Acquisition of November 1 st 2002. 2 Table of Contents I.Overview of Pegasus II.Transaction...

22

Acquisition of Acquisition of November 1 November 1 st st 2002 2002

-

date post

19-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Acquisition of November 1 st 2002. 2 Table of Contents I.Overview of Pegasus II.Transaction...

Acquisition ofAcquisition of

November 1November 1stst 2002 2002

2

Table of ContentsTable of Contents

I.I. Overview of PegasusOverview of Pegasus

II.II. Transaction RationaleTransaction Rationale

III.III. Pegasus ValuationPegasus Valuation

IV.IV. Transaction StructureTransaction Structure

I. I. Overview of PegasusOverview of Pegasus

4

Overview of Pegasus Overview of Pegasus BackgroundBackground

Historical Current Ownership Structure 44

1994 - Pegasus is founded by Andrade Gutierrez

1998 - The Company is granted by Anatel an SLE 1 license to provide corporate network services on a national and international basis

1999 - Pegasus launches commercial operations as a “carriers' carrier”

Alcatel provides vendor financing

2000 - Acquisition of VIS 2 and of 360km of fiber optic deployed by Talb 3 in São Paulo

Focus on the corporate client segment

Strategic investment by GP Investimentos, Opportunity, Banco do Brasil and Telemar

2001 - Pegasus completes its long-distance backbone and activates its main metropolitan rings

Strategic investment by ABN Amro and increase in Banco do Brasil and Telemar’s ownership interest in Pegasus

2002 - Pegasus continues to expand both its carrier’s carrier and corporate businesses

EBITDA positive in early 2002

24.4%

GP GP InvestimentosInvestimentos

GP GP InvestimentosInvestimentos

ABN ABN AMROAMROABN ABN

AMROAMRO

AG TelecomAG TelecomAG TelecomAG Telecom

OpportunityOpportunityOpportunityOpportunity

Banco do Banco do BrasilBrasil

Banco do Banco do BrasilBrasil

La FonteLa FonteLa FonteLa Fonte

TNLTNLTNLTNL

10.9%

6.7%

7.1%

7.1%

11.7%

32.1%

Source: Pegasus Telecom1 Serviço limitado especializado2 VIS - Versolato Informática e Soluções Ltda., a provider of broadband data transmission services via radio technology3 Talb Participações S.A., one of Grupo GP Investimentos' portfolio companies4 Does not include potential dilution from options granted to Pegasus management totaling 4.27%

5

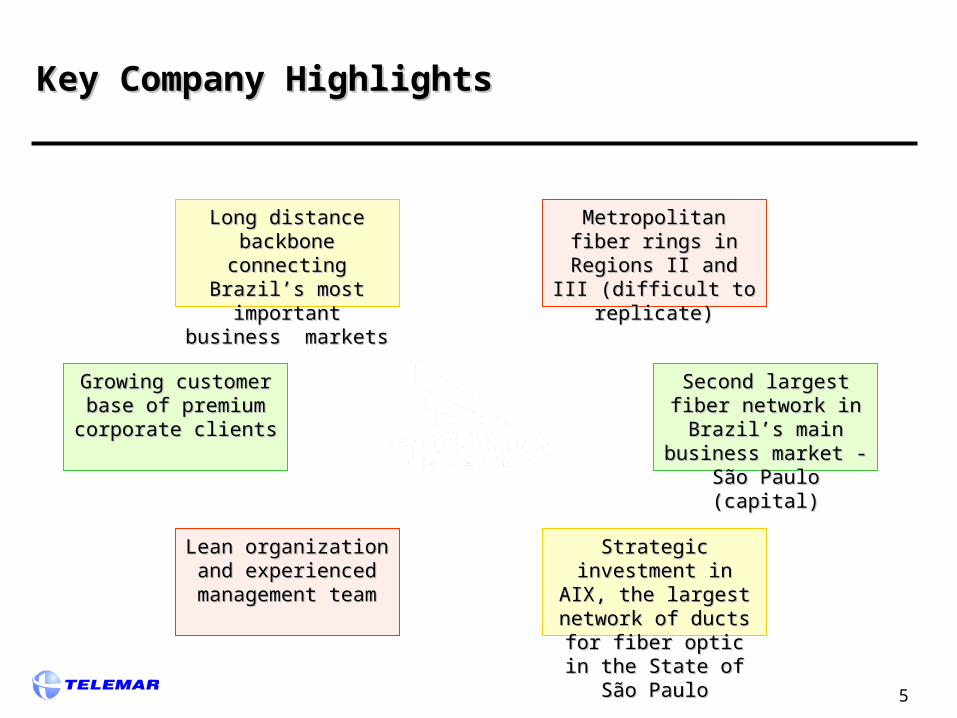

Key Company Highlights Key Company Highlights

Second largest fiber Second largest fiber network in Brazil’s main network in Brazil’s main business market - São business market - São

