ACO Technical Assistance: Finances and … 2, 2017 ACO Technical Assistance: Finances and...

98

June 2, 2017 ACO Technical Assistance: Finances and Infrastructure for Value Based Payment Readiness

Transcript of ACO Technical Assistance: Finances and … 2, 2017 ACO Technical Assistance: Finances and...

June 2, 2017

ACO Technical Assistance: Finances and Infrastructure for Value Based Payment

Readiness

Agenda

Time Topic Facilitator

9:30 –10:00

Welcome and Introductions

Review of the VBP TA Series and Goals for Today

Ellen Hafer, Mass League

10:00 –11:00

Overview of VBP, Drivers of Revenue and Financial Dilemma

Peter Epp

11:00 –12:30

Defining the Tasks; Defining the Responsibilities Lisa Whittemore

12:30 –1:30

LUNCH

1:30 – 3:00 Detailed Walkthrough of the Financial Model Peter Epp

3:00 – 3:30 Wrap Up and Implications for Next Steps Peter Epp; Lisa Whittemore

2

Agenda

3

Goals for Today

Overview of VBP, Drivers of Revenue and Financial Dilemma

Defining the Tasks; Defining the Responsibilities

Detailed Walkthrough of the Financial Model

Wrap Up and Implications for Next Steps

Four-Part Series on Value Based Payment Readiness: Overview

4

Overview of Readiness Roadmap:

How to Succeed in New

Environment

• Setting the tone for change

• Review of roadmap

• Building the pyramid: risk

stratification

Elements for Success – Finances and

Infrastructure:

• Negotiation strategies

• Funds flow, infrastructure

investments and levels of risk

• Quality and incentive model

Elements for Success –

Population Management:

• Empanelment/engagement

• Enrollment

• Best practices to achieve quality,

outcomes improvements

• Health risk assessments and

follow-up

Elements for Success: ACO Risk

Stratification and Coding for

Improvement

• Coding in new MassHealth

environment

• Approaches to risk stratification for

financial and quality improvements

• Role of social determinants

Goals for Today

5

• Develop knowledge and capacity at CHCs for financial management in the Value Based Payment context

• Bring together financial, administrative and clinical leaders to think about shared accountability

• Build knowledge of choices related to service delivery, member supports and associated costs

• Build skills and awareness for negotiations with ACOs and MCOs

Agenda

6

Goals for Today

Overview of VBP, Drivers of Revenue and Financial Dilemma

Defining the Tasks; Defining the Responsibilities

Detailed Walkthrough of the Financial Model

Wrap Up and Implications for Next Steps

Introduction

7

To prepare for payment reform, health centers must:

• Improve cost efficiencies today and revenue cycle management

– Create positive operating margins

– Generate reserves

• Create business processes and reporting necessary for success in the future

Health centers require a financial modeling process that:

‒ Manages current financial performance of baseline operations AND

‒ Layers on top the financial impact of Value Based Payment (VBP)

Fee-for-service Value Based Payment

Improving the Current Baseline Financial Performance

8

Due to the peaks-and-valleys in the timing of VBP payments and their uncertainties, health centers current baseline operations need to exhibit positive operating performance

The current budget model, and its underlying drivers, need to be managed to enhance revenue and create cost efficiencies

Operating Revenue:

‒ Measure uncompensated care versus grant subsidies

‒ Enhance net patient services revenue per visit:• Payor mix of visits

• Bad debt % (collection rates)

• Coding

• Provider productivity

Improving the Current Baseline Financial Performance

9

Operating Expenses:

The following variables impact the all-inclusive cost per visit and must be managed to improve financial performance:

• Salary levels, benefit packages and staffing mix

• Support staff ratios (direct care versus patient support)

• Amount of enabling and ancillary services

• Administrative/overhead infrastructure

• Provider productivity/clinician capacity

Capital Link’s Performance Evaluations Profiles provide noteworthy benchmarks for identifying cost efficiency opportunities!

$ 1,542,100

⁼ $ 154.21 per visit10,000 visits

Improving the Current Baseline Financial Performance

10

Below are selected financial metrics from Capital Link’s

Performance Evaluation Profile, displaying the

Massachusetts 50th percentiles (medians)

Capital Link’s Performance Evaluations Profiles provide noteworthy benchmarks for identifying cost efficiency opportunities!

2013 2014 2015

Days Cash on Hand 42 42 40

Current Ratio 2.5:1 2.3:1 2.3:1

Net Patient Revenue per Visit $ 140 $ 146 $ 152

Operating Revenue per Visit $ 213 $ 226 $ 264

Operating Expense per Visit $ 224 $ 225 $ 251

Operating Margin (0.4%) 0.4% 0.4%

Physician Productivity 2,824 2,596 2,398

Mid-level Productivity 2,226 2,155 1,922

VBP Arrangements – “The 3-Legged Stool”

11

VBP arrangements contain a hybrid of several different payment methodologies to incentivize and tie together desired behaviors

The key components of VBP arrangements include: Base Compensation Models

• Fee-for-service• Partial capitation

Care Coordination Fee PMPM Quality Incentive Payments Global Payments/Budgets

• Surplus-sharing/Risk-sharing• Global capitation

Care Coordination

Qu

alit

y In

ce

ntiv

e P

ay

me

nts

VBP Arrangements

12

Preparation for VBP requires an understanding of the key metrics that drives each payment methodology

− Quality and risk-adjusting embedded through-out

Payment Model Key Metric

Base Compensation Move from “per visit” to “per patient” (capitation)

Care Coordination New core competencies and cost

Quality Incentive Payments Measuring performance metrics

Global Budgets/Payment Monitoring the total health care spend (and quality)

VBP – Quality Metrics & Incentive Payments

13

“Value-inspired” metrics, of late, revolve around the following areas:

• Patient quality measures

• Process measures

• Population health metrics

• Patient satisfaction measures

• Access

• Efficiency

Measurement and payment thresholds include -

• Event based

• Population based

– Maintenance

– Improvement

VBP – Quality Metrics & Incentive Payments

14

Understand metrics being measured• Discussion of metrics selected

• Calculation of the metric (including data elements)

• Identify benchmarks

• Evaluate current performance and anticipated future performance

Project revenue based on anticipated performance and benchmarks

• Fixed payment per measure for improvement

• Fixed payment per measure for maintenance

• Incremental bonus based on movement of metric

• Composite scoring across multiple metrics

• Amount of surplus-sharing/risk-sharing payments earned

VBP – Quality Metrics & Incentive Payments

15

Types and how payment determined

Type of Payment Formula to Earn Payment Examples

Fixed amount paid for improvement of metric

Improvement of metric from one quartile to another

Various HEDIS measures

Fixed amount paid for maintenance of metric

Maintain metric that currently exceeds the specific

percentile

Various HEDIS measures

Incremental bonus based on size of movement in metric

Amount of payment increases incrementally based on size of

% change

Reduction in urgent/non-emergent ER use

Composite scoring across multiple metrics

Negotiated set of metrics assigned points; % earned based on number of points scored versus total points

available

Numerous HEDIS measures defined that, as a group, determine

payment

VBP – Quality Metrics & Incentive Payments

16

Sample Efficiency Metrics (TennCare’s PCMH Demo):

