Advanced Airline Sourcing - - Get a Free Blog Here

54

1 Advanced Airline Sourcing Scott Gillespie Managing Partner tClara – Travel Data Made Brighter August 2013 San Diego © 2013 Scott Gillespie

Transcript of Advanced Airline Sourcing - - Get a Free Blog Here

1

Advanced Airline Sourcing

Scott Gillespie Managing Partner tClara – Travel Data Made Brighter August 2013 San Diego

© 2013 Scott Gillespie

2

About Scott Gillespie

Leading expert on travel procurement, data analysis and Managed Travel 2.0

Managing Partner of tClara, an on-demand data analysis shop specializing in the travel category

Author of a U.S. patent covering airline bid analysis

Author, “Gillespie’s Guide to Travel+Procurement”

Founder and CEO of Travel Analytics, the industry’s leading independent travel consultancy (1999-2008)

A.T Kearney’s global expert on travel sourcing (1993-1999)

MBA, University of Chicago

3

Where we’re headed

• Key concepts

• Assessing your supplier landscape

• The impact of the AA-US merger on airfares

• Building good scenarios

• Finding the best negotiating targets

• Analyzing your options

• Avoid these mistakes

• Q&A

4

Revenue Management Illustration

Illustrative 100-seat Aircraft

$50,000

$900

X 30 Seats

$400

X 70 Seats

$55,000

$500

X 100 Seats

$1,500

X 10 Seats

$1,200 X 20 Seats

$700

X 30 Seats

$300 X 40 Seats

$72,000

5

Airfare Inventory Booking Classes – Coach Cabin

Illustrative

Airfare Inventory Classes

High prices help ensure last-minute

availability

Low prices make planned trips more

affordable

Less Flexible

Lower Quality Product

More Flexible

Higher Quality Product

6

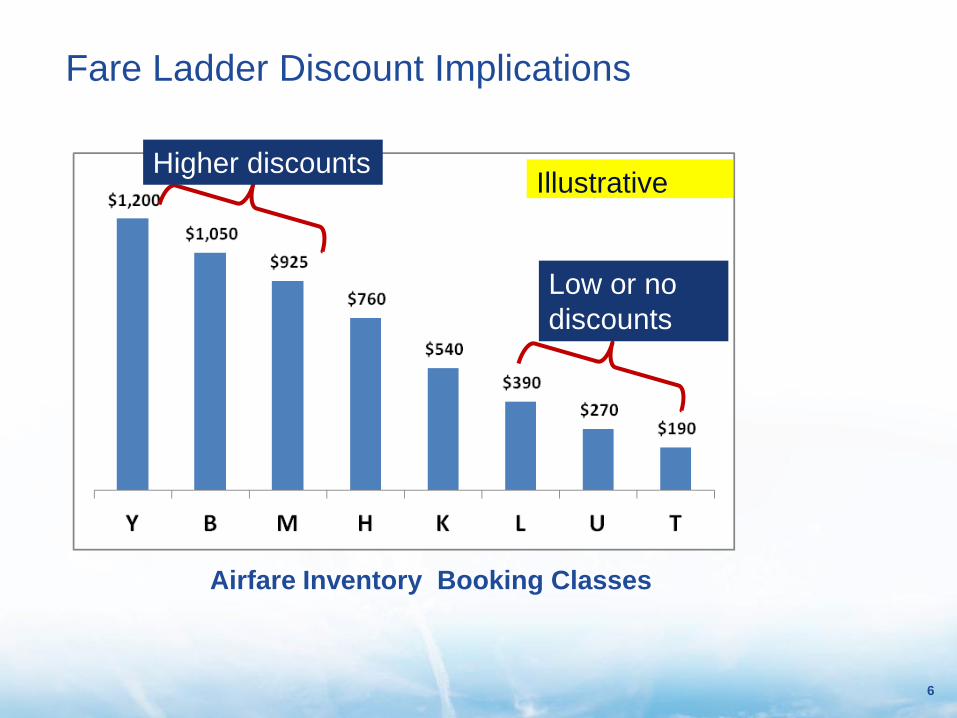

Airfare Inventory Booking Classes

Illustrative

Fare Ladder Discount Implications

Higher discounts

Low or no

discounts

7

Standard Air Sourcing Data Fields Key Field: POS-CP-CR-BC Two Data Fields

Each in-

scope

country

Non-

directional

airport

codes

Trimmed

from fare

basis code.

