Adaptive Filtering - Theory and Applicationssc.enseeiht.fr/doc/Seminar_Bermudez.pdf · Adaptive...

107

Adaptive Filtering - Theory and Applications Jos´ e C. M. Bermudez Department of Electrical Engineering Federal University of Santa Catarina Florian´ opolis – SC Brazil IRIT - INP-ENSEEIHT, Toulouse May 2011 Jos´ e Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 1 / 107

Transcript of Adaptive Filtering - Theory and Applicationssc.enseeiht.fr/doc/Seminar_Bermudez.pdf · Adaptive...

Adaptive Filtering - Theory and Applications

Jose C. M. Bermudez

Department of Electrical EngineeringFederal University of Santa Catarina

Florianopolis – SCBrazil

IRIT - INP-ENSEEIHT, ToulouseMay 2011

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 1 / 107

1 Introduction

2 Adaptive Filtering Applications

3 Adaptive Filtering Principles

4 Iterative Solutions for the Optimum Filtering Problem

5 Stochastic Gradient Algorithms

6 Deterministic Algorithms

7 Analysis

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 2 / 107

Introduction

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 3 / 107

Estimation Techniques

Several techniques to solve estimation problems.

Classical Estimation

Maximum Likelihood (ML), Least Squares (LS), Moments, etc.

Bayesian Estimation

Minimum MSE (MMSE), Maximum A Posteriori (MAP), etc.

Linear Estimation

Frequently used in practice when there is a limitation in computational

complexity – Real-time operation

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 4 / 107

Linear Estimators

Simpler to determine: depend on the first two moments of data

Statistical Approach – Optimal Linear Filters◮ Minimum Mean Square Error◮ Require second order statistics of signals

Deterministic Approach – Least Squares Estimators◮ Minimum Least Squares Error◮ Require handling of a data observation matrix

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 5 / 107

Limitations of Optimal Filters and LS Estimators

Statistics of signals may not be available or cannot be accuratelyestimated

There may not be available time for statistical estimation (real-time)

Signals and systems may be non-stationary

Memory required may be prohibitive

Computational load may be prohibitive

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 6 / 107

Iterative Solutions

Search the optimal solution starting from an initial guess

Iterative algorithms are based on classical optimization algorithms

Require reduced computational effort per iteration

Need several iterations to converge to the optimal solution

These methods form the basis for the development of adaptivealgorithms

Still require the knowledge of signal statistics

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 7 / 107

Adaptive Filters

Usually approximate iterative algorithms and:

Do not require previous knowledge of the signal statistics

Have a small computational complexity per iteration

Converge to a neighborhood of the optimal solution

Adaptive filters are good for:

Real-time applications, when there is no time for statistical estimation

Applications with nonstationary signals and/or systems

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 8 / 107

Properties of Adaptive Filters

They can operate satisfactorily in unknown and possibly time-varyingenvironments without user intervention

They improve their performance during operation by learningstatistical characteristics from current signal observations

They can track variations in the signal operating environment (SOE)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 9 / 107

Adaptive Filtering Applications

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 10 / 107

Basic Classes of Adaptive Filtering Applications

System Identification

Inverse System Modeling

Signal Prediction

Interference Cancelation

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 11 / 107

System Identification

+ +

_

+x(n) d(n)

d(n)

y(n) e(n)

eo(n)

other signals

unknownsystem

adaptive

adaptive

algorithm

filter

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 12 / 107

Applications – System Identification

Channel Estimation

Communications systems

Objective: model the channel to design distortion compensation

x(n): training sequence

Plant Identification

Control systems

Objective: model the plant to design a compensator

x(n): training sequence

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 13 / 107

Echo Cancellation

Telephone systems and VoIP

Echo caused by network impedance mismatches or acousticenvironment

Objective: model the echo path impulse response

x(n): transmitted signal

d(n): echo + noise

H H

Tx

Rx

H H

Tx

Rx

EC

+

_

x(n)

d(n)e(n)

Figure: Network Echo Cancellation

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 14 / 107

Inverse System Modeling

Adaptive filter attempts to estimate unknown system’s inverse

Adaptive filter input usually corrupted by noise

Desired response d(n) may not be available

++ +

_UnknownSystem

Adaptive

AdaptiveFilter

Algorithm

Delay

othersignals

x(n)

s(n) e(n)

y(n)

d(n)z(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 15 / 107

Applications – Inverse System ModelingChannel Equalization

++ +

_Channel

Adaptive

AdaptiveFilter

Algorithm

Local gen.

x(n)

x(n)

s(n) e(n)

y(n)

d(n)z(n)

Objective: reduce intersymbol interference

Initially – training sequence in d(n)

After training: d(n) generated from previous decisions

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 16 / 107

Signal Prediction

+_

Delay

Adaptive

AdaptiveFilter

Algorithmothersignals

x(n − no)

x(n) e(n)

y(n)

d(n)

most widely used case – forward prediction

signal x(n) to be predicted from samples{x(n − no), x(n − no − 1), . . . , x(n − no − L)}

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 17 / 107

Application – Signal Prediction

DPCM Speech Quantizer - Linear Predictive Coding

Objective: Reduce speech transmission bandwidth

Signal transmitted all the time: quantization error

Predictor coefficients are transmitted at low rate

+

_+

+

Speech

signalsignal DPCM

Quantizer

Predictor

prediction errorQ[e(n)]

e(n)

y(n) + Q[e(n)] ∼ d(n)

d(n)

y(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 18 / 107

Interference Cancelation

One or more sensor signals are used to remove interference and noise

Reference signals correlated with the inteference should also beavailable

Applications:◮ array processing for radar and communications◮ biomedical sensing systems◮ active noise control systems

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 19 / 107

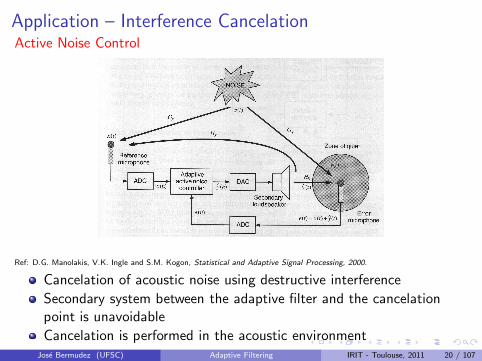

Application – Interference CancelationActive Noise Control

Ref: D.G. Manolakis, V.K. Ingle and S.M. Kogon, Statistical and Adaptive Signal Processing, 2000.