VBP – Quality Metrics & Incentive Payments

17

Sample Quality Metrics (TennCare’s PCMH Demo):

VBP – Quality Metrics & Incentive Payments

18

Example of composite scoring formula

• Analysis of metric

• Comparison to benchmark (1 point for meeting benchmark)

MeasureCurrent Actual

Year One Year Two

Improve % Metric Improve % Metric

Comprehensive Diabetes Care (#1)

40.00% 25% 50.00% 15% 57.50%

Measure Benchmark (Threshold)

Projected Score

Year One Year Two

Comprehensive Diabetes Care (#1)

≥ 50% 1 1

VBP – Quality Metrics & Incentive Payments

19

Example of composite scoring formula (continued)

• Composite scoring and amount of payment

• Some payors may set a minimum score before QIP payments will be made

• Quality scores may also impact potential surplus-sharing distributions

Year One Year Two

Total Actual Points – all measures 3 5

Total Available Points (10 metrics) 10 10

% of Total Attained 30% 50%

Maximum QIP Pool Available $ 500,000 $ 500,000

Total Projected QIP Payment $ 125,000 $ 250,000

VBP - Global Budgets/Payments

20

Example Calculation of Surplus-Sharing/Risk-Sharing Amounts:

Actual Expense vs. Benchmark Scenario A Scenario B

Actual Expenses:

Fee for Service $42,500,000 $47,500,000

Capitation (Health Center) $5,000,000 $4,000,000

Total Actual Expense $47,500,000 $51,500,000

Target Spend/Benchmark $50,000,000 $50,000,000

Surplus/(Loss) $2,500,000 ($1,500,000)

Shared-Surplus Arrangement (50%) $1,250,000 N/A

Risk-Sharing Arrangement (60% upside; 30% downside)

$1,500,000 ($450,000)

VBP – Surplus/Risk-Sharing

21

Example revenue projection

$ PMPM

# of Member

Months Total Amount

Targeted Spend/Benchmark $500.00 100,000 $50,000,000

Actual Spend (Projected) $475.00 100,000 $47,500,000

Projected Surplus (Deficit) $25.00 $2,500,000

Surplus-Sharing % 50%

Amount Available for Distribution $1,250,000

Quality Score 75%

Adjusted Distribution for Quality Score $937,500

Surplus/Risk-Sharing – Key Considerations

22

Key items which impact success: Panel formation

Enrollment

Attribution

Development of overall budget Utilization assumption based (bottom up) – “Paid Claims”

Historic baseline or revenue based (top down) – “Medical Loss Ratio”

Protections against outliers Stop Loss

Carve-Outs

Risk Corridors

Reserves

Quality modifiers/adjusters

New York – Total Cost of Care Benchmarking Guideline

23

Budget/Benchmark Setting

24

Setting a Budget Target (using historical claims data):

Service Description

Expected

Utilization Unit Cost

Cost Per Patient

Per Year

Inpatient Care 1 $3,000 per discharge $ 3,000

Emergency Room 5 $300 per visit 1,500

Specialty Care 2 $250 per visit 500

Primary Care 2 $100 per visit 200

Behavioral Health Care 1 $100 per visit 100

Laboratory 8 $25 per lab test 200

Radiology 2 $100 per xray 200

Pharmacy 12 $25 per script 300

TOTAL – Per Member per Year $6,000 PMPY

TOTAL – Per Member per Month ($6,000 / 12 months) $500 PMPM

What factors can be impacted to reduce the Total Cost of Care?

Differs based on Health Condition of

Patient

Case Study: MCO Surplus Sharing

Baseline (Target) Calculation (1/1/2013 – 12/31/2013)

Type of Service Admits/Visits

A/V per 1000

Amount Paid Cost perA/V PMPM

Inpatient 360 169 $2,817,435 $7,826 $110.19

O/P Facility – ED 2,381 1,117 $494,354 $208 $19.33

O/P Facility – Surgery 79 37 $145,548 $1,842 $5.69

O/P Facility – Other 5,599 2,628 $1,104,074 $197 $43.18

O/P Facility Subtotal 8,059 3,782 $1,743,976 $216 $68.20

Professional – Primary Care 4,423 2,076 $55,774 $13 $2.18

Professional – Specialty Care 15,346 7,202 $1,606,835 $105 $62.84

Dental 1,856 871 $0 $0 $0.00

Vision 343 161 $0 $0 $0.00

Prescription 31,233 14,658 $2,264,304 $72.50 $88.50

Other Services (e.g., Home Health) 701 329 $0 $0 $0.00

Grand Total 62,321 29,247 $8,488,323 $331.96

Case Study: MCO Surplus Sharing

Surplus Calculation (1/1/2014 – 12/31/2014)

Change from Baseline experience

Type of Service Admits/Visits

A/V per 1000

Amount Paid Cost perA/V PMPM

Inpatient 248 121 $2,057,460 $8,296 $83.64

O/P Facility – ED 1,934 943 $429,540 $222 $17.46

O/P Facility – Surgery 50 24 $83,045 $1,661 $3.38

O/P Facility – Other 6,904 3,368 $955,824 $138 $38.85

O/P Facility Subtotal 8,888 4,336 $1,468,209 $165 $59.69

Professional – Primary Care 3,246 1,583 $39,256 $12 $1.60

Professional – Specialty Care 14,962 7,299 $1,307,260 $87 $53.14

Dental 1,962 962 $0 $0 $0.00

Vision 528 258 $0 $0 $0.00

Prescription 30,928 15,087 $1,932,026 $62 $78.54

Other Services (e.g., Home Health) 0 0 $0 $0 $0.00

Grand Total $6,804,411 $276.60

Using Third-Party Claims Data

27

• Analyze the high cost and high utilizing members

• Combine Claims data files– Determine the Total Cost of Care by patient and PMPM– Determine Total Cost of Care for patients with like conditions (e.g., all

diabetic patients regardless of comorbidities)

• Stratify the high cost/high utilizing members and develop plans to better manage care and reduce the Total Spend– Clinical interventions to manage utilization– Outreach efforts/patient engagement– Specialty referral practices and high cost specialists

• Link to EHR/PMS, ED Use and High Risk Member Reports

• Analyze “systemic” anomalies– Physician practice patterns – cost and outcomes– Specialty referral practices and high cost/low quality specialists– Care locations

VBP – New Core Competencies

28

Improved coding and clinical documentation• Traditional coding (claims)

• Enhanced coding and documentation (EHR)

• Social determinants of health

Managing patient centered care (per patient)

Data analytics (including business intelligence)

Care management/delivery• HIT/HIE

Partnerships and collaboration

MCO contracting

Financial management systems

Care Coordination Fees

29

One of the foundational elements of most, if not all, VBP arrangements is the need for effective care coordination and management

Third party payors are sometimes including care coordination fees in their VBP arrangements, however health centers need to sell the value of the care coordination proposal

− Stand-alone fee PMPM− Advance against future shared-savings distributions

Development of a proposed care coordination fee:− What services are required?− What services should be provided at the health center sites versus reside

at the ACO/IPA level?− How to “cost-out” care coordination services?