NOT Cabin

Half a round

trip, regardless

of connections

8

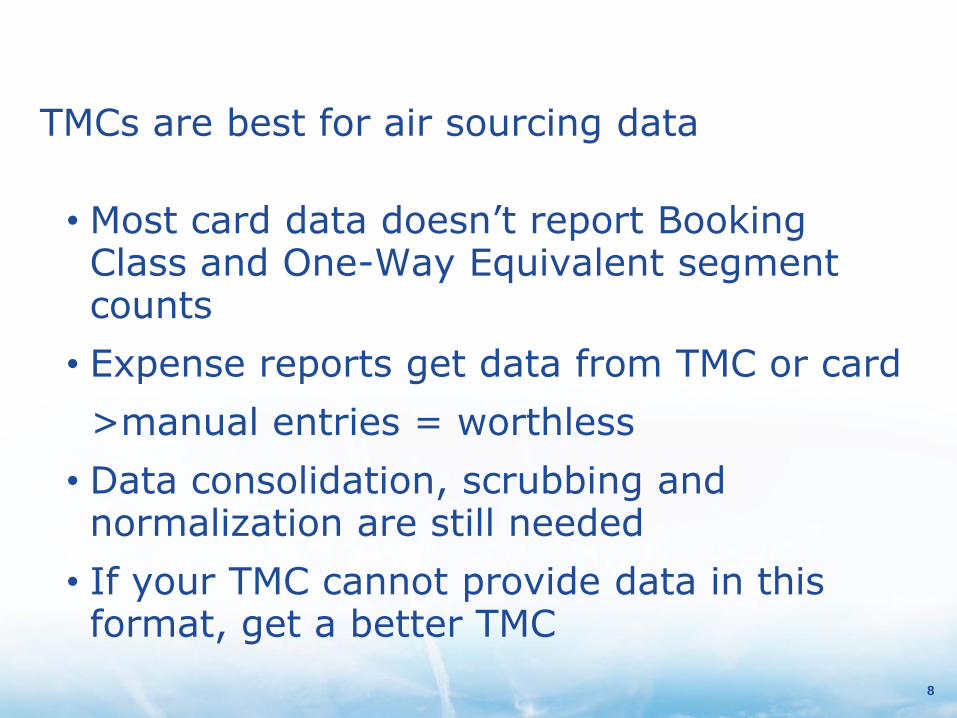

TMCs are best for air sourcing data

• Most card data doesn’t report Booking Class and One-Way Equivalent segment counts

• Expense reports get data from TMC or card

>manual entries = worthless

• Data consolidation, scrubbing and normalization are still needed

• If your TMC cannot provide data in this format, get a better TMC

9

More market share!

Lower prices!

made simple

Airline sourcing

10

Recognize

a good deal

11

Q: Which is the better deal? A. 30% off F, C, Y, B and M in all markets

served globally by United, or

B. 10% off all fares in all markets served by Delta from Atlanta and Minneapolis

A: Depends on

• Your travel footprint (city pairs)

• Each airline’s coverage

• Your fare mix

12

Fair Market Share (FMS), aka QSI or Quality of Service Index

• Measures neutral capacity, before price or brand loyalty

• Expressed as a percentage of the market, e.g.,

–AA’s FMS in DFW<>JFK is 54% (illustrative)

• Time periods, connections and direction can matter a lot

13

Fair Market Share is the airline’s expected share of seats in a market,

based on seats, schedules and routings

Airport A Airport B

Delta

100 seats a day

United

100 seats a day

Fair Market Share Delta’s FMS = 50%

United’s FMS = 50% (assumes wing-to-wing

schedules)

14

Fair Market Share

Airport A Airport B

Delta

100 seats a day

United

100 seats a day

Delta’s FMS = 40%

United’s FMS = 40%

Southwest = 20%

Connecting Airport

Southwest

100 seats a day

Less weight for connections, and for longer connections

15

Getting FMS: Inputs are City Pairs and their spend

Fair Market

Share (FMS,

aka QSI)

Calculator

Beware – many versions of “Fair”

- include or ignore extra connections?

- JV/Alliance/Interline, or not?

- Define “good” connection?

16

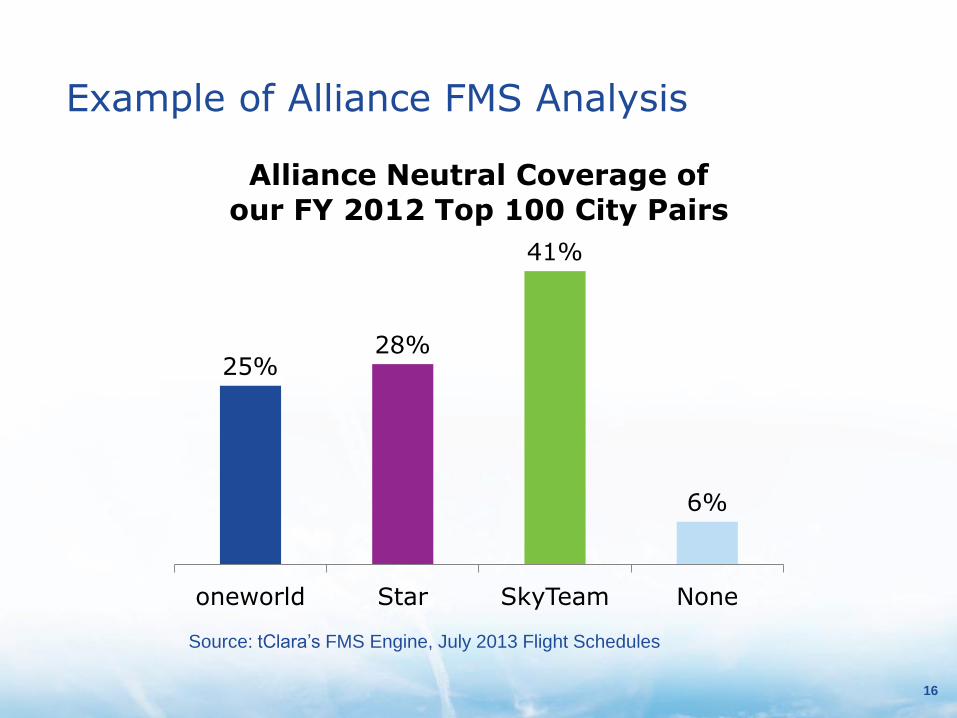

Example of Alliance FMS Analysis

25% 28%

41%

6%

oneworld Star SkyTeam None

Alliance Neutral Coverage of

our FY 2012 Top 100 City Pairs

Source: tClara’s FMS Engine, July 2013 Flight Schedules

17

Scenario Modeling is Critical

•Basis for modern airline sourcing

•Scenarios are “What if” options

•Typically involve Tier 1, 2 and 3 airlines

A.k.a. Primary, Secondary and Tertiary

Can have Co-primaries, co-secondaries, etc.

•Easy to model alliances

•Calculates detailed market shares by carrier and buyer’s savings for each scenario.