Cancelation of acoustic noise using destructive interference

Secondary system between the adaptive filter and the cancelationpoint is unavoidable

Cancelation is performed in the acoustic environmentJose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 20 / 107

Active Noise Control – Block Diagram

s++

−

AdaptiveAlgorithm

wo

w(n)

x(n)

xf (n)

S

S

y(n) ys(n) yg(n)

d(n)

z(n)

e(n)

g(ys)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 21 / 107

Adaptive Filtering Principles

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 22 / 107

Adaptive Filter Features

Adaptive filters are composed of three basic modules:

Filtering strucure◮ Determines the output of the filter given its input samples◮ Its weights are periodically adjusted by the adaptive algorithm◮ Can be linear or nonlinear, depending on the application◮ Linear filters can be FIR or IIR

Performance criterion◮ Defined according to application and mathematical tractability◮ Is used to derive the adaptive algorithm◮ Its value at each iteration affects the adaptive weight updates

Adaptive algorithm◮ Uses the performance criterion value and the current signals◮ Modifies the adaptive weights to improve performance◮ Its form and complexity are function of the structure and of the

performance criterion

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 23 / 107

Signal Operating Environment (SOE)

Comprises all informations regarding the properties of the signals andsystems

Input signals

Desired signal

Unknown systems

If the SOE is nonstationary

Aquisition or convergence mode: from start until close to bestperformance

Tracking mode: readjustment following SOE’s time variations

Adaptation can be

Supervised – desired signal is available ➪ e(n) can be evaluated

Unsupervised – desired signal is unavailable

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 24 / 107

Performance Evaluation

Convergence rate

Misadjustment

Tracking

Robustness (disturbances and numerical)

Computational requirements (operations and memory)

Structure◮ facility of implementation◮ performance surface◮ stability

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 25 / 107

Optimum versus Adaptive Filters in Linear Estimation

Conditions for this study

Stationary SOE

Filter structure is transversal FIR

All signals are real valued

Performance criterion: Mean-square error E[e2(n)]

The Linear Estimation Problem

+

−

Linear FIR Filter

w

x(n) y(n)

d(n)

e(n)

Jms = E[e2(n)]

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 26 / 107

The Linear Estimation Problem

+

−

Linear FIR Filter

w

x(n) y(n)

d(n)

e(n)

x(n) = [x(n), x(n − 1), · · · , x(n − N + 1)]T

y(n) = xT (n)w

e(n) = d(n) − y(n) = d(n) − xT (n)w

Jms = E[e2(n)] = σ2d − 2pT w + wT Rxxw

wherep = E[x(n)d(n)]; Rxx = E[x(n)xT (n)]

Normal Equations

Rxxwo = p ➪ wo = R−1xx p for Rxx > 0

Jmsmin= σ2

d − pT R−1xx p

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 27 / 107

What if d(n) is nonstationary?

+

−

Linear FIR Filter

wx(n) y(n)

d(n)

e(n)

x(n) = [x(n), x(n − 1), · · · , x(n − N + 1)]T

y(n) = xT (n)w(n)

e(n) = d(n) − y(n) = d(n) − xT (n)w(n)

Jms(n) = E[e2(n)] = σ2d(n) − 2p(n)T w(n) + wT (n)Rxxw(n)

wherep(n) = E[x(n)d(n)]; Rxx = E[x(n)xT (n)]

Normal Equations

Rxxwo(n) = p(n) ➪ wo(n) = R−1

xx p(n) for Rxx > 0

Jmsmin(n) = σ2

d(n) − pT (n)R−1xx p(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 28 / 107

Optimum Filters versus Adaptive Filters

Optimum Filters

Computep(n) = E[x(n)d(n)]

Solve Rxxwo = p(n)

Filter with wo(n) ➪

y(n) = xT (n)wo(n)

Nonstationary SOE:Optimum filter determinedfor each value of n

Adaptive Filters

Filtering: y(n) = xT (n)w(n)

Evaluate error: e(n) = d(n) − y(n)

Adaptive algorithm:

w(n + 1) = w(n) + ∆w[x(n), e(n)]

∆w(n) is chosen so that w(n) is close towo(n) for n large

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 29 / 107

Characteristics of Adaptive Filters

Search for the optimum solution on the performance surface

Follow principles of optimization techniques

Implement a recursive optimization solution

Convergence speed may depend on initialization

Have stability regions

Steady-state solution fluctuates about the optimum

Can track time varying SOEs better than optimum filters

Performance depends on the performance surface

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 30 / 107

Iterative Solutions for the

Optimum Filtering Problem

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 31 / 107

Performance (Cost) Functions

Mean-square error ➪ E[e2(n)] (Most popular)Adaptive algorithms: Least-Mean Square (LMS), Normalized LMS(NLMS), Affine Projection (AP), Recursive Least Squares (RLS), etc.

Regularized MSE

Jrms = E[e2(n)] + α‖w(n)‖2

Adaptive algorithm: leaky least-mean square (leaky LMS)

ℓ1 norm criterionJℓ1 = E[|e(n)|]

Adaptive algorithm: Sign-Error

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 32 / 107

Performance (Cost) Functions – continued

Least-mean fourth (LMF) criterion

JLMF = E[e4(n)]

Adaptive algorithm: Least-Mean Fourth (LMF)

Least-mean-mixed-norm (LMMN) criterion

JLMMN = E[αe2(n) +1

2(1 − α)e4(n)]

Adaptive algorithm: Least-Mean-Mixed-Norm (LMMN)

Constant-modulus criterion

JCM = E[(γ − |xT (n)w(n)|2

)2]

Adaptive algorithm: Constant-Modulus (CM)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 33 / 107

MSE Performance Surface – Small Input Correlation

−20 −10 0 10 20

−20

0

200

500

1000

1500

2000

2500

3000

3500

w1

w2

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 34 / 107

MSE Performance Surface – Large Input Correlation

−20 −15 −10 −5 0 5 10 15 20

−20

−10

0

10

200

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

w1

w2

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 35 / 107

The Steepest Descent Algorithm – Stationary SOE

Cost Function

Jms(n) = E[e2(n)] = σ2d − 2pT w(n) + wT (n)Rxxw(n)

Weight Update Equation

w(n + 1) = w(n) + µc(n)

µ: step-sizec(n): correction term (determines direction of ∆w(n))Steepest descent adjustment:

c(n) = −∇Jms(n) ➪ Jms(n + 1) ≤ Jms(n)

w(n + 1) = w(n) + µ[p − Rxxw(n)]

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 36 / 107

Weight Update Equation About the Optimum Weights

Weight Error Update Equation

w(n + 1) = w(n) + µ[p − Rxxw(n)]

Using p = Rxxwo

w(n + 1) = (I − µRxx)w(n) + µRxxwo

Weight error vector: v(n) = w(n) − wo

v(n + 1) = (I − µRxx)v(n)

Matrix I − µRxx must be stable for convergence (|λi| < 1)

