Addressing Together the Bank’s High for transforming 5 ... · Addressing Together the Bank’s...

139

Industrialize Africa Addressing Together the Bank’s High for transforming North Africa 5 Feed Africa Integrate Africa Improve the Quality of Life for the People of Africa Light up & Power Africa 2016 2016 Africain Development Bank in North Africa

Transcript of Addressing Together the Bank’s High for transforming 5 ... · Addressing Together the Bank’s...

IndustrializeAfrica

Addressing Together the Bank’s High for transformingNorth Africa

5

FeedAfrica

IntegrateAfrica

Improve the Quality of Lifefor the People of Africa

Light up &Power Africa

20162016

Africain Development Bankin North Africa

www.afdb.org

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

32

The Annual Report of the African Development Bank’s North Africa Regional Department was prepared by Vincent Castel (Chief CountryEconomist), Kaouther Abderrahim Ben Salah (Senior Macro-economist) and Alia Amimi (Economist). The report presents Bank’s Engagementin the region and socio and economic development as of December 31, 2015.

This work benefited from contributions from Hervé Lohoues (Principal Country Economist - Algeria), Tarik Benbahmed (Country Economist)and Malek Bouzgarrou (Principal Country Programme Officer - Algeria and Mauritania) for Algeria, Angus Downie (Chief Country Economist)and Prajesh Bhakta (Chief Country Programme Officer - Egypt) for Egypt, Kaouther Abderrahim (Senior Macro-economist), Olivier Brétéché(Principal Country Programme Officer - Morocco) and Vincent Castel (Chief Country Economist - Morocco) for Morocco, Marcellin NdongNtah (Resident Chief Country Economist - Mauritania) and Amine Mouaffak (YPP, ORNA) for Tunisia, Philippe Trape (Principal CountryEconomist - Tunisia) and Mickaelle Chauvin (Economist, ORNA) for Tunisia and Raïs Wadii (Financial Analyst - Morocco).

The Thematic Section (chapters 1 to 4) was prepared by Vincent Castel (Chief Country Economist - Morocco), Kaouther Abderrahim BenSalah (Senior Macro-economist) and William Shaw (Economist, AfDB). The chapters are based on the African Economic Outlook of the sixcountries of the North Africa region, written by AfDB’s economists : Tarik Benbahmed (Country Economist), Hervé Lohoues (PrincipalCountry Economist - Algeria) and Mickaelle Chauvin (Economist, ORNA) for Algeria, Prajesh Bhakta (Chief Country Programme Officer -Egypt), Diarra-Thioune Assitan (Regional Economist, ORNA) and Angus Downie (Chief Country Economist) for Egypt, Kaouther AbderrahimBen Salah (Senior Macro-economist) for Libya, Vincent Castel (Chief Country Economist - Morocco) for Morocco, Marcellin Ndong Ntah(Resident Chief Country Economist - Mauritania), Isiyaka Sabo (UNDP), Selma Cheikh Malainine (UNDP) for Mauritania, Kaouther AbderrahimBen Salah (Senior Macro-economist) and Philippe Trape (Principal Country Economist - Tunisia) for Tunisia.

The authors would like to thank for their contributions: Assitan Diarra-Thioune (Regional Economist), Leila Mokadem (Resident Representative- Egypt), Yacine Fal (Resident Representative - Morocco), Boubacar Traoré (Resident Representative - Algeria), Yasser Ahmad (Chief CountryProgramme Officer - Egypt, Libya), Thouraya Triki (Chief Country Economist) and Yasmine Moustapha Eita (Principal Country ProgrammeOfficer).

Projects Briefs were also reviewed by various Operations Officers from Sector Departments: Mr. Mohamed Ould Tolba (Chief AgriculturalEconomist, OSAN), Mrs. Audrey Chouchane (Chief Research Economist, EDRE), Mr. Mamadou Yaro Chief (regional Financial ManagementCoordinator, ORPF), Mr. William Coovi Firmin Dakpo (Chief Regional Procurement Coordinator, ORPF), Mrs. Selma Ennaifer (Chief FinancialManagement Specialist, ORPF), Mr. Riadh Belhaj (Principal Risk Officer, FFMA), Mrs. Blandine Wu Chebili (Principal Procurement Officer,ORPF), Mr. Mouhamed Gueye (Principal Education Economist, OSHD), Mr. Fernando Rodrigues (Senior Investment Officer, OPSD), Mr. Oussama Ben Abedelkarim (Senior Education Economist, OSHD), Mrs Sonia Barbaria (Consultant), Mrs. Charlotte Karagueuzian(Consultant, EDRE), Mohamed Labben (Consultant, ORPF), Mr. Ali Kies (Consultant, OITC), Mr. Emmanuel Diarra (Principal FinancialEconomist), Mr. Adama Moussa (Principal Electrical Engineer), Mr. Pierre More Ndong (Principal Transport Engineer), Mr. Driss Khiati(Agricultural Expert), Mr. Mohammed El Ouahabi (Water and Sanitation Specialist), Mrs. Leila Kilani-Jaafor (Social Development Specialist),Raïs Wadii (Financial Analyst - Morocco), Ms. Gehane El Sokkary (Senior Socio Economist), Mr. Tarek Ammar (Principal Private SectorSpecialist), Mr. Khaled El Askari (Senior Infrastructure Specialist) and Mr. Yasser Alwan (Senior Irrigation Engineer).

This report was prepared under the guidance of Mr. Jacob Kolster (Director, ORNA).

The African Development Bank (AfDB)

This document was prepared by the African Development Bank (AfDB). Designations employed in this publication do not imply the expressionof any opinion on the part of the institution concerning the legal status of any country, or the limitation of its frontier. While efforts have beenmade to present reliable information, the AfDB accepts no responsibility whatsoever for any consequences of its use.

Published by: the African Development Bank (AfDB)

HeadquartersAfrican Development Bank Group Avenue Joseph Anoma01 BP 1387 Abidjan 01Côte d'IvoireTél.: (+225) 20 26 44 44Fax: (+225) 20 21 31 00

Tunis AgencyAvenue du Dollar, Berges du Lac 2 1053 – Tunis, TUNISIETel.: (+216) 71 10 29 53Fax: (+216) 71 19 45 23

Design and LayoutYasso creation: Hela Chaouachi ([email protected])

Copyright © 2015 African Development BankWebsite: www.afdb.org

3

Table of contents

5 Preface

9 Acronyms

15 CHAPTER 1 OVERVIEW – NORTH AFRICA IN 201616 Macroeconomic Developments and Prospects

18 Private Sector Development and the Financial Sector

19 Public Sector Management and the Political Context

19 Natural Resource Management

19 Human Resource Development

20 Poverty Reduction, Social Protection and Labour

20 Gender Equality

23 CHAPTER 2 MACROECONOMIC DEVELOPMENTS AND PROSPECTS IN NORTH AFRICA24 Recent Developments and Prospects

27 Fiscal Policy

28 Monetary Policy

31 Economic Co-operation and the External Sector

32 Debt P olicy

37 CHAPTER 3 CHALLENGES FACING PUBLIC SECTOR MANAGEMENT AND PRIVATE SECTOR DEVELOPMENT

38 Private Sector Development

39 Financial Sector

41 Public Sector Management

43 Political Context

45 Natural Resources and the Environment

49 CHAPTER 4 SOCIAL DEVELOPMENTS IN NORTH AFRICA50 Human Resource Development53 Poverty Reduction, Social Protection and Labour57 Gender Equality

61 CHAPTER 5 THE AFRICAN DEVELOPMENT BANK GROUP IN BRIEF63 Who We Are & What We Do63 Five Operational Priorities65 How We Are Financed66 Africa’s Knowledge Bank

