Adi Sarana Armada (Maintain)

15

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 1 COMPANY FOCUS │ 7 March, 2021 Company Data Year end Dec 2018 2019F 2020F 2021F 2022F Revenue (IDR bn) 1,863 2,330 2,957 3,876 5,265 Net Profit (IDR bn) 144 110 93 150 178 EPS Growth (%) 39.1 -23.1 -15.4 60.2 18.9 P/E (x) 34.1 44.3 52.4 32.7 27.5 P/BV (X) 4.5 4.1 3.8 3.4 3.0 EBITDA (IDR bn) 787 866 873 1,072 1,334 EV/EBITDA 8.9 8.7 8.9 7.7 6.4 Div Yield (%) 0.8 0.0 0.0 0.0 0.0 Adi Sarana Armada Blue Chip in Presence, Meaningful in Impact: Part II Conquering ecosystem is what set the company apart Valuation of digital banks valuation (E.g. ~$30bn for WeBank, ~$9.15bn for Kakao Bank, and ~$5.5bn for Tinkoff) highly depends on how a bank can conquer a person’s ecosystem. Similar with digital technology adoptions in the logistics industry, one should value a logistic company based on the company’s ability to operate in a seamless end to end logistic chain. ASSA is able to adopt and combine technology/digital and operational excellence both simultaneously. Anteraja’s (55% owned by ASSA) shareholder, SF Holdings, plans to acquire 51.8% of Kerry Logistics Network Ltd. (a logistic company based in HK), creating the biggest logistic group in Asia. We believe ASSA will be part of the supply chain to the international markets as well. It is worth noting that ASSA’s sister company, Puninar, has partnership with Kerry Logistics since 5 years ago. After a very strong last-mile delivery performance (Anteraja’s parcel delivery up 7x to ~50m deliveries in 2020 from ~6m in 2019), the company further expands its logistic wings by establishing Bisnisaja (customized B2B shipping process), travylite (collaboration with Angkasa Pura II airport for excess baggage services) and Titipaja (e- fulfillment services with multi-location warehouses to serve inter-region services). Indonesia’s logistic value is ~Rp3,300trn/year and Anteraja’s 2021 revenue is only ~0.05% of this. SF Holdings and Kerry Logistics have both market cap combined of $73bn (Rp1,000trn) with combined 2020 revenue size of ~$30bn (Rp429trn). Logistic last mile is still at growing stage We estimate avg. spending of Shopee transactions/user/year is ~$42 and ~6% of the $42 would be logistic costs ($2.6). We believe the number of transactions done still has lots of upside especially from non-Jakarta areas. ASSA’s goal to pursue ~2m parcels per/day by 2024 is becoming more plausible looking at the current growth trajectory. China’s parcel delivery (~174k/day) is ~44x larger than Indonesia (~4m/day) while China’s population is only ~5x larger. Upgrade TP to Rp2.7k (+88% ups.), Buy We expect earnings to book +34% CAGR in the next 5 years (2020-25) driven mainly by Anteraja’s multi-beggar growth coupled with solid double-digit growth from its rental business. Our new SOP-based TP is Rp2.7k. The new TP is mainly premised on 50% discount to Anteraja’s 2m parcel/day target by 2024 coupled with valuation/delivery transactions/year of $2.6. We believe that Anteraja will be one of the top key players in this e-commerce logistics industry and our confidence on Anteraja reaching that 2m/day delivery level is substantially increasing after proving exponential growth since April 2019’s inception. BUY (Maintain) Current TP IDR2,700 (+88%) Previous TP IDR770 Current Price IDR1,440 Willinoy Sitorus [email protected] 021 - 2924 9107 Hasbie [email protected] +62-21 2924 6322 Stock Data & Indices Bloomberg Code ASSA.IJ JCI Member JAKINFR MSCI Indonesia No JII No LQ45 No Kompas 100 No Key Data Issued Shares (mn) 3.397.5 Free Float (est) 35.7 Mkt. Cap (IDRbn) 4,892.4 Mkt. Cap (USDmn) 339.3 ADTV 6 months (USDmn) 16.3 52 Wk-range 1615 / 268 Performance (%) YTD 1m 3m 12m Absolute 126.8 42.6 166.7 174.3 Relative to JCI 122.1 41.8 161.4 160.5

Transcript of Adi Sarana Armada (Maintain)

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 1

COMPANY FOCUS │ 7 March, 2021

Company Data

Year end Dec 2018 2019F 2020F 2021F 2022F

Revenue (IDR bn) 1,863 2,330 2,957 3,876 5,265

Net Profit (IDR bn) 144 110 93 150 178

EPS Growth (%) 39.1 -23.1 -15.4 60.2 18.9

P/E (x) 34.1 44.3 52.4 32.7 27.5

P/BV (X) 4.5 4.1 3.8 3.4 3.0

EBITDA (IDR bn) 787 866 873 1,072 1,334

EV/EBITDA 8.9 8.7 8.9 7.7 6.4

Div Yield (%) 0.8 0.0 0.0 0.0 0.0

Adi Sarana Armada Blue Chip in Presence, Meaningful in Impact:

Part II

Conquering ecosystem is what set the company apart

Valuation of digital banks valuation (E.g. ~$30bn for WeBank, ~$9.15bn for Kakao

Bank, and ~$5.5bn for Tinkoff) highly depends on how a bank can conquer a

person’s ecosystem. Similar with digital technology adoptions in the logistics

industry, one should value a logistic company based on the company’s ability to

operate in a seamless end to end logistic chain. ASSA is able to adopt and combine

technology/digital and operational excellence both simultaneously. Anteraja’s (55%

owned by ASSA) shareholder, SF Holdings, plans to acquire 51.8% of Kerry

Logistics Network Ltd. (a logistic company based in HK), creating the biggest

logistic group in Asia. We believe ASSA will be part of the supply chain to the

international markets as well. It is worth noting that ASSA’s sister company,

Puninar, has partnership with Kerry Logistics since 5 years ago. After a very strong

last-mile delivery performance (Anteraja’s parcel delivery up 7x to ~50m deliveries

in 2020 from ~6m in 2019), the company further expands its logistic wings by

establishing Bisnisaja (customized B2B shipping process), travylite (collaboration

with Angkasa Pura II airport for excess baggage services) and Titipaja (e-

fulfillment services with multi-location warehouses to serve inter-region services).