Assuming convergence, limn→∞ v(n) = 0

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 37 / 107

Convergence Conditions

v(n + 1) = (I − µRxx)v(n); Rxx positive definite

Eigen-decomposition of Rxx

Rxx = QΛQT

v(n + 1) = (I − µQΛQT )v(n)

QT v(n + 1) = QT v(n) − µΛQT v(n)

Defining v(n + 1) = QT v(n + 1)

v(n + 1) = (I − µΛ)v(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 38 / 107

Convergence Properties

v(n + 1) = (I − µΛ)v(n)

vk(n + 1) = (1 − µλk)vk(n), k = 1, . . . , N

vk(n) = (1 − µλk)nvk(0)

Convergence modes

◮ monotonic if 0 < 1 − µλk < 1

◮ oscillatory if −1 < 1 − µλk < 0

Convergence if |1 − µλk| < 1 ➪ 0 < µ < 2λmax

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 39 / 107

Optimal Step-Size

vk(n) = (1 − µλk)nvk(0); convergence modes: 1 − µλk

max |1 − µλk|: slowest mode

min |1 − µλk|: fastest mode

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 40 / 107

Optimal Step-Size – continued

1

0

|1−

µλ

k|

1/λmax 1/λminµo µ

minµ

max{|1 − µλk|}

1 − µoλmin = −(1 − µoλmax)

µo = 2λmax+λmin

Optimal slowest modes: ±ρ−1ρ+1 ; ρ = λmax

λmin

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 41 / 107

The Learning Curve – Jms(n)

Jms(n) = Jmsmin+

Excess MSE︷ ︸︸ ︷

vT (n)Λv(n)= Jmsmin+

N∑

k=1

λkv2k(n)

Since vk(n) = (1 − µλk)nvk(0),

Jms(n) = Jmsmin+

N∑

k=1

λk(1 − µλk)2nv2

k(0)

λk(1 − µλk)2 > 0 ➪ monotonic convergence

Stability limit is again 0 < µ < 2λmax

Jms(n) converges faster than w(n)

Algorithm converges faster as ρ = λmax/λmin → 1

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 42 / 107

Simulation Results

x(n) = α x(n − 1) + v(n)

0 20 40 60 80 100 120 140 160 180 200−70

−60

−50

−40

−30

−20

−10

0

iteration

MS

E (

dB)

Steepest Descent − Mean Square Error

Input: White noise (ρ = 1)

0 20 40 60 80 100 120 140 160 180 200−70

−60

−50

−40

−30

−20

−10

0

iteration

MS

E (

dB)

Steepest Descent − Mean Square Error

Input: AR(1), α = 0.7 (ρ = 5.7)

Linear system identification - FIR with 20 coefficients

Step-size µ = 0.3

Noise power σ2v = 10−6

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 43 / 107

The Newton Algorithm

Steepest descent: linear approx. of Jms about the operating point

Newton’s method: Quadratic approximation of Jms

Expanding Jms(w) in Taylor’s series about w(n),

Jms(w) ∼Jms[w(n)] + ∇T Jms[w − w(n)]

+1

2[w − w(n)]T H(n)[w − w(n)]

Diferentiating w.r.t. w and equating to zero at w = w(n + 1),

∇Jms[w(n + 1)] = ∇Jms[w(n)] + H [w(n)][w(n + 1) − w(n)] = 0

w(n + 1) = w(n) − H−1[w(n)]∇Jms[w(n)]

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 44 / 107

The Newton Algorithm – continued

∇Jms[w(n)] = −2p + 2Rxxw(n)

H(w(n)) = 2Rxx

Thus, adding a step-size control,

w(n + 1) = w(n) − µR−1xx [−p + Rxxw(n)]

Quadratic surface ➪ conv. in one iteration for µ = 1 ,

Requires the determination of R−1xx /

Can be used to derive simpler adaptive algorithms

When H(n) is close to singular ➪ regularization

H(n) = 2Rxx + 2εI

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 45 / 107

Basic Adaptive Algorithms

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 46 / 107

Least Mean Squares (LMS) Algorithm

Can be interpreted in different ways

Each interpretation helps understanding the algorithm behavior

Some of these interpretations are related to the steepest descentalgorithm

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 47 / 107

LMS as a Stochastic Gradient Algorithm

Suppose we use the estimate Jms(n) = E[e2(n)] ≃ e2(n)

The estimated gradient vector becomes

∇Jms(n) =∂e2(n)

∂w(n)= 2e(n)

∂e(n)

∂w(n)

Since e(n) = d(n) − xT (n)w(n),

∇Jms(n) = −2e(n)x(n) (stochastic gradient)

and, using the steepest descent weight update equation,

w(n + 1) = w(n) + µe(n)x(n) (LMS weight update)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 48 / 107

LMS as a Stochastic Estimation Algorithm

∇Jms(n) = −2p + 2Rxxw(n)

Stochastic estimators

p = d(n)x(n) Rxx = x(n)xT (n)

Then,∇Jms(n) = −2d(n)x(n) + 2x(n)xT (n)w(n)

Using ∇Jms(n) is the steepest descent weight update,

w(n + 1) = w(n) + µe(n)x(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 49 / 107

LMS – A Solution to a Local Optimization

Error expressionse(n) = d(n) − xT (n)w(n) (a priori error)ǫ(n) = d(n) − xT (n)w(n + 1) (a posteriori error)

We want to maximize |ǫ(n) − e(n)| with |ǫ(n)| < |e(n)|

ǫ(n) − e(n) = −xT (n)∆w(n)

∆w(n) = w(n + 1) − w(n)

Expressing ∆w(n) as ∆w(n) = ˜∆w(n)e(n)

ǫ(n) − e(n) = −xT (n) ˜∆w(n)e(n)

For max |ǫ(n) − e(n)| ➪ ˜∆w(n) in the direction of x(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 50 / 107

➪ ˜∆w(n) = µx(n) and

∆w(n) = µx(n)e(n)

andw(n + 1) = w(n) + µe(n)x(n)

Asǫ(n) − e(n) = −xT (n)∆w(n) = −µxT (n)x(n)e(n)

|ǫ(n)| < |e(n)| requires |1 − µxT (n)x(n)| < 1, or

0 < µ < 2‖x(n)‖2 (stability region)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 51 / 107

Observations - LMS Algorithm

LMS is a noisy approximation of the steepest descent algorithm

The gradient estimate is unbiased

The errors in the gradient estimate lead to Jmsex(∞) 6= 0

Vector w(n) is now random

Steepest descent properties are no longer guaranteed➪ LMS analysis required

The instantaneous estimates allow tracking without redesign

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 52 / 107

Some Research Results

J. C. M. Bermudez and N. J. Bershad, “A nonlinear analytical model for thequantized LMS algorithm - the arbitrary step size case,” IEEE Transactions onSignal Processing, vol.44, No. 5, pp. 1175-1183, May 1996.