69 CHAPTER 6 BANK GROUP ACTIVITIES IN NORTH AFRICA

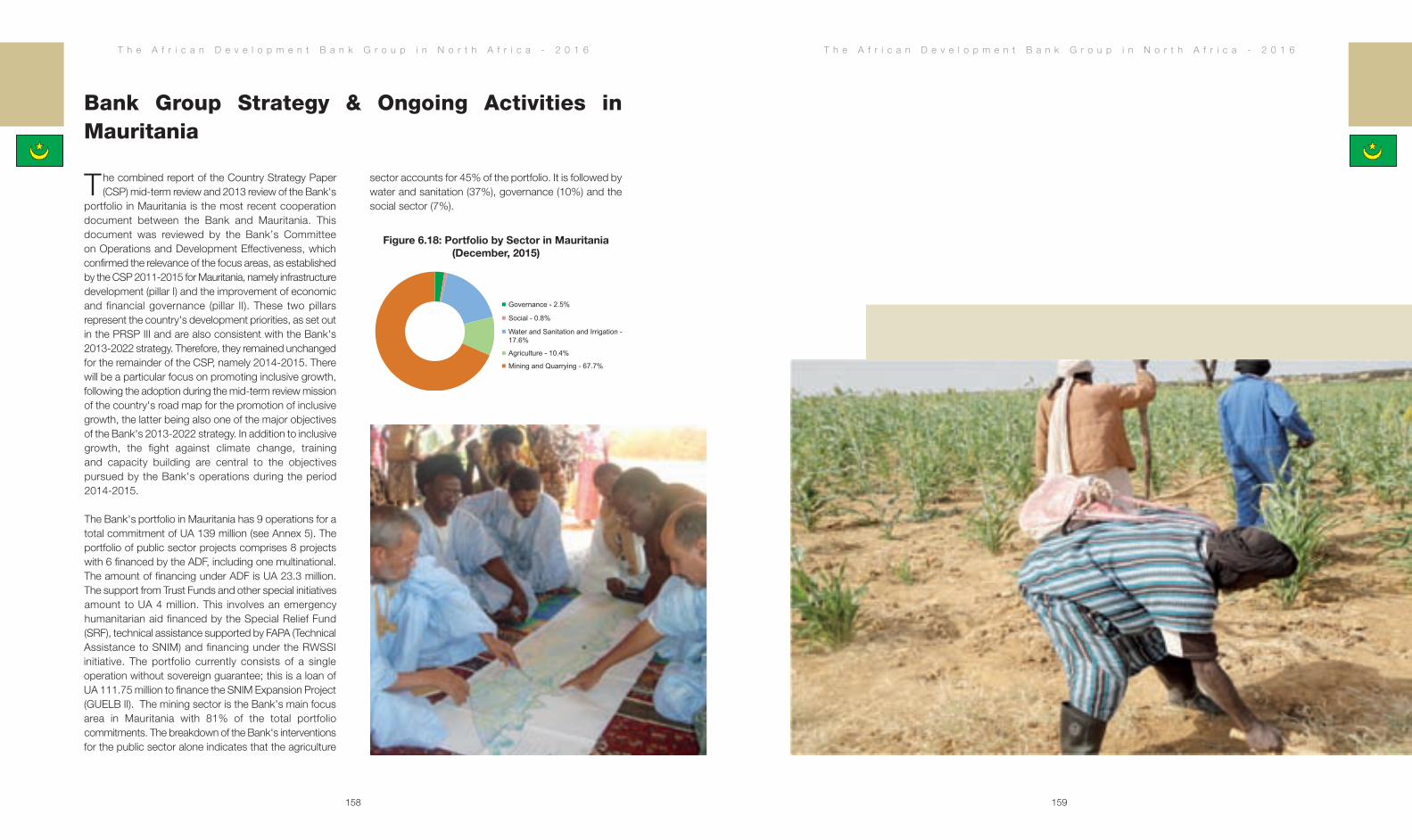

71 Regional Overview

77 Algeria

101 Egypt

143 Libya

153 Mauritania

167 Morocco

227 Tunisia

269 CHAPTER 7 STAFF & CONTACT DETAILS

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

54

Preface

Since 2015, and to accelerate the transformation ofthe African continent, the African Development

Bank is committed to focus its efforts on five priority areas : Lighting Africa, Feeding Africa, Integrating Africa,Industrializing Africa and improving the quality of life for the people of Africa. These new priorities perfectlymeet the challenges facing North Africa to ensure a more inclusive development as highlighted by the socialdemands which were in several countries of the regionsince 2011.

The industrialization of the region through thedevelopment of value chains and the sophistication ofgoods and services is one of the most importantchallenges to be addressed, for these economies torespond to the issue of unemployment especially amongyouth and to create better jobs. Indeed, economies whoseexport structure is more diverse tend to have a higherincome per capita and countries that export moresophisticated products tend to have faster growth.

From the perspective of energy, the rapid increase indemand observed in all North African countries isexplained by population growth, the development ofproductive activities and the improvement of the qualityof life. The changes in demand and structure, are a majorchallenge for all electricity companies that must investheavily to satisfy this demand. Fossil fuels (oil, naturalgas, coal) in all North African countries account forbetween 95% and almost all of the primary energy supply. The efficient use of these resources must be strengthened. However, these countries have aconsiderable bearing on renewable energy, and countriesthe ability to deploy multiple technological options. Effortsby all countries in this direction should be supported andare full of promises.

Integration, should also be promoted throughinfrastructure development that strengthen the national

network and those that connect the countries with eachother and the world. This development is necessary to expand the size of markets and reduce the cost of movement of goods, persons and services. Thisdevelopment also strengthens the cooperation, exchangeand reduces inequalities in the region by ensuring betteraccess to basic services and economic opportunities.

Agriculture in North Africa is back on the front scenesince the rising of food prices at the end of 2006 as thefood security of the region largely depends on globalmarkets. Social movements in the region have also drawnattention to the importance of agriculture, because peoplein the least developed regions are heavily dependent(directly or indirectly) on this sector. But it is also a sectorwhere value chains must be developed and which mustbe industrialized so that economies can benefit from thesector’s full potential and so that rural living conditionscan be improved.

Finally, improving the quality of life of African andespecially women and young people is at the heart ofaspirations of North African populations. Indeed, the toppriority today is to allow them to participate in theeconomy with all the advantages and the potential they represent. For that, the quality of all basic servicesincluding education, access to quality health care,vocational training must be improved as well as thepromotion of entrepreneurship.

This annual report in Chapter 6 presents for each countryand for each project financed by the Bank how the Banksupports North Africa to meet these five priorities.

Moreover, the report presents in the thematic sectionprogress but also short and medium term issues andchallenges that countries face and which influence theprogresses made in achieving the objectives of the fivepriorities set by the Bank.

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

7

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

In Chapter 1, "Overview of the region of North Africa",we present an overview of the situation in the North Africancountries in light of recent experience.

Chapter 2, entitled "Development and macroeconomicprospects in North Africa," presents the economic trendbut also the forecast for regional growth in the future.

Chapter 3, entitled " Challenges Facing Public SectorManagement and Private Sector Development"introduces the recent changes concerning thedevelopment of private sector and public sectormanagement.

Chapter 4, entitled "Social Development in North Africa,"examines social developments, in particular, improvementsin the coverage of health services and education,reducing inequalities but also to the promotion of genderin region.

We hope that this report will be useful and look forwardto receiving any feedback from you.

Jacob KolsterDirector

North Africa Regional Department

6

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

98

AEOAfDBAFESDAIDSAMINAAMUASEAN BCIBCMBIOBMC BMICECBECEN-SADCESECIMRCNAMCNEACNEDCNSSCORCCSPCTFDAIPDBPMFDPEFDWSDZFOECECOWASEEDC EGFOEIBEMAFENID EUFAOFAPAFDI

African Economic OutlookThe African Development Bank GroupArab Fund for Economic and Social DevelopmentAcquired Immune Deficiency SyndromeMicrofinance Initiative for Africa of the African Development fundArab Maghreb UnionAssociation of Southeast Asian Nations Banque pour le Commerce et l’IndustrieBanque Centrale de Mauritanie Belgian Investment Company for Developing Countries Basic Medical CoverageThe Maghreb Bank for Investment and Foreign Trade Central Bank of EgyptThe Community of Sahel-Saharan StatesConseil Economique, Social et Environnemental du MarocCaisse Interprofessionnelle Marocaine de RetraiteNational Health Insurance Fund National Business Environment Committee Caisse Nationale d’Equipement pour le DéveloppementNational Social Insurance Fund Cairo Oil Refining Company Country Strategy Paper Clean Technology Fund Assistance mechanisms for the professional integration Directorate for Public Sector Banks and the Financial Market Directorate of Education and Training ProjectsDrinking Water SupplyAlgeria Country OfficeEuropean CommissionEconomic Community of West African States Egypt Economic Development ConferenceEgypt Country OfficeEuropean Investment BankExport Market Access FundingEgypt Network for Integrated Development European UnionUnited Nations Food and Agriculture OrganizationFund for African Private Sector AssistanceForeign direct investment

Acronyms

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

11

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

10

FIVFPMEIFRRFSAPGCC GDAGDPGEFGISGNAGNCGoEGSM HDIHIVIADPICAICSPIDBIFCIFESILOIMFIMPIPEIRMSISETJBICJISAKFAEDKOFEAC LEPCLPALTSMAFOMAPMMCCMDBsMDGMENA

MERCOSUR MFIMFN MICMIC-TAF

Neighbourhood Investment FacilityFonds pour les PME et l’innovationRevenue Regulation Fund Financial Sector Assessment ProgramGulf Cooperation Council Support for Agricultural Development Groups Gross Domestic Product Global Environment FacilityGeographic information system Government of National Accord General National Congress Government of Egypt Global system for mobile communication Human Immunodeficiency IndexHuman Immunodeficiency Virus North Gafsa Integrated Agricultural Development Project Infrastructure Consortium for AfricaInterim Country Strategy Paper Islamic Development BankInternational Finance CorporationInternational Foundation for Electoral Systems International Labour Organization International Monetary FundIT Master Plan Job Loss Allowance Integrated Resources Management StrategyInstitut Supérieur d’Enseignement TechnologiqueJapanese Bank for Investment and CooperationJoint Integrated Sector Approach Kuwait Fund for Arab Economic DevelopmentKorea Africa Cooperation Trust FundLibyan Export Promotion CentreLibyan Political Agreement Long-Term Strategy Morocco Country OfficeMinistry of Agriculture and Maritime FisheriesMillennium Challenge Corporation Multilateral Development BanksMillennium Development Goals Middle East and North Africa Maghreb Leasing Algeria Memorandum of UnderstandingMercado Común Sur (Argentina, Brazil, and Uruguay)Mircro finance isntitutions Most Favored NationMiddle income countries Middle Income Country Technical Assistance Fund

MLAMoUMPCMSEMTSMWMWPPNAFTA NBE NDPNGONPLs NREANSSDNTFNTMs OCPOECDONEEOPECORNAPAAFEPADESFIPAES IIPAFEJPAFTA PAIPANEPAPMV-2PARAPPARCOUM IIIPARGEFPDAI IIPDRTREPIEHERPISAPISEAU IIPMIPMNPNDSEPNEEIPPCPPPPRECAMFPRPRADEEMA