Indonesia’s logistic value is ~Rp3,300trn/year and Anteraja’s 2021 revenue is only

~0.05% of this. SF Holdings and Kerry Logistics have both market cap combined of

$73bn (Rp1,000trn) with combined 2020 revenue size of ~$30bn (Rp429trn).

Logistic last mile is still at growing stage

We estimate avg. spending of Shopee transactions/user/year is ~$42 and ~6% of

the $42 would be logistic costs ($2.6). We believe the number of transactions done

still has lots of upside especially from non-Jakarta areas. ASSA’s goal to pursue

~2m parcels per/day by 2024 is becoming more plausible looking at the current

growth trajectory. China’s parcel delivery (~174k/day) is ~44x larger than

Indonesia (~4m/day) while China’s population is only ~5x larger.

Upgrade TP to Rp2.7k (+88% ups.), Buy

We expect earnings to book +34% CAGR in the next 5 years (2020-25) driven

mainly by Anteraja’s multi-beggar growth coupled with solid double-digit growth

from its rental business. Our new SOP-based TP is Rp2.7k. The new TP is mainly

premised on 50% discount to Anteraja’s 2m parcel/day target by 2024 coupled

with valuation/delivery transactions/year of $2.6. We believe that Anteraja will be

one of the top key players in this e-commerce logistics industry and our confidence

on Anteraja reaching that 2m/day delivery level is substantially increasing after

proving exponential growth since April 2019’s inception.

BUY (Maintain) Current TP IDR2,700 (+88%) Previous TP IDR770 Current Price IDR1,440

Willinoy Sitorus [email protected] 021 - 2924 9107 Hasbie [email protected] +62-21 2924 6322

Stock Data & Indices

Bloomberg Code ASSA.IJ

JCI Member JAKINFR

MSCI Indonesia No

JII No

LQ45 No

Kompas 100 No

Key Data

Issued Shares (mn) 3.397.5

Free Float (est) 35.7

Mkt. Cap (IDRbn) 4,892.4

Mkt. Cap (USDmn) 339.3

ADTV 6 months (USDmn) 16.3

52 Wk-range 1615 / 268

Performance (%)

YTD 1m 3m 12m

Absolute 126.8 42.6 166.7 174.3

Relative to

JCI 122.1 41.8 161.4 160.5

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 2

Cash Flow

Year end Dec (IDR bn) 2018 2019F 2020F 2021F 2022F

Net Profit 144 110 93 150 178

Depr / Amort 431 517 529 601 691

Chg in Working Cap 188 (99) (46) (90) (1)

Others (639) (675) (340) (314) (227)

CF's from oprs 123 (146) 236 346 641

Capex (736) (590) (484) (782) (797)

Others 623 441 0 0 0

CF's from investing (113) (149) (484) (782) (797)

Net change in debt 348 560 50 450 650

Others (215) (237) 8 (22) (86)

CF's from financing 133 323 58 428 564

Net cash flow 143 28 (189) (8) 408

Cash at BoY 85 228 255 65 57

Cash at EoY 228 256 65 57 465

Income Statement

Year end Dec (IDR bn) 2018 2019F 2020F 2021F 2022F

Revenue 1,863 2,330 2,957 3,876 5,265

Gross Profit 599 740 825 1,003 1,326

Opr. Profit 357 349 345 471 642

EBITDA 787 866 873 1,072 1,334

Net Int Inc/(Exp) -173.2 -229.1 -239.6 -258.7 -324.2

Other Income (Expense) (3) 0 0 0 0 Pre-tax Profit 182 117 105 212 318

Income Tax Expense (40) (26) (20) (40) (54)

Minority Interest 1 19 8 (22) (86)

Net Profit 144 110 93 150 178

Dividend payout ratio (%) 28 0 0 0 0

Balance Sheet

Year end Dec (IDR bn) 2018 2019F 2020F 2021F 2022F

Cash and equivalents 228 255 65 57 465

Other curr asset 309 398 451 565 602

Net fixed asset 3,412 3,894 4,189 4,685 5,017

Other non-current assets 114 303 303 303 303

Total Asset 4,063 4,849 5,008 5,610 6,387

ST debt 747 847 847 997 1,247

Other curr liab 403 394 401 425 461

LT debt 1,604 2,064 2,114 2,414 2,814

Other LT Liab 170 207 207 207 207

Minority interest 2,924 3,511 3,568 4,043 4,728

Total Liabilities 52 146 155 132 46

Shareholders Equity 1,086 1,192 1,285 1,435 1,613

Net debt / (cash) 2,123 2,656 2,895 3,353 3,595

Total cap employed 2,912 3,609 3,761 4,188 4,680

Net Working capital (613) (588) (731) (800) (640)

Ratio Analysis

Year end Dec 2018 2019F 2020F 2021F 2022F

Profitability

Gross Margin (%) 32.1 31.8 27.9 25.9 25.2

Opr Margin (%) 19.1 15.0 11.7 12.2 12.2

EBITDA Margin (%) 42.2 37.2 29.5 27.7 25.3

Core Net Margin (%) 7.7 4.7 3.2 3.9 3.4

ROE (%) 13.9 9.7 7.5 11.0 11.7

ROA (%) 3.9 2.5 1.9 2.8 3.0

Stability

Current ratio (x) 0.5 0.5 0.4 0.4 0.6

Net Debt to Equity (x) 2.0 2.2 2.3 2.3 2.2

Net Debt to EBITDA (x) 2.7 3.1 3.3 3.1 2.7

Interest Coverage (x) 2.0 1.4 1.4 1.7 1.9

Efficiency

Account Payable (days) 10 12 12 12 12

Account Receivable (days) 42 39 39 39 30

Inventory Day (days) 10 8 8 8 8

Major Shareholders

Major Shareholders

PT Adi Sarana Armada Tbk (ASSA) is

one of the largest car rental

company with >20k rental units and

44 branch & service points. It

entered the car auction business

back in 2014.