Care Coordination Services

30

What care coordination/management services are required to be successful under VBP?

* May be provided by the ACO/IPA

Service Type Health Center ACO/IPA

Care Managers √

Care Management Central Support and Technology

√

Data Analytics Technology and Support

√* √

Health Informatics √* √

Quality Improvement √ √

Others ??? ???

Care Coordination Costs – Health Center

31

Example calculation of cost of care coordination services − Total cost and PMPM

Service Type Costing MethodologyCost

Estimate

Care Managers (blended staffing) 4.00 FTE X $60,000 $ 240,000

Quality Improvement 1.00 FTE X $75,000 75,000

Health Informatics 1.00 FTE X $75,000 75,000

Support Staff 1.00 FTE X $30,000 30,000

Care Management/Data Analytics Technology Solutions

Covered by ACO/IPA (charged to the center?)

???

Others TBD ???

TOTAL ANNUAL COSTS $ 420,000

Number of Member Months 10,000 members X 12 mos. 120,000

COST PMPM $ 3.50

Care Coordination Costs – ACO

32

Example calculation of cost of care coordination services − Total cost and PMPM

Service Type Costing MethodologyCost

Estimate

Care Management Central Support 2.00 FTE X $60,000 $ 120,000

Support Staff 1.00 FTE X $30,000 30,000

Others TBD ???

Overhead 15% of direct costs 22,500

Care Managers Paid directly to centers ???

Care Management Technology Solution $3.00 PMPM 3,600,000

TOTAL ANNUAL COSTS $ 3,772,500

Number of Member Months 100,000 members X 12 mos. 1,200,000

COST PMPM $ 3.14

Why Form an ACO/IPA?

33

• Share infrastructure and realize cost efficiencies

• Quality improvements through sharing of best practices

• Pool resources to attract talent

• Expansion of geographic reach/market share

• Pool members to spread insurance risk in VBP arrangements and improve bargaining position with third party payors

• Expansion of service offerings and improve care coordination

• Improved access to capital resources (e.g. DSRIP)

Funds Flow Within the ACO/IPA

34

Hospitals

DSRIP Incentive

Payments

ACOs

Physicians FQHCs LTC Providers

MassHealth / MCOs

Funds Flow Within the ACO/IPA

35

ACO/IPAs cash flow projections• What services will the ACO/IPA provide on behalf of its members?• Reserves?

– Working capital– VBP reserve requirements

• What revenue sources are available to the ACO/IPA to defray the cash needs?

• Distribution methodology of quality incentive/VBP surplus payments to members

Payments to ACO/IPA members• Pass-through of care coordination/quality incentive payments• Surplus-sharing/Risk-sharing allocations

– Attributed lives– Quality scores

– Participation and engagement

– Other

Overview – ACO Distribution Methodologies

36

Distribution methodologies developed often change over time as experience with VBP matures

In developing a distribution methodology, the following hierarchy is often utilized

1st Investment in reserves

2nd Repayment of capital

3rd Performance incentive payments

Investment in Reserves – setting aside cash for future investments, maintenance of minimum cash balances and/or establishment of reserves for VBP arrangements

Repayment of Capital – based on Board decision-making, additional paid-in capital may be repaid

− In its entirety before performance incentive payments begin OR

− In pre-defined amounts over a specific period of time

Performance Incentive Payments –Distribution Methodologies

37

Example of Separate Pools each with its own, distinct distribution methodology

− Allocation %’s between pools may change over time (e.g. weighted heavier to participation in earlier years as VBP capacity is built, transitioning to performance as VBP experience increases)

− Distribution of participation pool (e.g. 20%)

− Distribution of performance pool (e.g. 80%)

− Additional Decision Point – How to address undistributed funds

Total Pool X% Allocated to

Participation PoolX

AttributedMembers as %

of TotalX

Participation Score

=Participation

Payment

Total Pool X% Allocated to

Performance PoolX

AttributedMembers as %

of TotalX

Quality Score

=Performance

Payment

Performance Incentive Payments –Distribution Methodologies

38

Example of Aggregate Pool with one, single distribution formula

− Additional Decision Point – How to address undistributed funds

Total Pool XAttributed

Members as % of Total

X Quality Score X% Reduction in

Total Cost of Care

=Participation

Payment

DSRIP Funds Flow

39

DSRIP Funding Levels (Statewide)

• $1.8B over 5 years (eff. July 1, 2017)

• Payments to Commonwealth contingent upon hitting pre-defined metrics and milestones

• To be replaced with savings generated from VBP in 5 years

DSRIP Funds Flow

40

ACO Funding Stream:

Uses:

‒ Infrastructure and start-up

‒ On-going/operational costs

‒ Flexible services (not currently covered by MassHealth)

‒ Transitional funding for certain safety net hospitals currently funded through the Delivery System Transformation Initiatives program

Award Calculation:

‒ ACO start-up and on-going support

• Funded based on proportional size of attributed members at a $ PMPY

• Safety Net PMPY increase for ACOs with high % of safety net providers

• ACO Model PMPY increase for advanced ACO models

• MassHealth to designate a portion for investment in primary care

‒ Glide Path for Certain Safety Net Hospitals based on MassHealth guidance

‒ Flexible services – PMPY amount fixed across all 5 DSRIP years

DSRIP Funds Flow

41

ACO Funding Stream (cont’d): Decision Rights on Spending:

‒ ACO start-up and ongoing support• MassHealth to develop guidance on allocation of dollars for safety net “glide

path” funding and PC investment dollars• Balance allocated at the ACO’s discretion

‒ Flexible services funding is “use it or lose it” and allocated at the ACO’s discretion

Accountability to the State:‒ ACOs will have accountability for the total cost of care of their attributed

members in DY1‒ An increasing amount of DSRIP funds will be at risk over the 5 year DSRIP

period (0-20%) based on an accountability score including the following variables:

• Avoidable hospital utilization• Reduction in State spending• Attaining quality metrics

• Progress towards integration across physical health, behavioral health and LTSS

DSRIP Funds Flow

42

What to expect: During the governance development, committees will be formed -

‒ Executive

‒ Finance (budget and funds flow)

‒ Clinical

‒ Workforce

‒ Technology

Projects will be developed to accomplish the goals of DSRIP and population health management

Discussions will ensue with regards to what services to be performed at the ACO versus those to be delegated down to the ACO’s members

The Funds Flow of the DSRIP waiver dollars will follow the responsibilities and participation in projects

Generally DSRIP funds will be paid based on performance, so the timing of fund distributions may occur after-the-fact

The VBP Dilemma

43

The timing of potential new revenue streams under VBP are not aligned with the costs for successful participation in VBP

Payment Model

Timing of Cost

Timing of RevenueOne-time,

UpfrontOn-going,

Operational

Base Compensation√

Through-out the year as services are provided

Care Coordination√ √

Through-out the year as services are provided

Quality Incentive Payments

√ √6-9 months after the end of the measurement period

GlobalBudgets/Payment

√ √6-9 months after the end of the measurement period

VBP – Financial and Operational Considerations

44

What is this going to cost?