Maghreb Leasing AlgeriaMemorandum of UnderstandingMonetary Policy Committee Micro and Small EnterprisesMedium Term StrategyMegawattMulti-Donor Water Partnership ProgramNorth American Free Trade Agreement National Bank of EgyptNational Drainage Programme Non Governmental OrganisationsNonperforming loans New & Renewable Energy AuthorityNational Strategy of Sustainable Development The Nigeria Trust FundNontariff measures Cherifian Phosphates Company Organization for Economic Cooperation and Development National Electricity and Drinking Water Authority The Organization of the Petroleum Exporting CountriesCountry Regional Department North AfricaProgramme for matching training-employment The Financial Sector Development Support ProgramSecond Secondary Education Support Project Support to the Training and Employment of Young People Pan-Arab Free Trade Area Integration Support ProgramNational Action Plan for the Environment Green Morocco Plan Support Programme - Phase 2 Public Administration Reform Support Programme Medical Coverage Reform Support Programme Economic and Financial Governance Revitalization Support ProgrammeGabes Integrated Agricultural Development Project Electricity Transmission and Distribution Network Development Project Integrated Wind Energy Hydropower Rural Electrification ProgrammeProgram for International Student Assessment Water Sector Investment Project Phase 2Industrial Modernization ProgramIndustrial Upgrading ProgramEducation System Development Support ProjectNational Irrigation Water Saving Programme Petroleum Pipeline Company Purchasing Power ParityProject to build the capacities of Microfinance StakeholdersPoverty Reduction ProgramMarrakesh Autonomous Water and Electricity Distribution Authority

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

13

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

12

RAMEDRERIEEPRMCsRRARWSSISESP IISFDSFD*SIFEMSINEAUSMESNATSNIMSNTFSTRI TFSTRAINS UAUNUNAIDSUNCTAD UNDPUNICEFUPSUSA USAIDUTICAVATWB WTO

Régime d’Assistance Médicale aux Economiquement DémunisRenewable energy Rural Income and Economic Enhancement Project Regional Member CountriesRenewables Readiness Assessment Rural Water Supply and Sanitation InitiativeSecondary Education Support Project Phase IIEgypt Social Fund for DevelopmentSaudi Fund for DevelopmentSwiss Investment Fund for Emerging MarketsNational Water Information System Small and Medium EnterprisesNational Scheme of Land Planning National Industrial and Mining Company of MauritaniaSociété Nationale des Transports Ferroviaires Services Trade Restrictiveness Index Technical feasibility study Trade Analysis and Information System Unit of AccountsUnited NationsUNAIDS, the Joint United Nations Programme on HIV/AIDSUnited Nations Conference on Trade and Development United Nations Development ProgramLe Fonds des Nations unies pour l'enfanceUnified Power SystemUnited States of America United States Agency for International DevelopmentUnion tunisienne de l'industrie, du commerce et de l'artisanatValue-added TaxWorld BankWorld Trade Organization

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

15

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

14

Chapter 1 Overview – North Africa in 2016

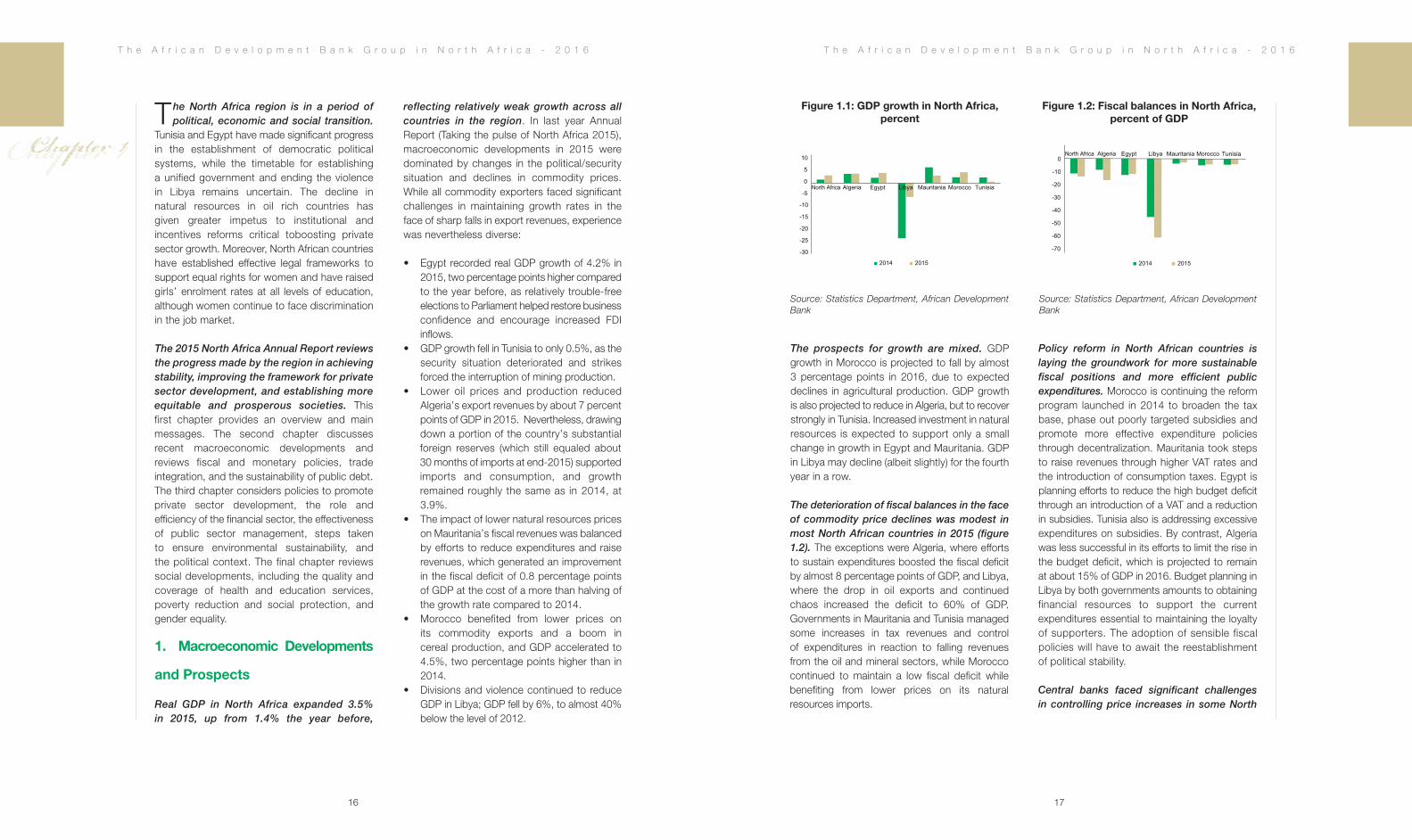

The prospects for growth are mixed. GDPgrowth in Morocco is projected to fall by almost 3 percentage points in 2016, due to expecteddeclines in agricultural production. GDP growth is also projected to reduce in Algeria, but to recoverstrongly in Tunisia. Increased investment in naturalresources is expected to support only a smallchange in growth in Egypt and Mauritania. GDP in Libya may decline (albeit slightly) for the fourth year in a row.

The deterioration of fiscal balances in the faceof commodity price declines was modest inmost North African countries in 2015 (figure1.2). The exceptions were Algeria, where efforts to sustain expenditures boosted the fiscal deficitby almost 8 percentage points of GDP, and Libya,where the drop in oil exports and continued chaos increased the deficit to 60% of GDP.Governments in Mauritania and Tunisia managedsome increases in tax revenues and control of expenditures in reaction to falling revenues from the oil and mineral sectors, while Moroccocontinued to maintain a low fiscal deficit whilebenefiting from lower prices on its naturalresources imports.

Policy reform in North African countries islaying the groundwork for more sustainablefiscal positions and more efficient publicexpenditures. Morocco is continuing the reformprogram launched in 2014 to broaden the taxbase, phase out poorly targeted subsidies andpromote more effective expenditure policiesthrough decentralization. Mauritania took steps to raise revenues through higher VAT rates and the introduction of consumption taxes. Egypt isplanning efforts to reduce the high budget deficitthrough an introduction of a VAT and a reductionin subsidies. Tunisia also is addressing excessiveexpenditures on subsidies. By contrast, Algeriawas less successful in its efforts to limit the rise inthe budget deficit, which is projected to remain at about 15% of GDP in 2016. Budget planning inLibya by both governments amounts to obtainingfinancial resources to support the currentexpenditures essential to maintaining the loyalty of supporters. The adoption of sensible fiscalpolicies will have to await the reestablishmentof political stability.

Central banks faced significant challenges in controlling price increases in some North

Source: Statistics Department, African DevelopmentBank

-70

-60

-50

-40

-30

-20

-10

0North Africa Algeria Egypt Mauritania Morocco Tunisia

2014 2015

Libya

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

17

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

16

The North Africa region is in a period ofpolitical, economic and social transition.

Tunisia and Egypt have made significant progressin the establishment of democratic politicalsystems, while the timetable for establishing a unified government and ending the violence in Libya remains uncertain. The decline in natural resources in oil rich countries has given greater impetus to institutional andincentives reforms critical toboosting privatesector growth. Moreover, North African countrieshave established effective legal frameworks tosupport equal rights for women and have raisedgirls’ enrolment rates at all levels of education,although women continue to face discriminationin the job market.

The 2015 North Africa Annual Report reviewsthe progress made by the region in achievingstability, improving the framework for privatesector development, and establishing moreequitable and prosperous societies. This first chapter provides an overview and mainmessages. The second chapter discussesrecent macroeconomic developments andreviews fiscal and monetary policies, tradeintegration, and the sustainability of public debt.The third chapter considers policies to promoteprivate sector development, the role andefficiency of the financial sector, the effectivenessof public sector management, steps taken to ensure environmental sustainability, and the political context. The final chapter reviews social developments, including the quality andcoverage of health and education services,poverty reduction and social protection, andgender equality.

1. Macroeconomic Developments

and Prospects

Real GDP in North Africa expanded 3.5% in 2015, up from 1.4% the year before,

reflecting relatively weak growth across allcountries in the region. In last year AnnualReport (Taking the pulse of North Africa 2015),macroeconomic developments in 2015 weredominated by changes in the political/securitysituation and declines in commodity prices. While all commodity exporters faced significantchallenges in maintaining growth rates in theface of sharp falls in export revenues, experiencewas nevertheless diverse:

• Egypt recorded real GDP growth of 4.2% in 2015, two percentage points higher compared to the year before, as relatively trouble-free elections to Parliament helped restore businessconfidence and encourage increased FDI inflows.