Company Background

PT Adi Dinamika Investindo 25.1%

PT Daya Adicipta Mustika 19.2%

Drs. Prodjo Sunarjanto SP 9.9%

Public 45.8%

SWOT Analysis

Threat -Increase in cost

of funds.

-High discount

for new car.

Strength -Strong customer

base (corporate).

-Lower car

acquisition price

-Synergy within

business units

-technology

driven

Weakness -Exposure to

change in

interest rates.

Opportunity -Increase in

second hand

car price.

-Trend to

outsource

transportation

needs

(increase in

potential

customer base)

-Monetize

technology to

make

businesses

more efficient

Major Shareholders

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 3

INDUSTRY OUTLOOK

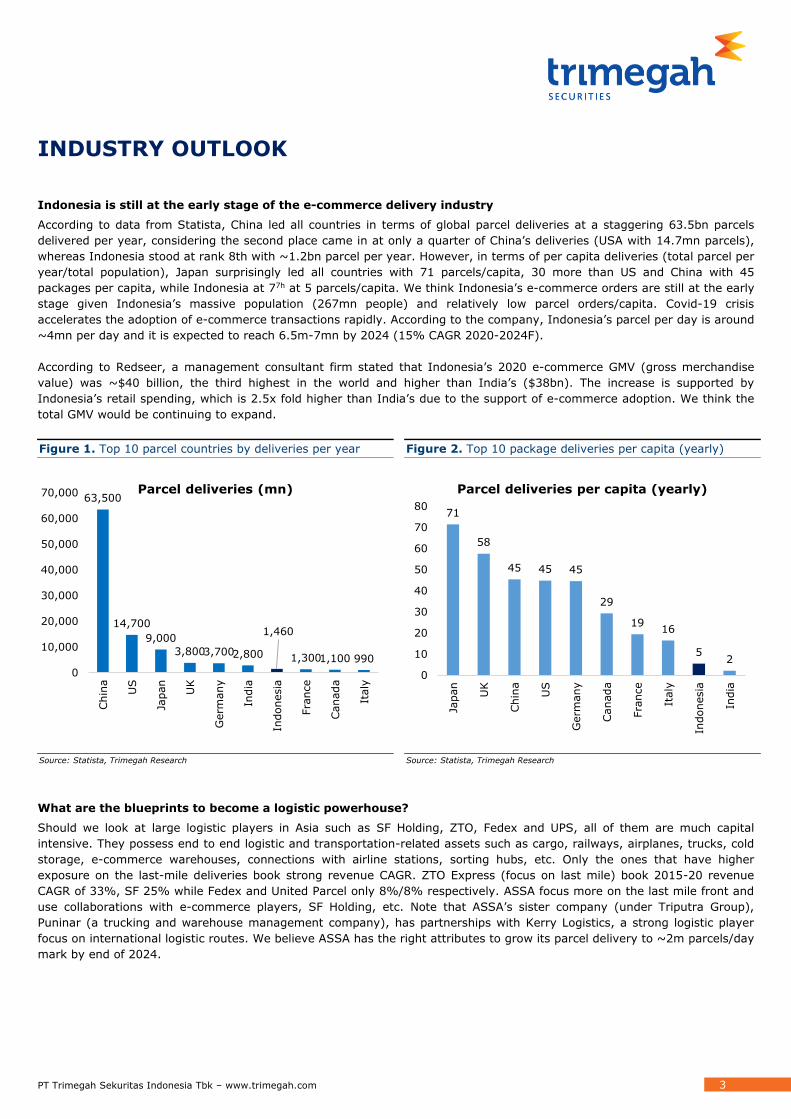

Indonesia is still at the early stage of the e-commerce delivery industry

According to data from Statista, China led all countries in terms of global parcel deliveries at a staggering 63.5bn parcels

delivered per year, considering the second place came in at only a quarter of China’s deliveries (USA with 14.7mn parcels),

whereas Indonesia stood at rank 8th with ~1.2bn parcel per year. However, in terms of per capita deliveries (total parcel per

year/total population), Japan surprisingly led all countries with 71 parcels/capita, 30 more than US and China with 45

packages per capita, while Indonesia at 77h at 5 parcels/capita. We think Indonesia’s e-commerce orders are still at the early

stage given Indonesia’s massive population (267mn people) and relatively low parcel orders/capita. Covid-19 crisis

accelerates the adoption of e-commerce transactions rapidly. According to the company, Indonesia’s parcel per day is around

~4mn per day and it is expected to reach 6.5m-7mn by 2024 (15% CAGR 2020-2024F).

According to Redseer, a management consultant firm stated that Indonesia’s 2020 e-commerce GMV (gross merchandise

value) was ~$40 billion, the third highest in the world and higher than India’s ($38bn). The increase is supported by

Indonesia’s retail spending, which is 2.5x fold higher than India’s due to the support of e-commerce adoption. We think the

total GMV would be continuing to expand.

Figure 1. Top 10 parcel countries by deliveries per year Figure 2. Top 10 package deliveries per capita (yearly)

Source: Statista, Trimegah Research Source: Statista, Trimegah Research

What are the blueprints to become a logistic powerhouse?