18

Primary, or Tier 1

Secondary, or Tier 2

Tertiary, or Tier 3

FMS Determines Airline’s Scenario Status

19

Scenario Examples

•DL as Primary, Star as Secondary

•DL/AF/KL as Primary, Star as Secondary

•DL + AA as Co-Primaries, then Star

•Star as Tier 1, then DL + AA as Tier 2

•Avoid DL: Make FL/AA/UA/US as Tier 1

•Modeling tools test 50-250 scenarios

20

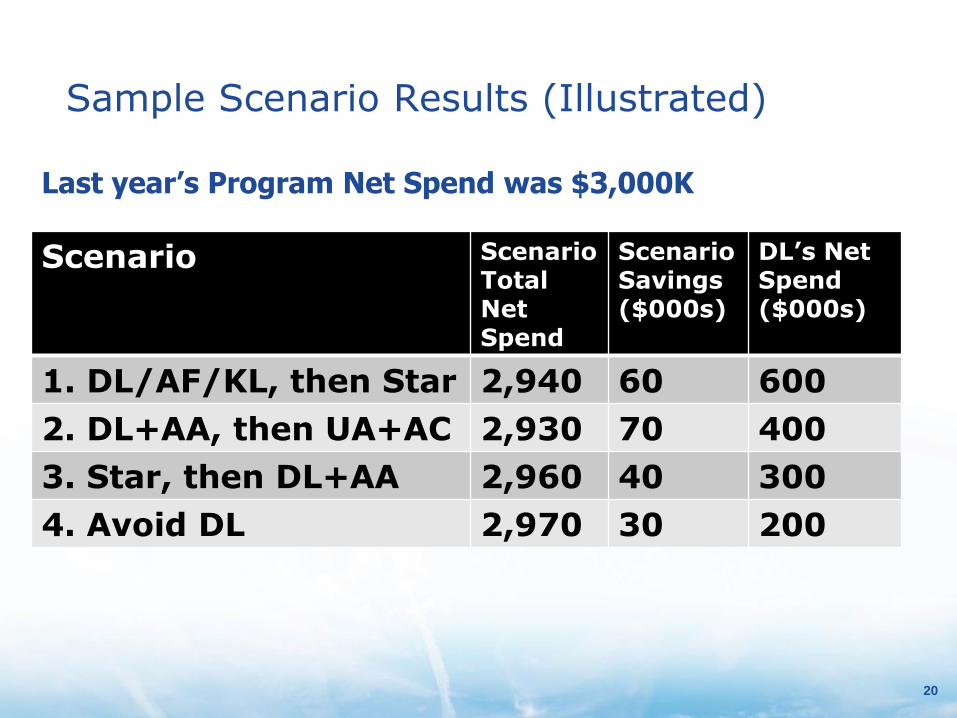

Sample Scenario Results (Illustrated)

Scenario ScenarioTotal Net Spend

Scenario Savings ($000s)

DL’s Net Spend ($000s)

1. DL/AF/KL, then Star 2,940 60 600

2. DL+AA, then UA+AC 2,930 70 400

3. Star, then DL+AA 2,960 40 300

4. Avoid DL 2,970 30 200

Last year’s Program Net Spend was $3,000K

21

Scenario Scenario Total Net Spend

Scenario Savings ($000s)

DL’s Net Spend ($000s)

1. DL/AF/KL, then Star 2,940 60 600

2. DL+AA, then UA+AC 2,930 70 400

3. Star, then DL+AA 2,960 40 300

4. Avoid DL 2,970 30 200

Buyer prefers No. 2

DL JV prefers No. 1

Scenario Implications

“So, Delta, here are your options…”

22

Goals Matter, Too!

• “We’ll give you a 30% discount, so long as you give us 75% market share”

• Two types of goal risk:

• Can you deliver 75%? (Unrealistic?)

• Have you promised more than 25% to any other airline? (Unachievable!).

23

Risky goals need attention

• Compare goal share to

–Historic Share

–Fair Market Share

–Scenario (projected) Share

• Identify overlapping goals (promising more than 100% share in a same market

• Negotiate for achievable goals, or take your risk of a reduced discount

24

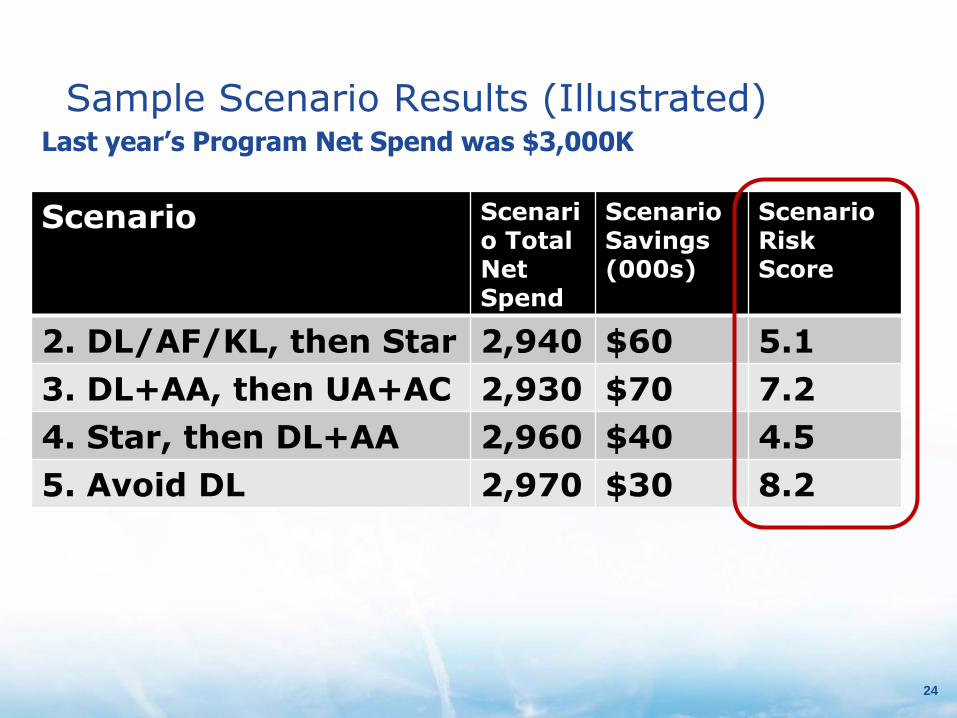

Sample Scenario Results (Illustrated)

