

told analysts. “We had a very good July. We live

by previous statements. We think the US will

double our business.”

At present, analysts believe the US represented

circa 10% of Catena’s revenues in the first half and

with Pennsylvania coming on stream they expect

that percentage to rise to circa 15% by the end of

the year.

Hellberg referred to the good news on states

such as Pennsylvania opening up when he said

that with regards to the process of state-by-state

legislation, “everything improves for the better”,

not just for the second half of this year, but also

for 2020 and beyond. “We are very happy with the

Part 2: The US affiliate opportunity

outcome over there (in the US),” he added. “We

have a good reputation and want to build on it.”

The DFS problemOne aspect of the US business alluded to on the

call which will be examined closely is the degree

to which, in New Jersey at least, the affiliates

have been somewhat sidelined due to the daily

fantasy sport (DFS) beginnings of the early

market leaders. Both DraftKings and the Flutter-

owned FanDuel have extensive and ‘live’ customer

lists from their DFS operations, which they have

successfully relied on to fuel their market entry

into sports betting.

Hellberg suggested that Catena’s fortunes

would reverse once there was further operator

competition, particularly in New Jersey. “There

are also more operators and they don’t have the

databases,” he told the assembled analysts. “So

they will need more affiliation; it will take a larger

part of the revenues.”

This could well be true; the newer market

entrants – whether that is MGM, Bet365 or Fox

Bet – do not have the DFS customer lists of

DraftKings and FanDuel. But they do have other

strings to their marketing bows; MGM has the

huge M life customer loyalty scheme, while Fox

Bet has the Fox Sports ownership behind it, on

The degree to which affiliates have been sidelined due to DraftKings and FanDuel’s extensive and ‘live‘ customer lists from their DFS operations will be examined closely.

iGaming Business • Affiliate Monitor • October 2019 10

Part 2: The US affiliate opportunity

the US affiliates but there are others. Land-based

registration processes as adopted in some states,

particularly Illinois, for instance, will be the cause of

obvious problems, as will states that don’t initially

opt for online operations at all, such as New York.

There is a layer of cultural and consumer context

that also needs to be addressed, according to

Charles Gillespie, chief executive at Gambling.com

Group, which also has US ambitions.

“Particular types of content and the maturity

of the consumer differ significantly from Europe

so the actual execution does require a different

approach in terms of product,” he says.

This was also mentioned by Søgaard on the

earnings call. “We also expect it will need a

different and dedicated approach,” he said. “Each

state is like an individual country. Some products

can work across the entire US market whereas

others need to be tailored for a single state.”

The cultural differences extend to the

regulatory level. Gillespie points out that US

state regulators tend to “prioritise suitability”

over other aspects of corporate probity. As he

says, this is to, “make sure that the people in

the business have a clean background and are

suitable enough for the privilege of operating in

the regulated gambling sector”.

However, this approach makes some

assumptions about “suitable” businesses making

decisions regarding their commercial objectives

and to what extent the business should be

pushed to hit target.

“But businesses need black and white objective

rules handed down by the regulator to tell them

where the boundaries are, or they will simply push

as hard as they can,” he says. “The US regulators,

by and large, do not prioritise the issues that

top of the gaming experience of Stars. Bet365,

of course, may have more of a need for affiliate

marketing and that, along with many other

reasons, is why the Stoke company’s entrance on

the US scene is exciting so much interest.

To an extent, the DFS database issue has

effectively been confronted head on by Better

Collective, which bought out leading DFS-

related affiliate RotoGrinders in May. As Søgaard

acknowledged, this “brings an audience”. BC has

also subsequently added to its US presence by

snapping up two tips sites, VegasInsider.com and

ScoresandOdds.com.

“These two websites have been the platforms

preferred by millions of visitors and they have the

potential to become the largest revenue-generating

assets for Better Collective in the coming years,”

Søgaard said during the earnings call.

With both the RotoGrinder and VegasInsider

and ScoresandOdds deals, it is clear that Better

Collective has gone for established brands. “With

the regulated market, these sites are already

reaching the exact demographic we want to

target,” said Søgaard. “That’s why we see such a

big opportunity.”