Should we look at large logistic players in Asia such as SF Holding, ZTO, Fedex and UPS, all of them are much capital

intensive. They possess end to end logistic and transportation-related assets such as cargo, railways, airplanes, trucks, cold

storage, e-commerce warehouses, connections with airline stations, sorting hubs, etc. Only the ones that have higher

exposure on the last-mile deliveries book strong revenue CAGR. ZTO Express (focus on last mile) book 2015-20 revenue

CAGR of 33%, SF 25% while Fedex and United Parcel only 8%/8% respectively. ASSA focus more on the last mile front and

use collaborations with e-commerce players, SF Holding, etc. Note that ASSA’s sister company (under Triputra Group),

Puninar (a trucking and warehouse management company), has partnerships with Kerry Logistics, a strong logistic player

focus on international logistic routes. We believe ASSA has the right attributes to grow its parcel delivery to ~2m parcels/day

mark by end of 2024.

63,500

14,700

9,000

3,8003,7002,800

1,460

1,3001,100 990

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Chin

a

US

Japan

UK

Germ

any

India

Indonesia

Fra

nce

Canada

Italy

Parcel deliveries (mn)

71

58

45 45 45

29

1916

52

0

10

20

30

40

50

60

70

80

Japan

UK

Chin

a

US

Germ

any

Canada

Fra

nce

Italy

Indonesia

India

Parcel deliveries per capita (yearly)

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 4

Figure 3. SF, ZTO, Fedex, and UPS revenue CAGR 2015-2020

Source: Trimegah Research, Bloomberg

Figure 4. Anteraja’s revenue growth 2019-2024F Figure 5. Anteraja’s average no parcel delivery per day

Source: Trimegah Research, company Source: Trimegah Research, company

Figure 6. Anteraja’s business model

Source: Company

33%

25%

8% 8%

0%

5%

10%

15%

20%

25%

30%

35%

ZTO EXPRESSCAYMAN INC

S F HOLDING CO LTD-A

FEDEX CORP UNITED PARCELSERVICE-CL B

83

801

1,705

3,023

4,408

6,249

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2019 2020F 2021F 2022F 2023F 2024F

(IDRbn)

91

214

450

799

1,153

1,603

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2019 2020F 2021F 2022F 2023F 2024F

(No. of parcel delivery, in 000 per day)

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 5

Figure 7. ASSA’s new business initiatives: Tapping various delivery business using the adoption of technology

Source: Company

Figure 8. Anteraja’s peers comparison

Source: Trimegah Research, Bloomberg

Figure 9. Changes of estimate

Source: Trimegah Research, Bloomberg

Ticker Market cap

(USDMn) 2020Y 2021Y 2020Y 2021Y 2020Y 2021Y 2020Y 2021Y 2020Y 2021Y

*as of 3/5/2021

Courier

China

S F HOLDING CO LTD-A 002352 CH EQUITY 68,098 59.72 47.69 8.80 7.48 29.65 24.03 2.90 2.34 14.97 16.15

KERRY LOGISTICS NETWORK LTD 636 HK EQUITY 5,269 24.73 21.92 1.62 1.54 10.63 10.03 0.89 0.83 6.60 5.94

ZTO EXPRESS CAYMAN INC 2057 HK EQUITY 29,411 38.52 34.28 3.66 3.34 24.78 19.37 7.44 6.08 9.95 11.35

SINOTRANS LIMITED-H 598 HK EQUITY 4,539 7.42 6.93 0.61 0.57 9.06 8.54 0.35 0.33 8.60 8.93

Japan

YAMATO HOLDINGS CO LTD 9064 JP EQUITY 9,984 50.77 23.22 1.91 1.80 9.90 7.17 0.66 0.64 3.81 7.98

SG HOLDINGS CO LTD 9143 JT EQUITY 14,537 33.31 21.53 4.02 3.77 16.50 12.60 1.34 1.23 13.10 17.85

US

UNITED PARCEL SERVICE-CL B UPS US EQUITY 142,541 21.36 18.51 18.71 24.26 14.97 13.00 1.73 1.63 119.41 205.48

FEDEX CORP FDX US EQUITY 68,200 29.68 14.76 3.57 3.07 12.94 8.51 1.00 0.86 12.01 22.00

Average 42,822 33.19 23.60 5.36 5.73 16.05 12.91 2.04 1.74 23.55 36.96

PER (x) PBV (x) EV/EBITDA (x) ROE (%)P/S (x)