• GDP growth fell in Tunisia to only 0.5%, as the security situation deteriorated and strikes forced the interruption of mining production.

• Lower oil prices and production reduced Algeria’s export revenues by about 7 percent points of GDP in 2015. Nevertheless, drawing down a portion of the country’s substantial foreign reserves (which still equaled about 30 months of imports at end-2015) supported imports and consumption, and growth remained roughly the same as in 2014, at 3.9%.

• The impact of lower natural resources prices on Mauritania’s fiscal revenues was balanced by efforts to reduce expenditures and raise revenues, which generated an improvement in the fiscal deficit of 0.8 percentage points of GDP at the cost of a more than halving of the growth rate compared to 2014.

• Morocco benefited from lower prices on its commodity exports and a boom in cereal production, and GDP accelerated to 4.5%, two percentage points higher than in 2014.

• Divisions and violence continued to reduce GDP in Libya; GDP fell by 6%, to almost 40% below the level of 2012.

Figure 1.1: GDP growth in North Africa,percent

Source: Statistics Department, African DevelopmentBank

-30

-25

-20

-15

-10

-5

0

5

10

North Africa Algeria Egypt Libya Mauritania Morocco Tunisia

2014 2015

Figure 1.2: Fiscal balances in North Africa,percent of GDP

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

19

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

African countries over 2015, but broadlyspeaking price increases remained moderate,except in Egypt and Libya. Accommodatingmonetary policies to support demand allowedsome rise in inflation in Algeria and Morocco(although price increases remained below 2percent in the latter country), and continued,relatively high inflation in Tunisia. Authoritiesfollowed a somewhat more restrictive policystance in Mauritania, and inflation fell to below 2percent. In Egypt, exchange rate depreciation wasassociated with increasing inflationary pressurestowards the end of the year, and authoritiesadopted a more restrictive stance in December,which is likely to reduce inflation this year.Monetary policy remained in disarray in Libya, with a (somewhat unreliable) estimate of a rise in the CPI of more than 8%.

The sustainability of the macroeconomicprogram is constrained by the level of publicdebt in some North African countries. Egypt willface a significant challenge in servicing its publicdebt (95.5% of GDP) while financing the rise inpublic expenditures necessary for growth andavoiding crowding out private sector demand forcredit. Mauritania’s difficulties in servicing its highdebt level of 77.4% of GDP are exacerbated by

institutional weaknesses. By contrast, Algeria hasa relatively small level of public debt, but this mayexpand if oil prices remain low and economicdiversification remains limited. Morocco’s debt isslightly higher than Tunisia’s (in relation to GDP),but Morocco’s high share of domestic debtprovides some insulation from external shocks,while Tunisia has greater exposure to externalcreditors. Libya’s public debt is only about 20% ofGDP, but macroeconomic policy is in shamblesand huge demands to sustain life and supportrecovery will arise once political stability is restored.

2. Private Sector Development

and the Financial Sector

Efforts are underway to ease regulatoryconstraints that limit competition anddiscourage investment in Tunisia, Egypt,Mauritania, and to some extent in Algeria, andseveral North African countries achieved someimprovement in global rankings of the qualityof business environment in 2015. Morocco has achieved the most success in establishing adiversified economy and supporting private sectorgrowth, in part because of the strength of its publicinstitutions, in part because unlike other countriesin the region, Morocco lacks the energy or mineralresources that result in real exchange rateappreciation and thus impair the competitiveposition of manufactures.

North African financial systems remainrelatively under-developed, heavily bank-focused, and for the most part dominated bythe public sector. Government efforts wereunderway in 2015 to rationalize state bankinginstitutions in Tunisia, to strengthen bankingsupervision and encourage the development of electronic banking in Mauritania, to establish a central credit registry for businesses andhouseholds in Algeria, to establish an on-linesystem to track the use of movable property ascollateral in Egypt (which should facilitate an

18

expansion of lending to small businesses), and to strengthen the legal framework for bankingsupervision in Morocco. Nevertheless, thetransition to a more dynamic, private sectorbanking system remains slow and reliance oncapital markets as a source of funding is extremelylimited, except in Morocco’s diversified andprivate-sector oriented financial system. TheLibyan financial sector has suffered with theexplosion of violence, and will require a thoroughoverhaul once political stability is re-established.

3. Public Sector Management

and the Political Context

Public sector management in North Africasuffered some deterioration over the past few years with the political disturbancessurrounding the Arab Spring. Programs in 2015to strengthen public sector management focusedon improving the legal framework for the provisionof public services and using the Internet to improve the efficiency of services in Morocco,strengthening merit-based recruitment in Egyptand Tunisia, rationalizing compensation systemsand strengthening transparency in Mauritania, and improving the productivity of state enterprisesin Algeria. Public sector management continued to deteriorate in Libya with the establishment ofcompeting governments. Despite these considerableefforts, most North African countries scorerelatively poorly on international comparisons of the effectiveness of public institutions.

The consolidation of democracy continued in the region. The first Parliament under the new Egyptian regime was convened inJanuary 2016. Tunisia has made remarkableprogress towards democracy since 2011, and a new legislature was elected in late 2014. The Mauritanian Government is reaching out to establish a dialogue with the opposition and isencouraging greater participation of the young in politics. Political stability was maintained inAlgeria, although the Government undertook a

reshuffling of the cabinet and changes in theleadership of state corporations. Further progresswas made in Morocco in the process ofdecentralization enshrined in the 2011 Constitution.In Libya, however, rival governments are competingfor political legitimacy, while in many areas powerremains in the hands of militias.

4. Natural Resource Management

North Africa faces severe environmentalchallenges. Most seriously, the region is one ofthe most water-scarce regions in the world, and isvulnerable to further deterioration with the onset ofclimate change. Morocco made progress last yearin decentralizing environmental protection activitiesand promoting organic agriculture. Tunisia has an effective legal framework for the protection of the environment, although strikes in the wastemanagement services and difficulties in enforcingthe law have led to some deterioration inenvironmental management since 2011. Mauritaniatook steps in 2015 to strengthen the regulatoryand legal framework for the environment, boththrough the ratification of international agreementsand the development of domestic policies.Environmental planning in Algeria is focusing onthe preservation of natural resources, pollutioncontrol, and increasing reliance on renewableenergy sources. Egypt’s National Strategy forSustainable Development provides for review of the environmental implications of investmentprojects and promotes sustainable developmentpractices, although implementation has beenlimited. Finally, the security situation in Libya has made it impossible to address pressingenvironmental issues.

5. Human resource development

Social sectors absorb a substantial portion ofState expenditures in North African countries.Net enrolment rates in primary education are high,and the incidence of communicable diseases islow. Significant efforts were made in 2015 toexpand health and education services in the

Source: Statistics Department, African DevelopmentBank

2014 2015

0

2

4

6

8

10

12

North Africa Algeria Egypt Libya Mauritania Morocco Tunisia

Figure 1.3: Consumer price inflation inNorth Africa, percent

region, with a particular focus on reaching poorand disadvantaged groups. Examples include the provision of scholarships and health insurance to the poor in Morocco, educational reform inTunisia, and awareness campaigns and otherefforts to expand health services coverage inMauritania. Despite this progress, disparitiesamong regions and income groups in access toservices, and in health and education outcomes,remain profound. North African countries tend toscore poorly in international rankings of humandevelopment (figure 1.4). The average ranking forthe region on the UN Human Development Indexis 110 (out of a total of 188 countries), and onlyAlgeria ranks in the top half.

6. Poverty Reduction, Social

Protection and Labour

Poverty rates have fallen sharply in NorthAfrica. In the most recent surveys available, theshare of the population living in absolute povertyaccording to international comparisons haddropped to below one percent in Morocco, 2% in Tunisia, and 11% in Mauritania. Notableachievements in recent years have include

increased coverage of pensions and publicinsurance schemes in Morocco, policies thatsignificantly reduced inequality in Mauritania, andthe shift from universal to more targeted subsidyprograms in Algeria, Egypt, and Morocco. As withthe provision of services, considerable regionaland rural/urban disparities in income and povertylevels remain.

Labour market rules in North Africa haveemphasized the protection of labour, atsignificant cost in terms of private sectorgrowth, unemployment, and a proliferation of informal sector activities where socialprotection is limited. Moreover, the recentdecline in natural resources prices has underlinedthe importance of ensuring a more diversifiedeconomy led by private sector activity. Whileefforts are underway in the region to providesocial protection to the unemployed and assisttheir search for jobs, little progress was made in2015 in reforming labour market regulation.

7. Gender Equality

The legal framework in North Africa generallyprovides equal rights for women. Programsimplemented in 2015 to protect women includeefforts to combat violence against women inAlgeria and Morocco, and training targeted at girls who leave school in Tunisia. Discrimination in favour of women has substantially increased their participation in local and national legislativebodies in several countries. While women tend to have somewhat unequal access to secondaryschool education, the net enrolment rates inprimary school of boys and girls are almost equal, and in Algeria and Tunisia enrolment in tertiaryeducation is significantly higher among women.Nevertheless, women face severe discriminationin the job market, and North African countries areranked very low in international comparisons ofthe status of women. Labour force participationrates among women are only about 31% of rates among men. Of those participating in the

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

21

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

20

Figure 1.4: Human Development Index(ranking out of 188 countries)

Ranking

Algeria Egypt Libya Mauritania Morocco Tunisia 0

20406080

100120140160180

labour force, unemployment rates among womenexceed that of men by 9 percentage points in Tunisia and 7 percentage points in Algeria.Women also tend to have a higher share of

participation in vulnerable employment, a muchlower share of responsible positions, and toreceive lower compensation to equivalent jobs,compared to men in the private sector.