• Identify new services to be provided

• Evaluate whether to “go this alone” versus “join forces”

• Develop a 3-year financial model, including cash flow

• Quantify a range of capital requirements

• Identify outside funding sources to offset capital needs and reserves

What is the return on investment

• Understand financial requirements of participation in VBP arrangements

• Develop sound assumptions based on available data

• Utilize financial model to inform ACO/MCO negotiations

Agenda

45

Goals for Today

Overview of VBP, Drivers of Revenue and Financial Dilemma

Defining the Tasks; Defining the Responsibilities

Detailed Walkthrough of the Financial Model

Wrap Up and Implications for Next Steps

Re-visiting the Pyramid – Thinking about Population Needs

46

PATIENT POPULATION INTERVENTION

BH CPs…

High Risk

Moderate Risk

Low Risk

No or Limited Risk

Attributed Members/Not Yet Patients Engagement and Outreach

Risk Management

Risk Mitigation

Revenue Management

Expense Management

Care Management

Care Coordination

Complex Care Management

Wellness Initiatives

High Need, High Cost

Chronic Conditions

Well Populations

Elevated Need, Elevated Cost

High Risk

Moderate Risk

Low Risk

No or Limited Risk

Risk Management

Risk Mitigation

Revenue Management

Population Health Management: Different Perspectives – Payers and Providers

Providers and payers have different perspectives of the activities that are included in utilization management, case management, and chronic condition management.

The highly regulated nature of the health insurance industry presently requires that payers maintain oversight of functions that they shift to providers.

The current process for function oversight is tightly managed and highly controlled which poses challenges to making it scalable across a large network.

There is a significant change management challenge in sharing accountability between payers and providers. Clear communication of the driving factors behind the strategy to shift accountability will need top-down executive reinforcement as well as bottom-up operational buy-in

Not all providers within your ACO have the same capacity, expertise, or desire to perform these functions.

Three Truths

48

• There are a set of tasks that need to be done for the ACO to function and achieve triple-aim goals and for members to be supported

• These tasks need to be done either locally (in health centers) or centrally by the ACO or the MCO

• Decisions about who does the tasks have significant financial implications – Revenue impact

– Care efficiency and effectiveness

– Effective financial strategies

Ancillary services (e.g. lab)

Process Algorithms/

EBM Guidelines

Telemedicine

QA for network providers

Patient billingfor servicesrendered

Preventive Care

Capacity or access

management

Outpatientcare

ACO: financial/data management

Compliance management

Provider function Payer function

Plan billing (MCO

function)

Utilization management

Disease management

Quality measures /

analytics

Care management

Physician credentialing& privileging

Member enrollment

HIE / connectivity

Physician performance/

quality management

Wellness programs

Pre-auth for non-

formulary

Medical monitoring

Compliance enhancement

Provider process &

quality improvement

State and Federal

Advocacy

Medical management

Care enhancement

Network management

Admin. services

Member acquisition/

management

Quality/informatics

Member Engagement

Member services

Alternative payment

structures

Provider management

servicesCare delivery Pharmacy

Claims processing/

payment

Risk-pooling

Care coordination

Scheduling services

Inpatient care

Data warehousing

Formulary management

Provider contracting /

network participation

VBP Payer/Provider Service Continuum: Assess ACO Participants Current State

49

Payer Administrative Services

50

Plan billing (MCO

function

Admin.

services

Member services

Claims processing/

payment

Risk-pooling

• Basic administrative functions of a health plan: paying claims, actuarial risk calculations, benefit administration

• Member service: Basic health plan customer service

** For Model A ACOs, these functions done by

MCO; for Model B ACOs, these functions done by Mass Health.

Network Management

51

QA for network providers

Physician credentialing& privileging

Network management

Alternative payment

structures

Provider contracting /

network participation

• Network of primary care providers, specialty providers, hospitals, rehab facilities, ancillary services, behavioral health providers

• Traditionally health plans have not had a lot of non-medical services that may be important to care for your members

• Maintaining the quality of the network is important to members’ care and has long been a task done by health plans

• Monitoring performance on risk based contracts

Enrolling and Retaining Members

52

Member enrollment

State and Federal Advocacy

Member acquisition/

management

Member engagement

• Member enrollmento In the MCO or MassHealth AND

o With the ACO

• Marketing strategies and resources

• Growth strategy

• Work with State and Federal entities to ensure adequate program funding

Pharmacy Benefit Management

53

Pre-auth for non-formulary

Medical monitoring

Compliance enhancement

Pharmacy

Formulary management

• Pharmacy network• Developing and implementing

formulary including knowledge about costs

• Prior authorization process for primary care AND specialty providers

• Compliance

Care Delivery

54

Ancillary services (e.g. lab)

Telemedicine

Preventive Care

Outpatientcare

Care delivery

Inpatient care

Core services for taking care of members:

• Inpatient care, specialty care, primary care, BH care

• Labs and ancillary services

• Preventive Care, diagnoses

Is mostly outside any PMPM – Billing still done Fee for Service

Provider Management Services

55

Capacity or access management

Compliance management

Provider management

services

Patient billingfor services

rendered

ACO: financial/data management

Scheduling services

• Scheduling with providers

• Access management

• Billing

• Compliance

• ACO monitoring of performance

Care Enhancement

56

Care enhancement

Process algorithms/EBM

guidelines

Provider process & quality

improvement

Care coordination

Improving how care is delivered to members:• Care Coordination• Transitions of Care• Applying Evidence-Based Medicine

Interventions• Quality Improvement Efforts including

transparent data sharing efforts

Quality and Informatics

57

Quality measures /

analytics

HIE / connectivity

Physician performance/

quality management

Quality/informatics

Data warehousing

• Data!

o What data are you going to receive?

