Acquisition of Barclays’s credit card business in Spain & … · · 2016-04-28in Spain &...

12

Acquisition of Barclays’s credit card business in Spain & Portugal through bancopopular-e April 2016

Transcript of Acquisition of Barclays’s credit card business in Spain & … · · 2016-04-28in Spain &...

Acquisition of Barclays’s credit card business in Spain & Portugal through bancopopular-e

April 2016

This presentation has been prepared by Banco Popular Español solely for informational purposes. It may contain

estimates and forecasts with respect to the future development of the business and to the financial results of the

Banco Popular Group, which stem from the expectations of the Banco Popular Group and which, by their very

nature, are exposed to factors, risks and circumstances that could affect the financial results in such a way that they

might not coincide with such estimates and forecasts. These factors include, but are not restricted to: (i) changes in

interest rates, exchange rates or any other financial variables, both on the domestic as well as on the international

securities markets, (ii) the economic, political, social or regulatory situation, and (iii) competitive pressures. In the

event that such factors or other similar factors were to cause the financial results to differ from the estimates and

forecasts contained in this presentation, or were to bring about changes in the strategy of the Banco Popular Group,

Banco Popular does not undertake to publicly revise the content of this presentation.

The information contained in this presentation refers to the date that appears on it, and it is based on information

obtained from reliable sources. This presentation contains summarized information and may contain unaudited

information. In no case shall its content constitute an offer, invitation or recommendation to subscribe or acquire

any security whatsoever, to make or cancel any kind of investments, nor it is intended to serve as a basis for any

contract or commitment whatsoever. Its content shall not be considered as any kind of advice.

Banco Popular Group does not assume any responsibility for the losses, direct or indirect, which could derive from

the use of this document or its content. This document shall not be reproduced, distributed or published, not whole

not partially, without the previous written consent of the Bank.

Disclaimer

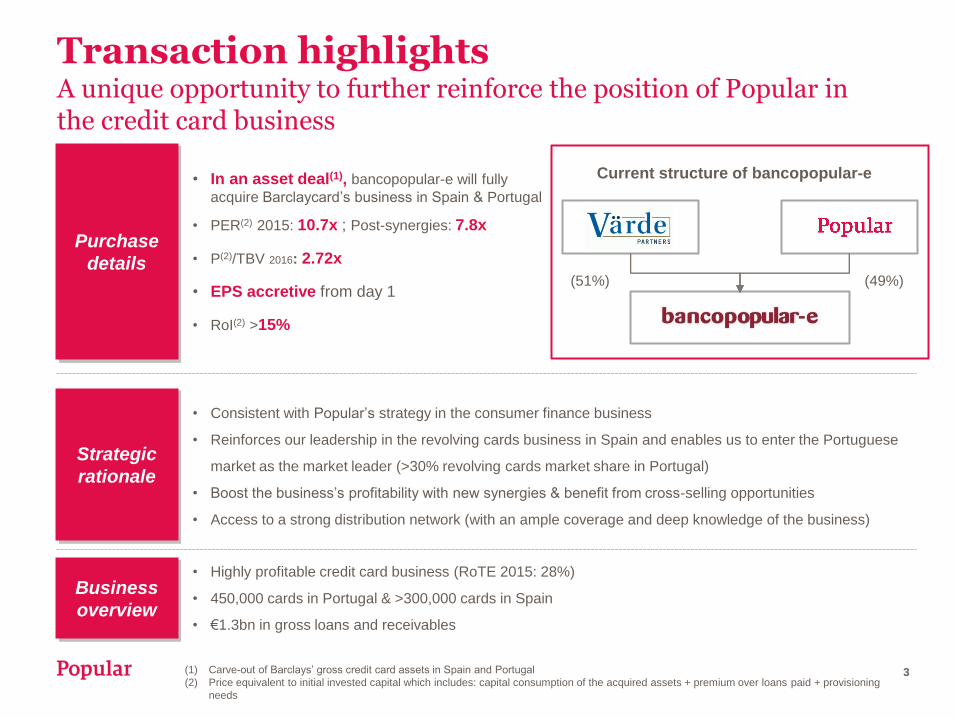

Transaction highlights A unique opportunity to further reinforce the position of Popular in the credit card business

3

Purchase

details

Strategic

rationale

• In an asset deal(1), bancopopular-e will fully

acquire Barclaycard’s business in Spain & Portugal

• PER(2) 2015: 10.7x ; Post-synergies: 7.8x

• P(2)/TBV 2016: 2.72x

• EPS accretive from day 1

• RoI(2) >15%

Business

overview

Current structure of bancopopular-e

(51%) (49%)

