ACG Final Pres

22

Fordham Capital ParentCo Proposal Eric Martina Ngoc(Tim) Do Edward Schwarzkopf Matthieu Frechin Samatha Howell

Transcript of ACG Final Pres

Fordham Capital

ParentCo Proposal

Eric MartinaNgoc(Tim) Do

Edward SchwarzkopfMatthieu Frechin

Samatha Howell

Agenda

• Options• Proposal• Valuations

– FashionCo– ApparelCo– MediaCo

• ParentCo Equity Carve-Out• Appendix

Appendix

Options

• Buy FashionCo• Sell ApparelCo• Sell MediaCo• Restructure ParentCo

Appendix

Fashion Industry Outlook- Low to mid single digit growth rate- Cyclical - Trendier brands trade at a higher multiple but fall in and out of favor - Not dramatically affected by economic outlook

Appendix

Debt/Total C

apitaliz

ation

Equity/T

otal Capita

lization

ROA

Current R

atio0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

52.7%47.3%

7.2%

146.7%

53.2%46.8%

6.4%

155.6%

20.4%

79.6%

7.1%

220.0%

Profit EBITDA Income0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

ApparelCoFashionCoMean

FashionCo Valuation

Perpetuity Growth Method DCF

In Mil $ Downside Base Upside

EV $34.40 $76.60 $115.40

Appendix

EBITDA Multiple Method DCF

In Mil $ Downside Base Upside

EV $66.50 $119.60 $166.20

P/E Approach

In Mil $ 14.0x 15.0x 16.0x

EV $100.80 $108.00 $115.20

Comparable Multiple EV/EBITDA

In Mil $ 8.0x 9.0x 10.0x

EV $123.02 $138.60 $154.00

Assumptions• WACC: 13.5%• Sale Growth

• Base: 7.2%• Upside: 8%• Downside: 5%

• Net Income 2014: $7.2 Mil• EBITDA 2014: $15.4 Mil

Reasons• High Asking Price - $250 Million• High End vs. Low End• Synergy Analysis • Disagreement from Investor• Core Business – Media Co

ApparelCo Valuation

Perpetuity Growth Method DCF

In Mil $ Downside Base Upside

EV $48.40 $87.40 $164.70

EBITDA Multiple Method DCF

In Mil $ Downside Base Upside

EV $81.70 $123.60 $194.70

P/E Approach

In Mil $ 16.0x 17.0x 18.0x

EV $161.60 $171.70 $181.80

Comparable Multiple EV/EBITDA

In Mil $ 8.0x 9.0x 10.0x

EV $164.20 $184.80 $205.30

Assumptions• WACC: 12.0%• Sale Growth

• Base: 7.5%• Upside: 8.5%• Downside: 5%

• Net Income 2014: $10.1 Mil• EBITDA 2014: $20.5 Mil

Appendix

Media Industry Outlook- Performance in line with general market until the last recession,

lagging since- Lots of consolidation taking place- Little to no expected revenue growth

Appendix

Debt/Total Capital-ization

E/cap ROA Current Ratio-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

109.5%

-9.5%

6.3%

99.7%

52.4% 47.6%

5.3%

152.8%

Profit EBITDA Income0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

MediaCoMean

MediaCo Valuation

Perpetuity Growth Method DCF

In Mil $ Downside Base Upside

EV $47.90 $247.60 $440.6

EBITDA Multiple Method DCF

In Mil $ Downside Base Upside

EV $79.60 $259.30 $498.30

P/E Approach

In Mil $ 14.0x 15.0x 16.0x

EV $358.40 $384.00 $409.60

Comparable Multiple EV/EBITDA

In Mil $ 6.0x 7.0x 8.0x

EV $384.80 $448.90 $513.10

Assumptions• WACC: 11.0%• Sale Growth

• Base: -1.0%• Upside: 2.5%• Downside: -4%

• Net Income 2014: $25.6 Mil• EBITDA 2014: $64.1 Mil

Appendix

ParentCo – Equity Carve-out• Carve-out stock of ApparellCo• Establish own equity – 100% owned by MediaCo to start

– If the parent keeps a majority interest, the subsidiary will be consolidated into the parent’s financial statements

– If the subsidiary issues new shares alone, and the parent doesn’t sell any shares of the subsidiary, the parent won’t recognize any immediate tax costs related to the transaction

– Retain low borrow rates of ParentCo– Option to completely divest if performance deteriorates.