Source: United Nations Human Development Index2015

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

23

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

22

Chapter 2Macroeconomic developments andprospects in North Africa

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

25

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

24

E conomic conditions broadly improved in North Africa in 2015. Regional GDP

increased 3.5%, up from 1.4% in 2014. Progressin achieving political stability in Egypt supporteda recovery in growth, which was two percentagepoints higher than in 2014. A deterioration insocial peace in Tunisia contributed to near-stagnation in GDP. Libya remains in a fragilesituation, although at least the pace of declinein GDP is easing. Sharp falls in the internationalprices of oil, iron, gold, and other commoditiesdepressed export revenues in most countries.However, the impact on GDP and externalaccounts varied considerably, depending on theextent of commodity dependence and thepolicies pursued. For example, Algeria sustainedpublic expenditures by drawing down financialassets, so that the fall in oil exports was reflectedin a sharp rise in the current account and fiscal deficits, and growth remained roughlyunchanged. By contrast, declining exportrevenues cut Mauritania’s growth rate in half, butits fiscal deficit fell as the government took stepsto control expenditures and raise revenues.Morocco had a very different experience,enjoying lower prices on its commodity importsand a boom in the agricultural sector that led toa near-doubling of GDP growth.

1. Recent Developments and

Prospects

The acceleration of GDP in 2015 on average(table 2.1) reflected a very mixed experienceacross countries. Continued security concernsand declines in the prices of key primarycommodity exports reduced GDP growth inMauritania and Tunisia, and continued the declinein GDP in Libya, albeit at a slower pace than in2014. By contrast, Algeria maintained growthat roughly the 2014 level in the face of falling oil prices; a bumper harvest almost doubled the rate of growth of GDP in Morocco, whileimproved political stability supported a rise ofGDP growth in Egypt.

Our forecast for regional growth in 2016-17also reflects diverging trends, as growth isprojected to continue at the 2015 pace in Egypt, and increase in Tunisia and (slightly) in Mauritania, while the decline in Libyan GDP continues to moderate. The growth ratein 2016 is forecast to actually slightly declineas the economy adjusts to low oil prices, andin Morocco due to an expected decline inagricultural production.

• Algeria

GDP in Algeria increased by 3.9% in 2015,compared to 3.8% in the previous year,despite the decline in the world market price of oil and a continued decline in oilproduction. As the oil sector generates 30% ofnominal GDP, 50% of State revenue and almostall exports, the Algerian economy has beenheavily affected by the decline in internationalprices. Non-oil sector trends have beensignificantly more favourable, as value added inreal terms for the 2015 fiscal year rose by 7.6%in agriculture, 5.9% in services and 5.3% inconstruction. GDP growth is expected to easeto 3.4% in 2016, as authorities take steps in limitinflationary pressures, and to decline to 3% in2017.

• Egypt

Real GDP in Egypt expanded 4.2 percent in2015, almost double the rate of increase inthe previous year. The recovery was supportedby increased political stability, marked by almosttrouble-free parliamentary elections (althoughparticipation was only about 30%), which hasimproved business sentiment. Greater politicalstability helped global credit rating agencies-Standard & Poor’s, Moody’s and Fitch-maintainpositive ratings for the economy.

The successful Egypt Economic DevelopmentConference (EEDC) held in March 2015,whichresulted in actual and pledged investmentagreements totaling $175.2 billion, was followedby the launching of the new Suez Canal AreaDevelopment Project (the SCZone), which aimsto increase the role of the Suez Canal region ininternational trading and to develop the ports ofIsmaila, Port Said and Ain Sokhna.

Real GDP growth is projected to reach 4.3% in 2016 and 4.5% in 2017, driven by new

investments in the oil and gas sector, and growth in public investment. Key elements ofthe Government’s policy reforms include fullyimplementing the subsidy smart card system,the second phase of fuel price increases,implementation of the VAT tax, and increasingefficiency of fiscal expenditures.

• Libya

Falling oil production and the civil war hasreduced real GDP in Libya by about 40% since2013. The pace of decline slowed in 2015, to afall in GDP of 6%. The departure of mostinternational oil company workers in 2015, thesharp fall in international oil prices, and thereduction of maintenance and capital investmentreduced oil output to an average of 400,000barrels per day from January to October 2015,compared to 1.55 million in 2010. Public andprivate investment fell sharply in 2015, on the backof falling oil output, and weak consumer andbusiness sentiment. Spending on infrastructureand economic diversification has been severelycurtailed to sustain current expenditure. Long-delayed reconstruction works will likely not be revived before the fighting ends and a unified government is established. Economicperformance for 2016 and beyond is highlydependent on the formation of a unifiedgovernment, the re-establishment of security,containment of Islamic State activities, and therecovery of oil production to pre-2011 levels.

• Mauritania

Mauritania’s GDP increased by 3.1% in 2015,less than half the 6.6% increase in 2014, largelydue to the decline in the price of iron ore, its main export product. The slowdown ineconomic growth in 2015 was also driven by afall in investment from 47.2% of GDP in 2014 to33.3% in 2015. Economic prospects remainpromising in the short term due to expected

Table 2.1: GDP growth in North Africa (percent)

2014 2015 (e) 2016 (p) 2017 (p)

North Africa 1.4 3.5 3.3 3.8

Algeria 3.9 3.9 3.4 3.0

Egypt 2.2 4.2 4.3 4.5

Libya -23.5 -6.0 -0.8 3.9

Mauritania 6.6 3.1 3.5 4.5

Morocco 2.4 4.5 1.8 3.5

Tunisia 2.3 0.5 2.0 2.4

Source: Data from domestic authorities; estimates (e) and projections (p) based on authors’ calculations)

doubled in five years, while the investmentbudget remains under-executed and subject tofrequent downward adjustments. Given its fragileeconomic performance and limited fiscal space,the Government has little flexibility in combatingunemployment, which equalled 15% of thelabour force in 2015.

2. Fiscal Policy

While reduced commodity prices placedconsiderable pressure on North African fiscalaccounts in 2015, fiscal outcomes depended

critically on government policies and the overall economic situation. Thus, the AlgerianGovernment maintained expenditures in the faceof the sharp drop in the price of oil, and the deficitnearly doubled as a share of GDP. In Libya, therise in the deficit owing to lower oil prices andreduced oil production was compounded by thedifficult security situation and political divisions.By contrast, Mauritania’s Government achieveda reduction in the deficit despite the drop in theprices of gold and iron ore, and some progresswas made in fiscal consolidation in Egypt,Morocco, and Tunisia.

• Algeria

Algeria’s fiscal position deteriorated in 2015. The nearly 12% rise in revenuesenvisioned in the 2015 Finance Law (passedin December 2014) had become clearlyunrealistic by mid-year. However, theComplementary Finance Law adopted in Julyencompassed only limited changes, and thebudget deficit widened from 8.3% of GDP in2014 to 16.0% in 2015, financed by drawingdown financial assets. The 2016 Finance Law includes a revaluation of the VAT rate on diesel, mobile internet access and electricityconsumption, and increases in the turnover

tax for mobile telephone operators and in thevehicle road tax.

• Egypt

Egypt’s fiscal deficit eased to 11.5% of GDPin 2015 compared to 12.2% in 2014. Despiteweak revenue performance, the Governmentfinanced increased expenditures on housing andtransport infrastructure, on health and educationsectors as mandated by the Constitution, and onsocial programs largely by reducing spending onelectricity and fuel subsidies. One reason thedeficit was larger than projected was the delay inthe law introducing the VAT, which has been

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

27

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

mining investments, including the new Guelb IImine. We forecast a slight rise in the GDP growthrate in 2016, to 3.5%. Prospects may be betterover the longer term, with substantial productionincreases envisioned in iron ore and gas.Moreover, diversification to fishing, agriculture,livestock, and transport activities holdconsiderable potential to reduce the country’sdependence on minerals, which account for four-fifths of all exports and one-third of Staterevenue.

• Morocco

Morocco’s economic growth, estimated at4.5% in 2015, was boosted by a sharp rise in cereals production, in part due toGovernment efforts to promote irrigation andmechanization of the sector. By contrast, thetourism sector was beset by the securityconcerns affecting other countries of the sub-region, leading to some decline in overnight staysby non-residents. In the secondary sector, theresumption of construction activities at the endof 2015 offset the poor performance of the mining and refining sectors. Householdconsumption continued to drive growth in 2015,boosted by increased rural incomes following agood crop year, low inflation (1.8%), easy accessto credit (which rose by 5.1%), reducedunemployment (8.7% in July 2015) as well asincreased remittances from Moroccans livingabroad. Nevertheless, consumption growthfuelled imports of finished products, thusexpanding the trade deficit and underscoring theurgent need to develop an export sector withhigher value-added.

Public investment in Morocco increased by1.8% in 2015. Large-scale infrastructure projectsare underway in ports, railways, and roads tointegrate the country into the world economy,boost its territorial integration and reduceinequalities. Foreign direct investment in Moroccoincreased by 6.8% at end-November 2015 (yoy)totalling over 3.2 billion euros. Political stability,

numerous infrastructure development investmentprojects, proximity to Europe and rapid growthin domestic demand have all encouraged FDIflows.

Morocco’s GDP is projected to increase by1.8% in 2016, following the expected declinein agricultural sector activities due to poorrainfall. Despite the need to control the deficit,public investment would be maintained at levelssimilar to those of 2015. The education sectoris to receive almost one-third of the new positionsin the public service.

• Tunisia

GDP growth in Tunisia fell from 2.3% in 2014to 0.5% in 2015, driven by deterioration of the security situation and persistenteconomic and social difficulties (especiallydisruptions in the mining sector). Industrialproduction, particularly in the energy sector andmining, is declining, while trends in the servicessector were mixed. The agriculture sectorbenefitted from growing cereal production anda bumper harvest of olives and dates. Growthin 2015 was mainly driven by consumption,which benefitted from public and private sectorwage increases and accessible consumptioncredit. Economic prospects appear modest,with growth forecasted at 2.0% in 2016 and2.4% in 2017. Tunisia’s economic outlookremains highly dependent on the Government'sability to improve the security and socialsituations. Investment is forecast to rise to18.5% of GDP in 2016, still well below the 21.9%in 2014, despite the rallying of foreign directinvestment.