Scenario Scenario Total Net Spend

Scenario Savings (000s)

Scenario Risk Score

2. DL/AF/KL, then Star 2,940 $60 5.1

3. DL+AA, then UA+AC 2,930 $70 7.2

4. Star, then DL+AA 2,960 $40 4.5

5. Avoid DL 2,970 $30 8.2

Last year’s Program Net Spend was $3,000K

25

Category (e.g., Air) Sourcing Options Map

<<Reward >> << Loss Savings >>

Risk

High

3 4

5

6

7

2

1

8

= Airline Supplier Scenario

26

Category (e.g., Air) Sourcing Options Map

<<Reward >> << Loss Savings >>

Risk

High

3 4

5

6

7

2

1

8

Apply

Logical

Elimination

= Airline Supplier Scenario

27

Sourcing Options for CEOs

Risk

High

4 6

7 “We recommend Option 6, but if you really want 7…”

= Airline Supplier Scenario

<<Reward >> << Loss Savings >>

28

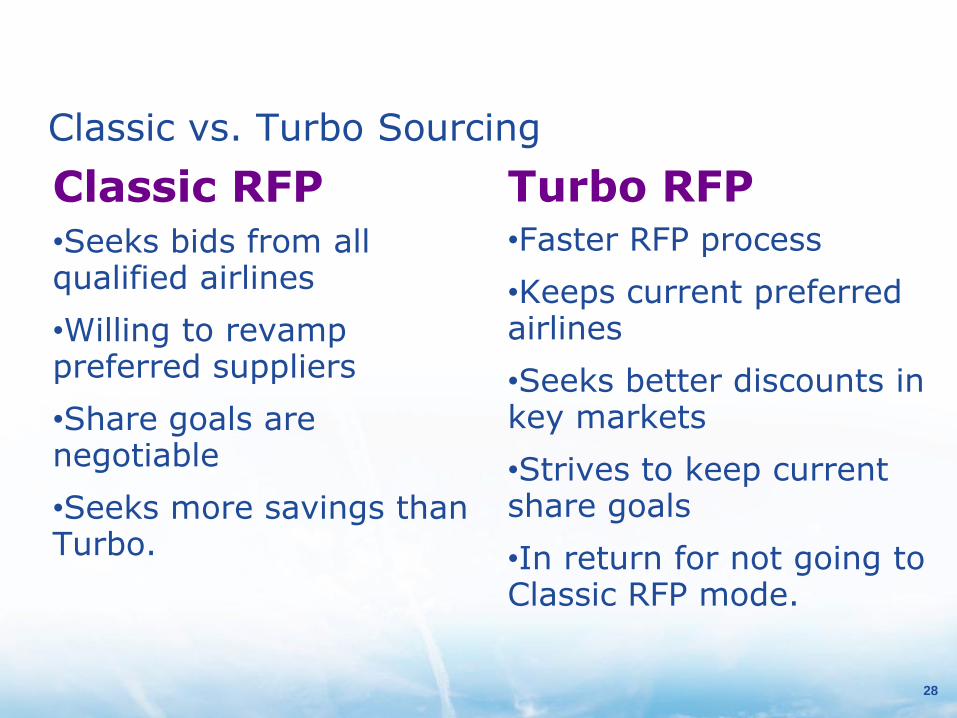

Classic vs. Turbo Sourcing

Turbo RFP •Faster RFP process

•Keeps current preferred airlines

•Seeks better discounts in key markets

•Strives to keep current share goals

•In return for not going to Classic RFP mode.

Classic RFP •Seeks bids from all qualified airlines

•Willing to revamp preferred suppliers

•Share goals are negotiable

•Seeks more savings than Turbo.