• Carve-outs are much more common than tracking stocks, so the market understands carve-outs better.

• Carve-outs on average have the strongest TRS performance of any restructuring option, while their effect on P/E multiples is roughly comparable to the effect of the other possibilities.

Appendix

Equity Carve-Out Benefits• Increase in analyst coverage

– Floating equity in business units not previously exposed to the market makes their operating performance more transparent and raises shareholder returns by revealing hidden value

• Attract new investors– Little overlap between those who would invest in a parent company and those who

would invest in it’s subsidiaries after restructuring

• Improved operating performance– Restructuring of ownership will permit the company to push management/cost

accountability deeper into the organization. New accountability becomes tangible for management through lower or higher compensation based on stock performance

• New shares can be used as acquisition currency

Appendix

Where to go from here?• MediaCo

– Use retained low cost of capital to borrow at L+250bp and new MediaCo shares as currency in acquisition of media content management believes will grow at over 5%/year

– Explore growth opportunities online and through mobile apps with the goal of capturing younger customers

– Explore opportunities re-introducing MediaCo branded apparel lines– Explore Reduction of CapEx on PP&E via outsourcing of periodical printing

• ApparelCo– Provide new stock based incentives to management to bring performance in-line with

industry leaders– Explore acquisition options to develop synergies utilizing L+250bp borrowing rate and

new ApparellCO shares as acquisition currency• FashionCo

– Management expects to be paid far more than business is worth– Better synergies to be found for acquisitions by ApparellCO with other high-end apparel

producers with good distribution network opportunities

Appendix

APPENDIX

- DCF- WACC- Comparable- Fashion Industry- Media Industry- Valuation Fashion- Valuation Apparel- Valuation Media

- Restructuring

Appendix

Discounted Cash Flow Analysis for FashionCoFigures in millions, except per share

Historical Projected2012 2013 2014 2015 2016 2017 2018 2019

Sales $169.2 $181.9 $194.5 $208.5 $224.0 $240.1 $257.1 $274.6Cost of goods sold (excluding depr.) 137.8 147.5 158.7 169.5 181.2 195.4 208.8 222.5Gross Profit 31.4 34.4 35.8 39.0 42.8 44.7 48.3 52.2

SG & A (excluding amortizations) 16.0 19.6 20.4 20.9 21.9 23.7 25.5 27.5Other operating expense 0.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0EBITDA 15.1 14.8 15.4 18.1 20.9 21.0 22.9 24.7

EBITDA Margin 8.9% 8.1% 7.9% 8.7% 9.3% 8.7% 8.9% 9.0%

Less: Depreciation (2.1) (2.7) (1.7) (2.9) (2.3) (3.3) (2.7) (4.0)Less: Amortization 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0EBIT 13.1 12.2 13.8 15.2 18.5 17.7 20.2 20.8Less: Taxes @ 40.0% (5.2) (4.9) (5.5) (6.1) (7.4) (7.1) (8.1) (8.3)Tax-effected EBIT 7.9 7.3 8.3 9.1 11.1 10.6 12.1 12.5

Plus: Depreciation & Amortization 2.7 1.7 2.9 2.3 3.3 2.7 4.0Less: Capital Expenditures (2.61) (2.93) (2.05) (2.86) (4.30) (4.11) (4.39)Less: Additions to Intangibles 0.0 0.0 0.0 0.0 0.0 0.0 0.0(Increase)/decrease in working capital 0.3 1.3 (3.7) (1.9) (2.2) (2.1) (2.2)Unlevered Free Cash Flow $7.7 $8.3 $6.3 $8.7 $7.4 $8.6 $9.9

Perpetuity Growth Method EBITDA Multiple Method

Weighted average cost of capital: 13.5% Weighted average cost of capital: 13.5% Net present value of free cash flow (a) $27.8 Net present value of free cash flow (a) $27.8

Terminal growth rate 2.5% Terminal multiple 7.0xTerminal value $91.9 Terminal value $173.0 Present value of the terminal value (b) 48.8 Present value of the terminal value (c) 91.9