J. C. M. Bermudez and N. J. Bershad, “Transient and tracking performanceanalysis of the quantized LMS algorithm for time-varying system identification,”IEEE Transactions on Signal Processing, vol.44, No. 8, pp. 1990-1997, August1996.

N. J. Bershad and J. C. M. Bermudez, “A nonlinear analytical model for thequantized LMS algorithm - the power-of-two step size case,” IEEE Transactions onSignal Processing, vol.44, No. 11, pp. 2895- 2900, November 1996.

N. J. Bershad and J. C. M. Bermudez, “Sinusoidal interference rejection analysisof an LMS adaptive feedforward controller with a noisy periodic reference,” IEEETransactions on Signal Processing, vol.46, No. 5, pp. 1298-1313, May 1998.

J. C. M. Bermudez and N. J. Bershad, “Non-Wiener behavior of the Filtered-XLMS algorithm,” IEEE Trans. on Circuits and Systems II - Analog and DigitalSignal Processing, vol.46, No. 8, pp. 1110-1114, Aug 1999.

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 53 / 107

Some Research Results – continued

O. J. Tobias, J. C. M. Bermudez and N. J. Bershad, “Mean weight behavior of theFiltered-X LMS algorithm,” IEEE Transactions on Signal Processing, vol. 48, No.4, pp. 1061-1075, April 2000.

M. H. Costa, J. C. M. Bermudez and N. J. Bershad, “Stochastic analysis of theLMS algorithm with a saturation nonlinearity following the adaptive filter output,”IEEE Transactions on Signal Processing, vol. 49, No. 7, pp. 1370-1387, July 2001.

M. H. Costa, J. C, M. Bermudez and N. J. Bershad, “Stochastic analysis of theFiltered-X LMS algorithm in systems with nonlinear secondary paths,” IEEETransactions on Signal Processing, vol. 50, No. 6, pp. 1327-1342, June 2002.

M. H. Costa, J. C. M. Bermudez and N. J. Bershad, “The performance surface infiltered nonlinear mean square estimation,” IEEE Transactions on Circuits andSystems I, vol. 50, No. 3, p. 445-447, March 2003.

G. Barrault, J. C. M. Bermudez and A. Lenzi, “New Analytical Model for theFiltered-x Least Mean Squares Algorithm Verified Through Active Noise ControlExperiment,” Mechanical Systems and Signal Processing, v. 21, p. 1839-1852,2007.

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 54 / 107

Some Research Results – continued

N. J. Bershad, J. C. M. Bermudez and J. Y. Tourneret, “Stochastic Analysis of theLMS Algorithm for System Identification with Subspace Inputs,” IEEE Trans. onSignal Process., v. 56, p. 1018-1027, 2008.

J. C. M. Bermudez, N. J. Bershad and J. Y. Tourneret, “An Affine Combination ofTwo LMS Adaptive Filters Transient Mean-Square Analysis,” IEEE Trans. onSignal Process., v. 56, p. 1853-1864, 2008.

M. H. Costa, L. R. Ximenes and J. C. M. Bermudez, “Statistical Analysis of theLMS Adaptive Algorithm Subjected to a Symmetric Dead-Zone Nonlinearity at theAdaptive Filter Output,” Signal Processing, v. 88, p. 1485-1495, 2008.

M. H. Costa and J. C. M. Bermudez, “A Noise Resilient Variable Step-Size LMSAlgorithm,” Signal Processing, v. 88, no. 3, p. 733-748, March 2008.

P. Honeine, C. Richard, J. C. M. Bermudez, J. Chen and H. Snoussi, “ADecentralized Approach for Nonlinear Prediction of Time Series Data in SensorNetworks,” EURASIP Journal on Wireless Communications and Networking, v.2010, p. 1-13, 2010. (KNLMS)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 55 / 107

The Normalized LMS Algorithm – NLMS

Most Employed adaptive algorithm in real-time applications

Like LMS has different interpretations (even more)

Alleviates a drawback of the LMS algorithm

w(n + 1) = w(n) + µe(n)x(n)

◮ If amplitude of x(n) is large ➪ Gradient noise amplification◮ Sub-optimal performance when σ2

x varies with time (for instance,speech)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 56 / 107

NLMS – A Solution to a Local Optimization Problem

Error expressionse(n) = d(n) − xT (n)w(n) (a priori error)ǫ(n) = d(n) − xT (n)w(n + 1) (a posteriori error)

We want to maximize |ǫ(n) − e(n)| with |ǫ(n)| < |e(n)|

ǫ(n) − e(n) = −xT (n)∆w(n) (A)

∆w(n) = w(n + 1) − w(n)

For |ǫ(n)| < |e(n)| we impose the restriction

ǫ(n) = (1 − µ)e(n), |1 − µ| < 1

➪ ǫ(n) − e(n) = −µe(n) (B)

For max |ǫ(n) − e(n)| ➪ ∆w(n) in the direction of x(n)

➪∆w(n) = kx(n) (C)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 57 / 107

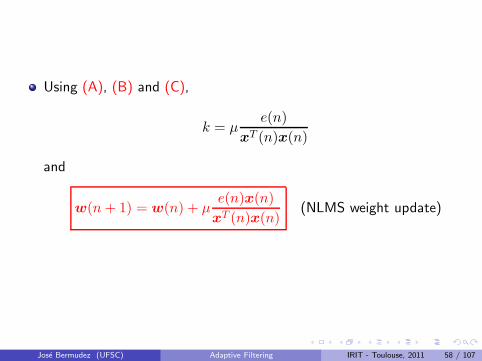

Using (A), (B) and (C),

k = µe(n)

xT (n)x(n)

and

w(n + 1) = w(n) + µe(n)x(n)

xT (n)x(n)(NLMS weight update)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 58 / 107

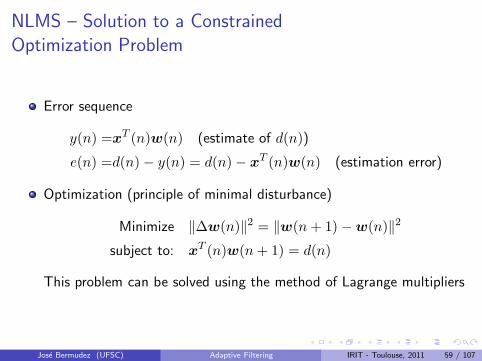

NLMS – Solution to a Constrained

Optimization Problem

Error sequence

y(n) =xT (n)w(n) (estimate of d(n))

e(n) =d(n) − y(n) = d(n) − xT (n)w(n) (estimation error)