• Consistent with Popular’s strategy in the consumer finance business

• Reinforces our leadership in the revolving cards business in Spain and enables us to enter the Portuguese

market as the market leader (>30% revolving cards market share in Portugal)

• Boost the business’s profitability with new synergies & benefit from cross-selling opportunities

• Access to a strong distribution network (with an ample coverage and deep knowledge of the business)

• Highly profitable credit card business (RoTE 2015: 28%)

• 450,000 cards in Portugal & >300,000 cards in Spain

• €1.3bn in gross loans and receivables

(1) Carve-out of Barclays’ gross credit card assets in Spain and Portugal

(2) Price equivalent to initial invested capital which includes: capital consumption of the acquired assets + premium over loans paid + provisioning

needs

Strategic rationale A unique opportunity to further reinforce the position of Popular in the credit card business

1. Brings a highly profitable business, adds synergies to the existing platform as well as provides cross-

selling opportunities

− Barclaycard is a highly profitable business (28.1% RoTE in 2015)

− Benefiting from economies of scale and synergies

− New customer base with high satisfaction standards, which provides significant cross-selling opportunities

2. Extremely powerful platform, which will enhance bancopopular-e’s activity

− Strong distribution network, with 1,200 sales reps

− >10 years of experience

− Well-recognised player in Spain, with a high level of expertise

− Low execution risk (IT, management,…).

3. bancopopular-e will reinforce its leading position in Spain and enter Portugal as the market leader,

becoming the benchmark in both countries

− 30% post-deal revolving cards market share in Spain

− 31% post-deal revolving cards market share in Portugal

4. In line with Popular’s strategy of strengthening its position in the consumer finance business, which

offers attractive returns in the current low-rate environment

4

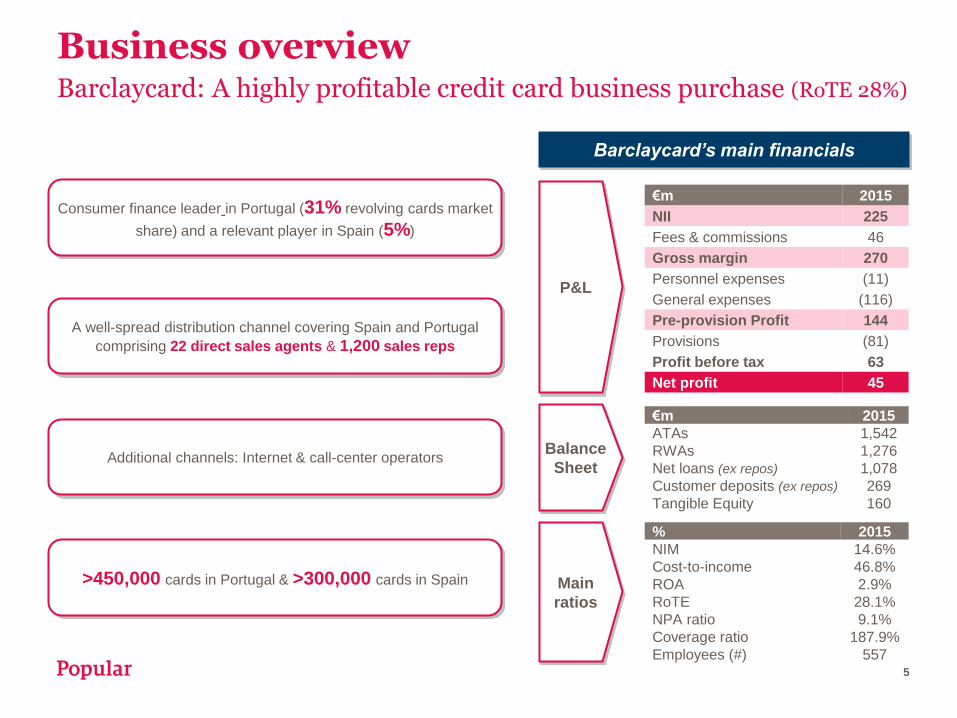

Business overview Barclaycard: A highly profitable credit card business purchase (RoTE 28%)

Barclaycard’s main financials

€m 2015

NII 225

Fees & commissions 46

Gross margin 270

Personnel expenses (11)

General expenses (116)

Pre-provision Profit 144

Provisions (81)