29

29

The Surprising Truth About Airline Discounts: Spend Doesn’t Matter

30

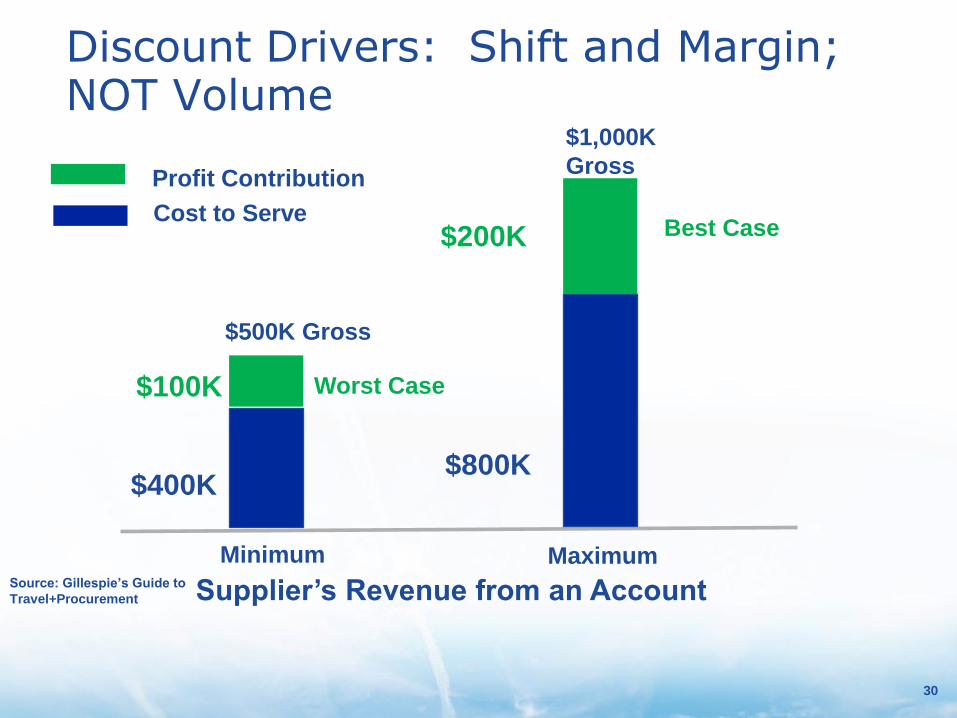

Discount Drivers: Shift and Margin; NOT Volume

Supplier’s Revenue from an Account

Minimum Maximum

$500K Gross

$400K

Profit Contribution

Cost to Serve

$800K

$200K

$1,000K

Gross

$100K Worst Case

Source: Gillespie’s Guide to

Travel+Procurement

Best Case

31

What’s the Maximum Discount?

$800K

$100K

Supplier’s Revenue from an Account

Minimum Maximum

$500K Gross

$400K

$1,000K Gross

Worst Case

$100K Worst Case,

NOT Negotiable

$100K Negotiable

Maximum Discount

$100K Negotiable

$1,000K

Gross

= 10%

Source: Gillespie’s Guide to

Travel+Procurement

Profit Contribution

Cost to Serve

32

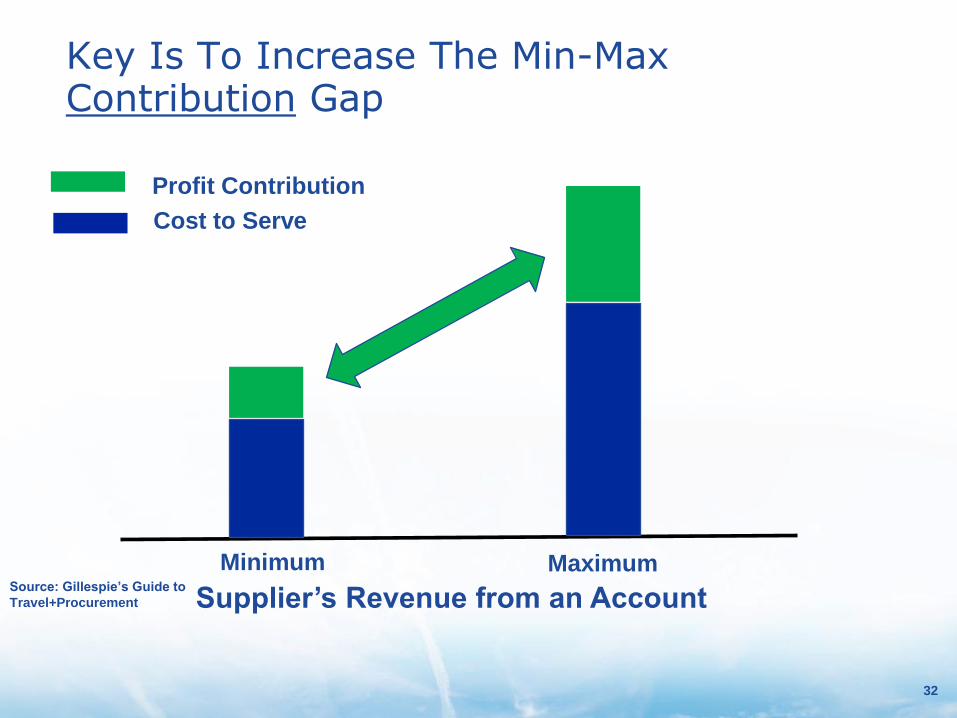

Key Is To Increase The Min-Max Contribution Gap

Supplier’s Revenue from an Account

Minimum Maximum Source: Gillespie’s Guide to

Travel+Procurement

Profit Contribution

Cost to Serve

33

Airfare Inventory Booking Classes

Illustrative

Fare Ladder Discount Implications

Higher discounts

Low or no

discounts

34

Expected Profit Margin and Share Shift, NOT Spend, Drives Discounts

More precisely, the credible threat or promise drives %

Y

Class

Disct.

Curve

35

Expected Profit Margin and Share Shift, NOT Spend, Drives Discounts

More precisely, the credible threat or promise drives %

Y

Class

Disct.

Curve

J

Class

Disct.