Enterprise Value $76.6 Enterprise Value $119.6 Less: Net debt (0.3) Less: Net debt (0.3) Add: Equity investment 0.0 Add: Equity investment 0.0 Equity Value $76.3 Equity Value $119.3

Appendix

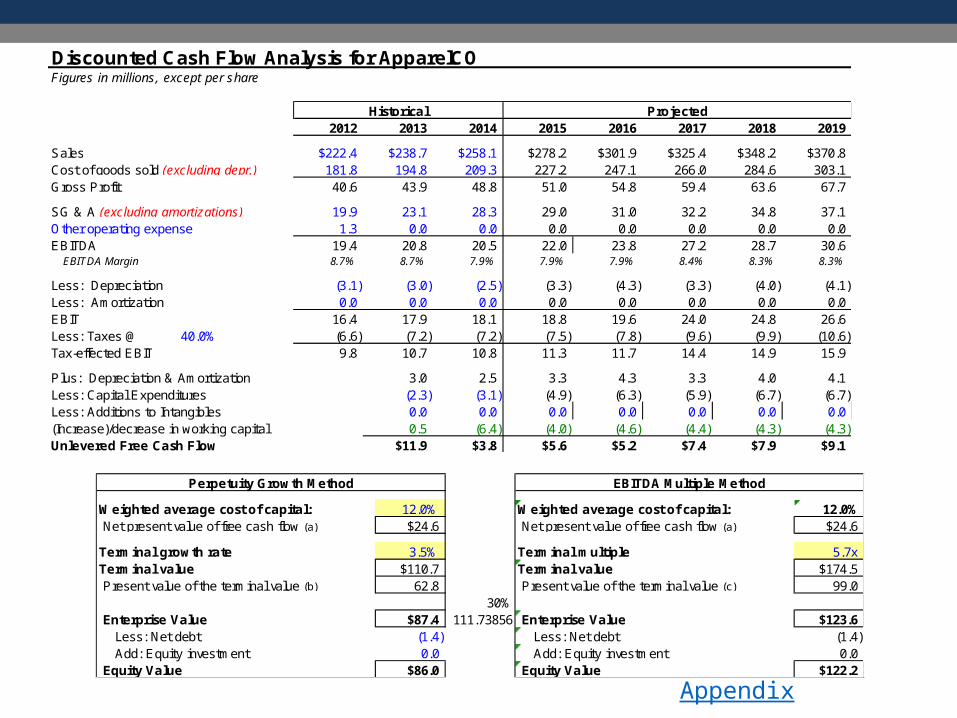

Discounted Cash Flow Analysis for ApparelCOFigures in millions, except per share

Historical Projected2012 2013 2014 2015 2016 2017 2018 2019

Sales $222.4 $238.7 $258.1 $278.2 $301.9 $325.4 $348.2 $370.8Cost of goods sold (excluding depr.) 181.8 194.8 209.3 227.2 247.1 266.0 284.6 303.1Gross Profit 40.6 43.9 48.8 51.0 54.8 59.4 63.6 67.7

SG & A (excluding amortizations) 19.9 23.1 28.3 29.0 31.0 32.2 34.8 37.1Other operating expense 1.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0EBITDA 19.4 20.8 20.5 22.0 23.8 27.2 28.7 30.6

EBITDA Margin 8.7% 8.7% 7.9% 7.9% 7.9% 8.4% 8.3% 8.3%

Less: Depreciation (3.1) (3.0) (2.5) (3.3) (4.3) (3.3) (4.0) (4.1)Less: Amortization 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0EBIT 16.4 17.9 18.1 18.8 19.6 24.0 24.8 26.6Less: Taxes @ 40.0% (6.6) (7.2) (7.2) (7.5) (7.8) (9.6) (9.9) (10.6)Tax-effected EBIT 9.8 10.7 10.8 11.3 11.7 14.4 14.9 15.9

Plus: Depreciation & Amortization 3.0 2.5 3.3 4.3 3.3 4.0 4.1Less: Capital Expenditures (2.3) (3.1) (4.9) (6.3) (5.9) (6.7) (6.7)Less: Additions to Intangibles 0.0 0.0 0.0 0.0 0.0 0.0 0.0(Increase)/decrease in working capital 0.5 (6.4) (4.0) (4.6) (4.4) (4.3) (4.3)Unlevered Free Cash Flow $11.9 $3.8 $5.6 $5.2 $7.4 $7.9 $9.1