Optimization (principle of minimal disturbance)

Minimize ‖∆w(n)‖2 = ‖w(n + 1) − w(n)‖2

subject to: xT (n)w(n + 1) = d(n)

This problem can be solved using the method of Lagrange multipliers

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 59 / 107

Using Lagrange multipliers, we minimize

f [w(n + 1)] = ‖w(n + 1) − w(n)‖2 + λ[d(n) − xT (n)w(n + 1)]

Differentiating w.r.t. w(n + 1) and equating the result to zero,

w(n + 1) = w(n) +1

2λx(n) (*)

Using this result in xT (n)w(n + 1) = d(n) yields

λ =2e(n)

xT (n)x(n)

Using this result in (*) yields

w(n + 1) = w(n) + µe(n)x(n)

xT (n)x(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 60 / 107

NLMS as an Orthogonalization Process

Conditions for the analysis◮ e(n) = d(n) − xT (n)w(n)◮ wo is the optimal solution (Wiener solution)◮ d(n) = xT (n)wo (no noise)◮ v(n) = w(n) − wo (weight error vector)

Error signal

e(n) = d(n) − xT (n)[v(n) + wo]

= xT (n)wo − xT (n)[v(n) + wo]

= −xT (n)v(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 61 / 107

e(n) = −xT (n)v(n)

Interpretation: To minimize the error v(n) should be orthogonal to allinput vectorsRestriction: We have only one vector x(n)

Iterative solution:

We can subtract from v(n) its component in the direction of x(n) ateach iteration

If there are N adaptive coefficients, v(n) could be reduced to zeroafter N orthogonal input vectors

Iterative projection extraction➪ Gram-Schmidt orthogonalization

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 62 / 107

Recursive orthogonalization

n = 0 : v(1) = v(0) − proj. of v(0) onto x(0)

n = 1 : v(2) = v(1) − proj. of v(1) onto x(1)

... :...

n + 1 : v(n + 1) = v(n) − proj. of v(n) onto x(n)

Projection of v(n) onto x(n)

Px(n)[v(n)] ={x(n)[xT (n)x(n)]−1xT (n)

}v(n)

Weight update equation

v(n + 1) = v(n) − µ

scalar︷ ︸︸ ︷

[xT (n)x(n)]−1

−e(n)︷ ︸︸ ︷

xT (n)v(n) x(n)

= v(n) + µe(n)x(n)

xT (n)x(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 63 / 107

NLMS has its owns problems!

NLMS solves the LMS gradient error amplification problem, but ...

What happens if ‖x(n)‖2 gets too small?

One needs to add some regularization

w(n + 1) = w(n) + µe(n)x(n)

xT (n)x(n)+ε(ε−NLMS)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 64 / 107

ε-NLMS – Stochastic Approximation of

Regularized Newton

Regularized Newton Algorithm

w(n + 1) = w(n) + µ[εI + Rxx]−1[p − Rxxw(n)]

Instantaneous estimates

p = x(n)d(n)

Rxx = x(n)xT (n)

Using these estimates

w(n + 1) = w(n) + µ[εI + x(n)xT (n)]−1x(n)

e(n)︷ ︸︸ ︷

[d(n) − xT (n)w(n)]

w(n + 1) = w(n) + µ[εI + x(n)xT (n)]−1x(n)e(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 65 / 107

w(n + 1) = w(n) + µ[εI + x(n)xT (n)]−1x(n)e(n)

Inversion of εI + x(n)xT (n) ?

Matrix Inversion Formula

[A + BCD]−1 = A−1 − A−1B[C−1 + DA−1B]−1DA−1

Thus,

[εI + x(n)xT (n)]−1 = ε−1I −ε−2

1 + ε−1xT (n)x(n)x(n)xT (n)

Post-multiplying both sides by x(n) and rearranging

[εI + x(n)xT (n)]−1x(n) =x(n)

ε + xT (n)x(n)

and

w(n + 1) = w(n) + µe(n)x(n)

xT (n)x(n) + ε

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 66 / 107

Some Research Results

M. H. Costa and J. C. M. Bermudez, “An improved model for the normalized LMSalgorithm with Gaussian inputs and large number of coefficients,” in Proc. of the2002 IEEE International Conference on Acoustics, Speech and Signal Processing(ICASSP-2002), Orlando, Florida, pp. II- 1385-1388, May 13-17, 2002.

J. C. M. Bermudez and M. H. Costa, “A Statistical Analysis of the ε-NLMS andNLMS Algorithms for Correlated Gaussian Signals,” Journal of the BrazilianTelecommunications Society, v. 20, n. 2, p. 7-13, 2005.

G. Barrault, M. H. Costa, J. C. M. Bermudez and A. Lenzi, “A new analyticalmodel for the NLMS algorithm,” in Proc. 2005 IEEE International Conference onAcoustics Speech and Signal Processing (ICASSP 2005) Pennsylvania, USA, vol.IV, p. 41-44, 2005.

J. C. M. Bermudez, N. J. Bershad and J.-Y. Tourneret, “An Affine Combination ofTwo NLMS Adaptive Filters - Transient Mean-Square Analysis,” In Proc.Forty-Second Asilomar Conference on Asilomar Conference on Signals, Systems &Computers, Pacific Grove, CA, USA, 2008.

P. Honeine, C. Richard, J. C. M. Bermudez and H. Snoussi, “Distributedprediction of time series data with kernels and adaptive filtering techniques insensor networks,” In Proc. Forty-Second Asilomar Conference on AsilomarConference on Signals, Systems & Computers, Pacific Grove, CA, USA, 2008.

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 67 / 107

The Affine Projection Algorithm

Consider the NLMS algorithm but using{x(n),x(n − 1), . . . ,x(n − P )}

Minimize ‖∆w(n)‖2 = ‖w(n + 1) − w(n)‖2

subject to:

xT (n)w(n + 1) = d(n)

xT (n − 1)w(n + 1) = d(n − 1)...

xT (n − P )w(n + 1) = d(n − P )

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 68 / 107

Observation matrix

X(n) = [x(n),x(n − 1), · · · ,x(n − P )]

Desired signal vector

d(n) = [d(n), d(n − 1), . . . , d(n − P )]

Error vector

e(n) = [e(n), e(n − 1), . . . , e(n − P )] = d(n) − XT (n)w(n)

Vector of the constraint errors

ec(n) = d(n) − XT (n)w(n + 1)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 69 / 107

Using Lagrange multipliers, we minimize

f [w(n + 1)] = ‖w(n + 1) − w(n)‖2 + λT [d(n) − XT (n)w(n + 1)]

Differentiating w.r.t. w(n + 1) and equating the result to zero,

w(n + 1) = w(n) +1

2X(n)λ (*)