Moreover, in partnering with NJ.com, one

of the largest publishers in New Jersey, Better

Collective is also aiming at pressing home its

message with a wider mass audience. “Clearly

we see this as an important business going

forward, as we are teaming up with publishers

that have huge traffic already,” said Søgaard,

who noted that the profit split on the NJ.com

deal was in Better Collective’s favour.

Further US hurdlesThe existing database issue is one problem for

The DFS database issue has effectively been confronted head on by Better Collective, which bought out leading DFS-related affiliate RotoGrinders in May.

iGaming Business • Affiliate Monitor • October 2019 11

Part 2: The US affiliate opportunity

really make a difference in online gambling, such

as sensible advertising restrictions and internal

controls to reduce gambling-related harm.”

Given such a scenario, it is entirely possible that

the sector will see similar issues arise in the US –

on the parts of affiliates and their own marketing

attempts – as have been highlighted in the UK

and Sweden. How the regulators react in such

circumstances will have a big role to play in the

success of the gaming affiliates working in the US,

whether homegrown or hailing from Europe.

The last word on the US comes from Ben

Robinson, partner at RB Capital. He makes the

point that the battle for market position that takes

place in the short- to medium-term might be one

where the affiliate sector could well be a bystander.

“The US market will be immense… at some

point in the future,” he says. “However, while

affiliation plays an integral part in the acquisition

funnel in other markets around the globe,

dominant brands in the USA already have such a

massive head start. Whether affiliates fit into the

equation in a significant way, I’m not putting my

money on that horse.”

Businesses need black and white objective rules handed down by the regulator to tell them where the boundaries are, or they will simply push as hard as they can.Charles Gillespie, Gambling.com Group

iGaming Business • Affiliate Monitor • October 2019 12

Part 3: RAIG and the regulatory push and pull

No one in the gambling affiliate sector

needs reminding of the growing

importance of regulation to the business.

It’s therefore no surprise that a new organisation

should have emerged with the express intention

of giving visibility to affiliate efforts in the arena of

responsible gambling.

However, whether the founding companies

behind the Responsible Affiliates in Gaming

(RAIG) will achieve their aim of signing up large

numbers of affiliates to their initiative is at present

open to question.

To recap, RAIG was formed in May by Better

Collective, the Racing Post and Oddschecker with

the express intention of helping “raise standards”

in the sector and foster further initiatives in the

area of social responsibility and to “help create a

safer gambling environment for consumers”.

As a condition of membership, each

organisation will submit itself to an audit by

independent third party Gambling Integrity.

Yet, while there was some fanfare in May

and widespread appreciation for the fact that

the affiliate sector was at least coming up with

some form of response to the pressure it is

facing, particularly in the UK, there have been

murmurings of discontent from some corners of

the sector.

Part 3: RAIG and the regulatory push and pull

Phil Blackwell, acquisitions operations manager

at Lindar Media, says that the £20,000 fee and

the loading of the board with members from the

founding partners, as well as Clive Hawkswood,

the ex-Remote Gambling Association (RGA) chief

executive, makes it look very much like a stich-up

in favour of the larger affiliates. Noting the lack

of activity since May, he suggests “it has all gone

quiet”. “If nobody supports it then it will have no

authority and it will fall apart,” he warns.

Certainly, Søgaard from Better Collective

said on the company’s earnings call that “more

affiliates need to come on board”. “It’s not just

the smaller affiliates that can cause issues for

the larger affiliates,” he said. “It’s any affiliate. We

have seen what can happen in the UK where the

authorities thought they had to crackdown.”

Paying heed to regulationSarah Ramanauskas, senior partner at Gambling

Integrity, says that “absolutely, standards need to

be raised for affiliates”.

“They are currently one of the weakest links in

the industry’s efforts to ensure compliance with

the many and varied aspects of responsible and

safer gambling in the UK,” she adds.

“The industry as a whole needs to work

together more closely and this includes affiliates.