Curve

36

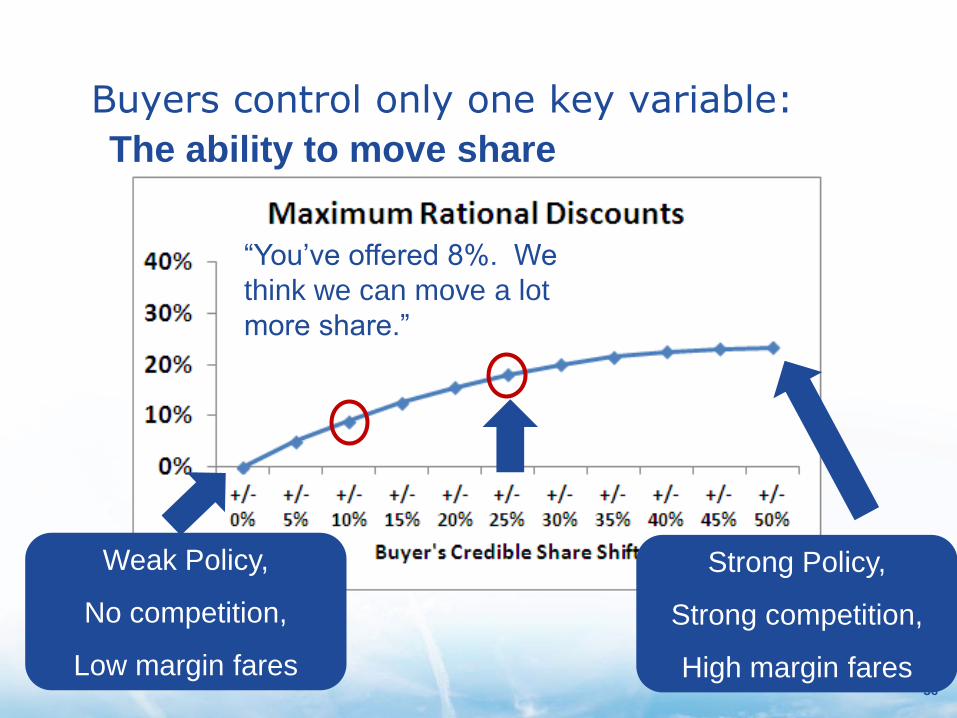

Buyers control only one key variable:

The ability to move share

“You’ve offered 8%. We

think we can move a lot

more share.”

Weak Policy,

No competition,

Low margin fares

Strong Policy,

Strong competition,

High margin fares

37

How will the AA-US merger affect our program?