Profit before tax 63

Net profit 45

P&L

Balance

Sheet

€m 2015

ATAs 1,542

RWAs 1,276

Net loans (ex repos) 1,078

Customer deposits (ex repos) 269

Tangible Equity 160

Main

ratios

% 2015

NIM 14.6%

Cost-to-income 46.8%

ROA 2.9%

RoTE 28.1%

NPA ratio 9.1%

Coverage ratio 187.9%

Employees (#) 557

Consumer finance leader in Portugal (31% revolving cards market

share) and a relevant player in Spain (5%)

A well-spread distribution channel covering Spain and Portugal

comprising 22 direct sales agents & 1,200 sales reps

>450,000 cards in Portugal & >300,000 cards in Spain

Additional channels: Internet & call-center operators

5

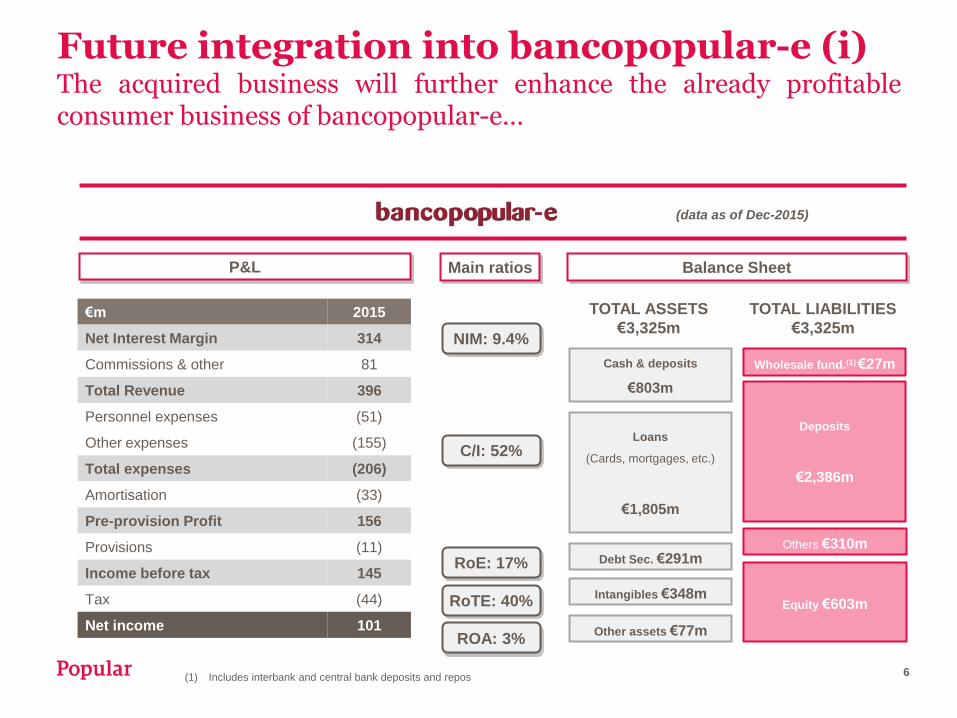

€m 2015

Net Interest Margin 314

Commissions & other 81

Total Revenue 396

Personnel expenses (51)

Other expenses (155)

Total expenses (206)

Amortisation (33)

Pre-provision Profit 156

Provisions (11)

Income before tax 145

Tax (44)

Net income 101

P&L Main ratios

NIM: 9.4%

C/I: 52%

RoTE: 40%

ROA: 3%

Balance Sheet

(data as of Dec-2015)

Cash & deposits

€803m

Loans

(Cards, mortgages, etc.)