• HIE and connectivity between systems

• Quality measures and analytics

• Quality directory and sharing results

• Predictive Analytics for Risk Stratification

Medical Management

58

Utilization management

Disease management

Care management

Wellness programs

Medical management • Managing patients care

outside of the traditional visit

• Developing and maintaining staffing patterns to support this care

• Ensuring your assigned members are receiving the right care at the right time

Ancillary services (e.g. lab)

Process Algorithms/

EBMguidelines

Telemedicine

QA for network providers

Patient billingfor servicesrendered

Preventive Care

Capacity or access

management

Outpatientcare

ACO: financial/data management

Compliance management

Provider function Payer function

Plan billing (MCO

function)

Utilization management

Disease management

Quality measures /

analytics

Care management

Physician credentialing& privileging

Member enrollment

HIE / connectivity

Physician performance/

quality management

Wellness programs

Pre-auth for non-

formulary

Medical monitoring

Compliance enhancement

Provider process &

quality improvement

State and Federal

Advocacy

Medical management

Care enhancement

Network management

Admin. services

Member acquisition/

management

Quality/informatics

Member engagement

Member services

Alternative payment

structures

Provider management

servicesCare delivery Pharmacy

Claims processing/

payment

Risk-pooling

Care coordination

Scheduling services

Inpatient care

Data warehousing

Formulary management

Provider contracting /

network participation

VBP Payer/Provider Service Continuum: Thinking about roles differently

59

Exercise: Determining the Provider Role (local)/Provider Role (Central or ACO)/

Payer Role?

Task Provider Role (if any)

ACO Role (if any)

MCO Role (if any)

Care Coordination

EBM/ Clinical Protocols

Quality Improvement

Data Warehousing

HIE/ Connectivity

Quality Measures/ Analytics

ACO Financial Data Management

HEALTH MANAGEMENT ASSOCIATES 60

Exercise: Determining the Provider Role (local)/Provider Role (Central or ACO)/

Payer Role?

Task Provider Role (if any)

ACO Role (if any)

MCO Role (if any)

Member Enrollment

Member Engagement

Provider Performance

Wellness Programs

Telemedicine

Formulary Development and Management

Formulary Compliance Enhancement

HEALTH MANAGEMENT ASSOCIATES 61

Exercise: Determining the Provider Role (local)/Provider Role (Central or ACO)/

Payer Role?

Task Provider Role (if any)

ACO Role (if any)

MCO Role (if any)

Utilization Management• Inpatient• Procedures

Care Management• Complex• Transitions of Care• Chronic Condition

Disease Management• Registry

Management• Active Engagement

HEALTH MANAGEMENT ASSOCIATES 62

Exercise Part 2

For each of the areas where you identified a provider role, which are your priorities?

What resources do you need to meet these goals?

How will you share accountability with the ACOs?

Where can you leverage resources through partnering with the ACO or the MCO?

HEALTH MANAGEMENT ASSOCIATES 63

PRIORITIES = Strategies you can deploy to ensure your patients receive the care

they need within the ACO + the resources required to deploy those models +factor in negotiating with ACO OR MCO to ensure those factors are met

Agenda

64

Goals for Today

Overview of VBP, Drivers of Revenue and Financial Dilemma

Defining the Tasks; Defining the Responsibilities

Detailed Walkthrough of the Financial Model

Wrap Up and Implications for Next Steps

Value Based Payment Financial Model

65

• Develop a financial model Prepare 3-year financial model, including cash flow

Decide on the services required to be provided for success under VBP

– In-house (personnel) versus outsourced (ACO vs. MSO)

– On-going versus one-time

Develop a cost projection based on services required

Project potential revenues under VBP arrangements

– Understand and develop “best estimates” for key assumptions

– Utilize financial model to inform VBP negotiations

Project opportunities under DSRIP

Estimate potential capital requirements

Other funding sources (e.g. Foundations; HRSA QI awards, reserves/existing operating surpluses)

WARNING! WARNING!

66

THE CONTENTS OF THE FOLLOWING FINANCIAL MODEL ARE BASED ON GROSS ASSUMPTIONS AND INTENDED TO

PROVIDE PARTICIPANTS WITH AN UNDERSTANDING OF THE KEY DRIVERS OF FINANCIAL PERFORMANCE UNDER

VBP AND COULD BE HARMFUL TO YOUR HEALTH!

THE FINANCIAL MODEL AND ITS RESULTS WILL CHANGE AS CHCs DECIDE ON THEIR INFRASTRUCTURE NEEDS AND

ACO/MCO ARRANGEMENTS NEGOTIATED.

ACTUAL RESULTS WILL VARY SIGNIFICANTLY!

Services to Be Provided Under VBP

67

Services

Decide on the services required to be provided for success under VBP

– Improved coding and clinical documentation

– Managing patient centered care (per patient)

– Data analytics (including business intelligence)

– Care management/delivery (HIT/HIE)

– Partnerships and collaboration

– MCO contracting

– Financial management systems

In-house (personnel) versus outsourced (ACO vs. MSO)

On-going versus one-time

Care Coordination/ Management Services –Staffing Model

68

Costs must be assigned to care coordination services identified Example - care managers Care manager capacity (productivity) Patient utilization

Number of care managers required = # of patients ÷ average panel size

• Panel sizes may be impacted based on risk-stratification of patients

Care Coordination Management Fees –Case Study

69

ABC MCO is looking to construct a VBP arrangement with CHC-ACO− ABC MCO has not historically paid providers for care

management/coordination services

CHC-ACO is looking to negotiate a care coordination PMPM with ABC MCO to include care management fees to be paid to member health centers as well as central support services

‒ Care management fees to be paid separately, directly, to health centers and CHC-ACO by ABC-MCO

‒ Health centers will directly employ the care managers

CHC-ACO has compiled data to assist with developing a cost estimate for the provision of these services

Task – Calculate the total annual cost and cost PMPM of care coordination services at both the ACO-level and individual health center level

Care Coordination Management Fees –Case Study (Assumptions)

70

CHC-ACO projects average ABC MCO covered lives = 50,000

CHC-ACO has identified 3 risk-categories of its patients and required level of case management services− Condition A – 40,000 members, 1 unit per member per year− Condition B – 5,000 members, 2 units per member per year− Condition C – 5,000 members, 5 units per member per year

Average capacity per care manager FTE = 5,000 units

Support staff ratios:− 1.00 FTE HC support staff for every 5.00 FTE care managers− 1.00 FTE ACO care management central support for every 10.00 FTE care

managers (no part-time; round-up)− 1.00 FTE ACO support staff for every 2.00 FTE care management central

support staff (no part-time; round-up)

Care Coordination Management Fees – Case Study (Assumptions, Continued)

71

Personnel costs:− Care managers (blended skill sets)= $50,000/FTE− Support staff = $20,000/FTE− Care management central support - $75,000

Care management technology outsourced through an MCO at the ACO-level for $5.00 PMPM

Overhead calculated at 10% excluding the cost of MCO services

Basic Assumptions in the Financial Model

72

Amounts are hypothetical and included to demonstrate the flow of the financial model and highlight the key drivers of performance

Patients

– The number of patients served is projected flat over the 3-year period (25,000 patients) and by month, pro-rated

» Used for staffing

– 50% (12,500 patients) are considered participating in the DSRIP/VBP program

» Used for payment

Payments from ACO

‒ $4 PMPM for care coordination/management services

‒ Participation in VBP arrangement

‒ DSRIP funding for participation in projects

Staffing Assumptions

73

Assess the need for oversight and technical support

Assess the need for care management/ coordination staff

‒ Staffing ratios differ by:

• Populations served

• Risk stratification of patients

• Staff type

VBP Oversight and Technical Support:Position FTE Salary

QI Coordinator 1.00 65,000

Data Analyst 1.00 45,000

Care Coordination/Care Management Function:

CM Ratios:Population Total Pop Low Risk Medium Risk High Risk

General Population 25,000 100% TBD TBD

Special Population -

Health Homes -

TOTAL 25,000 25,000 TBD TBD

FTE Calculation: Salary

Ratios 12,500 TBD TBD

RN CMs 2.00 2.00 0.00 0.00 85,000

Ratios 10,000 TBD TBD

CHWs 2.50 2.50 0.00 0.00 35,000

Ratios 12,500 TBD TBD

LCSWs 2.00 2.00 0.00 0.00 55,000

Projected Annual Salary Increases:

Year Two 3.00%

Year Three 3.00%

Please note that the above staffing ratios do not reflect actual data but are purely included as an example. These ratios need to be developed!