Perpetuity Growth Method EBITDA Multiple Method

Weighted average cost of capital: 12.0% Weighted average cost of capital: 12.0% Net present value of free cash flow (a) $24.6 Net present value of free cash flow (a) $24.6

Terminal growth rate 3.5% Terminal multiple 5.7xTerminal value $110.7 Terminal value $174.5 Present value of the terminal value (b) 62.8 Present value of the terminal value (c) 99.0

30% Enterprise Value $87.4 111.73856 Enterprise Value $123.6 Less: Net debt (1.4) Less: Net debt (1.4) Add: Equity investment 0.0 Add: Equity investment 0.0 Equity Value $86.0 Equity Value $122.2

Appendix

Discounted Cash Flow Analysis for MediaCoFigures in millions, except per share

Historical Projected2012 2013 2014 2015 2016 2017 2018 2019

Sales $540.5 $551.8 $535.1 $527.6 $522.3 $522.3 $522.3 $522.8Cost of goods sold (excluding depr.) 313.1 328.5 316.0 313.2 311.2 305.7 308.1 308.5Gross Profit 227.4 223.3 219.1 214.4 211.1 216.5 214.1 214.3

SG & A (excluding amortizations) 162.5 154.8 155.0 155.8 155.1 154.6 154.6 154.7Other operating expense 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0EBITDA 64.9 68.5 64.1 58.7 56.0 61.9 59.5 59.6

EBITDA Margin 12.0% 12.4% 12.0% 11.1% 10.7% 11.9% 11.4% 11.4%

Less: Depreciation (15.4) (14.9) (16.6) (16.0) (16.0) (14.2) (14.7) (15.3)Less: Amortization 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0EBIT 49.6 53.7 47.6 42.8 40.1 47.9 44.9 44.5Less: Taxes @ 40.0% (19.8) (21.5) (19.0) (17.1) (16.0) (19.2) (18.0) (17.8)Tax-effected EBIT 29.8 32.2 28.6 25.7 24.1 28.7 27.0 26.7

Plus: Depreciation & Amortization 14.9 16.6 16.0 16.0 14.2 14.7 15.3Less: Capital Expenditures (14.9) (16.8) (16.3) (15.8) (16.3) (16.8) (17.4)Less: Additions to Intangibles 0.0 0.0 0.0 0.0 0.0 0.0 0.0(Increase)/decrease in working capital 20.4 5.3 (7.4) (0.5) (0.2) 0.1 0.0Unlevered Free Cash Flow $52.6 $33.7 $18.0 $23.8 $26.4 $24.9 $24.6

Perpetuity Growth Method EBITDA Multiple Method

Weighted average cost of capital: 11.0% Weighted average cost of capital: 11.0% Net present value of free cash flow (a) $85.9 Net present value of free cash flow (a) $85.9

Terminal growth rate 1.8% Terminal multiple 4.9xTerminal value $272.5 Terminal value $292.2 Present value of the terminal value (b) 161.7 Present value of the terminal value (c) 173.4

Enterprise Value $247.6 Enterprise Value $259.3 Less: Net debt (14.2) Less: Net debt (14.2) Add: Equity investment 0.0 Add: Equity investment 0.0 Equity Value $233.4 Equity Value $245.1