The budget deficit eased from 4.4% of GDPin 2014 to 4.2% in 2015. Expenditures onsubsidies fell with the decline in oil prices, butthe wage bill rose and tax revenues fell. Thesignificant increase in public spending since theRevolution has mainly been oriented towardscurrent expenditure; the wage bill has almost

26

Table 2.2: Fiscal balances in North Africa, percent

2014 2015 (e) 2016 (p) 2017 (p)

North Africa -11.1 -13.3 -12.1 -11.3

Algeria -8.3 -16.0 -15.4 -14.7

Egypt -12.2 -11.5 -9.6 -8.7

Libya -43.5 -58.9 -60.7 -56.8

Mauritania -3.7 -2.9 -2.4 -2.2

Morocco -4.9 -4.3 -3.5 -3.0

Tunisia -4.4 -4.2 -3.9 -3.7

Source: Data from domestic authorities; estimates (e) and projections (p) based on authors’ calculations)

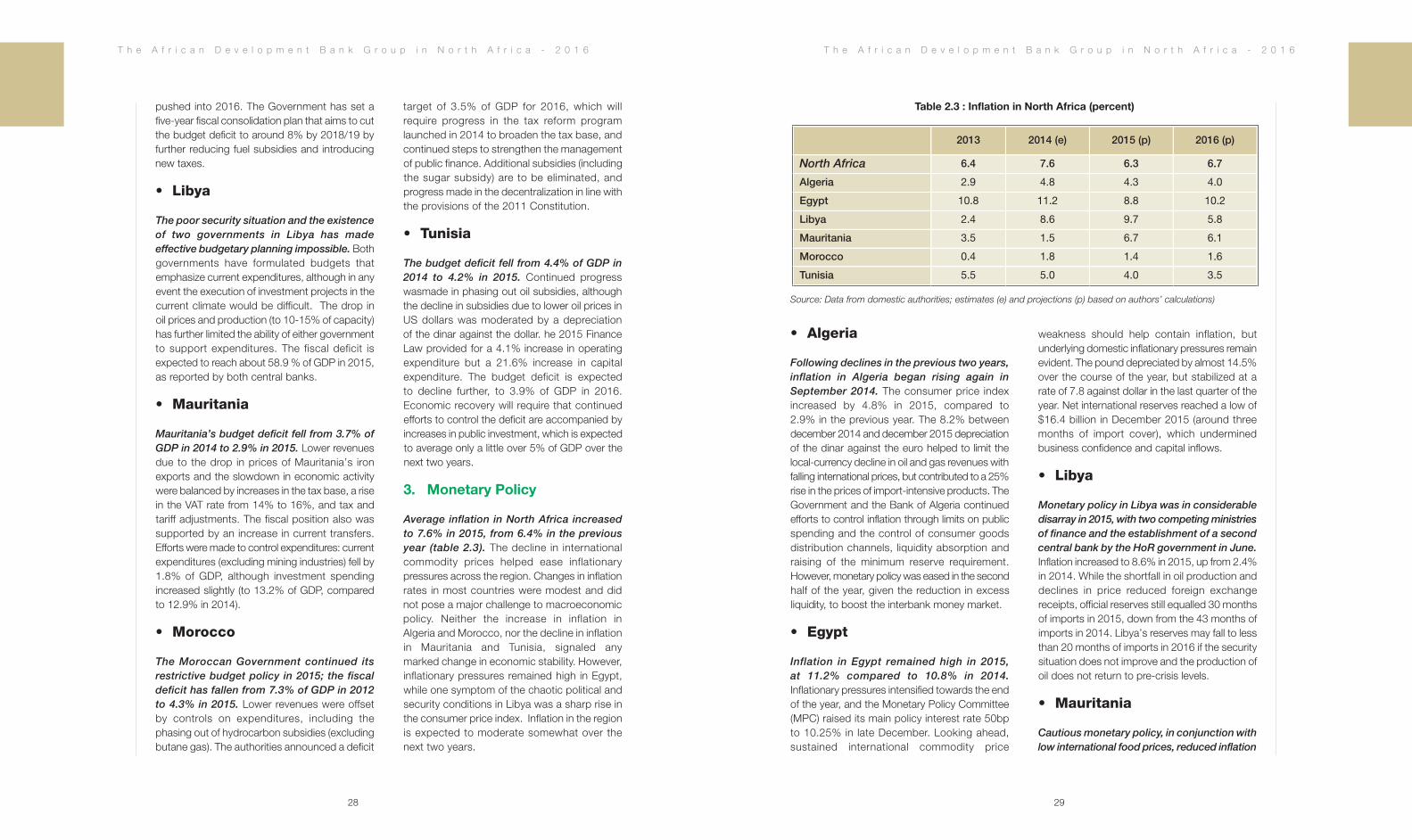

• Algeria

Following declines in the previous two years,inflation in Algeria began rising again inSeptember 2014. The consumer price indexincreased by 4.8% in 2015, compared to 2.9% in the previous year. The 8.2% between december 2014 and december 2015 depreciation of the dinar against the euro helped to limit thelocal-currency decline in oil and gas revenues withfalling international prices, but contributed to a 25% rise in the prices of import-intensive products. TheGovernment and the Bank of Algeria continuedefforts to control inflation through limits on publicspending and the control of consumer goodsdistribution channels, liquidity absorption andraising of the minimum reserve requirement.However, monetary policy was eased in the secondhalf of the year, given the reduction in excessliquidity, to boost the interbank money market.

• Egypt

Inflation in Egypt remained high in 2015,at 11.2% compared to 10.8% in 2014.Inflationary pressures intensified towards the endof the year, and the Monetary Policy Committee(MPC) raised its main policy interest rate 50bpto 10.25% in late December. Looking ahead,sustained international commodity price

weakness should help contain inflation, butunderlying domestic inflationary pressures remainevident. The pound depreciated by almost 14.5%over the course of the year, but stabilized at a rate of 7.8 against dollar in the last quarter of theyear. Net international reserves reached a low of$16.4 billion in December 2015 (around threemonths of import cover), which underminedbusiness confidence and capital inflows.

• Libya

Monetary policy in Libya was in considerabledisarray in 2015, with two competing ministriesof finance and the establishment of a secondcentral bank by the HoR government in June.Inflation increased to 8.6% in 2015, up from 2.4%in 2014. While the shortfall in oil production anddeclines in price reduced foreign exchangereceipts, official reserves still equalled 30 monthsof imports in 2015, down from the 43 months ofimports in 2014. Libya’s reserves may fall to lessthan 20 months of imports in 2016 if the securitysituation does not improve and the production ofoil does not return to pre-crisis levels.

• Mauritania

Cautious monetary policy, in conjunction withlow international food prices, reduced inflation

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

29

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

pushed into 2016. The Government has set afive-year fiscal consolidation plan that aims to cutthe budget deficit to around 8% by 2018/19 byfurther reducing fuel subsidies and introducingnew taxes.

• Libya

The poor security situation and the existenceof two governments in Libya has madeeffective budgetary planning impossible. Bothgovernments have formulated budgets thatemphasize current expenditures, although in anyevent the execution of investment projects in thecurrent climate would be difficult. The drop inoil prices and production (to 10-15% of capacity)has further limited the ability of either governmentto support expenditures. The fiscal deficit isexpected to reach about 58.9 % of GDP in 2015,as reported by both central banks.

• Mauritania

Mauritania’s budget deficit fell from 3.7% ofGDP in 2014 to 2.9% in 2015. Lower revenuesdue to the drop in prices of Mauritania’s ironexports and the slowdown in economic activitywere balanced by increases in the tax base, a risein the VAT rate from 14% to 16%, and tax andtariff adjustments. The fiscal position also wassupported by an increase in current transfers.Efforts were made to control expenditures: currentexpenditures (excluding mining industries) fell by1.8% of GDP, although investment spendingincreased slightly (to 13.2% of GDP, comparedto 12.9% in 2014).

• Morocco

The Moroccan Government continued itsrestrictive budget policy in 2015; the fiscaldeficit has fallen from 7.3% of GDP in 2012to 4.3% in 2015. Lower revenues were offsetby controls on expenditures, including thephasing out of hydrocarbon subsidies (excludingbutane gas). The authorities announced a deficit

target of 3.5% of GDP for 2016, which willrequire progress in the tax reform programlaunched in 2014 to broaden the tax base, andcontinued steps to strengthen the managementof public finance. Additional subsidies (includingthe sugar subsidy) are to be eliminated, andprogress made in the decentralization in line withthe provisions of the 2011 Constitution.

• Tunisia

The budget deficit fell from 4.4% of GDP in2014 to 4.2% in 2015. Continued progresswasmade in phasing out oil subsidies, althoughthe decline in subsidies due to lower oil prices inUS dollars was moderated by a depreciation of the dinar against the dollar. he 2015 Finance Law provided for a 4.1% increase in operatingexpenditure but a 21.6% increase in capitalexpenditure. The budget deficit is expected to decline further, to 3.9% of GDP in 2016.Economic recovery will require that continuedefforts to control the deficit are accompanied byincreases in public investment, which is expectedto average only a little over 5% of GDP over thenext two years.

3. Monetary Policy

Average inflation in North Africa increasedto 7.6% in 2015, from 6.4% in the previousyear (table 2.3). The decline in internationalcommodity prices helped ease inflationarypressures across the region. Changes in inflationrates in most countries were modest and didnot pose a major challenge to macroeconomicpolicy. Neither the increase in inflation in Algeria and Morocco, nor the decline in inflationin Mauritania and Tunisia, signaled any marked change in economic stability. However,inflationary pressures remained high in Egypt,while one symptom of the chaotic political andsecurity conditions in Libya was a sharp rise inthe consumer price index. Inflation in the regionis expected to moderate somewhat over thenext two years.