Salary Projections

74

Salaries for participation in VBP should include:

‒ Direct care services

‒ Oversight and technical support

Salaries should be projected to link to changes in patients utilizing appropriate staffing ratios

Additional staff may be required for DSRIP projectsYear One:

Description Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Totals

Salaries and wages:

QI Coordinator

FTE 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00

Salary 5,417 5,417 5,417 5,417 5,417 5,417 5,417 5,417 5,417 5,417 5,417 5,417 65,000

RN Case Managers

FTE 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00

Salary 14,167 14,167 14,167 14,167 14,167 14,167 14,167 14,167 14,167 14,167 14,167 14,167 170,000

Community Health Workers

FTE 2.50 2.50 2.50 2.50 2.50 2.50 2.50 2.50 2.50 2.50 2.50 2.50 2.50

Salary 7,292 7,292 7,292 7,292 7,292 7,292 7,292 7,292 7,292 7,292 7,292 7,292 87,500

LCSWs

FTE 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00

Salary 9,167 9,167 9,167 9,167 9,167 9,167 9,167 9,167 9,167 9,167 9,167 9,167 110,000

Data Analyst

FTE 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00

Salary 3,750 3,750 3,750 3,750 3,750 3,750 3,750 3,750 3,750 3,750 3,750 3,750 45,000

Total salaries and wages 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 477,500

Other Expense Projections

75

Fringe benefits should be projected at the health centers historical fringe rate (e.g. 20%)

Contracted Services

‒ ACO/MCO services – services to be provided by the ACO relative to performance under VBP are forecasted to be borne by the ACO

• If costs are to be passed along from the ACO to the health center, these must be budgeted as well

‒ DSRIP expenses – budget expenditures anticipated as a result of projects and other requirements for participation in DSRIP

‒ Outsourced Technology Solution – budgeted $.25 PMPM

• Other technology and data analytics projected to reside at the ACO

Program Administration/Overhead – budgeted at 15% of direct costs

Other

Revenue Projections -- VBP

76

Care management/coordination payments PMPM

‒ Model assumes a $4 PMPM

‒ This may come through the ACO out of DSRIP or MCO/MassHealth funding for these services

• Could also be paid directly from the MCO/MassHealth

• It is anticipated that if these funds are paid by DSRIP, that they would eventually be paid out of future shared savings generated under VBP

Surplus-sharing arrangements

‒ MCO/MassHealth projected to make surplus distributions to the ACO

‒ ACO to distribute surplus to its members based on an ACO distribution methodology

• In general, ACOs distribute funds based on attributed members and quality

• For purposes of the financial model, the amount of distribution to the FQHC will be based on –

‒ The projected % of the FQHC’s attributed members to total ACO members AND

‒ A projection of the FQHC’s quality scores

ACO – Surplus/ Risk Sharing

77

Revenue projection – complicated and various assumptions

Targeted Spend/Benchmark – Use of historic claims versus Medical Loss Ratio (MLR)

Projection of actual spend

Surplus-sharing and risk-sharing %s

Impact of quality scores on distribution amount

Timing of payments – interim versus annual

Key Assumptions – ACO Framework and Benchmarks

78

VBP Arrangement

‒ Surplus-sharing arrangement in Years One and Two (50%), transitioning to risk-sharing in Year Three (70% upside; 30% downside)

‒ Interim surplus calculation performed after 4 months of midpoint with final reconciliation paid 7 months after contract period ends

Benchmarks Benchmark set on a PMPM basis based on historical claims

experience (estimated for example purposes)

Future benchmarks projected based on projected savings, averaging the prior 2 years actual spend PMPM

Year

Projected Savings

%

Benchmark

PMPM

PMPM After

Savings

Next Year's

Benchmark

PMPM (@50%)

Yr. 1 2% $400.00 $392.00 $396.00

Yr. 2 3% $396.00 $380.24 $388.12

YR. 3 2% $388.12 $372.64 $380.38

ACO – Surplus/ Risk Sharing, Year 1

79

Number of

Description ACO Members PMPM Amount

83,333 50%

Targeted Benchmark $400.00 400,000,000

Projected Actual Spend $392.00 392,000,000

Projected ACO Surplus 8,000,000

Total ACO Surplus Available Surplus Only 50% 4,000,000

Projected Distribution (d) Quality Modifier 100% 4,000,000

Projected Payment Dates - 10/31/XXX1 40% 1,600,000

7/31/XXX2 60% 2,400,000

4,000,000

Notes:

(d) FQHC specific quality score will be used to adjust FQHC-specific distribution projection.

Year One

CHC – Surplus/ Risk Sharing Allocation (Year One)

80

Interim Final Total

Total ACO Projected Distribution 1,600,000 2,400,000 4,000,000

% of Members Attributed to FQHC (a) 15.00% 15.00% 15.00%

ACO Distribution Adjusted by Membership 240,000 360,000 600,000

FQHC-Specific Quality Score 50.00% 50.00% 50.00%

Projected FQHC Distribution 120,000 180,000 300,000

Payment Dates 10/31/XXX1 7/31/XXX2

Notes:

(a) % of Massachusetts FQHC members as a % of total ACO members:

FQHC-Specific Members 12,500

ACO Total Members 83,333

FQHC Members as % of Total Members 15.00%

Year One

FQHC Quality Score (Year One)

81

Measurement Period > Base Benchmark

Quality Measure Actual Improve % Score 50th %tile Year One

Measure A 45.00% 15.00% 51.75% 60.00% 0

Measure B 35.00% 15.00% 40.25% 50.00% 0

Measure C 45.00% 5.00% 47.25% 40.00% 1

Measure D 65.00% 15.00% 74.75% 85.00% 0

Measure E 40.00% 10.00% 44.00% 45.00% 0

Measure F 60.00% 10.00% 66.00% 55.00% 1

Measure G 30.00% 10.00% 33.00% 45.00% 0

Measure H 30.00% 10.00% 33.00% 30.00% 1

Measure I 45.00% 10.00% 49.50% 45.00% 1

Measure J 35.00% 5.00% 36.75% 30.00% 1

Total Points Earned 5

Maximum Points 10

Quality Score 50.00%

Quality Metrics - Actual and Projected

Year One Projected Score

Revenue Projections, Other

82

DSRIP

‒ Projected to cover DSRIP projected expenses

• This may not be the case as DSRIP funding is often earned based on performance and meeting metrics