Paulo (capital)Paulo (capital)

Metropolitan fiber rings Metropolitan fiber rings in Regions II and III in Regions II and III (difficult to replicate)(difficult to replicate)

Long distance Long distance backbone connecting backbone connecting

Brazil’s most important Brazil’s most important business marketsbusiness markets

Strategic investment in Strategic investment in AIX, the largest network AIX, the largest network of ducts for fiber optic in of ducts for fiber optic in the State of São Paulothe State of São Paulo

Growing customer base Growing customer base of premium corporate of premium corporate

clientsclients

Lean organization and Lean organization and experienced experienced

management teammanagement team

6

Network Coverage and Capacity Network Coverage and Capacity

Pegasus network consists of fiber optic cable distributed through a 5,723 km long distance backbone and 872 km of urban rings covering 10 cities with 770 POPs

Long Distance Network Urban Rings

Source: Pegasus Telecom

Long Distance Network Km

Main Long Distance Routes

São Paulo - Rio de Janeiro 458 São Paulo - Belo Horizonte 775 São Paulo - Curitiba 463 Curitiba - Florianopolis - Porto Alegre 737 Brasília - Belo Horizonte 984 Subtotal 3,417

Redundancy Long Distance Routes

São Paulo - Curitiba (via interior) 500 Curitiba - Florianopolis - Porto Alegre (via interior) 907 Subtotal 1,407

Regional Rings

São Paulo - Santos - Cubatão 110 São Paulo - Jundiaí - Campinas - Jacareí 216 São Paulo - Sorocaba - Campinas 166 São Paulo - Cotia 407 Subtotal 899

Total Long Distance 5,723

Metro Rings Km

Barueri 17 Brasília 29 Campinas 68 Curitiba 41 Guarulhos 2 Osasco 4 Porto Alegre 22 Santos 44 São José dos Campos 28 São Paulo 617

Total Metro Rings 873

7

Key Clients by Segment Key Clients by Segment

As of June 2002, Pegasus had a total of 32 carrier clients and 246 corporate and SME clients