Using this result in XT (n)w(n + 1) = d(n) yields

λ = 2[XT (n)X(n)]−1e(n)

Using this result in (*) yields

w(n + 1) = w(n) + µX(n)[XT (n)X(n)]−1e(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 70 / 107

Affine Projection

Solution to the Underdetermined Least-Squares Problem

We want minimize

‖ec(n)‖2 = ‖d(n) − XT (n)w(n + 1)‖2

where XT (n) is (P + 1) × N with (P + 1) < N

Thus, we look for the least-squares solution of the underdeterminedsystem

XT (n)w(n + 1) = d(n)

The solution is

w(n + 1) =[XT (n)

]+d(n) = X(n)[XT (n)X(n)]−1d(n)

Using d(n) = e(n) + XT (n)w(n) yields

w(n + 1) = w(n) + µX(n)[XT (n)X(n)]−1e(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 71 / 107

Observations:

Order of the AP algorithm: P + 1 (P = 0 → NLMS)

Convergence speed increases with P (but not linearly)

Computational complexity increases with P (not linearly)

If XT (n)X(n) is close to singular, use XT (n)X(n) + εI

The scalar error of NLMS becomes a vector error in AP (except forµ = 1)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 72 / 107

Affine Projection – Stochastic Approximation of

Regularized NewtonRegularized Newton Algorithm

w(n + 1) = w(n) + µ[εI + Rxx]−1[p − Rxxw(n)]

Estimates using time window statistics

p =1

P + 1

n∑

k=n−P

X(k)d(k) =1

P + 1X(n)d(n)

Rxx =1

P + 1

n∑

k=n−P

X(k)XT (k) =1

P + 1X(n)XT (n)

Using these estimates with ε = ε/(P + 1),

w(n + 1) = w(n) + µ[εI + X(n)XT (n)]−1X(n)

e(n)︷ ︸︸ ︷

[d(n) − XT (n)w(n)]

w(n + 1) = w(n) + µ[εI + X(n)XT (n)]−1X(n)e(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 73 / 107

w(n + 1) = w(n) + µ[εI + X(n)XT (n)]−1X(n)e(n)

Using the Matrix Inversion Formula

[εI + X(n)XT (n)]−1 = X(n)[εI + XT (n)X(n)]−1

and

w(n + 1) = w(n) + µX(n)[εI + XT (n)X(n)]−1e(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 74 / 107

Affine Projection Algorithm as a

Projection onto an Affine Subspace

Conditions for the analysis◮ e(n) = d(n) − XT (n)w(n)◮ d(n) = XT (n)wo defines the optimal solution in the least-squares

sense◮ v(n) = w(n) − wo (weight error vector)

Error vector

e(n) = d(n) − XT (n)[v(n) + w(n + 1)]

= XT (n)w(n + 1) − XT (n)[v(n) + w(n + 1)]

= −XT (n)v(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 75 / 107

e(n) = −XT (n)v(n)

Interpretation: To minimize the error v(n) should be orthogonal to allinput vectorsRestriction: We are going to use only {x(n),x(n− 1), . . . ,x(n−P )}

Iterative solution:

We can subtract from v(n) its projection onto the range of X(n) ateach iteration

v(n + 1) = v(n) − P X(n)v(n) (Proj. onto an affine subspace)

Using XT (n)v(n) = −e(n)

v(n + 1) = v(n) −{X(n)[XT (n)X(n)]−1XT (n)

}v(n)

= v(n) + µX(n)[XT (n)X(n)]−1e(n) (AP algorithm)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 76 / 107

Pseudo Affine Projection Algorithm

Major problem with the AP algorithmFor µ 6= 1, e(n) → e(n) ➪ large computational complexity

The Pseudo-AP algorithm replaces the input x(n) with its P -th orderautoregressive prediction

x(n) =

P∑

k=1

akx(n − k)

Using the least-squares solution for a = [a1, a2, . . . , aP ]T ,

a = [XT

p (n)Xp(n)]−1XT

p (n)x(n), Xp(n) = [x(n − 1), . . . , x(n − P )]

Now, we subtract from x(n) its projections onto the last P inputvectors

φ(n) = x(n) − Xp(n)a(n)

= x(n) −{Xp(n)[XT

p (n)Xp(n)]−1XTp (n)

}x(n)

= (I − P P )x(n); (P P : projection matrix)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 77 / 107

Example – Pseudo-AP versus AP

0 1000 2000 3000 4000 5000 6000−80

−70

−60

−50

−40

−30

−20

−10

0Mean Square Error

dB

Iterations

AR(8)=[−0.9 0.8 −0.7 0.6 −0.5 0.4 −0.3 0.2]N=64P=8SNR=80dBS=Null

AP(−72.82dB) PAP(−75.82)

α=0.7

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 78 / 107

Using φ as the new input vector for the NLMS algorithm,

w(n + 1) = w(n) + µφ(n)

φT (n)φ(n)e(n)

It can be shown that Pseudo-AP is identical to AP for an AR inputand µ = 1

Otherwise, Pseudo-AP is different from AP

Simpler to implement than AP for µ 6= 1

Can lead even to better steady-state results than AP for AR inputs

For AR inputs: NLMS with input “orthogonalization”

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 79 / 107

Some Research ResultsS. J. M. de Almeida, J. C. M. Bermudez, N. J. Bershad and M. H. Costa, “Astatistical analysis of the affine projection algorithm for unity step size andautoregressive inputs,” IEEE Transactions on Circuits and Systems - I, vol. 52, pp.1394-1405, July 2005.

S. J. M. Almeida, J. C. M. Bermudez and N. J. Bershad, “A Stochastic Model fora Pseudo Affine Projection Algorithm,” IEEE Transactions on Signal Processing, v.57, p. 107-118, 2009.

S. J. M. Almeida, M. H. Costa and J. C. M. Bermudez, “A Stochastic Model forthe Deficient Length Pseudo Affine Projection Adaptive Algorithm,” In Proc. 17thEuropean Signal Processing Conference (EUSIPCO), Aug. 24-28, Glasgow,Scotland, 2009.

S. J. M. Almeida, M. H. Costa and J. C. M. Bermudez, “A stochastic model forthe deficient order affine projection algorithm,” in Proc. ISSPA 2010, KualaLumpur, Malaysia, May 2010.

C. Richard, J. C. M. Bermudez and P. Honeine, “Online Prediction of Time SeriesData With Kernels,” IEEE Transactions on Signal Processing, v. 57, p.1058-1067, 2009.

P. Honeine, C. Richard, J. C. M. Bermudez, H. Snoussi, M. Essoloh and F.Vincent, “Functional estimation in Hilbert space for distributed learning in wirelesssensor networks,” In Proc. IEEE International Conference on Acoustics Speech andSignal Processing (ICASSP), Taipei, Taiwan, p. 2861-2864, 2009.