28

Table 2.3 : Inflation in North Africa (percent)

2013 2014 (e) 2015 (p) 2016 (p)

North Africa 6.4 7.6 6.3 6.7

Algeria 2.9 4.8 4.3 4.0

Egypt 10.8 11.2 8.8 10.2

Libya 2.4 8.6 9.7 5.8

Mauritania 3.5 1.5 6.7 6.1

Morocco 0.4 1.8 1.4 1.6

Tunisia 5.5 5.0 4.0 3.5

Source: Data from domestic authorities; estimates (e) and projections (p) based on authors’ calculations)

• Algeria

Algeria’s current account deficit rose from4.4% of GDP in 2014 to 15.6% in 2015. The60% decline in oil exports with the fall in the oilprice drove a deterioration in the trade balanceto 9.3% of GDP, the first significant trade deficitin 16 years. The authorities imposed more rigorousimport controls through quotas, application ofnew standard and quality requirements. Algeriais strengthening its bilateral relations with regionalcountries, including signature of a preferentialtrade agreement with Tunisia in 2014.

• Egypt

Egypt’s merchandise exports dropped by $4billion in 2015, owing to the global fall in oilprices, compounded by some decline in the export of oil products and in non-oilcommodities. The fall in exports was onlypartially compensated by a $2.3 billion increasein tourism revenues. Furthermore, a large fall inofficial remittances, along with depreciation ofthe pound, widened the current account deficitfrom 0.9% of GDP in 2014 to 3.7% in 2015.However, the surplus in the balance of paymentsrose by more than $2 billion, due to higher FDIinflows and deposits by GCC countries at theCBE. Government policy was challenged during2015 by a continued shortfall in foreign exchange

inflows. As a result, distortions arose in the foreignexchange market, which the Government triedto manage via the exchange rate peg, US dollardeposit caps, and foreign exchange bureaucontrols, although these have eased with the14.5% depreciation of the pound since early2016.

• Libya

The intense fighting between rival militias andthe political divisions in Libya, coupled withthe fall in oil prices, significantly reduced thecountry’s export revenues over 2014-2015.Libya’s trade balance shifted from a surplus30.5% of GDP in 2013 to a deficit of 35.8% in2015, which largely accounts for the deteriorationin the current account of 64.6 percentage pointsof GDP over the two years. Return to a moresustainable external position is likely to be slow.

• Mauritania

Mauritania’s trade deficit equalled about 15%of GDP in 2015, up from 14.5% in 2014. Thedecline in the prices of iron ore and gold wasbalanced by a similar fall in imports with the declinein international commodity prices. However, the current account deficit fell to 22.2% of GDP, compared to 30% in 2014, as currenttransfers rose. Mauritania has numerous areas

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

31

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

30

in Mauritania to 1.5% in 2015, from 3.5% inthe previous year. The key interest rate of theBCM and the reserve requirement rate weremaintained at 9% and 7% respectively. Nationalauthorities intend to adopt a formal frameworkfor predicting liquidity to enhance liquiditymanagement mechanisms and hopefully reduceforeign exchange interventions. Recapitalizationof the BCM should be undertaken to support theexecution of monetary policy.

• Morocco

Inflation increased in Morocco in 2015, drivenby the 2.8% rise in food product prices and3.9% increase in the cost of housing, water,electricity and other fuels.Nevertheless, inflationremained at only 1.8%, consistent with thecautious monetary policy initiated in 2011. BankAl-Maghrib maintained an accommodatingmonetary policy, keeping its lending rateunchanged in 2015 (after reducing this rate to itslowest-ever level of 2.5% in 2014) and loweringthe reserve ratio from 4% to 2% while adjustingthe volume of its cash injections to the cash flow needs of banks. By October 2015, netinternational reserves had increased year-on-yearby 23.8%, to exceed 6 months of imports ofgoods and services, owing to the decline in theprice of oil imports. First steps were taken in April2015 towards introducing greater flexibility inexchange rate determination by modifying the

dirham quotation basket to better reflect theexternal trade structure.

• Tunisia

Since 2011, the Central Bank of Tunisia (BCT)has adopted an accommodative monetarypolicy. The key money market rate (MMR) wasreduced from 4.75% to 4.3% in November 2015to support a resumption of economic activity.International reserves remained stable in 2015,equivalent to 113 days of imports at end-September. In the first nine months of 2015, thedinar depreciated against the dollar by 5.3%,although it appreciated against the euro by 2.8%.

4. Economic Co-operation and

the External Sector

Current account deficits remained high orincreased in all North African countries in 2015,except Morocco (table 2.4). The decline ininternational commodity prices contributed tohigher deficits in Algeria, Egypt and Libya,although Mauritania and Tunisia managed somedecline in the deficit despite a fall in exportprices. North African countries have continuedto make progress in trade integration over thepast few years, through agreements withregional partners, with countries in Sub-SaharanAfrica, and with Europe.

Table 2.4: Current account balances in North Africa (% of GDP)

2014 2015 (e) 2016 (p) 2017 (p)

North Africa -5.1 -9.3 -7.5 -6.6

Algeria -4.4 -15.6 -17.1 -15.2

Egypt -0.9 -3.7 -1.1 -1.4

Libya -30.1 -51.0 -44.5 -33.3

Mauritania -30.0 -22.2 -20.3 -19.3

Morocco -5.7 -2.7 -0.7 -0.9

Tunisia -9.0 -7.6 -5.9 -5.8

Source: Data from domestic authorities; estimates (e) and projections (p) based on authors’ calculations)

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

33

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

of cooperation with neighbouring countries,including: (i) heavy-goods vehicles from Morocco;(ii) sale of electricity to Senegal; (iii) combatingillegal migration, drug trafficking and terrorism; (iv)establishment of the banking network; and (v) theRosso bridge construction project on the SenegalRiver. In 2015, Mauritania and the European Unionsigned a new memorandum of understanding in the area of fishing for a period of 4 years.Mauritania is a member of the Arab MaghrebUnion (AMU), although its activities remain limited.Mauritania also engages in significant trade withthe countries in the Economic Community of WestAfrican States (ECOWAS), although it ceased tobe a member in 2000.

• Morocco

The development of “new trades of Morocco” which include the automobile andaeronautics sectors, continued in 2015 withthe announcement of an agreement between the authorities and PSA Peugeot-Citroën to opena manufacturing plant for the African and MiddleEast markets. Morocco has signed multiple freetrade agreements, especially with the EU, theUnited States, Turkey and several Arab and Africancountries. The country’s Trade Facilitation Indexranking improved from 75th in 2010 to 44th in 2014.Morocco’s open trade strategy contributed to the substantial rise in exports in 2015, particularly in the automobile and phosphate sectors. Thevalue of imports fell by 6% due to lower oil prices,and the current account deficit declined by 3 percentage points of GDP.

• Tunisia

Tunisia’s trade deficit fell from 14% of GDP in2014 to 7.8% in 2015, despite lower prices on

energy and minerals exports (although oliveoil exports rose). However, imports fell due toslower economic activity and investment (exceptin the food industry), and the drop in internationaloil prices, which reduced oil imports by 27.9%.Overall, Tunisia’s terms of trade improved by 4.9%in 2015. Tunisia has made considerable progressin trade negotiations over the past few yearsthrough its privileged partnership agreement with the European Union and bilateral tradeagreements with Morocco, Mauritania, Libya and Algeria. Special attention is also being given to economic relations with sub-Saharan African countries. According to Doing Business 2016, Tunisia has improved its ranking under the"trading across borders" to 91st, from 107th in theprevious year. Tunisia is likely to achieve furtherimprovements in trade through implementationof the customs reform recently approved by theCouncil of Ministers.

5. Debt Policy

The level of public debt compared to GDPvaried across North Africa, although thecontribution of debt to the sustainability ofeconomic policy is problematic. For example,Libya has a low level of debt, but the availabilityof resources to fund current expenditures remainsuncertain. Algeria, which is stable and has aminimal level of debt, will face challenges in fundingpublic investment going forward if oil prices do notrecover. Morocco and Tunisia both have moderatelevels of debt, but Morocco’slarge share ofdomestic debt will provide some insulation fromexternal shocks, while Tunisia has a large shareof external debt. A large portion of Mauritania’spublic debt is on concessional terms, but thecountry faces a substantial challenge to thesustainability of the debt.

• Algeria

Algeria’s public debt equalled only 10.7% ofGDP, despite some increase in 2015. Whilethe repayment of public debt has reduced itslevel to less than one-tenth that of 2004, thedecline in oil prices is forcing the Governmentto re-examine its debt management policies.While public investment has been funded almostexclusively with local financial resources since2009, the 2016 finance bill reintroduced thepossibility of relying on external financing formajor projects going forward. Moreover, theGovernment intends to tap domestic financialmarkets rather than relyon budgetary resourcesto fund some public investments. This policycould significantly increase the domestic publicdebt, although much of the debt owed by State-owned corporations (nearly a third of domesticdebt) should eventually disappear with theadoption of rules governing the bankruptcy ofnon-solvent State-owned companies. Thus,despite the still low level of debt, there is causeto wonder about the Algerian economy'scapacity to fund public investments through debtfinancing.

• Egypt

Egypt’s external debt was only 12.5% of GDP in March 2015. While borrowing from the GCCsubsequently increased external debt, thisborrowing has been on a concessional basis, sothat external debt service indicators remain low.The public sector’s domestic debt increased to90% of GDP in June 2015, largely reflectingongoing, large fiscal deficits that requirefinancing. The Government has resumed its debtconsolidation efforts and targets a debt-to-GDPratio of 80/85% for FY18/19, down from 95.5%in FY 2013/2014.