Appendix

FashionCo WACC

Cost of Debt

4.30%x After tax cost of debt

1 - Tax rate 2.58%1 - 40.00% x

% of debt8.80% Weighted average cost of capital

Risk free rate 14.00%2.24% % of equity

+ 86.40%Beta x

1.2 Cost of equityx 9.78%

Market risk premium6.00%

+Size premium

5.82%

Appendix

ApparelCo WACC

Cost of Debt

4.30%x After tax cost of debt

1 - Tax rate 2.58%1 - 40.00% x Weighted cost of debt

% of debt 0.34%13.30% Weighted average cost of capital

Risk free rate + 13.74%2.24% % of equity

+ 86.70% Weighted cost of equityBeta x 13.22%

1.24 Cost of equityx 15.25%

Market risk premium6.00%

+Size premium

5.82%

Appendix

MediaCo WACC

Cost of Debt

4.50%x After tax cost of debt

1 - Tax rate 2.70%1 - 40.00% x Weighted cost of debt

% of debt 0.42%15.50% Weighted average cost of capital

Risk free rate + 10.65%2.24% % of equity

+ 86.40% Weighted cost of equityBeta x 73.01%

1.2 Cost of equityx 84.50%

Market risk premium6.00%

+Size premium

2.70%

Appendix

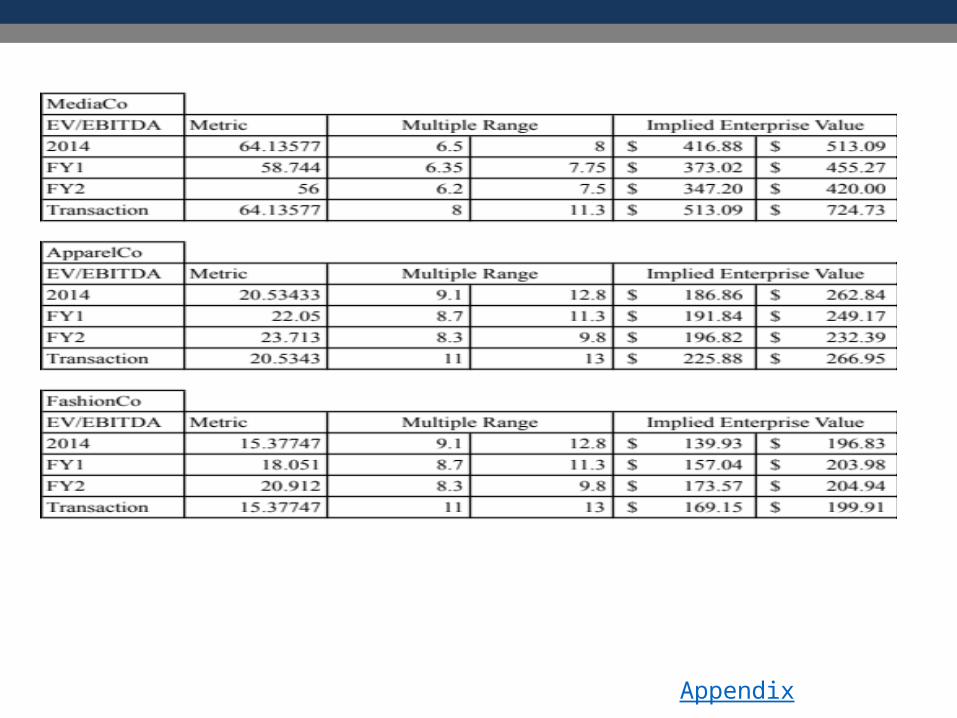

Comparable Company Multiples(figures in millions except per share amount)

Shares LTM LTM LTM LTM PECompany Ticker Stock Price Outstanding Debt Cash Sales EBITDA EBIT Earnings

Gannett Co., Inc. GCI $31.50 225.6 $4,112.6 $1,374.5 $5,675.2 $1,254.7 $1,023.9 $476.9 14.9Lee Enterprises, Incorporated LEE 3.73 53.7 815.0 17.8 657.1 160.2 112.9 (85.1) -2.4The McClatchy Company MNI 3.56 86.7 1,560.3 225.1 1,215.2 248.9 144.6 83.9 3.7The New York Times Company NYT 12.84 150.3 669.4 414.6 1,587.7 232.1 152.8 64.1 30.1Time Inc. TIME 22.59 109.0 1,376.0 325.0 3,352.0 510.0 352.0 8.0 307.7

Shares LTM LTM LTM LTM PECompany Ticker Stock Price Outstanding Debt Cash Sales EBITDA EBIT Earnings

Ever-Glory International Group, Inc. EVK $6.19 14.8 $55.4 $25.0 $422.3 $27.0 $20.8 $12.8 7.1G-III Apparel Group, Ltd. GIII 79.35 22.4 71.2 21.5 1,931.7 152.4 135.9 80.2 22.2Oxford Industries Inc. OXM 61.25 16.5 108.5 6.4 951.8 121.9 85.3 45.9 22.0Perry Ellis International Inc. PERY 20.45 15.7 172.5 49.2 899.0 34.7 21.3 (25.1) -12.8PVH Corp. PVH 114.35 82.4 3,907.4 461.1 8,250.7 1,202.2 948.9 321.0 29.3V.F. Corporation VFC 67.68 431.1 2,083.5 496.5 11,993.4 2,047.8 1,775.2 1,293.1 22.6