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 80 / 107

Deterministic Algorithms

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 81 / 107

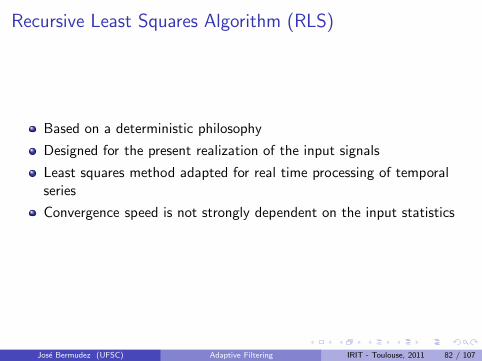

Recursive Least Squares Algorithm (RLS)

Based on a deterministic philosophy

Designed for the present realization of the input signals

Least squares method adapted for real time processing of temporalseries

Convergence speed is not strongly dependent on the input statistics

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 82 / 107

RLS – Problem Definition

Define

xo(n) = [x(n), x(n − 1), . . . , x(0)]T

x(n) = [x(n), x(n − 1), . . . , x(n − N + 1)]T input to the N-tap filter

Desired signal d(n)

Estimator of d(n): y(n) = xT (n)w(n)

Cost function – Squared Error

Jls(n) =n∑

k=0

e2(k) =n∑

k=0

[d(k) − xT (k)w(n)]2

= eT (n)e(n), e(n) = [e(n), e(n − 1), . . . , e(0)]T

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 83 / 107

In vector form

d(n) = [d(n), d(n − 1), . . . , d(0)]T

y(n) = [y(n), y(n − 1), . . . , y(0)]T , y(k) = xT (k)w(n)

y(n) =

N−1∑

k=0

wk(n)xo(n − k) = Θ(n)w(n)

Θ(n) =

x(n) x(n − 1) · · · x(n − N + 1)x(n − 1) x(n − 2) · · · x(n − N)

......

......

x(0) x(−1) · · · x(−N + 1)

= [xo(n),xo(n − 1), . . . xo(n − N + 1)]

e(n) = d(n) − Θ(n)w(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 84 / 107

e(n) = d(n) − Θ(n)w(n)

and we minimizeJls(n) = ‖e(n)‖2

Normal Equations

ΘT (n)Θ(n)w(n) = Θ

T (n)d(n)

R(n)w(n) = p(n)

Alternative representation for R and p

R(n) = ΘT (n)Θ(n) =

n∑

k=0

x(k)xT (k)

p(n) = ΘT (n)d(n) =

n∑

k=0

x(k)d(k)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 85 / 107

RLS – Observations

w(n) remains fixed for 0 ≤ k ≤ n to determine Jls(n)

Optimum vector w(n) is wo(n) = R−1

(n)p

The algorithm has growing memory

In an adaptive implementation,

wo(n) = R−1

(n)p

must be solved for each iteration n

Problems for an adaptive implementation◮ Dificulties with nonstationary signals (infinite data window)◮ Computational complexity

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 86 / 107

RLS - Forgetting the Past

Modified cost function

Jls(n) =

n∑

k=0

λn−ke2(k) =

n∑

k=0

λn−k[d(k) − xT (k)w(n)]2

= eT (n)Λe(n), Λ = diag[1, λ, λ2, . . . , λn]

Modified Normal Equations

ΘT (n)ΛΘ(n)w(n) = Θ

T (n)Λd(n)

R(n)w(n) = p(n)

where

R(n) = ΘT (n)ΛΘ(n) =

n∑

k=0

λn−kx(k)xT (k)

p(n) = ΘT (n)Λd(n) =

n∑

k=0

λn−kx(k)d(k)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 87 / 107

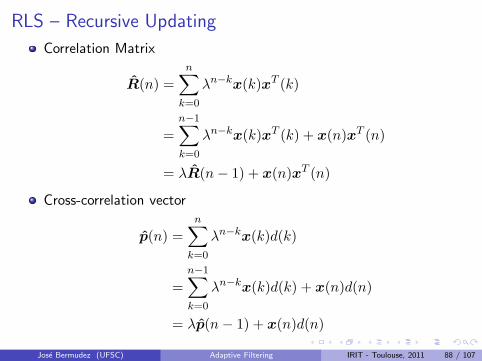

RLS – Recursive Updating

Correlation Matrix

R(n) =

n∑

k=0

λn−kx(k)xT (k)

=

n−1∑

k=0

λn−kx(k)xT (k) + x(n)xT (n)

= λR(n − 1) + x(n)xT (n)

Cross-correlation vector

p(n) =

n∑

k=0

λn−kx(k)d(k)

=

n−1∑

k=0

λn−kx(k)d(k) + x(n)d(n)

= λp(n − 1) + x(n)d(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 88 / 107

We have recursive updating expressions for R(n) and p(n)

However, we need a recursive updating for R−1

(n), as

wo(n) = R−1

(n)p(n)

Applying the matrix inversion lemma to

R(n) = λR(n − 1) + x(n)xT (n)

and defining P (n) = R−1

(n) yields

P (n) = λ−1P (n − 1) −λ−2P (n − 1)x(n)xT (n)P (n − 1)

1 + λ−1xT (n)P (n − 1)x(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 89 / 107

The Gain Vector

Definition

k(n) =λ−1P (n − 1)x(n)

1 + λ−1xT (n)P (n − 1)x(n)

Using this definition

P (n) = λ−1P (n − 1) − λ−1k(n)xT (n)P (n − 1)

k(n) can be written as

k(n) =

P(n)︷ ︸︸ ︷[λ−1P (n − 1) − λ−1k(n)xT (n)P (n − 1)

]x(n)

= R−1

(n)x(n)

➪ k(n) is the repres. of x(n) on the column space of R(n)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 90 / 107

RLS – Recursive Weight Update

w(n + 1) = wo(n)

Using

w(n + 1) = R−1

(n)p(n) = P (n)p(n)

p(n) = λp(n − 1) + x(n)d(n)

P (n) = λ−1P (n − 1) − λ−1k(n)xT (n)P (n − 1)

k(n) = P (n)x(n)

e(n) = d(n) − xT (n)w(n)

yields

w(n + 1) = w(n) + k(n)e(n) RLS weight update

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 91 / 107

RLS – Observations

The RLS convergence speed is not affected by the eigenvalues ofR(n)

Initialization: p(0) = 0, R(0) = δI, δ ≃ (1 − λ)σ2x

This results in R(n) changed to λnδI + R(n)➪ Biased estimate of wo(n) for small n(No problem for λ < 1 and large n)

Numerical problems in finite precision◮ Unstable for λ = 1◮ Loss of symmetry in P (n)

⋆ Evaluate only upper (lower) part and diagonal of P (n)⋆ Replace P (n) with [P (n) + P T (n)]/2 after updating from P (n − 1)

Numerical problems when x(n) → 0 and λ < 1

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 92 / 107

Some Research Results

C. Ludovico and J. C. M. Bermudez, “A recursive least squaresalgorithm robust to low- power excitation,” in. Proc. 2004 IEEEInternational Conference on Acoustics, Speech and Signal Processing(ICASSP-2004), Montreal, Canada, vol. II, p. 673-677, 2004.