2021F 2022F 2021F 2022F 2021F 2022F

Revenue 3,876 5,265 3,475 4,362 12% 21%

Gross profit 1,003 1,326 927 1,216 8% 9%

Gross margin 25.9% 25.2% 26.7% 27.9%

Operating profit 471 642 421 521 12% 23%

Op. profit margin 12.2% 12.2% 12.1% 11.9%

Pre-tax profit 212 318 171 231 24% 38%

Pre-tax margin 5.5% 6.0% 4.9% 5.3%

Net profit 150 178 138 164 9% 8%

Net margin 3.9% 3.4% 4.0% 3.8%

NEW OLD CHANGE

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 6

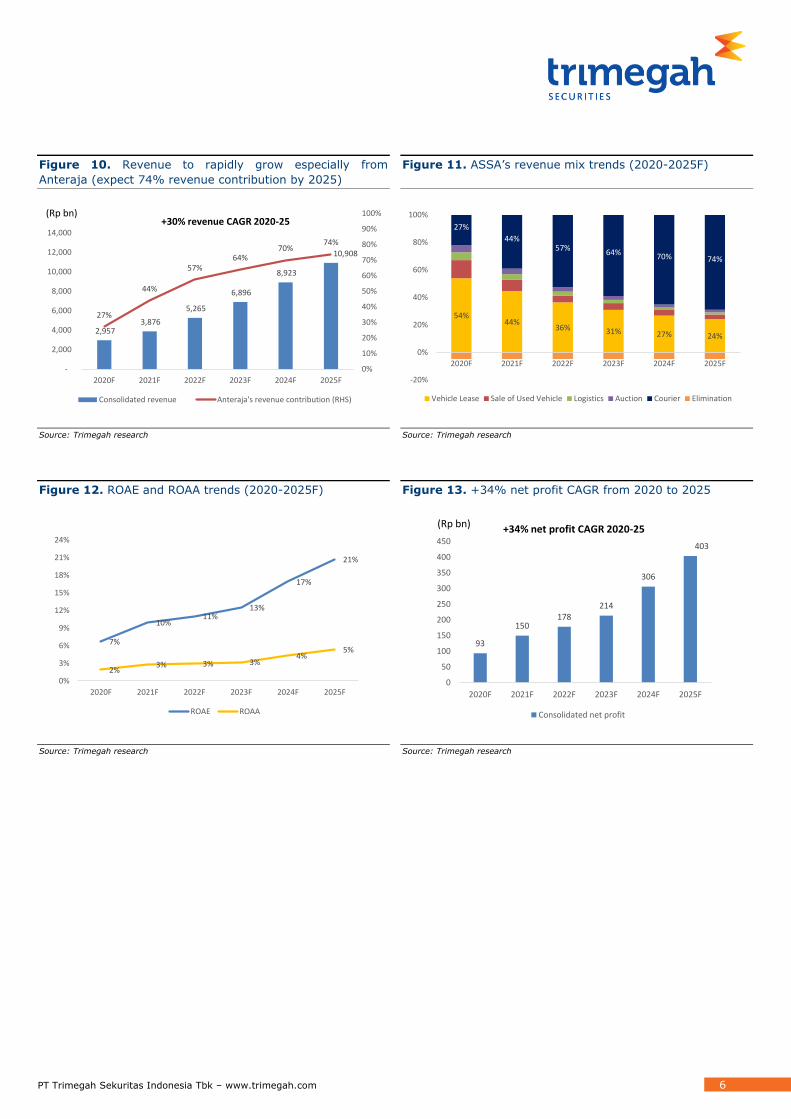

Figure 10. Revenue to rapidly grow especially from

Anteraja (expect 74% revenue contribution by 2025)

Figure 11. ASSA’s revenue mix trends (2020-2025F)

Source: Trimegah research Source: Trimegah research

Figure 12. ROAE and ROAA trends (2020-2025F) Figure 13. +34% net profit CAGR from 2020 to 2025

Source: Trimegah research Source: Trimegah research

2,957 3,876

5,265

6,896

8,923

10,908

27%

44%

57%64%

70%74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2020F 2021F 2022F 2023F 2024F 2025F

Consolidated revenue Anteraja's revenue contribution (RHS)

(Rp bn)+30% revenue CAGR 2020-25

54%44%

36% 31% 27% 24%

27%

44%57%

64% 70% 74%

-20%

0%

20%

40%

60%

80%

100%

2020F 2021F 2022F 2023F 2024F 2025F

Vehicle Lease Sale of Used Vehicle Logistics Auction Courier Elimination

7%

10%11%

13%

17%

21%

2%3% 3% 3%

4%5%

0%

3%

6%

9%

12%

15%

18%

21%

24%

2020F 2021F 2022F 2023F 2024F 2025F

ROAE ROAA

93

150178

214

306

403

0

50

100

150

200

250

300

350

400

450

2020F 2021F 2022F 2023F 2024F 2025F

Consolidated net profit

(Rp bn) +34% net profit CAGR 2020-25

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 7

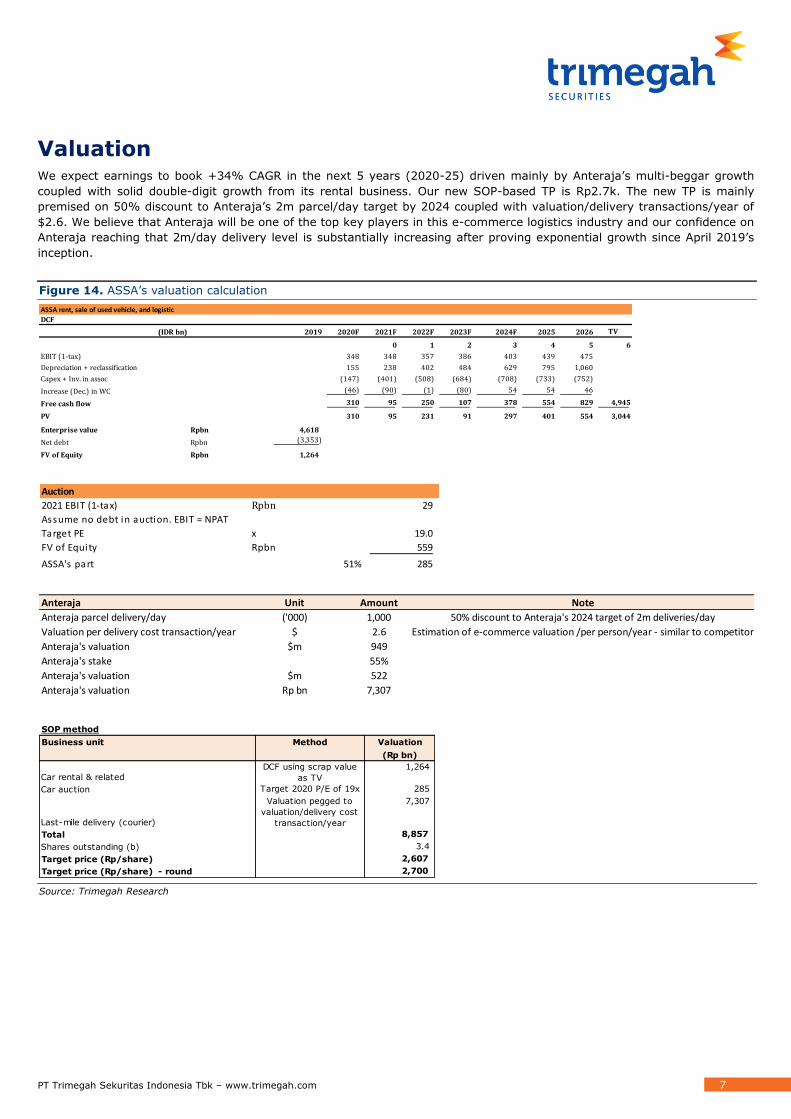

Valuation We expect earnings to book +34% CAGR in the next 5 years (2020-25) driven mainly by Anteraja’s multi-beggar growth