‒ To be received 3 months after each 6-month reporting period

Other Revenue (not projected)

‒ Potential additional patient service revenue to be generated from new care team members (RN Care Managers, LCSWs)

• Depends on services provided

• Whether payors will reimburse for care management services (e.g. Medicare)

‒ HRSA Quality Improvement awards

• This same team and its objectives are aligned with HRSA’s quality measures and their efforts could result in additional grant funding

Monthly Financial Projection (Year One)

83

Year One:

Description Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Totals

MCO/MassHealth 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 150,000

TOTAL MEMBERS 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 150,000

Operating Revenue:

Care Management Fee (PMPM) 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 600,000

Surplus/Risk-sharing 120,000 120,000

Other - DSRIP 75,000 75,000

TOTAL OPERATING REVENUE 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 125,000 170,000 50,000 50,000 795,000

Operating Expenses

Salaries and wages 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 39,792 477,500

Fringe benefits @ 20% 7,958 7,958 7,958 7,958 7,958 7,958 7,958 7,958 7,958 7,958 7,958 7,958 95,500

Total Personnel Costs 47,750 47,750 47,750 47,750 47,750 47,750 47,750 47,750 47,750 47,750 47,750 47,750 573,000

Contracted services

ACO/MSO costs -

DSRIP Project Implementation 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 12,500 150,000

Oursourced Technology Solution 3,125 3,125 3,125 3,125 3,125 3,125 3,125 3,125 3,125 3,125 3,125 3,125 37,500

Total Contracted Services 15,625 15,625 15,625 15,625 15,625 15,625 15,625 15,625 15,625 15,625 15,625 15,625 187,500

Prog Admin/Overhead @ 15% 9,506 9,506 9,506 9,506 9,506 9,506 9,506 9,506 9,506 9,506 9,506 9,506 114,075

TOTAL OPERATING EXPENSES 72,881 72,881 72,881 72,881 72,881 72,881 72,881 72,881 72,881 72,881 72,881 72,881 874,575

SURPLUS (LOSS) (22,881) (22,881) (22,881) (22,881) (22,881) (22,881) (22,881) (22,881) 52,119 97,119 (22,881) (22,881) (79,575)

Cumulative Surplus (Loss) (22,881) (45,763) (68,644) (91,525) (114,406) (137,288) (160,169) (183,050) (130,931) (33,813) (56,694) (79,575)

The VBP/QI “department” should be viewed as its own profit center!

Annual Cash Flows – Years One through Three

84

Description Amount PMPM Amount PMPM Amount PMPM

MCO/MassHealth 150,000 150,000 150,000

TOTAL MEMBER MONTHS 150,000 150,000 150,000

Operating Revenue:

Care Management Fee (PMPM) 600,000 $4.00 600,000 $4.00 600,000 $4.00

Surplus/Risk-sharing 120,000 $0.80 463,680 $3.09 945,809 $6.31

Other - DSRIP 75,000 $0.50 125,000 $0.83 50,000 $0.33

TOTAL OPERATING REVENUE 795,000 $5.30 1,188,680 $7.92 1,595,809 $10.64

Operating Expenses

Total salaries and wages 477,500 $3.18 491,825 $3.28 506,580 $3.38

Fringe benefits @ 20% 95,500 $0.64 98,365 $0.66 101,316 $0.68

Contracted services

ACO/MSO Costs - $0.00 - $0.00 - $0.00

DSRIP Project Implementation 150,000 $1.00 100,000 $0.67 - $0.00

Outsourced Technology Solution 37,500 $0.25 37,500 $0.25 37,500 $0.25

Program Admin/Overhead @ 15% 114,075 $0.76 109,154 $0.73 96,809 $0.65

TOTAL OPERATING EXPENSES 874,575 $5.83 836,844 $5.58 742,205 $4.95

SURPLUS (LOSS) (79,575) ($0.53) 351,837 $2.35 853,604 $5.69

Year One Year Two Year Three

Monthly Cumulative Cash Position –Years One through Three

85

Year One Year Two Year Three

Jan (22,881) (99,312) 260,411

Feb (45,763) (119,049) 248,561

Mar (68,644) (63,786) 286,710

Apr (91,525) (83,523) 274,860

May (114,406) (103,260) 263,009

Jun (137,288) (122,997) 251,159

Jul (160,169) 37,266 664,829

Aug (183,050) 17,529 652,978

Sep (130,931) 47,792 641,128

Oct (33,813) 311,735 1,149,567

Nov (56,694) 291,998 1,137,716

Dec (79,575) 272,262 1,125,866

The VBP Dilemma – Need for upfront capital and maintain a reserve!

Monthly Cumulative Cash Position – Reduced Care Management Fee

86

Care Management Fee at $3 PMPM

Year One Year Two Year Three

Jan (35,381) (261,812) (52,089)

Feb (70,763) (294,049) (76,439)

Mar (106,144) (251,286) (50,790)

Apr (141,525) (283,523) (75,140)

May (176,906) (315,760) (99,491)

Jun (212,288) (347,997) (123,841)

Jul (247,669) (200,234) 277,329

Aug (283,050) (232,471) 252,978

Sep (243,431) (214,708) 228,628

Oct (158,813) 36,735 724,567

Nov (194,194) 4,498 700,216

Dec (229,575) (27,739) 675,866

Monthly Cumulative Cash Position – No Interim Settlement

87

Year One Year Two Year Three

Jan (22,881) (219,312) (23,269)

Feb (45,763) (239,049) (35,119)

Mar (68,644) (183,786) 3,030

Apr (91,525) (203,523) (8,820)

May (114,406) (223,260) (20,671)

Jun (137,288) (242,997) (32,521)

Jul (160,169) 37,266 664,829

Aug (183,050) 17,529 652,978

Sep (130,931) 47,792 641,128

Oct (153,813) 28,055 629,277

Nov (176,694) 8,318 617,427

Dec (199,575) (11,419) 605,576

Financial and Operational – Key Considerations

88

Key assumptions in financial model to “refine”

Services provided – by FQHC versus ACO

Populations served (risk stratification)

Staff required and staffing ratios

DSRIP projects – cost versus revenue

Care coordination/management revenue PMPM

ACO distributions from MCO VBP arrangements

– ACO distribution methodology

– MCO surplus-sharing model

Other revenue opportunities

Financial and Operational – Key Considerations

89

ACO payment models/distribution methodologies

DSRIP

• Negotiate for DSRIP waiver funds specifically impacted/earmarked for

health centers

• Bump in DSRIP award PMPM for safety net providers

• Funds earmarked by MassHealth for investment in primary care

• Actively engage in conversations concerning services provided at the ACO

versus locally at provider sites

• Care coordination/management services

• Stay active in the development of the budget and funds flow methodology

• Projects the health center will impact (know your cost)

• Workforce

• Technology

• If a care coordination/management PMPM fee is developed, understand

your cost and how it will transition to VBP

Financial and Operational – Key Considerations

90

ACO payment models/distribution methodologies

MCO/MassHealth surplus distribution methodology

– Make sure your “value” is recognized (attributed members, quality)

– Understand dollars that are retained before the total pool available for

distribution is determined

– Stay involved in discussions on the design of the distribution

methodology

‒ Separation of pools (e.g. participation versus performance)

‒ Distribution formulae

‒ Attributes (attributed lives, quality, participation, etc.)