C. Ludovico and J. C. M. Bermudez, “An improved recursive leastsquares algorithm robust to input power variation,” in Proc. IEEEStatistical Signal Processing Workshop, Bordeaux, France, 2005.

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 93 / 107

Performance Comparison

System identification, N=100

Input – AR(1) x(n) = 0.9x(n − 1) + v(n)

AP algorithm with P = 2

Step sizes designed for equal LMS and NLMS performances

Impulse response to be estimated

0 10 20 30 40 50 60 70 80 90 100−0.1

−0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

sample

impu

lse

resp

onse

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 94 / 107

Excess Mean Square Error - LMS, NLMS and AP

0 1000 2000 3000 4000 5000 6000−80

−70

−60

−50

−40

−30

−20

−10

0

10

iteration

EM

SE

(dB

)

EMSE for LMS, NLMS and AP(2)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 95 / 107

Excess Mean Square Error - LMS, NLMS, AP and RLS

0 1000 2000 3000 4000 5000 6000−80

−70

−60

−50

−40

−30

−20

−10

0

10

iteration

EM

SE

(dB

)

EMSE for LMS, NLMS, AP(2) and RLS

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 96 / 107

Performance Comparisons

Computational Complexity

Adaptive filter with N real coefficients and real signals

For the AP algorithm, K = P + 1

Algorithm × + /

LMS 2N + 1 2N

NLMS 3N + 1 3N 1

AP (K2 + 2K)N + K3 + K (K2 + 2K)N + K3 + K2

RLS N2 + 5N + 1 N2 + 3N 1

For N = 100, P = 2

Algorithm × + / ≃ factor

LMS 201 200 1

NLMS 301 300 1 1.5

AP 1, 530 1, 536 7.5

RLS 10, 501 10, 300 1 52.5

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 97 / 107

Typical values for acoustic echo cancellation (N = 1024, P = 2)

Algorithm × + / ≃ factor

LMS 2, 049 2, 048 1

NLMS 3, 073 3, 072 1 1.5

AP 15, 390 15, 396 7.5

RLS 1, 053, 697 1, 051, 648 1 514

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 98 / 107

How to Deal with Computational Complexity?

Not an easy task!!!

There are ”fast” versions for some algorithms (especially RLS)

What is usually not said is that ... speed can bring◮ Instability◮ Increased need for memory

➪ Most applications rely on simple solutions

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 99 / 107

Understanding the Adaptive Filter Behavior

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 100 / 107

What are Adaptive Filters?Adaptive filters are, by design, systems that are

Time-variant (w(n) is time-variant)

Nonlinear (y(n) is a nonlinear function of x(n))

Stochastic (w(n) is random)

LMS:

w(n + 1) = w(n) + µe(n)x(n)

=[I − µ x(n)xT (n)

]x(n) + µ d(n)x(n)

y(n) = xT (n)w(n)

They are difficult to understand

Different applications and signals require different analyses

Simplifying assumptions are necessary

➪ Good design requires good analytical models.Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 101 / 107

LMS AnalysisBasic equations:

d(n) = xT (n)wo + z(n)

e(n) = d(n) − xT (n)w(n)

w(n + 1) = w(n) + µ e(n)x(n)

v(n) = w(n) − wo (study about the optimum weight vector)

Mean Weight Behavior:Neglecting dependence between v(n) and x(n)xT (n),

E[v(n + 1)] = (I − µRxx)E[v(n)]

Follows the steepest descent trajectory

Convergence condition: 0 < µ < 2/λmax

limn→∞

E[w(n)] = wo

However: w(n) is random➪ We need to study its fluctuations about E[w(n)] → MSE

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 102 / 107

The Mean-Square Estimation Error

e(n) = eo(n) − xT (n)v(n), eo(n) = d(n) − xT (n)wo

Square the error equation

Take the expected value

Neglect the statistical dep. between v(n) and x(n)xT (n)

Jms(n) = E[e2o(n)] + Tr{RxxK(n)}, K(n) = E[v(n)vT (n)]

This expression is independent of the adaptive algorithm

Effect of the alg. on Jms(n) is determined by K(n)

Jmsmin= E[e2

o(n)]

Jmsex = Tr{RxxK(n)}

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 103 / 107

The Behavior of K(n) for LMS

Using the basic equations

v(n + 1) =[I + µ x(n)xT (n)

]v(n) + µ eo(n)x(n)

Post-multiply by vT (n + 1)

Take the expected value assuming v(n) and x(n)xT (n) independent

Evaluate the expectations◮ Higher order moments of x(n) require input pdf

Assuming Gaussian inputs

K(n + 1) =K(n) − µ [RxxK(n) + K(n)Rxx]

+ µ2 {RxxTr[RxxK(n)] + 2RxxK(n)Rxx}

+ µ2 RxxJmsmin

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 104 / 107

Design Guidelines Extrated from the Model

Stability

0 < µ <m

Tr[Rxx]; m = 2 or m = 2/3

Jms(n) converges as a function of

[(1 − µλi)

2 + 2µ2λ2i

]n, i = 1, . . . , N

Steady-State

Jmsex(∞) ≃µ

2Tr[Rxx]Jmsmin

M(∞) =Jmsex(∞)

Jmsmin

(MSE Misadjustment)

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 105 / 107

Model Evaluation

x(n) = α x(n − 1) + v(n)

0 1000 2000 3000 4000 5000 6000−80

−70

−60

−50

−40

−30

−20

−10

0

10

EMSE. Blue: Simulation. Red: Analytical Model

EM

SE

LMS − Excess Mean Square Error

Input: White noise

0 1000 2000 3000 4000 5000 6000−80

−70

−60

−50

−40

−30

−20

−10

0

10

EMSE. Blue: Simulation. Red: Analytical Model

EM

SE

LMS − Excess Mean Square Error

Input: AR(1), α = 0.8

Linear system identification - FIR with 100 coefficients

Step-size µ = 0.05

Noise power σ2v = 10−6

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 106 / 107

Merci pour votre attention!!!

Jose Bermudez (UFSC) Adaptive Filtering IRIT - Toulouse, 2011 107 / 107