coupled with solid double-digit growth from its rental business. Our new SOP-based TP is Rp2.7k. The new TP is mainly

premised on 50% discount to Anteraja’s 2m parcel/day target by 2024 coupled with valuation/delivery transactions/year of

$2.6. We believe that Anteraja will be one of the top key players in this e-commerce logistics industry and our confidence on

Anteraja reaching that 2m/day delivery level is substantially increasing after proving exponential growth since April 2019’s

inception.

Figure 14. ASSA’s valuation calculation

Source: Trimegah Research

ASSA rent, sale of used vehicle, and logistic

DCF

(IDR bn) 2019 2020F 2021F 2022F 2023F 2024F 2025 2026 TV

0 1 2 3 4 5 6

EBIT (1-tax) 348 348 357 386 403 439 475

Depreciation + reclassification 155 238 402 484 629 795 1,060

Capex + Inv. in assoc (147) (401) (508) (684) (708) (733) (752)

Increase (Dec.) in WC (46) (90) (1) (80) 54 54 46

Free cash flow 310 95 250 107 378 554 829 4,945

PV 310 95 231 91 297 401 554 3,044

Enterprise value Rpbn 4,618

Net debt Rpbn (3,353)

FV of Equity Rpbn 1,264

Auction

2021 EBIT (1-tax) Rpbn 29

Assume no debt in auction. EBIT = NPAT

Target PE x 19.0

FV of Equity Rpbn 559

ASSA's part 51% 285

Anteraja Unit Amount Note

Anteraja parcel delivery/day ('000) 1,000 50% discount to Anteraja's 2024 target of 2m deliveries/day

Valuation per delivery cost transaction/year $ 2.6 Estimation of e-commerce valuation /per person/year - similar to competitor

Anteraja's valuation $m 949

Anteraja's stake 55%

Anteraja's valuation $m 522

Anteraja's valuation Rp bn 7,307

SOP method

Business unit Method Valuation

(Rp bn)

Car rental & related

DCF using scrap value

as TV

1,264

Car auction Target 2020 P/E of 19x 285

Last-mile delivery (courier)

Valuation pegged to

valuation/delivery cost

transaction/year

7,307

Total 8,857

Shares outstanding (b) 3.4

Target price (Rp/share) 2,607

Target price (Rp/share) - round 2,700

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 8

Figure 15. Peers comparison

Source: Trimegah Research, Bloomberg

Figure 16. ASSA 1-year historical forward P/E for the last 2 year

Source: Trimegah Research, Bloomberg

Stocks ASSA

Latest date 3/5/2021

Latest valuation 31.65

2-year average valuation 19.86

(disc)/premium to 2-year avg 59%

7.0

12.0

17.0

22.0

27.0

32.0

37.0

Fwd PE band ASSA avg 19.8x +1 STD 26.8x +2 STD 33.8x -1 STD 12.8x -2 STD 5.81x

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 9

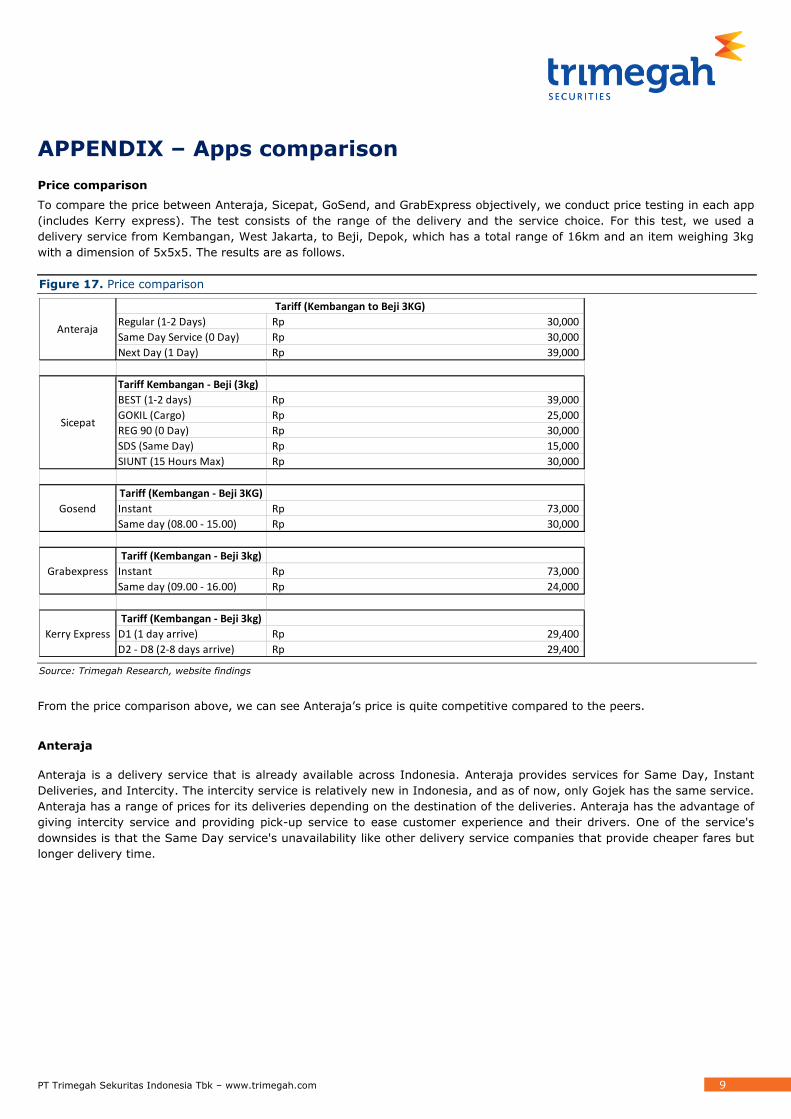

APPENDIX – Apps comparison

Price comparison

To compare the price between Anteraja, Sicepat, GoSend, and GrabExpress objectively, we conduct price testing in each app