Oneworld will become our largest alliance by capacity

Pre-merger Post-merger

Analysis of FY12’s top 500 global city pairs using tClara’s July 2013 FMS engine

Illustrative

38

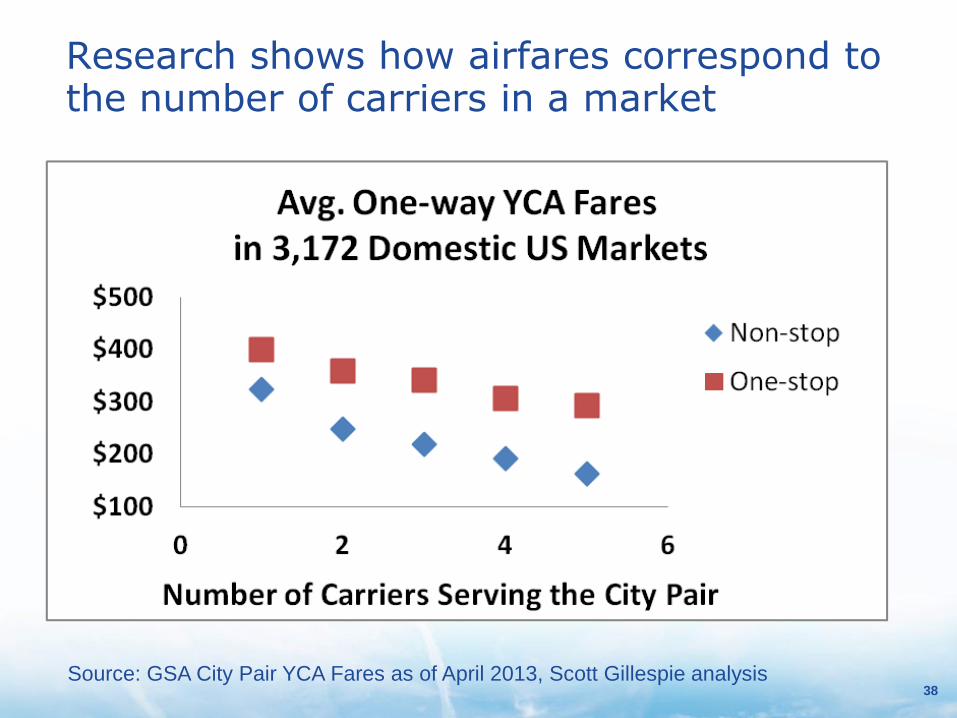

Research shows how airfares correspond to the number of carriers in a market

Source: GSA City Pair YCA Fares as of April 2013, Scott Gillespie analysis

39

Profit margins decline as competition increases

Source: GSA City Pair YCA Fares as of April 2013, Scott Gillespie analysis

40

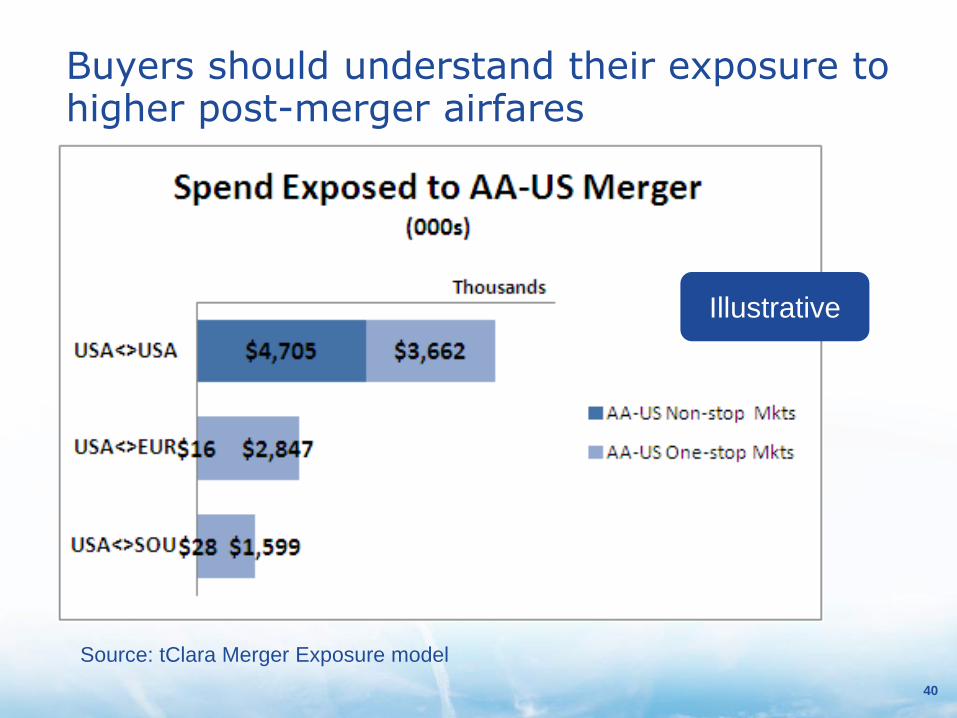

Buyers should understand their exposure to higher post-merger airfares

Illustrative

Source: tClara Merger Exposure model

41

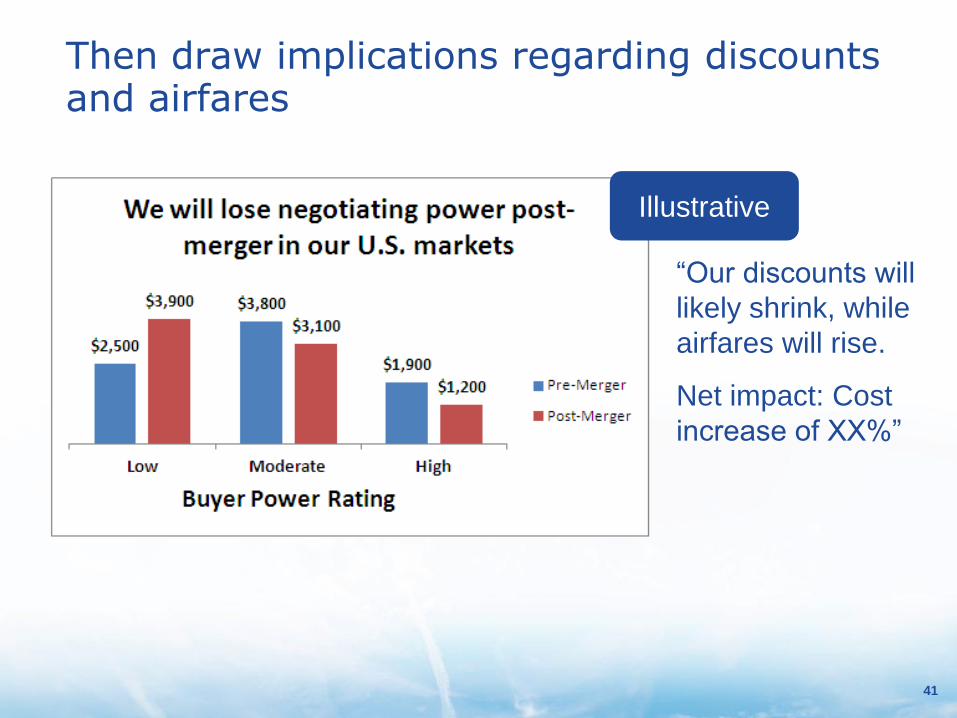

Then draw implications regarding discounts and airfares

“Our discounts will

likely shrink, while

airfares will rise.

Net impact: Cost

increase of XX%”

Illustrative

42

Airline Sourcing Mistakes to Avoid

43

Cramming the RFP process

“Here’s your RFP. You have two weeks to respond”

Should be:

Minimum 3 weeks for single point of sale

Minimum 4 weeks for Alliance bids – more if you need a bid from Air France during the summer

44

Over-estimating the procurement savings potential

“We should be able to save 10% by strategically sourcing our airlines”

Worse – when a consultant says that, especially without looking at your deals

Reality may be far different

Victory might be minimizing the cost increase

45

Wandering around the Land of

Stupid Statistics

Which

Cabin(s)?

Booked how

far in

advance?

Leisure or

Corporate?

$257, +/- ? Includes

taxes?

46

The Value of Benchmarking

• Diverse opinions of benchmarking’s value

• “Pricing comparisons among like-sized corporate contracts provides valuable feedback that can in fact highlight contract improvement opportunities.” Matthew Patterson, CWT Air Solutions, 2010

• “Airline price benchmarks are crap.”

Scott Gillespie, ~2001

Issues include:

– True “apples to apples” comparisons

– Doesn’t reveal share shift basis

– Timing of discounts and their associated jet fuel prices

47

De-coupling discounts from goals

• Some RFPs ask for discounts without their associated goals

–“We’ll talk about goals later”

• Better: “Show us how discounts change in return for more share shift”

48

Failure to agree on realistic market share goals

• Unrealistic goals

–Buyer commits more share than practical

–Factors: Uses poor FMS baseline, over-estimates traveler compliance

• Unachievable goals

–Overcommits to 2+ carriers, e.g. promises each 60% market share

49

Fare Mix, Discounts and NER, WAD (Net Effective Rate, a.k.a. Weighted Average Discount)

• Fare mix is key to calculating discounts

• Historic fare mix determines the spend-weighted Net Effective Rate

Share of Spend

Booked Fare Class

Discount Net Eff. Rate

10% J 30% 3.0%

20% Y 20% 4.0%

40% M 15% 6.0%

30% T 0% 0.0%

13.0% Net Effective Rate =

50

Buyer and Airline must use same fare mix

• Airlines may use an “expected” or “new” fare mix

• Impossible to guarantee availability.