€1,805m

Debt Sec. €291m

Intangibles €348m

Other assets €77m

TOTAL ASSETS

€3,325m

Wholesale fund.(1) €27m

Deposits

€2,386m

Others €310m

TOTAL LIABILITIES

€3,325m

Equity €603m

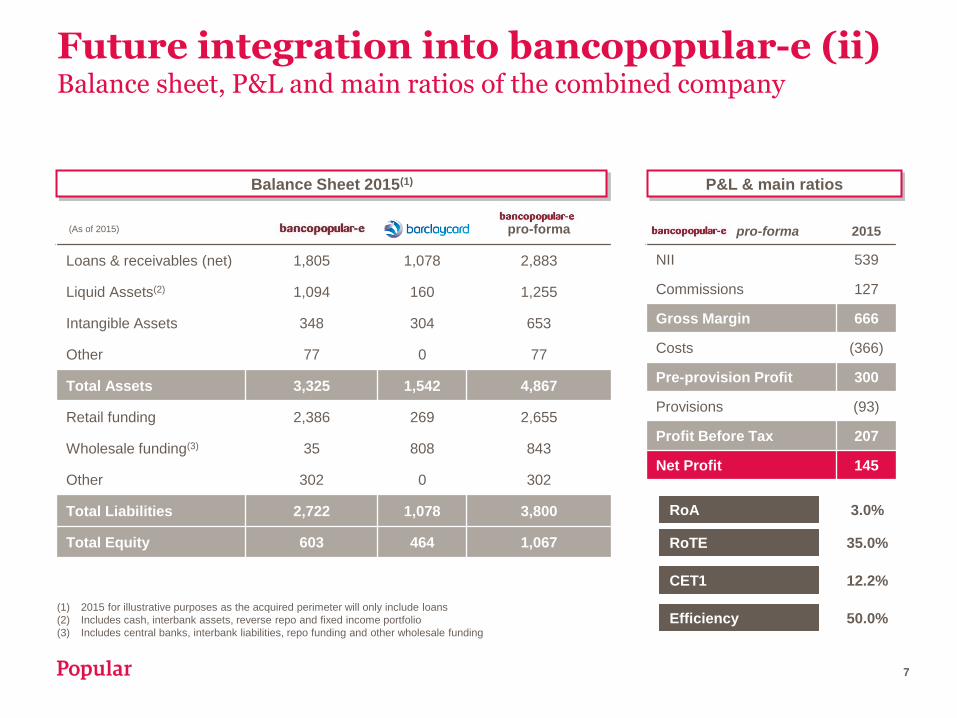

Future integration into bancopopular-e (i) The acquired business will further enhance the already profitable consumer business of bancopopular-e…

6

RoE: 17%

(1) Includes interbank and central bank deposits and repos

(1) 2015 for illustrative purposes as the acquired perimeter will only include loans

(2) Includes cash, interbank assets, reverse repo and fixed income portfolio

(3) Includes central banks, interbank liabilities, repo funding and other wholesale funding

pro-forma 2015

NII 539

Commissions 127

Gross Margin 666

Costs (366)

Pre-provision Profit 300

Provisions (93)

Profit Before Tax 207

Net Profit 145

(As of 2015) bp-e bc pro-forma

Loans & receivables (net) 1,805 1,078 2,883

Liquid Assets(2) 1,094 160 1,255

Intangible Assets 348 304 653

Other 77 0 77

Total Assets 3,325 1,542 4,867

Retail funding 2,386 269 2,655

Wholesale funding(3) 35 808 843

Other 302 0 302

Total Liabilities 2,722 1,078 3,800

Total Equity 603 464 1,067

RoA

RoTE

CET1

Efficiency

3.0%

35.0%

12.2%

50.0%

Future integration into bancopopular-e (ii) Balance sheet, P&L and main ratios of the combined company

Balance Sheet 2015(1) P&L & main ratios

7

Revolving cards business market share breakdown in Spain & Portugal

Future integration into bancopopular-e (iii) Leadership in Spain & Portugal

5%

5%

7%

8%

8%

15%

25%

Bank 5

Barclaycard

Bank 4

Bank 3

Bank 2

Bank 1

.

Pre-deal Post-deal

5%

7%

8%

8%

15%

30%

Bank 5

Bank 4

Bank 3

Bank 2

Bank 1

.

8%

13%

14%

16%

31%

Bank 4

Bank 3

Bank 2

Bank 1

.

8%

13%

14%

16%

31%

Bank 4

Bank 3

Bank 2

Bank 1

.