Source: Pegasus Telecom

Carrier Corporate SME

8

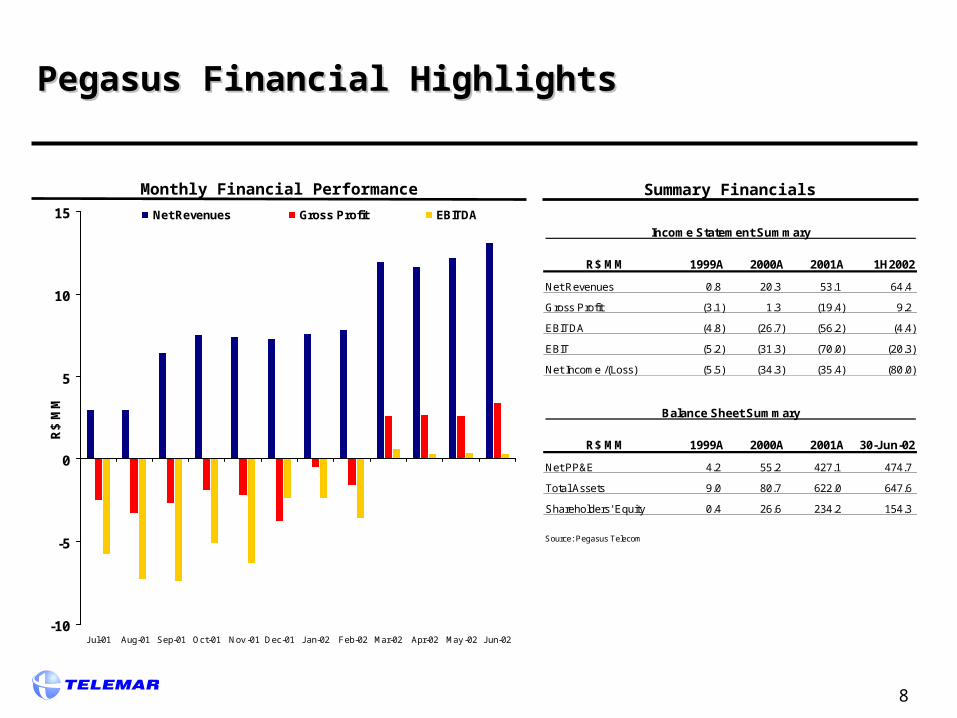

Pegasus Financial Highlights Pegasus Financial Highlights

-10

-5

0

5

10

15

Jul-01 Aug-01 Sep-01 Oct-01 Nov -01 Dec-01 Jan-02 Feb-02 Mar-02 Apr-02 May -02 Jun-02

R$

MM

Net Revenues Gross Profit EBITDA

Monthly Financial Performance Summary Financials

Income Statement Summary

R$ MM 1999A 2000A 2001A 1H2002

Net Revenues 0.8 20.3 53.1 64.4

Gross Profit (3.1) 1.3 (19.4) 9.2

EBITDA (4.8) (26.7) (56.2) (4.4)

EBIT (5.2) (31.3) (70.0) (20.3)

Net Income /(Loss) (5.5) (34.3) (35.4) (80.0)

Balance Sheet Summary

R$ MM 1999A 2000A 2001A 30-Jun-02

Net PP&E 4.2 55.2 427.1 474.7

Total Assets 9.0 80.7 622.0 647.6

Shareholders' Equity 0.4 26.6 234.2 154.3

Source: Pegasus Telecom

9

Overview of Brazilian Data Market Overview of Brazilian Data Market

Market Share by Total Data Revenues – 2001 Brazilian Data Market Revenues 1

0

1

2

3

4

5

6

7

2000A 2001E 2002E 2003E 2004E 2005E 2006E

US

$ b

n

IDC Pyramid

2001-2006 C

AGR

IDC = 23%

Pyram

id = 21%

Source: IDC – Brazil Data Network Services, 2002 and Pyramid Research

Note: 1. Excludes leased lines (wholesale) revenues and revenues associated with VAS (data centers, ASPs)

Brasil Telecom

10%

Alternative Carriers

14%

EMT43%

Telefonica18%

Telemar15%

Source: IDC – Brazil Data Network Services, 2002

II. II. TransactioTransaction Rationalen Rationale

11

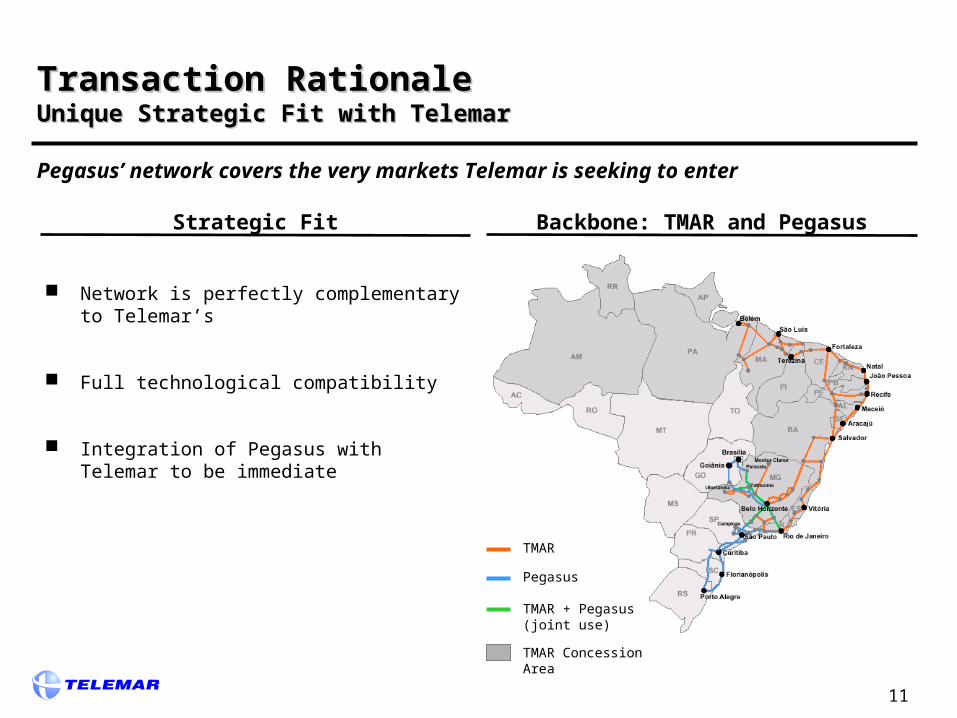

Transaction Rationale Transaction Rationale Unique Strategic Fit with TelemarUnique Strategic Fit with Telemar