– Evaluate the reasonableness of the quality benchmarks

– Stay active in VBP contract negotiations with MCOs/MassHealth as

they impact your financial model!

Financial and Operational – Key Considerations

91

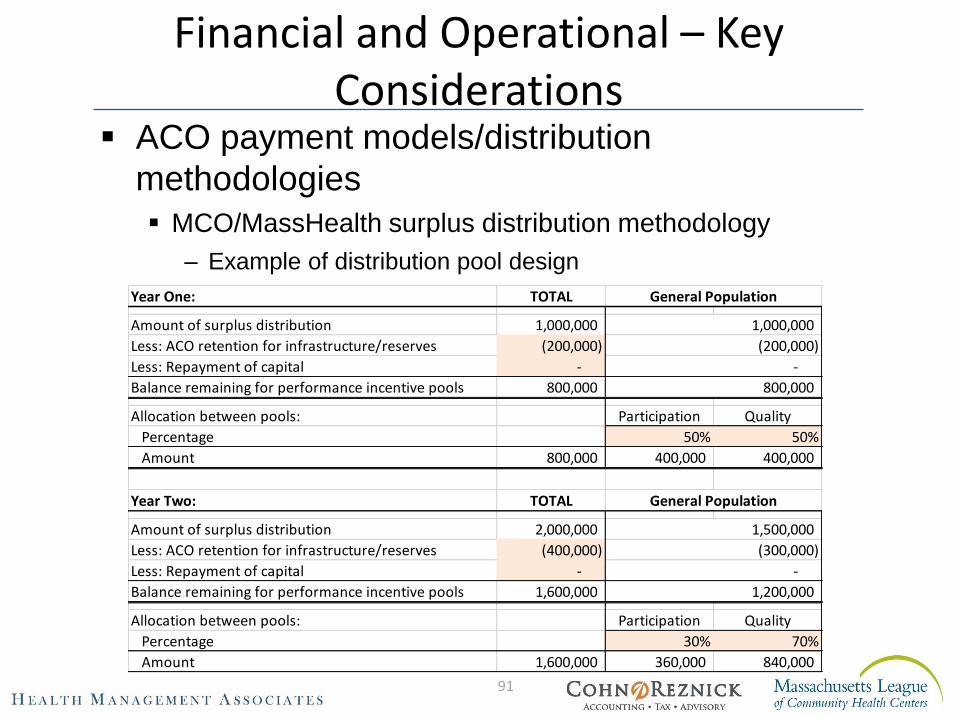

ACO payment models/distribution

methodologies

MCO/MassHealth surplus distribution methodology

– Example of distribution pool design

Year One: TOTAL

Amount of surplus distribution 1,000,000

Less: ACO retention for infrastructure/reserves (200,000)

Less: Repayment of capital -

Balance remaining for performance incentive pools 800,000

Allocation between pools: Participation Quality

Percentage 50% 50%

Amount 800,000 400,000 400,000

Year Two: TOTAL

Amount of surplus distribution 2,000,000

Less: ACO retention for infrastructure/reserves (400,000)

Less: Repayment of capital -

Balance remaining for performance incentive pools 1,600,000

Allocation between pools: Participation Quality

Percentage 30% 70%

Amount 1,600,000 360,000 840,000

(300,000)

-

1,200,000

General Population

General Population

1,500,000

1,000,000

(200,000)

-

800,000

Financial and Operational – Key Considerations

92

ACO payment models/distribution methodologies

MCO/MassHealth surplus distribution methodology

– Example of distribution formulae

‒ Participation Pool

‒ Performance/Quality Pool

Attribute 1 - Attribute 2 - Attribute 3 -

Y Y Y 33.3% 33.3% 33.3% 100.0%

#1

Attribute Score

TotalHealth Center

FQHC A

Attribute Met?

#3#2

# of

Members

% of Total

Members

Amount

Available

Participation

Score

Amount

Earned

12,500 19.3% 77,101$ 100.0% 77,101$

64,850 100.0% 400,000$ 400,000$

Health Center

FQHC A

Total

# of

Members

% of Total

Members

Amount

Available

Quality

Score

Total Amount

to be

Distributed

12,500 19.3% 115,652$ 50.0% 57,826$

64,850 100.0% 600,000$ 222,679$ Total

Health Center

FQHC A

Financial and Operational – Key Considerations

93

Use financial model to inform MCO/MassHealth VBP

negotiations

Utilize key assumptions in financial model around surplus-sharing and

risk-sharing arrangements when developing negotiation strategies

– Monthly care management/infrastructure fee (PMPM)

– Benchmarks

– Use of historic claims data versus Medical Loss Ratios (MLRs)

– Future adjustments to benchmarks

– Surplus-sharing and risk-sharing %s

– Transitioning from surplus- to risk-sharing

– Quality adjusters/modifiers

– Risk mitigating factors

– Reserves versus risk corridors, carve-outs and stop-loss

– Timing of payments

– Interim versus final distributions

The DSRIP Path to Payment Reform

94

CHCs must:

Decide where they “fit” within the current, proposed construct of ACOs and DSRIP Value-Based Payment models

– Ownership versus participating provider

Strategize on how to bring their value to discussions with ACOs/MCOs and have a say in payment reform

Get involved with governance and stay active in committee meetings

‒ Workforce decisions

‒ Funds flow – DSRIP waiver and VBP distributions

Be involved with the ACO meetings and the discussions with MCOs/MassHealth on Value-Based Payment

Continually update the financial model and refine assumptions

Monitor reserves and needs for capital

Financial Management Systems

95

Current financial health and positive operating performance

Reserves

Strong financial systems and internal controls

Financial modeling

What are the new services and infrastructure required?

What will it cost – upfront versus ongoing?

What resources are available to fund these costs?

What potential revenue streams are available?

What are the key assumptions that drive success?

What are the working capital needs?

What is the ROI?

Utilize the financial model to inform VBP negotiations!

Agenda

96

Goals for Today

Overview of VBP, Drivers of Revenue and Financial Dilemma

Defining the Tasks; Defining the Responsibilities

Detailed Walkthrough of the Financial Model

Wrap Up and Implications for Next Steps

Next Session

97

• July 14, 2017: Elements for Success, Population Management

Contact Information

98

Lisa Whittemore, Principal

Myra Sessions, Senior Consultant

Peter Epp, Partner