Share of Spend

Booked Fare Class

Discount Net Eff. Rate

10% J 30% 3.0%

5% Y 0% 0.0%

55% M 20% 11.0%

30% T 0% 0.0%

14.0% New Net Effective Rate =

13.0% Old Net Effective Rate =

51

51

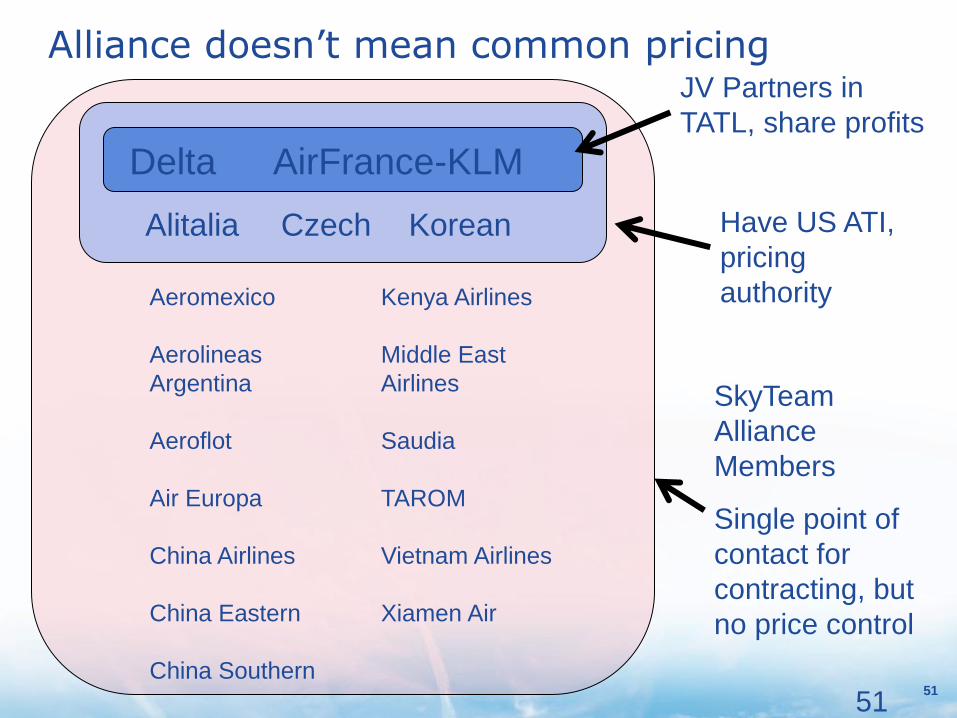

Alliance doesn’t mean common pricing

Delta AirFrance-KLM

Alitalia Czech Korean

Aeromexico

Aerolineas

Argentina

Aeroflot

Air Europa

China Airlines

China Eastern

China Southern

Kenya Airlines

Middle East

Airlines

Saudia

TAROM

Vietnam Airlines

Xiamen Air

JV Partners in

TATL, share profits

Have US ATI,

pricing

authority

SkyTeam

Alliance

Members

Single point of

contact for

contracting, but

no price control

52

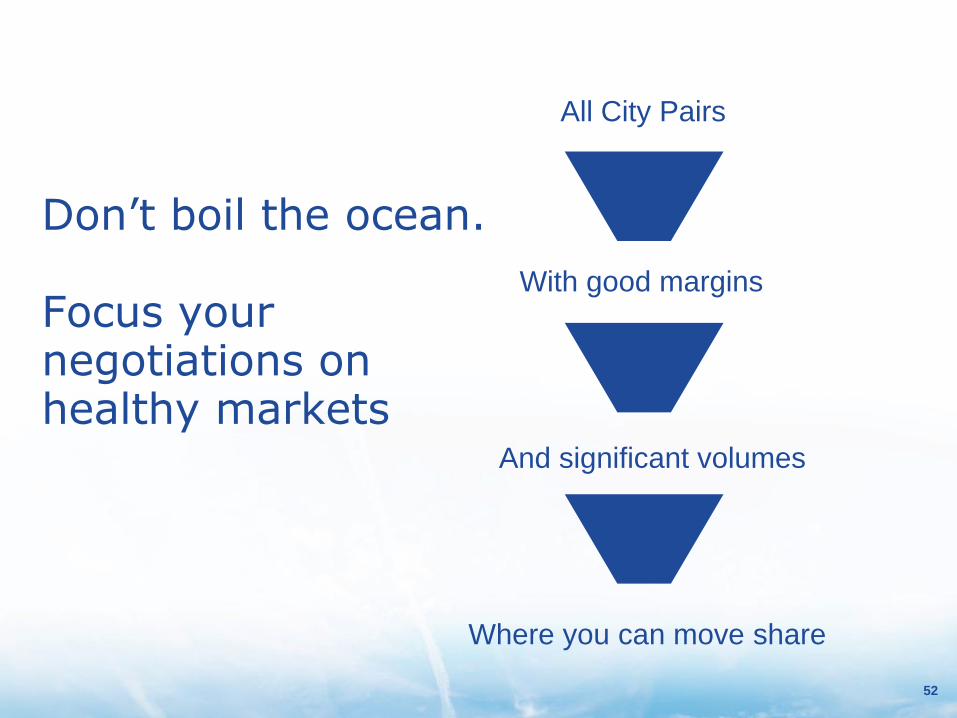

Don’t boil the ocean. Focus your negotiations on healthy markets

All City Pairs

Where you can move share

With good margins

And significant volumes

53

In Summary

• Understand Fair Market Share

• Use scenario modeling

• Use realistic market share goals and option maps

• Spend doesn’t drive discounts – share shift and profit margins drive discounts

• Expect higher airfares and smaller discounts in AA-US non-stop and one-stop markets

• Avoid making typical air sourcing mistakes

54

Thank You!

Scott Gillespie

(O) 440 248 4111

“Gillespie’s Guide to Travel+Procurement”

Active on LinkedIn