Network is perfectly complementary to Telemar’s

Full technological compatibility

Integration of Pegasus with Telemar to be immediate

Strategic Fit

TMAR

Pegasus

TMAR + Pegasus (joint use)

TMAR Concession Area

Backbone: TMAR and Pegasus

Pegasus’ network covers the very markets Telemar is seeking to enter

12

Transaction Rationale Transaction Rationale Consolidating Telemar’s Data BusinessConsolidating Telemar’s Data Business

Consolidate Telemar data strategy

Important time-to-market effect for nationwide presence

Strategic and defensive move

13

Transaction Rationale Transaction Rationale Alternatives to PegasusAlternatives to Pegasus

Purchase other Asset

Build up of a new network

Continue to rent capacity

14

Transaction Rationale Transaction Rationale Expected Revenue Synergies from Combination with TelemarExpected Revenue Synergies from Combination with Telemar

Accelerate market share increase in Regions II and III

Increase penetration in Telemar´s key accounts

Enhance Telemar Revenue stream by upgrading network quality

levels

Increase in revenues from other carriers

15

Transaction Rationale Transaction Rationale Expected Cost, Capex and Fiscal Synergies from Combination with TelemarExpected Cost, Capex and Fiscal Synergies from Combination with Telemar

Decrease in maintenance cost

Reduction in SG&A expenses

CAPEX

Fiscal

III. Pegasus ValuationIII. Pegasus Valuation

17

Pegasus Valuation Pegasus Valuation Overview of the ProcessOverview of the Process

Valuation process

1. Committee headed by BNDES

2. Teams composed by TMAR’s Senior Management

3. 1st Class Market Professionals

18

Pegasus ValuationPegasus ValuationMain AssumptionsMain Assumptions

Revenue Build-up

Costs / SG&A Build-up

CAPEX

WACC

Terminal Value

19

Final Valuation and Recommended PriceFinal Valuation and Recommended Price

Pegasus Equity Value: R$ 221,803,704

Debt: R$ 339,146,296 as of June 30, 2002

Acquisition price will be significantly below the valuation of Pegasus’ latest round of financing

R$ 513

R$ 222

Latest Round of Financing Current Equity Valuation

Implied Equity Value in R$ MM 1 Implied Equity Value in US$ MM 2

$261

$58

Latest Round of Financing Current Equity Valuation

- 57%- 78%

Note: Telemar currently has 24.4% of Pegasus. Total Telemar investment in Pegasus amount to R$100.5mm (US$51.5mm)

1. Assuming net debt of R$ 339,146,296 for Pegasus as of June 30, 2002

2. Assuming exchange rate of R$1.97/US$ as of December 21, 2000 for last round of financing and exchange rate of R$3.82/US$ for current equity valuation (PTAX of Oct 29, 2002)

IVIV. Transaction S. Transaction Structuretructure

21

Acquisition ProposalAcquisition Proposal

Structure

Transaction Value

Consideration

Acquisition of 99.999% of Pegasus capital through Telemar Norte Leste (TMAR)

Equity Value R$ 221,803,704

Synergies R$ 114,000,000

Tax Credit R$ 44,000,000 (upon materialization)

Cash + debt assumption

Terms R$ 50 million upon signing the contract and the balance in 90 days

Other Contingencies and adjustments to be deducted from price

Final Values to be calculated based on the transfer Balance Sheet

Debt and Working Capital variation to be adjusted as per transfer Balance Sheet

22

Acquisition ProposalAcquisition Proposal

Approval Process

Timing Transaction will be submitted to shareholders vote by Nov. 29 th , 2002

The Board of Directors of Telemar Norte Leste approved the terms of the transaction in Oct.30th , 2002, and recommended that the acquisition is submitted to a vote at an extraordinary shareholders meeting

Pending ANATEL and CADE approvals