If nobody supports [RAIG] then it will have no authority and it will fall apart.Phil Blackwell, Lindar Media

iGaming Business • Affiliate Monitor • October 2019 13

Part 3: RAIG and the regulatory push and pull

One of the aims of the RAIG audit is to create a

knowledge base of best practice, making it easier

for affiliates to understand what needs to be done

to comply with the many and varied UK regs, and

how best to do so.”

Ian Sims, chief executive at affiliate compliance

tools provider Rightlander, points out that the

organisation is still in its formative stages and

that it “shows promise”. But he adds a note of

scepticism. “I’ve heard some affiliates say it sounds

like a bit of a closed shop but when the premise

was first touted around, it met with a lot of verbal

support but no real commitment,” he says. “A lot

of affiliates liked the idea as long as someone else

was doing it and prepared to pay for it.”

He suggests that we will know the fate of RAIG

in six months. “These things are always easy

to criticise when you aren’t involved and don’t

understand what’s going on,” he adds.

Regardless of the fate of RAIG, there is unlikely

to be any relenting in the pressure that affiliates

find themselves under in regulated markets. And

it won’t just be the largest affiliate organisations

that see greater scrutiny as the price of doing

business, says Adam Bielinski from iGaming Nuts.

“We prefer to stay in the regulated markets,” he

says. “It is easier to calculate long-term revenues

and costs, which is less risky. It is easier to invest

in people and products when we know that

market will not change for a few months.”

Whether this message is being fully received

across the sector is open to doubt, however. Sims

says there has been “more engagement” from the

affiliates he has spoken to, adding that there is

recognition among them that “one bad apple is a

threat to all of them”.

He adds: “No affiliate wants a programme to

close down in a lucrative market but it’s a very

real prospect once the fines start rolling in.

“There is a still a little confusion over what is

needed but it is much clearer than a year ago and

generally speaking it is often down to a lack of

investment in time to learn and understand what

is needed.”

Ad bansThe UK regulations aside, the clearest threat to

the gambling affiliate sector comes from the

potential proliferation of gambling advertising and

marketing bans. As was noted in the first quarter

edition of Affiliate Monitor, Italy was the first to

instigate an outright ban and both operators

and affiliates are still attempting to understand

precisely what is and isn’t allowed.

According to Catena Media, the effects of the

new regulations – which came fully into force

in July – were “not as severe as expected” and

“detailed work by our compliance/legal teams

means our assets remain in a strong position there”.

As it stands, odds comparison sites are still

allowed under the Italian regulations although

whether this provision will stand should any new

Italian government, of whatever stripe, look once

again at the rules is very much open to question.

What can’t be doubted, however, is that ad

bans are a growing threat. The latest jurisdiction

to announce moves is Spain though the news

from there is somewhat confusing. While the

official Ombudsman has said that his proposals

for an outright ban, first published in May, had

been accepted in full by the government, recent

reports suggest that the Ministry of Finance has

[Affiliates] are currently one of the weakest links in the industry’s efforts to ensure compliance with the many and varied aspects of responsible and safer gambling in the UKSarah Ramanauskas, Gambling Integrity

iGaming Business • Affiliate Monitor • October 2019 14

Part 3: RAIG and the regulatory push and pull

said that the final decision has yet to be taken.

With rumblings of discontent over gambling

advertising also being voiced in Sweden and

Denmark, the direction of travel across regulated

Europe is certainly worrying for operators and

their affiliate marketing partners.

Yet, as Sims suggests, with the affiliate space

having shown itself to be resourceful throughout

the years, ad bans might yet be an opportunity as

much as a threat given the likelihood that, as with

Italy, loopholes around affiliate marketing could

leave them as the only game in town.

He concludes that the mix of regulation and

technology, as well as the changing nature of

the affiliate landscape due to continuing M&A,

simply means more affiliates will have to adapt

to survive. “The days of opinion-based content

writing are probably drawing to a close in many

markets but there are many other ways to find

customers with a bit of resourcefulness,” he says.

Ad bans might yet be an opportunity as much as a threat given the likelihood that, as with Italy, loopholes around affiliate marketing could leave them as the only game in town.

Grass is greenerOne potential solution to the threat of being

tied down by red tape in regulated markets is

to look at further geographic expansion.