(includes Kerry express). The test consists of the range of the delivery and the service choice. For this test, we used a

delivery service from Kembangan, West Jakarta, to Beji, Depok, which has a total range of 16km and an item weighing 3kg

with a dimension of 5x5x5. The results are as follows.

Figure 17. Price comparison

Source: Trimegah Research, website findings

From the price comparison above, we can see Anteraja’s price is quite competitive compared to the peers.

Anteraja

Anteraja is a delivery service that is already available across Indonesia. Anteraja provides services for Same Day, Instant

Deliveries, and Intercity. The intercity service is relatively new in Indonesia, and as of now, only Gojek has the same service.

Anteraja has a range of prices for its deliveries depending on the destination of the deliveries. Anteraja has the advantage of

giving intercity service and providing pick-up service to ease customer experience and their drivers. One of the service's

downsides is that the Same Day service's unavailability like other delivery service companies that provide cheaper fares but

longer delivery time.

Tariff (Kembangan to Beji 3KG)

Regular (1-2 Days) 30,000Rp

Same Day Service (0 Day) 30,000Rp

Next Day (1 Day) 39,000Rp

Tariff Kembangan - Beji (3kg)

BEST (1-2 days) 39,000Rp

GOKIL (Cargo) 25,000Rp

REG 90 (0 Day) 30,000Rp

SDS (Same Day) 15,000Rp

SIUNT (15 Hours Max) 30,000Rp

Tariff (Kembangan - Beji 3KG)

Instant 73,000Rp

Same day (08.00 - 15.00) 30,000Rp

Tariff (Kembangan - Beji 3kg)

Instant 73,000Rp

Same day (09.00 - 16.00) 24,000Rp

Tariff (Kembangan - Beji 3kg)

D1 (1 day arrive) 29,400Rp

D2 - D8 (2-8 days arrive) 29,400Rp

Anteraja

Sicepat

Gosend

Grabexpress

Kerry Express

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 10

Figure 18. Anteraja registration and login page, landing page, and delivery service’s user interface

Source: Trimegah Research, website findings

Registration Page Login Page

Profile Page Home Page Contact Us Page

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 11

Sicepat

Sicepat is a delivery service company that provides service for deliveries across Indonesia. It has five notable services called

BEST (Besok Sampai Tujuan), GOKIL (Cargo), REG (Instant Delivery), SDS (Same Day), and SIUNT (15-hour deliveries max

in jabodetabek). The advantage of Sicepat is that its service gives a relatively lower fare; however, the downside is in the

unavailable of intercity deliveries. However, due to the new account has not been verified by the customer service, we can

only provide the check ongkir (prices) feature and its landing page.

Figure 19. Sicepat Landing Page and Cek Ongkir Page

Source: Trimegah Research, website findings

GoSend

GoSend is one of the services that Gojek provides in its app that caters to deliveries inner and intercity. GoSend only

provides two delivery services which are Instant Delivery and Same Day Delivery. The Same Day Delivery service only

available between 08.00 AM until 03.00 PM. Gojek is also one of Indonesia's delivery services that have introduced their

intercity service alongside anteraja, making it feasible for users to deliver from and to different cities with affordable fares.

GoSend advantages are that they have a Same-day service that gives lower fares and has an intercity service. But on the

other hand, they also have a relatively expensive fare for its instant delivery service.

Figure 20. GoSend Service

Source: Trimegah Research, website findings

Landing Page Cek Ongkir Page Price

Gosend Service (Sameday and Instant)

GoSend Intercity Service

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 12

GrabExpress

GrabExpress is a delivery service provided by Grab. The service has changed its name from GrabSend to GrabExpress. Like

Gojek, GrabExpress also offers two services in its delivery services: Instant Delivery and Same Day Delivery. The Same Day

delivery service is only available from 09.00 AM to 16.00 AM. The advantages of grabexpress are the availability of same-

day service, which provides lower fares. Still, on the other hand, there is now an intercity option, and the fare for instant

deliveries is relatively expensive.

Figure 21. GrabExpress Delivery Service

Source: Trimegah Research, website findings

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 13

Research Team

Sebastian Tobing Strategy, Digital, Telecom, and Commodities

[email protected] +62-21 2924 9105

Willinoy Sitorus Banks, Automotive and Small Caps [email protected] +62-21 2924 9107

Fakhrul Fulvian Economics, Fixed Income [email protected] +62-21 2924 9097

Darien Sanusi Consumer Staples, Retail, Healthcare [email protected] +62-21 2924 9106

Heribertus Ariando Consumer Staples and Media [email protected] +62-21 2924 9060

Farah Rahmi Oktaviani Cement, Property and Infrastructure [email protected] +62-21 2924 6325

Rifina Rahisa Banks and Digital Financials [email protected] +62-21 2924 9103

Hasbie Small Cap & Automotive [email protected] +62-21 2924 6322

Kenny Vincent Economics, Fixed Income [email protected] +62-21 2924 6325

Pandu Megananda Digital Media [email protected] +62-21 2924 9088

Nur Marini Corporate Access [email protected] +62-21 2924 6323

Institutional Sales Team

Beatrix Susanto Head of Institutional Sales [email protected] +62-21 2924 9086

Henry Sidarta, CFTe Deputy Head of Institutional Sales [email protected] +62-21 3043 6309