• Libya

Libya’s public debt equalled only 19.6% of GDP in 2004, and foreign reserves were about 12 times the size of external debt. Nevertheless, the substantial declines ingovernment revenues in 2014 and 2015 haveforced the governments to borrow in order to finance expenditures. In order to avoid further social breakdown, the two governments have maintained their salary and subsidyexpenditures, despite the decline in revenues. Ifoil revenues do not recover quickly, these policiescould result in an unsustainable rise in borrowing.

• Mauritania

Mauritania’s external public debt equalled77.4% of GDP in 2014, largely owed toexternal creditors. The IMF’s 2014 debtsustainability analysis downgraded the country’sdebt distress risk status from ‘moderate’ to‘high’ because of a deterioration of itsinstitutional capacity and the higher volume ofnew scheduled debt disbursements. Theauthorities are undertaking efforts to improvethe institutional environment and stabilize debtlevels, including the definitive settlement of thepassive debt owed to Kuwait, in order to quicklyregain a moderate debt distress risk rating.

Figure 2.1: Public debt levels in NorthAfrica (% of GDP)

Note: Data for Algeria, Morocco, and Tunisia are end-2015, while Egypt, Libya, and Mauritania are end-2014Source: Statistics Department, African DevelopmentBank

(% of GDP)

Algeria Egypt Libya Mauritania Morocco Tunisia 0

20

40

60

80

100

120

32

• Morocco

The latest reports of the Moroccan CentralBank (Bank Al-Maghrib) and the IMFconcluded that Morocco’s public debt willremain sustainable in the medium term. Asabout three-quarters of the debt stock is domestic(47.9% of GDP versus 15.7% for external debt),the impact of exchange rate fluctuations is small.Also, 78.8% of the external debt is denominatedin euros, so that increases in the debt due tocurrency depreciation would be matched withimproved incentives for the exports required toservice the debt. Fiscal consolidation and activedebt management efforts made have reduced theaverage interest rate from 5.1% in 2010 to 4.4%in 2014, while the average maturity rose from 5.7

years to 6.5 years. Standard & Poor’s maintainedits outlook on Morocco at "stable" in April 2015,and also confirmed its long- and short-term foreignand local currency sovereign credit ratings at"BBB-/A-3".

• Tunisia

Tunisia’s debt stock amounted to 52.7% ofGDP in 2015, compared to 49.4% in 2014.Tunisia's public debt is considered sustainablebecause of its long maturities (10 years onaverage) and low interest rates - although it hasbeen on the increase over the past few years.However, since 61.1% of public debt is external,it remains highly exposed to exchange ratefluctuations.

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

35

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

34

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

36

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

37

Chapter 3Challenges Facing Public SectorManagement and Private SectorDevelopment

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

39

T h e A f r i c a n D e v e l o p m e n t B a n k G r o u p i n N o r t h A f r i c a - 2 0 1 6

38

administrative services. And efforts are underwayto encourage the use of arbitration and conventionalmediation to settle disputes. Immediate plans toimprove the investment climate include speeding thereimbursement of accrued VAT credit to enterprises,the drafting of a new investment law, and developingan action plan to improve control of corruption.

• Tunisia

Tunisia's economic model suffers from manystructural handicaps, which include labourregulations and administrative bottlenecks thatsignificantly constrain investment. According to aWorld Bank survey published in February 2014,business managers devote, on average, 25% oftheir time and 13% of their annual turnover tocomplying with regulations. Tunisia scores poorlyon the World Bank’s Doing Business rankings,particularly in starting a business and investorprotection. Efforts to improve the climate forinvestment include a new law to strengthencompetition and price control mechanisms, and the planned investment code to establish a more level playing field for investors, facilitateemployment of foreign experts, ease constraintson developing agricultural land, and establishinstitutions to oversee government activitiesaffecting investment.

2. Financial Sector

The financial sectors in most North Africaneconomies remain small, dominated by thepublic sector and dependent on public cashinfusions. Most North African economies rankpoorly on international comparisons on access tocredit and financial sector development. Givenlimited development and the availability of publicresources, most banking systems do not confrontserious, immediate threats to their solvency,although Tunisia is struggling to ensure that itsstate-owned banks are adequately capitalized.The major exceptions to this picture are Morocco,which boasts a strong, well-diversified financialsystem with widespread access to banking

The region achieved some improvement in the business climate in 2015, marked

by increased political stability in Egypt andprogress in reform programs in Mauritania,Morocco, and Tunisia. North African financialsystems mostly remain small and dominated byinefficient public sector banks, with the importantexception of Morocco’s strong, diversifiedprivate banking system. By contrast, NorthAfrican countries made significant improvementsin the efficiency and transparency of public sectoradministration, although the region’s rankings on international comparisons of public sectoradministration remain mediocre, at best. In Libya,however, violence and the division between two governments have devastated the privatesector and rendered public sector managementineffective.

1. Private sector development

The business climate in North African countrieshas continued its slow improvement since theevents of the Arab Spring, although substantialdifficulties remain, to a varying extent, acrossthe region. Morocco, Tunisia (marginally) andMauritania (significantly) advanced in globalrankings of the quality of the business environment,although Algeria’s position declined slightly. Libyaremains the lowest-ranked country in the world.New laws have been passed, or are nearingapproval, that would improve competition and ease constraints on investment in Tunisia, improve the policy and institutional framework facing private firms in Algeria, and simplify the businessenvironment and establish a new economic zonein Egypt. Morocco is continuing a reform of theregulatory system, and Mauritania is streamliningpublic services and promoting mediation andarbitration to settle business disputes.

• Algeria

The Algerian private sector remainsunderdeveloped, with the exception of a fewfamily-owned corporate groups with extensive

ties to the public sector. The World Bank’s 2016Doing Business Report ranks Algeria 163rd out of 189 countries. Regulation of labour and landmarkets remains constraining, and the measuresrecently taken are too partial to improve thebusiness environment. The size of the informalsector, which accounts for almost half of Algeria’stransactions, is also considered a major obstacleto commercial and industrial activities. Legislationrecently approved by the Council of Ministerswould address the regulatory framework for FDI,the incentives system for private firms, and theinstitutional framework facing business. In light ofthese activities, the private sector has alreadybeen encouraged to invest in major projects,particularly in the housing and transport sectors.

• Egypt

The Government of Egypt promulgated a newinvestment law in 2015 designed to facilitatemarket entry and exit procedures, andexpedite litigation and dispute resolution.Legislation has been passed to regulate the newEconomic Zone that has been created as part ofthe Suez Canal Area development project. As areflection of improved business sentiment, 2015witnessed a surge in mergers & acquisitions, with29 deals executed and 11 others in the pipelinefor the first quarter of 2016. The total value of theannounced deals is in excess of 20 billion pounds.

However, the business environment remainsweak with numerous challenges, reflected in the World Bank’s 2016 Doing Business rankfalling to 131 from 126 the year before.

• Libya

According to the Mo Ibrahim Index 2015, Libyais one of Africa’s poorest-performing countriesin terms of business environment, scoring 16.4out of 100 in 2014 compared to 40.3 in 2013,below the African average of 40.7. The 2016Doing Business report ranks the Libyan businessenvironment as the worst in the world. The

economy is dominated by the oil sector, and morethan 85 percent of the workforce is employed inthe public sector. More than 70 percent of publicexpenditure in the 2015 budget was allocated towages and subsidies, leaving few resources fordeveloping the infrastructure required to supportprivate sector growth. In addition, the politicaldivision has created significant uncertaintyconcerning the potential for reform.

• Mauritania

Mauritania is among the ten countries in DoingBusiness 2016 that made the most progress inimproving their business environment, thanksto programs to streamline payment procedures at the National Health Insurance Fund (CNAM) andthe National Social Insurance Fund (CNSS), theinstitution of a one-stop service and a single form for starting a business, the creation of anInternational Centre for Mediation and Arbitration,and a revision of the trade code. The countryintends to continue its improvement efforts in theareas in which it records poor performance inDoing Business rankings, especially in resolvinginsolvency (189th in 2016), paying taxes (187th),getting electricity (152nd), and protecting minorityinvestors (134th).

• Morocco

Morocco’s Government has embarked on a far-reaching program to improve the regulationsgoverning business. Last year, Moroccanauthorities established the National BusinessEnvironment Committee (CNEA), which bringstogether representatives from the public andprivate sectors to discuss regulatory reform. Thesimplification of 70 business measures, the reformof property registration and regulations governingbuilding permits, and the opening of an online tax payment system for an additional number of companies are being either finalized orimplemented. A common business identifierdatabase has been established to facilitatebusiness information sharing between the various

number of banks has risen from 10 in 2009 to 20,which has significantly narrowed intermediationmargins; the weighted average lending rate ofbanks fell from 15.1 percent in 2012 to 11.4percent in 2014. Some banks do not comply with the minimum capital requirement and areinadequately provisioned.

• Morocco

The Moroccan banking sector is one of the most developed on the continent. Some 64 percent of the population had access tobanking services at end-2014, nearing the Bank Al-Maghrib target of two-thirds of the population.Unlike other North African economies, Moroccoalso has a thriving stock market, with marketcapitalization equal to over 50 percent of GDP. In 2014 and 2015, the Moroccan governmentcontinued its policy of increasing the depth offinancial markets by establishing new mechanisms,such as a futures market for financial instruments,and new products, such as real estate investmentschemes. The Banking Law of 2015 strengthensthe supervisory powers of the Central Bank, seeksto modernize macro-prudential supervision, andintroduces a legal framework for the developmentof participatory banks. The directive on equityfunds went into effect from January 2014, andequity levels remain well above the Basel IIIrequirement. One challenge is ensuring that small- and medium-sized enterprises haveadequate access to credit. After the guaranteedloans launched in 2012, the Central Bankimplemented a new programme for SMEs, whichwas strongly supported by the banks.

• Tunisia