While Asia obviously got a mention by a

number of firms – and Raketech subsequently

announced a deal for the Japanese-facing

Casumba – the possibility of expanding into

Spanish and Portuguese language versions of

various sites was also discussed.

Catena Media said it would be launching its

AskGamblers sites in both languages in the

third quarter, Better Collective said Spain was

not core but was “meaningful” and Raketech

said it was looking at South America as a

potential region for expansion.

It is important to understand at this point

that any efforts towards either Spanish or

particularly Portuguese language versions of

successful sites likely is, as suggested above,

more about South American opportunities than

about either Spain or Portugal.

In the last case, certainly, the opportunities

for affiliates are necessarily limited due to the

low number of licensees. With only 11 operators,

the Portuguese online market offers affiliates

precious few firms to work with.

The problem with PortugalThe issue, of course, is the nature of the

regulated regime in Portugal and the tax rates

applied across both sports betting and online

casino.

Table 1: Portugal tax rates breakdown

Product Initial tax rate (on turnover) (%)

Upper rate threshold

Effective upper tax rate (%)

Sports betting 8 €30m 16

Gaming 15 €5m 30

iGaming Business • Affiliate Monitor • October 2019 15

Part 3: RAIG and the regulatory push and pull

Yet, if the number of market participants

has been held back due to the tax rates, gross

gaming revenues have sustained reasonable

growth since the new regime was instigated in

2015, with 24% growth seen last year. Indeed,

growth in the first half accelerated and was up

36% to €95.6m.

Still, the market remains small and hopes that

the government might revisit the tax rates issue

are in abeyance after a government working group

missed a reporting deadline earlier this year.

Player numbersThe relatively underdeveloped market is

confirmed by the latest data from the Gambling

Regulation and Inspection Service (SRIJ), which

suggested there were circa 297,000 active

accounts in the first half. This compares with

a cumulative player account number of 1.41m

registered since 2016.

The data showed that just under 50% of

the first half total made a sports bet only, 35%

played casino only and only 14% engaged with

both products.

Gabino Oliveira, president of the Portuguese

operator association APAJO, says the number

of active accounts measured places Portugal

in the average range for accounts per head of

population across Europe and in line with the

figures from France and Spain.

Moreover, and this is definitely worth bearing

in mind when it comes to affiliate activity in

and around Portugal, Oliveira cites research

undertaken by APAJO that suggests that

an increasing number of gamblers play with

licensed websites because they appreciate that

these sites are more secure and that pay-outs

will be quicker.

“The survey also found out that Portuguese

customers are extremely well informed about

which operators hold licenses and which do

not,” he added. “In fact, after three years into

the opening, the top four chosen operators by

customers are all licensed in Portugal.”

Oliveira believes the regulatory embrace

clearly evident in the UK and Holland of late is

finding echoes in the Portuguese market. “We

see today that the risk appetite diminishes with

this stricter approach on behalf of regulators,”

he says.

iGaming Business • Affiliate Monitor • October 2019 16

Part 4: M&A round-up

While there has been some semblance

of M&A activity over the summer,

with deals involving Raketech, Net

Gaming Europe and Better Collective, the general

trend towards less acquisitions than in the buyout

frenzy of 2017-18 remains the central case.

Better Collective aside, the trend towards

fewer acquisitions has been matched by similarly

lower levels of transaction prices. At the peak in

2017/18, buyouts closer to €10m were common;

now, Better Collective’s deals in the US aside, the

money being splashed out is very much in the

lower single-figure millions.

Part 4: M&A round-up

Those seeking an answer for why the pace

of M&A has slackened have a range of potential

reasons. Clearly, the fact that the most voracious

player Catena Media has effectively shut up

shop on M&A pending the digestion of its 34

acquisitions up to November last year is one

reason for the slackening of the pace of deals.

The company itself has signalled that its

buying spree has come to a temporary halt.