Dewi Yusnita Equity Institutional Sales [email protected] +62-21 2924 9082

Raditya Andyono Equity Institutional Sales [email protected] +62-21 2924 9146

Calvina Karmoko Equity Institutional Sales [email protected] +62-21 2924 9080

Morgan Gindo Simorangkir Equity Institutional Sales [email protected] +62-21 2924 9076

Gerry Benedict Equity Institutional Sales [email protected] +62-21 2924 9081

Retail Sales Team

Andrew Jatmiko Head of Retail Equity Sales [email protected] +62-21 3043 6310

Hasbie Sukaton Deputy Head of Retail of Sales [email protected] +62-21 2924 9088

Jakarta Area

Untung Wijaya Kelapa Gading, Artha Graha, Jakarta [email protected] +62-21 4503 345

Windra Djulnaily Pluit, Jakarta [email protected] +62-21 6660 1456

Ignatius Candra Perwira BSD, Tangerang [email protected] +62-21 5386 700

Sumatera

Juliana Effendy Medan, Sumatera Utara [email protected] +62-61 4520 336

East Indonesia

Pandu Wibisono Surabaya, Jawa Timur [email protected] +62-31 5623 720

Carlo Ernest Frits Coutrier Makasar, Sulawesi Selatan [email protected] +62-41 1850 222

Central Java, Area

Mariana Kusuma Wati Semarang, Jawa Tengah [email protected] +62-24 8452 333

Antonius Santoso Solo, Jawa Tengah [email protected] +62-27 1733 328

West Java

Asep Saepudin Bandung, Jawa Barat [email protected] +62-22 4267 929

Ariffianto Cirebon, Jawa Barat [email protected] +62-23 1829 1155

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 14

Disclaimer

This report has been prepared by PT Trimegah Sekuritas Indonesia Tbk on behalf of itself and its affiliated

companies and is provided for information purposes only. Under no circumstances is it to be used or

considered as an offer to sell, or a solicitation of any offer to buy. This report has been produced

independently and the forecasts, opinions and expectations contained herein are entirely those of PT

Trimegah Sekuritas Indonesia Tbk.

While all reasonable care has been taken to ensure that information contained herein is not untrue or

misleading at the time of publication, PT Trimegah Sekuritas Indonesia Tbk makes no representation as to

its accuracy or completeness and it should not be relied upon as such. This report is provided solely for

the information of clients of PT Trimegah Sekuritas Indonesia Tbk who are expected to make their own

investment decisions without reliance on this report. Neither PT Trimegah Sekuritas Indonesia Tbk nor any

officer or employee of PT Trimegah Sekuritas Indonesia Tbk accept any liability whatsoever for any direct

or consequential loss arising from any use of this report or its contents. PT Trimegah Sekuritas Indonesia

Tbk and/or persons connected with it may have acted upon or used the information herein contained, or

the research or analysis on which it is based, before publication. PT Trimegah Sekuritas Indonesia Tbk

may in future participate in an offering of the company’s equity securities.

This report is not intended for media publication. The media is not allowed to quote this report in any

article whether in full or in parts without permission from PT Trimegah Sekuritas Indonesia Tbk. For

further information, the media can contact the head of research of PT Trimegah Sekuritas Indonesia Tbk.

This report was prepared, approved, published and distributed by PT Trimegah Sekuritas Indonesia Tbk

located outside of the United States (a “non-US Group Company”). Neither the report nor any analyst who

prepared or approved the report is subject to U.S. legal requirements or the Financial Industry Regulatory

Authority, Inc. (“FINRA”) or other regulatory requirements pertaining to research reports or research

analysts. No non-US Group Company is registered as a broker-dealer under the Exchange Act or is a

member of the Financial Industry Regulatory Authority, Inc. or any other U.S. self-regulatory

organization.

INVESTMENT RATING RULE:

Buy : Share price is expected to exceed more than 10% over the next 12 months

Neutral : Share price is expected to trade within the range of 0%-10% over the next 12 months

Sell : Share price is expected to trade below 0% over the next 12 months

Not Rated : The company is not within Trimegah research coverage

PT Trimegah Sekuritas Indonesia Tbk – www.trimegah.com 15

Analysts Certification

The research analyst(s) of PT Trimegah Sekuritas Indonesia Tbk. primarily responsible for the content of

this research report, in whole or in part, certifies that with respect to the companies or relevant securities

that the analyst(s) covered in this report: (1) all of the views expressed accurately reflect his or her

personal views on the company or relevant securities mentioned herein; (2) no part of his or her

remuneration was, is, or will be, directly or indirectly, connected with his or her specific recommendations

or views expressed in the research report; and (3) the report does not contain any material non-public

information.

The disclosure column in the following table lists the important disclosures applicable to each company

that has been rated and/or recommended in this report:

Company Ticker Disclosure (as applicable)

ASSA -

Trimegah Disclosure Data

Trimegah represents that:

1. Within the past year, it has managed or co-managed a public offering for this company, for which

it received fees.

2. It had an investment banking relationship with this company in the last 12 months.

3. It received compensation for investment banking services from this company in the last 12

months.

4. It expects to receive or intends to seek compensation for investment banking services from the

subject company/ies in the next 3 months.

5. It beneficially owns 1% or more of any class of common equity securities of the subject company.

6. It makes a market in securities in respect of this company.

7. The analyst(s) or an individual who assisted in the preparation of this report (or a member of

his/her household) has a financial interest position in securities issued by this company. The

financial interest is in the common stock of the subject company, unless otherwise noted.

8. The analyst (or a member of his/her household) is an officer, director, employee or advisory board

member of this company or has received compensation from the company.