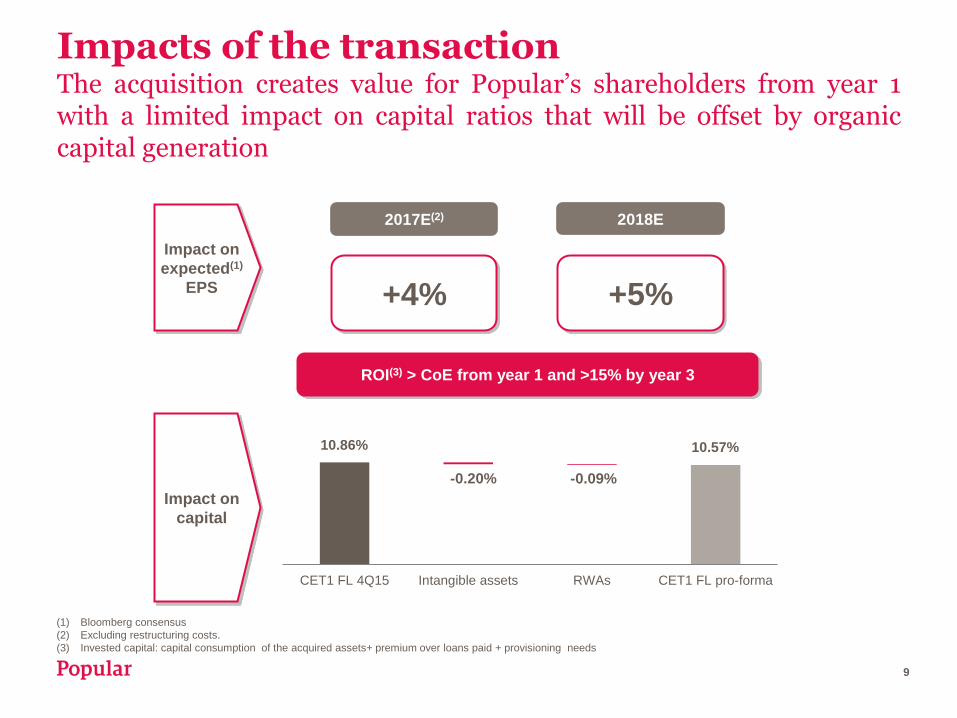

8 Source: Mckinsey

(1) Bloomberg consensus

(2) Excluding restructuring costs.

(3) Invested capital: capital consumption of the acquired assets+ premium over loans paid + provisioning needs

10.86% 10.57%

-0.20% -0.09%

CET1 FL 4Q15 Intangible assets RWAs CET1 FL pro-forma

Impacts of the transaction The acquisition creates value for Popular’s shareholders from year 1 with a limited impact on capital ratios that will be offset by organic capital generation

Impact on

expected(1)

EPS

Impact on

capital

9

2018E

+5%

2017E(2)

+4%

ROI(3) > CoE from year 1 and >15% by year 3

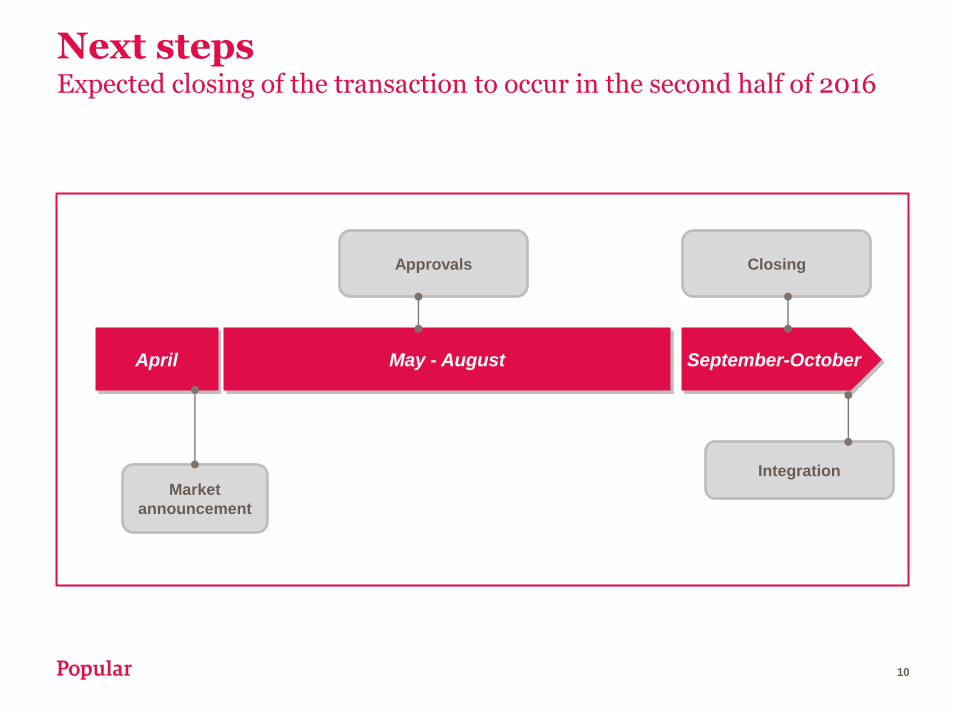

September-October April May - August

Market

announcement

Approvals

Integration

Next steps Expected closing of the transaction to occur in the second half of 2016

10

Closing

1. Strategically makes sense: Popular will reinforce its position in some of the Bank’s key

segments, such as SMEs and consumer finance

2. This transaction strengthens Popular’s leadership in the highly profitable revolving cards

business

3. The transaction is accretive for shareholders from day 1, with limited capital consumption

which will be offset by organic capital generation

4. Strong platform which provides economies of scale and important synergies

5. Enter new markets (Portugal) and provide significant cross-selling opportunities

11

Final remarks

Further information: [email protected]