The quality over quantity strategy is in itself an

admission of that and Hjalmar Ahlberg, analyst at

Kepler Cheuvreux in Stockholm, certainly thinks

that Catena has at least temporarily placed the

We recently scanned some acquisitions for a big affiliate to help them check if historical content was compliant in the territory the site was targeting, so it’s certainly on acquirers’ minds.Ian Sims, Rightlander

Table 2: Acquisitions in the affiliate space May-September 2019

Date Acquirer Target Market focus Initial price

May-19 Better Collective RotoGrinders US sports $21m

Jun-19 Raketech CasinoFever.ca Canada Unkn

Jun-19 Net Gaming Europe BettingGuide.se Sweden Unkn

Jul-19 Net Gaming Europe BettingOnline.co.uk UK £1.6m

Jul-19 Better Collective VegasInsider/

ScoresAndOdds US sports $20m

Aug-19 Raketech Casumba Japan €2m

Sep-19 Better Collective MyBettingSites UK £1.5m

Source: Affiliate Monitor

iGaming Business • Affiliate Monitor • October 2019 17

Part 4: M&A round-up

chequebook back in the drawer.

As he suggests, Catena Media now has

“limited funds” to spend on acquisitions given

its committed earnout payments. As of the end

of the second quarter, €53.5m of asset purchase

commitments are outstanding, of which circa

€25m is to be paid in cash.

Another reason for the general slowdown

in M&A in the affiliate space comes as a by-

product of the previous frenzy – the inflated

expectations on the part of vendors. Catena and

the others have been keen to stress they will

only pay multiples of EBITDA within set limits

but that doesn’t stop those being approaching

overestimating what they think their business is

worth. A big enough valuation gap could easily

put paid to many a deal.

Then there is the regulatory shadow spoken

about earlier in this report. Sims at Rightlander

suggests that ensuring that the content on your

site is compliant will be a big factor in all future

deals. “We recently scanned some acquisitions for

a big affiliate to help them check whether historical

content was actually compliant in the territory the

site was targeting so it is certainly on the mind of

an acquiring party, that is for sure,” he adds.

“Popular M&A targets (apart from special

situations and distressed assets) are rarely

situated in markets that face uncertainty,” says

Robinson from RB Capital. “Multiples are directly

related to the return on a buyer’s investment

(ROI) and how fast they can recoup the purchase

price and start generating profit. When a market

faces uncertainty, the sustainability of a business

is unclear.”

Then there is the issue of the compound annual

growth rate of the business and what that means

for multiples. “Unless an affiliate is bucking the

trend that is facing the majority of UK affiliates,

this will be reduced considering the challenges

(currently facing the affiliate sector),” he says.

Sector consolidation and client concentration riskOne aspect of the drive towards bigger affiliate

businesses is the risk it poses in terms of client

concentration. The most visible relationship in this

regard is between Better Collective and its main

client Bet365. According to an analyst initiation

note from the team at Redeye in May this year,

Bet365 accounts for circa 25% of total revenues,

while the Better Collective IPO document in

2018 said that the top 10 clients were worth

circa 52% of total revenues. However, this latter

Popular M&A targets (apart from special situations and distressed assets) are rarely situated in markets that face uncertainty.Ben Robinson, RB Capital

Better Collective’s top 10 clients were worth circa 52% of revenues according to the IPO document, while Gambling.com Group’s were worth 59% according to its bond prospectus. Neither percentage is thought to have significantly changed since listing.

iGaming Business • Affiliate Monitor • October 2019 18

Part 4: M&A round-up

figure isn’t necessarily a standout. According to

the Gambling.com Group bond prospectus, the

company made 59% of total revenues from its top

10 clients.

Neither percentage is thought to have

significantly changed since being made public

and indeed Jonas Amnesten, analyst from

Redeye, says that further consolidation will likely

bring even further concentration with “fewer

larger clients with larger purchasing power”.

Nevertheless, in the case of Better Collective

and Bet365, Amnestan sees the greater reliance

as a plus. Bearing in mind Bet365’s recent launch

in the US, his comment that he views the close

partnership with Bet365 as “primarily a strength

in the ongoing expansions” is significant.

iGaming Business Fulham Green, Bedford House

69 - 79 Fulham High StreetLondon, SW6 3JW

Tel: +44 (0) 207 384 7700

www.igamingbusiness.com