LTM Operating Indications LTM Margins 2-Year Compound Annual Growth RateGross Net Gross Net

Company Revenue Profit EBITDA EBIT Income Profit EBITDA EBIT Income

Gannett Co., Inc. $5,675.2 $2,652.3 $1,254.7 $1,023.9 $476.9 46.7% 22.1% 18.0% 8.4%Lee Enterprises, Incorporated 657.1 374.0 160.2 112.9 (85.1) 56.9% 24.4% 17.2% -12.9%The McClatchy Company 1,215.2 675.6 248.9 144.6 83.9 55.6% 20.5% 11.9% 6.9%The New York Times Company 1,587.7 945.1 232.1 152.8 64.1 59.5% 14.6% 9.6% 4.0%Time Inc. 3,352.0 2,000.0 510.0 352.0 8.0 59.7% 15.2% 10.5% 0.2%

LTM Operating Indications LTM Margins 2-Year Compound Annual Growth RateGross Net Gross Net

Company Revenue Profit EBITDA EBIT Income Profit EBITDA EBIT Income

Ever-Glory International Group, Inc. $422.3 $110.0 $27.0 $20.8 $12.8 26.0% 6.4% 4.9% 3.0%G-III Apparel Group, Ltd. 1,931.7 672.1 152.4 135.9 80.2 34.8% 7.9% 7.0% 4.2%Oxford Industries Inc. 951.8 530.8 121.9 85.3 45.9 55.8% 12.8% 9.0% 4.8%Perry Ellis International Inc. 899.0 303.7 34.7 21.3 (25.1) 33.8% 3.9% 2.4% -2.8%PVH Corp. 8,250.7 4,330.2 1,202.2 948.9 321.0 52.5% 14.6% 11.5% 3.9%V.F. Corporation 11,993.4 5,824.1 2,047.8 1,775.2 1,293.1 48.6% 17.1% 14.8% 10.8%

Appendix

Appendix

Earnings Impact of Parent Co Acquisition of FashionCo at $0.00 per share50.0% Cash, 50.0% Stock

2015E 2016E 2017EParent Co diluted EPS $1.12 $1.18 $1.34Shares (MM) 30.000 30.000 30.000Parent Co Net Income $33.5 $35.4 $40.1

FashionCo diluted EPS $0.00 $0.00 $0.00Shares (MM) 0.000 0.000 0.000FashionCo Net Income $8.5 $10.6 $10.0

Combined Net Income (before adjustments) $42.0 $46.0 $50.1

Pre-tax Adjustments

Less: Additional interest expense(1) ($5.5) ($5.5) ($5.5)

+ / ( - ): Synergies(2) 1.7 1.7 1.7

+ / ( - ): Depreciation from write-up(3) (2.6) (2.6) (2.6)

+ / ( - ): Amortization from write-up(3) (0.6) (0.6) (0.6)Total Pre-tax Adjustments ($7.0) ($7.0) ($7.0) Less: taxes @ 40.0% 2.8 2.8 2.8Total After-tax Adjustments ($4.2) ($4.2) ($4.2)

Pro Forma Combined Net Income $37.8 $41.8 $45.9

Pro Forma Shares(4) 36.827 36.827 36.827

Pro Forma GAAP EPS $1.03 $1.13 $1.25Parent Co stand-alone GAAP EPS $1.12 $1.18 $1.34

Accretion / (Dilution)(5)

GAAP EPS Accretion / (Dilution) - $ ($0.09) ($0.05) ($0.09)GAAP EPS Accretion / (Dilution) - % (8.0%) (3.9%) (6.8%)Additional Pre-tax (Cushion) / Synergies to Breakeven $5.5 $2.8 $5.6

Synergy as a % of S&A

Estimated Synergies

EPS Accretion/Dilution

2.0% $0.97 -9.1%2.5% $1.22 -8.7%3.0% $1.46 -8.4%

3.5% $1.70 -8.0%4.0% $1.95 -7.7%4.5% $2.19 -7.3%5.0% $2.44 -6.9%9.7% $4.72 0.0%